riverside county state of california $6,785,000 …cdiacdocs.sto.ca.gov/2012-1048.pdf ·...

TRANSCRIPT

NEW ISSUE - BOOK-ENTRY-ONLY NO RATING

(See “CONCLUDING INFORMATION - No Rating on the Bonds” herein)

In the opinion of Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel, subject, however, to certain qualifications described herein, under existing laws, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, as amended (“Code”). In the further opinion of Bond Counsel, interest on the Bonds is not an item of tax preference for purposes of the federal alternative minimum taxes imposed on individuals and corporations, although Bond Counsel observes that such interest is included as an adjustment in the calculation of federal corporate alternative minimum taxable income and may therefore affect a corporation’s alternative minimum tax liabilities. In the further opinion of Bond Counsel, interest on the Bonds is exempt from State of California personal income taxation. Bond Counsel expresses no other opinion regarding or concerning any other tax consequences related to the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See “LEGAL MATTERS - Tax Matters.”

RIVERSIDE COUNTY STATE OF CALIFORNIA

$6,785,000 COMMUNITY FACILITIES DISTRICT NO. 2002-1

OF THE TEMECULA VALLEY UNIFIED SCHOOL DISTRICT (IMPROVEMENT AREA NO. 1)

SERIES 2012 SPECIAL TAX REFUNDING BONDS Dated: Date of Delivery Due: September 1 as shown on the inside front cover page.

The above-captioned “Series 2012 Special Tax Refunding Bonds” (the “Bonds”) are being issued under the Mello-Roos Community Facilities Act of 1982 (the “Act”), the Resolution of Issuance (as defined herein) and a Fiscal Agent Agreement, dated as of August 1, 2012 (the “Fiscal Agent Agreement”), by and between Community Facilities District No. 2002-1 of the Temecula Valley Unified School District (the “District”) and U.S. Bank National Association, as fiscal agent (the “Fiscal Agent”), and are payable from certain proceeds of special taxes levied on property within Improvement Area No. 1 of the District according to the rate and method of apportionment of special tax of the District approved by the qualified electors within Improvement Area No. 1 of the District (“Improvement Area No. 1”) and by the Board of Education of the Temecula Valley Unified School District (the “School District”) acting as the legislative body of the District and certain other funds as described herein.

The Bonds are being issued to (i) provide funds for the refinancing of outstanding indebtedness of the District, (ii) fund a reserve fund for the Bonds, and (iii) pay the costs of issuing the Bonds. See “THE FINANCING PLAN - Estimated Uses of Funds” herein.

Interest on the Bonds is payable on March 1 and September 1 of each year, commencing March 1, 2013. The Bonds will be issued in denominations of $5,000 or integral multiples thereof. The Bonds, when delivered, will be initially registered in the name of Cede & Co., as nominee of The Depository Trust Company (“DTC”), New York, New York. DTC will act as securities depository for the Bonds as described herein under “APPENDIX G - DTC AND THE BOOK-ENTRY-ONLY SYSTEM.”

The Bonds are subject to optional redemption, mandatory sinking fund redemption and special mandatory redemption from prepaid special taxes as described herein. See “THE BONDS - Redemption” herein

A DETAILED MATURITY SCHEDULE IS SET FORTH ON THE INSIDE FRONT COVER PAGE HEREOF

THE PRINCIPAL AND REDEMPTION PREMIUM, IF ANY, OF THE BONDS AND THE INTEREST THEREON ARE NOT AN INDEBTEDNESS OF THE STATE OF CALIFORNIA (THE “STATE”) OR ANY OF ITS POLITICAL SUBDIVISIONS, AND NEITHER THE DISTRICT (EXCEPT TO THE LIMITED EXTENT DESCRIBED HEREIN), THE SCHOOL DISTRICT, THE STATE, NOR ANY OF ITS POLITICAL SUBDIVISIONS IS LIABLE ON THE BONDS. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT (EXCEPT TO THE LIMITED EXTENT DESCRIBED HEREIN), THE SCHOOL DISTRICT, OR THE STATE, OR ANY OTHER POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE BONDS. OTHER THAN THE NET TAXES OF IMPROVEMENT AREA NO. 1 OF THE DISTRICT, AS DEFINED HEREIN, NO TAXES ARE PLEDGED TO THE PAYMENT OF THE BONDS. THE BONDS ARE NOT A GENERAL OBLIGATION OF THE DISTRICT, BUT ARE LIMITED OBLIGATIONS OF THE DISTRICT, PAYABLE SOLELY FROM THE NET TAXES OF IMPROVEMENT AREA NO. 1 OF THE DISTRICT AND AMOUNTS PLEDGED UNDER THE FISCAL AGENT AGREEMENT AS MORE FULLY DESCRIBED HEREIN.

This cover page contains certain information for quick reference only. It is not a summary of the issue. Potential investors must read the entire Official Statement to obtain information essential to the making of an informed investment decision with respect to the Bonds. Investment in the Bonds involves risks which may not be appropriate for some investors. See “RISK FACTORS” herein for a discussion of special risk factors that should be considered in evaluating the investment quality of the Bonds.

The Bonds are offered when, as and if issued and delivered to the Underwriter, subject to the approval as to their legality by Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel to the District. Certain legal matters will be passed upon for the District by Bowie, Arneson, Wiles & Giannone, Counsel to the District and by McFarlin & Anderson LLP, Laguna Hills, California, Disclosure Counsel, and for the Underwriter by its Counsel, Nossaman LLP, Irvine, California. It is anticipated that the Bonds will be available for delivery in book-entry form through the facilities of DTC on or about August 14, 2012.

The date of the Official Statement is July 26, 2012.

$6,785,000 COMMUNITY FACILITIES DISTRICT NO. 2002-1

OF THE TEMECULA VALLEY UNIFIED SCHOOL DISTRICT (IMPROVEMENT AREA NO. 1)

SERIES 2012 SPECIAL TAX REFUNDING BONDS

MATURITY SCHEDULE

$5,435,000 Serial Bonds

(Base CUSIP®† 87970H)

Maturity Date Principal Interest Reoffering

September 1 Amount Rate Yield CUSIP®†

2013 $220,000 1.000% 1.125% JZ9

2014 240,000 2.000 1.750 KA2

2015 245,000 2.000 2.000 KB0

2016 245,000 3.000 2.375 KC8

2017 255,000 3.000 2.750 KD6

2018 260,000 3.000 3.100 KE4

2019 270,000 3.125 3.375 KF1

2020 275,000 3.375 3.600 KG9

2021 285,000 3.500 3.750 KH7

2022 295,000 3.750 3.900 KJ3

2023 310,000 4.000 4.000 KK0

2024 320,000 4.000 4.120 KL8

2025 335,000 4.000 4.220 KM6

2026 345,000 4.125 4.320 KN4

2027 360,000 4.250 4.420 KP9

2028 375,000 4.250 4.500 KQ7

2029 390,000 4.375 4.550 KR5

2030 410,000 5.000 4.600* KS3

$1,350,000 5.00% Term Bond maturing September 1, 2033, Yield 4.75%* CUSIP®† KT1

* Priced to the September 1, 2022 optional call date

† CUSIP® A registered trademark of the American Bankers Association. CUSIP® data herein is provided by Standard & Poor’s CUSIP® Service Bureau. This data in not intended to create a database and does not serve in any way as a substitute for the CUSIP® Service Bureau. CUSIP® numbers are provided for convenience of reference only. Neither the District, the Financial Advisor nor the Underwriter takes any responsibility for the accuracy of such numbers.

GENERAL INFORMATION ABOUT THIS OFFICIAL STATEMENT

Use of Official Statement. This Official Statement is submitted in connection with the offer and sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not to be construed as a contract with the purchasers of the Bonds.

Estimates and Forecasts. This Official Statement contains statements which, to the extent they are not recitations of historical fact, constitute “forward-looking statements,” within the meaning of the United States Private Securities Litigation Reform Act of 1995, Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended. In this respect, such forward-looking statements are generally identified by the use of words “estimate,” “project,” “plan,” “budget,” “anticipate,” “expect,” “intend,” or “believe” or the negative thereof or other variations thereon or comparable terminology.

The achievement of certain results or other expectations contained in such forward-looking statements involves known or unknown risks, uncertainties and other factors which may cause actual results, performance or achievements to be significantly different than those expressed or implied by such forward-looking statements. These risks and uncertainties include, but are not limited to, uncertainties relating to economic conditions, the effect of changes in the amounts and timing of receipt of revenues, the availability and sufficiency of Net Taxes, change in circumstances adversely affecting the projected use of proceeds, and risks involving pertinent court decisions. The District does not plan to issue any updates or revisions to those forward-looking statements if or when its expectations, or events, conditions or circumstances on which such statements are based change. Potential investors are cautioned that such statements are only predictions and that actual events or results may differ materially. In evaluating such statements, potential investors should specifically consider the various factors which could cause actual events or results to differ materially from those indicated by such forward-looking statements.

Limit of Offering. No dealer, broker, salesperson or other person has been authorized by the District, the School District, the Financial Advisor or the Underwriter to give any information or to make any representations in connection with the offer or sale of the Bonds other than those contained herein and if given or made, such other information or representation must not be relied upon as having been authorized by the District, the School District, the Financial Advisor or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

Involvement of Underwriter. The Underwriter has provided the following statement for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with, and as a part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information.

The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the District or the School District or any other entity described or referenced herein since the date hereof. All summaries of the documents referred to in this Official Statement are made subject to the provisions of such documents, respectively, and do not purport to be complete statements of any or all of such provisions.

Stabilization of Prices. In connection with this offering, the Underwriter may overallot or effect transactions which stabilize or maintain the market price of the Bonds at a level above that which might otherwise prevail in the open market. Such stabilizing, if commenced, may be discontinued at any time. The Underwriter may offer and sell the Bonds to certain dealers and others at prices lower than the public offering prices set forth on the inside front cover page hereof and said public offering prices may be changed from time to time by the Underwriter.

THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXCEPTION FROM THE REGISTRATION REQUIREMENTS CONTAINED IN SUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE.

TEMECULA VALLEY UNIFIED SCHOOL DISTRICT

BOARD OF EDUCATION

Bob Brown, President Dr. Kristi Rutz-Robbins, Clerk Dr. Allen Pulsipher, Member

Vincent O’Neal, Member Richard Shafer, Member

______________________________________________

ADMINISTRATION

Timothy Ritter, District Superintendent Lori Ordway-Peck, Assistant Superintendent of Business Support Services

Jodi McClay, Assistant Superintendent of Educational Support Services Bill Behrens, Ed. D., Assistant Superintendent of Human Resources Development

________________________________________

PROFESSIONAL SERVICES

Bond Counsel Bowie, Arneson, Wiles & Giannone

Newport Beach, California

Disclosure Counsel McFarlin & Anderson LLP

Laguna Hills, California

Financial Advisor Harrell & Company Advisors, LLC

Orange, California

Special Tax Consultant Special District Financing & Administration

Escondido, California

Fiscal Agent U.S. Bank National Association

Los Angeles, California

Underwriter’s Counsel Nossaman LLP

Irvine, California

Verifications Grant Thornton LLP

Minneapolis, Minnesota

TABLE OF CONTENTS

INTRODUCTION ...................................................... 1 The District ................................................................ 1 The School District .................................................... 2 Purpose ...................................................................... 2 Security and Sources of Payment .............................. 2 Property Values .......................................................... 3 Tax Matters ................................................................ 3 Special Risks .............................................................. 3 Professionals Involved in the Offering ...................... 4 Offering of the Bonds ................................................ 4 Information Concerning this Official Statement ........ 4

THE BONDS ............................................................... 5 Authority for Issuance ............................................... 5 General Provisions ..................................................... 5 No Additional Bonds ................................................. 6 Redemption ................................................................ 6 Debt Service Schedule ............................................... 9

THE FINANCING PLAN ........................................ 10 The Refunding Program........................................... 10 Estimated Uses of Funds.......................................... 10

SECURITY FOR THE BONDS .............................. 11 General ..................................................................... 11 Special Taxes ........................................................... 12 Proceeds of Foreclosure Sales ................................. 12 Special Tax Fund ..................................................... 13 Bond Fund ............................................................... 14 Reserve Fund ........................................................... 14 Special Taxes and the Teeter Plan ............................ 15

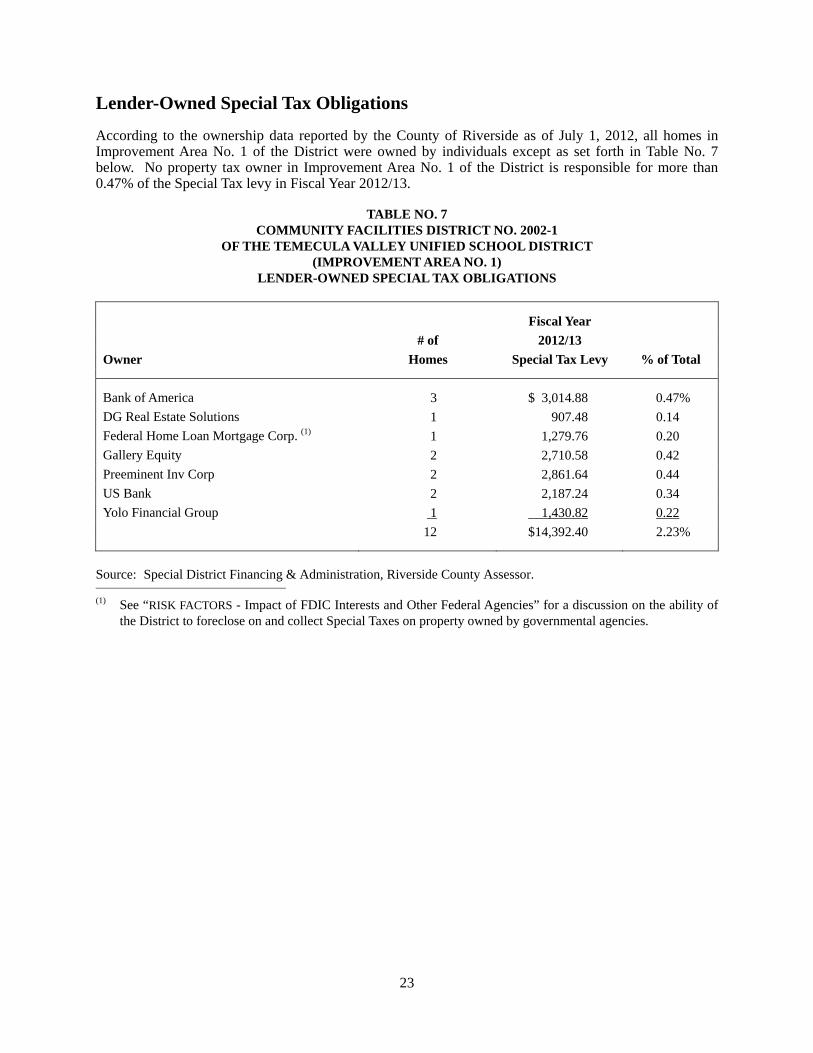

THE DISTRICT – IMPROVEMENT AREA NO. 1 ....................................................................... 15 General ..................................................................... 15 Assessed Values ....................................................... 16 Estimated Assessed Value-to-Lien Ratios ................ 18 Special Tax Rates ..................................................... 21 Lender-Owned Special Tax Obligations .................. 23 Effective Tax Rates .................................................. 24 Delinquencies .......................................................... 25 Projected Special Tax Levy ..................................... 26 Direct and Overlapping Debt ................................... 27

RISK FACTORS ....................................................... 28 General ..................................................................... 28 Risks of Real Estate Secured Investments

Generally ............................................................... 28 Risks Related to Current Real Estate Market

Conditions ............................................................. 28 Property Values ........................................................ 28 Other Possible Claims Upon the Value of Taxable

Property ................................................................. 30 Economic Uncertainty ............................................. 31 Disclosure to Future Purchasers............................... 31 Adjustable Rate and Non-Conventional

Mortgages ............................................................. 31 Hazardous Substances ............................................. 31

Levy and Collection of the Special Tax ................... 32 Exempt Property ...................................................... 33 Depletion of Reserve Fund ...................................... 33 Direct and Overlapping Indebtedness ...................... 34 Bankruptcy and Foreclosure Delays ........................ 34 Payment of Special Tax Not a Personal Obligation

of the Property Owners ......................................... 36 Factors Affecting Parcel Values and Aggregate

Value ..................................................................... 36 No Acceleration Provisions ..................................... 36 Limited Obligation of the District to Pay Debt

Service .................................................................. 36 District Formation ................................................... 37 Proposition 218 ........................................................ 37 Impact of FDIC Interests and Other Federal

Agencies ............................................................... 38 IRS Audits of Bond Issues ....................................... 40 Ballot Initiatives and Legislative Measures ............. 40 Limited Secondary Market ...................................... 40 Limitations on Remedies ......................................... 40

LEGAL MATTERS .................................................. 41 Legal Opinion .......................................................... 41 Tax Matters .............................................................. 41 Absence of Litigation .............................................. 43

CONCLUDING INFORMATION .......................... 43 No General Obligation of School District or

District .................................................................. 43 No Rating on the Bonds .......................................... 43 Underwriting ........................................................... 43 Verifications of Mathematical Computations .......... 43 The Financial Advisor ............................................. 44 Continuing Disclosure ............................................. 44 Execution ................................................................. 44

APPENDIX A - RATE AND METHOD OF APPORTIONMENT OF THE SPECIAL TAX

APPENDIX B - SUMMARY OF CERTAIN PROVISIONS OF THE FISCAL AGENT AGREEMENT

APPENDIX C - GENERAL INFORMATION ABOUT THE TEMECULA VALLEY UNIFIED SCHOOL DISTRICT AND THE CITY OF TEMECULA

APPENDIX D - FORM OF CONTINUING DISCLOSURE CERTIFICATE

APPENDIX E - PROPOSED FORM OF OPINION OF BOND COUNSEL

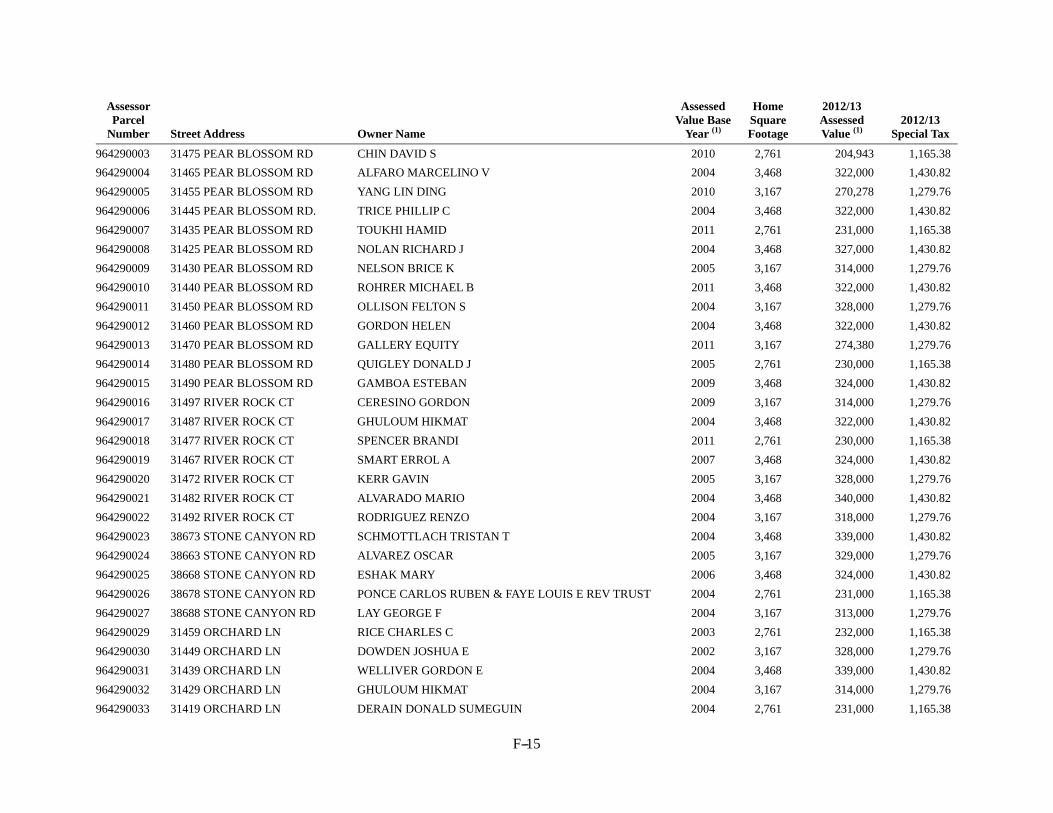

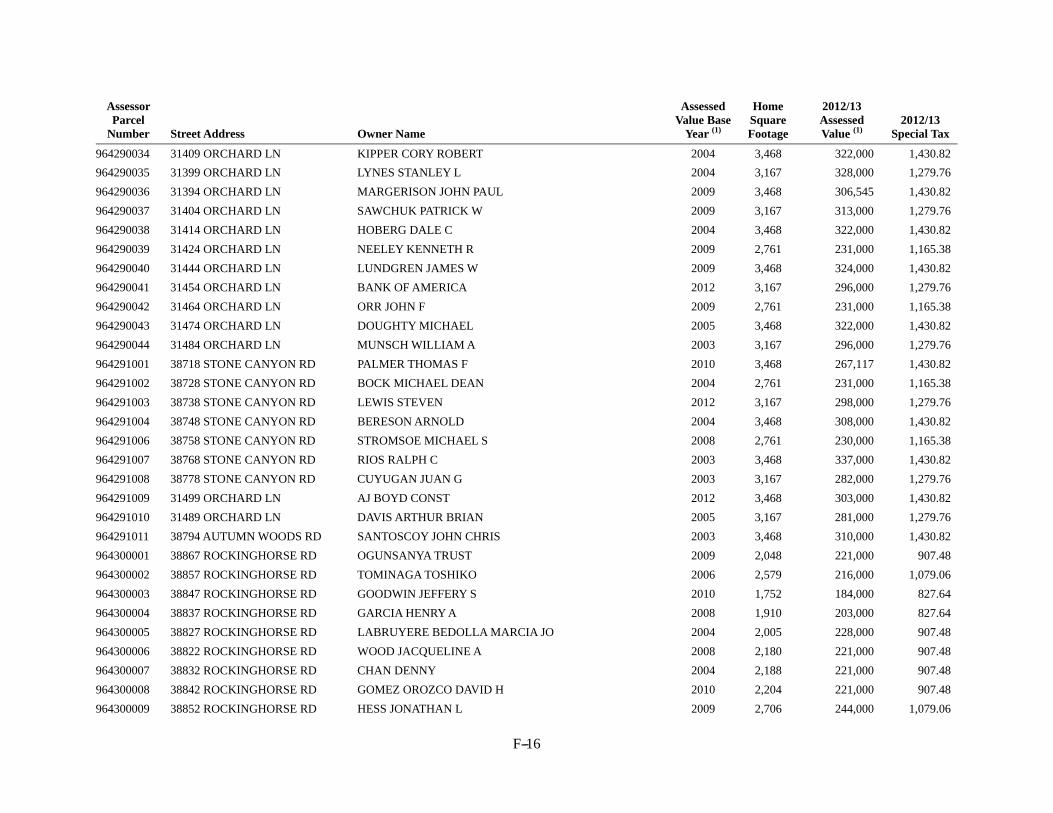

APPENDIX F - PARCEL LISTING

APPENDIX G - DTC AND THE BOOK-ENTRY-ONLY SYSTEM

TEMECULA VALLEY Unified School District

u~~a_,

Ci

Regional Location Map Desert

Hot Springs .,__ ___ a)

'-I

I --...... ' '

ORANGE j C OUNT Y

USMC Camp Pendleton

&. k-..--l.-d2miles NORTH APPROXIMATE

Moreno Valley

RIVERSIDE C O UNT Y

MEX I CO

La Quint

-------

Borrego Springs

[THIS PAGE INTENTIONALLY LEFT BLANK]

1

OFFICIAL STATEMENT

$6,785,000 COMMUNITY FACILITIES DISTRICT NO. 2002-1

OF THE TEMECULA VALLEY UNIFIED SCHOOL DISTRICT (IMPROVEMENT AREA NO. 1)

SERIES 2012 SPECIAL TAX REFUNDING BONDS

This Official Statement, including the cover page and appendices hereto, is provided to furnish information regarding the sale of Community Facilities District No. 2002-1 of the Temecula Valley Unified School District (Improvement Area No. 1) Series 2012 Special Tax Refunding Bonds (the “Bonds”) in the aggregate principal amount of $6,785,000.

INTRODUCTION This introduction is not a summary of this Official Statement. It is only a brief description of and guide to, and is qualified by, more complete and detailed information contained in the entire Official Statement, including the cover page and appendices hereto, and the documents summarized or described herein. A full review should be made of the entire Official Statement. The offering of the Bonds to potential investors is made only by means of the entire Official Statement.

The District

The Mello-Roos Community Facilities Act of 1982, as amended, constituting Sections 53311, et seq. of the Government Code of the State (the “Act”), was enacted by the California Legislature to provide an alternative method of financing certain public facilities, improvements and services. The Act authorizes local governmental entities to establish community facilities districts as legally constituted governmental entities within defined boundaries, with the legislative body of the local applicable governmental entity acting on behalf of a community facilities district. Subject to approval by at least a two-thirds vote of the votes cast by qualified electors within a district or with respect to an improvement area within a district and compliance with the provisions of the Act, the legislative body may issue bonds for the community facilities district or with respect to an improvement area within a district established by it and may levy and collect a special tax within such district or improvement area to repay such bonds. In accordance with such provisions, qualified electors within Improvement Area No. 1 of the District were entitled to cast one vote for each acre, or portion of an acre, of land they owned within Improvement Area No. 1 of the District. The property owners within Improvement Area No. 1 of the District at the time of the election cast more than two-thirds of votes at the election held on October 1, 2001 in favor of the levy of the Special Taxes and the authorization of bonds in a principal amount not to exceed $8,500,000 with respect to Improvement Area No. 1 of the District (“Improvement Area No. 1”).

On October 1, 2002, the Board of Education (the “Board”) of the Temecula Valley Unified School District (the “School District”) established Community Facilities District No. 2002-1 (the “District”) by the adoption of Resolution No. 2002-03/16 and the Improvement Areas therein, including Improvement Area No. 1. See “THE DISTRICT - IMPROVEMENT AREA NO. 1” herein. Within the District, the Board established four separate improvement areas with a separate rate and method of apportionment of Special Tax and bond authorization for each improvement area (see “APPENDIX A - RATE AND METHOD OF APPORTIONMENT OF THE SPECIAL TAX” herein). The Bonds are secured by and payable from proceeds of special taxes levied in Improvement Area No. 1 only.

2

The District is primarily within the master planned community known as Rancho Bella Vista, and is located generally northeast of the junction of Highway 79 and Murrieta Hot Springs Road in an unincorporated area of Riverside County. The entire Community Facilities District No. 2002-1 consists of four separate improvement areas and was originally formed to be developed with 1,995 homes as follows: Improvement Area No. 1 - 581 homes; Improvement Area No. 2 - 686 homes; Improvement Area No. 3 - 464 homes; and Improvement Area No. 4 - 264 homes.

Improvement Area No. 1. Improvement Area No. 1 consists of approximately 248 gross acres located in an unincorporated area of Riverside County developed with 451 single-family homes as part of the Rancho Bella Vista master planned community and 130 single-family homes in a separate subdivision known as “Avondale.” See “THE DISTRICT - IMPROVEMENT AREA NO. 1” herein.

The School District

The School District was originally established as the Temecula Valley Union School District, providing educational services to grades K-8. In 1989, the School District took over administration of the two high schools within its boundaries previously served by the Elsinore Union High School District. The School District encompasses approximately 148 square miles in the City of Temecula, surrounding cities and unincorporated Riverside County. The School District includes 17 elementary schools, four charter schools, one K-8 home school, six middle schools, three comprehensive high schools, one continuation high school, one independent study high school and one adult study school. For Fiscal Year 2012/13, the School District’s estimated enrollment is 27,143, excluding charter school enrollment.

Purpose

The Bonds are being issued to current refund the District’s outstanding Community Facilities District No. 2002-1 of the Temecula Valley Unified School District (Improvement Area No. 1) 2003 Special Tax Bonds (the “2003 Bonds”), to fund a reserve fund for the Bonds and to pay the costs of issuance of the Bonds. See “THE FINANCING PLAN” herein.

Security and Sources of Payment

The Bonds are issued pursuant to the Act, the Resolution of Issuance, as defined herein, and a Fiscal Agent Agreement, dated as of August 1, 2012 (the “Fiscal Agent Agreement”), by and between the District and U.S. Bank National Association, Los Angeles, California as fiscal agent (the “Fiscal Agent”). See “THE BONDS - Authority for Issuance” herein.

The Bonds are secured by and payable from a first pledge of all the Net Taxes of Improvement Area No. 1 received by the District (the “Net Taxes”). Net Taxes are defined as all special taxes (“Special Taxes”) collected within Improvement Area No. 1 of the District and net proceeds from the sale of property pursuant to foreclosure actions resulting from the delinquency of such Special Taxes less the Administrative Expense Requirement. See “SECURITY FOR THE BONDS - General” herein. The Bonds are also secured by amounts on deposit in the Reserve Fund as described in “SECURITY FOR THE BONDS - Reserve Fund.”

The District has covenanted in the Fiscal Agent Agreement, so long as any Bonds are outstanding, to annually levy the Special Taxes against all land within Improvement Area No. 1 of the District that is taxable under the Act and pursuant to the rate and method of apportionment of Special Taxes (the “Rate and Method”) (see “APPENDIX A - RATE AND METHOD OF APPORTIONMENT OF THE SPECIAL TAX”) in accordance with the proceedings for the authorization and issuance of the Bonds (“Taxable Property”) in amounts which will be sufficient to pay interest on and principal of the Bonds as such becomes due and payable, to replenish the Reserve Fund as necessary, to pay Administrative Expenses, subject to any maximum on the amount of Special Taxes that may be levied in any year, and to make provision for the collection of the Special Taxes. See “SECURITY FOR THE BONDS - Special Taxes” herein.

3

The District has covenanted to cause foreclosure proceedings to be commenced and diligently pursued against certain parcels with delinquent installments of Special Taxes. For a more detailed description of the foreclosure covenant see “SECURITY FOR THE BONDS - Proceeds of Foreclosure Sales.”

THE PRINCIPAL OF AND REDEMPTION PREMIUM, IF ANY, AND INTEREST ON THE BONDS ARE NOT AN INDEBTEDNESS OF THE STATE OR ANY OF ITS POLITICAL SUBDIVISIONS, AND NEITHER THE DISTRICT (EXCEPT TO THE LIMITED EXTENT DESCRIBED HEREIN), THE SCHOOL DISTRICT, THE STATE, NOR ANY OF ITS POLITICAL SUBDIVISIONS IS LIABLE ON THE BONDS. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT (EXCEPT TO THE LIMITED EXTENT DESCRIBED HEREIN), THE SCHOOL DISTRICT, OR THE STATE, OR ANY OTHER POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE BONDS. OTHER THAN THE NET TAXES OF IMPROVEMENT AREA NO. 1, NO TAXES ARE PLEDGED TO THE PAYMENT OF THE BONDS. THE BONDS ARE NOT A GENERAL OBLIGATION OF THE DISTRICT, BUT ARE LIMITED OBLIGATIONS OF THE DISTRICT, PAYABLE SOLELY FROM THE NET TAXES OF IMPROVEMENT AREA NO. 1 AND AMOUNTS PLEDGED UNDER THE FISCAL AGENT AGREEMENT AS MORE FULLY DESCRIBED HEREIN.

Pursuant to the Act, all lands owned by a public entity within Improvement Area No. 1 are exempt from the levy of the Special Tax, unless the public entity acquires the property after recordation of the Notice of Special Tax Lien, in which case the public entity will be obligated to pay the Special Tax, subject to certain limitations. The Rate and Method exempts from the Special Tax all property owned by the State, the federal government and local governments, as well as certain other properties, subject to certain limitations. See “THE DISTRICT - IMPROVEMENT AREA NO. 1 - Special Tax Rates” and “RISK FACTORS - Exempt Property.”

Property Values

The School District has relied on the assessed valuations of the County Assessor used for the purposes of general taxes for the valuations for all of the property within Improvement Area No. 1 of the District presented in this Official Statement. See “RISK FACTORS” and “THE DISTRICT - IMPROVEMENT AREA NO. 1 - Assessed Values.”

Tax Matters

In the opinion of Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel to the District, subject, however, to certain qualifications described herein, under existing laws, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, as amended (“Code”) and is exempt from State of California personal income taxes. In the further opinion of Bond Counsel, interest on the Bonds is not an item of tax preference for purposes of the federal alternative minimum taxes imposed on individuals and corporations, although Bond Counsel observes that such interest is included as an adjustment in the calculation of federal corporate alternative minimum taxable income and may therefore affect a corporation’s alternative minimum tax liabilities. Bond Counsel expresses no opinion regarding any other tax consequences related to the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See “LEGAL MATTERS - Tax Matters” and “APPENDIX E - PROPOSED FORM OF OPINION OF BOND COUNSEL” herein.

Special Risks

See the section of this Official Statement entitled “RISK FACTORS” for a discussion of special factors which should be considered, in addition to the other materials set forth herein, in considering the investment quality of the Bonds.

4

Professionals Involved in the Offering

U.S. Bank National Association, Los Angeles, California, will serve as the paying agent, registrar, authentication and transfer agent for the Bonds and perform the functions required of it under the Fiscal Agent Agreement for the payment of the principal of and interest on the Bonds. U.S. Bank National Association will also serve as Escrow Agent with respect to the 2003 Bonds. Bowie, Arneson, Wiles & Giannone, Newport Beach, California, will act as Bond Counsel and McFarlin & Anderson LLP, Laguna Hills, California will act as Disclosure Counsel. Harrell & Company Advisors, LLC, Orange, California, Financial Advisor, advised the District as to the financial structure and certain other financial matters relating to the Bonds. Certain matters will be passed upon for the District by Bowie, Arneson, Wiles & Giannone, Newport Beach, California and for the Underwriter by its Counsel, Nossaman LLP, Irvine, California. Special District Financing & Administration, Escondido, California, acts as Special Tax Consultant to the District. Grant Thornton LLP, Minneapolis, Minnesota will verify the mathematical accuracy of certain computations. Payment of the fees of Bond Counsel, Disclosure Counsel, Underwriter’s Counsel and the Financial Advisor is contingent on the sale and delivery of the Bonds.

Offering of the Bonds

The Bonds are offered, when, as and if issued, subject to the approval as to their legality by Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel. It is anticipated that the Bonds, in book-entry form, will be available for delivery on or about August 14, 2012, through the facilities of The Depository Trust Company.

Information Concerning this Official Statement

This Official Statement speaks only as of its date. The information set forth herein has been obtained by the District, with the assistance of Harrell & Company Advisors, LLC (the “Financial Advisor”), from sources which are believed to be reliable and such information is believed to be accurate and complete, but such information is not guaranteed as to accuracy or completeness, nor has it been independently verified and is not to be construed as a representation by the Financial Advisor, Bond Counsel, Underwriter’s Counsel or Disclosure Counsel. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended as such and are not to be construed as representations of fact. The information and expressions of opinion herein are subject to change without notice and the delivery of this Official Statement shall not, under any circumstances, create any implication that there has been no change in the information or opinions set forth herein or in the affairs of the District or the School District since the date hereof.

Availability of Legal Documents. The summaries and references contained herein with respect to the Fiscal Agent Agreement, the Bonds and other statutes or documents do not purport to be comprehensive or definitive and are qualified by reference to each such document or statute, and references to the Bonds are qualified in their entirety by reference to the form thereof included in the Fiscal Agent Agreement. Capitalized terms used herein and not defined shall have the meaning set forth in the Fiscal Agent Agreement. Copies of the documents described herein may be obtained after delivery of the Bonds from the District at Temecula Valley Unified School District, 31350 Rancho Vista Road, Temecula, California 92592, Attention: Assistant Superintendent of Business Support Services, telephone (951) 506-7940 upon request and payment of a charge for copying, mailing and handling.

5

THE BONDS Authority for Issuance

The Bonds are issued pursuant to the Act, the Fiscal Agent Agreement and Resolution No. 2012-13/1 adopted on July 17, 2012 by the Board, acting as the legislative body of the District (the “Resolution of Issuance”).

The District and Improvement Area No. 1 were established and bonded indebtedness was authorized pursuant to provisions of the Act. In accordance with such provisions, qualified electors within Improvement Area No. 1 were entitled to cast one vote for each acre, or portion of an acre, of land they owned within Improvement Area No. 1. The property owners within the Improvement Area No. 1 of the District at the time of the election cast all 432 votes at the election held on October 1, 2002 in favor of the levy of the Special Taxes and the authorization of bonds in a maximum amount of $8,500,000 with respect to Improvement Area No. 1.

General Provisions

The Bonds will be originally dated as of their date of delivery, and will bear interest at the rates per annum set forth on the inside front cover page hereof, payable semiannually on each March 1 and September 1, commencing on March 1, 2013 (each, an “Interest Payment Date”), and will mature in the amounts and on the dates set forth on the inside front cover page hereof. The Bonds will be issued in fully registered form without coupons in denominations of $5,000 and any integral multiple thereof. Interest on the Bonds will be calculated on the basis of a 360-day year comprised of twelve 30-day months.

The Bonds shall be payable both as to principal and interest, and as to any premiums upon the redemption thereof, in lawful money of the United States of America. The principal of the Bonds and any premiums due upon the redemption thereof shall be payable upon presentation thereof at the Principal Corporate Trust Office of the Fiscal Agent.

Interest on any Bond shall be payable from the Interest Payment Date next preceding the date of authentication, unless (i) such date of authentication is an Interest Payment Date, in which event interest shall be payable from such date of authentication, (ii) the date of authentication is after a Record Date (defined as the 15th day of the calendar month preceding an Interest Payment Date whether or not such day is a Business Day) but prior to the immediately succeeding Interest Payment Date, in which event interest will be payable from such Interest Payment Date, or (iii) the date of authentication is prior to the close of business on the first Record Date, in which event interest will be payable from the Dated Date; provided, however, that if at the time of authentication of a Bond, interest is in default, interest on that Bond shall be payable from the last date on which the interest has been paid or made available for payment, or if no interest has been paid or made available for payment, interest shall be payable from the Dated Date.

Subject to the book-entry-only system described below, interest on any Bond shall be paid to the person whose name shall appear in the Bond Register as the Owner of such Bond as of the close of business on the Record Date. Such interest shall be paid by check of the Fiscal Agent mailed on the Interest Payment Date to such Owner by first class mail at his or her address as it appears on the Bond Register as of the Record Date; provided that, in the case of an Owner of $1,000,000 or more in aggregate principal amount of the Bonds, upon the Fiscal Agent’s receipt of written request of such Owner prior to the Record Date accompanied by wire transfer instructions, such interest shall be paid on the Interest Payment Date in immediately available funds by wire transfer to an account in the United States.

6

Book-Entry-Only System. The Depository Trust Company (“DTC”), New York, New York, will act as securities depository for the Bonds. The Bonds will be issued as fully registered securities registered in the name of Cede & Co. (DTC’s partnership nominee) or such other name as may be requested by an authorized representative of DTC. Interest on and principal of the Bonds will be payable when due by wire of the Fiscal Agent to DTC which will in turn remit such interest and principal to DTC Participants (as defined herein), which will in turn remit such interest and principal to Beneficial Owners (as defined herein) of the Bonds (see “APPENDIX G - DTC AND THE BOOK-ENTRY-ONLY SYSTEM” herein). As long as DTC is the registered owner of the Bonds and DTC’s book-entry method is used for the Bonds, the Fiscal Agent will send any notices to Bondowners only to DTC.

Discontinuance of Book-Entry-Only System. DTC may discontinue providing its services as securities depository with respect to the Bonds at any time by giving reasonable notice to the District or the Fiscal Agent. Under such circumstances, in the event that a successor securities depository is not obtained, Bonds are required to be printed and delivered as described in the Fiscal Agent Agreement. The District may decide to discontinue use of the system of book-entry transfers through DTC (or a successor securities depository). In that event, the Bonds will be printed and delivered as described in the Fiscal Agent Agreement and described above under the caption “General Provisions.”

Transfer or Exchange of Bonds. Subject to the book-entry-only system, the registration of any Bond may, in accordance with its terms, be transferred upon the Bond Register by the person in whose name it is registered, in person or by his or her duly authorized attorney, upon surrender of such Bond for cancellation at the Principal Corporate Trust Office of the Fiscal Agent, accompanied by delivery of a written instrument of transfer in a form approved by the Fiscal Agent and duly executed by the Owner or his or her duly authorized attorney. Bonds may be exchanged at the Principal Corporate Trust Office of the Fiscal Agent for a like aggregate principal amount and maturity of Bonds of other authorized denominations. The Fiscal Agent may charge the Owner any tax or other governmental charge required with respect to such transfer or exchange. The cost of printing the Bonds and any services rendered or expenses incurred by the Trustee in connection with any transfer or exchange thereof shall be paid by the District. Whenever any Bonds shall be surrendered for registration of transfer or exchange, the District shall execute, and the Fiscal Agent shall authenticate and deliver, a new Bond, for a like aggregate principal amount and maturity; provided, that the Fiscal Agent shall not be required to register transfers or make exchanges of (i) Bonds for a period of 15 days next preceding the date established by the Fiscal Agent for selection of the Bonds to be redeemed, or (ii) any Bonds chosen for redemption.

No Additional Bonds

The District has covenanted in the Fiscal Agent Agreement to not issue any additional bonds, notes or other similar evidences of indebtedness payable in whole or in part out of Net Taxes of Improvement Area No. 1 of the District except (i) bonds issued to fully or partially refund the Outstanding Bonds, or (ii) subordinate bonds, notes or other evidences of indebtedness.

Redemption

Optional Redemption. The Bonds may be redeemed prior to maturity at the option of the District on any date on or after September 1, 2022, in whole, or in part from such maturities as are selected by the District in writing, and by lot within a maturity, at a redemption price equal to the principal amount to be redeemed, together with accrued interest to the date of redemption, without premium.

7

Special Mandatory Redemption from Prepaid Special Taxes. The Bonds are subject to special mandatory redemption prior to their stated maturities, on any Interest Payment Date for which timely notice can be given, in whole or in part from such maturities as are selected by the District in writing, and by lot within a maturity, in integral multiples of $5,000, from monies on deposit in the Prepayment Account of the Special Tax Fund that are transferred to the Mandatory Redemption Account, at the redemption prices set forth below, which are expressed as a percentage of the principal amount thereof, together with accrued interest to the date fixed for redemption, as follows:

Redemption Dates Redemption Prices Any Interest Payment Date through and including March 1, 2020 103% September 1, 2020 and March 1, 2021 102% September 1, 2021 and March 1, 2022 101% September 1, 2022 and any Interest Payment Date thereafter 100%

Prepaid Special Taxes collected by the District within Improvement Area No. 1 (net of any costs of collection) (“Prepaid Special Taxes”) shall be transferred, no later than 10 days after receipt thereof, to the Fiscal Agent and the District shall direct the Fiscal Agent to deposit the Prepaid Special Taxes in the Prepayment Account of the Special Tax Fund. The Prepaid Special Taxes shall be held in trust in the Prepayment Account for the benefit of the Bonds and shall be transferred by the Fiscal Agent to the Mandatory Redemption Account of the Redemption Fund to call Bonds on the next Interest Payment Date for which timely notice can be given.

Mandatory Sinking Fund Redemption. The Bonds maturing September 1, 2033 (the “Term Bonds”) are subject to mandatory redemption in part commencing September 1, 2031 and on each September 1 thereafter to maturity, by lot, at a redemption price equal to the principal amount thereof to be redeemed, together with accrued interest to the date fixed for redemption, without premium, from mandatory sinking payments, as follows:

SCHEDULE OF MANDATORY SINKING PAYMENTS TERM BONDS MATURING SEPTEMBER 1, 2033

September 1 Year

Principal Amount

2031 $425,000

2032 450,000

2033 (maturity) 475,000

Selection of Bonds for Redemption. If less than all of the Outstanding Bonds are to be redeemed, the District shall select Bonds to be redeemed proportionally among maturities so as to maintain approximately level debt service as directed in writing to the Fiscal Agent. If less than all of the Outstanding Bonds are to be redeemed the portion of any such Bond of a denomination of more than $5,000 to be redeemed shall be in the principal amount of $5,000 or a multiple thereof, and, in selecting portions of such Bonds for redemption, the Fiscal Agent shall treat such Bond as representing that number of Bonds of $5,000 denomination which is obtained by dividing the principal amount of such Bond to be redeemed in part by $5,000.

8

Purchase In Lieu of Redemption. In lieu of, or partially in lieu of, any redemption, monies deposited in the Redemption Fund may be used to purchase the Outstanding Bonds that were to be redeemed with such funds. Purchases of Outstanding Bonds may be made by the District prior to the selection of Bonds for redemption by the Fiscal Agent, at public or private sale as and when and at such prices as the District may in its discretion determine but only at prices (including brokerage or other expenses) not more than par plus accrued interest, and, in the case of funds in the Optional Redemption Account or the Mandatory Redemption Account, and the applicable premium to be paid in connection with the proposed redemption.

Notice of Redemption. When the Fiscal Agent shall receive notice from the District to redeem Bonds, or when the Fiscal Agent is required to redeem Bonds, the Fiscal Agent shall give notice, in the name of the District of the redemption of such Bonds. At least 30 days but no more than 60 days prior to the redemption date, the Fiscal Agent shall mail by first class mail a copy of such notice, postage prepaid, to the respective Owners thereof at their addresses appearing on the Bond Register. The actual receipt by the Owner of any Bond of notice of such redemption shall not be a condition precedent thereto, and neither failure to receive such notice nor any defect therein shall affect the validity of the proceedings for the redemption of such Bond, or the cessation of interest on the redemption date. A certificate by the Fiscal Agent that notice of such redemption has been given shall be conclusive as against all parties, and it shall not be open to any Owner to show that he or she failed to receive notice of such redemption. Such notice shall state that, on the date fixed for redemption, there shall become due and payable on each Bond or portion thereof called for redemption the principal thereof, together with any premium, and interest accrued to the redemption date, and that, from and after such date, interest thereon shall cease to accrue and be payable.

In addition, the notice of redemption shall be sent at least 30 days before the redemption date to the Securities Depository and, upon written request of the District, to any other registered securities depositories then in the business of holding substantial amounts of obligations of types comprising the Bonds and to the National Information Service or at the request of the District, any other information services that disseminate notice of redemption of obligations such as the Bonds.

Any redemption notice may specify that redemption of the Bonds designated for redemption on the specified date will be subject to the receipt by the District and/or the Fiscal Agent, as applicable, of monies sufficient to cause such redemption, and neither the District nor the Fiscal Agent will have any liability to the Owners of any Bonds, or any other party, as a result of the District’s failure to redeem the Bonds designated for redemption as a result of insufficient monies therefor.

Any notice of redemption may be cancelled and annulled if for any reason funds are not, or will not, be available on the date fixed for redemption for the payment in full of the Bonds then called for redemption. Such cancellation and annulment is not a default under the Fiscal Agent Agreement. The District will not have any liability to the Owners, or any other party, as a result of the District’s failure to redeem the Bonds designated for redemption as a result of insufficient monies therefore.

Additionally, the District may rescind any optional redemption of the Bonds, and notice thereof, for any reason on any date prior to the date fixed for such redemption by causing written notice of the rescission to be given to the Owners of the Bonds so called for redemption. Notice of rescission of redemption shall be given in the same manner in which notice of redemption was originally given. The actual receipt by the Owner of any Bond of notice of such rescission shall not be a condition precedent to rescission, and failure to receive such notice or any defect in such notice shall not affect the validity of the rescission. Neither the District nor the Fiscal Agent will have any liability to the Owners of any Bonds, or any other party, as a result of the District’s decision to rescind redemption of any Bonds pursuant to the provisions of this subsection.

9

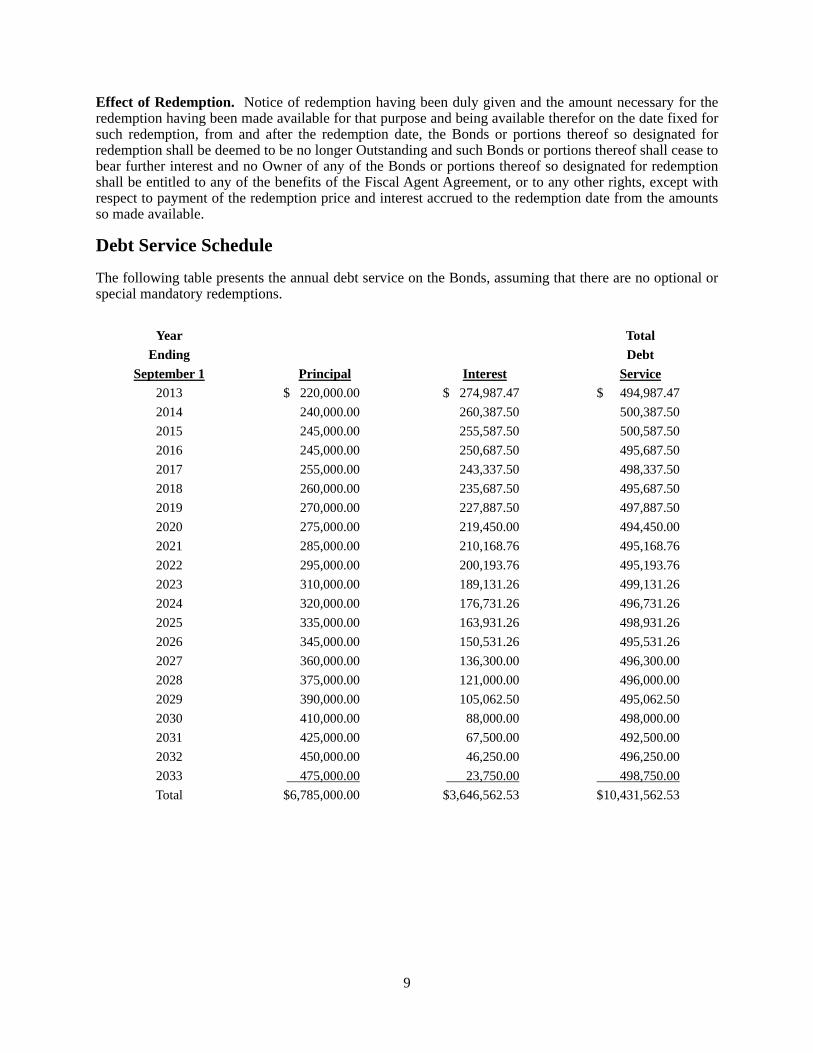

Effect of Redemption. Notice of redemption having been duly given and the amount necessary for the redemption having been made available for that purpose and being available therefor on the date fixed for such redemption, from and after the redemption date, the Bonds or portions thereof so designated for redemption shall be deemed to be no longer Outstanding and such Bonds or portions thereof shall cease to bear further interest and no Owner of any of the Bonds or portions thereof so designated for redemption shall be entitled to any of the benefits of the Fiscal Agent Agreement, or to any other rights, except with respect to payment of the redemption price and interest accrued to the redemption date from the amounts so made available.

Debt Service Schedule

The following table presents the annual debt service on the Bonds, assuming that there are no optional or special mandatory redemptions.

Year Total

Ending Debt

September 1 Principal Interest Service

2013 $ 220,000.00 $ 274,987.47 $ 494,987.47

2014 240,000.00 260,387.50 500,387.50

2015 245,000.00 255,587.50 500,587.50

2016 245,000.00 250,687.50 495,687.50

2017 255,000.00 243,337.50 498,337.50

2018 260,000.00 235,687.50 495,687.50

2019 270,000.00 227,887.50 497,887.50

2020 275,000.00 219,450.00 494,450.00

2021 285,000.00 210,168.76 495,168.76

2022 295,000.00 200,193.76 495,193.76

2023 310,000.00 189,131.26 499,131.26

2024 320,000.00 176,731.26 496,731.26

2025 335,000.00 163,931.26 498,931.26

2026 345,000.00 150,531.26 495,531.26

2027 360,000.00 136,300.00 496,300.00

2028 375,000.00 121,000.00 496,000.00

2029 390,000.00 105,062.50 495,062.50

2030 410,000.00 88,000.00 498,000.00

2031 425,000.00 67,500.00 492,500.00

2032 450,000.00 46,250.00 496,250.00

2033 475,000.00 23,750.00 498,750.00

Total $6,785,000.00 $3,646,562.53 $10,431,562.53

10

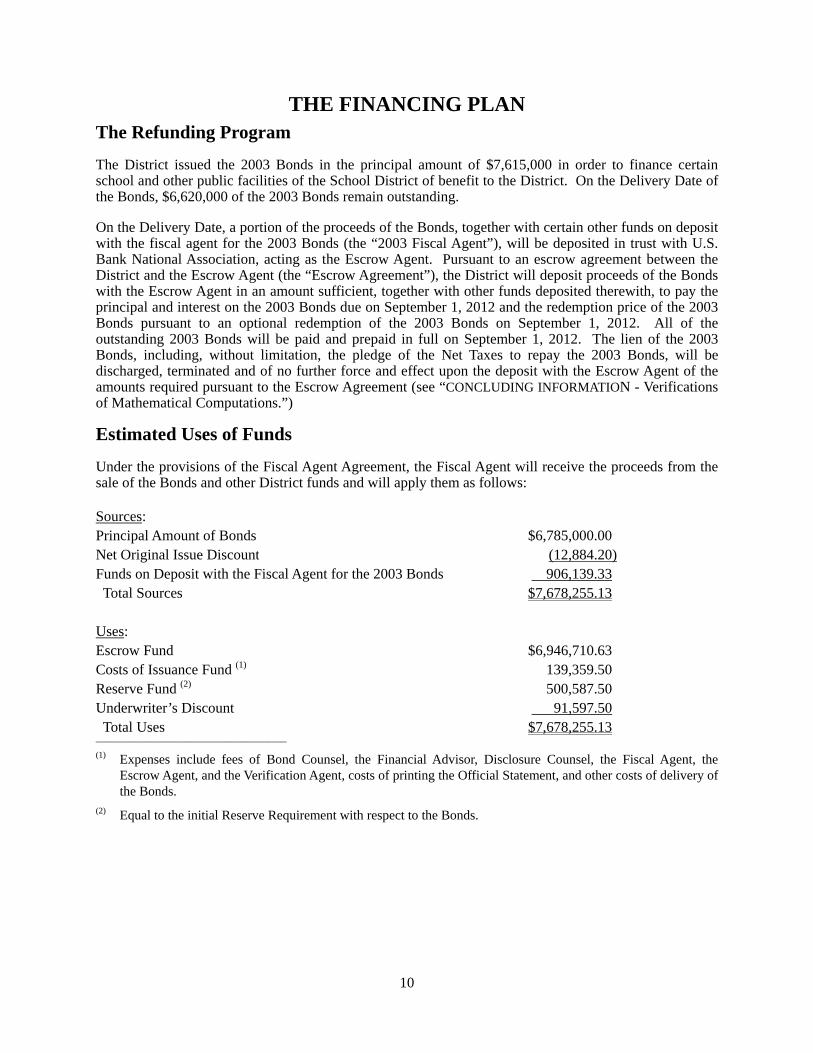

THE FINANCING PLAN The Refunding Program

The District issued the 2003 Bonds in the principal amount of $7,615,000 in order to finance certain school and other public facilities of the School District of benefit to the District. On the Delivery Date of the Bonds, $6,620,000 of the 2003 Bonds remain outstanding.

On the Delivery Date, a portion of the proceeds of the Bonds, together with certain other funds on deposit with the fiscal agent for the 2003 Bonds (the “2003 Fiscal Agent”), will be deposited in trust with U.S. Bank National Association, acting as the Escrow Agent. Pursuant to an escrow agreement between the District and the Escrow Agent (the “Escrow Agreement”), the District will deposit proceeds of the Bonds with the Escrow Agent in an amount sufficient, together with other funds deposited therewith, to pay the principal and interest on the 2003 Bonds due on September 1, 2012 and the redemption price of the 2003 Bonds pursuant to an optional redemption of the 2003 Bonds on September 1, 2012. All of the outstanding 2003 Bonds will be paid and prepaid in full on September 1, 2012. The lien of the 2003 Bonds, including, without limitation, the pledge of the Net Taxes to repay the 2003 Bonds, will be discharged, terminated and of no further force and effect upon the deposit with the Escrow Agent of the amounts required pursuant to the Escrow Agreement (see “CONCLUDING INFORMATION - Verifications of Mathematical Computations.”)

Estimated Uses of Funds

Under the provisions of the Fiscal Agent Agreement, the Fiscal Agent will receive the proceeds from the sale of the Bonds and other District funds and will apply them as follows:

Sources: Principal Amount of Bonds $6,785,000.00 Net Original Issue Discount (12,884.20) Funds on Deposit with the Fiscal Agent for the 2003 Bonds 906,139.33 Total Sources $7,678,255.13

Uses: Escrow Fund $6,946,710.63 Costs of Issuance Fund (1) 139,359.50 Reserve Fund (2) 500,587.50 Underwriter’s Discount 91,597.50 Total Uses $7,678,255.13 _________________________________________

(1) Expenses include fees of Bond Counsel, the Financial Advisor, Disclosure Counsel, the Fiscal Agent, the Escrow Agent, and the Verification Agent, costs of printing the Official Statement, and other costs of delivery of the Bonds.

(2) Equal to the initial Reserve Requirement with respect to the Bonds.

11

SECURITY FOR THE BONDS General

The Bonds are secured by and payable from a first pledge of all of the Net Taxes of Improvement Area No. 1 of the District, subject to the provisions of the Fiscal Agent Agreement. Net Taxes of Improvement Area No. 1 are defined as Gross Taxes (defined as all Special Taxes collected within Improvement Area No. 1 of the District and net proceeds from the sale of property pursuant to foreclosure actions resulting from the delinquency of such Special Taxes) less the Administrative Expense Requirement. The Administrative Expense Requirement means an amount up to $25,000 annually for the payment of Administrative Expenses. Administrative Expenses include administrative costs with respect to the calculation and collection of the Special Taxes and any other costs related to the Bonds, costs and legal expenses of foreclosure actions to the extent not recovered pursuant to statutory authorization or costs otherwise incurred by the District with respect to Improvement Area No. 1 in order to carry out the authorized purposes of the Bonds. Subject to the limitations contained in the Rate and Method, the District has covenanted in the Fiscal Agent Agreement to annually levy the Special Taxes in accordance with the Rate and Method described below, which amount, if timely paid, is sufficient to pay the principal of and interest on the Bonds, to replenish the Reserve Fund, if necessary, to fund Administrative Expenses and to pay the cost of additional school facilities. The Bonds are further secured by a first pledge on all monies deposited in the Bond Fund, the Redemption Fund and the Reserve Fund, and, until disbursed as provided in the Fiscal Agent Agreement, the Special Tax Fund. The Net Taxes of Improvement Area No. 1 and all monies deposited into said funds (until disbursed as provided in the Fiscal Agent Agreement) are pledged to the payment of the principal of, and interest and any premium on, the Bonds as provided in the Fiscal Agent Agreement and in the Act until all of the Bonds have been paid and retired or until monies or Federal Securities (as defined in the Fiscal Agent Agreement) have been set aside irrevocably for that purpose.

Notwithstanding anything to the contrary in the Fiscal Agent Agreement, Net Taxes deposited in the Administrative Expense Fund and the Rebate Fund shall no longer be considered pledged to the Bonds and the Administrative Expense Fund and the Rebate Fund established under the Fiscal Agent Agreement shall not be construed as trust funds held for the benefit of the Owners of the Bonds. The facilities acquired or constructed with the proceeds of the 2003 Bonds are not in any way pledged to pay the debt service on the Bonds, and any proceeds of condemnation, destruction or other disposition of such facilities are not pledged to pay the debt service on the Bonds and are free and clear of any lien or obligation imposed under the Fiscal Agent Agreement.

THE PRINCIPAL OF AND REDEMPTION PREMIUM, IF ANY, AND INTEREST ON THE BONDS ARE NOT AN INDEBTEDNESS OF THE STATE OR ANY OF ITS POLITICAL SUBDIVISIONS, AND NEITHER THE DISTRICT (EXCEPT TO THE LIMITED EXTENT DESCRIBED HEREIN), THE SCHOOL DISTRICT, THE STATE, NOR ANY OF ITS POLITICAL SUBDIVISIONS IS LIABLE ON THE BONDS. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT (EXCEPT TO THE LIMITED EXTENT DESCRIBED HEREIN), THE SCHOOL DISTRICT, OR THE STATE, OR ANY OTHER POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE BONDS. OTHER THAN THE NET TAXES OF IMPROVEMENT AREA NO. 1 AS DEFINED HEREIN, NO TAXES ARE PLEDGED TO THE PAYMENT OF THE BONDS. THE BONDS ARE NOT A GENERAL OBLIGATION OF THE DISTRICT, BUT ARE LIMITED OBLIGATIONS OF THE DISTRICT, PAYABLE SOLELY FROM THE NET TAXES OF IMPROVEMENT AREA NO. 1 AND AMOUNTS PLEDGED UNDER THE FISCAL AGENT AGREEMENT AS MORE FULLY DESCRIBED HEREIN.

12

Special Taxes

The Special Taxes are levied and collected according to the Rate and Method set forth in “APPENDIX A - RATE AND METHOD OF APPORTIONMENT OF THE SPECIAL TAX.” The Special Taxes are to be levied by the Board acting as the legislative body of the District each Fiscal Year on all Taxable Property within Improvement Area No. 1 of the District in accordance with the Rate and Method.

The Special Taxes are required to be collected by the County of Riverside Tax Collector in the same manner and at the same time as regular ad valorem property taxes are collected by the County Tax Collector. The Fiscal Agent Agreement requires the Special Taxes to be transferred by the District to the Fiscal Agent for deposit in the Special Tax Fund. However, the District has instructed the County of Riverside to remit the Special Taxes directly to the Fiscal Agent.

Although the Special Taxes, when levied, will constitute a lien on parcels subject to taxation, it does not constitute a personal indebtedness of the owners of property. There is no assurance that the owners of real property will be financially able to pay the annual Special Tax or that they will pay such tax even if financially able to do so. See “RISK FACTORS” herein.

Proceeds of Foreclosure Sales

Pursuant to the Act, in the event of any delinquency in the payment of the Special Tax, the District may order the institution of a superior court action to foreclose the lien therefore within specified time limits. In such an action, the real property subject to the unpaid amount may be sold at judicial foreclosure sale. Such judicial foreclosure action is not mandatory and will be pursued only as provided in the following paragraphs.

The District has covenanted for the benefit of the owners of the Bonds that, not later than August 1 of each Fiscal Year, the District will compare the amount of Special Taxes theretofore levied in Improvement Area No. 1 of the District to the amount of Special Taxes theretofore collected by the County as of such date, and:

A. Individual Delinquencies. If the District determines that (i) any single parcel within Improvement Area No. 1 is subject to a Special Tax delinquency in the aggregate amount of $3,000 or more, or (ii) any owner owns one or more parcels subject to a Special Tax delinquency in an aggregate amount of $5,000 or more, then the District will send or cause to be sent a notice of delinquency (and a demand for immediate payment thereof) to the property owner within 45 days of such determination, and (if the delinquency remains uncured) foreclosure proceedings shall be commenced by the District within 120 days of such determination, to the extent permissible under applicable law and shall thereafter diligently pursue such proceedings.

B. Aggregate Delinquencies. If the District determines that the total amount of delinquent Special Tax for the prior Fiscal Year for Improvement Area No. 1 exceeds 5% of the total Special Taxes due and payable for the prior Fiscal Year, the District will notify or cause to be notified all property owners who are then delinquent in the payment of Special Taxes (and demand immediate payment of the delinquency) within 45 days of such determination, and (if the delinquency remains uncured) shall commence foreclosure proceedings within 120 days of such determination against each parcel of land in Improvement Area No. 1 with a Special Tax delinquency, to the extent permissible under applicable law and shall thereafter diligently pursue such proceedings.

The net proceeds received following a judicial foreclosure sale of land within Improvement Area No. 1 of the District resulting from a property owner’s failure to pay the Special Taxes when due are included within the Net Taxes pledged to the payment of principal of and interest on the Bonds under the Fiscal Agent Agreement.

13

The District is expressly authorized to include costs and attorneys’ fees related to foreclosure of delinquent Special Taxes as Administrative Expenses pursuant to the Fiscal Agent Agreement.

It should be noted that any foreclosure proceedings commenced as described above, could be stayed by the commencement of bankruptcy proceedings by or against the owner of the property being foreclosed. See “RISK FACTORS - Bankruptcy and Foreclosure Delays.”

No assurances can be given that a judicial foreclosure action, once commenced, will be completed or that it will be completed in a timely manner. See “RISK FACTORS - Bankruptcy and Foreclosure Delays.” If a judgment of foreclosure and order of sale is obtained, the judgment creditor (the District) must cause a Notice of Levy to be issued. Under current law, a judgment debtor (property owner) has 120 days (or in some cases a shorter period) from the date of service of the Notice of Levy and 20 days from the subsequent notice of sale in which to redeem the property to be sold. If a judgment debtor fails to so redeem and the property is sold, his only remedy is an action to set aside the sale, which must be brought within 90 days of the date of sale. If, as a result of such action, a foreclosure sale is set aside, the judgment is revived and the judgment creditor is entitled to interest on the revived judgment as if the sale had not been made. The constitutionality of the current law, which repeals the former one-year redemption period, has not been tested; and there can be no assurance that, if tested, such law will be upheld. Any parcel subject to foreclosure sale must be sold at the minimum bid price unless a lesser minimum bid price is authorized by the Owners of 75% of the principal amount of Bonds Outstanding.

No assurances can be given that the real property subject to sale or foreclosure will be sold or, if sold, that the proceeds of sale will be sufficient to pay any delinquent Special Tax installment. The Act does not require the School District or the District to purchase or otherwise acquire any lot or parcel of property offered for sale or subject to foreclosure if there is no other purchaser at such sale. The Act does specify that the Special Taxes will have the same lien priority in the case of delinquency as for ad valorem property taxes and special assessments.

If the Reserve Fund is depleted and delinquencies in the payment of Special Taxes exist, there could be a default or delay in payments to the Owners pending prosecution of foreclosure proceedings and receipt by the District of foreclosure sale proceeds, if any.

Special Tax Fund

There is established pursuant to the Fiscal Agent Agreement, as a separate account to be held by the Fiscal Agent, a Special Tax Fund. The District is required to transfer to the Fiscal Agent for deposit into the Special Tax Fund (exclusive of Prepaid Special Taxes received which shall be deposited into the Prepayment Account of the Special Tax Fund), no later than 10 days after receipt thereof, all Special Taxes and other amounts constituting Gross Taxes collected by the District within Improvement Area No. 1. Monies in the Special Tax Fund will be held by the Fiscal Agent for the benefit of the Owners of the Bonds and, pending any disbursement, will be subject to a lien in favor of the Owners of the Bonds. The District has instructed the County to remit the Special Taxes directly to the Fiscal Agent.

The Fiscal Agent will withdraw from the Special Tax Fund and transfer: (i) to the Administrative Expense Fund, an amount up to a maximum of $25,000 per year (the “Administrative Expense Requirement”) for Administrative Expenses, (ii) to the Interest Account of the Bond Fund an amount such that the balance in the Interest Account, one Business Day prior to each Interest Payment Date shall equal the installment of interest due on the Bonds on said Interest Payment Date, (iii) to the Principal Account of the Bond Fund an amount up to the amount needed to make the principal payment due on the Bonds during the current Bond Year, (iv) to the Reserve Fund the amount, if any, necessary to replenish the Reserve Fund to the Reserve Requirement, (v) to the extent there are additional Administrative Expenses of the District, to the Administrative Expense Fund in the amount set forth by the District in writing, and (vi) at the end of the Bond Year, any remaining funds in the Special Tax Fund which are not required to cure a delinquency in the payment of principal and interest on the Bonds, to restore the Reserve Fund to

14

the Reserve Requirement, or to pay current or pending Administrative Expenses, to the District for any lawful purpose under the District proceedings free and clear of the lien of the Fiscal Agent Agreement. See “APPENDIX B - SUMMARY OF CERTAIN PROVISIONS OF THE FISCAL AGENT AGREEMENT.”

Bond Fund

There is established pursuant to the Fiscal Agent Agreement, as a separate fund to be held by the Fiscal Agent, the Bond Fund (in which there is established an Interest Account and a Principal Account). The Bond Fund is used to disperse payments of principal of and interest on the Bonds to the Owners on each respective Interest Payment Date. Monies in the Interest Account are allocated to the payment of interest due on the Bonds on each Interest Payment Date, and monies in the Principal Account are allocated to the repayment of principal on the Bonds on the corresponding Interest Payment Date. Upon final maturity of the Bonds and the payment of all principal of and interest on the Bonds, any monies remaining in the Bond Fund shall be transferred to the Special Tax Fund.

Reserve Fund

In order to further secure the payment of principal of and interest on the Bonds, the Fiscal Agent Agreement provides that, from the proceeds of the sale of the Bonds, an amount will be deposited into the Reserve Fund equal to the Reserve Requirement. The Reserve Requirement is defined in the Fiscal Agent Agreement to mean, as of the date of any calculation, an amount equal to the least of (a) 10% of the original principal amount of the Bonds, (b) Maximum Annual Debt Service, or (c) 125% of average Annual Debt Service. The Reserve Requirement is initially equal to $500,587.50.

Except as provided in the next paragraph with respect to certain investment earnings, monies in the Reserve Fund shall be used solely for the purpose of (i) making transfers to the Bond Fund or the Redemption Fund to pay the principal of, including Mandatory Sinking Payments, and interest on Bonds when due to the extent that monies in the Interest Account and the Principal Account of the Bond Fund or monies in the Sinking Fund Redemption Account of the Redemption Fund are insufficient therefore, (ii) making any required transfer to the Rebate Fund upon written direction from the District, (iii) making any transfers to the Bond Fund or Mandatory Redemption Account of the Redemption Fund in connection with prepayments of the Special Taxes, (iv) paying the principal and interest due on the Bonds in the final Bond Year, and (v) application to the defeasance of the Bonds. If the amounts in the Interest Account or the Principal Account of the Bond Fund and the Sinking Fund Redemption Account of the Redemption Fund are insufficient to pay the principal of, including Mandatory Sinking Payments, or interest on the Bonds when due, the Fiscal Agent shall, one Business Day prior to an Interest Payment Date, withdraw from the Reserve Fund for deposit in the Interest Account and the Principal Account of the Bond Fund, or the Sinking Fund Redemption Account of the Redemption Fund, monies necessary for such purpose. Following any transfer to the Interest Account or the Principal Account of the Bond Fund, or the Sinking Fund Redemption Account of the Redemption Fund, the Fiscal Agent shall notify the District of the amount needed to replenish the Reserve Fund to the Reserve Requirement and the District shall include such amount as is required at that time to correct such deficiency in the next Special Tax levy to the extent of the permitted maximum Special Tax rates.

Monies in the Reserve Fund in excess of the Reserve Requirement (exclusive of Excess Investment Earnings) shall be withdrawn on each March 1 and transferred to the Interest Account of the Bond Fund, and any remaining excess shall be transferred to the Principal Account of the Bond Fund, or to the Sinking Fund Redemption Account of the Redemption Fund to the extent required to make any principal payment or Mandatory Sinking Payments on the next following September 1. The Fiscal Agent shall transfer Excess Investment Earnings from Reserve Fund earnings upon written direction of the District.

15

Special Taxes and the Teeter Plan

The County has adopted a Teeter Plan as provided for in Section 4701 et seq. of the California Revenue and Taxation Code, under which a tax distribution procedure is implemented and secured roll taxes are distributed to taxing agencies within the County on the basis of the tax levy, rather than on the basis of actual tax collections. By policy, the County does not include assessments, reassessments and special taxes of the District in its Teeter program.

THE DISTRICT – IMPROVEMENT AREA NO. 1 The information set forth herein has been included because it is considered relevant to an informed evaluation of Improvement Area No. 1 of the District and the security for the Bonds.

The owners of property within Improvement Area No. 1 of the District will not be personally liable for payments of the Special Taxes to be applied to pay the principal of and interest on the Bonds. Accordingly, no property owner’s financial statements have been included in this Official Statement.

Investors must recognize the uncertainties with respect to the assessed values of the parcels within Improvement Area No. 1. The Bonds are secured by certain proceeds of the Special Taxes levied on such parcels and are not a personal indebtedness of the property owners. See “RISK FACTORS” herein.

General

The District is primarily within the master planned community known as Rancho Bella Vista, and is located generally northeast of the junction of Highway 79 and Murrieta Hot Springs Road in an unincorporated area of Riverside County. The entire Community Facilities District No. 2002-1 consists of four separate improvement areas and was originally formed to be developed with 1,995 homes. The development as described herein relates only to Improvement Area No. 1 and Bonds are secured and payable only from certain proceeds of the Special Taxes levied in Improvement Area No. 1.

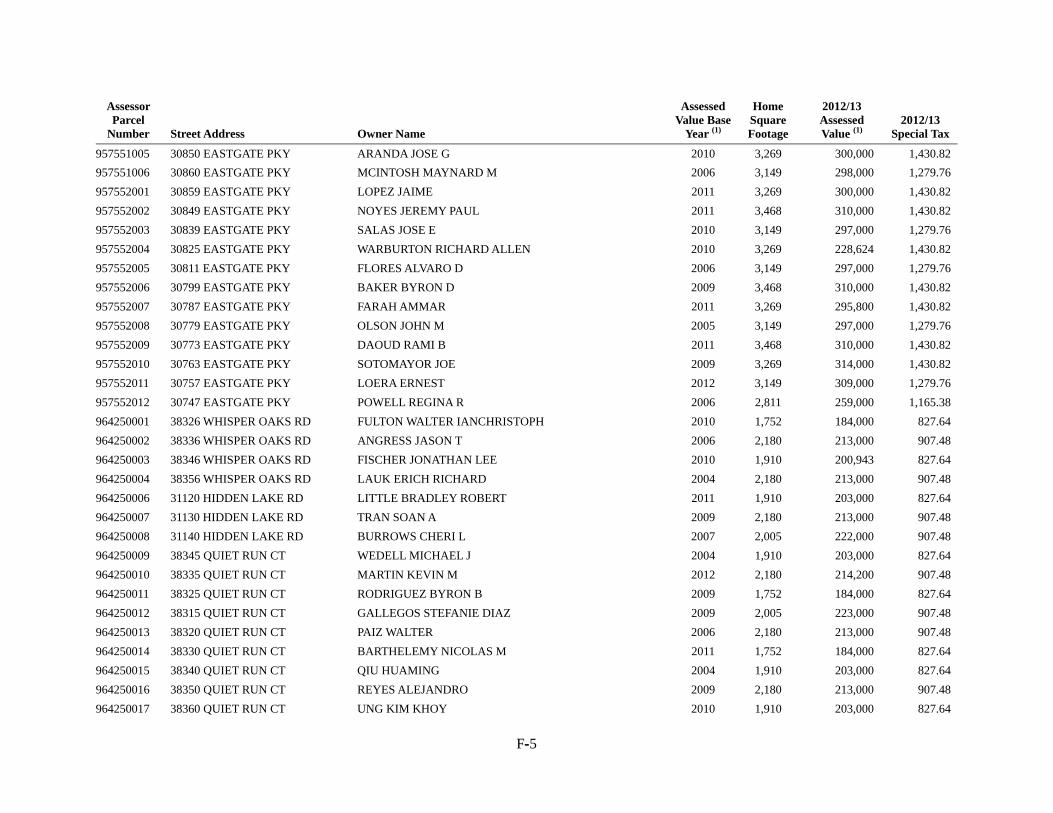

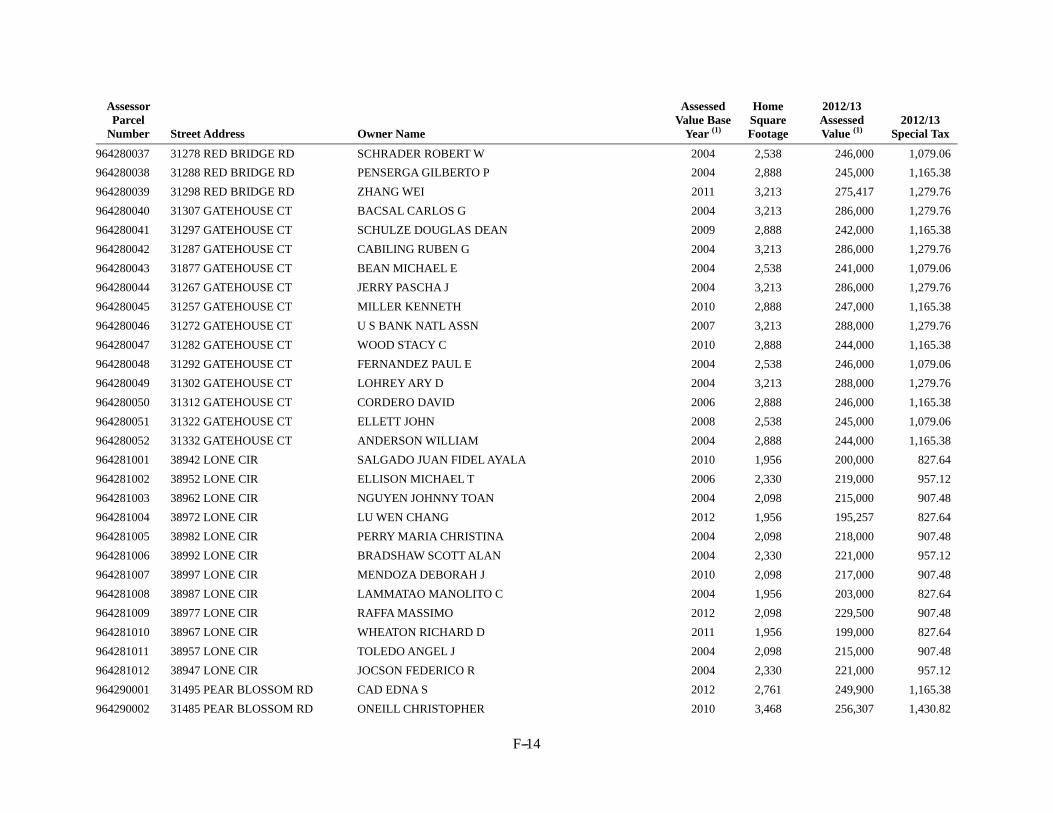

There are 581 homes developed in Improvement Area No. 1. Property in Improvement Area No. 1 of the District is located in two non-contiguous areas. The first area has been developed as “Monterra Ranch,” “Miranda Ranch” and “Belcerro Ranch” by Richmond American Homes of California, Inc. and as “San Lucas” and “San Marino” by Centex Homes. This area includes 451 homes within the Rancho Bella Vista development. The second area has been developed by Richmond American as “Avondale” with 130 homes. All homes were built between 2002 and 2003, with the exception of the Avondale neighborhood, which was built between 2004 and 2005. According to the ownership data reported by the County as of July 1, 2012, all units were owner-occupied as of July 1, 2012, except for 12 units shown as being owned by lenders. See “Lender-Owned Special Tax Obligations” and “APPENDIX F - PARCEL LISTING” herein for more detailed ownership information.

Directly adjacent to the Rancho Bella Vista development, the School District constructed a new elementary school (Alamos Elementary School) and a new middle school (Bella Vista Middle School) in 2004.

16

The home sizes and number of homes in each of the neighborhoods in Improvement Area No. 1 are shown in Table No. 1.

TABLE NO. 1 COMMUNITY FACILITIES DISTRICT NO. 2002-1

OF THE TEMECULA VALLEY UNIFIED SCHOOL DISTRICT (IMPROVEMENT AREA NO. 1)

Neighborhood # of Units Square Footages

Monterra Ranch 68 2,761 - 3,468

Miranda Ranch 76 1,956 - 2,330

Belcerro Ranch 85 2,538 - 3,213

San Lucas 112 1,752 - 2,180

San Marino 110 2,188 - 2,706

Avondale 130 2,811 - 3,468

581

Source: Special District Financing & Administration.

The number of building permits issued by year are shown in Table No. 2.

TABLE NO. 2 COMMUNITY FACILITIES DISTRICT NO. 2002-1

OF THE TEMECULA VALLEY UNIFIED SCHOOL DISTRICT (IMPROVEMENT AREA NO. 1)

BUILDING PERMITS ISSUED BY YEAR

# of

Building Permit Date Units

March 2, 2001 - March 1, 2002 3

March 2, 2002 - March 1, 2003 403

March 2, 2003 - March 1, 2004 45

March 2, 2004 - March 1, 2005 76

March 2, 2005 - March 1, 2006 53

March 2, 2006 - March 1, 2007 1

Total 581

Source: Special District Financing & Administration.

Assessed Values

For all property in Improvement Area No. 1 of the District, the County-determined assessed valuation is provided as an estimate for purposes of valuation. The County-determined assessed valuation is derived from the Fiscal Year 2012/13 County Assessor’s assessed valuation of land and improvements. The County’s assessed valuation of land and improvements is based on the base year assessed value (which may or may not be reflective of the fair market value of the land and improvements) increased by a

17

maximum of 2% a year each year thereafter, as allowed under Article XIIIA of the Constitution of the State of California. Values may also be decreased if inflation is negative (for example, the inflation factor for Fiscal Year 2010/11 was -0.237%). See “RISK FACTORS - Property Values - Article XIIIA” and “- Reduction in Inflationary Rate.” Therefore, the assessor’s value typically does not accurately reflect the fair market value of the land and improvements which may be higher or lower than the County Assessor’s value. Further, due to timing, the Assessor’s value may not reflect the most recent sale price of a parcel. The fair market value can only be established through the sale of the property or an appraisal of the property within Improvement Area No. 1 of the District. The School District has not undertaken to obtain an appraisal of the property within Improvement Area No. 1 of the District.

Proposition 8 Reductions. Proposition 8 provides for the assessment of real property at the lesser of its originally determined (base year) full cash value compounded annually by the inflation factor, or its full cash value as of the lien date, taking into account reductions in value due to damage, destruction, obsolescence or other factors causing a decline in market value. Reductions based on Proposition 8 do not establish new base year values, and the property may be reassessed as of the following lien date up to the lower of the then-current fair market value or the factored base year value.

Since 2008/09, the County Assessor has made numerous adjustments to assessed values of property within Improvement Area No. 1 where no change in ownership had occurred, some resulting in decreases in value for particular properties and some resulting in increases in value for particular properties. For example, based on a comparison using July 1, 2008 and July 1, 2009 ownership data provided by Riverside County, more than 80% of the homes in Improvement Area No. 1 with no change in ownership saw a decrease in value between 2008/09 and 2009/10, with an average decline of approximately $89,000 (26% of the existing value of such homes). In the following year, based on a comparison using July 1, 2009 and July 1, 2010 ownership data provided by Riverside County, 57% of homes with no change in ownership saw a decrease in value, with an average decline of approximately $14,000 (5% of existing value of such homes), but approximately 20% of homes with no change in ownership saw an average increase in value from the prior year of approximately $13,000.