sample leasehold enfranchisement paper

TRANSCRIPT

© Hussein Hijazi 2016 1

SAMPLE

Leasehold Enfranchisement Valuation Report:

Cameron House, London, W1

Valuation Date: 03 May 2016

By: Hussein Hijazi

© Hussein Hijazi 2016 2

Contents 1. Individual Tenant Leasehold Enfranchisement Valuation ........................................................................................................................................................................................................................................... 3

2. Freehold Valuation of Cameron House Residential Block .......................................................................................................................................................................................................................................... 7

1.1 Assured Shorthold Tenancy (AST) ...................................................................................................................................................................................................................................................................... 8

1.2 Regulated Tenancies (Rent Controlled) ............................................................................................................................................................................................................................................................... 8

References...................................................................................................................................................................................................................................................................................................................... 13

Appendices ..................................................................................................................................................................................................................................................................................................................... 15

Appendix 1: Relevant Paragraph Provisions Under Schedule 13 of the 1993 Act ....................................................................................................................................................................................................... 15

Appendix 2: Relativity Graphs for Lessee’s Current Interest in Prime Central London ................................................................................................................................................................................................ 16

Appendix 3: BCIS Cost for Flat Conversion in City of Westminster ............................................................................................................................................................................................................................. 16

Appendix 4: BCIS Duration Calculator......................................................................................................................................................................................................................................................................... 17

© Hussein Hijazi 2016 3

1. Individual Tenant Leasehold Enfranchisement Valuation

The law surrounding leasehold enfranchisement has taken several forms over the years, and is an extremely complex and specialised field. For the purposes of the valuation within this section and simplicity,

exclusive attention is given to the law surrounding the leasehold enfranchisement of flats, particularly the granting of a new lease to an individual tenant of a flat under a long leasehold tenancy.

The primary statutory legislation that introduced the granting of a new lease of a flat to an individual tenant is the Leasehold Reform, Housing and Urban Development Act 1993 (1993 Act), as amended by

subsequent acts. Within the provisions of the Act;

1. A tenant has the right to acquire a new lease [Section 39(1)]; if

2. the tenant has been for two years a qualifying tenant [Section 39(2)];

3. for which a qualifying tenant is one that has a long lease [Section 5(1)];

4. for which a long lease is a lease granted for a term of years certain exceeding 21 years [Section 7(1)(a)].

The tenant, therefore, is entitled under Section 42 of the 1993 Act, to claim to exercise his/her right to acquire a new lease as per Section 56 of the 1993 Act, whereby:

1. the landlord “shall be bound to grant to the tenant, and the tenant shall be bound to accept [Section 56(1)]

a. substitution of the existing lease;

b. on payment of a premium as per Schedule 13 of the 1993 Act for;

2. a new lease at peppercorn rent (nominal rent);

3. for a term expiring 90 years after the term date of the existing lease;

4. however, no statutory security of tenure provisions will apply as per Section 59 of the 1993 Act

Therefore, in carrying out an enfranchisement valuation of the premium payable in regards to Ms Jocasta Grimeley-Ffiennes’ flat, the relevant provisions under Schedule 13 of 1993 Act are to be implemented as

provided under [Appendix 1]. It is important to note, however, that “the exercise of the collective right to enfranchise or to buy a new extended lease, is a form of compulsory purchase” (RICS, 2005, p 1). The

aforementioned quote signifies the importance of the principal of equivalence in regards to compulsory purchase, in that compensation is determined “by ensuring that the property owners are in no better and no

worse position financially than they would have been if the interest had not been compulsorily acquired” (Vaughan and Clements Smith, 2014, p185) . Therefore, the price payable is subject to assumptions, which

include:

1. the interest is being sold on the open market as if there is no influence of compulsory purchase (RICS, 2005, p 1),

2. the parties involved in the transaction are not the ones seeking to gain the interest of the benefit of the transaction (RICS, 2005, p 1),

3. any improvement works carried out by the existing or former tenant are disregarded from the valuation and the flat is taken at its current state [1993 Act, Schedule 13 para. 3(2)(c)].

4. exclusion of the right to a new lease (Hayward, 2008)

In the case of Ms Grimeley-Ffiennes, the details surrounding her flat and the associated lease are shown under Table 1 below.

© Hussein Hijazi 2016 4

Table 1

Property 2 Bed Flat, Cameron House, London, W1

Valuation Date 03 May 2016

Lease Details

Date of Lease Commencement 24 April 1978

Date of Lease Expiry 23 April 2077

Lease Length (Term) in Years 99 Years

Unexpired Term in Years 61 Years

Expired Term so far in Years 38 Years

Ground Rent per annum (Stepped Variable

Rent Every 33 Years)

From 1978 to 2011 £300

From 2011 to 2044 £600

From 2044 to 2077 £900

Ground Rent Remaining

From 2016 to 2044 28 Years @ £600

From 2044 to 2077 33 Years @ £900

Based on the details provided under Table 1, a determination of the price payable can thus be calculated using the method and format as presented under Page 16, Example 4, Appendix 4 of (RICS, 2005). The

calculations and their relevant explanatory adaptions are presented under Table 2 and Table 3 respectively below.

© Hussein Hijazi 2016 5

Table 2: Calculation of Price Payable RE Leasehold Enfranchisement of Ms Grimeley-Ffiennes’ Flat

a) Diminution in the value of the landlord's interest

A. i) Ground Rent Now

From 2016 to 2044 £600.00

B. YP for 28 years @ 7% 12.1371

B1. £7,282.26

From 2044 to 2077 £900.00

YP for 33 Years @7% 12.7538

C. Deferred for 28 years (PV of £1 today) 0.1504022

C1. £1,726.38

D. Total Ground Rent £9,008.64

E. ii) Vacant possession comparable value £1,350,000.00

F. Deferred for 61 Years @ 5% 0.0509862

F1. £68,831.37

G. Landlord's interest before lease extension £77,840.01

iii) Vacant possession comparable value £1,350,000.00

H. Deferred for 151 Years @ 5% 0.0006315

H1. Landlord's interest after lease extension £852.53

I. Diminution in the value of the landlord's interest £76,987.48

b) Landlord's share of marriage value

i) Interests after marriage

J. Value of extended lease £1,350,000.00

J1. Landlord's interest after lease extension £852.53

K. Value of combined interests after lease extension £1,350,852.53

ii) Interests before marriage

L. Value of lessee's current interest @81.36% of market value £1,098,360.00

L1. Landlord's interest before lease extension £77,840.01

M. Value of combined interests before lease extension £1,176,200.01

N. Marriage value therefore £174,652.52

O. Landlord's share of marriage value @ 50% share £87,326.26

P. Price Payable £164,313.74

Say: £165,000.00

© Hussein Hijazi 2016 6

Table 3: Explanatory Adaptions of Calculations under Table 2

A. i) This is the value of the ground rent for which the landlord will be losing throughout the term of the lease.

ii) As the ground rent is variable every 33 years, it is important to value the ground rent as of the date of valuation.

iii) 38 years of the term of the lease have already passed, i.e. the first £300 during the first 33 years and subsequent 5 years of ground

rent at £600 are assumed to have already been paid by Ms Grimeley-Ffiennes, and thus have nil value. Only the remaining 28 years

of ground rent at £600 and further 33 years at £900 are of interest to the landlord in this case.

iv) Graph 1 below demonstrates the current position of the ground rent, and the remaining ground rent to be incurred.

B. The yield purchase at 7% was estimated using the sum of:

i) Bank of England base current base rate at 0.5% (Bankofengland.co.uk, 2016)

ii) The risk free rate based on the 10 Year Gilt Rate of the UK Government Bonds at 2% (Bloomberg.com, 2016)

iii) Current Consumer Price Index (CPI) Inflation in the UK at 0.5% (Ons.gov.uk, 2016).

iv) The risk premium that is commanded by the landlord, which is assumed to be 4% as determined in the case of Earl Cadogan and

Cadogan Estates v Sportelli [2006].

C. The YP for 33 years was calculated in the conventional manner, however, as it is assumed that the ground will be received in 28 years’

time, the value was discounted back to today as per the examples in (Peterbarry.co.uk, 2016).

D. B1+C1

E. This is the expected current open market value if a comparable flat to that of Ms Grimeley-Ffiennes.

F. The deferral rate of 5% is based on the deferral rate used in the case of Earl Cadogan and Cadogan Estates v Sportelli [2006] which

confirmed the deferral rate at 4.75% for house including a 0.25% increase for flats. This includes a market risk free rate and the estimated

risk premium demand by the investor.

G. F1+D

H. i) The deferral rate is the same as that stated in (F) above.

ii) The 151 Years is sum of the remaining term of the existing lease (61 years) and the extension of the lease granted (90 years).

I. G – H1

J. Same as stated in (E) above.

K. J+J1

L. This is the current value of the leasehold interest in the flat with 61 years remaining. The 81.36% was obtained from using relativity graphs

as explained by (RICS, 2009) and the figure obtained from the average as presented under [Appendix 2] by (Graphsofrelativity.co.uk,

2016)

M. L+L1

N. K-M, where Marriage Value is value that “arises from the combination of two or more assets to create a new asset that has a higher value

than the sum of the individual assets” (Isurv.com, 2016)

O. 50% of N

P. I+O

© Hussein Hijazi 2016 7

Graph 1: Stepped Variable Ground Rent as per the terms of Ms Grimeley-Ffiennes’ Tenancy

Therefore, based on the above calculations, based on the relevant statutory legislation, the price payable by Ms Grimeley-Ffiennes for statutory enfranchisement of the said flat is say £165,000.

2. Freehold Valuation of Cameron House Residential Block

In aiming to value the freehold interest of Cameron House, London, W1, it is essential to consider whether it is possible to value the freehold interest of the building as per the provisions of Sections 1 to 38 of the

1993 Act in the form of a collective enfranchisement of the building by its residents.

The statutory provisions as per the 1993 Act in order for the tenants of the building to qualify to collectively acquire the freehold interest in a block of flats include:

1. the building has to be self-contained [Section 3(1)(a)];

2. two or more flats within the building are owned by qualifying tenants [Section 3(1)(b)] and;

3. at least two thirds of the total number of flats within the building are owned by qualifying tenants [Section 3(1)(c)];

4. for which a qualifying tenant is one that has a long lease [Section 5(1)];

5. for which a long lease is a lease granted for a term of years certain exceeding 21 years [Section 7(1)(a)].

Table 4 below provides the tenant mix of Cameron House as provided.

£0

£100

£200

£300

£400

£500

£600

£700

£800

£900

£1,000

1978 1987 1996 2005 2014 2023 2032 2041 2050 2059 2068 2077

Gro

un

d R

ent

Lease Term

Stepped Ground Rent Chart Current Position

£300 £600 £900

2016 Current Position

© Hussein Hijazi 2016 8

Table 4: Tenant Breakdown of Cameron House

Flat Type Number Tenancy

1 Bed 30 Assured Shorthold Tenancy

2 Bed 15 Rent Controlled

3 Bed 30 Rent Controlled

Total 75

In determining, therefore, whether the tenant mix of Cameron House allows for a collective acquisition of the freehold interest of the building, a brief explanation regarding the types of tenancies within the building

is necessary.

1.1 Assured Shorthold Tenancy (AST)

As explained in (Hayward, 2008), ASTs were introduced under Section 20 of the Housing Act 1988 and they are tenancies that do not provide security of tenure to tenants and there is limited control over the rent

charged by landlords. Tenancy term dates are generally sixth months (Propertyhawk.co.uk, 2016) and two features of an AST is that the tenant, as per the terms of the lease, can be evicted within short notice and

the rate at which rents are changed are subject to the terms of the lease or within the discretion of the landlord. All tenancies granted after 28 February 1997 are automatically considered ASTs, unless expressly

stated, for which a tenancy can only be an AST where:

1. The term of the lease is not less than sixth months

2. The landlord has no power to terminate the tenancy prior to sixth months from the date of commencement

3. A notice by the landlord to the tenant states that the tenancy is an AST

1.2 Regulated Tenancies (Rent Controlled)

Regulated tenancies are tenancies where the Rent Act 1977 applies, where tenants benefit from security of tenure including the benefit of paying a restricted or controlled rent, which is assessed by a rent officer,

or a rent assessment committee (RAC) on appeal (Hayward, 2008). As tenants of regulated tenancies benefit from security of tenure, they can only be evicted from the premises through a court order obtained by

the landlord, which meets specific criteria, even if the lease term has reached its determination date.

Based on the brief definitions of the relevant leases, it can be assumed that all 30 AST tenants of Cameron House have tenancies for a period of six months, thus these tenants do not meet the qualifying criteria

under the provisions of the 1993 Act. Therefore, assuming the remaining 45 tenants under Rent Controlled tenancies are under long leases, the tenant mix within Cameron House does not allow for a freehold

acquisition through collective enfranchisement, as two thirds of the total tenant mix of 75 will have to equal 50 qualifying tenants.

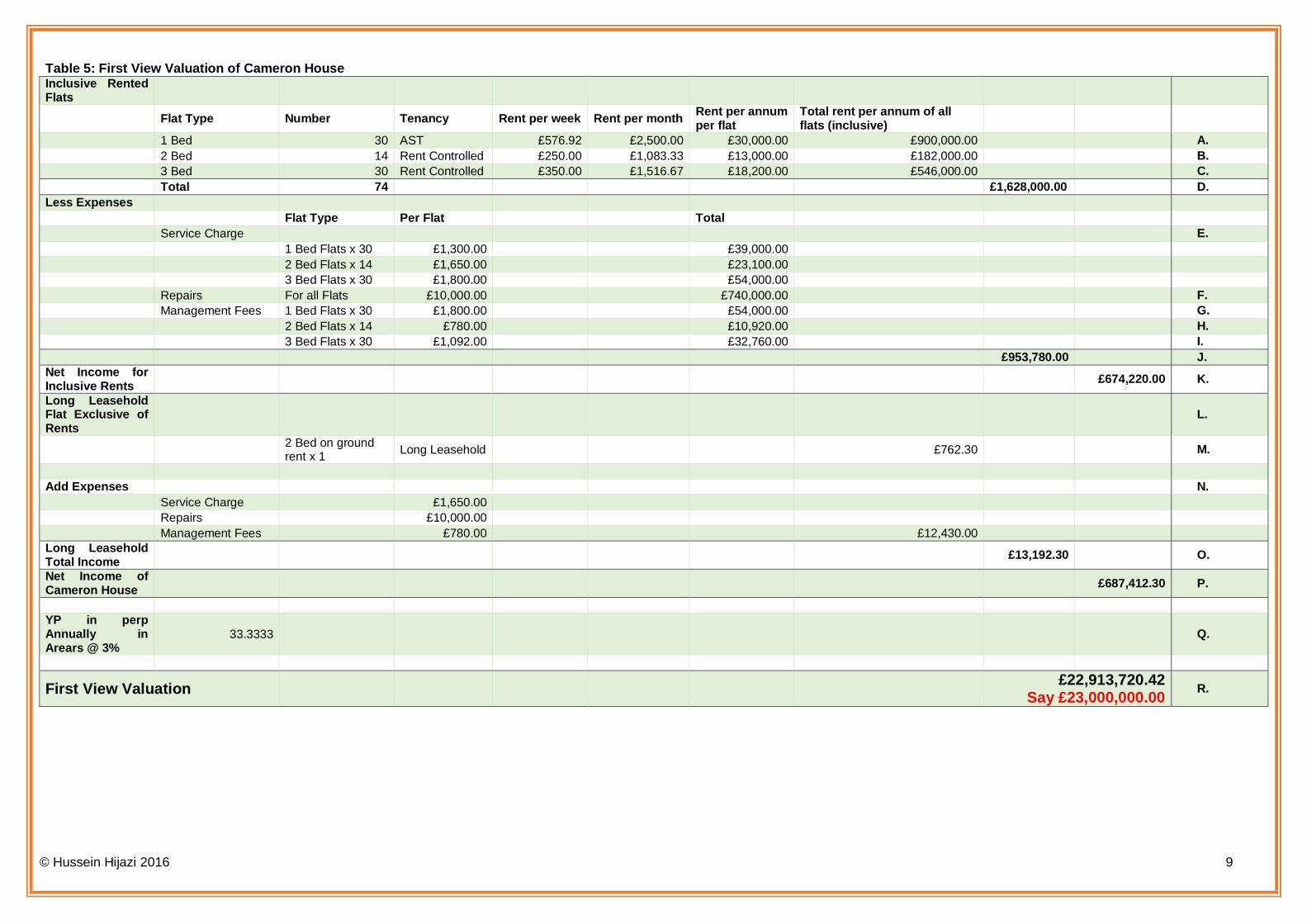

Therefore, a standard first view and second view valuation is carried out in order to determine the freehold interest of Cameron House. These valuations are presented under Tables 5 and 7 below, respectively,

with explanations of calculation adaptions under Table 6 and 8 respectively.

© Hussein Hijazi 2016 9

Table 5: First View Valuation of Cameron House Inclusive Rented Flats

Flat Type Number Tenancy Rent per week Rent per month Rent per annum per flat

Total rent per annum of all flats (inclusive)

1 Bed 30 AST £576.92 £2,500.00 £30,000.00 £900,000.00 A.

2 Bed 14 Rent Controlled £250.00 £1,083.33 £13,000.00 £182,000.00 B.

3 Bed 30 Rent Controlled £350.00 £1,516.67 £18,200.00 £546,000.00 C.

Total 74 £1,628,000.00 D.

Less Expenses

Flat Type Per Flat Total

Service Charge E.

1 Bed Flats x 30 £1,300.00 £39,000.00

2 Bed Flats x 14 £1,650.00 £23,100.00

3 Bed Flats x 30 £1,800.00 £54,000.00

Repairs For all Flats £10,000.00 £740,000.00 F.

Management Fees 1 Bed Flats x 30 £1,800.00 £54,000.00 G.

2 Bed Flats x 14 £780.00 £10,920.00 H.

3 Bed Flats x 30 £1,092.00 £32,760.00 I.

£953,780.00 J.

Net Income for Inclusive Rents

£674,220.00 K.

Long Leasehold Flat Exclusive of Rents

L.

2 Bed on ground rent x 1

Long Leasehold £762.30 M.

Add Expenses N.

Service Charge £1,650.00

Repairs £10,000.00

Management Fees £780.00 £12,430.00

Long Leasehold Total Income

£13,192.30 O.

Net Income of Cameron House

£687,412.30 P.

YP in perp Annually in Arears @ 3%

33.3333 Q.

First View Valuation £22,913,720.42

Say £23,000,000.00 R.

© Hussein Hijazi 2016 10

Table 6: Explanatory Adaptions of Calculations under Table 5

A. Rent per annum per flat x Number of flats

B. Rent per annum per flat x Number of flats

C. Rent per annum per flat x Number of flats

D. Sum of total rents for all flats

E. Service charge values are assumed as per (Homeowners Alliance, 2016)

F. As it is assumed that the new landlords have spent £750,000 on internal and external repairs including the carpets, it is assumed that as

the rents are inclusive of this figure, it is equally apportioned to every flat. However, as Ms Grimeley-Ffiennes only pays the ground rent,

her contribution is excluded as explained further below point (L).

G. As per (Hayward, 2008), management fees are assumed to be 5% of annual rent plus V.A.T at 20% for all flats with inclusive rents

H. As per (Hayward, 2008), management fees are assumed to be 5% of annual rent plus V.A.T at 20% for all flats with inclusive rents

I. As per (Hayward, 2008), management fees are assumed to be 5% of annual rent plus V.A.T at 20% for all flats with inclusive rents

J. Sum of all rent inclusive expenses

K. D – J

L. Ms Grimeley-Ffiennes is assumed to be the only tenant within Cameron House that has a long leasehold interest, for which under the

terms of her lease, she pays only the ground. Ms Grimeley-Ffiennes does not have an inclusive rent, therefore, as it is assumed to be

within the terms of her lease, she is required to pay for all the expenses that are incurred within Cameron House to the landlords. Therefore,

any outstanding expenses, as equally apportioned between the tenants with inclusive rents, are incurred by Ms Grimeley-Ffiennes and

are thus an addition to the first view valuation.

M. As the inclusive rents are estimated be in perpetuity, Ms Grimeley-Ffiennes has ground rents liabilities up to the end of her lease in 61

years. Therefore, to ascertain an estimated ground rent in perpetuity, this was calculated as follows:

(28 years x £600)+(33 years x £900) divided by 61 years = £762.30 per annum in perpetuity.

N. Expenses deducted from inclusive rents, added to the Ms Grimeley-Ffiennes’ liability to pay.

O. M + N

P. K + O

Q. YP at 3% was estimated as per (Knight Frank, 2016), where the Yield for prime central london properties is estimated at 2.91%. An extra

percentage was added due to the age of the building, being from the Edwardian era.

R. K + P provides for the First View Valuation of Cameron House.

© Hussein Hijazi 2016 11

Table 7: Second View Valuation of Cameron House

Vacant Possession Value Without Basement Conversion Flat Type Number of Units Tenancy Type Open Market Vacant

Possession Value A5 Discount Rate A1 Vacant Possession

Estimated Value Total Estimated Value

1 Bed 30 Assured Short Hold £795,000.00 10% A2 £722,727.00 £21,681,818.18 2 Bed 15 Regulated Tenancy £1,350,000.00 40% A3 £964,286.00 £14,464,285.71 3 Bed 30 Regulated Tenancy £1,950,000.00 40% A4 £1,392,857.00 £41,785,714.29

Vacant Possession Value Without Basement Conversion Total £77,931,818.18

Residual Valuation for Basement Conversion into Flats Calculations Open Market Value

Total Value

A. 6 x 1 Bed flats @ 60 sqm 360 £795,000.00 £4,770,000.00

B. 2 x 2 Bed flats @ 75 sqm 150 £1,350,000.00 £2,700,000.00

B1. 1 x 3 Bed flat @ 90 sqm 90 £1,950,000.00 £1,950,000.00

C. Gross Development Value (GDV) A+B+C £9,420,000.00

D. Purchaser’s cost at 5.75% of GDV 0.0575 x C £541,650.0000

E. Net Development Value (NDV) C - D £8,878,350.00

F. Conversion Costs for GIA of 600m2 at £1,948/m2 600x1948 £1,168,800.00

G. Ancillary Costs at 3% of building costs 0.03 x F £35,064.00

H. Sum of building and ancillary costs £1,203,864.00

I. Contingency costs at 5% of building and ancillary costs 0.05 x H £60,193.20

J. Marketing and agency fees at 1.7% of NDV 0.017 x E £150,931.95

K. Costs subtotal 1 F + G + I + J £1,414,989.15

L. Interest on half of costs subtotal at 5.5% for 1 years 0.055 x 0.5 x (0.5 x K) £19,456.10

M. Professional Fees at 13.5% of building and ancillary costs 0.135 x H £162,521.64

N. Interest on two thirds of fees at 5.5% for 1 years 0.055 x 0.5 x (2/3 x M) £2,994.46

O. Gross Development Costs (GDC) F + G + I + J + L + M + N

£1,599,961.35

P. Developer's profit at 20% of GDC 0.2 x O £319,992.27

Q. GDC plus Developer's profit O + P £1,919,953.62

R. Gross Residual Value (GRV) E – Q £6,958,396.38

S. Value of £1 today at 5.5% in 1 years (Parry's Valuation Tables)

- 0.9478673

T. Net Residual Value S x R £6,595,636.39

U. Profit £2,824,363.61

V. Second View Valuation £80,756,181.79

Say: £81,000,00

Table 8: Explanatory Adaptions of Calculations under Table 7

A1, A2, A3 and A4 In calculating the second view freehold valuation of the Cameron House, it is assumed that the entire block has been vacated by all tenants, however, the state of the flats are as

the tenants have left them. It is assumed, therefore, that due to disrepair and lack of improvements, a discount rate to the open market vacant possession value (OMVPV) is applied.

Based on the brief provided, the OMVPV for the 1, 2 and 3 bed flats are as presented under A5 above.

i) For ASTs, the discount rate is assumed to be 10%. This is due to the nature of ASTs, in that they have short term times and the turnover of tenants is higher than flats

under Regulated Tenancies. Therefore, as tenants vacate and enter the flats, certain elements of improvements are carried out. However, these are not up to the standards

as well modernised flats.

ii) For Regulated Tenancies (A3 & A4), the tenant turnover is significantly lower, as tenants benefit from security of tenure and are assumed to carry out significantly fewer

improvements to their flats during their tenancy. Therefore, a discount rate of 40% is assumed in this case due to obsolescence and neglect.

Therefore, without taking into account the basement conversion, the Vacant Possession value is assumed to be £77,931,818.18 say £78,000,000

© Hussein Hijazi 2016 12

Converting the basement of 600 sqm into flats, subject to the necessary planning approvals, can help increase the vacant possession value of Cameron House. It is assumed, therefore, that the basement is

converted into 6x1 bed flats @ 60sqm each, 2x2 bed flats @ 75sqm each and 1x3 bed flat @ 90sqm. As the flats will be of open market standards as being well modernised, the VPOMV is assumed as per

A, B and B1.

A. See above

B. See above

B1. See above

C. Gross Development Value, sum of value of all flats as per the VPOMV.

D. This is assumed to take into account stamp duty land tax at 4% and legal fees at 1.75%.

E. -

F. Average conversion costs of the basement into flats as provided by (BCIS, 2016) [Appendix 3].

G. Ancillary costs percentage based on (Isaac and O'Leary, 2012) estimate.

H. -

I. 5% contingency used due to the age of the block, assuming that extra mitigation is taken during the conversion process in case of any unexpected issues arising.

J. Assumed market rate for marketing costs @1.7%

K. -

L. Interest rate assumed to be 5.5% based on (Knightfrank.co.uk, 2016). Duration of conversion is assumed to be 1 year as provided by (BCIS, 2016) [Appendix 4].

M. Professional fees at 13.5% based on the sum of the percentages under Core consultant fees for projects between £3m-£10m in (Designingbuildings.co.uk, 2016) website.

N. -

O. -

P. Landlord’s compensation for undertaking the conversion

Q. -

R. -

S. Percentage taken as same as interest rate

T. -

U. Profit gained. GDV less NRV.

V. i) Second View Valuation of Cameron House, therefore, assumed to be say £81,000,000 with basement conversion into flats.

ii) The sum of the profits gained from converting the basement, added the vacant possession value of Cameron House.

© Hussein Hijazi 2016 13

References

Bankofengland.co.uk. (2016). Bank of England Statistical Interactive Database | Interest & Exchange Rates | Official Bank Rate History. [online] Available at:

http://www.bankofengland.co.uk/boeapps/iadb/repo.asp [Accessed 28 Apr. 2016].

BCIS. (2016). BCIS. [online] Available at: http://service.bcis.co.uk/BCISOnline/Duration/Calculation [Accessed 28 Apr. 2016].

Bloomberg.com. (2016). United Kingdom Rates & Bonds. [online] Available at: http://www.bloomberg.com/markets/rates-bonds/government-bonds/uk [Accessed 28 Apr. 2016].

DCLG, (2011). Regulated Tenancies. [online] London: DCLG and Welsh Assembly Government. Available at: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/11445/138295.pdf

[Accessed 28 Apr. 2016].

Designingbuildings.co.uk. (2016). Building design and construction fees - Designing Buildings Wiki. [online] Available at:

http://www.designingbuildings.co.uk/wiki/Building_design_and_construction_fees#Fee_calculations [Accessed 28 Apr. 2016].

Graphsofrelativity.co.uk. (2016). Graphs of Relativity. [online] Available at: http://www.graphsofrelativity.co.uk/inputs/3/valDate/2016-05-03/unexpTerm/61/hiddens/null/checkeds/null [Accessed 28 Apr. 2016].

Hayward, R. (2008). Valuation: Principles into Practice. 6th ed. London: Estates Gazette.

Homeowners Alliance. (2016). Service charges and maintenance companies: problems with your leasehold property | Homeowners Alliance. [online] Available at: http://hoa.org.uk/advice/guides-for-

homeowners/i-am-managing-2/should-i-extend-my-lease/service-charges-and-maintenance-companies-problems-with-your-leasehold-property/ [Accessed 28 Apr. 2016].

Isaac, D. and O'Leary, J. (2012). Property valuation principles. Basingstoke: Palgrave Macmillan.

Isurv.com. (2016). Synergistic/marriage value - Synergistic value: worked examples - isurv. [online] Available at: http://www.isurv.com/site/scripts/documents_info.aspx?documentID=3867 [Accessed 28 Apr.

2016].

Knight Frank, (2016). London Residential Review Spring 2016. [online] London: Knight Frank. Available at: http://content.knightfrank.com/research/78/documents/en/spring-2016-3721.pdf [Accessed 28 Apr.

2016].

Knightfrank.co.uk. (2016). UK Residential Development Finance Report. [online] Available at: http://www.knightfrank.co.uk/research/residential-development-finance-report-2015-3243.aspx [Accessed 28 Apr.

2016].

Ons.gov.uk. (2016). Inflation and price indices- Office for National Statistics. [online] Available at: https://www.ons.gov.uk/economy/inflationandpriceindices [Accessed 28 Apr. 2016].

Peterbarry.co.uk. (2016). Leasehold Valuation Calculations - 2 Worked Examples | Peter Barry. [online] Available at: http://www.peterbarry.co.uk/blog/2011/mar/12/leasehold-valuation-calculations-2-worked-

examples/ [Accessed 28 Apr. 2016].

© Hussein Hijazi 2016 14

Propertyhawk.co.uk. (2016). Magazine : Does an assured shorthold tenancy (ast) have to be six months long?. [online] Available at: http://www.propertyhawk.co.uk/?tenancy-agreement-how-long [Accessed 28

Apr. 2016].

RICS, (2005). Valuation Information Paper No 7. Coventry: RICS Business Services Limited.

RICS, (2009). Leasehold Reform: Graphs of Relativity. [online] London: RICS. Available at: http://www.viewsontheblock.co.uk/insights/extending_files/ricsreport.pdf [Accessed 28 Apr. 2016].

RICS, (2015). Leasehold Reform in England and Wales. [online] London: RICS. Available at: http://www.rics.org/uk/knowledge/professional-guidance/guidance-notes/leasehold-reform-in-england-and-wales-3rd-

edition/ [Accessed 27 Apr. 2016].

Vaughan, D. and Clements Smith, L. (2014). An introduction to compulsory purchase valuation principles spanning 150 years. Journal of Building Survey, [online] 3(2), pp.184-189. Available at:

http://www.blmlaw.com/images/uploaded/File/News/Sep14/JBSAV106.pdf [Accessed 20 Apr. 2016].

© Hussein Hijazi 2016 15

Appendices

Appendix 1: Relevant Paragraph Provisions Under Schedule 13 of the 1993 Act

2.

The premium payable by the tenant in respect of the grant of the new lease shall be the aggregate of—

(a) the diminution in value of the landlord's interest in the tenant's flat as determined in accordance with paragraph 3,

(b) the landlord's share of the marriage value as determined in accordance with paragraph 4, and

(c) any amount of compensation payable to the landlord under paragraph 5.

3.

(1) The diminution in value of the landlord's interest is the difference between—

(a) the value of the landlord's interest in the tenant's flat prior to the grant of the new lease; and

(b) the value of his interest in the flat once the new lease is granted.

(2) Subject to the provisions of this paragraph, the value of any such interest of the landlord as is mentioned in sub-paragraph (1)(a) or (b) is the amount which at [the relevant date] 1 that interest might be

expected to realise if sold on the open market by a willing seller (with [neither the tenant nor any owner of an intermediate leasehold interest] 2 buying or seeking to buy) on the following assumptions—

(c) on the assumption that any increase in the value of the flat which is attributable to an improvement carried out at his own expense by the tenant or by any predecessor in title is to be disregarded; and

4.

(1) The marriage value is the amount referred to in sub-paragraph (2), and the landlord's share of the marriage value is [50 per cent. of that amount.]

(2) [Subject to sub-paragraph (2A), the] 2 marriage value is the difference between the following amounts, namely—

(a) the aggregate of—

(i) the value of the interest of the tenant under his existing lease,

(ii) the value of the landlord's interest in the tenant's flat prior to the grant of the new lease, and

(iii) the values prior to the grant of that lease of all intermediate leasehold interests (if any); and

(b) the aggregate of—

(i) the value of the interest to be held by the tenant under the new lease,

(ii) the value of the landlord's interest in the tenant's flat once the new lease is granted, and

(iii) the values of all intermediate leasehold interests (if any) once that lease is granted.

(2A) Where at the relevant date the unexpired term of the tenant's existing lease exceeds eighty years, the marriage value shall be taken to be nil.

© Hussein Hijazi 2016 16

Appendix 2: Relativity Graphs for Lessee’s Current Interest in Prime Central London

Figure Source: (Graphsofrelativity.co.uk, 2016)

Appendix 3: BCIS Cost for Flat Conversion in City of Westminster

© Hussein Hijazi 2016 17

Appendix 4: BCIS Duration Calculator