retail division 2003-2006 strategic plan luca majocchi head of retail division investor day -...

TRANSCRIPT

RETAIL DIVISION

2003-2006 STRATEGIC PLAN

Luca Majocchi Head of Retail Division

Investor Day - Bologna, June 13th 2003

2

AGENDA

Structure of Retail Division

P&L targets

Strategic guidelines & goals

3

THE RETAIL DIVISION COVERS THE ITALIAN MARKET THROUGH A NUMBER OF PRODUCT & CHANNEL SPECIALISTS…

Product specialisation

Retail Division Channel

specialisation

Retail investment products through

captive and non captive

networks

Consumer credit

products through direct

channels, partners and

captive networks

Banking products for households and small business through

proprietary branch network

Mortgages and home related

products through organised

intermediaries (real estate

agents, insurers…)

per la casa

4

…LEVERAGING SKILLS AND FOCUS OF PRODUCT SPECIALISATION AND SCALE AND MARKET POWER OF THE LARGEST DISTRIBUTION NETWORK IN ITALY

Retail Division

Partners(23)

Real estate agents (2500)Third

partiesStock

exchange

Leads Leads

per la casa

Branches(2750)

5

AGENDA

Structure of Retail Division

Strategic guidelines & goals

P&L targets

6

THE ITALIAN RETAIL MARKET WILL SEE GROWING COMPETITION AS MARGIN INCREASE WILL COME FROM MARKET SHARE GAIN RATHER THAN CROSS SELLING

Market

environment

Customers

demand

Competitors

behaviour

Low volume growth due to slow economic recovery

Low interest rates and risk aversion of retail investors affecting deposits and asset management revenues

No one-off revenue stream comparable with asset management and stock trading fees of II H 90’s

Declining satisfaction in the whole industry

No significant effect on customers turnover yet, but share of “potentially mobile” customers growing fastly

Large players focused on carrying out large and complex restructuring processes, with less drive for organic growth

Mid-sized and small players looking for best model to keep local focus and build further efficiency in business processes (where room for improvement is decreasing)

7

UNICREDIT RETAIL DIVISION IS COMMITTED TO GROW AS THE PREFERRED BANK FOR ITALIAN HOUSEHOLDS AND SMALL BUSINESS CUSTOMERS

MISSION

Exploit potential of superior S3 model to become “the largest, local Italian bank”, committed to help households and small businesses “make their life projects real”

STRATEGIC GOALS

To become the preferred bank for Italian retail customers thanks to high quality service and close, personal relationship with clients

To grow revenues faster than market average by increasing market share in all core products line

To remain cost leader in the industry thanks to superior operations, logistics and network management

8

DIVISIONAL REVENUE GROWTH WILL BE DRIVEN BY SUBSTANTIAL INCREASE IN BUSINESS VOLUME, ASSUMING STABLE AVERAGE MARGINS

Revenues

+ 35%

2002 2006

TOP LINE GROWTH 2002-2006Euro bn

4,7

6,4

Total volumes (assets & liabilities)

Margin

2,45%2,45%

193

263

+ 35%

Number of customers

Volume per customer

34 th29 th6,5 mln

7,7 mln

+ 17% + 16%

2002 2006

Deposits & Asset mgmt

Lending

2002 2006

2,18% 2,02% 3,44% 3,59%

2002 2006

= x

- 7% + 4%

9

+ 8.0%

1.9%

1.7%

4.5%

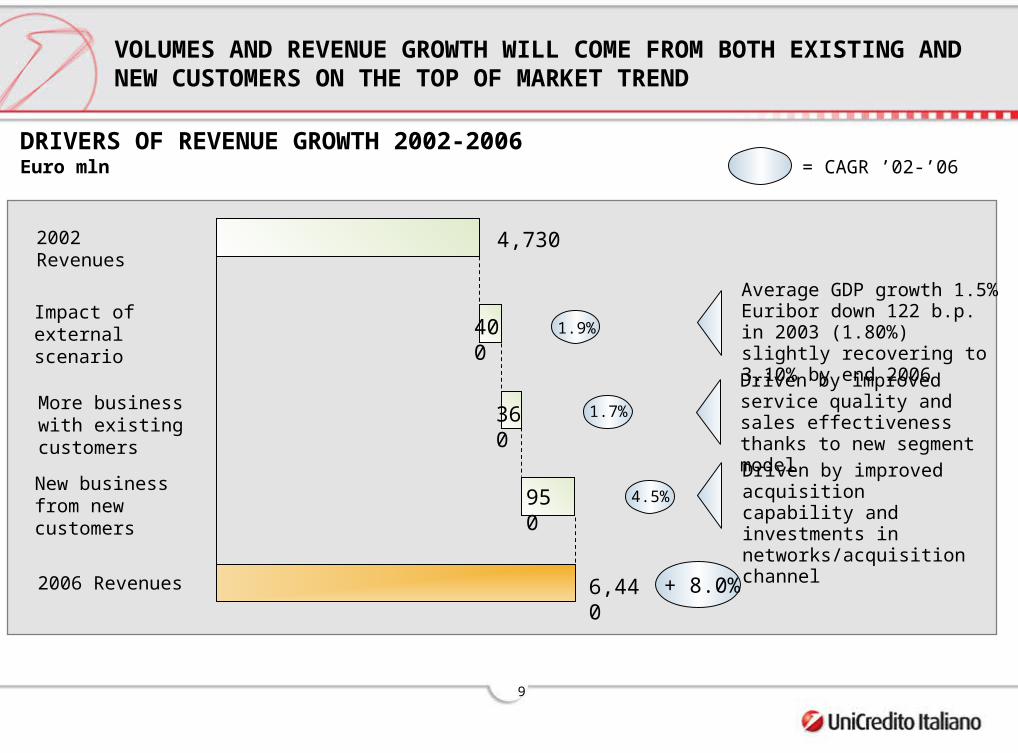

VOLUMES AND REVENUE GROWTH WILL COME FROM BOTH EXISTING AND NEW CUSTOMERS ON THE TOP OF MARKET TREND

Average GDP growth 1.5% Euribor down 122 b.p. in 2003 (1.80%) slightly recovering to 3.10% by end 2006

Driven by improved service quality and sales effectiveness thanks to new segment model

Driven by improved acquisition capability and investments in networks/acquisition channel

DRIVERS OF REVENUE GROWTH 2002-2006Euro mln

2002 Revenues

Impact of external scenario

More business with existing customers

New business from new customers

2006 Revenues

= CAGR ’02-’06

4,730

400

360

950

6,440

10

BUSINESS VOLUMES WILL GROW FASTER THAN MARKET AVERAGE THANKS TO FOCUSED INITIATIVES, MOST OF WHICH ALREADY STARTED

Asset gathering (UniCredit Banca, TradingLab & Pioneer)

Share of wallet increases thanks to new service model for mass affluent

Leverage pension business to grow on existing and new customers

Leverage excellence in product development to expand non captive business in Italy and abroad

> 10%2002

2006+ 10%

> 11%

MARKET SHARE IN KEY PRODUCT AREAS

Households current accounts (UniCredit Banca)

2002

2006

~ 9%

~ 10%

+ 10%

Launch new Genius product line by I Q ‘04

Improved “banking at work” offer

Cross selling on consumer lending (Clarima) and mortgage (UniCredit banca per la casa) customers

11

BUSINESS VOLUMES WILL GROW FASTER THAN MARKET AVERAGE THANKS TO FOCUSED INITIATIVES, SOME OF WHICH ALREADY LAUNCHED

MARKET SHARE IN KEY PRODUCT AREAS (Cont.)

Retail mortgages (UniCredit Banca & Unicredit Banca per la casa)

Consumer lending (Clarima & UniCredit Banca)

2002

2002

2006

2006

Further exploitation of partnership with real estate agents

Opening of specialised branches

Use of CRM to increase cross selling

Aggressive cross selling on captive customers

Scaling up of already proved direct marketing and partnership skills

Development of innovative sales model for credit at PoS

> 12%

> 15%

+ 25%

~ 7,5%

> 9%

+ 20%

Small Business lending (UniCredit Banca)

2002

2006

< 7%

> 8%

+ 20%

Launch new segment-focused Imprendo packages

Strengthening of specialised branches Leverage state of the art credit skills to

grow penetration on existing customers and expand client base

12

GROWTH IN ASSET GATHERING FROM MASS AFFLUENT CUSTOMERS WILL START FROM IMPROVEMENTS IN CURRENT SERVICE MODEL ADDRESSING SOME ISSUES OF CURRENT APPROACHES

MARKET RESEARCH ON MASS AFFLUENT CUSTOMERS

11%

Press

1. Share of wallet growth is closely linked to customer satisfaction due to multi-bank relationships

2. Banks are pushing sales to improve profitability of asset gathering business, harmed by risk aversion of investors and negative performance of stock markets

4. Large size of client portfolios and sales approach focused on cross selling constrains time invested in customer care

Friends/ Colleagues

20%

Self

35%

71%

Bank Total Retail

Mass affluent

68%

59%

Retail customers ask for advice……..

Source of advice when deciding on investments

….but satisfaction is low

Customers satisfied of professional level of advisers

3. Financial markets fall and turbulence brought customers to ask for more time from their account mgr’s

- 13%

13

DEVELOPMENT OF A NEW SERVICE MODEL FOR MASSAFFLUENT SEGMENT IS WELL UNDER WAY AND ALREADY PRODUCING POSITIVE RESULTS

KEY ITEMS OF “NEW” MASS AFFLUENT SERVICE MODEL

1. Differentiated offer and service levels for mass affluent sub-segments (by wallet size and investment behaviour/ preferences)

3. Centralised and improved support to financial advisors to help them to be more effective and save time for customers care

2. Investor care considered as important as cross selling in driving advisors activities

RESULTS TO DATE

1. Review of account portfolios almost completed (2,500 advisors involved)

2. Centralised help desk (60 investments experts) operational since feb ’03 (~ 1,800 calls managed daily)

3. First large scale “investor care campaign” on 120,000 mass affluent customers to be completed by end of June

14

IN FIRST PART OF 2003, S3 ALREADY STARTEDDELIVERING SUPERIOR RESULTS COMPARED TOTHE OLD FEDERAL MODEL

SALES OF HIGH VALUE PRODUCTSJan-May 2003 vs. 2002

Structured bonds

Jan-May 2002

Jan-May 2003

1.4 bn

2.9 bn+109%

Bancassurance single premiums

Jan-May 2002

Jan-May 2003

1.7 bn

2.5 bn+43%

Bancassurance recurring premiums

Jan-May 2002

Jan-May 2003

110 mln

293 mln+166%

share of total insurance sales

6%

10%

15

Geography Italy Italy & core Europe International

REVENUE GROWTH IN RETAIL INVESTMENT SERVICES WILL LEVERAGE TRADINGLAB PRODUCT INNOVATION SKILLS TO FURTHER BROADEN MARKET REACH IN ITALY AND INTERNATIONALLY

TRADINGLAB HISTORY AND STRATEGIC GUIDELINES

Target Self-directed investors

Advice seekers Advice seekers

'98-'00

'

01-'02 '03-'06

Stock markets Stock marketsCaptive networksThird parties

Stock marketsCaptive networksThird partiesSynergy with Pioneer

Distribution channels

Revenues mixMarket making

Origination (Captive)

Origination (Non Captive)

80%

16%

2%

55%

36%

5%

52%

31%

13%

Revenue growth (CAGR)

n.s. -7.4% (’00-’02) >10% (’02-’06)

Products Covered Warrant Covered Warrant Structured Bonds

Covered Warrant Structured Bonds

From leadership in CW to leadership position in retail investment products in Italy

Consolidate leadership in Italy and grow selectively in high potential markets

Company start up as covered warrant specialist

Goal

16

CONSUMER CREDIT GROWTH WILL BE DRIVEN BY CLARIMATHAT, COMPLETED THE START UP PHASE, WILL EXPLOITALL POTENTIAL OF CONSUMER CREDIT FOCUS

~ 120,000 cards to date with share of revolving higher than expected

23 active partnerships generating significant inflows of new customers (> 22,000 in Jan-May ‘03)

Full speed development of direct market activity starting June ‘03

Clarima re-focused on development of whole consumer lending product line (cards, personal loans, consumer credit)

Spin off of existing personal loan business from UCB to Clarima by IIIQ ‘03

Cross selling activity on captive customers under extensive testing, preparing for large scale roll out

CLARIMA STRATEGIC GUIDELINES

17

SMALL BUSINESS LENDING WILL BENEFIT FROMEXCELLENCE IN CREDIT TECHNOLOGY THAT ALREADYPROVED TO BE A KEY DRIVER FOR GROWTH

~ 103,000 customers involved (minimum Credit line 5,000 Euro)

Good credit quality (top three – out of five – performing loan classes)

Results to date

Two out of four months of campaign

Outstanding at 31.01.03

Outstanding at 30.04.03

Target

Campaign Call centre & account rep

contact

Packaged pricing offer linked to new credit product (Credit Più)

Four months time frame starting 01.03.03

1,2 bn

1,4 bn +16%

SMALL BUSINESS “LENDING GROWTH CAMPAIGN”

18

TO BECOME QUALITY LEADER, UCB LAUNCHED ANAMBITIOUS PROJECT IN JUNE 2002 TO BUILD SUPERIORINSTITUTIONAL SKILLS IN CUSTOMER SATISFACTION MANAGEMENT

Project approach

Key findings

1. Use of standard satisfaction measure widely applied in retailing and manufacturing

2. Huge research effort to measure satisfaction at micro-market level

3. Broad change management programme to build institutional skills and empower the front line

Customer satisfaction analysis gives actionable results only when done at micro-market level and vis a vis local competitors

1.

All aspects of human relation prove to be more important than physical and operational factors

2.

3. Effective management of “moments of truth” (sale of “key” products, claims management, …) is crucial for customers satisfaction

4. Substantial improvements can be achieved only by building understanding and commitment at the front line and orchestrating company-wide initiatives sponsored by the top mgmt team

CUSTOMER SATISFACTION INITIATIVE

19

20

30

40

50

60

70

Mar

ket

A

Mar

ket

B

Mar

ket

C

Mar

ket

D

Mar

ket

E

Mar

ket

F

Mar

ket

G

Mar

ket

H

Mar

ket

I

Mar

ket

J

Mar

ket

K

Mar

ket

L

Mar

ket

M

Mar

ket

N

Mar

ket

O

Mar

ket

P

Mar

ket

Q

Competitors’ average

Unicredit Banca

Regional Average

CU

STO

MER

SA

TIS

FAC

TIO

N

IND

EX

Unicredit Banca

Local competitors

CUSTOMER SATISFACTION ANALYSIS AT LOCAL MARKET LEVEL GIVES ACTIONABLE AND SPECIFIC HINTS FOR LOCAL ACTION PLANS FOR CUSTOMER SATISFACTION AND RETENTION

EXAMPLECUSTOMER SATISFACTION DIAGNOSTIC

Local competitorBanca X

Local competitorBanca Y

20

Monthly progress meetings at top mgmt level

Extensive involvement of front line mgmt

Structured action plans at regional level already completed

Company wide projects launched, on operational excellence, claims management, product innovation and employee satisfaction

THE “CUSTOMER SATISFACTION IMPROVEMENTINITIATIVE” ALREADY HAD A DEEP AND WIDESPREADIMPACT ON BANK’S ORGANISATION AND MANAGEMENT FOCUS

CEO

COO

Marketing Sales Operations

Regions

Markets

Branches

Task force created to co-ordinate initiatives and monitor results

Top mgmt team responsible for satisfaction improvement programme

New role, responsible of devising and monitoring local action plans

Key part of the organisation, deeply involved and empowered in customer satisfaction improvement plans

Customer satisfaction

specialists

Customer satisfaction

team

21

14,7%

Branches share

4,9%

Branches Share

UNICREDIT BANCA WILL STRENGTHEN ITS BRANCHNETWORK (ALREADY THE 1ST IN ITALY) FOCUSING ONATTRACTIVE MARKETS WHERE THE BANK HAS (OR CANBUILD) A COMPETITIVE ADVANTAGE

12,3%

Branches share

11,8%

Branches share

15,3%

Branches share

8,5%

Branches share

6,7%

Branches share

2,5%

Branches share

4,8%

Branches share

5 6 5

15 16 16

1015 12

Low Medium High

Low

Medium

Highn. Number of

provinces

Focus

Market attractiveness

UC

B c

ompe

titiv

enes

s

2%

6%

2%

5%

8%

4%

22%

40%

11%

%Share of UCB branches

22

BRANCH NETWORK RATIONALISATION AND EXPANSIONWILL INVOLVE ABOUT ONE FOURTH OF BRANCHES

BRANCH NETWORK IMPROVEMENT PLAN 2002 – 2006Number of branches

Saving of skilled resources to be used to strengthen existing branches/open new ones

Improvements in service quality and sales effectiveness in key customers segments/markets

2002

Closures

Specialisation/Optimisation

Openings

2006

2.753

120

250

430

3.060

~ 9%

+ 16%

+ 11%

- 5%

23

+3.5%

+ 4.5%

+2.0%

-1.0%

VOLUME AND REVENUE GROWTH WILL BE FINANCED BY EFFICIENCY IMPROVEMENT IN EXISTING BUSINESS PROCESSES AND CAREFUL INVESTMENT MANAGEMENT

OPERATING COST DYNAMICS 2002-2006Euro mln

2002 cost base

Impact of inflation

Cost savings initiatives

Cost increase due to new business

2006 cost base

Average inflation 2% Average increase of banking industry personnel cost 1.3%

Rationalisation of existing branch network

Simplification of services/processes

Efficiency in low value activities

Cost increase (+15%) lower than growth of business (+35%)

= CAGR ’02-’06

3,590

3,010

260

-140

460

24

COST OF RISK IS SUPPOSED TO GROW SLIGHTLY IN LINE WITH EXPANSION OF RISKIER (BUT HIGHER MARGIN) BUSINESS LINES

EVOLUTION OF LOANS MIX AND COST OF RISK

Consumer credit

Small business lending

Mortgages

Other

2002Loans

43 bp 49 bp100%=41 bn 100%=72 bn

Net provision/loans

Net provisions /loans

Revolving growing faster than existing personal loan business

Growth on existing and new customers

48 bp

60 bp

29 bp

36 bp

176 bp

66 bp

24 bp

2006Loans

51%

31%

52%

34%

6%8%

3%

15%105 bp

25

AGENDA

Structure of Retail Division

P&L targets

Strategic guidelines & goals

26

DIVISION’S GOAL IS TO GROW REVENUE KEEPING COSTS AND RISKS UNDER CONTROL

High importance

Low importance

Existing customers

New customers

Efficiency Risk mgmtIntra-group synergies

Retail businessPioneerUBI

Corporate businessUCBUPB

Private Banking businessUBMUBI

New EuropePioneerUBMTradingLab

Revenue growth

27

DOUBLE DIGIT OPERATING MARGIN GROWTH WILL BE ACHIEVED BY HEAVILY INVESTING IN NEW BUSINESS, SOME AT LOW MARGINAL COST/INCOME

P&L FORECAST 2002 – 2006Euro mln

Driven by volume growth

Driven by new investments, net of efficiency improvements

Driven by efficiency improvements in UniCredit Banca and low marginal cost/income in Clarima and in TradingLab

2002 2006 CAGR

Operating costs & depreciation

3,010 3,590 4.5%

Revenues 4,730 6,440 8.0%

Operating margin 1,720 2,850 13.5%

Cost / income ratio 64% 56%

Rarorac 16% 20%

28

IN SUMMARY...

The Italian retail market will see growing competition for market share, key driver of future top line growth

UniCredit will leverage its superior organisational model and business focus to gain market share on existing and new clients and become the preferred bank for Italian retail customers

Double digit operating margin growth will be driven by consistent execution of a growth plan, leveraging skills acquired over the last 3-5 years at all levels of the organisation