review of the livestock/meat and milk value chains and ... of the livestock/meat and milk value...

TRANSCRIPT

REVIEW OF THE LIVESTOCK/MEAT AND MILK

VALUE CHAINS AND POLICY INFLUENCING

THEM IN GHANA

ii

REVIEW OF THE LIVESTOCK/MEAT AND MILK VALUE CHAINS AND

POLICY INFLUENCING THEM IN GHANA

Kwame Oppong-Apane

Edited by

Olanrewaju Smith

Abdou Salla

Berhanu Bedane

Published by the Food and Agriculture Organization of the United Nations and

the Economic Community of West African States

2016

ii

The designations employed and the presentation of material in this information product do not imply the expression of any

opinion whatsoever on the part of the Food and Agriculture Organization of the United Nations (FAO), or of the Economic

Community of West African States (ECOWAS) concerning the legal or development status of any country, territory, city or

area or of its authorities, or concerning the delimitation of its frontiers or boundaries. The mention of specific companies or

products of manufacturers, whether or not these have been patented, does not imply that these have been endorsed or

recommended by FAO, or ECOWAS in preference to others of a similar nature that are not mentioned.

The views expressed in this information product are those of the author(s) and do not necessarily reflect the views or policies

of FAO, or the ECOWAS.

© FAO and ECOWAS, 2016

FAO encourages the use, reproduction and dissemination of material in this information product. Except where otherwise

indicated, material may be copied, downloaded and printed for private study, research and teaching purposes, or for use in

non-commercial products or services, provided that appropriate acknowledgement of FAO as the source and copyright holder

is given and that FAO’s endorsement of users’ views, products or services is not implied in any way.

All requests for translation and adaptation rights, and for resale and other commercial use rights should be made via

www.fao.org/contact-us/licence-request or addressed to [email protected].

FAO information products are available on the FAO website (www.fao.org/publications) and can be purchased through

Cover photos

Top row left to right 1. A bucher selling meat cuts in Tajikstan - © FAO / Vasily Maximov 2. A child looking after cattle in

Beinam, Niger - © FAO / Ado Youssouf 3. Weighing milk in Naivasha, Kenya - © FAO / Simon Maina

Bottom row left to right 1. Chopping meat in Kumasi, Ghana - © FAO / Pietro Cenini 2. Masai men at livestock market in

Kenya - © FAO / Simon Maina 3. A women after milking in Chifra, Ethiopia - © FAO / Giulio Napolitano

iii

Table of contents

LIST OF ACRONYMS AND ABBREVIATIONS ............................................................................................... vii

LIST OF TABLES ...................................................................................................................................................... viii

LIST OF FIGURES ....................................................................................................................................................... x

EXECUTIVE SUMMARY .......................................................................................................................................... xi

1. INTRODUCTION ........................................................................................................................................ 1

2. SOCIO-ECONOMIC CONTEXT OF THE MEAT AND MILK VALUE CHAINS ....................... 3

2.1. Ghana land area and human population trend........................................................................................ 3

2.2 Current GDP of the country and trends in recent years ..................................................................... 3

2.3 Contribution of each of the meat and milk value chains to the national GDP and its trend ....... 4

2.4 Contribution to house-hold income, wellbeing, employment .............................................................. 4

2.5 Proportion of population engaged in meat and milk value chains ....................................................... 5

2.5.1. The main objectives of producing meat and milk ........................................................................... 5

3. THE DESCRIPTION AND MAPPING OF THE MEAT AND MILK VALUE CHAINS ................ 6

3.1. The structure of the meat and milk value chains ................................................................................... 6

3.2. Physical flows of meat and milk among the different components .................................................... 6

3.3 Milk value chain ................................................................................................................................................ 7

3.4. Primary production process ...................................................................................................................... 10

3.4.1. Prevailing livestock farming or other animal production systems ............................................ 10

3.4.2. Average farm size ................................................................................................................................. 11

3.4.3. Yield per unit weight per species of animal and milk production per cow per day and per

lactation .................................................................................................................................................. 11

3.4.4. Total production of meat and milk from each farming system ................................................. 12

3.4.5. Meat and milk post-harvest losses ................................................................................................... 12

3.4.6. Output storage capacity ..................................................................................................................... 12

3.5 Inputs and factors for primary production ............................................................................................. 13

3.5.1. Type and quantity of input required for the meat and milk value chain ................................. 13

3.5.2. Purchase prices of input per type for the meat and milk value chain. .................................... 14

3.5.3. Seasonality in prices and quantities of the main inputs ............................................................... 14

3.5.4. Stocking costs of inputs ...................................................................................................................... 14

3.5.5. Transportation costs of inputs from various locations ............................................................... 15

3.6. Processing stages up to the final commodity......................................................................................... 15

3.7 Various by-products and/or joint products ............................................................................................ 16

3.8 Geographical location of the different value chain components ........................................................ 17

iv

3.9 Amount of land and other natural resources allocated to the meat and milk value chains ........ 17

3.10 Resources ..................................................................................................................................................... 18

3.11 Impact of the meat and milk value chains on environment .............................................................. 18

3.12 Production and value addition potential ................................................................................................ 19

3.13 Number of value chain actors by component ...................................................................................... 19

3.14 Current and potential (domestic) demand of meat and milk ........................................................... 19

3.15 Current and potential (foreign) demand of meat and milk ............................................................... 20

3.16 Specific features of products, including product differentiation ...................................................... 20

The products capacity to fulfill international requirements (sanitary and other .................................. 20

3.17 Urban rural relationships .......................................................................................................................... 20

3.18 Synergies with other activities ................................................................................................................. 21

3.19 Role in local production systems ............................................................................................................ 21

4. INFRASTRUCTURE AND OTHER SUPPORT SERVICES ............................................................... 22

4.1 Transport ....................................................................................................................................................... 22

4.2 Packaging and stocking costs of output .................................................................................................. 22

4.3 Equipment, required investment, facilities and related ....................................................................... 22

4.4 Extension and technical support .............................................................................................................. 22

4.5 Quality control and certification .............................................................................................................. 23

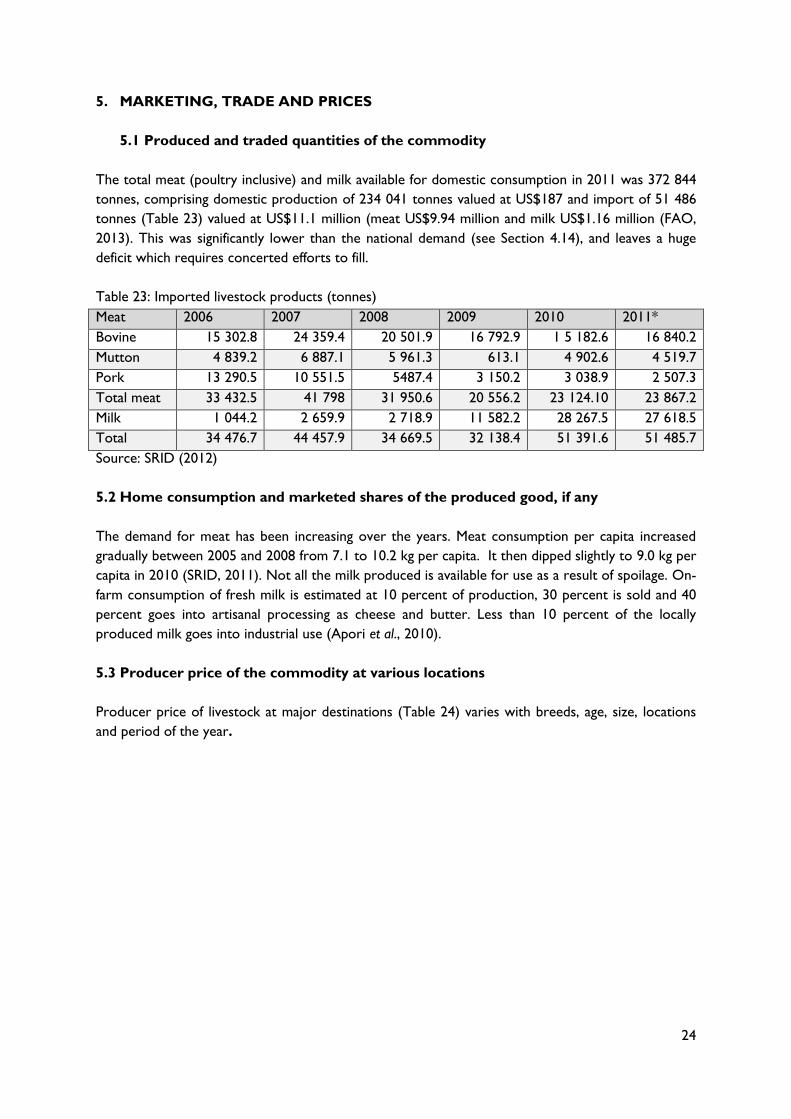

5. MARKETING, TRADE AND PRICES ..................................................................................................... 24

5.1 Produced and traded quantities of the commodity .............................................................................. 24

5.2 Home consumption and marketed shares of the produced good, if any ....................................... 24

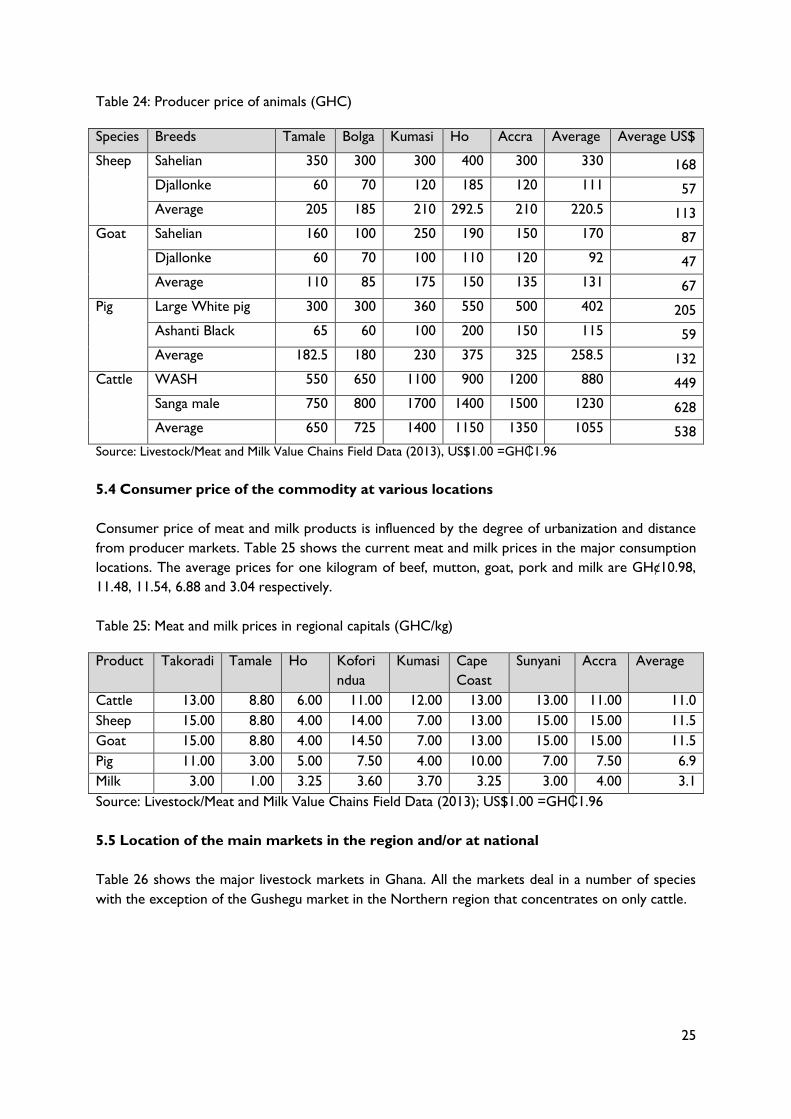

5.3 Producer price of the commodity at various locations ...................................................................... 24

5.4 Consumer price of the commodity at various locations ................................................................... 25

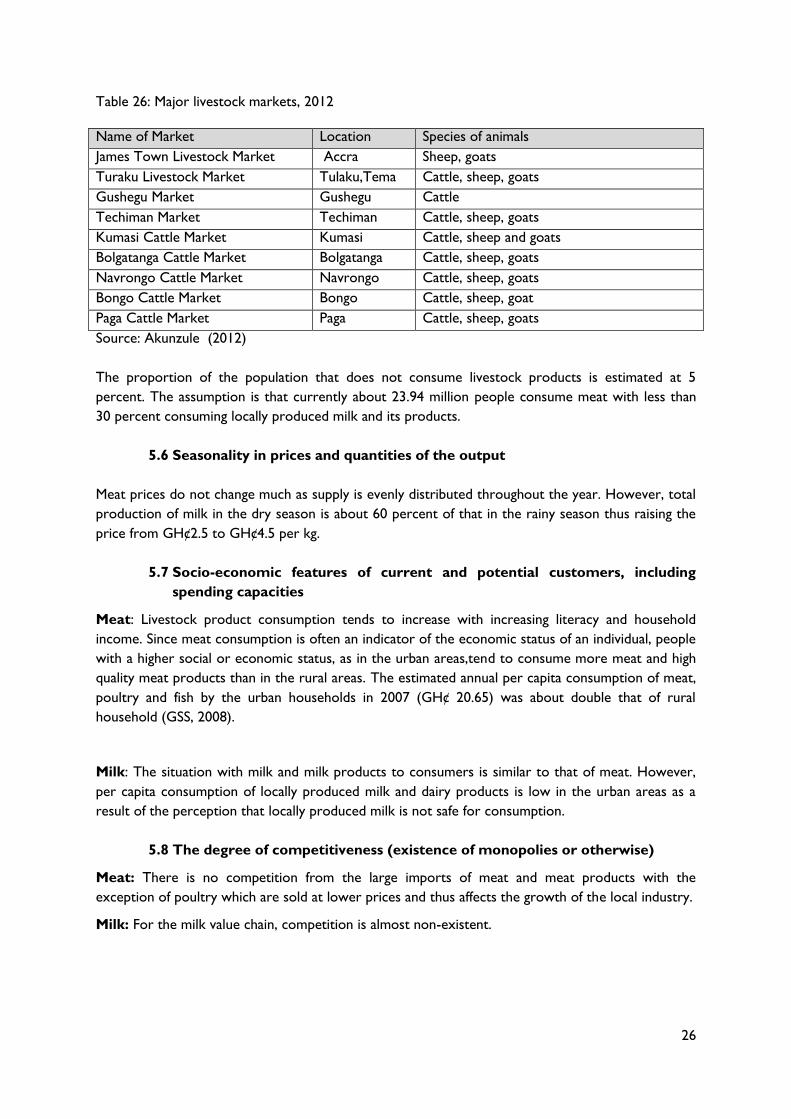

5.5 Location of the main markets in the region and/or at national ........................................................ 25

5.6 Seasonality in prices and quantities of the output ............................................................................... 26

5.7 Socio-economic features of current and potential customers, including spending capacities .. 26

5.8 The degree of competitiveness (existence of monopolies or otherwise) ..................................... 26

5.9 Control over prices (different prices setting and control) ................................................................ 27

5.10 Wholesale and retail distribution ............................................................................................................ 27

v

5.11 International price trends .......................................................................................................................... 27

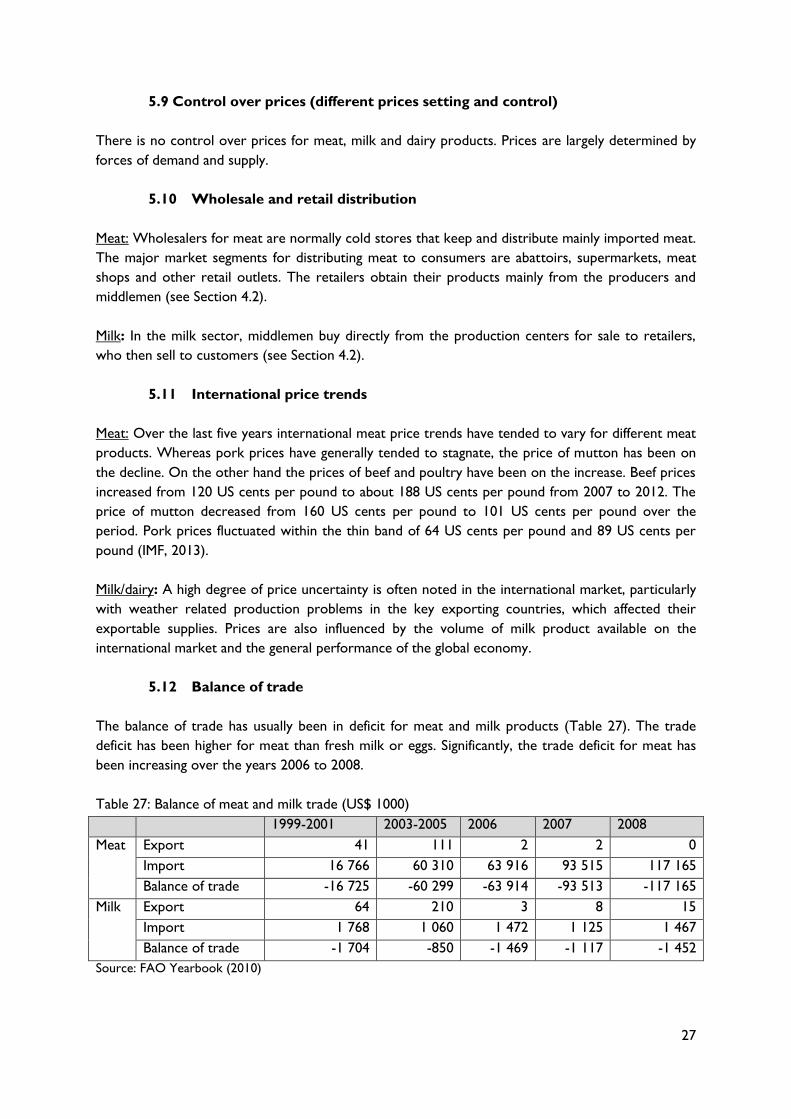

5.12 Balance of trade ........................................................................................................................................... 27

5.13 Current and potential competitors ......................................................................................................... 28

6. GOVERNANCE AND INSTITUTIONAL ARRANGEMENT .......................................................... 29

6.1 The organization and interactions among the different value chain actors in vertical

integration processes. ................................................................................................................................. 29

6.2 Existence of association/cooperatives and their strength .................................................................. 29

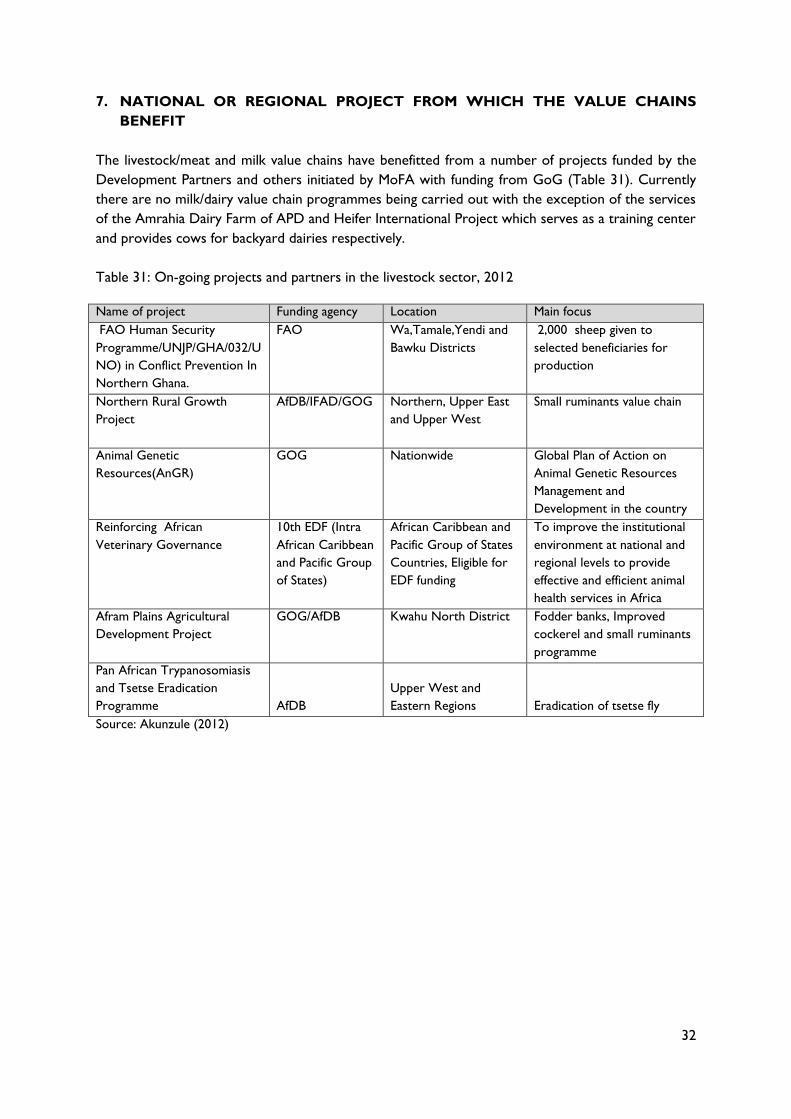

7. NATIONAL OR REGIONAL PROJECT FROM WHICH THE VALUE CHAINS BENEFIT .... 32

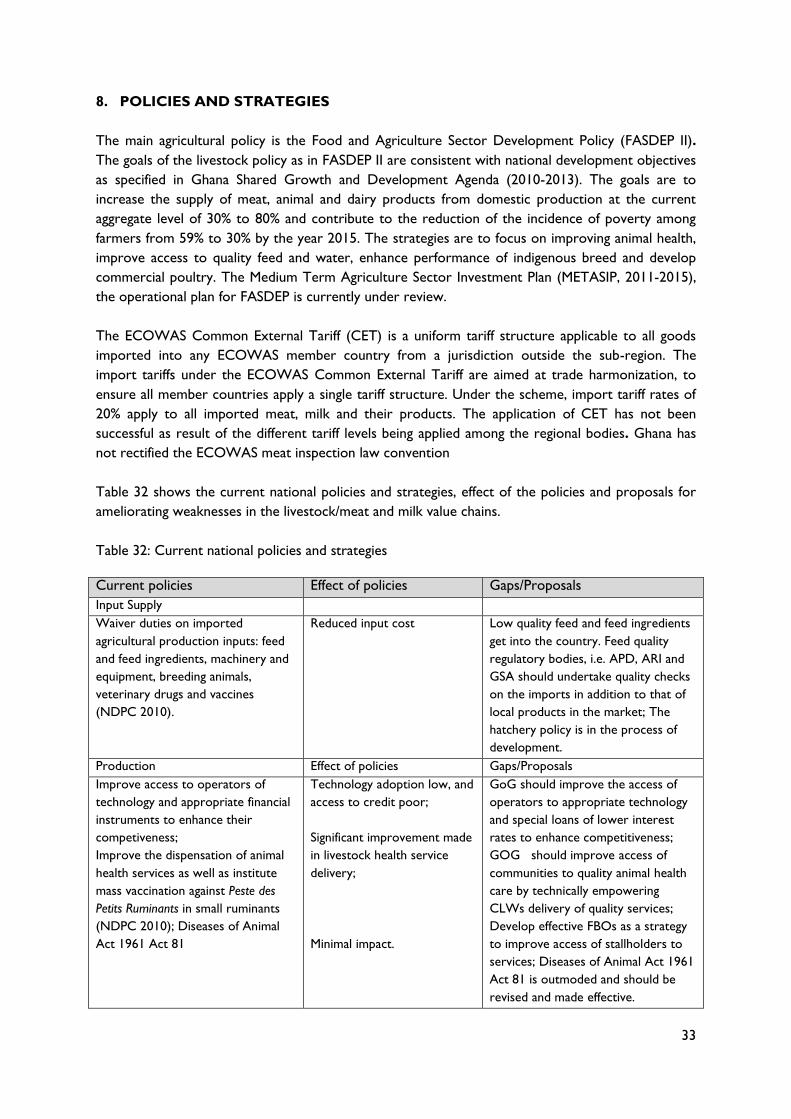

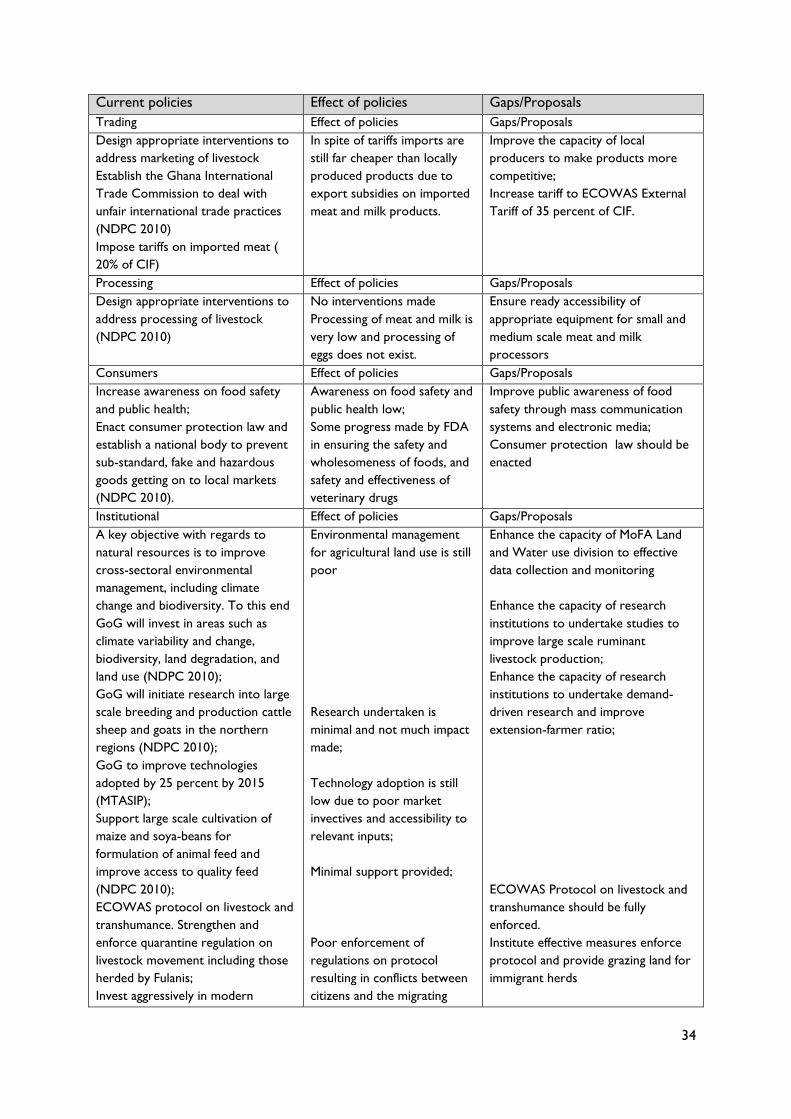

8. POLICIES AND STRATEGIES .................................................................................................................. 33

8.1 Incentives or disincentives to producers and consumers ................................................................... 35

8.2 Credit policies .............................................................................................................................................. 35

8.3 International trade policies ........................................................................................................................ 35

8.4 Acts, regulations and laws governing the value chain ......................................................................... 36

8.5 Major constraints requiring policy interventions ................................................................................. 36

8.6 Suggested policies for smooth operation of meat and milk value ................................................... 37

9. CONSTRAINTS AFFECTING MEAT AND MILK VALUE CHAINS AND PROPOSED

SOLUTIONS .............................................................................................................................................................. 39

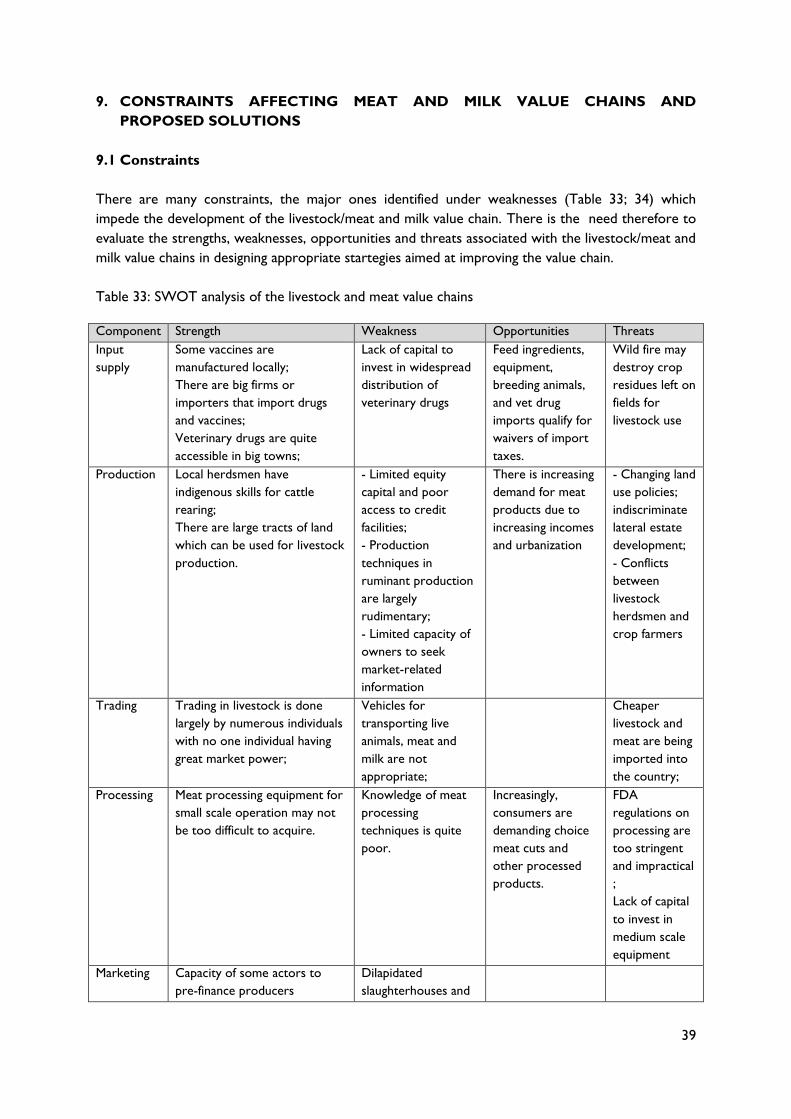

9.1 Constraints .................................................................................................................................................... 39

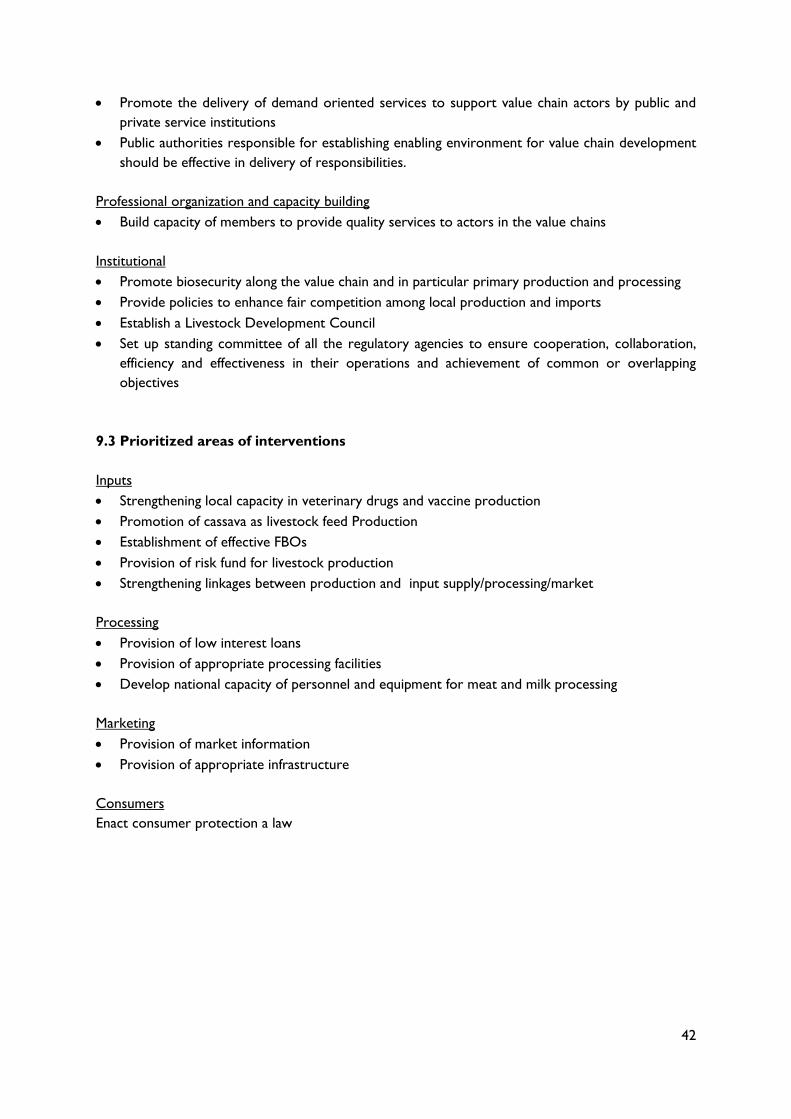

9.2 Proposed solutions ...................................................................................................................................... 41

9.3 Prioritized areas of interventions ............................................................................................................ 42

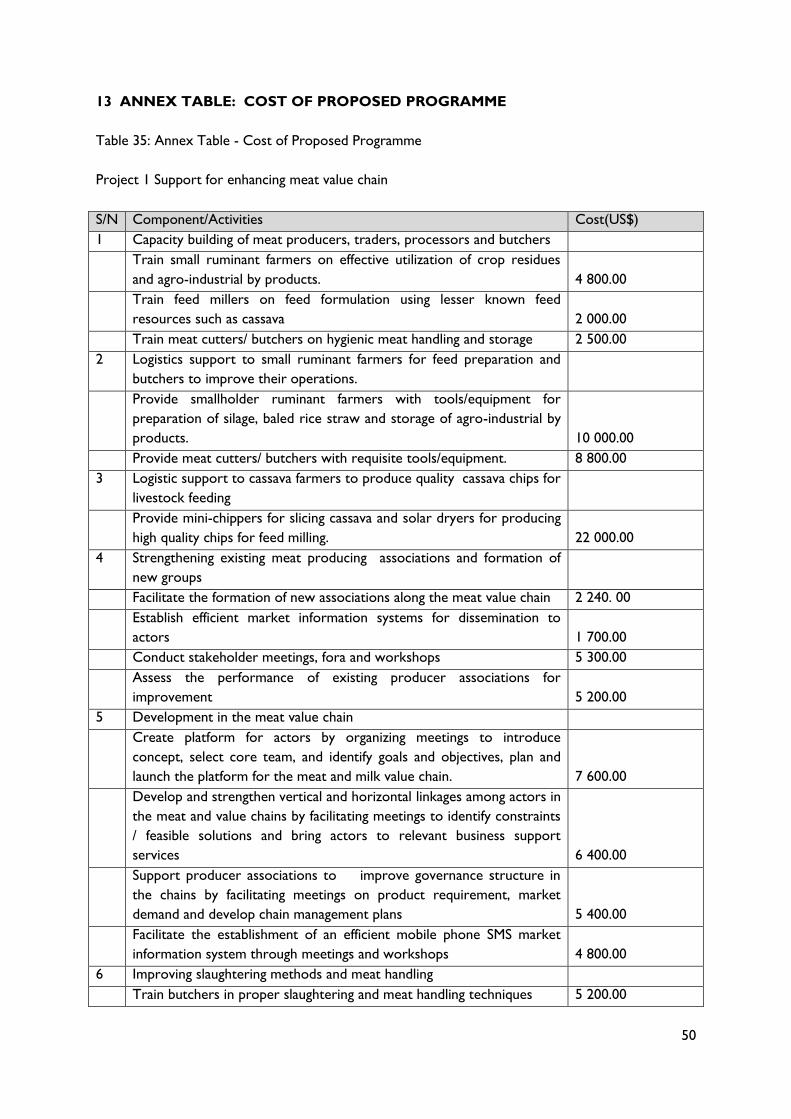

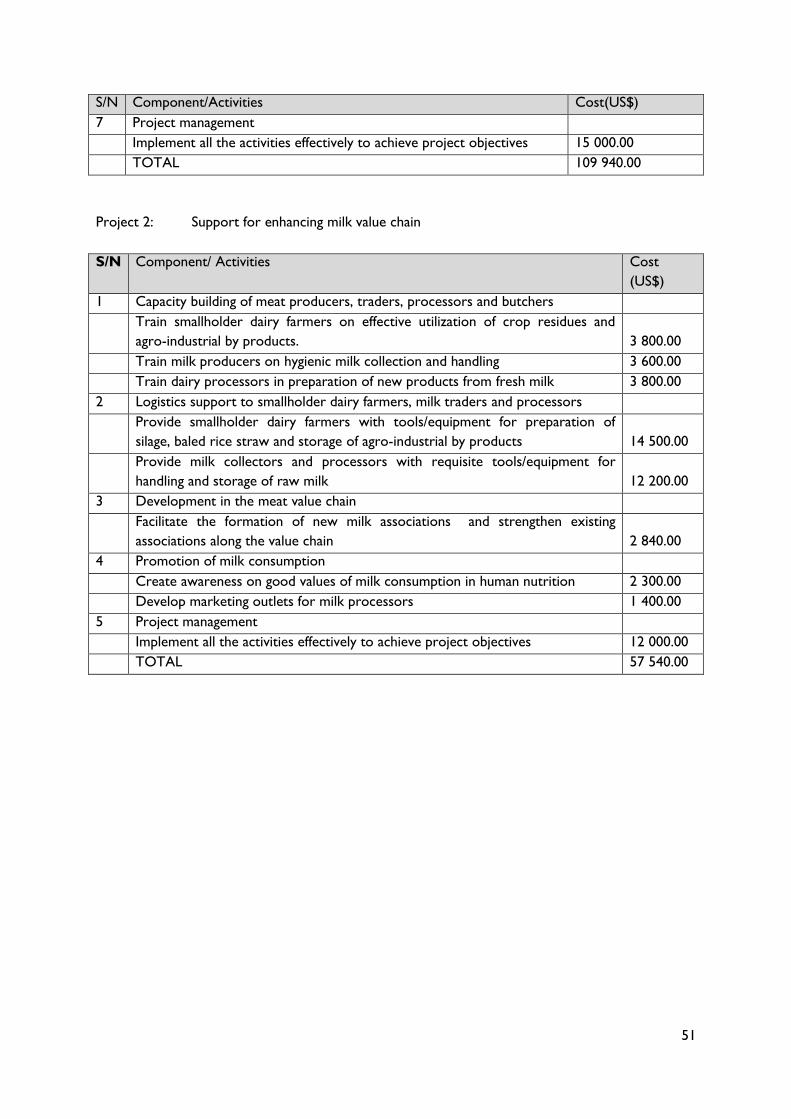

10 SUGGESTED PROJECTS AND PROGRAMMES ................................................................................ 43

11 CONCLUSIONS ......................................................................................................................................... 47

12 REFERENCES ................................................................................................................................................ 48

13 ANNEX TABLE: COST OF PROPOSED PROGRAMME ................................................................ 50

vi

vii

LIST OF ACRONYMS AND ABBREVIATIONS

AfDB African Development Bank

AI Artificial Insemination

APD Animal Production Directorate

ARI Animal Research Institute

CET Common External Tariff

CFI Cost Insurance and Freight

CSIR Council for Scientific and Industrial Research

ECOWAS Economic Commission of West African States

FAO Food and Agriculture Organization of the United Nations

FASDEP Food and Agriculture Sector Development Policy

FBO Farmer Based Organisation

FDA Food and Drugs Authority

GDP Gross Domestic Product

GH¢ Ghanaian cedi

GoG Government of Ghana

GSA Ghana Standards Authority

GSS Ghana Statistical Service

GTZ German Technical Cooperation

IFAD International Fund for Agricultural Development

Kg Kilogram

MoFA Ministry of Food and Agriculture

MTASIP Medium Term Agricultural Sector Investment Plan

NDPC National Development Planning Council

NGO Non-Governmental Organisations

SRID Statistics Research and Information Directorate

US$ United States dollars

VSD Veterinary Services Directorate

WASH West African Short Horn

viii

LIST OF TABLES

Table 1: Ghana land area and human population trend ..................................................................................... 3

Table 2: Contribution of Agriculture and Livestock to GDP ........................................................................... 3

Table 3: Breeds, types and population of livestock ............................................................................................ 4

Table 4: Trends in annual domestic production of meat and milk (tonnes) ................................................ 4

Table 5: Monetary value of domestic livestock products in 2011 (US$ million) ......................................... 4

Table 6: Imports of live animals, heads .................................................................................................................. 6

Table 7: Milk imports (tonnes) ................................................................................................................................ 8

Table 8: Main types of market agents in traditional milk product markets .................................................. 8

Table 9: Average farm sizes for various species of livestock ......................................................................... 11

Table 10: Mature weight, dressing percentage and carcass weight of livestock ........................................ 11

Table 11: Domestic milk production per cow ................................................................................................... 12

Table 12: Meat and milk production from farming systems, tonnes (2013) ............................................... 12

Table 13: Quantity of inputs required for the meat and milk value chain .................................................. 13

Table 14: Importation of veterinary products, 2009 ........................................................................................ 13

Table 15: Prices of inputs for livestock production ......................................................................................... 14

Table 16: Transportation of maize from producer markets, GHC .............................................................. 15

Table 17: Processing stages of the commodities ............................................................................................... 15

Table 18: Processing stages of milk ...................................................................................................................... 15

Table 19: Meat and milk by-products and joint-products ............................................................................... 16

Table 20: Processing level of meat and milk....................................................................................................... 17

Table 21: Geographical location of components in the meat and milk value chain .................................. 17

Table 22: Environmental impacts through meat and milk value chains ....................................................... 18

Table 23: Imported livestock products (tonnes) ............................................................................................... 24

Table 24: Producer price of animals (GHC) ...................................................................................................... 25

Table 25: Meat and milk prices in regional capitals (GHC/kg) ....................................................................... 25

Table 26: Major livestock markets, 2012 ............................................................................................................ 26

Table 27: Balance of meat and milk trade (US$ 1000) .................................................................................... 27

Table 28: National dairy and butchers/meat cutters/ small livestock owners association ...................... 29

Table 29: Major NGOs acting in support to the livestock/meat and milk value chains .......................... 30

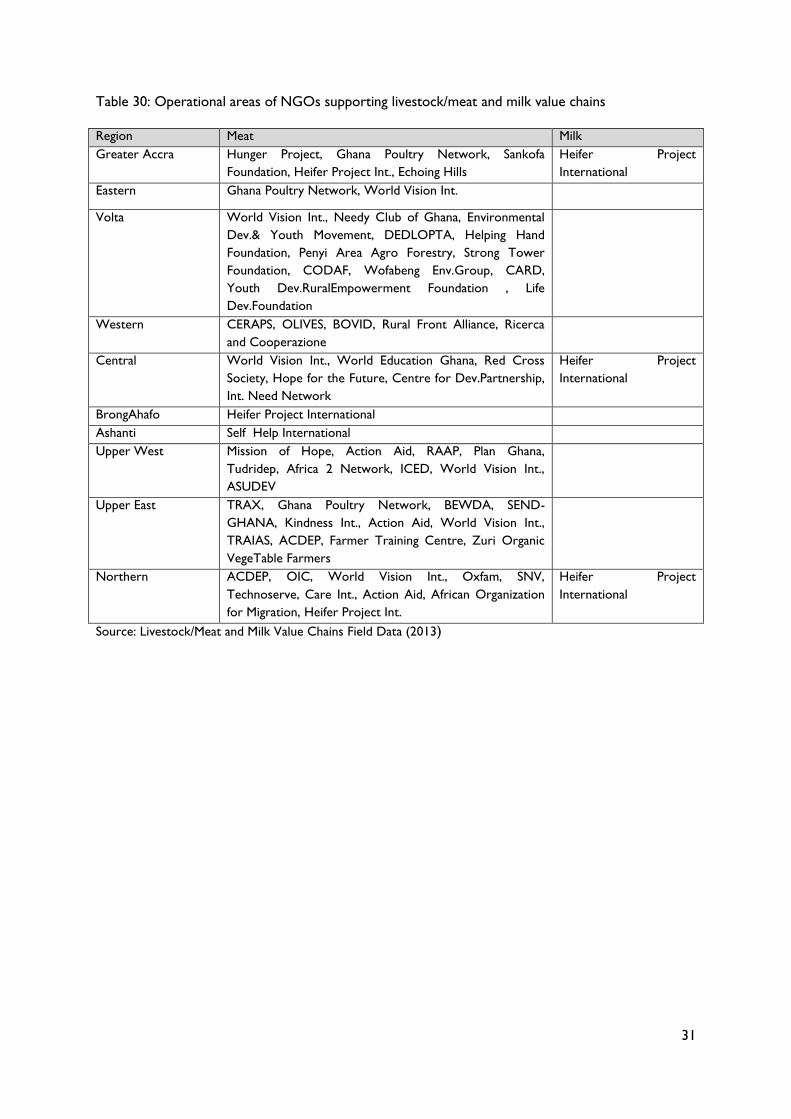

Table 30: Operational areas of NGOs supporting livestock/meat and milk value chains ....................... 31

Table 31: On-going projects and partners in the livestock sector, 2012 .................................................... 32

Table 32: Current national policies and strategies ........................................................................................... 33

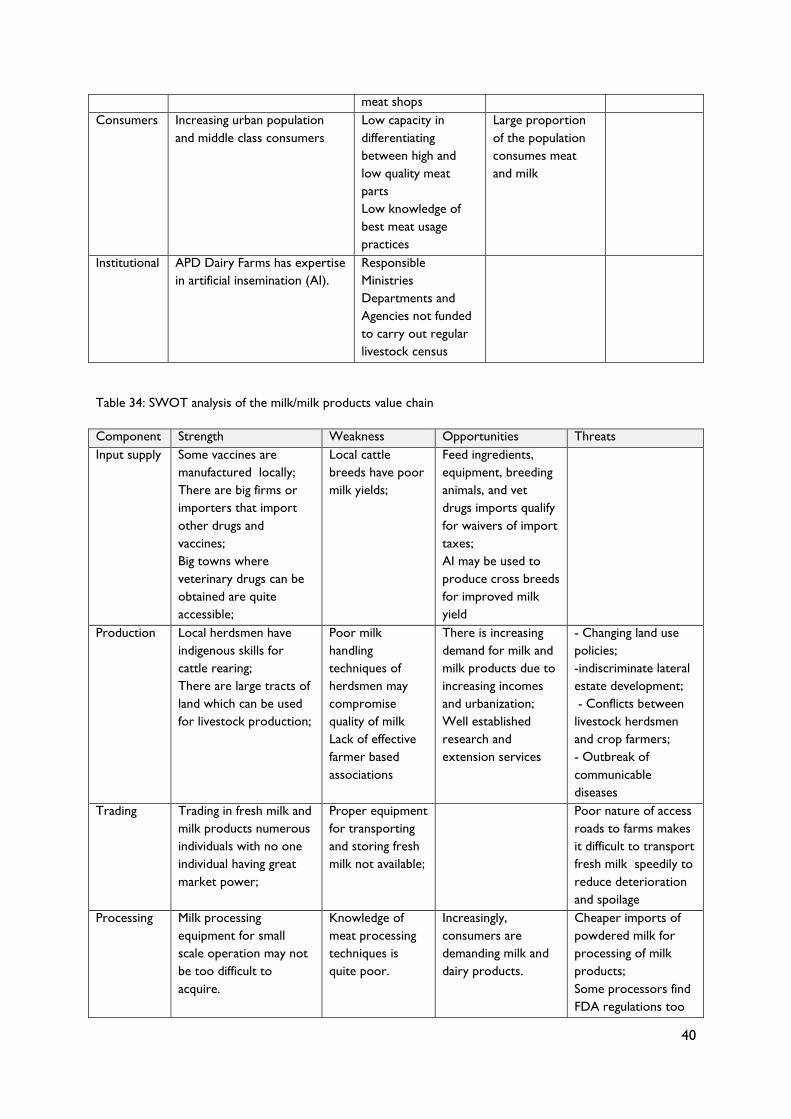

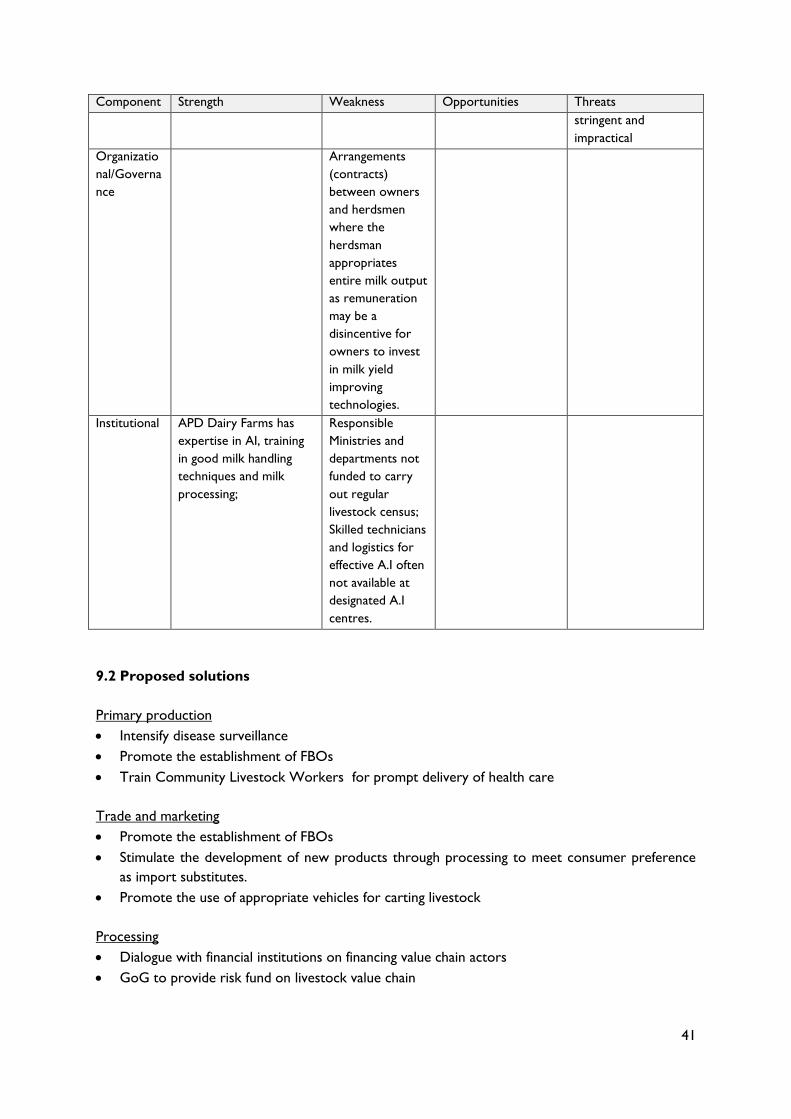

Table 33: SWOT analysis of the livestock and meat value chains ................................................................ 39

ix

Table 34: SWOT analysis of the milk/milk products value chain .................................................................. 40

Table 35: Annex Table - Cost of Proposed Programme ................................................................................ 50

x

LIST OF FIGURES

Figure 1: Livestock/meat value chain ...................................................................................................................... 7

Figure 2: Milk value chain .......................................................................................................................................... 9

xi

EXECUTIVE SUMMARY

The study provides an overview of Ghana’s livestock/meat and dairy value chains. It addresses the

current status of the value chains, makes an inventory of the strengths and constraints of the value

chains, as well as policies that could affect them. It also identifies gaps and prescribes solutions. A

programme is proposed for investment in the value chains.

Socio economic context

The livestock sector contributes significantly to the national economy through its positive impacts on

food security, employment opportunities for a large proportion of the population, prospects for

wealth creation, income enhancement and improvement in rural livelihoods. The main objectives of

producing livestock products in the smallholder system are for subsistence and household

consumption, while the commercial farms have profit as a motive.The livestock sector contributed

GH¢1 159 million amounting to 1.7 percent of the national Gross Domestic product (GDP) and

about 7.4 percent of agricultural GDP in 2012. The sector grew at 5.1 percent in 2011, falling slightly

to 5.0 percent in 2012, and produced a total of 234 041 tonnes of meat, eggs and milk in 2011

valued at US$851.03 million (FAO, 2013). Import figures for 2011 were 138 803 tonnes (M0FA,

2012) valued at US$553.57 (FAO, 2013) and the sector engaged 41.3 percent of the Ghanaian

population in 2011 (Akunzule, 2012).

Current status of livestock/meat and milk value chains

The structure of the livestock /meat and milk value chains reflects the economic relations among

players at each stage of the chains. Actors in the value chains comprised input dealers, producers,

processors, wholesalers, retailers, consumers research scientists and policy makers.There are

several governmental, non-governmental organisations (NGOs) and associations in the value chains

scattered all over the country performing different functions including advocacy. The associations are

poorly linked and have not been very effective in their functions and need to be strengthened to play

effective roles in the development of the chains.

For all the livestock commodities there are a few companies that import inputs such as veterinary

drugs, vaccines, feed additives, feed ingredients and concentrates. Two major vaccines against

Newcastle Disease and Anthrax are produced locally by the Veterinary Services Directorate (VSD)

of the Ministry of Food and Agriculture (MoFA). A few feed milling companies produce compounded

and concentrate feeds for livestock farmers. There are only four standard abattoirs for the slaughter

of cattle, sheep, goats and pigs and six processing plants for poultry in the country.

The uptake of research output has been low in the past, partly as a result of the top-down approach

to research. The introduction of the Research Extension Linkage Committee concept has improved

extension delivery and uptake and is benefiting primary producers in the value chains. There is,

however, a need to strengthen the capacity of both researchers and extensionists.

There are several regulatory bodies currently ensuring the quality control and certification of feed,

meat, milk and dairy products. Those for feed control are the Animal Production Directorate (APD)

of MoFA, Ghana Standards Authority (GSA) and Food and Drugs Authority (FDA). The Veterinary

Services Directorate, together with FDA, has the responsibility for veterinary drugs, vaccines, and

livestock products and by-products quality control. Coordination among the regulatory institutions

has not been very effective thus militating against the development of the meat and milk value chains.

xii

Policies on livestock/meat and milk value chains

Policy instruments to improve the effectiveness of the livestock/meat and milk value chains can be

found in the medium term national development policy framework: Ghana Shared Growth and

Development Agenda by the National Development Planning Council (NDPC, 2010). Some of the

policies have also been captured under the Food and Agriculture Sector Development Policy II

(FASDEP II). The policies include: Provision of waiver of duty on imported agricultural inputs;

Improving access to operators of technology; Improving appropriate financial instruments to

enhance the competiveness of the actors in production, processing and marketing; Improving the

dispensation of animal health service and Design appropriate interventions to address processing and

marketing of meat and milk products and by-products.

Others are: Establishing a commission to deal with unfair international trade practices; Impose

tariffs on imported meat; Increase awareness on food safety and public health; Enacting consumer

protection law and establish a national body to prevent sub-standard, fake and hazardous goods

getting on to local markets; Improving cross-sectoral environmental management, including climate

change and biodiversity; Improving technology adoption; Supporting large scale cultivation of maize

and soybeans for formulation of animal feed and improve access to quality feed.

Some of the key strategies being implemented under FASDEP II are: Focusing on improving animal

health; Improving access to quality feed and water; Enhancing performance of indigenous breeds

through a programme of selection; Developing commercial poultry as the priority for improving

meat supply in the short term, while measures are implemented to transform smallholder

production into profitable enterprises; Improve access of operators to technology and appropriate

financial instruments to enhance their competitiveness with imports.

Some gaps identified in the operation of the policies include: Importation of low quality feed and feed

ingredients; Ineffectiveness of feed quality regulatory bodies and quality checks of imported and local

products in the market; Inadequate access to technology and high interest on loans; Lack of access

to quality animal health care in some communities; Farmer Based Organizations (FBOs) that are not

very effective in seeking smallholder access to services ; Low capacity of local producers to make

products more competitive with imported ones; Inadequate capacity of research institutions to

deliver technologies and inadequate extension delivery resulting from low extension-farmer ratio.

The major constraints in the livestock/meat and milk value chains and the gaps identified in the

operation of the policies were confirmed by a cross section of participants representing various

actors in the value chains at the livestock/meat and milk value chain workshop. A programme titled

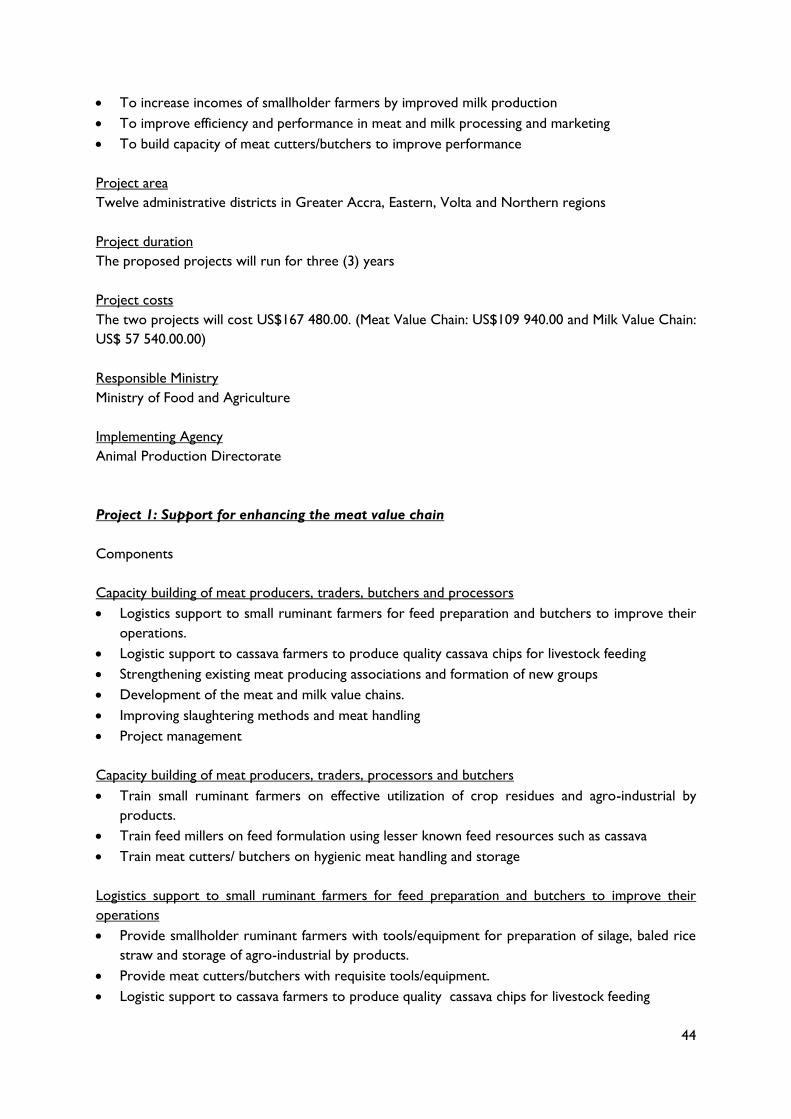

“Enhancing the performance of meat and milk value chains through improved animal genetic

resources, feed resources and meat processing systems” comprising two projects (i) Support for

enhancing livestock /meat value chain, and (ii) Support for enhancing milk value chain in Ghana are

proposed to improve the performance of the livestock, meat and milk value chains at a cost of

US$167 480.00. The programme will run for a period of three years.

1. INTRODUCTION

The Ghana livestock sub-sector is dominated by small scale operators who are mainly crop farmers

keeping livestock to supplement their incomes and/or for food security purposes. There are few

well-organized commercial poultry and pig operations in the country (MoFA, 2010).

Livestock population statistics are generally poor as there has been no livestock census for several

decades in Ghana. MoFA has been relying on projections, which do not accurately portray the

livestock situation (MoFA, 2010) as there has not been any consistent monitoring of the livestock

population since the last census.

The livestock sector is an important component of Ghana’s agriculture, and contributes in direct

products about 8.69 and 1.7 percents of agricultural and national GDP respectively (GSS, 2013).

These amounts do not include the value of secondary products, such as manure, draught power and

transport provided to the crop sector. The sector’s socio-economic importance in the reduction of

rural poverty is well acknowledged, particularly among farmers in the Northern, Upper West and

Upper East regions. Manure from livestock is now an invaluable resource to the crop and vegetable

farmers for the maintenance of soil fertility and structure as well as control of soil erosion.

Livestock supply not only meat, milk and eggs, but also skins for leather, bones, blood and horns for

animal feed.

The use of bullocks for land preparation allows farmers to crop larger areas than would have been

possible in view of the high cost involved in using tractor power. Among the numerous

contributions of the livestock, meat and dairy value chain to the national economy is food security as

it provides animal protein to enhance the nutritional status of the human population. Livestock offer

prospects for employment, wealth creation, income enhancement and improvement in rural

livelihoods. The livestock sector is dominated by small scale operators who are mainly crop farmers

keeping livestock to supplement their incomes and/or for security purposes. There are, however,

few well-organized commercial poultry and pig operations in the country (MoFA, 2010).

The livestock value chain describes the full range of activities which are required to bring livestock,

meat and milk products and their by-products or service from conception, through the input of

various services (such as feed milling, hatching and health care), the different phases of production

(involving a combination of physical transformation such as processing) to the delivery of products

to final consumers, and final disposal after use. Since 2005, German Technical Cooperation (GTZ)

has focused on the development of the Guinea fowl value chain in the three northern regions, and

this has led to the establishment of a vibrant Guinea fowl farmer’s associations in the area. In

general, the value chain development in the country’s livestock sector is limited (Akunzule, 2012).

The Government of Ghana (GoG) with assistance from some Non-Governmental Organisations

(NGOs) and Donor Partners have applied a number of instruments in the implementation of

projects to address the constraints in the livestock sector. However, most of the projects did not

achieve the desired impact. This might have resulted partially from too much emphasis being put on

production with not enough attention given to the other components along the livestock value

chain. It is expected that future development in the livestock sector will be more successful and

sustainable if interventions are done using the value chain approach.

2

The objective of the consultancy was to review the livestock/meat and milk value chains and take

stock of policies influencing them, and assist the national focal person for livestock/meat and milk

value chain in organizing and conducting a national validation workshop. More specifically, the

following were to be undertaken; i. Establish the current status of livestock/meat and milk value

chains, ii) Conduct an inventory of current policies on livestock/meat and milk value chains and

identify gaps, iii) Identify projects and programmes for the development/enhancement of

livestock/meat and milk value chains and propose priority investment plans for each value chain, iv)

Identify policies facilitating the development or enhancement of livestock/meat and milk value chains

and suggest mechanism of embedding them in key national policy documents.

Data were sourced directly or indirectly from international organisations such as the Food and

Agriculture Organization of the United Nations (FAO), Ghanaian public sector institutions, private

sector organizations and farmer/processor associations as well as some key actors involved in the

livestock sector. Data obtained from field studies were used to fill gaps and confirm some secondary

data.

The document is presented in thirteen chapters. The First and Second chapters present Executive

Summary and Introduction to the study respectively. The Third, Fourth and Fifth Chapters present

Overview of the Socio-Economic Context, Mapping, Infrastructure and Other Support Services of

the Meat and Milk Value Chains. Chapter Six deals with the Marketing, Trade and Prices of Livestock

and Livestock Products; Chapter Seven presents the Governance and Institutional Arrangement of

the different Value Chain Actors while Chapter Eight presents the National or Regional Projects

from which the Value Chains Benefit. Chapter Nine presents Policies and Strategies Influencing the

Meat and Milk Value Chains and Chapter Ten deals with the Constraints Affecting Value Chains and

Proposed Solutions. Chapter Eleven suggests a Programme for Improving the Performance of the

Value Chains, while Chapter Twelve presents the Conclusions emanating from the study. Chapter

Thirteen provides References to data used in the document.

3

2. SOCIO-ECONOMIC CONTEXT OF THE MEAT AND MILK VALUE CHAINS

2.1. Ghana land area and human population trend

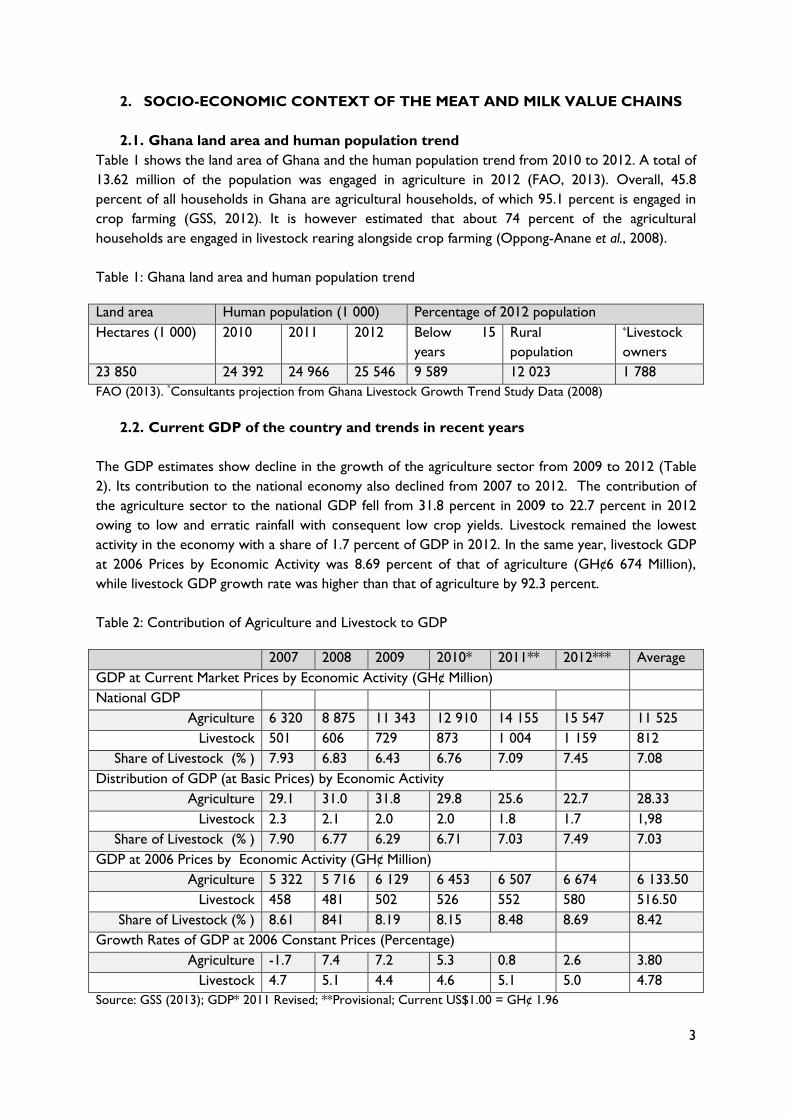

Table 1 shows the land area of Ghana and the human population trend from 2010 to 2012. A total of

13.62 million of the population was engaged in agriculture in 2012 (FAO, 2013). Overall, 45.8

percent of all households in Ghana are agricultural households, of which 95.1 percent is engaged in

crop farming (GSS, 2012). It is however estimated that about 74 percent of the agricultural

households are engaged in livestock rearing alongside crop farming (Oppong-Anane et al., 2008).

Table 1: Ghana land area and human population trend

Land area Human population (1 000) Percentage of 2012 population

Hectares (1 000) 2010 2011 2012 Below 15

years

Rural

population

*Livestock

owners

23 850 24 392 24 966 25 546 9 589 12 023 1 788

FAO (2013). *Consultants projection from Ghana Livestock Growth Trend Study Data (2008)

2.2. Current GDP of the country and trends in recent years

The GDP estimates show decline in the growth of the agriculture sector from 2009 to 2012 (Table

2). Its contribution to the national economy also declined from 2007 to 2012. The contribution of

the agriculture sector to the national GDP fell from 31.8 percent in 2009 to 22.7 percent in 2012

owing to low and erratic rainfall with consequent low crop yields. Livestock remained the lowest

activity in the economy with a share of 1.7 percent of GDP in 2012. In the same year, livestock GDP

at 2006 Prices by Economic Activity was 8.69 percent of that of agriculture (GH¢6 674 Million),

while livestock GDP growth rate was higher than that of agriculture by 92.3 percent.

Table 2: Contribution of Agriculture and Livestock to GDP

2007 2008 2009 2010* 2011** 2012*** Average

GDP at Current Market Prices by Economic Activity (GH¢ Million)

National GDP

Agriculture 6 320 8 875 11 343 12 910 14 155 15 547 11 525

Livestock 501 606 729 873 1 004 1 159 812

Share of Livestock (% ) 7.93 6.83 6.43 6.76 7.09 7.45 7.08

Distribution of GDP (at Basic Prices) by Economic Activity

Agriculture 29.1 31.0 31.8 29.8 25.6 22.7 28.33

Livestock 2.3 2.1 2.0 2.0 1.8 1.7 1,98

Share of Livestock (% ) 7.90 6.77 6.29 6.71 7.03 7.49 7.03

GDP at 2006 Prices by Economic Activity (GH¢ Million)

Agriculture 5 322 5 716 6 129 6 453 6 507 6 674 6 133.50

Livestock 458 481 502 526 552 580 516.50

Share of Livestock (% ) 8.61 841 8.19 8.15 8.48 8.69 8.42

Growth Rates of GDP at 2006 Constant Prices (Percentage)

Agriculture -1.7 7.4 7.2 5.3 0.8 2.6 3.80

Livestock 4.7 5.1 4.4 4.6 5.1 5.0 4.78

Source: GSS (2013); GDP* 2011 Revised; **Provisional; Current US$1.00 = GH¢ 1.96

4

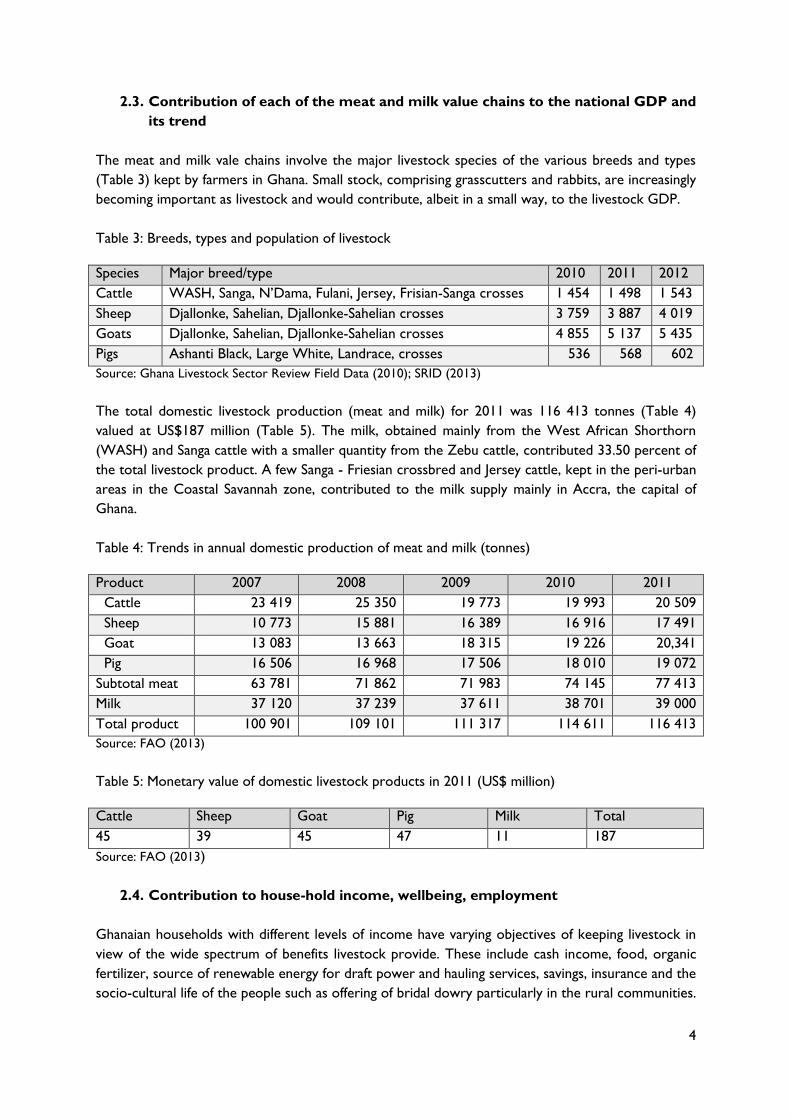

2.3. Contribution of each of the meat and milk value chains to the national GDP and

its trend

The meat and milk vale chains involve the major livestock species of the various breeds and types

(Table 3) kept by farmers in Ghana. Small stock, comprising grasscutters and rabbits, are increasingly

becoming important as livestock and would contribute, albeit in a small way, to the livestock GDP.

Table 3: Breeds, types and population of livestock

Species Major breed/type 2010 2011 2012

Cattle WASH, Sanga, N’Dama, Fulani, Jersey, Frisian-Sanga crosses 1 454 1 498 1 543

Sheep Djallonke, Sahelian, Djallonke-Sahelian crosses 3 759 3 887 4 019

Goats Djallonke, Sahelian, Djallonke-Sahelian crosses 4 855 5 137 5 435

Pigs Ashanti Black, Large White, Landrace, crosses 536 568 602

Source: Ghana Livestock Sector Review Field Data (2010); SRID (2013)

The total domestic livestock production (meat and milk) for 2011 was 116 413 tonnes (Table 4)

valued at US$187 million (Table 5). The milk, obtained mainly from the West African Shorthorn

(WASH) and Sanga cattle with a smaller quantity from the Zebu cattle, contributed 33.50 percent of

the total livestock product. A few Sanga - Friesian crossbred and Jersey cattle, kept in the peri-urban

areas in the Coastal Savannah zone, contributed to the milk supply mainly in Accra, the capital of

Ghana.

Table 4: Trends in annual domestic production of meat and milk (tonnes)

Product 2007 2008 2009 2010 2011

Cattle 23 419 25 350 19 773 19 993 20 509

Sheep 10 773 15 881 16 389 16 916 17 491

Goat 13 083 13 663 18 315 19 226 20,341

Pig 16 506 16 968 17 506 18 010 19 072

Subtotal meat 63 781 71 862 71 983 74 145 77 413

Milk 37 120 37 239 37 611 38 701 39 000

Total product 100 901 109 101 111 317 114 611 116 413

Source: FAO (2013)

Table 5: Monetary value of domestic livestock products in 2011 (US$ million)

Cattle Sheep Goat Pig Milk Total

45 39 45 47 11 187

Source: FAO (2013)

2.4. Contribution to house-hold income, wellbeing, employment

Ghanaian households with different levels of income have varying objectives of keeping livestock in

view of the wide spectrum of benefits livestock provide. These include cash income, food, organic

fertilizer, source of renewable energy for draft power and hauling services, savings, insurance and the

socio-cultural life of the people such as offering of bridal dowry particularly in the rural communities.

5

Livestock may also be sold to increase farm size and to procure inputs such as seeds, fertilizer, farm

tools and labour. Livestock stabilizes the socio-economic capability of households by providing

reliable income in times when prices of crops are low due to bumper harvest.

2.5. Proportion of population engaged in meat and milk value chains

The proportion of population engaged in agriculture is 41.3 percent and the proportion of

population (from total agriculture) engaged in livestock production is 40.0 percent (Akunzule, 2012)

2.5.1. The main objectives of producing meat and milk

The main objective of producing livestock products in the smallholder system is for subsistence and

for satisfying household consumption. Medium and large scale producers of livestock products are

commercial enterprises with the motive of producing for the general market and enhancement of

financial status. Currently, domestic meat and milk production are geared towards domestic

production with no intention of export.

6

3. THE DESCRIPTION AND MAPPING OF THE MEAT AND MILK VALUE CHAINS

3.1. The structure of the meat and milk value chains

Major actors in the meat and milk value chain comprise importers, input dealers, producers,

processors, wholesalers, retailers and consumers. For all the livestock commodities, there are a few

large companies that import veterinary inputs. Formulated feed which is used largely in poultry and

pig production is produced by few large feed milling companies though a number of the farms

produce their own feed. Cattle, sheep, goat, pigs and milk are produced largely by smallholders who

generally sell livestock and milk to middlemen.

3.2. Physical flows of meat and milk among the different components

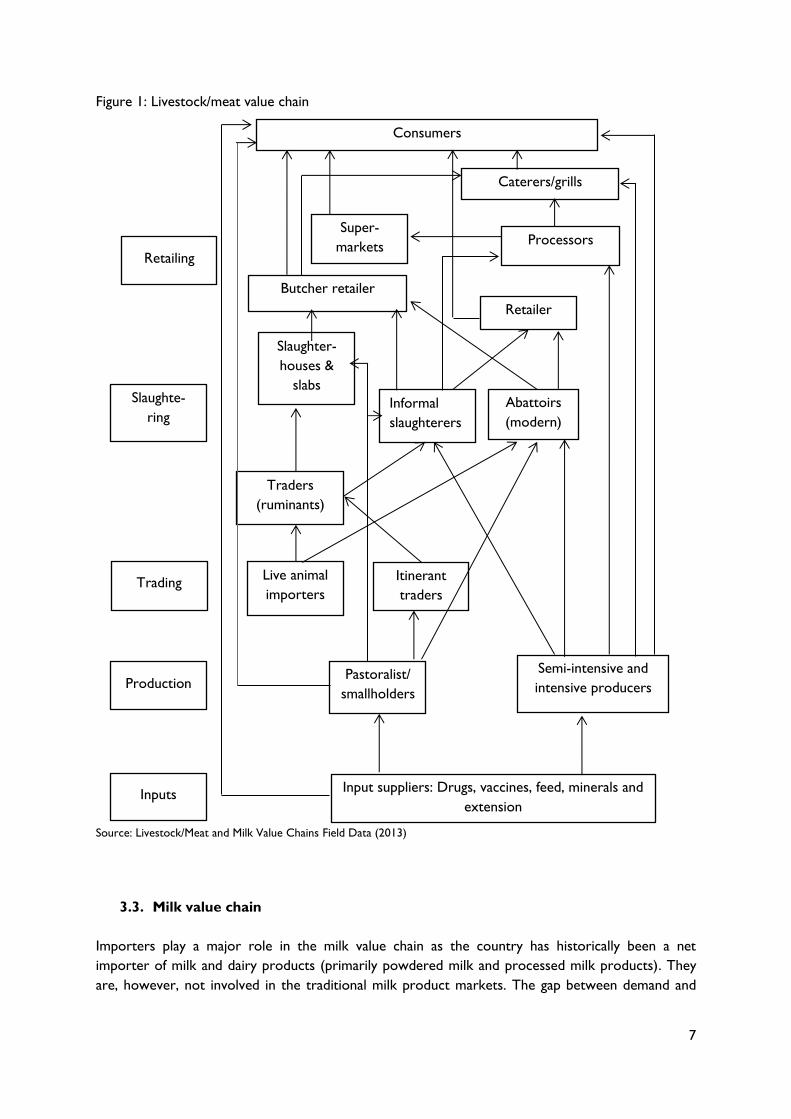

The physical flow of livestock/meat for cattle, sheep, goats, and pigs (Figure 1) starts with the

production of cattle by pastoralists, sheep and goats by smallholder farmers, and pigs reared mostly

under intensive production. Also live cattle (Zebu), sheep and goats imported from neighboring

West-African countries such as Burkina Faso, Mali and Niger get into the chain. A number of live

animals get into the country uncounted for as a result of the porous nature of the borders. The

movement of trade animals across the borders through official entry points, with quarantine stations,

is monitored by the VSD staff in order to prevent the introduction and spread of animal diseases.

Since most of the animals do not come through appropriate points of entry, data of live animal

imports are not reliable.

Table 6 shows the trade animals that passed through the official entry points.

Table 6: Imports of live animals, head

Type of animals 2011 2012

Cattle 9 384 23 622

Sheep 2 835 9 840

Goats 2 495 10 008

Source: VSD (2013)

Itinerant traders may collect animals from pastoralists and smallholders. These end up with traders

in live animal markets and then to butchers who may formally slaughter the animals in abattoirs,

slaughterhouses and slaughter slabs. Butchers may also obtain animals directly from pastoralists and

smallholders. Most of them retail the animals they slaughter. Meat from butchers may also go to

caterers, khebab sellers (grills) or to consumers directly. Some supermarkets usually have in-house

processing units and may receive their meat supplies from abattoirs and informal slaughterers.

Producers who rear animals intensively (e.g. pigs) may slaughter their animals informally and retail

the meat themselves. They may also supply livestock directly to processors who may use the

services of abattoirs or do their own slaughtering. Such processors may supply meat and meat

products to supermarkets which may be integrated to the processing facilities or sell to caterers and

grill operators. Supermarkets retail their meat to consumers, while caterers also reach consumers

by using the meat for food. Meat also reaches consumers through khebab sellers and grill operators.

Consumers may also get their animal supplies directly from the producers or live animal markets.

7

Figure 1: Livestock/meat value chain

Source: Livestock/Meat and Milk Value Chains Field Data (2013)

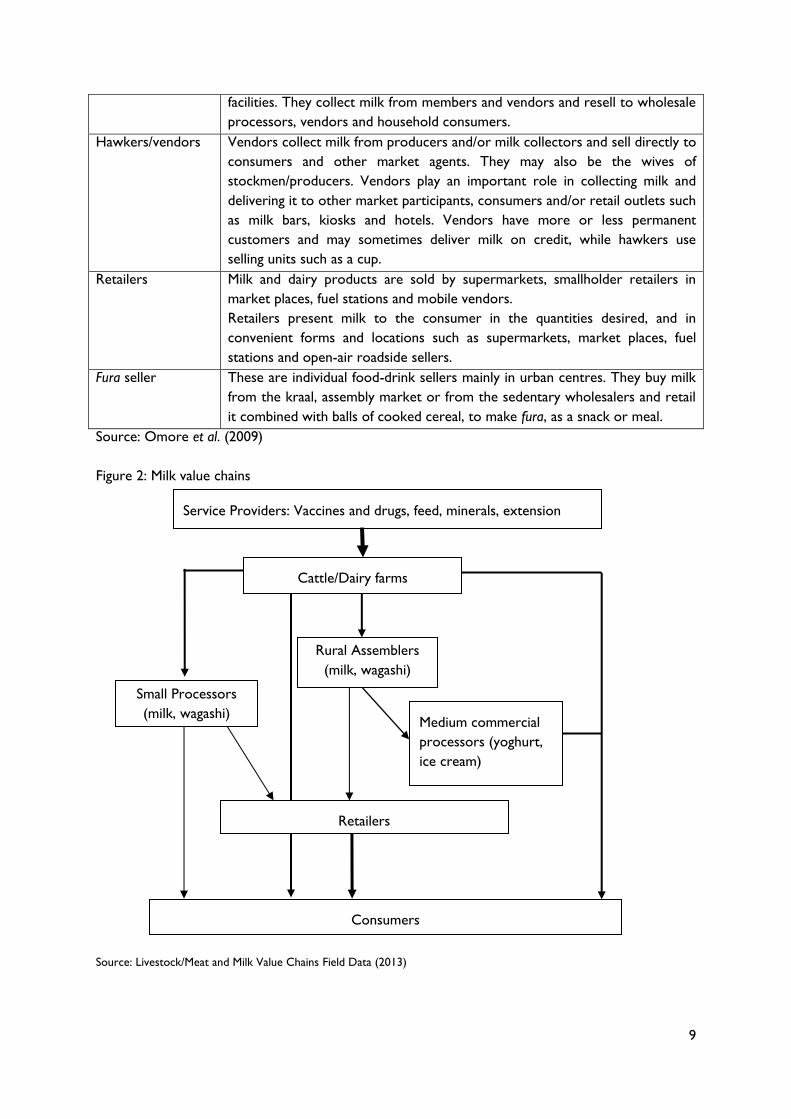

3.3. Milk value chain

Importers play a major role in the milk value chain as the country has historically been a net

importer of milk and dairy products (primarily powdered milk and processed milk products). They

are, however, not involved in the traditional milk product markets. The gap between demand and

Pastoralist/

smallholders

Semi-intensive and

intensive producers

Live animal

importers

Itinerant

traders

Traders

(ruminants)

Informal

slaughterers

Abattoirs

(modern)

Super-

markets

Consumers

Caterers/grills

Input suppliers: Drugs, vaccines, feed, minerals and

extension Inputs

Production

Slaughte-

ring

Retailing

Trading

Processors

Slaughter-

houses &

slabs

Butcher retailer

Retailer

8

local production of milk and dairy products keeps on widening year after year to the extent that the

imported milk and dairy products increased by 2 268 percent from 2006 to 2012 (Table 7).

Ghana’s dairy processors (including ice cream, baby foods, chocolate milk, yoghurt, and long-life milk

producers) rely on combining and reconstituting milk powder imported mostly from the European

Union countries. Dairy products such as infant formula, cheese, butter and ice cream are imported.

A total of 34 local dairy processors had registered with the Ghana Food and Drugs Authority by

2009. Prominent among the producers were Nestles Ghana Ltd, Fan Milk, Promisidor and West

Africa Distribution Ltd. Artisanal production of yogurt from locally produced milk is reducing in

favour of industrial production that uses almost solely imported milk powder. The small scale

yoghurt manufactures use approximately 20 percent locally produced milk to 80 percent imported

milk powder (Apori, et al. 2010).

Table 7: Milk imports (tonnes)

Year 2006 2007 2008 2009 2010 2011 2012

Quantity 1 044 2 656 2 719 11 406 27 323 27 619 24 728

Source: SRID (2013)

An important feature about domestic milk supply in Ghana is that there is usually a separation

between cattle owning and cattle keeping. While cattle owners can be from any ethnic group, they

arrange to have the cattle kept and milked by herdsmen mainly from the Fulani tribe, who have

greater indigenous knowledge of husbandry practices. While the owners buy and sell the animals,

the herdsmen or stockmen collect and sell the milk. Milk is produced largely by pastoralists using

WASH and Sanga cattle and few intensive producers who use Friesian X Sanga crossbreds and the

exotic Jersey breed. Market agents in the traditional milk value chain are shown in Table 8 and figure

2.

Table 8: Main types of market agents in traditional milk product markets

Type of seller Description

Producer-seller Producers who also sell their milk. These are herdsmen or their wives who

sell their own milk at the farm/kraal or in the village, rural town or roadside.

They often consume some of the milk. They are included among processors

below.

Processors These types of sellers procure milk to process into other products like

yoghurt, ice cream and cheese. These include home processors of soft cheese

known as wagashi, generally wives of stockmen/producers. Processors of

yogurt may also receive their supplies from specialized dairy farmers using

exotic breeds

Private

wholesalers/

Assembler

Wholesalers buy milk in bulk from producers and/or rural assemblers and sell

it to retailers. Assemblers sell generally to other wholesalers. No chilling is

generally used. They therefore play the role of bulkers in the marketing

system.

Collection centres/

dairy cooperatives

Dairy cooperatives facilitate milk collection and marketing; this activity is

located around collection centres. Most dairy cooperatives have cooling

9

facilities. They collect milk from members and vendors and resell to wholesale

processors, vendors and household consumers.

Hawkers/vendors Vendors collect milk from producers and/or milk collectors and sell directly to

consumers and other market agents. They may also be the wives of

stockmen/producers. Vendors play an important role in collecting milk and

delivering it to other market participants, consumers and/or retail outlets such

as milk bars, kiosks and hotels. Vendors have more or less permanent

customers and may sometimes deliver milk on credit, while hawkers use

selling units such as a cup.

Retailers Milk and dairy products are sold by supermarkets, smallholder retailers in

market places, fuel stations and mobile vendors.

Retailers present milk to the consumer in the quantities desired, and in

convenient forms and locations such as supermarkets, market places, fuel

stations and open-air roadside sellers.

Fura seller These are individual food-drink sellers mainly in urban centres. They buy milk

from the kraal, assembly market or from the sedentary wholesalers and retail

it combined with balls of cooked cereal, to make fura, as a snack or meal.

Source: Omore et al. (2009)

Figure 2: Milk value chains

Source: Livestock/Meat and Milk Value Chains Field Data (2013)

Cattle/Dairy farms

Rural Assemblers

(milk, wagashi)

Small Processors

(milk, wagashi) Medium commercial

processors (yoghurt,

ice cream)

Retailers

Consumers

Service Providers: Vaccines and drugs, feed, minerals, extension

10

3.4. Primary production process

3.4.1. Prevailing livestock farming or other animal production systems

Ghana’s agriculture is predominantly smallholder, traditional and rain-fed, and the farming systems

vary. There are three main farming systems, crop only, livestock only and crop-livestock systems,

with the second and third systems giving rise to the prevailing animal production systems. The major

system practiced nationwide is mixed farming (crop-livestock system) where about 74 percent of the

rural households cultivate crops and rear some livestock (Oppong-Anane et al. 2008).

Non-ruminant production systems

Pigs: Semi-extensive pig production occurs under the traditional smallholder practice in the rural

areas. The system is based mainly on the indigenous Ashanti Black Forest pig which is found

throughout the country and constitutes about 70 percent of the national pig population. Crosses

between the indigenous and exotic breeds are also used in this system. The pigs are kept in pens and

given minimal feed based on household leftovers, and in particular fresh and boiled cassava and

cassava peels. In some cases, the pigs are allowed to scavenge for food. Intensive pig production

system is based mainly on the exotic Large White and Landrace breeds and their crosses. The

system, practiced mainly in the southern areas of the country is commercialized and may be

classified as small, medium or large scale (Oppong-Anane, 2010).

Ruminant production Systems

Sheep and Goats: The extensive sheep and goat production system, also known as traditional small

ruminant production system, consists largely of free grazing village flocks of Djallonké sheep and

goats normally exhibiting poor productivity. Diseases, mostly helminthiasis and peste des petits

ruminants (PPR), are the main causes of poor productivity and high mortality among the animals. This

system is progressively changing into semi-intensive system throughout the country. In the semi-

intensive system simple pens are provided for the animals within or attached to the owner’s house.

The system is based on cut and carry of forages and the use of household wastes. Various other

crop residues and by-products are also used. The intensive system is similar to that of the semi-

intensive except that in the former all the feed is provided in the pen. This system is commonly

practiced in the peri-urban areas (Oppong-Anane, 2010).

Cattle: The extensive beef cattle production system is the main cattle production system practiced

in the country and is based mainly on extensive grazing by smallholder herds. It is linked with a milk

production system whereby milk is shared between the herdsman and the calf, with the surplus

going to the market. In this system, settled farmers whose main occupation is crop cultivation own

cattle. Ownership may be direct, personal and individual, or in the form of trusteeship for family

property. Where a large herd is found, the family groups owning them may be several, varying

widely in size and in relationship. Very few cattle farms fall under the semi-intensive system. In this

commercial production system, cattle are owned mainly by professionals and businessmen living

elsewhere with little or no involvement in the management of the animals. A few farms belonging to

state institutions also fall under this system. In this case, cattle may graze on sown pastures as well as

natural pastures which are often improved with introduced forage legumes (Oppong-Anane, 2010).

There are no intensive cattle farms in the country.

11

Over 90 percent of the domestic milk production comes from agro-pastoral herds with low milk off-

take of about 0.8 and 0.4 kg/cow/day in the rainy and dry seasons respectively. The local breeds of

cattle used in this system have low genetic potential for milk production and remain mediocre

producers even when the best possible feeding and husbandry conditions are available. There are

about a hundred households keeping between one and six dairy cows at their backyards on

commercial basis, and using Friesian - Sanga crossbreds or Jersey cows in the peri-urban Savannah

areas of the Greater Accra and Eastern regions. Such cattle may produce as much as 2 700 kg of

milk per lactation (Oppong-Anane, 2008).

3.4.2. Average farm size

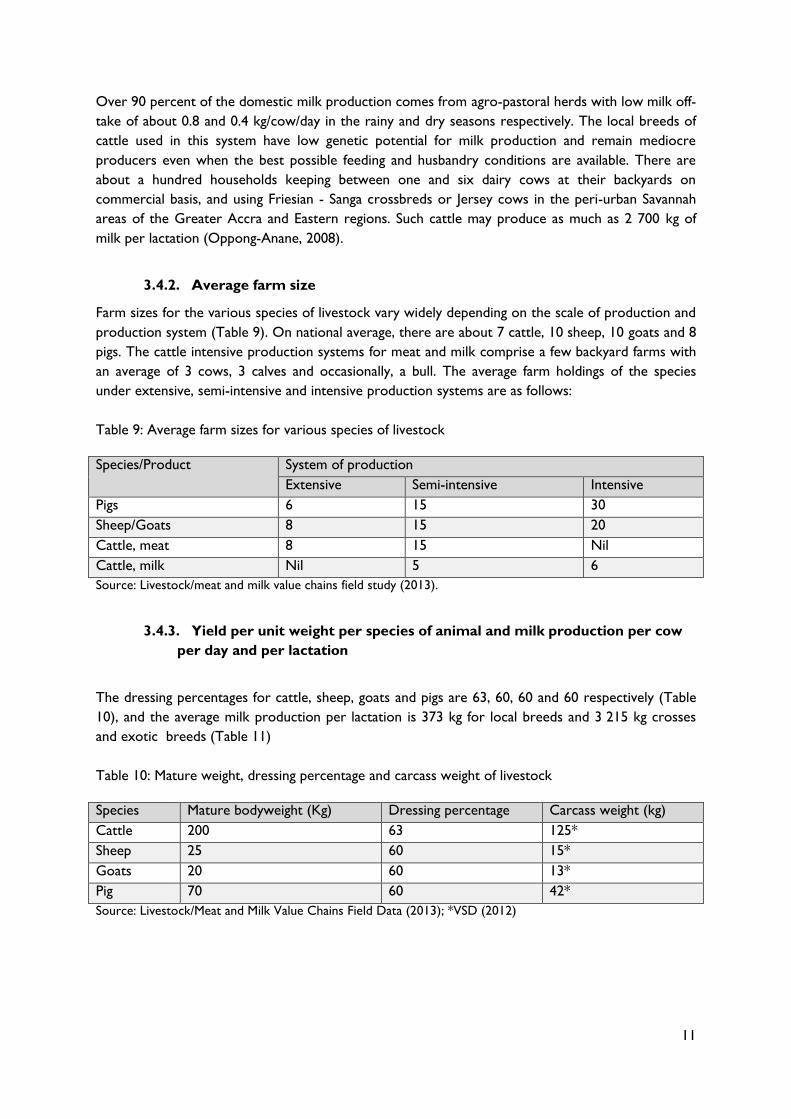

Farm sizes for the various species of livestock vary widely depending on the scale of production and

production system (Table 9). On national average, there are about 7 cattle, 10 sheep, 10 goats and 8

pigs. The cattle intensive production systems for meat and milk comprise a few backyard farms with

an average of 3 cows, 3 calves and occasionally, a bull. The average farm holdings of the species

under extensive, semi-intensive and intensive production systems are as follows:

Table 9: Average farm sizes for various species of livestock

Species/Product System of production

Extensive Semi-intensive Intensive

Pigs 6 15 30

Sheep/Goats 8 15 20

Cattle, meat 8 15 Nil

Cattle, milk Nil 5 6

Source: Livestock/meat and milk value chains field study (2013).

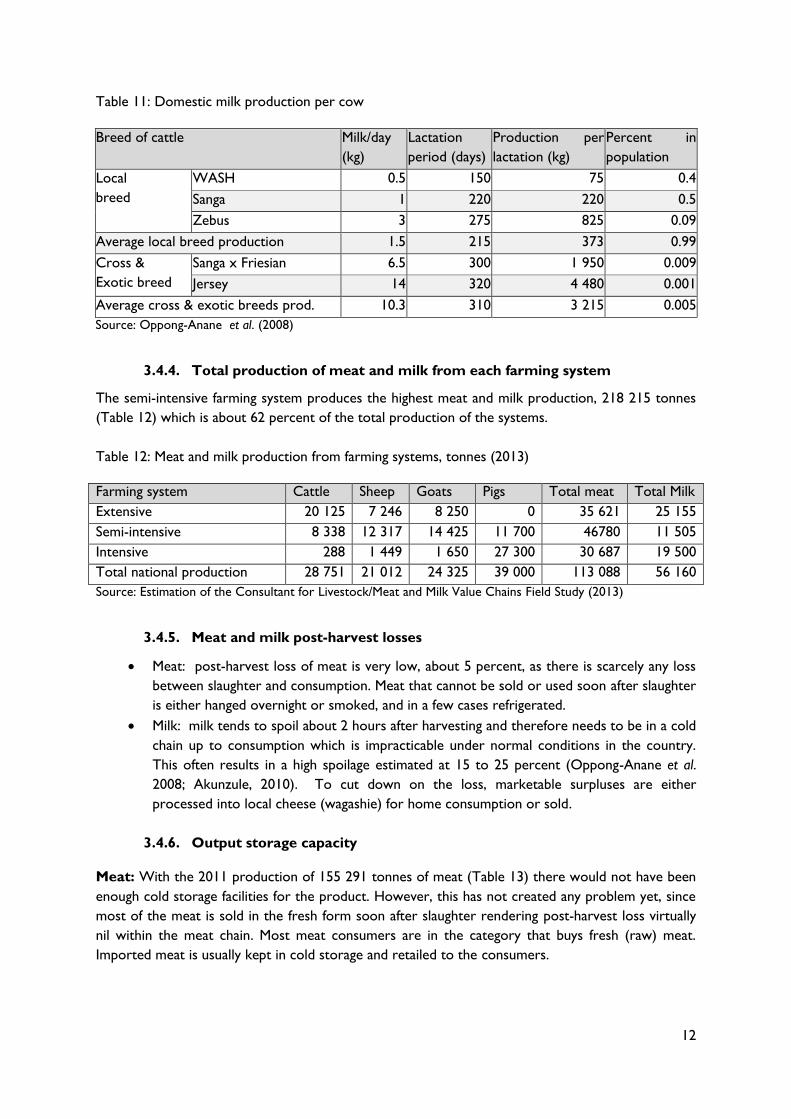

3.4.3. Yield per unit weight per species of animal and milk production per cow

per day and per lactation

The dressing percentages for cattle, sheep, goats and pigs are 63, 60, 60 and 60 respectively (Table

10), and the average milk production per lactation is 373 kg for local breeds and 3 215 kg crosses

and exotic breeds (Table 11)

Table 10: Mature weight, dressing percentage and carcass weight of livestock

Species Mature bodyweight (Kg) Dressing percentage Carcass weight (kg)

Cattle 200 63 125*

Sheep 25 60 15*

Goats 20 60 13*

Pig 70 60 42*

Source: Livestock/Meat and Milk Value Chains Field Data (2013); *VSD (2012)

12

Table 11: Domestic milk production per cow

Breed of cattle Milk/day

(kg)

Lactation

period (days)

Production per

lactation (kg)

Percent in

population

Local

breed

WASH 0.5 150 75 0.4

Sanga 1 220 220 0.5

Zebus 3 275 825 0.09

Average local breed production 1.5 215 373 0.99

Cross &

Exotic breed

Sanga x Friesian 6.5 300 1 950 0.009

Jersey 14 320 4 480 0.001

Average cross & exotic breeds prod. 10.3 310 3 215 0.005

Source: Oppong-Anane et al. (2008)

3.4.4. Total production of meat and milk from each farming system

The semi-intensive farming system produces the highest meat and milk production, 218 215 tonnes

(Table 12) which is about 62 percent of the total production of the systems.

Table 12: Meat and milk production from farming systems, tonnes (2013)

Farming system Cattle Sheep Goats Pigs Total meat Total Milk

Extensive 20 125 7 246 8 250 0 35 621 25 155

Semi-intensive 8 338 12 317 14 425 11 700 46780 11 505

Intensive 288 1 449 1 650 27 300 30 687 19 500

Total national production 28 751 21 012 24 325 39 000 113 088 56 160

Source: Estimation of the Consultant for Livestock/Meat and Milk Value Chains Field Study (2013)

3.4.5. Meat and milk post-harvest losses

Meat: post-harvest loss of meat is very low, about 5 percent, as there is scarcely any loss

between slaughter and consumption. Meat that cannot be sold or used soon after slaughter

is either hanged overnight or smoked, and in a few cases refrigerated.

Milk: milk tends to spoil about 2 hours after harvesting and therefore needs to be in a cold

chain up to consumption which is impracticable under normal conditions in the country.

This often results in a high spoilage estimated at 15 to 25 percent (Oppong-Anane et al.

2008; Akunzule, 2010). To cut down on the loss, marketable surpluses are either

processed into local cheese (wagashie) for home consumption or sold.

3.4.6. Output storage capacity

Meat: With the 2011 production of 155 291 tonnes of meat (Table 13) there would not have been

enough cold storage facilities for the product. However, this has not created any problem yet, since

most of the meat is sold in the fresh form soon after slaughter rendering post-harvest loss virtually

nil within the meat chain. Most meat consumers are in the category that buys fresh (raw) meat.

Imported meat is usually kept in cold storage and retailed to the consumers.

13

Milk: Domestic milk production is far more than the available storage facilities can cope with. Apart

from the government established Amrahia Dairy Farm and the few private mini dairy centres such as

Wankam Farms and that of the research institutions that have bulk tanks and other storage facilities,

storage for raw milk does not exist. Milk is mostly sold fresh.

3.5. Inputs and factors for primary production

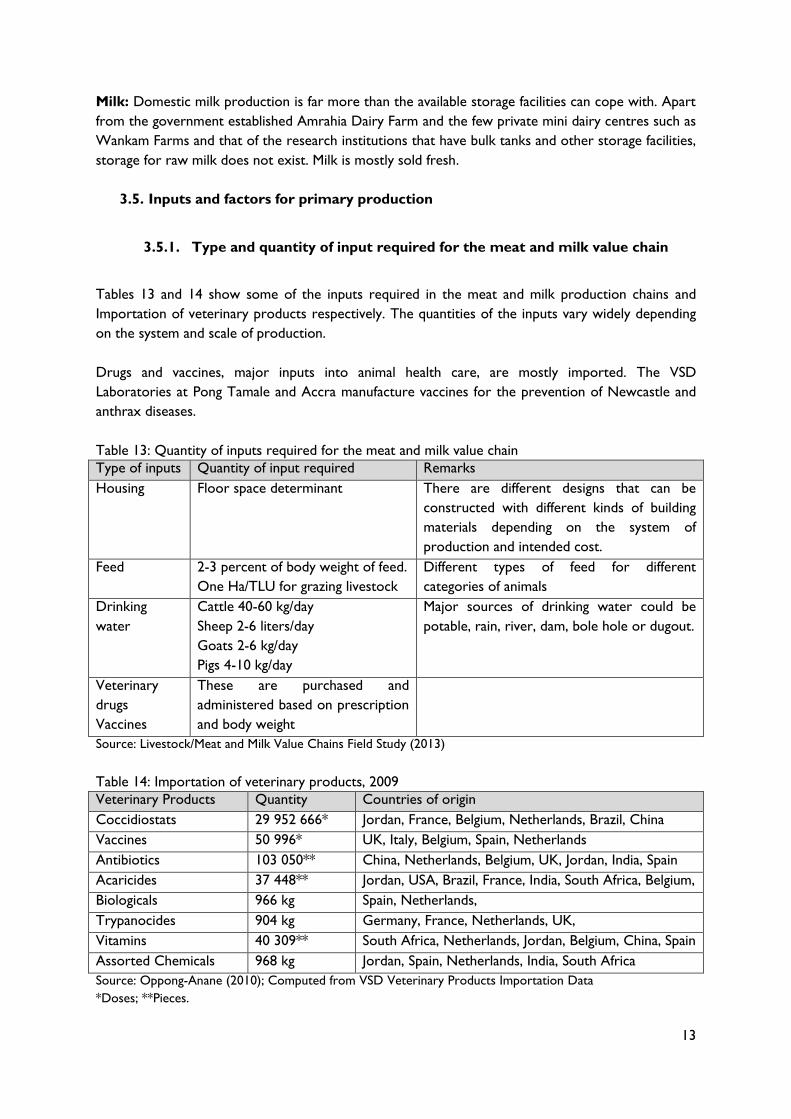

3.5.1. Type and quantity of input required for the meat and milk value chain

Tables 13 and 14 show some of the inputs required in the meat and milk production chains and

Importation of veterinary products respectively. The quantities of the inputs vary widely depending

on the system and scale of production.

Drugs and vaccines, major inputs into animal health care, are mostly imported. The VSD

Laboratories at Pong Tamale and Accra manufacture vaccines for the prevention of Newcastle and

anthrax diseases.

Table 13: Quantity of inputs required for the meat and milk value chain

Type of inputs Quantity of input required Remarks

Housing

Floor space determinant There are different designs that can be

constructed with different kinds of building

materials depending on the system of

production and intended cost.

Feed

2-3 percent of body weight of feed.

One Ha/TLU for grazing livestock

Different types of feed for different

categories of animals

Drinking

water

Cattle 40-60 kg/day

Sheep 2-6 liters/day

Goats 2-6 kg/day

Pigs 4-10 kg/day

Major sources of drinking water could be

potable, rain, river, dam, bole hole or dugout.

Veterinary

drugs

Vaccines

These are purchased and

administered based on prescription

and body weight

Source: Livestock/Meat and Milk Value Chains Field Study (2013)

Table 14: Importation of veterinary products, 2009

Veterinary Products Quantity Countries of origin

Coccidiostats 29 952 666* Jordan, France, Belgium, Netherlands, Brazil, China

Vaccines 50 996* UK, Italy, Belgium, Spain, Netherlands

Antibiotics 103 050** China, Netherlands, Belgium, UK, Jordan, India, Spain

Acaricides 37 448** Jordan, USA, Brazil, France, India, South Africa, Belgium,

Biologicals 966 kg Spain, Netherlands,

Trypanocides 904 kg Germany, France, Netherlands, UK,

Vitamins 40 309** South Africa, Netherlands, Jordan, Belgium, China, Spain

Assorted Chemicals 968 kg Jordan, Spain, Netherlands, India, South Africa

Source: Oppong-Anane (2010); Computed from VSD Veterinary Products Importation Data

*Doses; **Pieces.

14

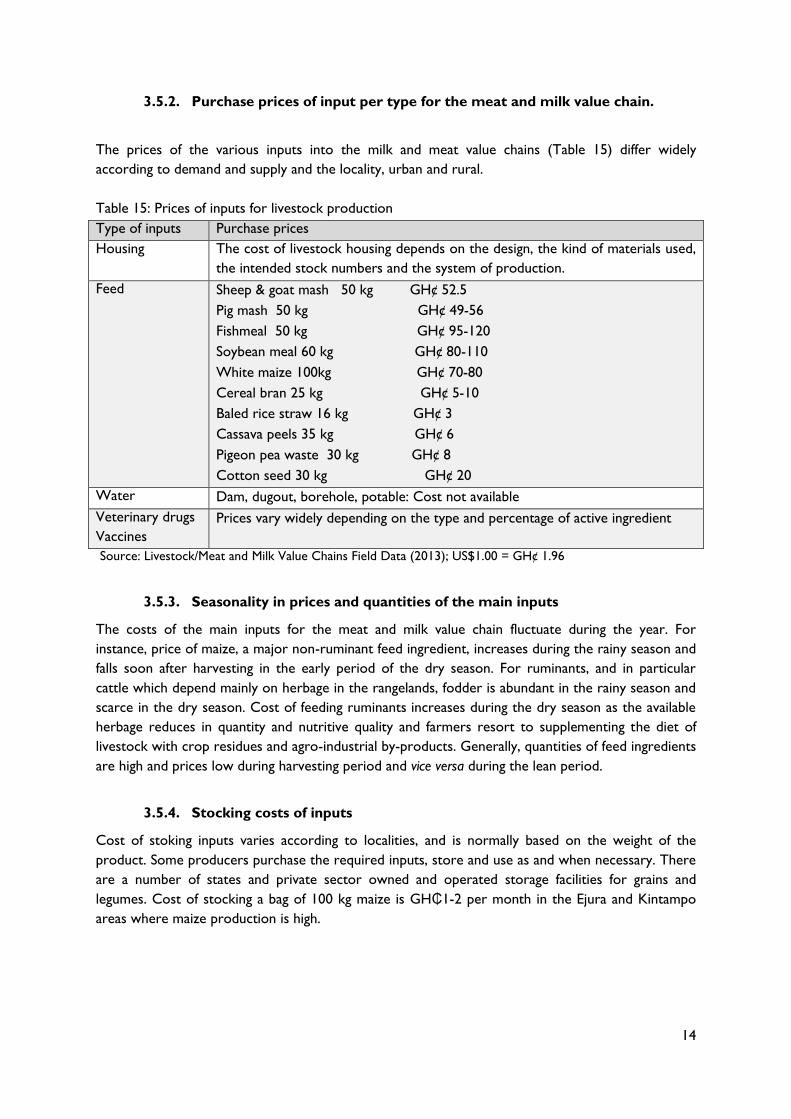

3.5.2. Purchase prices of input per type for the meat and milk value chain.

The prices of the various inputs into the milk and meat value chains (Table 15) differ widely

according to demand and supply and the locality, urban and rural.

Table 15: Prices of inputs for livestock production

Type of inputs Purchase prices

Housing The cost of livestock housing depends on the design, the kind of materials used,

the intended stock numbers and the system of production.

Feed

Sheep & goat mash 50 kg GH¢ 52.5

Pig mash 50 kg GH¢ 49-56

Fishmeal 50 kg GH¢ 95-120

Soybean meal 60 kg GH¢ 80-110

White maize 100kg GH¢ 70-80

Cereal bran 25 kg GH¢ 5-10

Baled rice straw 16 kg GH¢ 3

Cassava peels 35 kg GH¢ 6

Pigeon pea waste 30 kg GH¢ 8

Cotton seed 30 kg GH¢ 20

Water Dam, dugout, borehole, potable: Cost not available

Veterinary drugs

Vaccines

Prices vary widely depending on the type and percentage of active ingredient

Source: Livestock/Meat and Milk Value Chains Field Data (2013); US$1.00 = GH¢ 1.96

3.5.3. Seasonality in prices and quantities of the main inputs

The costs of the main inputs for the meat and milk value chain fluctuate during the year. For

instance, price of maize, a major non-ruminant feed ingredient, increases during the rainy season and

falls soon after harvesting in the early period of the dry season. For ruminants, and in particular

cattle which depend mainly on herbage in the rangelands, fodder is abundant in the rainy season and

scarce in the dry season. Cost of feeding ruminants increases during the dry season as the available

herbage reduces in quantity and nutritive quality and farmers resort to supplementing the diet of

livestock with crop residues and agro-industrial by-products. Generally, quantities of feed ingredients

are high and prices low during harvesting period and vice versa during the lean period.

3.5.4. Stocking costs of inputs

Cost of stoking inputs varies according to localities, and is normally based on the weight of the

product. Some producers purchase the required inputs, store and use as and when necessary. There

are a number of states and private sector owned and operated storage facilities for grains and

legumes. Cost of stocking a bag of 100 kg maize is GH₵1-2 per month in the Ejura and Kintampo

areas where maize production is high.

15

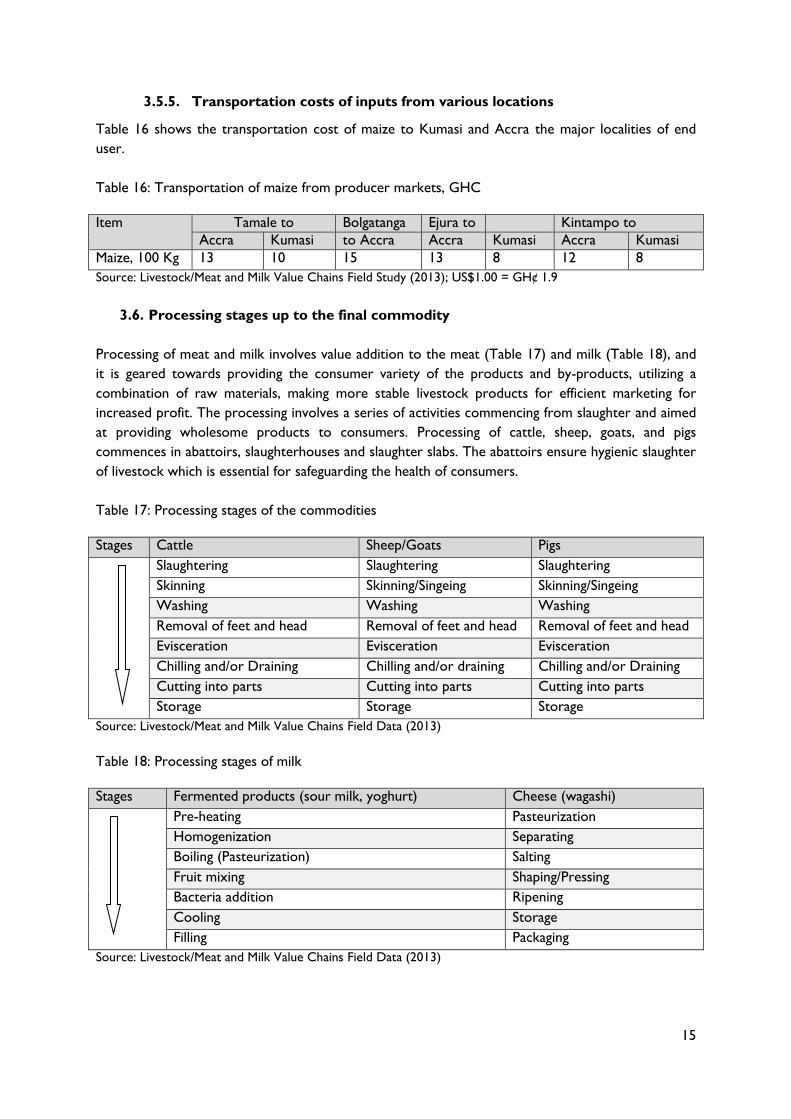

3.5.5. Transportation costs of inputs from various locations

Table 16 shows the transportation cost of maize to Kumasi and Accra the major localities of end

user.

Table 16: Transportation of maize from producer markets, GHC

Item Tamale to Bolgatanga Ejura to Kintampo to

Accra Kumasi to Accra Accra Kumasi Accra Kumasi

Maize, 100 Kg 13 10 15 13 8 12 8

Source: Livestock/Meat and Milk Value Chains Field Study (2013); US$1.00 = GH¢ 1.9

3.6. Processing stages up to the final commodity

Processing of meat and milk involves value addition to the meat (Table 17) and milk (Table 18), and

it is geared towards providing the consumer variety of the products and by-products, utilizing a

combination of raw materials, making more stable livestock products for efficient marketing for

increased profit. The processing involves a series of activities commencing from slaughter and aimed

at providing wholesome products to consumers. Processing of cattle, sheep, goats, and pigs

commences in abattoirs, slaughterhouses and slaughter slabs. The abattoirs ensure hygienic slaughter

of livestock which is essential for safeguarding the health of consumers.

Table 17: Processing stages of the commodities

Stages Cattle Sheep/Goats Pigs

Slaughtering Slaughtering Slaughtering

Skinning Skinning/Singeing Skinning/Singeing

Washing Washing Washing

Removal of feet and head Removal of feet and head Removal of feet and head

Evisceration Evisceration Evisceration

Chilling and/or Draining Chilling and/or draining Chilling and/or Draining

Cutting into parts Cutting into parts Cutting into parts

Storage Storage Storage

Source: Livestock/Meat and Milk Value Chains Field Data (2013)

Table 18: Processing stages of milk

Stages Fermented products (sour milk, yoghurt) Cheese (wagashi)

Pre-heating Pasteurization

Homogenization Separating

Boiling (Pasteurization) Salting

Fruit mixing Shaping/Pressing

Bacteria addition Ripening

Cooling Storage

Filling Packaging

Source: Livestock/Meat and Milk Value Chains Field Data (2013)

16

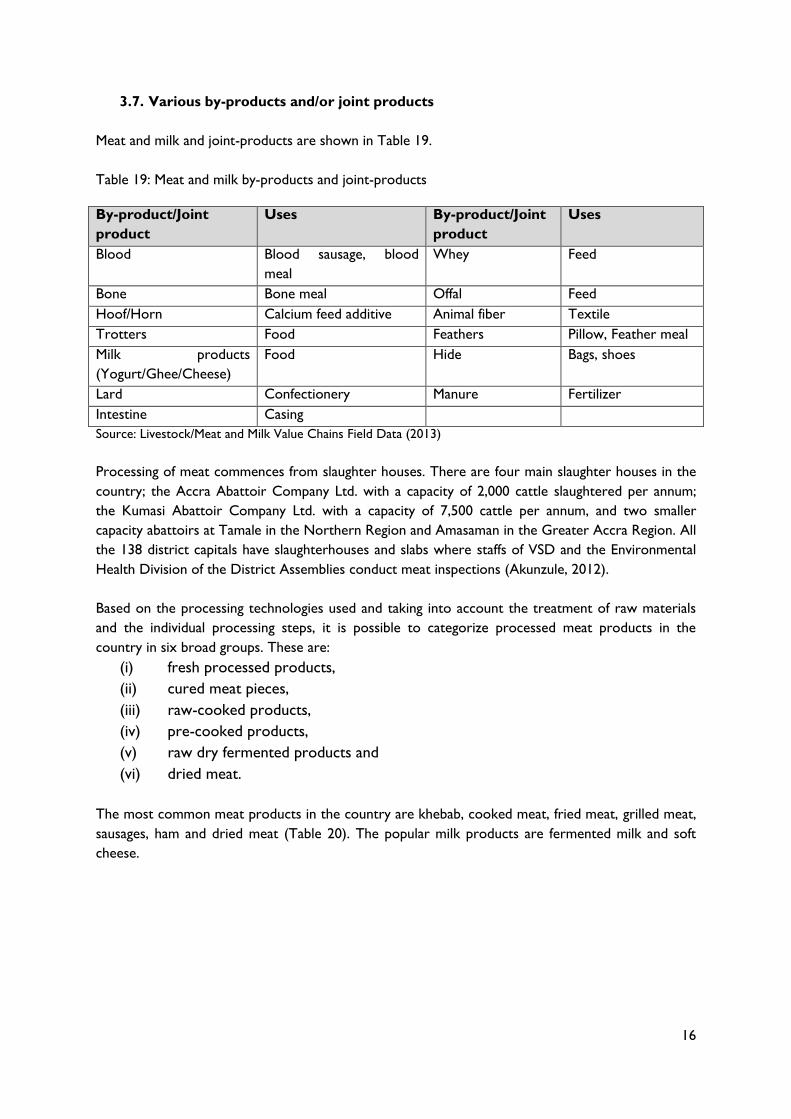

3.7. Various by-products and/or joint products

Meat and milk and joint-products are shown in Table 19.

Table 19: Meat and milk by-products and joint-products

By-product/Joint

product

Uses By-product/Joint

product

Uses

Blood Blood sausage, blood

meal

Whey Feed

Bone Bone meal Offal Feed

Hoof/Horn Calcium feed additive Animal fiber Textile

Trotters Food Feathers Pillow, Feather meal

Milk products

(Yogurt/Ghee/Cheese)

Food Hide Bags, shoes

Lard Confectionery Manure Fertilizer

Intestine Casing

Source: Livestock/Meat and Milk Value Chains Field Data (2013)

Processing of meat commences from slaughter houses. There are four main slaughter houses in the

country; the Accra Abattoir Company Ltd. with a capacity of 2,000 cattle slaughtered per annum;

the Kumasi Abattoir Company Ltd. with a capacity of 7,500 cattle per annum, and two smaller

capacity abattoirs at Tamale in the Northern Region and Amasaman in the Greater Accra Region. All

the 138 district capitals have slaughterhouses and slabs where staffs of VSD and the Environmental

Health Division of the District Assemblies conduct meat inspections (Akunzule, 2012).

Based on the processing technologies used and taking into account the treatment of raw materials

and the individual processing steps, it is possible to categorize processed meat products in the

country in six broad groups. These are:

(i) fresh processed products,

(ii) cured meat pieces,

(iii) raw-cooked products,

(iv) pre-cooked products,

(v) raw dry fermented products and

(vi) dried meat.

The most common meat products in the country are khebab, cooked meat, fried meat, grilled meat,

sausages, ham and dried meat (Table 20). The popular milk products are fermented milk and soft

cheese.

17

Table 20: Processing level of meat and milk

Cattle Sheep Goat Pig Milk

Beef Mutton Chevron Pork Raw milk

Khebab Khebab Khebab Khebab Pasteurized milk

Sausage Sausage Sausage Sausage Fermented milk

Grilled Grilled Grilled Grilled Cheese

Fried Fried Fried Fried Butter

Cooked Cooked Cooked Cooked Ghee

Source: Livestock/Meat and Milk Value Chains Field Data (2013)

3.8. Geographical location of the different value chain components

Most of the meat from ruminant sources is obtained from the northern part of Ghana while poultry

and pork are mostly obtained from commercial farms in the middle and southern Ghana. Milk comes

mainly from the northern and coastal areas. Table 21 shows the geographical actors in the meat and

milk value chain.

Table 21: Geographical location of components in the meat and milk value chain

Components Geographical location

Meat Milk

Input suppliers

Feed millers

Drug shops

Accra, Kumasi

Regional and district capitals

Accra, Kumasi

Regional and district capitals

Primary producers

Maize

Soybeans

Livestock

Countrywide

Derived Savannah zone

Countrywide

Countrywide

Derived Savannah zone

Countrywide/MoFA livestock stations

Marketing

Middlemen

Slaughterhouses

Processors

Wholesalers

Retailers

Countrywide

Regional and district centres

Regional centres

Regional and district centres

Countrywide

Countrywide

On-farm/Regional centres

Regional and district centres

Countrywide

Consumers Countrywide Countrywide

Source: Adapted from Akunzule (2012)

3.9. Amount of land and other natural resources allocated to the meat and milk

value chains

Rangeland comprising savannah woodlands and unimproved pastures which cover an area of 89 000

square kilometers, i.e. 37 percent of total land area of Ghaba, is available for grazing of livestock and

wildlife. In addition, some parts of the 45,000 square kilometers of land under bush fallow and other

uses are also available for grazing (SRID, 2011). The decline in the size and condition of the

rangelands in the last 30 years (Alhassan et al., 1999; Oppong-Anane et al., 2008) is manifested in the

loss of plant and wildlife species, the seasonality and drying out of water bodies resulting from a

18

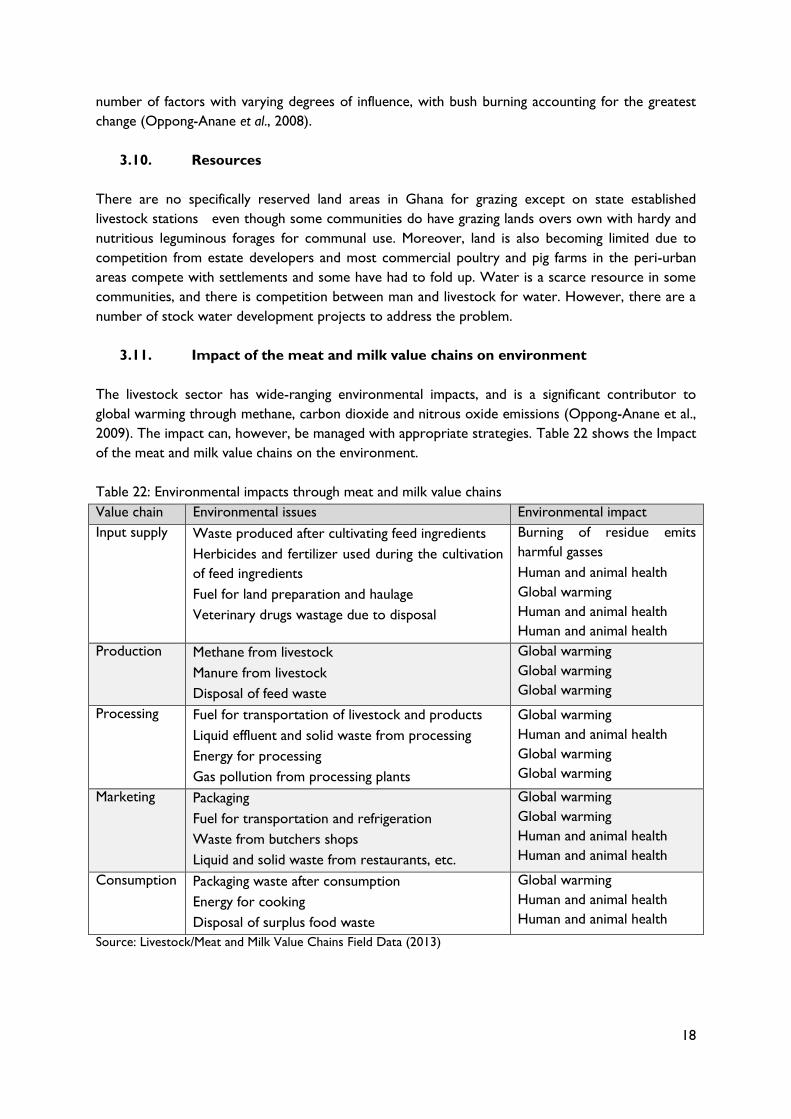

number of factors with varying degrees of influence, with bush burning accounting for the greatest

change (Oppong-Anane et al., 2008).

3.10. Resources

There are no specifically reserved land areas in Ghana for grazing except on state established

livestock stations even though some communities do have grazing lands overs own with hardy and

nutritious leguminous forages for communal use. Moreover, land is also becoming limited due to

competition from estate developers and most commercial poultry and pig farms in the peri-urban

areas compete with settlements and some have had to fold up. Water is a scarce resource in some

communities, and there is competition between man and livestock for water. However, there are a

number of stock water development projects to address the problem.

3.11. Impact of the meat and milk value chains on environment

The livestock sector has wide-ranging environmental impacts, and is a significant contributor to

global warming through methane, carbon dioxide and nitrous oxide emissions (Oppong-Anane et al.,

2009). The impact can, however, be managed with appropriate strategies. Table 22 shows the Impact

of the meat and milk value chains on the environment.

Table 22: Environmental impacts through meat and milk value chains

Value chain Environmental issues Environmental impact

Input supply Waste produced after cultivating feed ingredients

Herbicides and fertilizer used during the cultivation

of feed ingredients

Fuel for land preparation and haulage

Veterinary drugs wastage due to disposal

Burning of residue emits

harmful gasses

Human and animal health

Global warming

Human and animal health

Human and animal health

Production Methane from livestock

Manure from livestock

Disposal of feed waste

Global warming

Global warming

Global warming

Processing Fuel for transportation of livestock and products

Liquid effluent and solid waste from processing

Energy for processing

Gas pollution from processing plants

Global warming

Human and animal health

Global warming

Global warming

Marketing Packaging

Fuel for transportation and refrigeration

Waste from butchers shops

Liquid and solid waste from restaurants, etc.

Global warming

Global warming

Human and animal health

Human and animal health

Consumption Packaging waste after consumption

Energy for cooking

Disposal of surplus food waste

Global warming

Human and animal health

Human and animal health

Source: Livestock/Meat and Milk Value Chains Field Data (2013)

19

3.12. Production and value addition potential

High production and value addition potential exist for all the livestock commodities in particular

poultry and pigs and milk as a product. The value addition potential of pigs is higher than that of the

ruminants as pork may be processed into more popular products. A major value addition potential

of ruminants that has not been fully exploited in Ghana is the skin for leather products.

3.13. Number of value chain actors by component

There is no available data on the number of value chain actors in the country. The meat and milk

value chain actors comprise:

Inputs and services providers

Input dealers for the provision of inputs

Transporters of various inputs

Feed millers for the provision of feed.

Livestock breeders for the supply of breeding animals

Drug suppliers for provision of drugs and vaccines.

Farmers for primary production

Farmers producing maize and soybean for livestock feed

Livestock producers: pigs, cattle, sheep and goats

Market actors

Middlemen for intermediary trade or marketing

Butchers for slaughtering and cutting of meat

Processors for value addition to meat and milk

Wholesalers for storage and sale of meat and milk and by-products

Retailers for sale of meat and milk and by-products

Consumers

Industrial (hotels, restaurants, etc.)

Home consumers

3.15. Current and potential (domestic) demand of meat and milk

With a current domestic meat consumption estimated at 13.9 kg/capita/annum, it is estimated that

for a population of about 25.20 million the country needs a total of 350 280 tonnes of meat to meet

demand.

Also with a current milk consumption estimated at 8.48 kg/capita/annum a total of 221 760 tonnes of

milk would be required to meet national demands. The total current demand for meat and milk,

572 040 tonnes, is significantly higher than the potential domestic production in view of the fact that

the total production of meat, eggs and milk was 234 041 tonnes in 2011. There is therefore a high

potential demand for the products considering the increasing demand that will come from increasing

incomes, growing population and increasing urbanization.

20

3.16. Current and potential (foreign) demand of meat and milk

There is no current export demand for meat, milk and dairy products from Ghana, neither is there

any potential for exporting livestock products in the foreseeable future. Nevertheless, a total of

79.26 tonnes of livestock meat and offal amounting to US$1 141.00 was exported in 2011 (MoFA,

2012).

3.17. Specific features of products, including product differentiation

There are different kinds of clients who consume milk and meat products in Ghana.

It is mostly foreign clients and a few persons in urban areas who buy choice cuts of meat such as

pork chops, spare ribs and fillet that are not provided by butchers at meat shops, but are obtainable

mainly from supermarkets. Though milk is sold fresh, there is a relatively higher degree of product

differentiation. Fresh milk is processed into wagashi cheese, fermented cultured milk and ghee

targeted at clients of Hausa and northern Ghana extraction. The high valued milk products are

available only in supermarkets.

3.18. The products capacity to fulfill international requirements (sanitary and

other

Sanitary condition for slaughtering and processing of meat in Ghana has improved significantly.

However, the capacity to export in the first place and to fulfill international requirements is low. The

law concerning the inspection of meat (Local Government Act, 1961; Act 54) has not been reviewed

nor updated thus making it inapplicable in the present time. For instance meat inspection function is

not a monopoly of the VSD as the mandate for meat inspection by the Public Health Department of

the Metropolitan, Municipal and District Assemblies has not been repealed though the later may not

have the capacity to do so.

3.19. Urban rural relationships

Generally most producers of meat and milk are in the rural areas whereas the majority of

consumers are in the urban areas. The demand and consumption of livestock meat and dairy

products are highly influenced by household income. Per capital consumption of the products are

higher in urban than rural areas because of the high income level differentials. However, a number of

factors affect fresh milk consumption in the urban areas where most people are not used to

consuming fresh milk. These include lactose intolerance and unwholesome milking procedures used

by some herdsmen (Akunzule, 2012) and lack of good cold/refrigeration facilities for milk.

Hides and skin from cattle, sheep and goats are used for the leather industry and in particular for the

manufacturing of bags and footwear in the northern regions of the country. Cattle (bullocks) are