revise lecture 30 1. statement of cash flows – ias 7 2

TRANSCRIPT

1

Revise lecture 30

2

•Statement of cash flows – IAS 7

3

Statement of cash flows – IAS 7

• Although IAS 7 does not prescribe a format for statements of cash flows, it does require the cash flows to be classified into:

1. Operating activities2. Investing activities3. Financing activities

4

Adjustments to profit before tax

Depreciation

Depreciation is not a cash flow.

• Capital expenditure will be recorded under ‘investing activities’ at the time of the cash outflow.

• Depreciation has to be added back to reported profit in deriving cash from operating activities.

5

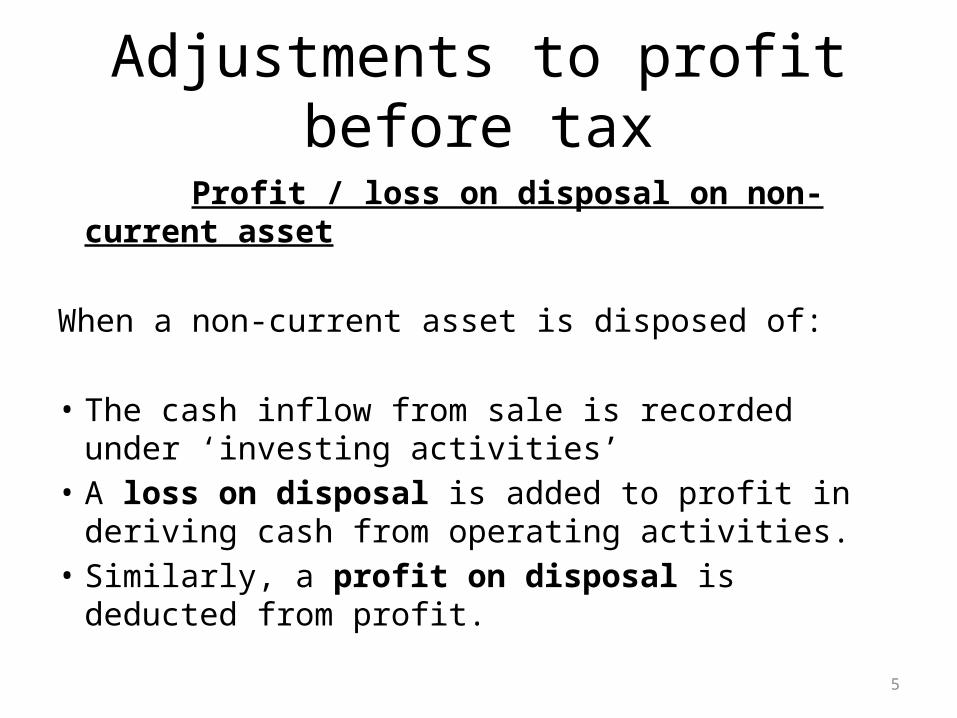

Adjustments to profit before tax

Profit / loss on disposal on non-current asset

When a non-current asset is disposed of:

• The cash inflow from sale is recorded under ‘investing activities’

• A loss on disposal is added to profit in deriving cash from operating activities.

• Similarly, a profit on disposal is deducted from profit.

6

Adjustments to profit before tax

Change in receivables

• An increase in receivables is a deduction from profit in deriving cash from operating activities.

• Similarly, a decrease in receivables is an addition to profit.

7

Adjustments to profit before tax

Change in inventory

• An increase in inventory is a deduction from profit in deriving cash from operating activities.

• Similarly, a decrease in inventory is an addition to profit.

8

Adjustments to profit before tax

Change in payables

• An increase in payables is an addition to profit in deriving cash from operating activities.

• Similarly, a decrease in payables is a deduction from profit

9

Adjustments to profit before tax

Interest paid and income taxes paid

The final adjustments to find cash flow from operating activities are:

• Deduct interest paid• Deduct interest element of finance lease

payments• Deduct income taxes paid

10

Investing activities

Investing cash flows include:

1. Cash paid for property, plant and equipment and other non-current assets

2. Cash received on the sale of property, plant and equipment and other non-current assets

3. Cash paid for investments in or loans to other entities

4. Dividends received on investments.

11

Financing activities

Financing cash flows comprise receipts or repayments of principal from or to external providers of financing including:

• Receipts from issuing shares or other equity instruments.

• Repayments of amounts borrowed (other than overdrafts)

12

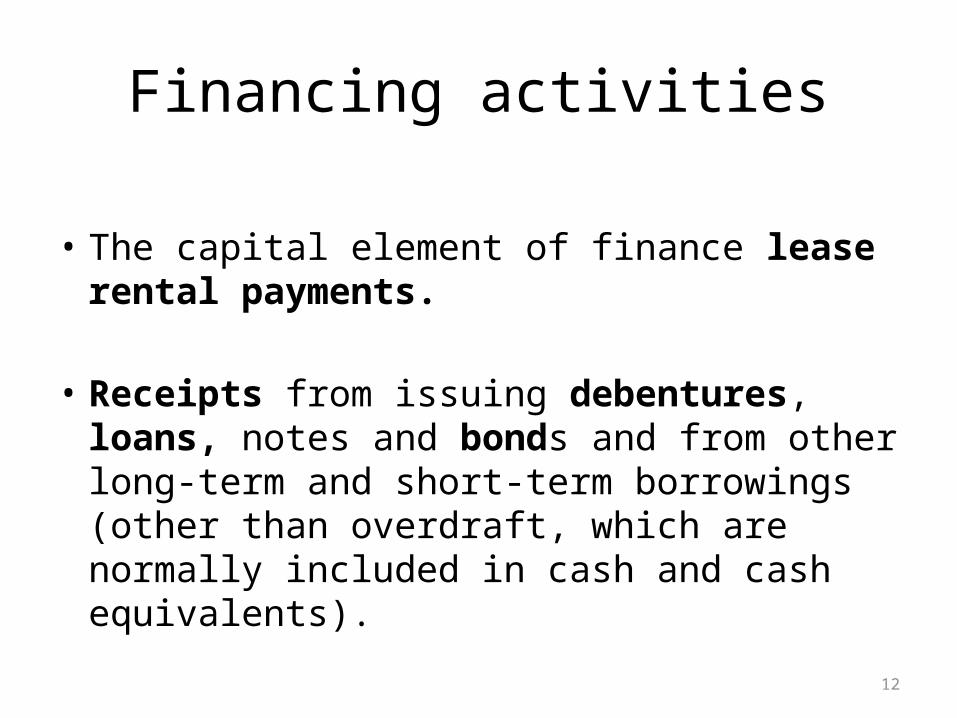

Financing activities

• The capital element of finance lease rental payments.

• Receipts from issuing debentures, loans, notes and bonds and from other long-term and short-term borrowings (other than overdraft, which are normally included in cash and cash equivalents).

13

Advantages of the statement of cash flows

• It may assist users of financial statements in making judgements on the amount, timing and degree of certainty of future cash flows.

• It gives an indication of the relationship between profitability and cash generating ability and thus of the quality of the profit earned.

14

Advantages of the statement of cash flows

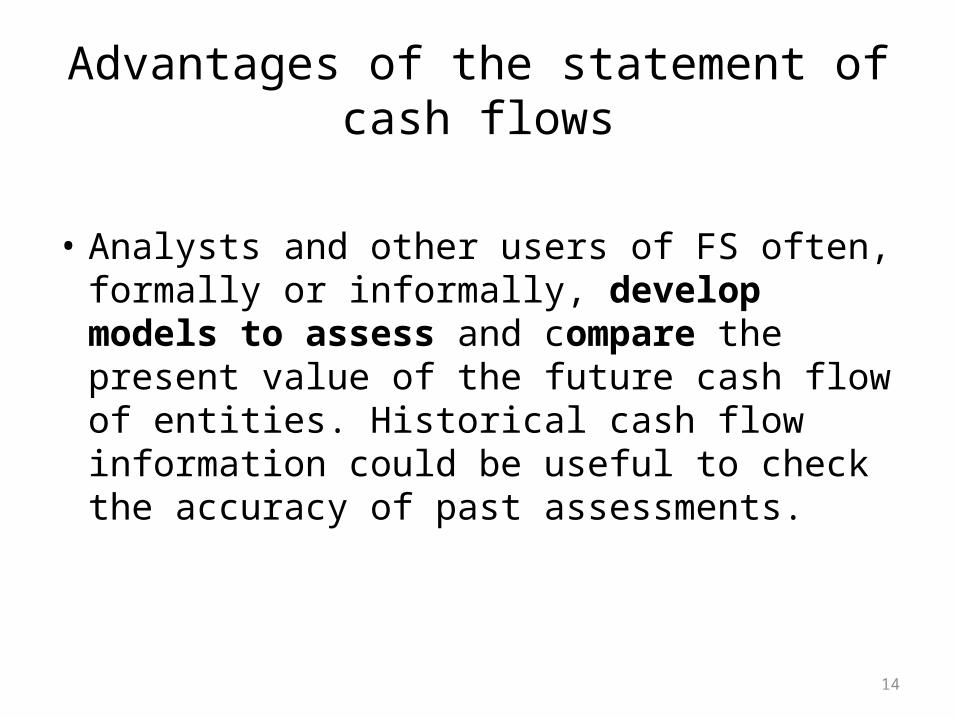

• Analysts and other users of FS often, formally or informally, develop models to assess and compare the present value of the future cash flow of entities. Historical cash flow information could be useful to check the accuracy of past assessments.

15

Advantages of the statement of cash flows

• A statement of cash flows in conjunction with a statement of financial position provides information on liquidity, viability and adaptability.

• Cash flows cannot be manipulated easily and are not affected by judgement or by accounting policies.

16

Interpretation of statements of cash flow

• The statement of cash flows should be reviewed after preparation. In particular, cash flows in the following areas should be reviewed:

1. Cash generation from trading operations2. Dividends and interest payments3. Capital expenditure4. Financial investment5. Management of financing6. Net cash flow

17

Limitations of the statement of cash flows

• Statements of cash flows are based on historical information and therefore do not provide complete information for assessing future cash flows.

• There is some scope for manipulation of cash flows, e.g. a business may delay paying suppliers until after the year end.

18

Limitations of the statement of cash flows

• Cash flow is necessary for survival in the short-term, but in order to survive in the long-term a business must be in profitable.

A huge cash balance is not a sign of good management if the cash could be invested elsewhere to generate profit.

19

• Principles of consolidated financial statements

20

Principles of consolidated financial statements

The concept of group accounts

What is a group? If one company owns more than 50% of the ordinary

shares of another company:

• This will usually give the first company ‘control’ of the second company.

• The first company (the parent company, P) has enough voting power to appoint all the directors of the second company (the subsidiary company, S).

21

Principles of consolidated financial statements

Group accounts The key principle undertaking group accounts is the need to reflect

the economic substance of the relationship.

• P is an individual legal entity.• S is an individual legal entity.• P controls S and therefore they from a single economic entity, the

group.

22

Principles of consolidated financial statements

The single economic unit concept The purpose of consolidated accounts is to:

1. Present financial information about a parent undertaking and its subsidiary undertakings as a single economic unit.

2. Show the economic resources controlled by the group.3. Show the obligations of the group.4. Show the results the group achieves with its resources.

23

• IFRS 10 consolidated financial statements

24

IFRS 10

IFRS 10 consolidated financial statements uses the following definitions:

• Parent: an entity that controls one or more entities

• Subsidiary: an entity that is controlled by another entity (known as the parent)

• Control of an investee: an investor controls an investee when the investor is exposed.

25

IFRS 10

• IFRS 10 outlines the circumstances in which a group is required to prepare consolidated financial statements.

• Consolidated financial statements should be prepared when the parent company has control over the subsidiary (control is usually established based on ownership of more than 50% of voting power).

26

IFRS 10

Control is identified by IFRS 10 as the sole basis for consolidation and comprises the following three elements:

1. Power over the investee2. Exposure, or rights, to variable returns from

its involvement with the investee3. The ability to use its power over the investee

to affect the amount of the investor’s returns

27

Exemption from preparation of group financial statements

• A parent need not present consolidated financial statements if and only if:

1. The parent itself is wholly owned subsidiary or a partially-owned subsidiary and its owners, have been informed about, and do not object to, the parent not preparing consolidated financial statements.

28

Exemption from preparation of group financial statements

2. The parent’s debt or equity instruments are not traded in a public market.

3. The parent did not file its financial statements with a securities commission or other regulatory organisation for the purpose of issuing any class of instruments in a public market.

29

Reasons for wanting to exclude a subsidiary

The directors of a parent company may not wish to consolidate some subsidiaries due to:

1. Poor performance of the subsidiary2. Poor financial position of the subsidiary3. Differing activities of the subsidiary from the

rest of the group.These reasons are not permitted according to

IFRSs.

30

Non-coterminous year ends

• Some companies in the group may have differing accounting dates. In practice such companies will often prepare financial statements up to the group accounting date for consolidation purposes.

• For the purpose of consolidation, IFRS 10 states that where the reporting date for a parent is different from that of a subsidiary, the subsidiary should prepare additional financial information as of the same date as the financial statements of the parent unless it is impracticable to do so.

31

Non-coterminous year ends

• If it is impracticable to do so, IFRS 10 allows use of subsidiary financial statements made up to a date of not more than three months earlier or later than the parent’s reporting date, with due adjustment for significant transactions or other events between the dates.

32

Uniform accounting policies

• If a member of a group uses accounting policies other than those adopted in the consolidated financial statements for like transactions and events in similar circumstances,

• Appropriate adjustments are made to that group member’s financial statements in preparing the consolidated financial statements to ensure conformity with the group’s accounting policies.