revisional assignments / sample papers - … assignments / sample papers - class 12 ... business and...

TRANSCRIPT

REVISIONAL ASSIGNMENTS / SAMPLE PAPERS - CLASS 12- ACCOUNTANCY

ASSIGNMENT 1

STD XII

ACCOUNTANCY

Time: 3 Hours

M.M.:80

General Instructions:

1. Attempt all questions

2. Transactions should be clearly recorded .

3. All parts of a question must be done together in one place.

4. Marks allotted to each question are given in brackets.

5. Calculations shown clearly adjacent to the rest of the answer.

1. Finserve Ltd is carrying on a Mutual Fund business. It invested Rs. 30,00,000 in

shares and Rs.15,00,000 in debentures of various companies during the year. It received

Rs.3,00,000 as dividend and interest. Find out cash flows from investing activities.

(1)

2. How will Issue of Shares against purchase of equipment impact cash flow activities.

(1)

3. A , B and C are partners sharing profits in 3:1:2.C retires by gifting half of his profit

share to A, his daughter .Calculate the new profit sharing ratio of new firm.

(1)

4. For acquiring which right does the new partner brings capital.

(1)

5. Y withdraws Rs.5,000 at end of each Quarter. Compute Interest on Drawings@6%p.a.

(1)

6. Karan, Nakul and Asha were partners in a firm sharing profits and losses in the ratio

3:2:1. At the time of admission of a partner, the goodwill of the firm was valued at

Rs.2,00,000. The accountant of the firm passed the entry in the books of accounts and

thereafter showed goodwill at Rs.2,00,000 as an asset in the Balance Sheet. Was he

correct in doing so? Why?

(1)

7. Ideal current ratio is 2:1.What would high ratio indicate.

(1)

8. Under what circumstances will the fixed capital account of the partners undergo a

change.(1)

9. Give the major headings and sub-headings under which the following items would

appear in the financial statements of the company as per Revised Schedule VI.

(a) Bank Charges; (b) Staff welfare expenses (c) Consumption of loose tools

(d)Excess Provision written back (e) Computer hiring expenses (f) Sale of scrap

(3)

10 (a) Name the sub heads under the head ‗Current liabilities‘ in a company‘s Balance

Sheet as per Schedule III part I of the Companies Act 2013.

(2)

10 (b) Give one example of commitment and contingent liability each.

(1)

11. Ankur and Bobby were into the business of providing software solutions in India.

They were sharing profits and losses in the ratio 3:2. They admitted Cheenu for a 1/5

share in the firm. Cheenu who belong to poor family but an educated person was taken

as a partner to help them to expand their business to various South African countries where

he had been working earlier. Cheenu is guaranteed a minimum profit of Rs.2,00,000 for the

year. Any deficiency in Cheenu share is to be borne by Ankur and Bobby in the ratio

4:1. Losses for the year were Rs.10,00,000. Pass the necessary journal entries and values

pursued by them. (3)

12. Calculate the amount of Opening trade receivables and Closing trade receivables from

the following:

Trade receivables turnover ratio 5 times

Cost of revenue from operations Rs.12,00,000

Gross profit ratio 20%

Closing Trade receivables were Rs.30,000 more than opening Trade receivables. Cash

revenue from operations being 1/3rd

of credit revenue from operations.

(3)

13. L, M and N are partners sharing profits and losses in the ratio of 5:3:2. On 1.4.2016,

they decide to change future PSR to 3:2:1. On that date they had the following balances in

undistributed profits:

a. General Reserve Rs. 1,20,000

b. P& L A/c [Cr.] Rs. 90,000

c. Miscellaneous Expenditure (yet to be written off ) Rs. 2,70,000

Give necessary journal entry, when partners do not want to disturb the General

Reserve,

P& L A/c and Miscellaneous Expenditure .

(4)

14 . Geeta and Seeta were partners carring on recycling of old papers sharing profits in

the ratio of 3:1.Reeta was their manager with a physical disability ,receiving a monthly

salary of Rs.2,000 p.m. and a commission of 5% of net profits after charging his salary

and commission. On 1st April 2015 Reeta was admitted as a partner for 1/5

th share. It was

also agreed that if amount receivable by Reeta as a partner exceeds the amount receivable

by him as a manager, will be borne by Geeta alone. Profits for the year ended 31st

March 2016 was Rs. 3,85,032 before charging anything.. Prepare Profit and loss

appropriation a/c.

Name two values of this business.

(3+1=4)

15. Nimani Ltd. is into the business of back office operations. Honesty and hard work are

the two pillars on which the business has been built. It has a good turnover and profits.

Encouraged by huge profits, it decided to give the workers bonus equal to two months

salary.

Particulars 31.3.2016 (Rs.)

Revenue from operations

Cost of Goods Sold

Other Income

Finance Cost

Other Operating Expenses

Income Tax

10,00,000

7,00,000

1,00,000

50,000

2,50,000

50% of Net Profit before

Tax

(a) Prepare common size Income Statement ending 31st March 2016

(b) Identify any two values which Nimani Ltd. wants to communicate to the society.

(3+1)

16. A,B,C are partners in a firm. Their fixed capital accounts stood at Rs.15,000,7,500

and 7,500 respectively on 31.12.2011 .

Their drawing were Rs.3,000 p.a each .

As per the provisions of the deed

1. C was allowed a salary of Rs.1500.p.a

2. Interest on the capital and drawings were@ of 5%.p.a

3. Profits to be taken up in 2:2:1.

4. Ignoring the terms of the deed, profits for the, year was Rs.9,000 and it was

distributed in the equally. Pass an adjusting entry to rectify the error.

(4)

17. Naresh, David and Aslam are partners sharing profits in the ratio of 5: 3:7. On 1st

April, 2016, Naresh gave a notice to retire from the firm. David and Aslam decided to

share future profits in the ratio of 2:3. The adjusted capital accounts of David and Aslam

show a balance of

33,000 and 70,500 respectively. The total amount to be paid to Naresh is 90,500

as

40,500 in cash and rest by giving a draft for the balance. David and Aslam will

make their capital proportionate to their new profit sharing ratio and adjustments to be

done through current accounts. Pass necessary journal entries for the above transactions.

(4)

18. Amar commenced business with a capital of Rs.1,25,000 on 1.4.11. During the five

years he made following amounts of profits and losses

Rs.

31.3.12- 2,500(loss)

31.3.13-6,500(Profit)

31.3.14-8,500(Profit)

31.3.15-10,000(Profit)

31.3.16-12,500(Profit)

During this period he withdrew Rs.20,000On 1.4.2016 he admitted Baskar on the

following terms. He would bring capital equal to Amar for his half the share in the

business and his share of goodwill on the basis of three times average profit of last five

years. Journalise. (4)

19. In the following accounts you are required to fill the missing information:

PROFIT AND LOSS ACCOUNT

Particulars Rs Particulars Rs

To Interst on B‖s Loan 3,000 By ? ?

To ? ?

To ? ?

98,800 98,800

PROFIT AND LOSS APPROPRIATION ACCOUNT

Particulars Rs Particulars Rs

To ? ? By ? ?

To ? ? By ? ?

To ? ? By ? ?

To ? ? By ? ?

To ? ?

To ? ?

To ? ?

CAPITAL ACCOUNTS

Particulars

P

A B C Particulars

P

A B C

? ? ? ? By Bal

B/d

2,00,000 1,50,000 1,00,000

? ? ? ? ? ?

CURRENT ACCOUNTS

Particulars

P

A B C Particulars P A B C

To Bal B/d - - 3000 By Bal B/d 5000 4000 -

To ? 20,000 20,000 20,000 By IOC 10000 7500 5000

To IOD 600 600 600 By Rent - 12000 -

? ? ? ? By commission - - 4000

By Profits 19700 19700 19700

? ? ? ? ? ?

(6)

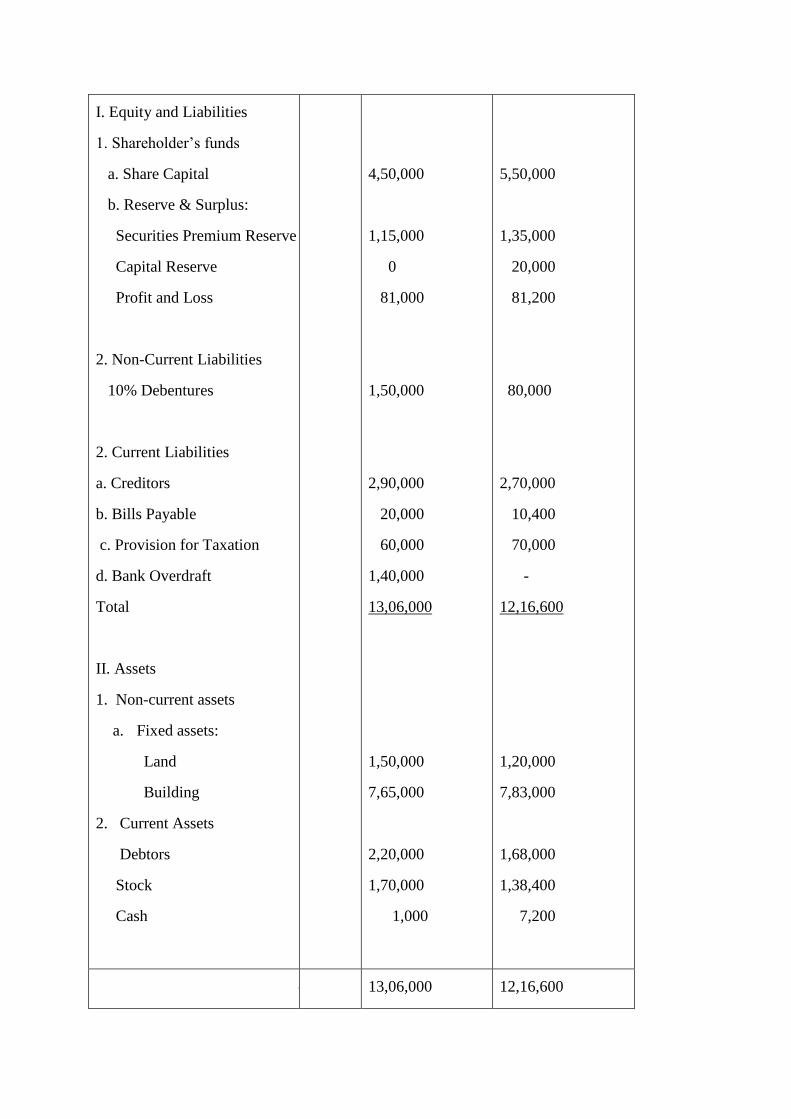

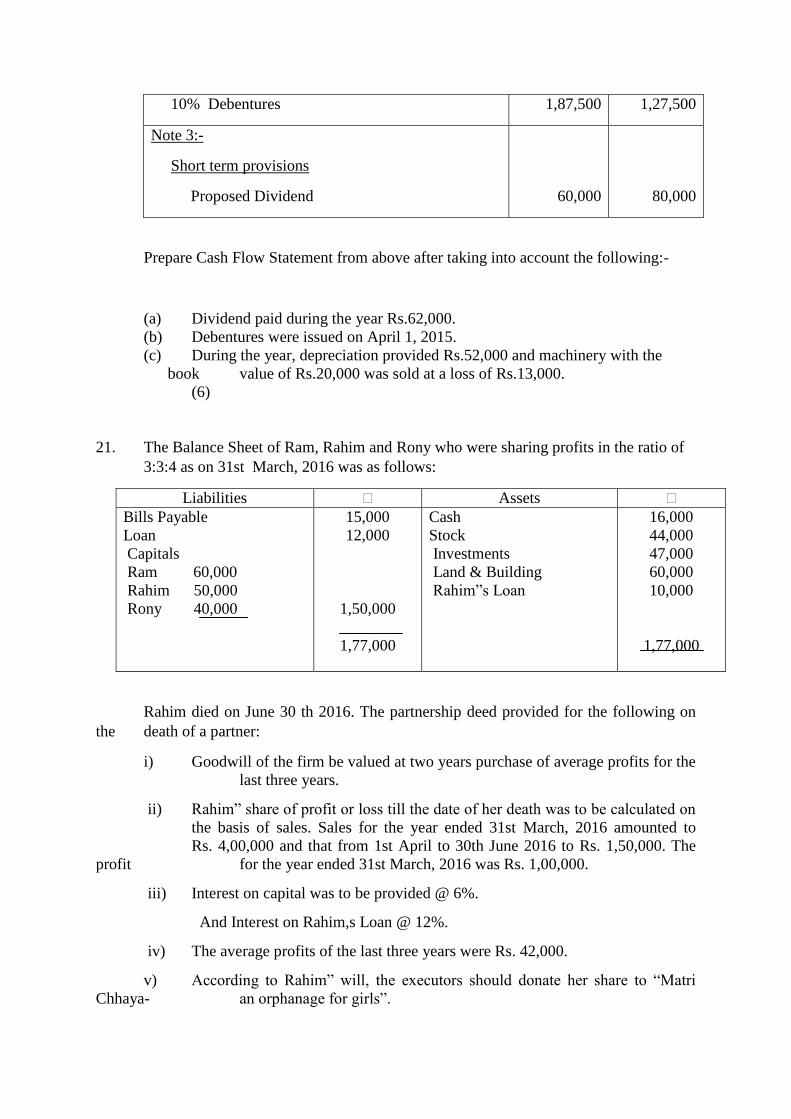

20. Prepare Cash Flow Statement From The following information:

Particulars Note No. 31st March, 2015 (Rs.) 31

st March, 2016 (Rs.)

I. Equity and Liabilities

1. Shareholder‘s funds

a. Share Capital

b. Reserve & Surplus:

Securities Premium Reserve

Capital Reserve

Profit and Loss

2. Non-Current Liabilities

10% Debentures

2. Current Liabilities

a. Creditors

b. Bills Payable

c. Provision for Taxation

d. Bank Overdraft

Total

II. Assets

1. Non-current assets

a. Fixed assets:

Land

Building

2. Current Assets

Debtors

Stock

Cash

4,50,000

1,15,000

0

81,000

1,50,000

2,90,000

20,000

60,000

1,40,000

13,06,000

1,50,000

7,65,000

2,20,000

1,70,000

1,000

5,50,000

1,35,000

20,000

81,200

80,000

2,70,000

10,400

70,000

-

12,16,600

1,20,000

7,83,000

1,68,000

1,38,400

7,200

otal 13,06,000 12,16,600

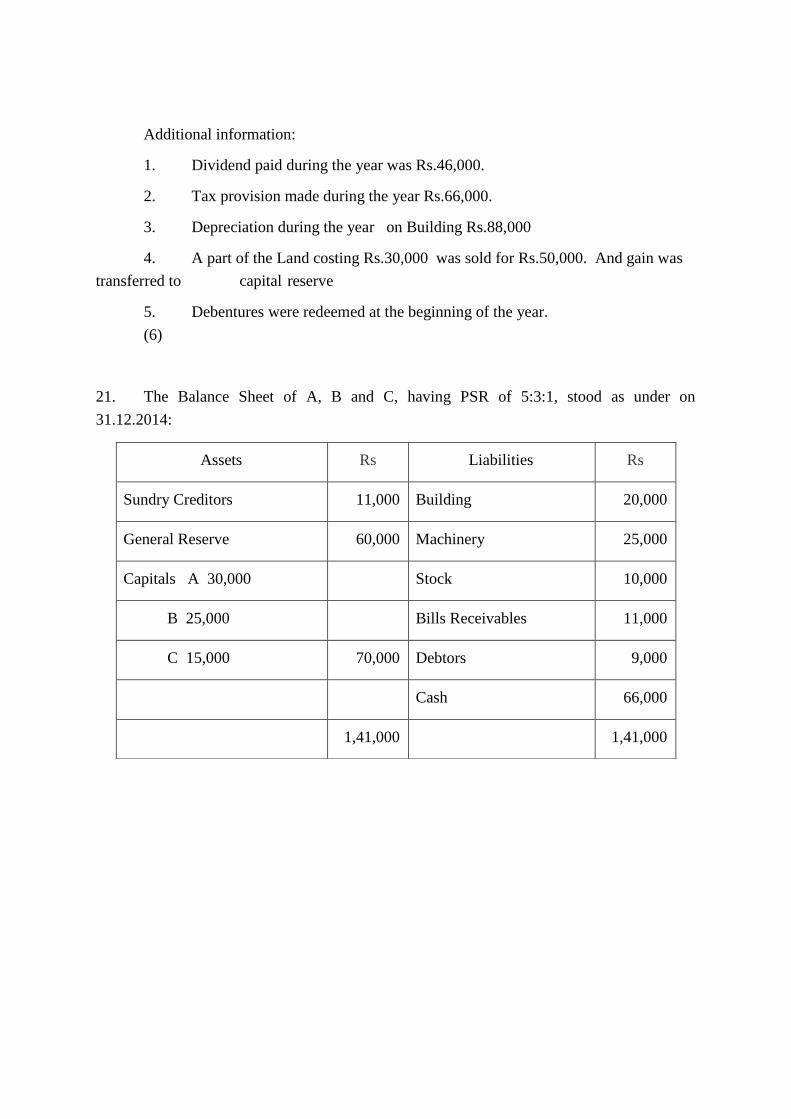

Additional information:

1. Dividend paid during the year was Rs.46,000.

2. Tax provision made during the year Rs.66,000.

3. Depreciation during the year on Building Rs.88,000

4. A part of the Land costing Rs.30,000 was sold for Rs.50,000. And gain was

transferred to capital reserve

5. Debentures were redeemed at the beginning of the year.

(6)

21. The Balance Sheet of A, B and C, having PSR of 5:3:1, stood as under on

31.12.2014:

Assets Rs Liabilities Rs

Sundry Creditors 11,000 Building 20,000

General Reserve 60,000 Machinery 25,000

Capitals A 30,000 Stock 10,000

B 25,000 Bills Receivables 11,000

C 15,000 70,000 Debtors 9,000

Cash 66,000

1,41,000 1,41,000

B died on 1.08.2015 in a car accident. It was agreed between his executors and the

remaining partners that:

a. Goodwill to be valued at Rs.18,000

b. Profits for the given period was taken as having accrued at the same rate as that of

the previous year which was Rs.3,600

c. Interest on capital is provided at 12% irrespective of the time period to B.

d. A sum of Rs.14,700 due to B to be paid immediately to the executor and the

balance paid in four equal half yearly installments, together with Interest at 12%

p.a.

e. A and C intends to admit D, unemployed daughter of B in his place from next

financial year.

Prepare B‘s Capital Account and Executor‘s Accounts, till final settlement. Identify

values

involved in offering D partnership contract. (7+1)

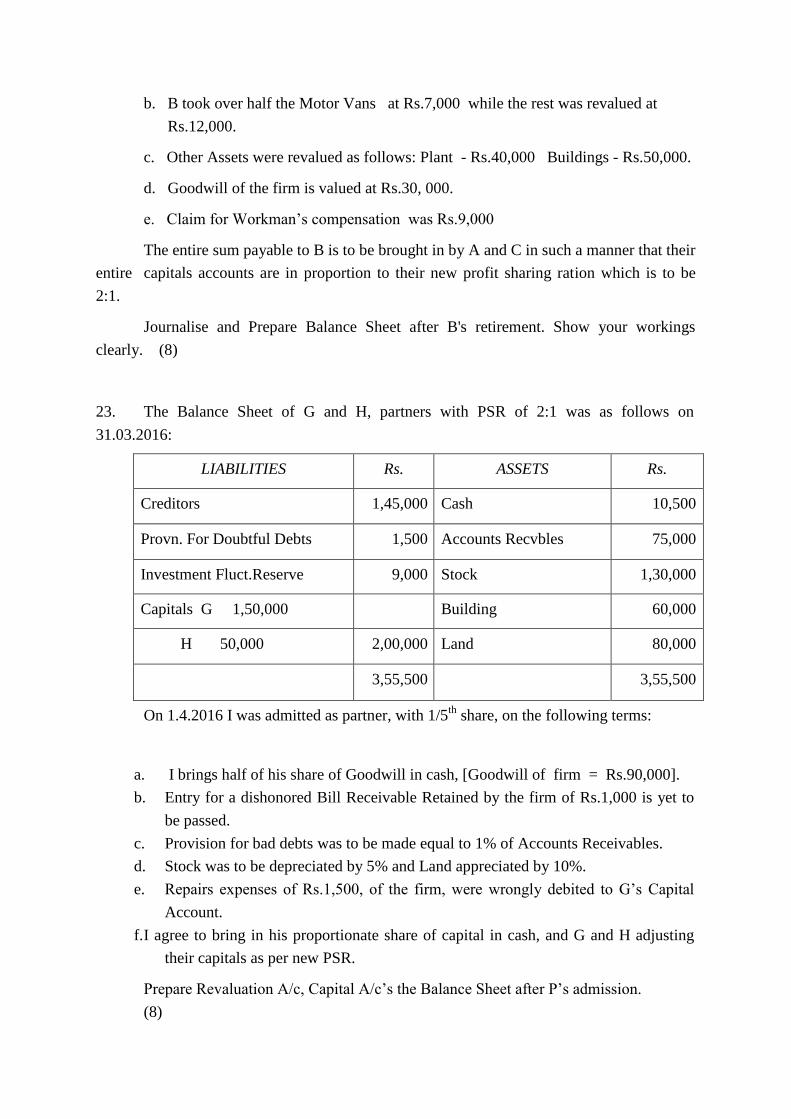

22. The following is the Balance Sheet of A, B and C on 31st March 2016.

B retired on 31.03.2016 and the following arrangement was decided upon:

a. All the debtors prove to be good.

LIABILITIES Rs ASSETS Rs.

Sundry Creditors 26,000 Building 62,000

Workmans compensation 15,000 Motor Vans 20,000

General Reserve 1,20,000 Plant 21,000

Capitals A 50,000 Stock 15,000

B 40,000 Debtors 40,000

C 20,000 [-] P.D.D. 3,000 37,000

Cash 1,16,000

2,71,000 2,71,000

b. B took over half the Motor Vans at Rs.7,000 while the rest was revalued at

Rs.12,000.

c. Other Assets were revalued as follows: Plant - Rs.40,000 Buildings - Rs.50,000.

d. Goodwill of the firm is valued at Rs.30, 000.

e. Claim for Workman‘s compensation was Rs.9,000

The entire sum payable to B is to be brought in by A and C in such a manner that their

entire capitals accounts are in proportion to their new profit sharing ration which is to be

2:1.

Journalise and Prepare Balance Sheet after B's retirement. Show your workings

clearly. (8)

23. The Balance Sheet of G and H, partners with PSR of 2:1 was as follows on

31.03.2016:

LIABILITIES Rs. ASSETS Rs.

Creditors 1,45,000 Cash 10,500

Provn. For Doubtful Debts 1,500 Accounts Recvbles 75,000

Investment Fluct.Reserve 9,000 Stock 1,30,000

Capitals G 1,50,000 Building 60,000

H 50,000 2,00,000 Land 80,000

3,55,500 3,55,500

On 1.4.2016 I was admitted as partner, with 1/5th

share, on the following terms:

a. I brings half of his share of Goodwill in cash, [Goodwill of firm = Rs.90,000].

b. Entry for a dishonored Bill Receivable Retained by the firm of Rs.1,000 is yet to

be passed.

c. Provision for bad debts was to be made equal to 1% of Accounts Receivables.

d. Stock was to be depreciated by 5% and Land appreciated by 10%.

e. Repairs expenses of Rs.1,500, of the firm, were wrongly debited to G‘s Capital

Account.

f. I agree to bring in his proportionate share of capital in cash, and G and H adjusting

their capitals as per new PSR.

Prepare Revaluation A/c, Capital A/c‘s the Balance Sheet after P‘s admission.

(8)

ASSIGNMENT- 2

STD XII

ACCOUNTANCY

Time: 3 Hours

M.M.:80

General Instructions:

1. Attempt all questions

2. Transactions should be clearly recorded .

3. All parts of a question must be done together in one place.

4. Marks allotted to each question are given in brackets.

5. Calculations shown clearly adjacent to the rest of the answer.

1. Sterling Ltd., a mutual fund company, provides you the following information:

10% bank loan repaid was 1,00,000

Dividend received during the year was 20,000

Find out the cash flow from various activities. (1)

2. Emerald Ltd is engaged in business of tours and travels. It had purchased a lottery

ticket

and won a prize of Rs.5,00,000. Under which head will it be shown while preparing

cash

flow statement. (1)

3. A, B and C are partners in the ratio of 3:2:1. W is admitted with 1/6th

share in profits.

C would retain his original share. Calculate new profit sharing ratio. (1)

4. For acquiring which right does the new partner brings goodwill. (1)

5. Y withdraws Rs.5,000 at Beginning of each Quarter. Compute Interest on drawings

@ 6% p.a. (1)

6. L,M were partners in a firm sharing profits and losses in the ratio 3:2. At the time of

admission of partner N for1/5 share, the reserve of the firm was valued at Rs.25,000.

and firm decided to show the reserve at the same value in the books of the new firm. What

Journal entry should be passed for the same? (1)

7. Ideal debt equity ratio is 2:1.What would high ratio indicate. (1)

8. Under what circumstances Interest on capital is recorded in Profit and loss a/c only?

(1)

9. Give the major headings and sub-headings under which the following items would

appear in the financial statements of the company as per Revised Schedule VI.

(a) Bank Charges b) Interest earned (c)Courier charges

(d) Profit on sale of fixed Assets (e) refund of Income Tax (f)Sale of

scrap (3)

10. Name the sub heads under the head ‗Current Assets‘ in a company‘s Balance Sheet

as per Schedule III part I of the Companies Act 2013. (3)

11. Poppy and Dolly are partners in a firm .Interest on capital @ 10% p.a is allowed.

Liabilities Rs. Assets Rs.

Profit and Loss Appropriation

Poppy‘s Capital

Dolly‘s Capital

50,000

80,000

70,000

_________

2,00,000

FixedAssets

Drawings of Poppy‘s

Other Assets

1,50,000

20,000

30,000

2,00,000

During the year Poppy and Dolly had withdrawn Rs. 20,000 and Rs.25,000

respectively. Profit for the year was Rs.75,000. Journalize.

(3)

12 A company has Rs. 40,00,000 as Capital Employed(including 20,00,000 as 10% loan

component). The rate of income tax is 40%. Company at the end of the year after

paying tax had profit of Rs. 4,20,000 for equity shareholders. Calculate Return on

Investment Ratio.

(3)

13. A and B are partners sharing profits and losses in the ratio of 5:3. On 1.4.2016, they

decide to change future PSR to 1:1. On that date they had the following balances in

undistributed profits:

a. General Reserve Rs. 80,000

b. . Miscelleneous. Expenditure (yet to be written off ) Rs. 1,60,000

Give necessary journal entries, when partners

a) do not want to continue with the General Reserve and Miscellaneous

Expenditure.

b) want to continue with the General Reserve and Miscellaneous. Expenditure

(4)

14. A, B and C are partners sharing profits in the ratio of 5:4:3. They were manufacturing

shoes in India and exporting to Italy. Being a socially aware organization, they wanted

to pay back to the society. They decided to not only supply free shoes to 50 orphanages

in various parts of the country but also give employment to children from those orphanages

who were above 18 years of age Their Capitals on 1st April, 2015 were Rs.50,000,

Rs.40,000 and Rs. 20,000

respectively.

After closing the accounts for the year ended 31st March, 2016 it was found out that

according to the partnership agreement interest at 10% p.a. on partners‘ capitals, a

salary of Rs.4,000 per year to B and a salary of Rs.9, 000 per year to C were not

provided before distribution of profit. It was agreed among the partners to make an

adjustment entries assuming that capitals are not fixed. Also name the values that bind the

organization.

(3+1=4)

15. Nitron Ltd. is into the business of back office operations. It has a good turnover and

profits. Encouraged by huge profits, it decided to give the workers bonus equal to two

months salary.

(a) Prepare common size Income Statement ending 31st March 2016

(b) Identify any two values which Nitron Ltd wants to communicate to the

society. :

Revenue from Operations (% of material consumed) 150%

Cost of materials consumed 8,00,000

Employee benefit expenses (% of materials consumed) 15%

Other expenses (% of materials consumed) 10%

Other Income (% of Revenue from operations) 10%

Tax 30%

(3+1)

16. X, Y and Z are partners in a firm. On 1st April, 2015 the balance in their capital

accounts stood at Rs.8,00,000 , Rs.6,00,000 and Rs.4,00,000 respectively. They shared

profits in proportion of 5:3:2. Partners are entitled to interest on capital at 5% p.a. and

salary to Y Rs.3,000 per month and a commission of Rs. 12,000 to Z as per the

provisions of the partnership deed.

X‘s share of profit excluding interest on capital, is guaranteed by firm at not less than

Rs.40,000 p.a. Y‘s share of profit including interest on capital but excluding salary is

guaranteed by Z at a minimum of Rs. 55,000 p.a. The profits of the firm for the year

ended 31st March, 2016 amounted to Rs. 2,16,000.

Prepare Profit and Loss Appropriation Account for the year ended 31st March, 2016.

(4)

17) Sun, Moon and Star are Partners. Moon retires and his claim including his capital and

his share of goodwill is Rs. 1,20,000. He is paid partly in cash and partly in kind. There

was an unrecorded Vehicle valued at Rs.60,000in the books of the firm which Moon agreed

to take and balance was paid in cash to settle his account. Journalize.

(4)

18. Anil, Sunil and Tuhil were partners sharing P&L in the ratio 5:3:2. Tuhil retires from

the firm. Their capital balances after all necessary adjustments of Revaluation

Profits/Losses, Reserves and Goodwill were Rs. 4,40,000; Rs. 2,50,000 and Rs.

3,10,000 respectively. Tuhil was to be paid his dues immediately. Amount payable to

Tuhil was brought in by Anil and Sunil equally. Thereafter Rumil is admitted as a new

partner for 20% share. Rumil will bring capital of Rs.3,00,000. The capitals of other

partners were to be adjusted on the basis of Rumil‘s capital contribution. Pass necessary

journal entries for the amount payable or brought in by all the partners along with

goodwill treatment assuming that Rumil does not bring in his share of goodwill . Show

your workings clearly. (4)

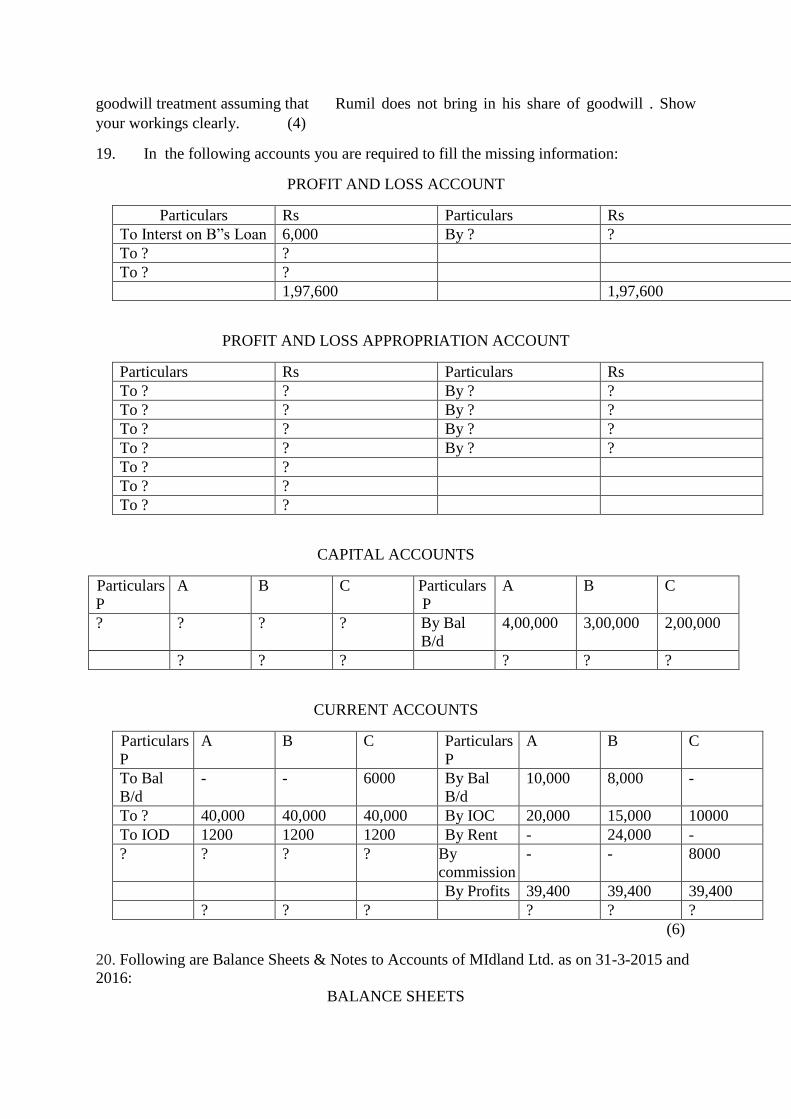

19. In the following accounts you are required to fill the missing information:

PROFIT AND LOSS ACCOUNT

Particulars Rs Particulars Rs

To Interst on B‖s Loan 6,000 By ? ?

To ? ?

To ? ?

1,97,600 1,97,600

PROFIT AND LOSS APPROPRIATION ACCOUNT

Particulars Rs Particulars Rs

To ? ? By ? ?

To ? ? By ? ?

To ? ? By ? ?

To ? ? By ? ?

To ? ?

To ? ?

To ? ?

CAPITAL ACCOUNTS

Particulars

P

A B C Particulars

P

A B C

? ? ? ? By Bal

B/d

4,00,000 3,00,000 2,00,000

? ? ? ? ? ?

CURRENT ACCOUNTS

Particulars

P

A B C Particulars

P

A B C

To Bal

B/d

- - 6000 By Bal

B/d

10,000 8,000 -

To ? 40,000 40,000 40,000 By IOC 20,000 15,000 10000

To IOD 1200 1200 1200 By Rent - 24,000 -

? ? ? ? By

commission

- - 8000

By Profits 39,400 39,400 39,400

? ? ? ? ? ?

(6)

20. Following are Balance Sheets & Notes to Accounts of MIdland Ltd. as on 31-3-2015 and

2016:

BALANCE SHEETS

PARTICULARS NOTE

No.

2015-16

(Rs.)

2014-15

(Rs.)

I EQUITY & LIABILITIES

Shareholders‘ Funds

Share Capital

Reserves & Surplus

Non Current Liabilities

Long Term Borrowings

Current Liabilities

Trade Payables

Bank Overdraft

Short term provisions

1

2

3

5,40,000

(90,000)

1,87,500

3,000

7,000

60,000

3,00,000

(75,000)

1,27,500

6,000

70,000

80,000

TOTAL 7,07,500 5,08,500

II ASSETS

Non Current Assets

Fixed Assets

Current Assets

Current Investments

Inventories

Trade Receivables

Cash & Cash Equivalents

6,03,000

12,500

14,000

9,500

68,500

3,63,000

33,500

5,000

23,000

84,000

TOTAL 7,07,500 5,08,500

Notes to Accounts:-

PARTICULARS 2015-16

(Rs.)

2014-15

(Rs.)

Note 1:-

Reserves and Surplus:-

Surplus (balance in Statement of Profit and Loss)

(90,000)

(75,000)

Note 2:-

Long Term Borrowings

10% Debentures 1,87,500 1,27,500

Note 3:-

Short term provisions

Proposed Dividend

60,000

80,000

Prepare Cash Flow Statement from above after taking into account the following:-

(a) Dividend paid during the year Rs.62,000.

(b) Debentures were issued on April 1, 2015.

(c) During the year, depreciation provided Rs.52,000 and machinery with the

book value of Rs.20,000 was sold at a loss of Rs.13,000.

(6)

21. The Balance Sheet of Ram, Rahim and Rony who were sharing profits in the ratio of

3:3:4 as on 31st March, 2016 was as follows:

Liabilities ₹ Assets ₹

Bills Payable

Loan

Capitals

Ram 60,000

Rahim 50,000

Rony 40,000

15,000

12,000

1,50,000

1,77,000

Cash

Stock

Investments

Land & Building

Rahim‖s Loan

16,000

44,000

47,000

60,000

10,000

1,77,000

Rahim died on June 30 th 2016. The partnership deed provided for the following on

the death of a partner:

i) Goodwill of the firm be valued at two years purchase of average profits for the

last three years.

ii) Rahim‖ share of profit or loss till the date of her death was to be calculated on

the basis of sales. Sales for the year ended 31st March, 2016 amounted to

Rs. 4,00,000 and that from 1st April to 30th June 2016 to Rs. 1,50,000. The

profit for the year ended 31st March, 2016 was Rs. 1,00,000.

iii) Interest on capital was to be provided @ 6%.

And Interest on Rahim,s Loan @ 12%.

iv) The average profits of the last three years were Rs. 42,000.

v) According to Rahim‖ will, the executors should donate her share to ―Matri

Chhaya- an orphanage for girls‖.

Rahim is paid Rs. 2,200 immediately in cash and balance transferred to his loan

account on which interest @ 6% is payable. The loan is repaid by four equal annual

installment together with interest.

Prepare Rahim‖ Capital Account to be rendered to her executor and executor and

Rahim Executor‘s Account till it is finally paid. Also identify the values being highlighted in

the question.

(7+1)

22. Ram, Mohan and Sohan were partners sharing profits and losses in the ratio of 2:2:1.

On 31st March, 2016, their Balance Sheet was as under :

Liabilities Rs. Assets Rs.

Capitals :

Ram 1,50,000

Mohan 1,25,000

Sohan 75,000

Investment Fluct. Reserve

Creditors

3,50,000

30,000

1,70,000

5,50,000

Leasehold

Patents

Machinery

Investments

Stock

Cash at Bank

1,25,000

30,000

1,50,000

55,000

90,000

1,00,000

5,50,000

Sohan retired on 31.03.2016 and the following arrangement was decided upon:

a. Stock is under valuedby10%

b. Investments are valued at Rs.20,000

c. Goodwill of the firm is valued at Rs.25, 000.

The entire sum payable to Sohan is to be brought in by Ram and Mohan in such a

manner that their entire capitals accounts are in proportion to their new profit sharing

ration which is to be 2:1. And there will be a minimum cash balance of Rs.1,50,000.

Prepare Journalize and prepare Balance Sheet after B's retirement. (8)

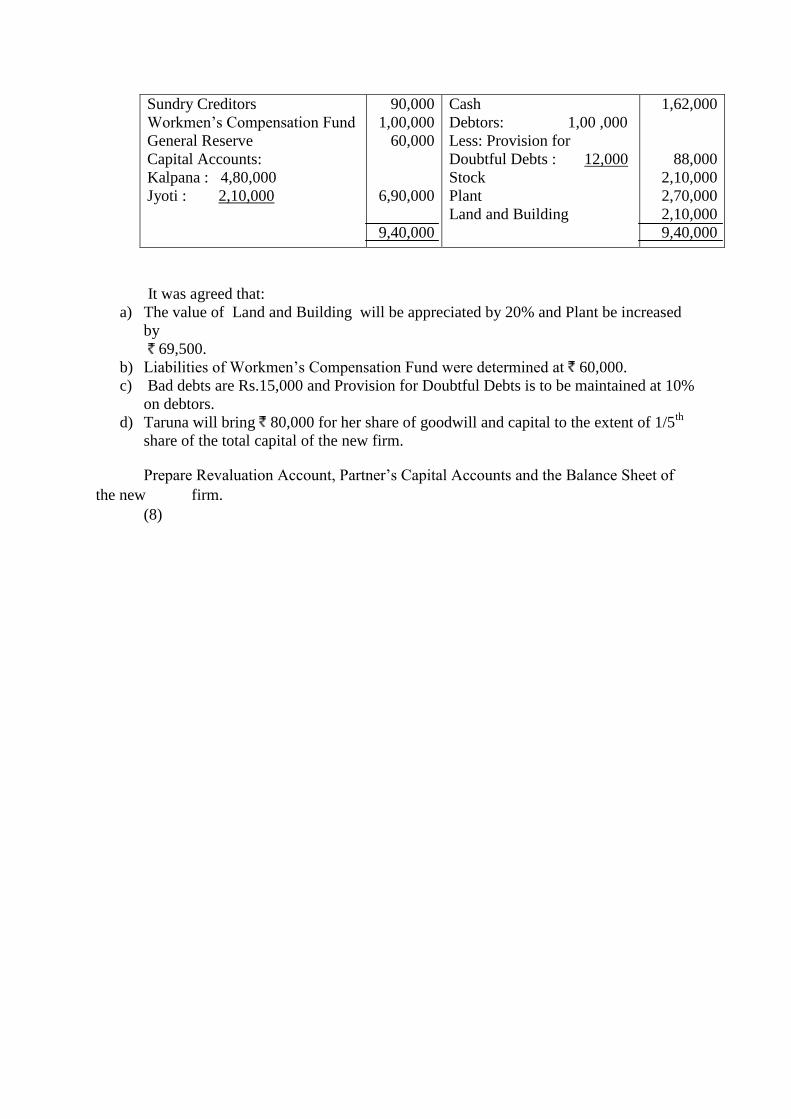

23. Kalpana and Jyoti were partners in a firm sharing profits in the ratio of 3:2. On 1st

April, 2016 they admitted Taruna as a new partner.

The Balance Sheet of Kalpana and Jyoti as on 1st April, 2016 was as follows:

Liabilities Assets

Sundry Creditors

Workmen‘s Compensation Fund

General Reserve

Capital Accounts:

Kalpana : 4,80,000

Jyoti : 2,10,000

90,000

1,00,000

60,000

6,90,000

9,40,000

Cash

Debtors: 1,00 ,000

Less: Provision for

Doubtful Debts : 12,000

Stock

Plant

Land and Building

1,62,000

88,000

2,10,000

2,70,000

2,10,000

9,40,000

It was agreed that:

a) The value of Land and Building will be appreciated by 20% and Plant be increased

by

69,500.

b) Liabilities of Workmen‘s Compensation Fund were determined at 60,000.

c) Bad debts are Rs.15,000 and Provision for Doubtful Debts is to be maintained at 10%

on debtors.

d) Taruna will bring 80,000 for her share of goodwill and capital to the extent of 1/5th

share of the total capital of the new firm.

Prepare Revaluation Account, Partner‘s Capital Accounts and the Balance Sheet of

the new firm.

(8)

ASSIGNMENT- 3

CLASS XII

Subject – Accountancy

Time Allowed:3 hrs. M.M:80

Q 1. If A makes drawings of Rs. 15,000 every month in the beginning, what will be the

interest @5 % p.a. (1)

Q 2. What is meant by self purchased goodwill? (1)

Q 3. A firm earns profit of Rs. 3,00,000 as its annual profits, the rate of return being 12%.

Assets and liabilities of the firm amounted to Rs. 36,00,000 and Rs. 12,00,000 respectively.

Calculate the value of goodwill by capitalisation method. (1)

Q 4. A, B and C shared profits and losses in the ratio of 3:2:1respectively. With effect from

1st April 2016 they decided to share profits equally. The goodwill of the firm was valued at

Rs.18,000. Pass necessary journal entry. (1)

Q 5.State any one right acquired by a new partner in firm. (1)

Q 6. At what rate is interest payable on the amount remaining unpaid to the executor of

deceased partner? (1)

Q 7.`In case of dissolution of a firm which liabilities are to be paid first? (1)

Q 8. List any two reasons when a court may dissolve a firm. (1)

Q 9.Rat, Cat and Bat sharing profits and losses equally have capitals of Rs. 1,20,000; 90,000

and Rs. 60,000. For the year 2016, interest was credited to them @ 9% instead of 10%. Give

adjustment journal entry. (3)

Q 10. Pass journal entries in the firm‘s journal for the following on the admission of a

partner:

a) Unrecorded investments worth Rs. 5,000.

b) Unrecorded liabilities towards suppliers for Rs. 1,500.

c) An item of Rs. 600 included in S. Creditors is not likely to be claimed, hence should

be written back. (3)

Q 11. A, B and C are partners in a firm whose books are closed on 31st March each year. A

died on 30th June 2016 and according to the agreement, the share of profits of a deceased

partner up to the date of death is to be calculated on the basis of the average profit for the last

five years. The net profits for the last five years have been : 2012 Rs. 14,000; 2013 Rs.

18,000; 2014 Rs. 16,000; 2015 Rs. 10,000(loss) and 2016 Rs. 16,000. Calculate A's share of

the profits up to the date of death and pass necessary journal entry.

(3)

Q 12. 70% of machinery was taken over by Aman, a partner, at a valuation of 90% and

remaining machinery was sold at 80% less 5% selling commission.(Book values given in

Balance Sheet just before dissolution: Machinery= Rs. 2,00,000; Provision for depreciation=

Rs. 25,000) Journalise. (3)

Q 13. A business earned an average profit of Rs. 8,00,000 during the last few years. The

normal rate of profits in the similar type of business is 10%. The total value of assets and

liabilities of the business were Rs. 22,00,000 and Rs. 5,60,000 respectively. Calculate the

value of goodwill of the firm by super profit method if it is valued at 2.5 years purchase of

super profits. (4)

Q 14. Differentiate between Sacrificing Ratio and Gaining Ratio. (4)

Q 15.P and Q are partners sharing profits and losses in the ratio of 2:3. On 1.4.16, they

decided to share profit and loss in the ratio of 2:1. An extract of Balance Sheet as at 31st

March 2016 is as follows: (4)

EXTRACT OF BALANCE SHEET AS AT 31st MARCH 2016

Liabilities Amount Assets Amount

Investment fluctuation Reserve

5,000

Investment

1,00,000

Show the accounting treatment in each of the following alternative cases:

i. If the market value of investment is Rs. 95,000.

ii. If the market value of investment is Rs. 1,10,000.

Q 16. A and B are partners in a firm sharing profits and losses in the ratio of 5:2. On 31st

March ' 2016 their Balance Sheet showed a General Reserve of Rs. 35,000. On that date, they

decided to admit C as a new partner and the new profit sharing ratio will be 5:3:2. Record

necessary journal entries in the books of the firm under following circumstances:

i. When they want to transfer General Reserve to their capital accounts.

ii. When they don't want to transfer general reserve in their capital accounts but prefer to

record an adjustment entry for the same. (4)

Q 17. Distinguish between private debts and Firm debts. (4)

Q 18. Nikhil, Princy and Riya were partners in a firm sharing profits and losses in the ratio of

5:3:2. Inspite of repeated reminders by the authorities, they kept dumping hazardous material

into a nearby river. The court ordered for the dissolution of their partnership firm on 31st

March 2016. Following settlements were done, You are required to pass journal entries for

the same: (4+2)

i. Princy agreed to pay off her husband's loan of Rs. 19,500.

ii. A debtor whose debt of Rs. 9,300 was written off as bad in the books paid Rs. 7,500

in full settlement.

iii. Riya took over all investments at Rs. 13,300.

iv. S. Creditors Rs. 10,000 were paid at 9% discount.

State the values which have been violated by the firm which led to this dissolution.

Q 19. M,N ,O and P are partners having capitals of Rs. 2,00,000; Rs. 1,50,000 Rs. 1,00,000

and Rs. 50,000 respectively. They share profits and losses in the ratio of 3:2:2:1. They have

agreed upon following terms:

i. Partners are entitled to interest on capital @ 8% p.a.

ii. O will get a salary @ 5,000 per month.

iii. N's share of profit excluding interest on capital has been guaranteed to be not less than

Rs. 2,60,000.

iv. P's share of profits including interest on capital has been guaranteed by M to be not

less than Rs. 1,10,000.

The profits for the year ended 31st March 2016 were Rs. 9,00,000 before any

appropriations. Prepare P& L Appropriation Account. (6)

Q 20.a) A. B, C and D were partners sharing profits in the ratio of 3:3:2:2. On 1st April, 2015,

D died owing to ill health. It was decided by A, B and C that in future their profit sharing

ratio would be 3:2:1. Goodwill of the firm is valued at Rs.6,00,000. Goodwill already

appeared in the balance sheet at Rs. 50,000. Complete the following journal entries in this

regard:

DATE PARTICULARS L.F

Dr.

(Rs.)

Cr.

(Rs.)

2015

April 1

A's capital A/c Dr. ____________

B's capital A/c Dr. ____________

C's capital A/c Dr. ____________

D's capital A/c Dr. ____________

To __________________ ____________

(being the existing goodwill written

off)

A's capital A/c Dr. ____________

B's capital A/c Dr. ____________

To C's capital A/c ____________

To D's capital A/c ____________

(Being the adjustment for goodwill

made on death of D and change in

profit sharing ratio)

b) A and B are partners with capitals of Rs. 1,80,000 and Rs. 2,00,000 respectively. They

decided to admit C into partnership for 1/4th share in future profits . C is to bring in a sum of

Rs. 1,60,000 as his capital. Calculate the amount of goodwill. (4+2)

Q 21. The Balance Sheet of A, B and C who were partners in a firm sharing profits according

to their capitals as at 31st March 2015 was as under:

Liabilities

Rs. Assets Rs.

General Reserve

Creditors

Capital

A 80,000

B 40,000

C 40,000

20,000

21,000

1,60,000

Cash at bank

Sundry Debtors 20,000

- Pro. 1,000

Stock

Machinery

Building

14,000

19,000

18,000

50,000

1,00,000

2,01,000 2,01,000

On that date, B decided to retire from the firm and was paid for his share in the firm subject

to the following:

a) Building to be appreciated by 20%.

b) Provision for bad debts to be increased to 15% on debtors.

c) Machinery to be depreciated by 20%.

d) Goodwill of the firm is valued at Rs. 72,000 and the retiring partner's share is

adjusted through the capital account of remaining partners.

e) Capital of the new firm be fixed at Rs. 1,20,000.

Prepare Revaluation Account, Partner's Capital Account and Balance Sheet after retirement

of B. (6)

Q 22.P and Q are partners sharing profits in 3:1 ratio. On 1.4.2016 they admitted R as a new

partner for 1/4th share in the firm which he acquired from P. Their Balance Sheet on that date

was as follows:

Liabilities

Rs. Assets Rs.

General Reserve

Creditors

Capital

P 1,00,000

Q 70,000

32,000

54,000

1,70,000

Cash

Sundry Debtors 40,000

- Pro. 3,000

Stock

Machinery

Land & Building

Investments

44,000

37,000

15,000

60,000

50,000

50,000

2,56,000 2,56,000

a) R will bring Rs. 40,000 as capital for his share in profits.

b) Provision for bad debts was found to be in excess by Rs. 800 .

c) Goodwill of the firm is valued at Rs. 24,000.

d) Land and Building were valued at Rs. 70,000.

e) There is a liability of Rs. 2,000 included in creditors that is not likely to

arise.

f) The capitals of partners be adjusted on the basis of R's contribution of

capital to the firm.

h) Excess or shortfall, if any, to be transferred to current accounts.

Prepare Revaluation Account, Partner's Capital Account and Balance Sheet of the new firm.

(8)

OR

Following is the Balance Sheet of X and Y, who share profits and losses in the ratio of 4:1 as

at 31st March 2016.

Liabilities Rs. Assets Rs.

Sundry Creditors

X's Brother's Loan

Y's Loan

Bank overdraft

Invest. Fluctuation Fund

X's Capital

Y's Capital

8,000

8,000

3,000

6,000

5,000

50,000

40,000

Buildings

Investments

Debtors Rs.17,000

- Pro. Rs. 2,000

Stock

Bank

Goodwill

Profit & loss A/C

25,000

25,000

15,000

15,000

20,000

10,000

10,000

1,20,000 1,20,000

The firm was dissolved on the above date and the following agreements took place:

a) X agreed to pay off his brother's loan.

b) Debtors of Rs. 5,000 proved bad.

c) Other assets realised : Investments 20% less; and goodwill at 60%.

d) One of the creditors for Rs. 5,000 was paid only Rs. 3,000.

e) Building were auctioned for Rs. 30,000 and the auctioneer's commission

amounted to Rs. 1,000.

f) Y took over part of stock at Rs. 4,000.(being 20% less than the book value).

Balance Stock realised 50%.

g) Realisation expenses amounted to Rs. 2,000.

Prepare Realisation Account, Partner's Capital Accounts and Cash A/C.

Q 23. A, B and C were in the partnership sharing profits and losses in the ratio of 5:3:2. C

retires from the firm. After all the necessary adjustments, his capital account shows a net

credit balance of Rs. 55,000 as on 1st Jan 12 C is to be paid Rs. 15,000 immediately and

balance in four equal annual instalments together with interest @ 10% p.a. on the outstanding

balance. Prepare C's Loan Account until he is paid the entire amount due to him. The firm

closes its books on 31st December of every year. OR

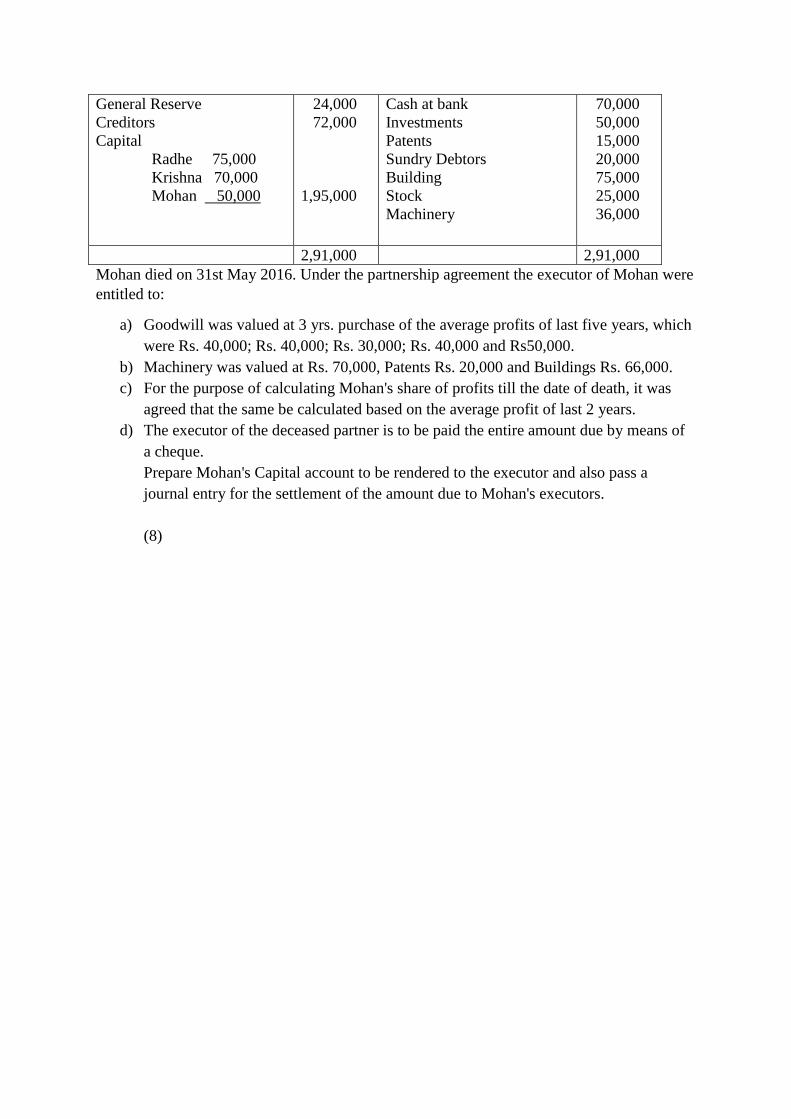

Following is the Balance Sheet of Radhe, Krishna and Mohan, who share profits and losses in

the ratio of 3:2:1 as at 31st March 2016.

Liabilities

Rs. Assets Rs.

General Reserve

Creditors

Capital

Radhe 75,000

Krishna 70,000

Mohan 50,000

24,000

72,000

1,95,000

Cash at bank

Investments

Patents

Sundry Debtors

Building

Stock

Machinery

70,000

50,000

15,000

20,000

75,000

25,000

36,000

2,91,000 2,91,000

Mohan died on 31st May 2016. Under the partnership agreement the executor of Mohan were

entitled to:

a) Goodwill was valued at 3 yrs. purchase of the average profits of last five years, which

were Rs. 40,000; Rs. 40,000; Rs. 30,000; Rs. 40,000 and Rs50,000.

b) Machinery was valued at Rs. 70,000, Patents Rs. 20,000 and Buildings Rs. 66,000.

c) For the purpose of calculating Mohan's share of profits till the date of death, it was

agreed that the same be calculated based on the average profit of last 2 years.

d) The executor of the deceased partner is to be paid the entire amount due by means of

a cheque.

Prepare Mohan's Capital account to be rendered to the executor and also pass a

journal entry for the settlement of the amount due to Mohan's executors.

(8)

ASSIGNMENT-4

SUBJECT – ACCOUNTANCY

CLASS – XII

MAX TIME: 3 HOUR MAX. MARKS: 80

Q1 At what rate of interest on call in advance may paid by a company according to Table F

of schedule I of Companies Act 2013. 1

Q 2 Why is ‗goodwill‘ considered an Intangible assets but not a ‗Fictitious Assets‘? 1

Q 3 Kajal, Neerav and Alisha are partners in a firm sharing profit in the ratio of 3:2:1. They

decided to admit Rajan, their landlord as a partner in the firm. Rajan brought sufficient

amount of capital and his share of goodwill premium. The accountant of the firm

passed the entry of rent paid for the building to Rajan in Profit and loss Appropriation

Account. Is he correct in doing so? Give reason in support of your answer.

1

Q 4 A, B and C were partners in a firm sharing profits and losses in the ratio of 3:2:1. On

1st January 2014, A died due to heart attack so B and C decided to admit D, A‘s son as

a partner in the firm for 1/5th

share of profit. On this date General Reserve appeared in

the books of the firm at Rs. 24, 000. It was decided to keep 25% of General Reserve as

provision for doubtful debts. Pass journal entry for recording General Reserve. The

new profit sharing ratio is 2:1:1.

1

Q 5 Journalise if Securities Premium Reserve is used to issue bonus shares. 1

Q 6 If creditors amounting to Rs. 4,000 took over furniture of Rs. 3,000 during dissolution

of the firm then what entry will be passed? 1

Q 7 What share of profit would a sleeping partner will get who has contributed 75% of the

total capital, get in the absence of partnership deed 1

Q 8 Pass the journal entry when 10,000 debentures of Rs.100 each are issued as collateral

security against a bank loan of Rs 8,00,000. 1

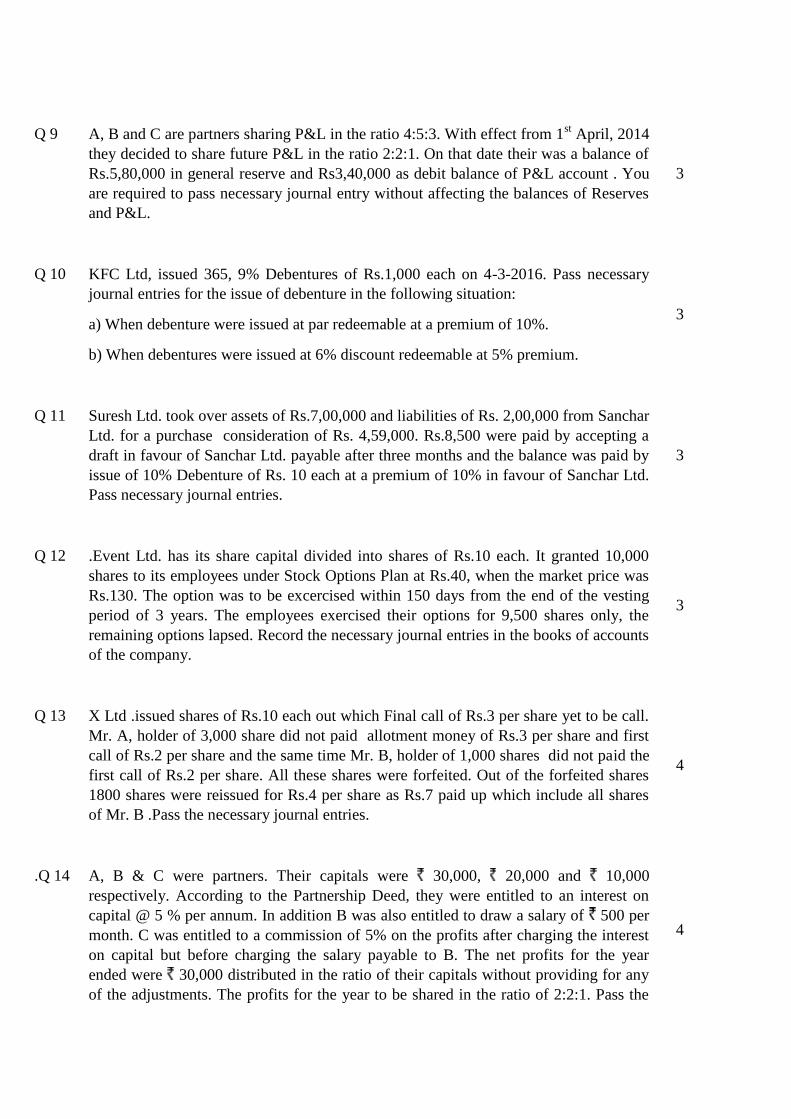

Q 9 A, B and C are partners sharing P&L in the ratio 4:5:3. With effect from 1st April, 2014

they decided to share future P&L in the ratio 2:2:1. On that date their was a balance of

Rs.5,80,000 in general reserve and Rs3,40,000 as debit balance of P&L account . You

are required to pass necessary journal entry without affecting the balances of Reserves

and P&L.

3

Q 10 KFC Ltd, issued 365, 9% Debentures of Rs.1,000 each on 4-3-2016. Pass necessary

journal entries for the issue of debenture in the following situation:

a) When debenture were issued at par redeemable at a premium of 10%.

b) When debentures were issued at 6% discount redeemable at 5% premium.

3

Q 11 Suresh Ltd. took over assets of Rs.7,00,000 and liabilities of Rs. 2,00,000 from Sanchar

Ltd. for a purchase consideration of Rs. 4,59,000. Rs.8,500 were paid by accepting a

draft in favour of Sanchar Ltd. payable after three months and the balance was paid by

issue of 10% Debenture of Rs. 10 each at a premium of 10% in favour of Sanchar Ltd.

Pass necessary journal entries.

3

Q 12 .Event Ltd. has its share capital divided into shares of Rs.10 each. It granted 10,000

shares to its employees under Stock Options Plan at Rs.40, when the market price was

Rs.130. The option was to be excercised within 150 days from the end of the vesting

period of 3 years. The employees exercised their options for 9,500 shares only, the

remaining options lapsed. Record the necessary journal entries in the books of accounts

of the company.

3

Q 13 X Ltd .issued shares of Rs.10 each out which Final call of Rs.3 per share yet to be call.

Mr. A, holder of 3,000 share did not paid allotment money of Rs.3 per share and first

call of Rs.2 per share and the same time Mr. B, holder of 1,000 shares did not paid the

first call of Rs.2 per share. All these shares were forfeited. Out of the forfeited shares

1800 shares were reissued for Rs.4 per share as Rs.7 paid up which include all shares

of Mr. B .Pass the necessary journal entries.

4

.Q 14 A, B & C were partners. Their capitals were 30,000, 20,000 and 10,000

respectively. According to the Partnership Deed, they were entitled to an interest on

capital @ 5 % per annum. In addition B was also entitled to draw a salary of 500 per

month. C was entitled to a commission of 5% on the profits after charging the interest

on capital but before charging the salary payable to B. The net profits for the year

ended were 30,000 distributed in the ratio of their capitals without providing for any

of the adjustments. The profits for the year to be shared in the ratio of 2:2:1. Pass the

4

necessary adjustment entry showing the workings clearly.

Q 15 On 1st

April 2012, Vishwas Ltd. was formed with an authorized capital of Rs.

10,00,000 divided into 1,00,000 equity shares of Rs. 10 each. The company issued

prospectus inviting applications for 90,000 equity shares. The company received

applications for 85,000 shares equity shares. During the first year Rs.8 per share called.

Ram holding 1,000 shares and Shyam holding 2,000 shares did not pay the first call of

Rs. 2 per share. Shyam‘ share were forfeited after the first call and later on 1500 shares

of the forfeited shares were reissued at Rs.6 per share, Rs 8 called up.

Show the following:

a) Share Capital in the Balance Sheet of the company as per schedule III Part I of

the companies Act 2013.

b) Also prepare notes to accounts..

4

Q 16 a) Write difference between Dissolution of partnership and Dissolution of firm.

b) The average profit earned by a firm is 80,000 which includes undervaluation of

stock Rs 8,000 on an average basis. The capital invested in the business is 8,00,000

and the normal rate of return is 8%. Calculate goodwill of the firm on the basis of 7

times the super profit.

2+2

Q 17 Ganga and Harry are partners in a firm sharing profits and losses in 5:3. They admit

Chandrika, the widow of their friend, into partnership for ¼ share. As between

themselves, Ganga and Harry decide to share profits equally in future.

Chandrika brings in ₹60,000 as her capital and unable to bring in her share of premium

for goodwill. For this purpose a current account has to be opened. Calculate the

sacrificing ratio and pass journal entries.

4

Q 18 A,B and C were partners in a firm sharing profit in the ratio of 5:3:2. On 31st March

2015 their Balance Sheet as under:

Liabilities Rs Assets Rs

Creditors 7,000 Building 20,000

Reserves 10,000 Machinery 30,000

Capital A/cs

A 30,000

B 25,000

C 15,000 70,000

Stock 10,000

Patents 6,000

Debtors 8,000

Cash 13,000

6

-----------

Total 87,000 Total 87,000

B died on 1st October 2015. It was agreed between his executors and the remaining

partners that:

i) Goodwill be valued at two year purchase of average profit of the previous 5 years,

which were 2011:Rs 15,000, 2012:Rs 13,000, 2013:Rs 12,000, 2014:Rs 15,000 and

2015: Rs 20,000

ii) Patents be valued at Rs 8,000, Machinery at Rs 28,000 and Building at Rs 30,000

iii) Profit for the year 2015-16 be taken as having accrued at the same rate as in

previous year.

iv) Interest on Capital be provided at 10% p.a.

Prepare B‘s Capital account and Rs 4250 was immediately paid to his executors.

Q 19 Archana, Suresh and Deepak are partners in a firm. On 1st April 2011 the balance in

their capital accounts stood at Rs.6,00,000 ,Rs5,00,000 and Rs.4,00,000 respectively.

They shared profits in the ratio and 4:2:3. Partners are entitled to interest on capital @

7% p.a. and salary to Suresh @ Rs10,000 per quarter and a commission of Rs2,000p.m.

to Deepak as per the provision of the partnership deed. Suresh‘s share of profit

excluding interest on capital is guaranteed at Rs. 30,000p.a.Deepak‘s share of profit

including interest on capital but excluding salary is guaranteed at Rs.60,000 p.a. Any

deficiency arising on that account shall be met by Archana. The profit of the firm for

the year ended 31st March 2012 amounted to Rs.2,59,000. Prepare Profit and loss

Appropriation Account.

6

Q 20 A, B and C were in a partnership sharing profits in proportion to their capitals. Their

Balance Sheet as at 31.03.2015 was as follows:

Liabilities Rs Assets Rs

Creditors 15,600 Cash 16,000

Reserve 6,000 Debtors 20,000

19,600

A‘s Capital 90,000 Less: Prov for

B‘s Capital 60,000 Doubtful debts 400

C‘s Capital 30,000 Stock 18,000

Machinery 48,000

Buildings 1,00,000

2,01,600 2,01,600

On the above date B retired

Goodwill of the firm be valued at Rs 36,000 and be adjusted into the Capital Account

of A and C who share the profits in the ratio of 3:2.

Fill in the missing information in the Revaluation Account, Partner‘s Capital Accounts

and the Balance Sheet of the new firm after B‘s retirement.

6

Revaluation Account

Particulars Rs Particulars Rs

To Provision for Doubtful Debts 600 By Building 10,000

To ______________ _____ By_______ ______

To ___________________ _____ By ______ ______

To Profit transferred to:

A‘s Capital A/c ______

B‘s Capital A/c _______

C‘s Capital A/c _______ _____

Total _____ _____

Capital Accounts

Particulars A B C Particulars A B C

To B‘s Capital A/c

(Goodwill)

------ ------ By Bal b/d ------ ------ ------

To Cash A/c 9,000 By _____ ------ ------ ------

To B‘s Loan A/c ------ By _____ ------ ------ ------

To bal c/d ------ ------ By A‘s Capital

A/c (Goodwill)

------

By C‘s Capital

A/c (Goodwill)

-------

Total ------ ------- ------ Total ------ ------- -----

Balance Sheet

As at 31st March, 2015

Liabilities Rs Assets Rs

Creditors 13,800 Cash -------

Provision for Repairs 3,000 Debtors 20,000

Less: Provision for 1,000

Doubtful Debts 19,000

B‘s Loan --------

Capitals:

A ---------

C --------- -------

Stock -------

Machinery 40,800

Buildings ------

Prepaid Insurance 2,000

Total ------- Total --------

Q 21 Pass necessary journal entries for the following transactions on the dissolution of the

firm of Parul, Payal and Priyanka after the various assets and outside liabilities have

been transferred to realisation account.

(i) There were total debtors of Rs. 76,000. A provision for doubtful debts also stood in

the books at Rs. 6,000. Rs.12,000 debtors proved bad and rest paid the due amount.

(ii) Parul agreed to pay her husband‘s loan of Rs. 7,000 at a discount of 5%.

(iii) Unrecorded asset was taken by Payal at Rs. 3,000.

(iv) The firm had a debit balance of Rs. 27,000 in the Profit & Loss account on the date

6

of dissolution.

(v) A contingent liability (not provided for) of Rs. 4,000 was also discharged.

(vi) Priyanka was to get a remuneration of Rs. 18,000 for completing the dissolution

process

Q 22 A, B and C are partners sharing profit & losses in the ratio of 2:2:1. They agreed to

dissolve the firm. The Balance Sheet of the firm at that date was as follows:

Liabilities Rs Assets Rs

Bank Overdraft 4,000 Debtors 40,000

Creditors 30,000 Stock 50,000

B/P 6,000 Furniture 2,000

B‘s Wife Loan 10,000 Fixed Assets 49,000

Capital A/c s

A 70,000

B 70,000 1,40,000

Prepaid Expenses 1,000

Profit & Loss A/c 40,000

C‘s Capital 8,000

Total 1,90,000 Total 1,90,000

1. Assets realized as follows: Stock Rs 32,000; Fixed Assets Rs 45,000 and full amount

was received from Debtors.

2. A agreed to take over furniture at Rs 1,600 and also agrees to make the payment of

B/P.

3. B agreed to discharge his wife‘s loan.

4. There was an unrecorded assets of Rs 10,000, which was taken over by C at Rs

7,000.

5. A B/R for Rs 5,000 was received from a customer Mohan and the bill was

discounted from the bank. Mohan become insolvent and 60 paise per rupee has been

received from his estate.

6. Creditors were paid at a discount of Rs 1,500.

Prepare Realisation Account and Capital Accounts.

OR

X and Y were partners in a firm sharing profits in 3:1 ratio. They admitted Z as a new

partner for 1/4th share in the profits. Z was to bring Rs.20,000 as his capital and the

capitals of X and y were to be adjusted on the basis of Z‘s capital in the profit sharing

ratio. The balance sheet of X and Y on 31.3.2006 was as follows:

8

Liabilities Amount Assets Amount

Sundry Creditors 18,000 Cash 5,000

Bills Payable 10,000 Debtors 17,000

General Reserve 12,000 Stock 12,000

Capitals :

X 25,000

Y 10,000 35,000

Machinery 21,000

Building 20,000

75,000 75,000

Other terms of agreement on Z‘s admission were as follows:

(i) Z will bring Rs.6,000 for his share of goodwill.

(ii) Building will be valued at Rs.25,000 and Machinery at Rs.19,000.

(iii)A Provision at 5% on debtors will be created for bad debts.

(iv)Capital accounts of X and y were adjusted by opening current accounts.

Prepare Revaluation A/c, Partners Capital A/cs and Balance Sheet of new firm.

Q 23 Z Ltd. invited applications for issuing 70,000 Equity Shares of Rs. 10

each at par. The amount was payable as follows:

On application—Rs. 4 per share

On allotment---- Rs. 4 per share

On first and final call--- Balance

Applications for 80,000 shares were received. Applications for 5,000 shares were

rejected and the shares were allotted on pro rata basis to the remaining applicants.

Excess money received with applications were utilized towards sum due on allotment.

Jonney, who had applied for 1,500 shares, failed to pay the allotment money, his shares

were forfeited immediately after allotment. Afterwards the first & final call was made.

First & final call was not received on 700 shares held by Rommy. Her shares were also

forfeited. 1,500 forfeited shares (including 100 shares of Rommy ) were reissued at Rs.

13 per share fully paid-up. The reissued shares included all the shares of Jonney.

OR

Hari Limited issued a prospectus inviting applications for 20,000 shares of

Rs.10 each at a premium of Rs.2 per share payable as follows:

On application - Rs.2

On allotment - Rs.5 (including premium)

8

On first call - Rs.3

On second & final call- Rs.2

Applications were received for 30,000 shares and pro-rata allotment was made on the

applications for 24,000 shares. Money overpaid on applications was employed on

account of sum due on allotment. Ramesh to whom 400 shares were allotted, failed to

pay the allotment money and on his subsequent failure to pay the first call, his shares

were forfeited. Mohan, the holder of 600 shares, failed to pay the two calls, and his

shares were forfeited after the second call. Of the shares forfeited, 800 shares were sold

to Krishna credited as fully paid for Rs.9 per share, the whole of Ramesh‘s share being

included. Show journal entries.

HALF YEARLY EXAMINATION (2016-17)

SUBJECT – ACCOUNTANCY (SET-II)

CLASS – XII

MAX TIME: 3 HOUR MAX. MARKS: 80

Q1 Why is ‗goodwill‘ considered an Intangible assets but not a ‗Fictitious Assets‘? 1

Q 2 Kajal, Neerav and Alisha are partners in a firm sharing profit in the ratio of 3:2:1. They

decided to admit Rajan, their landlord as a partner in the firm. Rajan brought sufficient

amount of capital and his share of goodwill premium. The accountant of the firm

passed the entry of rent paid for the building to Rajan in Profit and loss Appropriation

Account. Is he correct in doing so? Give reason in support of your answer.

1

Q 3 A, B and C were partners in a firm sharing profits and losses in the ratio of 3:2:1. On

1st January 2014, A died due to heart attack so B and C decided to admit D, A‘s son as

a partner in the firm for 1/5th

share of profit. On this date General Reserve appeared in

the books of the firm at Rs. 24, 000. It was decided to keep 25% of General Reserve as

provision for doubtful debts. Pass journal entry for recording General Reserve. The

new profit sharing ratio is 2:1:1.

1

Q 4 Journalise if Securities Premium Reserve is used to issue bonus shares. 1

Q 5 If creditors amounting to Rs. 4,000 took over furniture of Rs. 3,000 during dissolution

of the firm then what entry will be passed? 1

Q 6 What share of profit would a sleeping partner will get who has contributed 75% of the

total capital, get in the absence of partnership deed 1

Q 7 Pass the journal entry when 10,000 debentures of Rs.100 each are issued as collateral

security against a bank loan of Rs 8,00,000. 1

Q 8 At what rate of interest on call in advance may paid by a company according to Table F

of schedule I of Companies Act 2013. 1

Q 9 KFC Ltd, issued 365, 9% Debentures of Rs.1,000 each on 4-3-2016. Pass necessary

journal entries for the issue of debenture in the following situation:

a) When debenture were issued at par redeemable at a premium of 10%.

b) When debentures were issued at 6% discount redeemable at 5% premium.

3

Q 10 Suresh Ltd. took over assets of Rs.7,00,000 and liabilities of Rs. 2,00,000 from Sanchar

Ltd. for a purchase consideration of Rs. 4,59,000. Rs.8,500 were paid by accepting a

draft in favour of Sanchar Ltd. payable after three months and the balance was paid by

issue of 10% Debenture of Rs. 10 each at a premium of 10% in favour of Sanchar Ltd.

Pass necessary journal entries.

3

Q 11 .Event Ltd. has its share capital divided into shares of Rs.10 each. It granted 10,000

shares to its employees under Stock Options Plan at Rs.40, when the market price was

Rs.130. The option was to be excercised within 150 days from the end of the vesting

period of 3 years. The employees exercised their options for 9,500 shares only, the

remaining options lapsed. Record the necessary journal entries in the books of accounts

of the company.

3

Q 12 A, B and C are partners sharing P&L in the ratio 4:5:3. With effect from 1st April, 2014

they decided to share future P&L in the ratio 2:2:1. On that date their was a balance of

Rs.5,80,000 in general reserve and Rs3,40,000 as debit balance of P&L account . You

are required to pass necessary journal entry without affecting the balances of Reserves

and P&L.

3

Q 13 A, B & C were partners. Their capitals were 30,000, 20,000 and 10,000

respectively. According to the Partnership Deed, they were entitled to an interest on

capital @ 5 % per annum. In addition B was also entitled to draw a salary of 500 per

month. C was entitled to a commission of 5% on the profits after charging the interest

on capital but before charging the salary payable to B. The net profits for the year

ended were 30,000 distributed in the ratio of their capitals without providing for any

of the adjustments. The profits for the year to be shared in the ratio of 2:2:1. Pass the

necessary adjustment entry showing the workings clearly.

4

.Q 14 On 1st

April 2012, Vishwas Ltd. was formed with an authorized capital of Rs.

10,00,000 divided into 1,00,000 equity shares of Rs. 10 each. The company issued

prospectus inviting applications for 90,000 equity shares. The company received

applications for 85,000 shares equity shares. During the first year Rs.8 per share called.

Ram holding 1,000 shares and Shyam holding 2,000 shares did not pay the first call of

Rs. 2 per share. Shyam‘ share were forfeited after the first call and later on 1500 shares

4

of the forfeited shares were reissued at Rs.6 per share, Rs 8 called up.

Show the following:

a) Share Capital in the Balance Sheet of the company as per schedule III Part I of

the companies Act 2013.

b) Also prepare notes to accounts..

Q 15 a) Write difference between Dissolution of partnership and Dissolution of firm.

b) The average profit earned by a firm is 80,000 which includes undervaluation of

stock Rs 8,000 on an average basis. The capital invested in the business is 8,00,000

and the normal rate of return is 8%. Calculate goodwill of the firm on the basis of 7

times the super profit.

2+2

Q 16 Ganga and Harry are partners in a firm sharing profits and losses in 5:3. They admit

Chandrika, the widow of their friend, into partnership for ¼ share. As between

themselves, Ganga and Harry decide to share profits equally in future.

Chandrika brings in ₹60,000 as her capital and unable to bring in her share of premium

for goodwill. For this purpose a current account has to be opened. Calculate the

sacrificing ratio and pass journal entries.

4

Q 17 X Ltd .issued shares of Rs.10 each out which Final call of Rs.3 per share yet to be call.

Mr. A, holder of 3,000 share did not paid allotment money of Rs.3 per share and first

call of Rs.2 per share and the same time Mr. B, holder of 1,000 shares did not paid the

first call of Rs.2 per share. All these shares were forfeited. Out of the forfeited shares

1800 shares were reissued for Rs.4 per share as Rs.7 paid up which include all shares

of Mr. B .Pass the necessary journal entries.

4

Q 18 Archana, Suresh and Deepak are partners in a firm. On 1st April 2011 the balance in

their capital accounts stood at Rs.6,00,000 ,Rs5,00,000 and Rs.4,00,000 respectively.

They shared profits in the ratio and 4:2:3. Partners are entitled to interest on capital @

7% p.a. and salary to Suresh @ Rs10,000 per quarter and a commission of Rs2,000p.m.

to Deepak as per the provision of the partnership deed. Suresh‘s share of profit

excluding interest on capital is guaranteed at Rs. 30,000p.a.Deepak‘s share of profit

including interest on capital but excluding salary is guaranteed at Rs.60,000 p.a. Any

deficiency arising on that account shall be met by Archana. The profit of the firm for

the year ended 31st March 2012 amounted to Rs.2,59,000. Prepare Profit and loss

Appropriation Account.

6

Q 19 A, B and C were in a partnership sharing profits in proportion to their capitals. Their

Balance Sheet as at 31.03.2015 was as follows:

Liabilities Rs Assets Rs

6

Creditors 15,600 Cash 16,000

Reserve 6,000 Debtors 20,000

19,600

A‘s Capital 90,000 Less: Prov for

B‘s Capital 60,000 Doubtful debts 400

C‘s Capital 30,000 Stock 18,000

Machinery 48,000

Buildings 1,00,000

2,01,600 2,01,600

On the above date B retired

Goodwill of the firm be valued at Rs 36,000 and be adjusted into the Capital Account

of A and C who share the profits in the ratio of 3:2.

Fill in the missing information in the Revaluation Account, Partner‘s Capital Accounts

and the Balance Sheet of the new firm after B‘s retirement.

Revaluation Account

Particulars Rs Particulars Rs

To Provision for Doubtful Debts 600 By Building 10,000

To ______________ _____ By_______ ______

To ___________________ _____ By ______ ______

To Profit transferred to:

A‘s Capital A/c ______

B‘s Capital A/c _______

C‘s Capital A/c _______ _____

Total _____ _____

Capital Accounts

Particulars A B C Particulars A B C

To B‘s Capital A/c

(Goodwill)

------ ------ By Bal b/d ------ ------ ------

To Cash A/c 9,000 By _____ ------ ------ ------

To B‘s Loan A/c ------ By _____ ------ ------ ------

To bal c/d ------ ------ By A‘s Capital

A/c (Goodwill)

------

By B‘s Capital

A/c (Goodwill)

-------

Total ------ ------- ------ Total ------ ------- -----

Balance Sheet

As at 31st March, 2015

Liabilities Rs Assets Rs

Creditors 13,800 Cash -------

Provision for Repairs 3,000 Debtors 20,000

Less: Provision for 1,000

Doubtful Debts 19,000

B‘s Loan --------

Capitals:

A --------- ------- Stock -------

C --------- Machinery 40,800

Buildings ------

Prepaid Insurance 2,000

Total ------- Total --------

Q 20 Pass necessary journal entries for the following transactions on the dissolution of the

firm of Parul, Payal and Priyanka after the various assets and outside liabilities have

been transferred to realisation account.

(i) There were total debtors of Rs. 76,000. A provision for doubtful debts also stood in

the books at Rs. 6,000. Rs.12,000 debtors proved bad and rest paid the due amount.

(ii) Parul agreed to pay her husband‘s loan of Rs. 7,000 at a discount of 5%.

(iii) Unrecorded asset was taken by Payal at Rs. 3,000.

(iv) The firm had a debit balance of Rs. 27,000 in the Profit & Loss account on the date

of dissolution.

(v) A contingent liability (not provided for) of Rs. 4,000 was also discharged.

(vi) Priyanka was to get a remuneration of Rs. 18,000 for completing the dissolution

process.

6

Q 21 A,B and C were partners in a firm sharing profit in the ratio of 5:3:2. On 31st March

2015 their Balance Sheet as under:

Liabilities Rs Assets Rs

Creditors 7,000 Building 20,000

Reserves 10,000 Machinery 30,000

Capital A/cs

A 30,000

B 25,000

C 15,000

----------- 70,000

Stock 10,000

Patents 6,000

Debtors 8,000

Cash 13,000

Total 87,000 Total 87,000

B died on 1st October 2015. It was agreed between his executors and the remaining

partners that:

i) Goodwill be valued at two year purchase of average profit of the previous 5 years,

which were 2011:Rs 15,000, 2012:Rs 13,000, 2013:Rs 12,000, 2014:Rs 15,000 and

2015: Rs 20,000

ii) Patents be valued at Rs 8,000, Machinery at Rs 28,000 and Building at Rs 30,000

6

iii) Profit for the year 2015-16 be taken as having accrued at the same rate as in

previous year.

iv) Interest on Capital be provided at 10% p.a.

Prepare B‘s Capital account and Rs 4250 was immediately paid to his executors.

Q 22 Z Ltd. invited applications for issuing 70,000 Equity Shares of Rs. 10

each at par. The amount was payable as follows:

On application—Rs. 4 per share

On allotment---- Rs. 4 per share

On first and final call--- Balance

Applications for 80,000 shares were received. Applications for 5,000 shares were

rejected and the shares were allotted on pro rata basis to the remaining applicants.

Excess money received with applications were utilized towards sum due on allotment.

Jonney, who had applied for 1,500 shares, failed to pay the allotment money, his shares

were forfeited immediately after allotment. Afterwards the first & final call was made.

First & final call was not received on 700 shares held by Rommy. Her shares were also

forfeited. 1,500 forfeited shares (including 100 shares of Rommy ) were reissued at Rs.

13 per share fully paid-up. The reissued shares included all the shares of Jonney.

OR

Hari Limited issued a prospectus inviting applications for 20,000 shares of

Rs.10 each at a premium of Rs.2 per share payable as follows:

On application - Rs.2

On allotment - Rs.5 (including premium)

On first call - Rs.3

On second & final call- Rs.2

Applications were received for 30,000 shares and pro-rata allotment was made on the

applications for 24,000 shares. Money overpaid on applications was employed on

account of sum due on allotment. Ramesh to whom 400 shares were allotted, failed to

pay the allotment money and on his subsequent failure to pay the first call, his shares

were forfeited. Mohan, the holder of 600 shares, failed to pay the two calls, and his

shares were forfeited after the second call. Of the shares forfeited, 800 shares were sold

to Krishna credited as fully paid for Rs.9 per share, the whole of Ramesh‘s share being

included. Show journal entries.

8

Q 23 A, B and C are partners sharing profit & losses in the ratio of 2:2:1. They agreed to

dissolve the firm. The Balance Sheet of the firm at that date was as follows: 8

Liabilities Rs Assets Rs

Bank Overdraft 4,000 Debtors 40,000

Creditors 30,000 Stock 50,000

B/P 6,000 Furniture 2,000

B‘s Wife Loan 10,000 Fixed Assets 49,000

Capital A/c s

A 70,000

B 70,000 1,40,000

Prepaid Expenses 1,000

Profit & Loss A/c 40,000

C‘s Capital 8,000

Total 1,90,000 Total 1,90,000

1. Assets realized as follows: Stock Rs 32,000; Fixed Assets Rs 45,000 and full amount

was received from Debtors.

2. A agreed to take over furniture at Rs 1,600 and also agrees to make the payment of

B/P.

3. B agreed to discharge his wife‘s loan.

4. There was an unrecorded assets of Rs 10,000, which was taken over by C at Rs

7,000.

5. A B/R for Rs 5,000 was received from a customer Mohan and the bill was

discounted from the bank. Mohan become insolvent and 60 paise per rupee has been

received from his estate.

6. Creditors were paid at a discount of Rs 1,500.

Prepare Realisation Account and Capital Accounts.

OR

X and Y were partners in a firm sharing profits in 3:1 ratio. They admitted Z as a new

partner for 1/4th share in the profits. Z was to bring Rs.20,000 as his capital and the

capitals of X and y were to be adjusted on the basis of Z‘s capital in the profit sharing

ratio. The balance sheet of X and Y on 31.3.2006 was as follows:

Liabilities Amount Assets Amount

Sundry Creditors 18,000 Cash 5,000

Bills Payable 10,000 Debtors 17,000

General Reserve 12,000 Stock 12,000

ASSIGNMENT- 5

ACOUNTANCY – XII

TIME : 3 Hrs.

M.M:- 80

General Instructions :-

This paper contains two parts, A and B.

Both parts are compulsory.

All parts of a question should be attempted at one place.

PART:- A

PARTNERSHIP ACCOUNTS

Q1. Why are ―Reserves and Surplus‖ distributed at the time of reconstitution of the firm?

1

Q2. State with reason whether at the time of Admission of a partner, partnership is

dissolved or partnership firm is dissolved.

1

Q3. State any two items of deductions that may have to be made from the amount payable

to a retiring partner.

1

Q4. What do you understand by reconstitution of a partnership firm?

1

Q5. Name the account which is opened to credit the share of profit of the deceased

partner, till the time of his death to his account.

1

Q6. What is the difference between gaining ratio and sacrificing ratio?

1

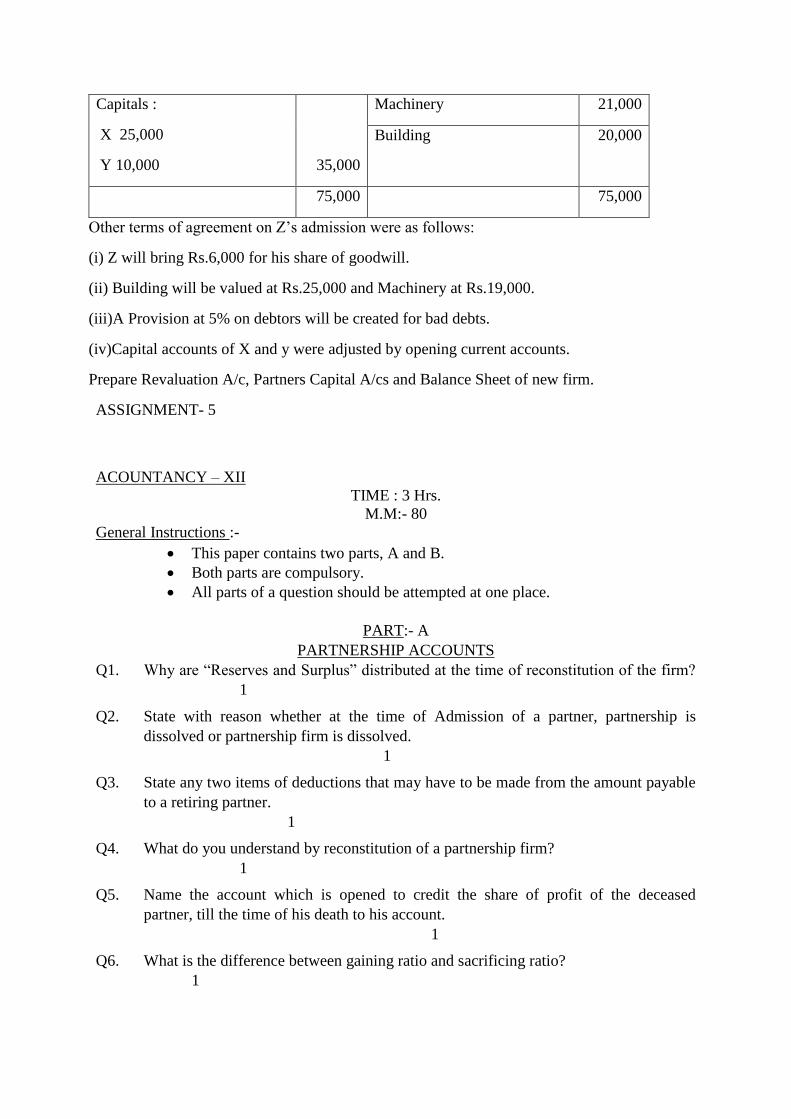

Capitals :

X 25,000

Y 10,000 35,000

Machinery 21,000

Building 20,000

75,000 75,000

Other terms of agreement on Z‘s admission were as follows:

(i) Z will bring Rs.6,000 for his share of goodwill.

(ii) Building will be valued at Rs.25,000 and Machinery at Rs.19,000.

(iii)A Provision at 5% on debtors will be created for bad debts.

(iv)Capital accounts of X and y were adjusted by opening current accounts.

Prepare Revaluation A/c, Partners Capital A/cs and Balance Sheet of new firm.

Q7. X, Y and Z are sharing profits and losses in the ratio of 5:3:2. They decided to share

future profits and losses in the ratio of 2:3:5 with effect from 1st April 2015. They also

decide to record the effect of the following accumulated profits, losses and reserves

without affecting their book figures by passing a single entry.

3

Advertisement Suspense A/C ` 24,000

Profit and Loss A/C (Credit) ` 48,000

General Reserve ` 12,000

Q8. Hari, Ravi and Kavi were partners in a firm sharing profits in the ratio of 3:3:1. They

admitted Guru as a new partner for 1/7th

share in the profits. The new profit sharing

ratio will be 2:2:2:1 respectively. Guru brought in `3,00,000 for his capital and `

45,000 for his 1/7th

share of goodwill. Showing your working clearly, pass necessary

Journal entries in the books of the firm for the above mentioned transactions. 3

Q9. A partnership firm earned net profits during the last three years as follows:

3

Years Net Profits

`

2007-2008 1,90,000

2008-2009 2,20,000

2009-2010 2,50,000

The capital employed in the firm throughout the above mentioned period has been `

4,00,000. Having regard to the risk involved, 15% is considered to be a fair return on

the capital. The remuneration of all the partners during this period is estimated to be `

1,00,000 per annum.

Calculate the value of goodwill on the bases of (i) two year‘s purchase of super profits

earned on average basis during the above mentioned three years and (ii) by

capitalisation method.

Q10. Nandan. John, and Rosa are partners sharing profits in the ratio of 4:3:2. On 1st April

2012, John gave a notice to retire from the firm. Nandan and Rosa decided to share

future profits in the ratio of 1:1. The Capital accounts of Nandan and Rosa after all

adjustments showed a balance of 43,000 and 80,500 respectively. The total amount

to be paid to john was 95,500. This amount was to be paid by Nandan and Rosa in

such a way that their capitals become proportionate to their new profit sharing ratio.

3

Pass necessary Journal entries in the books of the firm for the above transactions

Show your working clearly.

Q11. A, B and C are partners in a firm which is engaged in the manufacturing of shoes.

They offer a discount of 30% on shoes for the school children belonging to the below

poverty line category. On 1st January 2011, their capitals stood at 3,00,000;

1,50,000 and 1,50,000 respectively. As per the deed: 4

a) C is entitled to a salary of 30,000 p.a.

b) Partners are entitled to interest on capital @5% p.a.

c) Profits are shared in the ratio of partners‘ capitals.

The net profit for the year 2011 of 1,80,000 was distributed equally without

providing for the above terms.

i) Pass an adjustment entry in the journal to rectify the above error

ii) Identify the values that were affected.

Q12. A,B and C are sharing profits in the ratio of 2:2:1. B died on 30th

June, 2015.

Accounts are closed on 31st March. Sales for the year ended 31

st March, 2015

amounted to ` 3,00,000. Sales of ` 1,00,000 amounted between the period from 1st

April,2015 to 30th

June, 2015. The profits for the year ended 31st March, 2015

amounted to ` 30,000. Remaining partners decided to admit D for 1/5th

share in the

firm. 4

a) Calculate deceased partner‘s share in the profits of the firm.

b) Find new profit sharing ratio of A, C and D.

Q13. Pass the necessary journal entries for the following transactions on the dissolution of

the firm of Sudha and Shiva after the various assets (other than cash) and outside

liabilities have been transferred to realisation Account:

6

i). Sudha agreed to pay off her husband‘s loan `19,000.

ii) A Debtor whose debt of `9,000 was written off in the books paid `7,500 in full

settlement.

iii) Shiva took over all investments at ` 13,300.

iv) Sundry creditors ` 10,000 were paid at 9% discount.

v) Realisation expenses ` 3,400 were paid by Sudha for which she was allowed ` 3,000.

vi) Loss on realisation ` 9,400 was divided between Sudha and Shiva in 3:2 ratio.

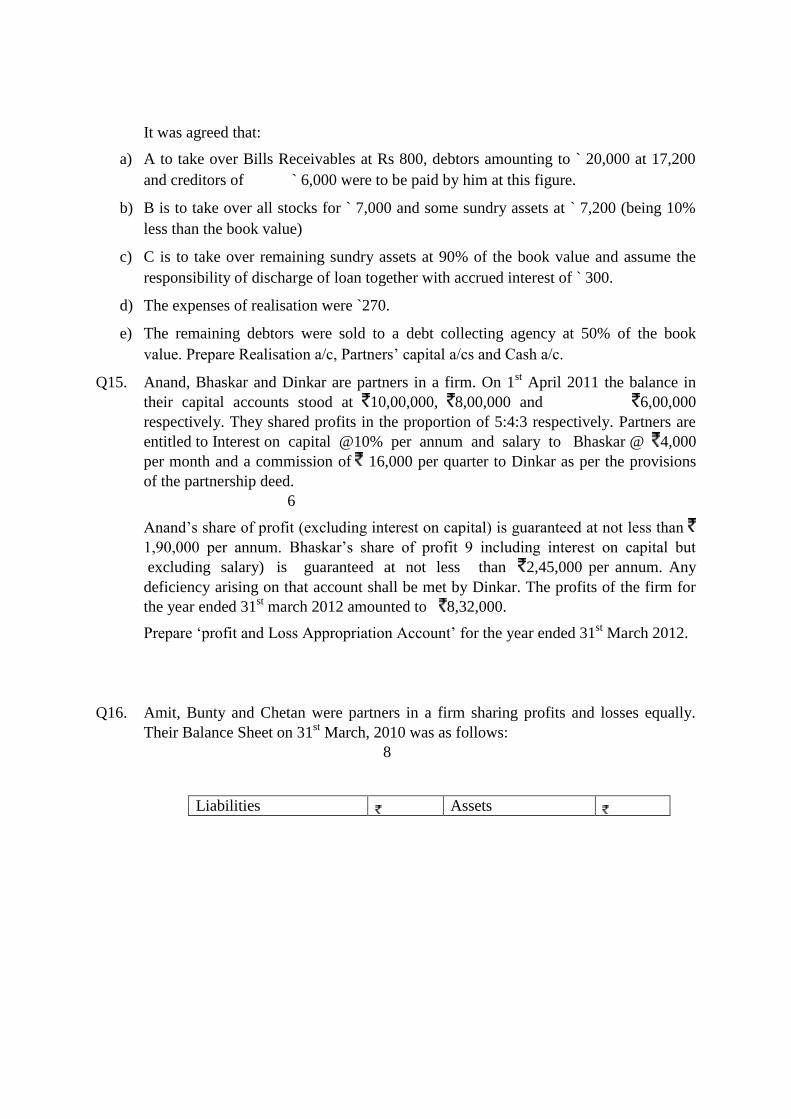

Q14. A, B and C were partners sharing profits in the ratio of 3:1:1. Their balance sheet as

on 31st March 2009, the date on which they dissolve their firm was as follows:

6

Liabilities Amount

`

Assets Amount

`

Capitals Sundry Assets 17,000

A-27,500 Stock 7,800

B-10,000 Debtors 24,200

C-17,000 44,500 Less

provision

11,200

Loan 1,500 for doubtful debts 23,000

Creditors 6,000 Bills Receivables 1,000

Cash 3,200

52,000 52,000

It was agreed that:

a) A to take over Bills Receivables at Rs 800, debtors amounting to ` 20,000 at 17,200

and creditors of ` 6,000 were to be paid by him at this figure.

b) B is to take over all stocks for ` 7,000 and some sundry assets at ` 7,200 (being 10%

less than the book value)

c) C is to take over remaining sundry assets at 90% of the book value and assume the

responsibility of discharge of loan together with accrued interest of ` 300.

d) The expenses of realisation were `270.

e) The remaining debtors were sold to a debt collecting agency at 50% of the book

value. Prepare Realisation a/c, Partners‘ capital a/cs and Cash a/c.

Q15. Anand, Bhaskar and Dinkar are partners in a firm. On 1st April 2011 the balance in

their capital accounts stood at 10,00,000, 8,00,000 and 6,00,000

respectively. They shared profits in the proportion of 5:4:3 respectively. Partners are

entitled to Interest on capital @10% per annum and salary to Bhaskar @ 4,000

per month and a commission of 16,000 per quarter to Dinkar as per the provisions

of the partnership deed.

6

Anand‘s share of profit (excluding interest on capital) is guaranteed at not less than