s alfa c orp p resentation iii c hile e quity o ne on o ne c onference – l ondon, m ay 2013

TRANSCRIPT

SALFACORP PRESENTATION

III CHILE EQUITY ONE ON ONE CONFERENCE – LONDON, MAY 2013

www.salfacorp.com

CONTENTS 01 - WHO WE ARE02 - INDUSTRY OVERVIEW03 - OUR BUSINESS UNITS & RESULTS04 - TOPICS OF INTEREST05 – FINAL COMMENTS

2

WHO WE ARE01

3

A Company with vast experience in the engineering, construction and real estate sectors

4

More than 83 years of history and leadership

One of the most important conglomerates in Latin America

Growing international presence in markets with potential growth

Leading market position in Engineering & Construction Salfa Ingeniería y

Construcción S.A. (“ICSA”)

Well positioned in mining services

Specialized technologies

Long term & regional relationships with customers

Leading position in Real Estate Development Aconcagua S.A. (“Aconcagua”)

Good Diversification by product and geographic location

Vertically integrated manufacture of houses

Long position in Land

Strong brand recognition and reputation

30,000+ employees

Publicly traded since 2004; member of the IPSA Index (groups the 40 largest

traded companies in Chile’s exchange)

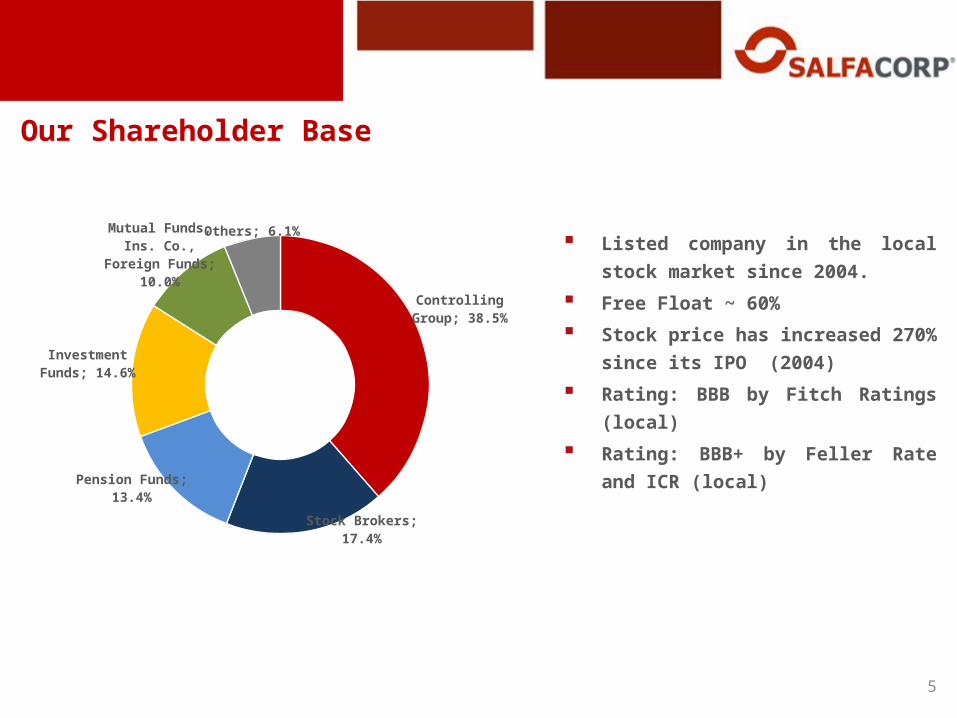

Our Shareholder Base

5

Listed company in the local

stock market since 2004.

Free Float ~ 60%

Stock price has increased 270%

since its IPO (2004)

Rating: BBB by Fitch Ratings

(local)

Rating: BBB+ by Feller Rate

and ICR (local)

Controlling Group; 38.5%

Stock Brokers; 17.4%

Pension Funds; 13.4%

Investment Funds; 14.6%

Mutual Funds, Ins. Co., Foreign Funds;

10.0%

Others; 6.1%

62004 2006 2007 2008 2011

100%

100%

80%

100%

100%

40%80%

66,7%

100%Merger with

ConsolidationSALFA PERÚ

Significant organic growth Growth over the last 5 years through mergers and

acquisitions in complementary businesses International expansion: Peru, Colombia, Panama 2012 focused on consolidating these acquisitions

and generate synergies Revenues increased 472% between 2004-2012

Timeline of Growth

DES&SAL

70%DES&SAL

100%

90%

Among the main construction companies in Latam (USD million)

7

Main E&C and Real Estate Companies in Chile

OD

EBRE

CHT

Andr

ade

Guti

erre

z

ICA

Cam

argo

Cor

rea

OAS

Salfa

corp

Gra

ña M

onte

ro

Besa

lco

Soco

vesa

EISA

Sidg

o Ko

pper

s

Inge

vec

PAZ

Clar

o Vi

cuña

14.922

4.337 3.9373.146

2.5692.214

1.239 804 690 447 443 262 238 178

Source: Bloomberg; Superintendencia de Valores y Seguros; company reports

Revenues for Camargo Correa are as of Dec-2011.

Operations in countries with good economic perspectives

8

Operations in countries with low risk in the Region

Source: Fitch Ratings; based on foreign debt

Source: International Monetary Fund as of Dec-2012

5,9%

5,4%

4,9%

4,6%

6,6%

4,0%

4,0%

4,5%

6,9%

6,2%

6,2%

6,1%

10,8

%

10,6

%

8,9%

7,2%

2011 2012 2013e 2014e

Chile

Colombia

Peru

Panama

GDP as of Dec-2012 (USD Million) GDP Growth Forecast

Salfa

Corp

Salfa

Corp

Salfa

Corp

Salfa

Corp

268.177

199.003

366.020

36.253

Chile Peru Colombia Panama

A+

BBB BBB BBBBBB- BBB- BBB-

BB-B+

B-

CC

Source: International Monetary Fund as of Dec-2012

INDUSTRYOVERVIEW IN CHILE

02 9

Chile’s GDP grew 5,6% in 2012, year over year.

Construction GDP grew by nearly 8% in 2012, year over year.

Construction activity correlated to GDP growth.

Markets where we operate: Engineering & Constructionand Real Estate

Evolution of GDP Construction (Chile) Monthly Construction Activity Index (Chile)

80

85

90

95

100

105

110

115

120

125

Dic

-07

Jun-

08

Dic

-08

Jun-

09

Dic

-09

Jun-

10

Dic

-10

Jun-

11

Dic

-11

Jun-

12

Dic

-12

Variation (%)IM

ACO

N

IMACON Var. % Monthly Var. % 12 months

(*) Source: Central Bank of Chile and Cámara Chilena de la Construcción10

-10,0%

-5,0%

0,0%

5,0%

10,0%

15,0%

1Q-2

009

2Q-2

009

3Q-2

009

4Q-2

009

1Q-2

010

2Q-2

010

3Q-2

010

4Q-2

010

1Q-2

011

2Q-2

011

3Q-2

011

4Q-2

011

1Q-2

012

2Q-2

012

3Q-2

012

4Q-2

012

GDP Construction GDP

Investments in Construction are concentrated in the Mining and Energy industries.

Markets where we operate: Engineering & Construction and Real Estate (Cont.)

Construction Investments per Economic Sector (Chile) *

US$ 110,888 million

Mining59,4%

Energy22,9%

Real Est. Non-household

6,5%Infrastructure

2,7%Industrial

2,8%

Others5,7%

Growth of Construction Investments (Chile) *

54.2

15

77.4

96

89.8

40

97.2

11

95.3

75

110.

888

0

20.000

40.000

60.000

80.000

100.000

120.000

2007 2008 2009 2010 2011 2012

US$

mill

ions

CAGR: 15.4%

(*) Source: Cámara Chilena de la Construcción 11

Markets where we operate: Engineering & Construction and Real Estate (Cont.)

Household Sales in Santiago Market Share in Chile (USD million) (*)

(*) Estimated market calculated as SalfaCorp’s consolidated revenues in Chile over Total Investment in Construction.

Source: Cámara Chilena de la Construcción

0

5

10

15

20

25

30

35

0

10.000

20.000

30.000

40.000

50.000

60.000

Dic

-07

Mar

-08

Jun-

08

Sep-

08

Dic

-08

Mar

-09

Jun-

09

Sep-

09

Dic

-09

Mar

-10

Jun-

10

Sep-

10

Dic

-10

Mar

-11

Jun-

11

Sep-

11

Dic

-11

Mar

-12

Jun-

12

Sep-

12

Dic

-12

months in stock

hous

ehol

d sa

les

and

stoc

k (u

nits

)

Household sales (LTM)Household supplyMonths in stock 76

4

954

1.12

2

1.51

4

1.60

9

2.08

0

3,8%4,5%

5,1%5,8%

6,7%

6,8%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

-

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2.000

2.200

2007 2008 2009 2010 2011 2012

12

Household sales and stock in Santiago represents more than 50% of the market nationwide.

OUR BUSINESS

UNITS

03 13

Salfa Ingeniería y Construcción S.A.

(Engineering & Construction) GROWTH AND PROFITABILITY

FOCUS ON SEGMENTS WITH POTENTIAL

DEMAND GROWTH:

MINING & ENERGY

LARGE PROJECTS

POSITION IN REGIONAL MARKETS WITH

POTENTIAL GROWTH

COMMERCIAL

SPECIALIZED SERVICES WITH VALUE ADDED

AND HIGHER MARGINS:

UNDERGROUND MINING

DRILLING & BLASTING

LONG TERM CONTRACTS

SUSTAINABILITY

CONTROL OF RISKS & PROCEDURES

COST CONTROL

SUPPORTING SYSTEMS (SAP)

DEVELOPMENT OF HUMAN RESOURCES &

COMPETENCIES

Strategic Drivers for each Business Unit

14

Aconcagua S.A.

(Real Estate)

GROWTH AND PROFITABILITY

RELEVANT POSITION NATIONWIDE

“DECOMMODITIZATION” OF SUPPLY THROUGH

INNOVATION

DIFFERENT MECHANISMS OF

ASSOCIATIONS/PARTNERSHIPS

INTEGRATED MANUFACTURING UNITS ALLOWS

BETTER CONTROL OF SUPPLY CHAIN

COMMERCIAL

BETTER UNDERSTANDING OF FINAL CUSTOMER

DIFFERENTIATION: LAGOONS, THERMAL

EFFICIENCY, ETC.

SEGMENTS OF HIGHER VALUE: HOUSING AND

OFFICES

TAKING OPPORTUNITIES ABROAD… GAINING

EXPERIENCE

SUSTAINABILITY

LAND BANK FOR APP. 10 OF LONG TERM

DEVELOPMENT.

SUPPORTING SYSTEMS (SAP)

DEVELOPMENT OF HUMAN RESOURCES &

COMPETENCIES

ENGINEERING &

CONSTRUCTION

BUSINESS UNIT:

“ICSA”

03.1

15

ICSA’s Business Structure

SALFA INGENIERÍA Y CONSTRUCCIÓN S.A.

CHILE PERU PANAMACOLOMBIA

Assembly Works

Civil Works

Assembly Works

Civil Works

Assembly Works

Underground Mining

Industrial Maintenance

Ground Movement

Infrastructure

Drilling & Blasting

Ports Ports

16

AS OF DEC-31-12 SALFA ICSA

REVENUES MM$ 749,265 (MMUS$ 1,561)

EBITDA MM$ 39,850(MMUS$ 83)

ASSETS MM$ 458.403 (MMUS$ 955)

# EMPLOYEES 22.585

INTERNATIONALOPERATIONS

Financial Summary

ICSA consolidating its international presence

17

GDP: +10.6%Backlog: USD 24 mRevenues: USD 39 m

GDP: +4.0%Backlog: USD 15 mRevenues: USD 2 m

GDP: +6.2%Backlog: USD 87 mRevenues: USD 98 m

GDP: +5.4%Backlog: USD 1.2 bnRevenues: USD 1.6 bn

ICSA only consolidates entities in Peru.

Figures of entities in Colombia and Panama of Dec-2012 represent 100% of their

business

Backlog at Dec-2012 practically at the same level as of Dec-2011 (in USD), but mix has

improved

Reduction of Backlog in Units with less value contribution

Backlog ICSA – US$ 1,300 million

1Q-11 2Q-11 3Q-11 4Q-11 1Q-12 2Q-12 3Q-12 4Q-12

89

6.7

1,0

59

.7

1,3

50

.1

1,3

02

.3

1,6

34

.3

1,8

05

.0

1,6

20

.0

1,3

00

.0

Backlog of Contracted Projects

Assembly Works37.0%

Civil Works11.0%

Mining Services45.0%

Interna-tional7.0%

Backlog per Line of Business

(*) Estimado en base al tipo de cambio de cierre de cada período.

• Near MM$412 (US$ 860m) of backlog to be

executed during 2013;

• Close to MM$200 (US$ 420m) for 2014

onwards.

• Backlog of US$ 1,300 million reflects the

strategy to reduce lines of business with

lower margins and focus in more profitable

projects and segments. 18

-

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

450.000

2013 2014 2015+

Assembly Works Mining Services Civil Works

Others International

ICSA – Breakdown of Revenues per Line of Business

Revenues per Line of Business * (Dec-12)

Assembly Works43%

Mining Services

24%Construction19%

International6%

Others7%

19

(*) Mining Services include Earth Movement, Underground Mining and Drilling & Blasting.Construction includes Civil Works and Sothern Zone lines of business.International revenues include only subsidiaries abroad which consolidate (Peru)

Revenues per Line ofBusiness

Dec-2012$ million

Dec-2011$ million

Chg. %

Assembly Works 322.160 226.159 42,4%

Mining Services 180.883 99.054 82,6%

Construction 145.350 235.519 -38,3%

International 46.893 65.729 -28,7%

Others 53.978 44.120 22,3%

Total 749.265 670.581 11,7%

Revenues with good diversification.

Assembly Works and Mining Services drivers of growth.

Highly specialized lines of business with greater value contribution.

20

ICSA: Results as of Dec-12 (in CLP million)

Revenues

ProfitEBITDA / Mg %

Gross Profit / Mg %

3.3%

5.3%

4.7%6.3%

448.

001

590.

867

670.

581

749.

265

Dec-09 Dec-10 Dec-11 Dec-12

46.2

25

50.0

64

47.9

82

57.1

07

Dec-09 Dec-10 Dec-11 Dec-12

28.0

49

28.0

01

21.8

03

39.8

50

Dec-09 Dec-10 Dec-11 Dec-12

20.4

27

15.8

65

3.06

9

10.5

02

Dec-09 Dec-10 Dec-11 Dec-12

7.2%

7.6%8.5%

10.3%

CAGR: -20%CAGR: +12%

CAGR: +19%CAGR: +7%

ICSA: Key Financial Ratios as of Dec-12

21

Liquidity

ROENet Financial Leverage

Leverage

1,891,60 1,54 1,57

Dec-09 Dec-10 Dec-11 Dec-12

1,83 1,822,06 2,16

Dec-09 Dec-10 Dec-11 Dec-12

7.42%

28.57%

19.84%

2.27%

Dec-09 Dec-10 Dec-11 Dec-12

0,35

0,57 0,66

0,91

Dec-09 Dec-10 Dec-11 Dec-12

ICSA: Some of our projects

22

Civil Works; Costanera Center Project, Cencosud

Underground Mining; ADITS Construction, CODELCO

Marine Works; Port Expansion, Puerto de Lirquén

Assembly Works; Acid plant; Ministro Hales Project

REAL ESTATE BUSINESS

UNIT:“ACONCAGUA

”23

03.2

Aconcagua’s Business Structure

24

ACONCAGUA S.A.

100% OwnershipReal Estate

Development

Real Estate Associations with Partners

Real Estate (Inmobiliaria

Aconcagua S.A.)

Home Building(Novatec S.A.)

Other Units (Newall, Vertical,

Noval)

International Division

Financial Summary

AS OF DEC-31-12 ACONCAGUA S.A

REVENUES MM$ 329,927 (MMUS$ 687)

EBITDA MM$ 20,897(MMUS$ 43)

ASSETS MM$ 468,114 (MMUS$ 975)

# EMPLOYEES 10.418

INTERNATIONALOPERATION Miami JV startup

Growth in Pre-sales and Deliveries

Pre-sales Combined (1)

UF millions (3)

Deliveries Combined (2)

UF millions

25

2010 2011 1T - 2012 2T -2012 3T-2012 4T-2012 2012 0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

9.0

12.1

3.34.1 3.6 3.6

14.6

2010 2011 1T - 2012 2T - 2012 3T - 2012 4T- 2012 2012 0.0

2.0

4.0

6.0

8.0

10.0

12.0

8.3 8.4

2.4 1.9 2.1

4.7

11.1

Δ+21% Dec-12 / Dec-11

Δ+32% Dec-12 / Dec-11

(1) Includes pre-sales in Chile and abroad, from businesses which consolidate and do not consolidate. Miami represents app. UF 1 million(2) Only includes projects of Inmobiliaria Aconcagua in Chile.(3) 1UF = USD 48 as of Dec-2012. UF is local currency indexed to inflation; housing prices are denominated in this currency.

Evolution & Seasonality of the Real Estate Business

26

$ million

• Seasonality marked during 4Q of each year• Account Receivables + Inventory correlated with ST debt real estate cash cycle

-

50.000

100.000

150.000

200.000

250.000

300.000

1Q-1

0

2Q-1

0

3Q-1

0

4Q-1

0

1Q-1

1

2Q-1

1

3Q-1

1

4Q-1

1

1Q-1

2

2Q-1

2

3Q-1

2

4Q-1

2

Revenues Acc Rec Inventory Total Fin. Debt

Breakdown of Revenues per Business Segment

Revenues per Segment (Dec-12)

27

Houses29%

Apartments9%

Land16%

Construction43%

Other revenues

3%

Revenues with good diversification.

Construction Revenues reaching a maturity level.

Good land sales, consistent with attractive conditions of the industry and the

large land bank of Aconcagua.

Revenues by ProductDec-2012

M$Dec-2011

M$Var. %

Households 125.152.434 113.343.209 10,4%Land 53.126.854 13.005.681 308,5%Construction 142.384.591 117.312.576 21,4%Other revenues 9.263.007 3.317.366 179,2%Total Revenues 329.926.886 246.978.832 33,6%

In the case of Aconcagua 2009-2012

28

Taking advantage of the opportunities given the upside of the market.

2012’s Margin del 2012 considers a higher cost of land sales as a result of the application of IFRS 3 – Business Combination.

Taking advantage of the opportunities given the upside of the market.

2012’s Margin del 2012 considers a higher cost of land sales as a result of the application of IFRS 3 – Business Combination.

Land Revenues – Comparatives with the market

Good market conditions boosted sales of land during 2012 from all players of the industry.

Good market conditions boosted sales of land during 2012 from all players of the industry.

(*) Source: Superintendencia de Valores y Seguros; Companies’ Financial Statements

$ million Δ%Aconcagua 53.126 13.005 40.121 308,5%Socovesa (*) 45.984 14.747 31.237 211,8%Paz (*) 5.124 1.089 4.035 370,5%Manquehue (*) 37.217 13.652 23.565 172,6%Total 141.451 42.493 98.958 232,9%

$ million 20112012Variation

$ million 2009 2010 2011 2012Land Revenues 11.126 10.416 13.006 53.126 Costs of land 12.015 7.155 9.573 50.081 Gross Mg (889) 3.261 3.433 3.045

Land Rev. Asociations 63 2.010 12.777 2.195 Cost of land Asociations 64 1.993 6.340 1.787 Gross Mg (1) 17 6.437 408

Aconcagua manages approximately 1,700 has. of land for future real estate developments.

Book value as of Dec-2012, reached $ 77 billion vs. a fair value of $ 116 billion as of the same date.

Current volume of land is an important element of Aconcagua’s strategy and strengthens its sustainability for the long term.

As part of its financial strategy, Aconcagua maintains control of its lands with options, agreements and ownership of land.

Land Bank Solid position for long term development

By Geographic Zone

29

Central30%

Northern28%

Southern42%

Aconcagua: Results as of Dec-12 (in CLP million)

30

Revenues Gross Profit / Margin %

EBITDA / Margin % Profit

170.

628

187.

655

246.

979

329.

927

Dec-09 Dec-10 Dec-11 Dec-12

26.8

48

35.1

12

34.9

45

37.0

12

Dec-09 Dec-10 Dec-11 Dec-12

14.1%11.2%

18.7%

15.7%

6.35

2

14.1

22

17.1

49

20.8

97

Dec-09 Dec-10 Dec-11 Dec-12

73 5.88

2

10.6

61

14.5

71

Dec-09 Dec-10 Dec-11 Dec-12

CAGR: +11%

CAGR: +484%CAGR: +49%6.9%

6.3%

7.5%3.7%

CAGR: +25%

31

Liquidity

ROENet Financial Leverage

Leverage

Aconcagua: Key Financial Ratios as of Dec-12

1,75

3,74

2,51

1,25

Dec-09 Dec-10 Dec-11 Dec-12

2,96

2,26 2,533,09

Dec-09 Dec-10 Dec-11 Dec-12

0,09%

7,73%

12,76%

15,55%

Dec-09 Dec-10 Dec-11 Dec-12

2,00 1,78 1,702,18

Dec-09 Dec-10 Dec-11 Dec-12

32

Aconcagua: Some of our projects

Live Costanera Building, Metropolitan Region

Deloitte Building, Metropolitan Building Laguna del Mar Project, La Serena, 4th Region

Punta Águila Project, Metropolitan Region

SALFACORPCONSOLIDAT

EDFINANCIALS

33

03.3

SalfaCorp: Balance Sheet as of Dec-2012

34

$ Million %

Current assets 562.111 453.668 108.443 23,9%Cash and cash equivalents 31.989 45.271 (13.282) -29,3%Trade and other current receivables 257.553 184.592 72.961 39,5%Current related parties receivables 36.603 38.346 (1.743) -4,5%Inventories 208.521 160.829 47.693 29,7%Others 27.445 24.631 2.814 11,4%

Non-current assets 411.305 346.051 65.253 18,9%Non-current inventories 54.370 21.005 33.365 158,8%Non-current related parties receivables 27.357 29.593 (2.236) -7,6%Investments in related companies 35.233 32.564 2.670 8,2%Intangible assets other than goodwill 69.686 54.749 14.937 27,3%Goodwill 24.093 35.202 (11.110) -31,6%Property, plant and equipment 80.202 74.313 5.889 7,9%Investment property 77.467 60.669 16.798 27,7%Non-current tax assets 8.271 6.985 1.286 18,4%Deferred tax assets 28.830 27.501 1.329 4,8%Others 5.797 3.471 2.326 67,0%

Total assets 973.416 799.720 173.696 21,7%

Current liabilities 403.094 239.456 163.638 68,3%Other current financial liabilities

Financing of land 10.175 0 10.175 - Other financing 175.189 20.883 154.307 738,9%

Trade and other current payables 143.815 137.275 6.540 4,8%Current tax liabilities 21.009 17.862 3.147 17,6%Other current non-financial liabilities 49.302 55.105 (5.803) -10,5%Others 3.604 8.331 (4.727) -56,7%

Non-current liabilities 265.261 287.015 (21.754) -7,6%Other non-current financial liabilities

Financing of land 31.558 17.787 13.771 77,4%Other financing 190.007 241.856 (51.849) -21,4%

Other accounts payable 1.733 2.078 (345) -16,6%Deferred tax liabilities 21.176 16.631 4.545 27,3%Others 20.787 8.662 12.125 140,0%

Equity attributable to parent company 281.599 265.741 15.858 6,0%Non-controlling interests 23.461 7.507 15.954 212,5%Total equity 305.061 273.249 31.812 11,6%Total equity and liabilities 973.416 799.720 173.696 21,7%

Balance Sheet$ Million of each period

Dec-12 Dec-11 Change

SalfaCorp: P&L as of Dec-2012

35

$ Mill %

Revenues 1.062.636 901.465 161.171 17,9%Gross profit 92.776 85.522 7.254 8,5%

% of revenues 8,7% 9,5%Other income 15.795 746 15.050 2018,0%Selling & administrative expenses (62.087) (53.669) (8.419) 15,7%

% of revenues -5,8% -6,0%Operating profit 46.484 32.600 13.884 42,6%

% of revenues 4,4% 3,6%

Non-operating profit (18.628) (11.783) (6.845) 58,1%Other gains (losses) (62) 1.643 (1.705) -103,8%Finance costs net of Finance income (14.203) (12.638) (1.565) 12,4%Share of profit (loss) of associates and joint 492 3.733 (3.241) -86,8%Exchange rate differences (742) 441 (1.183) -268,2%Gains (losses) from readjustable units (4.113) (4.963) 850 -17,1%

Income tax expense (2.139) (3.487) 1.347 -38,6%

Profit (loss), Parent Company 23.182 15.933 7.250 45,5%% of revenues 2,2% 1,8%

EBITDA 59.776 41.027 18.749 45,7%% of revenues 5,6% 4,6%

EBITDA Adjusted 60.268 44.760 15.508 34,6%% of revenues 5,7% 5,0%

ChangeDec-12 Dec-11

P&L Statement($ million of each period)

36

SalfaCorp: Consolidated Financials as of Dec-12 (in CLP million)

Revenues

ProfitEBITDA

Gross Profit / Mg

+46%

+18% +9%

+46%

901.465

1.062.636

Dec-11 Dec-12

85.522

92.776

Dec-11 Dec-12

9,5% 8,7%

41.027

59.776

Dec-11 Dec-12

4,6% 5.6%

15.933

23.182

Dec-11 Dec-12

37

Liquidity

ROENet Financial Leverage

Leverage

SalfaCorp: Key Consolidated Ratios as of Dec-12

1,89

1,39

Dec-11 Dec-12

1,932,19

Dec-11 Dec-12

0,86

1,23

Dec-11 Dec-12

6,00%

8,23%

Dec-11 Dec-12

TOPICS OF INTERST04

38

39

ICSASubsidiary

Sector Engineering & Construction Real Estate

Main Elements

• Highly specialized labor force• Focus on specialized construction• Lower number of customers: B2B• Dependent on productive investment,

mainly mining, energy, forestry and industrial

• Development of real estate projects• Search for value-added products• High number of customers: B2C• Dependent on level of interest rates,

employment, access to mortgages and economic growth

Use of capital Low High

Level of Debt Low High

Recent Events … Company is evaluating the division of SalfaCorp into two separate and publicly traded business units

Division of SalfaCorp - Rationale

40

FOCUS

Profitability in each business Higher management control of

the business. Strategic & Operational.

Specialization in each business: Management and Board

of Directors. Business Model. TI systems to support

management.

FINANCING

Different needs of financial resources.

Different capital structure E&C less leveraged. Real estate more working capital

intensive and higher leveraged in order to be profitable.

Different groups of investors.

GROWTH

Both Business Units are in a stage of growth.

They have reached such an operational scale in order to operate independently.

Different business strategies, thus Investment Plans.

Each company could capitalize growth opportunities in a better approach.

Aconcagua has its own Construction unit (Novatec) in the Real Estate business since 2 years ago Operating synergies between Real Estate and Novatec have already been achieved.

Management is currently working as two independent companies There are two Executive Vice-presidents in charge of these companies Each structure operates independently There are no synergy losses The cost of this division is not significant

FINAL COMMENTS

05 41

Final Comments

SalfaCorp, a company with a leading position in the Engineering & Construction

and Real Estate sectors in Chile.

Both Business Units have a diversified source of revenues.

In a good position for year 2013 and those to come.

ICSA:

Focus on Profitability lines of business with better margins – Assembly

Works and Mining Services. Reduction of lines with lower returns.

Good Backlog Longer contracts and more focused.

Positioned to continue international growth

Aconcagua:

Differentiation Strategy successfully continues its course.

Solid land bank position for long term development.

Good Backlog value added projects.

42

SALFACORP PRESENTATION

III CHILE EQUITY ONE ON ONE CONFERENCE – LONDON, MAY 2013

www.salfacorp.com