rocky mtn glut

TRANSCRIPT

Rocky Mountain GlutAssessing Condensate Production Volumes in the Rocky

Mountains and Existing Takeaway Infrastructure to Identify Opportunities for Supply Investment

Eric Peterson

Senior Business Analyst

Condensate Markets, Export & Takeaway Capacity 2014

Houston, TX

October 2014

Introduction to ARB Midstream

• Denver based infrastructure development company providing midstream solutions

• Strong financial support from private equity

• Utilize in-depth fundamental analysis to identify value propositions of our assets

• Emphasis on early stage development opportunities

• Developing a new crude-by-rail terminal• Niobrara Connector “NiCon”

• Centrally located in the DJ Basin

• Unit train capable

• Scheduled in-service date: Q3 2015

2

Observations

3

• High IRR plays incentivize drilling activity

• DJ Basin provides some of the best economics in North America

• Growing play with significant production growth in the future

• Average of 65% of DJ Basin production is +45 API, more than any other Rockies play and getting lighter

• Midstream infrastructure is not adequate for long term production volumes

• Niobrara Connector “NiCon” crude-by-rail facility will provide additional takeaway optionality getting crude and condensate to market

IRR’s of Various Plays – High IRR Drives Drilling Activity

4

Utica

Marcellus - Dry

Uinta

Dry Gas

Wet Gas

Oil

Permian

Bakken

DJ Basin

Eagle Ford

40-71%

Granite Wash

Miss Lime55%

24%

28%66%

24%

74%73%

45%-73%

61%

Marcellus - Wet

Source: Credit Suisse

44%Woodford

Horizontal drilling activity drives production

5

Horizontal

Vertical

Directional

Source: RigData, HPDI

-16 /

+768

-8 /

+377

+19 /

+114

+62 /

+409 Rig Change /

Production

Increase

Comparison of Rockies Basins

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

0 12 24 36 48 60 72

Incre

me

nta

l P

rod

uctio

n (

bp

d)

Months Developed

Bakken

PRB

DJ Basin

6

Mature Play

Growing Plays

Bakken Production Forecast

7

-

200

400

600

800

1,000

1,200

1,400

1,600

Pro

du

cti

on

(b

pd

) Th

ou

sa

nd

s

Condensate (>45°)

Light (>38° and <45°)

Intermediate (>22° and <38°)

Heavy (<22°)

Source: Genscape

-

200

400

600

800

1,000

1,200

1,400

1,600

Th

ou

sa

nd

s

2014 2019

PRB Production Forecast

8

-

10

20

30

40

50

60

70

80

90

100

Pro

du

cti

on

(b

pd

) Th

ou

sa

nd

s

Condensate (>45°)

Light (>38° and <45°)

Intermediate (>22° and <38°)

Heavy (<22°)

Source: Genscape

-

5

10

15

20

25

30

35

40

45

Th

ou

sa

nd

s

2014 2019

DJ Production Forecast

9

0

50

100

150

200

250

300

350

400

450

500

Pro

du

cti

on

(b

pd

) Th

ou

sa

nd

s

Condensate (>45°)

Light (>38° and <45°)

Intermediate (>22° and <38°)

Heavy (<22°)

Source: ARB Midstream

-

50

100

150

200

250

300

350

400

Th

ou

sa

nd

s

2014 2019

All Basin API

20 25 30 35 40 45 50 55 60 65 70 75 80 85 90

Eagle Ford

SCOOP

Utica

Bakken

Miss Lime

DJ Basin

PRB

Canadian Condensate

Natural Gasoline

API Gravity

10

Condensate Preferred Diluent

Bulk of the increased production volumes are +45 API

11

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Pro

du

ctio

n (

bp

d)

API Gravity

DJ Production by API(Jan 2014 vs May 2014)

Jan-14 May-14

Source: EIA

Production Increase: 61kbpd

>45 API: 62% to 70%

WAVG API: 45.4 to 47.1

Additional +45 API: 54kbpd

High API production centered in the core area of the Wattenberg Field

12Source: HPDI

Cru

de A

PI G

ravity

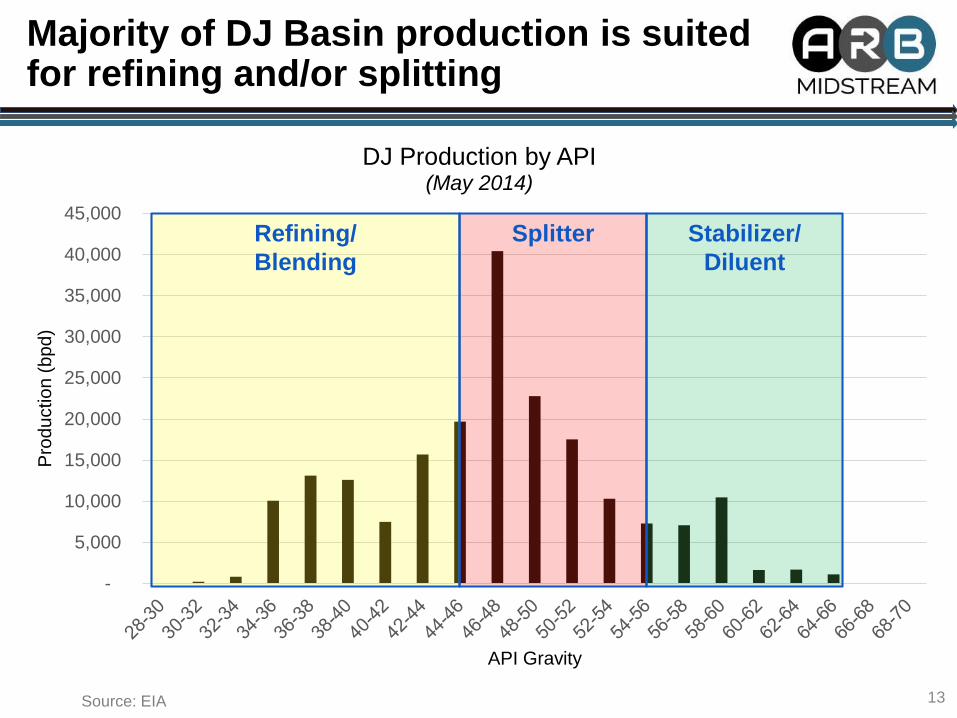

Majority of DJ Basin production is suited for refining and/or splitting

13

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Pro

du

ctio

n (

bp

d)

API Gravity

DJ Production by API(May 2014)

Splitter Stabilizer/

Diluent

Refining/

Blending

Source: EIA

End Markets

East Coast Waterborne Imports –Q4 2009 vs Q4 2013

-

50,000

100,000

150,000

200,000

250,000

300,000

Wate

rborn

e Im

port

s (

bp

d)

API Gravity

Q4 2009 Q4 2013

15Source: EIA

Imports are down from

1.2MM to 592kbpd (-52%)

West Coast Waterborne Imports –Q4 2009 vs Q4 2013

-

50,000

100,000

150,000

200,000

250,000

300,000

Wate

rborn

e Im

port

s (

bp

d)

API Gravity

Q4 2009 Q4 2013

16Source: EIA

Imports have increased

from 985k to 1.115MMbpd

(+13%)

Gulf Coast Waterborne Imports –Q4 2009 vs Q4 2013

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Wa

terb

orn

e Im

po

rts (

bp

d)

API Gravity

Q4 2009 Q4 2013

17Source: EIA

Imports have decreased

from 5.5MM to 3.5MMbpd

(-36%)

US Light Capacity Additions

18Source: Argus

Takeaway Infrastructure

Current pipeline infrastructure leaving the basin all leads to Cushing

20

PXP NECL

White Cliffs Expansion

21

0

20

40

60

80

100

120

140

160

Mb

/d

Flow Capacity

Source: Genscape

Pony Express Line Fill + Walk Up Shipments

22

0

50

100

150

200

250

Mb

/d

Flow Capacity

Source: Genscape

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Pro

du

ctio

n &

Cap

acit

y (b

pd

)Midstream infrastructure is not adequate for long term production volumes

23

NiCon

Pony Express

White Cliffs Twin

Existing Rail

WC Exp #2WC Exp #1

White Cliffs

Refining Demand

70,000 – 250,000 bpd of

additional takeaway capacity

needed(announced pipelines)

Niobrara Connector “NiCon” –Centrally located in the DJ Basin

24

PXP NECL

Niobrara Connector “NiCon” –Specifications

25

• 79,000 bpd nameplate capacity

• 120 car unit train capable

• 224 Acres

• Industrial spur serviced by the UP

• In Service date Q3 2015

• Segregation of product in up to 4 - 100,000 bbl tanks

Summary

• High IRR plays incentivize drilling activity

• DJ Basin provides some of the best economics in North America

• Growing play with significant production growth in the future

• Average of 65% of DJ Basin production is +45 API, more than any other Rockies play and getting lighter

• Midstream infrastructure is not adequate for long term production volumes

• Niobrara Connector “NiCon” crude-by-rail facility will provide additional takeaway optionality getting crude and condensate to market

26