republic of trinidad and tobago - …webopac.ttlawcourts.org/libraryjud/judgments/coa/... · page 1...

TRANSCRIPT

Page 1 of 44

REPUBLIC OF TRINIDAD AND TOBAGO

IN THE COURT OF APPEAL

Civil Appeal No. 187 of 2011

BETWEEN

BAUHUIS COATING INTERNATIONAL LIMITED

Appellant

AND

THE BOARD OF INLAND REVENUE

Respondent

PANEL: A. Mendonça J.A.

R. Narine J.A.

M. Mohammed J.A.

APPEARANCES:

Mr. G. Pantin instructed by Ms. A. Peters for the appellant.

Ms. L. Lucky-Samaroo and Mr. D. Ali instructed by Ms. L. Singh-Dan for the respondent.

DATE OF DELIVERY: March 12th

, 2014

Page 2 of 44

JUDGMENT

Delivered by Mendonça, J.A.

[1] I have read the judgment of Mohammed, J.A. and I also agree that this appeal should be

allowed and with the order he proposes to make. I however wish to add a few words of my

own.

[2] This appeal is by way of the case stated from the Tax Appeal Board (the Board). The issue

in this appeal is whether commercial supplies made by the Appellant fall within Item 12 of

Schedule 2 of the Value Added Tax Act Chap. 75:06 (the VAT Act). Item 12 of Schedule 2

is as follows:

“12. Any services which are supplied for a consideration that is payable in a

currency other than that of Trinidad and Tobago, to a recipient who is not within

Trinidad and Tobago at the time when the services are performed.”

A supply of services falling within Item 12 is zero rated and is therefore not chargeable

to value added tax.

[3] The issue arose in this way. The Appellant is a company duly incorporated under the laws

of this jurisdiction. It was at all material times engaged principally in the business of

providing pipe coating services. It is a wholly owned subsidiary of Bauhuis Coating

Limited (BCL) a foreign company registered in Cyprus. The commercial supplies

concerned pipe coating services supplied under a contract between the Appellant and BCL.

The Appellant regarded those supplies as zero- rated under Item 12 because they were

supplied for a consideration that was payable in United States dollars to its parent company

who was not within Trinidad and Tobago at the time of the supply.

[4] The Board of Inland Revenue (the Respondent) did not agree with that position. It assessed

the Appellant in respect of the supplies of value added tax at 15% and varied the

Appellant’s liability to value added tax. The Respondent considered an objection to its

assessment by the Appellant but affirmed the assessment. On appeal to the Board, the

Board also affirmed the assessment. The Appellant now appeals to this Court.

Page 3 of 44

[5] Before the Board the parties filed and relied on a statement of agreed facts. The statement is

as follows:

1. The Appellant is a company duly registered under the laws of the Republic of

Trinidad and Tobago and whose registered address is c/o PricewaterhouseCoopers

11-13 Victoria Avenue, Port of Spain. The Appellant was with effect from August

17, 2000 registered pursuant to the provisions of section 20 of the VAT Act, as

number 118195. The tax periods under appeal are 200106, 200108, 200110 and

200112.

2. At all material times the Appellant provided pipe coating services under subcontract

to a non-resident company, BCL, registered in Cyprus. The Appellant performed all

activity under the contract in Trinidad and Tobago. All the supplies made by the

Appellant were commercial supplies.

3. BCL was not registered in Trinidad and Tobago, was not resident in Trinidad and

Tobago and had no branch here. The invoices were issued to BCL payable in United

States dollars.

4. The Appellant duly filed its value added tax returns for the tax periods and by

inadvertence reported no commercial supplies for the tax period 200106. It reported

no output value added tax. It reported its input value added tax as follows:

Period 200106 - $1,168,886.62

Period 200108 - $1,107,282.46

Period 200110 - $1,791,292.64

Period 200112 - $96,280.03

The Appellant regarded all its commercial supplies as zero rated under Item 12 of

Schedule 2 of the VAT Act. The Appellant, therefore, charged no output tax on its

supplies. It offset the above sums against the output tax of nil and claimed value

added tax refundable in each period to the full extent of the input tax.

Page 4 of 44

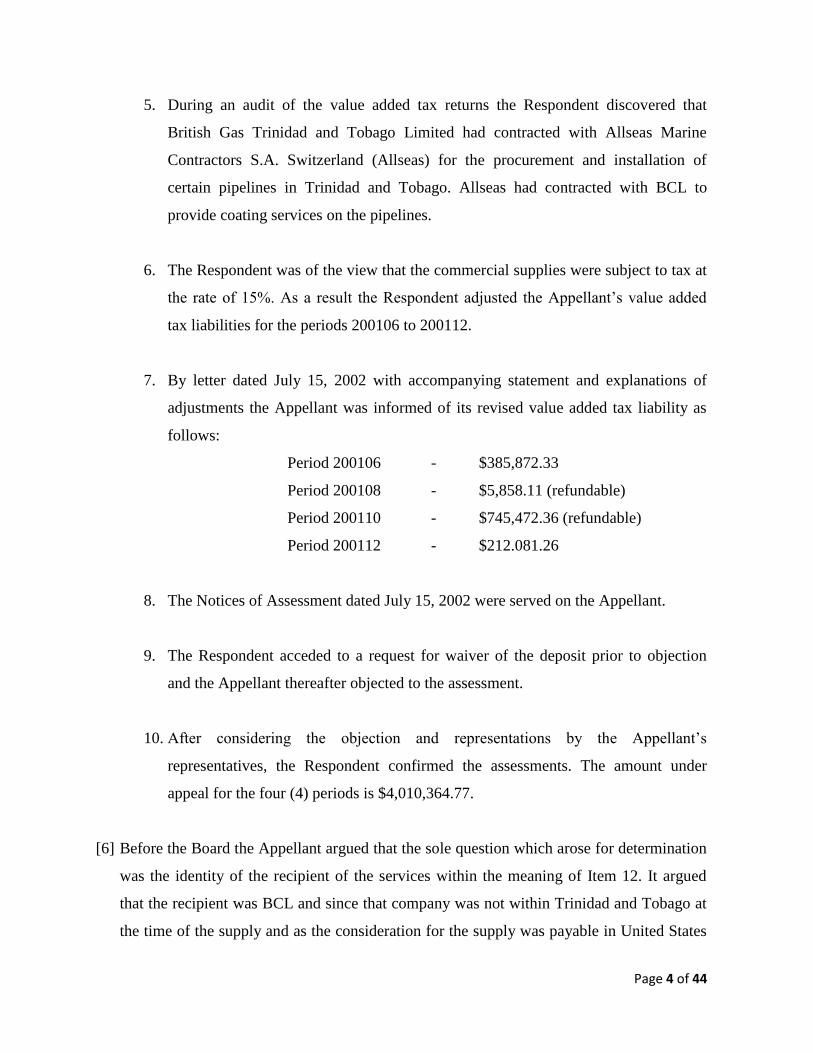

5. During an audit of the value added tax returns the Respondent discovered that

British Gas Trinidad and Tobago Limited had contracted with Allseas Marine

Contractors S.A. Switzerland (Allseas) for the procurement and installation of

certain pipelines in Trinidad and Tobago. Allseas had contracted with BCL to

provide coating services on the pipelines.

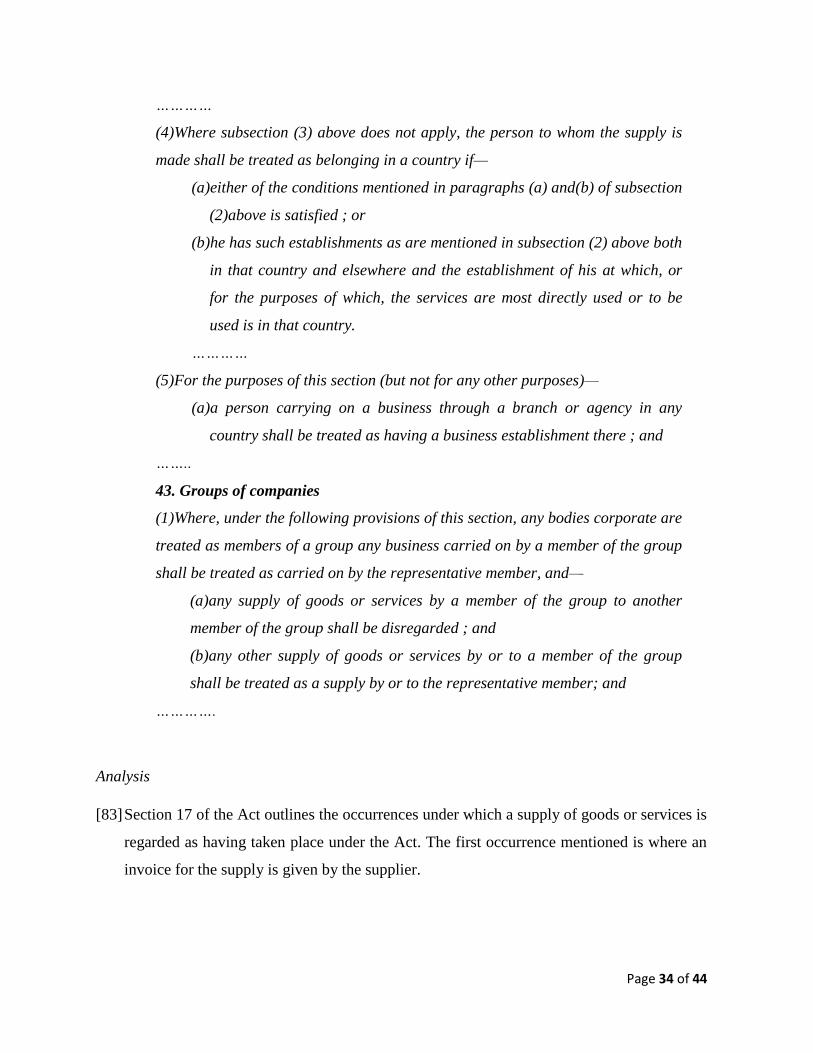

6. The Respondent was of the view that the commercial supplies were subject to tax at

the rate of 15%. As a result the Respondent adjusted the Appellant’s value added

tax liabilities for the periods 200106 to 200112.

7. By letter dated July 15, 2002 with accompanying statement and explanations of

adjustments the Appellant was informed of its revised value added tax liability as

follows:

Period 200106 - $385,872.33

Period 200108 - $5,858.11 (refundable)

Period 200110 - $745,472.36 (refundable)

Period 200112 - $212.081.26

8. The Notices of Assessment dated July 15, 2002 were served on the Appellant.

9. The Respondent acceded to a request for waiver of the deposit prior to objection

and the Appellant thereafter objected to the assessment.

10. After considering the objection and representations by the Appellant’s

representatives, the Respondent confirmed the assessments. The amount under

appeal for the four (4) periods is $4,010,364.77.

[6] Before the Board the Appellant argued that the sole question which arose for determination

was the identity of the recipient of the services within the meaning of Item 12. It argued

that the recipient was BCL and since that company was not within Trinidad and Tobago at

the time of the supply and as the consideration for the supply was payable in United States

Page 5 of 44

dollars the supply fell within Item 12 of Schedule 2 of the VAT Act and was therefore zero

rated. The Respondent on the other hand contended that British Gas Trinidad and Tobago

Limited (BGTT) was the recipient within the meaning of Item 12 and since that is a

Trinidad and Tobago company carrying on business in Trinidad and Tobago, the supply by

the Appellant did not qualify to be zero rated. It further submitted that even if the Board did

not agree that BGTT was the recipient, the supplies would still not be zero rated as BCL

was “within Trinidad and Tobago” as that term is used in Item 12.

[7] The Board, in affirming the assessment of the Respondent, based its decision in its

judgment on the ground that the recipient was BGTT. In the case stated (which

incorporated the judgment) the Board said that it found as a fact that BCL must be regarded

“as having a constructive presence within Trinidad and Tobago having regard to their

connection with the [Appellant]”. This finding of fact might support an alternative ground

for the Board’s decision namely that BCL was the recipient and within Trinidad and

Tobago for the purposes of Item 12.

[8] Before this Court, Mr. Pantin, Counsel for the Appellant, submitted that the Board erred in

law in concluding that the recipient was BGTT. He argued, as the Appellant had done

before the Board, that the recipient within the meaning of Item 12 on a proper construction

of the VAT Act could only be BCL. Accordingly the commercial supplies were caught by

Item 12 and were therefore zero rated.

[9] Ms. Lucky-Samaroo, Counsel for the Respondent, on the other hand sought (with one

exception) to support the conclusion of the Board.

[10] The exception to which reference is made is with respect to the Board’s view as to whether

the issue as to the identity of the recipient was a question of fact or law. The Board was of

the view that the issue was one of fact only. This is obviously material since an appeal lies

to the Court of Appeal from the Board on the questions of law only (see the Tax Appeal

Board Act section 9). Counsel for the Appellant submitted that this view of the Board was

erroneous as the identity of the “recipient” called for a proper construction of that word as

Page 6 of 44

it appears in the VAT Act and that was a question of law. Counsel for the Respondent did

not seek to support the position of the Board and conceded that the issues on appeal would

involve questions of law. This is clearly a correct concession.

[11] Before I come to consider the submissions in more detail it would be appropriate to put the

issue in its proper statutory context.

[12] Value added tax is charged on a commercial supply within Trinidad and Tobago of goods

and prescribed services by persons registered under the VAT Act (see section 6(b)). What

constitutes a “commercial supply” for the purposes of this appeal is dealt with in section

14 (1). This section provides as follows:

“14 (1) A supply of goods or prescribed services that is made in the course of, or

furtherance of, any business is a ‘commercial supply’ for the purposes of this

Act.”

It is not in dispute that in this case that there were commercial supplies and that the

supplies were of services.

[13] Section 7(1) prescribes the rate of tax. The amount of tax shall be calculated at the rate of

15% “or such other rate as the Minister by Order specifies, except in the case of an entry or

supply that is zero-rated”. Section 8 deals with the zero-rating of a supply of goods and

services and, insofar as is relevant to this appeal, provides as follows:

“8. (2) Where services are, or the supply of services is, prescribed in Schedule 2,

the supply of those services is zero-rated for the purposes of this Act.

(3) Where the entry or supply of any goods or the supply of any services is

zero-rated, the rate at which tax is regarded as being charged shall be nil, and

consequently no tax shall be charged on the entry or supply.”

[14] From a reading of these sections it is fair to say that for value added tax to be charged there

must be a commercial supply of services within Trinidad and Tobago which is not

prescribed in Schedule 2. Here the contention by the Appellant is that the commercial

supplies were caught by Item 12 of Schedule 2. The only issue in dispute is whether it was

Page 7 of 44

made to a recipient who was not within Trinidad and Tobago at the time the services were

performed.

[15] Counsel for the Appellant submitted that the Board misdirected itself on the meaning of

the word “recipient”. “Recipient”, he submitted, is the counterparty to the transaction

undertaken by the registered person. The counterparty is (a) the person to whom the

registered person is obligated to provide the commercial supply, (b) the person to whom

the registered person is obligated to provide the tax invoice and (c) the person who is

obligated to pay to the registered person sums in settlement of the tax invoice. This

position, it was submitted, is supported by reference to the provisions of the VAT Act.

Specific reference was made to sections 17(1), 36(1) and 37. Counsel contended that it was

clear on the facts of the case that BCL was the counterparty and therefore the recipient.

[16] Counsel for the Respondent submitted to the contrary. She argued that it was clear from

the provisions of the VAT Act that the word “recipient” refers to any person who receives

goods or services. As BGTT had pipe coating services provided to its pipelines it was clear

that BGTT was the recipient within the meaning of the Act. The Respondent further

contended that it was open to the Board to find that BCL was within Trinidad and Tobago

when the commercial supplies were made.

[17] The reasoning of the Board is I think evident from the following paragraph of the case

stated:

“18.5 ...what is not in doubt is the location and beneficiary of the Recipient which

was BGTT. The ordinary principles and scheme of the VAT Act is that VAT is

charged in the place where the supply takes place or is deemed to have taken

place. The basic rule with the supply of services is that services are deemed to be

supplied where the supplier’s business is established or located. There is no doubt

in this case that the supplier is a company registered in and having its place of

business in Trinidad and Tobago. It is also not in doubt that the actual supply was

carried out in Trinidad and Tobago, nor is it in doubt that the subject matter for

the purposes of the VAT Act was owned by a Trinidad and Tobago company,

Page 8 of 44

BGTT. As such although the contract for these services was between two non-

resident companies, this is not a matter which could legitimately influence the

Court to hold the supply as a zero-rated supply under Schedule 2 Item 12, and as

such that output tax should be charged on the recipient of the supply.”

This is essentially repeated in the judgment at paragraph 14.5.

[18] The Board was therefore of the view that there were three material considerations, namely:

(1) that the supply of the services was within Trinidad and Tobago; (2) the services (i.e.

the coating services) were actually performed in Trinidad and Tobago and on pipelines

owned by BGTT, a local company; and (3) the contractual arrangements were not relevant.

[19] It is difficult to apprehend the Board’s reliance, in determining the recipient, on the place

of supply as occurring within Trinidad and Tobago. Section 6 of the VAT Act provides

that value added tax shall be charged on a commercial supply of goods or services within

Trinidad and Tobago. Item 12 is an exception to this general rule. It acknowledges that if

the exception does not apply that value added tax will be charged on a commercial supply

occurring within Trinidad and Tobago. The exception has nothing to do with the place of

supply but rather who is and the place of the recipient. Identifying the place of supply

therefore does not bring one any closer to understanding the exception or in this case

determining whether the supply was made to a recipient who was not within Trinidad and

Tobago.

[20] Similarly the fact that the services were actually performed in Trinidad and Tobago is of

no assistance to determining who is the recipient. That fact might be relevant to the place

of supply but not the identity of the recipient (see s. 16(1)(b) (ii)).

[21] The Board placed great emphasis on its finding that BGTT was the owner of the pipelines.

It was of the view that this “crucial finding of fact overshadows all the issues contended

for by the Appellant” (see para. 22 of the case stated).

Page 9 of 44

[22] There is, however, really no evidence to support the finding that BGTT was the owner of

the pipelines. The agreed facts do not identify BGTT as the owner of the pipelines and that

is not a reasonable inference that can be drawn from them. According to the agreed facts

BGTT contracted with Allseas Marine Contractors S.A. Switzerland (Allseas) (see para. 5

of the agreed facts at para. 5 of this judgment) for the provision and installation of

pipelines in Trinidad and Tobago. Allseas retained the services of BCL to provide coating

services to the pipelines which in turn subcontracted that work to the Appellant. The only

reasonable inference is that Allseas in the performance of its contract with BGTT required

the pipelines to be coated. BGTT did not contract for the supply of coated pipelines but

rather the procurement and installation of pipelines. It is not reasonable to infer that BGTT

was the owner of the pipelines before Allseas performed its contract and installed the

pipelines. There is no evidence that that had taken place and the only reasonable inference

is that it had not.

[23] In any event ownership of the pipelines is not relevant to determining who is the recipient

of the coating services. I think this can be demonstrated by a simple example. A home

owner retains the services of a contractor to paint his house. The contractor has quoted a

price for the job inclusive of labour and materials. As he is registered under the VAT Act,

he charges value added tax on that price. The contractor must purchase paint from a paint

shop to do the job. The recipient of the supply of paint by the paint shop is the contractor,

not the home owner although he is the owner of the house and in the end may be the

ultimate beneficiary of the paint; ownership of the house is not relevant.

[24] By considering the owner of the pipelines to be material, what the Board seems to have

done is considered that the ultimate consumer of the services is the recipient. But that is

not the correct approach. The fact of the matter is that before a supply of goods or services

reaches the final consumer there may be several stages at which a supply of goods or

services is made to a recipient and at which value added tax is chargeable. The principle

behind the value added tax system is that at each stage value added tax will be charged on

the value added. It is not correct to look down the road and say that the recipient of an

earlier supply is the end user. To do so will be to defeat the principle of the value added

Page 10 of 44

tax system. The question at each stage of the supply chain is who is the recipient of that

particular supply. It is evident from the provisions of the VAT Act that the answer to that

question is the person to whom the particular supply of goods or services is made. In other

words, the recipient is an immediate party to the transaction not some remote party that

may ultimately benefit from the supply.

[25] The first section of relevance is section 3. This section defines “recipient” as follows:

“recipient”, in relation to a supply of goods or services, means the person to

whom the goods or services are supplied.”

It is relevant to note that the definition uses the words “in relation to a supply”. Bearing in

mind that throughout the chain of the supply of goods or services to the end user there may

be different stages at which a supply is made, the definition refers to the recipient of a

supply at each stage.

[26] The other relevant sections are sections 17, 36 and 37.

[27] Section 17 deals with when a supply takes place. Section 17(1) is of note and provides that

a supply takes place on the occurrence of any one or three events (whichever is the earlier),

namely; (a) when an invoice for the supply is given by the supplier, or (b) when payment

is made for the supply or (c) when the goods are made available, or the services are

rendered, as the case may be, to the recipient.

[28] Although under section 17(1) a supply may take place before an invoice is given by the

supplier, section 36 requires the tax invoice to be given to the recipient. An invoice may be

provided to the recipient either to accord with section 36(2) or 36(3). Common to both

sections is that the invoice must make reference to the consideration for the supply and

must include the tax. Under 36(2) it seems that the tax must be set out separately from the

price of the supply (see 36(2)(f) and (h)) whereas under section 36(3) the invoice must set

out the consideration for the supply inclusive of tax.

Page 11 of 44

[29] Section 37 deals with credit and debit notes in respect of a commercial supply that is

cancelled, altered or returned. Section 37(2) provides as follows:

“37(2) Where this section applies, the supplier shall give to the recipient a credit

note or a debit note, as the case requires, to adjust the amount shown on the tax

invoice as being in respect of tax to the amount, if any, that would have been so

shown if -

(a) the cancellation or alteration referred to in subsection (1)(a) or (b)

had taken place before the tax invoice was given; or

(b) the goods or services returned had not been supplied, as the case

requires.”

[30] The VAT Act, therefore, requires that an invoice be provided to the recipient. The

recipient under the VAT Act is the person to whom the supply of goods or services is

made. As the invoice is provided to the recipient he also is the one liable for the

consideration and the tax in respect of the supply. This is also a clear inference from

section 37(2) which provides that credit and debit notes shall be given to the recipient

where a supply is altered, cancelled or returned. If the recipient was not also liable for the

tax but was in receipt of a credit or debit note the situation might arise where although

there is no liability on the part of the recipient to pay the tax on the supply, he might be

obligated either to increase his liability to tax or be entitled to reduce his liability to tax.

[31] In my judgment when the sections are read together they point to the conclusion that the

recipient is an immediate party to the transaction in respect of the supply. He is the person

to whom the supply is made and is liable for the consideration for the supply and the tax.

He is certainly not some remote person who between himself and the supplier has no

liability for the consideration or the tax but at some point down the chain of supply may

derive a benefit from a supply made higher up the chain.

[32] The Board found as a fact that the supply was made to a party which was a foreign entity

(see para. 15.8 of the case stated). That is so and that foreign entity is BCL. There is no

disputing that BCL was the entity to which contractually the services were to be supplied,

Page 12 of 44

was contractually liable for the consideration for the supplies, including the tax if

chargeable, and the one to whom the invoice should have been sent and was indeed sent. It

should follow from that, that the recipient is BCL. The Board, however, thought it could

ignore the contractual arrangements between the Appellant and BCL, and between the

latter and Allseas and between Allseas and BGTT and somehow reconstruct the

contractual arrangements to regard them as one between the Appellant and BGTT. This is

evident from paragraph 18.5 of the case stated, which was quoted earlier in this judgment,

and also from paragraph 16. (2) where the Board stated:

“We also hold that in applying the provisions of the VAT Act there is no room to

permit any concession to the supplier of services for substituting a contractual

recipient for the bona fide presence of the owner of the pipelines during the time

of the particular VAT periods.”

[33] Counsel for the Respondent submitted that the Board was entitled to do just that. She

submitted that the Board was entitled to disregard those contracts that had no commercial

purpose and to look at the end result. The Board was in the circumstances entitled to

disregard the arrangements between BGTT and Allseas, between Allseas and BCL and

between BCL and the Appellant. When those arrangements are disregarded the reality is a

supply of the coating services by the Appellant to BGTT. The Board in adopting this

approach, it was submitted, was making the distinction between tax avoidance and tax

evasion and implementing the principles laid down in the case of W.T Ramsay Limited v

IRC [1982] AC 300.

[34] In the Ramsay case the taxpayer sought to create an allowable loss to offset a gain that

was chargeable to tax. It sought to create the loss without in fact suffering any and it did so

by entering into a series of transactions whereby both losses and matching gains were

created. The House of Lords held that the Court was not bound to consider individual steps

in a series of transactions, where the steps were so closely associated with each other as to

form a single composite arrangement. The Court was therefore entitled to have regard to

the effect of the transactions as a whole and was not bound to have regard to individual

components of the arrangements. Lord Wilberforce in his judgment said (at pp 323-324):

Page 13 of 44

“1. A subject is only to be taxed upon clear words, not upon

‘intendment’ or upon the ‘equity’ of an Act. Any taxing Act of Parliament is

to be construed in accordance with this principle. What are ‘clear words’ is

to be ascertained upon normal principles: these do not confine the courts to

literal interpretation. There may indeed should, be considered the context

and scheme of the relevant Act as a whole, and its purpose may, indeed

should, be regarded: ....

2. A subject is entitled to arrange his affairs so as to reduce his liability to

tax. The fact that the motive for a transaction may be to avoid tax does not

invalidate it unless a particular enactment so provides. It must be

considered according to its legal affect.

3. It is for the fact-finding commissioners to find whether a document, or a

transaction, is genuine or a sham. In this context to say that a document or

transaction is a “sham” means that while professing to be one thing, it is in

fact something different. To say that a document or transaction is genuine,

means that, in law, it is what it professes to be, and it does not mean

anything more than that. I shall return to this point.

Each of these three principles would be fully respected by the decision we are

invited to make. Something more must be said as to the next principle.

4. Given that a document or transaction is genuine, the court cannot go

behind it to some supposed underlying substance. This is the well-known

principle of Inland Revenue Commissioner v. Duke of Westminster [1936]

A.C. 1. This is a cardinal principle but it must not be overstated or

overextended. While obliging the court to accept documents or transactions,

found to be genuine, as such, it does not compel the court to look at a

document or a transaction in blinkers, isolated from any context to which it

properly belongs. If it can be seen that a document or transaction was

Page 14 of 44

intended to have effect as part of a nexus or series of transactions, or as an

ingredient of a wider transaction intended as a whole, there is nothing in

the doctrine to prevent it being so regarded: to do so is not to prefer form to

substance, or substance to form. It is the task of the court to ascertain the

legal nature of any transaction to which it is sought to attach a tax or a tax

consequence and if that emerges from a series or combination of

transactions, intended to operate as such, it is that series or combination

which may be regarded.....

For the commissioners considering a particular case it is wrong, and an

unnecessary self limitation, to regard themselves as precluded by their own

finding that documents or transactions are not ‘shams,’ from considering what, as

evidenced by the documents themselves or by the manifested intentions of the

parties, the relevant transaction is....”

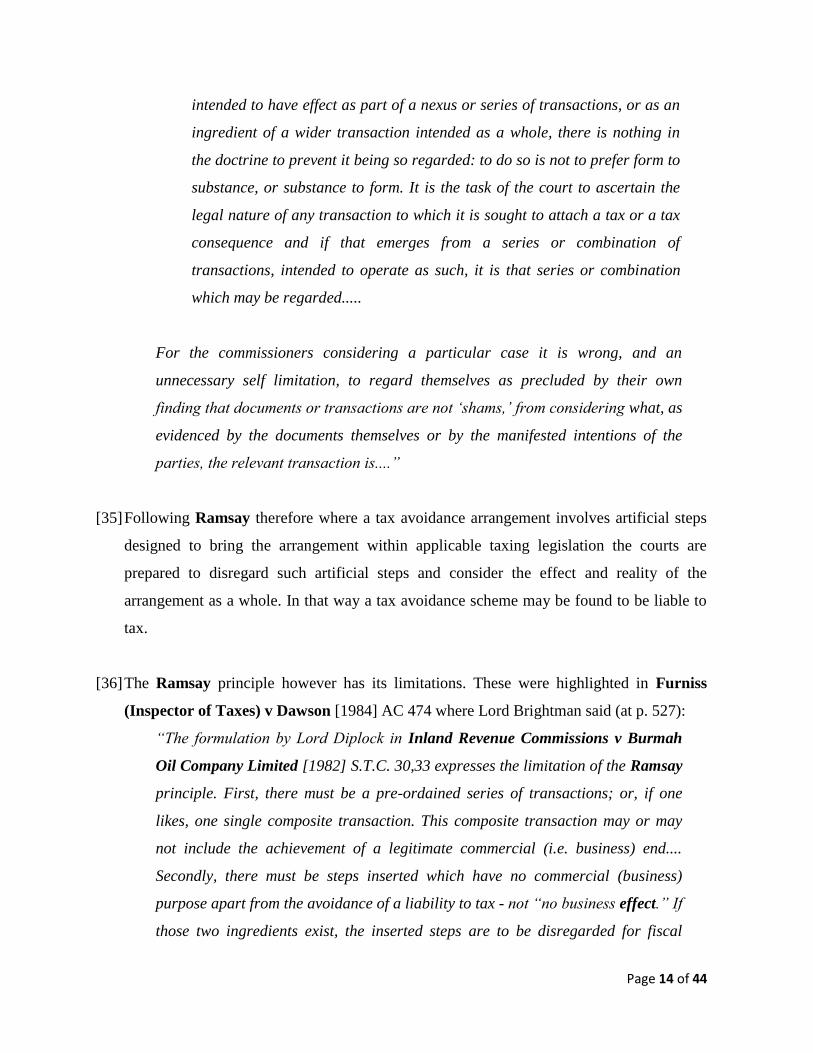

[35] Following Ramsay therefore where a tax avoidance arrangement involves artificial steps

designed to bring the arrangement within applicable taxing legislation the courts are

prepared to disregard such artificial steps and consider the effect and reality of the

arrangement as a whole. In that way a tax avoidance scheme may be found to be liable to

tax.

[36] The Ramsay principle however has its limitations. These were highlighted in Furniss

(Inspector of Taxes) v Dawson [1984] AC 474 where Lord Brightman said (at p. 527):

“The formulation by Lord Diplock in Inland Revenue Commissions v Burmah

Oil Company Limited [1982] S.T.C. 30,33 expresses the limitation of the Ramsay

principle. First, there must be a pre-ordained series of transactions; or, if one

likes, one single composite transaction. This composite transaction may or may

not include the achievement of a legitimate commercial (i.e. business) end....

Secondly, there must be steps inserted which have no commercial (business)

purpose apart from the avoidance of a liability to tax - not “no business effect.” If

those two ingredients exist, the inserted steps are to be disregarded for fiscal

Page 15 of 44

purposes. The court must then look at the end result. Precisely how the end result

will be taxed will depend on the terms of the taxing statute sought to be applied...

The formulation, therefore, involves two findings of fact, first whether there was a

preordained series of transactions, i.e., the single composite transaction,

secondly, whether that transaction contained steps which were inserted without

any commercial or business purpose apart from a tax advantage. Those are facts

to be found by the commissioners. They may be primary facts or, more probably,

inferences to be drawn from primary facts. If there are inferences, there are

nevertheless facts to be found by the commissioners.

[37] The application of the Ramsay principle is therefore one that is dependent on the finding

of certain facts. There must be the finding of the facts as outlined by Lord Brightman. The

Board in this matter did not make such findings of fact. Moreover, there was no basis on

which the Board could have found such facts on the evidence that there was before it.

Indeed it would have been unfair and prejudicial for the Board to have so decided as there

were no issues before it that the arrangements between the various parties constituted a

single composite transaction and that steps had been inserted which had no commercial or

business purpose apart from the avoidance of a liability to tax. Similarly it is unfair and

prejudicial for these issues to be raised before this Court even if there were some basis on

which the Board could have come to those findings of fact. In the circumstances it was

wrong for the Board to disregard the contractual arrangements between the parties.

[38] In the circumstances the question regarding the recipient does not lend itself to any doubt

in this case. BCL contracted with its subsidiary to provide the coating services. There was

a supply by the Appellant to BCL, its parent company, which was liable as between itself

and its subsidiary for the payment of the consideration and the value added tax, if

chargeable. There is nothing sinister in a company subcontracting works to another

company, even its subsidiary. For the purposes of Item 12 therefore the recipient is BCL.

[39] This leaves the question whether the recipient was within Trinidad and Tobago at the time

when the services were performed. I do not think that “performed” in Item 12 carries a

Page 16 of 44

different meaning to “supplied”. So the question therefore is whether the recipient was

within Trinidad and Tobago at the time when the services were supplied.

[40] Item 12 was not always worded in its present form. The provision was amended in 1989

and had formerly read:

“Any services which are supplied for a consideration that is payable in a

currency other than that of Trinidad and Tobago, to a recipient who is neither a

resident of Trinidad and Tobago nor within Trinidad and Tobago at the time

when the services are performed.“

The amendment therefore removed any requirement for the recipient to be a non-resident

of Trinidad and Tobago.

[41] The literal meaning of “within” is “inside the range of an (area or boundary)” (see Oxford

Dictionary of English (2nd

ed.)). I do not think that the word is used to convey any

meaning other than its natural meaning in Item 12 and simply means that the recipient

must be in Trinidad and Tobago. A company having a registered office, place of business

or agent in Trinidad and Tobago would be within Trinidad and Tobago for the purposes of

Item 12.

[42] According to the agreed statement of facts, BCL was not registered in Trinidad and

Tobago, nor resident and had no branch in Trinidad and Tobago. The Board, however,

found that BCL must be regarded as having a constructive presence having regard to its

connection with the Appellant. It is not correct, in my judgment, to infer or imply that BCL

is present in Trinidad and Tobago simply because the Appellant is its subsidiary. A

subsidiary is separate and distinct from its parent company. Moreover, a company has a

legal identity separate and apart from its shareholders. The presence of the subsidiary in

Trinidad and Tobago cannot be regarded as the presence of its shareholders and

accordingly that of BCL.

Page 17 of 44

[43] It was submitted by the Respondent that the construction of Item 12 should be influenced

by section 16(1)(b)(ii). This section is as follows:

“16. (1) For the purposes of this Act, the supply of goods and services shall,

subject to subsections (3) and (4), be regarded as taking place within Trinidad

and Tobago if-

(b) the supplier is not resident in Trinidad and Tobago but-

(ii) in the case of a supply of services, the services are physically

performed in Trinidad and Tobago by a person who is in Trinidad and

Tobago at the time the services are performed.”

[44] As far as I understand the submission it was to the effect that insofar as the section treats

the supply of services as taking place within Trinidad and Tobago where it is physically

performed in Trinidad and Tobago by a person who is in Trinidad and Tobago so too in

such cases the recipient should be regarded as within Trinidad and Tobago.

[45] I however see no merit in that submission. Section 16 is relevant to determining the place

of the supply not the recipient. It has no bearing on that question. Further, if the contention

of the Appellant is correct that the place of supply is relevant to determining the meaning

of recipient within Item 12, it would mean that since value added tax is chargeable on a

commercial supply within Trinidad and Tobago, in every case the recipient would be

regarded as within Trinidad and Tobago. The result would be that Item 12 would never be

applicable. This would produce an absurd result and could not have been intended by the

draftsman.

[46] In my judgment the evidence does not establish that BCL was within Trinidad and Tobago.

On the agreed facts the appropriate inference is that it was not within Trinidad and Tobago

at the time of the supply of the services. As Mohammed, J.A has pointed out, the position

might have been different if there were provisions in our VAT Act similar to sections 9

and 43 of the 1994 VAT Act of the United Kingdom.

Page 18 of 44

[47] In the circumstances the commercial supplies in this matter fell within Item 12 of Schedule

2. There were supplies of services for a consideration payable in a foreign currency to a

recipient not within Trinidad and Tobago at the time when the services were performed.

The supplies were therefore zero-rated and consequently no value added tax was

chargeable on them.

A. Mendonça,

Justice of Appeal

Delivered by Mohammed J.A.

[48] This appeal was made by way of case stated pursuant to Part 61 of the Civil Proceedings

Rules 1998 (the CPR) and sections 9 and 10 of the Tax Appeal Board Act1. The decision

under review is that of the Tax Appeal Board (the Appeal Board) dated July 21st 2001,

whereby the respondent’s (the Board of Inland Revenue [the BIR]) assessment of the

appellant’s (Bauhuis Coating International Limited [BCIL]) Value Added Tax (VAT)

liability for the tax periods 200106, 200108, 200110 and 200112 was upheld.

[49] The BIR’s assessment was based primarily on the interpretation given to the word

“recipient” as contained in the Value Added Tax Act (the Act).2 The Appeal Board upheld

the BIR’s interpretation of the word “recipient” and concluded that a recipient, in relation

to the Act, was a third party to whom a service was provided and not a parent company in

a situation where it created, and contracted with, a subsidiary to provide services to that

third party. The Appeal Board rejected BCIL’s arguments and concluded that the various

contractual relationships it entered into amounted to a “mask”, established simply to derive

financial benefits under the Act. It further concluded that BCIL’s parent company could

not be the recipient of services and had a constructive presence in Trinidad and Tobago by

virtue of its subsidiary, BCIL.

1 Chap. 4:50.

2 Chap. 75:06.

Page 19 of 44

[50] I am of the view that the BIR, and subsequently the Appeal Board, erred in their

interpretation of the Act as to the meaning of the term “recipient”. A finding that the term

“recipient”, in relation to the Act, encompassed a third party ultimate recipient ignored the

plain wording of the Act as well as the commercial reality of business transactions.

Accordingly, the commercial supplies provided by BCIL were properly zero rated as it

was supplied for a consideration that was payable in a currency other than that of Trinidad

and Tobago, to a recipient who was not within Trinidad and Tobago at the time when the

services were performed. The recipient was not within Trinidad and Tobago as merely

having a subsidiary within a jurisdiction does not, without more, amount to a constructive

presence of the parent company in that jurisdiction.

[51] The interpretation of the Act is purely a question of law and accordingly, this court has the

jurisdiction to review the Appeal Board’s ruling. The case stated will be amended and the

Appeal Board’s decision is hereby reversed.

Facts

[52] An agreed statement of facts was filed before the Appeal Board on December 16th

, 2003.3

BCIL was duly registered under the laws of Trinidad and Tobago4 and at all material times

provided pipe coating services, under a subcontract, to a non-resident company, Bauhuis

Coating Limited (BCL).

[53] BCIL coated pipelines for the ultimate benefit of British Gas Trinidad and Tobago Limited

(BGTT). BGTT contracted with Allseas Marine Contractors S.A. Switzerland (Allseas) for

the procurement and installation of certain pipelines in Trinidad and Tobago. Allseas then

contracted with BCL, a Cyprus based company, to coat these pipes. BCL subcontracted the

actual coating of the pipelines to BCIL, a wholly owned subsidiary of BCL. BCIL

performed these services locally and issued invoices to BCL, payable in U.S. Dollars.

3 See pgs 9-10 of the case stated by the Appeal Board.

4 See The Companies Act Chap. 81:01; section 20 of the Value Added Tax Act Chap. 75:06.

Page 20 of 44

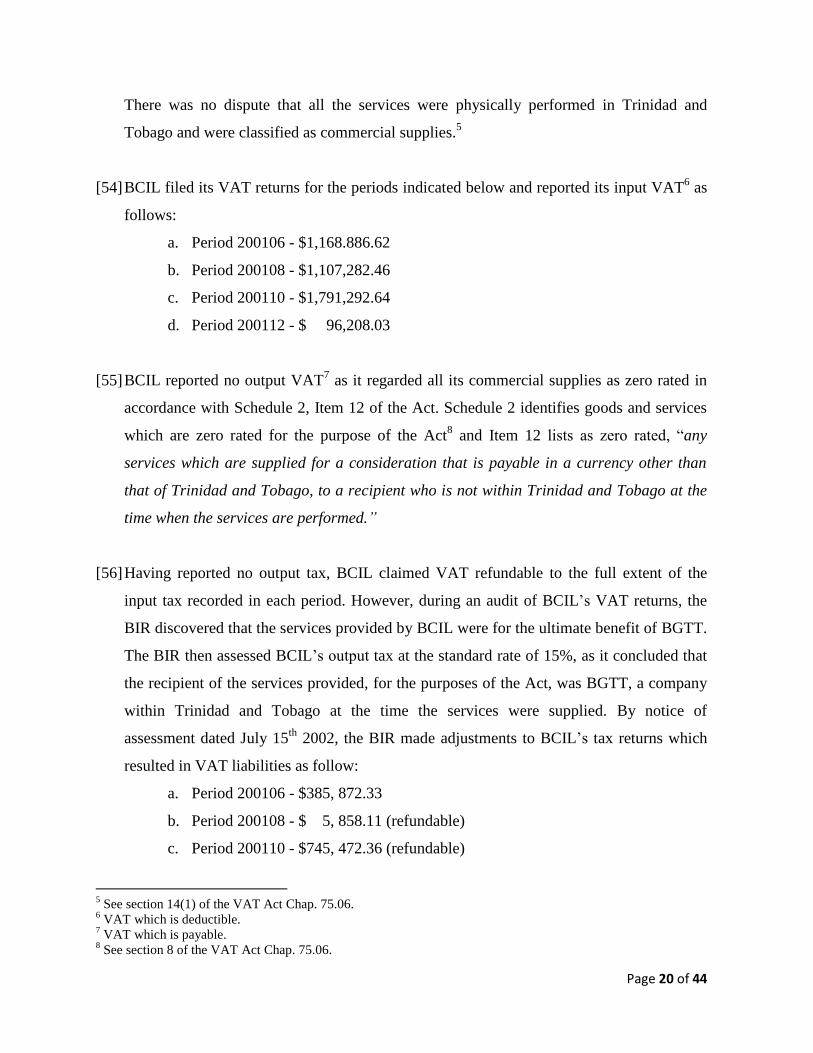

There was no dispute that all the services were physically performed in Trinidad and

Tobago and were classified as commercial supplies.5

[54] BCIL filed its VAT returns for the periods indicated below and reported its input VAT6 as

follows:

a. Period 200106 - $1,168.886.62

b. Period 200108 - $1,107,282.46

c. Period 200110 - $1,791,292.64

d. Period 200112 - $ 96,208.03

[55] BCIL reported no output VAT7 as it regarded all its commercial supplies as zero rated in

accordance with Schedule 2, Item 12 of the Act. Schedule 2 identifies goods and services

which are zero rated for the purpose of the Act8 and Item 12 lists as zero rated, “any

services which are supplied for a consideration that is payable in a currency other than

that of Trinidad and Tobago, to a recipient who is not within Trinidad and Tobago at the

time when the services are performed.”

[56] Having reported no output tax, BCIL claimed VAT refundable to the full extent of the

input tax recorded in each period. However, during an audit of BCIL’s VAT returns, the

BIR discovered that the services provided by BCIL were for the ultimate benefit of BGTT.

The BIR then assessed BCIL’s output tax at the standard rate of 15%, as it concluded that

the recipient of the services provided, for the purposes of the Act, was BGTT, a company

within Trinidad and Tobago at the time the services were supplied. By notice of

assessment dated July 15th

2002, the BIR made adjustments to BCIL’s tax returns which

resulted in VAT liabilities as follow:

a. Period 200106 - $385, 872.33

b. Period 200108 - $ 5, 858.11 (refundable)

c. Period 200110 - $745, 472.36 (refundable)

5 See section 14(1) of the VAT Act Chap. 75.06.

6 VAT which is deductible.

7 VAT which is payable.

8 See section 8 of the VAT Act Chap. 75.06.

Page 21 of 44

d. Period 200112 - $212,081.26

[57] BCIL appealed each assessment and by order dated June 30th

2003, the four appeals were

consolidated and heard together as all appeals raised one central issue – whether the

supplies made by BCIL were zero rated under the Act.9

The Tax Appeal

[58] The relevant sections of the Act which were set out before the Appeal Board in an attempt

to resolve the issue were as follows:

Section 3(1):

“recipient” in relation to a supply of goods or services, means the person to whom

the goods or services are supplied;

“supplier” in relation to a supply of goods or services, means the person by whom

the goods or services are supplied;

“tax invoice” means a tax invoice given under section 36.

Section 4:

(1) In this Act “business” includes any trade, profession or vocation.

(2) For the purposes of this Act—

(a) an activity that is carried on, whether or not for pecuniary profit, and

involves or is intended to involve, in whole or in part, the supply of goods or

services for consideration;

(b) the activities of a club, association or organisation, other than a trade

union registered under the Trade Unions Act, in providing, for a

subscription or other consideration, facilities or advantages to its members;

or (c) an activity involving the admission, for a consideration, of persons to

any premises.

9 See pg 5 of the case stated by the Tax Appeal Board.

Page 22 of 44

Section 14:

(1) A supply of goods or prescribed services that is made in the course of, or

furtherance of, any business is a “commercial supply” for the purposes of this Act.

Section 16:

(1) For the purposes of this Act, the supply of goods and services shall, subject to

subsections (3) and (4), be regarded as taking place within Trinidad and Tobago

if—

(a) the supplier is resident in Trinidad and Tobago; or

(b) the supplier is not resident in Trinidad and Tobago but—

(i) in the case of a supply of goods, the goods supplied are in

Trinidad and Tobago at the time of the supply; or

(ii) in the case of a supply of services, the services are physically

performed in Trinidad and Tobago by a person who is in Trinidad

and Tobago at the time the services are performed.

(2) For the purposes of this Act, the supply of goods or services shall, subject to

subsections (1)(b) and (5), be regarded as not taking place within Trinidad and

Tobago if the supplier is not resident in Trinidad and Tobago.

Section 17:

(1) Except as otherwise provided in this section, a supply of goods or services takes

place, for the purposes of this Act, when—

(a) an invoice for the supply is given by the supplier;

(b) payment is made for the supply; or

(c) the goods are made available, or the services are rendered, as the case

may be, to the recipient,

whichever is the earlier.

Section 36:

(1) Subject to subsection (3A), a registered person making a commercial supply

exceeding the sum of twenty dollars on or after the appointed day shall, at the time

when the supply takes place, give the recipient a tax invoice, in accordance with

Page 23 of 44

subsection (3), in respect of the supply or, if he is requested by the recipient to do

so, a tax invoice in accordance with subsection (2).

……..

(3A) A registered person carrying on a business listed in Schedule 3A may make a

commercial supply without issuing a tax invoice but such person shall, if requested

by the recipient to do so, give a tax invoice in accordance with subsection (2).

Section 37:

(1) This section applies where a registered person has given a tax invoice in

respect of a commercial supply and thereafter—

(a) the supply is cancelled;

(b) the consideration for the supply is altered, whether due to a discount or

otherwise; or

(c) the goods or services, or any part of the goods or services supplied, are

returned to the supplier.

(2) Where this section applies, the supplier shall give to the recipient a credit note

or a debit note, as the case requires, to adjust the amount shown on the tax invoice

as being in respect of tax to the amount, if any, that would have been so shown if—

(a) the cancellation or alteration referred to in subsection (1)(a) or (b) had

taken place before the tax invoice was given; or

(b) the goods or services returned had not been supplied,

as the case requires.

(3) A credit note or debit note required by subsection (2) to be given shall

include—

(a) the words “credit note” or “debit note”, as the case requires, shown

conspicuously thereon;

(b) the name, address and registration number of the supplier;

(c) the name and address of the recipient;

(d) the date on which the credit note or debit note, as the case requires, is

given;

(e) the identifying number of the tax invoice to which it relates and the date

on which it was given;

Page 24 of 44

(f) the amount shown on the tax invoice as being in respect of tax, the

adjusted amount, and the amount of the credit or debit, as the case requires,

that is necessary to make the adjustment; and

(g) a brief explanation of the circumstances giving rise to the note being

given.

Schedule 2, Item 12 as outlined at paragraph 55 above.

[59] BCIL submitted that the sole question was, who was the recipient of services in the context

of the provisions of the Act. It contended that the issue should be resolved with guidance

from other provisions of the Act and argued that section 17 identified that the two pertinent

parties to a transaction were the supplier and the recipient. Further, BCIL submitted that

section 36 of the Act outlined that the supplier and recipient were the two parties to the tax

invoice and the recipient was the person from whom VAT was claimed. Taking that into

account, it was submitted that the commercial supplies made by BCIL were zero rated

because they were supplied, for a consideration that was payable in U.S. dollars, to the

recipient, BCL, which was not within Trinidad and Tobago at the time when the services

were performed.

[60] The BIR defended its assessment with assistance from the definition of the term

“recipient” as outlined by section 3(1) of the Act. According to the BIR, the identity of the

recipient was simply and readily identifiable. The BIR contended that BCIL coated

pipelines belonging to BGTT and as such BGTT was the recipient of the services provided

by BCIL services. Further, matters of privity of contract and the issuing of tax invoices

were not relevant when determining the identity of the recipient as the imposition of

several contracts might well obscure the true picture. It was further contended that even if

BCIL’s arguments were accepted, on an altogether separate limb, the commercial supplies

were still not zero rated as the test of presence in Trinidad and Tobago was gleaned from

whether or not the company was involved in commercial activity in Trinidad and Tobago

in accordance with section 16 (1)(b) of the Act. The BIR submitted that for the purposes of

the Act, BCL must be considered to be within Trinidad and Tobago since it made supplies

in Trinidad and Tobago.

Page 25 of 44

[61] In response to the BIR, BCIL submitted that the Act must be construed as a whole and the

use of the word “recipient” throughout the Act must be consistent with the meaning set out

in the definition at section 3(1). Sections 17, 36 and 37 identifies the recipient as the

second party to the contract, which is the person named on the invoice, and this informs

and substantiates the meaning to be given to the word “recipient” in Item 12 of Schedule 2.

In addition, the absence of a contractual relationship between BCIL and BGTT precluded

BGTT from being the recipient under the Act. Any suggestion to the contrary was an

attempt to impermissibly enlarge the restricted meaning of the term “recipient”, there

being nothing to suggest that the meaning of the term in Item 12 of Schedule 2 had

suddenly varied from its meaning throughout the Act. Further, BCIL reasoned that a

finding that the services were supplied in Trinidad and Tobago could not by itself deem

BCL to be within Trinidad and Tobago for the purposes of the Act. BCIL contended that

such a conclusion required a specific deeming provision in the Act to facilitate it, since it

ignored the realities of the world of commerce and contract.

The decision of the Tax Appeal Board

[62] The consolidated appeals were dismissed on July 27th

2005. However, due to technical

difficulties the written judgment was delivered July 21st, 2011.

The submissions of both

parties were considered and the Tax Appeal Board stated:

“13.4 …… We agree fully with the Respondent on the identity of the recipient. It

has been clearly established at this trial that it was British Gas Trinidad and

Tobago Ltd. which requested BCL the parent company to provide it with these

goods and services. It would be a contradiction in terms to regard BCL, the

company responsible for forming its subsidiary, that is BCIL, as the recipient of

these goods and services.

13.5 We do not accept the contentions of the Appellant that various contractual

relationships can supplant the legal status of the recipient of the services from the

Appellant. Further, the Appellant should not be allowed to mask that very

Page 26 of 44

important fact as it relates to the Value Added Tax Act in order to derive financial

benefits under the said VAT Act.

….

14.5……..The basic rule with the supply of services is that services are deemed to

be supplied where the supplier’s business is established or located. There is no

doubt in this case that the supplier is a company registered in and having its

place of business in Trinidad and Tobago. It is also not in doubt that the actual

supply was carried out in Trinidad and Tobago, nor is it in doubt that the subject

matter for the purposes of the VAT Act was owned by a Trinidad and Tobago

company, BGTT. As such, although the contract for the services was between two

non-resident companies, this is not a matter which could legitimately influence

the Court to hold that the supply is a zero rated supply under Schedule 2 Item 12,

and as such that output tax should not be charged in the recipient of the supply.

….

16.2 ……the Appellant has not satisfied the legal onus of proof which was placed

on it, and has not discharged the onus of providing that in each appeal the

assessment by the Respondent, the Board of Inland Revenue is excessive or

wrong.”10

[63] The Appeal Board also found, as a fact, that BCL must be regarded as having a

constructive presence within Trinidad and Tobago, having regard to its connection with

BCIL.11

[64] By letter dated August 12th

2005, BCIL requested that the Appeal Board state and sign a

case for the court of appeal as BCIL was dissatisfied with the decision of the Appeal Board

as being erroneous in point of law. The Appeal Board contended, by way of case stated,

that there was no question of law submitted for the opinion of the court of appeal as the

10

See Bauhuis Coating International Limited v The Board of Inland Revenue Tax Appeal Nos. V12-V15 of

2003 at pgs 26-28. 11

See pg 34 of the case stated by the Tax Appeal Board.

Page 27 of 44

matter turned on one of fact only. That was, that the recipient of the supplies from the

appellant was BGTT with respect to all four appeals.12

Submissions of the appellant on this appeal

[65] BCIL sought the following reliefs:

1. That the court of appeal amend the Appeal Board’s case stated by deleting

paragraph 31 and inserting “The points of law for consideration by, and the opinion

of, the court of appeal are:

i. Whether the Tax Appeal Board was correct in its statutory construction

and/or interpretation of the word “recipient” as defined by section 3(1) of

the Value Added Tax Act (“VAT Act”) for the purposes of the VAT Act;

and

ii. Whether the Tax Appeal Board was correct in its application of the VAT

Act as it so construed and interpreted to the facts as agreed between the

appellant and respondent by the Agreed Statement of Facts filed in the tax

appeals on 16th

December 2003.”

2. That the court of appeal reverses the determination of the Tax Appeal Board;

3. That the Respondent pay the appellant the costs of this appeal; and

4. Any further relief as the court deems just.

[66] In support of the reliefs requested, BCIL noted the Appeal Board’s statement that the sole

question which arose for determination was “who in the context of the provisions of the Vat

Act was the recipient of the services from the Appellant?”13

According to BCIL, the

resolution of this issue required the statutory interpretation and construction of the word

“recipient” and the interpretation of a term used in a statutory provision was a question of

law.14

Therefore the Appeal Board’s purported finding of fact, that BGTT was the

recipient, was not in substance a finding of fact but rather was based on a determination of

a point of law and thus subject to review by the court of appeal.

12

ibid at paragraph 31. 13

ibid at paragraph 13.1. 14

See Adam v Newham London Borough Council [2001] EWCA Civ 916.

Page 28 of 44

[67] BCIL further submitted that the Appeal Board erred in its construction of the word

“recipient” as it failed to consider the meaning of the word “recipient” in its full and true

context within the four corners of the VAT Act.15

In construing the section, the Appeal

Board was entitled to look at other sections of the Act for guidance and an analysis of

other sections in the Act, as was contended in BCIL’s submissions at the tax appeal,

clearly illustrated that, for the purposes of the Act, the parties to the tax invoice must be

the supplier and the recipient.

[68] BCIL also submitted that the decision of the Appeal Board was perverse in that no

reasonable tribunal could have arrived at such a decision, that for the purposes of the Act,

a recipient of commercial supplies could be a third party entity (BGTT). By parity of the

reasoning of the Appeal Board, Allseas was also the beneficiary of commercial supplies

(to whom services were rendered by BCL in fulfillment of its contract) and so it could be

argued that Allseas should be considered a recipient under the Act. BCIL contended that

the Appeal Board’s conclusion left room for uncertainty as to who the recipient would be

for the purposes of the Act.

Submissions of the respondent on this appeal

[69] The BIR contended that the question of who is a recipient must at least be a mixed

question of law and fact. However, it submitted that if a literal interpretation was applied,

the recipient would be the entity ultimately receiving the services, that being BGTT. It was

argued that limiting the meaning to a person to whom an invoice was sent made a mockery

of the legislative intent of taxing legislation.

[70] Further, a company need not be registered in nor resident in Trinidad and Tobago for the

purpose of Item 12 and since there was no agreement on whether or not BCL was within,

or not within, Trinidad and Tobago when the commercial supply was made, the Appeal

Board was entitled to make that finding of fact, if that finding was necessary for the

determination of the appeals. In support of this contention the wording of the current Item

15

See Reynolds v Income Tax Commissioner 7 WIR 154 at pages 156-157 per Wooding CJ.

Page 29 of 44

12 of Schedule 2 was distinguished from that used in the previous Item 12 of Schedule 2,

amended December 22nd

1989. Item 12 now reads:

“Any services which are supplied for a consideration that is payable in a

currency other than that of Trinidad and Tobago, to a recipient who is not within

Trinidad and Tobago at the time when the services are performed.”

[71] Item 12 formerly read:

“…..to a recipient who is neither a resident of Trinidad and Tobago nor within

Trinidad and Tobago at the time when the services are performed.”

[72] The BIR submitted that in amending the Act, the legislature must have intended that there

was no requirement for the recipient to be a non-resident. Even if the supplier was not a

resident, it may be deemed to be within the country for the purposes of the Act.

[73] In response to BCIL’s argument that the decision of the Appeal Board was perverse, the

BIR contended that it was entirely appropriate for the Appeal Board to consider the other

contracts for the purpose of determining the nature of the transactions and the bona fides of

the tax invoice. By taking into account the other contracts and arrangements, the Appeal

Board was making the distinction between tax avoidance and tax evasion by analyzing a

series of connected transactions as a whole with emphasis being given to the end result.16

What were considered self cancelling transactions were disregarded, as was the

recommended approach for interpreting taxing statutes.17

[74] Taken as a whole, it was contended that BCIL failed to show that the Appeal Board erred

on a point of law and so the appeal should be dismissed.

Appellant’s reply to the submissions of the respondent

[75] BCIL objected to the BIR’s response on the basis that it introduced, for the first time, the

issue of whether BCIL’s actions constituted tax avoidance or tax evasion. Accordingly, it

16

See W.T. Ramsay Ltd v IRC [1982] AC 300. 17

See Statuory Interpretation 4th

Edn F A R Bennion at section 32.

Page 30 of 44

was inappropriate at this stage for the court to consider that argument. The argument was

also challenged as being inappropriate given the legislative framework of the Act. It was

contended that unlike other taxing legislation, there was no express provision in the Act

which requires the BIR to consider whether any transactions constituted a tax avoidance or

tax evasion scheme.18

Rather than applying what has become known as the “Ramsay

approach” reflexively, the court ought to be mindful of the reasoning in McNiven (H.M.

Inspector of Taxes) v Westmoreland Investments Limited 3 ITLR 342, which cautioned

against the over-literal application of the Ramsay approach in an area of the law which was

not appropriate for absolutes and which also recognized the paramount importance of the

interpretation of the particular statutory context and its application to the relevant facts.

Issues

[76] The three main issues raised on in this appeal are:

1. Whether the tax appeal was determinable on a question of fact or one of law? If it is

found that the question was one of a point of law, then this court was permitted to

delve further and to consider the second and third issues.

2. What is the interpretation to be given to the word “recipient” in relation to the Act?

3. Whether BCL was ‘within’ Trinidad and Tobago for the purposes of the Act?

1. Question of law or fact?

[77] Section 9 of the Tax Appeal Board Act19

provides:

“the court of appeal shall hear and determine any question or questions of law

arising on the case and shall reverse, affirm or amend the determination in

respect of which the case has been stated or shall remit the matter to the appeal

board with the opinion of the court thereon or make such other order in relation

to the matters as to the court may seem fit.”

18

See section 67(1) of the Income Tax Act Chap. 75:01; the Corporation Tax Act Chap. 75:02. 19

ibid (n. 1).

Page 31 of 44

[78] The BIR has not, on this appeal, taken any issue that, at its highest, the point involved is a

mixed question of fact and law. The only issue involved is one of statutory construction,

and thus, a question of law.

2. What is the interpretation to be given to the word “recipient”?

The Law

[79] In W.T. Ramsay Ltd v IRC [1982] AC 300, Lord Wilberforce said at page 323:

“While the techniques of tax avoidance progress and are technically improved,

the courts are not obliged to stand still. Such immobility must result either in loss

of tax, to the prejudice of other taxpayers, or to Parliamentary congestion or

(most likely) to both. To force the courts to adopt, in relation to closely integrated

situations, a step by step, dissecting, approach….would be a denial rather than an

affirmation of the true judicial process.”

[80] In the case of McNiven v Westmoreland, Gibson L.J. summarized the principles

developed from the Ramsay case at pages 350-352:

“First, when it is sought to attach a tax consequence to a transaction, the task of

the courts is to ascertain the legal nature of the transaction. If that emerges from

a series or combination of transactions, intended to operate as such, it is that

series or combination which may be regarded. Courts are entitled to look at a

prearranged tax avoidance scheme as a whole. It matters not whether the parties’

intention to proceed with a scheme through all its stages takes the form of a

contractual obligation or is expressed only as an expectation without contractual

force.

Second, this is not to treat a transaction, or any step in a transaction, as though it

were a ‘sham’, meaning thereby, that it was intended to give the appearance of

having a legal effect different from the actual legal effect intended by the parties

(see the classic definition of Diplock LJ in Snook v London and West Riding

Investments Ltd [1967] 2 QB 786 at 802). Nor is this to go behind a transaction

Page 32 of 44

for some supposed underlying substance. What this does is to enable the court to

look at a document or transaction in the context to which it properly belongs.

Third, having identified the legal nature of the transaction, the courts must then

relate this to the language of the statute. For instance, if the scheme has the

apparently magical result of creating a loss without the taxpayer suffering any

financial detriment, is this artificial loss a loss within the meaning of the relevant

statutory provision? Thus, in W T Ramsay Ltd v IRC [1981] STC 174, [1982] AC

300 the taxpayer company sought to create an allowable loss to offset against a

chargeable gain it had made on a sale-leaseback transaction. It sought to do so

without suffering any financial detriment, by embarking on and carrying through

a scheme which created both a loss which was allowable for tax purposes and a

matching gain which was not chargeable. In rejecting the efficacy of this

contrived ‘loss-creating’ scheme, Lord Wilberforce observed that a loss which

comes and goes as part of a preplanned, single continuous operation ‘is not such

a loss (or gain) as the legislation is dealing with’….

The Ramsay principle or, as I prefer to say, the Ramsay approach to ascertaining

the legal nature of transactions and to interpreting taxing statutes, has been the

subject of observations in several later decisions. These observations should be

read in the context of the particular statutory provisions and sets of facts under

consideration. In particular, they cannot be understood as laying down factual

prerequisites which must exist before the court may apply the

purposive Ramsay approach to the interpretation of a taxing statute. That would

be to misunderstand the nature of the decision in Ramsay. Failure to recognise

this can all too easily lead into error. In particular, the much-quoted observation

of Lord Brightman in Furniss (Inspector of Taxes) v Dawson [1984] STC 153 at

166, [1984] AC 474 at 527 seems to have suffered in this way. Lord Brightman

described, as the "limitations of the Ramsay principle", that there must be a

preordained series of transactions, or a single composite transaction, containing

steps inserted which have no business purpose apart from the avoidance of a

Page 33 of 44

liability to tax. Where those two ingredients exist, the inserted steps are to be

disregarded for fiscal purposes.

....The Ramsay approach is no more than a useful aid. This is not an area for

absolutes. The paramount question always is one of interpretation of the

particular statutory provision and its application to the facts of the case. Further,

as I have sought to explain, Ramsay did not introduce a new legal principle. It

would be wrong, therefore, to set bounds to the circumstances in which the

Ramsay approach may be appropriate and helpful. The need to consider a

document or transaction in its proper context, and the need to adopt a purposive

approach when construing taxation legislation, are principles of general

application. Where this leads depends upon the particular set of facts and the

particular statute.”

[81] The Vat Act of the United Kingdom (UK Vat Act)20

contains provisions which specifically

identify how one determines where a recipient is located and addresses the tax liability to

be attributed to groups of companies.

[82] Sections 9 and 43 of the UK Vat Act provides:

9. Place where supplier or recipient of services belongs

(1) Subsection (2) below shall apply for determining, in relation to any supply of

services, whether the supplier belongs in one country or another and

subsections (3) and (4) below shall apply for determining, in relation to any

supply of services, whether the recipient belongs in one country or another.

(2) The supplier of services shall be treated as belonging in a country if—

(a)he has there a business establishment or some other fixed establishment

and no such establishment elsewhere ; or

(b)he has no such establishment (there or elsewhere) but his usual place of

residence is there ; or

20

1994 Chapter 23.

Page 34 of 44

…………

(4)Where subsection (3) above does not apply, the person to whom the supply is

made shall be treated as belonging in a country if—

(a)either of the conditions mentioned in paragraphs (a) and(b) of subsection

(2)above is satisfied ; or

(b)he has such establishments as are mentioned in subsection (2) above both

in that country and elsewhere and the establishment of his at which, or

for the purposes of which, the services are most directly used or to be

used is in that country.

…………

(5)For the purposes of this section (but not for any other purposes)—

(a)a person carrying on a business through a branch or agency in any

country shall be treated as having a business establishment there ; and

……..

43. Groups of companies

(1)Where, under the following provisions of this section, any bodies corporate are

treated as members of a group any business carried on by a member of the group

shall be treated as carried on by the representative member, and—

(a)any supply of goods or services by a member of the group to another

member of the group shall be disregarded ; and

(b)any other supply of goods or services by or to a member of the group

shall be treated as a supply by or to the representative member; and

………….

Analysis

[83] Section 17 of the Act outlines the occurrences under which a supply of goods or services is

regarded as having taken place under the Act. The first occurrence mentioned is where an

invoice for the supply is given by the supplier.

Page 35 of 44

[84] The term “recipient” for the purposes of the Act and in relation to a supply of goods and

services is defined by section 3(1) of the Act to mean the person to whom the goods or

services are supplied.

[85] In the circumstances of this case which involved subcontracts, any tax evaluation which

sought to identify a third party ultimate recipient of services would have had to be wholly

fact based and explicitly founded upon the clearly articulated premise that the scope of that

exercise involved going behind the face of commercial arrangements set up. The case

before the Appeal Board did not proceed on that explicit premise.

[86] The argument that the term “recipient” under the Act, can, purely as an issue of statutory

construction and on a literal interpretation, encompass a third party ultimate recipient of

services, is not sustainable because it ignores the plain wording of the Act as to the

meaning of the term “recipient”. This meaning is consistently reinforced in other sections

of the Act. To construe it in the manner contended for by the BIR would be out of line

with the meaning of the same term in other provisions of the Act, without there being

anything to suggest that the term is meant differently or is to derive its meaning, in a

somewhat non-uniform fashion, according to the factual context.

[87] In addition, if the term “recipient” was to be construed in that generalized manner, then in

a situation which involves subcontracts, its application could be stretched quite artificially

beyond the usual boundaries of commercial arrangements and attendant obligations of

each discreet transactional arrangement. This is well illustrated by the facts of this case. If

the BIR’s argument is valid, then Allseas would also fall to be classified as a “recipient” of

services. Such a generalized interpretation would lead to highly undesirable uncertainty in

the operation of the VAT Act, especially where the provision of goods and services is

executed by various subcontractors.

[88] An example of this uncertainty would arise where goods and services are provided in

Trinidad and Tobago, by Company Y, for a local company (X), the ultimate beneficiary

being its parent company (Z), located in a foreign jurisdiction. If the BIR’s interpretation

Page 36 of 44

of the term “recipient” is valid, then if the local company issued an invoice for these goods

and services in U.S. dollars to Company Z, the local company might not be called upon to

pay output tax because they could reasonably argue that the ultimate recipient was the

parent company, which was outside of Trinidad and Tobago. This would, however,

completely ignore the fact and underlying commercial reality that, under a contract, the

goods were actually provided to a local company and so tax should be charged. The

generalized meaning of the term “recipient” under the Act contended for by the respondent

would then permit a selective application of the Act.

[89] In this case, if the BIR’s argument is correct, it would lead to the highly anomalous

position where BGTT is regarded as being the recipient of services although there was no

privity of contract between BCIL and BGTT. This would contradict commercial and

contractual reality.

[90] The conjoint effect of sections 3(1), 17, 31 and 36 of the Act is that the "recipient” of a

supply is the counterparty to the transaction undertaken by the registered person. That

counterparty being:

(a) The person to whom the registered person is obligated to provide the commercial

supply;

(b) The person to whom the registered person is obligated to provide a tax invoice

identifying among other things, the recipient and the value of the supply; and

(c) The person who is obliged to pay to the registered person the sums in settlement of

the tax invoice.

3. Whether BCL was within Trinidad and Tobago?

[91] Having concluded that the word “recipient” in the Act refers to the entity receiving the tax

invoice, the ability to zero rate the goods and services provided by BCIL was dependant on

the company proving the following:

i. That the tax invoice was quoted in U.S. dollars; and

ii. That the company recipient was not ‘within’ Trinidad and Tobago.

Page 37 of 44

[92] There is no dispute that the tax invoice was quoted in U.S. dollars. The only issue was

whether BCL was ‘within’ Trinidad and Tobago because the services were being

performed via its subsidiary, BCIL. The BIR contended that there was no need for BCL to

be physically present in the jurisdiction but rather, conducting business in Trinidad and

Tobago sufficed to establish that a company was ‘within’ the jurisdiction. However, a

conclusion that BCL had a constructive presence in Trinidad and Tobago ignores the

commercial realities involved in a situation with subcontracts. For the notion of

constructive presence to be legitimately incorporated into the Act, an explicit statutory

provision would have been necessary so as to in effect permit the displacement of the

usual prima facie inferences which attend commercial arrangements involving

subcontracts.

[93] If the equivalent of sections 9 and 43 of the UK Vat Act were contained in our legislation,

the subcontract between the subsidiary company (BCIL) and its parent company (BCL)

could, with explicit statutory sanction, be ignored and both entities treated as having the

same identity. Therefore, BCL would be considered to be within Trinidad and Tobago.

However, there is no counterpart to sections 8 and 29 of the UK Vat Act in Trinidad and

Tobago.

Disposition

[94] Rule 61.7(2) of the CPR deals with the way in which the court of appeal may treat with the

amendment of a case stated and establishes that:

“the court may amend the case or order it to be returned to the person or tribunal

stating the case for amendment.”

[95] The questions which arose in this matter were questions of law. The BIR erred in its

interpretation and the questions of law are answered in the following way:

i. The word “recipient” in the Act referred to the company with whom BCIL

contracted, that being, BCL; and

Page 38 of 44

ii. BCL was not ‘within’ Trinidad and Tobago, for the purposes of the Act, when

the invoices for the services provided by BCIL were issued.

[96] The Appeal is allowed. The Appeal Board’s decision is hereby reversed and the case stated

by the Tax Appeal Board is amended by deleting paragraph 31 and inserting “The points

of law for consideration by, and the opinion of, the court of appeal are:

i. Whether the Tax Appeal Board was correct in its statutory construction and/or

interpretation of the word “recipient” as defined by section 3(1) of the Value

Added Tax Act (“VAT Act”) for the purposes of the VAT Act; and

ii. Whether the Tax Appeal Board was correct in its application of the VAT Act

as it so construed and interpreted to the facts as agreed between the Appellant

and Respondent by the Agreed Statement of Facts filed in the tax appeals on

16th

December 2003.”

[97] In the context of the provisions of the Act the commercial supplies made by BCIL were

properly zero rated because they were supplied for a consideration that was payable in

U.S. dollars to the (transactional) recipient BCL, which was not in Trinidad and Tobago at

the time when the services were performed.

[98] The parties will be heard on the issue of costs.

M. Mohammed