roger lanctot, strategy analytics, managing the accelerating amount of software in cars

TRANSCRIPT

Red Bend Seminar:Managing the Accelerating Amount of Software in Cars

Roger C. Lanctot, Associate DirectorGlobal Automotive Practice

Strategy Analytics

September 2013

Where We Stand Today

Universal ConnectivityVs.

Consumer Indifference

Hardware in MarketOEM Embedded Telematics

Source: Automotive Multimedia & Communications - AMCS

2011 2013 2015 20170

25,000

50,000

75,000

100,000

125,000

150,000

24,716

39,548

73,895

140,430

Hardware in Market

Uni

ts 0

00's

Active SubsOEM Embedded Telematics

Source: Automotive Multimedia & Communications - AMCS

2011 2013 2015 20170

25,000

50,000

75,000

100,000

125,000

150,000

24,716

39,548

73,895

140,430

12,075

25,734

49,739

98,785

Hardware in MarketActive Subs

Uni

ts 0

00's

Inactive SubsOEM Embedded Telematics

Source: Automotive Multimedia & Communications - AMCS

2011 2013 2015 20170

25,000

50,000

75,000

100,000

125,000

150,000

24,716

39,548

73,895

140,430

12,075

25,734

49,739

98,785

12,641 13,814

24,156

41,645

Hardware in MarketActive SubsInactive Subs

Uni

ts 0

00's

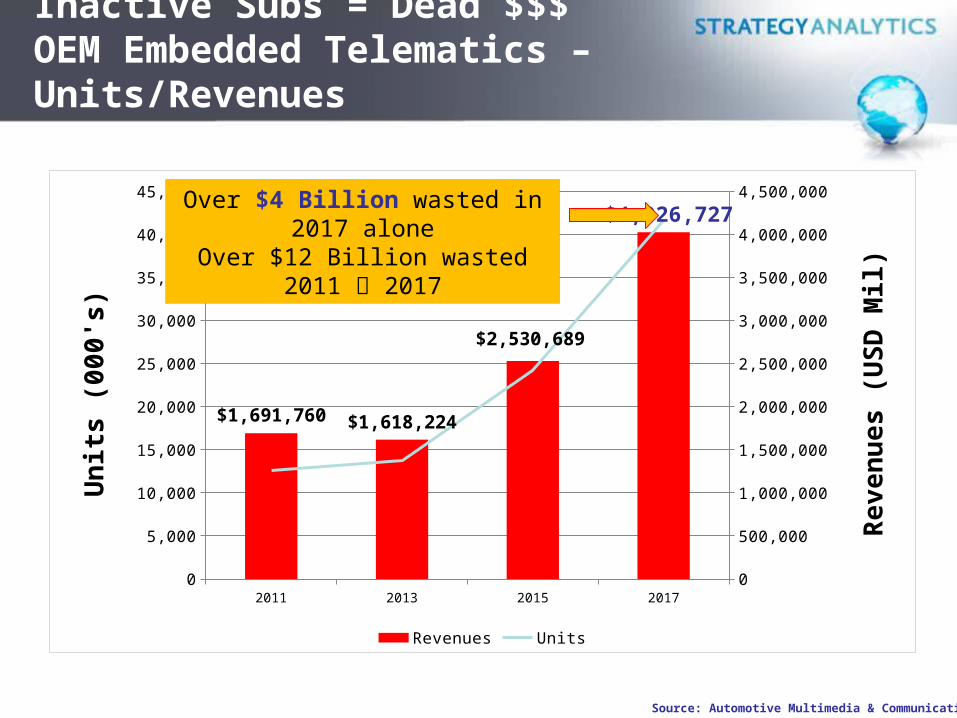

Inactive Subs = Dead $$$OEM Embedded Telematics – Units/Revenues

Source: Automotive Multimedia & Communications - AMCS

2011 2013 2015 20170

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

$1,691,760 $1,618,224

$2,530,689

$4,026,727

Revenues Units

Uni

ts (0

00's

)

Reve

nues

(USD

Mil)

Over $4 Billion wasted in 2017 aloneOver $12 Billion wasted 2011 2017

Customers Won’t Pay

Customers Don’t Use

Customers Don’t Care

Connected Car Going Nowhere

Big Picture

• Embedded telematics is not taking off• Smartphone connections are failing, fragmenting• Navigation/traffic has become a battleground – awareness

growing, solutions/service quality improving• Loss of focus on core value propositions

• But there is light at the end of the tunnel:– VRM-CRM– Safety

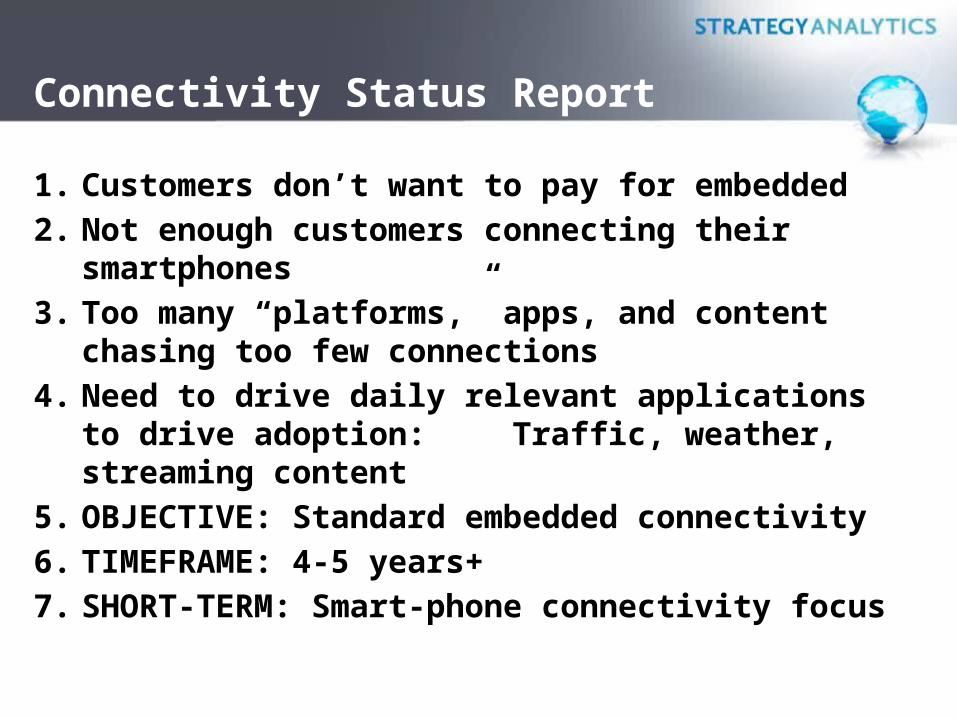

Connectivity Status Report

1. Customers don’t want to pay for embedded2. Not enough customers connecting their smartphones3. Too many “platforms,” apps, and content chasing too few

connections4. Need to drive daily relevant applications to drive adoption:

Traffic, weather, streaming content5. OBJECTIVE: Standard embedded connectivity6. TIMEFRAME: 4-5 years+7. SHORT-TERM: Smart-phone connectivity focus

Where We Stand Today

How is this picturechanging.

Big Three

• GM/OnStar – 100%!• Chrysler – will be ~ 10% for MY14 – FOTA via smartphone• Ford – EVs only for now – thumb drive updates - future?• Lincoln – Announced intention to embed

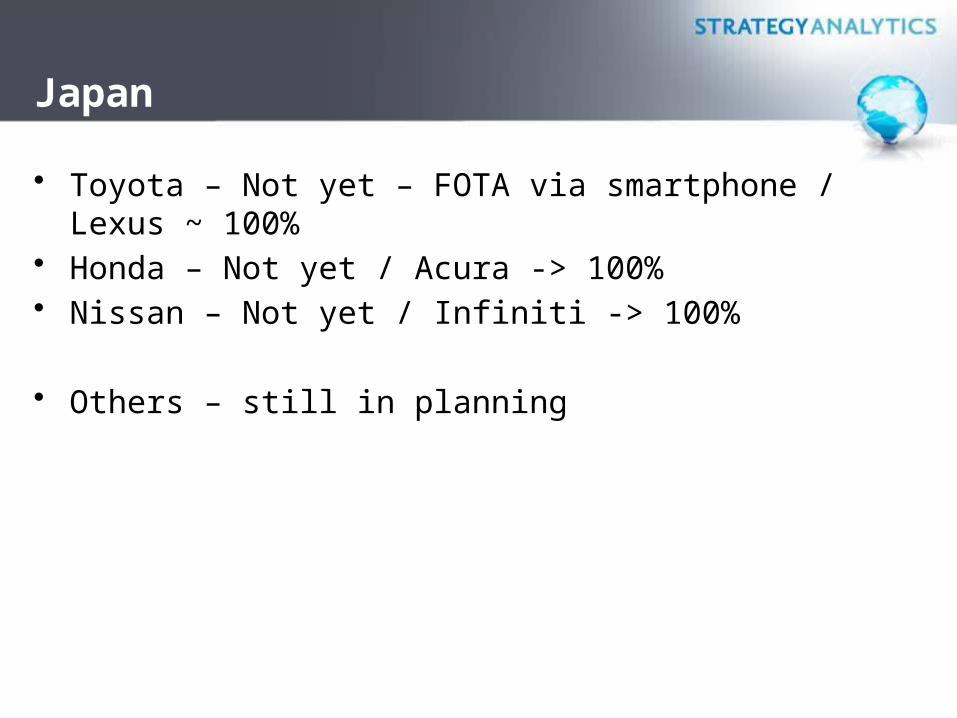

Japan

• Toyota – Not yet – FOTA via smartphone / Lexus ~ 100%• Honda – Not yet / Acura -> 100%• Nissan – Not yet / Infiniti -> 100%

• Others – still in planning

Germany

• BMW – 100%! – FOTA for CY2014?• Audi - ~ 50% - “aftermarket” SIM• Mercedes -> 100% - FOTA capable - “not replacing ECU software

yet”• VW -> 100%

France, Italy, UK, Sweden

• Fiat – not yet – thumb drive updates• Renault < 20%• PSA < 20%• Volvo -> 100% outside the U.S. – limited updates• Jaguar – not yet

Korea

• Kia – not yet• Hyundai -> 100%

Common Thread

• Japanese mass brands – value-oriented customer, highly reliable cars, low cost of ownership – difficult to justify embedded modem

• German luxury brands – BMW has made 100% fitment table stakes

• VW, Hyundai, Kia – similar value prop and challenge as Japanese• Domestics – GM’s planned shift to LTE will change the game –

true FOTA coming (ie. ECU updatability) – Chysler and Ford following slowly

Smartphone Connectivity

+ =

Customer Acquisition

Embedded Modem

+ =

Customer Retention

Why connect all cars?

RevenueMetrics – Can’t monetize or manage what you can’t measureRetention – What happened to our customers?Competitive threats – insurance companies, independent dealersPreserve the value of the fleet – lease customers, etc.

Why connect all cars?

Crowdsourcing – traffic, weather, safety, mapsCommunity building – ownership experienceFirmware updates – which version? Universal deploymentService – Dealer metrics for scheduled, ad hocReal-time customer connectionCustomer identification managementCustomer portalVehicle life-cycle management

Why FOTA?

• Hundreds of millions of lines of code• Why identify problems (diagnostics/prognostics) if you

can’t/won’t fix them?• Need to update mission-critical safety systems, powertrain etc.• Aftersales added value – enhance/transform ownership

experience• Reward consumer for being/staying connected• Software recalls – cost avoidance• Customer expectation/OEM obligation• We didn’t do it because we couldn’t – onset of LTE means “no

excuses”

Sirius XM Concept

Sirius XM is proposing a combination LTE/Satellite module as part of its plan to transition into telematics.Expected plan is to shift content distribution to XM while Sirius satellites are usedfor video and/or software updating. This concept has been greeted with skepticism by OEMs.

Biggest FOTA Challenges

• Role of the dealer – lost sales/service revenue, out of the loop• Consumer awareness/understanding/acceptance – customer

MUST be notified – customer MUST accept• Frequency – ad hoc, monthly, quarterly• Threshold for update – safety, security, size, timing, functionality

Big Customer Relationship Win + Potential Dealer AlienationGoal: Make it Win-Win for all

Current Dealer Landscape

• Hostile to FOTA• Misinformation/confusion regarding updates due to changes from

hardwire to wireless updating at the dealer• Lack of dealer-integrated management system for tracking

versions etc.• Software updates = customer visit = opportunity!• Software updates as a customer value proposition – a means to

exclude aftermarket – updates disable “mods”

• Updating ECUs is an important new phase!

Telematics ECU: OEM Global Shipments - Units and Revenues

• Telematics ECU Opportunity: 2012 vs. 2020 – ECU Shipments: +500% : 7.0 Million units in 2012 42 Million units in 2020– ECU Revenues: +320% : $910 Million in 2012 $3.8 Billion in 2020– Average Selling Price 2012: $130/unit 2020: $92/unit– The high volume Mass-Market Product in 2020 will have limited features

• E.g. eCall and support for Location Based Services/B2B communications: • Typical mass market product will have 3G Cell Modem + GPS/location capability

Source: Automotive Multimedia & Communications - AMCS

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Un

its (

000's

)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Reven

ues (

US

$ M

il)

Units Revenues

OEM Telematics ECUCellular Modem Choice - Global

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Un

its

(000

's)

2010 2011201220132014201520162017201820192020

4G

3G

2.5G

2G

• Telematics ECU Modem forecast 2012 vs. 2020 (7.0 Mil. units $42 Mil. units)– 2G Wireless Network: 21K units in ‘12 to Zero units in ‘20 Units – 2.5G Wireless Network: 6.3 Mil units to 0K units – 3G Wireless Network: 670K units to 26.6 Mil units – 4G Wireless Network: 55K units to 15.6 Mil units

Source: Automotive Multimedia & Communications - AMCS

Connectivity ECU - OEM: Units and Revenues

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Un

its

(000

's)

0

500

1,000

1,500

2,000

2,500

Rev

enu

es (

US

$ M

il)

Units Revenues

• Connectivity ECU Opportunity: 2012 vs. 2020 – ECU Shipments: +360% (7.2 Mil units in 2012 33.7 Mil units in 2020)– ECU Revenues: +220% ($725 Million in 2012 $2.3 Billion in 2020)

– Average Selling Price 2012: $100/unit 2020: $69– Examples include: SYNC, Entune, Blue&Me, Kia UVO, Mini Connected etc.

Source: Automotive Multimedia & Communications - AMCS

World ECU $ Per Vehicle

Polk: Average Age of Vehicles Hits Record High

Dealer share of collision business in decline

Tesla: Industry Disruption

Tesla – Industry Disruption

• Field upgradable telecom module• Field upgradable graphics• Company-owned stores• Streaming content via embedded modem• Limited HMI overhead + touch-centric vs. voice-centric• Firmware over the air updates• Top safety rating• Top score in Consumer Reports• Top Strategy Analytics customer clinic evaluation• Non-traditional sourcing and development• Googlemap! (VIDEO #1)

Tesla Update Process

• Notification message in car “Tesla has an update”• “Press here to download”• Timing of download and time required for download provided• Approve or change timing• Post update: Message detailing contents of update

• Biggest update thus far: addition of “creep” – addition of voice to make phone calls

Tesla Software Update Report

Google Disruption

Google – Industry Disruption

• Self-contained – no connection necessary• Uses its own map• Multiple consumer, commercial applications

• Quanergy: targeting replacing $70K Lidar unit with $500 unit with rotating element -> $200 solid state device

Elements Enabled by LTE

• Personalized, contextualized content engine (audio & video)• Live map – hybrid on/off-board – map updating• Ad hoc/mesh networked connectivity – Wi-Fi, cellular, other• Secure gateway (Cisco)• Alert-driven/workload managed interface – traffic, weather, etc.• Communication efficiency optimized – on/off-board data

management/processing “delta-focused”• Voice (Nuance), Metadata (Gracenote)• Preferences/policy-managed – data, app use, privacy

Four Core Value Propositions for Connectivity

1. Navigation/traffic/location – contextual awareness2. VRM/CRM3. Streaming content4. Connected safety – anticipating/avoiding crashes

OBJECTIVE: Telematics 2.0 = collision avoidance + delivering critical, real-time information safely to the driver before/as it is needed

Telematics 1.0 -> Telematics 2.0

Telematics 1.0

Automatic Crash Notification +Stolen Vehicle Recovery + Remote Diagnostics=Good Enough Telematics

44

Telematics 1.0 - Shortcomings

ReactiveLimited dealer engagementLimited use of vehicle dataLimited consumer access to dataLimited dealer access to data

45

Telematics 2.0

Firmware over the air updatesPrognosticsVRMIP-based traffic data, hybrid speech recognitionStreaming content

46

FOTA as a core connected car value proposition

• Necessary for mission-critical, safety updates• Strengthening bonds to the customer AND the car• Adding value after the sale• Avoiding costly recalls and, in some cases, inconvenient dealer

visits• Enhancing the customer experience• Maintaining vehicle software integrity

Thank you!

Roger C. LanctotAssociate DirectorGlobal Automotive PracticeStrategy [email protected]+1 (617) 614-0714Twitter: @rogermud