reviewertraining presentation - reviewer recruitment · •thank you for serving as a reviewer for...

TRANSCRIPT

COMMUNITY DEVELOPMENT

FINANCIAL INSTITUTIONS FUNDwww.cdfifund.gov

Reviewer Training Presentation2017 New Markets Tax Credit Program

PREPARED ON

June 20, 2017The CDFI Fund is an equal opportunity employer.

• Thank You for serving as a Reviewer for the 2017

Allocation Round of the New Markets Tax Credit

Program.

• Questions? Contact:

– NMTC staff for training and program related questions

– A contact list is provided on the last slide

– F2 Solutions for personnel matters

• Please have a copy of the 2017 Phase 1 Review

Form in front of you during this presentation.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

2

Welcome

• After completion of the independent study and

viewing this presentation, Reviewers will understand

the mechanics of the Phase 1 review process,

including:

– Roles and responsibilities

– Review criteria and guidelines

– Phase 1 Review Form questions

– Other sections of the Phase 1 Review Form

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

3

Presentation Goals

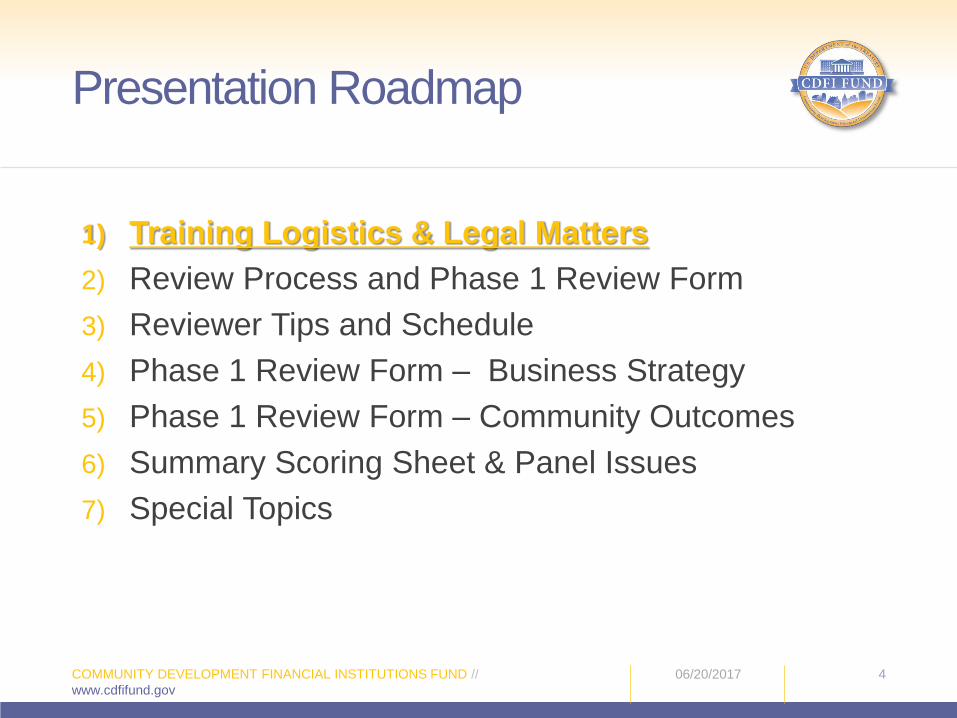

1) Training Logistics & Legal Matters

2) Review Process and Phase 1 Review Form

3) Reviewer Tips and Schedule

4) Phase 1 Review Form – Business Strategy

5) Phase 1 Review Form – Community Outcomes

6) Summary Scoring Sheet & Panel Issues

7) Special Topics

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

4

Presentation Roadmap

• All training will be completed remotely

• In accordance with the Phase 1 Reviewer Training Plan, at this point you should have reviewed:

– “2017 Introduction to the NMTC Program” Presentation Slides

– “2017 NMTC Program Application Roadmap” Presentation Slides

– 2017 NMTC Allocation Application (Applicant Information, Business Strategy and Community Outcomes sections only)

– 2017 NMTC Program Application FAQs (particularly Qs. 27, 34, 35, 51, 53, 54, 57, 65, 66, 67, 68, 72, and 73 as well supplemental FAQs A, B, and D)

– 2017 Phase 1 Review Form

– 2017 Phase 1 Review Form Calculations Worksheet

– Online Review Form Instructions

– Reviewer Tip Sheet: Panel Issues

• This presentation assumes you are already familiar with the content of these documents.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

5

Training Materials

• This training presentation is the final part of the

Independent Study portion. You will be required to

complete test questions following each section of this

presentation.

• You will have only 3 attempts to correctly answer all

of the test questions for each section.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

6

Training Logistics – Test Questions

• Make sure to read all elements of the Phase 1 Reviewer Training Plan

• Test questions after Section 1 will refer to these documents.

• If you have not done so already, stop this presentation and review these documents.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

7

Training Logistics –Test Questions

• You need to complete the presentation and all related test questions by August 15, 2017.

• You must complete the entire training program before you can access your assignments.

• A MANDATORY wrap-up conference call with NMTC staff will be scheduled by a Team Leader between August 15, 2017 and August 16, 2017.

• You will be compensated for 10 hours of training time.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

8

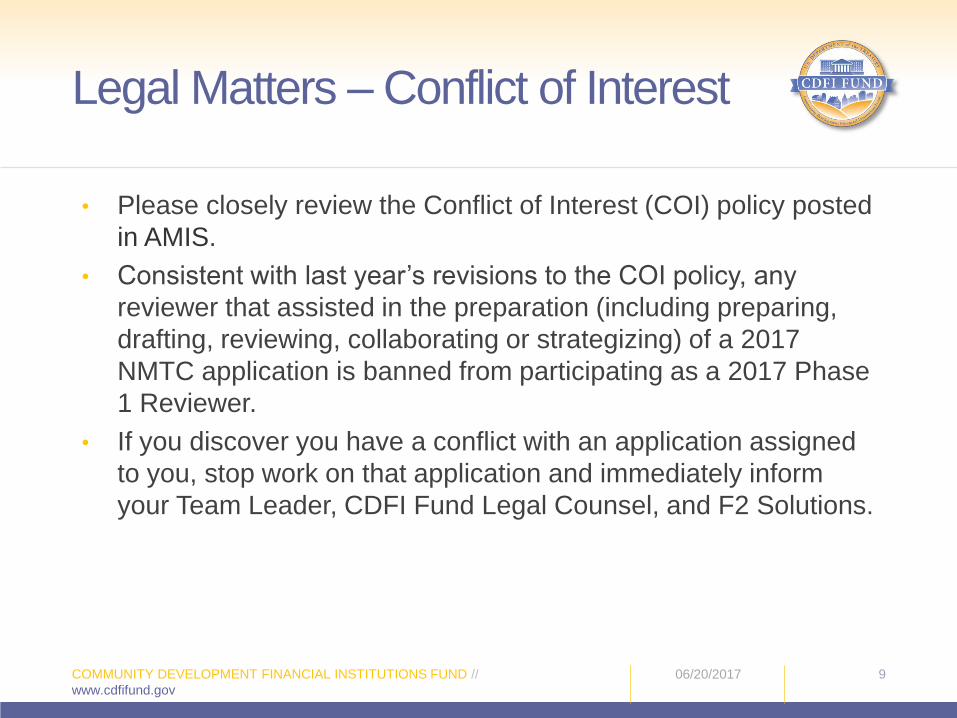

Training Logistics

• Please closely review the Conflict of Interest (COI) policy posted

in AMIS.

• Consistent with last year’s revisions to the COI policy, any

reviewer that assisted in the preparation (including preparing,

drafting, reviewing, collaborating or strategizing) of a 2017

NMTC application is banned from participating as a 2017 Phase

1 Reviewer.

• If you discover you have a conflict with an application assigned

to you, stop work on that application and immediately inform

your Team Leader, CDFI Fund Legal Counsel, and F2 Solutions.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

9

Legal Matters – Conflict of Interest

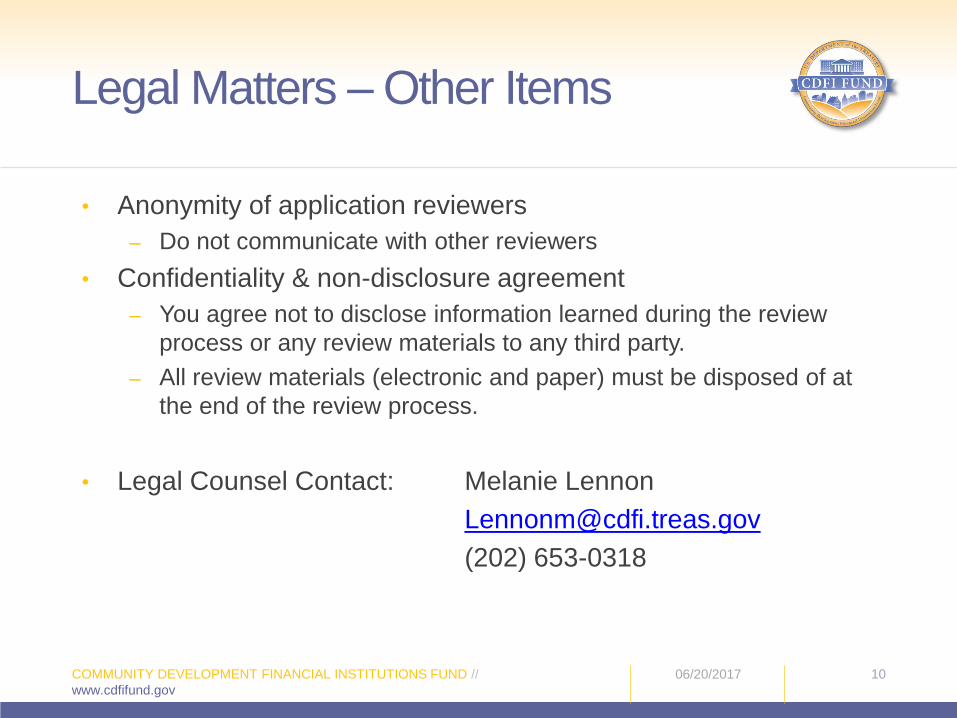

• Anonymity of application reviewers

– Do not communicate with other reviewers

• Confidentiality & non-disclosure agreement

– You agree not to disclose information learned during the review

process or any review materials to any third party.

– All review materials (electronic and paper) must be disposed of at

the end of the review process.

• Legal Counsel Contact: Melanie Lennon

(202) 653-0318

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

10

Legal Matters – Other Items

1) Training Logistics & Legal Matters

2) Review Process and Phase 1 Review Form

3) Reviewer Tips and Schedule

4) Phase 1 Review Form - Business Strategy

5) Phase 1 Review Form – Community Outcomes

6) Summary Scoring Sheet & Panel Issues

7) Special Topics

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

11

Presentation Roadmap

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

12

Overview of Review Process

Phase 1: Peer ReviewExternal Reviewers evaluate applications.

Phase 2: Panel ReviewApplications that meet minimum scoring thresholds in

Business Strategy and Community Outcomes are sent to a CDFI Fund staff panel for consideration in rank order.

Selection of ApplicantsSelecting Official makes Award Determinations based upon

panel recommendations.

3 Stages of the Review Process

• Application Reviewers (You)

• Team Leader

– CDFI Fund staff or

– a Federal employee (from another agency)

• NMTC Program Manager

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

13

Phase 1 Review Process – Key

Roles

Application Reviewer:

• On a timely basis, evaluate approximately 10-12 applications.

– Quality reviews and workload balance are both important! If you experience workload balance issues or extenuating circumstances affecting your working pace/quality, please contact your Team Leader for guidance.

– There may be opportunity for additional assignments for those who work ahead and receive positive feedback from their Team Leader.

• Evaluate applications based on the criteria in the review form as well as the guidance provided by the CDFI Fund in Reviewer training materials and by your Team Leader.

• Justify your selection for each question with brief, thoughtful, and substantive rationale.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

14

Phase I Review Responsibilities

Team Leaders:

• Ensure Reviewers complete reviews on schedule

• Monitor quality and ensure consistency with guidance

• Return reviews to Reviewer if quality or consistency issues

need to be addressed

• Respond to Reviewer questions and provide guidance as

needed on the Phase 1 Review Form

• Do not tell Application Reviewer which responses to select,

except where indicated in the guidance

• Serve as liaison to NMTC Program Manager

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

15

Phase I Review Responsibilities

NMTC Program Manager:

• Enforces evaluation standards and procedures

• Fields technical inquiries from Team Leaders on

behalf of Reviewers

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

16

Phase I Review Responsibilities

• The Phase 1 Review Form will be completed & submitted online through AMIS

• Please refer to the Online Review Form Instructions for details on accessing AMIS and navigating the Phase 1 Reviewer Form Scorecard

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

17

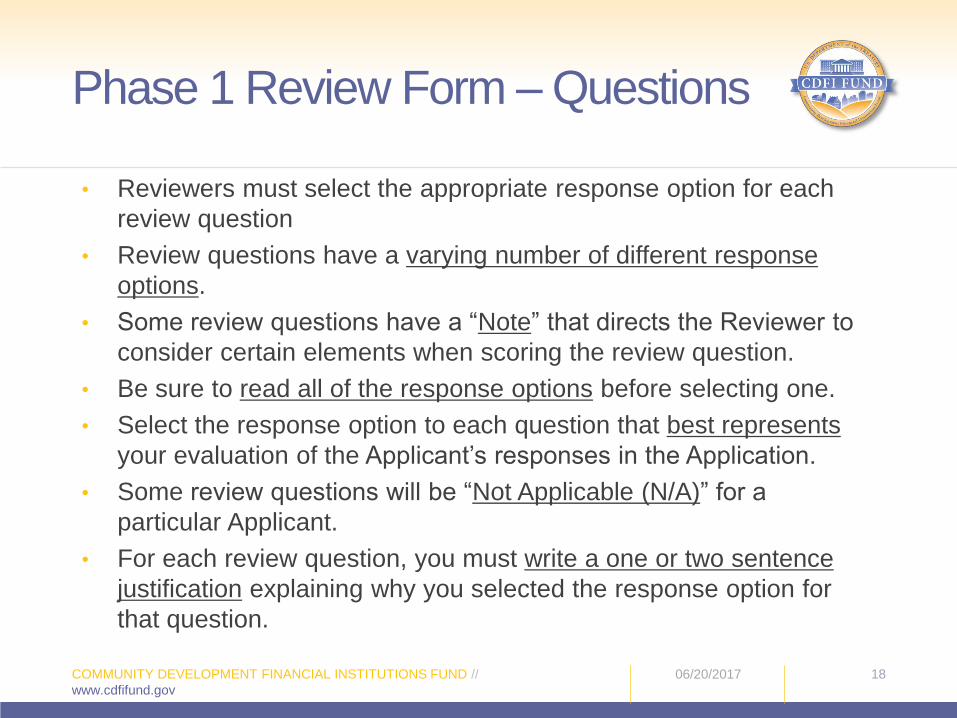

Phase I Review Form

• Reviewers must select the appropriate response option for each

review question

• Review questions have a varying number of different response

options.

• Some review questions have a “Note” that directs the Reviewer to

consider certain elements when scoring the review question.

• Be sure to read all of the response options before selecting one.

• Select the response option to each question that best represents

your evaluation of the Applicant’s responses in the Application.

• Some review questions will be “Not Applicable (N/A)” for a

particular Applicant.

• For each review question, you must write a one or two sentence

justification explaining why you selected the response option for

that question.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

18

Phase 1 Review Form – Questions

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

19

Phase I Review Form

Section Title

Sub-Section

Review Question

Justification

Note -Additional Guidance

Response Options

Please provide at least one sentence justification.

Business Strategy

Products, Services and Investment criteria (Qs. 14-16).

• Some review questions will be pre-populated from

responses in the Application.

• You must not change these selections and a justification

will be automatically generated.

• Pre-population is primarily related to:

– A review question being Not Applicable for a particular

Applicant, OR

– A review question being directly pre-populated based on

responses in the Application (e.g., Review Question 5).

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

20

Phase I Review Form –

Question Pre-population

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

21

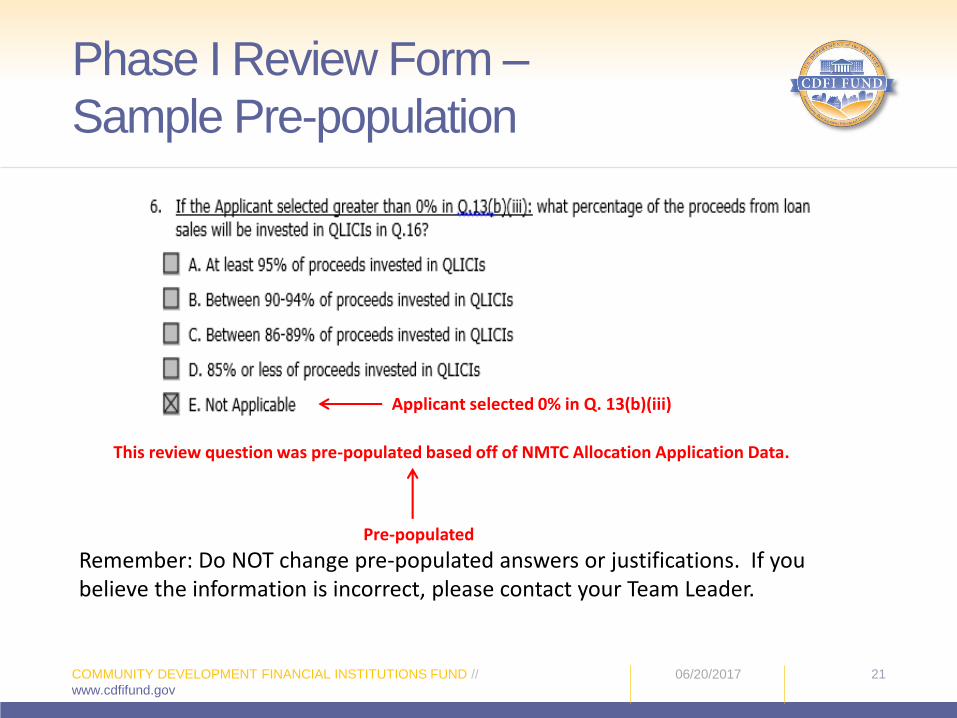

Phase I Review Form –

Sample Pre-population

This review question was pre-populated based off of NMTC Allocation Application Data.

Pre-populated

Remember: Do NOT change pre-populated answers or justifications. If you believe the information is incorrect, please contact your Team Leader.

Applicant selected 0% in Q. 13(b)(iii)

1) Training Logistics & Legal Matters

2) Review Process and Introduction to Phase 1 Review

Form

3) Reviewer Tips and Schedule

4) Phase 1 Review Form - Business Strategy

5) Phase 1 Review Form – Community Outcomes

6) Summary Scoring Sheet & Panel Issues

7) Special Topics

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

22

Presentation Roadmap

Getting Started:

• Review applications in specified order

• Preview/skim the application before you start answering

review form questions, so you get a sense of its overall

contents

• Ignore all attachments

• Contact your Team Leader if you have any questions or if

any issues affecting your work arise

• Remember, Application narratives and tables work

together

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

23

Reviewers Tips

Evaluation:

• Read the Business Strategy and Community Outcomes sections of the Application before you begin your evaluation of each section

• Read each review question carefully

• Read any “Notes” under review questions for specific scoring guidance

• Carefully read all response options for each question before selecting one

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

24

Reviewers Tips

Evaluation:

• Each review question refers to specific application questions. You may reference information from other parts of the Business Strategy and Community Outcomes sections when selecting ratings, if the information is directly related to that review question and not specifically evaluated in another review question.

– Be sure to explain in your justification comments

– If unsure, ask your Team Leader

• Only evaluate the Applicant on information presented in the Application

• Don’t change any information that’s been pre-populated in the review form

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

25

Reviewers Tips

Explanation of Key Terms: Likelihood

• Many review questions (e.g., Review Question 4) ask the

Reviewer to determine the likelihood of a particular outcome or

expected result

• Definitions:

– Highly Likely: Reviewer feels near-certainty outcome or result will

occur

– Probably: Not as confident as “Highly Likely” but greater than 50%

that outcome or result will occur

– Possibly: Odds are 50/50 that outcome or result will occur

– Unlikely: Less than 50% chance outcome or result will occur

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

26

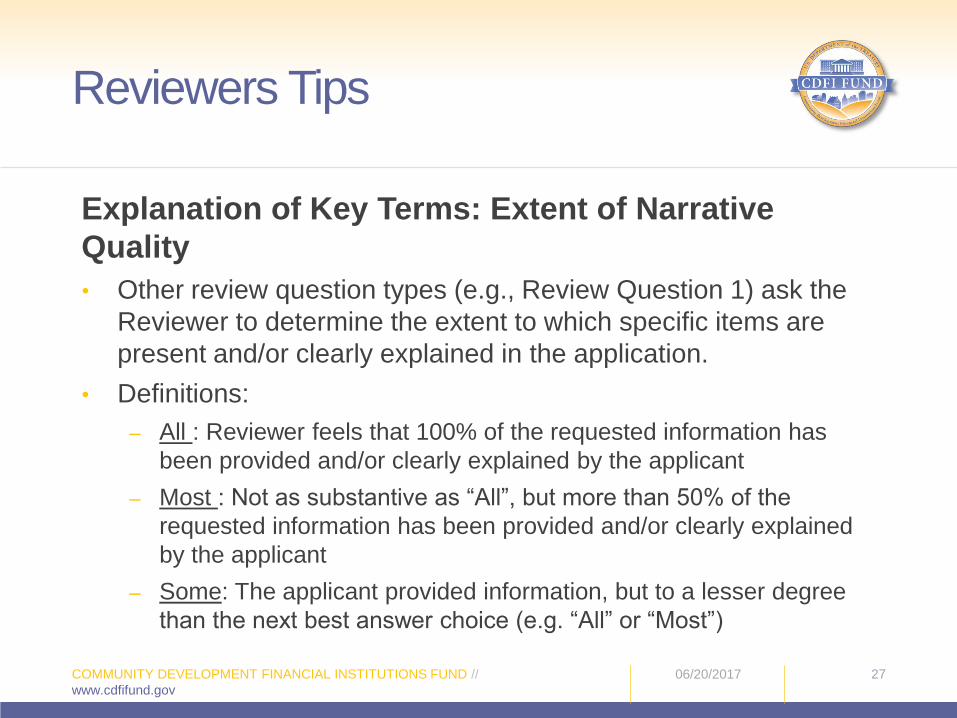

Reviewers Tips

Explanation of Key Terms: Extent of Narrative

Quality

• Other review question types (e.g., Review Question 1) ask the

Reviewer to determine the extent to which specific items are

present and/or clearly explained in the application.

• Definitions:

– All : Reviewer feels that 100% of the requested information has

been provided and/or clearly explained by the applicant

– Most : Not as substantive as “All”, but more than 50% of the

requested information has been provided and/or clearly explained

by the applicant

– Some: The applicant provided information, but to a lesser degree

than the next best answer choice (e.g. “All” or “Most”)

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

27

Reviewers Tips

Justification Comments:

• Address only the question/criteria being evaluated

• Do not compare Applicants

• Provide clear and substantive analysis

– Clearly identify the key factors that led you to the response option selected.

• For instance, if you selected “B. Probably”, you should provide evidence (i.e. missing information, inadequate supporting data, etc.) to validate why the information provided meets the criteria for your selection.

– Do not simply re-state items from the application. Focus on an ANALYSIS of the information provided

• Address any “Notes” associated with the review question.

• Write in complete sentences or bullet points

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

28

Reviewers Tips

Here is an example of a good justification:

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

29

Reviewers Tips

Justification: The Applicant provides a comprehensive track record and robust methodology for tracking most of the community outcomes it identified in Application Q. 25- Job Creation/Retention, Quality Jobs, Accessible Jobs, and Commercial Goods or Services to Low-Income Communities. However, the Applicant does not outline a track record or address methods for tracking community outcomes for Housing Units.

Here is an example of a bad justification:

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

30

Reviewers Tips

Justification: The applicant’s proposed QLICIs are projected to serve 1000 students annually and 500 homeless individuals annually, therefore they are likely to achieve their projected outcomes.

Review Form Submission:

• Meet the deadlines contained in the delivery

schedule attached to the Training Plan

• Make sure all items are complete before submission

• Be on the lookout for comments from your Team

Leader

• Reviews returned to you by your Team Leader are

due for resubmission within 2 business days

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

31

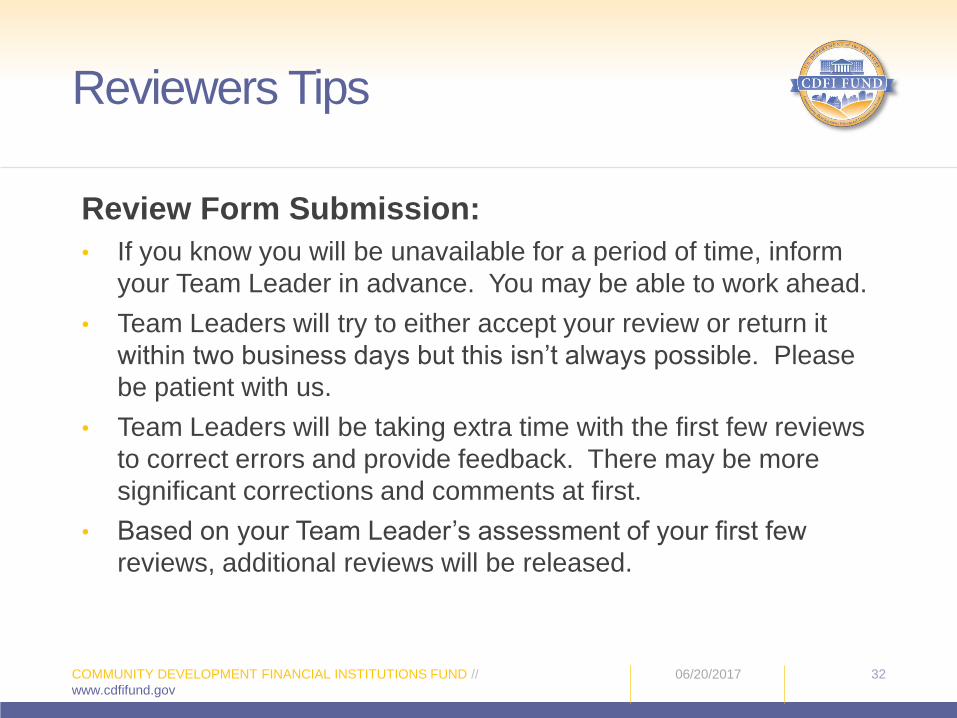

Reviewers Tips

Review Form Submission:

• If you know you will be unavailable for a period of time, inform

your Team Leader in advance. You may be able to work ahead.

• Team Leaders will try to either accept your review or return it

within two business days but this isn’t always possible. Please

be patient with us.

• Team Leaders will be taking extra time with the first few reviews

to correct errors and provide feedback. There may be more

significant corrections and comments at first.

• Based on your Team Leader’s assessment of your first few

reviews, additional reviews will be released.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

32

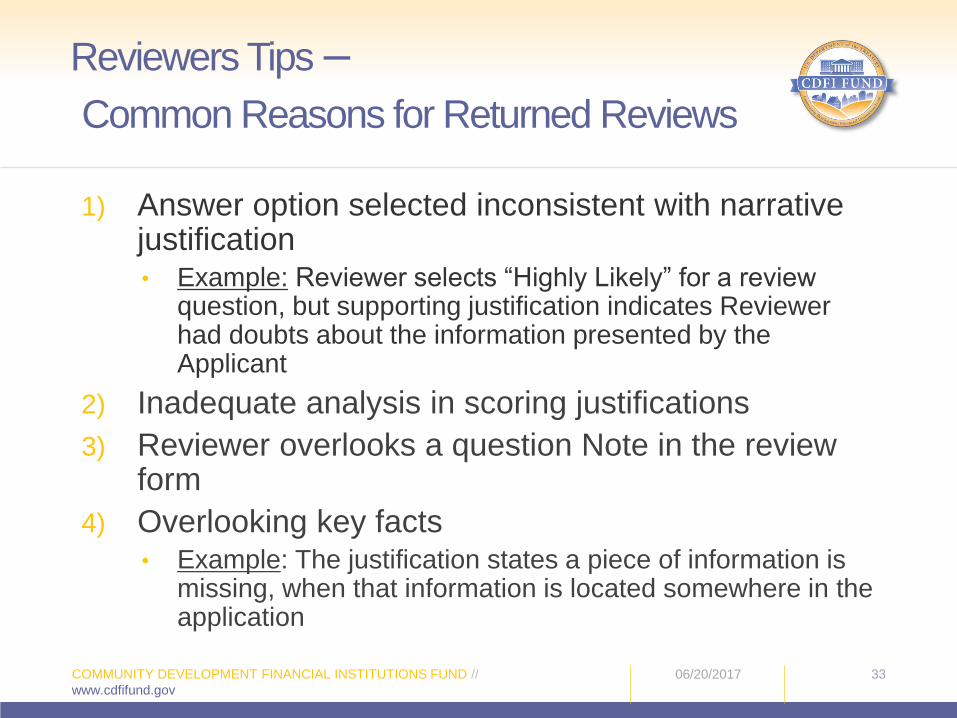

Reviewers Tips

1) Answer option selected inconsistent with narrative justification• Example: Reviewer selects “Highly Likely” for a review

question, but supporting justification indicates Reviewer had doubts about the information presented by the Applicant

2) Inadequate analysis in scoring justifications

3) Reviewer overlooks a question Note in the review form

4) Overlooking key facts• Example: The justification states a piece of information is

missing, when that information is located somewhere in the application

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

33

Reviewers Tips –

Common Reasons for Returned Reviews

Here is the schedule for completing reviews. For an assignment to be

considered on-time it is due at 11:59 PM ET on the schedule bonus-

eligible due date.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

34

Schedule for Completing Reviews

** If assigned

Bonus Eligible Dates:

Application Assignment Group A Group B

1 Monday, August 21, 2017 Wednesday, August 23, 2017

2 Monday, August 28, 2017 Wednesday, August 30, 2017

3 Thursday, August 31, 2017 Tuesday, September 05, 2017

4 Wednesday, September 06, 2017 Thursday, September 07, 2017

5 Friday, September 08, 2017 Monday, September 11, 2017

6 Tuesday, September 12, 2017 Wednesday, September 13, 2017

7 Thursday, September 14, 2017 Friday, September 15, 2017

8 Monday, September 18, 2017 Tuesday, September 19, 2017

9 Wednesday, September 20, 2017 Thursday, September 21, 2017

10 Friday, September 22, 2017 Monday, September 25, 2017

11** Tuesday, September 26, 2017 Wednesday, September 27, 2017

12** Thursday, September 28, 2017 Friday, September 29, 2017

13** Monday, October 02, 2017 Tuesday, October 03, 2017

14** Wednesday, October 04, 2017 Thursday, October 05, 2017

1) Training Logistics & Legal Matters

2) Review Process and Phase 1 Review Form

3) Reviewer Tips and Schedule

4) Phase 1 Review Form – Business Strategy

5) Phase 1 Review Form – Community Outcomes

6) Summary Scoring Sheet & Panel Issues

7) Special Topics

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

35

Presentation Roadmap

06/20/2017

13

COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

36

Phase 1 Review Form – Overview

Two sections of the NMTC Allocation Application are

evaluated by Phase 1 Reviewers:

(1) Business Strategy, including Priority Points

(2) Community Outcomes

The purpose of this section is to evaluate the Applicant’s

overall business strategy based on the following 5 sub-

sections.

(1) Products, Services, and Investment Criteria

(2) Projected Business Activities

(3) Prior Performance

(4) Prior Performance and Projected Business Activity

(5) Notable Relationships

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

37

Phase 1 Review Form –

Business Strategy

Overview: Evaluate the financial products/services that the Applicant

intends to offer QALICBs or other CDEs.

• Please note:

– Financial products associated with the Leverage Model are often

structured with multiple financial notes (for instance, a Senior A

Note and a Subordinate B Note, etc.). In this case, you should

evaluate the financial notes collectively as a single financial

product.

– If using the Unleveraged Model, the financial product may only

have one financial note.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

38

(1) Products, Services, and

Investment Criteria

Question 1:

• You, as the reviewer, should be able to clearly understand the rates and terms for the products the Applicant intends to offer

• To score “A”, the Applicant must

– If the Applicant provides a range for any of the rates/terms (e.g., interest rates range from 2-4%) then the Applicant must specify the circumstances that would dictate the specific rates and terms to borrowers/investees AND

– For financial products structured with multiple financial notes, the Applicant must discuss the rates and terms of the financial notes on a blended basis

– Example: If a financial product is structured with an A Note with a 5% rate and a B Note with a 1% interest rate, the Applicant must discuss the blended interest rate for both the A and B notes

– Please review questions 34-36 in the 2017 NMTC Allocation Application FAQs document

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

39

(1) Products, Services, and

Investment Criteria

• Question 2: If the Applicant did not compare the

rates, terms, and features of its products to what it

typically offers AND to similar financial products

offered by other financial institutions in the Applicant’s

service area, then the response must be “B” (No)

• Question 3: To score “A” Applicant must provide an

example from Q. 17(c) for each financial product it

intends to offer

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

40

(1) Products, Services, and

Investment Criteria

• Question 4: will only be applicable if the

Applicant plans to invest or loan to other CDEs

• Question 5: pre-populated from the Applicant’s

response to Application Q. 15. DO NOT

CHANGE THIS RESPONSE.

• Question 6: will only be applicable if the

Applicant plans to purchase loans from other

CDEs.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

41

(1) Products, Services, and

Investment Criteria

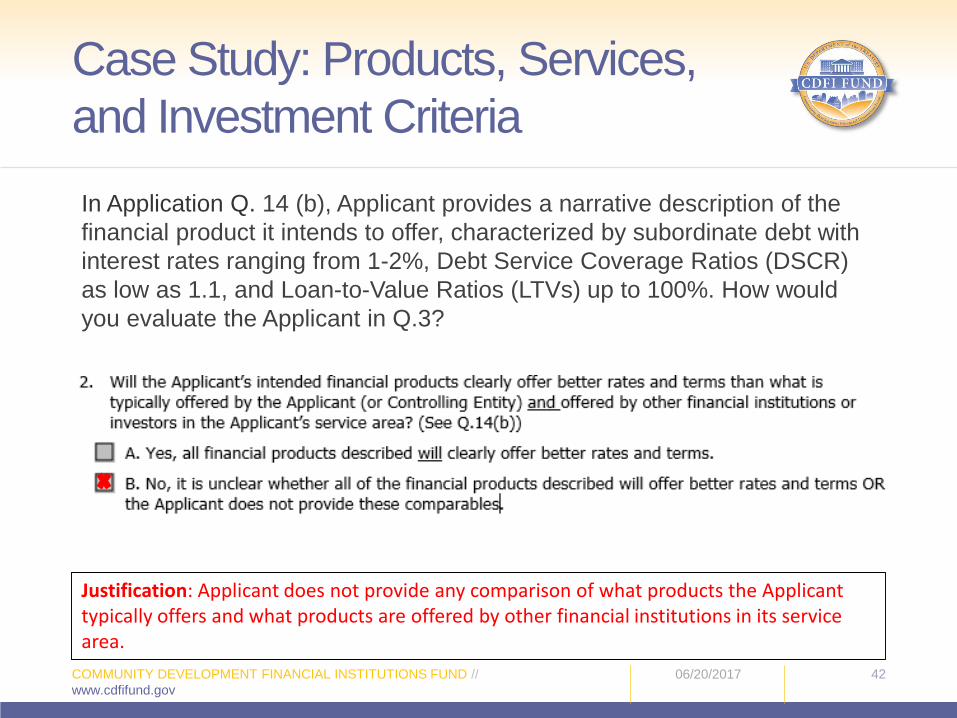

In Application Q. 14 (b), Applicant provides a narrative description of the

financial product it intends to offer, characterized by subordinate debt with

interest rates ranging from 1-2%, Debt Service Coverage Ratios (DSCR)

as low as 1.1, and Loan-to-Value Ratios (LTVs) up to 100%. How would

you evaluate the Applicant in Q.3?

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

42

Case Study: Products, Services,

and Investment Criteria

Justification: Applicant does not provide any comparison of what products the Applicant typically offers and what products are offered by other financial institutions in its service area.

Overview: Evaluate the Applicant’s projected business activities –

either a single or discrete number of investments OR a general

pipeline of investments.

• Questions 7-8: Mostly pre-populated N/A. Only evaluate if

“single or discrete investments” is selected by the Applicant.

• Questions 9-12: Only evaluated if “general pipeline” is

selected by the Applicant.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

43

(2) Projected Business Activities

• Question 9: Evaluate whether the Applicant

provides all necessary details for its overall

pipeline of activities.

• Question 10: Evaluate whether the Applicant

provides the necessary details for each

sample transaction in its pipeline.

• The necessary details the Applicant must

provide are listed in the Note before each

question.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

44

(2) Projected Business Activities

• Question 11: Evaluate whether or not the

details of the Applicant’s sample transactions

validate its deployment projections (Exhibit

A).

• Question 12: Evaluate the likelihood that the

Applicant’s business identification strategy

will yield the types of investments described

in its general pipeline.

8/8/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

45

(2) Projected Business Activities

Overview: Evaluate the Applicant’s (or Controlling Entity’s) track

record providing direct and indirect financing.

• Please note:

– Direct financing activities are loans a/o equity investments that are financed

with the Applicant’s (or Controlling Entity’s) own at-risk capital. These

activities also include investments in other CDEs, purchasing loans from

other CDEs, and FCOS provided by the Applicant (or Controlling Entity).

– Indirect financing activities are loans a/o equity investments that are

financed by third-parties where the Applicant (or Controlling Entity)

participate, but had no capital at risk (e.g., loan packaging, project

development, etc.)

– DO NOT consider any financing activities closed after May 2nd, 2017 in your

evaluation of prior performance.

– Applicants were instructed not to include grants made to others as part of

their financing track record, so please disregard any grant-making activity in

your evaluation.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

46

(3) Prior Performance

• Question 13: Response choices include criteria for both direct and indirect financing activities.

– Carefully read the Phase 1 Review Form Calculations Worksheet to know where in Exhibit B to locate both direct and indirect financing.

– Ensure to select the highest response that aligns with the Applicant’s track record. For example, if the Applicant has less than 2 years of DIRECT financing activity, but 5 or more years of INDIRECT financing activity, then the score should be “B,” not “D.”

• Question 14: This question asks only about the Applicant’s DIRECT financing track record as presented in Tables B1-B3 and Application Question 19. DO NOT include financing in Table B4 and Application Question 20.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

47

(3) Prior Performance

• Question 15: Compare Applicant’s proposed QLICIs

and business/project types to determine if its track

record includes comparable financing activities

– Applicant’s Proposed QLICIs – See Application Question

13(b)

– Business/Project Type is the category of business(es) the

Applicant plans to invest in, such as community facilities,

retail, industrial, and mixed-use real estate, among others.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

48

(4) Prior Performance and

Projected Business Activity

An Applicant has a track record of providing FCOS to early childhood education

centers and community health centers. The Applicant’s pipeline consists of

providing debt financing for the development of new community health centers.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

49

Case Study: Prior Performance

and Projected Business Activity

Justification: The Applicant’s pipeline consists entirely of community health centers and the Applicant demonstrates a track record of serving community health centers. However, the Applicant does not show a track record of providing debt financing.

• Question 16: Compare projected deployment in Exhibit A (all tables) with financing track record (both DIRECT and INDIRECT financing) in Exhibit B.– Carefully read the notes before Q. 16 to know what you

should take into account for total projected deployment in Exhibit A.

– Calculate % to select the highest response that aligns with the Applicant’s track record.

– Formula: • Historical Financing Percentage =

Financial Track Record ÷ Projected Deployment

• (See Phase 1 Form Q. 16 Notes and the Phase 1 Reviewer Calculations Worksheet for more details)

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

50

(4) Prior Performance and

Projected Business Activity

Justification: The Applicant’s track record of direct financing represents 30% ($18MM) of its $60MM total projected deployment in Exhibit A. However, the Applicant has a stronger track record of indirect financing that represents 70% ($42MM)of its projected deployment.

Total projected deployment in Exhibit A is $60MM. The Applicant has a

track record of $18MM in direct financing and $42MM in indirect financing

listed in Exhibit B.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

51

Case Study: Prior Performance

and Projected Business Activity

Overview: Evaluate if the Applicant will have a notable

relationship(s) in proposed investments and whether benefits will

be passed to unaffiliated end users

• “Added value” means that notable relationships will create

benefits for non-affiliated end-users. Consider the community

outcomes described in Q.25 of the Application when evaluating

notable relationships

• If Applicant answers “No” for Q. 23(a)-Q.23(e), select “A” for

Review Form Question 17

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

52

(5) Notable Relationships

The Applicant indicates that it will act as a “Master Tenant” in some projects

for the purposes of twinning NMTCs and historic tax credits. In these

instances, the Applicant indicates that the dual subsidies are necessary for

the project to occur and deliver community benefits. The Applicant won’t

gain any material financial benefit by being “Master Tenant”.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

53

Case Study:

Notable Relationships

Justification: Notable relationship is a function of structuring the financing and does not create any material financial benefit for the Applicant or its Affiliates. Also, based on Q. 25, these projects will generate significant community outcomes, including quality jobs and healthcare services for LIPs.

• Applicants can earn up to 10 “bonus” points:

– Priority 1 (5 points): based on track record of serving

Disadvantaged Businesses and Communities (DBCs)

– Priority 2 (5 points): based on a commitment to invest in

unrelated entities (Application Question 22)

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

54

Priority Points

Overview: Evaluate the number of years and percentage of dollar

volume of financing that has been provided to DBCs

• Please note:

– Track record of principals, board members, and other management

individuals are not relevant for this section

– If Exhibit B is Not Applicable or includes only zeros for direct

financing, then the response selection for Q. 18 must be “C” and Q.

19 must be “E.”

• Question 18: Be sure to include years of financing in all four

tables (B1-B4), both direct and indirect financing. Applicants

may take into account the narratives in Application Questions

Q.19 and Q.20.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

55

Priority Points 1:

Track Record of Serving DBCs

• Question 19:

– Formula (Exhibits B1-B4): % of DIRECT financing activities provided to DBCs = Totals to DBCs & Communities ÷ Totals (2012-2017)

– DO NOT include indirect financing in the calculation.

8/8/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

56

Priority Points 1:

Track Record of Serving DBCs

Evaluation Elements:

• Based on application Q.22

• Applicant is automatically granted these Priority Points based on

its response

• Reviewer cannot alter score

• If you feel these points were erroneously claimed, you should

indicate this in the Panel Issues section of the review form

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

57

Priority Points 2:

Investments in Unrelated Entities

1) Training Logistics & Legal Matters

2) Review Process and Phase 1 Review Form

3) Reviewer Tips and Schedule

4) Phase 1 Review Form - Business Strategy

5) Phase 1 Review Form – Community Outcomes

6) Summary Scoring Sheet & Panel Issues

7) Special Topics

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

58

Presentation Roadmap

The purpose of this section is to evaluate the Applicant’s

strategy to generate community outcomes based on the

following 5 sub-sections.

(1) Targeting Areas of Higher Distress

(2) Community Outcomes

(3) Tracking Community Outcomes

(4) Community Accountability and Involvement

(5) Other Community Benefits

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

59

Community Outcomes

Overview: Evaluate the Applicant’s strategy for prioritizing QLICIs

in areas of higher distress

• Question 20: Pre-populated based on Applicant’s response in the application

• Question 21: Consider the Applicant’s criteria for prioritizing QLICIs, given limited allocation

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

60

(1) Targeting Areas of Higher

Distress

Overview: Evaluate the Applicant’s track record and projected

community outcomes.

• Please note:

– To facilitate a more in-depth review, individual community outcomes

listed in Q.25 have been grouped into 4 categories. Each category

is evaluated with a similar set of questions and all categories are

equally weighted when determining the overall section score.

– The CDFI Fund has no preference for one outcome over another

– Reviewers will only answer review questions for a category if the

Applicant has selected one or more outcomes in that category,

otherwise those review questions will be pre-populated N/A.

– Reviewers should collectively evaluate the outcomes if there is

more than one outcome selected in that category.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

61

(2) Community Outcomes

• Other important notes:– For Application Q. 25(a), Applicants that select (1) Job

Creation/Retention as an outcome are also required to

provide a response for both (2) Quality Jobs and (3)

Accessible Jobs

– For the other categories, it does not matter how many

outcomes they select

• For example, an Applicant should not be evaluated

differently whether it selects only one or all three Goods

and Services to Low-Income Communities Outcomes.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

62

(2) Community Outcomes

Four Community Outcome Categories:

1. Job-Related Community Outcomes– 1. Job Creation/Retention

– 2. Quality Jobs

– 3. Accessible Jobs

2. Goods and Services for Low-Income Communities– 4. Commercial Goods or Services

– 5. Healthy Food Financing

– 6. Community Goods or Services

3. Financing Minority Businesses and Housing Units– 7. Financing Minority Businesses

– 8. Housing Units

4. Additional Community Development Outcomes– 9. Flexible Lease Rates

– 10. Environmentally Sustainable Outcomes

– 11. & 12. Other

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

63

(2) Community Outcomes

Questions 22, 29, 35, and 40: Did the Applicant quantify the projected outcomes.

Questions 23, 30, 36, and 41: Evaluate the methods used to estimate outcomes.

• A method is the procedure the Applicant used to obtain the numbers for quantifying its projections for each selected Community Outcome.

• Examples include: – Using XYZ economic impact modeling software to estimate the number of

construction jobs;

– Calculating projections (e.g. square feet, jobs, clients served) based on similar projects previously financed by the Applicant;

– Obtaining projected outcome data from the project sponsor or business;

– Analyzing QALICB financial projections to determine future lease rates to third-party tenants;

– or Evaluating the reduction in energy or water use based on the environmental features incorporated by the QALICB

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

64

(2) Community Outcomes

Questions 24, 31, and 42: Evaluate the metrics used to estimate the outcomes.

• A metric is the numerical basis the Applicant used to validate the reasonableness of the quantified projections for each selected outcome.

• Applicants should include the source of the metric, even if it has been identified from a third-party source

• Metrics are not evaluated for Financing Minority Businesses and Housing Units

• Examples of metrics include: – X square feet of commercial real estate development results in the creation of Y full-

time construction jobs;

– Charter schools create X Full Time Equivalent jobs for every Y students;

– X full-time primary care doctors equals Y patient visits per year;

– X% reduction in rent for an early childhood education center results in Y number of additional children enrolled; OR

– X environmental remediation costs will result in Y square feet of reusable space in a LIC.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

65

(2) Community Outcomes

Using the actual jobs created from similar projects previously financed by the Applicant, the Applicant’s proposed pipeline projects are projected to create 400 jobs. Based on its track record, 4 jobs are created for every 1,000 square feet in new retail, 3 jobs per 1,000 square feet in new office space, and 1.5 jobs per 1,000 square feet in new industrial development.

• What is the method?

– Calculating the actual jobs created from similar projects previously financed by the Applicant

• What is the metric?

– 4 jobs for 1,000 sf retail, 3 jobs for 1,000 sf office, 1.5 jobs for 1,000 sf industrial

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

66

Case Study: Methods/Metrics

An Applicant projects that the community health centers in its pipeline will

serve 50,000 LIP patients annually. To estimate this projection, the Applicant

provides a comprehensive explanation of how it conducted a market study that

evaluated the medical needs of the surrounding community for each center,

especially among LIPs who reside nearby.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

67

Case Study: Methods/Metrics

Justification: Applicant clearly explains how it used a market study of the medical needs of the surrounding LIC for each health center to make its projections.

Although the Applicant scored high on methods, same

is not true for metrics.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

68

Case Study: Methods/Metrics

Justification: Applicant does not indicate the metrics it used to validate the reasonableness of its projections for number of patients served by the new health centers.

Questions 25, 32, 37, and 43: Evaluate the likelihood that the

Applicant’s proposed QLICIs will generate the outcomes it has

proposed.

• Reviewers should refer to the Applicant’s proposed investments in

Application Q.17.

• Determine how likely the Applicant is to generate the proposed outcomes

based on the types of investments it has proposed.

• For instance, if the Applicant projects X number of LIP patients will

receive health care services, does it propose community health centers or

related investments in Question 17?

• Another example: If Applicant proposes the development of X number of

housing units as an outcome, does it propose mixed-use

commercial/residential or similar investments in Question 17?

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

69

(2) Community Outcomes

For each outcome category, reviewers will evaluate if the

community outcomes will benefit Low-Income Persons or

Residents of Low-Income Communities.

• For Job-Related Community Outcomes:

– Will the created/retained jobs be quality jobs (Question 26)

• Quality jobs are jobs that provide living wages; benefits such as

health insurance or retirement plans; and/or opportunities for

training and advancement.

– Also, will the jobs be targeted and/or accessible to Low-

Income Persons (LIPs), residents of Low-Income

Communities (LICs), people with lower levels of education,

or people who face other barriers to employment (e.g. longer

term unemployed, ex-convicts, etc.) (Question 27)

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

70

(2) Community Outcomes –

Benefits to LIPs and LICs

For Goods and Services for Low-Income Communities:

Question 33: Will projected outcomes increase the

provision and access of

– commercial goods or services,

• (e.g., restaurants, retail, pharmacies),

– fresh and healthy food options (e.g. grocery stores),

– and/or community goods or services

• (e.g., healthcare, social services, educational, cultural)

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

71

(2) Community Outcomes –

Benefits to LIPs and LICs

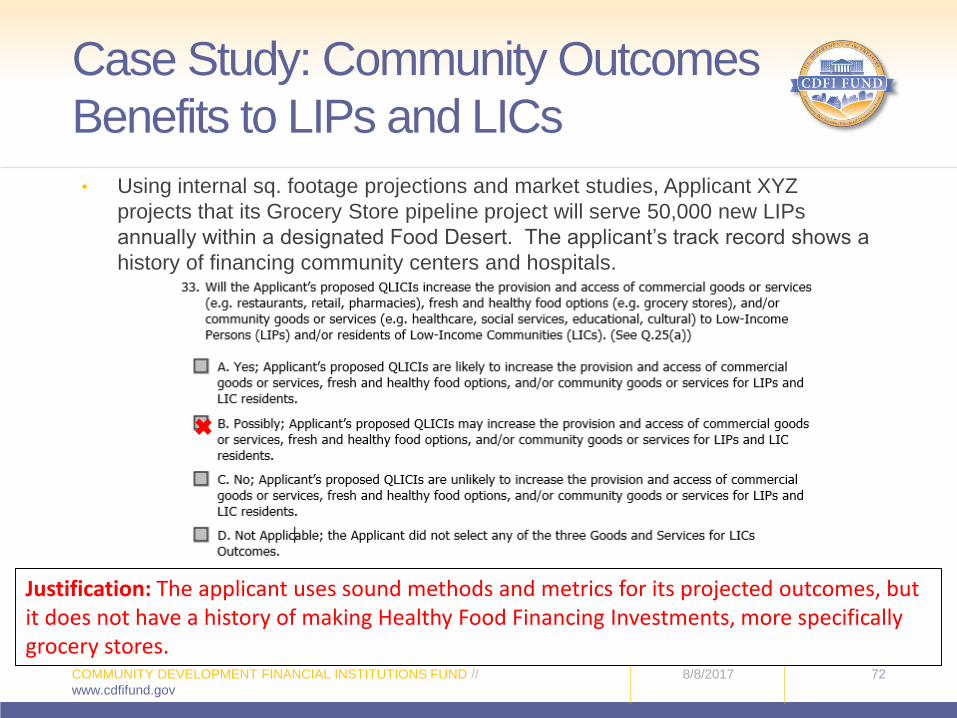

• Using internal sq. footage projections and market studies, Applicant XYZ

projects that its Grocery Store pipeline project will serve 50,000 new LIPs

annually within a designated Food Desert. The applicant’s track record shows a

history of financing community centers and hospitals.

8/8/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

72

Case Study: Community Outcomes

Benefits to LIPs and LICs

Justification: The applicant uses sound methods and metrics for its projected outcomes, but it does not have a history of making Healthy Food Financing Investments, more specifically grocery stores.

• For Financing Minority Businesses/Housing Units and Additional Community Development Outcomes:

– Question 38: Will the projected Financing Minority Businesses and Housing Units clearly benefit Low-Income Persons (LIPs) and/or residents of Low-Income Communities (LICs)?

– Question 44: Will the projected Additional Community Development outcomes clearly benefit Low-Income Persons (LIPs) and/or residents of Low-Income Communities (LICs)?

– Location in a LIC is NOT sufficient to demonstrate benefit to LIPs/LIC residents.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

73

(2) Community Outcomes –

Benefits to LIPs and LICs

For Question 38, examples of Financing Minority Businesses and Housing Units clearly benefiting LIPs and residents of LICs includes (but not limited to):

• Financing Minority Businesses – the business will employ LIPs and/or residents of the LIC AND/OR provide goods and services to LIPs and/or residents of LICs

• Housing Units – the project will result in affordable housing units for LIPs and/or LIC residents

8/8/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

74

(2) Community Outcomes –

Benefits to LIPs and LICs

• Inadequate Versus Good Justification for Question 38

– Inadequate Justification: The new housing

development will likely benefit LIPs because it will be

located in a economically distressed neighborhood.

– Good Justification: The new housing development will

likely benefit LIPs because X% of the units will be set

aside for residents with incomes 80% or below the

AMI.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

75

(2) Community Outcomes –

Benefits to LIPs and LICs

For Question 44, examples of Additional Community Development Outcomes clearly benefiting LIPs and residents of LICs includes (but not limited to):

• Flexible Lease Rates – the project will provide reduced rent or lease payments charged to a community healthcare center serving LIPs and/or LIC residents.

• Environmentally Sustainable Outcomes – remediation of environmental contamination of project location will eliminate illness among LIPs and/or LIC residents; building a water treatment plant that provides clean and safe water for LIPs and/or LIC residents.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

76

(2) Community Outcomes –

Benefits to LIPs and LICs

• Inadequate Versus Good Justification for Question 44

– Inadequate Justification: The environmental brownfield

remediation will likely benefit LIPs because it will occur

within an economically distressed neighborhood that

has experienced persistent poverty.

– Good Justification: The environmental brownfield

remediation will likely benefit LIPs because it will

alleviate LIC environmental ailments by removing all

contaminants from the remediated area.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

77

(2) Community Outcomes –

Benefits to LIPs and LICs

Questions 28, 34, 39, and 45: Evaluate the Applicant’s

track record of producing similar community outcomes.

A similar track record should include:

• Outcomes that are similar in type (e.g., job creation,

community goods/services, flexible lease rates).

• Outcomes that are similar in quantity (e.g., number of jobs

created, square feet of community facilities, percent below

market rent).

– While outcomes with similar quantities are important, it is more

significant for you to establish whether or not the Applicant has

relevant experience generating those outcomes

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

78

(2) Community Outcomes

• Question 46: Evaluate the Applicant’s ability

to effectively track ALL projected community

outcomes.– The Applicant’s response to application Q.25(b) should

address how it will track all outcomes selected in Q.25(a).

– In order to select “A”, the Applicant must describe BOTH its

methodology for tracking future projected outcomes AND its

track record of documenting similar outcomes in the past

• The Applicant must also address their tracking methods for all

selected outcomes to score “A.”

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

79

(3) Tracking Community Outcomes

Overview: Evaluate the Applicant’s track record of community engagement and process for ensuring that future investments align with community priorities.

• Question 47: Evaluate the role of LIC Representatives on the Applicant’s Advisory and/or Governing Board in setting the Applicant’s investments parameters, formulating the Applicant’s pipeline of investments, and approving the Applicant’s investment decisions.

• Question 48: Evaluate the Applicant’s process for determining whether its investments align with community priorities. The following elements should be considered:

– The Role of LIC Representatives on the Advisory/Governing Board

– The Applicant’s process for analyzing potential benefits to DBCs

– The Applicant’s process for determining if investments align with community priorities

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

80

(4) Community Accountability and

Involvement

Question 49: Applicants are expected to describe a track record of activities beyond simply consulting with its Advisory Board. Examples may include:

• Partnerships with local community or economic development entities

• Public hearings or community meetings

• Support from elected officials

• Community design charrettes

Note: Past community engagement activities must be clearly related to investment decisions when evaluating this question.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

81

(4) Community Accountability and

Involvement

• Question 50: Evaluate the extent to which the Applicant’s investments contribute to broader community and/or economic development strategies. Examples may include:

– Neighborhood revitalization plans

– Regional economic development strategic plans

– Rural county master plans

– DOES NOT INCLUDE a private facility expansion plan of a business (e.g., university capital improvement plan).

Note: Certain areas (e.g. rural or Tribal areas) or financing activities (Smaller QLICIs, non-Real Estate activities) may not have a formal plan or planning process. Nevertheless, if the Applicant plans to invest in these areas or activities, it can score highly if it discusses the other methods it used to ensure alignment with the community’s strategic priorities.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

82

(4) Community Accountability and

Involvement

Overview: Evaluate the likelihood that the Applicant’s investments will attract additional private investment or the ability of operating businesses financed to attract subsequent private investment after the initial QLICI is made.

• Questions 51-52: Additional private investment DOES NOT include how much private capital will be leveraged within the NMTC transaction structure or outside the structure during a simultaneous closing. Examples of additional private investment may include:

– X years after an NMTC investment made to an operating business, that business was able to raise private equity to fund a factory expansion.

– After an NMTC-funded project was completed, the owner of several adjoining properties financed façade improvements.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

83

(5) Other Community Benefits

1) Training Logistics & Legal Matters

2) Review Process and Phase 1 Review Form

3) Reviewer Tips and Schedule

4) Phase 1 Review Form - Business Strategy

5) Phase 1 Review Form – Community Outcomes

6) Summary Scoring Sheet & Panel Issues

7) Special Topics

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

84

Presentation Roadmap

• In the Award Determination, reviewers provide:

– A final YES/NO award recommendation

– Award recommendation justification

• Reviewers DO NOT recommend specific award

amounts.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

85

Award Determination

• Aside from the evaluation criteria, you will also provide

information on the following factors that the CDFI Fund will

consider in Panel Phase (Phase 2) of review:

1. Ineligible or questionable QLICI activities

2. Adjustments to allowable QLICI activities

3. Erroneously claiming Priority 2 points

4. Other critical items

• NOTE: Panel issue comments do not factor into Phase 1

scoring.

• If you do not find any issues, simply mark “No”

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

86

Panel Issues

• Does the Applicant’s business strategy include aspects

that are not clearly eligible per IRS regulations? Such as:

– Residential rental housing that is not part of a mixed-use

project

– Direct provision of individual consumer loans by the

Applicant (e.g., home mortgages)

• If yes:

– Provide a brief explanation

– List the question number where the ineligible activities

were referenced

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

87

Panel Issues: (1) Ineligible or

Questionable QLICI Activities

• Were there activities checked in Q. 13(b) that you believe

the Applicant should be prohibited from doing?

• Were there activities that were NOT checked in Q. 13(b)

that you believe the Applicant should be allowed to do?

• If yes:

– Provide a brief explanation

– List the QLICI activities which should be removed and/or added

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

88

Panel Issues: (2) Adjustments to

Allowable QLICI Activities

• Priority for investing in Unrelated entities is self-reported in

Q. 22

• You should notify the CDFI Fund if you feel that Q.22 was

answered incorrectly by the Applicant

• Example: An Applicant’s sole QLICI transaction will

capitalize a subsidiary entity.

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

89

Panel Issues: (3) Erroneously

Claiming Priority 2 Points

• Do not use this area for general comments about the application

• Only address issues that were not included in other areas of the review form, which you think the CDFI Fund should consider – e.g.:

– Material concerns related to the Applicant’s ability to manage and/or raise QEIs for an NMTC allocation

– Other critical areas of concern not appropriately reflected in the scoring or in any of the other required fields

– You have concerns about any prior NMTC activities discussed in the application

– You have knowledge of information not presented by the Applicant in its application that may influence the CDFI Fund’s decision

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

90

Panel Issues: (4) Other Critical

Issues

1) Training Logistics & Legal Matters

2) Overview of Review Process and Introduction to Phase 1 Review Form

3) Reviewer Tips and Schedule

4) Overview of Phase 1 Review Form - Business Strategy

5) Overview of Phase 1 Review Form – Community Outcomes

6) Summary Scoring Sheet & Panel Issues

7) Special Topics

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

91

Presentation Roadmap

NMTC Investment Models

06/20/2017COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

92

Special Topics

NMTC Investment Structures -

Unleveraged Structure

CDE $1MM

QEI

QALICB

An Investor purchases the New Markets Tax Credits and funds the Qualified Equity Investment of $1 million dollars.

$390K$1MM

The CDFI Fund Awards an Allocation of New Markets Tax Credits to the CDE.

Fees, Costs, and

Expenses

$50K

$950KThe CDE provides a QLICI of $950K to the QALICB.

Investor

The CDE receives $50K to cover the fees, costs and expenses.

06/20/2017

NMTC Investment Structures -

Leveraged Structure

Investor

CDE $1MM

QEI

QALICB

$390K

The CDFI Fund Awards an Allocation of New Markets Tax Credits to the CDE.

Fees, Costs, and

Expenses

$50K

$950KThe CDE provides a QLICI of $950K to the QALICB.

Leverage Debt Provider

$312K

Investment Fund$1MM in Capital

$688K

$1MM

The difference between the $312K generated from the sale of the NMTCs and QEI of $1MM is provided as Leveraged Debt.

The CDE receives $50K to cover the fees, costs and expenses.

An Investor purchases the NMTCs. This assumes a credit price of 80¢.

06/20/2017

• The CDFI Fund does not have a preference for the Leveraged or Unleveraged Structure

• Not all Applicants will use the Leveraged Structure

• There are benefits to using either Structure (e.g., providing Qualified Businesses with access to below market rate capital in Low Income Communities, etc.)

• Applicants should not be scored differently based on the structure an Applicant intends to use

• Direct any questions about NMTC Investment Structures to your Team Leader

NMTC Investment Structures -

Notes

06/20/2017

CDFI Fund Contact Information

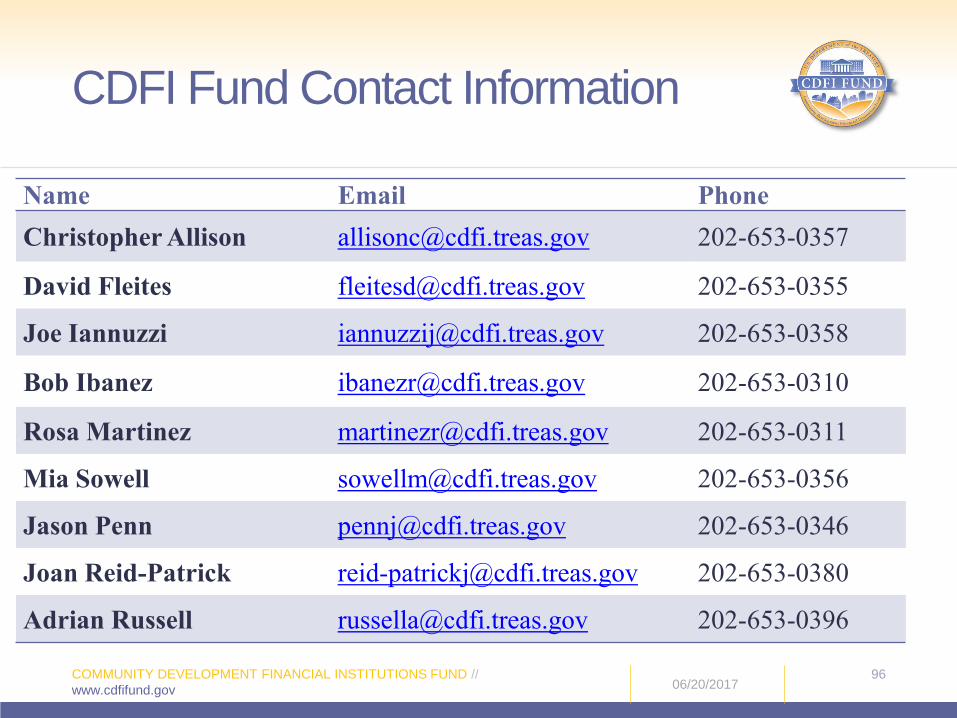

Name Email Phone

Christopher Allison [email protected] 202-653-0357

David Fleites [email protected] 202-653-0355

Joe Iannuzzi [email protected] 202-653-0358

Bob Ibanez [email protected] 202-653-0310

Rosa Martinez [email protected] 202-653-0311

Mia Sowell [email protected] 202-653-0356

Jason Penn [email protected] 202-653-0346

Joan Reid-Patrick [email protected] 202-653-0380

Adrian Russell [email protected] 202-653-0396

COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND //

www.cdfifund.gov

9606/20/2017