revenue procedure 2013-39 - appliedselfdirection revenue... · deposits per the deposit schedule...

TRANSCRIPT

Revenue Procedure 2013-39

Effective 12/12/2013 By:

Mollie Murphy, NRCPDS

Overview

Describes and updates the procedure for requesting the IRS to authorize an agent under Section 3504 of the Internal Revenue Code and Section 31.3504-1 of the Employment Tax Regulations for purposes of FICA tax, RRTA tax, FUTA, collection of income tax, and general provisions related to employment taxes.

2

Key Changes

All HCSR employers, whether served by government agent or not, must have an EIN

Sub-agent must use own name and EIN when representing an agent

Sub-agent allowed for government and non-government agents

Process to mark “some employees” on Form 2678 is formalized

IRS may independently revoke an agent authorization

3

Key Changes

Notices of appointment of agent for HCSR employers are only sent to the agent, rather than to the agent and the employer

HCSR employers served by government agents must have an EIN EINs must be obtained now for any employers who did not

have them previously

4

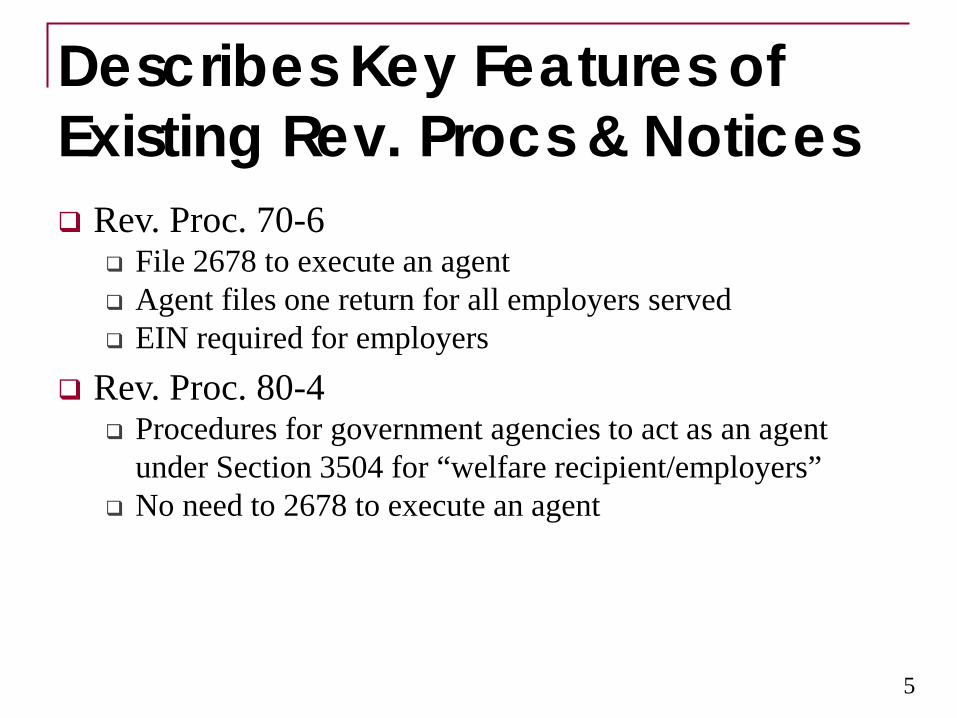

Describes Key Features of Existing Rev. Procs & Notices Rev. Proc. 70-6

File 2678 to execute an agent Agent files one return for all employers served EIN required for employers

Rev. Proc. 80-4 Procedures for government agencies to act as an agent

under Section 3504 for “welfare recipient/employers” No need to 2678 to execute an agent

5

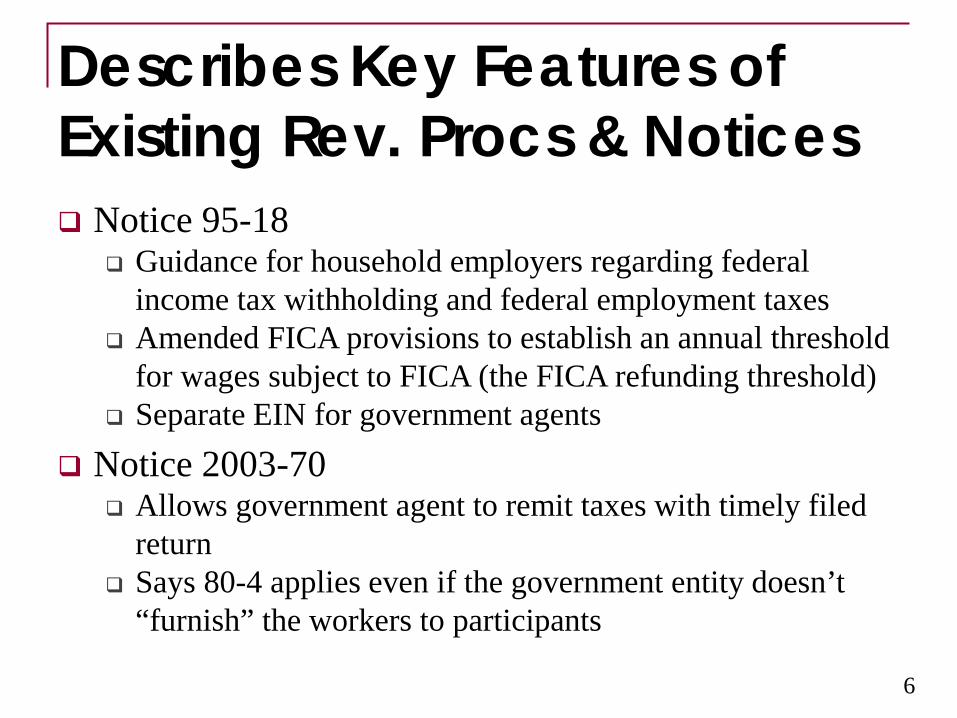

Describes Key Features of Existing Rev. Procs & Notices Notice 95-18

Guidance for household employers regarding federal income tax withholding and federal employment taxes

Amended FICA provisions to establish an annual threshold for wages subject to FICA (the FICA refunding threshold)

Separate EIN for government agents Notice 2003-70

Allows government agent to remit taxes with timely filed return

Says 80-4 applies even if the government entity doesn’t “furnish” the workers to participants

6

Describes Key Features of Existing Rev. Procs & Notices Notice 2003-70 Continued

Allows “service recipients” to designate the government entity without having an EIN

Government agent can remit taxes with timely filed return Reporting agent to government agent is allowed Should use government agent’s special EIN Should remit taxes with timely filed return

Sub-agent (assigned per Rev. Proc. 70-6) is also allowed Should use government agent’s special EIN Should remit taxes per the deposit schedule for the

entire aggregate liability

7

Summary of Changes

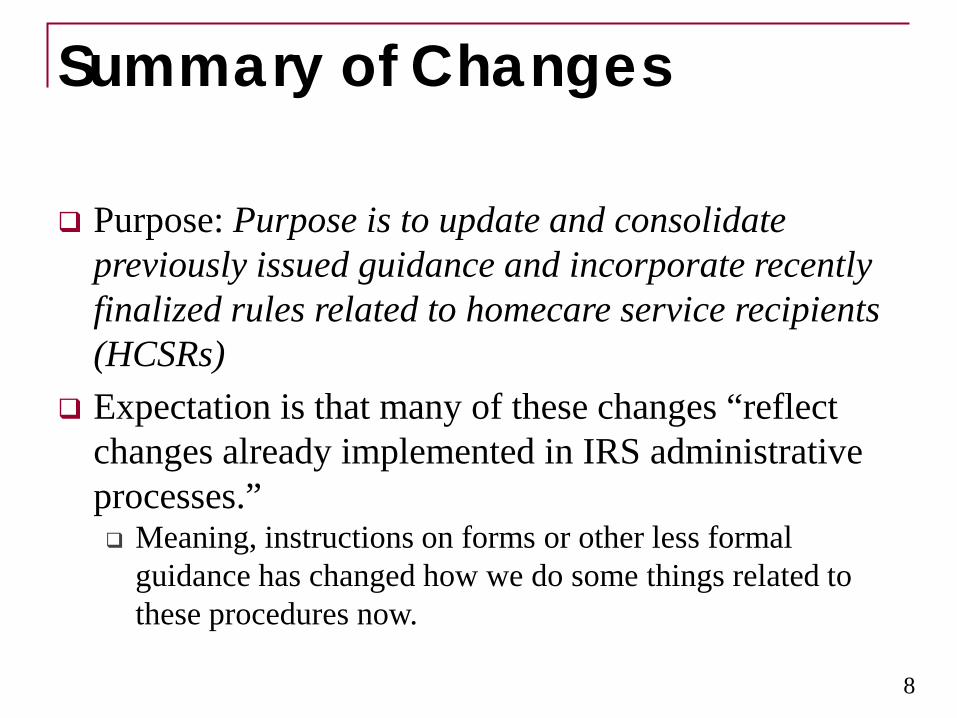

Purpose: Purpose is to update and consolidate previously issued guidance and incorporate recently finalized rules related to homecare service recipients (HCSRs)

Expectation is that many of these changes “reflect changes already implemented in IRS administrative processes.” Meaning, instructions on forms or other less formal

guidance has changed how we do some things related to these procedures now.

8

“Some Employees” on 2678

Hasn’t changed: submit a Form 2678, Employer Appointment of Agent, to assign an agent

Maybe hasn’t changed, but is at least formalized: If the employer may pay wages to his/her employees either

through another business or because the employer will supplement the program wages, “the employer must indicate on Form 2678 that the appointment of the agent is only for some of its employees.”

9

Authorization to Act as Agent

Hasn’t changed: The Authorization to Act as Agent is effective on the date

indicated in the letter of approval mailed by the IRS This has not changed, but is emphasized in Rev. Proc.

2013-39 Programs should have contracts with their Fiscal/Employer

Agents (F/EA) that specify that the program holds the F/EA responsible for appropriately filing returns and depositing taxes even prior to the IRS granting the authorization to act as agent

10

Employer Appoints Agent for All Employees: Final Return This hasn’t changed, but is clarified here:

If the employer wishes to authorize an agent and the employer has previously used the EIN to pay wages: The employer should file a final return for any forms the

agent is now authorized to file. If employer is authorizing agent to file 941 and 940 on the

employer’s behalf, employer must “enter its name and EIN in the spaces provided for the employer and indicate that it is a final return in the manner provided in the form instructions.”

If the employer wishes to authorize an agent and has not ever paid wages before: the employer will need an EIN filing a final return is not appropriate

11

Employer Appoints Agent for Some Employees If the employer plans to pay any wages, bonuses, other

employee compensation to his HCSR employees, OR If the employer plans to use this EIN for other wage-

paying purposes, THEN The employer does not file a final return, but must

continue filing a return if the employer with regard to the wages paid by the employer to his employees is separate from the agent.

This may work for Federal taxes, but consider state taxes.

12

General Procedures for Filing Returns by Agent with 2678 Agent files one return for each tax-return period

Report wages and employment taxes paid to agent employees. Called in Rev. Proc. “aggregate return”

Agent’s name and EIN are entered on the returns and executed per form instructions

Agent must complete an allocation schedule and attach it to each aggregate return as described in form instructions Currently, this is Schedule R for Forms 941 and 940

13

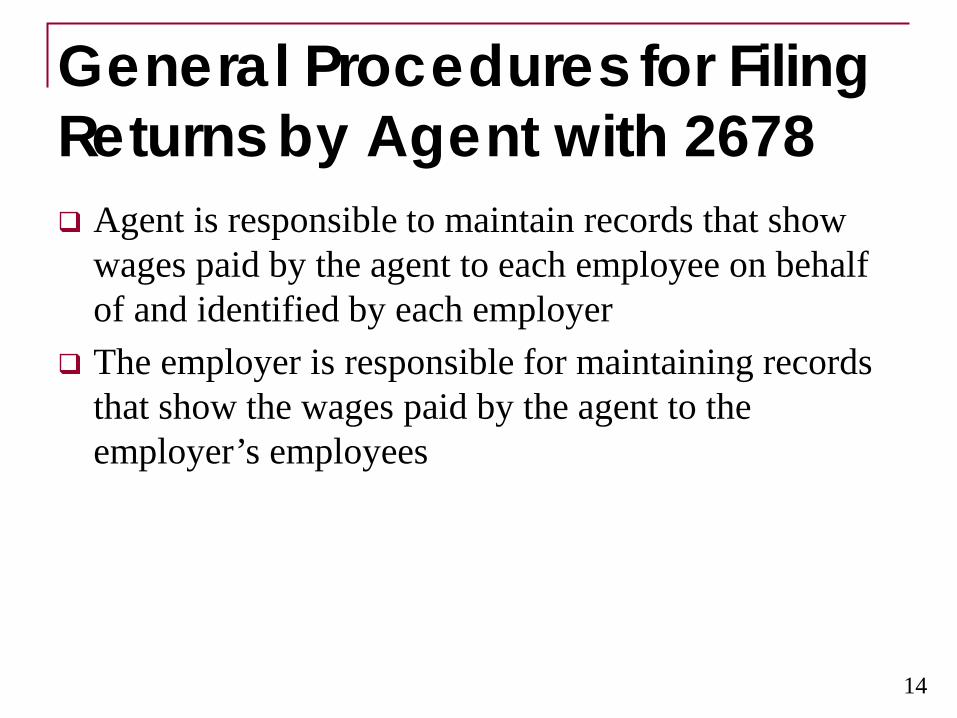

General Procedures for Filing Returns by Agent with 2678 Agent is responsible to maintain records that show

wages paid by the agent to each employee on behalf of and identified by each employer

The employer is responsible for maintaining records that show the wages paid by the agent to the employer’s employees

14

General Procedures for Filing Returns by Agent with 2678 Wages paid to an employee are considered for each

employer separately for purposes of dollar threshold or wage base applicable in determining employment tax liability That is, for purposes of FICA tax, the wages paid from one

employer to a single employee are counted to see if wages paid to the employee are taxable. The wages paid by another employer represented by the agent to the same employee are not counted

Same example for the FUTA taxable wage base

15

Agent Filing Form W-2

Generally agent furnishes one Form W-2, Wage and Tax Statement, for each employee

Agent’s EIN is entered in spaces provided for the EIN Name of agent, followed by “Agent for (name of

employer” is entered in the space provided for the employer

Form W-2 is issued and filed for each employee unless the compensation is excepted from both federal income tax withholding and FICA tax

3 conditions are given for when the agent would file a separate W-2 for each employer/employee relationship

16

3 Conditions for Separate W-2 for each EE/ER Relationship Two of the conditions would almost always be met by

a Fiscal/Employer Agent This condition: “the total of the individual’s social

security wages from these employers is greater than the social security wage base” would not always be met when paying HCSR employees

Conditions (b) and (c) are connected with an “and” Does the IRS intend for all three conditions to be met?

This is problematic for the name on the W-2 and for the state section of Form W-2

17

General Procedures for Deposits by Agent with 2678 For Government Agents and their reporting agents

only, deposits can be made with a timely filed return Taxes can be paid when return is filed

For Government Sub-Agents and Non-Government Agents (Vendor Fiscal/Employer Agents): The deposit rules apply to the agent based on the total

employer taxes accumulated by the agent on behalf of all employers for whom agent is authorized to act In other words, agent is likely to deposit more

frequently than if abided by deposit rules for any single employer represented by the agent

18

Wage Corrections by Agent

Wages erroneously reported by the agent must be corrected by the agent on behalf of the employer using the form that corresponds to the return being corrected e.g. a Form 941 filed by an agent is corrected using Form

941-X Agent’s name and EIN are entered in the spaces provided for

the employer as it appeared on the form being corrected Generally, an agent’s obligation to make the correction is not

affected by the subsequent revocation of the authorization (e.g. just because you’re not the agent now doesn’t mean you don’t have to correct the return from when you were the agent. You do.)

Agent cannot make corrections if the IRS decided to revoke the authorization of the agent 19

Agents using Reporting Agents Agent can appoint a reporting agent with an IRS

approved Form 8655 More info in Rev. Proc. 2012-31, 2012-35

Essentially, the reporting agent makes deposits and files returns as if the reporting agent were the agent Uses Agent’s EIN and name on returns Files an aggregate return on agent’s behalf Deposits per the agent’s deposit schedule

Agent is responsible for maintaining records that show the wages paid by the agent on behalf of, and identified by, each employer the agent serves

20

Agents using Sub-Agents An Agent (government & non-government) with

approved Form 2678 can appoint a sub-agent New because this used to be only allowed for government agents First agent gets Forms 2678 from employers then executes one

Form 2678 with sub-agent Sub-agent makes deposits and files returns using the sub-

agent’s EIN and name Uses sub-agent’s own EIN and name on returns Files an aggregate return on agent’s behalf using sub-agent’s

own name Deposits per the deposit schedule caused by aggregate liability

Sub-Agent & agent are responsible for maintaining records that show the wages paid by the agent on behalf of, and identified by, each employer the agent serves

Provisions of law, including penalties, with respect to the employer apply to the employer, first agent and sub-agent

21

Revoking an Authorization of Agent The employer or agent with an approved Form 2678

may request to revoke an existing Form 2678 Just one party has to sign the 2678 – both are not required

IRS confirms the revocation by letter to the agent and employer Revocation is effective on the date indicated in the letter

from the IRS The IRS may independently revoke an existing

authorization if facts and circumstances indicate it is warranted Revocation is by notice to agent and employer

22

Liability After Revocation

Form 2678 is filed to revoke an authorization if there is no longer an agency relationship, e.g.: Employer or agent goes out of business Employer is deceased Employer appoints another agent on Form 2678 to act as agent

for the same acts the agent is authorized to perform If agent authorization revoked because a new agent is

appointed: Old agent is liable to report, deposit and pay taxes on behalf of

the employer for wages it paid during periods it was authorized Remains liable even after the authorization is revoked Supports what Judy Davis said at the 2013 FMS Conference

– new agent does not take on employer’s old liabilities

23

Special Rules for Agents of HCSRs Only government agencies can be “state agents”

“Third parties, whether non-profit or for-profit that are engaged by a government agency to administer all or some aspects of a home care services program are not state agents for purposes of this revenue procedure.” (page 14)

31.3504-1(b) provides that an agent can be authorized for purposes of the HCSR employer’s FUTA, provided the same agent has been authorized as an agent for income tax withholding and FICA

Rules to request an agent for an HCSR are the same, but the letter mailed by the IRS approving the request is only sent to the agent

24

Special Rules for Government Agents: Form 2678 A government agent (called in the Rev. Proc. “state

agent”) may request authorization to act as an agent without using a Form 2678 This does NOT apply to non-government agents (vendor agents) Government Agent may solicit appointment by each HCSR on

forms program participants complete to enroll in the program Government Agent submits a letter to the IRS address where it

would have sent the 2678 Letter references the forms used in lieu of the Form 2678 and

includes a list of employers the agent is representing with: Each HCSR’s name & EIN (or properly completed Form SS-

4, if no EIN yet)

25

HCSRs Served by Government Agents MUST have an EIN Because allocation schedules (Schedules R for Form

941 and 940) must be filed by Government Agents, even those employers served by Government Agents MUST have an EIN

HCSRs whose agents were authorized before the effective date of this Revenue Procedure who do not have an EIN must apply for one within “a reasonable period of time after the effective date of this revenue procedure” Effective date is 12/12/2013

26

Government Agents Need a “Special EIN” Use Form SS-4 to request a “special EIN” for the

government agent to report and pay taxes on behalf of the HCSRs for whom agent acts May not use the special EIN to report or pay employment

taxes for wages paid for services other than home care services or for an employer who is not an HCSR.

Government agents can deposit taxes with a timely filed return

Allocation schedules (Schedule R) is required with any aggregate returns submitted by the government agent

27

Special Rules for Agents of HCSRs Agent may act for FUTA tax purposes (filing in the aggregate

for FUTA) while an HCSR is enrolled in a public program and for the remainder of the calendar year in which he or she ceases to be enrolled If HCSR ceases to be enrolled in a government program during the

year, agent may report and pay FUTA on behalf of the HCSR for all wages paid that year or for only a portion of the calendar year

Agent files a Form 2678 to revoke the appointment of agent before the end of the calendar year in which the program participant ceases to be a HCSR Agent can continue to represent HCSR until the end of the calendar

year if agent and employer so choose, even if employer is not in a public program

If Agent does not represent the HCSR as soon as the HCSR ceases to be in the public program, the agent must revoke the Form 2678 then

Agent can still act as agent for FICA and FIT withholding 28

Examples: Final Return

Example 1. Final return. Employer B and Agent W complete and file Form 2678 to request the IRS authorize Agent W to file Form 941 with respect to all of Employer B’s employees. The IRS approves the authorization effective April 1, 2014. Employer B files a Form 941 for the first quarter of 2014, indicating that it is a final return by checking the appropriate box and entering that it stopped paying wages as of March 31, 2014. For periods beginning on and after April 1, 2014, Agent W pays wages to all of Employer B’s employees, makes related employment tax deposits and payments, and reports the wages and taxes on an aggregate Form 941. Agent W attaches Schedule R (Form 941) listing Employer B as a client. Employer was active, now using an agent for all wages. Employer must file a final return before agent’s authorization takes over.

29

Examples: No Final Return

Example 2. No final return. Same facts as Example 1, except that Employer B is a new business that has not paid wages to any employees prior to the effective date of the authorization. Therefore, Employer B does not file a final Form 941. Employer is new employer without any prior employment history. Appoints agent. Nothing else to do.

30

Examples: Authorization for Some Employees Example 3. Authorization for Some Employees. Employer C and Agent V complete and file Form 2678 to request the IRS authorize Agent V to file Form 941 with respect to some of Employer C’s employees. The IRS approves the authorization effective April 1, 2014. For periods beginning on and after April 1, 2014, Agent V pays wages to some of Employer C’s employees, makes related employment tax deposits and payments, and reports the wages and taxes on an aggregate Form 941. Agent V attaches Schedule R (Form 941) listing Employer C as a client. Employer C continues to pay wages for some employees, make related employment tax deposits, and report the wages and taxes on its Form 941. Employer has an agent for some employees, but employer also has some of his/her own employees that he/she pays without use of the agent. “Some employees” is marked on Form 2678. Agent operates as agent always would and employer operates using his/her EIN as he always would. This may work for IRS purposes, but state unemployment would require coordination or could be a mess. Only one return usually permitted per employer for State Unemployment purposes.

31

Examples: HCSR & Other Employer Example 4. HCSR and other employer. Agent Y is authorized to file Form 941 for Employer S and for Employer T, who is a home care service recipient (HCSR) as defined in §31.3504-1(b)(3). Agent Y is also authorized to file Form 940 for Employer T. Agent Y pays wages to all of Employer S’s and Employer T’s employees, makes related employment tax deposits and payments, and reports the wages and taxes on an aggregate Form 941. Agent Y attaches Schedule R (Form 941) listing Employer S and Employer T as clients. Agent Y also reports wages and taxes with respect to home care services provided to Employer T on an aggregate Form 940. Agent Y attaches Schedule R (Form 940) listing Employer T as a client. Employer S files Form 940 with respect to wages paid to its employees. Agent serves one employer who is an HCSR and one employer who is not. Agent lists both employers on Schedule R for 941. Agent lists only the HCSR on Schedule R for 940. An individual Form 940 is filed for the non-HCSR using the non-HCSR’s name and EIN on the Form 940.

32

Examples: State Agent

Example 5. State agent. State K funds a program to provide home care services to eligible individuals. Department H administers the home care services program, including disbursing the funds to pay for the services. Each of the individuals enrolled in the program is a HCSR, as defined in § 31.3504-1(b)(3). As part of the enrollment process, each HCSR completes a form to appoint Department H as agent under section 3504 of the Code to file Form 940 and Form 941 for the HCSRs. Department H sends a letter to the IRS stating it is a government agency that wishes to become a state agent. Department H attaches to the letter a sample copy of the form it uses to be appointed by a HCSR, a list of the names and EINs of each HCSR that has appointed Department H as agent, and a Form SS-4 with respect to each HCSR named in its letter that does not have an EIN. Department H also attaches a Form SS-4 to apply for a special EIN for it to use as state agent of the HCSRs enrolled in its home care services program that have appointed Department H as agent. Department H receives a letter from the IRS authorizing it as agent for each HCSR. Department H pays wages to the HCSR’s employees and reports the wages and taxes on an aggregate Form 941, with its name and special EIN entered in the space provided for the employer. Department H attaches Schedule R (Form 941), listing each HCSR as a client. Because Department H is a state agent, it remits payment with its timely filed aggregate Form 941. Department H also reports wages and taxes with respect to the HCSRs on an aggregate Form 940 with its name and special EIN entered in the space provided for the employer. Department H attaches Schedule R (Form 940), listing each HCSR as a client. Because Department H is a state agent, it remits payment with its timely filed aggregate Form 940. Example of a Government Agent not using a Form 2678 for employers to appoint it as agent. Government Agent files and pays all federal taxes in the aggregate and uses Schedules R for Form 941 and 940 when it does.

33

Examples: State Agent Designates Reporting Agent Example 6. State agent designates a reporting agent. Same facts as Example 5. The following year (Year 2) Department H designates reporting agent R with respect to HCSRs for whom Department H is authorized as state agent, by following the procedures described in Rev. Proc. 2012-32. Reporting agent R enters Department H’s name and special EIN in the space provided for the employer on the aggregate employment tax returns and on the attached allocation schedules. Reporting agent R lists each HCSR as a client on each allocation schedule. Reporting agent R also remits payment for employment taxes with the timely filed employment tax returns. Example of a government agent using a reporting agent. Reporting agent puts government agent’s name and EIN on all aggregate returns filed by reporting agent.

34

Examples: State Agent Designates Sub-Agent Example 7. State agent designates a sub-agent. Same facts as Example 5, except in Year 2, Department H appoints S as its sub-agent on Form 2678 with respect to the HCSRs for whom Department H is authorized as state agent. The IRS approves the authorization. Sub-agent S pays wages to the HCSRs’ employees, makes related employment tax deposits and payments, and reports the wages and taxes on an aggregate Form 941, with its name and EIN entered in the space provided for the employer. Sub-agent S attaches Schedule R (Form 941), listing each HCSR as a client. Sub-agent S also reports wages and taxes with respect to the HCSRs on an aggregate Form 940 with its name and EIN entered in the space provided for the employer. Sub-agent S attaches Schedule R (Form 940), listing each HCSR as a client. Example of a government agent using a sub-agent. Sub-agent puts its own name and EIN on all aggregate returns filed by sub-agent for government agent.

35

Examples: HCSR Disenrolls & Private Pays for Calendar Year Example 8. Form 940 revocation – end of year. Individual A, a HCSR as defined in §31.3504-1(b)(3), has only home care service employees. Individual A and Agent X complete and file Form 2678 to request the IRS to authorize Agent X to file Form 941 and Form 940 with respect to the employees providing home care services to Individual A. The IRS approves the authorization effective January 1, 2014. On July 31, 2014, Individual A ceases to be enrolled in the government program but continues to receive home care services which Agent X pays for with private funds provided by Individual A. Under §31.3504-1(b)(3), Individual A continues to be a HCSR for the remainder of the calendar year after ceasing to be enrolled in the government program. Agent X reports the wages and taxes with respect to Individual A for the entire year on an aggregate Form 940. Agent X attaches Schedule R (Form 940) listing Individual A as a client. The IRS approves Agent X’s request, filed on Form 2678, to revoke its authorization to file Form 940 for Individual A, effective December 31, 2014. Agent X remains authorized to file Form 941 for Individual A. Example of Agent serving HCSR who, mid-year, disenrolls from the government program. Agent continues to represent the HCSR with HCSR private pay funds until the end of the calendar year. For new calendar year, Agent just serves as such for FICA and FIT using aggregate Form 941. Form 940 is filed and paid individually for the private-pay employer.

36

Examples: HCSR Disenrolls & Private Pays for Calendar Year Example 9. Form 940 revocation – before end of year. Same facts as Example 8, except that the IRS approves Agent X’s request, filed on Form 2678, to revoke its authorization to file Form 940 for Individual A, effective August, 1, 2014. Agent X reports the wages and taxes accrued with respect to Individual A on or before July 31, 2014, on an aggregate Form 940. Agent X attaches Schedule R (Form 940), listing Individual A as a client. Individual A is responsible for reporting wages and taxes accrued with respect to wages paid for home care services on or after August 1, 2014. Example of Agent serving HCSR who, mid-year, disenrolls from the government program. Agent discontinues to represent the HCSR with HCSR private pay funds until the end of the calendar year. Agent includes HCSR on aggregate Form 940 only for wages paid by Agent. Employer files individual Form 940 for all private pay wages from the same year.

37

Items for Follow Up

Person? “authorize a person to act as agent under section 3504” Why person and not organization?

4.03 says that the agent must complete an allocation schedule and list “the name and EIN of each employer for whom the agent is authorized to act…” The Schedule R for 941 and 940 does not have a field for

the employer’s name Non-government agents told to include own

employees in aggregate returns

38

Items for Follow Up

The employer is responsible for maintaining records that show the wages paid by the agent to the employer’s employees

Must all three conditions be met for an agent to issue a separate W-2 for each employer/employee relationship? If so, poses issues for naming “Agent for (employer)” on Form

W-2 and for completing the state section of Form W-2

If the agent will have a sub-agent, the employers should complete the 2678 with only the first agent as such, right?

39

Items for Follow Up

Can non-government agents obtain a “special EIN” or use “special EINs” if they already have them?

Sub-Agents who had been filing as the first agent – should they file a final return as the first agent before switching to filing using the Sub-Agent’s own information?

40

QUESTIONS?