risks in doing m&a in russia_anatoly andriash

TRANSCRIPT

FINANCIAL INSTITUTIONS

ENERGY

INFRASTRUCTURE, MINING AND COMMODITIES

TRANSPORT

TECHNOLOGY AND INNOVATION

PHARMACEUTICALS AND LIFE SCIENCES

Risks in Doing M&A in Russia

Anatoly Andriash Head of Moscow, Partner

Norton Rose (Central Europe) LLP 17 April 2013 NES/CEFIR Public Seminar

Risks in Doing M&A in Russia 2

Motivation in M&A transactions

Buyer’s Motivation

- Acquisition of relevant asset (real estate, mining licenses, cash flows, etc.)

- Access to skilled personnel, resources and goodwill of the target

- Technology and intellectual property (including software, trademarks, patents, etc.)

- Expansion of market share – client base

- Reduced number of competitors

- Economy of scale

- Trends in particular sector

- Speculative trading

- Synergy – reduced organizational costs and enhanced benefits from investments

- Diversification

- Management ambitions

Seller’s Motivation

– The selling price exceeds the estimated value of the business

– Uncertainty that positive trend will prevail

– Difficulties with management

– Pressure from monopolists (infrastructure, buyers, sellers)

– Difficulties with liquidity (e.g. forecasted financial stress)

– Structuring of “withdrawal”: e.g. private placement, IPO

– Sale of non-core assets

– Pressure from creditors

– Personal reasons

Risks in Doing M&A in Russia 3

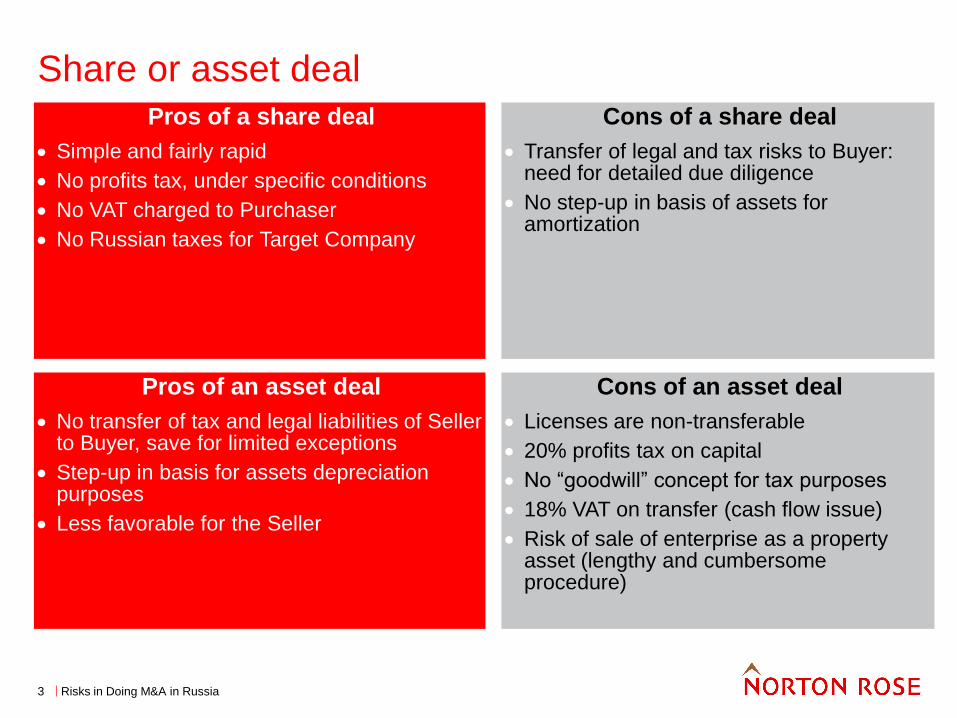

Share or asset deal

Pros of a share deal

Simple and fairly rapid

No profits tax, under specific conditions

No VAT charged to Purchaser

No Russian taxes for Target Company

Cons of a share deal

Transfer of legal and tax risks to Buyer: need for detailed due diligence

No step-up in basis of assets for amortization

Pros of an asset deal

No transfer of tax and legal liabilities of Seller to Buyer, save for limited exceptions

Step-up in basis for assets depreciation purposes

Less favorable for the Seller

Cons of an asset deal

Licenses are non-transferable

20% profits tax on capital

No “goodwill” concept for tax purposes

18% VAT on transfer (cash flow issue)

Risk of sale of enterprise as a property asset (lengthy and cumbersome procedure)

Risks in Doing M&A in Russia 4

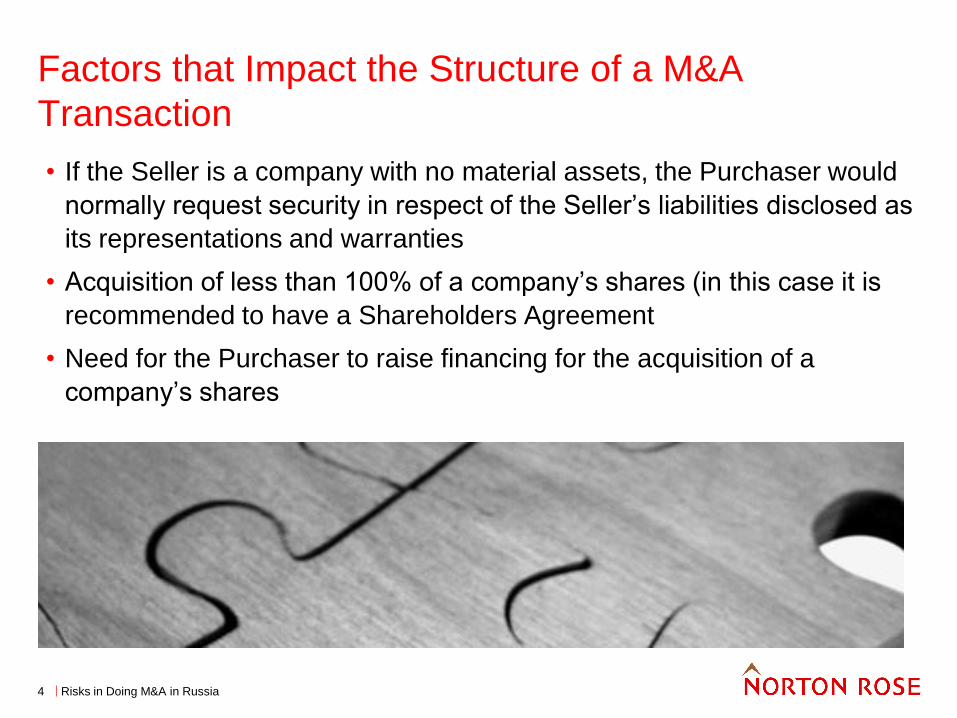

Factors that Impact the Structure of a M&A

Transaction

• If the Seller is a company with no material assets, the Purchaser would

normally request security in respect of the Seller’s liabilities disclosed as

its representations and warranties

• Acquisition of less than 100% of a company’s shares (in this case it is

recommended to have a Shareholders Agreement

• Need for the Purchaser to raise financing for the acquisition of a

company’s shares

Risks in Doing M&A in Russia 5

Typical stages in a buy side M&A process

Illustrative timeline

Weeks 1-2

Phase 1

Initial

contact by

Seller

• Review information memorandum (auction)

• Sign confidentiality agreement/ exclusivity agreement

Weeks 3-4

Phase 2

Indicative

bids

• Communicate indication of interest to Seller

• Prepare for due diligence

• Assess financing alternatives

Weeks 5-9

Phase 3

Buyer due

diligence

• Assemble due diligence team

• Review data room

• Site visit

• Preliminary enquiries

• Attend management presentation

• Verify valuation assumptions

• Review SPA

Weeks 10

Phase 4

Binding bids

• Submit bid letter/ determine final bid terms

• Submit marked-up SPA

• Seller assesses bids

• Obtain preliminary Board approvals

Weeks 11-14

Phase 5

Negotiate

contracts

• Sign exclusivity agreement (if not signed previously)

• Negotiate and sign SPA and other transaction documents

• Secure financing

• Obtain final Board approval

Weeks 15-18

Phase 6

Closing

• Satisfy conditions precedent

• Close transaction

• Post-closing price adjustments filings and other matters

Risks in Doing M&A in Russia 6

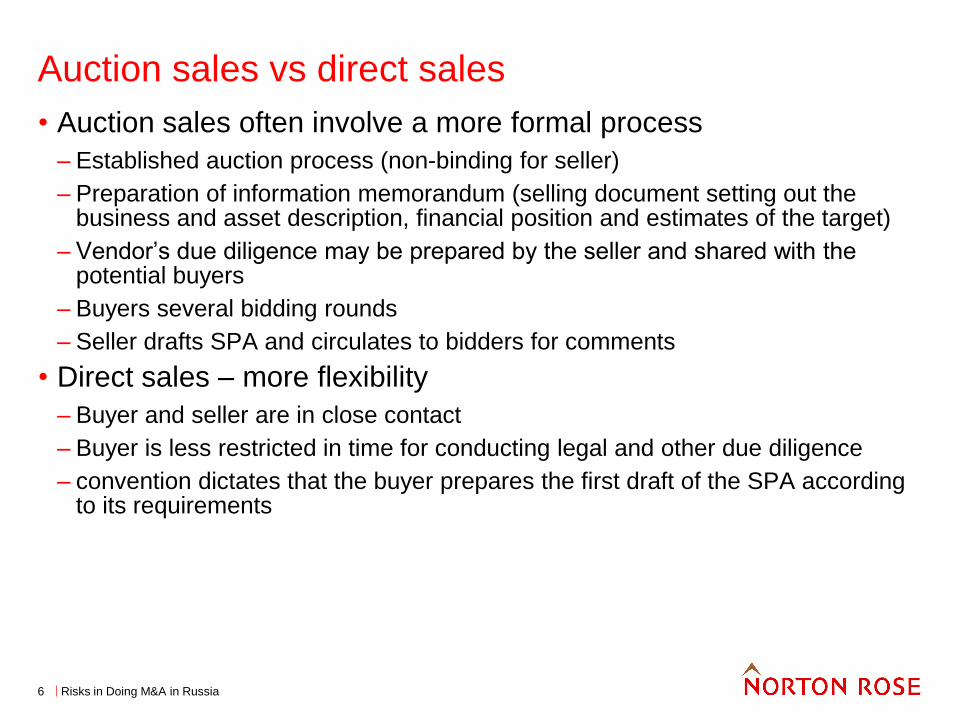

Auction sales vs direct sales

• Auction sales often involve a more formal process

– Established auction process (non-binding for seller)

– Preparation of information memorandum (selling document setting out the business and asset description, financial position and estimates of the target)

– Vendor’s due diligence may be prepared by the seller and shared with the potential buyers

– Buyers several bidding rounds

– Seller drafts SPA and circulates to bidders for comments

• Direct sales – more flexibility

– Buyer and seller are in close contact

– Buyer is less restricted in time for conducting legal and other due diligence

– convention dictates that the buyer prepares the first draft of the SPA according to its requirements

Risks in Doing M&A in Russia 7

Confidentiality agreement/NDA

• An early transaction step

• Usually drafted by Seller

• Buyer obliged to keep all “confidential information” strictly confidential and not disclose

• Negotiation points

– Exclusions from the “confidential information”

– Permitted disclosure

– Validity period (on average 6 months to 5 years)

– Obligations after expiration of the validity period

• Top tip: little to be gained from negotiating too hard

– can spend a lot of time and expense negotiating technical points which are low risk for you (some lawyers love to do this)

– can start you off on the wrong foot in a competitive process

Risks in Doing M&A in Russia 8

Exclusivity

• Prevents seller from talking/engaging with other parties for a specified

period

• Obligations may be incorporated in NDA or heads of terms

• Negotiation points

– Seller to compensate Buyer for time and expense of due diligence etc in

case Seller breaches exclusivity or withdraws from negotiations

Risks in Doing M&A in Russia 9

Buyer’s Due Diligence

Why conduct due diligence?

• To understand the asset to be purchased (buy / not buy)

– Financial, tax and strategic performance

– Legal matters

– Specialised matters (environmental, technical, etc)

• Identify issues

– Can problems be rectified before or after acquisition?

– Deal with the issues by amending terms of the deal, etc:

– Reduce price / hold back / walk away right

– Add indemnities

– Fine-tune seller’s warranties

When conduct due diligence?

• After NDA is signed but before the final version of the SPA is agreed

• After SPA is signed – as needed

Risks in Doing M&A in Russia 10

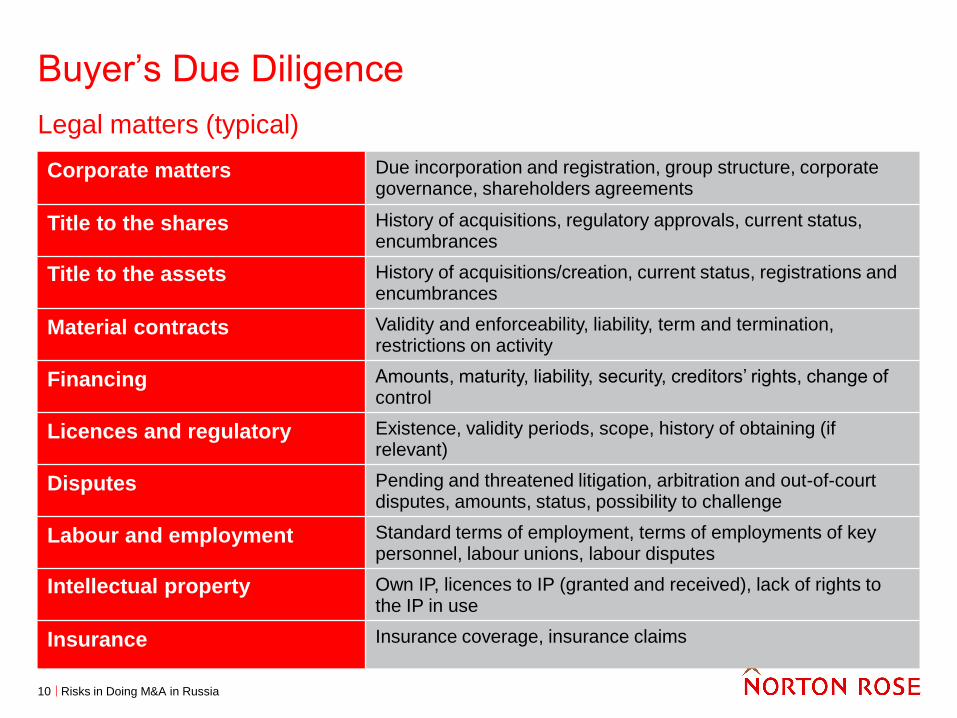

Buyer’s Due Diligence

Legal matters (typical)

Corporate matters Due incorporation and registration, group structure, corporate governance, shareholders agreements

Title to the shares History of acquisitions, regulatory approvals, current status, encumbrances

Title to the assets History of acquisitions/creation, current status, registrations and encumbrances

Material contracts Validity and enforceability, liability, term and termination, restrictions on activity

Financing Amounts, maturity, liability, security, creditors’ rights, change of control

Licences and regulatory Existence, validity periods, scope, history of obtaining (if relevant)

Disputes Pending and threatened litigation, arbitration and out-of-court disputes, amounts, status, possibility to challenge

Labour and employment Standard terms of employment, terms of employments of key personnel, labour unions, labour disputes

Intellectual property Own IP, licences to IP (granted and received), lack of rights to the IP in use

Insurance Insurance coverage, insurance claims

Risks in Doing M&A in Russia 11

Buyer’s Due Diligence

Typical mistakes and problems

• Poorly organised documents and information

• Lack of necessary documents

• No single point of contact/responsible person

• Poorly organised Q&A process and delivery of additional documents

• Lack of qualified specialists

• Too generic (rather than tailor-made) request list

• Extremely wide scope

• Seller’s unfriendly approach

Risks in Doing M&A in Russia 12

Benefits of using English law

• Flexible and convenient deal structure

– Possibility to reflect commercial agreements exactly as agreed

– Conditions precedent and conditions subsequent may depend on the parties

– Price adjustment may be linked to the target’s performance

– Availability of escrow arrangements

– Commonly accepted and well developed structure of transaction documents

• Additional buyer’s protection

– Availability of the seller’s warranties covering the target

– Availability of indemnities

• Predictability of court practice

• Recognition and enforcement of foreign arbitral awards in Russia

Risks in Doing M&A in Russia 13

Points to note when English law is to be chosen

• “Foreign element” is required

– E.g., a foreign counterparty

• Specific performance in Russia is not guaranteed

– Preferably to structure the deal as sale of shares in a foreign company

• Controversial practice of Russian courts on arbitrability of corporate

disputes

Risks in Doing M&A in Russia 14

Structure of the SPA under English law

Common clauses

Clauses in bold are the key operative clauses. Others are “boilerplate” and less heavily negotiated.

1. Parties 9. Confidentiality

2. Definitions and interpretation 10. Waivers/severance/set-off

3. [Conditions precedent] 11. Notices

4. [Pre-completion undertakings] 12. Assignment

5. Completion 13. Counterparts

6. Warranties and indemnities 14. Amendments

7. Claims limitations 15. Governing law and jurisdiction

8. [Non-compete]

Risks in Doing M&A in Russia 15

Conditions precedent

• Typical conditions

– Regulatory consents and approvals

– Corporate approvals

– Financier consents

– Rectification of issues identified through due diligence

– Pre-sale restructuring

– Waivers of the right of first refusal / pre-emptive rights

• Additional risks for the parties

– Circumstances change but the parties are bound to complete

– Ability of a party to withdraw (e.g. no corporate approval is granted)

• Ways to minimise the risks

– Long-stop date

– Pre-completion undertakings

– Repeated warranties

– Buyer’s right to withdraw in case of “material adverse circumstances”

Risks in Doing M&A in Russia 16

Pre-completion undertakings

• Seller undertakings to the buyer to restrict the target’s activity in

the period between exchange and completion

• Typical pre-completion undertakings:

– No activity outside the normal course of business

– No major transactions, no disposal of assets

– No transactions with shares

– No dividends

– No termination or amendment of material contracts

– No shareholders’ meetings

– Buyer to have unrestricted access to the target’s documentation

– etc. as the circumstances may dictate

…unless approved by the Buyer in advance in writing.

Risks in Doing M&A in Russia 17

MAC clauses

• Allows Buyer to walk away if there is a material adverse change

(MAC) in the business between exchange and completion:

– company/business MAC

– general MAC

• Negotiation points

– how to measure/what is “material”?

– distribution of risks in case MAC is not under control of either party

• Rights under MAC clauses are rarely exercised in practice

Risks in Doing M&A in Russia 18

Price adjustment (1)

• Completion accounts

• “Locked box”

• Earn-outs

• Anti-embarrassment

• Retentions and escrow accounts

Risks in Doing M&A in Russia 19

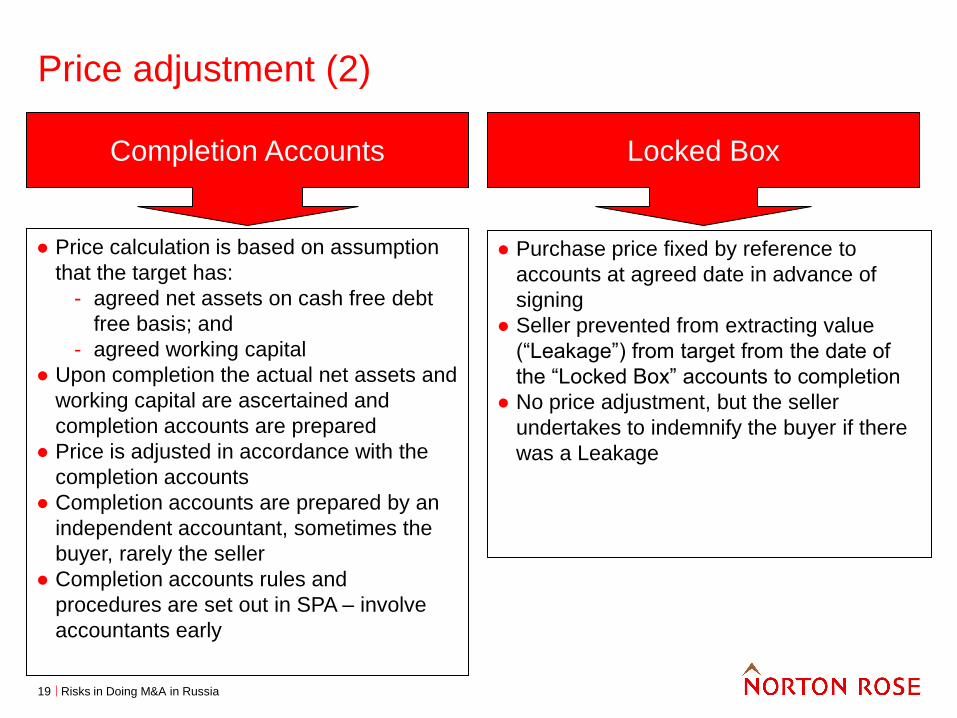

Price adjustment (2)

Completion Accounts Locked Box

● Price calculation is based on assumption

that the target has:

- agreed net assets on cash free debt

free basis; and

- agreed working capital

● Upon completion the actual net assets and

working capital are ascertained and

completion accounts are prepared

● Price is adjusted in accordance with the

completion accounts

● Completion accounts are prepared by an

independent accountant, sometimes the

buyer, rarely the seller

● Completion accounts rules and

procedures are set out in SPA – involve

accountants early

● Purchase price fixed by reference to

accounts at agreed date in advance of

signing

● Seller prevented from extracting value

(“Leakage”) from target from the date of

the “Locked Box” accounts to completion

● No price adjustment, but the seller

undertakes to indemnify the buyer if there

was a Leakage

Risks in Doing M&A in Russia 20

Price adjustment (3)

Earn-out Anti-embarassment

● The parties may not agree the price

● Purchase price is split in two parts: – one part equals to the agreed

(conservative) valuation

– second part is calculated by reference to

future performance

● Second part is payable only if specified

targets are satisfied within specified

periods after completion

● Performance is ascertained by review of

the accounts under agreed procedures

● Performance may be ascertained by an

independent accountant

● Purchase price is increased if the buyer

on-sells the assets at a higher price (i.e.

the seller is protected against being

“embarrassed” by selling cheap)

● Used in case of emergency sales (e.g.

pre-bankruptcy) or where the seller is a

public or state owned company

● Rarely used in Russia

Risks in Doing M&A in Russia 21 21

Pros and cons of Completion Accounts

Pros for the buyer

Ability to true-up. Only pays for what it gets: price will be adjusted if business has deteriorated before completion

Reduces the risks of unidentified issues

Ability to check completion accounts when in full control of business

Cons for the buyer

Extra costs and potential for dispute

Seller can manipulate accounts

Takes economic risk of the business right up to completion

Price may turn to be higher

Pros for the seller

Speed of execution as Buyer may need less comfort on balance sheet before completion. May speed up negotiations

Economic benefit in the business. Gets credit for running the business and receives profits right up until completion

Cons for the seller

Extra costs and potential for dispute

Less control over the completion accounts/adjustment process

Takes economic risk of the business right up to completion

Price may turn to be lower

Risks in Doing M&A in Russia 22 22

Pros and cons of Locked Box

Pros for the buyer

Predictability – price is not adjusted (especially relevant when acquisition is financed)

Cost – no completion mechanism so cost savings

Simplicity – no management time spent debating completion accounts post completion

Cons for the buyer

No completion mechanism to exploit – need to rely on warranties and DD

Risk of business deteriorating between locked box date and completion

Need to debate debt and working capital earlier, with less detailed knowledge

Need a well defined transaction perimeter

Pros for the seller

Gives certainty of price resulting in ability to distribute proceeds quickly

Increases control over process

Hard-wires consistency with previous accounting policies – there is no debate over completion accounts policies pre completion

Simplicity and cost – no management time spent debating completion accounts

Cons for the seller

Price is based on the last accounts and may differ from the current value

Economic benefits are transferred from the accounts date rather than completion date

Risks in Doing M&A in Russia 23 23

Pros and cons of Earn-out

Pros for the buyer

Values target more accurately and protection against overpaying

Defers payment of part of purchase price

Where sellers continue to be involved in business, ties them into business and incentivizes them to maximise profit

Can be used to offset claims under the SPA against the seller

Cons for the buyer

May restrict its control of target – restrictions on Buyer’s ability to make significant changes to Target’s business

Can be detrimental to target in the long term (if seller is managing Target in earn-out period and manipulates business solely to achieve earn-out targets)

Pros for the seller

Possibility of getting higher purchase price than would otherwise have received

Opportunity to benefit from synergies achieved by the Target being integrated with the Buyer’s business

Cons for the seller

Prevents clean break

Potential impact of unforeseen external “shocks”

Makes seller vulnerable to buyer’s actions

Might be used by buyer to offset claims it has under the SPA

Risks in Doing M&A in Russia 24

Use of escrow accounts

Purpose

• Reduce risks if the transfer of shares and payment of purchase price are not simultaneous

• Security for the performance of obligations

– by the buyer to pay deferred part of the purchase price

– by the seller to satisfy buyer’s warranty claims

Use in Russia

• Analogous Russian law concepts do not allow to utilise the full potential of the escrow accounts

• In practice, parties open escrow account with a foreign bank (or foreign escrow agent) and settle payments through that account

Risks in Doing M&A in Russia 25

Buyer and seller’s protections

• Buyer’s protections

– Warranties

– Representations

– Indemnities

• Seller’s protections

– Limitation of liability

– Disclosure

Risks in Doing M&A in Russia 26

Warranties (1)

• Purpose

– Disclosure by the Seller of outstanding tax and other liabilities,

defects, disputes and other tax and legal risks

– Make the Seller financially liable before the Buyer for breach of

warranties

• Structure

– General warranties

– Tax warranties

Risks in Doing M&A in Russia 27

Warranties (2)

• Practical issues

– A tax warranty from a Russian seller is usually only a confirmation

that tax returns have been made in a true and accurate manner

and that tax has been fully paid under these tax returns, rather

than a declaration accepting full responsibility for tax relating to

the pre-completion period

– Tax for the pre-completion period may arise as a result of a post-

completion event i.e. as a result of allocation of revenue under a

multi-period contract

– Tax assessment can be initiated directly by the tax office rather

than by the taxpayer through a tax return, in which case there will

be no technical breach of warranty

Risks in Doing M&A in Russia 28

Questionable Legal Force of Warranties and

Indemnities under Russian Law

• Many Russian sellers are not familiar with the practice of

representation, warranties and indemnities

• Substantial effort required to educate and convince them

• Many Russian sellers are unfamiliar with such concepts which may take

them by surprise at the negotiation stage

• As a result, the SPA discussions will usually take longer than planned

and the position of the buyers on these clauses will be weaker than

initially expected

Risks in Doing M&A in Russia 29

Indemnities

Purpose

To oblige the Seller to indemnify the Buyer, by reimbursing for

a) Tax and other liabilities related to the periods and instances

covered by the SPA prior to the Completion Date (with limited

exceptions), and

b) Associated expenses, including legal fees incurred by the Target

to settle all tax disputes and rectify revealed deficiencies in

connection with additional tax assessments and inspections by

governmental agencies

Risks in Doing M&A in Russia 30

The Changing Face of M&As

• Rationale

– Rationalization of business

– Improvement of liquidities

• Trends

– Disposal of non-core assets & “fast cash” considerations

– Rapidity is key to successful distressed M&A deals

– More non-cash & “hybrid” transactions

– New approach to KPIs (Key Performance Indicators)

Risks in Doing M&A in Russia 31

Financing of a M&A Deal

• Lack of financing for small and medium companies

• Swaps are an alternative to cash in a M&A deal

• Russian M&A market demonstrated increasing interest in non-cash

acquisitions

• Conversion of debt into equity is permitted under Russian law

Risks in Doing M&A in Russia 32

Holdback Amount

The purchase price can be paid / retained in installments (“hold-back”)

– Holdback is normally equal to a percentage of the price

– The price percentage could be paid before the limitation period

expires (i.e. 3 years in Russia)

– In practice, such arrangements are rare and commercially

inconvenient for the Seller

Risks in Doing M&A in Russia 33

Contact Details

Anatoly Andriash

Head of Moscow, Partner

Norton Rose (Central Europe) LLP

White Square Office Center

Ulitsa Butyrsky Val.10, Bldg.A Moscow 125047

Russian Federation

Tel +7 499 924 5101

Fax +7 499 924 5102

Risks in Doing M&A in Russia 34

Disclaimer

The purpose of this presentation is to provide information as to developments in the law. It does not contain a full analysis of the law nor does it constitute an opinion of Norton Rose (Central Europe) LLP on the points of law discussed. No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any constituent part of Norton Rose Group (whether or not such individual is described as a “partner”) accepts or assumes responsibility, or has any liability, to any person in respect of this presentation. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of, as the case may be, Norton Rose LLP or Norton Rose Australia or Norton Rose Canada LLP or Norton Rose South Africa (incorporated as Deneys Reitz Inc) or of one of their respective affiliates.