research article investment timing and capacity choice

TRANSCRIPT

Research ArticleInvestment Timing and Capacity Choice under Uncertainty

Xiumei Lv Shiqin Xu and Xiaoling Tang

School of Finance Chongqing Technology and Business University Chongqing 400067 China

Correspondence should be addressed to Xiumei Lv lvxium126com

Received 10 January 2014 Revised 22 February 2014 Accepted 23 February 2014 Published 27 March 2014

Academic Editor Qun Lin

Copyright copy 2014 Xiumei Lv et al This is an open access article distributed under the Creative Commons Attribution Licensewhich permits unrestricted use distribution and reproduction in any medium provided the original work is properly cited

This paper examines strategic investment between two firms that compete not only for investment timing but also for capacity understochastic market demand The value functions of real option for the follower the dominant leader and the preemptive leader arederived and their investment decisions are investigated It finds that both firms will delay investment and the delayed margin of thefollower will surpass that of the leader under greater uncertainty Furthermore both firms will provide more outputs in the face ofincreasing uncertainty and the growth rate of the followerrsquos capacity will exceed that of the leaderrsquos In addition this paper findsthat the follower will end up with a larger capacity than the leader

1 Introduction

In the traditional theory investment decision is analyzed bythe net present value (NPV) method However the methodcannot reflect uncertainty existing in the investment processeffectively Furthermore when making decision NPV ismechanical and passive since there are only two choicesinvest now or never Considering the uncertain irreversibleand flexible feature of investment the real option approachsees investment opportunity as an American option and isproper to deal with investment problem in the real world (see[1ndash4])

As a matter of fact investment strategies will be influ-enced and restricted with each other so the value of theinvestment project depends not only on the companyrsquosown decision but also on the reaction of its competitorsThe option game approach the combination of real optionwith game theory is elaborated by Smit and Trigeorgis [5]Some literature applies the option game method to analyzeinvestment problem under a duopoly or oligopoly marketGrenadier [6] develops an equilibrium framework for strate-gic option exercise games and provides an explanation forwhy some markets may experience building booms in theface of declining demand Grenadier [7] provides a tractableapproach for deriving equilibrium investment strategies ina continuous-time Cournot-Nash framework and obtainsthe impact of competition drastically eroding the value of

the option to wait and lead to investment at near the zeronet present value threshold Chu and Sing [8] consider thesubgame equilibrium strategies for a duopoly real optionmodel with asymmetric demand functions and find that therelative strength of the firms has significant impact on thefirms equilibrium strategies Kong and Kwok [9] examinestrategic investment games between twofirmswhich competefor optimal investment under uncertain revenue flows ina duopoly market with negative externality and positiveexternality

One common character of the above option game isthat they assume a given investment output and are usuallyonly concerned with the choice of investment opportunitiesHowever in reality the scale of investment is an importantfactor that drives a personrsquos decision-making For examplereal estate developers should choose the construction area tobe explored and firms should decide the output quantity Dueto the uncertainty in the investment process improper choiceof investment opportunities or capacity will bring about greatrisks In order to control risks this paper investigates a realoption model and applies option game method to analyzethe investment timing and capacity choice problem understochastic market environment

There are still some literature considering the questionof investment capacity Wang and Zhou [10] derive closed-form solutions for an equilibrium real options exercisemodel under stochastic revenues and costs for oligopoly

Hindawi Publishing CorporationAbstract and Applied AnalysisVolume 2014 Article ID 801862 9 pageshttpdxdoiorg1011552014801862

2 Abstract and Applied Analysis

and competitivemarketswith different production capacitiesAguerrevere [11] studies the effects of competitive interac-tions on investment decisions and on the dynamics of theprice of a nonstorable commodity in a model of incrementalinvestment with time to build and operating flexibility Yangand Zhou [12] extends Dangl [13] to a duopoly in which oneof the firms is the incumbent and the other firm is the entrantNovy-Marx [14] analyzes the optimal investment decisionsof heterogeneous firms in a competitive and uncertain envi-ronment and shows that in the competitive equilibrium realoption premia remains significant Comparing these paperswith ours the main difference and contribution are that ourwork analyzes the influence of capacity choice and obtainsmany interest conclusions For example previous literatureusually predicts that the leader is better off by providing alarger capacity than his rival while this paper proves that thefirst mover enters with a smaller capacity than the secondmover and sheds light on why firm lacks incentive to pursuea large capacity preemption in an uncertain market

This paper is divided into five sections In Section 2 welay out the model framework Section 3 derives the valuefunctions and investment thresholds when the firms serveas the follower preemptive leader and dominant leaderSection 4 explores a comparative static on the volatility ofstochasticmarket demand In Section 5we draw a conclusionof this paper

2 Model Framework

The model of this paper comes from the redevelopmentinvestment problem of land in Capozza and Li [4] Intheir paper cash flow is uncertain in the whole investmentprocess and satisfies Algebra Brown Motion When investormakes his investment strategy he must consider not only theinvestment timing but also the investment scale while thelatter is reflected by intensity What is different from Capozzaand Li [4] is that this paper deals with investment problemin a duopoly market and uses product capacity to reflect eachinvestorrsquos scale For these two firms they must decide whento enter the market and what capacity they should produce

Suppose that both firms are rational risk-neutral andprofit-maximizing The model adopts riskless interest rate 119903to discount their payoff Furthermore two firms can provideunstorable commodity the price of which is related to themarket supply Specially we assume that the price119875(119905) at time119905 satisfies the following simple inverse demand function

119875 (119905) = 119883 (119905) minus 120574119876 (1)

where 119883(119905) is the exogenous market demand shock 119876 is thetotal market supply and nonnegative parameter 120574 is the slopeof the linear demand function and is used to reflect the pricesensitivity to the supply From (1)we know that the increase ordecrease of the total market supply will cause the price to riseor fall Furthermore function (1) indicates that the change ofthe market demand 119883 will be reflected on inverse demandcurve Since the variable changes unpredictably we suppose

that it is stochastic and evolves as a geometric Brownianmotion

119889119883 (119905) = 120583119883119889119905 + 120590119883119889119885 (119905) (2)

where 120583 is a given positive constant and denotes the expectedgrowth of119883120590 represents the volatility of themarket demandand 119889119885 is an increment of a standard Wiener motion anddenotes the resource of uncertainty Furthermore (2) meansthat investors only know the current level of the marketdemand while the future level meets with a lognormaldistributionTherefore ln119883 increases at a certain growth rateand is disturbed by a normally distributed random variableIn addition to guarantee that the option is exercised within afinite period of time we assume that 119903 gt 120583

Each firm has only one chance to invest As long as theinvestment opportunity exists the firm has to consider whento take action and what capacity to provide Suppose that theinvestment sunk cost is governed by the relation 119862(119876) = 119896119876where 119896 is a nonnegative parameter Hence the investmentcost will increase with their capacity choice

In the existing literature there are two types of invest-ment One is lumpy investment such as Mason and Weeds[15] Besanko et al [16] and Nishihara and Fukushima[17] the other is incremental investment such as Pindyck[3] Aguerrevere [11] and Novy-Marx [14] In the lumpyinvestment investment scale is decided at the investmenttime and all commodities are provided into the marketfor one time In the incremental investment commoditiescan be increased by an infinitesimal amount and the initialinvestment scale is expanded in the investment process Bar-Ilan and Strange [18] make a comparison with these twotypes Pindyck [3] points out that incremental investment isan extreme case of lumpy investment and can be calculatedconveniently Therefore this paper adopts lumpy investmentto analyze capacity choice problem under uncertainty that isto say investor can adjust his output flexibly according to theexternal uncertainty in the environment while all productsare supplied into the market the moment he exercises hisoption

3 Investment Problem in an Duopoly Market

In this section we will discuss strategic and competitiveinvestment problem in a duopoly market where uncertaintyis reflected on the stochastic market demand Two firms haveto decide not only their investment timing but also theiroptimal capacity Competitive behavior will be discussedfrom two aspects One is a dominant case and the other is apreemptive case Namely the leader is dominant in the gameor preempts the market

When the leader makes his decision he must considerthe possible strategy of the follower For the dominant leaderthe leadership may be determined by two situations Oneis determined exogenously in which the leader can choosehis optimal investment timing and optimal capacity since heknows his competitor will be prone to be a follower Theother is determined endogenously in which the leadershipis obtained after intense competition since the firm does

Abstract and Applied Analysis 3

not have comparative advantage over his rival in the gameDenote the leader and the follower as 119897 and 119891 respectively

Just as the standard method in dynamic programmingwe will adopt inverse induction Firstly consider the valuefunction of the follower Secondly consider the investmentproblem of the dominant leader Thirdly premeditate thevalue function of the preemptive leader The value functionsin the case where two firms take action simultaneously arejust the same as the value of themselves to be a follower

31 Follower Since the leader has taken investment actionthe follower can make his decision optimally Denote theinvestment timing and capacity of the follower as 119879lowast

119891and

119902lowast

119891 respectively If his competitor 119897 enters the market with

capacity 119902119897 the value function of the follower can be expressed

as

119865 (119883 119902119891) = max119879lowast

119891

119864119905int

infin

119879lowast

119891

[119883 (119904) minus 120574 (119902119897+ 119902119891)] 119890minus119903(119904minus119905)

119889119904

minus119896119890minus119903(119879lowast

119891minus119905)

119902119891

(3)

When the payoff of the firm is large enough that is 119883surpasses his investment trigger 119883lowast

119891 the follower begins to

exercise his option Furthermore the question to look for119883lowast119891

is equivalent to the maximization of the option valueBy dynamic programming (3) can be translated into the

following partial differential equation

1

2

1205902

11988321205972

119865 (119883)

1205971198832

+ 120583119883

120597119865 (119883)

120597119883

minus 119903119865 (119883) = 0 (4)

At the optimal trigger 119883lowast119891 the value of the firm satisfies the

value-matching condition

119865 (119883lowast

119891 119902119891) =

119883lowast

119891119902119891

119903 minus 120583

minus

120574 (119902119897+ 119902119891) 119902119891

119903

minus 119896119902119891

(5)

and the smooth-pasting condition

120597119865 (119883lowast

119891 119902119891)

120597119883

=

119902119891

119903 minus 120583

(6)

Solving (4) associated with conditions (5) and (6) we canobtain the followerrsquos value function119865 (119883 119902

119891)

=

119902119891

120573 minus 1

(

120574 (119902119897+ 119902119891)

119903

+ 119896)

times(

119883

119883lowast

119891

)

120573

if 119883 lt 119883lowast119891(119902119897 119902119891)

119883119902119891

119903 minus 120583

minus

120574 (119902119897+ 119902119891) 119902119891

119903

minus119896119902119891 if 119883 ge 119883lowast

119891(119902119897 119902119891)

(7)

and the optimal trigger of the follower

119883lowast

119891(119902119897 119902119891) =

120573 (119903 minus 120583)

120573 minus 1

(

120574 (119902119897+ 119902119891)

119903

+ 119896) (8)

where 120573 is the positive solution of

1

2

1205902

120573 (120573 minus 1) + 120583120573 minus 119903 = 0 (9)

Before the investment threshold is reached the followermakes a preparation to enter the market the investmentopportunity which is similar to an American option in amonopolymarket After the investment trigger is reached thepayoff is equivalent to the net present value and the followerexercises his option immediately

From (8) we know that the investment triggers of the twofirms to be a follower are identical to each other In otherwords if both firms are prone to be a follower each one has12 possibility to be successful

At the time when the firm draws up his investmenttiming he must consider the optimal capacity which can bedetermined by the maximization of the intrinsic value Theintrinsic value represents the value of a perpetual warrant oroption to invest in the project at any future date From (3) theintrinsic value of the follower can be expressed by

119882119891(119883) = max

119902lowast

119891

[

119883 (119905)

119903 minus 120583

119902119891minus

120574 (119902119897+ 119902119891) 119902119891

119903

minus 119896119902119891] (10)

Therefore119882119891(119883)must be governed by the first-order condi-

tion with respect to 119902119891

119883 (119905)

119903 minus 120583

minus

120574 (119902119897+ 2119902lowast

119891)

119903

minus 119896 = 0 (11)

That is to say when the current market demand is 119883(119905) andthe leaderrsquos capacity is 119902

119897 the optimal capacity of the follower

meets with

119902lowast

119891(119883 119902119897) =

1

2

[

119903

120574

(

119883

119903 minus 120583

minus 119896) minus 119902119897] (12)

From (12) it is easy to know that the follower will considerproviding more outputs when the total demand 119883(119905) is in agood state The reasoning is clear the price will also be highif the market demand is high More commodities will bringabout more profit Combining (8) and (12) we obtain theoptimal trigger and the capacity of the follower

119883lowast

119891(119902119897) =

120573120574 (119903 minus 120583)

119903 (120573 minus 2)

[119902119897+

119896119903

120574

] (13)

119902lowast

119891(119902119897) =

1

120573 minus 2

(119902119897+

119896119903

120574

) (14)

Expression (13) tells that the followerrsquos trigger is proportionalto the leaderrsquos capacity In other words if the leader providesmore outputs the follower will enter the market when

4 Abstract and Applied Analysis

the market demand is larger Obviously the leader investsearlier than the follower so he can enjoy a monopoly profitfor some time and occupy a large market share Only whenthe follower exercises his option at a high demand level doesthe firm obtain certain profit

In addition (14) means that a higher capacity of leaderwill bring about a higher capacity of follower which maybecontradict (12) As a matter of fact (12) implies that theleaderrsquos capacity and the followerrsquos capacity will changeinverse on condition that the market demand is fixed Theone invested earlier occupies a larger market share and leavesa smaller share to the follower so the follower can only enterthe market with little output However the stochastic marketdemand makes influence not only on the leaderrsquos capacitybut also on the followerrsquos and thus brings about the followerrsquoscapacity increase along with the leaderrsquos eventually

32 The Dominant Leader In the competitive game theleader 119897 must consider his rival 119891rsquos possible investmentstrategy Furthermore the leader knows that the follower willchoose to enter the market when the demand level is 119883lowast

119891(119902119897)

if the leader chooses 119902119897 There are two possibilities for the

follower One is to take action after the leader and thus resultsin sequential equilibrium the other is to invest as soon asthe leader does and thus results in simultaneous equilibriumTherefore if the leader wants to dominate the game he muststop his rival investing earlier than himself Suppose that theinitial demand level is 119883 To let the selected capacity preventthe competition of the follower successfully there must be119883lowast

119891(119902119897) gt 119883 since the follower must invest after the leader

Denote the solution of 119883lowast119891(119902119897) = 119883 as 119902

119897and substitute (13)

into this expression we obtain the following proposition

Proposition 1 To let the rival enter the market later than thefirm himself he can choose a capacity larger than a threshold119902119897to prevent his competitor where 119902

119897satisfies

119902119897=

119883119903 (120573 minus 2)

120573120574 (119903 minus 120583)

minus

119896119903

120574

(15)

Furthermore if one firm chooses a capacity lower than 119902119897 that

is 119902119897le 119902119897 his competitor will enter the market immediately

Equation (15) says that there must be a larger leadercapacity to prevent his rivalrsquos action when facing with highermarked demand If the firm prevents successfully the rivalwill then take action at some time later Let 119883lowast

119897119889(119905) and 119879lowast

119897119889

denote the leaderrsquos optimal trigger and optimal investmenttiming respectively If the initial state level119883(119905) is lower than119883lowast

119897119889(119905) the leader can enter the market when 119879lowast

119897119889is reached

Obviously there must be 119879lowast119891gt 119879lowast

119897119889 The value function of the

dominant leader 119871119897119889(119883 119902119897) is

119871119897119889(119883 119902119897) = max119879lowast

119897119889

119864119905int

119879lowast

119891

119879lowast

119897119889

[119883 (119904) minus 120574119902119897] 119890minus119903(119904minus119905)

119902119897119889119904

minus 119896119902119897119890minus119903(119879lowast

119897119889minus119905)

+ int

infin

119879lowast

119891

[119883 (119904) minus 120574 (119902119897+ 119902119891)]

times 119902119897119890minus119903(119904minus119905)

119889119904

(16)

In the above equation the first part denoted by 119871(1)119897119889(119883 119902119897)

indicates the monopoly value enjoyed by the leader beforethe follower exercises his optionThe remaining part denotedby 119871(2)119897119889(119883 119902119897) refers to the duopoly value after the followerrsquos

action In this case 119871(1)119897119889(119883 119902119897) satisfies the following value-

matching and smooth-pasting conditions

119871(1)

119897119889(119883lowast

119897119889) =

119883lowast

119897119889119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897

120597119871(1)

119897119889(119883lowast

119897119889)

120597119883

=

119902119897

119903 minus 120583

(17)

At the followerrsquos threshold 119883lowast119891 however the value function

meets with

119871(1)

119897119889(119883lowast

119891) =

119883lowast

119891119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus 119896119902119897 (18)

Solving the partial differential equation like (4) subject tothese above constraints we derive the expression of119871(1)

119897119889(119883 119902119897)

and the investment threshold of the dominant leader

119883lowast

119897119889(119902119897) =

120573 (119903 minus 120583)

120573 minus 1

(

120574

119903

119902119897+ 119896) (19)

By Itorsquos Lemma and the expression of (16) 119871(2)119897119889(119883 119902119897) can be

arranged as

1

2

1205902

11988321205972

119871(2)

119897119889(119883)

1205971198832

+ 120583119883

120597119871(2)

119897119889(119883)

120597119883

minus 119903119871(2)

119897119889(119883)

+ (119883 minus 120574119902119897) 119902119897= 0

(20)

Given that the negative effect of the followerrsquos option exerciseon leaderrsquos payoff is minus120574119902

119897119902119891 it should be subject to the

following condition

119871(2)

119897119889(119883lowast

119891) =

minus120574119902119897119902119891

119903

(21)

Solving (20) subject to the above condition yields the valuefunction of 119871(2)

119897119889(119883 119902119897)

Abstract and Applied Analysis 5

Summing up the derived 119871(1)119897119889(119883 119902119897) and 119871(2)

119897119889(119883 119902119897) the

resultant value function is119871119897119889(119883 119902119897)

=

119902119897

120573 minus 1

(

120574119902119897

119903

+ 119896)(

119883

119883lowast

119897119889

)

120573

minus

120574119902119897119902119891

119903

(

119883

119883lowast

119897119889

)

120573

if 119883 lt 119883lowast119897119889(119902119897)

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897

minus

120574119902119897119902119891

119903

(

119883

119883lowast

119897

)

120573

if 119883lowast119897119889(119902119897)le119883 lt 119883

lowast

119891(119902119897)

119883119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus 119896119902119897 if 119883 ge 119883lowast

119891(119902119897)

(22)

The value function of the dominant leader is composed bythree parts Before the leader enters the market he holds anAmerican option to enter preferentially At the time the leaderhas taken action and the follower does not exercise his optionthe leader enjoys amonopoly profit After the follower investsthe leader value is the net present value of the payoff

From (16) the intrinsic value of the dominant leader is

119882119897119889(119883 119902119897) = max119902lowast

119897119889

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897minus

120574119902119897119902119891

119903

(

119883

119883lowast

119891

)

120573

(23)

To maximize this value the optimal capacity 119902lowast119897119889must satisfy

the following first order condition

119883

119903 minus 120583

minus

2120574119902lowast

119897119889

119903

minus 119896

=

120574

119903

(

119883

119883lowast

119891

)

120573

[119902119891+

119902lowast

119897119889

120573 minus 2

minus 120573119902lowast

119897119889119902lowast

119891sdot

120597119883lowast

119891

120597119902lowast

119897119889

119883lowast

119891]

(24)

At the investment moment 119883 = 119883lowast

119897119889 Substituting (13) and

(14) into the above equation we obtain

119883lowast

119897119889

119903 minus 120583

minus

2120574119902lowast

119897119889

119903

minus 119896 =

120574

(120573 minus 2) 119903

(

119883lowast

119897119889

119883lowast

119891

)

120573

(2119902lowast

119897119889+

119896119903

120574

minus 120573119902lowast

119897119889)

(25)

Solving (25) we get the following proposition

Proposition 2 When one firm is dominating the other in aduopoly market under uncertainty the two firms will choosetheir optimal investment triggers and capacities with the forms

119883lowast

119897119889=

120573119896 (119903 minus 120583)

120573 minus 2

119902lowast

119897119889=

119896119903

(120573 minus 2) 120574

119883lowast

119891=

(120573 minus 1) (119903 minus 120583) 120573119896

(120573 minus 2)2

119902lowast

119891=

(120573 minus 1) 119896119903

(120573 minus 2)2

120574

(26)

33 The Preemptive Leader In this scenario each firm maybe prone to be a leader so the leadership is determined bytheir strategic interaction If the two firms enter the marketat the same time the equilibrium is not a sequential one buta simultaneous one To avoid the simultaneous investmentsuppose that the leader is decided by coin-toss method theneach firm has half of the possibility to be a leader After theleader takes action he will enjoy amonopoly profit before thefollower enters the game If the initial state level119883 is low and119883 le 119883

lowast

119891 the value function of the preemptive leader can be

expressed as

119871119897119901(119883 119902119897) = 119864119905int

119879lowast

119891

119879119897119901

[119883 (119904) minus 120574119902119897] 119890minus119903(119904minus119905)

119902119897119889119904 minus 119896119902

119897119890minus119903(119879119897119901minus119905)

+int

infin

119879lowast

119891

[119883 (119904) minus 120574 (119902119897+ 119902119891)] 119902119897119890minus119903(119904minus119905)

119889119904

(27)where 119879

119897119901denotes the investment timing of the preemptive

leader From (27) 119871119897119901(119883) meets with the following value-

matching condition

119871119897119901(119883lowast

119891) =

119883lowast

119891119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus 119896119902119897 (28)

Solving the partial differential equation like (20) subject tothe above constraint we obtain the value function of thepreemptive leader

119871119897119901(119883 119902119897) =

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897

minus

120574119902119897119902119891

119903

(

119883

119883lowast

119897

)

120573

if 119883 lt 119883lowast119891(119902119897)

119883119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus119896119902119897 if 119883 ge 119883lowast

119891(119902119897)

(29)Comparing (29) and (22) we find that the value functionof the preemptive leader is more complex than that of thedominant one At the time the follower enters the valuefunction of the leader is not continuous This is because theentrance of the follower will bring about negative impact onthe leader

For the preemptive leader his optimal capacity is alsodetermined by the maximization of his intrinsic value thatis

119882119897119901(119883 119902119897) = max119902lowast

119897119901

[

[

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897minus

120574119902119897119902119891

119903

(

119883

119883lowast

119891

)

120573

]

]

(30)Taking the first derivative on (30) with respect to 119902

119897 the

capacity of the preemptive leader 119902lowast119897119901meets with

119883

119903 minus 120583

=

120574

119903

(2119902lowast

119897119901+ 119902lowast

119891+

119902lowast

119897119901

120573 minus 2

) + 119896 (31)

6 Abstract and Applied Analysis

Substituting (14) into the above equation we obtain

119902lowast

119897119901(119883) =

119903

2120574

[

119883 (120573 minus 2)

(119903 minus 120583) (120573 minus 1)

minus 119896] (32)

Hence the optimal capacity is positive proportional to thetotal market demand

Now consider the investment strategy of the preemptiveleader If one firm decides to provide 119902

119897unit of output he

faces two choices One is to compete the leadership in thegame and obtain the payoff 119871

119897119889(119883 119902119897) the other is to be

a follower and get the payoff 119865(119883 119902119897) When the market

demand is low the leader value in (29) will be negative andlower than the followerrsquos strictly and preemptive competitionwill not happen Only when the preemptive leaderrsquos value islarger than the followerrsquos the preemptive action will occurTherefore the function 119871

119897119889(119883 119902119897) is defined in the range 119883 ge

0 119871119897119889(119883 119902119897) ge 119865(119883 119902

119897) 119883119897119901must be the solution of the

equation 119871119897119889(119883 119902119897) = 119865(119883 119902

119897) that is

119883119897119901119902lowast

119897119901

119903 minus 120583

minus

120574

119903

119902lowast2

119897119901minus 119896119902lowast

119897119901minus

120574

119903

119902lowast

119897119901119902lowast

119891(

119883119897119901

119883lowast

119891

)

120573

=

119902lowast

119897119901

120573 minus 1

[

120574

119903

(119902lowast

119897119901+ 119902lowast

119891) + 119896](

119883119897119901

119883lowast

119891

)

120573

(33)

Substituting (13) and (14) into the above equation andcombining (32) we obtain the following proposition

Proposition 3 If two firms preempt the game in a duopolymarket under uncertainty the optimal capacity of the preemp-tive leader 119902lowast

119897119901is the solution of

120573119902lowast

119897119901+

119896119903

120574

= 2(119902lowast

119897119901+

119896119903

120574

)[

[

(120573 minus 1) (2119902lowast

119897119901+ 119896119903120574)

120573 (119902lowast

119897119901+ 119896119903120574)

]

]

120573

(34)

and the solution must exist and be unique Furthermorethe investment threshold of the preemptive leader 119883

119897119901can be

expressed as

119883119897119901=

(119903 minus 120583) (120573 minus 1) 119903

120573 minus 2

[

2120574119902lowast

119897119901

119903

+ 119896] (35)

The followerrsquos trigger and optimal capacity satisfy

119883lowast

119891=

120574120573 (119903 minus 120583)

119903 (120573 minus 2)

(119902lowast

119897119901+

119896119903

120574

) 119902lowast

119891=

1

120573 minus 2

(119902lowast

119897119901+

119896119903

120574

)

(36)

Proof Simplifying (33) we can obtain the following equation

119883119897119901

119903 minus 120583

minus

120574119902lowast

119897119901

119903

minus 119896 =

2120574

(120573 minus 2) 119903

(

119883119897119901

119883lowast

119891

)

120573

(119902lowast

119897119901+

119896119903

120574

) (37)

Substituting (32) into the above equation we get (34)Now prove the existence and uniqueness of the preemptivecapacity Suppose that

(120573 minus 1) (2119902lowast

119897119901+

119896119903

120574

) = 119911120573(119902lowast

119897119901+

119896119903

120574

) (38)

where 119911 is a parameter to be determined Therefore

120573119902lowast

119897119901+

119896119903

120574

= 2119911120573

(119902lowast

119897119901+

119896119903

120574

) (39)

Simplifying the above two equations we get

119902lowast

119897119901=

120573119911 minus 120573 + 1

120573 minus 1 minus 120573119911

119896119903

120574

119902lowast

119897119901=

2119911120573

minus 1

120573 minus 2119911120573

119896119903

120574

(40)

These two optimal capacities must be identical to each otherAfter combining the above two equations we have

2119911120573

minus 120573119911 + 120573 minus 2 = 0 (41)

Obviously one solution is 1 that is 119902lowast119897119901= 119896119903120574(120573 minus 2) After

calculation we derive 119883119897119901= 119883lowast

119891 The expression means

that the preemptive leader and the follower will enter themarket simultaneously which contradicts the definition ofthe preemptive trigger Hence 119911 = 1 is ignored Consider theexistence and uniqueness of the other solution in the range(0 1) Suppose that 119891(119911) = 2119911120573 minus 120573119911 + 120573 minus 2 then 11989110158401015840(119911) =2120573(120573 minus 1) gt 0 from which we know that 119891(119911) is convexMeanwhile 119891(0) = 120573 minus 2 gt 0 119891(1) = 0 1198911015840(0) = minus120573 lt 01198911015840

(1) = 120573 gt 0 Consequently there must be one uniquesolution 119911lowast isin (0 1) such that 119891(119911) = 0 Thus the optimalcapacity has the form

119902lowast

119897119901=

120573119911lowast

minus 120573 + 1

120573 minus 1 minus 120573119911lowast

119896119903

120574

(42)

and the capacity is unique After the optimal capacity of thepreemptive leader is determined the investment triggers ofthe leader and the follower and the followerrsquos capacity can bedetermined

Although there are not explicit expressions for the invest-ment triggers and their capacities in the preemptive case wecan see that each personrsquos trigger is positive to his capacityMoreover the higher the capacity of the leader is the higherthe capacity of the follower isThese conclusions are the sameas that in the dominant case

When the initial state level is larger than the followertrigger two firms will take action at once Therefore when119883 gt 119883

lowast

119891 they will enter the market immediately with their

optimal capacities that maximize the intrinsic value 119882(119883)where

119882(119883) = max119902lowast

119883119902

119903 minus 120583

minus

21205741199022

119903

minus 119896119902 (43)

After solving (43) we can derive the optimal capacityThe following proposition gives the investment strategy insimultaneous equilibrium

Proposition 4 If the initial market demand level is highthen two firms will enter the market at the same time

Abstract and Applied Analysis 7

The optimal capacity and the market demand have the follow-ing correlation

119902lowast

(119883) =

119903

4120574

(

119883

119903 minus 120583

minus 119896) (44)

Furthermore this optimal capacity must surpass 119896119903(120573 minus1)[2120574(120573 minus 2)]

What should be mentioned is that there still exists onespecial situation in which two firms collude with each otherIn this case they combine into one organization and enter themarket simultaneously

4 Comparative Static

Consider the dominant case In this case the optimal invest-ment triggers and capacities satisfy (26) For these investmentthresholds we find that

120597119883lowast

119897119889

120597120590

= minus2 (119903 minus 120583) 119896

120597120573

120597120590

gt 0

120597119883lowast

119891

120597120590

= minus119896 (119903 minus 120583)

(3120573 minus 2)

(120573 minus 2)3

120597120573

120597120590

gt 0

(45)

The above two equations tell that each firm will postpone hisinvestment action when facing greater uncertainty whateverrole he is This is because that greater uncertainty meansgreater risk during investment Thus they will wait and lookfor better opportunity

Furthermore

120597 (119883lowast

119891119883lowast

119897119889)

120597120590

= minus

1

(120573 minus 2)2sdot

120597120573

120597120590

gt 0 (46)

which says that the difference between the trigger of theleader and that of the follower will be larger in the faceof increasing uncertainty In other words if there is greateruncertainty in the market both firms will delay investmentand the delayed margin of the follower will surpass that ofthe leader This is because the dominant leader will enjoymore monopoly profit if he takes action earlier and will notbe reluctant to postpone investment

Comparing these two optimal capacities we find

120597119902lowast

119897119889

120597120590

= minus

119896119903

120574(120573 minus 2)2

120597120573

120597120590

gt 0

120597119902lowast

119891

120597120590

= minus

120573119896119903

120574(120573 minus 2)3

120597120573

120597120590

gt 0

(47)

The above two equations show that two optimal capacitieswill increase along with the increase of uncertainty In otherwords when there is more uncertainty in the market twofirms will be prone to provide more outputs One primaryreason is that two firms will delay investment under greateruncertainty Therefore they will take action at a largerdemand level with more commodities

In addition

119902lowast

119891

119902lowast

119897119889

=

120573 minus 1

120573 minus 2

gt 1 (48)

120597 (119902lowast

119891119902lowast

119897119889)

120597120590

= minus

1

120574(120573 minus 2)2

120597120573

120597120590

gt 0 (49)

From (48) we know that the optimal capacity of thefollower is larger than that of the dominant leader Howeverin A Sadanand and V Sadanand [19] and Maggi [20] theydraw an opposite conclusion In their opinion if two firmscompete for the leadership the one with a larger capacitycan obtain the leadership successfully which is contrary tothe investment behavior in reality For example in the hotspot industry a company named T-mobile entered the Wi-Fi services market with a smaller capacity than its competitornamed Cometa Network After competition T-mobile suc-ceeded and drove its rival out of the market although thecapacity of Cometa Network was three times as T-mobilersquosThis event indicates that the firm with a smaller capacity canpreempt the leadership and confirms our conclusion In otherwords if one firm chooses a larger capacity the firmhas givenup the competition of the leadership and destines to fail inthe game since it will be turned out of the market by its rivalthrough smaller capacities In addition the conclusion canbe explained through their investment thresholds For thesetwo firms the investment trigger of the follower is larger thanthat of the leader which means that the follower will enterthe market in a larger market demand state and thus morecommodities will be provided

Furthermore although the leader takes action earlierthan the follower the payoff of the leader is lower than thatof the follower because of the smaller capacity of the formerTherefore the one invested later will obtain more profit Itdoes not mean each firm will be prone to be a follower Thereason is as follows Before the follower enters the marketthe leader will obtain a monopoly profit after investmentfor a period of time During that time the leader can alsoestablish brand reputation develop corporate culture andadvertise to consumers provide better facilities or servicesand thus occupy better market position Let T-mobile be anexample it preempted the market with small scale of wirelesshot spot and then provided free Wi-Fi service Thereforeother companies cannot compete with it by similar service

Equation (49) tells that both firms will provide more out-puts when the uncertainty in themarket increases Moreoverthe growth rate of the followerrsquos capacity will exceed that ofthe leaderrsquos Just as mentioned above the follower will waitfor the coming of a much higher demand state as greateruncertainty exists so the follower should provide a largeroutput to satisfy the demand

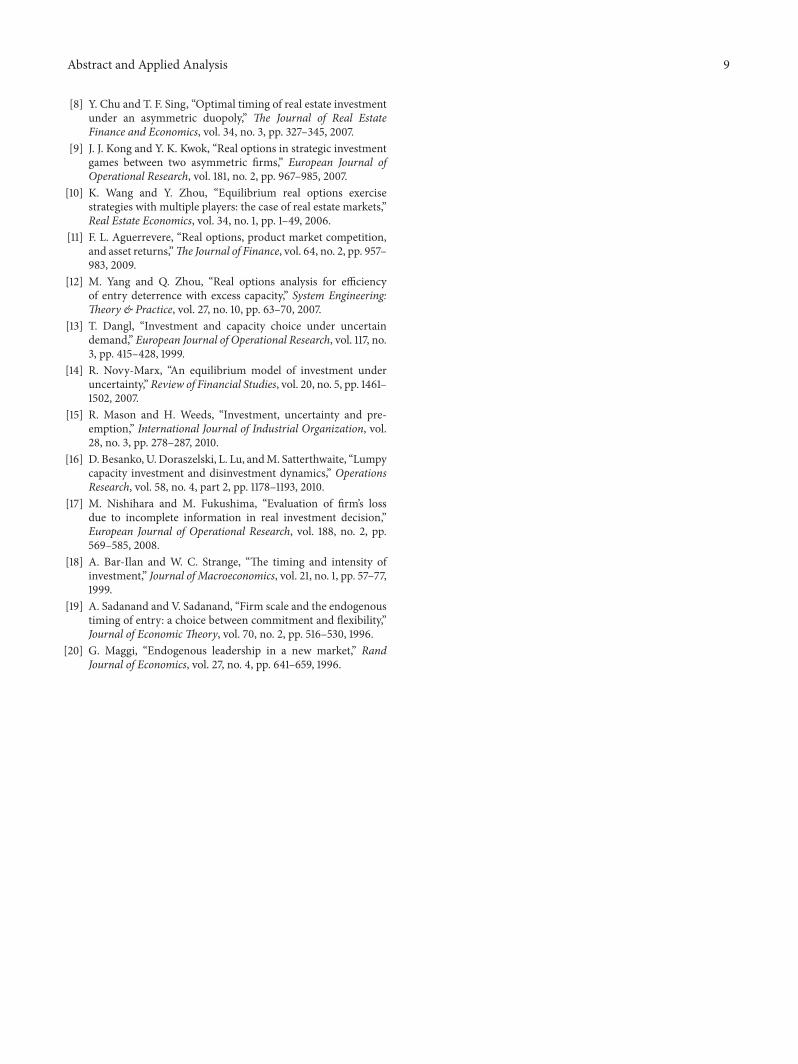

Now consider the preemptive case Since we cannotobtain explicit form of the preemptive trigger from (36) theproblem will be analyzed by numerical method just as listedin Figure 1

FromFigure 1we know that the conclusions of investmentstrategies in the preemptive case are similar to the resultsobtained in the dominant case Figure 1(a) says that both

8 Abstract and Applied Analysis

005 01 015 020

5

10

15

20

Xlowastf

X

120590

Xlp

(a) Investment trigger

01 015 020

2

4

6

qlowastf

Q

120590

qlp

(b) Optimal capacity

Figure 1 Investment strategies in the preemptive case The parameter values are 119903 = 005 119896 = 40 120583 = 0001 and 120574 = 4

the preemptive leader and the follower will postpone theirinvestment action when greater uncertainty exists in themarket and the postponed time of the leader will notsurpass that of the follower Consider their capacity strategiesFigure 1(b) shows that the leader capacity is lower than thefollower capacity Moreover both 119902lowast

119897119901and 119902lowast

119891increase along

with the increase of 120590 and the growth rate of 119902lowast119891is larger than

that of 119902lowast119897119901 Therefore the follower will be prone to enter the

market with a larger increased margin of capacity than hisrival These conclusions can be explained by the same reasonas in the dominant case

5 Conclusion

In the traditional real option literature such as Grenadier [6]andWang and Zhou [10] investment scale is fixed Firms willonly consider their investment timing of entering themarketIn this paper investment scale should be chosen by investorsthemselves For any firm it must consider when to enter themarket and howmuch production to be provided Moreovereach firm will provide its output by lumpy investment

In the duopolymarket the leader whether he is dominantor preemptive in the game will make great influence on thefollowerrsquos investment strategyWhen facing great uncertaintytwo firms will postpone their investment action Meanwhilethe delayed degree on both investment timing and capacity ofthe follower will surpass that of the leader Most important ofall the optimal capacity of the leader will be lower than thatof the follower under uncertainty which is contrary to theconclusion in Stackelberg model under certain environmentIn addition the one with less capacity can compete with hisrival successfully He can obtain monopoly profit and occupybettermarket position before the entrance of the follower andtherefore gain more consumers in the end

Conflict of Interests

The authors declare that there is no conflict of interestsregarding the publication of this paper

Acknowledgments

The authors are grateful to the referees for their helpful anduseful comments This research is partially supported bythe Scientific Research Fund of Chongqing Technology andBusiness University (no 1351004) and by the Research Fundof School of Finance in Chongqing Technology and BusinessUniversity (no 20132011031)

References

[1] A K Dixit and R S Pindyck Investment under UncertaintyPrinceton University Press Princeton NJ USA 1994

[2] E S Schwartz and L Trigeorgis Real Options and Investmentunder Uncertainty Classical Readings and Recent ContributionsThe MIT Press Cambridge Mass USA 2001

[3] R S Pindyck ldquoIrreversible investment capacity choice and thevalue of the firmrdquo The American Economic Review vol 78 no5 pp 969ndash985 1988

[4] S Capozza and Y Li ldquoThe timing and intensity of investmentrdquoThe American Economics Review vol 84 no 4 pp 889ndash9041994

[5] H T J Smit and L Trigeorgis Strategic Investment Real Optionsand Games Princeton University Press Princeton NJ USA2004

[6] S R Grenadier ldquoThe strategic exercise of options developmentcascades and overbuilding in real estate marketsrdquoThe Journal ofFinance vol 51 no 5 pp 1653ndash1679 1996

[7] S R Grenadier ldquoOption exercise games an application to theequilibrium investment strategies of firmsrdquo Review of FinancialStudies vol 15 no 3 pp 691ndash721 2002

Abstract and Applied Analysis 9

[8] Y Chu and T F Sing ldquoOptimal timing of real estate investmentunder an asymmetric duopolyrdquo The Journal of Real EstateFinance and Economics vol 34 no 3 pp 327ndash345 2007

[9] J J Kong and Y K Kwok ldquoReal options in strategic investmentgames between two asymmetric firmsrdquo European Journal ofOperational Research vol 181 no 2 pp 967ndash985 2007

[10] K Wang and Y Zhou ldquoEquilibrium real options exercisestrategies with multiple players the case of real estate marketsrdquoReal Estate Economics vol 34 no 1 pp 1ndash49 2006

[11] F L Aguerrevere ldquoReal options product market competitionand asset returnsrdquoThe Journal of Finance vol 64 no 2 pp 957ndash983 2009

[12] M Yang and Q Zhou ldquoReal options analysis for efficiencyof entry deterrence with excess capacityrdquo System EngineeringTheory amp Practice vol 27 no 10 pp 63ndash70 2007

[13] T Dangl ldquoInvestment and capacity choice under uncertaindemandrdquo European Journal of Operational Research vol 117 no3 pp 415ndash428 1999

[14] R Novy-Marx ldquoAn equilibrium model of investment underuncertaintyrdquo Review of Financial Studies vol 20 no 5 pp 1461ndash1502 2007

[15] R Mason and H Weeds ldquoInvestment uncertainty and pre-emptionrdquo International Journal of Industrial Organization vol28 no 3 pp 278ndash287 2010

[16] D BesankoUDoraszelski L Lu andM Satterthwaite ldquoLumpycapacity investment and disinvestment dynamicsrdquo OperationsResearch vol 58 no 4 part 2 pp 1178ndash1193 2010

[17] M Nishihara and M Fukushima ldquoEvaluation of firmrsquos lossdue to incomplete information in real investment decisionrdquoEuropean Journal of Operational Research vol 188 no 2 pp569ndash585 2008

[18] A Bar-Ilan and W C Strange ldquoThe timing and intensity ofinvestmentrdquo Journal of Macroeconomics vol 21 no 1 pp 57ndash771999

[19] A Sadanand and V Sadanand ldquoFirm scale and the endogenoustiming of entry a choice between commitment and flexibilityrdquoJournal of Economic Theory vol 70 no 2 pp 516ndash530 1996

[20] G Maggi ldquoEndogenous leadership in a new marketrdquo RandJournal of Economics vol 27 no 4 pp 641ndash659 1996

Submit your manuscripts athttpwwwhindawicom

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Mathematical Problems in Engineering

Hindawi Publishing Corporationhttpwwwhindawicom

Differential EquationsInternational Journal of

Volume 2014

Applied MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Probability and StatisticsHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Mathematical PhysicsAdvances in

Complex AnalysisJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

OptimizationJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

CombinatoricsHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

International Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Operations ResearchAdvances in

Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Function Spaces

Abstract and Applied AnalysisHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

International Journal of Mathematics and Mathematical Sciences

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

The Scientific World JournalHindawi Publishing Corporation httpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Algebra

Discrete Dynamics in Nature and Society

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Decision SciencesAdvances in

Discrete MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom

Volume 2014 Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Stochastic AnalysisInternational Journal of

2 Abstract and Applied Analysis

and competitivemarketswith different production capacitiesAguerrevere [11] studies the effects of competitive interac-tions on investment decisions and on the dynamics of theprice of a nonstorable commodity in a model of incrementalinvestment with time to build and operating flexibility Yangand Zhou [12] extends Dangl [13] to a duopoly in which oneof the firms is the incumbent and the other firm is the entrantNovy-Marx [14] analyzes the optimal investment decisionsof heterogeneous firms in a competitive and uncertain envi-ronment and shows that in the competitive equilibrium realoption premia remains significant Comparing these paperswith ours the main difference and contribution are that ourwork analyzes the influence of capacity choice and obtainsmany interest conclusions For example previous literatureusually predicts that the leader is better off by providing alarger capacity than his rival while this paper proves that thefirst mover enters with a smaller capacity than the secondmover and sheds light on why firm lacks incentive to pursuea large capacity preemption in an uncertain market

This paper is divided into five sections In Section 2 welay out the model framework Section 3 derives the valuefunctions and investment thresholds when the firms serveas the follower preemptive leader and dominant leaderSection 4 explores a comparative static on the volatility ofstochasticmarket demand In Section 5we draw a conclusionof this paper

2 Model Framework

The model of this paper comes from the redevelopmentinvestment problem of land in Capozza and Li [4] Intheir paper cash flow is uncertain in the whole investmentprocess and satisfies Algebra Brown Motion When investormakes his investment strategy he must consider not only theinvestment timing but also the investment scale while thelatter is reflected by intensity What is different from Capozzaand Li [4] is that this paper deals with investment problemin a duopoly market and uses product capacity to reflect eachinvestorrsquos scale For these two firms they must decide whento enter the market and what capacity they should produce

Suppose that both firms are rational risk-neutral andprofit-maximizing The model adopts riskless interest rate 119903to discount their payoff Furthermore two firms can provideunstorable commodity the price of which is related to themarket supply Specially we assume that the price119875(119905) at time119905 satisfies the following simple inverse demand function

119875 (119905) = 119883 (119905) minus 120574119876 (1)

where 119883(119905) is the exogenous market demand shock 119876 is thetotal market supply and nonnegative parameter 120574 is the slopeof the linear demand function and is used to reflect the pricesensitivity to the supply From (1)we know that the increase ordecrease of the total market supply will cause the price to riseor fall Furthermore function (1) indicates that the change ofthe market demand 119883 will be reflected on inverse demandcurve Since the variable changes unpredictably we suppose

that it is stochastic and evolves as a geometric Brownianmotion

119889119883 (119905) = 120583119883119889119905 + 120590119883119889119885 (119905) (2)

where 120583 is a given positive constant and denotes the expectedgrowth of119883120590 represents the volatility of themarket demandand 119889119885 is an increment of a standard Wiener motion anddenotes the resource of uncertainty Furthermore (2) meansthat investors only know the current level of the marketdemand while the future level meets with a lognormaldistributionTherefore ln119883 increases at a certain growth rateand is disturbed by a normally distributed random variableIn addition to guarantee that the option is exercised within afinite period of time we assume that 119903 gt 120583

Each firm has only one chance to invest As long as theinvestment opportunity exists the firm has to consider whento take action and what capacity to provide Suppose that theinvestment sunk cost is governed by the relation 119862(119876) = 119896119876where 119896 is a nonnegative parameter Hence the investmentcost will increase with their capacity choice

In the existing literature there are two types of invest-ment One is lumpy investment such as Mason and Weeds[15] Besanko et al [16] and Nishihara and Fukushima[17] the other is incremental investment such as Pindyck[3] Aguerrevere [11] and Novy-Marx [14] In the lumpyinvestment investment scale is decided at the investmenttime and all commodities are provided into the marketfor one time In the incremental investment commoditiescan be increased by an infinitesimal amount and the initialinvestment scale is expanded in the investment process Bar-Ilan and Strange [18] make a comparison with these twotypes Pindyck [3] points out that incremental investment isan extreme case of lumpy investment and can be calculatedconveniently Therefore this paper adopts lumpy investmentto analyze capacity choice problem under uncertainty that isto say investor can adjust his output flexibly according to theexternal uncertainty in the environment while all productsare supplied into the market the moment he exercises hisoption

3 Investment Problem in an Duopoly Market

In this section we will discuss strategic and competitiveinvestment problem in a duopoly market where uncertaintyis reflected on the stochastic market demand Two firms haveto decide not only their investment timing but also theiroptimal capacity Competitive behavior will be discussedfrom two aspects One is a dominant case and the other is apreemptive case Namely the leader is dominant in the gameor preempts the market

When the leader makes his decision he must considerthe possible strategy of the follower For the dominant leaderthe leadership may be determined by two situations Oneis determined exogenously in which the leader can choosehis optimal investment timing and optimal capacity since heknows his competitor will be prone to be a follower Theother is determined endogenously in which the leadershipis obtained after intense competition since the firm does

Abstract and Applied Analysis 3

not have comparative advantage over his rival in the gameDenote the leader and the follower as 119897 and 119891 respectively

Just as the standard method in dynamic programmingwe will adopt inverse induction Firstly consider the valuefunction of the follower Secondly consider the investmentproblem of the dominant leader Thirdly premeditate thevalue function of the preemptive leader The value functionsin the case where two firms take action simultaneously arejust the same as the value of themselves to be a follower

31 Follower Since the leader has taken investment actionthe follower can make his decision optimally Denote theinvestment timing and capacity of the follower as 119879lowast

119891and

119902lowast

119891 respectively If his competitor 119897 enters the market with

capacity 119902119897 the value function of the follower can be expressed

as

119865 (119883 119902119891) = max119879lowast

119891

119864119905int

infin

119879lowast

119891

[119883 (119904) minus 120574 (119902119897+ 119902119891)] 119890minus119903(119904minus119905)

119889119904

minus119896119890minus119903(119879lowast

119891minus119905)

119902119891

(3)

When the payoff of the firm is large enough that is 119883surpasses his investment trigger 119883lowast

119891 the follower begins to

exercise his option Furthermore the question to look for119883lowast119891

is equivalent to the maximization of the option valueBy dynamic programming (3) can be translated into the

following partial differential equation

1

2

1205902

11988321205972

119865 (119883)

1205971198832

+ 120583119883

120597119865 (119883)

120597119883

minus 119903119865 (119883) = 0 (4)

At the optimal trigger 119883lowast119891 the value of the firm satisfies the

value-matching condition

119865 (119883lowast

119891 119902119891) =

119883lowast

119891119902119891

119903 minus 120583

minus

120574 (119902119897+ 119902119891) 119902119891

119903

minus 119896119902119891

(5)

and the smooth-pasting condition

120597119865 (119883lowast

119891 119902119891)

120597119883

=

119902119891

119903 minus 120583

(6)

Solving (4) associated with conditions (5) and (6) we canobtain the followerrsquos value function119865 (119883 119902

119891)

=

119902119891

120573 minus 1

(

120574 (119902119897+ 119902119891)

119903

+ 119896)

times(

119883

119883lowast

119891

)

120573

if 119883 lt 119883lowast119891(119902119897 119902119891)

119883119902119891

119903 minus 120583

minus

120574 (119902119897+ 119902119891) 119902119891

119903

minus119896119902119891 if 119883 ge 119883lowast

119891(119902119897 119902119891)

(7)

and the optimal trigger of the follower

119883lowast

119891(119902119897 119902119891) =

120573 (119903 minus 120583)

120573 minus 1

(

120574 (119902119897+ 119902119891)

119903

+ 119896) (8)

where 120573 is the positive solution of

1

2

1205902

120573 (120573 minus 1) + 120583120573 minus 119903 = 0 (9)

Before the investment threshold is reached the followermakes a preparation to enter the market the investmentopportunity which is similar to an American option in amonopolymarket After the investment trigger is reached thepayoff is equivalent to the net present value and the followerexercises his option immediately

From (8) we know that the investment triggers of the twofirms to be a follower are identical to each other In otherwords if both firms are prone to be a follower each one has12 possibility to be successful

At the time when the firm draws up his investmenttiming he must consider the optimal capacity which can bedetermined by the maximization of the intrinsic value Theintrinsic value represents the value of a perpetual warrant oroption to invest in the project at any future date From (3) theintrinsic value of the follower can be expressed by

119882119891(119883) = max

119902lowast

119891

[

119883 (119905)

119903 minus 120583

119902119891minus

120574 (119902119897+ 119902119891) 119902119891

119903

minus 119896119902119891] (10)

Therefore119882119891(119883)must be governed by the first-order condi-

tion with respect to 119902119891

119883 (119905)

119903 minus 120583

minus

120574 (119902119897+ 2119902lowast

119891)

119903

minus 119896 = 0 (11)

That is to say when the current market demand is 119883(119905) andthe leaderrsquos capacity is 119902

119897 the optimal capacity of the follower

meets with

119902lowast

119891(119883 119902119897) =

1

2

[

119903

120574

(

119883

119903 minus 120583

minus 119896) minus 119902119897] (12)

From (12) it is easy to know that the follower will considerproviding more outputs when the total demand 119883(119905) is in agood state The reasoning is clear the price will also be highif the market demand is high More commodities will bringabout more profit Combining (8) and (12) we obtain theoptimal trigger and the capacity of the follower

119883lowast

119891(119902119897) =

120573120574 (119903 minus 120583)

119903 (120573 minus 2)

[119902119897+

119896119903

120574

] (13)

119902lowast

119891(119902119897) =

1

120573 minus 2

(119902119897+

119896119903

120574

) (14)

Expression (13) tells that the followerrsquos trigger is proportionalto the leaderrsquos capacity In other words if the leader providesmore outputs the follower will enter the market when

4 Abstract and Applied Analysis

the market demand is larger Obviously the leader investsearlier than the follower so he can enjoy a monopoly profitfor some time and occupy a large market share Only whenthe follower exercises his option at a high demand level doesthe firm obtain certain profit

In addition (14) means that a higher capacity of leaderwill bring about a higher capacity of follower which maybecontradict (12) As a matter of fact (12) implies that theleaderrsquos capacity and the followerrsquos capacity will changeinverse on condition that the market demand is fixed Theone invested earlier occupies a larger market share and leavesa smaller share to the follower so the follower can only enterthe market with little output However the stochastic marketdemand makes influence not only on the leaderrsquos capacitybut also on the followerrsquos and thus brings about the followerrsquoscapacity increase along with the leaderrsquos eventually

32 The Dominant Leader In the competitive game theleader 119897 must consider his rival 119891rsquos possible investmentstrategy Furthermore the leader knows that the follower willchoose to enter the market when the demand level is 119883lowast

119891(119902119897)

if the leader chooses 119902119897 There are two possibilities for the

follower One is to take action after the leader and thus resultsin sequential equilibrium the other is to invest as soon asthe leader does and thus results in simultaneous equilibriumTherefore if the leader wants to dominate the game he muststop his rival investing earlier than himself Suppose that theinitial demand level is 119883 To let the selected capacity preventthe competition of the follower successfully there must be119883lowast

119891(119902119897) gt 119883 since the follower must invest after the leader

Denote the solution of 119883lowast119891(119902119897) = 119883 as 119902

119897and substitute (13)

into this expression we obtain the following proposition

Proposition 1 To let the rival enter the market later than thefirm himself he can choose a capacity larger than a threshold119902119897to prevent his competitor where 119902

119897satisfies

119902119897=

119883119903 (120573 minus 2)

120573120574 (119903 minus 120583)

minus

119896119903

120574

(15)

Furthermore if one firm chooses a capacity lower than 119902119897 that

is 119902119897le 119902119897 his competitor will enter the market immediately

Equation (15) says that there must be a larger leadercapacity to prevent his rivalrsquos action when facing with highermarked demand If the firm prevents successfully the rivalwill then take action at some time later Let 119883lowast

119897119889(119905) and 119879lowast

119897119889

denote the leaderrsquos optimal trigger and optimal investmenttiming respectively If the initial state level119883(119905) is lower than119883lowast

119897119889(119905) the leader can enter the market when 119879lowast

119897119889is reached

Obviously there must be 119879lowast119891gt 119879lowast

119897119889 The value function of the

dominant leader 119871119897119889(119883 119902119897) is

119871119897119889(119883 119902119897) = max119879lowast

119897119889

119864119905int

119879lowast

119891

119879lowast

119897119889

[119883 (119904) minus 120574119902119897] 119890minus119903(119904minus119905)

119902119897119889119904

minus 119896119902119897119890minus119903(119879lowast

119897119889minus119905)

+ int

infin

119879lowast

119891

[119883 (119904) minus 120574 (119902119897+ 119902119891)]

times 119902119897119890minus119903(119904minus119905)

119889119904

(16)

In the above equation the first part denoted by 119871(1)119897119889(119883 119902119897)

indicates the monopoly value enjoyed by the leader beforethe follower exercises his optionThe remaining part denotedby 119871(2)119897119889(119883 119902119897) refers to the duopoly value after the followerrsquos

action In this case 119871(1)119897119889(119883 119902119897) satisfies the following value-

matching and smooth-pasting conditions

119871(1)

119897119889(119883lowast

119897119889) =

119883lowast

119897119889119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897

120597119871(1)

119897119889(119883lowast

119897119889)

120597119883

=

119902119897

119903 minus 120583

(17)

At the followerrsquos threshold 119883lowast119891 however the value function

meets with

119871(1)

119897119889(119883lowast

119891) =

119883lowast

119891119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus 119896119902119897 (18)

Solving the partial differential equation like (4) subject tothese above constraints we derive the expression of119871(1)

119897119889(119883 119902119897)

and the investment threshold of the dominant leader

119883lowast

119897119889(119902119897) =

120573 (119903 minus 120583)

120573 minus 1

(

120574

119903

119902119897+ 119896) (19)

By Itorsquos Lemma and the expression of (16) 119871(2)119897119889(119883 119902119897) can be

arranged as

1

2

1205902

11988321205972

119871(2)

119897119889(119883)

1205971198832

+ 120583119883

120597119871(2)

119897119889(119883)

120597119883

minus 119903119871(2)

119897119889(119883)

+ (119883 minus 120574119902119897) 119902119897= 0

(20)

Given that the negative effect of the followerrsquos option exerciseon leaderrsquos payoff is minus120574119902

119897119902119891 it should be subject to the

following condition

119871(2)

119897119889(119883lowast

119891) =

minus120574119902119897119902119891

119903

(21)

Solving (20) subject to the above condition yields the valuefunction of 119871(2)

119897119889(119883 119902119897)

Abstract and Applied Analysis 5

Summing up the derived 119871(1)119897119889(119883 119902119897) and 119871(2)

119897119889(119883 119902119897) the

resultant value function is119871119897119889(119883 119902119897)

=

119902119897

120573 minus 1

(

120574119902119897

119903

+ 119896)(

119883

119883lowast

119897119889

)

120573

minus

120574119902119897119902119891

119903

(

119883

119883lowast

119897119889

)

120573

if 119883 lt 119883lowast119897119889(119902119897)

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897

minus

120574119902119897119902119891

119903

(

119883

119883lowast

119897

)

120573

if 119883lowast119897119889(119902119897)le119883 lt 119883

lowast

119891(119902119897)

119883119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus 119896119902119897 if 119883 ge 119883lowast

119891(119902119897)

(22)

The value function of the dominant leader is composed bythree parts Before the leader enters the market he holds anAmerican option to enter preferentially At the time the leaderhas taken action and the follower does not exercise his optionthe leader enjoys amonopoly profit After the follower investsthe leader value is the net present value of the payoff

From (16) the intrinsic value of the dominant leader is

119882119897119889(119883 119902119897) = max119902lowast

119897119889

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897minus

120574119902119897119902119891

119903

(

119883

119883lowast

119891

)

120573

(23)

To maximize this value the optimal capacity 119902lowast119897119889must satisfy

the following first order condition

119883

119903 minus 120583

minus

2120574119902lowast

119897119889

119903

minus 119896

=

120574

119903

(

119883

119883lowast

119891

)

120573

[119902119891+

119902lowast

119897119889

120573 minus 2

minus 120573119902lowast

119897119889119902lowast

119891sdot

120597119883lowast

119891

120597119902lowast

119897119889

119883lowast

119891]

(24)

At the investment moment 119883 = 119883lowast

119897119889 Substituting (13) and

(14) into the above equation we obtain

119883lowast

119897119889

119903 minus 120583

minus

2120574119902lowast

119897119889

119903

minus 119896 =

120574

(120573 minus 2) 119903

(

119883lowast

119897119889

119883lowast

119891

)

120573

(2119902lowast

119897119889+

119896119903

120574

minus 120573119902lowast

119897119889)

(25)

Solving (25) we get the following proposition

Proposition 2 When one firm is dominating the other in aduopoly market under uncertainty the two firms will choosetheir optimal investment triggers and capacities with the forms

119883lowast

119897119889=

120573119896 (119903 minus 120583)

120573 minus 2

119902lowast

119897119889=

119896119903

(120573 minus 2) 120574

119883lowast

119891=

(120573 minus 1) (119903 minus 120583) 120573119896

(120573 minus 2)2

119902lowast

119891=

(120573 minus 1) 119896119903

(120573 minus 2)2

120574

(26)

33 The Preemptive Leader In this scenario each firm maybe prone to be a leader so the leadership is determined bytheir strategic interaction If the two firms enter the marketat the same time the equilibrium is not a sequential one buta simultaneous one To avoid the simultaneous investmentsuppose that the leader is decided by coin-toss method theneach firm has half of the possibility to be a leader After theleader takes action he will enjoy amonopoly profit before thefollower enters the game If the initial state level119883 is low and119883 le 119883

lowast

119891 the value function of the preemptive leader can be

expressed as

119871119897119901(119883 119902119897) = 119864119905int

119879lowast

119891

119879119897119901

[119883 (119904) minus 120574119902119897] 119890minus119903(119904minus119905)

119902119897119889119904 minus 119896119902

119897119890minus119903(119879119897119901minus119905)

+int

infin

119879lowast

119891

[119883 (119904) minus 120574 (119902119897+ 119902119891)] 119902119897119890minus119903(119904minus119905)

119889119904

(27)where 119879

119897119901denotes the investment timing of the preemptive

leader From (27) 119871119897119901(119883) meets with the following value-

matching condition

119871119897119901(119883lowast

119891) =

119883lowast

119891119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus 119896119902119897 (28)

Solving the partial differential equation like (20) subject tothe above constraint we obtain the value function of thepreemptive leader

119871119897119901(119883 119902119897) =

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897

minus

120574119902119897119902119891

119903

(

119883

119883lowast

119897

)

120573

if 119883 lt 119883lowast119891(119902119897)

119883119902119897

119903 minus 120583

minus

120574119902119897(119902119897+ 119902119891)

119903

minus119896119902119897 if 119883 ge 119883lowast

119891(119902119897)

(29)Comparing (29) and (22) we find that the value functionof the preemptive leader is more complex than that of thedominant one At the time the follower enters the valuefunction of the leader is not continuous This is because theentrance of the follower will bring about negative impact onthe leader

For the preemptive leader his optimal capacity is alsodetermined by the maximization of his intrinsic value thatis

119882119897119901(119883 119902119897) = max119902lowast

119897119901

[

[

119883119902119897

119903 minus 120583

minus

1205741199022

119897

119903

minus 119896119902119897minus

120574119902119897119902119891

119903

(

119883

119883lowast

119891

)

120573

]

]

(30)Taking the first derivative on (30) with respect to 119902

119897 the

capacity of the preemptive leader 119902lowast119897119901meets with

119883

119903 minus 120583

=

120574

119903

(2119902lowast

119897119901+ 119902lowast

119891+

119902lowast

119897119901

120573 minus 2

) + 119896 (31)

6 Abstract and Applied Analysis

Substituting (14) into the above equation we obtain

119902lowast

119897119901(119883) =

119903

2120574

[

119883 (120573 minus 2)

(119903 minus 120583) (120573 minus 1)

minus 119896] (32)

Hence the optimal capacity is positive proportional to thetotal market demand

Now consider the investment strategy of the preemptiveleader If one firm decides to provide 119902

119897unit of output he

faces two choices One is to compete the leadership in thegame and obtain the payoff 119871

119897119889(119883 119902119897) the other is to be

a follower and get the payoff 119865(119883 119902119897) When the market

demand is low the leader value in (29) will be negative andlower than the followerrsquos strictly and preemptive competitionwill not happen Only when the preemptive leaderrsquos value islarger than the followerrsquos the preemptive action will occurTherefore the function 119871

119897119889(119883 119902119897) is defined in the range 119883 ge

0 119871119897119889(119883 119902119897) ge 119865(119883 119902

119897) 119883119897119901must be the solution of the

equation 119871119897119889(119883 119902119897) = 119865(119883 119902

119897) that is

119883119897119901119902lowast