risk management in financial institutions (ii) 1 risk management in financial institutions (ii):...

Post on 20-Dec-2015

226 views

TRANSCRIPT

Risk Management in Financial Institutions (II) 1

Risk Management in Financial Institutions (II):Hedging with Financial Derivatives

• Forwards

• Futures

• Options

• Swaps

Risk Management in Financial Institutions (II) 2

In April 2006, Bank of America holds $10 million face value treasury bonds. The coupon rate of the bond is 10%, and the bond is sold at par. The bond matures on April 2016. Bank of America worries about its interest rate risk faced in the next year.

Illustrate Fleet’s interest rate risk?

Risk Management in Financial Institutions (II) 3

Forward Contracts

Agreements by two parties to engage in a financial transaction at a future point of time

Risk Management in Financial Institutions (II) 4

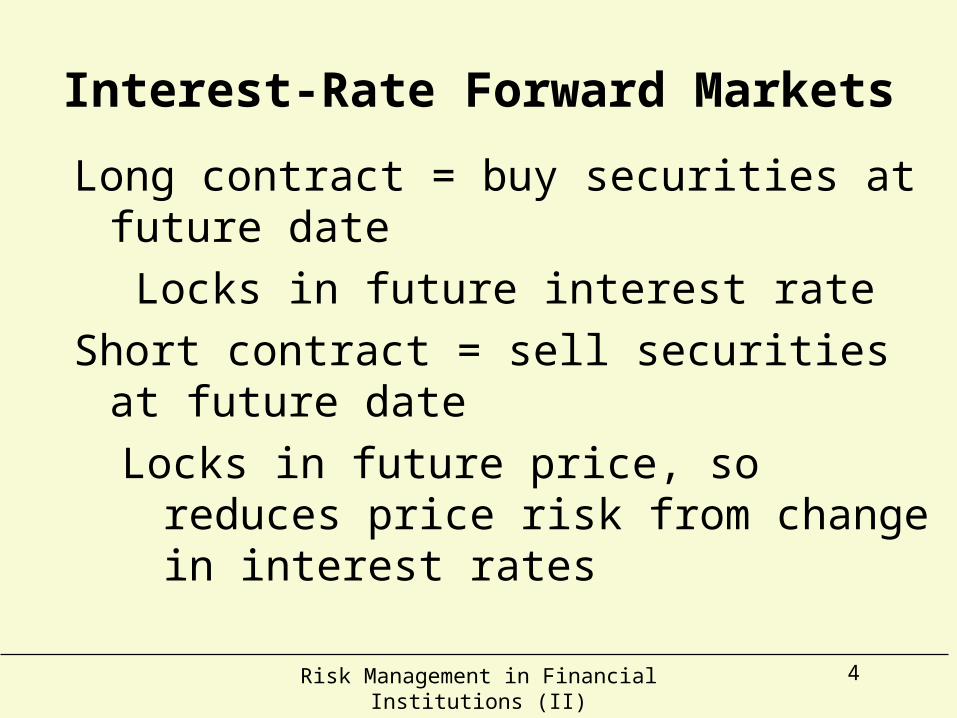

Interest-Rate Forward Markets

Long contract = buy securities at future date

Locks in future interest rate

Short contract = sell securities at future date

Locks in future price, so reduces price risk from change in interest rates

Risk Management in Financial Institutions (II) 5

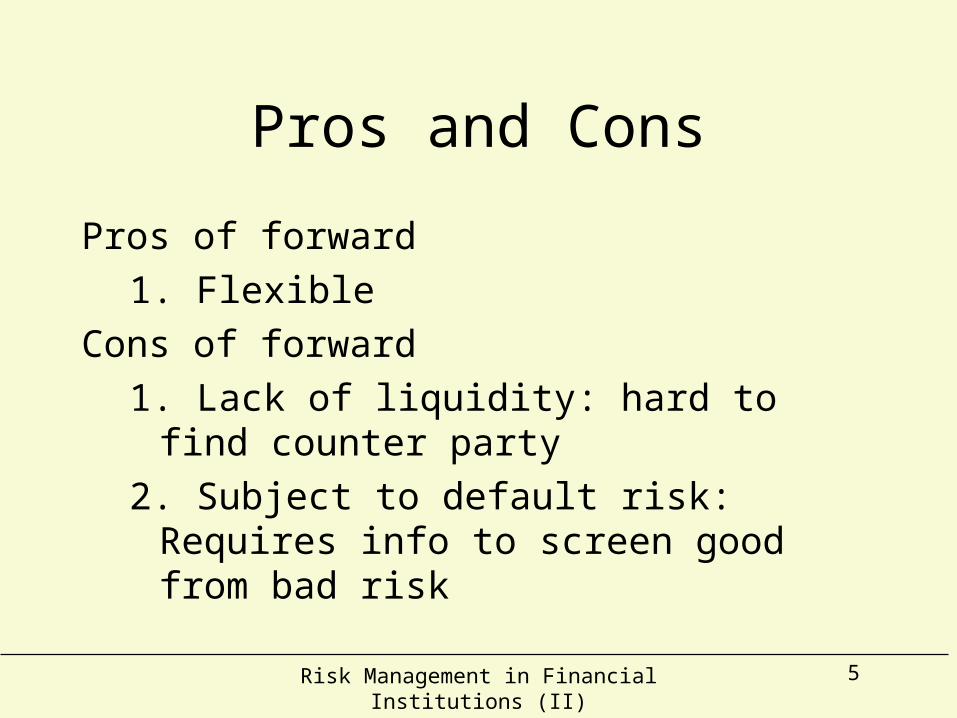

Pros and Cons

Pros of forward

1. Flexible

Cons of forward

1. Lack of liquidity: hard to find counter party

2. Subject to default risk: Requires info to screen good from bad risk

Risk Management in Financial Institutions (II) 6

Financial Futures MarketsTraded on Exchanges: Global competition Regulated by CFTC

Financial Futures Contract

1. Specifies delivery of type of security at future date

2. Arbitrage At expiration date, price of contract = price of the underlying asset delivered

3. i , long contract has loss, short contract has profit

Differences in Futures from Forwards

1. Futures more liquid: standardized, can be traded again, delivery of range of securities

2. Delivery of range prevents corner

3. Mark to market: avoids default risk

4. Don't have to deliver: net long and short

Risk Management in Financial Institutions (II) 7

Bank of America could take a short position in an interest rate forward. Specifically, it shorts/sells the treasury bond to a counterpart in April 2007 (that is 1 year later)) at a price of $10 million (which is today’s bond price).

• 2007/4 is called the settlement date.

• The counterparty could take a long position on this US treasury bonds

Risk Management in Financial Institutions (II) 8

Alternatively, to hedge its interest rate risk, Bank of America could take a short position of $10 million 10% 2006 T- bond futures contract with the settlement date of April/2007 and at a price of $10 million.

The face value for each treasury bond futures contract is $100,000. What is the number of contracts (NC) should be used here?

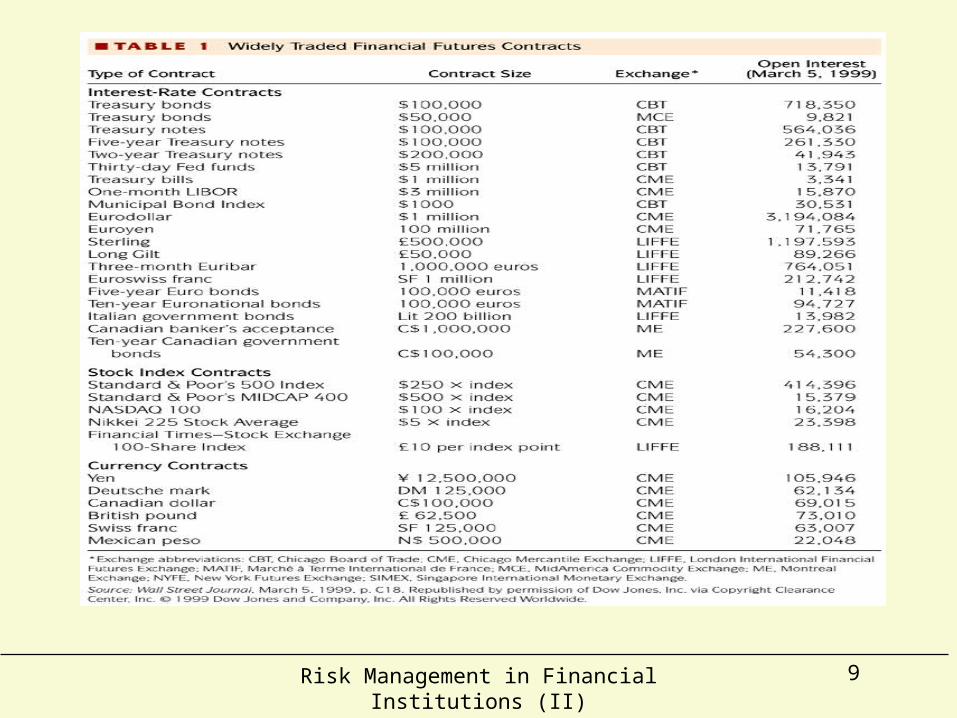

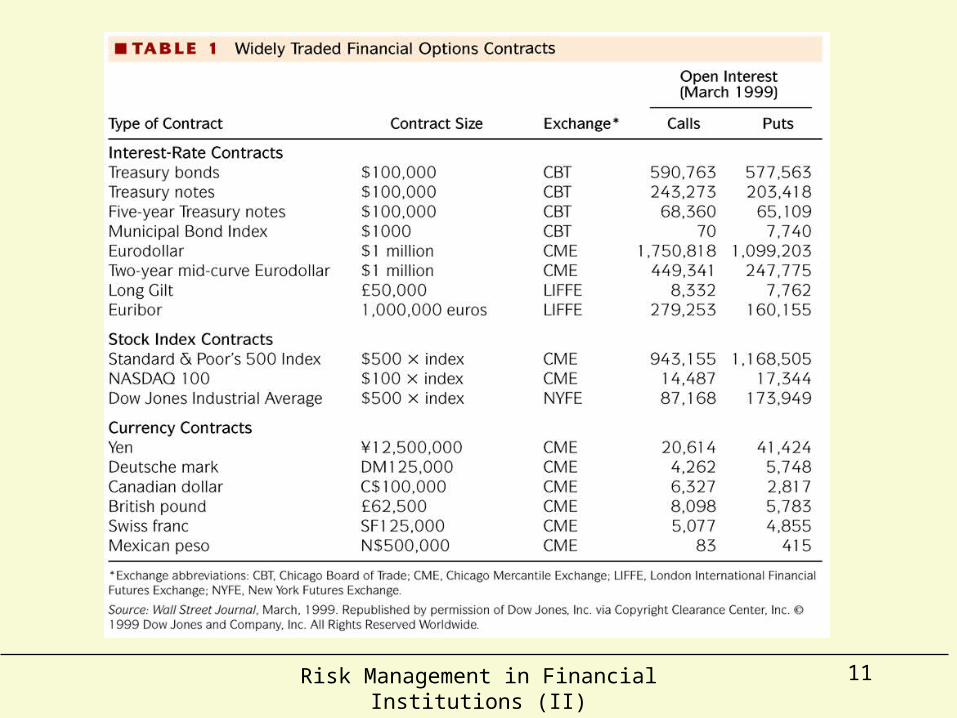

Risk Management in Financial Institutions (II) 9

Risk Management in Financial Institutions (II) 10

Options

Options Contract

Right to buy (call option) or sell (put option) instrument at exercise (strike) price up until expiration date (American) or on expiration date (European)

Risk Management in Financial Institutions (II) 11

Risk Management in Financial Institutions (II) 12

Payoffs of Call option

Risk Management in Financial Institutions (II) 13

Payoff of a put option

Risk Management in Financial Institutions (II) 14

Hedge BOA Risk with Option

What type of option should be applied?

How?

Face value of T-bond option is $100,000. BOA needs to buy 100 contracts of T-bond ____ option here.

Risk Management in Financial Institutions (II) 15

Covered Call – A trading Strategy

Buy Stock and sell a call on the stock.

Risk Management in Financial Institutions (II) 16

Example

Current price of the IBM stock is:

Let’s look at the call option of IBM in ____,

Strike price is ____.

If in ______, the stock price is ____, then the profit from the covered call option is ____; if the stock price is _____, then the profit is _____

Risk Management in Financial Institutions (II) 17

SWAP• SWAPs are financial contracts that obligate

each party to the contract to exchange (swap) a set of payments it owns for another set of payments owned by another party.

• Is a set of forward contracts

• Purpose– Risk management– Get lower cost of capital

Risk Management in Financial Institutions (II) 18

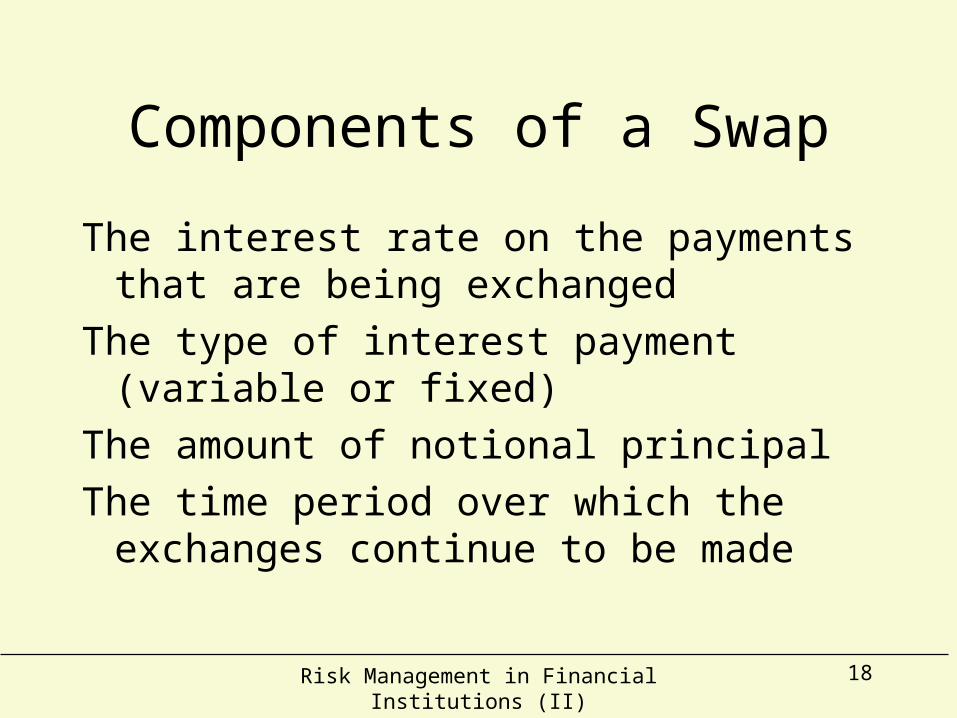

Components of a Swap

The interest rate on the payments that are being exchanged

The type of interest payment (variable or fixed)

The amount of notional principal

The time period over which the exchanges continue to be made

Risk Management in Financial Institutions (II) 19

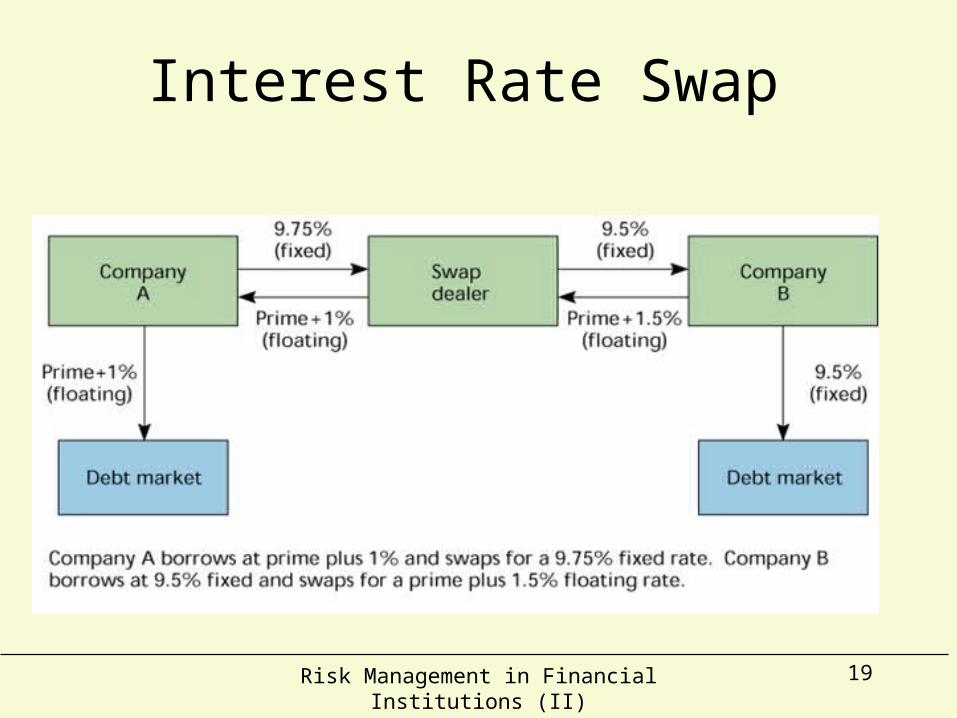

Interest Rate Swap

Risk Management in Financial Institutions (II) 20

Why Engage in SWAP?

• Company A can borrow cheaper with floating rate, while its investment income is mainly fixed rated

• Having an income gap, trying to immunize interest rate risk

Risk Management in Financial Institutions (II) 21

Dangers of Using Derivatives

• Allow financial institutions to increase leverage– Money placed in margin accounts is only a

small portion of the price of futures contracts– Expose banks to large credit risk since holding

of financial derivatives could exceed the amount of bank capital

• Too complicated for most managers– Notional amount versus credit risks