retail risk fheili.mohammad

TRANSCRIPT

Mohammad Fheili – [email protected]

Mohammad Fheili “Over 30 years of Experience in Banking. [email protected] (961) 3 337175

Risk & Capacity Building Specialist. Trainer in Risk & Compliance University Lecturer: Economics, Risk, and Banking

Operations Currently serves in the capacity of an Executive (AGM) at

JTB Bank in Lebanon. Served as:

• An Economist at ABL,• Senior Manager at BankMed• Senior Manager & Chief Risk Officer at Group

Fransabank Mohammad received his college education

(undergraduate & graduate) at Louisiana State University(LSU), and has been teaching Economics and Finance forover 25 continuous years at reputable universities in theUSA (LSU) and Lebanon (LAU).

Finally, Mohammad published over 25 articles, of thosemany are in refereed Journals (e.g., Journal of MoneyLaundering & Control; Journal of Operational Risk;Journal of Law & Economics; etc.) and Bulletins.”

Mohammad Fheili – [email protected]

The TruthAbout Retail Banking

• The Customer is at theHeart of Retail Banking

• Knowing the Customer andDriving Profitability ThroughThis knowledge is theLifeblood of Retail Banking.

Mohammad Fheili – [email protected]

However,• Increased Competition• Advent of Technology• Proliferation of Channels to service the Customerhave led to:• Increased Usage of Impersonal Electronic Services: Low Cost Electronic Services;Widespread and Diffused Customer Base. This, in turn led to: Lower Customer Intimacy (How much intimacy can one get out of e‐Banking!).Reduced Switching Costs Between Different Banks (Customers these days are constantly

shopping for the better deal). Increased Chances of Fraud and Credit Risk (Law 318 on Fraud & BDL Basic Circulars 83 –

Regulator’s Version of Law 318, and BDL Intermediate Circular 371 – Compliance Officer at POS, and BDLBasic Circular 81 on Credit Risk – Compared to BDL Basic Circular 58)

Increased the Demand for Transparency (BDL Basic Circular 134; and BCCL Circular 281)• Less Time to Know and Influence Customers.

Research shows that Customer Interest peaks and falls rapidly especially inresponse to a Promotional Event.

This makes it absolutely necessary for banks to optimally leverage all availablecustomer touch points so as to be able to influence the customer (e.g., You find ads andoffers on ATM receipts).

TheTruthA

boutRetail Banking

Mohammad Fheili – [email protected]

Information Technology.

Price/Value Propositions.

Customer Expectations.

Digital Competitors.

What Has Changed?

Retail Banking OrganizationNeeds To Adapt.

Changes

Mohammad Fheili – [email protected]

Information Technology at the forefront of Operational Risk:But ….!

The Introduction of any form of technology in a given production process or the meremodification of an existing IT environment necessitates a number of changes whichspillover on Branch Performance: Staff Skills, Workflows, Policies & Procedures, and ahost of other changes.

In today’s technologically intense productionprocesses, information technology (IT) risks cannot beconsidered independently of other types of risks sinceit reflects on our ability to serve and satisfy our clients. Recognizing these challenges and acknowledging thatthe Branch has a role to play in managing this risk willput management one step ahead. Because processes areTechnology dependent, data collection has changed from being mostly qualitative tooverwhelmingly quantitative; Types/Nature of Mistakes committed by BranchEmployees are Different; etc.

Head of Retail Banking is a Member of the IT Steering Committee,… Or Not!

Information Technology

Mohammad Fheili – [email protected]

SIMPLE! Bricks & Mortals

People Come First

Data Come First

The Risk of Not taking account of that in the Transformation Process. Interfacing with

Clients Delivery Channels Product Features Customer Needs &

Wants Service Proliferation Staff Skill Level

Requirements Agility Etc…

Mohammad Fheili – [email protected]

Changing Customer Expectations and the Power toPunish: Power has shifted to the customer as they become more connected, more demanding and lessloyal.

Instilling the vision and values needed to rebuild trust.

Harnessing big data analytics, social mediamonitoring and other new forms of insight toanticipate and respond proactively to changingcustomer demands. If you don’t Duly respond, some other Banks will;and the Cost of ‘Switching’ is negligent.

How to gain clearer line of sight to customers, speed up decision making andovercome institutional resistance to change.

Shift from product‐push to customer solutions.

Accent on product specialization (‘depth’) gives way to broader engagement,analytical and change management skills (‘Breadth’).

Retail Banking Unit must Anticipate and Respond to Changing Customer Demands!

Customer Expectations

Mohammad Fheili – [email protected]

Digital Competitors and the Age of Innovation:As thepace of innovation accelerates, developments that would have taken years to impact on the market can nowbecome consumer expectations in a matter of days or months.

New competitors have head start on trust. Operational barriers to entry are disappearing as tech‐enabled entrants use digital distribution

and advanced customer profiling to break into the market.

How to create a Business Model that is Flexible enough toreinvent itself when better technologies or potentialpartners come along.

How to lead innovation – even fast following could leave your business marginalized.

How to create an adaptable workforce, unbound by hierarchy, organizationalsiloes or restrictive practices.

The Culture & Practice of Retail Banking is the Backbone of Workforce Agility!

Agility in the Digital Age

It is about the ability to makechoices, decide and act swiftly.

Mohammad Fheili – [email protected]

Equipped to Compete: The most successful businesses are going much further by

re‐engineering their organizations towards new ways of meeting customer demands and opening up new marketopportunities. So is your business up to speed?

Is your thinking radical enough? … Your Customer decides; NOT YOU!

Does your mission embrace the values of the post‐crisisworld?

Does your organizational capability reflect your customers’ changingexpectations?

Do your organizational capabilities reflect the new economicsof your business?

Is your organization ready for change?

Since Branches are the Life‐Line of the Bank, Retail Banking Unit ought to be Responsible for securing Branch Staff Readiness!

Staff Readiness

Mohammad Fheili – [email protected]

Your Life Begins At the End OfYour Comfort Zone

Coping With a Rapidly Changing Banking Environment

Your Life Begins At the End OfYour Comfort Zone

Mohammad Fheili – [email protected]

R.I.S.K.

A Boat in the Harbor is Safe, But That is Not What Boats Were Made For

Mohammad Fheili – [email protected]

Credit Risk

Market Risk

Operational RiskReputational Risk

Business RiskStrategic Risk

. . . Other Risks

Let’s Explore Risk

Stay and Risk

Extinction

Comfort Zon

e

Coping With

Changes

Mohammad Fheili – [email protected]

We’re not advocatingSuicide; You Gear Up andJump.

Risk

Complia

nce

is Straight Forward

YES

NO

Mohammad Fheili – [email protected]

• Most of the Risks Identifiedthroughout the Branch Network areOperational Risks.

• Beware to Look In The RightDirection . . . .

• Operations/Transactions in the HeadOffice are Dramatically Differentfrom Operations in Branches.

• Therefore, the Types and Nature ofRisks Identified in the Head Officeare Significantly different from thosefound in the Branches.

Mohammad Fheili – [email protected]

Retail Banking Division is/has: The Biggest Employer in a Typical

Banking Organization The Most Active Processor of

Transactions (i.e., Traffic) in a TypicalBanking Organization

The Highest Utilization Rate of ITSystems in a Typical BankingOrganization

… there is more

Mohammad Fheili – [email protected]

Operational Risk& BCBS

PRIMARY SECONDARY

PEOPLE

Employee Fraud / Malice (Criminal)

PROCESSES

Payment / settlement / delivery risk

SYSTEMS

Technology investment risk

EXTERNAL

Legal / Regulatory Risk / Public Liability

Unauthorized activity / Employee misdeed (Willful) Employment LawWorkforce disruption Loss or lack of key personnel

Documentation or contract riskValuation / Pricing Internal / External reporting and complianceProject risk / Change management Selling Risks

System development and implementationSystems failuresSystems security breachSystems capacity

Criminal Activities Out‐sourcing / Supplier RiskIn‐sourcing RisksDisaster and Infrastructural utilities FailuresPolitical and Government Risks

There are no right/wronganswers here; only “Acceptable”ones. What is acceptable is verymuch driven by:• People’s risk attitudes and• The Organization’s culture.!

Mohammad Fheili – [email protected]

Operational Risk

& BCBS

Internalfraud

Externalfraud

Employment Practices &Workplace Safety

Clients, Products & Business Practices

Damage to Physical Assets

Business Disruption and systems failures

Execution, Delivery & Process

Management

Corporate Finance

Trading & Sales

Retail Banking

Commercial Banking

Payment & Settlements

Agency ServicesAsset

Management

Retail Brokerage

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Loss Data

Advanced Measurement Approach

Mohammad Fheili – [email protected]

Flying From “Beirut” To “Paris” Is a ‘Service’; Just Like Opening a Saving/Checking Account.Descent Below Safe Altitude is an Incident (With Zero Losses this time). …. BUT . . .

Minimum Safe Altitude (MSA)

IncidentAccident

Operational Risk

Loss Events YOU MUST Report ALL Incidents irrespective of Current Consequences/Impact

Mohammad Fheili – [email protected]

Operational Risk

Decision vs. O

utcomes

Brilliant Surgery!

Well Done!Shame the

patient died.

Do Outcomes Matter?

Mohammad Fheili – [email protected]

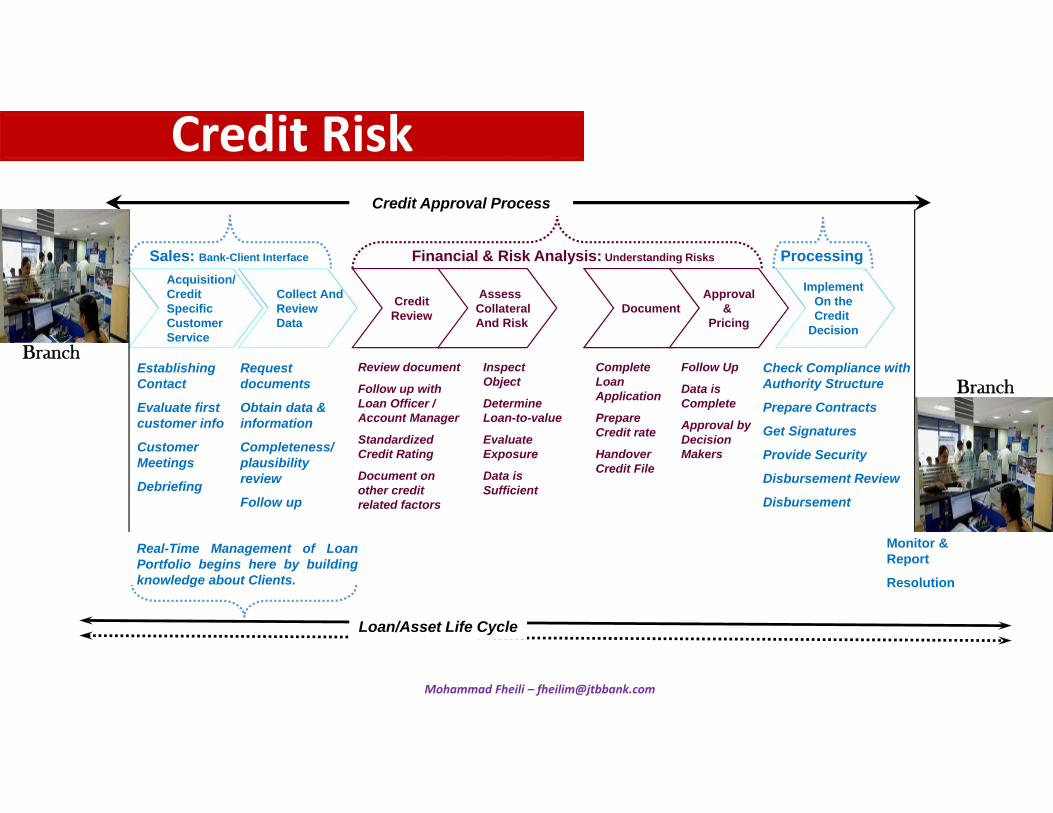

Acquisition/ Credit Specific Customer Service

Collect And Review Data

CreditReview

Assess Collateral And Risk

DocumentApproval

& Pricing

Sales: Bank-Client Interface Financial & Risk Analysis: Understanding Risks Processing

Establishing Contact

Evaluate first customer info

Customer Meetings

Debriefing

Request documents

Obtain data & information

Completeness/ plausibility review

Follow up

Review document

Follow up with Loan Officer / Account Manager

Standardized Credit Rating

Document on other credit related factors

Inspect Object

Determine Loan-to-value

Evaluate Exposure

Data is Sufficient

Complete Loan Application

Prepare Credit rate

Handover Credit File

Follow Up

Data is Complete

Approval by Decision Makers

Check Compliance with Authority Structure

Prepare Contracts

Get Signatures

Provide Security

Disbursement Review

Disbursement

Monitor & Report

Resolution

Loan/Asset Life Cycle

Credit Approval Process

Implement On the Credit

Decision

Real-Time Management of LoanPortfolio begins here by buildingknowledge about Clients.

Credit Risk

Branch

Branch

Mohammad Fheili – [email protected]

Consequences: Losses

Causes:

Risk Event: Loan

Default

• Loan Workout and Recovery

• Recovery is a Function of theQuality of the Credit File and theLegality of AccompanyingDocuments

• Losses (Total or Partial) ofPrincipal and Interests

Dried up Cash Flow Sources: Client’sbusiness received a bad hit.

Collaboration between the Branch Employeeand the Client in the provision of inflatedfigures (Sales, Revenues, Cash Flows, …)leading to a false‐favorable credit decision.

Over‐worked, and Under‐Staffed Branchesleading to overlooking some critical changesin business circumstances of the Client.

Incompetent Branch Manager Gave FalseRecommendation which led to a False‐favorable Credit Decision.

Poor/Inadequate Follow‐up at the Branch,absence of Loan monitoring and Reviewsrendering the process weak in capturing“Warning Signals”

Etc.

How Implicated is Branch Management in Credit Risk?

Now, Do You Think Branch Management

ought to be involved?

Credit Risk

Mohammad Fheili – [email protected]

Banking Model & RiskMAXIMIZE PROFIT subject to:

RISK , REGULATORY, Compliance, Reporting, Etc. Constraints

RISK . . . Default Liquidity Maturity Others . . . REGULATORY . . . Basel I Basel II Basel III Basel IV (In the making)

Sanctions Rules USA_FATCA Requirements

AML, Etc. . . .

Uses of Funds Sources of Funds

Reserves Loans Securities Other

Investments . . .

All Types of Deposits

Borrowings Other

Sources Equity . . .

Off-Balance Sheet

With every Dollar in Service a Typical Bank

Solicits, it MUST satisfy all these Regulatory

Constraints first!VERY COSTLY!

Legal Issues . . .

Who can best help the Bank recover some of the cost of Compliance?Yes, YOU – Branches. You can Increase Traffic:

• More Clients• More Transactions

which can be achieved Through cross‐selling

Follow up Diligently on the settlements of Loans (and ‘Bien Trouvé’, Updated Financials, Site Visits, etc….)

Reduce Loss‐Events. Promote the Bank

through your Social Networks.

Mohammad Fheili – [email protected]

Non‐Com

pliance By Mistake

… Due to lack of

understanding …

Simply Comply

Comply By Fear

AML [Operational] Risk

Mohammad Fheili – [email protected]

Client is Engaged

Compliance Cycle

Service Cycle

st1Client Interface

Interface

End

CIP, KYC

AML Compliance (Regulator Decides)Client Engagement is Constrained by: The Bank isDeemed AML‐Compliance Responsible & Accountable

Customer Satisfaction (Customer Decides)Client Engagement is Driven by: The Potential forRevenue: Interest Income, Commissions & Charges;and a Word‐of‐Mouth Free Marketing

Both Cycles Are Ongoing Processes; None is a Destination

by itself

The Most CriticalCustomer Interface;Manage With Care: YouEither Collect all theneeded information (CIP& KYC), or you haveplanted the seeds ofTroubles to Come . . .

AML [

Operational] Risk

Branch

Mohammad Fheili – [email protected]

CIP, KYCBranch

AML [

Operational] Risk

On Going Monitoring & Compliance

Client is Engaged

Compliance Cycle

Service Cycle

Interface

End

DD, EDD

On Going Follow up & Service

Handling Complaints Cross‐Selling Updating Customer

Profile (CIP), Etc….

Possible RISK: IF “Satisfaction” Ends Up Competing with “Compliance”

End

Customer Risk ScoringCustomer Due Diligence RiskAutomated Transaction Monitoring SystemsCash Aggregation and Reporting Systems,Etc…..

Mohammad Fheili – [email protected]

EmployeeIs Responsible For

Development and career

Supervising OfficerSupports and Challenges To Secure the Attainment

of Organizational Objectives

HR SpecialistProvides Advice, Processes,

Tools, Products

Staff Satisfaction

CustomerSatisfaction

BusinessPerformance

Service Excellence Growth

Feedback Process!

A Matter of Perception!

A Matter of Taste & Preferences!

A Matter of Commitment!

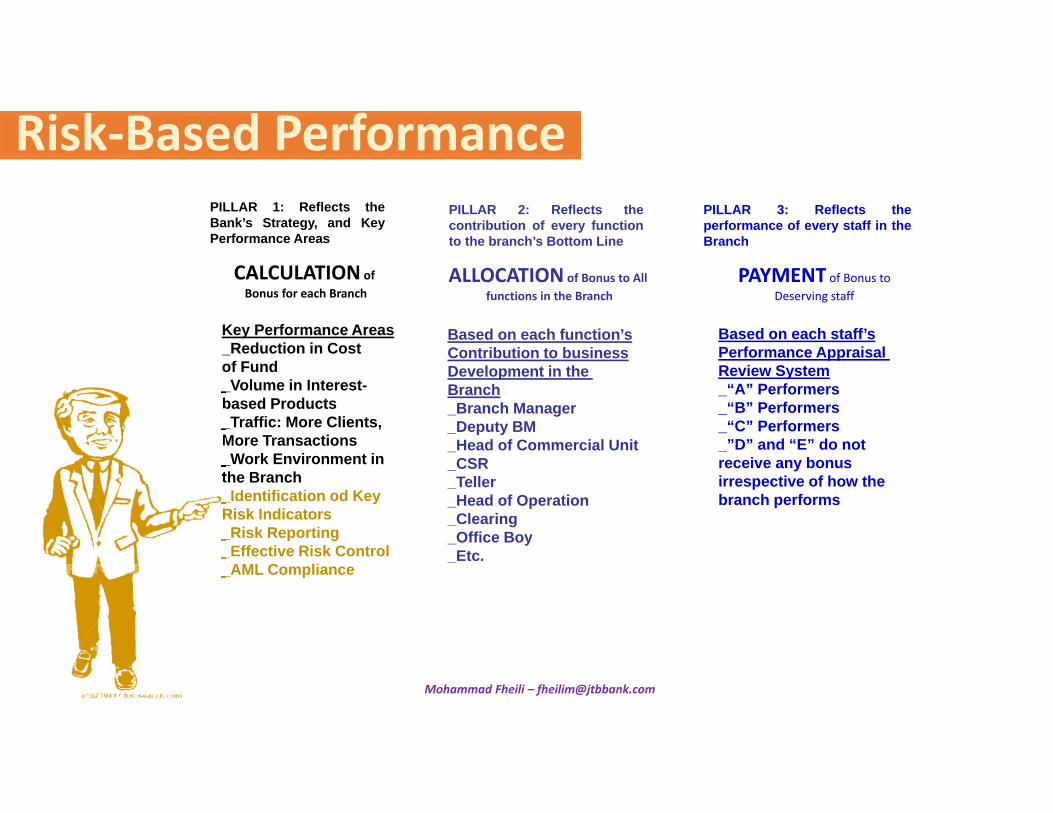

Risk‐Based PerformanceHow Is That

Related To Risk?

Mohammad Fheili – [email protected]

CALCULATIONof Bonus for each Branch

ALLOCATION of Bonus to All functions in the Branch

PAYMENT of Bonus toDeserving staff

Key Performance Areas_Reduction in Costof Fund_Volume in Interest-based Products_Traffic: More Clients,More Transactions_Work Environment inthe Branch_Identification od KeyRisk Indicators_Risk Reporting_Effective Risk Control_AML Compliance

Based on each function’sContribution to businessDevelopment in theBranch_Branch Manager_Deputy BM_Head of Commercial Unit_CSR_Teller_Head of Operation_Clearing_Office Boy_Etc.

Based on each staff’sPerformance Appraisal Review System_“A” Performers_“B” Performers_“C” Performers_”D” and “E” do notreceive any bonus irrespective of how thebranch performs

PILLAR 1: Reflects theBank’s Strategy, and KeyPerformance Areas

PILLAR 2: Reflects thecontribution of every functionto the branch’s Bottom Line

PILLAR 3: Reflects theperformance of every staff in theBranch

30

Risk‐Based Performance

Mohammad Fheili – [email protected]

Employees

Equitable

Sustainable

Bearable

Customers Viable Bank

Risk‐Based Performance

Mohammad Fheili – [email protected]

In Desperate Search for Data to Identify, and Assess Risks

(Intentional & Unintentional) which May Be Encountered By

Employees of the Various Business Units including Branches and . . .

Non‐Identifiable Risk

Non‐Identifiable Risk

Financial Institution’s Risk Population

What is Normally Used in Risk Identification: • CIP• KYC• DD• EDD• Complete Credit File,

EAD, LGD, PD, UL, EL, etc. and Proper Follow Up

• Comprehensive & Consistent Data about the Market

• Etc.

Identified & Identifiable

Risks

Importance of DataInvolve ALL Staff

Mohammad Fheili – [email protected]

Collect them all!

Data

Data

DataData

Data

Data

Data

Data

Data

A Data warehouse is a goodidea, but a warehouse onlyworks when Staff bother tomake deliveries into it –and that’s where BranchStaff need some sharp Inter‐Personal communicationskills, to persuade clients toshare their data. Withoutthe Right/Complete/TimelyData, Risk Decisions areAmbiguous, Ignorant, orUncertain!

Any Piece of Information Will Have Implications On

Success.

Importance of D

ata

All Data is IMPORTANT

Mohammad Fheili – [email protected]

Risk Management Is Everybody’s Business

StaffBranch Staff

Business Unit Branch Mgmt

Senior MgmtBranch Network Division

Assessment & Follow Up

Acceptance or Mitigation of Identified Risks

Follow Up on Decided Actions

Oversight & Control

Reports to Enable Senior Management Appraisal

IdentificationReporting

Registration of Incidents and Monitoring of the

Internal Control Environment

Importance of D

ata

Everybody’s Business

Mohammad Fheili – [email protected]

Increasing Our Understanding of Potential Outcomes

Increa

sing

Evide

nce on

Proba

bility of

occurren

ce

RiskManagement Ambiguity

Unc

erta

inty

Data‐Rich, Information‐Driven Decision‐Making Process: KYC, CIP, DD, EDD, RBA, Etc.. EL, UL, PD, EAD, LGD, Etc… DEaR, VaR, Etc…

Ignorance

A Bank is expected tocollect ALL neededdata to move closer toRisk Management andAway from: Ambiguity, Ignorance, and Uncertainty.

Importance of D

ata

Perception Vs. Reality!

Mohammad Fheili – [email protected]

1 2

34

Your Assignment is to PickOne Animal to take care of,• for One day,• Inside a 25m2 room; and• Alone?You May Ask Any QuestionTo Help You PrepareAdequately For ThisAssignment.

Importance of D

ata

Mohammad Fheili – [email protected]