ryobi kiso holdings ltd. - listed...

TRANSCRIPT

CIRCULAR DATED 4 JANUARY 2012

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION

If you are in any doubt as to the action you should take, you should consult your stockbroker(s), bank manager, solicitor, accountant, fi nancial, tax or other professional adviser(s) immediately.

If you have sold or transferred all your shares in the capital of Ryobi Kiso Holdings Ltd. (the “Company”), you should forward this Circular with the Notice of Extraordinary General Meeting and the accompanying Proxy Form immediately to the purchaser or transferee or to the agent through whom the sale or transfer was effected for onward transmission to the purchaser or transferee.

The Singapore Exchange Securities Trading Limited assumes no responsibility for the correctness of any of the statements made, reports contained or opinions expressed in this Circular.

RYOBI KISO HOLDINGS LTD. (Incorporated in the Republic of Singapore)

(Company Registration No. 200803985D)

CIRCULAR TO SHAREHOLDERS

in relation to

THE PROPOSED EXPANSION OF THE CORE BUSINESS OF THE GROUP TO INCLUDE THE PROPERTY DEVELOPMENT, TRADING AND INVESTMENT BUSINESS

IMPORTANT DATES AND TIMES:

Last date and time for lodgement of Proxy Form : 17 January 2012 at 10:00 a.m. Date and time of Extraordinary General Meeting : 19 January 2012 at 10:00 a.m.

Place of Extraordinary General Meeting : 6 Battery Road, #10-01, Singapore 049909

2

TABLE OF CONTENTS

Page

DEFINITIONS ...................................................................................................................................... 3

LETTER TO SHAREHOLDERS

1. INTRODUCTION ....................................................................................................................... 5

2. PROPOSED EXPANSION OF THE CORE BUSINESS OF THE GROUP TO INCLUDE THE PROPERTY BUSINESS ................................................................................................... 5

3. SGX-ST LISTING MANUAL ...................................................................................................... 23

4. INTERESTS OF DIRECTORS AND SUBSTANTIAL SHAREHOLDERS ................................. 24

5. DIRECTORS’ RECOMMENDATION ......................................................................................... 24

6. EXTRAORDINARY GENERAL MEETING ................................................................................ 24

7. ACTION TO BE TAKEN BY SHAREHOLDERS ........................................................................ 24

8. DIRECTORS’ RESPONSIBILITY STATEMENT ........................................................................ 25

9. INSPECTION OF DOCUMENTS .............................................................................................. 25

NOTICE OF EXTRAORDINARY GENERAL MEETING ..................................................................... 26

PROXY FORM

3

DEFINITIONS

In this Circular, the following words and phrases shall have the meanings set out against them unless the context otherwise requires:

“Act” or “Companies Act” The Companies Act, Chapter 50 of Singapore, as modified, supplemented or amended from time to time

“APSTP” Ascendas-Protrade Singapore Tech Park, Binh Duong Province, Vietnam “Articles” The Articles of Association of the Company “Associate” Shall have the same meaning as defi ned in the SGX-ST Listing Manual

or any other publication prescribing rules or regulations for corporations admitted to the Offi cial List of the SGX-ST as modifi ed, supplemented or amended from time to time

“Associated Company” A company in which at least 20% but not more than 50% of its shares are

held by the Company or the Group “Board” The board of Directors of the Company “CDP” The Central Depository (Pte) Limited “Code” The Singapore Code of Takeovers and Mergers, as amended or modifi ed

from time to time “Company” or “Ryobi Kiso” Ryobi Kiso Holdings Ltd. “Controlling Shareholder” A person who:

(a) holds directly or indirectly 15% or more of the nominal amount of all voting shares in the Company; or

(b) in fact exercises control over a Company “Director” A director of the Company for the time being “EGM” The extraordinary general meeting of the Company, the notice of which is

set out on page 2 6 of this Circular “EPS” Earnings per Share “Financial Year” or “FY” The fi nancial year ended or ending 30 June, as the case may be “Group” The Company and its subsidiaries collectively “Latest Practicable Date” or 23 December 2011, being the latest practicable date prior to the“LPD” printing of this Circular “Listing Manual” The Listing Manual of the SGX-ST as modified, supplemented or

amended from time to time “Listing Rules” The listing rules of the SGX-ST as set out in the Listing Manual as

modifi ed, supplemented or amended from time to time “Market Day” A day on which the SGX-ST is open for trading in securities

4

DEFINITIONS

“Memorandum” The Memorandum of Association of the Company “Property Business” Has the meaning ascribed to it in Section 1.1 of this Circular “n.m.” Not meaningful “NTA” Net tangible assets “Raffl es Piling Vietnam” Raffl es Piling Vietnam Company Limited (a wholly owned subsidiary of

the Company) “Ryobi Development” Ryobi Development Pte. Ltd. (a wholly owned subsidiary of the Company) “SGX-ST” The Singapore Exchange Securities Trading Limited “Shareholders” Registered holders of the Shares except that where the registered holder

is CDP, the term “Shareholders” shall, in relation to such Shares, mean the persons whose direct securities accounts maintained with CDP are credited with the Shares

“Shares” Ordinary shares in the capital of the Company “Subsidiary” or “Subsidiaries” Has the meaning ascribed to it in Section 5 of the Act “%” or “per cent” Per centum or percentage “S$” and “cents” Singapore dollars and cents, respectively “USD” United States dollars “VND” Vietnam Dong

The terms “Depositor”, “Depository Agent” and “Depository Register” shall have the meanings ascribed to them respectively in Section 130A of the Act.

Words importing the singular shall, where applicable, include the plural and vice versa, and words importing the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall, where applicable, shall include corporations.

Any reference in this Circular to any enactment is a reference to that enactment as for the time being amended or re-enacted. Any term defi ned under the Act or the Listing Manual or any statutory modifi cation thereof and used in this Circular shall, where applicable, have the same meaning assigned to it under the Act or the Listing Manual or any statutory modifi cation thereof, unless otherwise provided.

Any discrepancies in the fi gures included herein between the listed amounts and totals thereof are due to rounding. Accordingly, fi gures shown as totals in this Circular may not be an arithmetic aggregation of the fi gures that precede them.

Any reference to a time of day in this Circular shall be a reference to Singapore time unless otherwise stated.

5

LETTER TO SHAREHOLDERS

Ryobi Kiso Holdings Ltd.(Incorporated in the Republic of Singapore)(Company Registration No.: 200803985D)

Directors Registered Offi ce

Lee Yiok Seng@ Lee Geok Seng@Lee Yok Seng

Chairman and Non-Executive Director 58A Sungei Kadut Loop Ryobi Industrial BuildingSingapore 729505

Ong Tiong Siew Chief Executive Offi cer and Executive Director Ong Teng Choon Executive Director Lai Chin Yee Lead Independent DirectorLau Teik Soon Independent Director

4 January 2012

To: The Shareholders of Ryobi Kiso Holdings Ltd.

Dear Sir/Madam,

THE PROPOSED EXPANSION OF THE CORE BUSINESS OF THE GROUP TO INCLUDE THE PROPERTY DEVELOPMENT, TRADING AND INVESTMENT BUSINESS

1. INTRODUCTION

1.1 The Directors are convening an EGM to be held on 19 January 2012 to seek Shareholders’ approval for the expansion of the core business of the Group to include the investment in and trading of, and development of residential, commercial and industrial properties within Singapore and overseas (“Property Business”) (the “Proposal”).

1.2 The purpose of this Circular is to provide Shareholders with relevant information pertaining to the

Proposal to be tabled at the EGM and to seek Shareholders’ approval for the resolution relating to the same. The notice of the EGM is set out on page 26 of this Circular.

1.3 The SGX-ST assumes no responsibility for the correctness of any of the statements made, reports contained or opinions expressed in this Circular.

2. PROPOSED EXPANSION OF CORE BUSINESS OF THE GROUP TO INCLUDE THE PROPERTY BUSINESS

2.1 Introduction and Rationale

Presently, the principal business of the Group comprises bored piling, eco-friendly piling and geoservices, which are mainly carried out in Singapore (the “Current Core Business”). The Group intends to expand its core business to include the Property Business, in order to offer better prospects and returns to Shareholders, as well as to leverage on the expertise the Group has developed through its Current Core Business. Currently, the Company intends to embark on Property Business in Vietnam. However, the Company does not plan to restrict the Property Business to any specifi c markets as each project and investment would be evaluated and assessed by the Board on its own merits.

6

LETTER TO SHAREHOLDERS

The expansion of the Group’s core businesses forms part of its business development and diversifi cation strategy. In particular, the Group has decided to embark on the Property Business for the following reasons:

2.1.1 the expansion would provide Shareholders with diversifi ed returns and would contribute to a potential upstream capability of the Group in the construction industry. In all property development projects undertaken by the Group under the Property Business, the Group would be able to maximise the revenue generated from such projects. Besides the revenue generated from the sale of the development units, the Group also has an option to award the construction and piling works in relation to the development projects to the relevant companies within the Group, and accordingly secure and generate additional revenue from such development projects. This will contribute to an additional stream of the revenue to the Current Core Business;

2.1.2 the Property Business would allow the Group to participate in the growth prospects of the property development and investment industry in Singapore and overseas, for example, Vietnam, where the Company has established its presence via its wholly-owned subsidiary, Raffl es Piling Vietnam, since 2009. To date, Raffl es Piling Vietnam has secured fi ve piling contracts in Vietnam, three of which had been successfully completed. As a developing country, Vietnam’s construction sector’s outlook appears promising given its present and future requirements for property. To ensure that the Company’s venture in Vietnam proceeds smoothly, the Board has put in place a management team who is familiar with Vietnam operations and laws. For more information on the management team, please refer to Section 2.7.3 of this Circular; and

2.1.3 the Property Business is complementary to the Current Core Business as both the Property Business and the Current Core Business require project management expertise such as ensuring timeliness of delivery, skill in managing labour, skill in managing construction process and ability to manage construction costs, including the costs of labour and costs of materials. Due to these similarities, the Group can leverage on the expertise and knowledge of its management team in the construction industry as well as its network of contacts with main contractors, sub-contractors, project consultants, and building material suppliers to meet requirements for the proposed Property Business.

2.2 Prospects and future plans for the Property Business

2.2.1 The Group may venture into the following Property Business activities as and when the suitable opportunity arises:

(i) undertake property development activities in the residential, commercial and industrial sectors;

(ii) acquire and hold investments in property related assets, including buying and selling properties and/or acquiring or developing properties and holding such properties for long term investment through the collection of rental revenue; and

(iii) invest, acquire or dispose of, or trade from time to time any such assets, investments and shares/interests in any entity that is in the property investment and/or trading, or property development businesses.

Before entering into a new venture within the Property Business, the Group will consider, inter alia, the sustainability and growth potential of the new undertaking, the required resources and associated costs, and synergy with the Current Core Business, in accordance with the guidelines set out under Section 2.5 of this Circular.

7

LETTER TO SHAREHOLDERS

2.2.2 The Group may explore joint ventures and/or strategic alliances to carry out the proposed Property Business.

2.2.3 As and when required, the Company will make announcements and seek approvals from the Shareholders and/or the relevant authorities (including but not limited to the SGX-ST) in relation thereto. The Company has also set internal guidelines for approval before any projects or investments can be undertaken under the Property Business. Approval must be sought from the Executive Directors for all projects or investments undertaken under the Property Business, and approval must be sought from the Board of Directors of the Group, including the independent directors, for any project or investment exceeding S$20 million. Please see Section 2.5 (F) below for more details.

2.2.4 Ryobi Vietnam Project

The Company has on 27 September 2011 announced that the Company had, through its wholly owned subsidiary, Ryobi Development, entered into an in-principle agreement (the “APSTP Agreement”) with Ascendas-Protrade Company Limited (“ASPL”) in relation to the Ryobi Vietnam Project (as defi ned below). The Ryobi Vietnam Project is the Group’s fi rst venture into the Property Business.

ASPL is a company incorporated in Vietnam. It is jointly owned by Ascendas and Protrade (as defi ned below) and was established for the development of the APSTP.

Pursuant to the APSTP Agreement, Ryobi Development intends to lease a parcel of land within the APSTP to undertake the development of ready built factories (“RBF”) and built-to-suit (“BTS”) projects for small and medium enterprises and multinational corporations (the “Ryobi Vietnam Project”). Construction of the Ryobi Vietnam Project is expected to be completed within two years.

The details of the Ryobi Vietnam Project are as follows:

Land Area : 35,676m2(1) (3.56 hectares) Land Lease Price : USD1.64 million for entire Lease Term Lease Term : Up to 28 October 2057 Other Charges : Ryobi Development is to pay to ASPL an estate management fee

equivalent to USD0.06 per m2 per month of the total Land Area, for charges and other costs and expenses incurred by ASPL in maintaining common facilities and utilities in APSTP

Total Permissible : 24,322 m2

Gross Floor Area Plot Ratio : 0.68 Land Zoning : Industrial Park Estimated Total : USD8.9 million Development Costs (including land cost)

8

LETTER TO SHAREHOLDERS

Note:

(1) Under the APSTP Agreement, Ryobi Development has the option to lease additional land under future phases 2, 3, 4, 5 and 6 of the APSTP for construction of additional RBF and BTS. The total land area of the APSTP is approximately 498 hectares, which includes the Ryobi Vietnam Project (which occupies 3.56 hectares), and all futures phases 2, 3, 4, 5 and 6. Currently, Ryobi Development is the only developer that has managed to secure a project in the APSTP. While Ryobi Development has the option to lease additional future phases 2, 3, 4, 5 and 6 of the APSTP, should Ryobi Development choose not to exercise these options, ASPL will award the development of such phases to other developers.

As the developer for the Ryobi Vietnam Project, Ryobi Development may appoint Raffl es Piling Vietnam to undertake the piling and construction works.

The approvals required for the Ryobi Vietnam Project include formal address, permanent road connection, green space, fi re authority, environment and occupational approvals.

2.2.5 Information on Ascendas-Protrade Singapore Tech Park (“APSTP”)1

Ascendas-Protrade Singapore Tech Park (APSTP) is set within the 1,350 hectare integrated township of An Tay Industry and Service Complex2 and is well located at 40 km away from both Ho Chi Minh City and Tan Son Nhat International Airport. APSTP is specially designed to integrate complete clusters of business infrastructure with a host of amenities within the township. It offers a vibrant work-live-play industrial hub that blends high quality business space and reliable solutions with conducive business lifestyle.

Located in the Ben Cat District, in the province of Binh Duong and spreading over 500 hectares of land, APSTP offers an excellent range of options for companies in electronics, precision engineering, information technology, pharmaceutical, food and beverage and general industries.

The development of APSTP is undertaken by a partnership between Ascendas Pte. Ltd. (“Ascendas”), and a Vietnamese state-owned enterprise, Protrade Corporation (“Protrade”), who will jointly provide and develop the infrastructure and leased land for industrial usage. The APSTP is expected to support a working community of over 40,000 people, and will offer options of prepared land and built-to-suit as well as ready-built facilities that can provide businesses the option of effi cient, hassle-free start-up of their operations.

2.2.6 About Ascendas1

Ascendas is Asia’s premier provider of business space solutions, with a significant presence in regional markets including Singapore, China, India and South Korea. In Vietnam, Ascendas is a minority shareholder in the Vietnam-Singapore Industrial Park (“VSIP”). Ascendas develops, manages and markets information technology parks, industrial parks (manufacturing, logistics and distribution centres), business parks, science parks, hi-tech facilities, offi ce and retail space.

1 The information was extracted from the website of Ascendas at http://www.ascendas.com/downloads/fl yer_APS.pdf, http://www.ascendas.com/images_common/cms/press_release/22/Press_Release_151207_Ascendas_teams_up_with_Protrade.pdf and http://www.ascendas.com/english/ourMarkets/property.asp?bid=99 and the website of Vietnam Industrial Parks Promotions (VIIPIP) at http://viipip.com/ipen/?ipcode=212 on the Latest Practicable Date. We have not sought the consent of Ascendas or VIIPIP, nor has Ascendas or VIIPIP provided their consent to the inclusion of the relevant information extracted from the relevant website and disclaim any responsibility in relation to reliance on these statistics and information. While reasonable actions have been taken by our Directors to ensure that the relevant statements from the relevant information are reproduced in their proper form and context, and that the information is extracted accurately and fairly from the relevant website, all other parties and ourselves have not conducted an independent review of the information contained in the relevant website and have not verifi ed the accuracy of the contents of the relevant statements.

2 An Tay Industry and Service Complex comprises administrative building and amenity centre developed by APSTP. Other supporting services which APSTP will develop include clearances and warehousing facilities, full amenities of Food and Beverage outlet, convenience stores, clinics, child care centre and post offi ce.

9

LETTER TO SHAREHOLDERS

2.2.7 About Protrade1

Established from 1982, Protrade Corporation is a state-owned company with 5,000 employees. Protrade has its core business in major fi elds: Food and Beverage namely Dutch Lady Viet Nam Food and Beverage Company; Healthcare namely Hanh Phuc Hospital managed by Thomson Medical Center - Singapore; Leisure and Entertainment namely Song Be Golf Resort and Twin Doves Golf Resort; Real Estate namely Binh Duong-Hacota Serviced Apartment managed by Ascott - Singapore; Wood Processing and Furniture Manufacturing; Textile & Garment. Apart from the above established projects, Protrade also has business engagements with their Korean, Singaporean and Laos partners in rubber plantation, pig farms, golf resorts and turf club projects.

2.2.8 Prospects of the Ryobi Vietnam Project

(a) General Economic Overview3

In its April Knowledge Report, Colliers International Hanoi forecasts that industrial space sector will grow rapidly over the next three to four years. Land rentals will continue to grow in close correlation with demand and infl ation. Occupancy is likely to climb moderately, fuelled by the recovery of industrial production. New locations are still unable to compete on an even platform with the current centres of attraction4 that have unmatched advantages of location, infrastructure and economy.

Colliers International Hanoi is observing an increasing number of smaller occupiers wishing to lease premises under more fl exible terms, by way of renting either ready-built or built-to-suit facilities. This is largely in response to the high fi nancial investment and risk associated with land use right ownership. There are more industrial developers either building speculatively or offering a wider variety of build-to-suit packages. Monthly rents can range from USD3 to USD6 per m2 , loosely dependent upon construction quality, location and services provided.

The Company believes that APSTP will be a success given Ascendas’ track record in industrial park development coupled with Binh Duong’s strong GDP growth. In 2010, Binh Duong’s GDP growth was 14.5%, and in the fi rst six months of 2011, Binh Duong has attracted over USD214 million of foreign direct investment. Binh Duong also has two successful industrial parks developed by Singapore-Vietnam joint venture namely, VSIP 1 and 2.

(b) Location

Binh Duong is one of Vietnam’s four best performing provinces within the Southern Economic Zone, which is the country’s engine for economic growth. With strong governmental support and a keen focus on developing its industry and services sector, Binh Duong is well poised as an investment location of choice1.

3 The information was extracted from the website of Vietnamica at http://www.vietnamica.net/colliers-vietnam-industrial-space-outlook/ on the Latest Practicable Date. We have not sought the consent of Vietnamica or Colliers, nor has Vietnamica or Colliers provided their consent to the inclusion of the relevant information extracted from the relevant website and disclaim any responsibility in relation to reliance on these statistics and information. While reasonable actions have been taken by our Directors to ensure that the relevant statements from the relevant information are reproduced in their proper form and context, and that the information is extracted accurately and fairly from the relevant website, all other parties and ourselves have not conducted an independent review of the information contained in the relevant website and have not verifi ed the accuracy of the contents of the relevant statements

4 The current centres of attraction in Binh Duong province include Song Be Golf Club, Twin Doves Golf Club, Dai Nam Tourist Complex, Retail Promenade Mall at the Canary, GS Retail Mall, Metro Cash and Carry, Hanh Phuoc Hospital, Becamex Hospital, Homex @ The Canary, The Oasis, Ecolake, Singapore International School, Singapore Vocational School, Eastern International University.

10

LETTER TO SHAREHOLDERS

Located approximately 35 km to the north of Ho Chi Minh city and approximately 40 km from the international airport, Binh Duong enjoys convenient access to the city and airport via regional road networks. The province is also a growing hub for the manufacturing sector. Binh Duong houses factories of world-renowned brands and multinational corporations such as II-VI, Adidas, Fujikura, H&M, Nike, MacDonald’s, Sharp Takaya and Siemens1.

According to fi gures published by the Ministry of Planning and Investment of Vietnam in June 2011, Binh Duong has attracted 2,199 projects with a total registered capital of approximately USD14.3 billion5.

2.2.9 Save as the above, as at the Latest Practicable Date, the Group has not engaged in any discussion with any party for any joint ventures and/or strategic alliances relating to the Property Business. Should the Group decide to enter into such suitable joint ventures and/or strategic alliances, further announcements will be made at the appropriate time.

2.2.10 The Property Business is not expected to account for a signifi cant percentage of the Group’s total revenue for the current fi nancial year.

2.3 Funding for the Property Business

The Group may fund the proposed Property Business through internal funds and bank borrowings.

The Group intends to fund our land acquisitions for property development projects primarily through internal resources and bank borrowings. In the preliminary stages of the Group’s property developments, the Group intends to use its internal resources to pay land premiums for such acquisitions. The Group is generally able to obtain bank loans to fund its project development costs only after the Group has attained the relevant development licences. The Group will determine the amount of bank fi nancing it requires based on its available cash fl ow. Typically, banks would normally provide bank fi nancing for up to 70% of development costs as projected by the developer and verifi ed by the bank, with the remaining 30% fi nanced by the Group through internal resources and proceeds from sales and pre-sales.

The Group intends to fund its property investments and trading through internal funds and bank borrowings (subject to various borrowing limits imposed by different jurisdictions).

Though the Company does not have any present intention to fund the Property Business through any capital fund raising exercise, it does not rule out such option if in the future such option appears most viable under the circumstances. Any issuances of Shares or convertible securities will be made pursuant to the general or specifi c mandate granted by Shareholders at a general meeting.

The Group’s gearing ratio and consolidated cash and cash equivalent as at 30 September 2011 is 0.38 times and S$29.7 million respectively. The Group’s market capitalisation as at the Latest Practicable Date is S$98,481,141.

5 The information was extracted from the website of Ministry of Planning and Investment, Vietnam at http://fi a.mpi.gov.vn/News.aspx?ctl=newsdetail&aID=1093 on the Latest Practicable Date. We have not sought the consent of Ministry of Planning and Investment, Vietnam, nor has Ministry of Planning and Investment, Vietnam provided its consent to the inclusion of the relevant information extracted from the relevant website and disclaim any responsibility in relation to reliance on these statistics and information. While reasonable actions have been taken by our Directors to ensure that the relevant statements from the relevant information are reproduced in their proper form and context, and that the information is extracted accurately and fairly from the relevant website, all other parties and ourselves have not conducted an independent review of the information contained in the relevant website and have not verifi ed the accuracy of the contents of the relevant statements

11

LETTER TO SHAREHOLDERS

2.4 Risk Factors

The following is a list of identifi ed but by no means exhaustive list of risk factors which are associated with the Property Business:

General risks relating to the Property Business

No proven track record in the Property Business and uncertainties associated with entry into a new business area

The Group does not have a proven track record in the carrying out or implementation of the Property Business. There is no assurance that the Group will be able to derive suffi cient revenue to offset the capital and start-up costs as well as operating costs arising from the Property Business.

The Property Business involves business risks including the fi nancial costs of setting up new operations, capital investment and maintaining working capital requirements. If the Group does not derive suffi cient revenue from or does not manage the costs of the Property Businesses effectively, the overall fi nancial position and profi tability of the Group may be adversely affected.

Economic situation and property industry

The performance of the Group’s Property Business depends largely on the economic situation and the performance of the property industry. While there was substantial growth in the property market in the past decade, there is no assurance that such growth will maintain. Should the economy or the property market experience a downturn, due to reasons such as government regulations or global economic conditions, the performance of the Group’s Property Business and investments made thereunder may be adversely affected. In addition, as the gestation period for a property development project is long, typically between two to three years, any downturn in the economy or the property market, or changes in government regulations, during the course of a development project may affect the profi tability of such development project, thereby adversely affecting the Group’s fi nancial performance.

Capital investments

The proposed Property Business may require substantial capital investments or cash outlay. There is no assurance that fi nancing, either on a short-term or a long-term basis, will be made available or, if available, that such fi nancing will be obtained on commercially reasonable terms. In addition, any additional debt funding may restrict our freedom to operate our business as it may have conditions that:

(a) limit the Group’s ability to pay dividends or require us to seek consents for the payment of dividends;

(b) increase the Group’s vulnerability to general adverse economic and industry conditions;

(c) require the Group to dedicate a portion of the Group’s cash fl ow from operations to repayments of it’s debt, thereby reducing the availability of the Group’s cash fl ow for capital expenditures, working capital and other general corporate purposes; and

(d) limit the Group’s fl exibility in planning for, or reacting to, changes in the Group’s businesses and industry.

On the other hand, an issue of Shares or other securities to raise funds will dilute Shareholders’ equity interests and may, in the case of a rights issue, require additional investments by Shareholders. Further, an issue of Shares below the then prevailing market price will also affect the value of Shares then held by investors. Dilution in Shareholders’ equity interests may occur even if the issue of Shares is at a premium to the market price.

12

LETTER TO SHAREHOLDERS

Risks associated with acquisitions, joint ventures or strategic alliances

Depending on available opportunities, feasibility and market conditions, the Group’s expansion into the Property Businesses may involve acquisitions, joint ventures or strategic alliances with third parties, in Singapore as well as overseas markets that the Group intends to focus on. Participation in joint ventures, strategic alliances, acquisitions or other investment opportunities involves numerous risks, including the possible diversion of management attention from existing business operations and loss of capital or other investments deployed in such ventures, alliances, acquisitions or opportunities. In such event, the Group’s fi nancial performance may be adversely affected.

Government regulation

The property industry in countries in which the Group may operate is subject to signifi cant government regulation. In particular, regulatory approvals may be required for, among other things, land and title acquisition or divestment, development planning and design, construction, renovation and asset enhancement, and mortgage fi nancing and refi nancing. Such approvals may stipulate, among other things, maximum periods for the commencement of development of land. Some of these countries may also restrict the level, percentage and manner of foreign ownership and investment in real estate. Some of these laws and regulations are at times ambiguous, and their interpretations and applications can be inconsistent or uncertain, making compliance with them challenging, which may be potentially detrimental to us. If the Group fails to obtain the relevant approvals or comply with the applicable laws and regulations, the Group may be subject to penalties, have its licences or approvals revoked, or lose its right to own, develop or manage its properties, and the Group’s businesses, among other things, any or all of which could have a material and adverse impact on the Group’s business, fi nancial condition, results of operations and prospects.

In addition, in countries in which we may operate, in order to develop and complete a property development, a property developer may be required to obtain various permits, licences, certifi cates and other approvals (“Permits”) from the relevant administrative authorities at various stages of the property development process, including but not limited to, land use rights certifi cates, planning permits, construction permits, pre-sale permits and certifi cates or confi rmation of completion and acceptance. Such Permits are dependent on the satisfaction of certain conditions; in some circumstances, the Group may apply or may have applied for Permits in parallel with preliminary construction activities. The Group cannot give assurance it is able to fulfi ll the conditions required for obtaining the Permits, especially as new laws, regulations or policies may come into effect from time to time with respect to the real estate industry in general or the particular processes with respect to the granting of Permits. If the Group fails to obtain relevant Permits for the Property Business, any proposed investment may not proceed as scheduled, and the Group’s business, fi nancial condition, results of operations and prospects may be adversely affected.

Further, any changes in applicable laws and regulations could result in higher compliance costs and adversely affect the operations of the Group. There is no assurance that any changes in the applicable laws and regulations will not have an adverse effect on the fi nancial performance of the Group.

Risks relating to the property development industry

Pre-sale policies

The practice of pre-sales (that is, selling properties under construction prior to the receipt of construction completion and examination certifi cate) is adopted in the property market industry of many countries including Singapore. Should the Shareholders approve the Property Business, in line with the relevant industry practice, the Group may pre-sell most of the properties developed under the Property Business prior to completion. There are certain risks relating to the pre-sale of properties. In the event of a failure or delay in the delivery of pre-sold properties to purchasers, the Group may be liable for potential losses that purchasers may suffer as a result. There is no

13

LETTER TO SHAREHOLDERS

guarantee that these losses will not exceed the purchase price paid in respect of the pre-sold units. Failure to complete a property development on time may be attributed to factors such as the time taken and costs involved in completing construction, which are in turn adversely affected by factors such as delays in fi tting out works, shortages of labour, adverse weather conditions or natural disasters. If the delay in delivery extends beyond the contractually specifi ed period, the purchasers may also be entitled to terminate the pre-sale agreements and claim refunds of monies paid, damages and/or compensation for late delivery. There is no assurance that there will be no circumstances which will result in liabilities arising from pre-sale arrangements which have experienced signifi cant delays in completion or delivery, resulting in the Group having to compensate purchasers for late delivery, or refund of monies paid in situations where purchasers have terminated the sale and purchase agreements. This will adversely affect the Group’s business and fi nancial performance.

Unsold properties

In the event that the Group is unable to sell a signifi cant proportion of the properties it develops under the Property Business, the Group’s fi nancial performance will be materially and adversely affected. Furthermore, the unsold properties that the Group continues to hold for sale post-completion may be relatively illiquid, which will limit the Group’s ability to realise cash from unsold units on short notice. Such illiquidity may also have a negative effect on the prices of unsold units in the event that the Group is required to sell the unsold properties urgently, and limits the Group’s ability to vary its portfolio of property held for sale in response to changes in economic, political, social or regulatory conditions in a timely manner. In such event, the Group’s cash fl ow and fi nancial performance will be adversely affected.

Reliance on third party contractors

The Group may rely on third party contractors to construct its development projects under the proposed Property Business. Accordingly, it is subject to construction risks such as the failure of third party contractors to carry out their contractual obligations, failure of third party contractors to bear cost overruns, and any other unforeseen circumstances which may have an adverse impact on its fi nancial performance. Furthermore, the contractors engaged may experience fi nancial or other diffi culties that may affect their ability to carry out the work, thus delaying the completion of or failing to complete the development projects and resulting in additional costs or exposures to the risk of liquidated damages to the Group.

Claims for delays and defective works

The Group may face claims from purchasers and management corporations relating to delays and defective works under the proposed Property Business. Claims may also be made against the Group by owners or occupiers of neighboring properties in respect of the use of such properties. As such, the Group’s business and fi nancial position will be affected if the Group has to pay signifi cant amounts of compensation or spend signifi cant amounts of resources in legal costs in the event of legal proceedings. The Group’s reputation may also be affected as a result of such proceedings.

Fluctuations in property prices and the availability of suitable land sites

The performance of the Group may be subject to fl uctuations in property prices as well as the availability of suitable land sites. Should property market prices suffer a downward trend, the Group’s earnings may be adversely affected as the Group may have to postpone the sale of such property development project units to a later date, when market conditions improve. The Group may also have to sell its property development projects at lower prices, which in turn would adversely affect the Group’s sales revenue and profi t margin. If the Group is not able to procure suitable land sites to carry out its property development projects, property development projects on less favourable locations may not be as marketable, resulting in the Group’s sales volume and profi tability being adversely affected. There is competition with other property developers for new land sites and there is no assurance that suitable sites will always be available for the purposes of the proposed property development business of the Group.

14

LETTER TO SHAREHOLDERS

Intense competition

The proposed Property Business is highly competitive, with strong competition from established industry participants who may have larger fi nancial resources or a stronger track records. The Group may not be able to provide comparable services at lower prices or respond more quickly to market trends than future or existing competitors who may have larger fi nancial resources and stronger track records. Purchasers may opt for property development projects of future or existing competitors over the Group’s Property Business development projects, thereby resulting in the Group’s sales, business, fi nancial position and performance being adversely affected.

Changes in the business environment

The length of a property development project can typically last two to three years, depending on the size of the development. Consequently, changes in the business environment during the length of the Group’s projects may affect the revenue and cost of the development which will directly depress the profi t margin of such projects. Changes in the business environment for jurisdictions in which the Group operates can include delays in procuring the necessary relevant approvals, licenses or certifi cates from government bodies, changes in laws, regulations and policies in relation to the property development, fl uctuations in demand for properties, delays in construction schedules due to poor weather conditions, labour disputes and fl uctuation in costs of construction materials and other costs of development. Such delays will result in the Group incurring additional costs, such as additional labour cost, thus affecting the profi tability of the Group.

Fluctuations in foreign exchange rates may have a material and adverse effect on the Group’s profi tability

As the Company’s functional and presentation currency is denominated in S$, any depreciation in foreign exchange rates against the S$ may affect the Group’s profi tability and fi nancial position. For example, any income derived from the sale of property units overseas which is denominated in foreign currencies may decrease if the foreign exchange rates depreciate against the S$, hence the profi tability of the Group may be affected.

Risks relating to the property investment and trading industry

Property valuations and decline in property values

Valuations of the Group’s properties conducted by professional valuers are based on certain assumptions and are not intended to be a prediction of, and may not accurately refl ect, the actual values of these assets. The inspections of the properties and other works undertaken in connection with a valuation exercise may not identify all material defects, breaches of contracts, laws and regulations, and other defi ciencies and factors that could affect the valuation.

In addition, unfavourable changes to the economic or regulatory environment or other relevant factors may negatively affect the premises upon which the valuations are based and hence, the conclusions of such valuations may be adversely affected. As such, the properties of the Group may not retain the price at which they may be valued or be realised at the valuations or property values which were recorded.

The Group will apply fair value accounting standards in valuing its properties. The value of the properties of our Group may fl uctuate from time to time due to market and other conditions. Such adjustments to the Group’s shares of the fair value of the properties in the Group’s portfolio could have an adverse effect on the net asset value and profi tability of the Group.

15

LETTER TO SHAREHOLDERS

Material defects, breaches of laws and regulations and other defi ciencies

There is no assurance that the reviews, surveys or inspections (or the relevant review, survey or inspection reports on which the Group would rely on) would have revealed all defects or defi ciencies affecting properties that the Group has interests in. In particular, there is no assurance as to the absence of latent or undiscovered defects or defi ciencies or inaccuracies or defi ciencies in such reviews, surveys or inspections reports, any of which may have a material adverse impact on the business, fi nancial condition and results of operations of the Group in relation to such properties. As such, the Group may be exposed to risks of incurring additional costs to carry out repairs to rectify such defi ciencies, or litigations suits from third parties. For example, repair works carried out on tenanted units to rectify such latent defects may obstruct businesses of tenants, who may suffer losses as a result of such obstruction, and seek to claim such losses from the Group.

Uninsured losses

While the Group will obtain insurance policies to cover losses in respect to its properties, the insurance obtained may not be suffi cient to cover all potential losses. Examples of such potential losses include losses arising out of extraordinary events such as natural disasters like earthquakes or fl oods. Losses arising out of damage to the Group’s properties not covered by insurance policies in excess of the amount it is insured would affect the Group’s profi tability. Committing additional costs to the relevant project for its completion in the event there are uninsured damages would also adversely affect the fi nancial performance of the Group.

Risks relating to investments in Vietnam

Buyers might meet diffi culty in obtaining fi nancial support and may face increasing interest rates

According to Resolution No. 11/NQ-CP issued on 24 February 2011 by the Government of Vietnam, in order to curb infl ation, the State Bank of Vietnam will implement tight monetary policies to keep credit growth at or below 20.0% and reduce credits for non-manufacturing fi elds, particularly real estate and securities fi elds.

In line with solving macroeconomic problems, the government raised the refi nance rate for the second time to 15.0% per annum from 14.0% per annum, effective from 17 May 2011.

The acceleration in interest and refi nance rates will make it harder for businesses and individuals to borrow funds, especially for real estate purposes as the government is attempting to cool down this market.

Currently, the state banks charge real estate developers and investors with average annual interest rates of 21.5% to 22.0% per annum for short-term (3 to 12 months) and 23.0% to 23.5% for mid-term and long-term (1 to 5 years or longer). Individuals who want to borrow money to buy a house will be charged at an average interest rate of 22.0% to 23.0% per annum.

Joint stock banks normally charge higher interest rates, particularly at least 24.0% per annum for real estate developers and investors for a minimum three years and at least 22.5% per annum for individuals who want to borrow a loan to buy a house for a minimum one year. An average rate of 0.12% per annum will be added to the interest rate for each additional year after the minimum borrowing period.

The high interest rates for property fi nancing results in the acquisition of properties in Vietnam being very expensive, unless such property is acquired without financing. This may affect customers’ spending on purchase of properties, which may result in a reduction in the Group’s customer base and may affect the Group’s sales and profi tability.

16

LETTER TO SHAREHOLDERS

Foreign exchange regulations in Vietnam

Vietnam has implemented exchange control mechanisms which were designed to limit foreign currency outflows - generally requiring the use of the VND for domestic transactions and channelling the fl ow of foreign currencies into the banking system. The State Bank of Vietnam is the primary authority to formulate and administer exchange control policies in Vietnam. Dividends can be remitted overseas through certain registered accounts in accredited credit institutions, after payment of applicable Vietnam taxes. As the VND is not a freely convertible currency, conversion of dividend to non-residents into foreign currency is necessary prior to the outward remittance from Vietnam. Repatriation of funds out of Vietnam depends on the availability of the relevant foreign currency, which is controlled by the State Bank of Vietnam. If, for example, the Group intends to repatriate funds back to Singapore, the Group will only be able to do so when the State Bank of Vietnam has suffi cient S$ to allow the Group to repatriate the amount it so intends. If the State Bank of Vietnam does not have the required amount of S$ to do so, the Group will have to wait until such amount of S$ is available at the State Bank of Vietnam, before it is able to repatriate such funds back to Singapore.

On 18 November 2010, The Ministry of Finance of Vietnam issued a circular No. 186/2010/TT-BTC “Circular 186”, providing the guidance of the offshore remittance of profi ts earned by foreign organizations and individuals from their direct investment in Vietnam under the Investment Law. Under Circular 186, the Group may only repatriate funds on an annual basis. The Group will have to submit its audited fi nancial statements and corporate income tax fi nalisation returns for each fi nancial year to the local tax authorities in order to facilitate such repatriation. The Group will also be prohibited from transferring profi ts abroad if its investments in Vietnam still bears accumulative losses after losses carried forward from the previous fi nancial year still exists.

Any future restrictions on repatriation of funds may limit the Group’s ability to distribute dividends to Shareholders.

Notwithstanding the risks set out above, the Board, having considered the rationale of the proposed Property Business as set out above, believes that it is to the benefi t of the Group to expand the core business of the Group to include the proposed Property Business. The Directors will be mindful in managing the risks involved.

17

LETTER TO SHAREHOLDERS

2.5 Property Business Process

The following section is a summary of the key stages and processes which the Company will typically undertake in respect of (i) property development projects; and (ii) property investment and trading projects:

(A) Formulation of Strategy and

Investment Plans

(B) Property/ Land Evaluation and Assessment

(C) Property/ Land

Acquisition

Project Conceptualisation,

Planning and Design

Construction Work

Sales and Lease

After-Sales Services

Lease and Sales

(D) Property Development

(E) Property Investment and

Trading Projects

Projects

(A) Formulation of Strategy and Investment Plans

Market research will be conducted to review the economic policies, development plans, the economic growth and prospects and the demand and supply conditions in the property market of various targeted jurisdiction. This will assist the Group in forming its overall development strategies and investment plans for the Property Business. The formulation of the strategies and investment plans will be undertaken by the Board together with the Property Business management team upon in-depth deliberation and consideration of the various aforementioned factors. Such strategies and plans would include the amount of resources and investment the Group will commit, and the investment criteria. The Group’s strategies and plans will be reviewed from time to time and revised, if required, to adapt to changing economic, regulatory or market conditions.

18

LETTER TO SHAREHOLDERS

(B) Property / Land Evaluation and Assessment

The Property Business management team, with the assistance of its support teams, will identify available properties or land on the market through announcements of public tender, private tenders or sales through the Group’s network.

Property or land may be evaluated and assessed based on the Group’s strategic and investment plans, price, yield thresholds, occupancy and tenant characteristics, location, building characteristics, tenure of land, accessibility of the land, marketability and demand for properties within the area, availability of supporting infrastructure and financing requirements. The assessments could be done internally or externally by professional consultants engaged by the Group.

In respect of land identifi ed for potential development, a feasibility study will be carried out and prepared, where necessary. Based on the feasibility study, a proposal will be prepared by the Property Business management team, and such proposal will be reviewed and approved by the Executive Directors. For projects with values exceeding S$20 million, the approval of the Board is required. For properties identifi ed for investment purposes, only a proposal will be prepared.

(C) Property / Land Acquisition

Upon approval of the proposal, steps will be taken to acquire the property or land identifi ed by the Group. Depending on the jurisdiction where the property or land is situated, the property or land may be acquired through private sale, public tender or auctions.

(D) Property Development Projects

Project Conceptualisation, Planning and Design

Project conceptualisation will be carried out for property development. This may be carried out in-house by the Group, or outsourced to professional consultants, such as architects, interior designers, surveyors or engineers (mechanical, electrical, civil and structure). In appointing the relevant professionals, the Group will consider factors such as qualifi cations, reputation for reliability and quality, their size and portfolio. In addition, the Property Business management team, together with the relevant project team, will formulate marketing strategies and execute the necessary marketing activities, such as preparation of marketing materials and designing and setting up showrooms. Marketing consultants may be appointed to assist in the marketing activities.

At this stage, the Group will also implement fi nancial controls and budget planning processes to manage and control costs. The Group will also apply for and obtain the necessary approvals, licences and clearances require for the construction and sale of the project.

Construction Work

Upon fi nalising the design for the development, the Group will engage related or third party main contractors and subcontractors to commence construction works. Subcontractors will either be directly engaged by the Group or selected through an invitation tender process. Criteria for selection of main contractors and subcontractors will include licensed qualifi cations, fi nancial status, track record, ability to commit to project timeline and quality of workmanship and fi nishing.

A project management team will be formed to manage and supervise the construction of the development. The Group may also engage project management companies to assist in managing and supervising the project. The project management team is also responsible for ensuring that the construction of the development progresses in a timely manner, and that any cost control policies which we may adopt are effectively implemented in the construction process of our projects. Construction work will be constantly monitored through regular on-site inspections and progress reports.

19

LETTER TO SHAREHOLDERS

Regular reviews of project expenditure reports will be carried out by the project management team to ensure that costs are effectively managed and to prevent cost overrun.

Where the Group has acquired the necessary skills, expertise and experience in respect of any specific aspect of construction work, such as foundation works, installation, construction, fi tting-out works, and provided that the Group has obtained the relevant regulatory permits and/or licences in respect thereof, the Group may directly undertake such work itself.

Sales and Lease

Depending on the project, the Group may conduct pre-launches for the purpose of selling the properties prior to completion. Selling prices for properties are set after taking into considering market trends, development costs, expected investment returns and prevailing supply and demand conditions.

The Group will adopt a standard contract to be entered into with purchasers. An initial payment of a certain percentage of the sale price will be required to be paid upon the execution of a property sale and purchase contract. The amount of the initial payment will be subject to local laws and regulations. The balance of the purchase price is satisfi ed by the purchaser either directly by the purchaser or through a mortgage facility between the purchaser and a bank (where the purchaser will repay the bank through instalment payments). The purchase price will be required to be paid in full to the Group before possession is handed over to the purchasers.

For properties developed for investment purposes, the Group will enter into tenancies with its customers. As with the selling price, the tenure and rental of such tenancies will depend on the market trends, development costs, expected investment returns and prevailing supply and demand conditions.

After-Sales Services

After completion of the sale, the Group will arrange for purchasers to take possession of the individual units. Subject to local laws and regulations, the Group may be required to manage the development, such as provided maintenance services, pending the handover of the entire development to the management corporation.

(E) Property Investment and Trading Projects

Lease and Sale

Property or land acquired for investment purposes may be leased or sold. The selling price or tenure and rental for the property or land will depend on the market trends, expected investment returns and prevailing supply and demand conditions.

Where required, property or land which is leased or held pending sale will be managed by the Group. A management team will be formed in respect of such property or land, and will be responsible for dealing with the leases, maintenance and repairs and provision of building services, such as security, air-conditioning, heating and utilities.

(F) Limits on Transaction Value of Property Development and Investment and Trading

Projects

Before undertaking any projects or investments under the Property Business, a proposal will be prepared and presented by the project management team to the Executive Directors of the Group for their review and approval. The proposal will provide a detailed analysis of the investment or project, including the projected returns, market trends and funding requirements. The Executive Directors will review the proposal and may seek the

20

LETTER TO SHAREHOLDERS

advice of external consultants where appropriate. In reviewing the proposal, the Executive Directors will consider, amongst other things, the market conditions, growth potential and value enhancement of the investment or project for the Group. The Executive Directors will seek further clearance from the Board of Directors of the Group, including the independent directors, should the investment commitment exceed the approval limits set internally and approved by the Board. The current approval limit is up to S$20 million per investment or project.

Upon the approval of the proposal by the Executive Directors or by the Board (if necessary), the Property Business management team will then be authorised to perform all acts and take all measures necessary and required to implement the investment or project.

In addition, the Property Business management team will review and evaluate the performance of each investment and project quarterly.

2.6 Quality Assurance

Various quality assurance procedures will be implemented to ensure the quality of the properties developed by the Group. These would include:

(i) carrying out on-site inspection and quality and safety checks;

(ii) proper supervision of the construction progress and project timeline;

(iii) ensuring contracts utilise construction materials which satisfy the Group’s quality requirements;

(iv) implementing stringent process for appointment of contractors, consultants and professionals; and

(v) monitoring national quality control standards and market practice.

2.7 Management

2.7.1 The Company has set up a Property Business management team consisting of some of the current management team and will engage any additional manpower in relation to the Property Business as and when required;

2.7.2 The Group plans to leverage on the skills and capabilities of the Property Business management team for the expansion of the core businesses by:

(i) drawing on their expertise, experience and analytical ability to make collective and sound decisions on the Property Business; and

(ii) using each executive’s network of contacts to facilitate further strategic partnerships and commercial opportunities to support and strengthen the Group’s investments and venture into the Property Business.

The Property Business management team will also leverage on the considerable relevant experience of the Board and other members of the management gained in the development of the Current Core Business.

2.7.3 Property Business management team will be headed by Mr Ong Tiong Siew and comprises Mr Ong Teng Choon, Mr Lim Kok Hin, Mr James Wong Po Kwan and Mr Ong Kar Yin.

21

LETTER TO SHAREHOLDERS

Mr Ong Tiong Siew, a co-founder of the Group, and the Executive Director and Chief Executive Offi cer of the Company, is responsible for the formulation of the Group’s strategic direction and expansion plans, and the management of the Group’s overall business development. Mr Ong Tiong Siew has more than 28 years of experience in the area of civil engineering and foundation business, having worked in various construction related companies, including QBS System Pte. Ltd, Chee Hup Construction Pte. Ltd., Soh Beng Tee Civil Engineering Pte Ltd, ECA Construction Pte Ltd and Kiso Engineering (S) Pte Ltd before he formed Ryobi Kiso (S) Pte. Ltd. in 1990 where as its director, he has been responsible for the overall management of the operations, expansion plans and business development of Ryobi Kiso (S) Pte. Ltd. Mr Ong Tiong Siew was a merit scholar of the Government of the Republic of Singapore. During his services with the government, Mr Ong Tiong Siew participated in feasibility studies, master planning and implementation of national infrastructure projects. Mr Ong Tiong Siew graduated from the National University of Singapore with a Bachelor of Engineering (Civil) in 1981.

Mr Ong Teng Choon, an Executive Director, is responsible for overseeing the procurement and resources planning which includes appointment of third party contractors, allocation of resources, procurement of materials/equipment and logistics. Mr Ong Teng Choon has more than 25 years of experience in the area of civil engineering and foundation business, having worked in various construction related companies, including Kong Siong Construction Pte Ltd, ECA Construction Pte Ltd and Kiso Engineering (S) Pte Ltd. From 1983 to 1987, Mr Ong Teng Choon was a Project Manager in Kong Siong Construction Pte Ltd. He was involved in the planning and execution of public housing projects. From 1987 to 1989, Mr Ong Teng Choon was an Executive Director of ECA Construction Pte Ltd where he was involved in managing and developing the industrial and residential property projects. From 1989 to 1990, he worked as a project manager at Kiso Engineering (S) Pte Ltd and was involved in the execution of piling projects. In October 2007, prior to his appointment as Director, he was appointed a director of Ryobi Kiso (S) Pte. Ltd. and was responsible for overall co-ordination and general management of the Group’s piling projects, including the appointment of sub-contractors and the procurement of machinery, equipment and accessories. Between 1990 and 2007, he was employed by Ryobi Kiso (S) Pte. Ltd., fi rst as its senior project manager in 1990 where he was responsible for resources and project management and as its general manager from 2002. As general manager, Mr Ong Teng Choon was responsible for procurement and overall management of the Group. Mr Ong Teng Choon graduated with a Bachelor of Engineering (Civil) from the National University of Singapore in 1983 and is a senior member of the Institution of Engineers Singapore.

Mr Lim Kok Hin was appointed as the chief executive offi cer of Raffl es Piling Vietnam in April 2010, and is responsible for the overall operation of Raffl es Piling Vietnam. He is stationed in Ho Chi Minh City. Mr Lim’s experience in the property development industry of more than 30 years includes, amongst others, appointments as project engineer, project manager and director, and assistant vice president of projects. Among the more notable of Mr Lim’s experiences, from 1992 to 1994, Mr Lim was appointed by Construct, Development and Consult as senior engineer for the construction of the Junction 8 shopping centre in Bishan. Between 1994 and 1998, Mr Lim worked under Singapore Technologies Construction Pte. Ltd. as a construction manager for the project implementation of the USD30 million Summit Parkview Hotel in Yangon, Myanmar. In 1996, he was promoted to senior project manager, where he was involved in the design and construction for Redevelopment of Pulau Tekong Army Camp. In 1999, Mr Lim was appointed as the deputy group project manager for the consortium of SembCorp Engineers and Constructors Pte Ltd, Mitsubishi and ST Engineering in relation to the delivery of the C810 L.R.T system for Punggol New Town, where he worked on the safety, administration, security and ad hoc duties for consortium matters. From 2001 to 2006, Mr Lim was the project director of Sembawang Engineer and Constructors Pte Ltd, where he was overall responsible for the construction and delivery of Contracts 421, a 4 lane expressway of 1.3 km, linking East Coast Parkway to Nicoll Highway. From 2006 to 2009, Mr Lim was a

22

LETTER TO SHAREHOLDERS

Director (Project) in Asia Projects Consultant Pte Ltd in Vietnam. He managed the property development for the company’s Vietnam clients. Between 2009 and March 2010, prior to joining the Group, Mr Lim was the assistant vice president of projects for SembCorp Design and Construction Pte Ltd, where he was responsible for the civil and infrastructure work of SembCorp Utilities’ projects. Mr Lim obtained his Bachelors in Civil Engineering in 1980 from the University of Singapore, and subsequently obtained his Master in Building Science in 1988 from the National University of Singapore.

Mr James Wong Po Kwan was appointed as general manager of Raffl es Piling Vietnam in April 2010, and is stationed full-time in Ho Chi Minh City in Vietnam, where he is responsible for overseeing all commercial and contractual aspects of Raffles Piling Vietnam. Mr James Wong has more than 30 years of experience in various aspects of the property development and construction industry, ranging from quantity surveying, project management and other commercial function. More notably, from 1991 to 1994, Mr James Wong was the principal estimator in IPCO International Limited, a company listed on the Mainboard of the SGX-ST. As principal estimator, he was involved in pre-contract functions such as project cost estimation, planning and contracts administration. From 1997 to 2000, he was the general manager/director of AFP Land Pte Ltd (a subsidiary of AFP Land Ltd), where he was in charge of residential property development projects in Singapore and Malaysia. In 2000, Mr James Wong was stationed in South Korea as a project director for Jasper Investments Limited (formerly known as Econ International Limited), a company listed on the Mainboard of the SGX-ST, where he was involved in the planning and formulation of development projects in Korea. He was also appointed as joint project director by SembCorp Engineers and Constructors for the S$230 million C504 Changi Airport MRT Station Projection, and in-charge of the commercial aspect of C421, The 1.3 km Kallang-Paya Lebar Expressway Tunnel. He also served as a project director for project management consultancy contracts in Jurong International Consulting Pte Ltd from 2008 to 2010, where he was stationed in Abu Dhabi and Dubai to oversee all commercial and contractual aspects in the United Arab Emirates, including, amongst others, providing input to ongoing consultancy contracts and pre-contractual tendering stage. Mr James Wong graduated with Honours in Bachelor of Science in Quantity Surveying from the University of Reading in 1979.

The Group had on 1 October 2011 appointed Mr Ong Kar Yin as the business consultant to the Group in relation to the Property Business. Upon his appointment, Mr Ong Kar Yin would be tasked to assist the Property Business management team in the carrying out of its duties. The Group believes that it would be able to benefi t from the vast experience, knowledge and expertise of Mr Ong Kar Yin.

Mr Ong Kar Yin has more than 20 years of experience in property marketing, investment and fund management. Between 1991 and 1994, he was employed as a regional manager in Jones Lang Wootton Property Consultants Pte. Ltd., where he was tasked with marketing and sales of property developments located in Singapore, Malaysia, Indonesia, Hong Kong and China. Between 1995 and 1999, Mr Ong Kar Yin joined DBS Land Limited as an assistant director of the investment and business development division of China market, where he was in involved in sourcing for land and projects, negotiation of land contracts and relocation management with government authorities, designing investment and capital structures with exit strategies, investment evaluation, and formulation of marketing plans. From 2000 to 2002, he joined Ascendas Shanghai Co. Ltd. as an assistant vice president of its investment and business development division, where his duties included sourcing for investment opportunities, and designing unique “built-to-suit facilities” with fi nancial packages that were tailored to meet Fortune-1000 tenants’ design specifi cations. Between 2002 to 2004, he joined Douglas Mackenzie Property Consultants as a general manager where he provided property investment analysis, investment structure advisory, and investment sales and marketing services. In 2005, he joined the Pacifi c Star Fund Management Group as vice president for China market, where he was responsible for

23

LETTER TO SHAREHOLDERS

fi nancial analysis, sourcing for property investments, proposing creative investments and funding structures for initial public offerings, and making presentations to and negotiating with institutional investors. Mr Ong Kar Yin subsequently joined Asia Pacifi c Land in 2007 as a senior vice president where he took on similar duties, until 2009, where he joined Leedon Capital Pte. Ltd. as a business consultant and director, where he provided business advisory, property investment analysis and property marketing planning services. Mr Ong Kar Yin obtained his Diploma in Architecture Studies from Singapore Polytechnic in 1987, BBA in Finance from the Royal Melbourne Institute of Technology in 1991, and Masters in Finance and Investment from the University of Hull in 1996.

Mr Ong Kar Yin is the brother of Mr Ong Tiong Siew, our Executive Director and Chief

Executive Offi cer, and Mr Ong Teng Choon, our Executive Director.

2.7.4 The Board would continue to evaluate the manpower and expertise required in the carrying out of the proposed Property Business and the Group will consider hiring additional staff or in-house or external consultants and professional advisers as and when required in connection with the Property Business to assist the Property Business management team.

3. SGX-ST LISTING MANUAL

Upon the approval by Shareholders of the proposed expansion of the Group’s core business to include the Property Business, any acquisition which is in, or in connection with, the Property Business, may be deemed to be in the ordinary course of business and therefore not fall under the defi nition of a “transaction” under Chapter 10 of the Listing Manual.

However, Clause 3.2.3 of Practice Note 10.1 of the Listing Manual requires that when an acquisition would change the Company’s risk profi le, the Company will have to seek Shareholders’ approval. The following factors will be considered in determining whether the risk profi le of the Company has been changed:

(a) when the acquisition is a very substantial acquisition which will increase the scale of the Company’s existing operations such that any of the relative fi gures computed on the bases set out in Listing Rule 1006 (c) and 1006 (d) is 100% or more;

(b) when the acquisition will result in a change of control of the Company which will be treated as a reverse takeover;

(c) when the acquisition will have a signifi cant adverse impact on the Company’s earnings, working capital and gearing; and

(d) when the acquisition will result in an expansion of the Company’s business to a new geographical market.

Clause 3.2.4 of Practice Note 10.1 of the Listing Manual further provides that the factors in determining whether an acquisition would change the Company’s risk profi le as enumerated in Clause 3.2.3 of Practice Note 10.1 of the Listing Manual are neither exhaustive nor conclusive.

Where the proposed expansion of the Group’s core business to include the Property Business would involve an interested person transaction as defi ned under the Listing Manual, the Company will also comply with the provisions of Chapter 9 of the Listing Manual.

24

LETTER TO SHAREHOLDERS

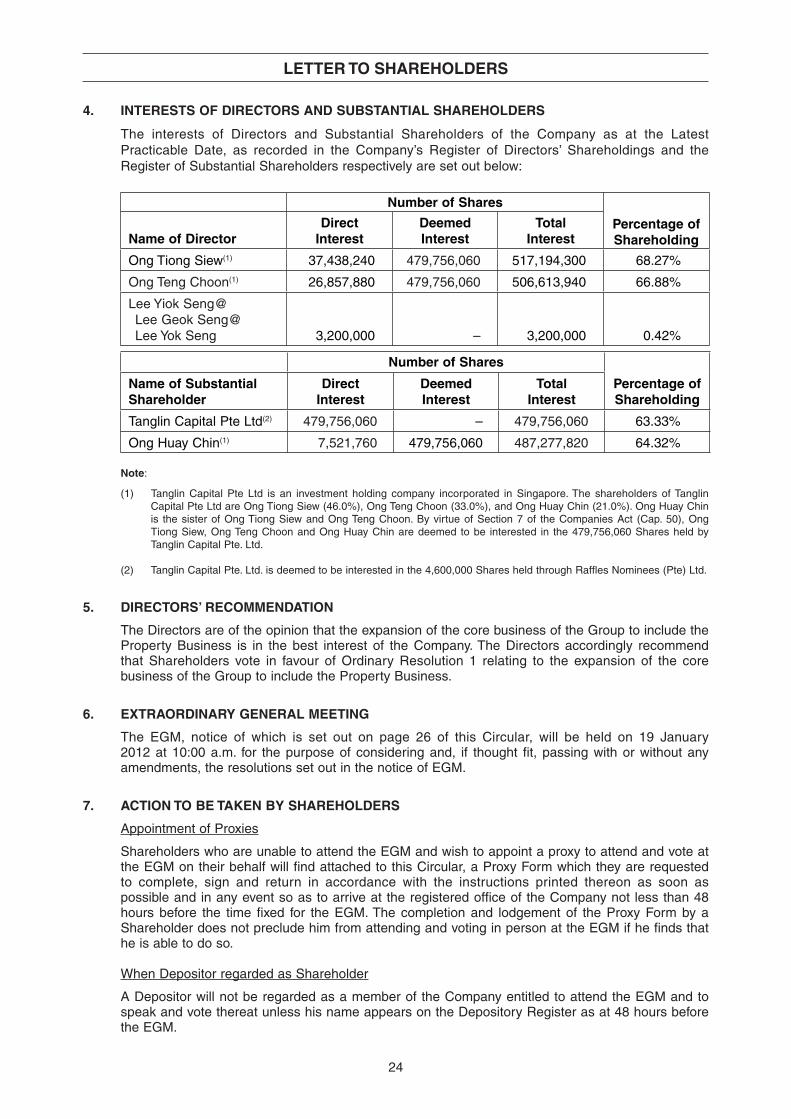

4. INTERESTS OF DIRECTORS AND SUBSTANTIAL SHAREHOLDERS

The interests of Directors and Substantial Shareholders of the Company as at the Latest Practicable Date, as recorded in the Company’s Register of Directors’ Shareholdings and the Register of Substantial Shareholders respectively are set out below:

Number of Shares Percentage of ShareholdingName of Director

DirectInterest

DeemedInterest

Total Interest

Ong Tiong Siew(1) 37,438,240 479,756,060 517,194,300 68.27%

Ong Teng Choon(1) 26,857,880 479,756,060 506,613,940 66.88%

Lee Yiok Seng@ Lee Geok Seng@ Lee Yok Seng 3,200,000 – 3,200,000 0.42%

Number of Shares

Name of SubstantialShareholder

DirectInterest

Deemed Interest

Total Interest

Percentage of Shareholding

Tanglin Capital Pte Ltd(2) 479,756,060 – 479,756,060 63.33%

Ong Huay Chin(1) 7,521,760 479,756,060 487,277,820 64.32%

Note:

(1) Tanglin Capital Pte Ltd is an investment holding company incorporated in Singapore. The shareholders of Tanglin Capital Pte Ltd are Ong Tiong Siew (46.0%), Ong Teng Choon (33.0%), and Ong Huay Chin (21.0%). Ong Huay Chin is the sister of Ong Tiong Siew and Ong Teng Choon. By virtue of Section 7 of the Companies Act (Cap. 50), Ong Tiong Siew, Ong Teng Choon and Ong Huay Chin are deemed to be interested in the 479,756,060 Shares held by Tanglin Capital Pte. Ltd.

(2) Tanglin Capital Pte. Ltd. is deemed to be interested in the 4,600,000 Shares held through Raffl es Nominees (Pte) Ltd.

5. DIRECTORS’ RECOMMENDATION

The Directors are of the opinion that the expansion of the core business of the Group to include the Property Business is in the best interest of the Company. The Directors accordingly recommend that Shareholders vote in favour of Ordinary Resolution 1 relating to the expansion of the core business of the Group to include the Property Business.

6. EXTRAORDINARY GENERAL MEETING

The EGM, notice of which is set out on page 2 6 of this Circular, will be held on 19 January 2012 at 10:00 a.m. for the purpose of considering and, if thought fi t, passing with or without any amendments, the resolutions set out in the notice of EGM.

7. ACTION TO BE TAKEN BY SHAREHOLDERS

Appointment of Proxies

Shareholders who are unable to attend the EGM and wish to appoint a proxy to attend and vote at the EGM on their behalf will fi nd attached to this Circular, a Proxy Form which they are requested to complete, sign and return in accordance with the instructions printed thereon as soon as possible and in any event so as to arrive at the registered offi ce of the Company not less than 48 hours before the time fi xed for the EGM. The completion and lodgement of the Proxy Form by a Shareholder does not preclude him from attending and voting in person at the EGM if he fi nds that he is able to do so.

When Depositor regarded as Shareholder

A Depositor will not be regarded as a member of the Company entitled to attend the EGM and to speak and vote thereat unless his name appears on the Depository Register as at 48 hours before the EGM.

25

LETTER TO SHAREHOLDERS

8. DIRECTORS’ RESPONSIBILITY STATEMENT

The Directors collectively and individually accepts full responsibility for the accuracy of the information given in this Circular and confi rm, after making all reasonable enquiries that to the best of their knowledge and belief, this Circular constitutes full and true disclosure of all material facts about the Proposal, the Company and its subsidiaries, and the Directors are not aware of any facts the omission of which would make any statement in this Circular misleading.

Where information in this announcement has been extracted from published or otherwise publicly available sources or obtained from a named source, the sole responsibility of the Directors has been to ensure that such information has been accurately and correctly extracted from those sources and/or reproduced in this announcement in its proper form and context.

9. INSPECTION OF DOCUMENTS

Copies of the following documents may be inspected at the business offi ce of the Company at 58A Sungei Kadut Loop, Ryobi Industrial Building, Singapore 729505, during normal business hours from the date of this Circular up to and including the date of the EGM:

(1) the Memorandum and Articles of Association of the Company; and

(2) the Annual Report of the Company for the fi nancial year ended 30 June 2011.

Yours faithfullyFor and on behalf of the Board of Directors ofRyobi Kiso Holdings Ltd.

Ong Tiong SiewChief Executive Offi cer and Executive Director

26