result presentation q4 and full year 2014

TRANSCRIPT

© Wärtsilä

WÄRTSILÄ CORPORATIONRESULT PRESENTATION 2014

29 JANUARY 2015Björn Rosengren,President & CEO

• Order intake EUR 5,084 million, +5%• Net sales EUR 4,779 million, +4%• Book-to-bill 1.06 (1.05)• EBIT EUR 569 million, 11.9% of net sales

(EUR 557 million or 12.1%)• EPS EUR 1.76 (1.98)• DPS proposal EUR 1.15• Acquisition of L-3 Marine Systems International

announced in December 2014• Joint venture for 2-stroke engine business

finalised in January 2015

EBIT is shown excluding non-recurring items.As of the third quarter of 2014, the two-stroke business is reported as discontinued operations. Income statement related comparison figures for 2013 have been restated.

Highlights 2014 – good performance in challenging markets

2 © Wärtsilä

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

Q4/2013 Q4/2014

14%

23%

23%

-2%

1,334

MEUR

Fourth quarter developmentMEUR

3

Order intake growth supported by Ship Power & Services

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

2010 2011 2012 2013 2014

1,522

Q1-Q3 Q4

Power Plants

Ship Power

Services

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

Q4/2013 Q4/2014

Net sales in line with our expectations

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2010 2011 2012 2013 2014

10%

11%

30%

-8%

1,403

MEUR

Fourth quarter developmentMEUR

1,549

4

Net sales in line with expectations

Power Plants

Ship Power

Services

Q1-Q3 Q4

© Wärtsilä

Net sales by business 1-3/2012

Ship Power36% (28)

Power Plants24% (32)

Services41% (40)

5

Net sales by business 2014

© Wärtsilä

0.88

1.07 1.05 1.05 1.06

0,0

0,2

0,4

0,6

0,8

1,0

1,2

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

2010 2011 2012 2013 2014

Order intake Net sales Book-to-bill

MEUR

6

Book-to-bill ratio remains above one

© Wärtsilä

Order book distribution

MEUR

7

Order book distribution

0

500

1000

1500

2000

2500

3000

3500

31.12.2013 31.12.2014

Delivery next year Delivery after next year

© Wärtsilä

MEUR

8

Profitability at upper end of guidance range

EBIT% before non-recurring itemsEBIT before non-recurring items

10.7% 11.1% 10.9% 11.2%11.9%

0%

2%

4%

6%

8%

10%

12%

14%

0

100

200

300

400

500

600

2010 2011 2012 2013 2014

2014 EBIT and EBIT% include continuing operations. Figures for 2010-2013 include both discontinued and continuing operations.

© Wärtsilä9

Power plant market activity improved in the second half

© Wärtsilä10

Power Plants quotations strong in 2014

0

2000

4000

6000

8000

10000

12000

14000

16000

18000Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MW

Quoted MW per Fuel Type

Others

Natural gas

Heavy fuel oil

70% of quotations for gas based installations

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

1800

2010 2011 2012 2013 2014

MEUR Review period developmentTotal EUR 1,293 million (1,292)

IPP’s*

Utilities

Industrials

Oil 39%

Gas61%

Review period order intake by fuel in MW

x%

11

Power Plants order intake stable despite challenges

33%

32%

35%

Q1-Q3 Q4

*IPP = Independent Power Producer

© Wärtsilä

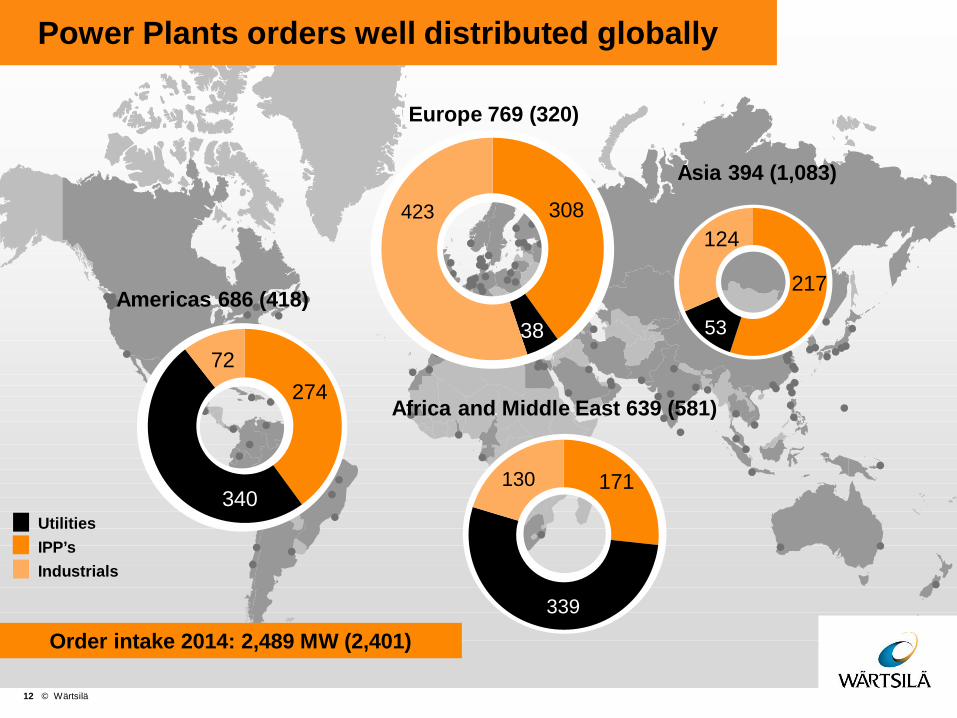

308

38

217

124

171130

Order intake 2014: 2,489 MW (2,401)

Americas 686 (418)

Asia 394 (1,083)

Africa and Middle East 639 (581)

UtilitiesIPP’sIndustrials

12

Power Plants orders well distributed globally

423

339

53

Europe 769 (320)

340

72274

© Wärtsilä

• Order placed by EUROCEMENT group• Scope of supply: 36 natural gas-fired Wärtsilä

34SG engines with a combined capacity of314 MW

• The plants will produce electricity for cement factories and work in parallel with the grid

• Wärtsilä’s total installed power generation capacity in Russia is approximately 1,000 MW

13

Orders for 11 industrial power plants from Russia

© Wärtsilä1414

12.7%55.2%

14.5%

1.8%

Market <500MW16.5 GW (27)

10.5%

3.6%

14

Market data includes all Wärtsilä power plants and other manufacturers’ gas and liquid fuelled turbine based power plants with prime movers above 5 MW, as well as estimated output of steam turbines for combined cycles. The data is gathered from the McCoy Power Report.Other combustion engines not included. In engine technology Wärtsilä has a leading position.

1.8%

Total market37.7 GW (38)

GE Siemens MHI WärtsiläAlstom Ansaldo Other GTs

26.3%

48.0%9.8%

5.0%

9.0%

1.6%0.8%

Market for gas and liquid fuel based power plants 1-9/2014

© Wärtsilä15

Ship Power order intake supported by activity in gas carriers and cruise vessels

© Wärtsilä16

Slowdown in vessel contracting

Source: Clarkson Research Services, figures exclude late contracting* CGT= gross tonnage compensated with workload

*

*

0

1

2

3

4

5

0

50

100

150

200

250

01.0

903

.09

05.0

907

.09

09.0

911

.09

01.1

003

.10

05.1

007

.10

09.1

011

.10

01.1

103

.11

05.1

107

.11

09.1

111

.11

01.1

203

.12

05.1

207

.12

09.1

211

.12

01.1

303

.13

05.1

307

.13

09.1

311

.13

01.1

403

.14

05.1

407

.14

09.1

411

.14

Mill

ion

CG

T

# of

ves

sels

Merchant Offshore Cruise and Ferry Special vessels 3 months moving average in CGT

© Wärtsilä

0

300

600

900

1200

1500

1800

2010 2011 2012 2013 2014

MEUR

Review period developmentTotal EUR 1,746 million (1,644)

Offshore28%

Traditional merchant

10%

Special vessels6%

17

6% growth in Ship Power order intake

Others 2%

Q1-Q3 Q4

Gas carriers34%

Cruise & Ferry16%

Navy 4%

© Wärtsilä

• Joint venture order intake totalledEUR 306 million (222) during January-December 2014

• In November Wärtsilä Hyundai Engine Company Ltd. received a major order to supply 54 dual-fuel engines for arctic LNG carriers for the Yamal project in Russia

MEUR

Ship Power order intake

Joint venture order intake, includes figures from Wärtsilä Hyundai Engine Company Ltd. and Wärtsilä Qiyao Diesel Company Ltd.

18

Joint venture ordering activity

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

Q1/2010

Q2/2010

Q3/2010

Q4/2010

Q1/2011

Q2/2011

Q3/2011

Q4/2011

Q1/2012

Q2/2012

Q3/2012

Q4/2012

Q1/2013

Q2/2013

Q3/2013

Q4/2013

Q1/2014

Q2/2014

Q3/2014

Q4/2014

Wärtsilä’s share of ownership in these companies is 50%, and the results are reported as a share of result of associates and joint ventures

© Wärtsilä

• Order received for 6 integrated solutions to Anchor Handling Tug Supply vessels, being built for Maersk Supply Service A/S

• Scope of supply: complete power generation solution, electrical distribution and drives, vessel automation and propulsion

• The fully integrated systems will provide optimal power, efficiency, versatility and redundancy, with the lowest operating expenditures and a minimal environmental impact

19

Orders for integrated solutions increasing

© Wärtsilä

Ship Power order book 31 December 2014

Offshore35%

Specialvessels

4%Navy

8%

Cruise & Ferry12%

Gas carriers24%

Non-vessel4%

Tankers4%

RoRo4%

Other merchant2%

Cargo1%

20

© Wärtsilä

Wärtsilä’s market shares are calculated on a 12 months rolling basis, numbers in brackets are from the end of the previous quarter. The calculation is based on Wärtsilä’s own data portal.

Wärtsilä52%(51)

Others 5%(21)

MAN D&T25%(17)

Caterpillar17%(11)

Total market volume last 12 months:4,484 MW (4,554)

Medium-speed main enginesWärtsilä3%(2)

Auxiliary engines

Total market volume last 12 months:6,682 MW (7,628)

Others97%(98)

21

Strong position in marine engine market

© Wärtsilä22

Wärtsilä strengthens its position in automation and electrical systems

• L-3 MSI is a global supplier of automation, navigation and electrical systems to the marine, naval and offshore markets

• Transaction value EUR 285 million (enterprise value), subject to customary adjustments

• Financing for the deal will be from existing cash resources and credit facilities

• The acquisition is subject to clearance from the regulatory authorities, and is expected to be closed during the second quarter of 2015

• The acquisition is expected to be EPS accretive as of 2015

© Wärtsilä23

Growth in service demand

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2010 2011 2012 2013 2014

-3%

0

100

200

300

400

500

600

Q4/2013 Q4/2014

MEUR

Fourth quarter development

MEUR

507

11%564

0%

24

All-time high fourth quarter supported Services sales growth

5%

Q1-Q3 Q4

5%

© Wärtsilä

Spare parts 51%(49)

Field service 25%(26)

Contracts 16%(16)

Projects9%(8)

25

Total EUR 1,939 million (1,842)

Services net sales distribution 2014

© Wärtsilä26

Services distribution per business 2014

Net salesTotal EUR 1,939 million

ShipPower

Installed baseTotal 181,000 MW

PowerPlants

PowerPlants

Ship Power 2-stroke

Ship Power 4-stroke

© Wärtsilä

• Service contracts bring flexibility to operations through optimisedmaintenance planning

• Several agreements signed during 2014 in various vessel segments, including:– 10-year maintenance and technical support

agreement with Royal Caribbean Cruises Ltd covering 36 vessels

– 3-year service agreement with Dutch dredging and marine contractor Van Oord

– 5-year technical maintenance agreement with three Greek LNG carrier owners for a total of 15 vessels

– 6-year maintenance agreement for 15 of Wagenborg’s dry cargo carriers

27

Growing interest in marine service agreements

© Wärtsilä28

Development of service agreements

MW

0%

5%

10%

15%

20%

25%

30%

0

2000

4000

6000

8000

10000

12000

14000

2009 2010 2011 2012 2013 2014

MW under agreement – Power Plants MW under agreement – Ship Power

% of Ship Power installed base% of Power Plants installed base

© Wärtsilä

Fleet utilisation

* Source Bloomberg. Sample of more than 25 000 vessels (>299 GT) covered by IHS AIS Live.** Source Bloomberg

29

Fleet utilisation

Fleet Average Speed, knots**

Anchored Vessels & Fleet Development*

8,0

8,5

9,0

9,5

10,0

10,5

07.12

10.12

01.13

04.13

07.13

10.13

01.14

04.14

07.14

10.14

01.1520500

21000

21500

22000

22500

23000

15%

20%

25%

30%

35%

07.12

10.12

01.13

04.13

07.13

10.13

01.14

04.14

07.14

10.14

01.15

Nr o

f A

ctiv

e V

esse

ls

Per

cent

Anc

hore

d

Anchored Active Fleet

© Wärtsilä30

Solid financial standing

© Wärtsilä31

Cash flow from operating activities

0

100

200

300

400

500

600

700

2010 2011 2012 2013 2014

MEUR

© Wärtsilä

118

235

465

313251

2.6%

5.6%

9.8%

6.8%

5.2%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1000

1200

1400

1600

2010 2011 2012 2013 2014

Working capital Total inventories Advances received Working capital / Net sales

MEUR

32

Working capital developed well

© Wärtsilä33

Gearing remains low

-0,10

0,00

0,10

0,20

0,30

0,40

0,50

2010 2011 2012 2013 2014

© Wärtsilä34

0,00

0,50

1,00

1,50

2,00

2,50

EPS Dividend Extra dividend

EUR

2010 2011 2012

*Dividend 2014 - Proposal of the Board

2013 2014*

EPS and dividend per share

1.76

1.15

© Wärtsilä

• Power Plants: The overall market for liquid and gas fuelled power generation is expected to continue to be challenging. Ordering activity remains focused on emerging markets and countries benefiting from a stronger US dollar.

• Ship Power: The outlook for shipping and shipbuilding is cautious, due to the current uncertainties in the market. Low oil prices are expected to limit the demand for offshore vessels. The outlook for gas carriers continues to be positive. The importance of fuel efficiency and environmental regulations are clearly visible, driving interest in environmental solutions and gas as a marine fuel for the broader marine markets.

• Services: The overall service market outlook remains stable. The service outlook for offshore and gas fuelled vessels remains favourable. Demand for services in the power plant segment continues to be good. Marine and power plant customers show healthy interest in long-term service agreements.

35

Market outlook

© Wärtsilä36

Wärtsilä expects its net sales for 2015 to grow by 0-10% and its operational profitability (EBIT% before non-recurring items) to be between 12.0-12.5%.

Prospects for 2015

IR Contact:Natalia ValtasaariDirector, Investor Relations Tel. +358 (0) 40 187 7809E-mail: [email protected]