rules, hereinafter the “rules”. - kdpw_ccp detailed... · 1 kdpw_ccp detailed clearing rules...

TRANSCRIPT

1

KDPW_CCP Detailed Clearing Rules

Valid as at 22 March 2012

Chapter One

Participation in KDPW_CCP

§ 1

1. The terms used in these provisions shall have the meaning defined in the Clearing

Rules, hereinafter the “Rules”.

2. Whenever these provisions refer to:

1) positions – this shall mean liabilities or receivables arising from transactions

cleared by KDPW_CCP;

2) correlated positions – this shall mean positions in financial instruments of the same

class, registered in the same portfolio, whose total risk is lower than the sum of risks

calculated separately for each position;

3) derivatives transactions portfolio – this shall mean positions arising from

transactions concluded in derivatives registered on the same entity account in the

settlement institution and marked with the same identifier;

4) cash transactions portfolio – this shall mean positions arising from transactions

concluded in securities registered on the same entity account in the settlement

institution and marked with the same identifier;

5) client classification number – this shall mean the individual identifier of a client

assigned by the relevant settlement institution or another identifier assigned to a

client or group of clients defined according to specific criteria or to a settlement

institution member.

3. Unless these provisions or the provisions of the Rules provide otherwise, in relations

between KDPW_CCP and participants, documents containing statements or information

referred to in these provisions shall be transmitted in electronic form, via the National

Depository, pursuant to the principles set out in agreements concluded between the

National Depository and participants, accepting as effective statements of will and

transmission of information in electronic form.

§ 2

1. Subject to § 28 subpara. 3 of the Rules and subpara. 2 herein, documents delivered

by participants or by entities applying for a participation agreement, as well as other

2

official documents, which have been drawn up originally in the English language,

should be submitted to KDPW_CCP in this language version. In instances where these

documents have been drawn up in a foreign language, they should be submitted in

Polish or English translation, written and endorsed by a certified translator.

2. An application for a participation agreement or for extension of the scope of

participation, a declaration on membership of the relevant ATS guarantee fund, as well

as a statement accepting jurisdiction of the arbitration court at the National

Depository, should be drawn up in Polish, and in addition they being submitted in an

English language version, however, the applicant should in such instances declare that

the Polish language document shall be deemed the definite version.

§ 3

1. Official documents delivered by participants or entities applying for a participation

agreement, which have been drawn up outside the Republic of Poland, shall become

legally authorised in accordance with the relevant legal regulations, subject to the

provisions of subpara. 2.

2. If an official document has been drawn up in a country which is a signatory of the

Hague Convention of 5 October 1961 which eliminated the need to legally authorise

foreign official documents, such a document should contain an apostille

(authentication) issued by the relevant authority issuing the document.

§ 4

1. A bank account indicated by a participant pursuant to § 20 subpara. 2 point 3 of the

Rules shall be the bank account used to settle cash liabilities and receivables of the

participant related to participation in the relevant settlement institution.

2. If a participant is not a participant of the relevant settlement institution, the bank

account indicated by the participant pursuant to § 20 subpara. 2 point 3 of the Rules

shall be the bank account used to settle cash liabilities and receivables related to the

participation of the participant’s settlement agent in that settlement institution.

3. If the National Depository is the relevant settlement institution and cash liabilities

and receivables of the participant or the participant’s settlement agent are settled in

two or more bank accounts held in the clearing bank, the bank account indicated

pursuant to § 20 subpara. 2 point 3 of the Rules shall be the primary bank account

within the meaning of regulations issued by the National Depository.

4. If transactions for which a participant holds clearing member status are cleared in

foreign currencies, the participant shall indicate a bank account for the clearing of

transactions in each of such currencies.

3

§ 5

1. If there is a take-over of an enterprise, whose operation is related to participation in

the clearing system operated by KDPW_CCP, in the form of a sale of the enterprise

between participants, those participants who are parties to the action leading to the

take-over are required to immediately notify the National Depository of this fact,

including with the notification documents that constitute the basis of the take-over of

the enterprise, as well as all appropriate declarations.

2. In the event referred to in subpara. 1, KDPW_CCP shall, on the joint application of

the interested participants, set the date of the merger of their cash liabilities and

receivables arising from participation in the clearing system.

3. The merger date is the date at the end of which KDPW_CCP ceases to clear the

transactions of the participant whose enterprise has been taken over, for purposes

relating to the basis of the take-over.

4. A consequence of the merger is the transfer of the status of the participant holding

clearing member status held by the participant being taken over, to the extent of the

enterprise being taken over, to the participant taking it over.

§ 6

1. A transaction concluded on a regulated market or in an alternative trading system

shall be considered a transaction concluded as a part of the performance, under an

agreement with the market or system operator, of obligations consisting in buying and

selling specific financial instruments, for purposes related to supporting liquidity or

organising trading, provided that prior to conclusion of a transaction KDPW_CCP is

informed by the entity that it has concluded an agreement with a KDPW_CCP

participant or another entity which is a party to the transaction or its client, whereby it

agrees to perform such obligations.

2. In case of transactions referred to in subpara. 1, reductions of fees charged by

KDPW_CCP from a participant shall only apply where such transactions are settled in

registration accounts in the relevant settlement institution used only to register such

transactions.

§ 7

Participants may be informed of the content of resolutions adopted by the Supervisory

Board of the KDPW_CCP or the Management Board of the KDPW_CCP, which result in

conclusion, amendment or termination of a participation agreement, and the content of

other resolutions of those bodies concerning participants, using electronic

communication systems according to the provisions of the agreements referred to in §

4 subpara. 2 of the Rules.

4

§ 8

On written application of a participant, KDPW_CCP shall provide the participant with an

analysis of an invoice issued to the participant.

5

Chapter Two

Clearing and collateral of transactions

§ 9

1. On the basis of documents containing terms of transactions, referred to in § 38

subpara. 1 of the Rules, no later than 23:00 on the transaction date, KDPW_CCP shall

prepare and make available:

1) to participants holding clearing member status and to their payers – documents

stating the amount of cash liabilities and receivables of the participant in respect of

the clearing and collateral of transactions;

2) only to participants holding clearing member status – documents stating balances in

securities arising from concluded transactions.

2. In case of transactions concluded on the stock exchange market or in the alternative

trading system operated by the Warsaw Stock Exchange by entities which are not

participants or by participants with the participant status type Non-clearing Member,

KDPW_CCP shall in addition make available to participants holding clearing member

status within the scope of such transactions documents stating the amount of cash

liabilities and receivables in respect of such transactions immediately upon the receipt

of documents containing terms of transactions referred to in § 38 subpara. 1 of the

Rules.

3. An order to settle a transaction sent by KDPW_CCP to the relevant settlement

institution shall indicate that settlement shall take place in the accounts indicated in

the document containing the terms of the transaction referred to in § 38 subpara. 1 of

the Rules. If the document does not indicate a bank account for the settlement of the

transaction, KDPW_CCP shall:

1) where the National Depository is the relevant settlement institution – indicate in the

transaction settlement instruction that the settlement should take place in the default

account within the meaning of regulations issued by the National Depository, kept for a

participant holding clearing member status within the scope of the transaction or for

the participant’s settlement agent;

2) where the National Depository is not the relevant settlement institution – in the

account indicated by a participant holding clearing member status or by that

settlement institution.

§ 10

A participant holding clearing member status shall ensure that amounts necessary to

6

settle the participant’s liabilities arising from participation in clearing are deposited in

the bank account indicated by the participant pursuant to § 20 subpara. 2 point 3 of

the Rules within a time limit enabling the relevant settlement institution to execute

timely settlement of the transaction or collect the required collateral.

§ 11

1. Margins include maintenance margins, initial margins and additional margins.

2. The following are accepted as margins:

1) in case of maintenance margins – cash or securities acceptable to KDPW_CCP;

2) in case of initial margins – cash, securities acceptable to KDPW_CCP or a bank

guarantee granted to KDPW_CCP on request of the participant, which fulfils the

conditions set out in § 47c subpara. 1 of the Rules;

3) in case of additional margins – only cash.

3. Margins referred to in subpara 1 secure the liabilities of the participant who

deposits the margins, which arise from the clearing member status held by the

participant, arising both before and after the margin is deposited.

§ 12

1. A maintenance margin and an additional margin shall be deposited in cash by

means of debiting the relevant bank account indicated by the participant pursuant to §

20 subpara. 2 point 3 of the Rules. The account is debited by the National Depository

acting on request of KDPW_CCP.

2. An initial margin shall be deposited in cash by means of transferring cash to the

account of KDPW_CCP.

3. A participant who deposits a margin in cash shall ensure that the relevant bank

account indicated by the participant pursuant to § 20 subpara. 2 point 3 of the Rules

shows a cash balance sufficient to settle the participant’s liabilities in respect of

deposited margins taking into consideration all other liabilities to be settled in this

account.

4. A margin deposited in cash shall be returned by means of crediting the bank account

to which the margin was debited. Cash deposited as initial margin shall be returned on

the basis of a request to return the cash submitted by the participant, by means of

crediting the bank account indicated in the request.

§ 13

1. Securities deposited by participants as collateral in respect of an initial margin and

7

a maintenance margin may only include:

1) Treasury bonds traded on the regulated market in the territory of the Republic of

Poland;

2) shares of companies participating in the WIG20 index;

3) Treasury bills

if they are included on the list of securities determined by KDPW_CCP.

2) The list of securities acceptable as collateral referred to in subpara. 1 and the

corresponding recognition rates shall apply as of the moment of publication in a

communiqué for participants.

§ 14

1. Securities deposited by participants as initial margin or maintenance margin shall

be transferred to the securities account of KDPW_CCP kept in the relevant settlement

institution. Upon the transfer, KDPW_CCP and the participant holding clearing member

status who deposits the margin enter into an agreement concerning a transfer of

securities in favour of KDPW_CCP to secure liabilities of the participant which may be

settled with the margin according to the Rules and to pay the cost of such settlement.

2. In the period for which securities deposited as margin are in the securities account

of KDPW_CCP, KDPW_CCP shall not dispose of such securities other than to establish

the margin.

3. An instruction to transfer securities to the securities account of KDPW_CCP,

submitted to the relevant settlement institution in order to deposit such securities as

margin, shall specify the type of margin, the participant who deposits the margin, and

in the case of a maintenance margin also the client (client classification number)

whose positions are covered by the margin, who is the holder of a securities or

derivatives account kept by that participant. If an instruction to transfer securities is

submitted by an entity other than the participant who deposits the margin or the

participant’s settlement agent, that entity shall, before depositing securities as margin

for the first time, submit to KDPW_CCP a written statement in this regard, in which the

participant who deposits the margin should be specified.

4. Payments received by KDPW_CCP in respect of entitlements from securities

transferred to KDPW_CCP as margin shall be transferred by KDPW_CCP to the

participant holding clearing member status who has deposited the margin in an

amount reduced by any tax withheld. If, however, the participant is in arrears with the

payment of any cash liabilities arising from the participant’s clearing member status,

KDPW_CCP may credit such payments against such liabilities instead of transferring

them to the participant.

5. If an issuer redeems or cancels securities transferred to KDPW_CCP as margin,

8

KDPW_CCP shall transfer such received payments in an amount reduced by any tax

withheld to the participant holding clearing member status who has deposited the

margin. However, KDPW_CCP shall be entitled to use the payments in order to settle

the liabilities of the participant arising from the participant’s clearing member status,

provided that such payments shall in the first place be credited against the margin

deposited in the form of the cancelled securities to the extent that the value of the

remaining assets deposited as margin is lower than, respectively, the minimum or the

required value of the margin.

6. A return transfer of securities transferred to KDPW_CCP shall require the participant

holding clearing member status to make a relevant request to KDPW_CCP. On receipt of

such request, subject to subpara. 7, KDPW_CCP shall submit to the relevant settlement

institution an order to transfer the securities indicated in the order to an account kept

in the settlement institution from which the securities were transferred to the

securities account of KDPW_CCP.

7. A return transfer of securities shall take place provided that:

1) the securities do not need to be used in order to settle liabilities of the participant

holding clearing member status secured with the margin deposited by the participant

in the form of these securities, and

2) the conditions set out in § 71 subpara. 3 of the Rules have been fulfilled or the

participant who has deposited the margin no longer holds clearing member status.

§ 15

2. The part of the market value of securities recognised as collateral referred to in § 13

subpara. 1 shall be determined on the basis of the applicable recognition rate

determined by KDPW_CCP.

4. A zero recognition rate assigned to securities marked with a specific identifier

means that in the period of such assignment no part of the value of securities marked

with this identifier shall be recognised in determining the value of collateral referred to

in § 13 subpara. 1 deposited by a participant.

3. Securities shall be recognised as an initial margin up to 100% of the initial margin

amount. In cases justified by the security of clearing, the Management Board of

KDPW_CCP may reduce this indicator for a determined period by way of a resolution.

4. Assets designated as maintenance margin shall be deposited and recognised as

follows:

1) cash shall be deposited and recognised in the amount of the difference between

margins calculated for the relevant client classification number and the value of

securities recognised as margin;

2) securities may be deposited without limitation, however, they shall be recognised

9

up to 60% of the maintenance margin amount calculated for the relevant client

classification number.

5. The liabilities of a participant in respect of maintenance margins shall be equal to

the sum of margins calculated separately for each derivatives transactions portfolio

and each cash transactions portfolio for which the participant holds clearing member

status.

§ 16

1. The mode of calculating derivatives market margins is set out in Appendix 1.

2. The mode of calculating cash market margins is set out in Appendix 2.

3. The mode of calculating collateral referred to in § 52 subpara. 1 of the Rules is set

out in Appendix 3.

4. The clearing day timetable is set out in Appendix 4.

5. The structure of messages containing risk parameters used in calculations according

to the principles referred to in subpara. 1 – 3 is set out in Appendix 5.

§ 17

Income derived from the management of cash forming a margin shall be paid to

participants on a quarterly basis net of fees due to KDPW_CCP in respect of

management and administration of assets deposited as margin.

§ 18

1. Securities acceptable as contributions to the clearing fund and the ATS guarantee

funds shall only include bonds issued by the State Treasury traded on the regulated

market in the territory of the Republic of Poland and Treasury bills.

2. Securities referred to in subpara. 1 shall be recognised as a participant’s

contribution to the clearing fund or the ATS guarantee funds up to 90% of the sum of

the participant’s updated contributions to the fund.

§ 19

1. A participant holding clearing member status who is obliged to make a cash

payment according to the CH daily report in respect of liabilities arising from the

clearing of transactions concluded by the participant on the derivatives and cash

market shall be obliged, not later than 15 minutes before the commencement of a

session on the derivatives market on day R+1, to hold in the bank account in the

10

clearing bank indicated pursuant to § 20 subpara. 2 point 3 of the Rules, for which the

relevant settlement institution is authorised to act, an amount sufficient to settle such

liabilities to KDPW_CCP taking into consideration all other liabilities of the participant

in connection with its participation.

2. If, after the expiry of the deadline referred to in subpara. 1, there is a shortage of

balance on the bank account in the clearing bank indicated by the participant holding

clearing member status pursuant to § 20 subpara. 2 point 3 of the Rules, the value of

the initial margin referred to in § 49 subpara. 1 of the Rules deposited by the

participant shall be reduced by the amount equivalent to the shortage of balance. The

initial margin shall be reduced before the commencement of a session on the

derivatives market on day R+1.

3. Day R+1 referred to in subpara. 1 and 2 shall be understood as the day following the

clearing date of a transaction on the derivatives market.

§ 20

1. The concentration level referred to in § 50 subpara. 3 of the Rules determines the

number of positions open on the account of the same person in derivatives of a given

series, which, when exceeded, gives rise to the obligation of the participant holding

clearing member status to deposit an additional margin.

2. Concentration levels and related percentage ratios shall be set by KDPW_CCP solely

for those series of derivative instruments whose number of open positions exceeds

30,000.

3. Concentration levels and related percentage ratios shall be published by KDPW_CCP

on its website.

4. If a concentration level is exceeded, KDPW_CCP shall notify the participant holding

clearing member status of the requirement to deposit an additional margin.

5. The notice referred to in subpara. 4 shall be given in the form of an electronic

message after the clearing of a session on the derivatives market on the day when the

concentration limit was exceeded.

6. The additional margin amount shall be calculated as the maintenance margin of the

portfolio or portfolios under the same client classification number, for which the

concentration limit was exceeded, times the percentage ratio. Liabilities and

receivables in respect of additional margin shall be netted with other liabilities and

receivables of the participant to KDPW_CCP determined on the day of clearing a

session on the derivatives market when the concentration limit was exceeded.

11

7. A participant holding clearing member status shall deposit an additional margin no

later than the day following the day of giving the participant the notice referred to in

subpara. 4.

8. A participant holding clearing member status shall be relieved of the obligation to

deposit an additional margin on the day when the participant receives from KDPW_CCP

a message to the effect that the position in derivatives does not exceed the

concentration level. The message shall be transferred in electronic form.

9. An additional margin shall be returned by KDPW_CCP to the participant holding

clearing member status on the day following the day when the participant receives the

message referred to in subpara. 8.

§ 21

1. The transaction limit referred to in § 51 subpara. 1 of the Rules determines the value

of the liabilities that a participant holding clearing member status may take on in a

given session on the derivatives market in respect of maintenance margins and

marking-to-market.

2. Where a position is opened (long or short) in index participation units or options, the

transaction limit shall be charged with the value securing the one-day variation of the

price of the given instrument.

3. On the last day of trading in futures contracts which are exercised through delivery

of pre-defined securities, the transaction limit shall be charged with the value of the

maintenance margin securing the delivery of those securities.

4. The degree to which the transaction limit is used by a participant holding clearing

member status shall be determined by comparing the liabilities of that participant

calculated at a set time during the session on the derivatives market with deposited

margins. During the session on the derivatives market, KDPW_CCP shall actively

monitor the degree to which the transaction limit and the engagement limit referred to

in § 51 subpara. 2 of the Rules have been used.

5. KDPW_CCP shall inform a participant holding clearing member status of the degree

to which the transaction limit is used, when the level of use rises over 90% and 95% of

the value of that margin.

6. If a participant holding clearing member status exceeds the transaction limit or the

engagement limit, derivatives market participants may be denied the right to conclude

transactions in which that participant is indicated as a clearing member within this

scope.

§ 22

12

1. On each day when transactions are cleared, KDPW_CCP shall prepare CH daily

reports and make them available to participants holding clearing member status.

2. The daily CH reports shall contain:

1) at the level of positions designed with a given ISIN code:

a) the derivatives balance;

b) the receivables or liabilities to be paid as part of marking-to-market and the

premium;

c) the receivables or liabilities arising from the final clearing of liabilities related to the

expiry or exercise of derivatives positions;

2) at the portfolio level:

a) a statement of balances in registers of securities deposited as maintenance margin;

b) the net receivables or liabilities to be paid as part of marking-to-market, the

premium, and the final clearing of liabilities related to the expiry or exercise of

derivatives positions;

c) the calculated value of the maintenance margin;

d) the value of the recognised margin in cash;

e) the value of the recognised margin in securities,

f) the receivables or liabilities to be paid in cash.

13

Chapter Three

Detailed rules of clearing transactions concluded on the derivatives market

§ 23

After each session on the derivatives market, KDPW_CCP shall calculate the liabilities

and receivables arising from positions taken in futures contracts that need to be paid

as part of marking to market. The calculation of these liabilities and receivables shall

be performed according to the following principles:

1) on the day a position is taken, the liabilities of the buyer and the receivables of

the seller shall be equal to the difference between the price of a futures contract

upon purchase and the settlement price for that series of futures contracts on the

day in question, provided that the difference is positive; otherwise, the difference

shall represent the liabilities of the seller and the receivables of the buyer;

2) on subsequent days, excluding the expiry date of a given series of futures

contracts, the liabilities of the buyer and the receivables of the seller shall be

equal to the difference between the settlement price from the preceding day and

the settlement price on the current day, provided that the difference is positive;

otherwise, the difference shall represent the liabilities of the seller and the

receivables of the buyer;

3) on the expiry date of a given series of futures contracts, the liabilities of the

parties shall be determined respectively according to the principles defined in

points 1 and 2 with the calculation of the difference between the settlement price

from the preceding day and the final settlement price for a futures contract in that

series or – if a position was taken on the expiry date of a given series of futures

contracts – the difference between the actual contract price and the final

settlement price for a futures contract in that series;

4) on the day of delivery of futures contracts in exercise of an option, the liabilities of

the holder of a long position in futures contracts and the receivables of the holder

of a short position in futures contracts shall be equal to the difference between the

option exercise price and the settlement price of the futures contract on the

current day, provided that the difference is positive; otherwise, the difference shall

represent the receivables of the holder of a long position in futures contracts and

the liabilities of the holder of a short position in futures contracts.

14

§ 24

1. If a long position in futures contracts is closed, the participant closing the position

shall be debited with the amount representing the difference between the settlement

price from the preceding day in the series in question and the price of the contract

closing the position, provided that the difference is positive; otherwise, the participant

closing the position shall be credited with the said amount.

2. If a long position in futures contracts is opened and closed on the same day, the

participant closing the position shall be debited with the amount representing the

difference between the price of the contract opening the position and the price of the

contract closing the position, provided that the difference is positive; otherwise, the

participant closing the position shall be credited with the said amount.

3. If a short position in futures contracts is closed, the participant closing the position

shall be debited with the amount representing the difference between the price of the

contract closing the position and the settlement price from the preceding day in the

series in question, provided that the difference is positive; otherwise, the participant

closing the position shall be credited with the said amount.

4. If a short position in futures contracts is opened and closed on the same day, the

participant closing the position shall be debited with the amount representing the

difference between the price of the contract closing the position and the price of the

contract opening the position, provided that the difference is positive; otherwise, the

participant closing the position shall be credited with the said amount.

§ 25

1. On the day of opening positions arising from concluded transactions in index

participation units or premium-style options, KDPW_CCP shall determine the liabilities

of the buyer and the receivables of the seller on the basis of the value of the premium,

whose level is defined in the terms of the transaction.

2. On days following the day of opening positions arising from concluded transactions

referred to in subpara. 1, the liabilities of the buyer and the receivables of the seller

shall not be determined.

§ 26

1. On the day of opening positions arising from concluded transactions in futures-style

options, KDPW_CCP shall not determine the liabilities and receivables of the buyer and

the seller in respect of the premium.

2. After each session on the derivatives market, KDPW_CCP shall calculate the

liabilities and receivables arising from positions taken in futures-style options. The

15

calculation of these liabilities and receivables shall be performed according to the

following principles:

1) on the day a position is taken, the liabilities of the buyer and the receivables of

the seller shall be equal to the difference between the price of options upon

purchase and the settlement price for that series of options on the day in question,

provided that the difference is positive; otherwise, the difference shall represent

the liabilities of the seller and the receivables of the buyer;

2) on subsequent days, excluding the option exercise date, the liabilities of the

buyer and the receivables of the seller shall be equal to the difference between the

settlement price from the preceding day and the settlement price on the current

day, provided that the difference is positive; otherwise, the difference shall

represent the liabilities of the seller and the receivables of the buyer;

3) on the option exercise date, the liabilities of the parties shall be determined

respectively according to the principles defined in points 1 and 2 with the

calculation of the difference between the settlement price from the preceding day

and the final settlement price for options or – if a position was taken on the option

exercise date – the difference between the price of the option and the final

settlement price for options in that series.

§ 27

1. If a long position in futures-style options is closed, KDPW_CCP shall debit the

participant closing the position with the amount representing the difference between

the settlement price of the options from the preceding day and the price of the options

closing the position, provided that the difference is positive; otherwise, the participant

closing the position shall be credited with the said amount.

2. If a long position in futures-style options is opened and closed on the same day,

KDPW_CCP shall debit the participant closing the position with the amount

representing the difference between the price of the options opening the position and

the price of the options closing the position, provided that the difference is positive;

otherwise, the participant closing the position shall be credited with the said amount.

3. If a short position in futures-style options is closed, KDPW_CCP shall debit the

participant closing the position with the amount representing the difference between

the price of the options closing the position and the settlement price of the options

from the preceding day, provided that the difference is positive; otherwise, the

participant closing the position shall be credited with the said amount.

4. If a short position in futures-style options is opened and closed on the same day,

KDPW_CCP shall debit the participant closing the position with the amount

16

representing the difference between the price of the options closing the position and

the price of the options opening the position, provided that the difference is positive;

otherwise, the participant closing the position shall be credited with the said amount.

§ 28

1. Index participation units and American-style options shall be exercised

automatically on the day of their expiry or at the request of the holder of a long

position.

2. European-style options shall be exercised automatically on the day of their expiry.

3. Premium-style options shall be exercised on condition that:

1) for call options – the difference between the settlement price and the option

exercise price is a positive number,

2) for put options – the difference between the option exercise price and the settlement

price is a positive number.

3. In the event of the exercise of an index participation unit, KDPW_CCP shall debit the

holder of the short position and credit the holder of the long position with an amount

corresponding to the settlement price, following the application of the appropriate

multiplier.

5. In the event of the exercise of a premium-style call option, KDPW_CCP shall debit the

holder of the short position and credit the holder of the long position with an amount

corresponding to the difference between the settlement price and the option exercise

price.

5. In the event of the exercise of a premium-style put option, KDPW_CCP shall debit the

holder of the short position and credit the holder of the long position with an amount

corresponding to the difference between the option exercise price and the settlement

price.

7. Futures-style options shall be exercised on the day of their expiry after the close of

trading on condition that:

1) for call options – the difference between the settlement price and the option

exercise price is not a negative number,

2) for put options – the difference between the option exercise price and the settlement

price is not a negative number.

8. In the event of the exercise of a futures-style option, KDPW_CCP shall credit the

holder of the short position and debit the holder of the long position with the premium

corresponding to the option settlement price on exercise date.

17

§ 29

The principles of determining settlement prices shall be laid down by the operator of

the relevant derivatives market.

§ 30

1. An order to exercise index participation units or American-style options shall be

executed by KDPW_CCP on a given day provided that a participant holding clearing

member status has introduced an exercise instruction into the clearing system no later

than 45 minutes after the close of trading on that day on the derivatives market

relevant for the given financial instrument. On the basis of the received exercise

instruction, KDPW_CCP shall submit to the relevant settlement institution an order to

block a relevant number of index participation unit or options. Such orders shall be

executed from the first day of trading until the day preceding the last day of trading.

2. Holders of short positions who are obliged to exercise shall be selected at random

taking into account the principle of minimising the number of accounts participating in

the execution of a single exercise order.

3. A holder of a long position may waive automatic exercise of an option provided that

a participant holding clearing member status submits a waiver instruction to

KDPW_CCP no later than 45 minutes after the close of trading on the last day of trading

in the given option series on the relevant derivatives market.

4. An instruction to change the status of index participation units or options to

“blocked for exercise”, referred to in subpara. 1, and a waiver instruction, referred to in

subpara. 4, cannot be cancelled after KDPW_CCP has received from the operator of the

derivatives market relevant for the given financial instrument documents which

constitute the basis for the clearing of transactions concluded on that market.

§ 31

If a transfer of positions referred to in § 69 subpara. 4 of the Rules has taken place, the

participant holding clearing member status who is the transfer recipient shall only be

responsible for liabilities for positions which have been transferred arising from the

day immediately following the transfer day.

§ 32

1. Orders to transfer positions opened as a result of transactions concluded on the

derivatives market submitted by KDPW_CCP to the relevant settlement institution may

concern:

1) positions taken as a result of a transaction concluded before the transfer date in

18

connection with the obligation to transfer their ownership or without the transfer of

their ownership;

2) positions registered in the incorrect account kept for the participant or the

participant’s settlement agent in the relevant settlement institution;

3) positions opened as a result of a transaction concluded on the basis of a collective

order issued by the manager of a portfolio, on account of clients for which the manager

pursues the same investment strategy;

4) positions taken as a result of a transaction concluded on the transfer date in

connection with the obligation to transfer their ownership or without the transfer of

their ownership.

2. Instructions to transfer positions between accounts kept in the relevant settlement

institution for different participants holding clearing members status or their

settlement agents shall be considered to match if they contain matching information

relating to:

1) the type of instruction;

2) the instruction matching mode;

3) the operation identifier, excluding the trading mode code;

4) the derivative instrument code number;

5) the number of positions;

6) the settlement date;

7) the numbers of accounts between which the positions are to be transferred;

8) the position identifier;

and

9) the clearing operation number – for transfers referred to in subpara. 1 point 2-4.

3. KDPW_CCP shall submit an order to transfer positions referred to in subpara. 1 point

1 on condition that on the transfer date the number of positions indicated in the

instruction or instructions ordering the transfer is at least equal to the number of

positions of the same type registered in the account from which the transfer is to be

carried out.

4. KDPW_CCP shall submit an order to transfer positions referred to in subpara. 1 point

2 on condition that the clearing operation number, the number of positions to be

transferred, the number of the account from which the transfer is to be carried out and

the transfer date, all indicated in the instruction ordering the transfer, correctly match,

as appropriate, the clearing operation number, the number of positions, the number of

the account and the transaction date indicated in the document referred to in § 38

subpara. 1 of the Rules, which is the basis for the clearing of the transaction and

incorrectly indicates the account through which the transaction is to be settled in the

relevant settlement institution.

19

5. KDPW_CCP shall submit an order to transfer positions referred to in subpara. 1 point

3 on condition that the clearing operation number, the number of the account from

which the transfer is to be carried out and the transfer date, all indicated in the

instruction or instructions ordering the transfer, correctly match, as appropriate, the

clearing operation number, the number of the account and the transaction date

indicated in the document referred to in § 38 subpara. 1 of the Rules, which is the

basis for the clearing of a transaction concluded on the basis of a collective order

issued by the manager and the sum of positions indicated in all the instructions

ordering these transfers does not exceed the number of positions of the same type

opened as a result of the transaction marked with a given clearing operation number.

7. KDPW_CCP shall submit an order to transfer positions referred to in subpara. 1 point

4 on condition that the clearing operation number, the number of the account from

which the transfer is to be carried out and the transfer date, all indicated in the

instruction or instructions ordering the transfer, correctly match, as appropriate, the

clearing operation number, the number of the account and the transaction date

indicated in the document referred to in § 38 subpara. 1 of the Rules, which is the

basis for the clearing of a transaction which opened these positions and the sum of

positions indicated in all the instructions ordering these transfers does not exceed the

number of positions of the same type opened as a result of the transaction marked with

a given clearing operation number.

8. The transfers referred to in subpara. 1 points 2-4 shall only be performed on the date

of the transaction involving the positions to be transferred.

9. The transfers referred to in subpara. 1 points 2-4 shall be performed according to

the price of the transaction marked with the same clearing operation number as the

transfer.

§ 33

1. In order to cancel an instruction to transfer positions opened as a result of

transactions concluded on the derivatives market, which has been introduced to the

clearing system, a participant shall submit to KDPW_CCP a cancellation instruction,

which should clearly identify the cancelled document.

2. A cancellation instruction referred to in subpara. 1 may be submitted after the close

of a session on the derivatives market. Submission of a cancellation instruction does

not mean that the instruction to transfer positions opened as a result of transactions

concluded on the derivatives market has been effectively cancelled. A cancellation

instruction may not be executed after the execution of the instruction to transfer

positions.

3. An instruction to cancel an instruction to transfer positions, which should be

20

matched with another instruction, may be submitted until the time of matching, and

after matching on condition that KDPW_CCP receives two matching cancellation

instructions submitted by both parties to clearing. An instruction which need not be

matched with another instruction may be cancelled until the time of execution of the

instruction to transfer positions.

4. Cancellation instructions submitted by both parties to clearing shall be considered

to match if cancelled documents indicated in these instructions are the basis of the

same operation in the clearing system.

21

Chapter Four

Transitional provisions

§ 34

1. Subject to the provisions of § 35 subpara. 2, until 28 September 2012, securities

shall be deposited as maintenance margin or initial margin by changing the status of

such securities to “blocked as margin” in the relevant settlement institution:

1) in the depository or securities account of a participant holding clearing member

status; or

2) in the depository account of the settlement agent of such participant; or

3) subject to the provisions of subpara. 2, in the depository account kept for another

entity.

2. Securities blocked in the depository account kept in the relevant settlement

institution for an entity referred to in subpara. 1 point 3 may only be deposited as a

maintenance margin. Before the first such block, a participant holding clearing

member status shall submit to KDPW_CCP a written statement indicating in particular

the depository account and the entity holding such depository account, in which

securities are to be blocked as a maintenance margin deposited by the participant.

3. In order to unblock securities deposited as a margin, a participant holding clearing

member status who has deposited the margin shall submit to KDPW_CCP an instruction

to change the status of the securities respectively. The instruction should specify the

type of margin, the securities to be unblocked, the holder of the depository or

securities account kept in the relevant settlement institution in which the securities are

blocked, and in case of a maintenance margin also the client (client classification

number) whose positions are covered by the margin.

4. On receipt of the instruction referred to in subpara. 3, KDPW_CCP shall submit to the

relevant settlement institution an order to unblock securities deposited as a margin

provided that:

1) the securities do not need to be used in order to settle liabilities of the participant

holding clearing member status secured with the margin deposited by the participant

in the form of these securities, and

2) the conditions set out in § 71 subpara. 3 of the Rules have been fulfilled or the

participant who has deposited the margin no longer holds clearing member status.

22

Ҥ 35

1. Starting from 1 October 2012, KDPW_CCP shall use for the purposes of maintenance

and initial margin only those securities which have been provided for this purpose by

the participant, in accordance with the principles described in § 14 subpara. 1, subject

to the provisions of subpara. 2 below.

2. Despite the expiry of the deadline, described in subpara. 1, KDPW_CCP may use

securities, which have been blocked for margining purposes according to the

principles described in § 34 subpara. 1, in the event of circumstances that indicate

there is a risk involved in their use for the purposes of meeting the obligations secured

using these securities and the participant has not conformed to the principles coming

into force on 1 October 2012.

3. In order to conform to the principles that come into force on 1 October 2012, relating

to the provision of securities for the purpose of using them as maintenance and initial

margin, a participant with the status of clearing member, who, in accordance with the

provisions of § 34 subpara. 1, has blocked securities on the depository account or the

securities account managed by the relevant settlement system for use as margin, shall

change the scope of this margin through the delivery to KDPW_CCP of the following not

later than 28 September 2012 before 12.00:

1) in instances where the margin consists of securities blocked for the purpose

of use as initial margin – a written declaration on these securities being used for

the purpose of initial margin, according to the principles described in § 14

subpara. 1;

2) in instances where the margin consists of securities blocked for the purpose

of use as maintenance margin –

a) an instruction changing the status of the blocked securities, which were

provided for margining purposes on 28 September 2012 and transferring these

securities according to the principles described in § 14 subpara. 1 onto the

account managed by the relevant settlement system on behalf of KDPW_CCP, or,

b) an instruction to transfer on that date for the purpose of maintenance margin,

according to the principles described in § 14 subpara. 1, other securities than

the securities which have been blocked, which correspond to them at least in

value calculated for margin purposes on 28 September 2012 onto the securities

account managed by the relevant settlement system on behalf of KDPW_CCP.

23

4. Following the receipt from the participant of the declaration, described in subpara. 3

item 1, KDPW_CCP shall send an instruction to the relevant settlement system, at the

closing clearing session on 28 September 2012, which shall change the status of the

blocked securities, which were provided on that date for the purpose of initial margin,

and which shall transfer these securities onto the securities account managed by the

relevant settlement system on behalf of KDPW_CCP, in order for them to be exercised

by that settlement system at the next settlement session dedicated to this type of

operation.

5. If a participant changes the scope of the initial margin in a manner described in

subpara. 3 item 2 a., KDPW_CCP, at the close of the clearing session on 28 September

2012, shall send the relevant settlement system an instruction changing the status of

blocked securities, which on that date had been provided for margining purposes and

transferring these securities onto the account managed on behalf of KDPW_CCP in this

settlement system in order for them to be exercised by that system at the next

settlement session dedicated to this type of operation.

6. If a participant changes the scope of the initial margin in a manner described in

subpara. 3 item 2 b., KDPW_CCP shall send on 28 September 2012 to the relevant

settlement system and instruction releasing the blocked securities used for the

purpose of maintenance margin, on condition that:

1) The instruction, described in § 34 subpara. 3 will be delivered by the

participant to KDPW_CCP before 12.00 on that date at the latest, and that

2) Other securities than blocked securities described in subpara. 3 item 2b. will

be registered on the securities account managed on behalf of KDPW_CCP for

the purpose of maintenance margin.

7. If the participant does not perform the activities described in subpara. 3, the

provisions of § 12 subparas. 1-3 shall apply accordingly.

24

Appendix No. 1

to the KDPW_CCP Detailed Clearing Rules

Calculating the level of margin deposits for the derivatives market

1 Methodology used to calculate the level of margin deposits for the derivatives market

Maintenance margin is used to safeguard against any potential future change in price of open

positions in derivatives in a given portfolio. Maintenance margins are calculated using SPAN®

methodology, using risk parameters set each day by KDPW_CCP on the basis of up-to-date

market analysis.

The size of the maintenance margin that needs to be posted by the participant is calculated

using the value of the participant’s payment liabilities arising from transactions, while

factoring in the reduction in risk as a result of the relevant correlation between financial

instruments.

KDPW_CCP provides a daily file containing in particular values for risk scenarios and risk

parameter values.

In order to maintain the security of the clearing process, KDPW_CCP may amend the risk

parameters during the course of a trading session on the stock exchange in order to mitigate

risk effectively.

Detailed information on the KDPW_CCP risk management system using SPAN methodology can

be found on the KDPW_CCP website.

25

1.1 Calculating the value of maintenance margin for a portfolio

The value of required maintenance margin (DZP) for portfolio p of a given clearing member is

the maximum value of the difference between the sum total of margins in each class (DZK) and

the sum of the excess of the value of long positions calculated for all classes (NOD) and the

figure zero.

k k

pkpkp NODDZKDZP 0;max

p - portfolio identifier

k - class identifier

The above formula enables the offsetting of maintenance margins in a single class using the

value of (positive) net positions in options in a different class.

1.2 Calculating maintenance margins per class in a portfolio

The required maintenance margin on a given accounting day for a given class k in a portfolio

(DZK) is calculated on the basis of the margin securing the risk of price change in a portfolio

(DZW) and the value of net positions in options (PNO).

1.3 Calculating the value of the excess of the value of long positions in options

In instances where the value (DZW – PNO) is a positive integer, it forms the margin requirement

for a given class in the portfolio. In instances where the value (DZW – PNO) is a negative value,

then this value is segregated as NOD and is used in order to lower margin requirements in

other classes in a given portfolio.

0;min pkpkpk PNODZWNOD

0;max pkpkpk PNODZWDZK

26

pkNOD - excess of the value of long positions in options in portfolio p and class k

1.4 Calculating the value of the margin securing the risk of portfolio price change

Margins used to secure the risk of changes in the value of instruments (DZW) belonging to

portfolio p in a given class, are calculated in a given time horizon as the sum total of the margin

for the scenario risk, the inter-class spread margin and delivery margin, less the value of the

inter-class spread credit. The margin calculates using this method cannot however be lower

than the value of the minimum margin deposit for short positions in options in this portfolio.

pkppkpkpkpk mdkocspkdddswkdrscDZW ;max

drsc - margin for scenario risk

dswk - margin for inter-class spread

dd - margin for delivery

cspk - inter-class spread credit

mdko - minimum deposit for short positions in options

1.5 Margin for scenario risk (drsc)

The margin for scenario risk is calculated on the basis of analysis of the reaction to the value of

the value of the portfolio in a given class within each risk scenario and it equals the level of the

risk when assuming the worse case market scenario (in SPAN® terminology, this is the

scenario with the highest positive risk value). When calculating risk scenarios for futures, only

the price change factor is used, while for options, the price change is used together with

changes in levels of volatility and time.

1.6 Margin for inter-class spread (dswk)

The margin for inter-class spread is calculated in relation to positions within a portfolio of a

given class with varying expiry dates in order to secure against the risk of non-correlated price

change.

1.7 Margin for delivery (dd)

The margin for delivery may be calculated in relation to positions within a portfolio which are

nearing their expiry, as well as positions within a delivery cycle and secures against the risk of

changes in the composition of a portfolio, or against the risk inherent in the delivery cycle.

27

1.8 Inter-class spread credit (cspk)

Inter-class spread credit can be calculated in relation to those portfolio positions whose risk is

mutually correlated, which leads to lower margin requirements.

1.9 Minimum deposit for short positions in options (mdko)

Portfolios with short positions in options contain a certain level of residual risk. The required

margin for the portfolio cannot be lower than the limit defined by KDPW_CCP, which is the

minimum margin deposit for short positions in options.

The value of the minimum deposit for short positions in options (mdko) are calculated as

follows:

kpkpk dmkomdko

ko - number of short positions in options

dm - minimum deposit for each short position in options

28

Appendix No. 2

to the KDPW_CCP Detailed Clearing Rules

Calculating margins for the cash market (share and bond positions)

1. Definitions

Whenever these provisions refer to:

1) liquidity class – this shall mean all series of securities other than derivatives, with a

similar risk profile;

2) duration class – this shall mean all series of non-equity (non-share based) securities,

within the meaning of Article 4, point 10 of the Law on Public Offerings and Conditions

Governing the Introduction of Financial Instruments to Organised Trading and Public

Companies of 29 July, 2005 (Dz. U. (Journal of Laws) of 2009 No. 185, item 1439), with

similar modified life spans and the same ratings class defined by KDPW_CCP, with similar

risk profiles;

3) portfolio – this shall mean a set of positions arising from executed transactions, which

have not yet been settled, with the same entity code;

4) k– this shall mean the liquidity class identifier;

5) p – this shall mean the portfolio identifier.

2. Methodology for calculating margins in the cash market

Margins are calculated using SPAN® methodology.

Following receipt of documents containing transaction details, KDPW_CCP calculates the value

of the maintenance margin for each portfolio taking into account in the calculation the

statistically highest possible position loss during the subsequent session, determined using

correlated positions within the portfolio.

The margin is calculated daily starting from the date of the execution of the

transaction, until the settlement date.

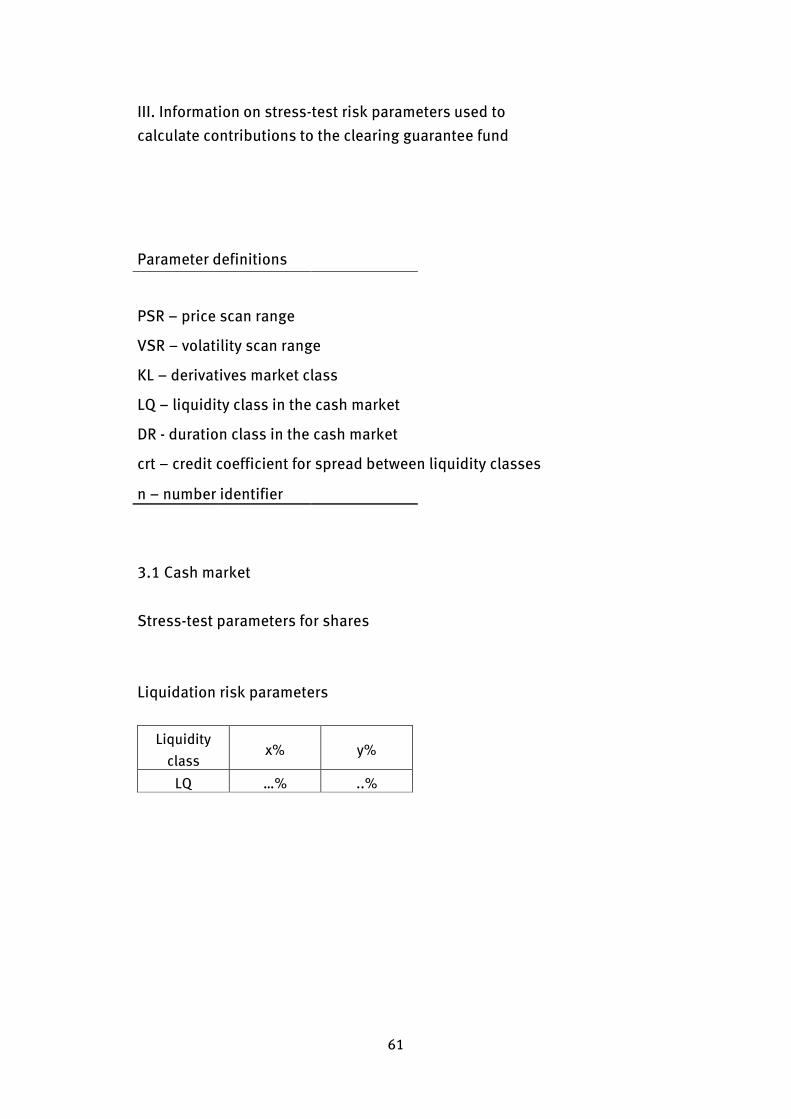

3. Calculating risk for shares

The algorithm used to assign instruments to a given liquidity class takes into account

the following:

The average liquidity of the instrument,

The instrument type.

29

3.1. Calculating the total net position in the portfolio (CPN)

The value of the positions in the portfolio in a given instrument is calculated by

multiplying the net number of instruments by the reference price. Adding together the

sum total of values for positions in each instrument in a given class, gives the value of

purchase positions (PK) and sell positions (PS).

The total net position in the portfolio ( CPN ) is calculated by liquidity class and

expresses an absolute value which is the difference between the total of purchase and

sale positions.

pkpkpk PSPKCPN

3.2. Calculating the total gross position in the portfolio (CPB)

The total gross position in the portfolio ( CPB ) is calculated by liquidity class and

corresponds to the total value of purchase and sale positions.

pkpkpk PSPKCPB

3.3. Calculating the margin for intermediate risk (DPLR)

The margin for intermediate risk ( DPLR ) is calculated as the sum of the margin for

market risk ( DRR ) and the margin for specific risk ( DRS ).

pkpkpk DRSDRRDPLR

3.3.1. Calculating margin for market risk (DRR)

Market risk is understood to mean the risk of price variation of financial instruments

within a given liquidity class. In order to calculate the margin for the value of margin

risk, the parameter yk is used,

The margin for market risk ( DRR ) is calculated by multiplying the total net position of

the portfolio (CPN ) by the level of market risk (yk ).

pkpkkpk PSPKyDRR

30

3.3.2. Calculating margin for specific risk (DRS)

Specific risk includes the variation risk inherent in a given liquidity class and the price

volatility of a given financial instrument. In order to calculate the margin for the value

of specific risk, the parameter xk is used, which defines the level of specific risk for a

given liquidity class.

The margin for specific risk is calculated by multiplying the total gross position of the

portfolio (CPB) by the parameter xk

pkpkkpk PSPKxDRS

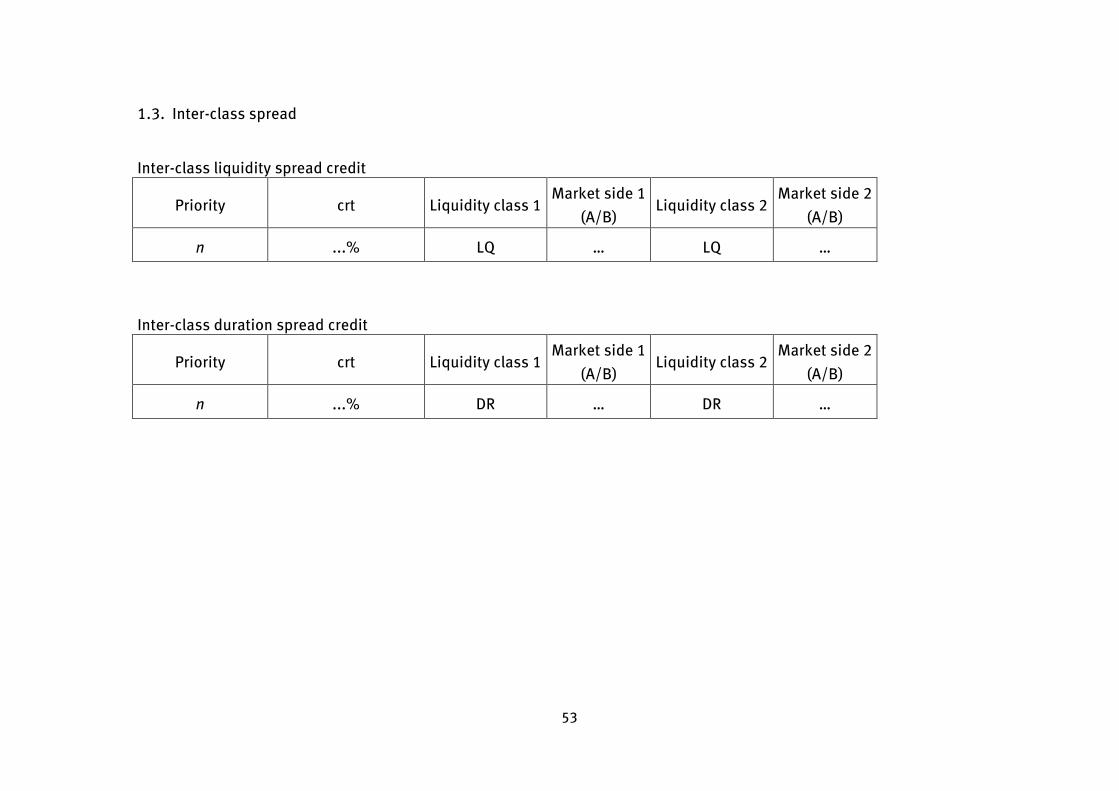

3. 4. Calculating the inter-class spread credit (KSPK)

Margin requirements for intermediate risk may be lowered by applying inter-class

spread credit, which reflects correlations between certain liquidity classes.

The value of the inter-class spread credit is calculated using the credit co-efficient (crt)

and the value of the total net position in each class. The priority in which spreads are

created is defined on the basis of tables containing credit spread priorities,

determined by KDPW_CCP.

2121

;min; /21 pkpkkkpkPSPKPSPKcrtkkSPK K

TABLE 1 Principles used for determining credits for spreads

LP. Principles

1. Total net positions in classes k1 and k2 must have opposite sides.

2. KDPW_CCP defines a table of valid class pairs for which credit is provided, the

value of the credit and the order in which each pair is credited.

3.

If a total net position in a given class remains unused for credit, then the next

opposite total net position is searched for, in accordance with the principles

contained in the priority table defined by KDPW_CCP.

4. The credit for the inter-class spread relates to each leg of the spread.

31

3. 5. Calculating margin for final intermediate risk (DOLR)

The margin for final intermediate risk ( DOLR ) for a given portfolio in a given class of

instruments is calculated on the basis of final market risk, which itself is determined

by deducting the value of the spread credit for a given class of instrument ( SPKK ) from

the value of intermediate market risk ( DPLR).

pkKSPKDPLRDOLR pkpk

4. Calculating risk for bonds

The risk for bonds is calculated on the basis of net purchase and sale positions

awaiting clearing. Bonds are assigned to a duration class indicated by KDPW_CCP for a

given day. Calculations are performed at the portfolio level.

4.1. Assigning bonds to a duration class

Each bond is assigned to a duration class on the basis of the value of the modified

duration indicator and rating class. The assignment is carried out at the end of each

day on which transaction clearing is performed. KDPW_CCP reserves the right to

change the change the manner in which the bond is assigned to take into account the

risk characteristics. KDPW_CCP provides information to market participants on each

bond assigned to the relevant duration class.

4. 2. Calculating net positions according to the bond type

The net position value in each instrument is calculated by multiplying the number of

instruments by the nominal value of the bond, the modified duration indicator and the

reference price.

The value of purchase positions (PK) and sale positions (PS) is obtained by adding the

value of calculated positions in each instrument in a given duration class.

4.3. Calculating the total net position (CPN)

The total net position (CPN ) is calculated for a duration class as the absolute value

from the difference between the total of purchase position values ( PK ) and the total

of sale position values ( PS ) in the portfolio of the clearing member.

pkpkpk PSPKCPN

4.4. Calculating the total gross position (CPB)

The total gross position (CPB ) is calculated for a duration class, as the total of

purchase position values ( PK ) and the total of sale position values ( PS ).

32

pkpkpk PSPKCPB

4.5. Calculating margin for intermediate market risk (DPLR)

Determining intermediate risk takes place on the basis of the calculation of the value of

the market risk and the value of the specific risk at the level of each duration class

within the portfolio.

The margin for intermediate market risk is calculated using the total margin

determined for market risk ( DRR ) and the margin determined for specific risk ( DRS ).

pkpkpk DRSDRRDPLR

4.5.1. Calculating the margin for market risk

Market risk is understood to mean the risk of variation in the income curve in a given

duration class. The parameter (yk ) is used to calculate the margin for the value of

market risk.

The (yk) parameter, which defines the level of market risk, is indicated by KDPW_CCP

for each duration class.

The margin for market risk ( DRR ) is calculated by multiplying the total net position for

a portfolio (CPN ) by the level of market risk (yk), for a given instrument class (k).

pkpkkpk PSPKyDRR

4.5.2. Calculating margin for specific risk

Specific risk includes the risk of variation of a given instrument from the standard

inherent in a given duration class, based on the instrument’s specific characteristics.

In order to calculate the margin for the value of specific risk, the parameter (xk) is used,

which is defined by KDPW_CCP for each duration class.

The margin for specific risk is calculated by multiplying the total gross position of the

portfolio (CPB ) by the parameter describing the specific risk (xk) for a given instrument

class.

pkpkkpk PSPKxDRS

33

4.6. Calculating margin for inter-class spread (DSWK)

The margin for inter-class spread is calculated in such a way as to secure against the

risk of an irregular repositioning of the income curve within a given duration class. This

margin is only calculated for bonds in relation to both opposite positions forming the

spread within a given class.

pkpkk PSPKdep ;minpkDSWK

where:

kdep - percentage for inter-class spread margin

4.7. Calculating the inter-class spread credit (KSPK)

Calculating the inter-class spread credit (KSPK) allows for the reduction of intermediate

market risk by recognising the correlation between positions in different duration

classes.

2121

;min; /21 pkpkkkpkPSPKPSPKcrtkkSPK K

TAB. 2 Principles used for calculating margins for spreads

LP. Principles

1. Total net positions in classes k1 and k2 must have opposite sides.

2. KDPW_CCP defines a table of valid class pairs for which credit is provided, the

value of the credit and the order in which each pair is credited.

3.

If a total net position in a given class remains unused for credit, then the next

opposite total net position is searched for, in accordance with the principles

contained in the priority table defined by KDPW_CCP.

4. The credit for the inter-class spread relates to each leg of the spread.

34

4.8. Calculating margin for final risk (DOLR)

The margin for final risk ( DOLR ) calculated for a portfolio in a given duration class is

equivalent to the margin for intermediate market risk ( DPLR), less the assigned credit

( SPKK ) and with the addition of the required deposit for spread in a given class

( SWKD ).

pkpk DK SWKSPKDPLRDOLR pkpk

4.9. Marking to market (WR)

Marking to market (WR ), is the process of calculating the debits and credits within a

portfolio using up-to-date market prices. It is calculated as the difference between the

value of positions in the clearing cycle re-valued using existing market prices and the

clearing value based on the executed transaction.

ipipipipi cSBWROZWR *

where:

piWROZ the number of securities i bought and sold for portfolio p multiplied by the

transaction unit price (this is a negative figure for purchase transactions),

ic securities reference price,

pipi SB , number of securities bought and sold.

The mark-to-market value, used to calculate maintenance margin is expressed in the

following formula:

i

ipupu WRWRD 0;min ,,,

5. Calculating maintenance margin

The required margin for a portfolio that is not marked-to-market (DZP) is equivalent to

the total final risk ( DCLR). The required margin for a portfolio is calculated as the sum

of the margin for final margin risk for each liquidity class and the margin for final

market risk for each duration class.

k

pk

k

pkpp SWKSPKDPLRDOLRDCLRDZP pkpk DK

35

The required margin for positions within a portfolio for transactions from the cash

market is the total of the values of the required margin (DZP) and the value arising from

the mark-to-market process (WRD).

ppp WRDDZPDZ

36

Appendix No. 3

to the KDPW_CCP Detailed Clearing Rules

Rules for calculating the minimum value of assets charged by participants to clients

placing transaction orders in the derivatives market

1. Methodology used to set initial margins by clearing members

KDPW_CCP approves the following methodologies to be used to set initial margins for

client portfolios:

1) SPAN® methodology;

2) Portfolio Risk Calculation Model (MPKR);

3) Other methodologies, following prior approval by KDPW_CCP.

1.1. SPAN® Methodology

The value of the initial margin required to be paid by clients of clearing members may

be determined using SPAN® methodology, in addition to up-to-date risk parameters

defined by KDPW_CCP. KDPW_CCP publishes a set of risk parameters at least once a

day, or at the end of a stock exchange session. The new set of risk parameters remains

in force until it is replaced by a new set.

The value of the required initial margin is calculated on the basis of the margin

securing the transaction price assigned to a given portfolio and the net value of options

positions.

Where a client delivers new transaction orders, the necessary initial margin will need to

reflect the least advantageous effect of their execution on the value of the portfolio,

arising respectively from the realisation of all pending client orders, their partial

realisation, or failure to realise them.

Where a client delivers an order for the execution of an option sale transaction settled

premium style, the value of the required initial margin calculated using SPAN®

methodology may be decreased by the value of the premium indicated in the order.

37

1.2. MPKR Methodology

1.2.1. Risk parameters

The Portfolio Risk Calculation Model (MPKR) uses parameters specified by KDPW_CCP

to calculate margins, with which the risk for a whole portfolio may be determined:

a. Level of maintenance margin for a given class ( kZ ),

b. Volatility of a given series of options in a year ( iVO ),

c. Credit co-efficient for a given class of long positions in options and index

participation units (CRT ),

d. Parameter modifying the volatility for a given options class ( kVM ),

e. Value of the parameter limiting the level of the risk for options positions in

scenarios 15 and 16 ( SATLMT ),

f. Free of risk rate for trading currency defined for a given series of options ( r ),

g. Annual dividend rate, set by the WSE for the underlying instrument for a given

options series, while for currency options, the free of risk rate for the currency of

the underlying instrument for a given series of options (q),

h. Parameters increasing the level of maintenance margin for each type of

derivative instrument: (futB ) – futures contracts,

(ipuB ) – index participation units, (

opB ) – options.

In order to calculate margins, fundamental variables arising from transaction execution

are also used, which relate to the contract settlement price, the premium, the number

of options contracts purchased

i. Number of positions in futures contract of series “i”- (negative number indicates

short position)( iL ),

j. Settlement price for futures contract in series “i” – or closing price for index

participation units series “i”- ( iC ).

38

1.2.2. Risk scenarios

In the MPKR model, simulations are carried out using 16 scenarios to verify how the

value of the portfolio will change with the impact of variation in the price of the

underlying instrument and changes in volatility.

Figure 1

Scenario

no. [j] Scenario

Range of

price

change

[uj]

Probability

[wj]

Direction of

volatility

[kj]

1 Const range, volatility ceiling 0,0 1 1

2 Const range, volatility floor 0,0 1 -1

3

Range 1/3 ceiling, volatility

ceiling 1/3

1

1

4 Range 1/3 ceiling, volatility floor 1/3 1 -1

5 Range 1/3 floor, volatility ceiling -1/3 1 1

6 Range 1/3 floor, volatility floor -1/3 1 -1

7

Range 2/3 ceiling, volatility

ceiling 2/3

1

1

8 Range 2/3 ceiling, volatility floor 2/3 1 -1

9 Range 2/3 floor, volatility ceiling -2/3 1 1

10 Range 2/3 floor, volatility floor -2/3 1 -1

11

Range 3/3 ceiling, volatility

ceiling 1,00

1

1

12 Range 3/3 ceiling, volatility floor 1,00 1 -1

13 Range 3/3 floor, volatility ceiling -1,00 1 1

14 Range 3/3 floor, volatility floor -1,00 1 -1

15 Range 2 x ceiling, const volatility 2,00 0,5 0

16 Range 2 x floor, const volatility -2,00 0,5 0

The value of margin jS in a given scenario „j” and for a given class of instruments

(typified by the same underlying instrument) is calculated as the sum:

39

n

i

ijj SS1 (Formula No. 1)

where:

ijS is the value of the margin for derivatives instrument of series “i” in scenario “j”,

n number of series in a given class of derivatives.

1.2.3. Principles of correlation

The level of the margin calculated for each of the 16 scenarios is the starting point for

calculating margins for client portfolios.

When applying the portfolio risk calculation model, correlation of positions may take

place for derivatives positions based on the same underlying instrument (in the same

class).

1.2.4. Calculating margins for each scenario

A. Futures contracts

The value of margin ijS for a given futures contract of series “i”- in scenario “j”- is

calculated according to the following formula:

jjfutkiiij wuBZCLS (Formula No. 2)

Where:

2;2;1;1;1;1;3

2;3

2;3

2;3

2;3

1;3

1;3

1;3

1;0,0;0,0 u

5,0;5,0;1;1;1;1;1;1;1;1;1;1;1;1;1;1w

B. Long position settled in index participation units

A long position settled in index participation units forms the margin for other positions

based on the same underlying instrument. The value of the margin at the close of the

day is equal to the reference price with a correction for a potential one-day change in

the price of the index participation unit, multiplied by the credit co-efficient (CRT). The

value of the margin for index participation units of series “i” in scenario “j”- is

calculated according to the following formula:

40

CRTwuBCZCLS jjipuikiiij (Formula No. 3)

C. Long position settled in put and call options

A long position settled in put and call options forms the margin for other positions

based on the same underlying instrument. The value of the margin is calculated using

the Black-Scholes model, based on Formulas 12 and 13 and is equal to the value of the

option premium divided by the value of the credit co-efficient CRT.

The value of margin ijS for options of series “i”- w „j”- in scenario “j”- is calculated

according to the following formula:

CRTPL

CRTPLS

p

iji

c

iji

ij (Formula No. 4)

where:

c

ijP - Value of the call option premium calculated using Formula No. 12

p

ijP - Value of the put option premium calculated using Formula No. 13

D. Short position settled in index participation units