risk americas final brochure

TRANSCRIPT

AMERICA’S PREMIER RISK & REGULATION CONVENTION

RISK AMERICAS 5TH ANNUAL

MAY 3-4, 2016 | HILTON MIDTOWN | NEW YORK CITY

KEYNOTE SESSIONS CRO line up delivering insights into strategic topics including:

The Role of the CRO | Risk Appetite | Risk Management in the Age of Volatility | Machine Learning | National & Global Regulators | Data Quality Analytics

STRESS TESTING & MODEL RISKSenior Stress Testing and Model Risk professionals deliver insights into:

CCAR Overview | CCAR & DFAST | Regulatory Challenges | Data | Sound Model Risk | PPNR Modeling | Model Risk Frameworks

LIQUIDITY RISK & CAPITAL MANAGEMENTNew For 2016 featuring Heads of Department and regulatory bodies discussing:

LCR | NSFR | TLAC | Interest Rate Risk | Basel III Capital Rules | Capital Planning | Lines of Defense

OPERATIONAL RISK New for 2016 featuring Heads of Department and Regulatory Bodies discussing:

Regulatory Agenda | Frameworks | Governance | Compliance | KRIs | Cyber | ERM | Data | RCSA

NICOLAS SILITCH Group CRO

Prudential Financial

MERVYN NAIDOO COO, Risk Analytics

Morgan Stanley

JAMES COSTA CRO

TCF Bank

YURY DUBROVSKY CRO

Lazard Group

JAY COOK CRO

Lloyds Banking GroupNA

PHILIPPA GIRLING CRO

Investors Bank

ANTHONY PECCIA Group CRO

Citibank Canada

JACOB ROSENGARTEN EVP, Chief Enterprise Risk Officer

XL Capital

BOGIE OZDEMIR CRO

Canadian Western Bank

AARON BROWN CRO

AQR Capital

FEDERICO GALIZIA CRO

Inter American Development Bank

CYNTHIA WILLIAMS CRO, Regulatory Coordinator

Credit Suisse

HEAR FROM MORE THAN 70 CROS & HEADS OF RISK INCLUDING:

TOPICS ADDRESSED FOR 2016

www.risk-americas.com | [email protected] | +1 888 677 7007

Co-Sponsors

POST CONVENTION MASTERCLASS - MAY 5PPNR MODELING & SCENARIO SELECTION MASTERCLASS Stress Testing Masterclass with a focus on PPNR Modeling and interactions with other models and Scenario selection for stress testing

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

Welcome to Risk Americas 2016The Center for Financial Professionals are delighted to release the agenda for the 5th Annual Risk Americas Convention taking place May 3-4, 2016, featuring new topics, speakers and venue. We have a new location for 2016, centrally located in Manhattan at The Hilton Midtown, Avenue of the Americas.

Firstly, we would like to thank the Blue Ribbon Panel for their insights, expertise and ongoing support and assistance; Peter Aerni, Bank of America; Patricio Contreras, Morgan Stanley; David D’Amico, MUFG Union Bank NA; Tom Day, PwC; Morgan Stanley and Christian Pichlmeier, Union Bank. The Blue Ribbon Panelists are joined by over 70 senior financial risk professionals to share their insights, case studies and expertise across the two days.

The 2016 Convention will feature two days of extensive discussions, learning and networking with some of the industry’s most highly regarded professionals. The Convention will open on each day with Keynote discussions with CROs and regulatory representatives to discuss the broader, strategic topics, before breaking off into three streams; Stress Testing & Model Risk, Liquidity Risk & Capital Management and Operational Risk. The Convention is designed to deliver a custom made experience. Participants can attend a single stream that will run across both days, or cut across streams to gain broader perspectives, as sessions start and finish at the same time.

The 5th Annual Risk Americas Convention allows for unprecedented networking opportunities, with refreshment breaks across the two days, luncheon roundtable discussions featuring 15+ tables to participate in, allowing for further discussion with industry professionals. Day One will conclude with a networking drinks reception, a perfect opportunity to carry on the discussions of the day in a more informal setting with drinks and canapés served. The Convention will also feature an exhibition hall to interact and discuss with the industry’s top solution providers in areas addressed across the two days.

We look forward to welcoming you to the 5th Annual Risk Americas Convention in May 2016.

Kind Regards

Andreas Simou & Alice Kelly Risk Americas Program Directors, Center for Financial Professionals

[email protected] | [email protected]

www.risk-americas.com | [email protected] | +1 888 677 7007

A NOTE FROM THE EVENT DIRECTORS

2

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

DON’T TAKE OUR WORD FOR IT…Hear what 2015 speakers, sponsors and attendees had to say on the quality of the event…

WHAT’S NEW FOR 2016:

KEYNOTE & PLENARY SESSIONSNEW CRO LINE UP & SESSIONS • Lloyds Banking Group NA, Lazard, PNC and AQR on the role of the CRO • Insights on Risk Management in the Age of Volatility with XL Capital and Morgan Stanley • The Group CRO for Citibank Canada addresses the challenges of machine learning for risk management • Heads of Data from M&T Bank and US Bank on Data Quality Analytics • National and domestic regulatory guidance with CROs from Credit Suisse, Inter American Development Bank, TCF Bank and Investors Bank • Group CRO of Prudential Financial on risk appetite and culture

RETURN OF THE STRESS TESTING & MODEL RISK STREAM • New and improved dedicated stream running across both days • Join industry discussions on a broad range of challenges within Stress Testing and Model Risk with Heads of Departments • Dedicated sessions spreading the focus across both CCAR and DFAST • Extended presentations and panels discussing model risk challenges within stress testing, PPNR modeling, and Model development

NEW FOR 2016: LIQUIDITY RISK & CAPITAL MANAGEMENT • Dedicated Liquidity Risk & Capital Management stream • Heads of Departments, CROs and regulatory bodies review and discuss regulatory changes in the liquidity landscape • Insights and thought leadership on Interest Rate Risk, Market Risk, Basel III, Capital Planning and Modeling

NEW FOR 2016: OPERATIONAL RISK • Dedicated Operational Risk stream addressing a range of challenges with the increased focus and pressure on operational risk professionals • Insights and expert opinion pieces from Citi, US Bank, Deutsche Bank, Bank of America and more • Topics addressed include: Regulatory changes, Vendor Management, Cyber, Data, Governance, Compliance, RCSA and many more

POST CONVENTION MASTERCLASSES Two separately bookable intensive and highly interactive Masterclasses

• New for 2016: Stress Testing Masterclass: PPNR Modeling and Scenario Selection led by Citizens Bank

• Updated for 2016: Model Risk Masterclass: Led by Morgan Stanley with guest presenters

INTERACTIVE AND ENGAGING • Up to 20 Luncheon Roundtables with industry experts to discuss and debate critical industry challenges • More than 65 sessions, across two days, six streams and seven plenary sessions • Increased networking, Q&A and discussion forums • App enabled technology to connect with attendees

Getting bigger and better every year! Vakifbank NY

3

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

CO-SPONSORS

SPONSORSHIP & EXHIBITION

EXHIBITORS

Reduce Spreadsheet Risk

4

AxiomSL’s enterprise-data management platform delivers data lineage, risk aggregation, workflow

automation, validation and audit functionality as well as internal and external reporting capabilities including XBRL. These features provide data and process governance across the entire enterprise and give decision makers the confidence in the automation of complex reporting business logic as well as full control over every step of the process.

AxiomSL’s platform seamlessly integrates all of the firm’s existing data across the enterprise and provides the analytics necessary to meet global regulatory standards, risk management requirements and internal and external reporting demands. The high-performance platform aggregates clients’ data to its lowest level of granularity from multiple siloes systems, enriches and validates the data, and then runs the data through relevant calculations and populates the reports. Analytical applications are delivered in the areas of data risk management, capital and liquidity reporting while addressing evolving regulatory requirements and market dynamics.

CenturyLink (NYSE: CTL) is a global communications, hosting, cloud and IT services company enabling millions of customers to transform their businesses and their lives

through innovative technology solutions. CenturyLink offers network and data systems management, Big Data analytics and IT consulting, and operates more than 55 data centers in North America, Europe and Asia. The company provides broadband, voice, video, data and managed services over a robust 250,000-route-mile U.S. fiber network and a 300,000-route-mile international transport network.

Darling Consulting Group (DCG) is a leading independent provider of balance sheet risk management services and solutions for the financial institution industry. DCG’s Quantitative Risk Analysis & Strategy Group provides specialized end-to-end validation for credit stress testing

models (DFAST/CCAR) which includes an evaluation of the mathematical approaches employed to project credit losses and PPNR forecasts, as well as ALM model integration, governance, controls and documentation.

For over 30 years DCG has helped financial institutions of all sizes make better strategic and risk management decisions. Services include comprehensive asset/liability management and strategy advisory, balance sheet risk modeling, broad-based model validation (e.g. ALM, liquidity, credit, ALLL, MSR,

capital, operational risk models), behavioral studies (deposits, prepayments), credit stress testing and challenger models, and liquidity management (including contingency planning, monitoring and stress testing analytics).

IBM Risk Analytics solutions provide sophisticated risk analytics for quantifying risk exposure to securities and portfolios, as well as for addressing the key regulatory requirements of Basel III, and Solvency II. Financial

services companies on all ve continents have implemented IBM Risk Analytics solutions for a more complete perspective on enterprise risk exposure and for making risk- aware business decisions.

KPMG LLP, the audit, tax and advisory firm, is the U.S. member firm of KPMG International Cooperative (“KPMG International”). KPMG is a global network of professional

firms providing Audit, Tax and Advisory services. We operate in 155 countries and have more than 174,000 people working in member firms around the world. Our high-performing people mobilize around our clients, using our experience and insight to deliver informed perspectives and clear methodologies that our clients and stakeholders value. Our client focus, commitment to excellence, global mind-set, and consistent delivery build trusted relationships that are at the core of our business and reputation.

Microsoft enables financial institutions to liberate data and democratize analytics to empower decision-making across business lines, improve

risk insight, identify new market opportunities, and ultimately fuel future growth. The Microsoft advantage is its highly acclaimed analytics platform, differentiated by its low cost, scale, and simplicity of use. With the elastic compute capability in Microsoft Azure, to enable improved risk modeling, this comprehensive approach enables financial institutions to improve the accuracy and integrity of insight for actuarial, financial, and operational risk.

Moody’s Analytics helps capital markets and risk management professionals worldwide respond to an evolving marketplace with confidence. The company offers unique tools and best practices

for measuring and managing risk through expertise and experience in credit analysis, economic research and financial risk management. By providing leading-edge software, advisory services and research, including proprietary analyses from Moody’s Investors Service, Moody’s Analytics integrates and customizes its offerings to address specific business challenges.

For more than 40 years, MSCI’s research-based indexes and analytics have helped the world’s leading investors build and manage better portfolios.

Clients rely on our offerings for deeper insights into the drivers of performance and risk in their portfolios, broad asset class coverage and innovative research.

Our line of products and services includes indexes, analytical models, data, real estate benchmarks and ESG research. MSCI serves 97 of the top 100 largest money managers, according to the most recent P&I ranking.

Novantas is the industry leader in analytic advisory and solution services for financial institutions. We create superior value for our

clients through deep and insightful analysis of the information that drives the financial services industry — across pricing, product development, treasury and risk management, distribution, marketing, and sales management. Our Global Treasury & Risk unit partners with banks to advance their analytic capabilities — bringing to bear our thought leadership, advanced modeling techniques, and extensive experience.

Risk Focus delivers trading, regulatory, risk and cloud-enabling solutions to the global capital markets. With offices in New York, London

and Riga, Risk Focus offers a full-service model from independent advisory and architecture services through full implementation and solution delivery. Our proprietary software platform, Report-it.Trade, offers component-based regulatory reporting solutions on the cloud or as packaged software, including Validate.Trade, the only data validation and emulation engine for the DTCC GTR.

Since 2004, the world’s top brokers, banks, clearing houses and hedge funds have relied on Risk Focus’ domain expertise and unrivaled track record of on-time delivery for their specialist solutions needs.

Whether complying with regulatory requirements or managing financial transactions, addressing a single key risk, or

working toward a holistic enterprise risk management strategy, Wolters Kluwer Financial Services works with customers worldwide to help them successfully navigate regulatory complexity, optimize risk and financial performance, and manage data to support critical decisions. Wolters Kluwer Financial Services provides risk management, compliance, finance and audit solutions that help financial organizations improve efficiency and effectiveness across their enterprise, with more than 30 offices in 20 countries.

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

Aaron Brown CRO, AQR Capital Aaron is AQR’s Chief Risk Officer, conducting independent oversight and monitoring of the risks assumed by portfolio managers. Prior to AQR, Aaron was an Executive Director in Risk Methodology at Morgan Stanley.

Aaron is also the author of renowed ‘Poker Face of Wall Street’.

Aaron will be joining the Keynote panel discussion on the role of the CRO.

Jay Cook CRO, North America,

Lloyds Banking Group Jay Cook is Chief Risk Officer for North America at Lloyds Banking Group. With over 30 years experience in financial risk, Jay was previously Chief Risk Officer at RBS until 2013.

Jay will be joining the Keynote panel discussion on the role of the CRO.

James Costa CRO, TCF BankJames M. Costa is Chief Risk Officer of TCF Financial Corporation overseeing TCF’s enterprise risk management function. Mr. Costa joined TCF in 2013.

James will be participating on a Keynote panel discussion on regulatory guidance across national and global regulators.

Yury Dubrovsky CRO, Lazard GroupYury Dubrovsky is a Managing Director, Chief Risk Officer of Lazard Ltd. And Head of Global Risk Management at Lazard Asset Management LLC. Prior to joining Lazard in 2015, Yury was Global Head of Market Risk for Emerging Markets and G20 Credit Products with Credit Suisse First Boston.

Yury will be joining the Keynote panel discussion on the role of the CRO.

Philippa Girling, CRO, Investors Bank Philippa Girling is the Chief Risk Officer for Investors Bank, with over 18 years experience in the Global Financial Services industry, within Operational Risk, training, project management and organizational change. Prior to joining Investors Bank, she was Commercial Business Chief Risk officer for Capital One Commercial Bank.

Philippa will be participating on a Keynote panel discussion on regulatory guidance across national and global regulators.

Federico Galizia, CRO, Inter-American Development Bank Federico is the CRO of the Inter-America Development Bank. Before joining the IDB, he served as Head of Risk and Portfolio Management and Chairman of the Investment and Risk Committee at the European Investment Fund in Luxembourg.

Federico will be participating on a Keynote panel discussion on regulatory guidance across national and global regulators.

Bogie Ozdemir, CRO, Canadian Western BankBogie Ozdemir is currently Chief Risk Officer and an Executive Vice President with Canadian Western Bank Group. Prior to joining Canadian Western Bank Group. Bogie held senior positions with Sunlife Financial Group, BMO Financial Group and Standard & Poors.

Bogie will be delivering a presentation on frameworks for capital and business mix optimization.

Anthony Peccia, Group CRO, Citibank CanadaMr. Peccia is Managing Director and CRO for Citibank Canada. He also chairs the Risk Committee and is a Director of Board of the Citi Trust Company of Canada. Prior to this he was MD, Operational Risk at Citigroup.

Anthony will be delivering a Keynote presentation on machine learning for risk management.

Jacob Rosengarten, EVP & Chief Enterprise Risk Officer, XL Capital Jacob Rosengarten was appointed Chief Enterprise Risk Officer for XL Group plc in September, 2008, reporting directly to XL’s CEO. He is also Chairman of XL Group’s Enterprise Risk Committee. Prior to joining XL Group, he was Managing Director of Risk Management and Analytics for Goldman Sachs Asset Management.

Jacob will be delivering a Keynote presentation on risk management in the age of volatility.

Nicholas Silitch, Group CRO, Prudential FinancialNick Silitch is Group Chief Risk Officer of Prudential Financial, Inc. In this role he oversees Prudential’s risk management infrastructure and risk profile across all business lines and risk types. Prior to joining Prudential he held the position of Chief Risk Officer of the Alternative Investment Services, Broker Dealer Services and Pershing businesses within Bank of New York Mellon.

Nick will be delivering a Keynote presentation on Risk Appetite from a CRO’s perspective.

Hear from and interact with over 70 CROs and senior risk executives from the buy and sell side. Below is a sample of the CROs on each day’s Keynotes and Plenary sessions:

Aaron Brown Jay Cook James Costa Yury Dubrovsky Philippa Girling Federico Galizia Bogie Ozdemir Anthony Peccia Jacob Rosengarten Nicholas Silitch

KEYNOTE SPEAKER FACULTY

5

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

SPEAKERS AT RISK AMERICAS 2016

KEYNOTE SESSIONSAaron Brown CRO, AQR Capital Jay Cook CRO, North America, Lloyds Banking Group James Costa CRO, TCF BankYury Dubrovsky CRO, Lazard Group Federico Galizia CRO, Inter-American Development BankPhilippa Girling CRO, Investors Bank Daniel Harty CRO (ALM & Capital Markets), PNC Bank, NAMervyn Naidoo COO, Risk Analytics, Morgan StanleyBogie Ozdemir CRO, Canadian Western BankAnthony Peccia Group CRO, Citibank CanadaJacob Rosengarten EVP & Chief Enterprise Risk Officer, XL Capital Nicholas Silitch Group CRO, Prudential

Kay Vicino Chief Data Officer, US BankCynthia Williams CRO, Regulatory Co-ordinator, Credit SuisseH Walter Young Chief Data & Liquidity Risk Officer, M & T Bank

STRESS TESTING & MODEL RISKPeter Abken VP, Model Risk, Federal Reserve Bank of New York Patricio Contreras Head of Stress Testing Methodology Morgan StanleySerigne Diop CCAR & Stress Testing, HSBCJorge Fonseca Head of Enterprise Stress Testing HSBC SecuritiesKen Fu Senior Vice President, Wells FargoDouglas Gardner MD, Head of Model Risk Management Bank of the WestDavid Ingram Head of Treasury Risk Strategy, Modeling & Policy, Citi Kresimir Marusic MD, CCAR Lead, Deutsche BankTong Peng MD, Wells FargoJulian Phillips Chief Model Risk Officer, GE CapitalManan Rawal SVP, CCAR & Stress Testing, Head of Scenarios & Modelling, HSBCGary Tognoni SVP, Head Stress Testing Execution, Treasury & Balance Sheet Management TD BankSoner Tunay Head of Risk Analytics, Citizens Bank Steve Zhou Director, Stress Testing Methodologies GE Capital

LIQUIDITY RISK & CAPITAL MANAGEMENTMichele Bourdeau Head of Model Risk Management TIAATally Ferguson SVP, Director of Market Risk Management, Bank of Oklahoma Federico Galizia CRO, Inter American Development Bank Michelle Hubertus MD, Basel III US Program Manager Deutsche BankWilliam Kugler Chief Market & Liquidity Risk Officer, Capital OneBogie Ozdemir CRO, Canadian Western Bank Christian Pichlmeier Head of Liquidity Risk, MUFG Union Bank NAMatthieu Royer Head of ALM & CPM, Americas, Credit Agricole CIB Frank Sansone SVP, Treasurer China Construction BankKaren Schneck Market Risk Department Head, Federal Reserve Bank of New YorkJonathan Tholen Liquidity & Capital Oversight, US Bank H Walter Young Chief Data & Liquidity Risk Officer, M&T Bank

OPERATIONAL RISKMaureen Vance Regional Head of Vendor Risk Management Americas, Deutsche BankClarice Carotti Head of Market, Liquidity & Operational Risk Management, Intesa San Paolo New York David D’Amico Director, ERM, MUFG Union Bank NAPhil Gledhill Supervisory Examiner, Operational Risk, Federal Reserve Bank of New YorkDeborah Hrvatin MD, Head of Operational Risk Management, Deutsche BankElizabeth Hughes Director, ERM, Validation & Advance Systems Review, MUFG Union Bank NAAndrew Kramer MD, Operational Risk, TIAAGustavo Ortega Director and Global Head of Issue and Risk Event Management, AIGJodi Richard Chief Operational Risk Officer, US Bank

Excellent speakers, important topics, great ability to switch between streams. BB&T

BRING THE TEAM& SAVE!

3RD COLLEAGUE HALF PRICE

OR 5TH COLLEAGUE GOES FREE

1 2 HALFPRICE

6

AGENDA | MAY 3 | DAY 1 | MORNING

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

STRESS TESTING & MODEL RISK2016 CCAR OVERVIEW PANEL DISCUSSION 11.10 Reviewing And Analyzing The 2016 CCAR Scenarios And Overview Of The Process • Reviewing 2016 tests • Automating the process towards 2017 • Sustainable solutions moving forward • Reviewing the process across different institutionsSoner Tunay, Head of Risk Analytics, Citizens Bank Mircea Pigili, Director, Commercial Risk Ananlytics, SVP, Fifth Third Bank Jonathan West, Managing Director, Novantas

CCAR AND DFAST PROCESSES 11.50 Aligning CCAR & DFAST Stress Tests To Run With Minimal Duplication Of Efforts• Running both stress tests without significant overlaps • Developing systems and tests for specific entity use • Developing bespoke models for CCAR and DFAST to automate the process

Steve Zhou, Director, Stress Testing Methodologies, GE Capital

LIQUIDITY RISK & CAPITAL MANAGEMENT REGULATORY OVERVIEW PANEL DISCUSSION 11.10 An Overview Of The Liquidity Risk Landscape Across Global And National Regulators • Definitions and interpretations across regulators • Influx of changes across liquidity landscape • Reviewing the structure regulators expect across business lines • Application across bordersChristian Pichlmeier, Head of Liquidity Risk, MUFG Union Bank NA Frank Sansone, SVP, Treasurer, China Construction Bank Jonathan Tholen, Liquidity & Capital Oversight, US Bank Moun Seo, Associate Director, Moody’s Ananlytics

11.50 A Look Into The Volcker Rule And The Impact On Non Trading Activity• Impact on banking and trading activities • Contract between spread: Safety and soundness • Effect on ALM, liquidity and treasury • Balance sheet optimization • Effect on both larger and smaller institutions

Tally Ferguson, SVP, Director of Market Risk Management, Bank of Oklahoma

OPERATIONAL RISKCRO OVERVIEW 11.10 Reviewing Regulatory Changes And Overview From A CRO Perspective • Implementing regulatory changes across the board • Senior management and the board • Governance • Challenges to consider in the futureOliver Jacob, International CRO, Mitsubishi UFJ Securities

GOVERNANCE 11.50 Establishing An Effective Governance Structure To Better Account For Operational Risks• Putting the operational risk accountability where it belongs • Ensuring sound governance for escalating operational risks • Moving away from noise while focusing on key risks and controls • Understanding the causes, impacts and value of operational risk managementGustavo Ortega, Director & Global Head of Issue and Risk Event Management, AIG

10.10 MACHINE LEARNING FOR RISK MANAGEMENT Understanding and reviewing the effect of machine learning in risk management, allowing computers to look for what may not be possible for humans.Anthony Peccia, Group CRO, Citibank Canada

8.40 REVIEWING THE ROLE OF THE CRO ACROSS THE INSTITUTION The panelists will discuss their roles with perspectives from different sized institutions. Aaron Brown, CRO, AQR Capital Yury Dubrovsky, CRO, Lazard Group Jay Cook, CRO, Lloyds Banking Group Daniel Harty, CRO, (ALM & Capital Markets), PNC Bank, NA

CRO PANEL DISCUSSION DOUBLE PRESENTATION KEYNOTE ADDRESS9.25 RISK MANAGEMENT IN THE AGE OF VOLATILITY This presentation aspires to explore some of the key drivers that underlie this “Age of Volatility.”Jacob Rosengarten, Executive Vice President & Chief Enterprise Risk Officer, XL Capital Mervyn Naidoo, COO, Risk Analytics, Morgan Stanley

DAY ONE KEYNOTE SESSIONS

10.40 MORNING BREAK & NETWORKING 10.40 MORNING BREAK & NETWORKING 10.40 MORNING BREAK & NETWORKING

7.30 REGISTRATION, COFFEE & BREAKFAST | 8 .30 CHAIR’S OPENING REMARKS

12.25 LUNCH BREAK, NETWORKING & ROUNDTABLE DISCUSSIONS (SEE PAGE 13 FOR L ISTING)

www.risk-americas.com | [email protected] | +1 888 677 7007 7

AGENDA | MAY 3 | DAY 1 | AFTERNOON

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

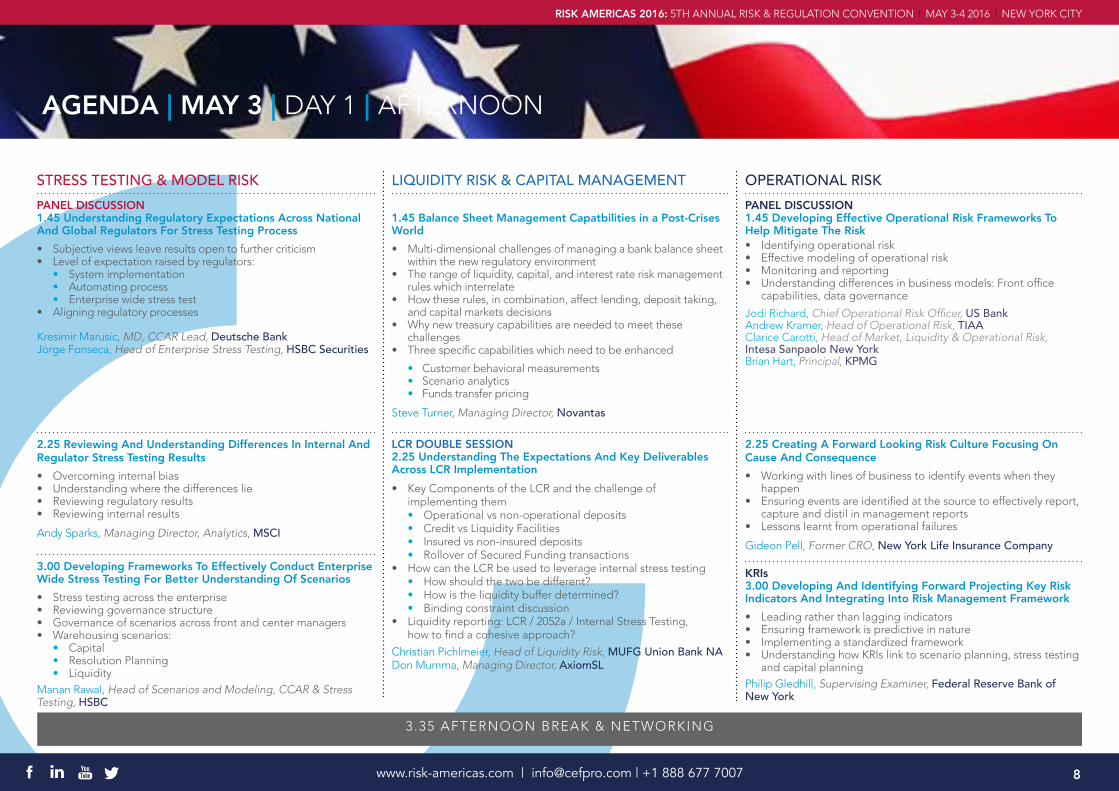

STRESS TESTING & MODEL RISKPANEL DISCUSSION 1.45 Understanding Regulatory Expectations Across National And Global Regulators For Stress Testing Process • Subjective views leave results open to further criticism • Level of expectation raised by regulators: • System implementation • Automating process • Enterprise wide stress test • Aligning regulatory processes

Kresimir Marusic, MD, CCAR Lead, Deutsche Bank Jorge Fonseca, Head of Enterprise Stress Testing, HSBC Securities

2.25 Reviewing And Understanding Differences In Internal And Regulator Stress Testing Results • Overcoming internal bias • Understanding where the differences lie • Reviewing regulatory results • Reviewing internal results

Andy Sparks, Managing Director, Analytics, MSCI

3.00 Developing Frameworks To Effectively Conduct Enterprise Wide Stress Testing For Better Understanding Of Scenarios• Stress testing across the enterprise • Reviewing governance structure • Governance of scenarios across front and center managers • Warehousing scenarios: • Capital • Resolution Planning • LiquidityManan Rawal, Head of Scenarios and Modeling, CCAR & Stress Testing, HSBC

LIQUIDITY RISK & CAPITAL MANAGEMENT 1.45 Balance Sheet Management Capatbilities in a Post-Crises World• Multi-dimensional challenges of managing a bank balance sheet within the new regulatory environment • The range of liquidity, capital, and interest rate risk management rules which interrelate • How these rules, in combination, affect lending, deposit taking, and capital markets decisions • Why new treasury capabilities are needed to meet these challenges • Three specific capabilities which need to be enhanced

• Customer behavioral measurements • Scenario analytics • Funds transfer pricing

Steve Turner, Managing Director, Novantas

LCR DOUBLE SESSION 2.25 Understanding The Expectations And Key Deliverables Across LCR Implementation • Key Components of the LCR and the challenge of implementing them • Operational vs non-operational deposits • Credit vs Liquidity Facilities • Insured vs non-insured deposits • Rollover of Secured Funding transactions • How can the LCR be used to leverage internal stress testing • How should the two be different? • How is the liquidity buffer determined? • Binding constraint discussion • Liquidity reporting: LCR / 2052a / Internal Stress Testing, how to find a cohesive approach?

Christian Pichlmeier, Head of Liquidity Risk, MUFG Union Bank NA Don Mumma, Managing Director, AxiomSL

OPERATIONAL RISKPANEL DISCUSSION 1.45 Developing Effective Operational Risk Frameworks To Help Mitigate The Risk • Identifying operational risk • Effective modeling of operational risk • Monitoring and reporting • Understanding differences in business models: Front office capabilities, data governance

Jodi Richard, Chief Operational Risk Officer, US Bank Andrew Kramer, Head of Operational Risk, TIAA Clarice Carotti, Head of Market, Liquidity & Operational Risk, Intesa Sanpaolo New York Brian Hart, Principal, KPMG

2.25 Creating A Forward Looking Risk Culture Focusing On Cause And Consequence• Working with lines of business to identify events when they happen • Ensuring events are identified at the source to effectively report, capture and distil in management reports • Lessons learnt from operational failures

Gideon Pell, Former CRO, New York Life Insurance Company

KRIs 3.00 Developing And Identifying Forward Projecting Key Risk Indicators And Integrating Into Risk Management Framework • Leading rather than lagging indicators • Ensuring framework is predictive in nature • Implementing a standardized framework • Understanding how KRIs link to scenario planning, stress testing and capital planning Philip Gledhill, Supervising Examiner, Federal Reserve Bank of New York

www.risk-americas.com | [email protected] | +1 888 677 7007

3.35 AFTERNOON BREAK & NETWORKING

8

AGENDA | MAY 3 | DAY 1 | AFTERNOON

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

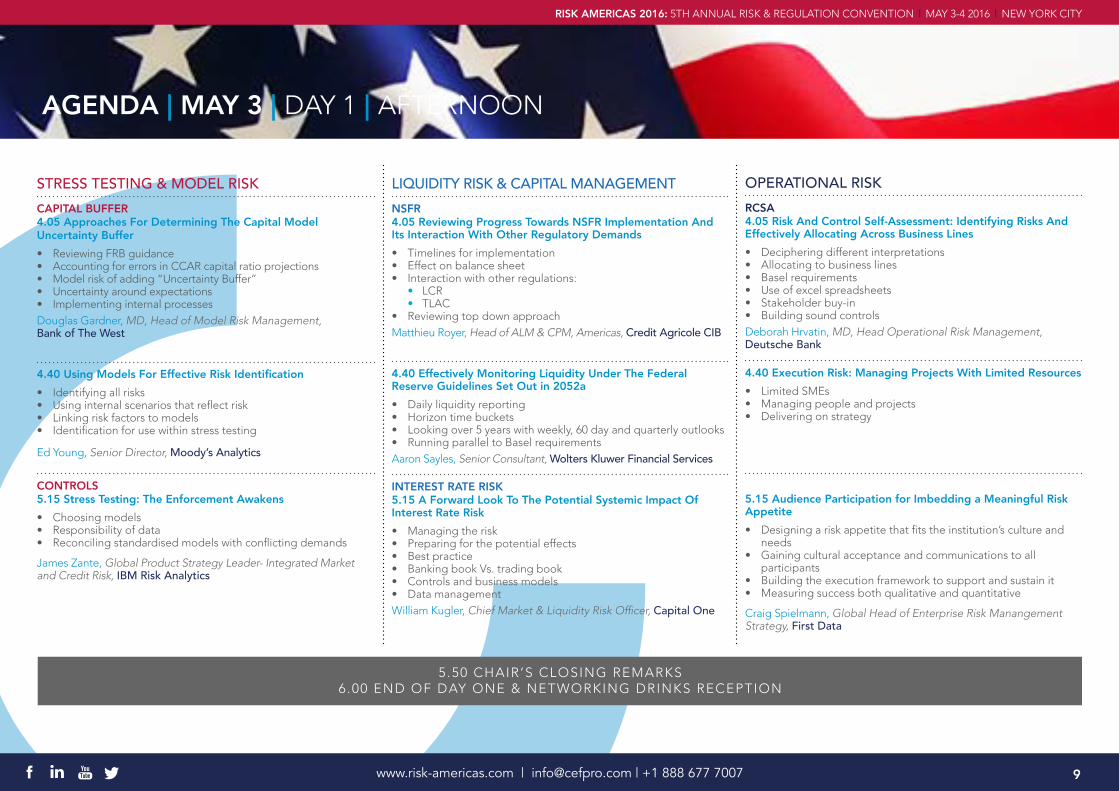

STRESS TESTING & MODEL RISKCAPITAL BUFFER 4.05 Approaches For Determining The Capital Model Uncertainty Buffer • Reviewing FRB guidance • Accounting for errors in CCAR capital ratio projections • Model risk of adding “Uncertainty Buffer” • Uncertainty around expectations • Implementing internal processes Douglas Gardner, MD, Head of Model Risk Management, Bank of The West

4.40 Using Models For Effective Risk Identification • Identifying all risks • Using internal scenarios that reflect risk • Linking risk factors to models • Identification for use within stress testing

Ed Young, Senior Director, Moody’s Analytics

CONTROLS 5.15 Stress Testing: The Enforcement Awakens• Choosing models • Responsibility of data • Reconciling standardised models with conflicting demands

James Zante, Global Product Strategy Leader- Integrated Market and Credit Risk, IBM Risk Analytics

www.risk-americas.com | [email protected] | +1 888 677 7007

5.50 CHAIR’S CLOSING REMARKS 6 .00 END OF DAY ONE & NETWORKING DRINKS RECEPTION

LIQUIDITY RISK & CAPITAL MANAGEMENT NSFR 4.05 Reviewing Progress Towards NSFR Implementation And Its Interaction With Other Regulatory Demands• Timelines for implementation • Effect on balance sheet • Interaction with other regulations: • LCR • TLAC • Reviewing top down approach Matthieu Royer, Head of ALM & CPM, Americas, Credit Agricole CIB

4.40 Effectively Monitoring Liquidity Under The Federal Reserve Guidelines Set Out in 2052a• Daily liquidity reporting • Horizon time buckets • Looking over 5 years with weekly, 60 day and quarterly outlooks • Running parallel to Basel requirementsAaron Sayles, Senior Consultant, Wolters Kluwer Financial Services

INTEREST RATE RISK 5.15 A Forward Look To The Potential Systemic Impact Of Interest Rate Risk • Managing the risk • Preparing for the potential effects • Best practice • Banking book Vs. trading book • Controls and business models • Data management William Kugler, Chief Market & Liquidity Risk Officer, Capital One

OPERATIONAL RISKRCSA 4.05 Risk And Control Self-Assessment: Identifying Risks And Effectively Allocating Across Business Lines• Deciphering different interpretations • Allocating to business lines • Basel requirements • Use of excel spreadsheets • Stakeholder buy-in • Building sound controls Deborah Hrvatin, MD, Head Operational Risk Management, Deutsche Bank

4.40 Execution Risk: Managing Projects With Limited Resources• Limited SMEs • Managing people and projects • Delivering on strategy

5.15 Audience Participation for Imbedding a Meaningful Risk Appetite• Designing a risk appetite that fits the institution’s culture and needs • Gaining cultural acceptance and communications to all participants • Building the execution framework to support and sustain it • Measuring success both qualitative and quantitative

Craig Spielmann, Global Head of Enterprise Risk Manangement Strategy, First Data

9

AGENDA | MAY 4 | DAY 2 | MORNING

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

STRESS TESTING & MODEL RISKSCENARIO ANALYSIS 11.10 Effective Scenario Analysis for CCAR & DFAST• Risk identification process and effective challenge • Alignment of risk identification process with existing BAU practice • Materiality assessment considerations • Scenario creation processEva Chan, Head of Enterprise Stress Testing, Americas, Barclays

11.45 Robust Documentation for Model Risk Management• A discussion of the Purpose, Process and People behind Model Documentation • Purpose: More than a system of record • Process: Beyond filling in a template • People: Finding and developing this skill in your organizationKeith Schleicher, Vice President, Decision Science, CenturyLink Cognilytics

8.40 DATA QUALITY ANALYTICS AND EFFECTIVE RISK MANAGEMENT A View from the CDO on improving data quality for effective management of riskH Walter Young, Chief Data & Liquidity Risk Officer, M&T Bank Kay Vicino, Chief Data Officer, U.S. Bank Jonathan Silverman, Industry Solutions Director, WW Insurance, Microsoft Corp

9.25 ASSESSING THE ROLE AND DEVELOPMENT OF AN EFFECTIVE RISK APPETITE WITHIN A FINANCIAL INSTITUTION: THE VIEW FROM THE CRO Exploring application across frameworks and effects on balance sheet and business linesNicholas Silitch, Group CRO, Prudential Financial

9.55 OVERCOMING CHALLENGES IN REGULATORY GUIDANCE ACROSS NATIONAL AND GLOBAL REGULATORSFederico Galizia, CRO, Inter American Development Bank James Costa, CRO, TCF Bank Philippa Girling, CRO, Investors Bank Cynthia Williams, CRO, Regulatory Coordinator, Credit Suisse

LIQUIDITY RISK & CAPITAL MANAGEMENT

MULTILATERAL DEVELOPMENT BANK 11.10 Exposure Exchange Agreements (EEA) Among MDBs• Why concentration matters for an MDB • How does the EEA reduce concentration • Does the EEA introduce risks of its ownFederico Galizia, CRO, Inter American Development Bank

MULTILATERAL DEVELOPMENT BANK 11.45 Risk Technology - Demystified• Complexities around Enterprise Risk Technology • Pre-Crisis (2008) Risk Manager use case • Business User’s need for control • Singular Focus – The Business user • Simple yet scalable architectures • Liquidity Risk example

Srikant Ganesan, Managing Partner, Risk Focus

OPERATIONAL RISK11.10 Outsourcing Governance, Monitoring And Risk Management • Vendor portfolio analysis • Internal sourcing validation and governance • Straight through processing • Control function review process • Cross functional risk calibration • Behavioral analytics and dynamic decisioning • Escalating and reporting Maureen Vance, Regional Head of Vendor Risk Management Americas, Deutsche Bank

11.45 Introduction To The National Cybersecurity & Communications Integration centre (NCCIC)• Federal cybersecurity• Authorities and directives• Cybersecurity coordination activities• Incident reporting• Protection of information• Strengthening the cyber and communications ecosystem for the futureThomas Baer, Deputy Director, National Cybersecurity & Communications Integration Center, US Department of Homeland Security

10.40 MORNING BREAK & NETWORKING 10.40 MORNING BREAK & NETWORKING 10.40 MORNING BREAK & NETWORKING

www.risk-americas.com | [email protected] | +1 888 677 7007

12.20 LUNCH BREAK, NETWORKING & ROUNDTABLE DISCUSSIONS (SEE PAGE 13 FOR L ISTING)

DAY TWO KEYNOTE SESSIONS

8.00 REGISTRATION, COFFEE & BREAKFAST | 8 .30 CHAIR’S OPENING REMARKS

DATA PANEL DISCUSSION KEYNOTE ADDRESS REGULATORY PANEL DISCUSSION

10

AGENDA | MAY 4 | DAY 2 | AFTERNOON

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

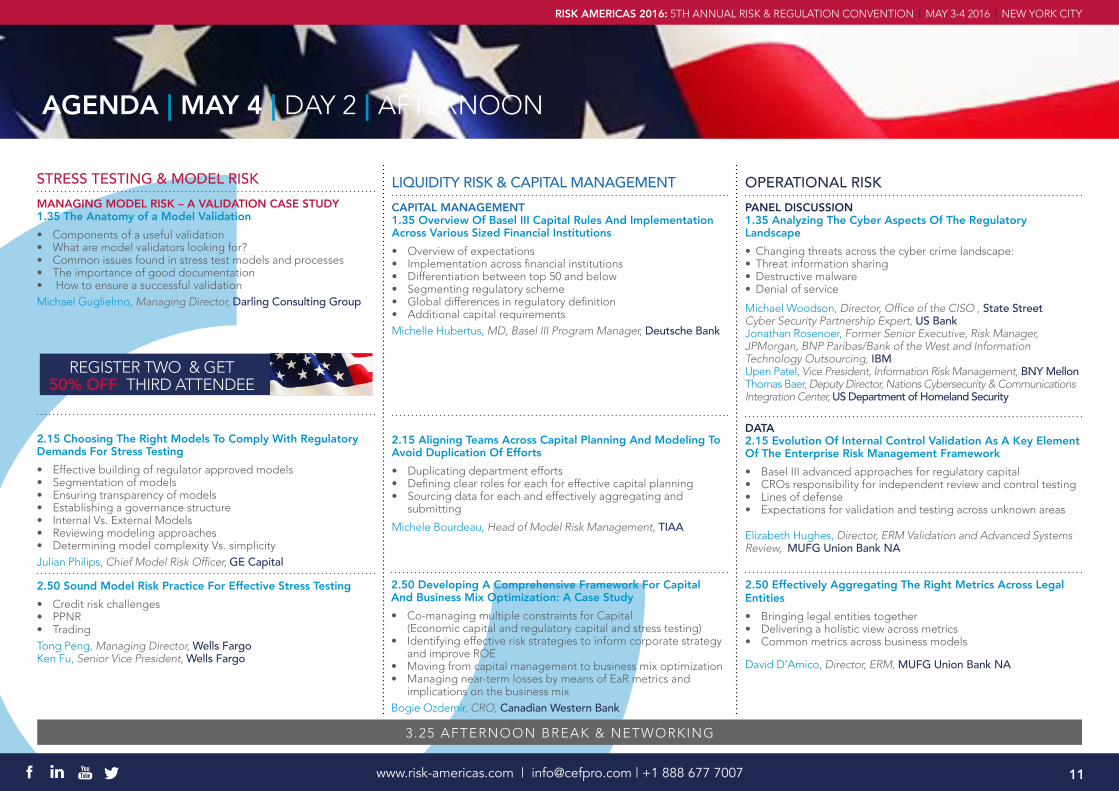

LIQUIDITY RISK & CAPITAL MANAGEMENT CAPITAL MANAGEMENT 1.35 Overview Of Basel III Capital Rules And Implementation Across Various Sized Financial Institutions• Overview of expectations • Implementation across financial institutions • Differentiation between top 50 and below • Segmenting regulatory scheme • Global differences in regulatory definition • Additional capital requirementsMichelle Hubertus, MD, Basel III Program Manager, Deutsche Bank

2.15 Aligning Teams Across Capital Planning And Modeling To Avoid Duplication Of Efforts• Duplicating department efforts • Defining clear roles for each for effective capital planning • Sourcing data for each and effectively aggregating and submitting

Michele Bourdeau, Head of Model Risk Management, TIAA

OPERATIONAL RISKPANEL DISCUSSION 1.35 Analyzing The Cyber Aspects Of The Regulatory Landscape• Changing threats across the cyber crime landscape: • Threat information sharing • Destructive malware • Denial of service

Michael Woodson, Director, Office of the CISO , State Street Cyber Security Partnership Expert, US Bank Jonathan Rosenoer, Former Senior Executive, Risk Manager, JPMorgan, BNP Paribas/Bank of the West and Information Technology Outsourcing, IBM Upen Patel, Vice President, Information Risk Management, BNY Mellon Thomas Baer, Deputy Director, Nations Cybersecurity & Communications Integration Center, US Department of Homeland Security

DATA 2.15 Evolution Of Internal Control Validation As A Key Element Of The Enterprise Risk Management Framework• Basel III advanced approaches for regulatory capital • CROs responsibility for independent review and control testing • Lines of defense • Expectations for validation and testing across unknown areas

Elizabeth Hughes, Director, ERM Validation and Advanced Systems Review, MUFG Union Bank NA

3.25 AFTERNOON BREAK & NETWORKING

2.50 Developing A Comprehensive Framework For Capital And Business Mix Optimization: A Case Study • Co-managing multiple constraints for Capital (Economic capital and regulatory capital and stress testing) • Identifying effective risk strategies to inform corporate strategy and improve ROE • Moving from capital management to business mix optimization • Managing near-term losses by means of EaR metrics and implications on the business mix Bogie Ozdemir, CRO, Canadian Western Bank

2.50 Effectively Aggregating The Right Metrics Across Legal Entities• Bringing legal entities together • Delivering a holistic view across metrics • Common metrics across business models

David D’Amico, Director, ERM, MUFG Union Bank NA

STRESS TESTING & MODEL RISKMANAGING MODEL RISK – A VALIDATION CASE STUDY 1.35 The Anatomy of a Model Validation• Components of a useful validation • What are model validators looking for? • Common issues found in stress test models and processes • The importance of good documentation • How to ensure a successful validationMichael Guglielmo, Managing Director, Darling Consulting Group

2.15 Choosing The Right Models To Comply With Regulatory Demands For Stress Testing• Effective building of regulator approved models • Segmentation of models • Ensuring transparency of models • Establishing a governance structure • Internal Vs. External Models • Reviewing modeling approaches • Determining model complexity Vs. simplicity Julian Philips, Chief Model Risk Officer, GE Capital

2.50 Sound Model Risk Practice For Effective Stress Testing • Credit risk challenges • PPNR • Trading Tong Peng, Managing Director, Wells Fargo Ken Fu, Senior Vice President, Wells Fargo

11

REGISTER TWO & GET 50% OFF THIRD ATTENDEE

AGENDA | MAY 4 | DAY 2 | AFTERNOON

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

5.05 CHAIR’S CLOSING REMARKS | 5 .10 END OF CONVENTION

STRESS TESTING & MODEL RISKPPNR MODELING 3.55 Addressing The Challenges, Pitfalls And Opportunities For Effective PPNR Modeling• Terms and concepts • PPNR and interaction with CCAR/DFAST • Regulatory requirements • Association with other models David Ingram, Head of Treasury Risk Strategy, Modeling & Policy, Citi

PANEL DISCUSSION 4.30 Review Outcomes of The PPNR PresentationGary Tognoni, Head of Stress Testing Execution, Treasury and Balance Sheet Management, TD Bank Serigne Diop, CCAR & Stress Testing, HSBC David Ingram, Head of Treasury Risk Strategy, Modeling & Policy, Citi Tom Day, Managing Director, PwC

LIQUIDITY RISK & CAPITAL MANAGEMENT 3.55 Reviewing The Roles of The Lines of Defense • Reviewing the roles of each line • How each line works • Reviewing The Roles of The Lines of Defense • Review of the fourth line

Jonathan Tholen, Liquidity & Capital Oversight, US Bank

4.30 Improving Data To Optimize The Balance Sheet And Improve Earnings • Using data as a tool • Sourcing necessary data • Improving data

H Walter Young, Chief Data & Liquidity Risk Officer, M&T Bank

OPERATIONAL RISKDOUBLE SESSION 3.55 Operational Risk Scenario Analysis: A Structured Approach

• Operational risk overview • Quantifying operational risk: approaches and supervisory guidance • Scenario analysis: traditional vs. structured • Structured scenario analysis: approach, illustration, lessons learned be a value-add for managing risk?

Andrew Kramer, MD, Operational Risk, TIAA

Karthik Ramakrishnan, Senior Manager, EY

12

4.30 Developing A Comprehensive Framework For Capital And Business Mix Optimization: A Case Study • Co-managing multiple constraints for Capital (Economic capital and regulatory capital and stress testing) • Identifying effective risk strategies to inform corporate strategy and improve ROE • Moving from capital management to business mix optimization • Managing near-term losses by means of EaR metrics and implications on the business mix Bogie Ozdemir, CRO, Canadian Western Bank

AGENDA | ROUNDTABLES

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

DAY ONE | MAY 3 | ROUNDTABLE DISCUSSIONS | 1.00-1.45 DAY TWO | MAY 4 | ROUNDTABLE DISCUSSIONS | 1.00-1.45

Lunch on both days will feature an opportunity to engage with like-minded professionals, enjoy a buffet lunch, visit the exhibitors and participate on one of the interactive roundtable discussions. During the course of the two day Convention, there will be 20 luncheon roundtables to chose from; below is a sample of some of the topics and moderators for each. All attendees will be asked prior to the Convention to select their preference.

Preparedness for EPS Liquidity

Requirements For Foreign Banking Organizations

Christian Pichlmeier Head of Liquidity Risk

Union Bank

The Challenges and Rewards For Documenting

Operational Risk Events Gustavo Ortega

Director and Global Head of Issue and Risk Event

Management AIG

Essential Skills For Model Risk

Management & Model Validation Professionals

Karen Schneck VP, Market Risk Department

Federal Reserve Bank of New York

CCAR – When Does Change The Bank

Become Run The Bank? Michelle Hubertus

MD, Basel III Program Manager

Deutsche Bank

Interest Rate Risk and ALM in Stress

Scenarios: Exploring Methods And Processes

Gary Tognoni Head of Stress Testing Execution, Treasury &

Balance Sheet Management

TD Bank

Risk Management Of Liquid Alternative

Products Aaron Brown

CROAQR Capital

Managing Models in Complex Organizationals

– Value Add or Just a Compliance Exercise

Sanjeev Mankotia Managing Director,

Risk Consulting

KPMG

Measuring and Managing Model Dependency Risk

Tong Peng Managing Director

Wells Fargo

The AMA Is Dead: Now What?

Anthony Peccia Group CRO

Citibank Canada

Sustainable Enterprise Risk Management Elizabeth Hughes

Director, ERM Validation & Advanced Systems Review

MUFG Union Bank NA

Economic and Financial Challenges in

Latin America Frederico Galizia

CRO

Inter-America Development Bank

How have you achieved success in your

Vendor Risk Management function and what do you do

differently? Maureen Vance

Director / Regional Head of Vendor Risk Management

Americas

Deutsche Bank

Can We Achieve Economic and

Environmental Sustainability in the

Next 30 Years? Mervyn Naidoo

CRO, Risk Analytics

Morgan Stanley

Finding Value in DFAST Beyond

Regulatory RequirementsTally Ferguson

SVP, Director of Market Risk Management

Bank of Oklahoma

Improving ROE Via Capital & Business

Mix Optimization & Effective Balance Sheet

Management Bogie Ozdemir

CRO

Canadian Western Bank

13

STRESS TESTING MASTERCLASS | MAY 5RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

STRESS TEST – NEW MODELING AND CAPITAL MANAGEMENT PARADIGM • A short history of Stress Test as a bank capital management tool • Comparison to Basel rules and modeling approach • How Stress Testing is compared to Economic Capital

HIGHLIGHTS OF THE CCAR RESULTS• Lessons learned • Regulatory expectations • Priorities for a bank preparing for CCAR submission

APPLICATIONS OF STRESS TESTING IN BANKS• Risk appetite • Capital adequacy • Portfolio allocation and pricing

SCENARIO DESIGN AND DEVELOPMENT FOR SUCCESSFUL STRESS TESTING • Risk identification • Key risk drivers and key macro variables to capture in modeling • Scenario extension • Use of macroeconomic models in scenario design and expansion • Determining the severity of scenarios • Linking scenario severity to capital adequacy

INTRODUCTION TO CREDIT LOSS MODELING• Available alternatives in modeling consumer portfolio • Empirical review of alternatives currently available in the literature • A walk through the applications in commercial portfolios • Comparative analysis of each alternatives in the literature

PPNR MODELING• Review of terms and concepts • CCAR results in PPNR and relevance to capital adequacy • Introduction to PPNR modeling with examples • Regulatory expectations • Connecting PPNR with credit modeling for an integrated Stress Testing framework

APPLICATIONS OF STRESS TESTING FRAMEWORK IN PORTFOLIO MANAGEMENT• Hands on exercises • Product origination strategies • Pricing considerations • Risk/return trade off • Linking Stress Test results to risk appetite and risk taking

The Masterclass will be led by industry expert Soner Tunay, Head of Risk Analytics, Citizens Bank who will lead the day’s agenda with presentations, case studies and group discussions.

The Masterclass will address challenges within Stress Testing with a particular focus on PPNR Modeling, Scenario Selection and Analysis.

Join like-minded colleagues to discuss new modeling techniques, CCAR results, application in banks, scenario designs and development, credit

loss modeling, PPNR modeling, and applications of stress testing on portfolio management.

Registration opens at 9AM with breakfast, Masterclass commences at 9:30AM, concluding at 5PM. There will be adequate time for refreshments, networking and lunch.To allow for interaction and discussion, seats at the Masterclass are strictly limited – to avoid disappointment, reserve your place today!

OUTLINE FOR THE STRESS TESTING MASTERCLASS

Led By: Soner Tunay, Head of Risk Analytics, Citizens BankABOUT THE MASTERCLASS

Loved 2014, higher expectations for 2015, so far so good! Microsoft

14

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

ESSENTIAL INFORMATION

Great range of coverage of areas of financial services industry risk, perspectives of many types not necessarily expected. Federal Reserve Bank of Boston

VENUENew York Hilton Midtown1335 Avenue of the AmericasNew York CityNew York 10019 USA Tel: 212-586-7000

ACCOMMODATION The Center for Financial Professionals have reserved a limited number of rooms at a preferential rate for Risk Americas 2016 attendees. Rooms are subject to availability and on a first come, first served basis.

Please click the link below for booking information. Risk Americas Convention 2016 Accomodation

DRESS CODE Business Attire

RISK INSIGHTSStay up to date on latest news, views, articles and Q&As from presenters at Risk Americas 2016. To stay up to date visit the event website at www.risk-americas.com

EARN UP TO 24 CPE CREDITSPrerequisites: Knowledge of financial risk management Advanced Preparation: No advanced preparation is required Program Level: Intermediate to advanced Delivery Method: Group-live

The Center for Financial Professionals is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.learningmarket.org

Attendees can earn up to 16.5 CPE Credits for the Main Convention (May 3-4), up to 7.5 CPE Credits for the Stress Testing Masterclass (May 5) or up to 7.5 CPE Credits for the Model Risk Masterclass (May 5)

www.risk-americas.com | [email protected] | +1 888 677 7007 16

LUNCHEON ROUNDTABLESJoin one of up to 20 roundtable discussions to further engage, discuss and interact with peers on topical issues within the industry.

COCKTAIL RECEPTIONImmediately following the end of day one, there will be a drinks reception to wrap up the first day. Unwind in a more informal setting with drinks and canapés to carry on the days discussions with colleagues and peers.

BRIEFINGSClosed-door briefings will be held with like-minded professionals (By Invitation Only), numbers are limited to bring together more intimate groups to discuss key subject matters. If you would like more information, or the opportunity to host a Briefing, contact us at [email protected]

NETWORKING Ample networking opportunities are available throughout the two days; breakfast, lunch and refreshments will also be served across both days to allow for further discussion and networking. Complementing the Luncheon Roundtables, Briefings and Drinks Reception.

TECHNOLOGY Be sure to bring a cellphone, tablet or laptop to make the most of our technology benefits at the event. Attendees can interact through electronic devices with Chair, Panelists and Presenters by sending questions related to the session.

RISK AMERICAS APP Two weeks prior to the Convention, you can access the Risk Americas App for the latest Insights, speaker Q&As, see who’s attending, view presentation, message attendees and more…

NETWORKING OPPORTUNITIES AT RISK AMERICAS 2016

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

www.risk-americas.com | [email protected] | +1 888 677 7007

RA

17

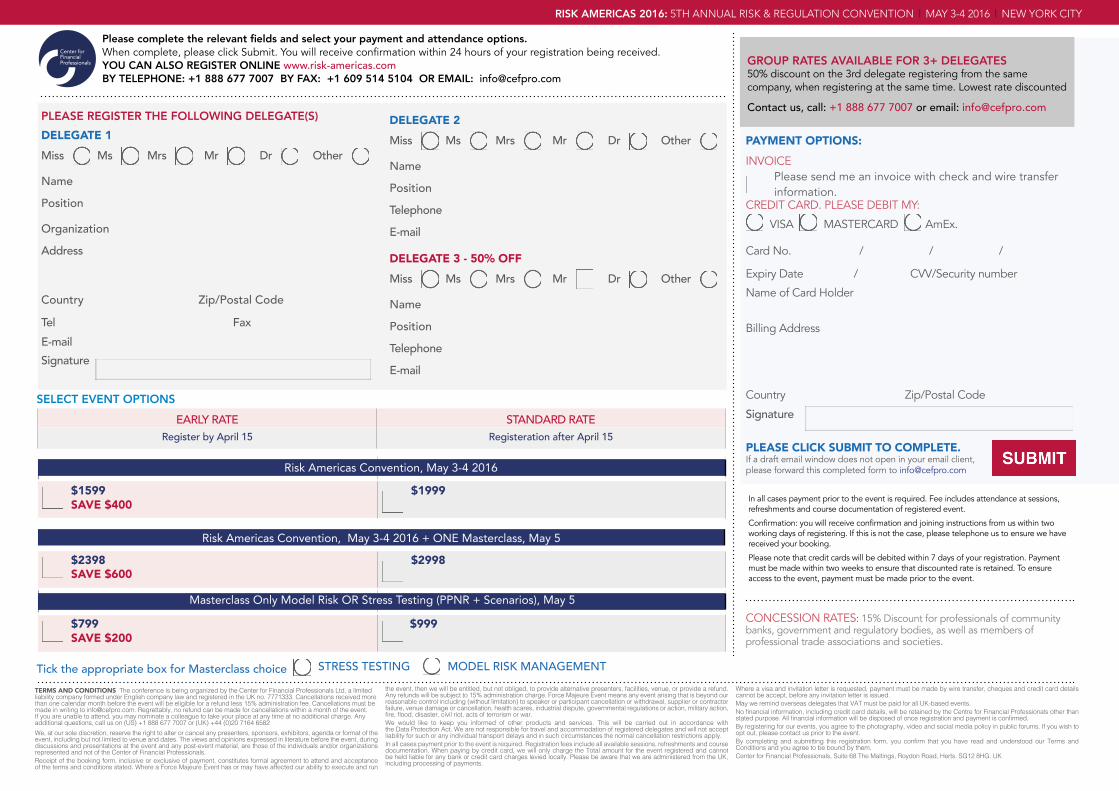

Tick the appropriate box for Masterclass choice STRESS TESTING MODEL RISK MANAGEMENT

RISK AMERICAS 2016: 5TH ANNUAL RISK & REGULATION CONVENTION | MAY 3-4 2016 | NEW YORK CITY

PLEASE REGISTER THE FOLLOWING DELEGATE(S) DELEGATE 1Miss Ms Mrs Mr Dr Other

Name

Position

Organization

Address

Country Zip/Postal Code

Tel Fax E-mail Signature

DELEGATE 2Miss Ms Mrs Mr Dr Other

Name

Position

Telephone

DELEGATE 3 - 50% OFFMiss Ms Mrs Mr Dr Other

Name

Position

Telephone

TERMS AND CONDITIONS The conference is being organized by the Center for Financial Professionals Ltd, a limited

liability company formed under English company law and registered in the UK no. 7771333. Cancellations received more

than one calendar month before the event will be eligible for a refund less 15% administration fee. Cancellations must be

made in writing to [email protected]. Regrettably, no refund can be made for cancellations within a month of the event.

If you are unable to attend, you may nominate a colleague to take your place at any time at no additional charge. Any

additional questions, call us on (US) +1 888 677 7007 or (UK) +44 (0)20 7164 6582

We, at our sole discretion, reserve the right to alter or cancel any presenters, sponsors, exhibitors, agenda or format of the

event, including but not limited to venue and dates. The views and opinions expressed in literature before the event, during

discussions and presentations at the event and any post-event material, are those of the individuals and/or organizations

represented and not of the Center of Financial Professionals.

Receipt of the booking form, inclusive or exclusive of payment, constitutes formal agreement to attend and acceptance

of the terms and conditions stated. Where a Force Majeure Event has or may have affected our ability to execute and run

the event, then we will be entitled, but not obliged, to provide alternative presenters, facilities, venue, or provide a refund.

Any refunds will be subject to 15% administration charge. Force Majeure Event means any event arising that is beyond our

reasonable control including (without limitation) to speaker or participant cancellation or withdrawal, supplier or contractor

failure, venue damage or cancellation, health scares, industrial dispute, governmental regulations or action, military action,

fire, flood, disaster, civil riot, acts of terrorism or war.We would like to keep you informed of other products and services. This will be carried out in accordance with

the Data Protection Act. We are not responsible for travel and accommodation of registered delegates and will not accept

liability for such or any individual transport delays and in such circumstances the normal cancellation restrictions apply.

In all cases payment prior to the event is required. Registration fees include all available sessions, refreshments and course

documentation. When paying by credit card, we will only charge the Total amount for the event registered and cannot

be held liable for any bank or credit card charges levied locally. Please be aware that we are administered from the UK,

including processing of payments.

Where a visa and invitation letter is requested, payment must be made by wire transfer, cheques and credit card details

cannot be accept, before any invitation letter is issued.

May we remind overseas delegates that VAT must be paid for all UK-based events.

No financial information, including credit card details, will be retained by the Centre for Financial Professionals other than stated purpose. All financial information will be disposed of once registration and payment is confirmed.By registering for our events, you agree to the photography, video and social media policy in public forums. If you wish to

opt out, please contact us prior to the event.

By completing and submitting this registration form, you confirm that you have read and understood our Terms and Conditions and you agree to be bound by them.

Center for Financial Professionals, Suite 68 The Maltings, Roydon Road, Herts. SG12 8HG. UK

In all cases payment prior to the event is required. Fee includes attendance at sessions, refreshments and course documentation of registered event.

Confirmation: you will receive confirmation and joining instructions from us within two working days of registering. If this is not the case, please telephone us to ensure we have received your booking.

Please note that credit cards will be debited within 7 days of your registration. Payment must be made within two weeks to ensure that discounted rate is retained. To ensure access to the event, payment must be made prior to the event.

PAYMENT OPTIONS:INVOICE

Please send me an invoice with check and wire transfer information. CREDIT CARD. PLEASE DEBIT MY:

VISA MASTERCARD AmEx.

Card No. / / /

Expiry Date / CVV/Security number

Name of Card Holder

Billing Address

Country Zip/Postal Code

Signature

GROUP RATES AVAILABLE FOR 3+ DELEGATES50% discount on the 3rd delegate registering from the same company, when registering at the same time. Lowest rate discounted

Contact us, call: +1 888 677 7007 or email: [email protected]

Please complete the relevant fields and select your payment and attendance options. When complete, please click Submit. You will receive confirmation within 24 hours of your registration being received.YOU CAN ALSO REGISTER ONLINE www.risk-americas.com BY TELEPHONE: +1 888 677 7007 BY FAX: +1 609 514 5104 OR EMAIL: [email protected]

PLEASE CLICK SUBMIT TO COMPLETE. If a draft email window does not open in your email client, please forward this completed form to [email protected]

EARLY RATE STANDARD RATERegister by April 15 Registeration after April 15

$1599 SAVE $400

$1999

Risk Americas Convention, May 3-4 2016 + ONE Masterclass, May 5

$2398 SAVE $600

$2998

$799 SAVE $200

$999

Risk Americas Convention, May 3-4 2016

Masterclass Only Model Risk OR Stress Testing (PPNR + Scenarios), May 5CONCESSION RATES: 15% Discount for professionals of community banks, government and regulatory bodies, as well as members of professional trade associations and societies.

SELECT EVENT OPTIONS