respa: update and best practices ruth a. dillingham, esq. first american title insurance co

TRANSCRIPT

RESPA:Update and Best Practices

Ruth A. Dillingham, Esq.First American Title Insurance Co.

Real Estate Settlement Procedures Act (RESPA)

Became law (RESPA) 1975Regulator-U.S. Department of Housing and

Urban Development (HUD) Regulation X

Re-Issued 1996; amended 2008Enforced by HUDIntent:

Help consumers better shop for settlement services Eliminate increases in costs of settlement services

2

Covered Transactions

• Mortgage loans secured by:• First or subordinate mortgage: including

– Refinances– Assumptions (where lender permission needed)– Home Equity Loans

• Residential property• One- to four-family

– Including condos and coops• Reverse Mortgage• Made by a ‘creditor’ (TILA)

3

Transactions NOT Covered• Primarily for:

– Business– Commercial – Agricultural purpose (TILA)

• 25 acres or more• Vacant Land• Temporary/Construction loan

– Unless loan converts to permanent or made to first user of constructed improvement

• No ‘Creditor’– Cash sale– Seller financing

4

Sections of the Act/Regulation

• Section 4- Settlement Statement– 3500.8-12 HUD-1 Form

• Section 5- Information Booklets & GFE– 3500.6-7 GFE and Settlement Charges

Booklet• Section 6/10- Servicing Issues

– 3500.21 Transfers of Servicing – 3500.17 Escrow Accounts

• Section 8- Kickbacks and Unearned Fees– 3500.14-Prohibited Payments– 3500.15-Affiliated Business Arrangements

5

Required Disclosures

RESPA requires that borrower receive different disclosures at various times:

• When loan application is made• At settlement• After settlement

6

Disclosures at Loan Application

Borrower must receive:– Special Information Booklet– Good Faith Estimate (GFE) of Settlement

Costs– Mortgage Servicing Disclosure Statement

If the borrowers do not get these documents at time of application, lender must mail them within 3 business days of receiving the applicationAffiliated Business Arrangement (AfBA)

Disclosure

7

Disclosures at SettlementHUD-1 Settlement Statement

Shows actual settlement costs of transaction

Initial Escrow Statement Itemizes estimated taxes, insurance

premiums, and other charges anticipated to be paid from escrow account during first 12 months of the loan.

8

Disclosures After Settlement

Annual Escrow Statement− Summarizes all escrow account

deposits and payments during the servicer’s 12-month computation year

Servicing Transfer Statement− Required if the loan servicer sells or

assigns the servicing rights to a borrower’s loan to another loan servicer

9

RESPA Rule Effective Dates

January 1, 2010All residential real estate loans get new

GFEAll loans with new GFE must close with

new HUD -1New Rules for:

Cost Disclosures Vendor Relationships

10

New GFE- “Application”

• Name• Social Security Number• Loan Amount• Property Value• Monthly Income• Property Address

• No charge to the consumer prior to receipt except Credit Report

• Can’t substitute ‘worksheet’ instead

11

New Disclosures - Timing

Within 3 days of application:GFETIL HUD Settlement Cost BookletList of Providers:

If do not allow borrower to shop• No list• All have 10 % tolerance (in the aggregate)

If do allow borrower to shop• Must provide list of Providers which• Contains one 10% tolerance provider for those

services

12

Truth in Lending/RESPA: The New Timelines

Sunday Monday Tuesday Wednesday Thursday Friday Saturday

1Application is Made

2^1

3

4 5^2

6^3Must Mail TIL/GFE

7*1

8*2

9*3TIL/GFE is “received”

10*4OK to collect fees

11 12*5

13*6

14*7

Earliest Date Loan can Close

15*8

16*9

17*10

GFE terms expire

13This lender is closed for general business purposes on Saturday

GFE Page 1

Interest Rate DateOther Fees DateRate Lock DateRate Lock-in Date

Summary of Loan Terms

Summary of Loan Costs

14

GFE Page 2

Loan Origination Charges-No Increase

Lender Costs-Most Capped (10%)

Other Costs-Some Capped

(10%)Some UnlimitedDepends on who

selects provider

15

This slide is for purposes of Notes View ONLY

the text is a continuation of that used for the previous

slide

16

GFE Page 3

Explanation-Grouping of

Costs

Trade-off Table

Shopping Chart

17

Zero Tolerance

• Lender charges for– Taking– Underwriting– Processing the application

• Points or origination fees (including yield spread premium)

• Real property transfer tax– Is state specific-statutory

18

10% Increase Permitted

• Total (aggregate) all charges– Lender required settlement services

• Where lender selects provider– Lender required settlement services

• Where borrower selects provider from lender’s list

– Title services and title insurance• Where lender selects the provider

– Title services and title insurance• Where borrower selects provider from

lender’s list– Recording fees

19

Unlimited Change Permitted

• Services where borrower selects provider– Including title and title insurance

• Escrow account amounts• Per diem interest• Homeowners insuranceFinal page of the GFE also contains

worksheet- like charts to compare different loans and terms

20

New GFE - Impact

All charges Except for

• Interest rate • Charges related to the interest rate• Per diem interest

When the rate is not locked

Must be available for at least 10 business days after the issuance of the GFE

21

Not bound by GFE?

Changed Circumstances affecting settlement costs

Changed Circumstances affecting loan

Borrower Request

GFE Expires

Interest Rate locked

22

New GFE?

Changed Circumstances: Acts of God Inaccurate Information used to prepare

the GFE New Information not relied on to prepare

the GFE Particular Information regarding the

transaction (ie- ‘boundary line disputes’)

23

If New GFE

Within 3 business days of new informationOnly increase fees that reflect the new

informationRetain documentation establishing

change for 3 years Both lender and broker

24

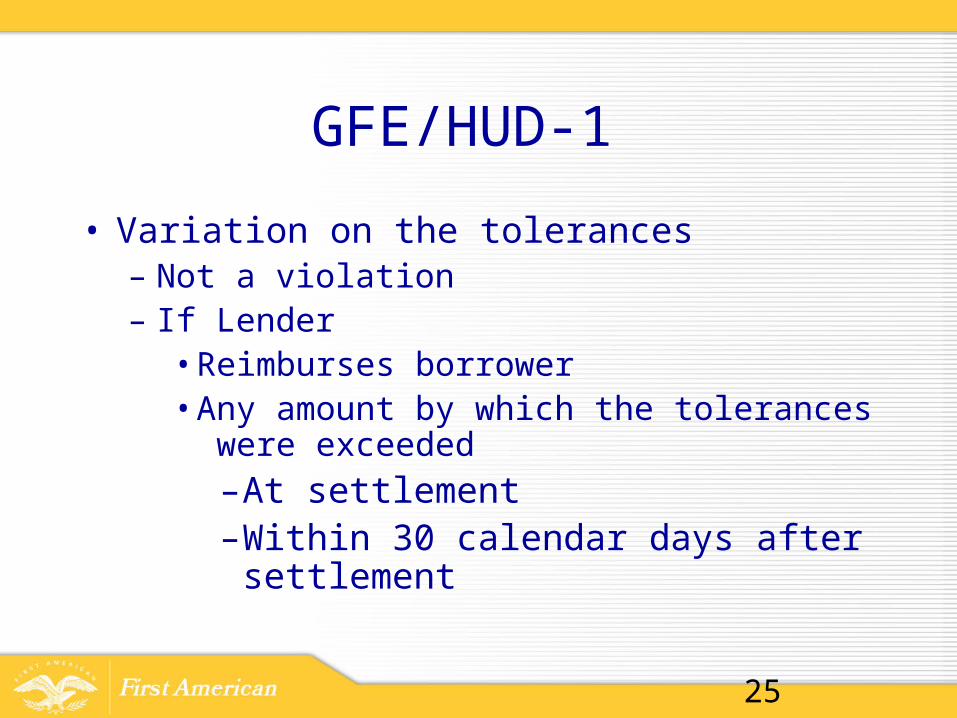

GFE/HUD-1

• Variation on the tolerances– Not a violation– If Lender

•Reimburses borrower•Any amount by which the tolerances

were exceeded–At settlement–Within 30 calendar days after

settlement

25

In Practice?

What to do with a borrower who is “just shopping?” pre-approvals?

How to confirm the borrower has/has not “expressed intent to continue with application?”

What do you do to show all costs? 1003; your internal forms?

When is a list of providers, not a ‘list’?

New HUD-1

• Page 1- No Major Changes• Page 2- Aligns GFE with HUD• Page 3- Comparison of GFE with HUD• If differences-

– Lender must make revisions– Lender must reimburse borrower– Lender cannot change GFE unless

• Borrower Request• “Changed Circumstances”

27

HUD-1 Page 1

Add settlement agent phone number

Adjustments-

Buyer/Seller

No longer Seller

costs on Page 2

Deposits

Summary of Costs

28

29

30

HUD-1 Page 2

Broker Commissions-700’s

Lender Charges- 800’s Origination Costs 3rd Party Costs

Prepaids/Escrows-900/1000

Closing Attorney/Title Insurance Fees- 1100’s

Recording Fees- 1200’s Other Fees- 1300’s

31

32

This slide is for purposes of Notes View ONLY

the text is a continuation of that used for the previous

slide

33

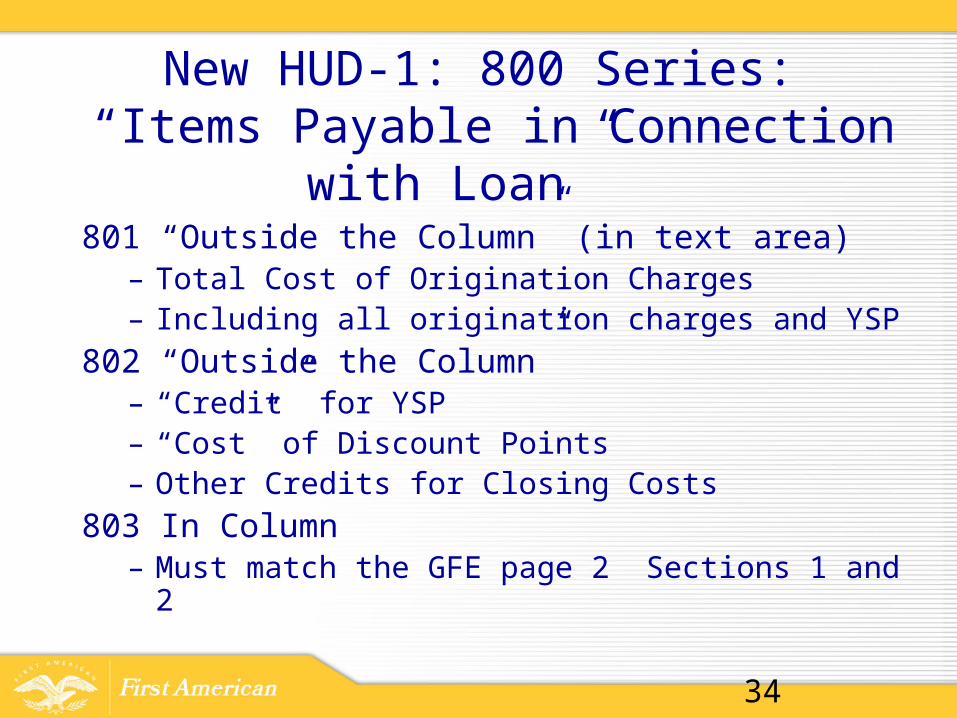

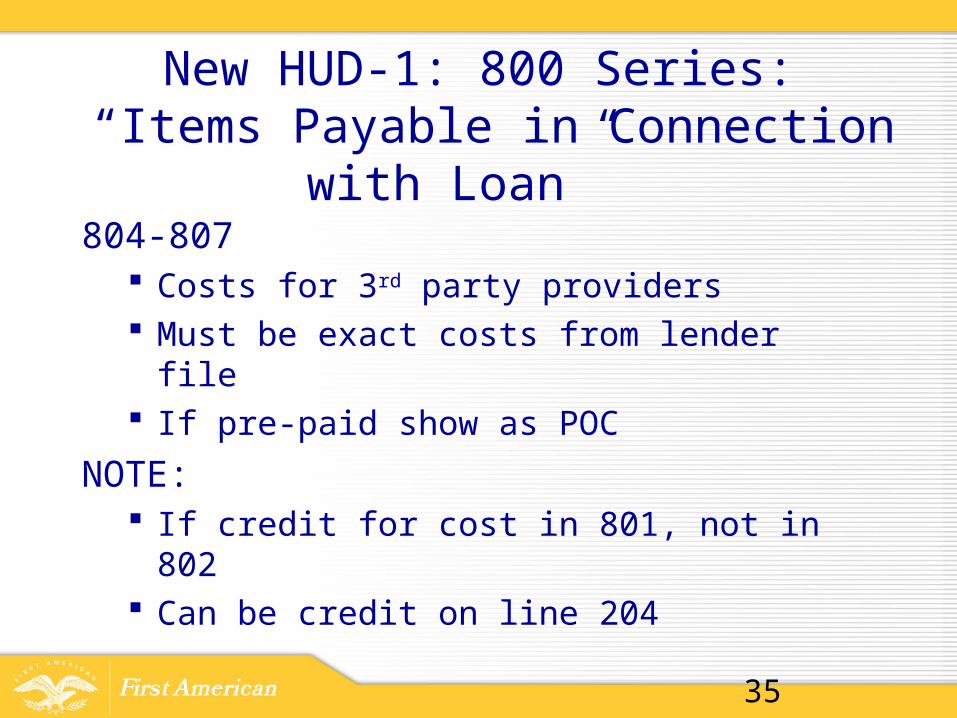

New HUD-1: 800 Series: “Items Payable in Connection with

Loan” 801 “Outside the Column” (in text area)

– Total Cost of Origination Charges– Including all origination charges and YSP

802 “Outside the Column”– “Credit” for YSP– “Cost” of Discount Points– Other Credits for Closing Costs

803 In Column– Must match the GFE page 2 Sections 1 and 2

34

New HUD-1: 800 Series: “Items Payable in Connection with

Loan” 804-807

Costs for 3rd party providers Must be exact costs from lender file If pre-paid show as POC

NOTE: If credit for cost in 801, not in 802 Can be credit on line 204

35

36

This slide is for purposes of Notes View ONLY

the text is a continuation of that used for the previous

slide

37

New 1101

• Total of all charges formerly itemized in the 1100 series:– Title search– Examination– Document preparation– Fee for conducting the closing

(including attorneys fees to represent a lender/buyer)

– Lender’s title insurance premium

38

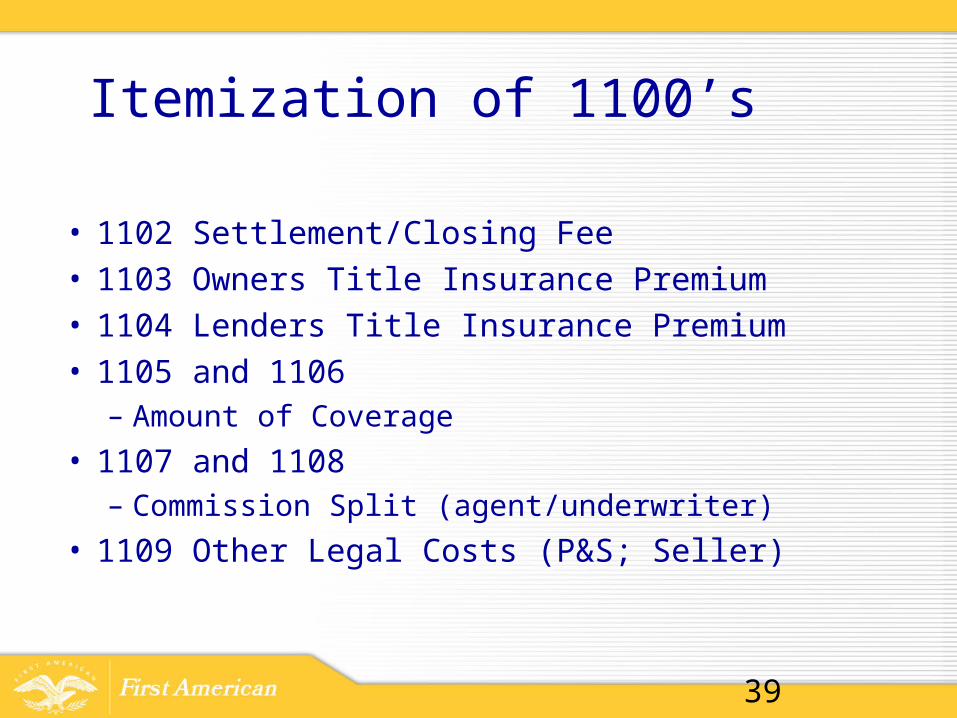

Itemization of 1100’s

• 1102 Settlement/Closing Fee• 1103 Owners Title Insurance Premium• 1104 Lenders Title Insurance Premium• 1105 and 1106

– Amount of Coverage

• 1107 and 1108– Commission Split (agent/underwriter)

• 1109 Other Legal Costs (P&S; Seller)

39

Itemization of 1100’s

–Disbursements to third parties•Itemized

–Amount–Payee

•May be–Included in the amount at 1101–Listed separately in the 1100 series

40

Calculating the Title Premiums

Sale Transaction: First- amount for owners and lenders

simultaneous issue (based on sales/loan) Second- amount for lenders only (loan) Difference equals cost of Owners

Example: Loan and Owners= $400. Loan only= $145. Owners= $ 255.

41

Other Line Items

• 1200 series– Amounts for recording fees

(subject to the 10% tolerance) – Transfer tax- check the GFE

(zero tolerance)

• 1300 series – Other services you can shop for – Relate to GFE Block 6

42

Transfer Tax

Transfer Tax defined (GFE Block 8 #1) Treatment (#2):

• See state or local law- only include if buyer/borrower pays

• If law is unclear-disclosure depends on “common practice or experience in the locality of the property”

• If seller pays and not on GFE-put in seller column of HUD-1

43

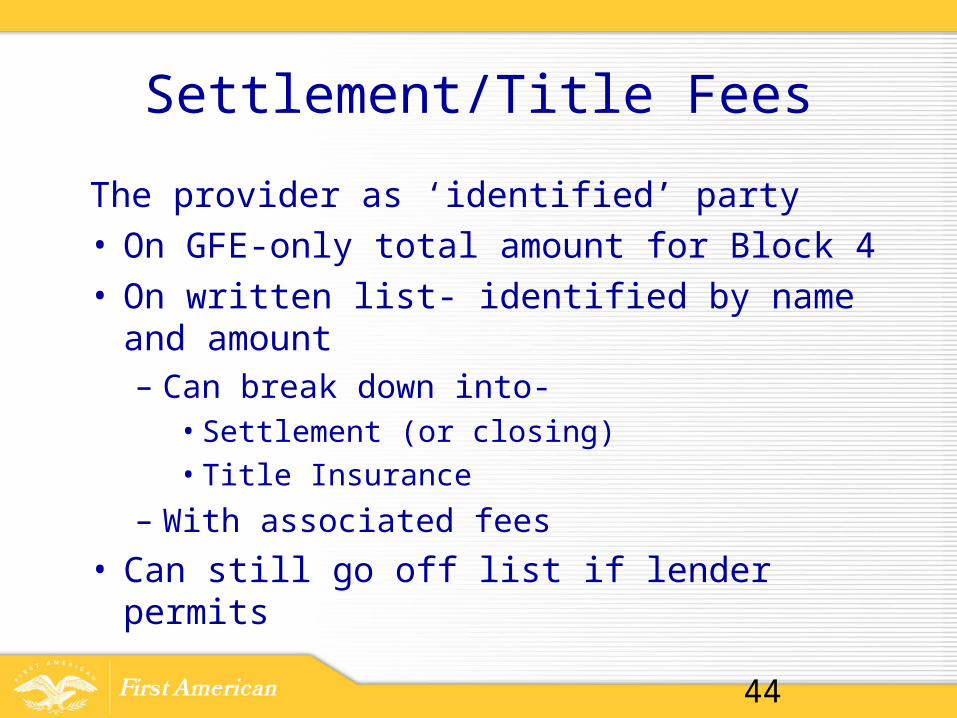

Settlement/Title Fees

The provider as ‘identified’ party• On GFE-only total amount for Block 4• On written list- identified by name and

amount– Can break down into-

• Settlement (or closing)• Title Insurance

– With associated fees

• Can still go off list if lender permits

44

Personal Representation

Where the borrower or seller has own attorney

• can’t be for the RESPA related charges

• The cost is not estimated on GFE• Shown on final HUD-1 on line 1109 (or

beyond)• Itemize the service and identify the

provider• Not included in tolerances

45

HUD-1 Page 3

46

GFE estimates left column

HUD-1 actual right column

Group 1- Charges that cannot change

Group 2- Charges that cannot change by no more than 10%

Group 3- Charges that can change

Recap of Loan Terms

Bifurcation of Lender Charges

How to show on HUD/correspond to GFEThe GFE is a single amount

The written list of providers shows individual costs

The final HUD-1 shows single cost (1101) 1102 shows settlement agent 1107 shows title agent

Presume same entity in Block H page 1

48

Same Entity Does Everything

49

Page 3 comparison

50

Different Entities

51

Page 3 Comparison

52

In Practice?

We just forgot to put the [xx] on the GFE…

The investor insists on a final GFE at closing even if no tolerance issue

They don’t want the owners policy so the tolerance saves the day

The credit is too much, so decrease 802

At and After-ServicingInitial Escrow Disclosure

Project cash in/cash out for escrow accounts

Annual Escrow Disclosure Reflect Actual cash in/cash out of account Make adjustments

Servicing Transfers Good Bye Letters Hello Letters

54

Kickbacks & Referral Fees

RESPA, Reg. X Prohibit Payment of:

• Kickbacks • Referral Fees • Unearned Fees• Duplicate FeesStrict InterpretationNarrow Exceptions allowed

55

Kickbacks & Referral Fees

Any thingOf value:

Money Services Payment of Expenses Discounts

56

Kickbacks & Referral Fees

Given Or Received For ActualOr Anticipated Referral of Business 1-4 family propertyBetween/Among settlement

service providers

57

Kickbacks & Referral Fees

Examples:Payment or Gifts for referralsTrips/Recreation ExpensesOffice ExpensesClosed lotteries/contests

“You can beg; but you cannot pay”

58

Unearned & Duplicate Fees

Unearned:• Little or No work Done• Fee paid

Duplicate:• Work done by second party• Unnecessarily• Fee paid

59

Permitted Payments

Work, actually done, With Commensurate

Payment

Normal Business Marketing Expenses

Normal Educational Expenses

Employers to Employees

60

New “Services” or Sham?

• FHA approved lender pays mortgage broker $1,500 to bring in refinance candidates– HUD aggressively cancelling FHA

approvals

• Hazard disclosure company pays RE broker $100 for every property report referred– HUD maintains services covered even if

not ‘on list’

61

New “Services” or Sham

RealtySouth (Alabama)Class Action- 30,000 consumersRESPA (section 8) violation

• 11th Circuit upheld Class Certification$149 “Administrative Brokerage Commission”

• Charged as separate item on Settlement statement

• Allegation: No Service performed

• Testimony:“Fee went to our overhead and bottom line”; “No benefit provided to consumers”

62

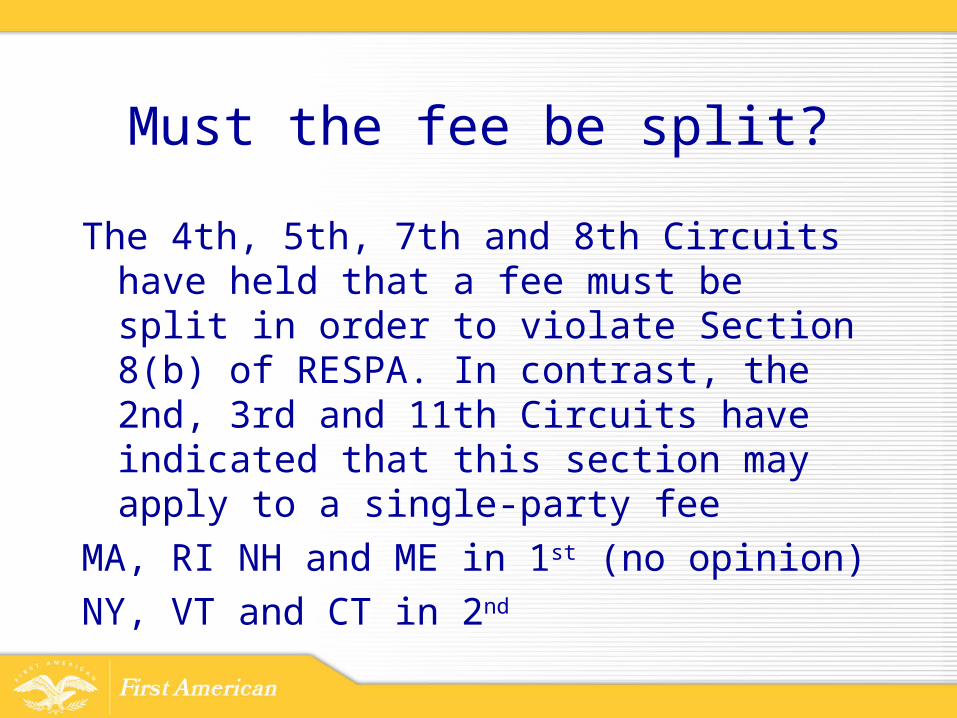

Must the fee be split?

The 4th, 5th, 7th and 8th Circuits have held that a fee must be split in order to violate Section 8(b) of RESPA. In contrast, the 2nd, 3rd and 11th Circuits have indicated that this section may apply to a single-party fee

MA, RI NH and ME in 1st (no opinion)NY, VT and CT in 2nd

Joint Advertising/Marketing

Whose Ad is it?– Joint Advertising/Co Branding ok– Must be paid for jointly– Proportional to business featured– Must it benefit the Payor?

• Who is the target market??

HUD issues new guidance on marketing of Home Warranties

64

Joint Advertising/Marketing

Marketing Fair Market Value Unrelated to Business Volume

• HUD settlement:• Title Agency ‘employs’ Company for

Title Marketing • Pays percentage of title premiums to

Marketing Company• HUD collects $100,000 in fines

65

RESPA Provisions

Section 8: Affiliated Business ArrangementsNarrow exception for certain business modelsMust be disclosed at application

Relationship Range of costs

Cannot require provider be used

66

New Issues

‘Required Use?’ Builder gives $10,000 discount to buyer

towards closing costs if buyer uses builder’s affiliated mortgage company

HUD addressed in Final Rule Home Builders filed suit

• New Rule suspended• Rule Making anticipated

67

Who Can Enforce?

Section 8 violations

HUD-Civil and Criminal ActionsFine up to $10,000.00Imprisoned for up to one year

68

Who Can Enforce?

Private law suit under RESPAFined up to 3 times the amount of the

charge paid for the serviceState Law-statutory, regulatory, case

Unfair and Deceptive Individual Suits Class Actions

69

RESPA: Tolerance Differences6) Q: If a loan originator pressures a settlement

agent to reduce their charges or to ‘cover the difference‘ to bring the costs into compliance with the tolerances, is that considered a violation of RESPA Section 8(a)?

A: If a loan originator (or other settlement service provider) pressures a settlement agent (or other settlement service provider) to reduce their charges or otherwise ’cover the difference‘ to bring the costs into compliance with the tolerances as a condition of receiving future referrals of business, it may be considered a potential violation of RESPA Section 8(a). Please contact the Office of RESPA and ILS to file a complaint.

70

RESPA: Enforcement12) Q: If I suspect someone is violating RESPA, is there a

phone number I can call to make a complaint to HUD?

A: We encourage anyone that suspects someone is potentially violating RESPA to contact us. You may either call 1-202-708-0502 or you may send your complaint to: Director, Office of RESPA and Interstate Land Sales US Department of Housing and Urban Development Room 9154 451 7th Street, SW Washington, DC 20410

For more information, please visit our website at www.hud.gov/respa or email our office at [email protected].

71

You Be the Judge-OK?

Lender keeps all business cards from every new application and uses them to send email newsletter of real estate issues to RE agents

Attorney sends out mailer reminding RE agents of June 1 tax rebate expiration; “Every deal you send between now and then makes enters you in our drawing to win dinner for two”

YES

NO

72

You Be the Judge-OK?

Attorney brings in cold cuts and soda to RE agents while conducting “Lunch and Learn” about Condominium law

Lender pays all RE agents’ office’s costs for “Staff Appreciation” party, but does not attend

Attorney pays RE agent for Conference room rental in RE agent’s office to conduct closings

YES

NO

YES

73

You Be the Judge-OK?

Lender creates pads and pens with own logo; leaves at RE agents office

Lender creates pads and pens with RE agentslogo; leaves at RE agents office

Attorney makes contribution to Lender’s favorite charity every time Lender sends a closing

74

YES

NO

NO

You Be the Judge-OK?Lender purchases list of “leads” from company based on public records to send out refinance solicitations

Lender pays RE agent marketing fee which requires agent to recommend only that lender and distribute only that lenders materials

Title Agent hires Marketing Consultant to use contacts with RE agents for business development and pays a percentage of the title premium for all closed transactions.

YES

NO

NO

75

You Be the Judge-OK?

Attorney pays RE Agent $100 for every “pre-title order” she completes at time of contract completion

FHA-Approved Lender pays Mortgage Brokers a third party originator fee for all FHA loans referred and closed

RE Agent charges Admin Fee to cover ‘internal expenses’

NO

NO

NO

76

You Be the Judge-OK?

Lender quotes cost on GFE; fee exceeds quote beyond tolerance; Lender pays borrower to reimburse

Lender uses Vendor Manager to distribute appraisals; all are same (list) price regardless of complexity/time

Lender uses Vendor Manager to distribute closings; Manager pays difference to Closer if fees exceed GFE to maintain tolerance

YES

YES

NO

77

You Be the Judge-OK?

Attorney prepays Greens Fees and Lunch at Club; leaves note and Pro Shop Gift Certificate at Mortgage Broker’s office

Attorney invites 3 RE agents to join foursome at Red Cross Charity Golf Event

Lender and Attorney go out after work every Friday; take turns picking up tab

78

NO

YES

YES

QUESTIONS AND ANSWERS

79