residual retail market demand analysis - mike layton

TRANSCRIPT

ResidualRetailMarketDemandAnalysis–420BathurstStreet,

Toronto,Ontario

Prepared for:

Riotrin Properties (Bathurst) Inc.

February 13, 2013

February13,2013

Mr.JordanRobinsSeniorVicePresidentDevelopmentRiotrinProperties(Bathurst)Inc.2300YongeStreet,Suite500Toronto,OntarioM4P1E4

DearMr.Robins:

Re:ResidualRetailMarketDemandAnalysis–420BathurstStreet–Toronto,Ontario

urbanMetricsinc.ispleasedtosubmitourreportthatsummariestheresultsofaresidualmarketdemandanalysis,whichassessesthecurrentandfuturemarketsupportavailabletotheproposedcommercialdevelopmentat420BathurstStreetintheCityofTorontoandwhethertheproposeddevelopmentwillhaveanyadverseeffectsontheeconomichealthofnearbyshoppingdistricts.

Thisreportrepresentsanupdatetoourearlierstudyentitled“RetailMarketReview–420BathurstStreet–Toronto,Ontario”datedDecember5,2011,whichexaminedthepotentialimpactoftheproposedredevelopmentonnearbyshoppingdistricts.Theproposeddevelopmentat420BathurstStreetwouldbecomprisedofsome135,000squarefeetofcommercialspaceonthreelevels.Some35,000squarefeetofretail/servicespacewouldbelocatedatstreetlevel,withtwofloorsoflargescaleretailuseslocatedabove,eitherastwoseparatetenantsorasonelargergeneralmerchandisetenantoccupyingthemajorityofthisupperlevelspace.

Theanalysesandappendicesintheattachedreportprovideourdetailedstudyfindingsandconclusions.Basedonthisresidualanalysis,itisourprofessionalopinionthatanyofthepotentialtenantsthatcouldlocateintheproposeddevelopmentcanbeeasilyaccommodatedinthemarketbasedonfuturemarketgrowthalonewithlimited,ifany,impactonexistinglocalshoppingdistrictsintheTradeArea.Inaddition,wehaveundertakenadetailedinventoryofallretailandservicefacilitiesinthefournearbyshoppingdistrictsandhavereviewedthisinventorydata.Itisstillourprofessionalopinionthatthesubjectproposalwillbeverydifferentfromtheseshoppingdistrictsintermsoftenanttypesandsizes.Inourview,thetenantslikely

tobeattractedtotheproposeddevelopmentonthesubjectsiteareverydifferentfromtenantsinnearbyshoppingdistricts.

IthasbeenapleasureconductingthisstudyonbehalfofRiotrinProperties(Bathurst)Inc.andwelookforwardtodiscussingourresults.

Yourstruly,

urbanMetrics inc.

DouglasR.Annand,CMC Partner

ResidualRetailMarketDemandAnalysis–420BathurstStreet

TABLE OF CONTENTS

1 INTRODUCTION........................................................................................................................1

2 TRADEAREAEXTENT.............................................................................................................3

3 POPULATIONANDINCOMEINTHETRADEAREA........................................................5

3.1 HISTORIC,CURRENTANDFUTUREPOPULATION...........................................................................................5 3.2 PERCAPITAINCOME...........................................................................................................................................7

4 RESIDUALMARKETANALYSIS............................................................................................8

4.1 RESIDUALFOODSTOREANALYSIS...................................................................................................................8 4.1.1 FSRExpenditurePotential..........................................................................................................................8 4.1.2 ResidualMarketAnalysisforaSupermarket.................................................................................10 4.1.3 ResidualMarketAnalysisforOtherFoodStoreSpace...............................................................11

4.2 RESIDUALNON‐FOODRETAILSTOREANALYSIS........................................................................................13 4.2.1 NFSRExpenditurePotential...................................................................................................................13 4.2.2 ResidualDepartmentStoreAnalysis...................................................................................................15 4.2.3 ResidualNon‐DepartmentStoreNFSRAnalysis...........................................................................16

5 NEARBYSHOPPINGDISTRICTS.........................................................................................18

5.1 KENSINGTONMARKETBUSINESSIMPROVEMENTAREA...........................................................................18 5.2 CHINATOWNBUSINESSIMPROVEMENTAREA.............................................................................................21 5.3 LITTLEITALYBUSINESSIMPROVEMENTAREA...........................................................................................23 5.4 TRINITYBELLWOODSBUSINESSIMPROVEMENTAREA.............................................................................26

APPENDIXA–RETAILMARKETREVIEW–420BATHURSTSTREET..........................28

APPENDIXB–TRADEAREAPOPULATIONPROJECTIONS..............................................45

APPENDIXC–TRADEAREAINVENTORY..............................................................................49

ResidualRetailMarketDemandAnalysis–420BathurstStreet

1

1 INTRODUCTION

Thefollowingreportoutlinestheresultsofaresidualretailmarketdemandanalysis,whichassessesthecurrentandfuturemarketsupportavailabletoaproposedcommercialprojecttobedevelopedbyRiotrinProperties(Bathurst)Inc.at420BathurstStreetintheCityofToronto.Thereportalsoassesseswhethertheproposeddevelopmentwilladverselyaffecttheeconomichealthofnearbyshoppingdistricts.

Theproposeddevelopmentwouldbecomprisedofsome135,000squarefeetofcommercialspaceonthreelevels.Some35,000squarefeetofretail/servicespacewouldbelocatedatstreetlevel,withtwofloorsoflargescaleretailuseslocatedabove,eitherastwoseparatetenantsorasonelargegeneralmerchandisetenant(likelyadepartmentstore)occupyingthemajorityofthisupperlevelspace.

Thisstudyrepresentsanupdatetoourearlierstudyentitled“RetailMarketReview‐420BathurstStreet‐Toronto,Ontario”datedDecember5,2011.Inthatstudy,whichisattachedasAppendixAtothisreport,weexaminedthepotentialimpactofthesubjectproposalonthenearbyshoppingdistricts,toaddressthepolicyconsiderationsetoutinOfficialPlanpolicy4.5.3(b).Fourlocalshoppingdistrictswereconsideredinthisstudy,including:theKensingtonMarketBIA,theChinatownBIA,theLittleItalyBIA,andtheretail/servicestripalongDundasStreetwestofBathurstStreet,knownastheTrinityBellwoodsBIA.

Thisearliermarketreviewconcludedthatthesubjectproposalat420BathurstStreetwouldbeverydifferentthanthesenearbyshoppingdistricts.Itwasourprofessionalopinionthattheseshoppingareasarenotonlydifferentinscaleandtype,butfunctionverydifferentlyfromthelargerformatstoresproposedfor420BathurstStreet,astheylargelyserveverydifferentanddiversesegmentsofabroaderGreaterTorontoArea(“GTA”)market.Consequently,itwasourconclusionthattheproposeddevelopment,onasitethathistoricallyhashadsignificantretailpermissions,wouldhavenoimpactonthenearbyshoppingdistrictsnotedabove.

TheearliermarketreviewwassubmittedtotheCityinsupportoftheminorvarianceapplicationforthe420BathurstStreetproject,andalsopresentedasevidenceattheOntarioMunicipalBoardhearingthatdealtwiththisapplication.TheBoardruledthattheproposeddevelopmentrequiredare‐zoning,andthisfurthermarketreport,alongwiththeearliermarketreview,isbeingsubmittedinsupportofthere‐zoningapplicationthatisnowbeingmadeforthesite.

Therefore,inthisstudywehavecarriedoutadetailedresidualmarketanalysisinaTradeAreadelineatedtorepresentthegeographicareafromwhichthevariouspotentialusesinthesubjectdevelopmentwoulddrawtheirsupport.Inthisarea,wehaveexaminedthecurrentandprojectedpopulationwhowillliveinthisarea,andtheadditionalmarketsupportthatthisfuturepopulationgrowthwillprovideforexistingandnewretailspaceintheTradeArea,includingthespaceproposedatthe420BathurstStreetsite.Weshouldnotethataresidual

ResidualRetailMarketDemandAnalysis–420BathurstStreet

2

typeanalysisisaconservativemethodfordeterminingthefuturemarketavailableinaTradeAreaandthefuturespacewarrantedasitprotectsexistingretailfacilitiesattheircurrentsalesperformancelevels.Therefore,notransferofsalesfromexistingstoresisrequiredtosupportnewretailspaceenteringtheTradeAreainfutureyears.

Inaddition,wehavecarriedoutadetailedinventoryofallretailandservicefacilitiesinthefournearbyshoppingdistrictsnotedabove,toidentifythedistributionoftenanttypesandsizesintheseareas.Thisdataassistsinillustratinghowtheseretailareasaredifferentfromanyofthepotentialtenantsthatwilllocateinthesubjectcommercialproject.

Theresultsofthisnewanalysisaresummarizedinthesectionsofthisreportthatfollow,whichstronglysupporttheconclusionsthatwerearrivedatfromourearlieranalysisinDecember,2011.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

3

2 TRADEAREAEXTENT

Forthepurposesofthisresidualanalysis,twoTradeAreashavebeendelineated;aPrimaryTradeAreaandaSecondaryTradeArea(Figure2‐1).ThePrimaryTradeAreahasbeenutilizedtoestimatetheavailablefoodstoreretail(FSR)expenditurepotential,asasupermarketmaybeapotentialtenantintheproposeddevelopmentandwouldlikelydrawthemajorityofitssalesfromthisgeographicarea.ItshouldbenotedthatthePrimaryTradeAreacoversaslightlylargergeographicareathanthelocalmarketareainourearlierRetailMarketReview,whichwaslargelydelineatedtodeterminethelocationofthenearbylocalshoppingdistrictswhereimpactwastobetested.Thislocalareathatwasdefinedinourearlierstudywasonlypartoftheareawherethesubjectdevelopmentandthefournearbyshoppingareaswouldderivethemajorityoftheirsalessupport.Asnotedabovethesefourlocalshoppingdistrictsinclude:theKensingtonMarketBIA;theChinatownBIA;theLittleItalyBIA;andtheTrinityBellwoodsBIA,whichareallwhollycontainedwithinthePrimaryTradeArea.

BoththePrimaryandSecondaryTradeAreaswereutilizedtoestimatetheavailablenon‐foodstoreretail(NFSR)potential.ThislargerTradeAreaisusedtoestimatethefutureNFSRpotential,asapossibledepartmentstoretenantorotherlargeformatNFSRretailerslocatingonthesubjectsitewouldattractcustomersfromalargergeographicareathanasupermarket.

FIGURE2‐1:PRIMARYANDSECONDARYTRADEAREAZONES

Source: Google Maps

ResidualRetailMarketDemandAnalysis–420BathurstStreet

4

ThePrimaryTradeAreaisborderedbyBloorStreetWestinthenorth,UniversityAvenueintheeast,QueenStreetWestinthesouthandOssingtonAvenueinthewest.TheSecondaryTradeAreaislocatedtothesouthofthePrimaryTradeArea,andisborderedbyQueenStreetWestinthenorth,UniversityAvenueintheeast,FrontStreetWestandtheCNRaillineinthesouthandextendssouthfromOssingtonAvenueinthewest.

Thisistheareafromwhichthepotentialtenantsinthe420BathurstStreetprojectwillderivethemajorityoftheirsales,thoughitisouropinionthattheBIAsintheareaandinparticularKensington,ChinatownandLittleItalywilldrawfromamuchbroaderarea.ItshouldbenotedthatthereareotherretailareasandBIAsmostlyontheborderoftheTradeArea,thatservetosomedegreeresidentslivinginbothzonesoftheTradeArea.However,theOfficialPlanpolicyconsideration,asstatedinPolicy4.5.3(b),seekstoensurethatlargescaleretailusesinMixedUseAreaswillnotadverselyaffecttheeconomichealthofnearbyshoppingdistricts.Inouropinion,onlythefourBIA’snotedabovecanbeconsideredasnearbyshoppingdistricts.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

5

3 POPULATIONANDINCOMEINTHETRADEAREA

TodeterminethepotentialdemandandmarketsupportforthevariouspotentialretailusesintheproposedcommercialdevelopmentonthesubjectsiteandtheirpotentialimpactonnearbyshoppingdistrictsintheTradeArea,itisnecessarytoestimatethefuturepopulationwithinthedefinedPrimaryandSecondaryTradeAreas.Populationchange,inadditiontoincome,representsthemostsignificantfactorsthatcaninfluencetheleveloffutureretailsalesavailableinanareaandtheretailspacewarrantedinfutureyears.

3.1 HISTORIC,CURRENTANDFUTUREPOPULATION

Figure3‐1summarizesthehistoric,currentandfuturepopulationinthePrimaryandSecondaryTradeAreas.ThehistoricpopulationisbasedonCensusofCanadadatafor1996,2001,2006and2011,asadjustedtoaccountfornetunder‐coverageintheCensus.

WhilethepopulationinthePrimaryTradeAreadeclinedduringthe1996to2001and2001to2006Censusperiods,itincreasedbetween2006and2011,recapturingallofthepopulationlostinthepreviousdecade.Conversely,theSecondaryTradeAreahasexperiencedstrongpopulationgrowthineachCensusperiodbetween1996and2011,duetothesignificantamountofnewcondominiumapartmentdevelopmentinthisarea.

FIGURE3‐1:TRADEAREAPOPULATION,1996TO2031

Current

1996 2001 2006 2011 2012 2014 2016 2021 2026 2031

Primary Trade Area 52,046 51,810 49,885 53,213 53,600 54,300 55,600 57,100 58,500 60,000

Periodic Growth (237) (1,924) 3,327 387 700 1,300 1,500 1,400 1,500

Periodic Growth Rate (%) ‐0.5% ‐3.7% 6.7% 0.7% 1.3% 2.4% 2.7% 2.5% 2.6%

Average Annual Growth (47) (385) 665 387 350 650 300 280 300

Average Annual Growth Rate (%) ‐0.1% ‐0.8% 1.3% 0.7% 0.7% 1.2% 0.5% 0.5% 0.5%

Secondary Trade Area 7,862 11,658 15,311 20,171 23,300 29,600 35,200 40,900 46,600 52,400

Periodic Growth 3,796 3,653 4,860 3,129 6,300 5,600 5,700 5,700 5,800

Periodic Growth Rate (%) 48.3% 31.3% 31.7% 15.5% 27.0% 18.9% 16.2% 13.9% 12.4%

Average Annual Growth 759 731 972 3,129 3,150 2,800 1,140 1,140 1,160

Average Annual Growth Rate (%) 8.2% 5.6% 5.7% 15.5% 12.7% 9.0% 3.0% 2.6% 2.4%

Total (Combined) Trade Area 59,909 63,468 65,197 73,384 76,900 83,900 90,800 98,000 105,100 112,400

Periodic Growth 3,559 1,729 8,187 3,516 7,000 6,900 7,200 7,100 7,300

Periodic Growth Rate (%) 5.9% 2.7% 12.6% 4.8% 9.1% 8.2% 7.9% 7.2% 6.9%

Average Annual Growth 712 346 1,637 3,516 3,500 3,450 1,440 1,420 1,460

Average Annual Growth Rate (%) 1.2% 0.5% 2.4% 4.8% 4.5% 4.0% 1.5% 1.4% 1.4%

1

2

Source: urbanMetrics inc. based on data from the Census of Canada and information from the City of Toronto

Historic1

Forecast2

Based on 1996, 2001, 2006 and 2011 Census of Canada. Data were adjusted to account for the net Census undercoverage, using Statistics Canada data

for the Toronto Census Division. The adjustment factors were 3.11% in 1996, 4.47% in 2001, 4.29% in 2006 and 4.92% in 2011.

Forecasts are based on residential development applications for the appropriate Trade Area, obtained from the City of Toronto in January 2013.

Forecast population has been rounded to the nearest 100 persons.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

6

Toforecastpopulationgrowthoverthestudyperiod(to2031),wehavereviewedtrendsinaveragehouseholdsizeandresidentialdevelopmentapplicationsintheTradeArea,availablefromtheCityofTorontoinJanuary2013(detailscanarefoundinAppendixB).AsistypicalinolderareasoftheCity,householdsizesintheexistinghousingstockhavetrendedlower,althoughtherateofdeclinehasslowedineachsubsequentperiodfrom1996to2011.Itisexpectedthathouseholdsizeswillcontinuetodeclineinfutureperiods,butlikelyatamuchslowerrate,whichisconsistentwithrecenttrendsintheCity.Therefore,incalculatingtheforecastpopulationinexistingdwellingunits,wehaveassumedthatthepersonsperunit(PPU)factorcontinuestodeclineintheexistinghousingstock,butataslowerratethaninpastCensusperiods.

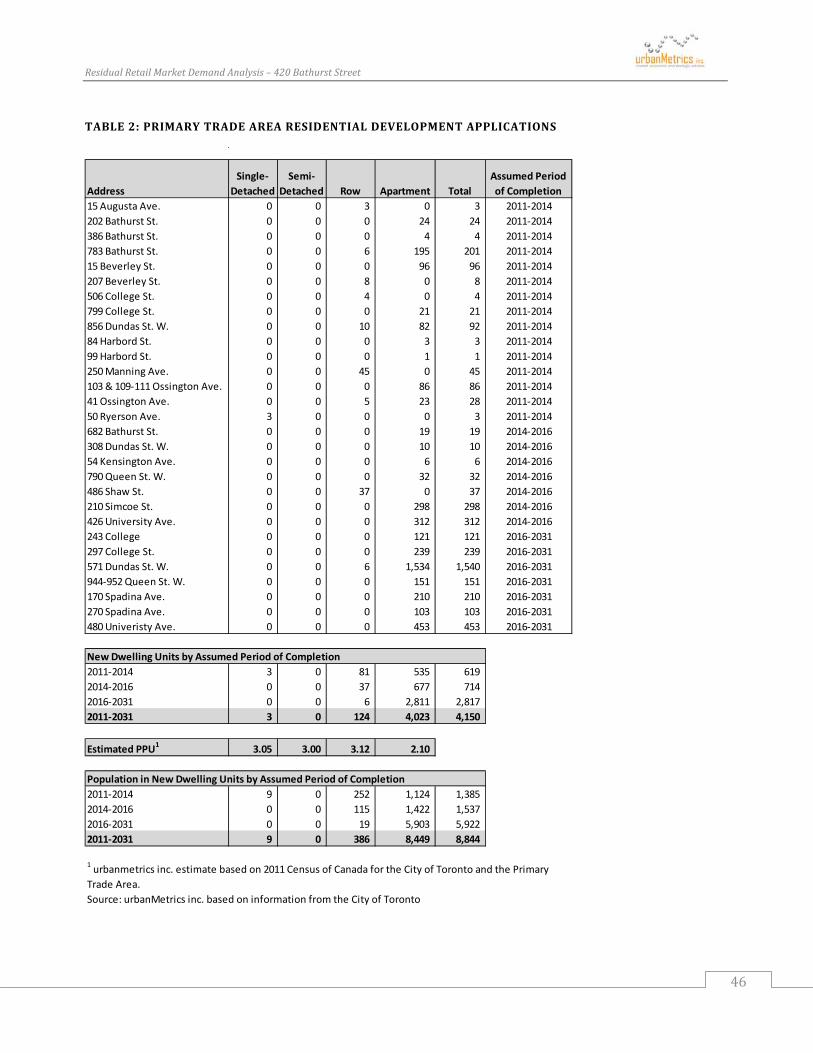

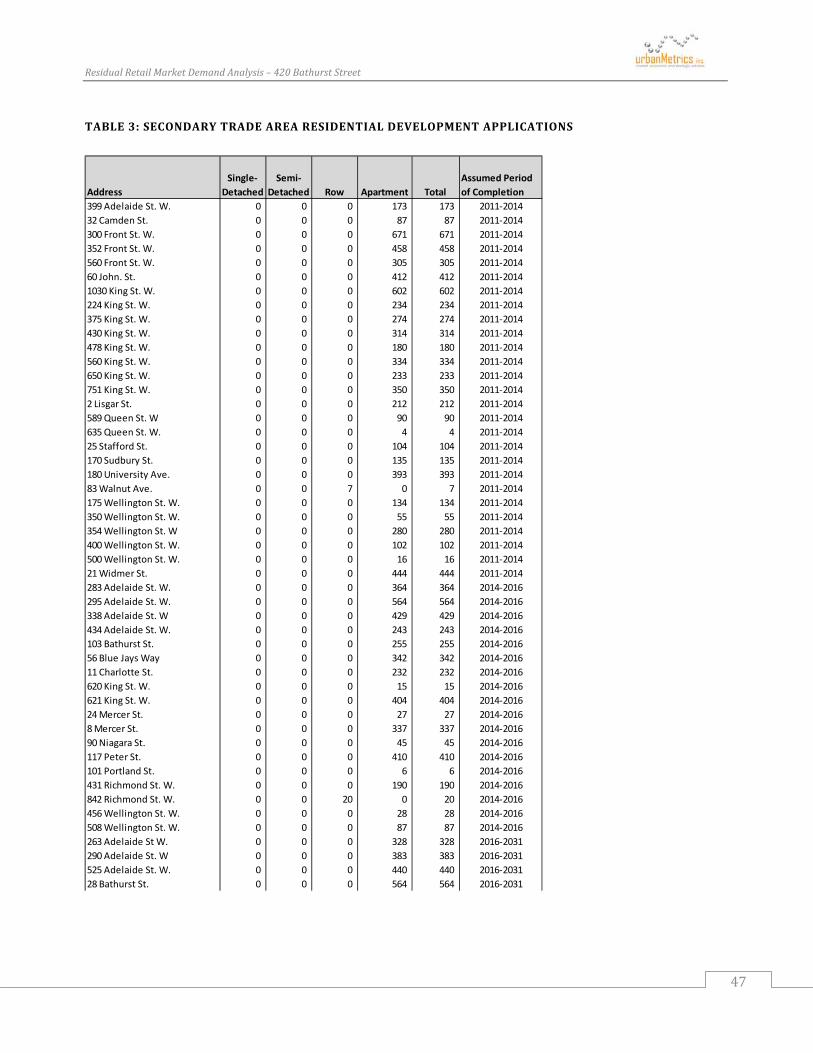

Inforecastingpopulationgrowthinnewdwellingunits(thoselikelytobecompletedbetween2011and2031),residentialdevelopmentapplicationsavailablefromtheCityofTorontowerereviewedtodeterminethenumberofproposeddwellingunitsbydwellingtype.Basedonthisdata,therearealmost4,200dwellingunitsinthePrimaryTradeAreathatwererecentlycompleted,areunderconstruction,orareproposedduringthe2011‐2031period.IntheSecondaryTradeArea,thereareapproximately23,500dwellingunitsthathavebeenrecentlycompleted,areunderconstruction,orareproposedoverthisforecastperiod.Whilemanyoftheproposedprojectswillproceedasscheduled,therewillbesomeprojectsthatarenotbuiltduringthestudyperiodordevelopedatlowerdensitiesthancurrentlyproposed.Thiscouldreduceourpopulationforecast.Ontheotherhandhowever,therewillbenewapplicationssubmittedtotheCityforresidentialdevelopmentsintheTradeAreainfutureyearsoftheforecastperiod,whichwilllikelymorethanoff‐setanycurrentapplicationsthatdonotmaterialize.Therefore,inouropiniontheforecastofpopulationlivingintheTradeAreaismorethanlikelyunderstated.Toforecastthepopulationgrowthexpectedfromthenewunits,estimatedPPU’sbydwellingtypefromthe2011CensuswereappliedtothesenewresidentialdwellingunitsincalculatingtheforecastpopulationineachTradeAreazone.

Basedonthismethodology,whichisfullydocumentedinAppendixBattached,wehaveforecastanincreaseinthepopulationinthePrimaryTradeAreaofapproximately2,400personsbetween2011and2016,andanadditional1,500personsby2021.IntheSecondaryTradeArea,populationisexpectedtoincreasebyapproximately15,000personsbetween2011and2016,withanadditional5,700personsaddedby2021.Whilewehaveforecastpopulationto2031,itisthepopulationgrowthexpectedoverthe2011to2021periodthatismostimportantinassessingthemarketsupportfortheproposedcommercialdevelopmentonthesubjectsite.

ThecombinedPrimaryandSecondaryTradeAreashaveaccountedforadisproportionateshareofthepopulationgrowthexperiencedintheCityofTorontoinrecentyears.Withthelargeinventoryofresidentialdevelopmentapplicationsinthepipeline,itislikelythatthePrimaryandSecondaryTradeAreaswillcontinuetoaccountforadisproportionateshareofpopulationgrowthintheCityoverthestudyperiod.

Therefore,itisouropinionthatthisincreaseinpopulationinthePrimaryandSecondaryTradeAreaswillsubstantiallyincreasetheavailablemarketsupportavailabletoretailersatthe

ResidualRetailMarketDemandAnalysis–420BathurstStreet

7

subjectsiteaswellasfortheexistinglocallyorientedretailersintheKensingtonMarketBIA,theChinatownBIA,theLittleItalyBIAandtheTrinity‐BellwoodsBIA.ItshouldalsobenotedthattheincreaseinmarketsupportavailablefortheTradeAreaswillonlyrepresentpartoftheoverallsourceofsalessupportfortheseuniqueretailareasthatcontinuetodrawfromthelargerGreaterTorontoArea.

3.2 PERCAPITAINCOME

PercapitaincomelevelsprovideareasonableguideorbasisfordeterminingtheexpenditurehabitsofthelocalpopulationlivingwithinadefinedTradeArea.Althoughcertaininterveningvariables,includingageandgeographiclocation,caninfluenceconsumerexpenditurehabitsandshoppingpreferences,populationgroupingswithsimilarincomecharacteristicstendtoexhibitsimilarexpenditurehabitsforbroadmerchandisegroupings.

FIGURE3‐2:PERCAPITAINCOME(2005),CENSUS2006

AreaPer Capita

IncomeIndex to Province

Ontario 30,723 100.0 City of Toronto 33,311 108.4

TRADE AREAPrimary Trade Area 27,035 88.0 Secondary Trade Area 50,837 165.5 Trade Area (Combined) 32,545 105.9

Source: urbanMetrics inc. based on the 2006 Census of Canada and Pcensus

Basedonthe2006Census(themostrecentdataavailable),theaverage2005percapitaincomesforthePrimaryandSecondaryTradeAreashavebeencalculated(Figure3‐2).TheaveragepercapitaincomeintheSecondaryTradeAreais65.5%abovetheprovincialaverage,whiletheaveragepercapitaincomeinthePrimaryTradeAreaisabout12%belowtheprovincialaverage.Overall,forthecombinedTradeArea,theaveragepercapitaincomewasabout6%higherthantheprovincialaverageandsimilartotheoverallCityofTorontoaverage.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

8

4 RESIDUALMARKETANALYSIS

Forthepurposesofouranalysis,wehaveestimatedtheretailsalespotentialavailableinthevariousportionsoftheTradeAreaforthefollowingstoretypes:

Supermarkets; Otherfoodstores(includinggrocery,convenienceandspecialtyfoodstores); Departmentstores;and AllNFSR,excludingdepartmentstoresandautomotive.

Thesestoretypeshavebeenanalyzed,astheyarethelikelytenant(s)ofthesecondandthirdfloorsoftheproposeddevelopment.Thesmallerretail/serviceusesthatwilloccupythegroundfloorarenotthefocusofthisanalysis,astheydonotrepresenttheintroductionoflargerscaleretailusesthatarethefocusofthepolicyconsiderationssetforthinOfficialPlanpolicy4.5.3(b).

4.1 RESIDUALFOODSTOREANALYSIS

4.1.1 FSREXPENDITUREPOTENTIAL

ThefollowingsectionincludesananalysisofthepercapitaFSRexpenditures,thedistributionofthoseexpenditures,andthetotalexpenditurepotentialavailablefromPrimaryTradeArearesidents.

4.1.1.1 PERCAPITAFSREXPENDITURES

BasedonStatisticsCanadaRetailTradedata,the2012averagepercapitafoodstoreexpenditureinOntarioisestimatedat$2,230.Foodstoreexpendituresincludethosemadeinsupermarkets,grocerystores,conveniencestoresandspecialtyfoodstores.

AsindicatedinFigure4‐1,the2012averagepercapitafoodstoreexpenditureinthePrimaryTradeAreahasbeenestimatedbasedontheincomerelationshipbetweentheProvinceandthePrimaryTradeAreaandanexpenditurebasedregressionequation,whichcalculatesanexpenditureindexbasedonincomelevels.

ForPrimaryTradeArearesidents,the2012averagepercapitaFSRexpenditurepotentialhasbeenincreasedatarateof0.25%peryear(realgrowth)overthestudyperiod.Itshouldbenotedthatfuturechangesinexpenditurepatternssolelyduetoinflationhavenotbeenrecognized.Therefore,futureexpenditurelevelsreflectthe2012valueoftheCanadiandollar.

4.1.1.2 FSREXPENDITUREPOTENTIALFROMPRIMARYTRADEAREARESIDENTS

BymultiplyingtheaveragepercapitafoodstoreexpenditurebythecurrentandprojectedpopulationresidinginthePrimaryTradeArea,thetotalfoodstorepotentialhasbeencalculated

ResidualRetailMarketDemandAnalysis–420BathurstStreet

9

overthestudyperiod.Intotal,thefoodstorepotentialhasbeenestimatedat$118.1millionin2012,increasingto$128.6millionby2021,agrowthof$10.5millionovertheperiod(expressedin2012dollars).

4.1.1.3 DISTRIBUTIONOFFSREXPENDITURES

Thetotalfoodstoreexpenditurepotentialhasbeendividedbetweensupermarketandotherfoodstores(i.e.grocery,convenienceandspecialtyfoodstores).BasedonourreviewoffoodstoresinthePrimaryTradeArea,whichincludesavarietyofindependentgrocerystoresandspecialtyfoodstores,andStatisticsCanadaRetailTradeData,wehaveestimatedthesupermarketshareofFSRexpendituresat70%,withgrocery/otherfoodstoresat30%.Thisishigherthantheprovincialaverage,wheresupermarketexpendituresrepresentapproximately85.0%ofFSRandotherspecialtystores15.0%.ThehigherspecialtyfoodstoreshareinthemarketreflectsthelargenumberofsmallergroceryandotherfoodsstoresthroughouttheTradeAreaandspecificallyKensingtonMarketandChinatown.Infutureyears,wehaveassumedthatthesupermarketsharewillremainconstantasbothnewsupermarketsandspecialtyfoodstoresenterthemarket.

AsindicatedinFigure4‐1,thesupermarketpotentialavailablefromthePrimaryTradeAreahasbeencalculatedat$82.7millionin2012,increasingto$90.0millionby2021.ItshouldalsobestatedthatFigure4‐1excludesexpendituresofpersonswhoresideoutsidethePrimaryTradeArea(i.e.inflow).Thesepersonscouldincludevisitors,thetravellingpublic,andindividualswhoseworkplaceiswithinthePrimaryTradeAreabutresideoutside.Thisinflowofretailsalesisconsideredinourmarketanalysis.TheinflowinthePrimaryTradeAreaislikelysignificant,particularlyforsupermarkets,astheexistingsupermarketsinthePrimaryTradeAreaareonthePrimaryTradeAreaborder.Inaddition,manyofthespecialtyfoodstoreslocatedinKensington,LittleItalyandChinatown,willattractsignificantinflowsalesfromoutsidetheTradeAreaduetotheuniquedrawingpowerofthesecommercialareas.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

10

FIGURE4‐1:TRADEAREAFSREXPENDITUREPOTENTIAL

PER CAPITA FOOD STORE RETAIL (FSR) EXPENDITURE POTENTIAL

2012 Dollars 2012Province of OntarioPer Capita FSR Expenditure $ 2,230 (1

2012 Dollars 2012 2014 2016 2021 2031

Primary Trade AreaIncome Index to Province 88.00 FSR Expenditure Index to Province 98.80 Per Capita FSR Expenditure $ 2,203 $ 2,214 $ 2,225 $ 2,253 $ 2,308Population 53,600 54,300 55,600 57,100 60,000 TOTAL FSR POTENTIAL ($Millions) $ 118.1 $ 120.2 $ 123.7 $ 128.6 $ 138.5

FSR - Supermarket Share (2 70.0% 70.0% 70.0% 70.0% 70.0%FSR - Grocery/Other Food Store Share (2 30.0% 30.0% 30.0% 30.0% 30.0%

Total 100.0% 100.0% 100.0% 100.0% 100.0%FSR - Supermarket Share (2 $ 82.7 $ 84.1 $ 86.6 $ 90.0 $ 97.0FSR - Grocery/Other Food Store Share (2 $ 35.4 $ 36.1 $ 37.1 $ 38.6 $ 41.6Total $ 118.1 $ 120.2 $ 123.7 $ 128.6 $ 138.6

Primary Trade Area (3TOTAL FSR POTENTIAL ($Millions) $ 118.1 $ 120.2 $ 123.7 $ 128.6 $ 138.5

TOTAL FSR - Supermarkets ($Millions) $ 82.7 $ 84.1 $ 86.6 $ 90.0 $ 97.0Cumulative Growth $ 1.4 $ 3.9 $ 7.3 $ 14.3

TOTAL FSR - Grocery/Other Food ($Millions) $ 35.4 $ 36.1 $ 37.1 $ 38.6 $ 41.6Cumulative Growth $ 0.7 $ 1.7 $ 3.2 $ 6.2

SOURCE: urbanMetrics inc.1) Based on Statistics Canada, Retail Trade. 2) urbanMetrics inc. estimate based on the provincial average and our review of the inventory of food store space.3) The per capita food store retail expenditure potential has only been estimated for the Primary Trade Area

4.1.2 RESIDUALMARKETANALYSISFORASUPERMARKET

ThissectionexaminesthesupermarketpotentialavailableinthePrimaryTradeAreainfutureyears.Thereiscurrentlyatotalofapproximately84,400squarefeetofsupermarketspaceinthreesupermarketsinthePrimaryTradeArea.Thesesupermarketsinclude:

Metro–735CollegeStreet(LittleItalyBIA)–26,800squarefeet Metro–425BloorStreetWest–12,900squarefeet Loblaws–585QueenStreetWest–44,700squarefeet

BasedonourexaminationoftheexistingsupermarketcompetitioninthePrimaryTradeAreathesesupermarketsareestimatedtobeperformingatsalesofapproximately$630persquarefoot,whichissignificantlyabovetheindustryaverage.TheOntarioaverageperformancelevelin2010wasonly$444persquarefoot.ThehighestimatedsalesperformancelevelforexistingsupermarketsreflectsthelimitedamountofsupermarketspaceintheTradeAreaatthistime.

RecognizingtheestimatedcapturerateforstoreswithinthePrimaryTradeAreaof45.0%,whichisestimatedtoincreaseto65.0%asnewstoresenterthemarketby2014,theassumedfirstfullyearofoperationfortheproposedstoreonthesite,aswellastheproposed20,000squarefootsupermarketintheproposedTributeCommunitiesdevelopmentat297CollegeStreet,theresidualpotentialhasbeenestimatedat$17.5millionfromPrimaryTradeArearesidentsin2014,increasingto$25.8millionby2021(Figure4‐2).Assumingaconservative

ResidualRetailMarketDemandAnalysis–420BathurstStreet

11

30%inflow,at$500persquarefoot,some50,000squarefeetofadditionalsupermarketspacewouldbewarrantedinthePrimaryTradeAreaby2014,increasingto73,700squarefeetby2021.Therefore,by2016therewillbeadequatemarketsupportavailabletoaccommodatebotha45,000squarefootsupermarketonthesubjectsiteandtheproposalbyTributeCommunitiesfora20,000squarefootsupermarketinthemixed‐usedevelopmentat297CollegeStreet.Notransferofsalesfromexistingsupermarketsorfoodstoresisrequiredtosupportthisnewspace.

FIGURE4‐2:SUPERMARKETRESIDUALANALYSIS

SUPERMARKET ANALYSIS

2012 Dollars 2012 2014 2016 2021 2031

Primary Trade AreaSupermarket Expenditures ($Millions) $ 82.7 $ 84.1 $ 86.6 $ 90.0 $ 97.0

Estimated Trade Area Share %(1 45.0% 65.0% 70.0% 70.0% 70.0%Estimated Trade Area Share ($ Millions) $ 37.2 $ 54.7 $ 60.6 $ 63.0 $ 67.9Residual Potential $ 17.5 $ 23.4 $ 25.8 $ 30.7

Primary Trade AreaTotal Supermarket Expenditures ($Millions) $ 82.7 $ 84.1 $ 86.6 $ 90.0 $ 97.0Total Estimated Trade Area Share ($Millions) $ 37.2 $ 54.7 $ 60.6 $ 63.0 $ 67.9Estimated Trade Area Share % 45.0% 65.0% 70.0% 70.0% 70.0%

Existing Sales from Trade Area Residents ($Millions) $ 37.2 $ 37.2 $ 37.2 $ 37.2 $ 37.2Residual Potential ($Millions) $ 17.5 $ 23.4 $ 25.8 $ 30.7

TOTAL RESIDUAL POTENTIAL (including inflow)Additional Residual Potential Available $ 17.5 $ 23.4 $ 25.8 $ 30.7Plus Inflow Sales @ 30.0% (1 $ 7.5 $ 10.0 $ 11.1 $ 13.2TOTAL ADDITIONAL SALES POTENTIAL AVAILABLE $ 25.0 $ 33.4 $ 36.9 $ 43.9

WARRANTED ADDITIONAL SQUARE FEET (2

@ $475 per sq. ft. 52,600 70,400 77,600 92,300 @ $500 per sq. ft. 50,000 66,900 73,700 87,700 @ $525 per sq. ft. 47,600 63,700 70,200 83,500

SOURCE: urbanMetrics inc.

1) urbanMetrics estimate reflecting the assumption that new supermarkets will locate in the Trade Area in future years including a store at the subject site.

2) Rounded to the nearest 100 square feet.

4.1.3 RESIDUALMARKETANALYSISFOROTHERFOODSTORESPACE

Thissectionanalysestheexpenditurepotentialavailabletootherfoodstores(includinggrocerystores,conveniencestoresandspecialtyfoodstores)inthePrimaryTradeArea.Figure4‐3detailsthepotentialmarketopportunityavailabletoexistingandadditionalotherfoodstorespaceinthePrimaryTradeArea.ThePrimaryTradeAreacapturerateintheotherfoodstorecategoryishigherthanutilizedinthesupermarketanalysis,recognizingthatconvenienceandspecialtyfoodstorespacetypicallyislocalserving.TheestimatedinflowintheotherfoodstoreanalysisislowerthaninthesupermarketanalysisasitacknowledgesthatmanyoftheotherspecialtyfoodstoresaredistributedthroughoutthePrimaryTradeAreaandarealsolocalserving.Basedonthisanalysis,thereisresidualpotentialof$4.1millioninotherfoodstoreexpendituresavailablefromPrimaryTradeArearesidentsin2014,increasingto$6.1millionin

ResidualRetailMarketDemandAnalysis–420BathurstStreet

12

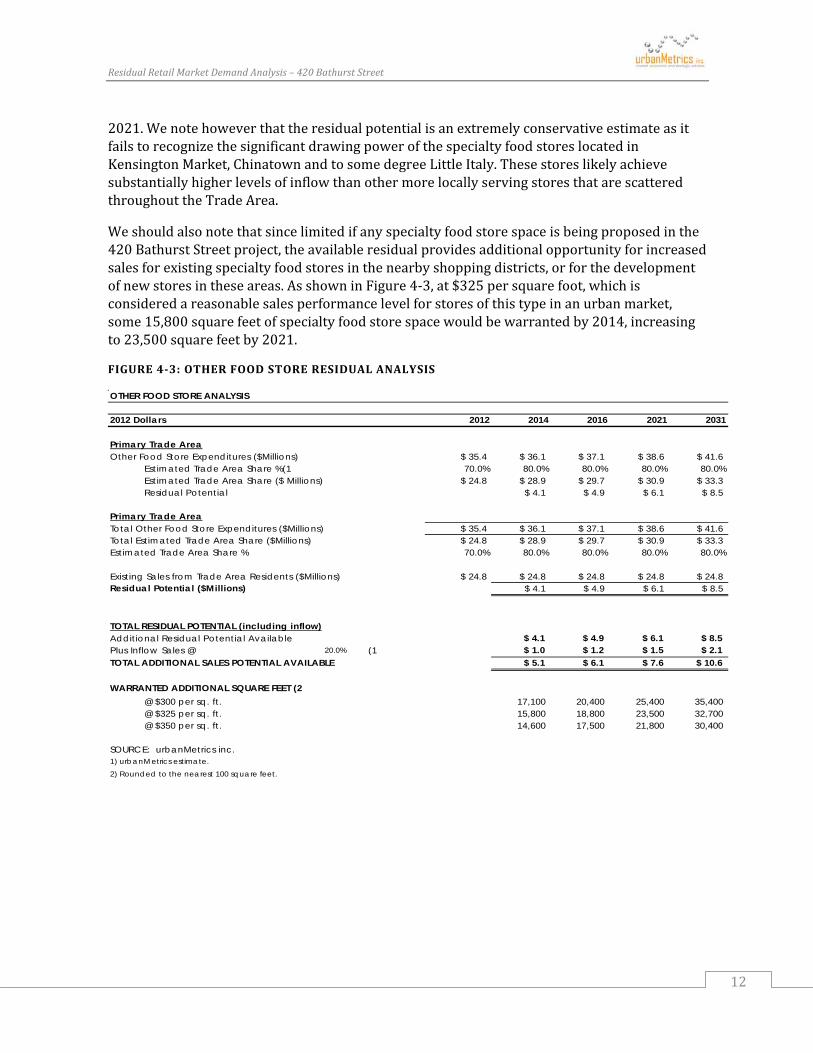

2021.WenotehoweverthattheresidualpotentialisanextremelyconservativeestimateasitfailstorecognizethesignificantdrawingpowerofthespecialtyfoodstoreslocatedinKensingtonMarket,ChinatownandtosomedegreeLittleItaly.ThesestoreslikelyachievesubstantiallyhigherlevelsofinflowthanothermorelocallyservingstoresthatarescatteredthroughouttheTradeArea.

Weshouldalsonotethatsincelimitedifanyspecialtyfoodstorespaceisbeingproposedinthe420BathurstStreetproject,theavailableresidualprovidesadditionalopportunityforincreasedsalesforexistingspecialtyfoodstoresinthenearbyshoppingdistricts,orforthedevelopmentofnewstoresintheseareas.AsshowninFigure4‐3,at$325persquarefoot,whichisconsideredareasonablesalesperformancelevelforstoresofthistypeinanurbanmarket,some15,800squarefeetofspecialtyfoodstorespacewouldbewarrantedby2014,increasingto23,500squarefeetby2021.

FIGURE4‐3:OTHERFOODSTORERESIDUALANALYSIS

OTHER FOOD STORE ANALYSIS

2012 Dollars 2012 2014 2016 2021 2031

Primary Trade AreaOther Food Store Expenditures ($Millions) $ 35.4 $ 36.1 $ 37.1 $ 38.6 $ 41.6

Estimated Trade Area Share %(1 70.0% 80.0% 80.0% 80.0% 80.0%Estimated Trade Area Share ($ Millions) $ 24.8 $ 28.9 $ 29.7 $ 30.9 $ 33.3Residual Potential $ 4.1 $ 4.9 $ 6.1 $ 8.5

Primary Trade AreaTotal Other Food Store Expenditures ($Millions) $ 35.4 $ 36.1 $ 37.1 $ 38.6 $ 41.6Total Estimated Trade Area Share ($Millions) $ 24.8 $ 28.9 $ 29.7 $ 30.9 $ 33.3Estimated Trade Area Share % 70.0% 80.0% 80.0% 80.0% 80.0%

Existing Sales from Trade Area Residents ($Millions) $ 24.8 $ 24.8 $ 24.8 $ 24.8 $ 24.8Residual Potential ($Millions) $ 4.1 $ 4.9 $ 6.1 $ 8.5

TOTAL RESIDUAL POTENTIAL (including inflow)Additional Residual Potential Available $ 4.1 $ 4.9 $ 6.1 $ 8.5Plus Inflow Sales @ 20.0% (1 $ 1.0 $ 1.2 $ 1.5 $ 2.1TOTAL ADDITIONAL SALES POTENTIAL AVAILABLE $ 5.1 $ 6.1 $ 7.6 $ 10.6

WARRANTED ADDITIONAL SQUARE FEET (2

@ $300 per sq. ft. 17,100 20,400 25,400 35,400 @ $325 per sq. ft. 15,800 18,800 23,500 32,700 @ $350 per sq. ft. 14,600 17,500 21,800 30,400

SOURCE: urbanMetrics inc.1) urbanMetrics estimate.

2) Rounded to the nearest 100 square feet.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

13

4.2 RESIDUALNON‐FOODRETAILSTOREANALYSIS

4.2.1 NFSREXPENDITUREPOTENTIAL

ThefollowingsectionexaminesthepercapitaexpenditureandtotalNFSRexpenditurepotentialavailablefromPrimaryandSecondaryTradeArearesidents.

4.2.1.1 PERCAPITANFSREXPENDITURES

BasedonStatisticsCanadaRetailTradedata,the2012averagepercapitaNFSRexpenditureinOntarioisestimatedat$5,471.AsindicatedinFigure4‐4,forTradeArearesidents,the2012averagepercapitanon‐foodstoreretailexpenditurehasbeenestimatedbasedontheincomerelationshipbetweentheProvinceandeachTradeAreazone,andanexpenditurerelatedregressionequation,whichcalculatesanexpenditureindexbasedonincomelevels.ForTradeArearesidents,the2012averagepercapitaNFSRexpenditureisexpectedtoincreaseatarateof1.5%peryearonanun‐inflatedbasisoverthestudyperiod.Thisratereflectslongtermaveragegrowthrates.Futurechangesinexpenditurepatternssolelyduetoinflationhavenotbeenrecognizedinthisanalysis.

4.2.1.2 NFSREXPENDITUREPOTENTIALFROMTRADEAREARESIDENTS

ThetotalNFSRpotentialfromTradeArearesidentsoverthestudyperiodhasbeencalculatedbymultiplyingtheaveragepercapitaNFSRexpenditureineachTradeAreazonebythecurrentandfuturepopulation.

Intotal,thecurrentNFSRexpenditurepotentialavailablefromTradeArearesidentshasbeenestimatedat$440.0millionin2012,increasingto$592.8millionby2021,agrowthof$152.8million(expressedin2012dollars).ItshouldberecognizedthattheexpenditurepotentialindicatedinFigure4‐4isthatwhichisavailablefromTradeArearesidentsonly,andrepresentstheexpenditurepotentialavailabletostoreslocatedbothwithintheTradeAreaandelsewhere.ItdoesnotincludeexpenditurepotentialfromresidentsoutsidetheTradeArea(e.g.thosewholiveoutside,butworkinside,theTradeArea)

4.2.1.3 DISTRIBUTIONOFNFSREXPENDITURES

WehavedividedthetotalNFSRexpenditurepotential,ascalculatedinFigure4‐4,intotwomajorcategories:departmentstoreandnon‐departmentstoreNFSR,whichincludesallNFSRstorecategories,excludingdepartmentstores.ThepercentagedistributionbystoretypeintheTradeAreahasbeenbasedonourreviewoftheProvincialretailsalesdistribution.Fortheforecastperiod,thisdistributionhasbeenheldconstant.Departmentstorepotentialhasbeenestimatedseparatelyasthisisapotentialtenantthatcouldoccupybothlevelstwoandthreeofthesubjectdevelopment.

AsshowninFigure4‐4,TradeArearesidents’departmentstoreexpenditureshavebeenestimatedat$65.6millionin2012,increasingto$88.3millionin2021,agrowthof$22.7million.Non‐departmentstoreNFSRexpendituresareexpectedtoincreasefrom$374.4million

ResidualRetailMarketDemandAnalysis–420BathurstStreet

14

in2012,to$504.5millionby2021,agrowthof$130.1millionovertheperiod.Storetypesinthiscategorythatcouldlocateinthesubjectdevelopmentcouldincludeawiderangeoflargerformatstoresinthegeneralmerchandise,apparelandelectronics,etc.categories.

FIGURE4‐4:TRADEAREANFSREXPENDITUREPOTENTIAL

PER CAPITA NFSR EXPENDITURE POTENTIAL

2012 Dollars 2012

Province of OntarioPer Capita NFSR Expenditure $ 5,471 (1

2012 Dollars 2012 2014 2016 2021 2031

Primary Trade AreaIncome Index to Province 88.00 NFSR Expenditure Index to Province 95.20 Per Capita NFSR Expenditure $ 5,208 $ 5,234 $ 5,260 $ 5,325 $ 5,455Population 53,600 54,300 55,600 57,100 60,000 TOTAL NFSR POTENTIAL ($Millions) $ 279.1 $ 284.2 $ 292.5 $ 304.1 $ 327.3

Department Store (2 14.9% 14.9% 14.9% 14.9% 14.9%Non-Department Store NFSR (2 85.1% 85.1% 85.1% 85.1% 85.1%

100.0% 100.0% 100.0% 100.0% 100.0%

Department Store (2 $ 41.6 $ 42.4 $ 43.6 $ 45.3 $ 48.8Non-Department Store NFSR (2 $ 237.5 $ 241.8 $ 248.9 $ 258.8 $ 278.5Total $ 279.1 $ 284.2 $ 292.5 $ 304.1 $ 327.3

Secondary Trade AreaIncome Index to Province 165.50 NFSR Expenditure Index to Province 126.20 Per Capita NFSR Expenditure $ 6,904 $ 6,939 $ 6,973 $ 7,059 $ 7,232Population 23,300 29,600 35,200 40,900 52,400 TOTAL NFSR POTENTIAL ($Millions) $ 160.9 $ 205.4 $ 245.4 $ 288.7 $ 379.0

Department Store (2 14.9% 14.9% 14.9% 14.9% 14.9%Non-Department Store NFSR (2 85.1% 85.1% 85.1% 85.1% 85.1%

100.0% 100.0% 100.0% 100.0% 100.0%Department Store (2 $ 24.0 $ 30.6 $ 36.6 $ 43.0 $ 56.5Non-Department Store NFSR (2 $ 136.9 $ 174.8 $ 208.8 $ 245.7 $ 322.5

Total $ 160.9 $ 205.4 $ 245.4 $ 288.7 $ 379.0

TOTAL TRADE AREATOTAL NFSR POTENTIAL ($Millions) $ 440.0 $ 489.6 $ 537.9 $ 592.8 $ 706.3

Cumulative Growth $ 49.6 $ 97.9 $ 152.8 $ 266.3Department Store ($Millions) $ 65.6 $ 73.0 $ 80.2 $ 88.3 $ 105.3

Cumulative Growth $ 7.4 $ 14.6 $ 22.7 $ 39.7Non-Department Store NFSR ($Millions) $ 374.4 $ 416.6 $ 457.7 $ 504.5 $ 601.0

Cumulative Growth $ 42.2 $ 83.3 $ 130.1 $ 226.6

SOURCE: urbanMetrics inc.1) Based on Statistics Canada, Retail Trade. 2) urbanMetrics inc. estimate based on the provincial average.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

15

4.2.2 RESIDUALDEPARTMENTSTOREANALYSIS

ThissectionexaminesthepotentialdepartmentstorepotentialavailableintheTradeArea(Figure4‐5).TherearenodepartmentstoresineitherthePrimaryorSecondaryTradeAreas.TheclosestdepartmentstorestothesubjectsitearetheWalmartintheDufferinMall,locatedapproximately2kilometerswestofthesite,andSearsandtheBayintheTorontoEatonCentre,whichareapproximately2kilometerstotheeast.

OurestimateofdepartmentstoreexpenditurepotentialintheTradeAreareflectsthefollowingassumptions:

Recapture:ItisassumedthatadepartmentstoreonthesubjectsitewillrecaptureexpendituresthatTradeArearesidentscurrentlymakeoutsidetheTradeArea.In2012theTradeAreashareinbothzonesis0%astherearenodepartmentstoresintheTradeAreaandlocalresidentsmustgoelsewheretomakedepartmentstorepurchases.TheTradeAreasharehasbeenincreasedto50%inthePrimaryTradeAreaand30%intheSecondaryTradeAreain2014toreflecttheentryofanewdepartmentstoresuchasaWalmartorTargetatthesubjectsite.

Inflow:Inflowsaleshavebeenassumedat20%forthenewdepartmentstore,whichinourviewisaveryconservativelevelinanurbanmarket.

SalesLevels:Theaveragesalesperformanceutilizedinouranalysisfornewdepartmentstorespacehasbeentestedat$450to$500persquarefoot,whichisconsideredatypical,ifnothigh,performancelevelfordepartmentstoressuchasWal‐MartorTarget.

Basedonouranalysis,itisestimatedthattheresidualsalespotentialintheTradeAreawillbe$30.4millionin2014,increasingto$35.6millionin2021.Assumingaconservative20%inflow,at$475persquarefoot,some80,000squarefeetofadditionaldepartmentstorespacewouldbewarrantedintheTradeAreaby2014,increasingto93,700squarefeetby2021atthesamesalesperformancelevel.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

16

FIGURE4‐5:DEPARTMENTSTORERESIDUALANALYSIS

DEPARTMENT STORE ANALYSIS

2012 Dollars 2012 2014 2016 2021 2031

Primary Trade AreaDepartment Store ($Millions) $ 41.6 $ 42.4 $ 43.6 $ 45.3 $ 48.8

Estimated Trade Area Share %(1 0.0% 50.0% 50.0% 50.0% 50.0%Estimated Trade Area Share ($ Millions) $ - $ 21.2 $ 21.8 $ 22.7 $ 24.4Residual Potential $ 21.2 $ 21.8 $ 22.7 $ 24.4

Secondary Trade AreaDepartment Store ($Millions) $ 24.0 $ 30.6 $ 36.6 $ 43.0 $ 56.5

Estimated Trade Area Share %(1 0.0% 30.0% 30.0% 30.0% 30.0%Estimated Trade Area Share ($ Millions) $ - $ 9.2 $ 11.0 $ 12.9 $ 17.0Residual $ 9.2 $ 11.0 $ 12.9 $ 17.0

TOTAL TRADE AREATotal Department Store Expenditures ($Millions) $ 65.6 $ 73.0 $ 80.2 $ 88.3 $ 105.3Total Estimated Trade Area Share ($Millions) $ - $ 30.4 $ 32.8 $ 35.6 $ 41.4Estimated Trade Area Share % 0.0% 41.6% 40.9% 40.3% 39.3%

Existing Sales from Trade Area Residents ($Millions) $ - $ - $ - $ - $ -Residual Potential ($Millions) $ 30.4 $ 32.8 $ 35.6 $ 41.4

TOTAL DEPARTMENT STORE RESIDUAL POTENTIAL (including inflow)Additional Residual Potential Available $ 30.4 $ 32.8 $ 35.6 $ 41.4Plus Inflow Sales @ 20.0% (2 $ 7.6 $ 8.2 $ 8.9 $ 10.4TOTAL ADDITIONAL SALES POTENTIAL AVAILABLE $ 38.0 $ 41.0 $ 44.5 $ 51.8

WARRANTED ADDITIONAL SQUARE FEET (3

@ $450 per sq. ft. 84,400 91,100 98,900 115,000 @ $475 per sq. ft. 80,000 86,300 93,700 108,900 @ $500 per sq. ft. 76,000 82,000 89,000 103,500

SOURCE: urbanMetrics inc. NOTE: 1) urbanMetrics estimate. There are currently no department stores in the Primary or Secondary Trade Areas.

2) urbanMetrics estimate.

3) Rounded to the nearest 100 square feet.

4.2.3 RESIDUALNON‐DEPARTMENTSTORENFSRANALYSIS

Inthissectionwehaveexaminedthepotentialnon‐departmentstoreNFSRexpenditurepotentialavailableintheTradeArea(Figure4‐6).Aspartofthisanalysis,wehavepreparedadetailedinventoryoftheKensingtonMarketBIA,theChinatownBIA,theLittleItalyBIAandtheTrinity‐BellwoodsBIA.WhilethesefourBIA’sdonotrepresentallofthenon‐departmentstoreNFSRspaceintheTradeArea,theyrepresentasizableportion.Basedonthisanalysis,whichhasbeencarriedoutusingasimilarmethodologytothedepartmentstoreanalysis,thereisresidualpotentialof$40.2millioninthenon‐departmentstoreNFSRcategoryavailablefromTradeArearesidentsin2014,increasingto$62.0millionin2021.ThisgrowthinresidualpotentialwouldsupportasignificantamountofnewNFSRspaceintheTradeAreainfutureyears.Atasalesperformancelevelof$400persquarefoot,125,600squarefeetofnewnon‐departmentstoreNFSRspacewouldbewarrantedby2014,andthisincreasesto193,800

ResidualRetailMarketDemandAnalysis–420BathurstStreet

17

squarefeetby2021.Thisiswellinexcessoftheamountofnon‐departmentstoreNFSRspacethatisproposedatthe420BathurstStreetdevelopment.

FIGURE4‐6:NON‐DEPARTMENTSTORENFSRRESIDUALANALYSIS

NON-DEPARTMENT STORE NFSR ANALYSIS

2012 Dollars 2012 2014 2016 2021 2031

Primary Trade AreaNon-Department Store NFSR ($Millions) $ 237.5 $ 241.8 $ 248.9 $ 258.8 $ 278.5

Estimated Trade Area Share %(1 35.0% 45.0% 45.0% 45.0% 45.0%Estimated Trade Area Share ($ Millions) $ 83.1 $ 108.8 $ 112.0 $ 116.5 $ 125.3Residual Potential $ 25.7 $ 28.9 $ 33.4 $ 42.2

Secondary Trade AreaNon-Department Store NFSR ($Millions) $ 136.9 $ 174.8 $ 208.8 $ 245.7 $ 322.5

Estimated Trade Area Share %(1 15.0% 20.0% 20.0% 20.0% 20.0%Estimated Trade Area Share ($ Millions) $ 20.5 $ 35.0 $ 41.8 $ 49.1 $ 64.5Residual $ 14.5 $ 21.3 $ 28.6 $ 44.0

TOTAL TRADE AREATotal Non-Department Store NFSR ($Millions) $ 374.4 $ 416.6 $ 457.7 $ 504.5 $ 601.0Total Estimated Trade Area Share ($Millions) $ 103.6 $ 143.8 $ 153.8 $ 165.6 $ 189.8Estimated Trade Area Share % 27.7% 34.5% 33.6% 32.8% 31.6%

Existing Sales from Trade Area Residents ($Millions) $ 103.6 $ 103.6 $ 103.6 $ 103.6 $ 103.6Residual Potential ($Millions) $ 40.2 $ 50.2 $ 62.0 $ 86.2

TOTAL NON-DEPARTMENT STORE RESIDUAL POTENTIAL (including inflow)Additional Residual Potential Available $ 40.2 $ 50.2 $ 62.0 $ 86.2Plus Inflow Sales @ 20.0% (1 $ 10.1 $ 12.6 $ 15.5 $ 21.6TOTAL ADDITIONAL SALES POTENTIAL AVAILABLE $ 50.3 $ 62.8 $ 77.5 $ 107.8

WARRANTED ADDITIONAL SQUARE FEET (2

@ $375 per sq. ft. 134,000 167,300 206,700 287,300 @ $400 per sq. ft. 125,600 156,900 193,800 269,400 @ $425 per sq. ft. 118,200 147,600 182,400 253,500

SOURCE: urbanMetrics inc. NOTE: 1) urbanMetrics estimate.

2) Rounded to the nearest 100 square feet.

Basedonthisresidualanalysis,itisourprofessionalopinionthatanyofthepotentialnon‐departmentstoreNFSRtenantsthatcouldpossiblylocateintheproposeddevelopmentcanbeeasilyaccommodatedinthemarketbasedonfuturemarketgrowthalonewithlimited,ifany,impactonexistingnearbyshoppingdistrictsintheTradeArea.Infact,thesignificantgrowthexpectedwouldalsosupportadditionalretailspaceintheseareas,aswellasprovidetheopportunityforexistingstorestoincreasetheircurrentsalesperformance.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

18

5 NEARBYSHOPPINGDISTRICTS

Thissectionofthereportexaminesthefournearbyshoppingdistrictsinthevicinityoftheproposeddevelopmentintermsoftheirretail/servicetenantmix,scaleandsizeofstores,existingfunctionandmarketsegmentsserved.TheshoppingdistrictsexaminedaretheKensingtonMarketBIA,theChinatownBIA,theLittleItalyBIA,andtheTrinityBellwoodsBIA.Eachoftheseareasisdescribedbelow.AcompleteretailandservicespaceinventoryhasbeenconductedbyurbanMetricsinc.oftheKensingtonMarketBIA,theLittleItalyBIAandtheTrinityBellwoodsBIAduringJanuary2013.IntheChinatownBIA,theinventoryincludedtheretailandserviceestablishments,asmeasuringtheactualspacebyspecificcategorywouldhavebeenimpossibleinthisarea.ThedetailedlistingofallstoresandservicesinthefourlocalshoppingdistrictsisattachedinAppendixC.

5.1 KENSINGTONMARKETBUSINESSIMPROVEMENTAREA

Figure5‐1illustratestheextentoftheKensingtonMarketBIA.AlthoughtheBIAboundaryextendsfromBathurstStreetinthewest,totheChinatownBIAintheeast,themajorityofretail/servicespaceislocatedsomedistancetotheeastoftheproposed420BathurstStreetdevelopment,alongAugustaAvenueandfurthereastalongKensingtonAvenueandBaldwinStreet.Nearlyalloftheretailersandservicesinthisareaareoneofakindandunique;infact,theBIAdiscourageschainstoresfromlocatingintheMarkettoretainitsuniquecharacter.Inadditiontotheretail/serviceoutletsalongAugustaAvenueandtotheeast,theBIAboundaryalsoincludesTorontoWesternHospital,whichhasasmallnumberofretail/serviceoutletsinthefoodcourtandinthevicinityofthebuilding.TorontoWesternHospitalalsoincludesmedicaloffices,butthesehavebeenexcludedfromtheanalysis.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

19

FIGURE5‐1:KENSINGTONMARKETBIA

SOURCE:urbanMetricsinc.basedonCityofTorontoBIAmapsBasedonourinventory,therearealmost280retail/serviceoutletsintheBIA,accountingforover330,000squarefeetofspace(Figure5‐2).TheKensingtonMarketBIAisalsocharacterizedbyalowvacancyrateofunder4.0%.Atypicalvacancyrateisnormallyinthe6%‐8%range.ManyofthefoodstoreswithintheKensingtonMarketBIAarelocatedinthesoutheasternsectionoftheBIA,mainlyalongBaldwinStreetandKensingtonAvenue.Thesefoodstoresaresomewhatremovedfromtheproposeddevelopmentat420BathurstStreetandareuniqueandverydifferentfromatraditionalsupermarket,whichmaybeatenantatthesubjectsite.ManyofthesefoodstoresalsodrawsupportfromtheentireCityofToronto,universitystudentslivingintheareaandtouristsfrombeyondtheCity.FoodstoresinKensingtonMarketwillcompetemoredirectlywithfoodstoresintheChinatownBIA,ratherthanwithapossiblesupermarketintheproposeddevelopmentat420BathurstStreet.

SimilartofoodstoresinKensingtonMarket,manyoftheclothingandaccessorystores,andmiscellaneousretailers(manyofwhichareclothingstoresthatsellusedmerchandise)arelocatedinthesoutheasternportionoftheBIA,mainlyalongKensingtonAvenue.Theseclothing

ResidualRetailMarketDemandAnalysis–420BathurstStreet

20

andaccessorystores,andmiscellaneousretailersaccountforone‐thirdoftheretail/serviceoutletsandtheamountofspaceinKensingtonMarket.Thesestoresareuniqueandareverydifferentfromadepartmentstoreorotherlarge‐scalefashionretailer,whichmaybeatenantintheproposeddevelopmentat420BathurstStreet.ThesestoresinKensingtonMarketlargelycaternotonlytolocalarearesidentsbutalsotonearbyuniversitystudents,touristsandotherGreaterTorontoArearesidents.

FoodservicesanddrinkingplacesalsoaccountforasignificantshareofthebusinessestablishmentsinKensingtonMarket.ManyoftheseestablishmentsarelocatedalongAugustaAvenueanddrawCity‐wide,appealingalsotonearbyuniversitystudents.FoodservicesanddrinkingplacesinKensingtonMarketwillnotcompetedirectlywithtenantsattractedtotheproposeddevelopmentat420BathurstStreet,aslimitedtoanyfoodservicefacilitiesarelikelytobelocatedintheproposeddevelopment.

FIGURE5‐2:KENSINGTONMARKETBIARETAILCOMPOSITION

STORE TYPE

Square

Feet Percent

Number of

Establishments Percent

Average Size of

Establishment

FOOD STORE RETAIL (FSR) 44,250 12.6 42 14.4 1,054

Supermarkets & Grocery 5,200 1.5 2 0.7 2,600

Convenience and Specialty Food Stores 39,050 11.1 40 13.7 976

BEVERAGE STORES 0 0.0 0 0.0 n.a.

Beer, Wine and Liquor Stores 0 0.0 0 0.0 n.a.

NON‐FOOD STORE RETAIL (NFSR) 134,400 38.3 107 36.6 1,256

Automotive 3,400 1.0 2 0.7 1,700

Furniture, Home Furnishings and Electronics Stores 7,500 2.1 5 1.7 1,500

Building and Outdoor Home Supply Stores 2,700 0.8 1 0.3 2,700

Pharmacies and Personal Care Stores 6,900 2.0 5 1.7 1,380

Clothing and Accessory Stores 44,000 12.5 39 13.4 1,128

Miscallaneous Retailers 69,900 19.9 55 18.8 1,271

General Merchandise Stores 0 0.0 0 0.0 n.a.

SERVICES 158,450 45.2 130 44.5 1,219

Finance 4,900 1.4 3 1.0 1,633

Insurance and Real Estate 500 0.1 1 0.3 500

Professional, Scientific and Technical Services 19,900 5.7 7 2.4 2,843

Selected Other Administrative Services 0 0.0 0 0.0 n.a.

Travel Agencies 0 0.0 0 0.0 n.a.

Automobile Rental 1,000 0.3 1 0.3 1,000

Consumer Goods Rental 500 0.1 1 0.3 500

Selected Educational Services 5,000 1.4 3 1.0 1,667

Health Care 3,600 1.0 3 1.0 1,200

Social Services 5,100 1.5 2 0.7 2,550

Cultural, Entertainment and Recreation 6,550 1.9 6 2.1 1,092

Food Services and Drinking Places 86,000 24.5 79 27.1 1,089

Personal and Household Goods Repair and Maintenance 500 0.1 1 0.3 500

Personal Care Services 16,600 4.7 18 6.2 922

Civic & Social Organizations 6,900 2.0 4 1.4 1,725

Municipal Services/Government Offices 1,400 0.4 1 0.3 1,400

VACANT 13,700 3.9 13 4.5 1,054

TOTAL 350,800 100.0 292 100.0 1,201

SOURCE:urbanMetricsinc.basedoninventoryconductedinJanuary2013

AlsoshowninFigure5‐2,theaveragestoresizeintheKensingtonMarketBIAisonly1,201squarefeet,significantlydifferentfromthetypeofstoresproposedat420BathurstStreet.This

ResidualRetailMarketDemandAnalysis–420BathurstStreet

21

providesanotherindicatorofthedifferenceinthetypeofstoresinthelocalshoppingdistrictcomparedtothoseinthesubjectproposal.

Basedonourreviewoftheinventorydata,itremainsouropinionthatthelargeformatretailfacilitiesattractedtothesecondandthirdfloorsoftheproposeddevelopmentat420BathurstStreetwillbeunliketheretailersinKensingtonMarket,whichareuniqueandspecialized,andwillnotnegativelyaffectthecontinuedviabilityofbusinessesinthisarea.Thisisdue,inpart,totheKensingtonMarketBIAdoinganexcellentjobatpromotingitselfCity‐wideandtovisitingtourists.Eventssuchas“PedestrianSundays”,wherestreetsareclosedtotraffic,havebeenverysuccessfulinattractingnewpatronstotheBIAandwilllikelycontinuetodoso,evenwiththeproposeddevelopmentofaretailfacilityat420BathurstStreet.KensingtonMarket’suniquemixofretail/servicespacealsoappealstoandissupportedstronglybylocalresidents.Inouropinion,thisstronglocalsupportwillcontinue,andtheresidualanalysiscontainedearlierinthisreportdemonstratethatthenewspaceproposedat420BathurstStreetiswarranted,withoutanytransfersofsalesfromexistingstoresintheTradeArea.

5.2 CHINATOWNBUSINESSIMPROVEMENTAREA

TheboundariesoftheChinatownBIAareillustratedinFigure5‐1.Thisareaisamajorethnic‐orientedretailarealocatedonSpadinaAvenue,betweenCollegeStreetandSullivanStreet;andalongDundasStreetbetweenAugustaAvenueandBeverleyStreet.TheChinatownBIAistheshopping,culturalandsocialfocalpointfortheChinesecommunityintheCityofTorontoandtheGreaterTorontoArea.AsignificantportionoftheretailersintheBIAareEastAsianrestaurants,apparelandaccessories,giftandsouvenirstores,beautyparlorsandhairsalons,mainlyorientedtoToronto’slargeEastAsiancommunity.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

22

FIGURE5‐3:CHINATOWNBIA

SOURCE:urbanMetricsinc.basedonCityofTorontoBIAmaps

ThesefourmostcommontypesoffacilitiesintheareacombinedmakeupnearlyhalfofallthestoresandservicesintheChinatownBIA.Figure5‐4showstheretailcompositionoftheChinatownBIA,categorizedbytheNAICS.Asindicatedearlierinthereport,theChinatownBIAinventoryinFigure5‐4includesretailandserviceestablishments,asmeasuringtheactualspacebyspecificcategorywouldhavebeenimpossibleinthisarea.ThereareafairnumberofvacanciesintheBIA,themajorityofwhicharelocatedinChinatownCentre(62ofthe87vacantunitsintheBIA),anenclosedmallfrontingSpadinaAvenuethatcontainsaSuper8HotelandHSBCasitsanchortenants.ItishoweverimportanttonotethatmostofthevacanciesinChinatownCentrearefoodcourtvendors,kiosksandsmallretailspaces.Itisimportanttonotethatvacanciesaccountforonly4.5%ofthetotalnumberofoutletsintheChinatownBIAthatarenotwithintheenclosedmallssuchasChinatownCentreandDragonCity.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

23

FIGURE5‐4:CHINATOWNBIARETAILCOMPOSITION

SOURCE:urbanMetricsinc.basedoninventoryconducedinJanuary2013andChinatownBIAbusinessdirectory

TheChinatownBIAisrecognizedasamajortouristdestinationintheCity,andispromotedassuch.TheareahasbeenabletomaintainitsprominenceandattractionfortheEastAsiancommunity,despitetheformationofmultipleother“Chinatowns”inotherpartsoftheCityofTorontoandGreaterTorontoArea.TheChinatownBIAcatersnotonlytoalargelylocalizedethnicmarket,butmoreimportantlyrepresentsamajorregionalandtouristattraction.Inourprofessionalopinion,thelargeformatretailfacilitiesproposedforthesubjectdevelopmentat420BathurstStreetarevastlydifferentfromtheretailandservicetenantsintheChinatownBIA.Moreover,itishighlyunlikelythattheChinatownBIAwillbeadverselyimpactedbytheproposeddevelopmentastheBIAisaverypedestrianorientedandtransitaccessibleshoppingdistrict.

5.3 LITTLEITALYBUSINESSIMPROVEMENTAREA

Figure5‐5illustratestheboundariesoftheLittleItalyBIA,whichismainlylocatedonthenorthandsouthsidesofCollegeStreetfromShawStreetinthewesttoBathurstStreetintheeast.Basedonourinventory,thereareapproximately300retail/serviceoutletswithintheBIA,accountingforover500,000squarefeetofspace(Figure5‐6).Nearlythree‐quartersoftheseretail/serviceoutletsareserviceoriented,themajorityofwhicharefoodservicesanddrinkingplaces,andhealthcarerelated.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

24

FIGURE5‐5:LITTLEITALYBIA

SOURCE:urbanMetricsinc.basedonCityofTorontoBIAmaps

BusinessesintheBIAarecharacterizedbyhigher‐endrestaurantsanddrinkingplacesthatareamajorCity‐wideattraction,cateringtopeopleinsideandoutsidetheTradeArea.ManyofthesefoodservicesanddrinkingplacesarelocatedinthewesternportionoftheBIA,awayfromtheproposeddevelopmentat420BathurstStreet.TheeasternpartoftheBIAischaracterizedbyhealthcarerelatedoutlets,dueinparttotheproximitytotheTorontoWesternHospital.Theseretail/serviceoutletsincludemedicalofficebuildings,andpharmaciesandpersonalcarestores.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

25

FIGURE5‐6:LITTLEITALYBIARETAILCOMPOSITION

Store Type

Square

Feet Percent

Number of

Establishments Percent

Average Size of

Establishment

FOOD STORE RETAIL (FSR) 37,300 7.0 11 3.4 3,391

Supermarkets & Grocery 26,800 5.1 1 0.3 26,800

Convenience and Specialty Food Stores 10,500 2.0 10 3.1 1,050

BEVERAGE STORES 3,500 0.7 1 0.3 3,500

Beverage Stores 3,500 0.7 1 0.3 3,500

NON‐FOOD STORE RETAIL (NFSR) 82,200 15.5 53 16.6 1,551

Selected Automotive 0 0.0 0 0.0 n.a.

Furniture, Home Furnishings and Electronics Stores 15,300 2.9 5 1.6 3,060

Building and Outdoor Home Supply Stores 1,200 0.2 1 0.3 1,200

Pharmacies & Personal Care 25,700 4.9 12 3.8 2,142

Apparel and Accessories 16,500 3.1 14 4.4 1,179

Other Miscellaneous 22,200 4.2 20 6.3 1,110

General Merchandise 1,300 0.2 1 0.3 1,300

SERVICES 378,700 71.5 239 74.7 1,585

Finance 22,400 4.2 9 2.8 2,489

Other 67,050 12.7 34 10.6 1,972

Automobile Rental 0 0.0 0 0.0 n.a.

Consumer Goods Rental 1,000 0.2 1 0.3 1,000

Selected Educational Services 16,100 3.0 5 1.6 3,220

Health Care 70,500 13.3 66 20.6 1,068

Social Services 14,650 2.8 5 1.6 2,930

Cultural, Entertainment & Recreation 14,400 2.7 4 1.3 3,600

Food Services & Drinking Places 148,500 28.0 89 27.8 1,669

Personal & Household Goods Repair & Maintenance ‐ Auto 2,600 0.5 1 0.3 2,600

Personal & Household Goods Repair & Maintenance ‐ Other 1,800 0.3 3 0.9 600

Personal Care 17,400 3.3 20 6.3 870

Selected Civic & Social Organizations 1,100 0.2 1 0.3 1,100

Religious Organizations 0 0.0 0 0.0 n.a.

Municipal Services/Government Offices 1,200 0.2 1 0.3 1,200

VACANT 28,100 5.3 16 5.0 1,756

TOTAL 529,800 100.0 320 100.0 1,656

SOURCE:urbanMetricsinc.basedoninventoryconductedinJanuary2013

Overall,theLittleItalyBIAappearsveryhealthy,withalowvacancyrateof5.3%.ThelargeconcentrationoffoodservicesanddrinkingplaceslocatedthroughouttheBIAwillnotbeimpactedbythelargerformatretailfacilitiesattractedtothesubjectsite,aslimitedifanyspaceofthistypeisproposed.Whileasupermarketisapossibletenantinthe420BathurstStreetdevelopment,itisunlikelytohaveanimpactontheMetrolocatedalargedistanceawayatShawStreetandCollegeStreet.TheMetroislocatedonthewesternboundaryofthePrimaryTradeArea,andthereforelikelyattractsalargeshareofitssalesfromoutsidethePrimaryTradeAreaboundary.InadditiontotheMetro,mostofthespecializedgroceryandfreshfoodshopslocatedintheBIAareinthewesternportion,closetotheMetro,andthereforealsolikelyattractcustomersfromoutsidethePrimaryTradeAreaboundary.Therefore,itisouropinionthatthelargerformatretailfacilitiesthatwouldlikelybeattractedtotheproposeddevelopmentat420Bathurstareverydifferentfromtheretail/serviceoutletsintheLittleItalyBIA.Inaddition,thepredominantstoresizesintheLittleItalyBIA,whichaverage1,656squarefeet,areverydifferentfromthestoresizesproposedonthesubjectsite.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

26

5.4 TRINITYBELLWOODSBUSINESSIMPROVEMENTAREA

TheboundariesoftheTrinityBellwoodsBIAareillustratedinFigure5‐7.TheareaextendsfromBathursttoGraceStreet(byTrinityBellwoodsPark)alongDundasStreetWest.Theshoppingdistrictcontainsover140establishmentsandisheavilyorientedtowardservicebasedfacilities.Withintheservicecategory,foodservicesanddrinkingplacescomprisethelargestamountofspaceandnumberofestablishmentsintheBIA.Furthermore,theretailandservicefacilitiesintheTrinityBellwoodsBIAarelargelyorientedtoservinglocalarearesidents.

FIGURE5‐7:TRINITYBELLWOODSBIA

SOURCE:urbanMetricsinc.basedonCityofTorontoBIAmaps

Figure5‐8showstheretailcompositionoftheTrinityBellwoodsBIA.Despitethelargenumberofvacancies,thisretailstripalongDundashasrecentlybeguntogentrify,asseveralnewrestaurants,cafesandbarshaveopened.Thesenewestablishmentsarehighlyunlikelytobenegativelyimpactedbythesubjectproposalastheyaredifferentfromtheusesproposedat420BathurstStreet.Furthermore,veryfewcomparisonretailstoresarelocatedinthisBIA,withlittleapparelandfurniture,homefurnishingsandelectronicsoutlets,whichmayultimatelybethetypeofstoresoccupyingthesecondandthirdfloorsoftheproposeddevelopment.Inaddition,nosupermarketsarelocatedintheareaandthereforeifsuchastoreweretobeincludedat420BathurstStreet,therewouldbenoimpactonthislocallyorientedretailarea.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

27

FIGURE5‐8:TRINITYBELLWOODSBIARETAILCOMPOSITION

SOURCE:urbanMetricsinc.basedoninventoryconductedinJanuary2013

Thelargeformatretailfacilitieslikelytooccupythesecondandthirdfloorsoftheproposeddevelopmentat420BathurstStreetwillbeverydifferentfromtheestablishmentsintheTrinityBellwoodsBIAbothintypeandsize(theaveragestoresizewithintheBIAis1,503squarefeet).VirtuallyalltheestablishmentsintheBIAaresmallscale,localservingservicesandretailers.Theareaisheavilyorientedtowardservicefacilities,withfoodservicesanddrinkingplacescomprisingthelargestamountofspaceandestablishmentsintheBIA.ItisalsoimportanttonotethatthenewNeroCondoandtownhomedevelopmentsatDundasStreetandManningAvenuewillincreaselocalmarketsupportforstoresandservicesintheTrinityBellwoodsBIAaswellasprovideadditionalcustomersupportforthesubjectproposal.Inourprofessionalopinion,itishighlyunlikelythattheproposeddevelopmentwillhaveanadverseimpactontheTrinityBellwoodsBIA.Infact,thelackofasupermarketintheBIA,thedevelopmentofnewresidentialprojectsintheareaandtherecentadditionofnewindependentserviceestablishmentsarefactorswillhelprevitalizethatmorelocalservingBIA.

Basedonadetailedinventoryofallretailandservicefacilitiesinthefournearbyshoppingdistricts,ourprofessionalopinionremainsthatthesubjectproposalwillhaveverylittle,ifany,impactonthefourlocalshoppingdistricts,andtheeconomichealthofthesenearbyshoppingdistrictswillnotbeadverselyaffected.Tenantsattractedtotheproposeddevelopmentwillbeverydifferentfromthenearbyshoppingdistrictsintermsoftenanttypeandsize.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

28

APPENDIXA–RETAILMARKETREVIEW–420BATHURSTSTREET

ResidualRetailMarketDemandAnalysis–420BathurstStreet

29

ResidualRetailMarketDemandAnalysis–420BathurstStreet

30

ResidualRetailMarketDemandAnalysis–420BathurstStreet

31

ResidualRetailMarketDemandAnalysis–420BathurstStreet

32

ResidualRetailMarketDemandAnalysis–420BathurstStreet

33

ResidualRetailMarketDemandAnalysis–420BathurstStreet

34

ResidualRetailMarketDemandAnalysis–420BathurstStreet

35

ResidualRetailMarketDemandAnalysis–420BathurstStreet

36

ResidualRetailMarketDemandAnalysis–420BathurstStreet

37

ResidualRetailMarketDemandAnalysis–420BathurstStreet

38

ResidualRetailMarketDemandAnalysis–420BathurstStreet

39

ResidualRetailMarketDemandAnalysis–420BathurstStreet

40

ResidualRetailMarketDemandAnalysis–420BathurstStreet

41

ResidualRetailMarketDemandAnalysis–420BathurstStreet

42

ResidualRetailMarketDemandAnalysis–420BathurstStreet

43

ResidualRetailMarketDemandAnalysis–420BathurstStreet

44

ResidualRetailMarketDemandAnalysis–420BathurstStreet

45

APPENDIXB–TRADEAREAPOPULATIONPROJECTIONS

ThisappendixpresentsbackgrounddatausedinpreparingpopulationprojectionfortheTradeArea:

Table1:Historicandforecastpopulationinexistingunits Table2:PrimaryTradeArearesidentialdevelopmentapplications Table3:SecondaryTradeArearesidentialdevelopmentapplications

TABLE1:HISTORICANDFORECASTPOPULATIONINEXISTINGUNITS

1996 2001 2006 2011 2014 2016 2021 2026 2031

Primary Trade Area

Adjusted Population 52,046 51,810 49,885 53,213 52,893 52,681 52,156 51,635 51,119

Occupied Dwelling Units 18,990 20,293 20,489 22,299 22,299 22,299 22,299 22,299 22,299

PPU3

2.74 2.55 2.43 2.39 2.37 2.36 2.34 2.32 2.29

Secondary Trade Area

Adjusted Population 7,862 11,658 15,311 20,171 19,764 19,498 18,847 18,218 17,610

Occupied Dwelling Units 3,290 5,597 8,490 11,973 11,973 11,973 11,973 11,973 11,973

PPU3

2.39 2.08 1.80 1.68 1.65 1.63 1.57 1.52 1.47

Trade Area

Adjusted Population 59,909 63,468 65,197 73,384 72,658 72,179 71,003 69,853 68,730

Occupied Dwelling Units 22,280 25,890 28,979 34,272 34,272 34,272 34,272 34,272 34,272

PPU3

2.69 2.45 2.25 2.14 2.12 2.11 2.07 2.04 2.01

1

2

3

Source: urbanMetrics inc. based on Census of Canada

Historic1

Forcast Population in Existing Units2

Based on 1996, 2001, 2006 and 2011 Census of Canada. Data were adjusted to account for the net Census undercoverage, using Statistics

Canada data for the Toronto Census Division. The adjustment factors were 3.11% in 1996, 4.47% in 2001, 4.29% in 2006 and 4.92% in

2011.

Forecast population is only for the population in dwelling units that were completed and occupied at the time of the 2011 Census. This

excludes forecast population in units completed after the 2011 Census of Canada.

PPU factors from 1996 to 2011 are calculated by dividing the adjusted population in the Trade Area by the number of occupied dwelling

units. The forecast PPU factors for each year of the future study period are urbanMetrics inc. estimates, derived by applying half of the

average annual change in persons per unit between 2006 and 2011 to the historic persons per unit factors in 2011 for the intervening

ResidualRetailMarketDemandAnalysis–420BathurstStreet

46

TABLE2:PRIMARYTRADEAREARESIDENTIALDEVELOPMENTAPPLICATIONS

Address

Single‐

Detached

Semi‐

Detached Row Apartment Total

Assumed Period

of Completion

15 Augusta Ave. 0 0 3 0 3 2011‐2014

202 Bathurst St. 0 0 0 24 24 2011‐2014

386 Bathurst St. 0 0 0 4 4 2011‐2014

783 Bathurst St. 0 0 6 195 201 2011‐2014

15 Beverley St. 0 0 0 96 96 2011‐2014

207 Beverley St. 0 0 8 0 8 2011‐2014

506 College St. 0 0 4 0 4 2011‐2014

799 College St. 0 0 0 21 21 2011‐2014

856 Dundas St. W. 0 0 10 82 92 2011‐2014

84 Harbord St. 0 0 0 3 3 2011‐2014

99 Harbord St. 0 0 0 1 1 2011‐2014

250 Manning Ave. 0 0 45 0 45 2011‐2014

103 & 109‐111 Ossington Ave. 0 0 0 86 86 2011‐2014

41 Ossington Ave. 0 0 5 23 28 2011‐2014

50 Ryerson Ave. 3 0 0 0 3 2011‐2014

682 Bathurst St. 0 0 0 19 19 2014‐2016

308 Dundas St. W. 0 0 0 10 10 2014‐2016

54 Kensington Ave. 0 0 0 6 6 2014‐2016

790 Queen St. W. 0 0 0 32 32 2014‐2016

486 Shaw St. 0 0 37 0 37 2014‐2016

210 Simcoe St. 0 0 0 298 298 2014‐2016

426 University Ave. 0 0 0 312 312 2014‐2016

243 College 0 0 0 121 121 2016‐2031

297 College St. 0 0 0 239 239 2016‐2031

571 Dundas St. W. 0 0 6 1,534 1,540 2016‐2031

944‐952 Queen St. W. 0 0 0 151 151 2016‐2031

170 Spadina Ave. 0 0 0 210 210 2016‐2031

270 Spadina Ave. 0 0 0 103 103 2016‐2031

480 Univeristy Ave. 0 0 0 453 453 2016‐2031

New Dwelling Units by Assumed Period of Completion

2011‐2014 3 0 81 535 619

2014‐2016 0 0 37 677 714

2016‐2031 0 0 6 2,811 2,817

2011‐2031 3 0 124 4,023 4,150

Estimated PPU1

3.05 3.00 3.12 2.10

Population in New Dwelling Units by Assumed Period of Completion

2011‐2014 9 0 252 1,124 1,385

2014‐2016 0 0 115 1,422 1,537

2016‐2031 0 0 19 5,903 5,922

2011‐2031 9 0 386 8,449 8,844

Source: urbanMetrics inc. based on information from the City of Toronto

1 urbanmetrics inc. estimate based on 2011 Census of Canada for the City of Toronto and the Primary

Trade Area.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

47

TABLE3:SECONDARYTRADEAREARESIDENTIALDEVELOPMENTAPPLICATIONS

Address

Single‐

Detached

Semi‐

Detached Row Apartment Total

Assumed Period

of Completion

399 Adelaide St. W. 0 0 0 173 173 2011‐2014

32 Camden St. 0 0 0 87 87 2011‐2014

300 Front St. W. 0 0 0 671 671 2011‐2014

352 Front St. W. 0 0 0 458 458 2011‐2014

560 Front St. W. 0 0 0 305 305 2011‐2014

60 John. St. 0 0 0 412 412 2011‐2014

1030 King St. W. 0 0 0 602 602 2011‐2014

224 King St. W. 0 0 0 234 234 2011‐2014

375 King St. W. 0 0 0 274 274 2011‐2014

430 King St. W. 0 0 0 314 314 2011‐2014

478 King St. W. 0 0 0 180 180 2011‐2014

560 King St. W. 0 0 0 334 334 2011‐2014

650 King St. W. 0 0 0 233 233 2011‐2014

751 King St. W. 0 0 0 350 350 2011‐2014

2 Lisgar St. 0 0 0 212 212 2011‐2014

589 Queen St. W 0 0 0 90 90 2011‐2014

635 Queen St. W. 0 0 0 4 4 2011‐2014

25 Stafford St. 0 0 0 104 104 2011‐2014

170 Sudbury St. 0 0 0 135 135 2011‐2014

180 University Ave. 0 0 0 393 393 2011‐2014

83 Walnut Ave. 0 0 7 0 7 2011‐2014

175 Wellington St. W. 0 0 0 134 134 2011‐2014

350 Wellington St. W. 0 0 0 55 55 2011‐2014

354 Wellington St. W 0 0 0 280 280 2011‐2014

400 Wellington St. W. 0 0 0 102 102 2011‐2014

500 Wellington St. W. 0 0 0 16 16 2011‐2014

21 Widmer St. 0 0 0 444 444 2011‐2014

283 Adelaide St. W. 0 0 0 364 364 2014‐2016

295 Adelaide St. W. 0 0 0 564 564 2014‐2016

338 Adelaide St. W 0 0 0 429 429 2014‐2016

434 Adelaide St. W. 0 0 0 243 243 2014‐2016

103 Bathurst St. 0 0 0 255 255 2014‐2016

56 Blue Jays Way 0 0 0 342 342 2014‐2016

11 Charlotte St. 0 0 0 232 232 2014‐2016

620 King St. W. 0 0 0 15 15 2014‐2016

621 King St. W. 0 0 0 404 404 2014‐2016

24 Mercer St. 0 0 0 27 27 2014‐2016

8 Mercer St. 0 0 0 337 337 2014‐2016

90 Niagara St. 0 0 0 45 45 2014‐2016

117 Peter St. 0 0 0 410 410 2014‐2016

101 Portland St. 0 0 0 6 6 2014‐2016

431 Richmond St. W. 0 0 0 190 190 2014‐2016

842 Richmond St. W. 0 0 20 0 20 2014‐2016

456 Wellington St. W. 0 0 0 28 28 2014‐2016

508 Wellington St. W. 0 0 0 87 87 2014‐2016

263 Adelaide St W. 0 0 0 328 328 2016‐2031

290 Adelaide St. W 0 0 0 383 383 2016‐2031

525 Adelaide St. W. 0 0 0 440 440 2016‐2031

28 Bathurst St. 0 0 0 564 564 2016‐2031

ResidualRetailMarketDemandAnalysis–420BathurstStreet

48

99 Blue Jays Way 0 0 0 157 157 2016‐2031

156 Front St. W 0 0 0 620 620 2016‐2031

578 Front St. W. 0 0 0 1,200 1,200 2016‐2031

1071 King St. W. 0 0 0 205 205 2016‐2031

266‐322 King St. W. 0 0 0 2,709 2,709 2016‐2031

327 King St. W. 0 0 0 304 304 2016‐2031

355 King St. W. 0 0 0 807 807 2016‐2031

357 King St. W. 0 0 0 350 350 2016‐2031

367 King St. W. 0 0 0 62 62 2016‐2031

401‐409 King St. W. 0 0 0 443 443 2016‐2031

15 Mercer St. 0 0 0 566 566 2016‐2031

21 Nelson St. 0 0 0 383 383 2016‐2031

89‐109 Niagara St. 0 0 0 359 359 2016‐2031

353 Adelaide St. W. 0 0 0 35 35 2016‐2031

81 Peter St. 0 0 0 598 598 2016‐2031

1001 Queen St. W. 0 0 0 179 179 2016‐2031

219 Queen St. W. 0 0 0 196 196 2016‐2031

181 Richmond St. W. 0 0 0 746 746 2016‐2031

306 Richmond St. W. 0 0 0 402 402 2016‐2031

324 Richmond St. W. 0 0 0 295 295 2016‐2031

520 Richmond St. W. 0 0 0 108 108 2016‐2031

40 Widmer St. 0 0 0 380 380 2016‐2031

New Dwelling Units by Assumed Period of Completion

2011‐2014 0 0 7 6,596 6,603

2014‐2016 0 0 20 3,978 3,998

2016‐2031 0 0 0 12,819 12,819

2011‐2031 0 0 27 23,393 23,420

Estimated PPU1

2.15 2.12 2.20 1.48

Population in New Dwelling Units by Assumed Period of Completion

2011‐2014 0 0 15 9,779 9,794

2014‐2016 0 0 44 5,898 5,942

2016‐2031 0 0 0 19,005 19,005

2011‐2031 0 0 59 34,682 34,741

Source: urbanMetrics inc. based on information from the City of Toronto

1 urbanmetrics inc. estimate based on 2011 Census of Canada for the City of Toronto and the Secondary

Trade Area.

ResidualRetailMarketDemandAnalysis–420BathurstStreet

49

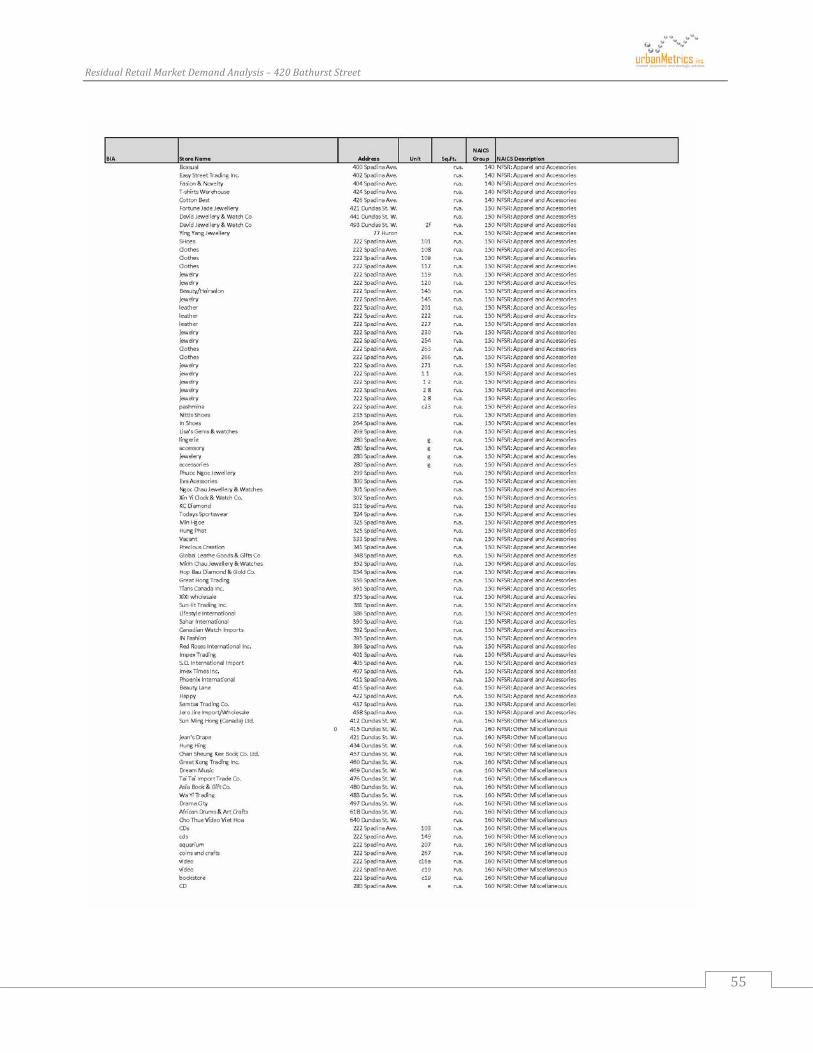

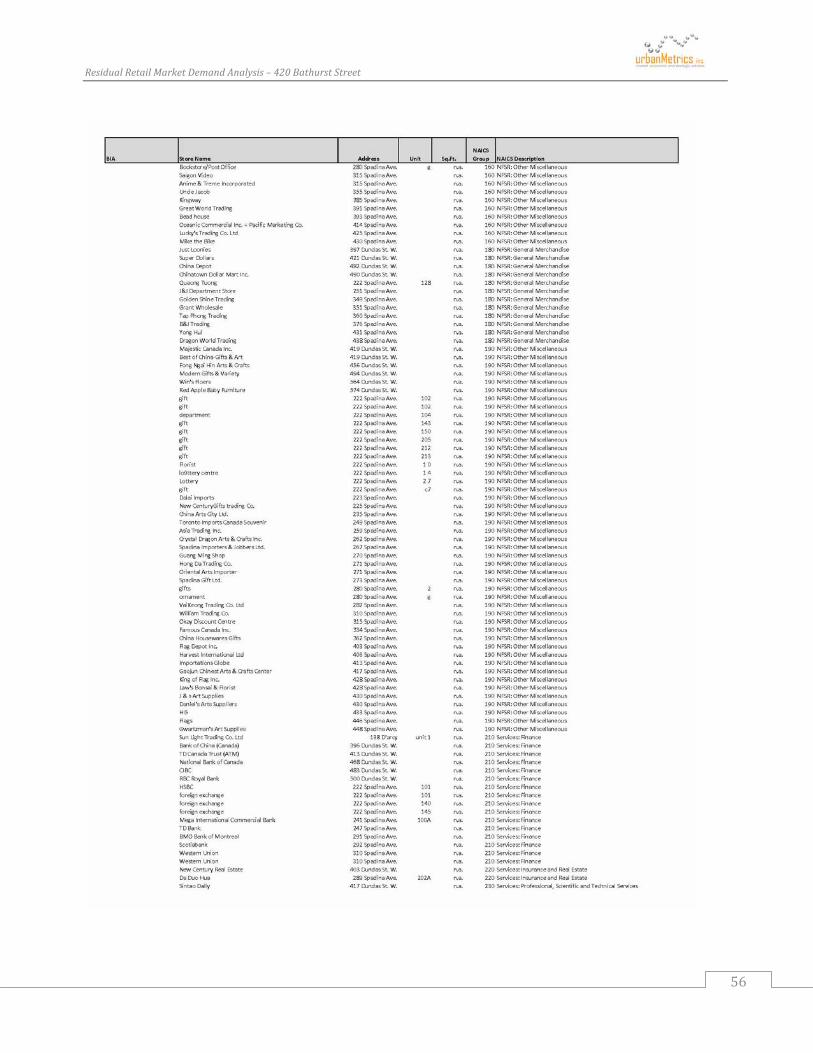

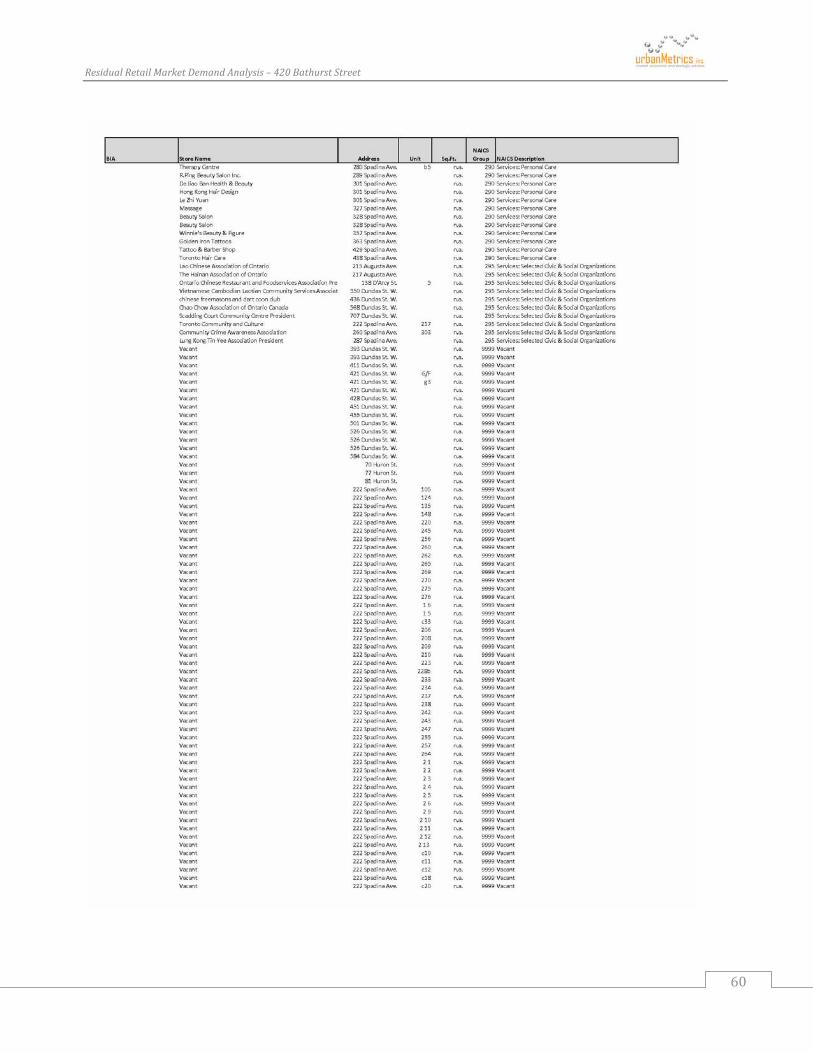

APPENDIXC–TRADEAREAINVENTORY

ResidualRetailMarketDemandAnalysis–420BathurstStreet

50

ResidualRetailMarketDemandAnalysis–420BathurstStreet

51

ResidualRetailMarketDemandAnalysis–420BathurstStreet

52

ResidualRetailMarketDemandAnalysis–420BathurstStreet

53

ResidualRetailMarketDemandAnalysis–420BathurstStreet

54

ResidualRetailMarketDemandAnalysis–420BathurstStreet

55

ResidualRetailMarketDemandAnalysis–420BathurstStreet

56

ResidualRetailMarketDemandAnalysis–420BathurstStreet

57

ResidualRetailMarketDemandAnalysis–420BathurstStreet

58

ResidualRetailMarketDemandAnalysis–420BathurstStreet

59

ResidualRetailMarketDemandAnalysis–420BathurstStreet

60

ResidualRetailMarketDemandAnalysis–420BathurstStreet

61

ResidualRetailMarketDemandAnalysis–420BathurstStreet

62

ResidualRetailMarketDemandAnalysis–420BathurstStreet

63

ResidualRetailMarketDemandAnalysis–420BathurstStreet

64

ResidualRetailMarketDemandAnalysis–420BathurstStreet

65

ResidualRetailMarketDemandAnalysis–420BathurstStreet

66