rystad energy gas perspectives -...

TRANSCRIPT

RYSTAD ENERGY GAS PERSPECTIVES

Jakarta, November 20th 2017

Agenda

1. Global LNG market outlook – Oversupply and new Asian demand2. Japan LNG Market outlook – LNG demand in a nuclear restart

2

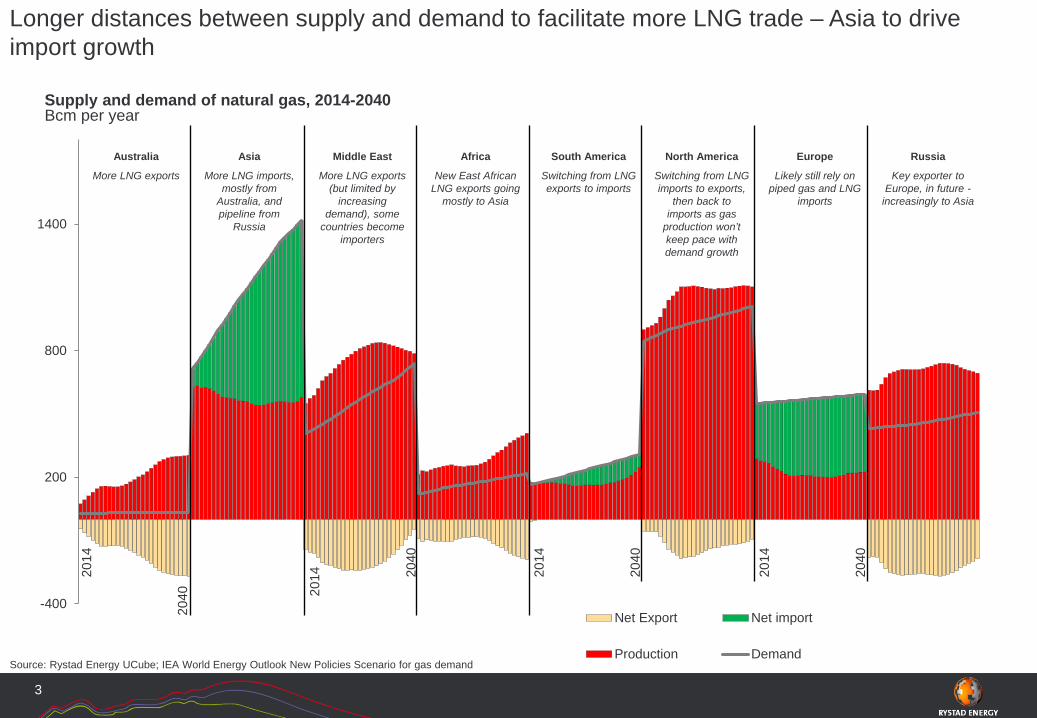

Longer distances between supply and demand to facilitate more LNG trade – Asia to drive import growth

-400

200

800

1400

Net Export Net import

Production DemandSource: Rystad Energy UCube; IEA World Energy Outlook New Policies Scenario for gas demand

3

Supply and demand of natural gas, 2014-2040Bcm per year

Australia Asia Middle East Africa South America North America Europe Russia

More LNG exports More LNG imports, mostly from

Australia, and pipeline from

Russia

More LNG exports (but limited by

increasing demand), some

countries become importers

New East African LNG exports going

mostly to Asia

Switching from LNG imports to exports,

then back to imports as gas

production won’t keep pace with demand growth

Switching from LNG exports to imports

Likely still rely on piped gas and LNG

imports

Key exporter to Europe, in future -

increasingly to Asia

2014

2040

2014

2040

2014 20

40

2014

2040

0

50

100

150

200

250

Philippines Malaysia/Thailand JDAVietnam BruneiMyanmar

0

20

40

60

80

100

120

India Pakistan Bangladesh

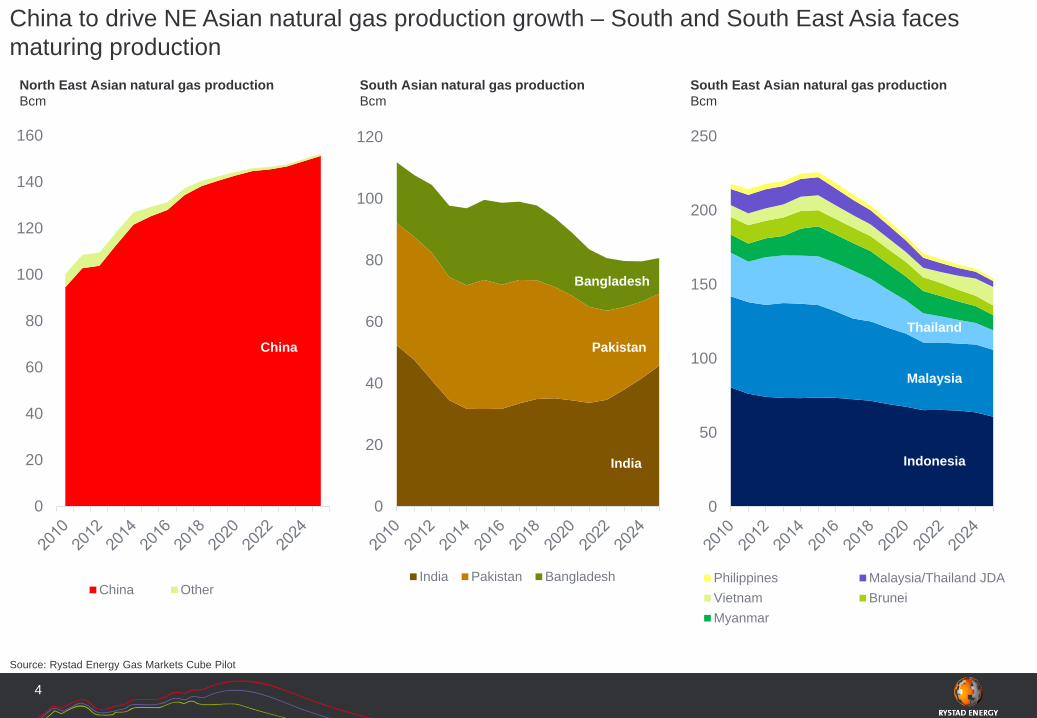

China to drive NE Asian natural gas production growth – South and South East Asia faces maturing production

Source: Rystad Energy Gas Markets Cube Pilot

4

0

20

40

60

80

100

120

140

160

China Other

North East Asian natural gas productionBcm

South Asian natural gas productionBcm

South East Asian natural gas productionBcm

China Pakistan

India

Bangladesh

Indonesia

Malaysia

Thailand

0

20

40

60

80

100

120

140

160

180

Production LNG demand

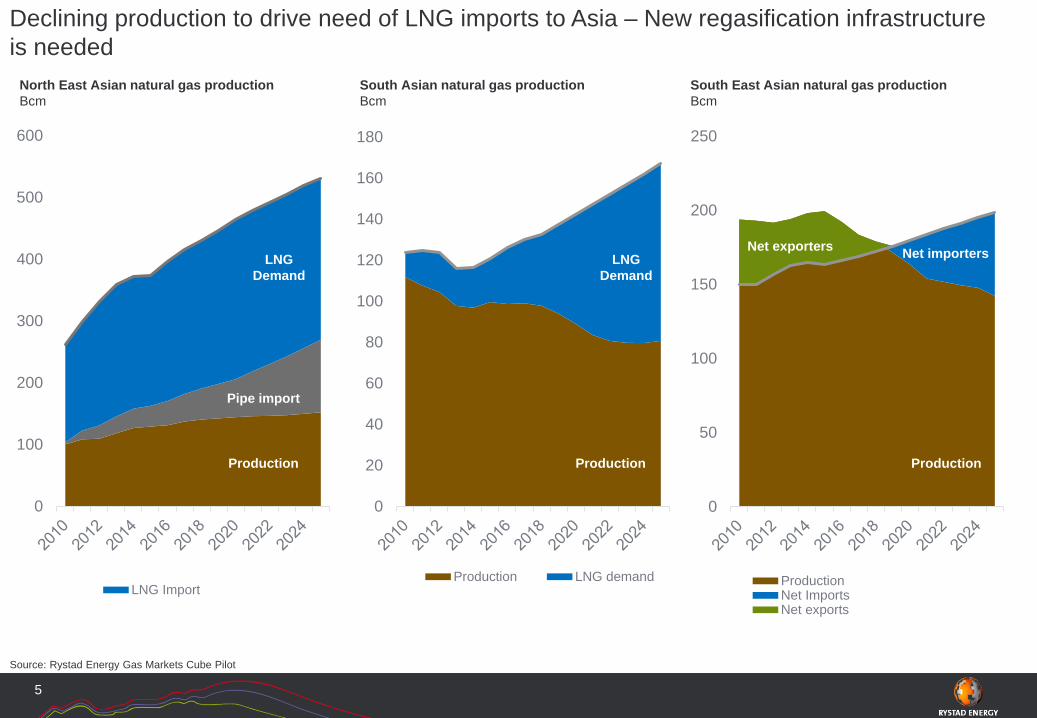

Declining production to drive need of LNG imports to Asia – New regasification infrastructure is needed

Source: Rystad Energy Gas Markets Cube Pilot

5

0

100

200

300

400

500

600

LNG Import

North East Asian natural gas productionBcm

South Asian natural gas productionBcm

South East Asian natural gas productionBcm

Production

LNG Demand

Indonesia

Malaysia

Thailand

0

50

100

150

200

250

ProductionNet ImportsNet exports

Net exporters Net importers

Production

LNG Demand

Pipe import

Production

0

50

100

150

200

250

300

350

400

45020

10

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Qatar

Australia

United States

Russia

Indonesia

Malaysia

Nigeria

Algeria

Trinidad and Tobago

Papua New Guinea

Other

17%

20%

20%

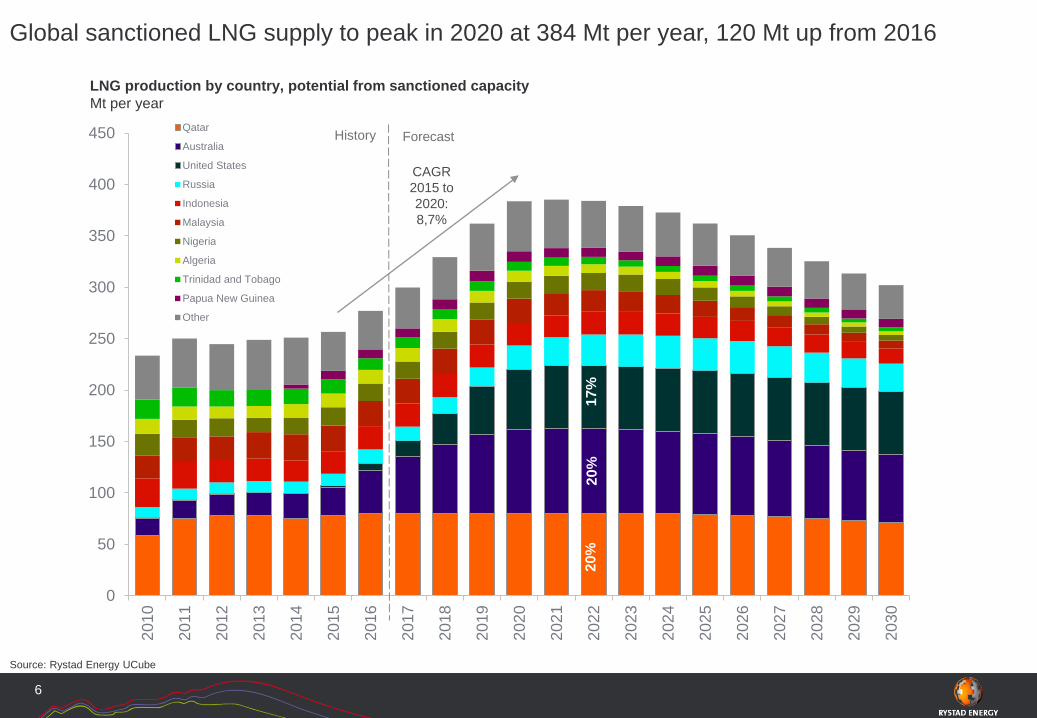

Global sanctioned LNG supply to peak in 2020 at 384 Mt per year, 120 Mt up from 2016

LNG production by country, potential from sanctioned capacityMt per year

Source: Rystad Energy UCube

6

ForecastHistory

CAGR 2015 to 2020:8,7%

Source: Rystad Energy UCube

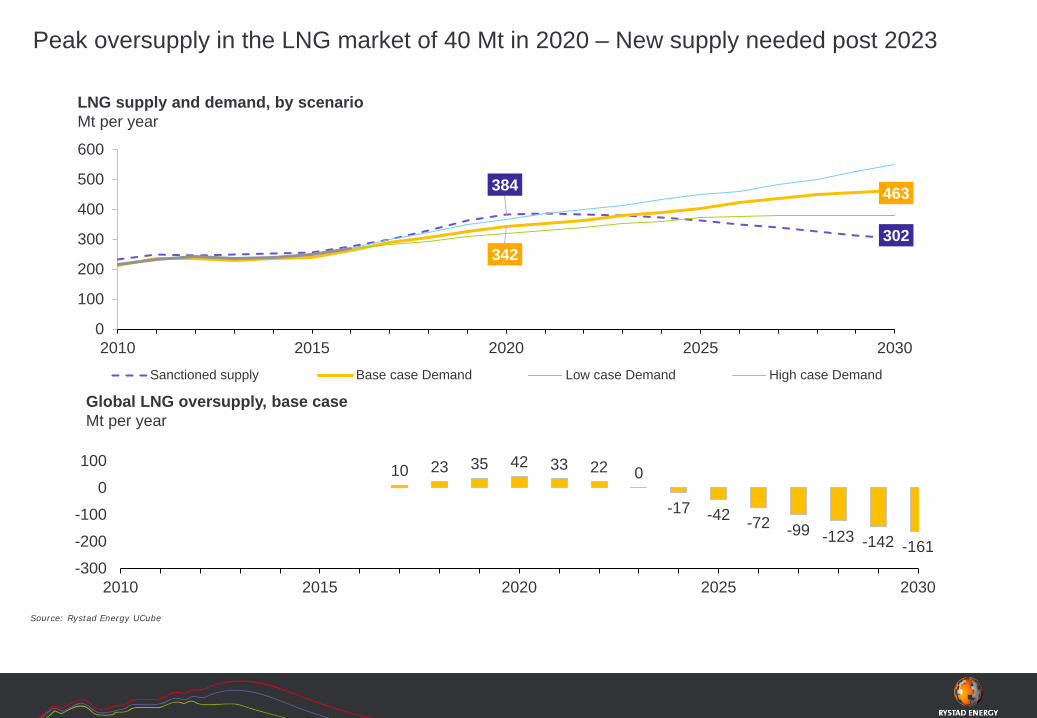

LNG supply and demand, by scenarioMt per year

384

302342

463

0

100

200

300

400

500

600

2010 2015 2020 2025 2030Sanctioned supply Base case Demand Low case Demand High case Demand

10 23 35 42 33 22 0

-17 -42 -72 -99 -123 -142 -161-300

-200

-100

0

100

2010 2015 2020 2025 2030

Global LNG oversupply, base caseMt per year

Peak oversupply in the LNG market of 40 Mt in 2020 – New supply needed post 2023

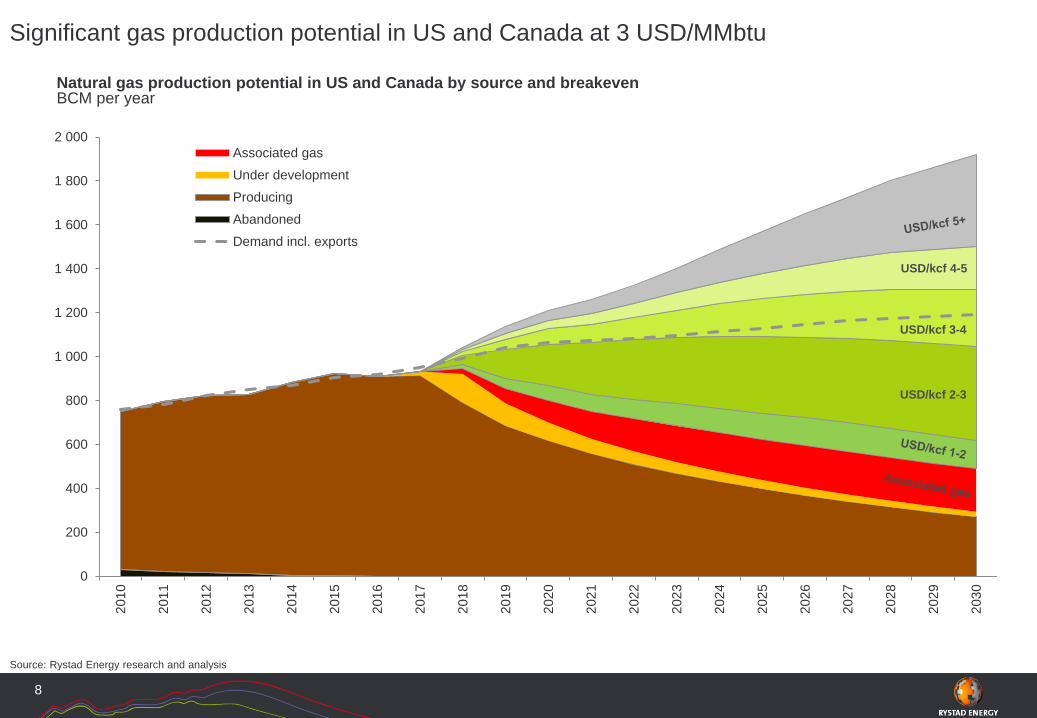

Significant gas production potential in US and Canada at 3 USD/MMbtu

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 00020

10

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Associated gasUnder developmentProducingAbandonedDemand incl. exports

Source: Rystad Energy research and analysis

8

Natural gas production potential in US and Canada by source and breakevenBCM per year

USD/kcf 4-5

USD/kcf 2-3

USD/kcf 3-4

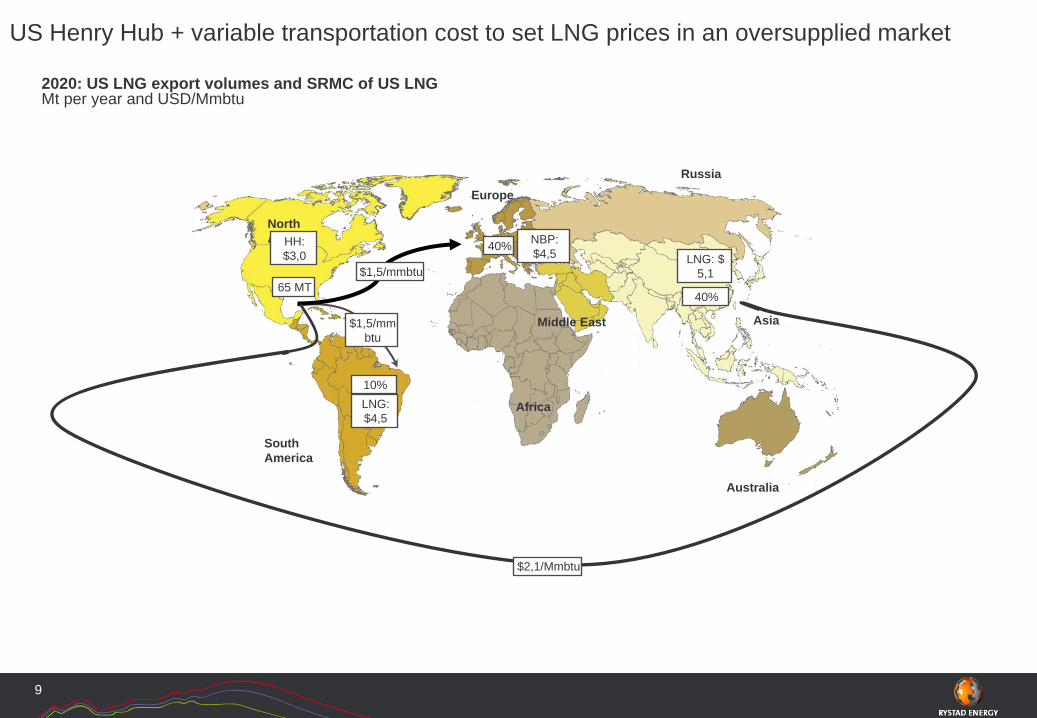

US Henry Hub + variable transportation cost to set LNG prices in an oversupplied market

9

2020: US LNG export volumes and SRMC of US LNGMt per year and USD/Mmbtu

Australia

Asia

South America

North America

EuropeRussia

Middle East

Africa

65 MT$1,5/mmbtu

$2,1/Mmbtu

$1,5/mmbtu

10%

40%

40%LNG: $

5,1

LNG: $4,5

HH: $3,0

NBP: $4,5

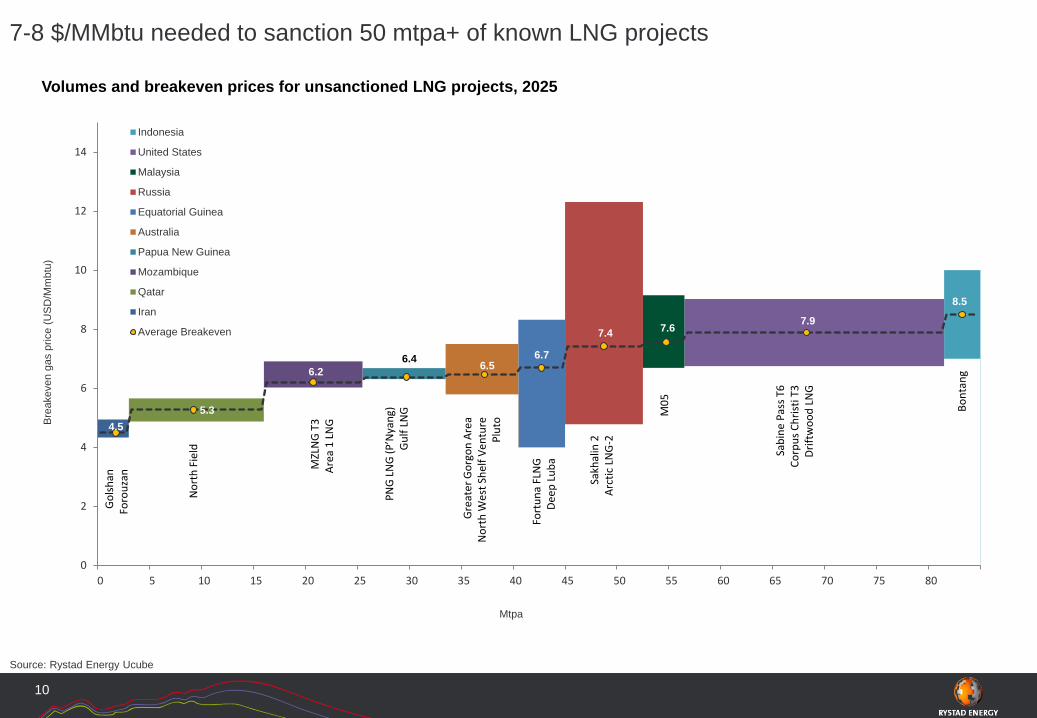

7-8 $/MMbtu needed to sanction 50 mtpa+ of known LNG projects

Source: Rystad Energy Ucube

10

4.55.3

6.26.4 6.5

6.7

7.4 7.6 7.9

8.5

0

2

4

6

8

10

12

14

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80

Bre

akev

en g

as p

rice

(US

D/M

mbt

u)

Mtpa

Indonesia

United States

Malaysia

Russia

Equatorial Guinea

Australia

Papua New Guinea

Mozambique

Qatar

Iran

Average Breakeven

Volumes and breakeven prices for unsanctioned LNG projects, 2025 G

olsh

anFo

rouz

an

MZL

NG

T3

Area

1 L

NG

Gre

ater

Gor

gon

Area

Nor

th W

est S

helf

Vent

ure

Plut

o

PNG

LNG

(P’N

yang

)G

ulf L

NG Bo

ntan

g

M05

Sakh

alin

2Ar

ctic

LN

G-2

Sabi

ne P

ass T

6Co

rpus

Chr

isti T

3Dr

iftw

ood

LNG

Nor

th F

ield

Fort

una

FLN

GDe

ep L

uba

5,1

7,5 7,5

4,5

7,5 7,5

3,0 3,1 3,3

0

50

100

150

200

250

300

350

400

450

500

0

2

4

6

8

10

12

14

16

18

20

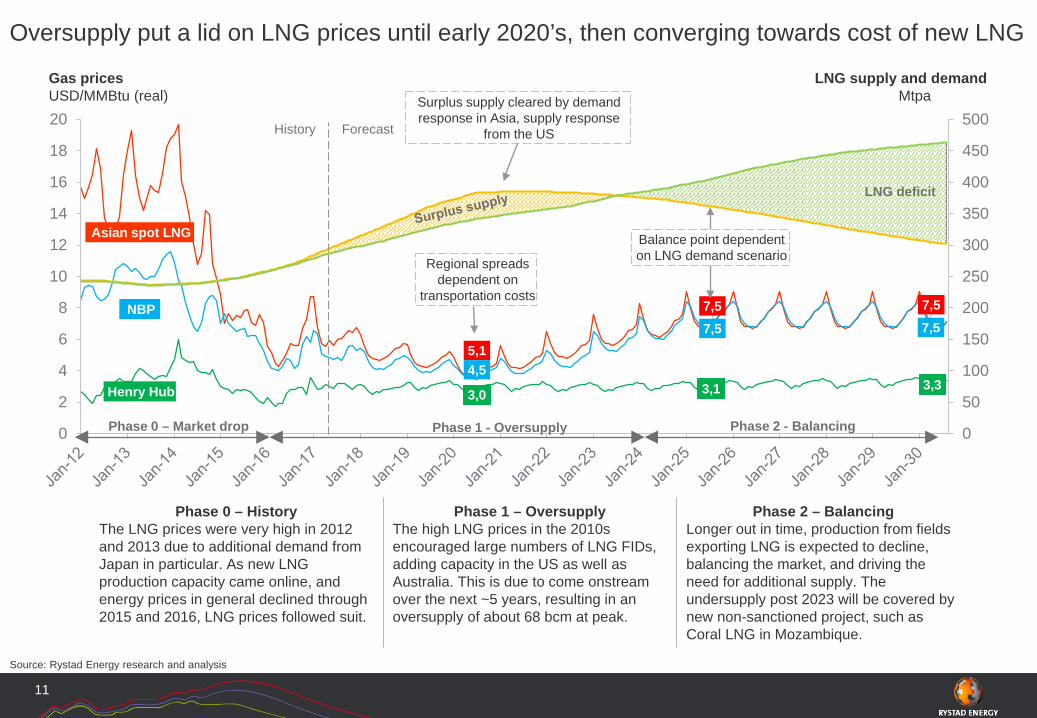

Oversupply put a lid on LNG prices until early 2020’s, then converging towards cost of new LNG

Source: Rystad Energy research and analysis

11

ForecastHistory

Phase 1 - Oversupply Phase 2 - Balancing

Phase 0 – HistoryThe LNG prices were very high in 2012 and 2013 due to additional demand from Japan in particular. As new LNG production capacity came online, and energy prices in general declined through 2015 and 2016, LNG prices followed suit.

Phase 1 – OversupplyThe high LNG prices in the 2010s encouraged large numbers of LNG FIDs, adding capacity in the US as well as Australia. This is due to come onstream over the next ~5 years, resulting in an oversupply of about 68 bcm at peak.

Phase 2 – BalancingLonger out in time, production from fieldsexporting LNG is expected to decline, balancing the market, and driving the need for additional supply. The undersupply post 2023 will be covered by new non-sanctioned project, such as Coral LNG in Mozambique.

Phase 0 – Market drop

Gas prices LNG supply and demandUSD/MMBtu (real) Mtpa

NBP

Henry Hub

Asian spot LNG

LNG deficit

Surplus supply cleared by demand response in Asia, supply response

from the US

Balance point dependent on LNG demand scenarioRegional spreads

dependent on transportation costs

Agenda

1. Global LNG market outlook – Oversupply and new Asian demand2. Japan LNG Market outlook – LNG demand in a nuclear restart

12

• The world’s largest LNG importer, with over 200 mtpa in import capacity

• Import most of its natural gas consumption

• LNG imports surged after Tohoku earthquake in 2011 leading to shutdown of nuclear power plants

• Gas for power is the main driver of LNG imports into Japan

LNG demand increased 17% in 2011 due to nuclear shut down

Source: Japan Gas Association, Japanese import statistics, Rystad Energy research and analysis

Japan total gas demand (mtpa) and average LNG import prices (USD/MMBtu)

13

-

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

70

80

90

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USD

/MM

Btu

mtp

a

Gas for power & heat Industry Residential & Commercial

Others Average LNG import prices

17%

• Rystad Energy’s base case: 12 out of 26 reactors initially under review become operational by 2020

• Another six reactors likely to restart by 2025, adding 15.8 GW of nuclear capacity or 10% of Japanese power generation in 2025

• Rystad Energy’s high case scenario assuming faster restarts, we expect 26 reactors to come online by 2025, adding 25 GW of capacity. This equates to power generation of about 160 TWh (16% of power generation in 2025)

2015 – 2025: Nuclear restart resets Japanese energy sector

Source: Rystad Energy research and analysis

Nuclear restart – Base case (GW)

14

15.8

1.70.8

2.8

3.01.1

1.60.8

0.80.6

1.90.9

0

5

10

15

20

25

30

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2025Total

Before Fukushima 48,8

25High case

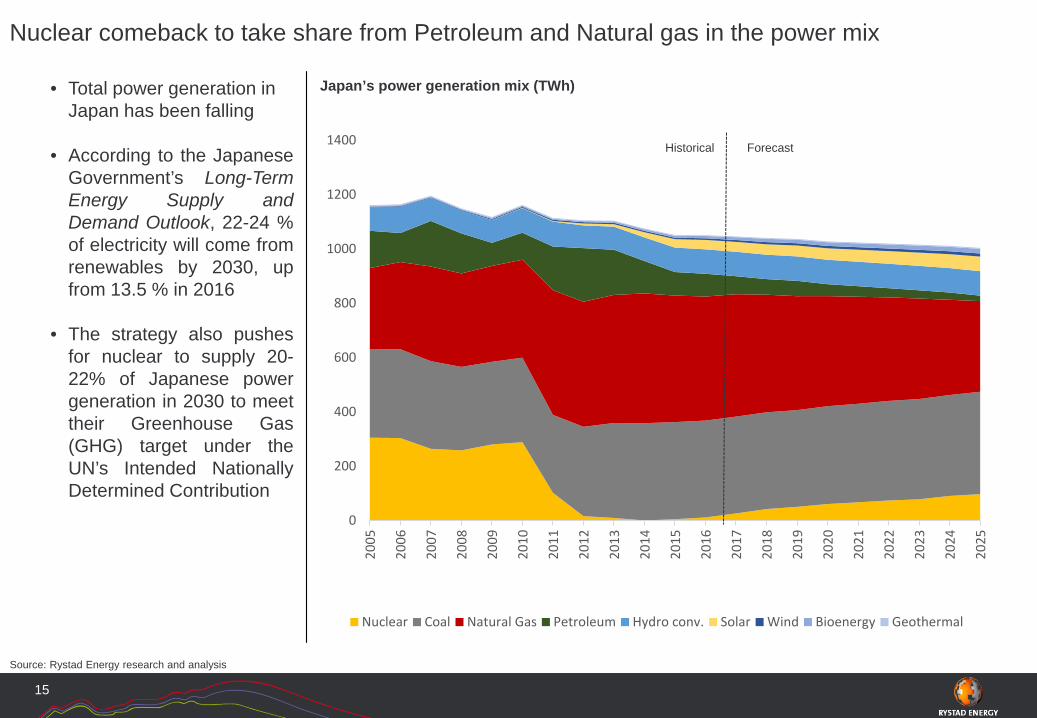

• Total power generation in Japan has been falling

• According to the JapaneseGovernment’s Long-TermEnergy Supply andDemand Outlook, 22-24 %of electricity will come fromrenewables by 2030, upfrom 13.5 % in 2016

• The strategy also pushesfor nuclear to supply 20-22% of Japanese powergeneration in 2030 to meettheir Greenhouse Gas(GHG) target under theUN’s Intended NationallyDetermined Contribution

Nuclear comeback to take share from Petroleum and Natural gas in the power mix

Source: Rystad Energy research and analysis

Japan’s power generation mix (TWh)

15

0

200

400

600

800

1000

1200

1400

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Nuclear Coal Natural Gas Petroleum Hydro conv. Solar Wind Bioenergy Geothermal

Historical Forecast

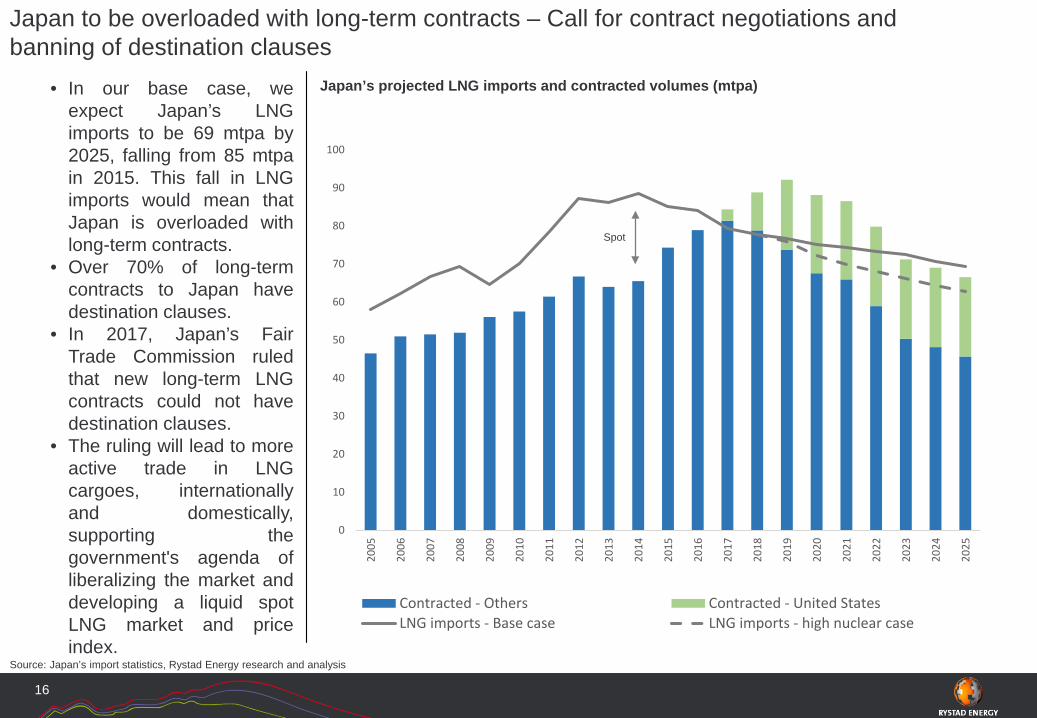

• In our base case, weexpect Japan’s LNGimports to be 69 mtpa by2025, falling from 85 mtpain 2015. This fall in LNGimports would mean thatJapan is overloaded withlong-term contracts.

• Over 70% of long-termcontracts to Japan havedestination clauses.

• In 2017, Japan’s FairTrade Commission ruledthat new long-term LNGcontracts could not havedestination clauses.

• The ruling will lead to moreactive trade in LNGcargoes, internationallyand domestically,supporting thegovernment's agenda ofliberalizing the market anddeveloping a liquid spotLNG market and priceindex.

Japan to be overloaded with long-term contracts – Call for contract negotiations and banning of destination clauses

Source: Japan’s import statistics, Rystad Energy research and analysis

Japan’s projected LNG imports and contracted volumes (mtpa)

16

0

10

20

30

40

50

60

70

80

90

100

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Contracted - Others Contracted - United StatesLNG imports - Base case LNG imports - high nuclear case

Spot

0

20

40

60

80

100

0

2

4

6

8

10

12

14

16

1820

10

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

USD

/bbl

USD

/MM

Btu

Henry Hub NBP

East Asian spot LNG JCC-indexed (14%)

Brent crude history Brent crude - Rystad Energy's base case

Spread between oil-linked gas contracts and LNG spot to widen as oil prices increase -Pressure for long-term contract renegotiation and gas-to-gas price indexation

Global gas prices (USD/MMBtu) and Brent crude price (USD/bbl), Real

Source: Rystad Energy research and analysis

17

ForecastHistorical

*Prices are real, annual average, assuming normal weather without seasonal variations. East Asian Spot LNG excludes regasification cost. Brent crude price forecast is Rystad Energy’s base case scenario. JCC-indexed is linked to Brent crude with a lag – History is based on historical Brent crude and Forecast is based on Rystad Energy’s Brent base case forecast. Brent crude forward as of 26 Apr 2017.

Gap JCC-LNG Spot call for renegotiations?

DATA SOURCES

Jakarta, November 20th 2017

POWER CUBEPOWER CAPACITIES AND PRODUCTION, ASSET BY ASSET

Tailored presentations and discussions

Source: Gas Markets Cube Pilot

GAS MARKETS CUBETHE NATURAL GAS VALUE CHAIN FROM UPSTREAM ASSET TO CONSUMERS SECTOR

Tailored presentations and discussions

GAS MARKETS SOLUTIONS

Quarterly Report

Onsiteworkshops

Tailored presentations and discussions

Medium and long-term gas market outlook

Weekly/ Monthly

commentsMonthly natural gas commentaries

Gas Markets Cube

Supply, demand, balance and trade