retirement options for machinists in british columbia 29/04/20111iamaw dl250 pension options

TRANSCRIPT

Retirement OptionsFor Machinists In British Columbia

29/04/2011 1IAMAW DL250 Pension Options

29/04/2011 2IAMAW DL250 Pension Options

Retirement IncomeWhere Will It Come From?

The retirement income system in Canadarests on three pillars:1) Universal government benefits for seniors2) The Canada Pension Plan3) Employment Pension Plans and

Individual Retirement Savings

29/04/2011 3IAMAW DL250 Pension Options

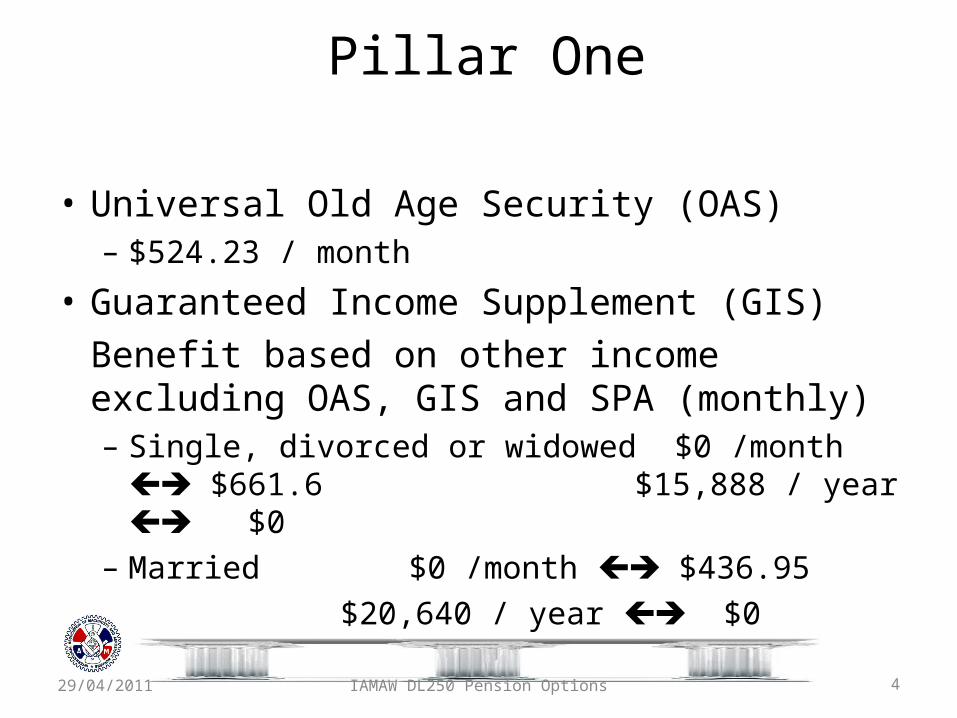

Pillar One

• Universal Old Age Security (OAS) – $524.23 / month

• Guaranteed Income Supplement (GIS)Benefit based on other income excluding OAS, GIS and SPA (monthly)– Single, divorced or widowed $0 /month $661.6

$15,888 / year $0– Married $0 /month $436.95

$20,640 / year $0

29/04/2011 4IAMAW DL250 Pension Options

Pillar One (con’t)

• Spouses Allowance (SPA)• SPA is a bridge for partners of retirees aged 60

to 64 while waiting to receive OASbenefit $0 / month $961.18income $29, 376 $0

29/04/2011 5IAMAW DL250 Pension Options

29/04/2011 6IAMAW DL250 Pension Options

Pillar Two

• Canada Pension Plan (CPP)• CPP based on previous yearly incomes• $960 max / $504 average per month

29/04/2011 7IAMAW DL250 Pension Options

Pillar Three Pension Plans

• Pension Plans can be employer, Union or multi-employer.

• A Defined Contribution (DC) pension has a set contribution by the employer to an employee account

• A Defined Benefit (DB) pension has a set benefit based on years of service

• A Hybrid pension has aspects of both DB and DC pensions

• Employer pensions are dependent on the health of the sponsoring employer. Many bankrupt companies, such as Nortel, have reneged on promised benefits.

29/04/2011 8IAMAW DL250 Pension Options

Pillar Three: Pension Plans (con’t) • A Union pension is dependent on sound investment and sustainable

benefit levels.• A multi-employee pension administers for many employers, allowing

small companies to offer pensions. The plan is independent of the employers and, like a Union plan, needs prudent management of funds and benefits.

• No benefits are cast in stone. A plan may increase benefits if returns on investment are good and reduce benefits if the assets of the plan are hit in a recession.

• All registered pension plans are supervised by the Commissioner of Pensions who makes sure pension can pay the retirees' pensions. If a plan assets slip below 100% of what is needed to pay out all obligations, the Commissioner of Pensions will order remedial action either by reducing benefits or increasing contributions.

• Likewise if the funds of a plan grow too great, the plan will be required to reduce contributions or increase benefits. A company plan will always do the former whereas a Union plan increases benefits.

29/04/2011 9IAMAW DL250 Pension Options

Pillar Three: RRSPs

• RRSP savings are the most common form of personal retirement savings.

• A maximum of $22,450 per year can be contributed in 2011.

• Money going in is not taxed but withdrawals are.

29/04/2011 10IAMAW DL250 Pension Options

Pillar Three: RRSPs (con’t)

• RRSPs have two major drawbacks. – First, the value of your savings is subject to the

economy, stock market and interest rates. – Second, the fees on RRSPs average 2 ½%. That is

2.5% which will be subtracted from any growth in your fund.

– A pension typically has a cost of 0.5% meaning 2% in extra returns per year over a RRSP.

29/04/2011 11IAMAW DL250 Pension Options

Pillar Three: RRSPs (con’t)• If two people saved each $500 a month for 25

years with an average return of 6.5%, their Pension account could accrue approximately $346, 500

• But the RRSP, with higher service fees, would come up to $257,000, nearly $90,000 less.

• If you think of the amount in terms of monthly retirement income, this amounts to $478 per month over a period of 24 years, based on a 4% interest rate for a total difference of $137,000!

29/04/2011 12IAMAW DL250 Pension Options

Pillar Three: TFSA

• Tax Free Savings Accounts (TFSA)– TFSA program allows a maximum investment of

$5,000 per year. – Unlike RRSPs, money going in is taxed; money

coming out is not.– This is an ideal savings plan for low income

earners whose income tax rate is low. – It is also a place to save if the RRSP contributions

are maxed out for the year.

29/04/2011 13IAMAW DL250 Pension Options

Pillat Three: RRIF

• All RRSPs must be cashed out or converted to Registered Retirement Income Funds (RRIF) by age 71.

• Otherwise taxes on entire balance become payable.• The return on a RRIF is dependent on interest rates or

investment depending on which flavour you choose. • It is subject to fees like RRSPs. You are required to withdraw a

minimum each month but may draw more up to a set limit. All withdrawals are subject to taxation.

• Retirees often outlive their RRIF money and are reduced to poverty.

29/04/2011 14IAMAW DL250 Pension Options

29/04/2011 15IAMAW DL250 Pension Options

Membership Options

• Option 1 • RRSP Plan - remain with current plan

29/04/2011 16IAMAW DL250 Pension Options

Membership Options (con’t)

• Option 2 – RRSP Plan - with a different group– Look for better service and /or better fee

structure– Some financial institutions are reluctant to set up

new group accounts

29/04/2011 17IAMAW DL250 Pension Options

Membership Options (con’t)

• Option 3– The IAM Labour Management Pension Fund

(Canada)– This is a true defined benefit plan where a set

contribution per hour earns a set monthly pension times the number of years of service

29/04/2011 18IAMAW DL250 Pension Options

Membership Options 3 (con’t)The IAM Labour Management Pension Fund (Canada)

• A defined benefit pension plan gives a set benefit for so many years of service.

• The IAM Multi-Employer Pension Fund (“the Fund”) is a hybrid plan because it gives a defined benefit based on years of service and the contribution rate.

• At retirement, the Fund pays a monthly pension as long as the member, or the spouse, is alive.

• The exact amount of pension a contribution rate will earn varies slightly due to demographic differences between shops but, as a general guideline, $2.00 per hour will pay $80 times the year of service a month.

• A $2 / hour contribution for 10 years will pay a pension of 10 X 80 = $800 a month at age 65.

29/04/2011 19IAMAW DL250 Pension Options

Membership Options 3 (con’t)The IAM Labour Management Pension Fund (Canada)

• The Plan was created in Canada by Machinists, for Machinists.

• The Plan is intended to give employees of small employers the same ability to have pensions as those who work for large corporations.

• The plan does allow small company's management to participate in the Fund as a sweetener for the employer as they also have no access to a true pension plan.

• This solidifies the relationship between the Union and the employer, making decertification attempts unlikely.

29/04/2011 20IAMAW DL250 Pension Options

Membership Option 4Lodge 692 Machinists Pension Plan

• Each member has a dollar account in his name which is used to calculate his / her pension at retirement.

• For members of the 692 Pension Plan, upon retirement a monthly pension is paid, avoiding the need for a fee-based Register Retirement Income Fund (RRIF).

• Your money will be paid as long as you or your spouse is alive. There is no danger you will run out of savings during your retirement; a calamity which does happen to those who must convert their RRSP money into a RRIF at retirement.

29/04/2011 21IAMAW DL250 Pension Options

Membership Option 4 Lodge 692 Machinists Pension Plan (con’t)

• The Plan uses a professional money manager, Leith Wheeler, and has enjoyed average annual returns of 8.75% over the last 20 years.

• The assets of the plan have grown since 1988 from a little over $10,000,000 to over $95,000,000 today.

• The plan is on sound financial footing and can continue to serve Machinists as long as the need is there.

• The 692 Pension Plan was created in British Columbia by and for members of the Machinists Union.

29/04/2011 22IAMAW DL250 Pension Options

Machinists Pension Plan (LL692) Returns

1988 10.000% 1996 15.750% 2004 12.750%

1989 11.500% 1997 17.000% 2005 10.250%

1990 -2.900% 1998 6.500% 2006 14.250%

1991 19.500% 1999 3.500% 2007 0.500%

1992 8.500% 2000 10.250% 2008 -16.000%

1993 25.000% 2001 4.500% 2009 16.000%

1994 0.000% 2002 2.000% 2010 ~10.750%

1995 13.250% 2003 13.750%

Average Return 8.78%

29/04/2011 IAMAW DL250 Pension Options 23

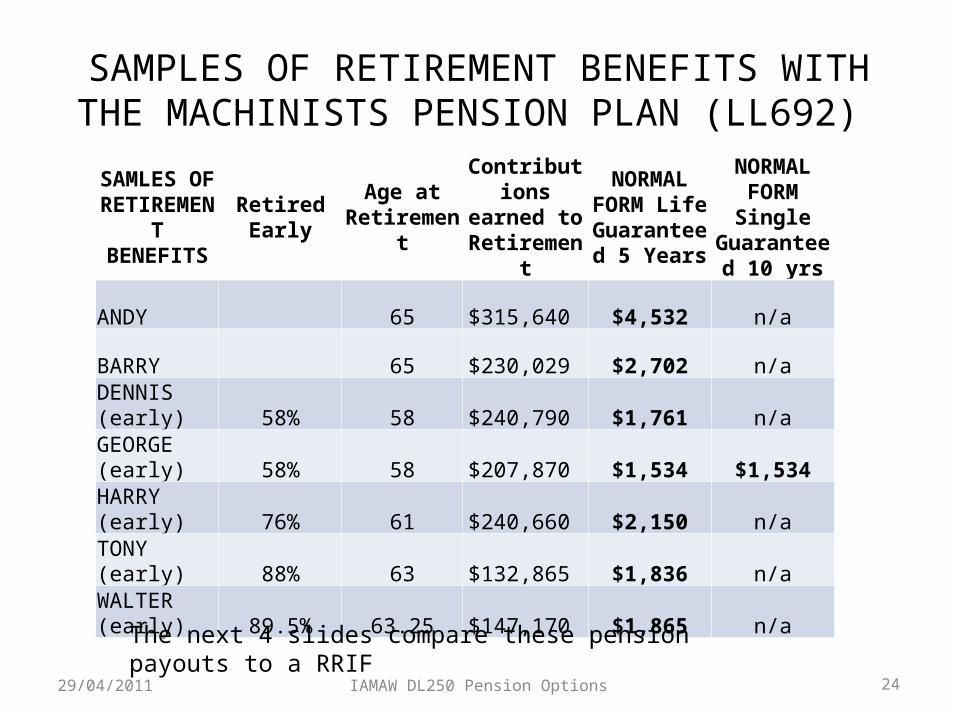

SAMPLES OF RETIREMENT BENEFITS WITH THE MACHINISTS PENSION PLAN (LL692)

SAMLES OF RETIREMENT

BENEFITSRetired Early Age at

Retirement

Contributions earned to

Retirement

NORMAL FORM Life

Guaranteed 5 Years

NORMAL FORM SingleGuaranteed

10 yrs

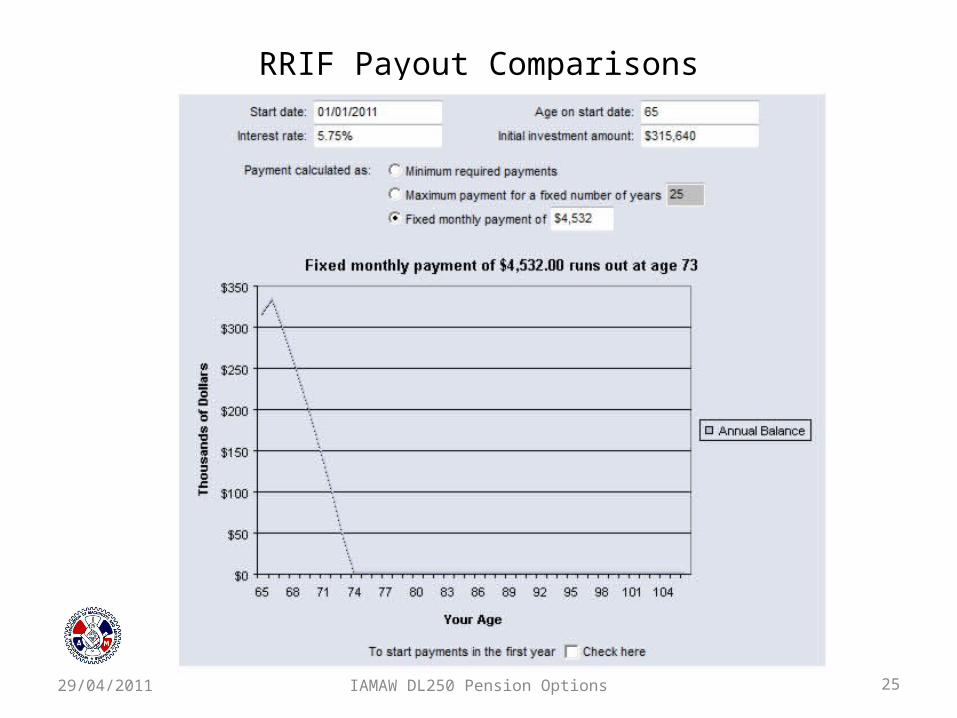

ANDY 65 $315,640 $4,532 n/a

BARRY 65 $230,029 $2,702 n/aDENNIS (early) 58% 58 $240,790 $1,761 n/aGEORGE (early) 58% 58 $207,870 $1,534 $1,534

HARRY (early) 76% 61 $240,660 $2,150 n/a

TONY (early) 88% 63 $132,865 $1,836 n/aWALTER (early) 89.5% 63.25 $147,170 $1,865 n/a

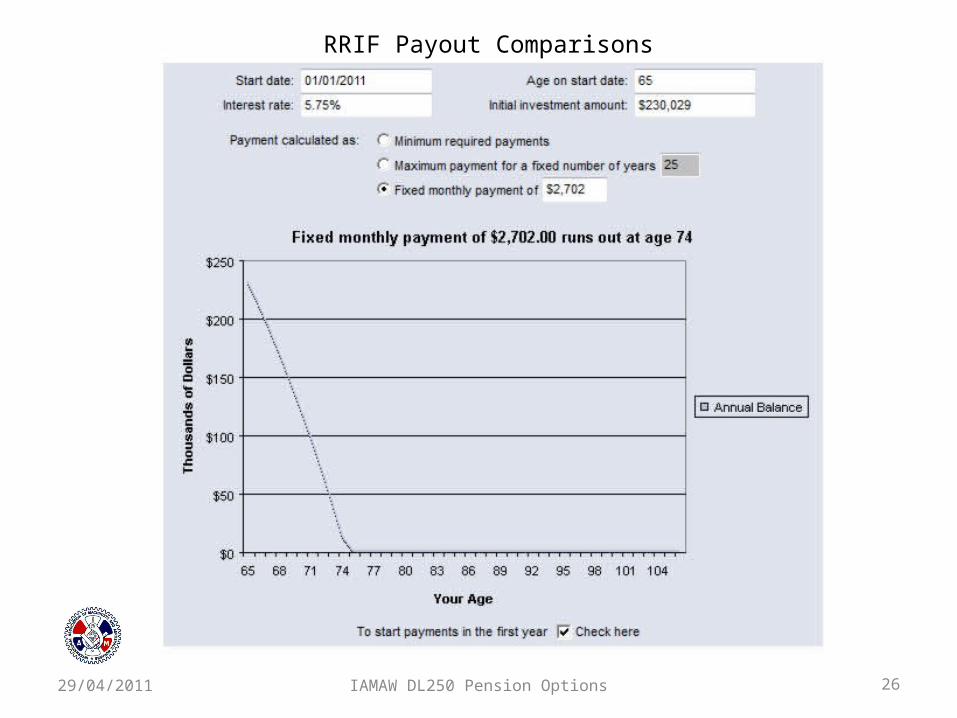

29/04/2011 IAMAW DL250 Pension Options 24

The next 4 slides compare these pension payouts to a RRIF

RRIF Payout Comparisons

29/04/2011 IAMAW DL250 Pension Options 25

29/04/2011 IAMAW DL250 Pension Options 26

RRIF Payout Comparisons

29/04/2011 IAMAW DL250 Pension Options 27

RRIF Payout Comparisons

29/04/2011 IAMAW DL250 Pension Options 28

RRIF Payout Comparisons

Vesting• Vesting is the number of years required to become a full

member of a plan.• Pension members always will receive credit for personal

contributions.• Company contributions are only locked in once vested.• The vesting period is currently 2 years but legislation is

expected to remove the vesting period like Ontario did.• The IAM Labour Management Fund gives past credits for

current employees. If you have worked at your employer for two years, you will probably be vested.

• The Machinists Pension plan requires 350 hours in two consecutive years to vest.

29/04/2011 29IAMAW DL250 Pension Options

Happy Dreams!

29/04/2011 30IAMAW DL250 Pension Options