rocky mountain region: cre quarter-in-review q3-2016

TRANSCRIPT

Denver, Phoenix and Salt Lake City economic and office overview

Q3 2016

Economy

Employment growth

-300.0

-250.0

-200.0

-150.0

-100.0

-50.0

0.0

50.0

100.0

150.0

200.0

12-m

onth

net c

hang

e (tho

usan

ds)

Phoenix Denver Salt Lake City

Most recent annual growth slightly slower than cyclical average, but trend remains one of stability

Source: JLL Research, Bureau of Labor Statistics

+101,800current cycle

average growth

+115,500previous cycleaverage growth

2

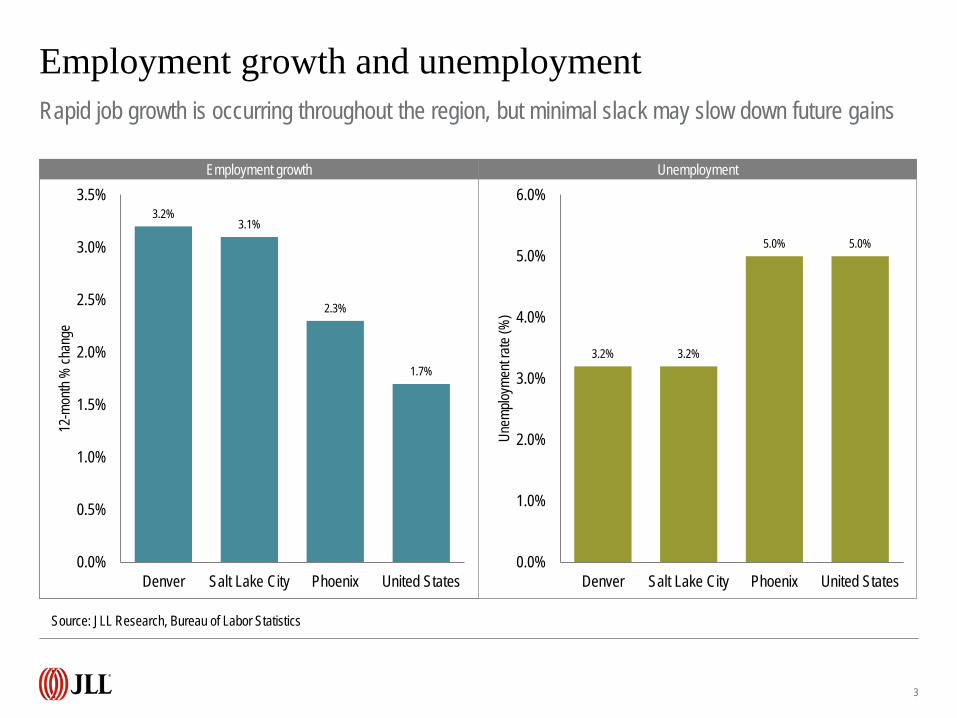

3.2%3.1%

2.3%

1.7%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Denver Salt Lake City Phoenix United States

12-m

onth

% ch

ange

Employment growth and unemploymentRapid job growth is occurring throughout the region, but minimal slack may slow down future gains

Source: JLL Research, Bureau of Labor Statistics

3.2% 3.2%

5.0% 5.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Denver Salt Lake City Phoenix United States

Unem

ploym

ent ra

te (%

)

Employment growth Unemployment

3

Employment growth

-5 0 5 10 15 20 25

Information

Manufacturing

Other services

Government

Trade, transportation and utilities

Financial activities

Leisure and hospitality

Professional and business services

Construction and mining

Education and health

12-month net change (thousands)

Phoenix Denver Salt Lake City

Job growth balanced across health, construction, professional services and leisure

Source: JLL Research, Bureau of Labor Statistics

4

Housing starts

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Autho

rized

units

Phoenix Denver Salt Lake City

Regional markets on track to surpass 2015 starts, but still well below previous peak

Source: JLL Research, U.S. Census Bureau

5

Office

Market Inventory (s.f.) YTD 2016 net absorption (s.f.)

Total vacancy (%)

Average asking rent

($ p.s.f.)

Under construction

(s.f.)

Denver 108,018,472 -20,603 13.8% $26.56 3,649,889

Phoenix 84,035,044 2,611,611 19.7% $24.22 1,692,140

Salt Lake City 49,442,083 1,247,276 7.3% $22.50 2,122,795

Region 241,495,599 3,838,284 14.5% $25.03 7,464,824

Regional office overviewEven as occupancy growth stalls in Denver, vacancy is falling regionally

Source: JLL Research

Comparison to U.S. office market

+70bpNet absorption (% of inventory)

7.1%Share of national construction

6.0%Share of national inventory

+0bpTotal vacancy

+50bpU/C as % of inventory

-$7.32 (-22.6%)Average asking rent

7

Net absorption

-4,000,000

-2,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2016

Net a

bsor

ption

(s.f.)

Denver Phoenix Salt Lake City

More than 1.0 m.s.f. of absorption in both Phoenix and SLC keeping annualized growth stable

Source: JLL Research

5.1 m.s.f.2016 annualized

absorption

8

1,384,779

625,814

413,118

246,778 239,670 224,516

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Tempe (Phoenix) Utah County (SaltLake City)

Draper (Salt LakeCity)

Chandler (Phoenix) Scottsdale Airpark(Phoenix)

Midtown Suburbs(Denver)

YTD

net a

bsor

ption

(s.f.)

Net absorptionLarge user-heavy suburban submarkets are driving regional occupancy growth

Source: JLL Research

9

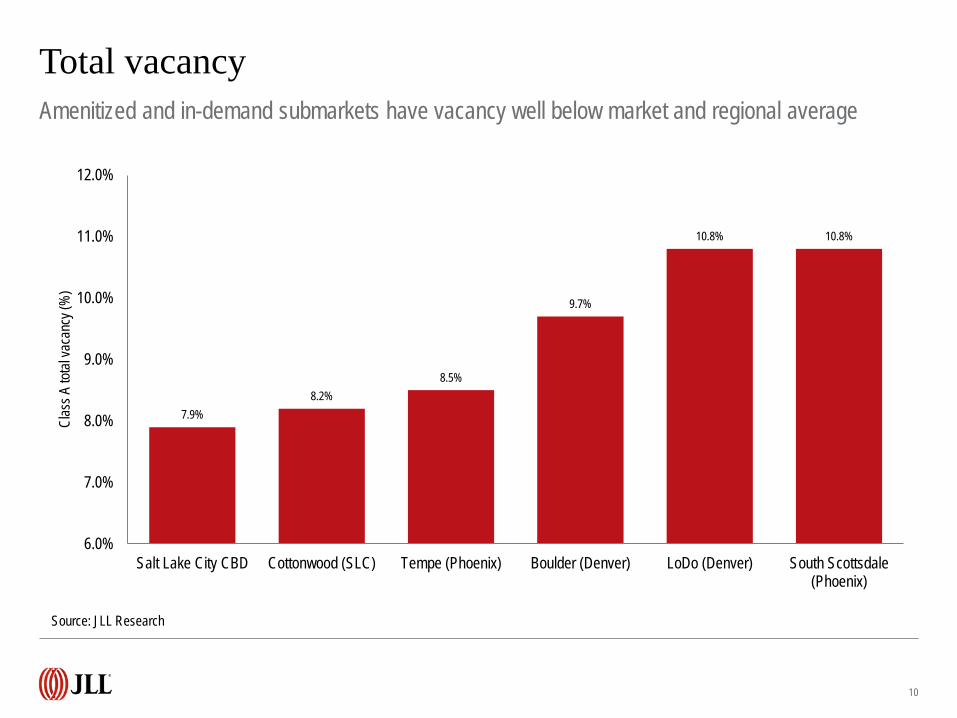

7.9%8.2%

8.5%

9.7%

10.8% 10.8%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

Salt Lake City CBD Cottonwood (SLC) Tempe (Phoenix) Boulder (Denver) LoDo (Denver) South Scottsdale(Phoenix)

Clas

s A to

tal va

canc

y (%

)Total vacancyAmenitized and in-demand submarkets have vacancy well below market and regional average

Source: JLL Research

10

Rent growth

44.8%

23.3%

20.8% 20.0%

13.8% 13.0%10.9%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Draper (SLC) Boulder (Denver) Tempe (Phoenix) Sandy SouthTowne (SLC)

Utah County (SLC) South Scottsdale(Phoenix)

Paradise Valley(Phoenix)

Clas

s A ye

ar-o

ver-y

ear r

ent g

rowt

h (%

)

Outside of Denver (except Boulder), double-digit rent growth unabated in many submarkets

Source: JLL Research

11

Rent growth

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014 2015 Q2 2016

Rent

grow

th sin

ce 20

10 (%

)

All regional markets are experiencing rent growth on the back of both new supply and tightening

Source: JLL Research

+26.5%Denver

+11.5%Phoenix

+20.3%Salt Lake City

12

Under construction

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q3 2016

Unde

r con

struc

tion (

s.f.)

Denver Phoenix Salt Lake City

As developments deliver, the construction pipeline will slow in response to market softening

Source: JLL Research

13

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016

TJ JaroszewskiDirector – Rocky Mountains Research+1 303 260 [email protected]

Phil RyanSenior Research Analyst – U.S. Office+1 202 719 [email protected]