retail strategy review - city of · pdf filecity of whitehorse retail strategy review prepared...

TRANSCRIPT

City of Whitehorse Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 1

1

PREPARED FOR THE LOCAL GOVERNMENT ASSOCIATION OF SOUTH AUSTRALIA

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd October 2010

MACROPLAN AUSTRALIA PTY LTDSYDNEY | MELBOURNE | BRISBANE | PERTH

City of Whitehorse Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 2

Signed*

………………………………… DATE: OCTOBER 2010

Project Director

Richard Brice General Manager Economics and Research

[email protected] www.macroplan.com.au

CONTACT

MacroPlan Australia Pty Ltd Level 4, 356 Collins Street, Melbourne, Vic. 3000 t 03 9600 0500 f 03 9600 1477

© MacroPlan Australia Pty Ltd All Rights Reserved. No part of this document may be reproduced, transmitted, stored in a retrieval system, or translated into any language in any form by any means without the written permission of MacroPlan Australia Pty Ltd. All Rights Reserved. All methods, processes, commercial proposals and other contents described in this document are the confidential intellectual property of MacroPlan Australia Pty Ltd and may not be used or disclosed to any party without the written permission of MacroPlan Australia Pty Ltd

MACROPLAN AUSTRALIA PTY LTD SYDNEY | MELBOURNE | BRISBANE | PERTH

Project Contact

Justin Malkiewicz Manager Activity Centres

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 3

EXECUTIVE SUMMARY ....................................................................................................... 5

INTRODUCTION 5 POLICY AND LITERATURE REVIEW .......................................................................................................... 6 STAKEHOLDER CONSULTATION ............................................................................................................. 7 POPULATION AND SOCIO-ECONOMIC CHARACTERISTICS ......................................................................... 8 RETAIL SUPPLY ANALYSIS ..................................................................................................................... 8 RETAIL DEMAND ANALYSIS ................................................................................................................... 9 KEY WHITEHORSE ACTIVITY CENTRES .................................................................................................. 11 POLICY AND ACTIONS ........................................................................................................................ 13

1 INTRODUCTION .......................................................................................... 18

1.1 PURPOSE OF STUDY ................................................................................................... 18 1.2 METHODOLOGY OVERVIEW ......................................................................................... 18 1.3 LOCATION AND CONTEXT ............................................................................................ 19 1.4 REPORT STRUCTURE .................................................................................................. 20 1.5 INFORMATION SOURCES ............................................................................................. 21 1.6 ABBREVIATIONS ......................................................................................................... 21 1.7 DISCLAIMER ............................................................................................................... 22

2 POLICY AND LITERATURE REVIEW........................................................... 23

2.1 STATE PLANNING POLICY FRAMEWORK ........................................................................ 23 2.2 LOCAL PLANNING POLICY FRAMEWORK (LPPF) ........................................................... 25 2.3 LOCAL PLANNING POLICY FRAMEWORK – SPECIFIC CENTRES ........................................ 27

3 STAKEHOLDER CONSULTATION .............................................................. 32

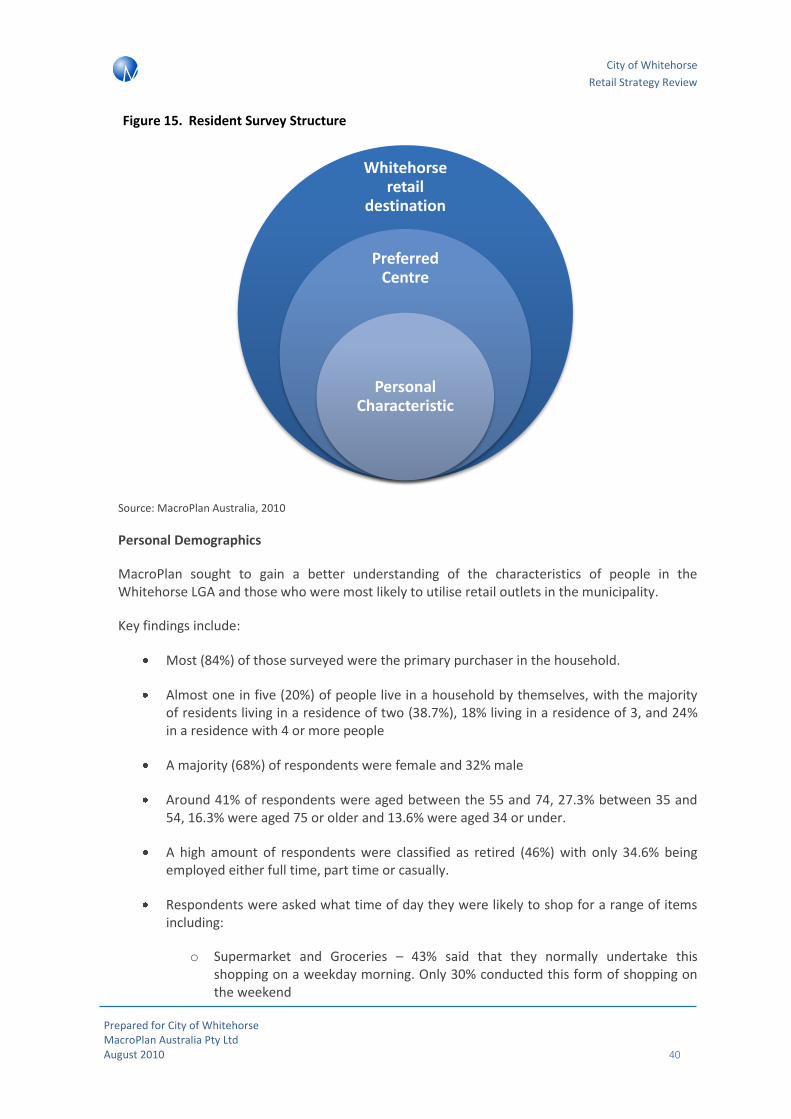

3.1 RETAIL BUSINESS SURVEYS......................................................................................... 32 3.2 IN CENTRE SURVEY ..................................................................................................... 36 3.3 WHITEHORSE RESIDENT SURVEY ................................................................................. 39 3.4 BUSINESS ASSOCIATIONS ........................................................................................... 44 3.5 SUMMARY.................................................................................................................. 45

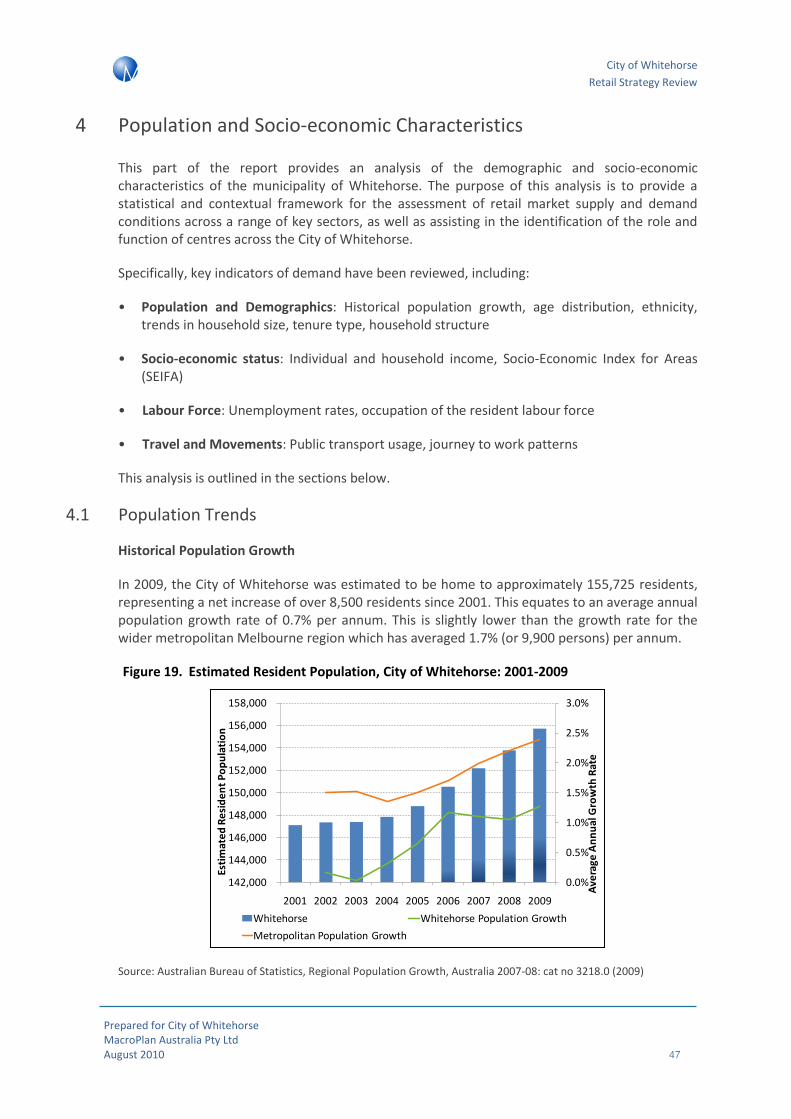

4 POPULATION AND SOCIO-ECONOMIC CHARACTERISTICS .................. 47

4.1 POPULATION TRENDS ................................................................................................. 47 4.2 DEMOGRAPHIC AND SOCIO-ECONOMIC TRENDS ........................................................... 48 4.3 EMPLOYMENT TRENDS ................................................................................................ 51 4.4 JOURNEY TO WORK .................................................................................................... 51 4.5 SUMMARY.................................................................................................................. 52

5 RETAIL SUPPLY ANALYSIS ........................................................................ 53

5.1 SUPPLY DEFINITIONS .................................................................................................. 53 5.2 EXISTING SUPPLY ....................................................................................................... 53 5.3 RETAIL FLOOR SPACE BY TYPE .................................................................................... 60 5.4 FUTURE & PLANNED CENTRES .................................................................................... 61 5.5 SUPPLY CONCLUSIONS ............................................................................................... 62

6 RETAIL DEMAND ANALYSIS ...................................................................... 63

6.1 TRADE AREAS ............................................................................................................ 63 6.2 POPULATION .............................................................................................................. 65 6.3 RETAIL EXPENDITURE PROFILE .................................................................................... 66 6.4 RETAIL FLOOR SPACE DEMAND ................................................................................... 67 6.5 WORKER AND BEYOND TRADE EXPENDITURE ............................................................... 70 6.6 RETAIL POTENTIAL ...................................................................................................... 72 6.7 RETAIL DEMAND CONCLUSIONS .................................................................................. 72

Contents

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 4

7 KEY WHITEHORSE ACTIVITY CENTRES ................................................... 73

7.1 KEY CENTRE ANALYSIS METHODOLOGY ....................................................................... 73 7.2 BOX HILL CENTRAL ACTIVITIES DISTRICT ...................................................................... 77 7.3 NUNAWADING/MEGAMILE MAJOR ACTIVITY CENTRE ..................................................... 83 7.4 FOREST HILL CHASE ACTIVITY CENTRE ........................................................................ 88 7.5 KMART / EAST BURWOOD PLAZA PRECINCT ................................................................. 93 7.6 KEY CENTRE SUMMARY .............................................................................................. 97

8 POLICY AND ACTIONS ............................................................................... 99

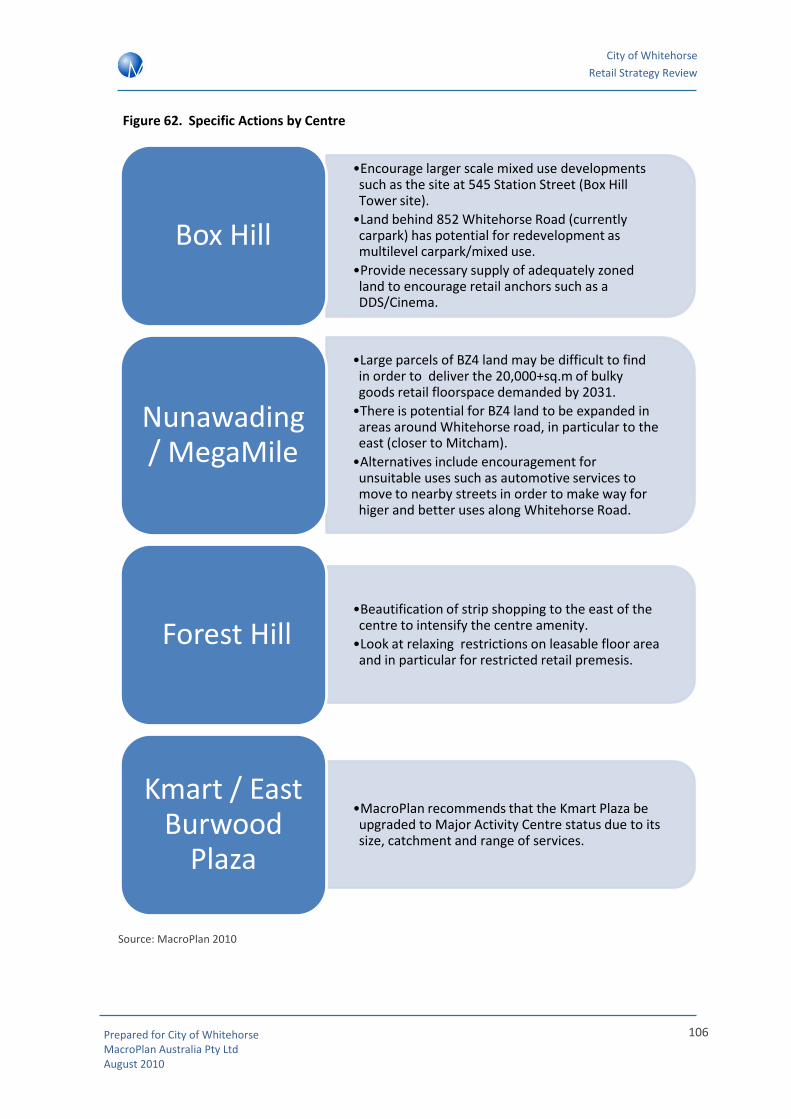

8.1 GUIDING PRINCIPLES .................................................................................................. 99 8.2 UNDERTAKING A RETAIL SUSTAINABILITY ASSESSMENT ................................................ 100 8.3 TRIGGER POINTS FOR A RETAIL SUSTAINABILITY ASSESSMENT BY HIERARCHY ................. 101 8.4 SPECIFIC POLICY INITIATIVES APPLYING TO THE LOCAL PLANNING POLICY ..................... 103 8.5 SPECIFIC ACTIONS BY CENTRE .................................................................................. 104 8.6 CONCLUDING RECOMMENDATIONS ........................................................................... 108

APPENDIX A – WHITEHORSE RETAIL PRECINCTS ...................................................... 109

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 5

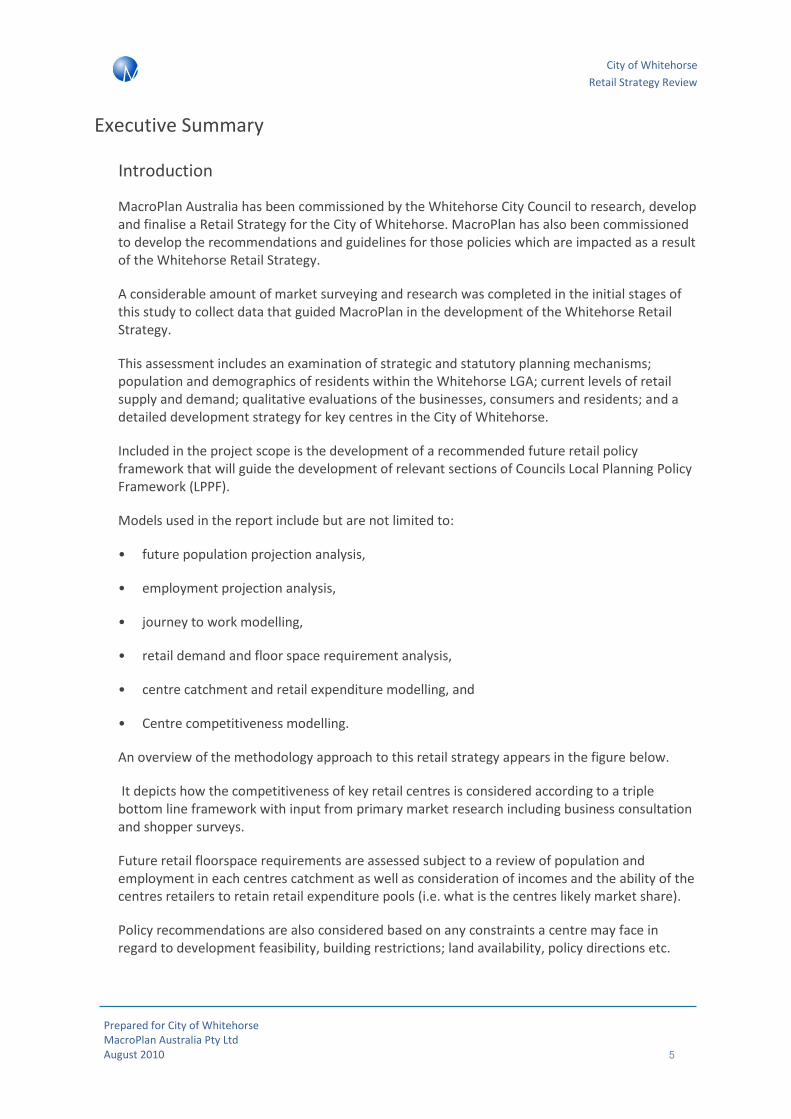

Executive Summary

Introduction

MacroPlan Australia has been commissioned by the Whitehorse City Council to research, develop and finalise a Retail Strategy for the City of Whitehorse. MacroPlan has also been commissioned to develop the recommendations and guidelines for those policies which are impacted as a result of the Whitehorse Retail Strategy.

A considerable amount of market surveying and research was completed in the initial stages of this study to collect data that guided MacroPlan in the development of the Whitehorse Retail Strategy.

This assessment includes an examination of strategic and statutory planning mechanisms; population and demographics of residents within the Whitehorse LGA; current levels of retail supply and demand; qualitative evaluations of the businesses, consumers and residents; and a detailed development strategy for key centres in the City of Whitehorse.

Included in the project scope is the development of a recommended future retail policy framework that will guide the development of relevant sections of Councils Local Planning Policy Framework (LPPF).

Models used in the report include but are not limited to:

• future population projection analysis,

• employment projection analysis,

• journey to work modelling,

• retail demand and floor space requirement analysis,

• centre catchment and retail expenditure modelling, and

• Centre competitiveness modelling.

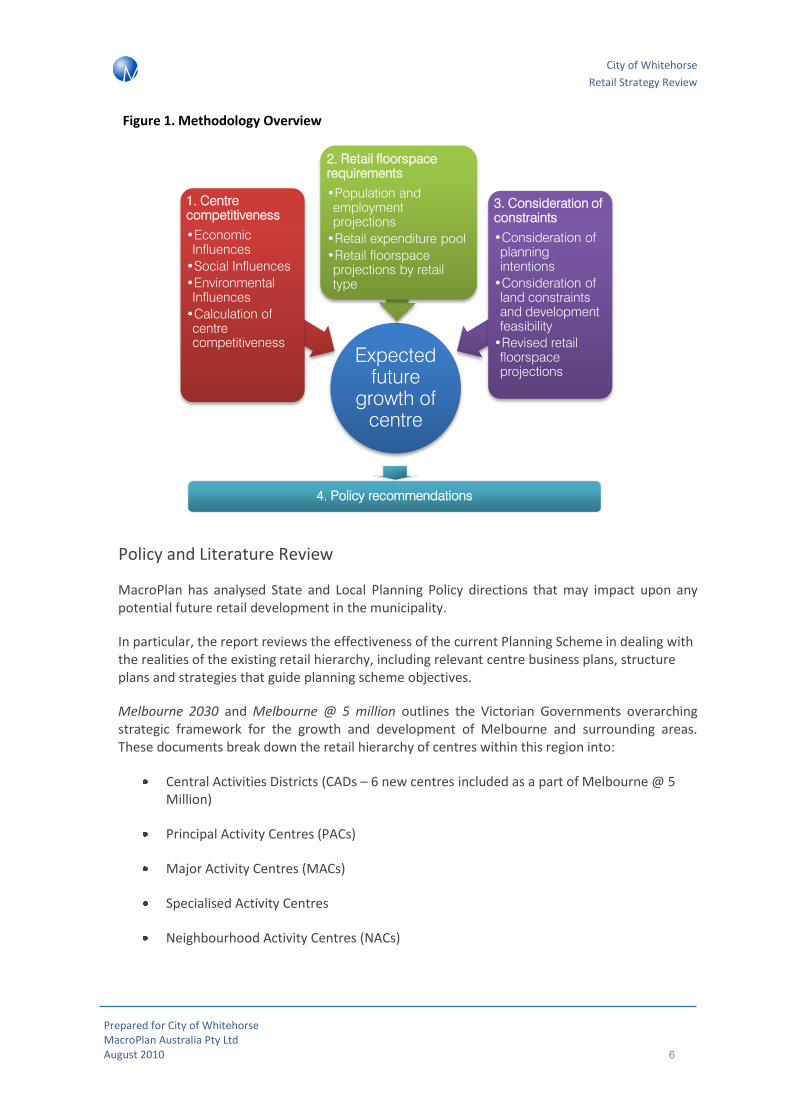

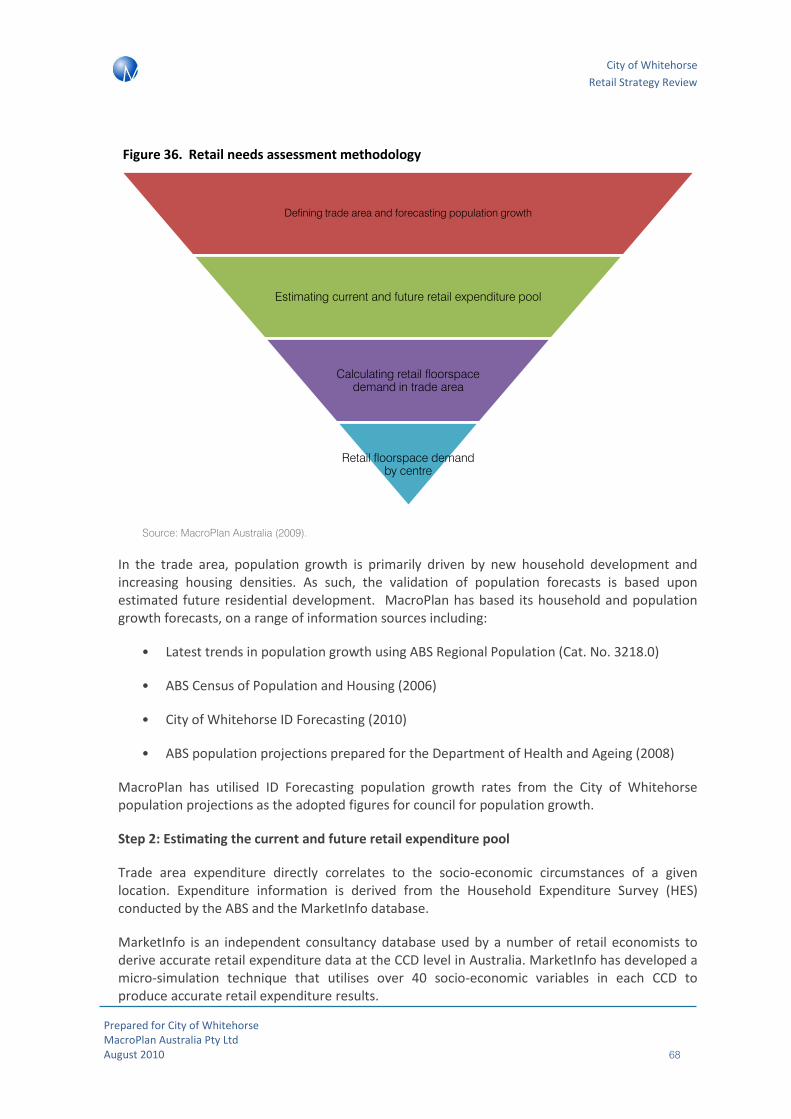

An overview of the methodology approach to this retail strategy appears in the figure below.

It depicts how the competitiveness of key retail centres is considered according to a triple bottom line framework with input from primary market research including business consultation and shopper surveys.

Future retail floorspace requirements are assessed subject to a review of population and employment in each centres catchment as well as consideration of incomes and the ability of the centres retailers to retain retail expenditure pools (i.e. what is the centres likely market share).

Policy recommendations are also considered based on any constraints a centre may face in regard to development feasibility, building restrictions; land availability, policy directions etc.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 6

Figure 1. Methodology Overview

Policy and Literature Review

MacroPlan has analysed State and Local Planning Policy directions that may impact upon any potential future retail development in the municipality.

In particular, the report reviews the effectiveness of the current Planning Scheme in dealing with the realities of the existing retail hierarchy, including relevant centre business plans, structure plans and strategies that guide planning scheme objectives.

Melbourne 2030 and Melbourne @ 5 million outlines the Victorian Governments overarching strategic framework for the growth and development of Melbourne and surrounding areas. These documents break down the retail hierarchy of centres within this region into:

Central Activities Districts (CADs – 6 new centres included as a part of Melbourne @ 5 Million)

Principal Activity Centres (PACs)

Major Activity Centres (MACs)

Specialised Activity Centres

Neighbourhood Activity Centres (NACs)

Expected future

growth of centre

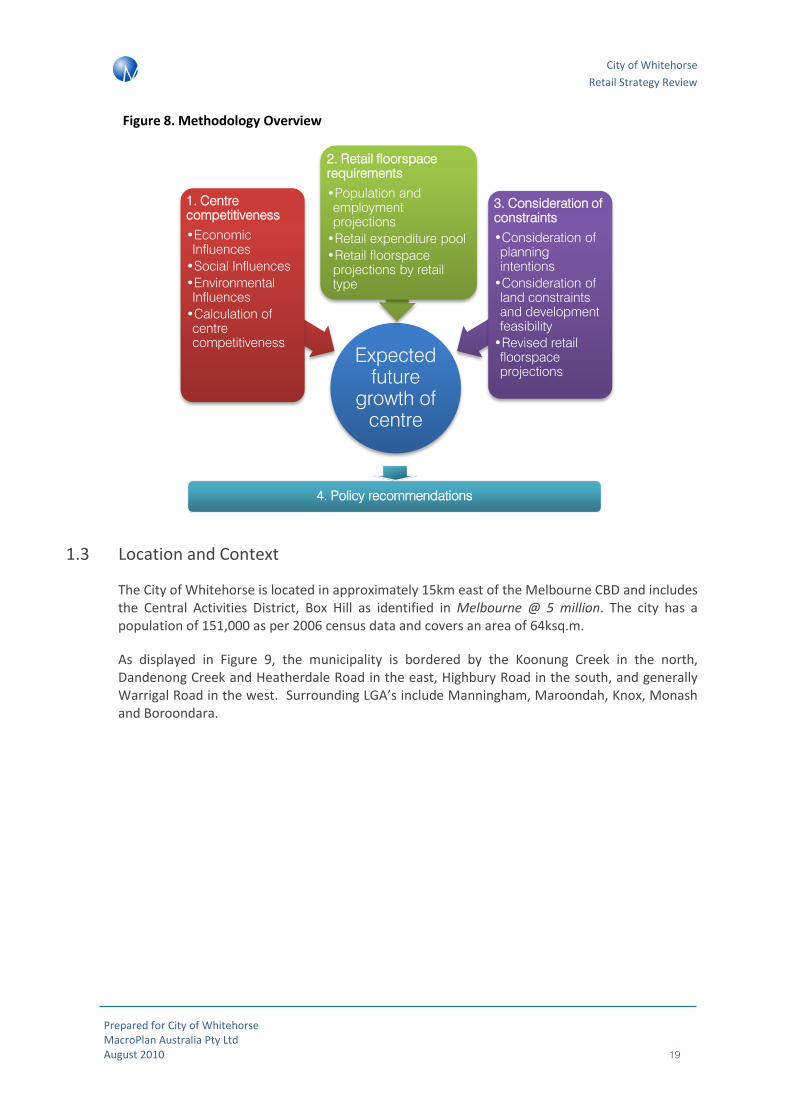

1. Centre competitiveness

•Economic Influences

•Social Influences

•Environmental Influences

•Calculation of centre competitiveness

2. Retail floorspace requirements

•Population and employment projections

•Retail expenditure pool

•Retail floorspace projections by retail type

3. Consideration of constraints

•Consideration of planning intentions

•Consideration of land constraints and development feasibility

•Revised retail floorspace projections

4. Policy recommendations

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 7

Depending on the strategic importance of the centre hierarchy there will be more of a focus on commercial, retail, higher order personal services, entertainment, education, government and tourism.

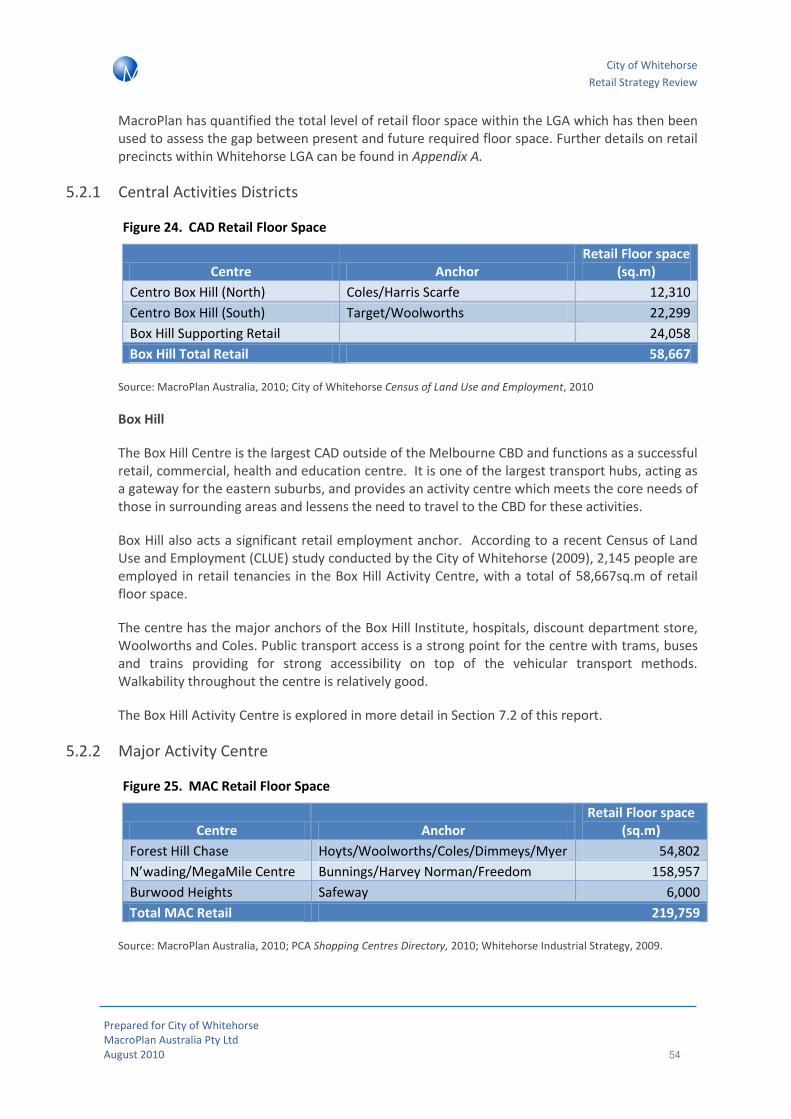

Box Hill has been designated as a CAD and for this reason has a large amount of future strategic importance to Whitehorse and metropolitan Melbourne more generally.

MacroPlan notes the importance of the centre hierarchy, specifically considering:

Box Hill Central Activities District

Nunawading/MegaMile Major Activity Centre

Forest Hill Major Activity Centre

Expansion of the Kmart / East Burwood Plaza Activity Centre to become of Major Activity Centre Status within the municipality.

Burwood Heights Major Activity Centre

The body of the report summarises relevant planning directions including the Planning Scheme in more detail and, where appropriate, have been commented on in the final section of the report where making future policy recommendations.

Stakeholder Consultation

As part of a qualitative review of centres in the City of Whitehorse, MacroPlan conducted a number of surveys across businesses, consumers and residents to better understand the needs, desires and characteristics of stakeholders for retail centres within the municipality.

The survey indicated that Whitehorse was facing a positive economic environment over the future six months, with more businesses seeking to employ additional staff than those who are looking to reduce employment. Businesses pointed to parking availability and economic conditions as issues and potential threats to their business.

Residents also outlined parking as the most dissatisfying aspect to shopping at centres within the municipality and there was also a low ‘positive’ reaction to the level of afterhours service provided.

The results of all three surveys were generally positive, revealing a well-functioning retail sector throughout the Whitehorse LGA. Overall, Whitehorse is viewed by respondents as a desirable shopping destination and by business owners as a good place to do business.

The primary issues of concern for local business owners revolve around the state of the economy and not around issues for which Council is responsible. Issues of concern that may be addressed by Council involve increasing convenient car parking and providing additional signage which may have the additional benefit of contributing to the identity of the centre.

The responses from the users of the centres provided an important link to the quantitative and strategic aspects of this report and assisted in the final policy recommendations.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 8

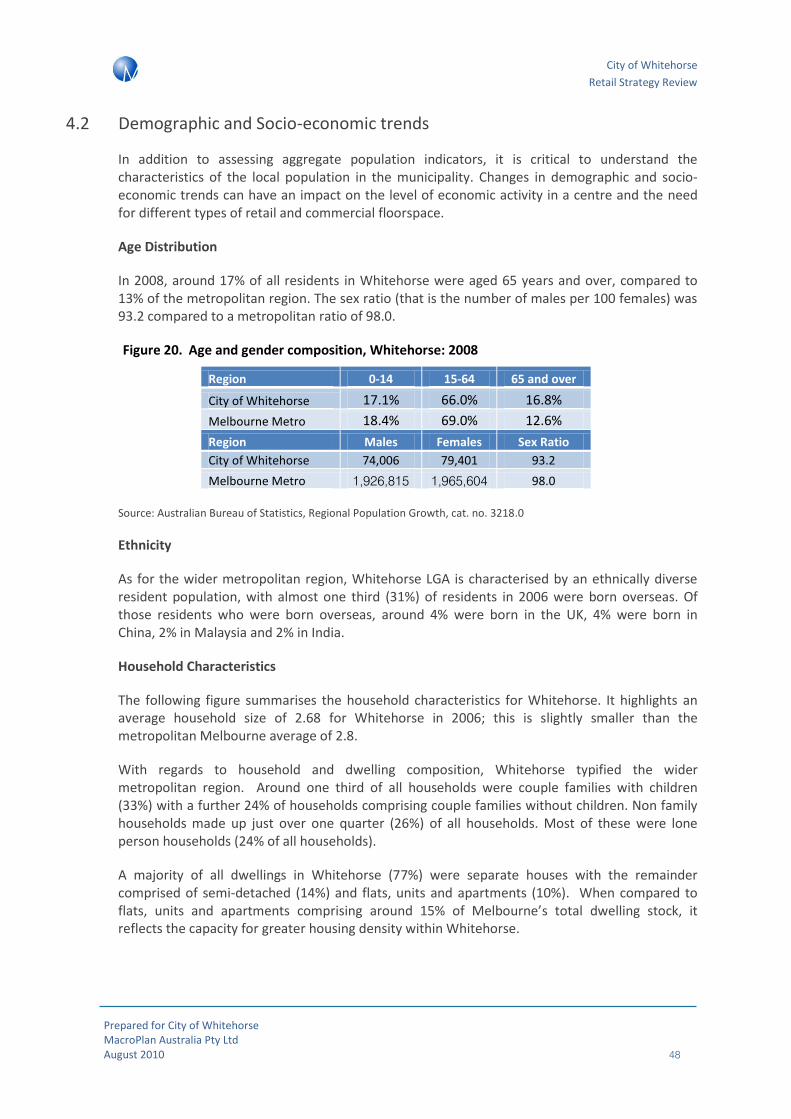

Population and Socio-economic Characteristics

MacroPlan has provided an analysis of the demographic and socio-economic characteristics of the municipality of Whitehorse. The purpose of this analysis is to provide a statistical and contextual framework for the assessment of retail market supply and demand conditions across a range of key sectors, as well as assisting in the identification of the role and function of centres across the City of Whitehorse.

Specifically, key indicators of demand have been reviewed, including:

• Population and Demographics: Historical population growth, age distribution, ethnicity, trends in household size, tenure type, household structure

• Socio-economic status: Individual and household income, Socio-Economic Index for Areas (SEIFA)

• Labour Force: Unemployment rates, occupation of the resident labour force

• Travel and Movements: Public transport usage, journey to work patterns

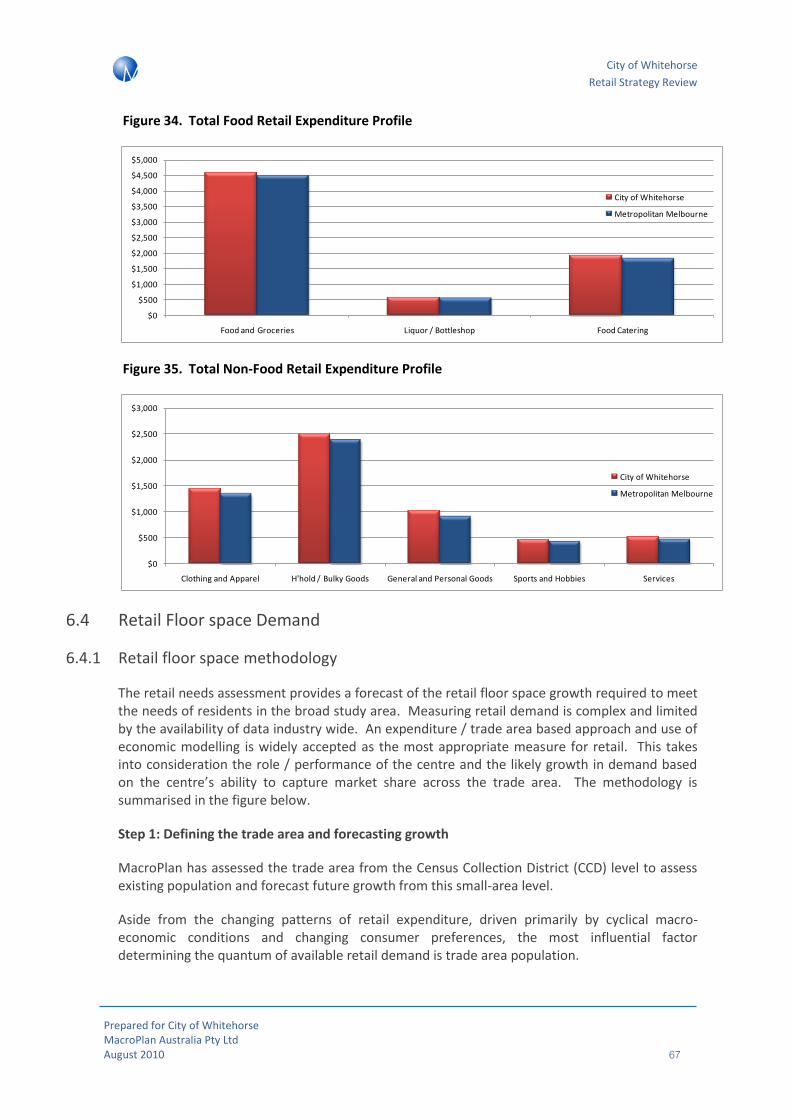

The City of Whitehorse is characterised by a diverse population both in age and ethnicity with a greater percentage of residents 65+ years than metropolitan Melbourne and almost one third of the population born abroad. However, compared to the metropolitan region, the area is comprised of an average population from a socio-economic perspective. In particular, residents in Whitehorse had similar taxable incomes compared to greater Melbourne. SEIFA scores in the area were 1,066 (where the mean score is 1,000) despite a median individual taxable income that was below the metropolitan average.

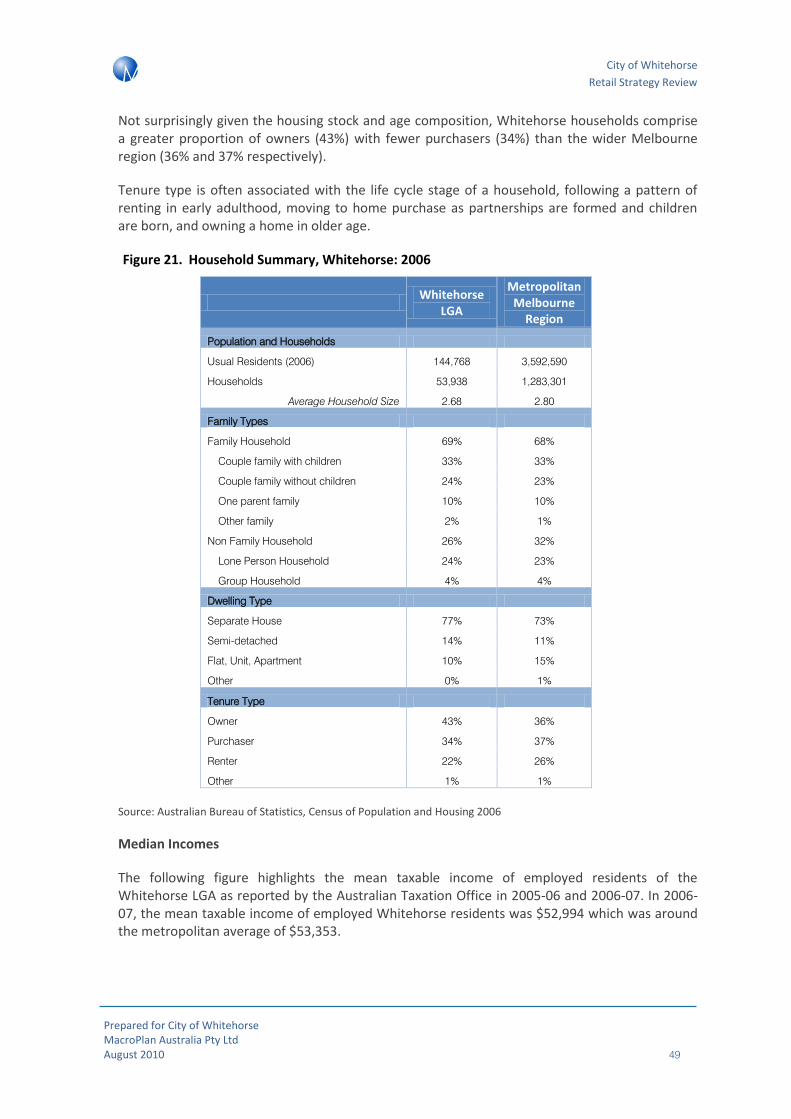

Generally residents are less likely to be renters and purchasers compared to the metropolitan region. This corresponds with the older population that have generally transitioned out of the rental phase of the housing life cycle. High incomes in the study area correlate with a significant capacity for retail expansion on discretionary goods (i.e. retail tenancies located in larger centres).

Retail Supply Analysis

The study investigated the amount and form of supply in the City of Whitehorse, focussing on the four key centres, but also assessing the retail floor space supply across the municipality as a whole, then comparing it to demand for retail floor space. Furthermore, the report outlines the types of centres within the Whitehorse LGA and considers the potential, if any, for further additions to floor space in the future.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 9

Figure 2. Retail Hierarchy by Floor Space

Source: MacroPlan Australia, 2010; PCA, 2010; Box Hill CLUE, 2009; Draft Neighbourhood Activity Centre Study, 2009.

In general, the Whitehorse LGA enjoys a diverse and healthy retail sector with a variety of retailing formats across all activity centres. In particular, the retail critical mass at the Box Hill CAD attracts those from outside the LGA and drives a strong competitive network that results in choice for the consumer.

MacroPlan has assessed the current total supply of retail floor space within the Whitehorse LGA to be approximately 635,000sq.m.

The current allocation of retail floor space in the study area is broadly consistent with averages in metropolitan Melbourne. However, floor space allocation is slightly concentrated at the CAD and MAC level which can have negative impacts of requiring consumers to travel further to access some retail formats. This increases traffic, environmental externalities, and may be particularly problematic for older and low income persons who may not have access to a motor vehicle. With significant volume of core retail floor space located within the Box Hill SLA, access to some retail formats may be reduced for some patrons.

Going forward, it will be important to encourage development at the neighbourhood and local level to ensure both high-end and amenity retailing meets the needs of the defined local catchments, with specific attention to the food versus non-food mix. Increasing the supply of local retailing has many social, environmental and economic benefits. Specifically, the activity centres may benefit from an increase in the desirability of the local residential markets, with increased amenity in turn encouraging higher density housing, and a lessening of the environmental impact through reduced travel time. Whilst these positive effects can occur at all levels of the activity centre hierarchy, they are especially important for the sustainable development of neighbourhood activity centres.

However, in regard to access it is important to note that most of Whitehorse’s larger centres have good public transport access.

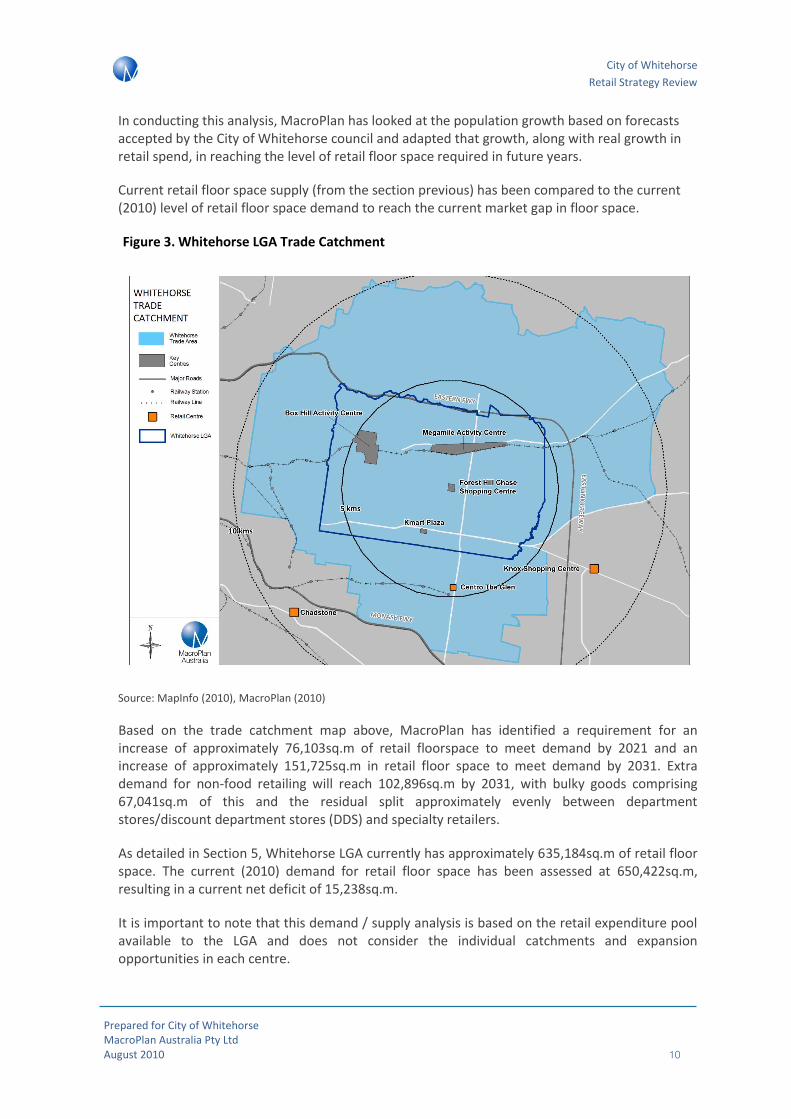

Retail Demand Analysis

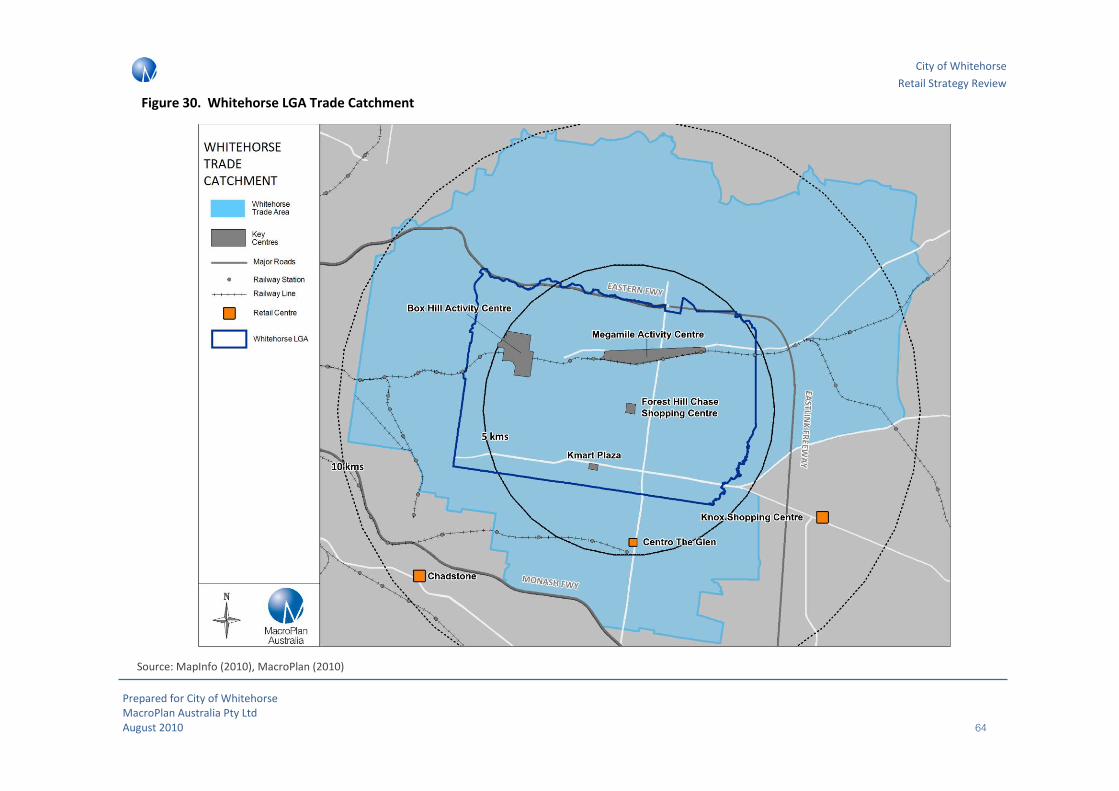

A demand analysis has been conducted based on the entire catchment of the Whitehorse LGA as illustrated in the following trade catchment map. Clearly, it is not only constituents within the LGA that utilise retail facilities – in particular with regards to Box Hill.

Hierarchy Type Retail m2 % m2

Central Activity District 58,667 9.2%

Major Activity Centre 219,759 34.6%

Large Neighbourhood Activity Centre 312,408 49.2%

Medium Neighbourhood Activity Centre 42,171 6.6%

Small Neighbourhood Activity Centre 2,179 0.3%

Total 635,184 100.0%

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 10

In conducting this analysis, MacroPlan has looked at the population growth based on forecasts accepted by the City of Whitehorse council and adapted that growth, along with real growth in retail spend, in reaching the level of retail floor space required in future years.

Current retail floor space supply (from the section previous) has been compared to the current (2010) level of retail floor space demand to reach the current market gap in floor space.

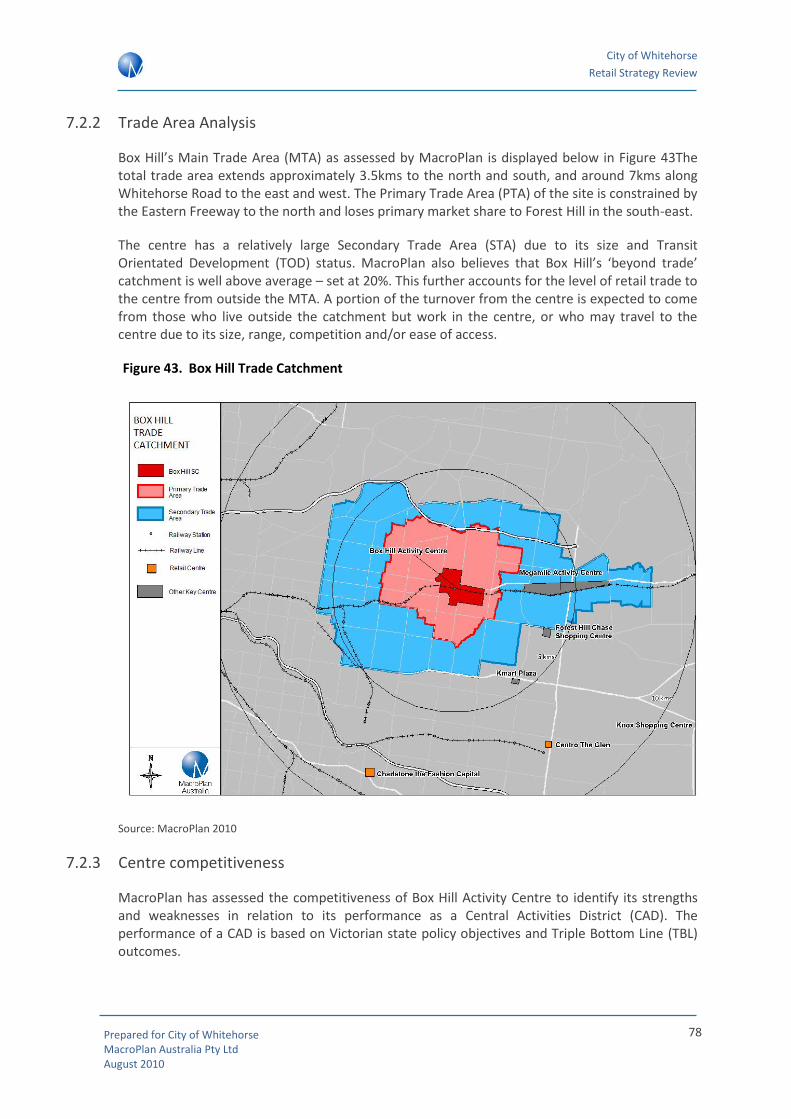

Figure 3. Whitehorse LGA Trade Catchment

Source: MapInfo (2010), MacroPlan (2010)

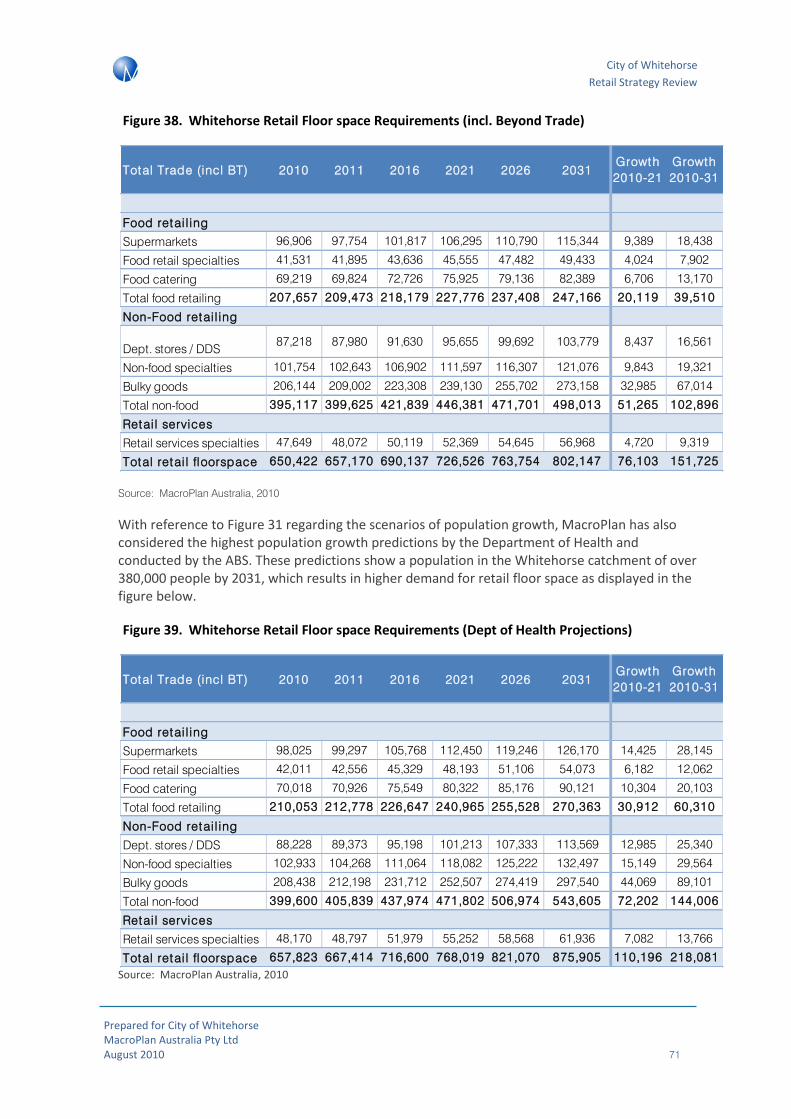

Based on the trade catchment map above, MacroPlan has identified a requirement for an increase of approximately 76,103sq.m of retail floorspace to meet demand by 2021 and an increase of approximately 151,725sq.m in retail floor space to meet demand by 2031. Extra demand for non-food retailing will reach 102,896sq.m by 2031, with bulky goods comprising 67,041sq.m of this and the residual split approximately evenly between department stores/discount department stores (DDS) and specialty retailers.

As detailed in Section 5, Whitehorse LGA currently has approximately 635,184sq.m of retail floor space. The current (2010) demand for retail floor space has been assessed at 650,422sq.m, resulting in a current net deficit of 15,238sq.m.

It is important to note that this demand / supply analysis is based on the retail expenditure pool available to the LGA and does not consider the individual catchments and expansion opportunities in each centre.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 11

Figure 4. Whitehorse Retail Floor space Requirements (incl. Beyond Trade)

Source: MacroPlan Australia, 2010

Retail floor space needs at the 2010 level are not currently being met. Evaluated in conjunction with the high levels of expenditure within the LGA (which are consistently above metropolitan Melbourne averages), the Whitehorse retail sector has the potential for expansion.

The existing floor space deficit may be mitigated by proposed future developments. However, the major proposed developments are clustered around the Kmart / East Burwood Activity Centre with smaller proposed developments (mostly in the form of supermarkets and few convenience retailers in mixed use developments) located in the other activity centres. Whilst the major developments will reduce any overall deficit, consideration should be given to meeting demand across the LGA and reflect this through the development of core retailing services.

In particular it is worth noting that there will be demand for an additional 13,200sq.m of supermarket retail floor space in the municipality over the period to 2021. These supermarkets should be delivered near or adjacent to NACs that may be underperforming and preferably adjacent to public transport subject to feasibility.

Key Whitehorse Activity Centres

MacroPlan has also conducted a more comprehensive analysis of four of the key centres within the Whitehorse LGA, providing a trade catchment analysis for each and assessing the competitiveness of the centre.

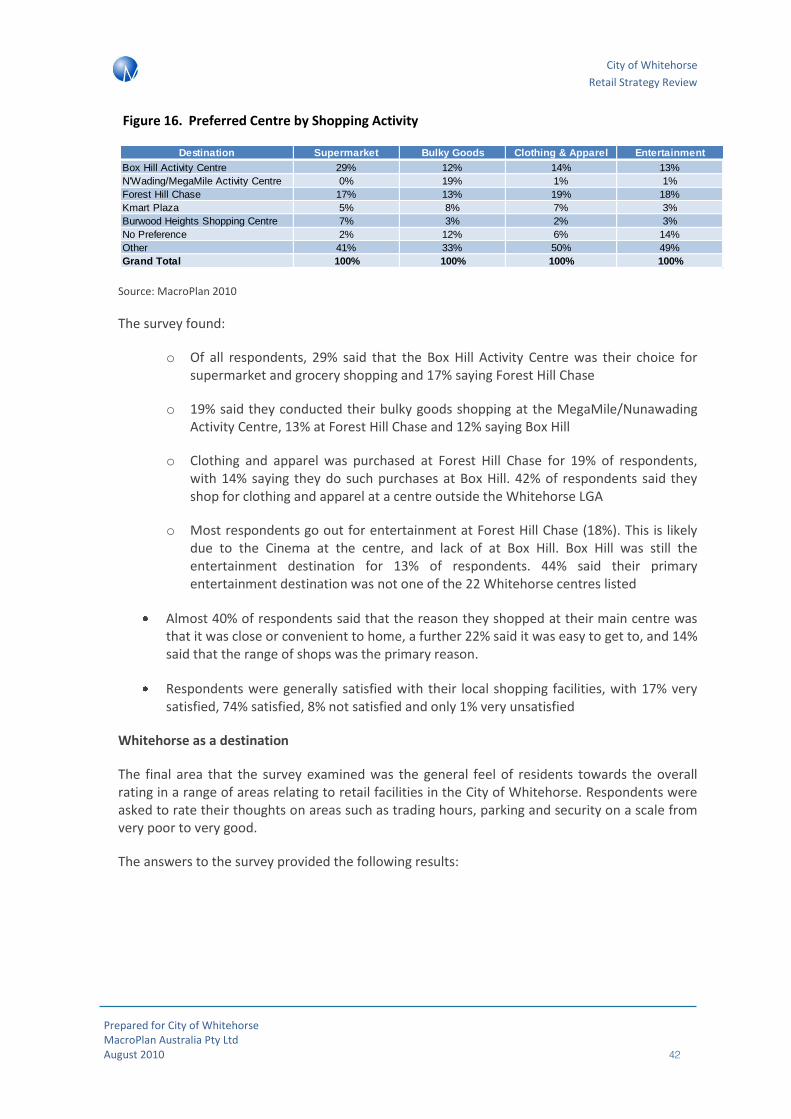

The competitiveness of Box Hill, Nunawading/MegaMile, Forest Hill and Burwood (Kmart) Plaza have been specifically assessed in the figure outlined below.

Total Trade (incl BT) 2010 2011 2016 2021 2026 2031Growth

2010-21

Growth

2010-31

Food retai l ing

Supermarkets 108,624 109,799 115,740 121,820 127,941 134,124 13,195 25,499

Food retail specialties 46,553 47,057 49,603 52,208 54,832 57,482 5,655 10,928

Food catering 77,589 78,428 82,671 87,014 91,386 95,803 9,425 18,214

Total food retailing 232,767 235,283 248,014 261,042 274,159 287,408 28,275 54,641

Non-Food retai l ing

Dept. stores / DDS 96,913 97,964 103,280 108,723 114,206 119,745 11,810 22,832

Non-food specialties 113,065 114,291 120,494 126,844 133,240 139,703 13,779 26,638

Bulky goods 209,978 212,254 223,774 235,567 247,445 259,448 25,589 49,470

Total non-food 419,956 424,509 447,548 471,133 494,891 518,896 51,178 98,941

Retai l services

Retail services specialties 48,456 48,982 51,640 54,362 57,103 59,873 5,905 11,416

Total retai l floorspace 701,178 708,774 747,202 786,537 826,152 866,177 85,358 164,998

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 12

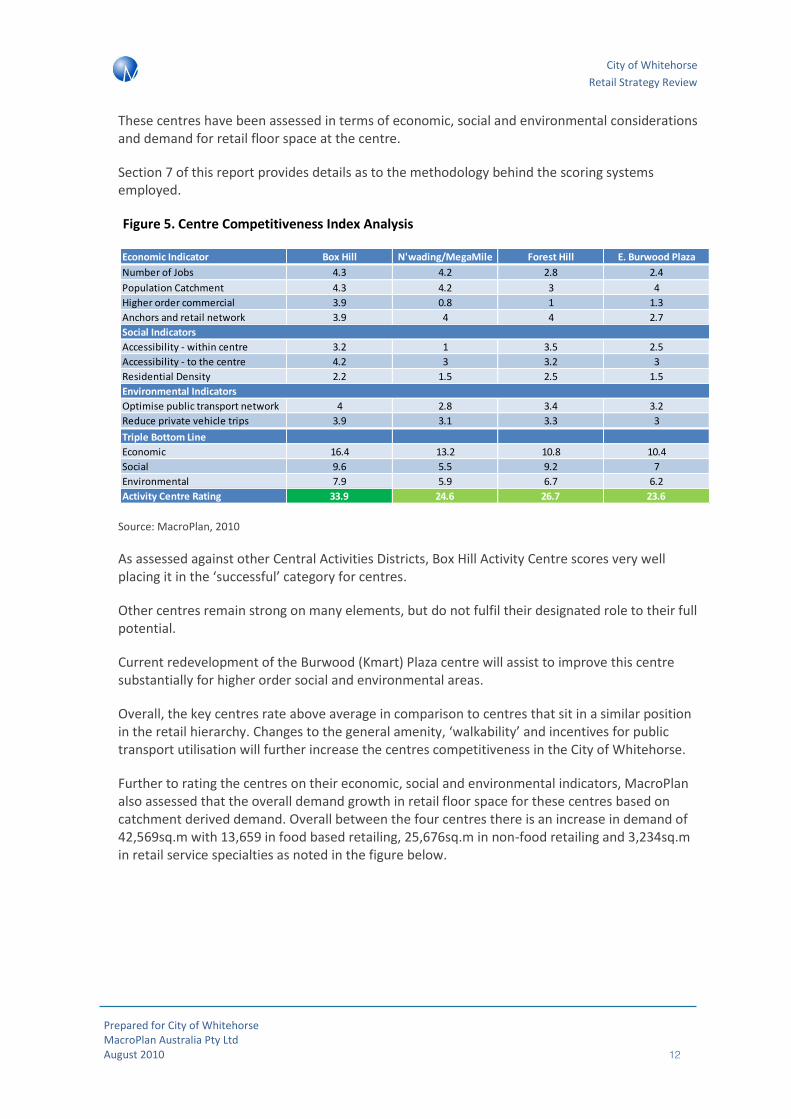

These centres have been assessed in terms of economic, social and environmental considerations and demand for retail floor space at the centre.

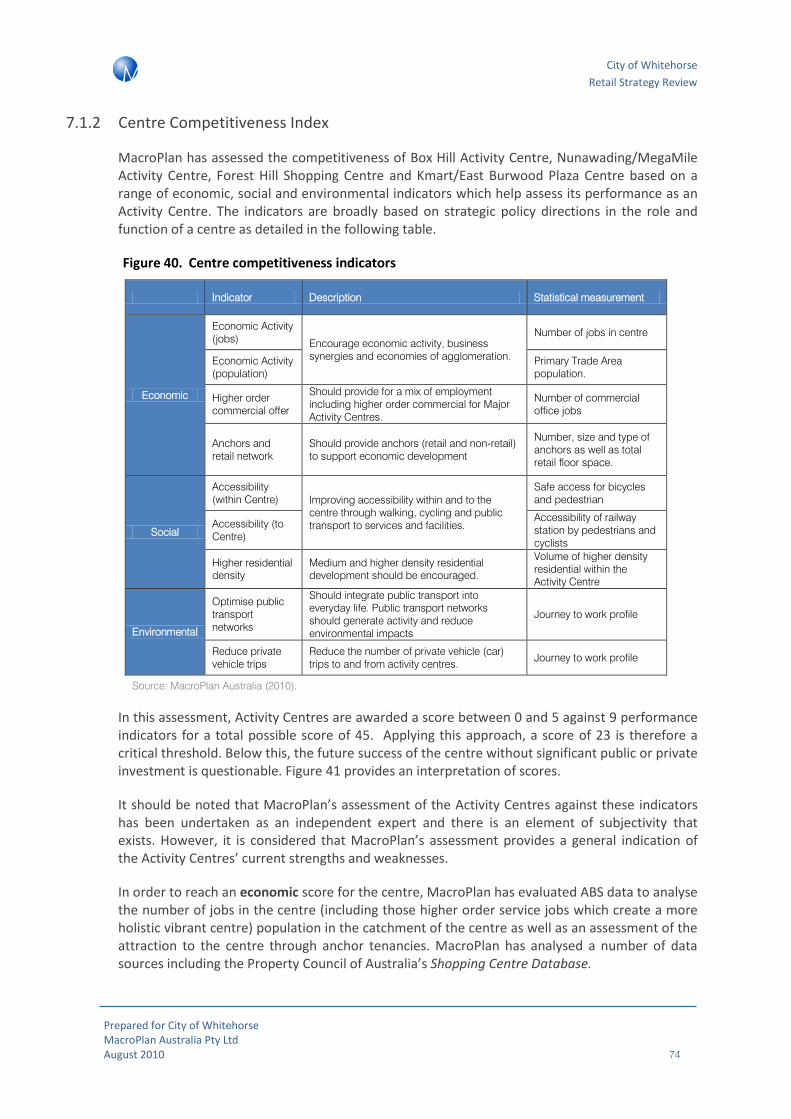

Section 7 of this report provides details as to the methodology behind the scoring systems employed.

Figure 5. Centre Competitiveness Index Analysis

Source: MacroPlan, 2010

As assessed against other Central Activities Districts, Box Hill Activity Centre scores very well placing it in the ‘successful’ category for centres.

Other centres remain strong on many elements, but do not fulfil their designated role to their full potential.

Current redevelopment of the Burwood (Kmart) Plaza centre will assist to improve this centre substantially for higher order social and environmental areas.

Overall, the key centres rate above average in comparison to centres that sit in a similar position in the retail hierarchy. Changes to the general amenity, ‘walkability’ and incentives for public transport utilisation will further increase the centres competitiveness in the City of Whitehorse.

Further to rating the centres on their economic, social and environmental indicators, MacroPlan also assessed that the overall demand growth in retail floor space for these centres based on catchment derived demand. Overall between the four centres there is an increase in demand of 42,569sq.m with 13,659 in food based retailing, 25,676sq.m in non-food retailing and 3,234sq.m in retail service specialties as noted in the figure below.

Economic Indicator Box Hill N'wading/MegaMile Forest Hill E. Burwood Plaza

Number of Jobs 4.3 4.2 2.8 2.4

Population Catchment 4.3 4.2 3 4

Higher order commercial 3.9 0.8 1 1.3

Anchors and retail network 3.9 4 4 2.7

Social Indicators

Accessibility - within centre 3.2 1 3.5 2.5

Accessibility - to the centre 4.2 3 3.2 3

Residential Density 2.2 1.5 2.5 1.5

Environmental Indicators

Optimise public transport network 4 2.8 3.4 3.2

Reduce private vehicle trips 3.9 3.1 3.3 3

Triple Bottom Line

Economic 16.4 13.2 10.8 10.4

Social 9.6 5.5 9.2 7

Environmental 7.9 5.9 6.7 6.2

Activity Centre Rating 33.9 24.6 26.7 23.6

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 13

Figure 6. Comparison of growth in retail floorspace (2009 – 2031)

Source: MacroPlan, 2010; MarketInfo, 2009

Policy and Actions

MacroPlan has used the above analysis and our assessment and consideration of best practice policy in other jurisdictions to provide policy and action guidance in the following:

1. Guiding policy principles for retail strategy

2. A framework for the conduct of retail sustainability assessments (RSAs) submitted as part of a development application

3. Trigger points for the requirement for a RSA

4. Specific policy initiatives for the retail hierarchy in the study area

5. Specific policy actions for key centres

Guiding principles

There are a number of key guiding policies and principles that should be considered by developers / landowners as part of a development application for an expansion in retail floorspace that may be inconsistent with an endorsed Structure Plan.

MacroPlan recommends the following key principles are considered by stakeholders and highlighted in the Planning Scheme as key objectives:

ACCESS TO SERVICES: Insuring a distribution of retail floorspace throughout Whitehorse to allow for improved access to retail goods and services by all members of the community

Retai l format type

(Growth 2009 - 2031)Box Hi l l

N'wading/Me

gaMi leForest Hi l l

E.Burwood

PlazaTotal

Food retailing

Supermarket 1,346 567 1,684 451 4,047

Food retail specialties 887 144 469 311 1,812

Restaurants and cafés 3,652 747 1,510 766 6,676

Total food-based 5,885 1,459 3,663 1,528 12,535

Non-Food retailing

Dept. Stores / DDS 600 3,908 1,010 1,172 6,690

Non-food specialties 451 2,853 671 834 4,809

Bulky goods 128 14,117 373 434 15,052

Total Non-food based 1,179 20,878 2,054 2,441 26,551

Retail services

Retail services specialties 319 618 570 258 1,765

Total retai l 7,383 22,954 6,288 4,227 40,852

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 14

COMPETITION: A catchment should be defined within reasonable boundaries to ensure consistency with the centres role in the retail hierarchy. This will assist in distributing market shares more evenly throughout the retail hierarchy.

EVIDENCE: Development applications that request an expansion in the size of a centre should be supported by evidence – preferably by a resident survey – to demonstrate why a centres catchment is growing and why demand exceeds existing supply.

INNOVATION: Innovation in retailing will continue to drive new retail formats and is supported where it can be demonstrated that consumer trends are evolving. In practice this means that new retail formats can be supported to meet changes in consumer preferences.

LOCATION: Activity centres should be located and planned to promote reduced transport energy demands and private vehicle kilometres per capita.

EMPLOYMENT IMPACT: A proposed development should consider the labour force profile of the catchment and demonstrate how it will assist in the improvement of employment self sufficiency across various industry sectors of the economy. Developments that improve employment self sufficiency in non-retail sectors as well as the retail sector will be viewed favourably.

ENVIRONMENTAL IMPACTS: Development applications should consider not only economic or turnover impacts on other centres but the environmental impact of the development in relation to traffic generation and emissions. MacroPlan notes for the purpose of this study it was not feasible to conduct an environmental assessment of centres throughout the Whitehorse LGA, however, Section 8 provides a number of general environmental guidelines.

RETURN ON GOVERNMENT INVESTMENT IN PUBLIC TRANSPORT: A development should encourage a more effective use of public transport (existing and planned) and retail expansions adjacent to principal public transport (particularly rail) will be considered more favourably.

SUPPORTING A HIERARCHY: A commitment to maintaining and enhancing the defined hierarchy of activity centres that balances the need for a distribution of retail floorspace with the importance of critical mass in non-food retailing at higher order centres.

SOCIAL IMPACTS: Development applications that include a Triple Bottom Line (TBL) assessment that clearly highlight positive social impacts will assist consideration of the application. Issues including impacts on night time activity, unemployment, community interaction, safety, amenity etc should be addressed for major development applications.

Subject to these policy principals MacroPlan has developed guidelines on what should be included in a RSA submitted as part of a development application and appropriate trigger points for the need for an RSA.

The purpose of these guidelines is to provided developers and centre owners with more certainty as to Council’s policy objectives and requirements.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 15

Undertaking a Retail Sustainability Assessment

Traditionally a RSA has as a minimum assessed turnover impacts on other centres and confirmed the demand for retail floorspace within a defined catchment.

Council’s clear commitment to sustainable economic development and triple bottom line consideration of development applications confirms that the overall costs and benefits of a proposed development including social and economic impacts is important in the consideration of activity centre development.

As a minimum a RSA should include the following:

Definition of a Primary and Secondary Trade Area for retail floorspace and a defined Main Trade Area

Calculation of the total retail expenditure pool generated by the catchment and the retained expenditure that is expected ‘pre’ and ‘post’ development.

Assessment of whether the volume of retail expenditure that is expected to be retained in the catchment ‘post’ development is consistent with the centres position in the retail hierarchy

An RSA should clearly define why the expected retail turnover per m2 has been chosen for a proposed retail format and compare it to State and National benchmarks. Variations in performance between the proposed retail tenancies and benchmark standards should be explained. (i.e. why is the proposed new supermarket expected to trade at $6,000 per m2 when existing older supermarkets are trading at $8,000 per m2)

Clear reporting on the market shares that are expected for retail floorspace across key retail categories in the Primary and Secondary trade areas including food and ‘non-food’ retail floorspace

Clear indications of where additional trade is expected to be sourced (i.e. from existing centres, future planned centres and centres outside the defined catchment (i.e. escape expenditure)

Expected trading impacts on existing and proposed centres for each stage of the development that is proposed in % and $ terms

Calculation of employment impacts and impacts on the unemployment rate in the region subject to the volume of jobs the centre is expected to support.

Trigger Points for a retail sustainability assessment by hierarchy

The trigger point for a retail sustainability assessment (RSA) is fundamentally important as it allows for the balancing of the sustainable development of activity centres in the City of Whitehorse with the target of ensuring an adequate supply of retail floorspace to meet consumer needs.

It is important that an RSA is not bluntly applied to any development application received for a retail centre. A trigger point for the requirement for an RSA is therefore critical. These trigger

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 16

points will allow for greater developer certainty and a smoother development assessment process.

MacroPlan believes that a more rigorous RSA framework does have a place in the assessment process, however it is not appropriate at all levels of the retail hierarchy. An RSA should not be required for a centre that is developing within the boundaries of an endorsed Centre Structure Plan and should only be required for centres that plan to deliver a significant variation in retail floorspace above the volume endorsed within the Centre Structure Plan.

The figure below outlines recommendations on the trigger point for an RSA for development inconsistent with a Centre Structure Plan.

These triggers are not only applicable for a centre that may be expanding within its designated retail hierarchy; they are also potentially applicable if a centre is proposing to deliver a format of retail floorspace or a volume of retail floorspace that would effectively elevate its role to a new level of the centres hierarchy.

MacroPlan recommends that there are no restrictions on the supply of non-retail floorspace (i.e. office) at the Box Hill CAD or MACs.

Using the figure overleaf as general policy, MacroPlan developed a set of specific actions for the LGA and for a number of key specific centres as outlined in Section 8 of this report with particular focus on potential changes to the Local Planning Scheme in part 8.6 of this report.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 17

Figure 7. Trigger points for a RSA – CADs, MACs and NACs

Source: MacroPlan, 2010

• The Box Hill CAD should expand in line with market need and any endorsed centre structure plan.

• Council should consider how expansions at the existing centre will assist in the achievement of employment growth in Whitehorse

• There should be no retail floorspace or commercial floorspace cap at this level of the hierachy

• Any expansion in retail floorspace by Centro should be supported given the centres co-location to the PPTN and employment

Cen

tral

A

ctiv

itie

s D

istr

ict

•Existing MACs should be required to submit a RSA for any expansion in shop floorspace above 3,000m2 NLA .

•Retail catchments defined in an RSA should preferably be supported by a resident survey.

• The RSA should include elements listed in part 8.2 of this report

•Expansions in retail floorspace at MACs co-located to principal public transport infrastructure (particularly rail) could be supported without a RSA if Council has a policy objective to activate the centre as a Transit Oreinted Development.M

ajo

r A

ctiv

ity

Cen

tres

•An RSA should be submitted for expansions above 2,000m2 or 1,000m2 for an individual shop if a Centre Structure Plan is not in place or does not provide guidance on requirements for additional retail floorspace.

•The expansion should meet the requirements of an RSA outlined in part 8.2 of this report.

•Expansions in retail floorspace at Neighbourhood Centres co-located to public transport infrastructure (particularly rail) could be supported without an RSA at the discretion of Council if activation as a TOD is consistent with Council policy.

• Residential densification around existing NACs should be enhanced to encourage utilisation of existing commercial and social infrastructure.N

eigh

bo

urh

oo

d

Act

ivit

y C

entr

es

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 18

1 Introduction

1.1 Purpose of Study

MacroPlan Australia has been commissioned by the Whitehorse City Council to research, develop and finalise a Retail Strategy for the City of Whitehorse. MacroPlan has also been commissioned to develop the recommendations and guidelines for those policies which are impacted as a result of the Whitehorse Retail Strategy.

A considerable amount of market surveying and research was completed in the initial stages of this study to collect data that guided MacroPlan in the development of the Whitehorse Retail Strategy.

This assessment includes an examination of strategic and statutory planning mechanisms; population and demographics of residents within the Whitehorse LGA; current levels of retail supply and demand; qualitative evaluations of the businesses, consumers and residents; and a detailed development strategy for key centres in the City of Whitehorse.

Included in the project scope is the development of a recommended future retail policy framework that will guide the development of relevant sections of Councils Local Planning Policy Framework (LPPF).

Models used in the report include but are not limited to:

• future population projection analysis,

• employment projection analysis,

• journey to work modelling,

• retail demand and floor space requirement analysis,

• centre catchment and retail expenditure modelling, and

• Centre competitiveness modelling.

1.2 Methodology Overview

An overview of the methodology approach to this retail strategy appears in the figure below.

It depicts how the competitiveness of key retail centres is considered according to a triple bottom line framework with input from primary market research including business consultation and shopper surveys.

Future retail floorspace requirements are assessed subject to a review of population and employment in each centres catchment as well as consideration of incomes and the ability of the centres retailers to retain retail expenditure pools (i.e. what is the centres likely market share).

Policy recommendations are also considered based on any constraints a centre may face in regard to development feasibility, building restrictions; land availability, policy directions etc.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 19

Figure 8. Methodology Overview

1.3 Location and Context

The City of Whitehorse is located in approximately 15km east of the Melbourne CBD and includes the Central Activities District, Box Hill as identified in Melbourne @ 5 million. The city has a population of 151,000 as per 2006 census data and covers an area of 64ksq.m.

As displayed in Figure 9, the municipality is bordered by the Koonung Creek in the north, Dandenong Creek and Heatherdale Road in the east, Highbury Road in the south, and generally Warrigal Road in the west. Surrounding LGA’s include Manningham, Maroondah, Knox, Monash and Boroondara.

Expected future

growth of centre

1. Centre competitiveness

•Economic Influences

•Social Influences

•Environmental Influences

•Calculation of centre competitiveness

2. Retail floorspace requirements

•Population and employment projections

•Retail expenditure pool

•Retail floorspace projections by retail type

3. Consideration of constraints

•Consideration of planning intentions

•Consideration of land constraints and development feasibility

•Revised retail floorspace projections

4. Policy recommendations

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 20

Figure 9. Whitehorse LGA Context Map

Source: MapInfo (2010), MacroPlan (2010)

1.4 Report Structure

This report is divided into the following sections:

Section 1: Introduction

Section 2: Review of Strategic and Statutory Planning Documents

Section 3: Population and Demographics

Section 4: Retail Supply Analysis

Section 5: Qualitative Survey Analysis

Section 6: Retail Demand Analysis

Section 7: Key Activity Centre Analysis

Section 8: Policy Recommendations

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 21

1.5 Information Sources

This report draws on a wide range of information sources as an input to our assessment. These sources include, but are not limited to:

Census of Population and Housing, Australian Bureau of Statistics (2006)

ABS population projections prepared for the Department of Health and Ageing (2008)

Latest trends in population growth using ABS Regional Population (Cat. No. 3218.0)

Household Expenditure Survey, Australian Bureau of Statistics (2003/04)

Population forecasts prepared by I.D. Consulting (2009)

Victoria in Future population projections (2008)

Melbourne 2030 – State Government Strategic Document (2006)

Melbourne @ 5 million - DPCD

1.6 Abbreviations

The following abbreviations are used in this report

ABS Australian Bureau of Statistics

CAD Central Activities District

CBD Central Business District

CCD Census Collection District

CLUE Census of Land Use and Employment

DDS Discount Department Store

GFC Global Financial Crisis

LGA Local Government Area

MAC Major Activity Centre

MTA Main Trade Area

NAC Neighbourhood Activity Centre

PTA Primary Trade Area

RSA Retail Sustainability Assessment

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 22

RTD Retail Turnover Densities

SEIFA Socio-Economic Index For Areas

STA Secondary Trade Area

TBL Triple Bottom Line

TDZ Transport Destination Zones

TOD Transport Orientated Development

1.7 Disclaimer

This study has been prepared by MacroPlan Australia Pty Ltd and is intended for the purpose described in this report and not for any other purpose. The contents of this paper should not be reproduced without the express permission of MacroPlan Australia Pty Ltd.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 23

2 Policy and Literature Review

MacroPlan has assessed the existing planning framework at the state and local level as it relates to centre and retail development within the City of Whitehorse.

In particular, this section reviews the effectiveness of the current Planning Scheme in dealing with the realities of the existing retail hierarchy, including relevant Centre business plans, structure plans and strategies that guide planning scheme objectives.

This section reviews the appropriateness of the existing framework and provides guidance in terms of future centre and retail development across the City of Whitehorse.

2.1 State Planning Policy Framework

Melbourne 2030 and Melbourne @ 5 Million – A Planning Update

Melbourne 2030 sets out the overarching strategic framework for the growth and development of Melbourne and surrounding areas. A key objective of Melbourne 2030 is that designated ‘activity centres’ should be the focus for major change over the next 30 years.

Included within Melbourne 2030 is a hierarchy of activity centres by type, and the intended functions of each type of centre:

Central Activities Districts (CADs – 6 new centres included as a part of Melbourne @ 5 Million)

Principal Activity Centres (PACs)

Major Activity Centres (MACs)

Specialised Activity Centres

Neighbourhood Activity Centres (NACs)

Box Hill was identified through Melbourne @ 5 Million as one of six new Central Activities Districts (in addition to Melbourne CBD) located throughout the Melbourne Metropolitan area. Box Hill was also previously an identified Transit City, and was a focus for State Government investment in projects linked to improving the use of existing public transport in established metropolitan and regional centres.

The objectives for the CADs are that they will provide:

Similar services and functions to central Melbourne, such as commercial, retail, high specialised personal services, entertainment, educations government and tourism;

Significant employment concentrations; and

High quality, well designed living and working urban environments.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 24

These six centres are also recognised as focus areas for State Government planning and investment, and will be expected to cater for CBD-type jobs, with a strong and diverse retail sector. The investment in the new CADs will centre around land assembly, infrastructure development and facilitating private investment

In addition, Whitehorse has four designated Major Activity Centres:

Burwood East, Tally Ho

Burwood Heights

Forest Hill Chase, and

Nunawading/MegaMile

There is also one Specialised Activity Centre located within the City of Whitehorse; Deakin University at Burwood.

Economic Development

The State Planning Policy Framework (SPPF) sets out objectives and policy principles for the development of activity centres and ‘out of centre’ retail and commercial development.

Clause 17.01 provides general directions in regard to the development of activity centres and Clause 17.02 provides directions for the establishment of new businesses.

Clause 17.01 directs that activity centres should be planned to:

Provide a range of shopping facilities in locations which are readily accessible to the community.

Incorporate and integrate a variety of land uses, including retail, office, education, human services, community facilities, recreation, entertainment and residential uses where appropriate.

Provide good accessibility by all available modes of transport (particularly public transport) and safe pedestrian and cycling routes, and to encourage multi-purpose trip making to such centres.

Facilitate ease of pedestrian movement between components of centres, public transport interchanges and parking areas.

Maximise opportunities for the co-location, multiple use and sharing of facilities.

Minimise the effects of commercial development on the amenity of residential and parkland areas, for example as a result of traffic congestion, noise or overshadowing.

Therefore key success factors are accessibility (including by public transport), land use mix and the co-location of uses.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 25

Clause 17.02 of the SPPF directs that commercial facilities should be located in existing or planned activity centres unless they are:

New freestanding commercial developments in new residential areas which have extensive potential for population growth or will accommodate facilities that improve the overall level of accessibility for the community, particularly by public transport.

New convenience shopping facilities to provide for the needs of the local population in new residential areas and within, or immediately adjacent to, existing commercial centres.

Outlets of trade-related goods or services directly serving or ancillary to industry and which have adequate on-site car parking.

The key message from this policy direction is that retail floor space should preferably be located within an activity centre boundary, however in cases where there is growth in demand or access by public transport a new development can be considered.

2.2 Local Planning Policy Framework (LPPF)

The Whitehorse Planning Scheme (the scheme) provides direction on the development of activity centres within the City of Whitehorse.

There are several relevant clauses within this scheme. These components are reviewed as follows.

Clause 21.07 – Economic Development

In regard to retail floor space and activity centres, the planning scheme provides the following overarching directions:

Council will continue to recognise the one billion dollar turnover contribution that Mega Mile contributes to the local economy by developing, managing and promoting the retail strip as one of Melbourne’s largest shopping districts.

Support the creation of vibrant and economically viable activity centres that provide a full range of products and services for residents and businesses.

Instil a corporate approach to the management and development of activity centres through the adoption of business plans for key precincts such as Box Hill, Mitcham, Burwood Heights, Brentford Square, East Burwood Plaza, Blackburn Station, Blackburn South, Mont Albert Village and Wattle Park.

These specific directions for retail floor space are consistent with support for employment and economic development more generally, as outlined in the scheme.

Clause 22.06 – Activity Centres

The role of activity centres in supporting economic growth is recognised by Clause 22.06-1. Key policy intent is stated as follows:

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 26

Within the City of Whitehorse, Box Hill is the nominated Central Activities District, while the Major Activity Centres are Forest Hill, Mega Mile (Nunawading), Burwood Heights and Burwood East – Tally Ho Business Park.

There are also a number of neighbourhood activity centres within the municipality. Each of the City’s seventy-eight centres makes a significant contribution to the City’s economy and plays a role in meeting the needs of the community.

One of the main retail strengths is the Whitehorse Road Mega Mile strip which Council wishes to consolidate its role through appropriate land use and development.

It is essential that these centres provide for appropriate community services and facilities consistent with their role and become a focus for social interaction. It is important to ensure that any new development assists Council’s aim to improve the amenity and visual appearance of each centre.

Council therefore supports the development of each of its activity centres however with the policy caveat that they can contribute to social interaction and improve amenity and visual appearance and accessibility including by sustainable transport modes.

This direction has been considered in this Strategy as part of the recommended directions for each centre, set out as follows:

Whitehorse Road Mega Mile shopping strip

This centre is the primary location in the City for homemaker retailing, supplemented by a significant motor vehicle retailing sector.

Development is of a high-quality design that enhances the streetscape.

New use and development should have regard to the vision and principles of the Nunawading/Mega Mile Major Activity Centre and Mitcham Neighbourhood Activity Centre Structure Plan.

Forest Hill Chase

Forest Hill Chase Shopping Centre continue as part of a Major Activity centre primarily providing convenience and comparison retail facilities, a cinema complex and entertainment facilities.

Burwood Heights

Burwood Heights includes a large vacant strategic development site. It offers a potential to be developed into an activity centre of a form envisaged by Melbourne 2030. A structure plan has been prepared to guide future development and improvement of Burwood Heights.

Neighbourhood Centres

The existing role of the East Burwood Plaza at the corner of Burwood Highway and Blackburn Road in the activity centre hierarchy will be maintained and enhanced.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 27

Large NACs continue to focus on providing convenience retailing with limited comparison retailing for the weekly shopping needs of the local community.

Smaller NACs continue to focus on providing limited convenience retailing.

The renovation of existing buildings and shop fronts, and other works should be encouraged to improve the visual amenity and streetscape of these centres.

Office and residential uses should be encouraged in appropriate centres where the retailing function is declining.

Adjoining NACs provide a supporting role to the Whitehorse Road Mega Mile retail precinct and Major Activity Centre.

New use and development should have regard to the vision and principles of the Nunawading/Mega Mile Major Activity Centre and Mitcham Neighbourhood Activity Centre Structure Plan.

These directions have significant application to the development of higher order retail centres and Neighbourhood Activity Centres (NACs).

In regard to higher order centres such as Nunawading / MegaMile and Forest Hill, their role as retail centres is to be enhanced, particularly in the case of Nunawading / MegaMile which is recognised as a key employer.

NACs that have a relatively higher volume of retail floor space are encouraged to continue to provide weekly and comparison shopping services, whereas smaller neighbourhood centres should supply retail products and services associated with a convenience shopping experience.

In all cases, centres that can build upon and enhance opportunities for social and commercial interaction are encouraged.

2.3 Local Planning Policy Framework – Specific Centres

2.3.1 Box Hill Central Activities District

Box Hill Structure Plan (2007)

As a Central Activities District (CAD), Box Hill will be the focus of a significant proportion of employment growth and public investment.

Box Hill provides a range of existing uses, with multi-modal public transport access and potential for major development. Council's Structure Plan intends to guide future development, improvement and investment of the CAD.

Objectives of the Structure Plan include: increase overall density, pedestrian access, public transport connectivity, minimise urban sprawl and minimise car dependency at Box Hill.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 28

Whitehorse Planning Scheme: Clause 22.07 Box Hill Central Activities District

The planning scheme describes the Box Hill CAD as providing retail, education, office, civic, medical, community service, entertainment, dining and recreational opportunities for the regional population, as well as acting as a hub for local community activities.

To achieve planning scheme directions, eight activity precincts and seven built form precincts were identified in the Box Hill Transit City Activity Centre Structure Plan.

These precincts aim to:

ensure that Box Hill provides accessible, lively and comfortable public spaces that offer diverse opportunities for recreation and social engagement

support walking as the primary means of access in and around Box Hill and encourage most trips of 1km or less to be taken on foot

encourage cycling as a sustainable and healthy means of travel within Box Hill and for trips of up to 5km between the Activity Centre and surrounding areas

encourage significantly increased use of public transport and reduced rates in the use of private vehicular transport for travel to and from the Box Hill Activity Centre

manage vehicular traffic in Box Hill to support choice of travel mode and create transit supportive roads (as defined by the Box Hill Transit City Activity Centre Structure Plan 2007)

ensure that car parking in Box Hill balances access, sustainable transport and land use needs

ensure that Box Hill accommodates a more intensive and diverse range of activities that increase choices and opportunities, support synergies between different uses, encourage use of sustainable transport and complement surrounding areas

Sustainable transport and travel is therefore a key focus of the development of Box Hill. It will be important for Council to consider and monitor how successfully the centre is utilising its public transport assets in promoting access by modes other than private vehicle.

Access for cyclists in and around the centre should be promoted, together with an increased supply of cycle bays. Pedestrian movement can be promoted by further improvements to passive and active surveillance which can be achieved by the delivery of residential development.

2.3.2 Burwood Heights Major Activity Centre

Burwood Heights Activity Centre Structure Plan

Clause 22.13 Burwood Heights MAC

Burwood Heights is acknowledged as a Major Activity Centre with potential to be a significant mixed use activity centre. The development of Burwood Heights should be consistent with the vision and principles developed for the Burwood Heights Structure Plan (see Section 2.3).

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 29

Development should complement the role and function of other activity centres and the range of services currently available at the centre.

Clause 22.14 Former Brickworks Site

The Former Brickworks Site forms part of the Burwood Heights Major Activity Centre. It is identified in the MSS as a strategic redevelopment site. The site is intended to facilitate the staged development of the Burwood Heights MAC. Ultimately the site should support the function of Burwood Heights as a MAC.

Land uses should focus into three mixed use precincts: leisure and lifestyle retail, entertainment and leisure, residential.

Given the focus on leisure and lifestyle, the policy specifies that entertainment uses and higher density residential that meets future housing requirements should be encouraged, while large scale retail and trade supplies and standalone uses should be restricted.

2.3.3 Burwood Village

Burwood Village Neighbourhood Activity Centre Framework Plan

The purpose of the plan is to encourage the transformation of the Burwood Highway corridor into a more attractive urban corridor, improving visual appearance and pedestrian environment.

The Plan focuses on Land use, promoting quality development, activity centre, existing residential and industrial areas and transport. Key considerations include allowing for moderated increases in building heights, providing for additional residential, promoting a renewal of building stock and improving the availability of on-street parking. Furthermore, the plan seeks to ensure new development applications provide an Integrated Transport Plan that ‘rigorously assesses parking needs’.

2.3.4 Nunawading/Mitcham/MegaMile/Blackburn Activity Centres

Nunawading / Mitcham Structure Plans

The purpose of the structure plan is to guide future development of the Nunawading and Mitcham Activity Centres for future planning and enhancement. The structure plan is divided into three precincts of Nunawading, Mitcham and MegaMile.

Nunawading Village is recognised in the structure plans to be in ‘crisis’ with poor building stock and multiple small land ownership making rapid change difficult. The area is acknowledged to require significant reinvestment in its facilities and access.

Mitcham has the benefits of co-location to the MegaMile activity centre and the Mitcham Station. The structure plan notes the potential benefits to arise from opening up the street frontage and allowing shop-top developments to assist in the long term viability of the centre.

MegaMile is understood to have accessibility issues for pedestrian and bikes. Initiative promoted in the structure plan include: upgrading streetscapes and new linkages; improving Nunawading Station; signalisation of pedestrian and car links to Nunawading Village; further public transport

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 30

linkages; extension of bike networks; and, the upgrade and expansion of public spaces at Nunawading Community Centre, Mitcham Village, and Daniel Robertson’s Brickworks.

MegaMile West and Blackburn Activity Centres Urban Design Framework

The purpose of the study is to guide change and development in the study area over the next 15 years, based on environmental, social and economic objectives. The study will investigate the opportunities and constraints of both the MegaMile West and Blackburn Activity Centres.

With regards to MegaMile West, the vision includes an increasing regional role as a bulky goods retailing destination, extending the streetscape in MegaMile east to the west. There is also an increasing focus on private vehicle access and improvement to the pedestrian environment.

Blackburn Neighbourhood Activity Centre will strengthen its role as an urban village focussed around the railway station. The plans vision includes a focus on a mix of retail, office, community and higher density residential.

2.3.5 Blackburn

Blackburn Station Village Business Plan

The business plan provides a road map to enable stakeholders to focus time and energy on the issues that achieve the vision which provides: an agreed consensus of the activity centre; a program of priorities and actions; identification of funding and people needed to deliver the results; a management system that enables coordination and integration of projects and activities; and, regular monitoring and review. Key areas of focus including marketing, physical environment (signage and parking), business development (business kit and service standards) and centre management (funding and performance).

Clause 22.12 Blackburn Station Shopping Centre

Blackburn Shopping Centre is identified in the Planning Scheme to be the preferred destination for local shopping, services and community uses. Council policy seeks to ensure that planning decisions are consistent with both the Blackburn Shopping Centre Business Plan and the Parking Strategy by providing a suitable mix of retail and office uses, enhancing the physical environment as well as appropriately addressing parking demands in the area.

The policy objectives highlight the need to encourage cluster of retail and community services at ground floor on the south of the railway line and office and supporting businesses on the north side of the railway line.

In regards to car parking, the policy aims to ensure that provision is appropriate to the demand generated at the centre. The rates of car parking should follow the guidelines provided in the policy (Table 1).

2.3.6 Neighbourhood Activity Centres

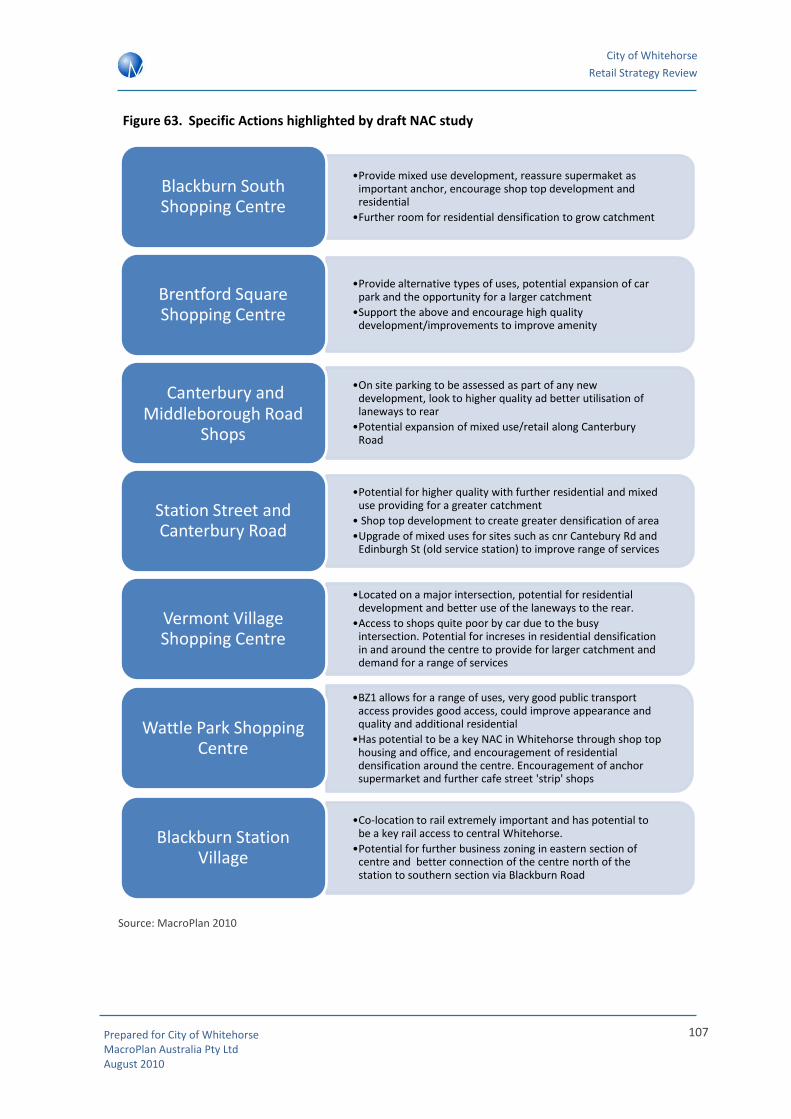

Draft Whitehorse Neighbourhood Activity Centre Study (April 2009)

The aim of this study was to provide a snapshot of the 53 Neighbourhood Activity Centres (NACs) located within the City of Whitehorse. The study identifies the future capacity of each NAC,

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 31

including constraints on development, height controls where required and using this information establishes a strategic framework for the development of NACs within Whitehorse in the future.

The study notes that all 53 centres are zoned Business 1 (B1Z), and at the time were subject to the Design and Development Overlay – Schedule 4 (DDO4), which was an interim control implementing design and built form requirements for the centres, including height limitations. This control has since expired.

The study breaks down the various NACs into the following categories:

Large NACs – up to 10,000m2, including 1 or 2 full-line supermarkets, speciality shops, offices, and community facilities.

Medium NACs – up to 2,500m2, including a small supermarket or grocery store, plus speciality shops.

Small NACs – 100-1,000m2 comprising speciality/convenience shops.

The study also undertook spatial analysis of each of the centres, considering factors that would contribute to future development potential such as demographics, proximity to public transport, open space, educational and community facilities and other land uses. The performance of each centre was then compared to prioritise centres in need for redevelopment or further investigations.

The implementation section of the study recommended introducing permanent Design and Development Overlays for all NACs to provide direction for future development proposals.

This study should be considered in the overall approach taken by Council.

2.3.7 Summary

MacroPlan has assessed the existing planning framework at the state and local level as it relates to centre and retail development within the City of Whitehorse.

The summaries above of relevant planning documents have been used in MacroPlan’s analysis throughout the report and, where appropriate, have been commented on in Section 8 of this report where making future policy recommendations.

In particular, MacroPlan has considered relevant structure plans of key centres studied in Section 7 and the recent Draft Whitehorse Neighbourhood Activity Centre study. At the higher level, MacroPlan has incorporated policy framework recommendations from Melbourne 2030 into activity centre recommendations, particularly at the CAD and MAC level.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 32

3 Stakeholder Consultation

In order to understand the operational and logistical opportunities and constraints for business operators within the City of Whitehorse, MacroPlan has undertaken various forms of consultation with key stakeholders within the community. These stakeholders include local business, residents and shoppers. The four-part process was conducted as follows.

1. Retail Business Surveys – Paper surveys were distributed to a sample local business owners and were comprised of questions pertaining to business operations, the Whitehorse environment and business/retail networks.

2. In-Centre Surveys – Face-to-face, in-centre surveys were conducted at nine shopping centres throughout the Whitehorse LGA. Questions asked pertained to the personal characteristics of the respondent and destination characteristics.

3. Resident Survey – A telephone survey was conducted amongst Whitehorse residents with questions regarding their personal characteristics, preferred centre and the Whitehorse retail destination.

4. Business Association Consultations – To gain a background understanding of the range of views held regarding various centres and issues related to Whitehorse.

It must be noted that while the surveys provide an indication of views relating to retail trading in the Whitehorse LGA, the data may not always represent the general views of the population of businesses or residents in Whitehorse. Due to factors such as the time and location of the surveys, results may slightly vary from the overall view in the municipality.

The issues covered in these surveys have provided MacroPlan with specific indicators that guide the assessment of each activity centre and the degree to which trading needs are currently met and the potential to do so in the future.

The qualitative data from interviews with key stakeholders and surveys has been considered in conjunction with the quantitative data obtained for floor space demand/supply and retail expenditure, as enumerated in Sections 5-6. This multi-pronged approach allows MacroPlan to provide policy recommendations that align with the perceptions and needs of the local workforce, retailers and residents and duly provide a framework for a thriving retail sector.

3.1 Retail Business Surveys

The Business Survey questionnaire was comprised of 19 questions and was completed by 191 businesses throughout the municipality, providing a diverse and fair spread of the views of the business operators. Survey questions can be broken down into the three broad categories of business operations, the Whitehorse environment and business/retail networks, as displayed in the graph below.

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 33

Figure 10. Business Survey Structure

Source: MacroPlan Australia, 2010

Business Operations

MacroPlan has assessed business operations according to the issues that are critical to trading successfully in an activity centre. Learning the financial well-being and sentiment of traders can present alternative information to quantitative data alone and as such, is an invaluable tool in judging the general economic activity within the municipality.

The following summary provides some key business indicators that point to a generally confident but cautious economic environment within the Whitehorse LGA. Key findings include:

14% of businesses are seeking to employ additional staff in the coming six months, while 6.7% said they expect to reduce staff. 79.2% will remain unchanged or are unsure about future staffing requirements. This is generally in line with the nationwide increase in business confidence after the GFC. The net difference between people seeking to employ over the coming months and those who are looking to reduce levels is a positive sign and points to stronger retail trade levels in the municipality.

68.8% of businesses employed 5 or less people, 25.9% employed 5 to 20 people and 5.3% employed more than 20 people. This large amount of very small businesses in the LGA indicates a healthy amount of competition, with the municipality not simply being dominated by larger businesses.

67% stated that their main trading days were during the week, whereas only 33% said the weekend. Businesses in the Box Hill Activity Centre generally had peak activity on weekdays, where as respondents from the more conventional Forest Hill centre had an even split between weekend and weekday trading.

Business / Retail

Networks

Whitehorse Environment

Business Operations

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 34

There was a reasonable spread of trading across the day with 30.7% of businesses saying that their peak trading hours were in the morning, 21.6% at lunch time and 36.6% in the afternoon. Only 11.1% of businesses had peak trading hours at night time.

Many businesses who responded to the survey had been located at their premises for a lengthy period with 65.8% being operational at the current location for more than 5 years, 28.9% for 1 to 5 years and only 5.3% being at the premises for less than a year.

When asked about potential future threats to their business, operators are more concerned about wider economic issues than the local environment, with 32.5% stating that economic conditions was a major threat, 22.9% saying increased business costs, 17.2% saying a lack of trade, 16% noting Parking/traffic issues while new retail developments nearby ranked low at 6%.

Businesses in Whitehorse engage in a range of environmental measures with 30.9% recycling and 19.4% using water efficiency measures.

Whitehorse Trading Environment

MacroPlan’s analysis of the Whitehorse environment explores how businesses feel about the wider operating environment. This may include areas that are outside the businesses direct control but within the control of retail centre owners and different levels of government for the Whitehorse municipality.

Analysis of the wider landscape within which the business operates provides the City of Whitehorse with an indication of sentiment towards the environment in which they operate.

The survey found:

15.2% of businesses who completed the survey were located within the Box Hill Activity Centre. This high amount is representative of the size of the centre and its dominance in the Whitehorse LGA.

Businesses had a wide range of opinions in the attraction of their centre as an operating environment:

o Almost 20% said that expected trading levels was a factor in their choice of location

o 18.6% said that being located close to where they live was an attraction

o Co-location with other retailers was a factor with 12% of businesses, as was the level of rent payable

o Public transport and high pedestrian traffic levels were factors with only a small amount of businesses - rating 11% and 10.3% respectively

Businesses noted the following major issues of operating in their current location:

o 30.6% said parking availability was a major issue

City of Whitehorse

Retail Strategy Review

Prepared for City of Whitehorse MacroPlan Australia Pty Ltd August 2010 35

o 20.2% believed that the lack of trading activity was an issue

o 17.3% believed high rents were a problem with their location

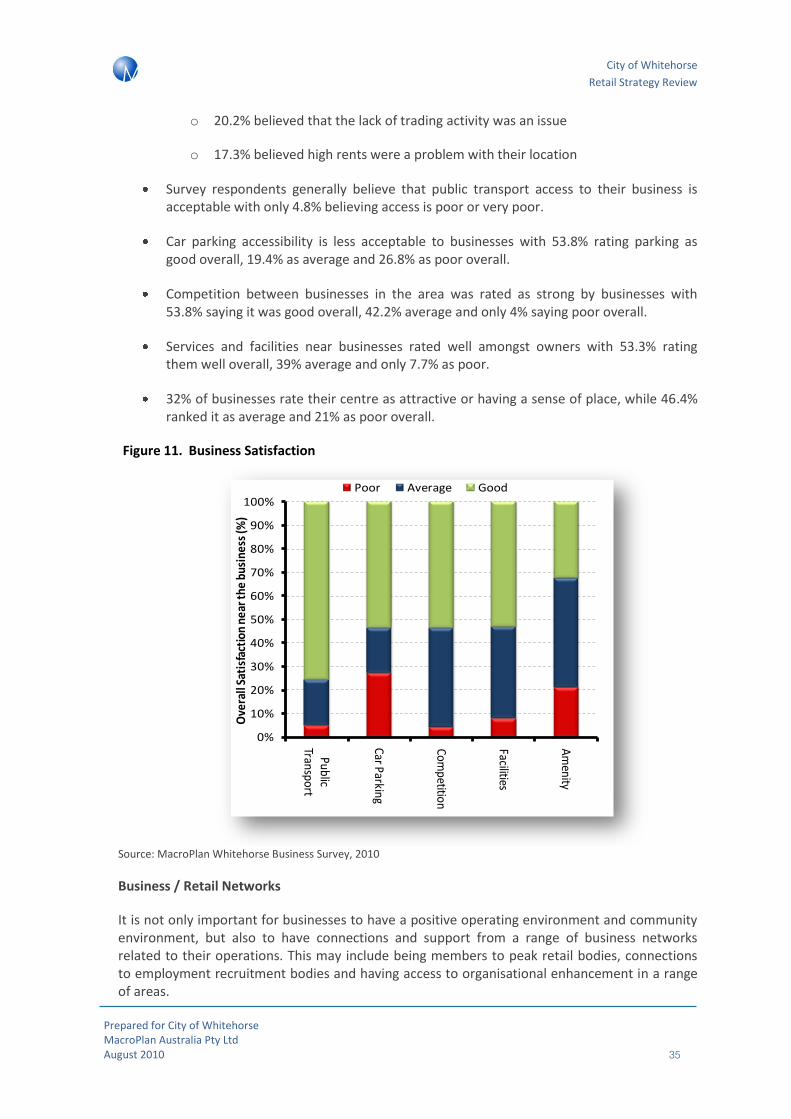

Survey respondents generally believe that public transport access to their business is acceptable with only 4.8% believing access is poor or very poor.

Car parking accessibility is less acceptable to businesses with 53.8% rating parking as good overall, 19.4% as average and 26.8% as poor overall.

Competition between businesses in the area was rated as strong by businesses with 53.8% saying it was good overall, 42.2% average and only 4% saying poor overall.

Services and facilities near businesses rated well amongst owners with 53.3% rating them well overall, 39% average and only 7.7% as poor.

32% of businesses rate their centre as attractive or having a sense of place, while 46.4% ranked it as average and 21% as poor overall.

Figure 11. Business Satisfaction

Source: MacroPlan Whitehorse Business Survey, 2010

Business / Retail Networks

It is not only important for businesses to have a positive operating environment and community environment, but also to have connections and support from a range of business networks related to their operations. This may include being members to peak retail bodies, connections to employment recruitment bodies and having access to organisational enhancement in a range of areas.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Public Transport

Car Parking

Competition

Facilities

Am

enityO

vera

ll Sa

tisf

acti

on n

ear t

he b

usin

ess

(%)

Poor Average Good

City of Whitehorse