rmb internalization, rational, establishing of clearing bank and requirement of becoming a hub

TRANSCRIPT

Strictly private & confidential 1

Private & Confidential

T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RMB Internalization

Strictly private & confidential

Index

2T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Index

• Executive Summary 03

• RMB Internationalization 04

• RMB Clearing Bank Development Process 17

• Requirements to be a RMB Hub 21

• Global RMB Hubs 24

• China-Africa Cooperation 35

• China-Russia Cooperation 44

• Appendix 51

Strictly private & confidential 3T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Executive Summary

The research is a joint collaboration between MCM Partners and the Chinese University of Hong Kong (CUHK)

In this presentation, we will first provide you the rationale behind the internationalization of RMB. It also describe the role and process of establishing of RMB clearing bank, as well as the list of requirements to becoming a a RMB hub.

Next, we will introduce the major RMB hubs in the world, which are Hong Kong, London and Frankfurt, by providing you with numerous facts, numbers and statistics.

Last but not least, in-depth analyses in the trade and cooperation between China and Africa, as well as China and Russia, will be included in this presentation.

At the end of the presentation, you would clearly understand the past, current and future development of the RMB hubs.

Strictly private & confidential 4T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RMB Internationalization

Strictly private & confidential

Lower cost RMB financing for foreign

entities

• RMB trade financing and CNH bonds financing have lower costs and can eliminate foreign exchange risk for foreign entities.

Greater investment choices for foreign entities

• FX forward, FX options, interest rate swap, cross currency swap and bespoke structured risk management products tend to have more liquidity.

More benefits from RMB appreciation

• There is a strong expectation of RMB appreciation which can be benefited through trading.

Broader access to onshore purchasers and suppliers for foreign counterparties

• Foreign corporates can freely pay and receive RMB for settlement of cross-border trade of goods and services with mainland corporates.

Lower trade transaction costs for foreign

counterparties

• Due to reduced FX risks bearing by mainland corporates, cost savings can be passed to their trade counterparties.

Less restrictions on RMB transferring

• Onshore-Offshore: RMB intercompany loans

• Offshore-Onshore: CNH shareholder loans, an injection of equity capital and remittance based on real trade to onshore

5T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Why Adopt RMB?

Strictly private & confidential 6

T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

• The exchange rate gap

with USD between

onshore and offshore

RMB is minimizing

since the start of CNH

market in Hong Kong

in 2010.

• The real EER is

exceeding nominal

EER since 2011

illustrates RMB strong

tendency to further

appreciate against

USD.

• The rocketing trading

volume of CNH

market indicates its

replacement of NDF

market in the

foreseeable future.

Market Content Regulators FX Scheme Investors Forward

Curve

CNYOnshore

RMB PBOC, SAFE

CFETS, daily

fixing with PBOC

intervention

Onshore residents,

approved offshore

investors

Onshore interest rate

CNH

Offshore

deliverable

RMB

HKMA,PBOC OTC, market

settlement

Offshore

investors

Offshore interest rate

NDFOffshore non-

deliverable

RMB

None

OTC, daily fixing

based on CNY

central parity rate

set by PBOC

Offshore

investors

Offshore interest rate,

expected and

influenced by CNH

market

Source: Bloomberg Source: Bank for International Settlements

One Currency, Two Curves, Three Markets

* Comparisons among CNY, CNH and NDF markets

Strictly private & confidential 7T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RMB Internationalization

2002-2008 2009 2010 2011

• QFII scheme

established.

• Dim sum bonds

issued in Hong

Kong.

• RMB cross border

trade settlement pilot

scheme between

Mainland Designated

Enterprises (MDEs)

in 5 cities and

corporates in Hong

Kong, Macau and

ASEAN.

• China's Ministry of

Finance issues the

first government dim

sum bond in the

offshore market.

• RMB cross border trade

settlement expanded to

20 provinces and

corporates all around the

world.

• Trade settlement

expended list of eligible

MDEs to over 67000.

• RMB bonds of all types

were open to all financial

intermediaries.

• China's Ministry of

Finance sells 8 billion

yuan of bonds of

different maturities in

Hong Kong.

• QFII allowed to

invest in the stock

index futures.

• RMB cross border

trade settlement

covered entire

China.

• RQFII scheme

established.

• RMB ODI was

allowed.

A Global Trade Settlement Currency

A Global Investment Currency

A Global Reserve Currency

Strictly private & confidential 8T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

A Global Trade Settlement Currency

A Global Investment Currency

A Global Reserve Currency

• A dim sum bond is

issued in London for

the first time.

• RMB cross border

trade settlement

expanded to all

Chinese corporates

with import/export

scope on their

business licenses.

• PBOC granted

RQFIIs access to

inter-bank bond

market.

• RMB business started in

Taiwan

• First issue of an offshore

yuan bond in Taiwan.

• First issue of an offshore

yuan bond in Singapore.

• PBOC granted QFIIs

access to inter-bank bond

market.

• RQFII launched in Taiwan,

Singapore and London.

• Simplified RMB cross

border trade settlement

process announced

• Shanghai Free Trade Zone

was set up.

• The first RMB bond

was issued in

Germany.

• The largest offshore

RMB bonds was

issued in Singapore.

• The first non-Chinese

sovereign yuan bond

issued in UK.

• Shanghai-Hong Kong

Stock Connect

Program was

officially launched.

2012 2013 2014

RMB Internationalization

Strictly private & confidential 9T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

A Global Trade Settlement Currency

Currently:

• RMB is the seventh mostly-used payment currency according to SWIFT.

• RMB is the ninth most actively traded currency according to BIS.

• RMB surpassed the EUR as the second most used currency in international trade finance

according to SWIFT.

• RMB trade settlement accounted for 3%, 9%, 12% of the total China trade respectively

in 2010, 2011 and 2012, presenting an increasing usage of RMB as a trade settlement

currency.

Source: CEIC Data

0

200

400

600

800

1000

1200

1400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

RMB Settlement for Cross-Border Trade (CNY billion)

2010 2011 2012 2013

Strictly private & confidential 10T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

What’s next?

• In 2013, China exceeded the United States, becoming world’s 1st largest trading

economy, the 1st largest export trading economy and the 2nd largest import trading

economy. It is predicted that the trade volume gap between China and the United

States will further widen, employing linear regression.

• China’s consistent and continual growth of exports and imports of merchandise

and services since 2005 demonstrates its sustainable development potential in the

foreseeable future.

Source: World Bank

1000

2000

3000

4000

5000

6000

7000

8000

9000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Exports and Imports of Merchandise and Services(annual basis, USD bn)

China

United States

Japan

United Kingdom

Germany

China-Regression

United States-Regression

Japan-Regression

United Kingdom-Regression

Germany-Regression

Strictly private & confidential 11

T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

What’s next?

• China’s merchandise export

with developing economies

exceed that with developed

economies in 2011.

• China’s excess merchandise

import with developing

economies over that with

developed countries increase

gradually on the whole.

• It is expected that RMB will

be increasingly used in cross-

border trade settlement

between China and

developing economies with

the increasing multilateral

trade volume.

Source: UNCTAD

Source: UNCTAD

0 200 400 600 800 1000 1200

200520062007200820092010201120122013

China Merchandise Export with Different Parties(annual basis, USD bn)

Developed Economies Developing Economies

0 200 400 600 800 1000 1200

2005

2006

2007

2008

2009

2010

2011

2012

2013

China Merchandise Import with Different Parties(annual basis, USD bn)

Developed Economies Developing Economies

Strictly private & confidential 12T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

A Global Investment Currency

CSRC SAFE PBOC

QFII

• Approves QFII

status

• Regulates onshore

securities

investments by

QFII

• Approves and allocates

QFII investment quota

• Regulates QFII’s

onshore accounts

• Regulates fund

repatriation/remittance

RQFII

• Approves RQFII

status

• Regulates onshore

securities

investments by

RQFII

• Approves and allocates

RQFII investment quota

• Regulates

onshore RMB

accounts

• Regulates fund repatriation/remittance

• The total QFII quota and RQFII

quota are increasing sharply,

especially for RQFII, 20 times as

much quota in 2013 as in 2011.

• The start of Stock Connect

between mainland and Hong Kong

in November strengthens the

expectation of further globalization

of mainland capital market.

• Despite the rocketing quota of

indirect investment for foreign

investment entities, its proportion

over China’s equity market

capitalization is still of

insignificance, indicating strong

potential development of China’s

equity market.

• The foreign direct investment are

lifting restrictions and it is

expected that further lifting is

imminent.

Source: SAFE

* Regulators of QFII and RQFII

Strictly private & confidential 13T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

What’s next?

Source: World Bank

Source: World Bank

• China’s net inflows of

foreign direct investment

exceed that of the United

States in 2009.

• China has always been the

most popular choice of

foreign direct investment

among developing

economies since 1990s.

• China’s net inflows of

portfolio equity has strongly

recovered since its sharp

decline in 2011 .

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010 2011 2012 2013

Foreign Direct Investment, net inflows(annual basis, USD bn)

China United States Japan United Kingdom Germany

-100.000

-50.000

0.000

50.000

100.000

150.000

200.000

250.000

300.000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Portfolio Equity, net inflows(annual basis, USD bn)

China United States Japan United Kingdom Germany

Strictly private & confidential 14T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

What’s next?

• Both China’s inward FDI and

outward FDI global market

shares are increasing,

accounting for over 8% and

7% in 2013, respectively.

• China’s inward FDI of stock

has a stable increase since

2005, showing strong

momentum. But its global

market share is relatively

small, only about 2%.

• It is expected that there’s huge

potential growth of inward and

outward FDI considering the

continual deregulation and

increasing quota of QFII,

RQFII and QDII programs.

Source: UNCTAD

Source: UNCTAD

Source: UNCTAD

Strictly private & confidential 15

What’s next?

Source: Bank for International Settlements

• In 2013, CNY consisted of 1% of the global FX market turnover. It is predicted that in

2027, CNY will account for 8% of the global FX market turnover. It is expected that

CNY global FX market turnover will exceed GBP before 2025.

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2001 2004 2007 2010 2013 2016 2019 2022 2025 2028

Global Foreign Exchange Market TurnoverNet-net basis, average daily turnover in April (USD bn)

CNY

USD

JPY

GBP

EUR

CNY-Regression

USD-Regression

JPY-Regression

GBP-Regression

EUR-Regression

Strictly private & confidential 16T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

A Global Reserve Currency

• In 2010, China’s GDP exceeded Japan, becoming world’s 2nd largest economy. It is

predicted that China’s GDP will exceed that of the United States around 2016 using

exponential regression.

• 1% increase in one country’s GDP global market share (based on real exchange rate)

reasonably leads to 0.55% increase of its currency reserve in central bank.

• It is reasonable to predict that RMB will become a global reserve currency in the next

five years.

Source: World Bank

0

10000

20000

30000

40000

50000

60000

70000

2005200620072008200920102011201220132014201520162017201820192020202120222023

Gross Domestic Product(annual basis, USD bn)

China

United States

Japan

United Kingdom

Germany

China-Regression

United States-Regression

Japan-Regression

United Kingdom-Regression

Germany-Regression

Strictly private & confidential 17T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RMB Clearing Bank Development Process

Strictly private & confidential 18T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Established RMB Clearing Banks

Strictly private & confidential 19T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Established RMB Clearing Banks

Strictly private & confidential 20T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

PBOC’s RMB Bilateral Swap Lines

AMERICAS

Country RMB Bn Country RMB Bn

Argentina 70 Brazil 190

Total RMB 260bn

AISA PARCIFIC

Country RMB Bn Country RMB Bn

Hong Kong 400 Indonesia 100

South Korea 360 Thailand 70

Singapore 300 New

Zealand

25

Australia 200 Japan 18

Malaysia 180 Mongolia 10

Total RMB 1663bn

EMEA

Country RMB Bn Country RMB Bn

ECB 350 Pakistan 10

UK 200 Turkey 10

Russia 150 Kazakhstan 7

UAE 35 Iceland 3.5

Belarus 20 Albania 2

Ukraine 15 Uzbekistan 0.7

Hungary 10

Total RMB 813.2bnSource:PBOC

Strictly private & confidential 21T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Requirements to be a RMB Hub

Strictly private & confidential 22T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Requirements to be a RMB Hub

HK London Frankfurt

RMB goods trade* 401 billion 70 billion 162 billion

Offshore RMB deposit 1053 billion 14.5 billion 2.5 billion

Clearing banks BoC, Hong Kong

branch

CCB, London

branch

BoC, Frankfurt

branch

Bilateral swap line 400 billion 200 billion 350 billion**

RQFII quota 270 billion 80 billion 80 billion

RMB denominated

bonds issued

116 billion 13.1 billion 1 billion

Infrastructure RTGS RTGS with

extended operating

hours (20.5h)

RTGS with

extended operating

hours (20.5h)* All data are denominated in RMB

**The 350 billion BSA is given to ECB

Settlement Currency Investment Currency Reserve Currency

Strictly private & confidential 23T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Requirements to be a RMB Hub

Political and economic stability

Sound legal system and comprehensive regulatory framework

Effective risk management

Considerable track record of innovation

Experience in capital markets trades

Strictly private & confidential 24T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RMB Hubs in the Globe

Strictly private & confidential 25T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Main Advantages of Three Global Hubs

• Hong Kong

Gateway toward Chinese market and policy initiatives

Large RMB business base and strong trade and investment relationship

Advantageous financial infrastructure

• London

World largest FX trading center

European time zone convenience: 15(6):30-23(4):30, 9:00-16:00 (hk)

• Frankfurt

Largest trade partner in Europe, with government Agreement to use more

RMB and Euros in settlement trade

European time zone convenience: 15:00-23:00

Strictly private & confidential 26T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RMB Deposits in Hong Kong and London

0

2

4

6

8

10

12

14

16

0

200

400

600

800

1000

RM

B D

epo

sit

in L

on

do

n

RM

B D

epo

sit

in H

on

g K

on

g

Year

RMB Deposit Amount

Hong Kong/ billion London/ billion

• Deposit in Hong Kong

surges after 2010

Chinese government

promoted a new series

of RMB policies in Jun

2010

• Deposit in London

fluctuates

Level remains as Hong

Kong in 2004

Source: HKMA, city of London

Strictly private & confidential 27T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RMB Deposits in Hong Kong and London

• Loan in Hong Kong

Increase at an annual

rate of 30% - 40%

• Loan-to-Deposit ratio

remains low

Recently above 15%

Source: HKMA

0%

5%

10%

15%

20%

0

200

400

600

800

1000

2012 2013 2014.9

Loan

to

Dep

osi

t

Dep

osi

t an

d L

oan

in B

illio

n R

MB

Year

RMB Deposit and Loan in Hong Kong

Deposit/ billion Loan/ billion Loan to Deposit

RMB Loan and Loan-to-Debt ratio in Hong Kong

Strictly private & confidential 28T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Trade Volume between Mainland China, Hong Kong, UK and Germany

Source: Ministry of Commerce of the People's Republic of China

-0.2

-0.1

0

0.1

0.2

0.3

0.4

050

100150200250300350400450

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gro

wth

Ra

te

Exp

ort

& I

mp

ort

in

Bil

lio

n U

SD

Year

Mainland-Hong Kong Trade Volume

Hong Kong Growth

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0

50

100

150

200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gro

wth

Ra

te

Exp

ort

& I

mp

ort

in

Bil

lio

n U

SD

Year

China-UK/ Germany Trade Volume

UK Germany UK Growth Germany Growth

Strictly private & confidential 29T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

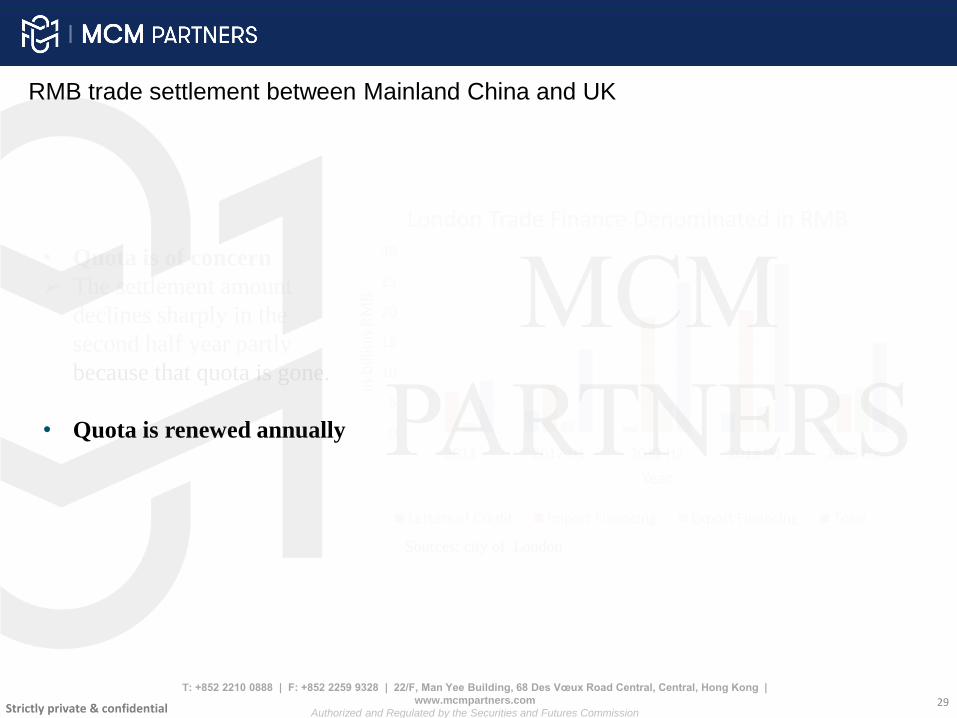

RMB trade settlement between Mainland China and UK

Sources: city of London

• Quota is of concern

The settlement amount

declines sharply in the

second half year partly

because that quota is gone.

• Quota is renewed annually 0

5

10

15

20

25

30

2011 2012 H1 2012 H2 2013 H1 2013 H2

in b

illio

n R

MB

Year

London Trade Finance Denominated in RMB

Letters of Credit Import Financing Export Financing Total

Strictly private & confidential 30T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

FDI Flows into China Mainland

Source: MOFCOM

0

0.5

1

1.5

2

2.5

0

20

40

60

80

100

2009 2010 2011 2012 2013

in B

illio

n U

SD (

UK

, Ger

man

y)

in B

illio

n U

SD (

Ho

ng

Ko

ng)

Year

China's FDI

Hong Kong UK Germany

• 66% of FDI cash

flows from Hong

Kong in 2013

34%

39%

1%

4%

3%

2%17%

China's FDI Structure of 2014H1Distribution Service

Other Service

Agriculture

Computer &

Communication

Transportation

Manufactoring

Chemical Engineering

Strictly private & confidential 31T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

OFDI Flows out of China Mainland

Source: MOFCOM

• 58% of OFDI cash

flows into Hong

Kong in 2013

0

2

4

6

8

10

0

100

200

300

400

500

2006 2007 2008 2009 2010 2011 2012 2013

in B

illio

n U

SD (

UK

, Ger

man

y)

in B

illio

n U

SD (

Ho

ng

Ko

ng)

Year

China's Outbound FDI

Hong Kong UK Germany

Strictly private & confidential 32T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Issuance of Offshore RMB Bonds

Source: Thomson Reuters

49%

20%

3%

4%

4%

20%

Offshore RMB bonds issued by countries

in 2010-2014

Mainland Hong Kong United States Germany South Korea Other

Total: $ 56.6 billion

• Dim Sum bond

Outstanding:

¥237.8 billion (2012)

¥309.2 billion (2013)

Growth: 30.0%

Issuance:

¥112.2 billion (2012)

¥116.0 billion (2013)

Growth: 3.4%

• Others

Includes UK, France,

Taiwan, Russia,

Singapore, etc.

Strictly private & confidential 33T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

RDFII Quota Possessed around the Globe

Sources: SAFE

RQFII Quota (Oct. 30th 2014) In Billion RMB

Hong Kong 270

Taiwan 100

UK 96

Singapore 88

France 60

0

1

2

3

4

5

6

0

50

100

150

200

250

300

2011 2012 2013 2014.1

Gro

wth

Rat

e

in b

illio

n R

MB

RQFII Quota in Hong Kong

Hong Kong Growth

Strictly private & confidential

RMB Trading and Settlement

34T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

0

1

2

3

4

5

0

1000

2000

3000

4000

5000

2010 2011 2012 2013

Gro

wth

Rat

e

in B

illio

n R

MB

HK Cross Border RMB Settlement

Cross Border RMB Settlement Growth

Source: HKMA, city of London

• Cross Border RMB

settlement increases

Faster than the growth

rate of trade

0

0.5

1

1.5

0

5

10

2011 2012 2013

In b

illio

n R

MB

Year

RMB Product Traded in London

Nondeliverable Product Spot FX

Forwards FX Swaps

FX Options

• Trading of non-

deliverable products are

decreasing, while the

opposite is increasing.

Strictly private & confidential 35T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Africa Cooperation

Strictly private & confidential 36T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Africa Trade and Cooperation

1950 1979 2000 2007 2009 2012 2013 2020

Beginning

Limited

Cooperation

Low trade volume:

US $12 million

Development

Forum on China-Africa

Cooperation (FOCAC),

50 African states

including South Africa,

Angola, Nigeria etc.

Trade volume: US

$10.6 billion

Fast Growth Special Loan for the

Development of African

SMEs (US $10 billion)

China became Africa's

largest trade partner

Trade volume: US

$91.07 billion

New High

Offer US $20 billion

loan in 3 years to

African states mainly

for infrastructure

projects

Trade volume: US

$209.6 billion

Adjustment

The reform and

opening-up policy

Trade volume: US

$0.82 billion

Speed-up

China-Africa

Development Fund.

Size reached US $5

billion

Trade volume: US

$73.57 billion

Expansion Period

60% of import from the 30

least developed Africa states

is duty free

Bilateral Investment Treaties

with 32 African states to

protect private investment

Trade volume: US $198.49

billion

New Stage

USD $400

billion

estimated

Source: National Bureau of Statistics of the People's Republic of China

2014

In-depth Cooperation

So far, South Africa,

Nigeria, Angola, Tanzania

and Kenya hold RMB as a

foreign exchange reserve

currency

Trade volume: US $104.77

billion for first half year

Strictly private & confidential 37T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Africa Trade and Cooperation

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

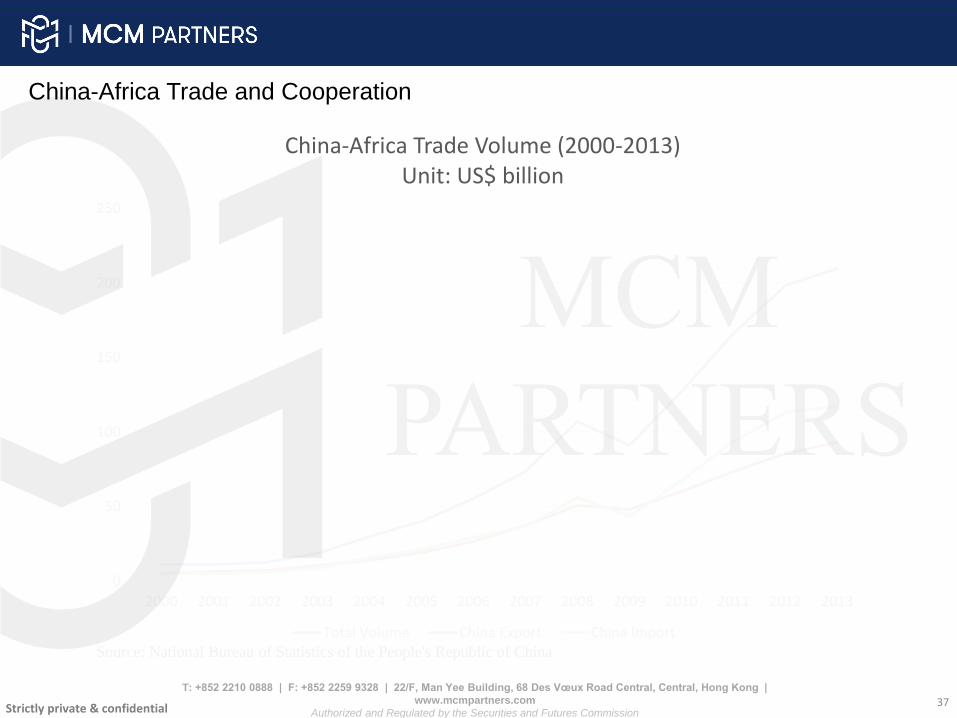

China-Africa Trade Volume (2000-2013)Unit: US$ billion

Total Volume China Export China ImportSource: National Bureau of Statistics of the People's Republic of China

Strictly private & confidential 38T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Africa Trade and Cooperation

Source: Ministry of Commerce of the People's Republic of China;

National Bureau of Statistics of the People's Republic of China

0 10 20 30 40 50 60 70

Algeria

Egypt

Nigeria

Angola

South Africa

Top 5 Trade Partners in 2013 (US $ Billion)

Trade Volume

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013

Trade Volume of Top 5 Partners (2009-2013, US $ Billion)

Algeria Egypt Nigeria Angola South Africa

Strictly private & confidential 39T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Africa Trade and Cooperation South Africa

Trade structure optimization: China’s largest trade partner in Africa. In the past, China mainly imports minerals and primary goods, exports final goods and have trade surplus. In recent years, South Africa exports more high value-added goods, such as motor vehicles, engine parts, electronic transformer and wines, imports machinery electrical equipment and textile. China have trade deficit.

Bilateral investment: Investment expands from home appliance, mining and smelting to finance, telecommunication, new energy and infrastructure.

Future cooperation: South Africa is promoting the development of manufacturing industry and encourage Chinese companies’ investment. South Africa will support the industries that create jobs and produce value-added products, including automobile, steel, agricultural products processing etc. South Africa plan to invest US $72 billion in infrastructure, which is a great opportunity for Chinese companies.

0

20

40

60

80

2009 2010 2011 2012 2013

Trade with South Africa (US$ Billion)

Total Volume China Export China Import

Source: National Bureau of Statistics of the People's Republic of China

0

1

2

3

4

5

6

2009 2010 2011 2012 2013

China’s Cumulative OFDI to South Africa (US$ Billion)

The Stock of FDI to South Africa

39

Strictly private & confidential

0

10

20

30

40

2009 2010 2011 2012 2013

Trade with Angola (US$ Billion)

Total Volume China Export China Import

Angola

Trade: China’s second largest trade partner and largest crude oil supplier in Africa. China

mainly imports crude oil and minerals from Angola, while exports electrical equipment,

steel and textile.

Bilateral investment: Angola’ investment to China is much less than China’s investment

to Angola. Before 2014, China’s cumulative investment to Angola was more than US $8

billion, mainly in oil, infrastructure, agriculture, telecommunication etc.

Future cooperation: First, Angola will make efforts to improve infrastructure and

strengthen related cooperation with China. Second, Angola has large amount of land to be

cultivated while China can provide funds and technologies to increase agriculture

production. Third, Angola has large demand for industrial products after war. China will

support domestic companies to invest in Angola’s manufacturing industry.

40T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Africa Trade and Cooperation

Source: National Bureau of Statistics of the People's Republic of China

Strictly private & confidential 41T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Africa Trade and Cooperation

Nigeria

Trade: The biggest economy in Africa.

China’s third largest trade partner in

Africa. China mainly imports crude oil,

natural gas and agricultural products,

while exports motorcycle, machinery,

clothing, home appliances etc. Nigeria is

China’s largest export market for

motorcycle.

Bilateral investment: Investment involves

agriculture, textile, mining, radio and

television, home appliance etc. Chinese

companies established factories in Lecky

and Ogun economic and trade cooperation

zone.

Nigeria is the first African state to hold

RMB as a foreign exchange reserve

currency.

Future cooperation: More investment in

textile, clothing, home appliance

industries to meet Nigeria’s demand. More

cooperation in rice breeding tropical crops

and infrastructure construction.

0

5

10

15

2009 2010 2011 2012 2013

Trade with Nigeria (US$ Billion)

Total Volume China Export China Import

Source: National Bureau of Statistics of the People's Republic of China

0

0.5

1

1.5

2

2.5

2009 2010 2011 2012 2013

China’s Cumulative OFDI to Nigeria(US$ Billion)

The Stock of FDI to Nigeria

Strictly private & confidential 42T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Chinese Companies in Africa

Industry Company Location Project Other Info

Infrastructure

Sinohydro

Corporation

AlgeriaMina Irrigation Expansion Project

SOUF Water Supply

AngolaIrrigation projects

Kuito Water Supply Works

BotswanaDikgatlhong Dam Irrigation scheme

Lotsane Dam

DR CongoBusanga Hydropower Station

Copper and Cobalt Mining Project

SudanMerowe Hydropower Project

El Renk-Malakal Road Project

China Road and

Bridge Corporation

(CRBC)

Kenya Mtito Andei - Bachuma Gate Road

Ethiopia Addis Ababa Beltway

Mauritania Nouakchott Friendship port

China Railway

Construction

Corporation Limited

(CRCC)

NigeriaRailway Modernization Project $8.3 billion

Railway Cooperation Framework $13 billion

Algeria East- West Expressway Project

Strictly private & confidential

Industry Company Location Project Other Info

Energy

China national

petroleum

Corporation (CNPC)

Tanzania Gas pipeline project $1.2 billion

Niger Agadem Oil and gas project

China Petroleum &

Chemical Corporation

(Sinopec)

AngolaAngola Block 18 deep-water oil

project50% shares

Nigeria Block OML138 oil field (20% shares) $2.46 billion

Telecommuni

cation

Zhongxing Telecom

Ltd (ZTE)

Ethiopia Telecom network construction project Term 1, 2, 3

South

AfricaOptical transmission network

Angola Bengla Metropolitan area network

Huawei TechnologiesEthiopia

Telecom network construction project Term 3

Addis Ababa Light rail telecom system

Nigeria Rural telecommunication network

Mining

China National

Nuclear

Corporation(CNNC)

Namibia Langer Heinrich uranium mine (25%) $190 million

China Non-Ferrous

Metals and

Construction (CNMC)Zambia

Chambishi Copper Mines

Luanshya Copper Mines

43

Chinese Companies in Africa

Strictly private & confidential 44T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Russia Cooperation

Strictly private & confidential 45T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Russia Trade and Cooperation

1993 1999 2000 2001 2009 2010 2012 2013

Early Stage

Low trade volume

US $7.68 billion

New Beginning

Economic Recovery

2001-2005 Trade

Agreement

Trade volume: US

$8 billion

Development

China and Russia’s

Investment

Cooperation Plan

Trade volume: US

$38.75 billion

Fast Growth

Russia-China

Investment Fund

US $2 billion

Trade volume: US

$88.16 billion

Collapse

Asian Crisis

Unstable conditions

and poor economy

Trade volume: US

$5.72 billion

Stable Growth

Sino-Russian Treaty

of Friendship

Trade volume: US

$10.67 billion

Speed-up

China became Russia's

largest trade partner

Agreement on natural

gas supply from Russia

to China

Trade volume: US

$55.53 billion

New stage

Russia became

China’s third largest

crude oil exporter

China-Russia Expo

Trade volume: USD

$89.26 billionSource: National Bureau of Statistics of the People's Republic of China

2014

In-depth Cooperation

The PBOC and Central

Bank of Russia signed a

3-year bilateral currency

swap agreement of

RMB 150 billion

Trade volume: US $100

billion estimated

Strictly private & confidential 46T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Russia Trade and Cooperation

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

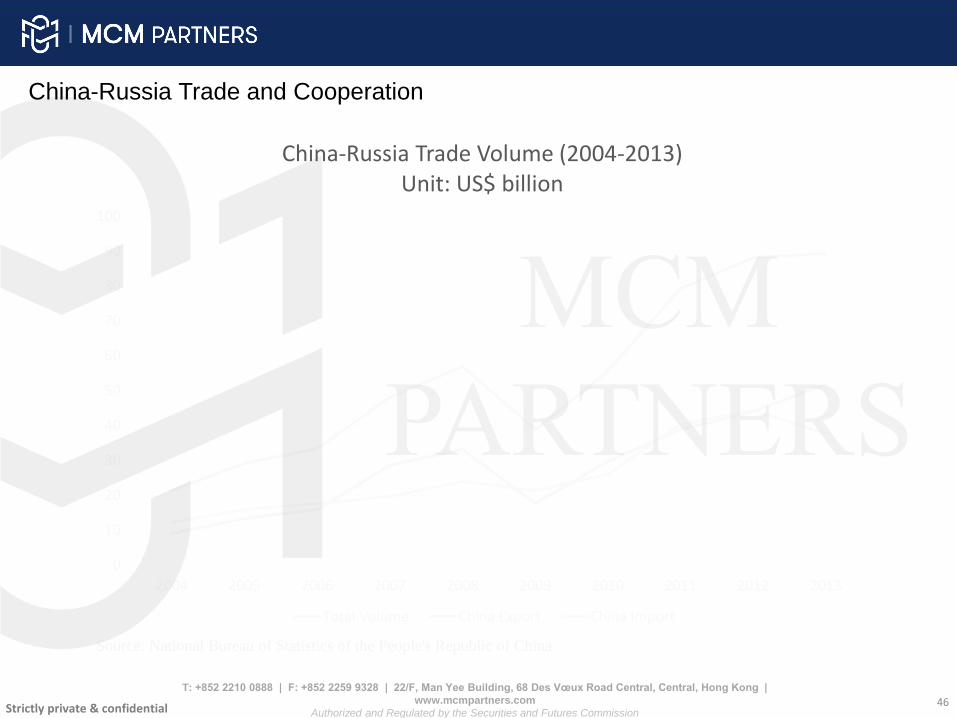

China-Russia Trade Volume (2004-2013)Unit: US$ billion

Total Volume China Export China Import

Source: National Bureau of Statistics of the People's Republic of China

Strictly private & confidential

Minerals51.7%

Wood andWooden Products

13.4%

Chemical product9.5%

Mechanical and electrical products

6.8%

Live animal, live animalproduct

6.1%

Cellulose pulp; Paper4.7%

Others7.7%

Structure of China’s Import from Russia 2013

Minerals Wood and Wooden ProductsChemical product Mechanical and electrical productsLive animal, live animal product Cellulose pulp; PaperOthers

47T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Russia Trade and Cooperation

Source: Ministry of Commerce of the People's Republic of China

Strictly private & confidential 48T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Russia Trade and Cooperation

Source: Ministry of Commerce of the People's Republic of China

Mechanical and electrical products

45.5%

Textiles and raw materials

10.0%

Base metals and metal products

7.9%

Furniture, toys, miscellaneous products

6.5%

Light industrial products5.6%

Transportation equipment

5.1%

Others19.4%

Structure of China’s Export to Russia 2013

Mechanical and electrical products Textiles and raw materials

Base metals and metal products Furniture, toys, miscellaneous products

Light industrial products Transportation equipment

Others

Strictly private & confidential 49T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

China-Russia Trade and Cooperation

Source: National Bureau of Statistics of the People's Republic of China

0

5

10

2008 2009 2010 2011 2012 2013

China’s Cumulative OFDI to Russia (2008-2013)

Unit: US$ Billion

China’s Cumulative OFDI to Russia

0

2

4

6

2008 2009 2010 2011 2012 2013

China's net ODFI to Russia(2008-2013)

Unit: US$ Billion

China's net ODFI to Russia

• Geographical distribution: big cities, e.g.

Moscow and St. Petersburg (tax advantages,

advanced market infrastructure and high ability

to pay); Siberia and the far east (rich natural

resources and near to China)

• Sectors: forestry, manufacturing industry,

mining industry and real estate

• Complementarity: China gets Natural resources

intensive products and Russia gets labor

intensive products

• Disadvantages: lack of labor force; Corruption

of judicial system and regulatory organizations;

unstable economic and political environment;

complicated market environment; different

culture and consumer habits

• Opportunities: sanctions against Russia

strengthen China-Russia relation; large

investment in infrastructure construction;

improvement of business environment

Strictly private & confidential 50

Chinese Companies in Russia

Industry Company Time Project Other Info

Energy

China national

petroleum

Corporation (CNPC)

2013.11 Yamal liquefied natural gas project 20% shares

Infrastructure

China Railway Group

Limited (CRG)2014.6

Cooperation agreement with

Roszheldorproject

China

Communications

Construction

Company Ltd.

(CCCC)

2014.8 Momorandum of Understanding

China Road and

Bridge Corporation

(CRBC)

2007.11 Infrastructure construction projectHaishenwai

& Sochi

Mining

Jilin HOROC

Nonferrous Metal

Group

2013.11 Mines in Kamchatka

China Metallurgical

Group Corporation

(MCC)

2010.12St. Petersburg cement clinker

production line

2012.3KIMKAN iron mine beneficiation

project

Strictly private & confidential 51T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Appendix

Strictly private & confidential 52T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Concept in RMB Internationalization• Qualified Foreign Institutional Investor - QFII

A program that permits certain licensed international investors to participate in China's mainland stockexchanges. The Qualified Foreign Institutional Investor program was launched by the People's Republicof China in 2002 to allow foreign investors access to its stock exchanges in Shanghai and Shenzhen.Prior to QFII, foreign investors were not able to buy or sell shares on China's stock exchanges because ofChina's tight capital controls. With the launch of the QFII program, licensed investors can buy and sellyuan-denominated "A" shares. Foreign access to these shares is limited by specified quotas thatdetermine the amount of money that the licensed foreign investors are permitted to invest in China'scapital markets.

• Dim Sum Bond

A bond denominated in Chinese yuan and issued in Hong Kong. Dim sum bonds are attractive to foreigninvestors who desire exposure to yuan-denominated assets, but are restricted by China's capital controlsfrom investing in domestic Chinese debt. The issuers of dim sum bonds are largely entities based inChina or Hong Kong, and occasionally foreign companies. The term is derived from the Chinese cuisinethat involves serving a variety of small delicacies and is especially popular in Hong Kong.

• Currency Swap

A swap that involves the exchange of principal and interest in one currency for the same in anothercurrency. It is considered to be a foreign exchange transaction and is not required by law to be shown ona company's balance sheet.

• Foreign Direct Investment – FDI

An investment made by a company or entity based in one country, into a company or entity based inanother country. Foreign direct investments differ substantially from indirect investments such asportfolio flows, wherein overseas institutions invest in equities listed on a nation's stock exchange.Entities making direct investments typically have a significant degree of influence and control over thecompany into which the investment is made. Open economies with skilled workforces and good growthprospects tend to attract larger amounts of foreign direct investment than closed, highly regulatedeconomies.

Strictly private & confidential 53T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

• Outward Direct Investment – ODI

A business strategy where a domestic firm expands its operations to a foreign country either via a Green field investment, merger/acquisition and/or expansion of an existing foreign facility. Employing outward direct investment is a natural progression for firms as better business opportunities will be available in foreign countries when domestic markets become too saturated.

• Real Effective Exchange Rate – REER

The weighted average of a country's currency relative to an index or basket of other major currencies adjusted for the effects of inflation. The weights are determined by comparing the relative trade balances, in terms of one country's currency, with each other country within the index. This exchange rate is used to determine an individual country's currency value relative to the other major currencies in the index, as adjusted for the effects of inflation. All currencies within the said index are the major currencies being traded today: U.S. dollar, Japanese yen, euro, etc.This is also the value that an individual consumer will pay for an imported good at the consumer level. This price will include any tariffs and transactions costs associated with importing the good.

Concept in RMB Internationalization

Strictly private & confidential 54T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Concept of RTGS

• Real time gross settlement systems (RTGS) are specialist funds transfer systems where transfer of money or

securities takes place from one bank to another on a "real time" and on "gross" basis.

• Settlement in "real time" means payment transaction is not subjected to any waiting period. "Gross settlement"

means the transaction is settled on one to one basis without bundling or netting with any other transaction.

• This "electronic" payment system is normally maintained or controlled by the central bank of a country.

• The World Bank has been paying increasing attention to payment system development as a key component of

the financial infrastructure of a country, and has provided various forms of assistance to over 100 countries.

Strictly private & confidential 55T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Existing RTGS Systems

Country RTGS Country RTGS

Albania AECH Croatia HSVP (Hrvatski sustav velikih

plaćanja)

Angola SPTR (Sistema de pagamentos em

tempo real)

Czech Republic CERTIS (Czech Express Real

Time Interbank Gross Settlement

System)

Azerbaijan AZIPS (Azerbaijan Interbank

Payment System)

Egypt RTGS

Australia RITS (Reserve Bank Information

and Transfer System)

European union TARGET2

Bosnia and Herzegovina RTGS Hong Kong CHATS(Clearing House

Automated Transfer System)

Bulgaria RINGS (Real-time INterbank

Gross-settlement System)

Hungary VIBER (Valós Idejű Bruttó

Elszámolási Rendszer)

Brazil STR (Sistema de Transferência de

Reservas)

India RTGS, NEFT, IMPS

Canada LVTS (Large Value Transfer

System)

Indonesia BI-RTGS (Sistem Bank Indonesia

Real Time Gross Settlement)

China CNAPS (China National Advanced

Payment System)

Iran SATNA ( آنیناخالصتسویهسامانه )

Chile LBTR/CAS (Liquidación Bruta en

Tiempo Real)

Japan BOJ-NET (Bank of Japan

Financial Network System)

Strictly private & confidential 56T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Existing RTGS Systems

Country RTGS Country RTGS

Kenya KEPSS (Kenya Electronic Payment

and Settlement System)

Pakistan PRISM (Pakistan Real Time

Inter-Bank Settlement

Mechanism)

Korea BOK-WIRE+ (The Bank of Korea

Financial Wire Network,한은금융망)

Peru LBTR (Liquidación Bruta en

Tiempo Real)

Kuwait KASSIP (Kuwait's Automated

Settlement System for Inter-

Participant Payments)

Philippines PhilPaSS

Macedonia MIPS (Macedonian Interbank

Payment System)

Poland SORBNET and ELIXIR

Malawi MITASS (Malawi Interbank

Settlement System)

Russia BESP (Banking Electronic Speed

Payment System)

Malaysia RENTAS (Real Time Electronic

Transfer of Funds and Securities)

Romania ReGIS system

Mexico SPEI (Sistema de Pagos

Electrónicos Interbancarios)

Saudi Arabia SARIE (Saudi Arabian Riyal

Interbank Express)

Namibia NISS (Namibia Inter-bank

Settlement System)

Singapore MEPS+ (MAS Electronic

Payment System Plus)

New Zealand ESAS (Exchange Settlement

Account System)

South Africa SAMOS (The South African

Multiple Option Settlement)

Nigeria CIFTS (CBN Inter-Bank Funds

Transfer System)

Sri Lanka LankaSettle (RTGS/SSSS)

Strictly private & confidential 57T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Existing RTGS Systems

Country RTGS Country RTGS

Sweden RIX (Riksbankens system för

överföring av kontoförda pengar)

Turkey EFT (Electronic Fund Transfer)

Switzerland SIC (Swiss Interbank Clearing) Ukraine SEP (System of Electronic

Payments of the National Bank of

Ukraine)

Taiwan CIFS (CBC Interbank Funds

Transfer System)

United Kingdom CHAPS (Clearing House

Automated Payment System)

Tanzania TIS (Tanzania interbank settlement

system)

United States Fedwire

Thailand BAHTNET (Bank of Thailand

Automated High value Transfer

Network)

Zambia ZIPSS-Zambian Inter-bank

Payment and Settlement System

Strictly private & confidential 58T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Milestones in Hong Kong

2003-20062003: BOC(HK) is established as an RMB clearing Bank.

2004: Hong Kong banks are allowed to offer personal RMB services to local Residents.

2007-2009

2007: The first offshore RMB bond is issued at Hong Kong.

2008: HKMA signs ¥200bn currency swap with PBOC.

2009: The first offshore RMB sovereign bond is issued at Hong Kong.

2010-2011

2011: The first RMB IPO is listed on the Hong Kong Stock Exchange.

2011: The RQFII pilot scheme is launched in Hong.

2012-2013

2012: The first RQFII A-ETF is listed on the Hong Kong.

2013: HKMA launches an interbank reference rate for offshore Yuan.

2014

2014: Shanghai-Hong Kong Stock Connect is prepared.

Strictly private & confidential 59T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Milestones in London

2011

UK-China economic and financial dialogue planed to build a renminbibusiness center.

2012

London off-shore Renminbi business center construction project set off.

HSBC issued the first renminbi off-shore bond outside Asia.

2013

London was given a quota of ¥80 billion in RQFII.

Pounds directly traded with renminbi.

2014Bank of England was denominated as a clearing bank in London by PBOC.

The Renminbidenominated sovereign bond was first issued in London.

Strictly private & confidential 60T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Milestones in Frankfurt

2011

The first Renminbidenominated bonds by German companies were issued.

2012

Germany and China agreed to use more RMB and Euros to settle their trade.

2013

The resolution to build Frankfurt as a Renminbi business center was published.

2014Deutsche Bundesbank will establish Renminbisettling and clearing service in Frankfurt as the first hub for trades clearing outside Asia.

Strictly private & confidential 61T: +852 2210 0888 | F: +852 2259 9328 | 22/F, Man Yee Building, 68 Des Vœux Road Central, Central, Hong Kong |

www.mcmpartners.com

Authorized and Regulated by the Securities and Futures Commission

Disclaimer

DisclaimerThis presentation is designed for MCM Partners customers exclusively for internal use of the client, and directly presented and delivered to the client (including the client's subsidiaries, the following referred to as the "Company"). This statement is intended to assist companies on the feasibility of a certain or several preliminary assessment of the potential transaction, the company has no right to publish or disclose to any other party all or part of this statement. This statement is for discussion purposes only, and can only be read in conjunction combined MCM Partners report. Unless a written consent is obtained from MCM Partners, this report or any content of it shall not be used for any other purpose.

Management information represented in this report is solely based on the company's forecast, our view, the above forecasts, the situation and perspectives may change at any time. This report is based on the information obtained from publicly available sources or provided to us by the company or a company representative, or a reviewed information by us. We assume that these data are accurate and complete without an independent review. In addition, we do not provide analysis on the company’s business, assets, stocks or its affiliates. MCM Partners does not evaluate nor represent the actual transaction value that may result or any legal, tax and accounting impact generated by it. Information contained in this report does not take into account the impact results from any potential changes in control over one or a number of potential transactions, of which the transaction(s) may have a significant impact on the valuation or other areas.

MCM Partners policy prohibits its employees to obtain business for consideration or inducement or reward, directly or indirectly, to provide favourable research rating or price target of a particular company, or to provide change in rating or price target. MCM Partners also prohibits its analysts to receive compensation from investment banks involved in the transaction, unless such participation is to achieve maximum benefits for the investors. This report does not constitute MCM Partners to underwrite, subscribe or placing any securities, provide or arrange credit or to provide any commitment to any other services.