research article what causes stock market volatility in

TRANSCRIPT

Research ArticleWhat Causes Stock Market Volatility in PakistanEvidence from the Field

Bushra Ghufran1 Hayat M Awan1

Aftab Khan Khakwani2 and Muhammad Azeem Qureshi3

1Air University Multan Campus Multan Pakistan2Government Emerson College Multan Pakistan3Oslo Business School Oslo and Akershus University College of Applied Sciences Oslo Norway

Correspondence should be addressed to Muhammad Azeem Qureshi muhammad-azeemqureshihioano

Received 10 April 2016 Accepted 5 July 2016

Academic Editor David E Giles

Copyright copy 2016 Bushra Ghufran et alThis is an open access article distributed under theCreative CommonsAttribution Licensewhich permits unrestricted use distribution and reproduction in any medium provided the original work is properly cited

We examined the presence of volatility at the Karachi Stock Exchange (recently changed the name to Pakistan Stock Exchange)(KSE) by fitting Exponential Generalized Autoregressive Conditional Heteroskedasticity (EGARCH)model to 25 yearsrsquo index dataWe found that the ARCH effects are present in the data indicating the stock market cluster volatility during the period understudyWe found persistent high volatility in the stock market and presence of negative leverage effect Moreover we tried to identifythe factors causing stock market volatility by collecting and analyzing the primary data obtained from 246 individual investors ofstock market and 28 brokers listed with KSE Our results show that investors consider political situation as the most importantfactor causing turbulence in the stock market Interviews with the brokers also confirmed this The second most important factoridentified by investors is the herd behavior among investors that results in over- and underpricing of stocks and the overall marketshows a volatile behavior Our findings suggest that individual investorrsquos behavioral dimensions of involvement risk attitude andoverconfidence are significantly associated with factors causing market volatility

1 Introduction

Financialmarkets channel the savings to efficient investmentsto facilitate economic growth and development Howeverstock market volatility may be an obstacle in this processespecially in an emerging economy where high volatility inprices leads to erosion of capital from the market As suchwhat causes high volatility in the stock market is a continueddiscussion among the market experts and academiciansVolatility apparently an easy and discerning concept refers tounexpected return due to unexpected events resulting in hugeprice movements with nonconstant variance Consequentlythe financial markets develop an unexpected behavior thatmay confuse the investors

Stock market in Pakistan is highly volatile as it is verysensitive and reactive to unanticipated shocks and news Ittakes no time to affect the market activities However at thesame time Pakistani stock market is resilient that recoverssoon after shocks We observe increased participation of

the individual investors in the financial markets over timemaking them more ldquopeopledrdquo As a result their behavioractions reactions and perceptions have a continuous impacton the stock prices that traditional models fail to explainThe behavioral quirks observed in individual investors domanifest themselves on a much larger scale in the overallstock market They lead to pricing anomalies and unexplain-able movements in stock prices Behavioral finance seeks toelucidate the unjustifiable stock price volatility

The objective of this study is to find out the presenceof the stock market volatility and its behavioral causes atKarachi Stock Exchange (KSE) the largest and the oldeststock exchange of Pakistan For this purpose we use Autore-gressive Conditional Heteroskedasticity (ARCH)models andits extension Generalized ARCH (GARCH) model andEGARCH To the best of our knowledge this is the first studythat applied both the primary (survey) data of 250 investorsand brokers and secondary data of 25 year to understandstock market volatility in Pakistani context We find cluster

Hindawi Publishing CorporationEconomics Research InternationalVolume 2016 Article ID 3698297 9 pageshttpdxdoiorg10115520163698297

2 Economics Research International

volatility in a highly volatile market where political situationand herd behavior are the two most important factors thatcontribute towards market volatility

Along with Introduction we organize this paper inthe following manner Section 2 presents literature reviewSection 3 depicts the data and the methodology Section 4describes the results and their discussion and Section 5presents conclusions We provide references at the end

2 Literature Review

Volatility is a vital input to determine the overall cost ofcapital [1] Stock prices generally demonstrate nonlinear andprobably chaotic behavior However some observe that stockpricesreturns are predictable imperfectly in the short-runbut unpredictable in the long-run and statistical distributionscan measure the return unevenness Literature has identifieda number of factors that cause stock market volatility Forexample credit policy inflation interest rate corporate earn-ings financial leverage dividend policies bonds prices andmany other macroeconomic social and political variablesResearchers also find stock market volatility transmissionbetween friendly countries of different regions (eg Pakistanand China) having economic links [2] They find evidence ofreduced volatility after implementation of financial liberal-ization policies in Pakistan [3] Some suggest that that stocktradesrsquo volume causes volatility [4 5] and an asymmetricalvolatility is due to response between volume and price[6] While others observe that volatility is an outcome ofthe trading volume followed by arrival of new informationregarding new floats or any kind of private informationincorporated into market stock prices [7] Madhavan [8]describes volatility in the form of price divergence and arguesthat investors demand low volatility to minimize the needlessrisk borne by them to enable them to liquidate their assetswithout facing threat of unfavorable huge price movements

There are a number of negative implications of the stockmarket volatility One implication is that market volatilitynegatively affects the economic growth [9] and businessinvestment [10] We use econometric techniques namelyARCH model [11] and the GARCH model [12] to determinethe presence of volatility at KSE In the past different studieswere carried out to check the market volatility at KSE Forexample Ali and Laeeq [13] studied the banking sector ofKSE by fitting AR(1) ARCH(1) and GARCH(1 1) modeland they assess the fitness of model by loss function Kanasroet al [14] studied theKSE-100 index andKSE all share price byfittingARCHandGARCHmodelThey confirm the presenceof high volatility in market Moreover Saleem [15] studiedvolatility of KSE-100 index using 9-year data and concludedthat ARCH and GARCH best fit the market and confirmvolatility clustering

Behavioral finance seeks to elucidate the unjustifiablestock price volatility Studies on the stock market [16 17]and on the bond market [18] found excess volatility in thesemarkets and observed that asset prices are far more unstablethan could be explained by traditional financial modelProper justification of extreme volatility is still missing

because researchers do not have complete knowledge aboutall the aspects of the valuation models used by investorsHowever financial economists believe that disagreementin the investor opinion directly affects the security-pricevolatility and trading volume [19] Standard finance failsto enlighten an ample divergence of opinion except to callit the effect of asymmetrical information We argue thatstudying behavior related factors might help explain the phe-nomenonWhile probing the volatility-volumephenomenonresearchers found the relationship between volatility andinvestor trades [20] However majority of volatility-volumestudies have ignored the impact of heterogeneous behavior ofinvestor trades Nevertheless some argue that herd behaviorcan result in over- or underpricing and can act as a sourceof stock market volatility Individual investors may not investproper time and effort to evaluate the market but choose tofollow the aggregated assessment of the majority and conse-quently the true value of the market may be incorrect [17]

Some studies attribute the excess volatility to investorsrsquooverconfidence They argue that overconfident investors feelit is a justifiable act to trade often [21] A survey of the1987 market crash notices investorsrsquo strong confidence andan insightful outlook about the postcrash course the marketwould take [22] suggesting that overconfidencemight explainthe phenomenon of volatility and huge price deviationsShefrin and Statman [23] observe that investors commit twocommon mistakes either they consider recent observationsmore important and do not give due importance to the priorinformation or they commit a gamblerrsquos fallacy and developa belief that recent events more closely resemble long termprobabilities thereby distorting prices and causing increasedvolatility while reducing market efficiency

Asset pricing theory suggests that if investors are rationalthen stock price should equal the present value of thestockrsquos expected cash distributions to shareholders Howeverempirical evidences suggest that stock prices aremore volatilethan what standard asset pricing models can explain [16 18]Shiller [18] further attributes it to psychology or irrationalityFinding a connection between investor behavior and thedynamics of asset prices is an important challenge facingbehavioral finance The proponents of behavioral paradigmare of the view that a large number of investors act irrationallyand are prone to behavioral heuristics that result in less thanoptimal investment choices [24]

3 Data and Methodology

The objective of study is to identify the presence of stockmarket volatility at KSE and to find the reasons of volatilityfrom individual investorsrsquo behavior perspective For thispurpose we collected both secondary and primary data Forsecondary data we obtained the daily changes in KSE-100index (from httpwwwksecompk) from January 1 1990to October 1 2014 Consequent to the decline in KSE indexto very low levels the market remained frozen from August27 2008 to December 12 2008 As these values may distortour results we conducted a reality check by including thedormant values (when the market remained frozen) during

Economics Research International 3

90 92 94 96 98 00 02 04 06 08 10 12 14 90 92 94 96 98 00 02 04 06 08 10 12 140

4000

8000

12000

16000

20000

24000

28000

32000 KSE 100KSE-100 with dormant values

0

4000

8000

12000

16000

20000

24000

28000

32000 KSE 100

Figure 1 KSE-100 index

this period and then by excluding these observations to drawsound conclusions Both data sets exhibit almost the samebehaviorWe also used an alternative statisticalmethod calledwinsorization that also yielded the same results

We also collected primary data by obtaining directresponses from 246 individual investors of the stock marketand 28 brokers listed with KSEWhile doing so we first iden-tified recurring themes and factors that may cause volatil-ity through preliminary interviews with the investors andbrokers After identifying recurring themes we developedstructured questionnaires administered to the individualinvestors and brokers selected using random sampling tech-nique from fourmajor cities Lahore Islamabad Karachi andMultan We used quantitative methods to analyze responsesobtained from individual investors whereas we used qual-itative method to analyze brokersrsquo responses to our open-ended questions based interviewsWe examined the presenceof volatility at KSE by fitting ARCH GARCH and EGARCHmodels ([11 12 25])

Engle [11] proposed the ARCH model to specify condi-tional volatility that incorporates the common sense logicthat observations belonging to the recent past should gethigher weights than those belonging to the distant past TheARCH process often requires large number of parameters toexplain the dynamic structure of financial phenomenon Toovercome these problems Bollerslev [12] proposed GARCHmodel that essentially generalizes the ARCH by mod-elling the conditional covariance as an ARMA process TheGARCH model helps find cluster volatility of financial mar-kets thicker tail distribution and predictability of volatilityfrom past patternsThe following system of (1) represents theARMA(119898 119899)-GARCH(119901 119902) for stock returns (119903

119905) and stock

return volatility (ℎ119905)

119903119905= 120583 +

119898

sum119894=1

120601119894119903119905minus119894+

119899

sum119894=0

120579119894119906119905minus119894

1205790= 1

119906119905= 119911119905radicℎ119905

ℎ119905= 1205720+

119901

sum119894=1

120572119894ℎ119905minus119894+

119902

sum119895=1

1205731198951199062

119905minus119895

(1)

where 120572119894gt 0 120573

119895gt 0 and 120582

119896gt 0 for all 119894 119895 and 119896 and119885

119905sim iid

with mean 0 and variance 1The virtue of this approach is that GARCH model with

a small number of terms appears to perform better thanARCH with many terms The EGARCH model has no suchconstraint of parameters [25] The variance equation has anadvantage over the ARCH and GARCH that it tends to beautomatically positive without imposition of restriction ofnonnegativity on parameters and it captures the ldquoleverageeffectrdquo Moreover EGARCH allows the asymmetric responseof volatility to downside and upside market movements Thesystem of (2) specifies EGARCHmodel

119903119905= 120583 +

119898

sum119894=1

120601119894119903119905minus119894+

119899

sum119894=0

120579119894119906119905minus119894

1205790= 1

119906119905= 119911119905radicℎ119905

log (ℎ119905) = 1205720+

119901

sum119894=1

120572119894log (ℎ

119905minus119894) +

119902

sum119895=1

120573119895

1003816100381610038161003816100381610038161003816100381610038161003816

119906119905minus119895

ℎ119905minus119895

1003816100381610038161003816100381610038161003816100381610038161003816

+

119903

sum119896=1

120574119896

119906119905minus119896

ℎ119905minus119896

(2)

where 119885119905sim iid with mean 0 and variance 1 Since 120573

119895show

the asymmetric function that is current volatility which isinfluenced by the past standardized residuals the term 120572

119894+120573119895

shows the effect of magnitude and 120574119896is for the representation

of sign effect The volatility persistence is equal to sum120572119894and

for unconditional variance it should be less than 1Furthermore we employ Analytical Hierarchical Process

(AHP) to rank the factors causing volatility and analysis ofvariance (ANOVA) to obtain the results of this study

4 Results and Their Discussion

Before fittingARCHandGARCHwe conducted preliminarygraphical analysis of the data for heteroskedasticity Figures 1and 2 reveal huge unevenness in the observations

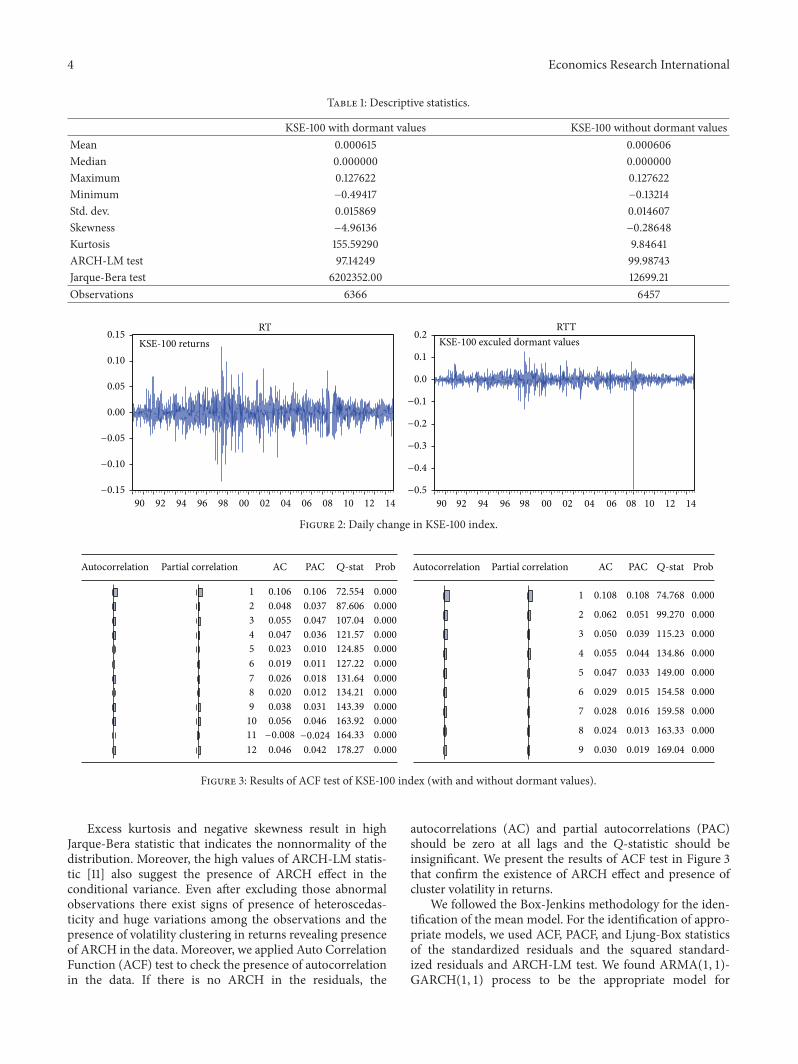

We present descriptive statistics in Table 1

4 Economics Research International

Table 1 Descriptive statistics

KSE-100 with dormant values KSE-100 without dormant valuesMean 0000615 0000606Median 0000000 0000000Maximum 0127622 0127622Minimum minus049417 minus013214Std dev 0015869 0014607Skewness minus496136 minus028648Kurtosis 15559290 984641ARCH-LM test 9714249 9998743Jarque-Bera test 620235200 1269921Observations 6366 6457

90 92 94 96 98 00 02 04 06 08 10 12 14

RT

90 92 94 96 98 00 02 04 06 08 10 12 14

RTTKSE-100 returns

minus015

minus010

minus005

000

005

010

015

minus05

minus04

minus03

minus02

minus01

00

01

02KSE-100 exculed dormant values

Figure 2 Daily change in KSE-100 index

1 0106 0106 72554 00002 0048 0037 87606 00003 0055 0047 10704 00004 0047 0036 12157 00005 0023 0010 12485 00006 0019 0011 12722 00007 0018 13164 00008 0020 0012 13421 00009 0038 0031 14339 0000

10 0056 0046 16392 000011 16433 000012 0046 0042 17827 0000

0026

-

Autocorrelation Partial correlation AC PAC Prob

minus0008 minus0024

Autocorrelation Partial correlation AC PAC Prob

1 0108 0108 74768 0000

2 0062 0051 99270 0000

3 0050 0039 11523 0000

4 0055 0044 13486 0000

5 0047 0033 14900 0000

6 0029 0015 15458 0000

7 0016 15958 0000

8 0024 0013 16333 0000

9 0030 0019 16904 0000

0028

Q-statQ-stat

Figure 3 Results of ACF test of KSE-100 index (with and without dormant values)

Excess kurtosis and negative skewness result in highJarque-Bera statistic that indicates the nonnormality of thedistribution Moreover the high values of ARCH-LM statis-tic [11] also suggest the presence of ARCH effect in theconditional variance Even after excluding those abnormalobservations there exist signs of presence of heteroscedas-ticity and huge variations among the observations and thepresence of volatility clustering in returns revealing presenceof ARCH in the data Moreover we applied Auto CorrelationFunction (ACF) test to check the presence of autocorrelationin the data If there is no ARCH in the residuals the

autocorrelations (AC) and partial autocorrelations (PAC)should be zero at all lags and the 119876-statistic should beinsignificant We present the results of ACF test in Figure 3that confirm the existence of ARCH effect and presence ofcluster volatility in returns

We followed the Box-Jenkins methodology for the iden-tification of the mean model For the identification of appro-priate models we used ACF PACF and Ljung-Box statisticsof the standardized residuals and the squared standard-ized residuals and ARCH-LM test We found ARMA(1 1)-GARCH(1 1) process to be the appropriate model for

Economics Research International 5

Table 2 Results of ARMA GARCH and EGARCH

Parameters Mean equation Variance equation120583 120601 120579 120572

01205721

1205731

120574 SBC AIC

GARCH(1 1) 000075(00000)

0766781(00000)

minus06697(00000)

0000005(00000)

0834785(00000)

0146561(00000) minus597 minus5977

EGARCH(1 1) minus00007(00000)

087746(00000)

minus07791(00000)

minus080484(00000)

092974(00000)

026901(00000)

minus00634(00000) minus595 minus59641

ARCH-LM test for GARCH119865-test 0389836 (08561) Obs lowast 1198772 19504 (08560)

conditional variance on the bases of Bayesian InformationCriterion (BIC) and Akaike Information Criterion (AIC) Inaddition the EGARCH model outperformed the GARCHcounterpart especially with Studentrsquos 119905 error as the errordistribution Therefore we use EGARCH(1 1) specificationfor variance equation In Table 2 we report the results of themean and the variance equation

The results reveal that estimated parameters ofGARCH(1 1) are highly significant The parameter 120573

1

is positive and significant This suggests that the measureof risk measured by own conditional variance indicatesthe positive and significant autocorrelation in return Theparameter 120572

1is also significant implying higher degree of

persistence Furthermore the condition 1205721+ 1205731is a measure

of volatility persistence and an estimation of the decay rateof response function on daily basis This condition reflectshow the historical conditional volatility affected the currentconditional variance of stock returns The 120572

1+ 1205731should be

less than one but in this case it is near to unity It suggests thatestimated conditional variance can be an integrated GARCH(IGARCH) process and is nonstationary The presence ofIGARCH suggests the persistence of volatility and a shockhas indefinite influence on volatility level To assess theldquoleverage effectrdquo we carried out normality test of standardizedresidualsThe JB-statistic rejected the hypothesis of normalitydue to the presence of ldquoleverage effectrdquo The coefficient 120573

1

corresponds to the asymmetric function and is statisticallysignificant indicating that current volatility is moderatelyinfluenced by the past standardized residuals Moreoverthe ldquoleverage effectrdquo term 120574

1is negative and significant

demonstrating the presence of negative ldquoleverage effectrdquoimplying that negative returns are associated with highervolatility than positive returns of equal magnitude

Robustness of Estimation GARCH(119901 119902) models are fittedto the return series using maximum-likelihood estimationIn the Gaussian quasi MLE method this estimation isdone under the assumption that the innovations [119885

119905] have

a Gaussian distribution The estimations are robust if theestimations of the parameters depend on the distributionalassumption of the innovations 119885

119905and if the residuals of the

estimated process have the same distribution as the assumeddistribution of the innovations When the estimation of theunknown parameters is done estimates of the standard devi-ation series can be calculated recursively via the definition ofthe conditional variance for the GARCH(119901 119902) process

In Figures 4(a) and 4(b) the log-return process andthe estimated conditional standard deviation process forKSE-100 index are plotted The estimated conditional stan-dard deviation process is derived from a EGARCH(1 1) fitThe estimated conditional standard deviation process reflectsthe behavior of the log-return process Based on Figure 4 theEGARCHmodel seems to be reasonable

Further with a 119876119876-Plot (Figure 5) one can examine thedistribution of the residuals to verify the robustness in theestimation With GARCH(1 1) fit using MLE under theassumption of Gaussian innovations the residuals from thefit on the simulated data are computed and plotted in a 119876119876-Plot against the normal distribution The fit is good whichindicates the process exhibits the Gaussian distribution andshows model robustness with 120572

0= minus0805 120572

1= 0930

1205731= 0269 and 120574

1= minus0063

41 Factors Causing Market Volatility After confirming pres-ence of market volatility with the help of existing literatureand preliminary interviews we identified the following sevenfactors that can cause market volatility in Pakistan

(i) News stories in the media(ii) Forecasts of the analysts(iii) Change in earnings of listed companies(iv) Herd behavior (individual investors following the

majority)(v) Government policies(vi) Political situation(vii) Manipulation by big investors

Majority of the brokers put political instability at the first rankto cause market volatility Among other major factors thatthey identified are poor government policies big investorsand their manipulations and herd behavior as the factorscausing volatility in stock market

We then asked the investors to rate the above seven factorson a scale from 1 (least important) to 7 (most important)In response to the role of media news stories to cause stockmarket volatility 159 of the investors considered it to beamong the most important factor while only 37 of theinvestors gave it the lowest rating Overall 659 of theinvestors (gave a rate of 5 or more) consider that news storiesin the media are an important factor causing stock market

6 Economics Research International

92 94 96 98 00 02 04 06 08 10 12 1490015

010

005

000

005

010

015

minus015

minus010

minus005

000

005

010

015

90 92 94 96 98 00 02 04 06 08 10 12 14

RT RT_D

minus010

minus005

000

005

010

(a)

Estimate of conditional standard deviation drived fromML estimation of EGARCH (1 1) model

90 92 94 96 98 00 02 04 06 08 10 12 14

Conditional standard deviation

90 92 94 96 98 00 02 04 06 08 10 12 14

Conditional standard deviation

000

001

002

003

004

005

006

000

001

002

003

004

005

006

(b)

Figure 4 (a) Log return of KSE-100 with dormant values (RT) and without dormant values (RT D) (b) Estimate of conditional standarddeviation drive fromML estimation of EGARCH(1 1)model with and without dormant values

Residual for estimated EGARCH (1 1) process with

015

01

005

minus005

minus01

00

00minus005minus01 005 01501

Residual

gausian innovations

Figure 5 The 119876119876-Plot Quantile-Quantile Plot

volatility Majority of the investors (63 gave rate of 4 orless) did not consider the forecasts of the analysts as animportant factor to cause volatility in the stock Regarding theimportance of changes in the earnings of the listed companiesin causing stock market volatility 138 of the investorsconsidered it as themost important factor in causing volatility

in the market while just 24 of the investors considered it asthe least important factor Overall 569 of the investors gaverating of 5 or above while 431 of the investors gave ratingof 4 or less

In response to our question regarding herd behavior caus-ing stock market volatility 26 of the investors considered itas the most important factor while just 37 of the investorsconsidered it as the least important factor Overall 825 ofthe investors gave high rating of 5 or above to herd behaviorand only 175 gave a rating of 4 or below Regarding the roleof government regulations and policies in causing volatility289 of the investors gave highest rating to this factor whilejust 04 of the investors gave the lowest rating Overall557 of the investors gave rating of 5 or above while 443of investors gave rating of 4 or less Moreover 553 of theinvestors regarded political situation of the country as themost important factor causing stockmarket volatility and just12 of the investors considered it the least important (gaverating of 1) On thewhole 886 of the investors considered itas more important factor (gave rating of 5 or above) whereas114 of the investors considered it as less important factor(gave rating of 4 or less) that causes market volatility Finally618 (highest frequency) of the investors considered the role

Economics Research International 7

Table 3 Relationship between determinants of investorsrsquo behavior and market volatility

Explanatory variables Coefficients SE of coeff Beta 119905 value 119901 valueIntercept 2551lowast 0308 8293 0000Involvement 0173lowast 0028 0335 6146 0000Risk attitude 0164lowast 0048 0187 3423 0001Optimism 0023 0037 0034 0623 0534Overconfidence 0221lowast 0040 0311 5545 0000lowastSignificant at 1 level

of manipulations by big investors as the most importantfactor (gave a rating of 7) in causing volatility but only 04of the investor as the least important factor (gave a rating of1)

We used Analytic Hierarchy Process (AHP) to findthe relative weights and ranking of these seven factors byadopting the following procedure

Step 1 We developed the hierarchical representation of theproblem by defining the factors perceived as most importantby the investors

Step 2 We compared all the factors in pairs On a scaleof 1 to 7 respondents assigned different degrees of relativeimportance For example if a respondent replies that factor(i) is more important than factor (ii) then factor (i) has arelative weight of 7 times than that of factor (ii) We created apairwise comparison matrix for each factor by dividing eachelement of the matrix by its column total

Step 3 We calculated the eigenvalue to determine the relativeweight of each factor in relation to the one immediatelyabove in the hierarchy The priority vector is established bycalculating the row averages At this point the consistencyindex is calculated by the following equation CR = CIRIConsistency index is calculated by the following equationCI = LEMDA max minus 119899119899 minus 1 where 119899 is the numberof subcriteria of each criterion The design of the AHPhierarchy must satisfy the goal of developing a model thatallows respondent to decide which factor they regard mostimportant in assessing factors causing market volatility

Step 4 We examined the consistency of the created pairsFor this purpose consistency ratio is used to check whethera criterion can be used for decision-making The CR valueof less than 01 is considered acceptable for estimating thepriority vector whereas the bigger value means that it shouldnot be used for estimating the priority vector

Step 5 The factor priorities are combined to disclose themostimportant factor in order to develop an overall priority rank-ing In order to set weights of the elements in a hierarchy weprefer the geometric means as the most common approachto set priorities

Following these AHP specified steps we determined therelative weights and rankings of the factors causing volatilityin KSE that we present in Figure 6

720

1011

1070

1166

1311

1827

2895

Analystsrsquo forecast

Media stories

Change in earnings

Government policies

Manipulation

Herd behaviour

Political situation

Figure 6 AHP results for factors causing market volatility

The results suggest that political situation andherd behav-ior are the most important factors to have major impact onthe stock market in terms of volatility Alternatively forecastsof the analysts cast least impact onmarketMoreover we usedthe data on investor behavior obtained from an earlier study(Awan et al 2011) that identified determinants of investorbehavior (Figure 7) to find the impact of investor behavioron the factors causing market volatility

We use Ordinary Least Squares (OLS) model to identifythe possible relationship of the investorsrsquo behavior with thefactors causing volatility and present the results in Table 3

The results of the model suggest that the behavioraldimensions of investor involvement risk attitude and over-confidence are significantly associated with factors causingmarket volatility as the 119901 values for these dimensions (00000001 and 0000) are less than the alpha value (005) thatsupports our argument that investor behavior is associatedwith factors causing volatility Moreover considering 1198772 andadjusted 1198772 we find that investor behavior has an impact of32 to 35 percent on the factors causing volatility

We also conducted ANOVA in order to check for dif-ferences in responses regarding factors causing volatility ofinvestors belonging to different age groups We observedthat investors with 50+ ages gave high rates to the factorsof herd behavior and political situation as the determinantsof volatility as compared to investors with age le50 yearsInvestors with education level of high-school or lower gavehigher rates to factors of media stories herd behavior andpolitical situations as determinants of volatility as comparedto their relatively higher educated peersWe also analyzed theresponses of investors with different levels of income and do

8 Economics Research International

Investment behavior

Overconfidence5042

optimism1396

Specific skills3241

Market knowledge1748

Stock picking2196

Quick money7961

Trade activity2039

Stable returns2880

Familiarity bias3889

Enjoyment from risky trade 849

Risk taking2381

Keep invested4706

Index recovery1319

2815Self-control

Increasedinvestment 1755

Price increase expectation 2220

Risk attitude1780

Involvement1784

Figure 7 Determinants of investorsrsquo behavior

not find any significant difference of opinions among themregarding the factors contributing towards market volatility

5 Conclusion

The objective of this study was to identify and investigate thevolatility at KSE from a behavioral finance perspective Forthis purpose we used the data of return series from January1 1990 to October 1 2014 to specify ARCH GARCH andEGARCH models to estimate volatility of KSE-100 indexreturns We found that the KSE-100 index returns seriesexhibited the stylized characteristics such as volatility cluster-ing excess kurtosis fat-tiredness time-varying conditionalheteroskedasticity and ldquoleverage effectrdquo The results indicatethat volatility is highly persistent at KSE implying that newshocks will have influence on returns for the shorter periodsEGARCH demonstrated the presence of negative ldquoleverageeffectrdquo suggesting that negative returns are associated withhigher volatility than positive returns of equal magnitude

Our results show that according to investors the fac-tor of political situation is the most important in causingturbulences in the stock market The interviews with thebrokers also conform political situation as the most impor-tant factor causing volatility The second most importantfactor identified by investors is the herd behavior amonginvestors that result in over- and underpricing of stocksand the overall market shows a volatile behavior Accordingto investors manipulations by the big investors also play amajor role in causing stock market volatility Moreover thegovernment policies and change in the earnings of listedcompanies and media stories also contribute towards the

market volatility Forecasts by the analysts are at the lowestrank Furthermore our findings of OLS model suggest thatindividual investorrsquos dimensions of involvement risk attitudeand overconfidence are significantly associated with factorscausing market volatility

Competing Interests

The authors declare that they have no competing interests

References

[1] G Bekaert and C R Harvey ldquoEmerging equity marketvolatilityrdquo Working Paper 5307 National Bureau of EconomicResearch (NBER) 1995

[2] Q Abbas S Khan and S Z A Shah ldquoVolatility transmission inregional Asian stock marketsrdquo Emerging Markets Review vol16 no 3 pp 66ndash77 2013

[3] K Kassimatis ldquoFinancial liberalization and stock marketvolatility in selected developing countriesrdquo Applied FinancialEconomics vol 12 no 6 pp 389ndash394 2002

[4] E F Fama ldquoThe behavior of stock-market pricesrdquo The Journalof Business vol 38 no 1 pp 34ndash105 1965

[5] K R French ldquoStock returns and the weekend effectrdquo Journal ofFinancial Economics vol 8 no 1 pp 55ndash69 1980

[6] H Bessembinder and P J Seguin ldquoPrice volatility tradingvolume andmarket depth evidence from futures marketsrdquoTheJournal of Financial and Quantitative Analysis vol 28 no 1 pp21ndash39 1993

[7] K R French and R Roll ldquoStock return variances The arrivalof information and the reaction of tradersrdquo Journal of FinancialEconomics vol 17 no 1 pp 5ndash26 1986

Economics Research International 9

[8] A Madhavan ldquoTrading mechanisms in securities marketsrdquoTheJournal of Finance vol 47 no 2 pp 607ndash641 1992

[9] P Arestis P O Demetriades and K B Luintel ldquoFinancialdevelopment and economic growth the role of stock marketsrdquoJournal of Money Credit and Banking vol 33 no 1 pp 16ndash412001

[10] H Zuliu ldquoStock market Volatility and Corporate InvestmentrdquoIMFWorking Paper 95102 1995

[11] R F Engle ldquoAutoregressive conditional heteroscedasticity withestimates of the variance of United Kingdom inflationrdquo Econo-metrica Journal of the Econometric Society vol 50 no 4 pp987ndash1007 1982

[12] T Bollerslev ldquoGeneralized autoregressive conditional het-eroskedasticityrdquo Journal of Econometrics vol 31 no 3 pp 307ndash327 1986

[13] A Ali and S Laeeq ldquoTime Series Modeling and Forecastingin Banking Sector of KSE-100 and distribution fitting on stockmarket datardquo Pakistan Journal of Social Sciences vol 32 no 1pp 93ndash112 2012

[14] H A Kanasro C L Rohra and M A Junejo ldquoMeasurementof stock market volatility through ARCH and GARCHmodelsa case study of Karachi stock exchangerdquo Australian Journal ofBasic and Applied Sciences vol 3 no 4 pp 3123ndash3127 2009

[15] K Saleem Modeling time varying volatility and asymmetry ofKSE 2007 httpssrncomabstract=964898

[16] S F LeRoy and R D Porter ldquoThe present-value relation testsbased on implied variance boundsrdquo Econometrica vol 49 no 3pp 555ndash574 1981

[17] R J Shiller ldquoDo stock prices move too much to be justified bysubsequent changes in dividendsrdquoAmerican Economic Reviewvol 71 no 3 pp 421ndash498 1981

[18] R J Shiller ldquoThe volatility of long-term interest rates andexpectations models of the term structurerdquo The Journal ofPolitical Economy vol 87 no 6 pp 1190ndash1219 1979

[19] G W Schwartz and A Robert Fquity Markets StructureTrading and Performance Harper Business New York NYUSA 1988

[20] J M Karpoff ldquoThe relation between price changes and tradingvolume a surveyrdquo Journal of Financial and Quantitative Analy-sis vol 22 no 1 pp 109ndash126 1987

[21] R J Shiller ldquoHuman behavior and the efficiency of the financialsystemrdquo Working Paper W6375 National Bureau of EconomicResearch 1998

[22] R J Shiller Market Volatility MIT Press Cambridge MassUSA 1987

[23] H Shefrin and M Statman ldquoBehavioral capital asset pricingtheoryrdquoThe Journal of Financial and Quantitative Analysis vol29 no 3 pp 323ndash349 1994

[24] M Andersson M Hedesstrom and T Garling ldquoA social-psychological perspective on herding in stock marketsrdquo TheJournal of Behavioral Finance vol 15 no 3 pp 226ndash234 2014

[25] D B Nelson ldquoConditional heteroskedasticity in asset returns anew approachrdquo Econometrica vol 59 no 2 pp 347ndash370 1991

Submit your manuscripts athttpwwwhindawicom

Child Development Research

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Education Research International

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Biomedical EducationJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Psychiatry Journal

ArchaeologyJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

AnthropologyJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Research and TreatmentSchizophrenia

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Urban Studies Research

Population ResearchInternational Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

CriminologyJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Aging ResearchJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

NursingResearch and Practice

Current Gerontologyamp Geriatrics Research

Hindawi Publishing Corporationhttpwwwhindawicom

Volume 2014

Sleep DisordersHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

AddictionJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Depression Research and TreatmentHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Geography Journal

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Research and TreatmentAutism

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Economics Research International

2 Economics Research International

volatility in a highly volatile market where political situationand herd behavior are the two most important factors thatcontribute towards market volatility

Along with Introduction we organize this paper inthe following manner Section 2 presents literature reviewSection 3 depicts the data and the methodology Section 4describes the results and their discussion and Section 5presents conclusions We provide references at the end

2 Literature Review

Volatility is a vital input to determine the overall cost ofcapital [1] Stock prices generally demonstrate nonlinear andprobably chaotic behavior However some observe that stockpricesreturns are predictable imperfectly in the short-runbut unpredictable in the long-run and statistical distributionscan measure the return unevenness Literature has identifieda number of factors that cause stock market volatility Forexample credit policy inflation interest rate corporate earn-ings financial leverage dividend policies bonds prices andmany other macroeconomic social and political variablesResearchers also find stock market volatility transmissionbetween friendly countries of different regions (eg Pakistanand China) having economic links [2] They find evidence ofreduced volatility after implementation of financial liberal-ization policies in Pakistan [3] Some suggest that that stocktradesrsquo volume causes volatility [4 5] and an asymmetricalvolatility is due to response between volume and price[6] While others observe that volatility is an outcome ofthe trading volume followed by arrival of new informationregarding new floats or any kind of private informationincorporated into market stock prices [7] Madhavan [8]describes volatility in the form of price divergence and arguesthat investors demand low volatility to minimize the needlessrisk borne by them to enable them to liquidate their assetswithout facing threat of unfavorable huge price movements

There are a number of negative implications of the stockmarket volatility One implication is that market volatilitynegatively affects the economic growth [9] and businessinvestment [10] We use econometric techniques namelyARCH model [11] and the GARCH model [12] to determinethe presence of volatility at KSE In the past different studieswere carried out to check the market volatility at KSE Forexample Ali and Laeeq [13] studied the banking sector ofKSE by fitting AR(1) ARCH(1) and GARCH(1 1) modeland they assess the fitness of model by loss function Kanasroet al [14] studied theKSE-100 index andKSE all share price byfittingARCHandGARCHmodelThey confirm the presenceof high volatility in market Moreover Saleem [15] studiedvolatility of KSE-100 index using 9-year data and concludedthat ARCH and GARCH best fit the market and confirmvolatility clustering

Behavioral finance seeks to elucidate the unjustifiablestock price volatility Studies on the stock market [16 17]and on the bond market [18] found excess volatility in thesemarkets and observed that asset prices are far more unstablethan could be explained by traditional financial modelProper justification of extreme volatility is still missing

because researchers do not have complete knowledge aboutall the aspects of the valuation models used by investorsHowever financial economists believe that disagreementin the investor opinion directly affects the security-pricevolatility and trading volume [19] Standard finance failsto enlighten an ample divergence of opinion except to callit the effect of asymmetrical information We argue thatstudying behavior related factors might help explain the phe-nomenonWhile probing the volatility-volumephenomenonresearchers found the relationship between volatility andinvestor trades [20] However majority of volatility-volumestudies have ignored the impact of heterogeneous behavior ofinvestor trades Nevertheless some argue that herd behaviorcan result in over- or underpricing and can act as a sourceof stock market volatility Individual investors may not investproper time and effort to evaluate the market but choose tofollow the aggregated assessment of the majority and conse-quently the true value of the market may be incorrect [17]

Some studies attribute the excess volatility to investorsrsquooverconfidence They argue that overconfident investors feelit is a justifiable act to trade often [21] A survey of the1987 market crash notices investorsrsquo strong confidence andan insightful outlook about the postcrash course the marketwould take [22] suggesting that overconfidencemight explainthe phenomenon of volatility and huge price deviationsShefrin and Statman [23] observe that investors commit twocommon mistakes either they consider recent observationsmore important and do not give due importance to the priorinformation or they commit a gamblerrsquos fallacy and developa belief that recent events more closely resemble long termprobabilities thereby distorting prices and causing increasedvolatility while reducing market efficiency

Asset pricing theory suggests that if investors are rationalthen stock price should equal the present value of thestockrsquos expected cash distributions to shareholders Howeverempirical evidences suggest that stock prices aremore volatilethan what standard asset pricing models can explain [16 18]Shiller [18] further attributes it to psychology or irrationalityFinding a connection between investor behavior and thedynamics of asset prices is an important challenge facingbehavioral finance The proponents of behavioral paradigmare of the view that a large number of investors act irrationallyand are prone to behavioral heuristics that result in less thanoptimal investment choices [24]

3 Data and Methodology

The objective of study is to identify the presence of stockmarket volatility at KSE and to find the reasons of volatilityfrom individual investorsrsquo behavior perspective For thispurpose we collected both secondary and primary data Forsecondary data we obtained the daily changes in KSE-100index (from httpwwwksecompk) from January 1 1990to October 1 2014 Consequent to the decline in KSE indexto very low levels the market remained frozen from August27 2008 to December 12 2008 As these values may distortour results we conducted a reality check by including thedormant values (when the market remained frozen) during

Economics Research International 3

90 92 94 96 98 00 02 04 06 08 10 12 14 90 92 94 96 98 00 02 04 06 08 10 12 140

4000

8000

12000

16000

20000

24000

28000

32000 KSE 100KSE-100 with dormant values

0

4000

8000

12000

16000

20000

24000

28000

32000 KSE 100

Figure 1 KSE-100 index

this period and then by excluding these observations to drawsound conclusions Both data sets exhibit almost the samebehaviorWe also used an alternative statisticalmethod calledwinsorization that also yielded the same results

We also collected primary data by obtaining directresponses from 246 individual investors of the stock marketand 28 brokers listed with KSEWhile doing so we first iden-tified recurring themes and factors that may cause volatil-ity through preliminary interviews with the investors andbrokers After identifying recurring themes we developedstructured questionnaires administered to the individualinvestors and brokers selected using random sampling tech-nique from fourmajor cities Lahore Islamabad Karachi andMultan We used quantitative methods to analyze responsesobtained from individual investors whereas we used qual-itative method to analyze brokersrsquo responses to our open-ended questions based interviewsWe examined the presenceof volatility at KSE by fitting ARCH GARCH and EGARCHmodels ([11 12 25])

Engle [11] proposed the ARCH model to specify condi-tional volatility that incorporates the common sense logicthat observations belonging to the recent past should gethigher weights than those belonging to the distant past TheARCH process often requires large number of parameters toexplain the dynamic structure of financial phenomenon Toovercome these problems Bollerslev [12] proposed GARCHmodel that essentially generalizes the ARCH by mod-elling the conditional covariance as an ARMA process TheGARCH model helps find cluster volatility of financial mar-kets thicker tail distribution and predictability of volatilityfrom past patternsThe following system of (1) represents theARMA(119898 119899)-GARCH(119901 119902) for stock returns (119903

119905) and stock

return volatility (ℎ119905)

119903119905= 120583 +

119898

sum119894=1

120601119894119903119905minus119894+

119899

sum119894=0

120579119894119906119905minus119894

1205790= 1

119906119905= 119911119905radicℎ119905

ℎ119905= 1205720+

119901

sum119894=1

120572119894ℎ119905minus119894+

119902

sum119895=1

1205731198951199062

119905minus119895

(1)

where 120572119894gt 0 120573

119895gt 0 and 120582

119896gt 0 for all 119894 119895 and 119896 and119885

119905sim iid

with mean 0 and variance 1The virtue of this approach is that GARCH model with

a small number of terms appears to perform better thanARCH with many terms The EGARCH model has no suchconstraint of parameters [25] The variance equation has anadvantage over the ARCH and GARCH that it tends to beautomatically positive without imposition of restriction ofnonnegativity on parameters and it captures the ldquoleverageeffectrdquo Moreover EGARCH allows the asymmetric responseof volatility to downside and upside market movements Thesystem of (2) specifies EGARCHmodel

119903119905= 120583 +

119898

sum119894=1

120601119894119903119905minus119894+

119899

sum119894=0

120579119894119906119905minus119894

1205790= 1

119906119905= 119911119905radicℎ119905

log (ℎ119905) = 1205720+

119901

sum119894=1

120572119894log (ℎ

119905minus119894) +

119902

sum119895=1

120573119895

1003816100381610038161003816100381610038161003816100381610038161003816

119906119905minus119895

ℎ119905minus119895

1003816100381610038161003816100381610038161003816100381610038161003816

+

119903

sum119896=1

120574119896

119906119905minus119896

ℎ119905minus119896

(2)

where 119885119905sim iid with mean 0 and variance 1 Since 120573

119895show

the asymmetric function that is current volatility which isinfluenced by the past standardized residuals the term 120572

119894+120573119895

shows the effect of magnitude and 120574119896is for the representation

of sign effect The volatility persistence is equal to sum120572119894and

for unconditional variance it should be less than 1Furthermore we employ Analytical Hierarchical Process

(AHP) to rank the factors causing volatility and analysis ofvariance (ANOVA) to obtain the results of this study

4 Results and Their Discussion

Before fittingARCHandGARCHwe conducted preliminarygraphical analysis of the data for heteroskedasticity Figures 1and 2 reveal huge unevenness in the observations

We present descriptive statistics in Table 1

4 Economics Research International

Table 1 Descriptive statistics

KSE-100 with dormant values KSE-100 without dormant valuesMean 0000615 0000606Median 0000000 0000000Maximum 0127622 0127622Minimum minus049417 minus013214Std dev 0015869 0014607Skewness minus496136 minus028648Kurtosis 15559290 984641ARCH-LM test 9714249 9998743Jarque-Bera test 620235200 1269921Observations 6366 6457

90 92 94 96 98 00 02 04 06 08 10 12 14

RT

90 92 94 96 98 00 02 04 06 08 10 12 14

RTTKSE-100 returns

minus015

minus010

minus005

000

005

010

015

minus05

minus04

minus03

minus02

minus01

00

01

02KSE-100 exculed dormant values

Figure 2 Daily change in KSE-100 index

1 0106 0106 72554 00002 0048 0037 87606 00003 0055 0047 10704 00004 0047 0036 12157 00005 0023 0010 12485 00006 0019 0011 12722 00007 0018 13164 00008 0020 0012 13421 00009 0038 0031 14339 0000

10 0056 0046 16392 000011 16433 000012 0046 0042 17827 0000

0026

-

Autocorrelation Partial correlation AC PAC Prob

minus0008 minus0024

Autocorrelation Partial correlation AC PAC Prob

1 0108 0108 74768 0000

2 0062 0051 99270 0000

3 0050 0039 11523 0000

4 0055 0044 13486 0000

5 0047 0033 14900 0000

6 0029 0015 15458 0000

7 0016 15958 0000

8 0024 0013 16333 0000

9 0030 0019 16904 0000

0028

Q-statQ-stat

Figure 3 Results of ACF test of KSE-100 index (with and without dormant values)

Excess kurtosis and negative skewness result in highJarque-Bera statistic that indicates the nonnormality of thedistribution Moreover the high values of ARCH-LM statis-tic [11] also suggest the presence of ARCH effect in theconditional variance Even after excluding those abnormalobservations there exist signs of presence of heteroscedas-ticity and huge variations among the observations and thepresence of volatility clustering in returns revealing presenceof ARCH in the data Moreover we applied Auto CorrelationFunction (ACF) test to check the presence of autocorrelationin the data If there is no ARCH in the residuals the

autocorrelations (AC) and partial autocorrelations (PAC)should be zero at all lags and the 119876-statistic should beinsignificant We present the results of ACF test in Figure 3that confirm the existence of ARCH effect and presence ofcluster volatility in returns

We followed the Box-Jenkins methodology for the iden-tification of the mean model For the identification of appro-priate models we used ACF PACF and Ljung-Box statisticsof the standardized residuals and the squared standard-ized residuals and ARCH-LM test We found ARMA(1 1)-GARCH(1 1) process to be the appropriate model for

Economics Research International 5

Table 2 Results of ARMA GARCH and EGARCH

Parameters Mean equation Variance equation120583 120601 120579 120572

01205721

1205731

120574 SBC AIC

GARCH(1 1) 000075(00000)

0766781(00000)

minus06697(00000)

0000005(00000)

0834785(00000)

0146561(00000) minus597 minus5977

EGARCH(1 1) minus00007(00000)

087746(00000)

minus07791(00000)

minus080484(00000)

092974(00000)

026901(00000)

minus00634(00000) minus595 minus59641

ARCH-LM test for GARCH119865-test 0389836 (08561) Obs lowast 1198772 19504 (08560)

conditional variance on the bases of Bayesian InformationCriterion (BIC) and Akaike Information Criterion (AIC) Inaddition the EGARCH model outperformed the GARCHcounterpart especially with Studentrsquos 119905 error as the errordistribution Therefore we use EGARCH(1 1) specificationfor variance equation In Table 2 we report the results of themean and the variance equation

The results reveal that estimated parameters ofGARCH(1 1) are highly significant The parameter 120573

1

is positive and significant This suggests that the measureof risk measured by own conditional variance indicatesthe positive and significant autocorrelation in return Theparameter 120572

1is also significant implying higher degree of

persistence Furthermore the condition 1205721+ 1205731is a measure

of volatility persistence and an estimation of the decay rateof response function on daily basis This condition reflectshow the historical conditional volatility affected the currentconditional variance of stock returns The 120572

1+ 1205731should be

less than one but in this case it is near to unity It suggests thatestimated conditional variance can be an integrated GARCH(IGARCH) process and is nonstationary The presence ofIGARCH suggests the persistence of volatility and a shockhas indefinite influence on volatility level To assess theldquoleverage effectrdquo we carried out normality test of standardizedresidualsThe JB-statistic rejected the hypothesis of normalitydue to the presence of ldquoleverage effectrdquo The coefficient 120573

1

corresponds to the asymmetric function and is statisticallysignificant indicating that current volatility is moderatelyinfluenced by the past standardized residuals Moreoverthe ldquoleverage effectrdquo term 120574

1is negative and significant

demonstrating the presence of negative ldquoleverage effectrdquoimplying that negative returns are associated with highervolatility than positive returns of equal magnitude

Robustness of Estimation GARCH(119901 119902) models are fittedto the return series using maximum-likelihood estimationIn the Gaussian quasi MLE method this estimation isdone under the assumption that the innovations [119885

119905] have

a Gaussian distribution The estimations are robust if theestimations of the parameters depend on the distributionalassumption of the innovations 119885

119905and if the residuals of the

estimated process have the same distribution as the assumeddistribution of the innovations When the estimation of theunknown parameters is done estimates of the standard devi-ation series can be calculated recursively via the definition ofthe conditional variance for the GARCH(119901 119902) process

In Figures 4(a) and 4(b) the log-return process andthe estimated conditional standard deviation process forKSE-100 index are plotted The estimated conditional stan-dard deviation process is derived from a EGARCH(1 1) fitThe estimated conditional standard deviation process reflectsthe behavior of the log-return process Based on Figure 4 theEGARCHmodel seems to be reasonable

Further with a 119876119876-Plot (Figure 5) one can examine thedistribution of the residuals to verify the robustness in theestimation With GARCH(1 1) fit using MLE under theassumption of Gaussian innovations the residuals from thefit on the simulated data are computed and plotted in a 119876119876-Plot against the normal distribution The fit is good whichindicates the process exhibits the Gaussian distribution andshows model robustness with 120572

0= minus0805 120572

1= 0930

1205731= 0269 and 120574

1= minus0063

41 Factors Causing Market Volatility After confirming pres-ence of market volatility with the help of existing literatureand preliminary interviews we identified the following sevenfactors that can cause market volatility in Pakistan

(i) News stories in the media(ii) Forecasts of the analysts(iii) Change in earnings of listed companies(iv) Herd behavior (individual investors following the

majority)(v) Government policies(vi) Political situation(vii) Manipulation by big investors

Majority of the brokers put political instability at the first rankto cause market volatility Among other major factors thatthey identified are poor government policies big investorsand their manipulations and herd behavior as the factorscausing volatility in stock market

We then asked the investors to rate the above seven factorson a scale from 1 (least important) to 7 (most important)In response to the role of media news stories to cause stockmarket volatility 159 of the investors considered it to beamong the most important factor while only 37 of theinvestors gave it the lowest rating Overall 659 of theinvestors (gave a rate of 5 or more) consider that news storiesin the media are an important factor causing stock market

6 Economics Research International

92 94 96 98 00 02 04 06 08 10 12 1490015

010

005

000

005

010

015

minus015

minus010

minus005

000

005

010

015

90 92 94 96 98 00 02 04 06 08 10 12 14

RT RT_D

minus010

minus005

000

005

010

(a)

Estimate of conditional standard deviation drived fromML estimation of EGARCH (1 1) model

90 92 94 96 98 00 02 04 06 08 10 12 14

Conditional standard deviation

90 92 94 96 98 00 02 04 06 08 10 12 14

Conditional standard deviation

000

001

002

003

004

005

006

000

001

002

003

004

005

006

(b)

Figure 4 (a) Log return of KSE-100 with dormant values (RT) and without dormant values (RT D) (b) Estimate of conditional standarddeviation drive fromML estimation of EGARCH(1 1)model with and without dormant values

Residual for estimated EGARCH (1 1) process with

015

01

005

minus005

minus01

00

00minus005minus01 005 01501

Residual

gausian innovations

Figure 5 The 119876119876-Plot Quantile-Quantile Plot

volatility Majority of the investors (63 gave rate of 4 orless) did not consider the forecasts of the analysts as animportant factor to cause volatility in the stock Regarding theimportance of changes in the earnings of the listed companiesin causing stock market volatility 138 of the investorsconsidered it as themost important factor in causing volatility

in the market while just 24 of the investors considered it asthe least important factor Overall 569 of the investors gaverating of 5 or above while 431 of the investors gave ratingof 4 or less

In response to our question regarding herd behavior caus-ing stock market volatility 26 of the investors considered itas the most important factor while just 37 of the investorsconsidered it as the least important factor Overall 825 ofthe investors gave high rating of 5 or above to herd behaviorand only 175 gave a rating of 4 or below Regarding the roleof government regulations and policies in causing volatility289 of the investors gave highest rating to this factor whilejust 04 of the investors gave the lowest rating Overall557 of the investors gave rating of 5 or above while 443of investors gave rating of 4 or less Moreover 553 of theinvestors regarded political situation of the country as themost important factor causing stockmarket volatility and just12 of the investors considered it the least important (gaverating of 1) On thewhole 886 of the investors considered itas more important factor (gave rating of 5 or above) whereas114 of the investors considered it as less important factor(gave rating of 4 or less) that causes market volatility Finally618 (highest frequency) of the investors considered the role

Economics Research International 7

Table 3 Relationship between determinants of investorsrsquo behavior and market volatility

Explanatory variables Coefficients SE of coeff Beta 119905 value 119901 valueIntercept 2551lowast 0308 8293 0000Involvement 0173lowast 0028 0335 6146 0000Risk attitude 0164lowast 0048 0187 3423 0001Optimism 0023 0037 0034 0623 0534Overconfidence 0221lowast 0040 0311 5545 0000lowastSignificant at 1 level

of manipulations by big investors as the most importantfactor (gave a rating of 7) in causing volatility but only 04of the investor as the least important factor (gave a rating of1)

We used Analytic Hierarchy Process (AHP) to findthe relative weights and ranking of these seven factors byadopting the following procedure

Step 1 We developed the hierarchical representation of theproblem by defining the factors perceived as most importantby the investors

Step 2 We compared all the factors in pairs On a scaleof 1 to 7 respondents assigned different degrees of relativeimportance For example if a respondent replies that factor(i) is more important than factor (ii) then factor (i) has arelative weight of 7 times than that of factor (ii) We created apairwise comparison matrix for each factor by dividing eachelement of the matrix by its column total

Step 3 We calculated the eigenvalue to determine the relativeweight of each factor in relation to the one immediatelyabove in the hierarchy The priority vector is established bycalculating the row averages At this point the consistencyindex is calculated by the following equation CR = CIRIConsistency index is calculated by the following equationCI = LEMDA max minus 119899119899 minus 1 where 119899 is the numberof subcriteria of each criterion The design of the AHPhierarchy must satisfy the goal of developing a model thatallows respondent to decide which factor they regard mostimportant in assessing factors causing market volatility

Step 4 We examined the consistency of the created pairsFor this purpose consistency ratio is used to check whethera criterion can be used for decision-making The CR valueof less than 01 is considered acceptable for estimating thepriority vector whereas the bigger value means that it shouldnot be used for estimating the priority vector

Step 5 The factor priorities are combined to disclose themostimportant factor in order to develop an overall priority rank-ing In order to set weights of the elements in a hierarchy weprefer the geometric means as the most common approachto set priorities

Following these AHP specified steps we determined therelative weights and rankings of the factors causing volatilityin KSE that we present in Figure 6

720

1011

1070

1166

1311

1827

2895

Analystsrsquo forecast

Media stories

Change in earnings

Government policies

Manipulation

Herd behaviour

Political situation

Figure 6 AHP results for factors causing market volatility

The results suggest that political situation andherd behav-ior are the most important factors to have major impact onthe stock market in terms of volatility Alternatively forecastsof the analysts cast least impact onmarketMoreover we usedthe data on investor behavior obtained from an earlier study(Awan et al 2011) that identified determinants of investorbehavior (Figure 7) to find the impact of investor behavioron the factors causing market volatility

We use Ordinary Least Squares (OLS) model to identifythe possible relationship of the investorsrsquo behavior with thefactors causing volatility and present the results in Table 3

The results of the model suggest that the behavioraldimensions of investor involvement risk attitude and over-confidence are significantly associated with factors causingmarket volatility as the 119901 values for these dimensions (00000001 and 0000) are less than the alpha value (005) thatsupports our argument that investor behavior is associatedwith factors causing volatility Moreover considering 1198772 andadjusted 1198772 we find that investor behavior has an impact of32 to 35 percent on the factors causing volatility

We also conducted ANOVA in order to check for dif-ferences in responses regarding factors causing volatility ofinvestors belonging to different age groups We observedthat investors with 50+ ages gave high rates to the factorsof herd behavior and political situation as the determinantsof volatility as compared to investors with age le50 yearsInvestors with education level of high-school or lower gavehigher rates to factors of media stories herd behavior andpolitical situations as determinants of volatility as comparedto their relatively higher educated peersWe also analyzed theresponses of investors with different levels of income and do

8 Economics Research International

Investment behavior

Overconfidence5042

optimism1396

Specific skills3241

Market knowledge1748

Stock picking2196

Quick money7961

Trade activity2039

Stable returns2880

Familiarity bias3889

Enjoyment from risky trade 849

Risk taking2381

Keep invested4706

Index recovery1319

2815Self-control

Increasedinvestment 1755

Price increase expectation 2220

Risk attitude1780

Involvement1784

Figure 7 Determinants of investorsrsquo behavior

not find any significant difference of opinions among themregarding the factors contributing towards market volatility

5 Conclusion

The objective of this study was to identify and investigate thevolatility at KSE from a behavioral finance perspective Forthis purpose we used the data of return series from January1 1990 to October 1 2014 to specify ARCH GARCH andEGARCH models to estimate volatility of KSE-100 indexreturns We found that the KSE-100 index returns seriesexhibited the stylized characteristics such as volatility cluster-ing excess kurtosis fat-tiredness time-varying conditionalheteroskedasticity and ldquoleverage effectrdquo The results indicatethat volatility is highly persistent at KSE implying that newshocks will have influence on returns for the shorter periodsEGARCH demonstrated the presence of negative ldquoleverageeffectrdquo suggesting that negative returns are associated withhigher volatility than positive returns of equal magnitude

Our results show that according to investors the fac-tor of political situation is the most important in causingturbulences in the stock market The interviews with thebrokers also conform political situation as the most impor-tant factor causing volatility The second most importantfactor identified by investors is the herd behavior amonginvestors that result in over- and underpricing of stocksand the overall market shows a volatile behavior Accordingto investors manipulations by the big investors also play amajor role in causing stock market volatility Moreover thegovernment policies and change in the earnings of listedcompanies and media stories also contribute towards the

market volatility Forecasts by the analysts are at the lowestrank Furthermore our findings of OLS model suggest thatindividual investorrsquos dimensions of involvement risk attitudeand overconfidence are significantly associated with factorscausing market volatility

Competing Interests

The authors declare that they have no competing interests

References

[1] G Bekaert and C R Harvey ldquoEmerging equity marketvolatilityrdquo Working Paper 5307 National Bureau of EconomicResearch (NBER) 1995

[2] Q Abbas S Khan and S Z A Shah ldquoVolatility transmission inregional Asian stock marketsrdquo Emerging Markets Review vol16 no 3 pp 66ndash77 2013

[3] K Kassimatis ldquoFinancial liberalization and stock marketvolatility in selected developing countriesrdquo Applied FinancialEconomics vol 12 no 6 pp 389ndash394 2002

[4] E F Fama ldquoThe behavior of stock-market pricesrdquo The Journalof Business vol 38 no 1 pp 34ndash105 1965

[5] K R French ldquoStock returns and the weekend effectrdquo Journal ofFinancial Economics vol 8 no 1 pp 55ndash69 1980

[6] H Bessembinder and P J Seguin ldquoPrice volatility tradingvolume andmarket depth evidence from futures marketsrdquoTheJournal of Financial and Quantitative Analysis vol 28 no 1 pp21ndash39 1993

[7] K R French and R Roll ldquoStock return variances The arrivalof information and the reaction of tradersrdquo Journal of FinancialEconomics vol 17 no 1 pp 5ndash26 1986

Economics Research International 9

[8] A Madhavan ldquoTrading mechanisms in securities marketsrdquoTheJournal of Finance vol 47 no 2 pp 607ndash641 1992

[9] P Arestis P O Demetriades and K B Luintel ldquoFinancialdevelopment and economic growth the role of stock marketsrdquoJournal of Money Credit and Banking vol 33 no 1 pp 16ndash412001

[10] H Zuliu ldquoStock market Volatility and Corporate InvestmentrdquoIMFWorking Paper 95102 1995

[11] R F Engle ldquoAutoregressive conditional heteroscedasticity withestimates of the variance of United Kingdom inflationrdquo Econo-metrica Journal of the Econometric Society vol 50 no 4 pp987ndash1007 1982

[12] T Bollerslev ldquoGeneralized autoregressive conditional het-eroskedasticityrdquo Journal of Econometrics vol 31 no 3 pp 307ndash327 1986

[13] A Ali and S Laeeq ldquoTime Series Modeling and Forecastingin Banking Sector of KSE-100 and distribution fitting on stockmarket datardquo Pakistan Journal of Social Sciences vol 32 no 1pp 93ndash112 2012

[14] H A Kanasro C L Rohra and M A Junejo ldquoMeasurementof stock market volatility through ARCH and GARCHmodelsa case study of Karachi stock exchangerdquo Australian Journal ofBasic and Applied Sciences vol 3 no 4 pp 3123ndash3127 2009

[15] K Saleem Modeling time varying volatility and asymmetry ofKSE 2007 httpssrncomabstract=964898

[16] S F LeRoy and R D Porter ldquoThe present-value relation testsbased on implied variance boundsrdquo Econometrica vol 49 no 3pp 555ndash574 1981

[17] R J Shiller ldquoDo stock prices move too much to be justified bysubsequent changes in dividendsrdquoAmerican Economic Reviewvol 71 no 3 pp 421ndash498 1981

[18] R J Shiller ldquoThe volatility of long-term interest rates andexpectations models of the term structurerdquo The Journal ofPolitical Economy vol 87 no 6 pp 1190ndash1219 1979

[19] G W Schwartz and A Robert Fquity Markets StructureTrading and Performance Harper Business New York NYUSA 1988

[20] J M Karpoff ldquoThe relation between price changes and tradingvolume a surveyrdquo Journal of Financial and Quantitative Analy-sis vol 22 no 1 pp 109ndash126 1987

[21] R J Shiller ldquoHuman behavior and the efficiency of the financialsystemrdquo Working Paper W6375 National Bureau of EconomicResearch 1998

[22] R J Shiller Market Volatility MIT Press Cambridge MassUSA 1987

[23] H Shefrin and M Statman ldquoBehavioral capital asset pricingtheoryrdquoThe Journal of Financial and Quantitative Analysis vol29 no 3 pp 323ndash349 1994

[24] M Andersson M Hedesstrom and T Garling ldquoA social-psychological perspective on herding in stock marketsrdquo TheJournal of Behavioral Finance vol 15 no 3 pp 226ndash234 2014

[25] D B Nelson ldquoConditional heteroskedasticity in asset returns anew approachrdquo Econometrica vol 59 no 2 pp 347ndash370 1991

Submit your manuscripts athttpwwwhindawicom

Child Development Research

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Education Research International

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Biomedical EducationJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Psychiatry Journal

ArchaeologyJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

AnthropologyJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Research and TreatmentSchizophrenia

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Urban Studies Research

Population ResearchInternational Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

CriminologyJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Aging ResearchJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

NursingResearch and Practice

Current Gerontologyamp Geriatrics Research

Hindawi Publishing Corporationhttpwwwhindawicom

Volume 2014

Sleep DisordersHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

AddictionJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Depression Research and TreatmentHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Geography Journal

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Research and TreatmentAutism

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Economics Research International

Economics Research International 3

90 92 94 96 98 00 02 04 06 08 10 12 14 90 92 94 96 98 00 02 04 06 08 10 12 140

4000

8000

12000

16000

20000

24000

28000

32000 KSE 100KSE-100 with dormant values

0

4000

8000

12000

16000

20000

24000

28000

32000 KSE 100

Figure 1 KSE-100 index

this period and then by excluding these observations to drawsound conclusions Both data sets exhibit almost the samebehaviorWe also used an alternative statisticalmethod calledwinsorization that also yielded the same results

We also collected primary data by obtaining directresponses from 246 individual investors of the stock marketand 28 brokers listed with KSEWhile doing so we first iden-tified recurring themes and factors that may cause volatil-ity through preliminary interviews with the investors andbrokers After identifying recurring themes we developedstructured questionnaires administered to the individualinvestors and brokers selected using random sampling tech-nique from fourmajor cities Lahore Islamabad Karachi andMultan We used quantitative methods to analyze responsesobtained from individual investors whereas we used qual-itative method to analyze brokersrsquo responses to our open-ended questions based interviewsWe examined the presenceof volatility at KSE by fitting ARCH GARCH and EGARCHmodels ([11 12 25])

Engle [11] proposed the ARCH model to specify condi-tional volatility that incorporates the common sense logicthat observations belonging to the recent past should gethigher weights than those belonging to the distant past TheARCH process often requires large number of parameters toexplain the dynamic structure of financial phenomenon Toovercome these problems Bollerslev [12] proposed GARCHmodel that essentially generalizes the ARCH by mod-elling the conditional covariance as an ARMA process TheGARCH model helps find cluster volatility of financial mar-kets thicker tail distribution and predictability of volatilityfrom past patternsThe following system of (1) represents theARMA(119898 119899)-GARCH(119901 119902) for stock returns (119903

119905) and stock

return volatility (ℎ119905)

119903119905= 120583 +

119898

sum119894=1

120601119894119903119905minus119894+

119899

sum119894=0

120579119894119906119905minus119894

1205790= 1

119906119905= 119911119905radicℎ119905

ℎ119905= 1205720+

119901

sum119894=1

120572119894ℎ119905minus119894+

119902

sum119895=1

1205731198951199062

119905minus119895

(1)

where 120572119894gt 0 120573

119895gt 0 and 120582

119896gt 0 for all 119894 119895 and 119896 and119885

119905sim iid

with mean 0 and variance 1The virtue of this approach is that GARCH model with