rpc group plc/media/files/r/rpc-group... · · 2018-01-04rpc group plc 2017 / 18 interim results....

TRANSCRIPT

RPC – THE ESSENTIAL INGREDIENT

© 2017 RPC Group Plc. All Rights Reserved.

29 November 2017

RPC GROUP PLC 2017 / 18 INTERIM RESULTS

2

First half highlights 2017 / 18

Revenue +53% to £1,876mFCF +45% to £171.7m with strong cash conversion

Continued organic growth at c.2% Healthy innovation pipeline

Operating profit (adj.) +58% to £214.7mAdjusted EPS +27% to 36.4pInterim dividend +28% to 7.8p

ROS up 30bps to 11.4%RONOA up 320bps to 28%ROCE at 15.1% well above WACC

Letica integration well advancedAcquisition of Astrapak completed

European synergy programme on track and nearing completion with total implementation costs lower than expected

3

AgendaVision 2020 Strategy Pim Vervaat

Financial Overview Simon Kesterton

Market Overview Pim Vervaat

Summary and Outlook Pim Vervaat

4

Progress of Vision 2020 strategy in the first half year

FOC

USE

D G

RO

WTH

Focus on organic growth

Selective consolidation in Europe

Creating a meaningful presence outside Europe

• Continued organic growth at c.2% with healthy innovation pipeline• Global roll-out of patented sports caps continuing

• European synergy programme nearing completion • Opportunities to further consolidate the European plastic packaging market estimated

at >€26bn combined sales

• Acquisition of ‘mini RPC’ Astrapak completed• Greenfield plant in China on stream with Brazilian plant starting up • Further opportunities emerging from leveraging global platform

Pursuing added value opportunities in non packaging markets

• Expansion of Zhuhai operations generating profitable growth in the automotive market• Good contribution of ESE in first year of RPC ownership

Capital allocation

• Capital expenditure to support future growth in attractive market segments• Utilised £12.4m under £100m share buyback • Interim dividend up 28% representing 25th consecutive year of growth

5

Returns since Vision 2020 strategy launch

Strategy generates returns consistently above WACC

£475m

£2,371m

£2,846m

19.4%

14.3% 15.1%

2017 / 18

Capital employed

Return on capital employed

RPC GroupSeptember 2017

Acquisitions &c.£165m organic investments > depreciation

5 years

ROCE

Capitalemployed

2012 / 13RPC Group

pre Vision 2020

6

Selective acquisition opportunities in Europe Size of the opportunity in Europe

Good quality acquisition opportunities in Europe with sales >€26bn

c.€63bn

Numerous opportunities driven by:

• Short term hold periods of private equity • Owner-managed businesses with succession challenges

Note: Not representative of total market, only those targets actively monitored

Size(by revenue)

Number Combinedrevenues

>€500m 12 >€13bn

€50m-€500m 60 >€11bn<€50m >100 >€2bnTotal >€26bn

Rigid and flexible plastic packaging

c.€3bnRPC

*Smithers Pira, 2017; converted to EUR using an exchange rate of 0.88

Europe*

Actively monitored targets

(European packaging only)

7

Financial Overview

8

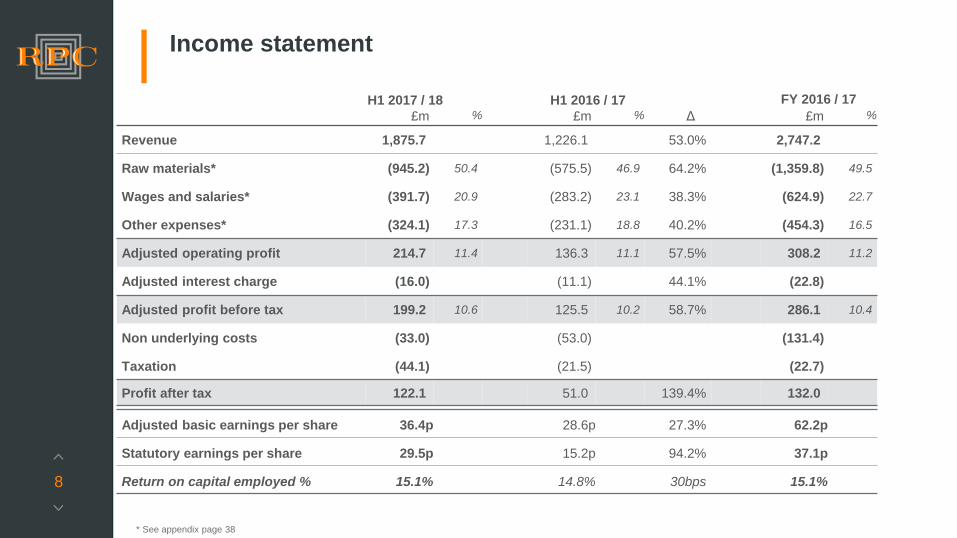

Income statement

H1 2017 / 18 H1 2016 / 17 FY 2016 / 17 £m % £m % Δ £m %

Revenue 1,875.7 1,226.1 53.0% 2,747.2

Raw materials* (945.2) 50.4 (575.5) 46.9 64.2% (1,359.8) 49.5

Wages and salaries* (391.7) 20.9 (283.2) 23.1 38.3% (624.9) 22.7

Other expenses* (324.1) 17.3 (231.1) 18.8 40.2% (454.3) 16.5

Adjusted operating profit 214.7 11.4 136.3 11.1 57.5% 308.2 11.2

Adjusted interest charge (16.0) (11.1) 44.1% (22.8)

Adjusted profit before tax 199.2 10.6 125.5 10.2 58.7% 286.1 10.4

Non underlying costs (33.0) (53.0) (131.4)

Taxation (44.1) (21.5) (22.7)

Profit after tax 122.1 51.0 139.4% 132.0

Adjusted basic earnings per share 36.4p 28.6p 27.3% 62.2p

Statutory earnings per share 29.5p 15.2p 94.2% 37.1p

Return on capital employed % 15.1% 14.8% 30bps 15.1%

* See appendix page 38

9

Revenue bridge (£m)

1,308

1,876

65

17

540

28

1,226

RevenueH1 2016 / 17

Impact FXtranslation

Polymer price Underlyingrevenue

H1 2016 / 17

Net acquisitions(prior yearrevenue)

Organic growth RevenueH1 2017 / 18

c.2%

30 9

501

Revenue H12016 / 17

FXtranslation

Polymer

Organic growth

10

Adjusted operating profit bridge (£m)

145

215(1)

(21)

10

49

42

136

Adjustedoperating

profitH1 2016 / 17

FXtranslation

Polymerpass through

variance

Underlyingoperating

profitH1 2016 / 17

Netacquisitions(prior year

profit)

Businessimprovement

Cost inflation Adjustedoperating

profitH1 2017 / 18

(1)3

47

Adjustedoperating profitH1 2016 / 17

FXtranslation

Polymer

Includes synergies* of £13m

* From Promens / GCS / BPI / Letica

11

Polymer pass through

€ PER TONNE: average of Platts / ICIS indices

HDPE BMPP HOMO

1,050

1,150

1,250

1,350

1,450

1,550

1,650

1,750

Mar 14 Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17 Sep 17

• Polymer pass through mechanisms in place (based on c. 65 indices) albeit with a time lag

• Proactive raw material stock and purchase contract management mitigating the pass through time lag effect

• Flexibility in purchasing various polymer grades for similar applications enhanced

800

900

1,000

1,100

1,200

1,300

1,400

Mar 14 Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17 Sep 17

£ PER TONNE: average of Platts / ICIS indices

Mainland Europe UK impacted by weakened sterling

Polymer price changes passed through to the customer base

$ PER TONNE: per IHS

1,200

1,400

1,600

1,800

2,000

2,200

2,400

Mar 14 Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17 Sep 17

US impacted by hurricanes

12

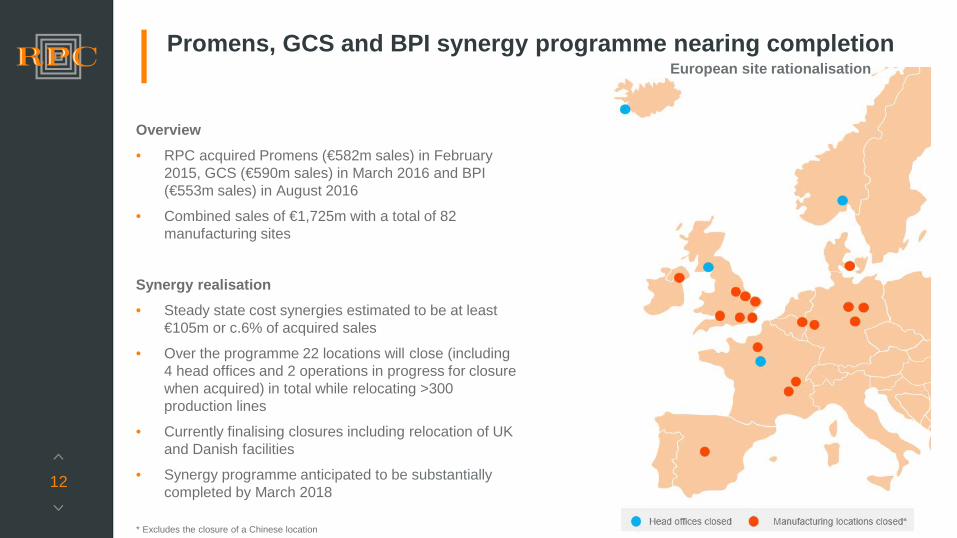

Promens, GCS and BPI synergy programme nearing completion

Overview• RPC acquired Promens (€582m sales) in February

2015, GCS (€590m sales) in March 2016 and BPI (€553m sales) in August 2016

• Combined sales of €1,725m with a total of 82 manufacturing sites

Synergy realisation• Steady state cost synergies estimated to be at least

€105m or c.6% of acquired sales

• Over the programme 22 locations will close (including 4 head offices and 2 operations in progress for closure when acquired) in total while relocating >300 production lines

• Currently finalising closures including relocation of UK and Danish facilities

• Synergy programme anticipated to be substantiallycompleted by March 2018

European site rationalisation

* Excludes the closure of a Chinese location

13

0

€35

€68€95 €105

14/15 15/16 16/17 17/18 18/19

€2

€30 €28€50

0

14/15 15/16 16/17 17/18 18/19

€(110)m

€30m

€45m

€(185)m

P&L charge Assetwrite downs

Proceeds,working capital & asset sales

Cash costs

Lower implementation costs than previously anticipated

• Total P&L charge is €185m, down from €190m previously announced

• The associated cash out is €110m, down from €120m previously announced – with steady state benefits remaining at least €105m per annum

Cash costs €m

By year

€6

€77 €77

€250

14/15 15/16 16/17 17/18 18/19

P&L costs €m

Synergy realisation

€m (cumulative)

Promens, GCS and BPI related synergy realisation costs

14

Non-underlying costs (see Appendix page 45 for definitions)

Interims Finals

£ million 2017 / 18 2016 / 17 2016 / 17 2015 / 16

Fitter for the Future - - - 3.8

Acquisition related expenditure 2.1 6.8 18.9 11.9

Deferred consideration on earn-outs 1.1 3.8 (11.2) (11.5)

Promens / GCS / BPI integration costs 10.3 19.1 66.8 58.6

Other integration and exceptional items (7.0) 3.0 9.7 5.4

Total exceptional items 6.5 32.7 84.2 68.2

Amortisation – acquired intangibles 25.3 11.0 31.0 10.3

Other (pension admin fees) 0.6 0.4 1.0 0.6

Total non-underlying operating items 32.4 44.1 116.2 79.1

Non-underlying finance costs 0.6 8.9 15.2 5.9

Total non-underlying costs 33.0 53.0 131.4 85.0

15

Underlying cash generation

Interims Finals

£ million 2017 / 18 2016 / 17 2016 / 17 2015 / 16

Adjusted EBITDA 296 199 441 251

Working capital 25 29 29 -

Net capex (108) (82) (176) (101)

Other* (1) - - 2

Operating cash flow 212 146 294 152

Net interest & tax (40) (28) (55) (29)

Free cash flow 172 118 239 123

Adj. conversion** 99% 107% 95% 87%

Statutory conversion# 97% 105% 82% 85%

80%

90%

100%

110%

0

80

160

240

H1 15/16 H1 16/17 H1 17/18

Adjusted operating profit Free cash flow Conversion (%)

£m

* Share based payments, disposal of fixed assets and pension deficit payments**Ratio of operating cash flow shown above to adjusted operating profit# see Appendix page 43

• Continued investment in growth; total capex to sales ratio of 5.8% (Capex / depreciation of 1.4x)

• Working capital synergies realised as acquisitions adopt RPC’s approach; working capital as a % of sales improved to 5.5% (2016: 6.1%)

• Both statutory cash flow conversion and underlying conversion remain strong

16

Net debt bridge

(1,070)

(108)(40) (1)

(77)(12) (9)

(74) (21)

296

25 (1,049)

Net DebtMar 2017

AdjustedEBITDA

WorkingCapital

InvestingActivities

Interest& Tax

Other freecashflowitems#

Acquisitions(inc. debt)

Sharebuyback

ExceptionalItems

Dividends Other* Net DebtSep 2017

Free cash flow £172m

# Share based payments, disposal of fixed assets and pension deficit payments* Includes exchange rate movements: (£18m), non-underlying cash provision movements: £17m, movement in provisions and financial instruments: £22m

17

Financial position

KPIs Sep 2017

Net debt (£m) 1,070

Headroom (£m) 1,077

Net debt to EBITDA ratio (pro forma)** 1.8x

Net debt to EBITDA covenant 3.5x

0

250

500

750

1,000

1,250

1,500

2017 2018 2019 2020 2021

Renewal date main facilities

USP

P

USP

P

£m

RC

F

RC

F

TER

M

Calendar year

*The 18 month term facility is extendable up to 2020 if required**Adjusted to include acquisitions on a pro forma basis

*

18

Capital allocation priorities

Profitable organic growth

Investing in organic growth and returns ahead of WACCTargeting through the cycle organic growth ahead of GDP

Acquisitions that meet strict investment criteria

17 acquisitions since launch of Vision 2020; demonstrating excellent returns well above WACC

Progressive dividend policy with dividend cover at 2.5x through the cycle

H1 17/18 DPS of 7.8p, up 28% and representing the 25th

consecutive year of growth

Leverage to remain at a suitable and responsible level

H1 17/18 net debt to EBITDA ratio of 1.8x (pro forma)Covenant 3.5x EBITDA

Announced inaugural share buyback programme of up to £100m* over a 12 month period to July 2018

Programme launched as share price undervalued the Group’s performance and future prospects

Capital priorities and structure

*£20.5m shares bought back to date at an average price of 906p

19

Technical guidance

For financial year 2017 / 18

Capex c. £230m

Depreciation c. £175m

Non-underlying cash provision utilisation c. £30m

Underlying tax rate c. 24.5%

Interest c. £34m

FX sensitivity: €1c move changes EBIT by c. £1.8m $1c move changes EBIT by c. £0.4m

Progressive dividend policy with cover targeted to be 2.5x across the cycle

Category GuidanceAcquisition related expenditure External cost on acquisition

activityDeferred consideration on earn-outs

• Ace: 40% c. £3m • Letica 40% c. £20m

Promens / GCS / BPI integration costs

P&L c. £21.5m (€25m) with c. £43m (€50m) cash

Other integration and exceptional items

Minor

Amortisation – acquired intangibles c. £50m

Other non-underlying items Minor

Non-underlying finance costs • Pension scheme interest c. £8m

• Interest on earn-outs:immaterial

• FX on earn-outs depends on FX rates

Non-underlying costs

20

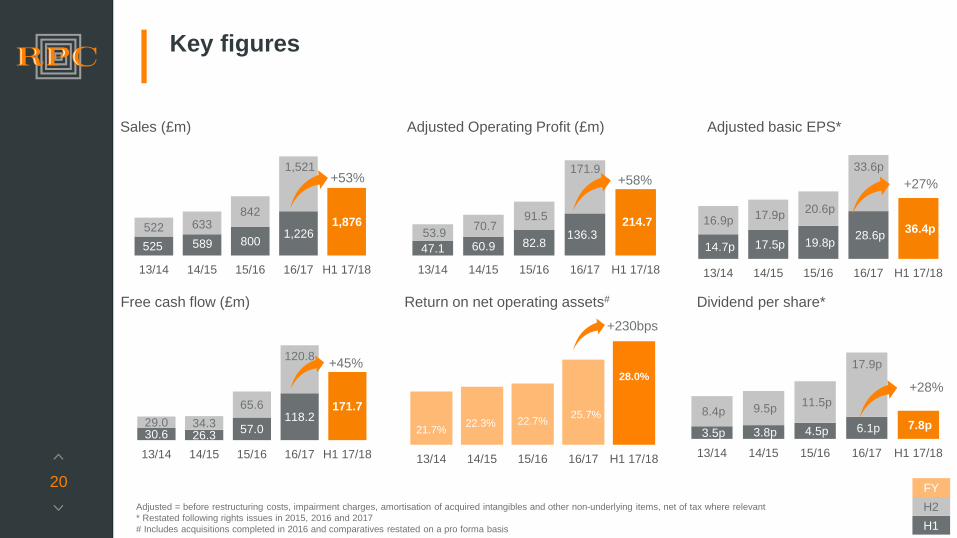

21.7% 22.3% 22.7% 25.7%

28.0%

13/14 14/15 15/16 16/17 H1 17/18

30.6 26.3 57.0 118.2

171.7 29.0 34.3

65.6

120.8

13/14 14/15 15/16 16/17 H1 17/18

+45%

+230bps

525 589 800 1,226 1,876 522 633

842

1,521

13/14 14/15 15/16 16/17 H1 17/18

+53%

47.1 60.9 82.8136.3

214.753.9 70.7

91.5

171.9

13/14 14/15 15/16 16/17 H1 17/18

+58%

Sales (£m) Adjusted Operating Profit (£m)

14.7p 17.5p 19.8p 28.6p 36.4p 16.9p 17.9p 20.6p

33.6p

13/14 14/15 15/16 16/17 H1 17/18

Adjusted basic EPS*

Adjusted = before restructuring costs, impairment charges, amortisation of acquired intangibles and other non-underlying items, net of tax where relevant* Restated following rights issues in 2015, 2016 and 2017 # Includes acquisitions completed in 2016 and comparatives restated on a pro forma basis

Key figures

+27%

Free cash flow (£m) Return on net operating assets#

3.5p 3.8p 4.5p 6.1p 7.8p 8.4p 9.5p 11.5p

17.9p

13/14 14/15 15/16 16/17 H1 17/18

Dividend per share*

+28%

H1H2FY

21

Market Overview

22

Organic growth in the first six months of 2017 / 18

Global plastic packaging markets over the next five years anticipated to grow c.4% with European growth rates at >2%* helped by ongoing material substitution

Good growth in Europe (representing 79% of total sales) with growth outside Europe tempered by hurricane impact in the US

Overall organic growth of c.2% reflecting improved activity levels in both packaging and non-packaging markets partially offset certain adverse natural events and by fewer trading days

Group targeting through the cycle growth ahead of GDP

Continued investment in innovation capabilities driving a healthy pipeline going forward

* Growth rates to 2022 (Source: Smithers Pira)

23

Sports Caps

Market leading beverage closure, developed in France Now produced in 6 countries across 3 continents; sold worldwide Efficient roll-out facilitated by internally developed standardised

approach Patented innovation incorporating functionality for on-the-go

consumption

Current sales

Growth through innovation and best practice sharing

2420 production lines installed with 17 still to come

Sports Caps (continued)

Current sales

Agreed additional sales

25

£353m H1 17 / 18+1% Organic growth

Key developments

RPC: growth in H1 driven by higher added value automotive components

Market: strong demand growth in complex automotive products, particularly in China

Outlook: portfolio of strong platforms for higher added value future growth

Technical Components

£378m H1 17 / 18+1% Organic growth

Key developments

RPC: good overall demand particularly for nicotine delivery systems offsetting decline in UK surface coatings

Market: growth driven by innovation in product design in various market segments

Outlook: continued growth in tobacco while staying focused on margin enhancement in mature market segments

Non-food

£565m H1 17 / 18+3% Organic growth

Key developments

RPC: good growth in agricultural films and confectionary products in H1

Market: growth driven by shelf-life enhancing solutions, portion control and minimising food waste. Agricultural market continues to grow

Outlook: ongoing growth with spreads market recovering as price of substitute (butter) increases

Food

Segmental development

26

£82m H1 17 / 18Static sales

Key developments

RPC: close to zero growth with new product launches later than envisaged

Market: dry powder inhalant devices set for longer term growth particularly in Western markets

Outlook: medium to longer term growth following formation of larger healthcare platform post Plastiape acquisition

Healthcare

£268m H1 17 / 18Static sales

Key developments

RPC: close to zero growth as demand in sport caps and CSD lite closures is offset by continued softness with European coffee capsule customers

Market: growing demand for higher added value single serve beverage capsules and closures

Outlook: continuing growth in closures combined with Brazilian coffee capsules plant starting up

Beverage

£230m H1 17 / 18+2% Organic growth

Key developments

RPC: increased sales in China driving growth in H1

Market: globalisation and higher quality products are key growth drivers

Outlook: further growth opportunities leveraging global platform and development of the air free DEFI system

Personal Care

Segmental development (continued)

27

Summary and Outlook

28

Second half of the year has started well

Encouraging trading in the first half with record profitability levels (both statutory and adjusted) and strong cash generation (both statutory and adjusted)

Will continue to target innovation based growth, leveraging global footprint, and expect to participate in the ongoing consolidation of the plastic packaging markets*

Unprecedented rationalisation of the European manufacturing footprint nearing completion, with the benefits being realised as anticipated

Letica integration progressing well with the expected cost savings on track

Summary and Outlook

* No significant acquisitions anticipated in the remainder of this financial year

29

Forward looking statementsThis presentation contains forward-looking statements, which:have been made by the directors in good faith based on the information available to them up to the time of the approval of this presentation and such information should be treated with caution due to the inherent uncertainties, including both economic and business risk factors, underlying such forward-looking information. The Group undertakes no obligation to update these forward-looking statements and nothing in this presentation should be construed as a profit forecast. Past performance is no guide to future performance and persons needing advice should consult an independent financial advisor.

Nothing in this presentation shall constitute, in any jurisdiction, an offer or solicitation to sell or purchase any securities or other financial instruments, nor shall it constitute a recommendation or advice in respect of any securities or other financial instruments or any other matter.

30

Supplementary Material

31

Appendices Disciplined and selective approach to acquisitions

Decentralised organisation enhances integration capability

Commitment to our people

Commitment to sustainability

Polymer capacity expected to increase

Income statement extract at FY 2014/15 polymer prices

Segmental and geographical analysis

Consolidated balance sheet

Employee benefits

Statutory cash flow

Adjusted earning reconciliation

Definitions

32

Core acquisition criteria Strategic fit Strength of incumbent management Financial track record Financial criteria:

• ROCE > WACC of RPC • Quantifiable cost and cash synergies• Impact on Group KPIs (ROS & RONOA)• Earnings accretion

Acquisitions generally concluded at below market average EBITDA multiples

Source:Mergermarket,company information

Overview (EV / EBITDA LTM)

2011-2013 Average 7.8x 2014-2017 Average 9.3x

Sector trading multiples

RPC major transactions =

Transaction multiples

Adding value Improving RPC’s overall commercial position Improving RPC’s strategic buying position Realising cost synergies (including procurement) Enhancing performance and innovation focus of acquired

businesses

Disciplined and selective approach to acquisitions

33

Disciplined and selective approach to acquisitions (continued)

>360

94

175%60% 25%

>215

Acquisition process

Acquired Hand over to divisional management team and corporate purchasing Of those reviewed in-depth, 17 were acquired equating to 18% More than one in three acquisitions have been off-market, one-to-one

processes initiated through existing industry relationships

Targets reviewed in-depth In-depth due diligence performed by RPC teams and external advisers Rejected when target does not meet RPC’s acquisition criteria

Desktop review Desktop review of businesses and market segment More attractive opportunities progressed to review involving business management teams Rejected where no strategic fit or value

Opportunities presented to RPC (since launch of Vision 2020) Industry is consolidating – numerous opportunities presented Database maintained with attractive assets to be actively approached40% Rejected without

extensive review

34

RPC divisions Strategic business units

Decentralised organisation enhances integration capability

“Mini RPC” sector management approach matching industry structure

Quality businesses acquired with key management retained

Central back office and procurement functions strengthened and scalable

Multiple growth platforms with strong divisional leadership teams - larger acquisitions spread in time and in different parts of the organisation

Proven track record of quickly integrating businesses and realising associated synergies

35

Commitment to our people

450

550

650

750

850

H1 15/16 H1 16/17 H1 17/18 2016/17

Reportable accident frequency rate (RAFR)*

Health & Safety

* number of accidents resulting in more than three days off work, excluding accidents where an employee is travelling to or from work, divided by average number of employees x 100k

• Health & Safety culture: • Number 1 priority for RPC; further reduction in RAFR• Annual Health & Safety week “Safety. It’s in our Hands”

• Sharesave:• New annual schemes launched across 23 countries• Take up of 4,468 employees (23%)

• Training & Development:• Apprentice training schemes established across many sites • International Graduate Development Programme• Succession plans in place across the organisation• Identification of key talent and potential• Range of talent development training programmes

RPC commitment to its employees

Full year results

36

Commitment to sustainability

• Raw Materials: Research and development of new materials such as biodegradable polymers

• Design & development:• Lightweighting• Use of recycled material in products• Product protection / waste reduction• Substitution of heavier materials

• Manufacturing:• Efficient use of water and electricity• Reduction of waste

• Recycling & the responsible disposal of plastic:• Closed loop recycling process – bpi recycled products & ESE

World• Involvement in external activities to increase recycling of plastic

e.g. New Plastics Economy Initiative

RPC commitment to sustainabilityThe plastic product lifecycle

We work with organisations including:

37

Polymer capacity expected to increase

• Capacity continues to grow and outpace demand

• Ability to source from outside Europe will become a key competitive advantage

• RPC’s scale, extensive network and flexibility provide a leading position from which to access global markets

• Key capacity additions are North America and Middle East, both targeting exports as markets globalise. China will look to become self-sufficient in PP, freeing capacity for other geographies

RPC’s European operations are well placed to take advantage of global markets

Global PP & PE:

70%

75%

80%

85%

90%

95%

100%

120135150165180195210225240255

2012 2013 2014 2015 2016 2017 2018 2019 2020

Capacity utilisation polymer industryTONNES (M) OPERATING RATE %

Operating rate Actual demand Free capacity Forecast demand

Source: IHS Markit

38

Income statement extract at FY 2014 / 15 polymer prices

H1 2017 / 18 2016 / 17 2015 / 16 2014 / 15£m % £m % £m % £m %

Revenue 1,876 2,747 1,642 1,222

Restated revenue 1,295 2,397 1,677 1,222

Raw materials (583) 45 (1,085) 45 (787) 47 (584) 48

Wages and salaries (288) 22 (558) 23 (384) 23 (280) 23

Other expenses (221) 17 (417) 17 (297) 18 (226) 18

• % of restated revenue• All costs exclude restructuring costs• Revenue and adjusted operating costs have been restated at FY 2014 / 15 polymer pricing

and before 2016 / 17 acquisitions

39

Segmental and geographical analysis

Interims % Finals

£ million 2017 / 18 2016 / 17 VarianceAt constant

exchange 2016 / 17

RevenuePackaging 1,592 1,055 50.8 43.4 2,365Non-packaging 284 171 66.6 56.2 382Total 1,876 1,226 53.0 45.2 2,747Operating profitPackaging 177.5 109.0 62.8 52.2 246.2Non-packaging 37.2 27.3 36.3 28.6 62.0Total 214.7 136.3 57.5 47.5 308.2Return on salesPackaging 11.2% 10.3% 90bps 70bps 10.4%Non-packaging 13.1% 16.0% (290)bps (280)bps 16.2%Total 11.4% 11.1% 30bps 20bps 11.2%

• Both packaging and non-packaging continue to grow with sales mix and acquisitions affecting non-packaging return on sales

40

Segmental and geographical analysis (continued)

Interims % Finals

£ million 2017 / 18 2016 / 17 VarianceAt constant

exchange 2016 / 17

RevenueEurope 1,477 1,052 40.4 33.6 2,363Rest of the world 399 174 128.7 115.4 384Total 1,876 1,226 53.0 45.2 2,747Operating profitEurope 161.5 106.9 51.1 41.8 245.1Rest of the world 53.2 29.4 81.0 68.0 63.1Total 214.7 136.3 57.5 47.5 308.2Return on salesEurope 10.9% 10.2% 80bps 60bps 10.4%Rest of the world 13.3% 16.9% (350)bps (370)bps 16.4%Total 11.4% 11.1% 30bps 20bps 11.2%

• Strong revenue growth by region; Rest of World return on sales affected by sales mix and acquisitions

41

Consolidated balance sheet

£ million SEP 2017 SEP 2016 MAR 2017

Property, plant and equipment 1,328.3 1,098.7 1,265.5

Goodwill 1,600.4 1,099.4 1,577.1

Other non-current assets 492.8 350.3 536.4

Working capital 207.7 169.1 220.3

Employee benefit liabilities (LT) (240.7) (300.9) (256.0)

Provisions, including deferred consideration (135.5) (171.3) (165.1)

Other assets & liabilities (317.6) (216.9) (312.0)

Assets held for sale - 1.8 5.6

Net debt (1,070.4) (833.0) (1,049.1)

Equity shareholder funds 1,865.0 1,197.2 1,822.7

42

H1 2017/18

H1 2016/17

FY 2016/17

Discount rate 2.7% 2.4% 2.6%

Inflation rate 2.1% 2.0% 2.1%

Employee benefits

£ million SEP 2017 SEP 2016 MAR 2017

Retirement benefit liability UK DBs 141.1 185.7 157.3

Other retirement benefit obligations 95.3 110.3 94.3

Termination benefits 0.7 0.8 0.9

Other employee benefit liabilities 3.6 4.1 3.5

Total employee benefit liability 240.7 300.9 256.0

• Improving discount rates plus deficit reduction payments have reduced the pension liability since the year end

• Key assumptions:

43

Statutory cash flow

Interims Finals

£ million 2017 / 18 2016 / 17 2016 / 17 2015 / 16

Adjusted EBITDA 296 199 441 251

Movement in working capital 25 29 29 -

Payment in respect of non-underlying items

(8) (28) (81) (50)

Movement in provisions and financial liabilities

(27) (21) (56) (19)

Cash generated by operations 286 179 333 182

Net capex (108) (82) (176) (101)

Cash flow 178 97 157 81

Statutory operating profit 182 92 192 95

Statutory conversion* 97% 105% 82% 85%

* Ratio of cash flow to statutory operating profit

• Capex ahead of depreciation (1.4x)

• Disciplined working capital management

• Costs and benefits of the Promens / GCS / BPI programme nearing completion with 87% investment in one time costs and 86% of the related benefits have been received

44

Adjusted earnings reconciliation

Earnings(£m)

Adjusted earnings & EPS 150.4

Acquisition and integration costs (12.4)

Deferred consideration on earn-outs (1.1)

Amortisation – acquired intangibles (25.3)

Other non-underlying items 5.8

Total non-underlying tax 4.7

Total adjustments (28.3)

Basic earnings & EPS 122.1 29.5p

(3.0)p

(0.3)p

(6.1)p

1.4p

1.1p

36.4p

(6.9)p

45

Definitions

Expense Description

Fitter for the Future All expenditure related to a business improvement programme announced before the Vision 2020 Focused Growth Strategy, which was centred on rationalising RPC’s European manufacturing footprint, optimising its business portfolio and realised value for the Group by disposing of its non-core businesses and redundant properties. This scheme was largely completed by the end of the 2014/15 financial year.

Acquisition related expenditure The advisors fees and other expenses directly relating to the Group’s completed acquisitions.

Deferred consideration on earn-outs

The remuneration earned by the shareholders of Ace and other acquisitions who must remain as employees of the Group for the duration of the earn-out period to qualify for the remuneration. It also includes adjustments related to the current expectation of the final payment.

Integration costs Costs relate to the integration of the Promens, GCS and BPI businesses into the RPC organisation, including related restructuring, redundancy, closure costs and impairment charges.

Other integration & exceptional items

Includes other items such as start up costs. It also includes restructuring, redundancy and closure costs of other business optimisation programmes not directly affected by the Promens, GCS and BPI integration and advisors fees directly relating to the group’s aborted acquisition processes.

Amortisation – acquired intangibles

Relates to amortisation of intangible assets such as brands and customer relationships related to acquired business (amortised to the income statement on a straight-line basis over their estimated useful life).

Other non-underlying items Other immaterial non underlying costs including the pension admin costs on closed DB schemes.

Non-underlying finance costs Includes finance charges related to the defined benefit pension schemes and the Ace contingent consideration finance cost and the associated foreign exchange impact on the US dollar liability.

46

Definitions (continued)

Category Description

Organic growth Period-on-period revenue change adjusted for constant exchange rates and polymer prices, pro forma for acquisitions completed in the current period and adjusted for disposals.

ROCE ROCE is measured over the relevant period (annualised for half year results) and normalised for the effect of acquisitions, is adjusted operating profit for continuing operations, divided by the average of opening and closing shareholders equity, after adjusting for net retirement benefit obligations, assets held for sale, acquisition intangibles and net borrowings for the year concerned.

RONOA RONOA is measured over the relevant period (annualised for half year results) and normalised for the effect of acquisitions, is adjusted operating profit for continuing operations divided by the average of opening and closing property plant and equipment and working capital for the year concerned. Comparatives are restated to include acquisitions on a pro forma basis.