reproductions supplied by edrs are the best that can … · types of accounts banking services....

TRANSCRIPT

DOCUMENT RESUME

ED 468 975 CE 083 857

TITLE Bank On It. FDIC Money Smart Financial Education Curriculum =Curso Bancario Basico. FDIC Money Smart Plan de Educacionpara Capacitacion en Finanzas.

INSTITUTION Federal Deposit Insurance Corp., Washington, DC.PUB DATE 2002-00-00NOTE 151p.; CD-ROM version not available from ERIC. For other

Money Smart modules, see CE 083 858-866.AVAILABLE FROM Federal Deposit Insurance Corporation, 550 17th Street, NW,

Washington, DC 20429 Attention: Money Smart Order Desk, PA-1730-7070B. Fax: 202-416-2111; Web site: http://www.fdic.gov/consumers/consumer/moneysmart/.

PUB TYPE Guides Classroom Learner (051) Guides ClassroomTeacher (052) Multilingual/Bilingual Materials (171)

LANGUAGE English, SpanishEDRS PRICE EDRS Price MF01/PC07 Plus Postage.DESCRIPTORS *Adult Education; *Banking; Banking Vocabulary; Basic

Business Education; Behavioral Objectives; *ConsumerEducation; Curriculum Guides; Financial Services;Instructional Materials; Learning Activities; LearningModules; *Money Management; Spanish; Teaching Guides

ABSTRACT

This module, an introduction to bank services, is one of tenin the Money Smart curriculum, and includes an instuctor guide and a take-home guide. It was developed to help adults outside the financial mainstreamenhance their money skills and create positive banking relationships. It isdesigned to enable participants to build a relationship with a financialinstitution. Topics are types of financial institutions, banking terms,deposits vs. nondeposit products, and additional bank services. Each moduleconsists of an instructor guide; sample promotional flyer, and take-homeguide for class participants. The instructor guide provides this information:preparing to present the course; materials and equipment list; and guide toicons. Each page is divided into two columns. The left presents icons toalert the instructor to discussion questions, exercises, transitions, andsummaries; the'right provides step-by-step directions that enable theinstructor to ask questions, provide explanations, show slides, handoutmaterials, and introduce exercises. Handouts and overheads are appended. Theflyer follows. The take-home guide is comprised of information sheets;frequently asked questions; checklists for choosing an account and a bank;glossary; course evaluation; and "What Do You Know," a pre-and post-form thatshows what participants know about banking basics. (YLB)

Reproductions supplied by EDRS are the best that can be madefrom the original document.

kr) rN00

Bank On It. FDIC Money Smart FinancialEducation Curriculum = Curso Bancario Basico.

FDIC Money Smart Plan de Educacion paraCapacitacion en Finanzas.

U.S. DEPARTMENT OF EDUCATIONOffice of Educational Research and ImprovementEDUCATIONAL RESOURCES INFORMATION

CENTER (ERIC)0 This document has been reproduced as

received from the person or organizationoriginating it.

13 Minor changes have been made to improvereproduction quality

o Points of view or opinions stated in thisdocument do not necessarily representofficial OERI position or policy.

ST COPY AVAILABLE

2

Bank On Itr U.S. DEPARTMENT OF EDUCATION -\

..

Office of Educational Research and ImprovementEDUCATIONAL RESOURCES INFORMATION

CENTER (ERIC)1)This document has been reproduced asreceived from the person or organizationoriginating it.

Minor changes have been made toimprove reproduction quality.

° Points of view or opinions stated in thisdocument do not necessarily representofficial OERI position or policy.

Building: Knowledge, Security, Confidence

FDIC Financial Education Curriculum

Building: Knowledge, Security, Confidence

FDIC Financial Education Curriculum

3

Table of Contents

Instructor Information 1

Before the Session 1

Materials and Equipment 1

Instructor Steps 2Icons 3

Bank On It 4Course Introduction 5What Do You Know 7Introduction to Banks. 8Keep Your Money in the Bank 10Types of Financial Institutions 11Basic Banking Terms 12Deposits Versus Nondeposit Products 20Additional Bank Services 22Tour of a Bank 29Course Summary 32End of Course Evaluation 33

Handouts 35

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

Instructor Information

Before the SessionTo properly present the Bank On It course, you should:

Review all materials in the Instructor Guide and the Participant Take-Home Guide.

Make copies of Participant Take-Home Guide.

Copy slides (overheads) onto transparencies.

Make copies and cut play money.

When appropriate, prepare chart paper examples.

Identify potential trouble spots in the exercises, as well as hints forassisting participants.

Select and prepare anecdotes from real-world experiences that can beused to illustrate special scenarios, generate discussion, and maintainparticipant interest.

Materials and EquipmentTransparency projector

Bank On It transparencies

Chart paper and easel

Markers for chart paper and transparencies

Name tents

Pencils or pens for each participant

Envelopes

Play money

Container marked "Bank" (e.g., box, hat)

Participant Take-Home Guides

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

J

Instructor Steps

Step-by-step directions are provided for the instructor. The text below is anexample of an instructor step:

Instructor Cue Instructions

You Will Know

Major types of insuredfinancial institutions

Basic banking terms

Differences between banks andcheck-cashing services

Bank employees and their jobs

Types of accounts

Banking services

Slide 2

Show Slide 2 (You Will Know).

Review course objectives.

Generally, these steps enable the instructor to ask questions, provideexplanations, show slides, hand out materials, and introduce exercises.

BEST COPY AVAILABLE6

Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Icons

Icons alert the instructor to discussion questions, exercises, transitions, andsummaries. They appear in the left margin:

?

/I\

RI

iHi

Ask questions or conduct a discussion.

Distribute a handout.

Report out exercise information or record the results of a brainstorm.

Refer to activity material.

Indicate the beginning of an individual activity or exercise.

Indicate the beginning of a group activity or exercise.

Summarize an activity or check for understanding.

Summarize the course.

Transition to the next topic.

Thumbnail-sized replicas of the slides have been placed in the left column.

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

Bank On It

Time65 Minutes

ObjectivesBy the end of this course, participants will be able to build a relationship with a financialinstitution. To achieve this objective, participants will be able to:

Recognize the major types of insured financial institutions

Recognize basic banking terms

Recognize differences between banks and check-cashing services

Identify bank employees and their jobs

Identify the types of accounts

Describe banking services

8

Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Course IntroductionInstructor Cue Instructions

Before the start of the class, hand out the followingmaterials to each participant:

Participant Take-Home Guide

Name tent

Pencil or pen

$100 of play money

Envelope

Bank on It

Slide 1

Show Slide 1 (Bank On It).

"Welcome to Bank On It!" Introduce yourself (e.g.,name, experience as an instructor or banker).

Explain: "By taking the Bank On It course, youare making an important first step to building abetter financial future for yourself and yourfamily. It all starts with understanding thebasics of personal finances."

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

5

Instructor Cue Instructions

You Will Know

Major types of insuredfinancial institutions

Basic banking terms

Differences between banks andcheck-cashing services

Bank employees and their jobs

Types of accounts

Banking services

Slide 2

Show Slide 2 (You Will Know).

Explain: "By the end of the course, you will beable to build a relationship with a financialinstitution. You will know:

The major types of insured financialinstitutions

Basic banking terms

Differences between banks and check-cashing services

Bank employees and their jobs

Types of accounts, and

Banking services."

Show the Participant Take-Home Guide to the class.

Explain: "Each of you has a copy of the Bank OnIt Take-Home Guide which contains highlightsof the course. We will be using this throughoutthe course. Take it home and use it as areference."

10

Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

What Do You KnowInstructor Cue Instructions

Explain: "Take out the last page of your Take-Home Guide, the What Do You Know form."

Explain: "The What Do You Know form lets youmeasure how much you have learned from thecourse."

Read the instructions and walk the participants througheach statement.

Explain: "Complete the Before-the-Coursecolumn only. You will complete the othercolumn at the end the course."

Provide enough time for participants to complete the WhatDo You Know form. (1-2 minutes)

Have participants put these forms aside until the end of thecourse when they will complete the After-the-Coursecolumn.

Transition: "Let's get started on banking basics!"

--*

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 11

7

Introduction to BanksInstructor Cue Instructions

Ask: "When I say 'bank' in this course, this alsoincludes credit unions and thrifts. What comesto mind when you hear the word 'bank?'"1117

Write participant responses on the chart paper.

Explain: "These words reflect how you viewbanks. A bank is a business that offers you aplace to keep your money and uses your moneyto make more money.

This business is also called a financialinstitution. Banks offer you different servicesfor keeping your money."

/I\

Guide a brief group discussion by asking the next threequestions to help you understand the participants'experiences and understanding of basic banking.

Ask: "What has been your experience with abank?"

1111)

Ask: "Where do you keep your money?"

12

8 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Instructor Cue

11117

Instructions

Ask: "What are some reasons for you to keepyour money in a bank?"

Write the participants' responses to the last question onchart paper.

Transition: "Many people keep their money inbanks. Let's take a look at some reasons whyyou might want to keep your money in a bank."4,

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 13

9

Keep Your Money in the BankInstructor Cue Instructions

Keep Your Money inthe Bank

Safety

Convenience

Cost

Security

Financial Future

ISlide 3

Show Slide 3 (Keep Your Money in the Bank). Show onereason at a time.

Relate each of the reasons below to the participants'discussion in the beginning of the course. If participants donot address all the factors, provide the missing answers.

Answer:

Safety Money is safe from theft, loss and fires.

Convenience You can get money quickly and easily.

Cost Using a bank is probably cheaper than usingother businesses to cash your check.

Security The basic insured amount of a depositor is$100,000. This means that if for some reason the bankcloses and cannot give its customers the money theyhad in the bank, the Federal Deposit InsuranceCorporation (FDIC) will return the money to thecustomer.

You can tell if the FDIC insures a bank by the FDIC logo.Similarly, most credit unions are insured by the NationalCredit Union Administration (NCUA).

Financial Future Building a relationship with a bankwill establish a record of paying bills, can help you savemoney, and is necessary for getting a loan.

Transition: "During this discussion we talkedabout why you should keep your money in afinancial institution. Now let's talk about thedifferent types of financial institutions."

14

10 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Types of Financial InstitutionsInstructor Cue Instructions

Types of FinancialInstitutions

Banks

Credit Unions

'Thrifts

L

Slide 4

Show Slide 4 (Types of Financial Institutions).

Remind the participants that the term "bank" and "financialinstitution" are used interchangeably in this course. Alltypes of institutions are regulated by state and federal rules.

Explain: "There are three major types of financialinstitutions:

Bank A financial institution run underfederal and state laws and regulations.Banks make loans, pay checks, acceptdeposits, and provide other financialservices.

Credit Union A nonprofit financialinstitution owned by people who havesomething in common. You have to becomea member of the credit union to keep yourmoney there.

Thrift A savings bank or savings and loanassociation that is similar to a bank. Thriftswere created to promote homeownership andmust have a majority of their assets inhousing-related loans. Although manybanks also make home loans, a thrift's mainbusiness is to make home loans."

Transition: "No matter what type of financialinstitution you use, all of them use some basicbanking terms."

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

15

11

Basic Banking TermsInstructor Cue Instructions

Explain: "Pull out the envelope and play money."

Walk participants through adding up the money. Write outthe totals on chart paper.

Explain: "Each of you should have $100.

Two $20s = $40

Four $10s = $40

Three $5s = $15

Five $1s = $5"

Explain: "The envelope represents an account.You cannot open the account until afteraccount verification. Let's discuss accountverification."

Explain: "Before opening an account, mostbanks will review your history of usingchecking accounts through companies such asTeleCheck or ChexSystems. Some banks willrun a full credit report to determine the level ofrisk.

Account information is collected from financialinstitutions. If you have a history of bouncingchecks or misusing your accounts, financialinstitutions might not open an account for you.

The bank will need your picture identification,usually a drivers license, and your SocialSecurity number to verify the information."

16

12 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Instructor Cue Instructions

Explain: "After the bank determines if you areeligible to open an account, you deposit moneyinto your new account."

Show Slide 5 (Deposit).

Explain: "A deposit is money you add to youraccount. When you add money to youraccount, you must fill out a deposit slip.

A deposit slip tells the bank how much moneyyou are adding to your account.

Depending on what you deposit cash, apayroll check, or a check drawn on an out-of-state bank, you may not have immediate use ofthe funds.

The bank must first make sure there are fundsat the originating bank to cover your check.You can ask the bank when you can use themoney you deposited."

De .osit

YA deposit is money you add toaccount using a deposit slip.

. _ , ,

I17- -...-.-T--:. -.........-,- ...AM WY VOL

Slide 5

Prompt: "Now put all the money into theenvelope."

Explain: "What you just did was make a deposit."

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 17

13

Instructor Cue Instructions

Show Slide 6 (Balance).

Explain: "Balance is the amount of money youhave in your bank account."

Balance

Balance is the amount oc moneyyou have in your bank account.

.:,

1Slide 6

Ask: "What is your balance?"

Answer: $100

Draw on chart paper a three-column table to track thebalance of upcoming transactions. For example:

Description +/- Balance

Opening Balance +$100 $100

Explain: "When you make a withdrawal, you aretaking money from your bank account. You dothis by writing a check, giving a teller awithdrawal slip, or by using an ATM."

14 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Instructor Cue Instructions

Show Slide 7 (Withdrawal).

Explain: "A withdrawal slip looks similar to adeposit slip, except you are taking money outrather than adding money to your account.

Know how much is in your account so youwon't try to withdraw more money than youhave. With a checking account, if youoverdraw, or 'bounce a check', you will becharged a fee."

Withdrawal

Withdrawal is die process oftaking money from your bankaccount using :

Cheeks "1MWithdrawal slips

ATMs

tiSlide 7

Prompt: "Take $20 out of the envelope."

Explain: "You just made a withdrawal."

Ask: "What is your balance now?"

Show calculation of the new balance on chart paper.($100 $20 = $80)

Description +/- Balance

Opening Balance +$ 100 $ 100Withdrawal - $ 20 -J)

$ 80

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 19

15

Instructor Cue. Instructions

Fees

A fee is when banks take moneyout of your account for:

Services (monthly maintenance fec)

Penalties (bouncing a check)

Slide 8

Show Slide 8 (Fees).

Explain: "Financial institutions charge you feesfor different services. For example, a monthlymaintenance fee might be charged for keepingyour account open.

In addition, you might also be charged a penaltyfee if you misuse your account, such as bybouncing a check."

Prompt: "Take $4 out of your envelope and givethe money to the banker."

Instructor Note: Collect money from participants and put itin the box called "bank."

Explain: "This demonstrates a monthlymaintenance fee being charged to youraccount."

Ask: "What is your balance now?"

Show calculation of the new balance on chart paper.($80 - $4 = $76)

Description Balance

Opening Balance +$ 100 $ 100Withdrawal $ 20 -$ 20

$ 80Fees - $ 4 -$ 4

$ 76

20

16 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Instructor Cue InstructionS.

Show Slide 9 (Interest).

Explain: "Interest is the extra money in youraccount that the bank pays you for keepingyour money at that bank. One of theadvantages of having a deposit account is theinterest you earn."

Interest

Interest is extra money in youraccount that the bank pays youfor keeping your money at thatbank

a/dr.;

Slide 9

Hand out $1 additional play money to each participant.

Prompt: "Add the $1 to your envelope."

Explain: "This demonstrates your accountearning interest."

Ask: "What is your balance now?"

Show calculation of new balance on the chart paper.($76 + $1 = $77)

Description +/- Balance

Opening Balance +$ 100 $ 100Withdraw - $ 20 -$ 20

$ 80Fees - $ 4 =S__

$ 76Interest +$ 1 t$__1

$77

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 21

17

Instructor Cue Instructions

Ask: "Who uses a check-cashing service?"

Ask a volunteer participant:

"How many checks do you cash per month?"

"How much are you charged per check?"

/I\Write the participant's responses on the left side of the chartpaper.

If no one volunteers information, use this example:

"One of the participants in an earlier class useda check-cashing store to cash her checks. Shecashed four checks a month and was charged$5 each time.

That means she paid $20 a month (4 x $5) or$240 a year ($20 x 12 months) just to cash herchecks."

22

18 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Instructor Cue Instructions

Compare the total yearly cost of using a check-cashingservice to using bank services on the right side of the chartpaper.

"Another participant had an account at a bankthat charged a monthly fee of $5, whichincluded 8 free checks per month and free useof the ATM.

Additionally, ordering a box of 100 checks costher about $18, since she purchased the checksthrough the bank.

In this case, using a checking account for oneyear cost her $78 ($5 x 12 months = $60 + $18 =$78). This equals a savings of $162 ($240 - $78)a year!"

Explain: "Even though banks charge monthlyfees, these examples show it is much cheaperto use a deposit account at a bank."

Transition: "Understanding these basic bankingterms will help you choose the best type ofaccount for you. Let's see what types ofaccounts are available."

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

23

19

Deposits Versus Nondeposit ProductsInstructor-,Pue Instructions

Explain: "Bank accounts that allow you to addmoney to the account are called depositaccounts. Checking and savings accounts aretwo examples of deposit products."

Show Slide 10 (Deposit Accounts).

Explain: "A checking account is an account thatlets you write checks to pay bills or to buygoods. The financial institution takes themoney from your account and pays it to theperson named on the check. The financialinstitution sends you a monthly record of thedeposits and withdrawals made. This is calleda bank statement."

De t osit Accounts

Checking Account

An account that lets you writechecks to pay bills or buy goods.

Savings Account

An account that always earnsinterest.

tSlide 10

Explain: "A savings account is an account thatalways earns interest. You cannot write checkson a savings account.

You can open a savings account with a fewdollars, but you might pay a monthly fee if thebalance is below a certain amount.

The bank will help you keep track of youraccount by either sending you a statement orproviding you with a booklet called apassbook." .

Explain: "It is a good idea to compare the rulesof the different accounts. For example, banksmight require you to have a certain balance toopen an account, earn interest, or avoid fees.This is usually called a minimum balance."

2420 Bank On It

FDIC Money Smart Financial Education CurriculumInstructor Guide

Instructor Cue Instructions

Prompt: "Turn to page 5 of your Take-HorheGuide, Choosing an Account."

Explain: "Carry this checklist with you when youlook for an account. Ask these questions tohelp you choose which account is right foryou."

Explain: "Many banks also offer nondepositproducts that are not insured by the FDIC.Stocks, bonds, and mutual funds are examplesof nondeposit investment products.

Bank personnel are supposed to provide awritten explanation that these products are notinsured by the FDIC and may lose value. Youcan find out more about these nondepositproducts at your bank.

Do not buy any product or service you do notunderstand."

Transition: "Most financial institutions offer theseprimary types of products and services. Thereare additional services you receive when youopen an account at a bank."

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

25

21

Additional Bank ServicesInstructor Cue Instructions

/I\Explain: "Banks provide various additionalservices for free or a low fee with some depositaccounts. It is important to keep track of thefees charged, if any. The following are commonservices offered at banks:

Direct Deposit

Money Order

Wire Transfer

Telephone Banking

ATM

Debit Card, and

Loans."

Write the list of additional services on chart paper.

4PTransition: "Let's see if you can guess whichbank service I'm describing. I'll describe one ofthe services from the list. You say which one itis."

Read: "This is a computer where you candeposit, withdraw, or transfer money from oneaccount to another 24 hours a day."

Ask: "Who can guess what I am describing?"

Answer: Automated Teller Machine (ATM)

26

22 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Instructor Cue Instructions

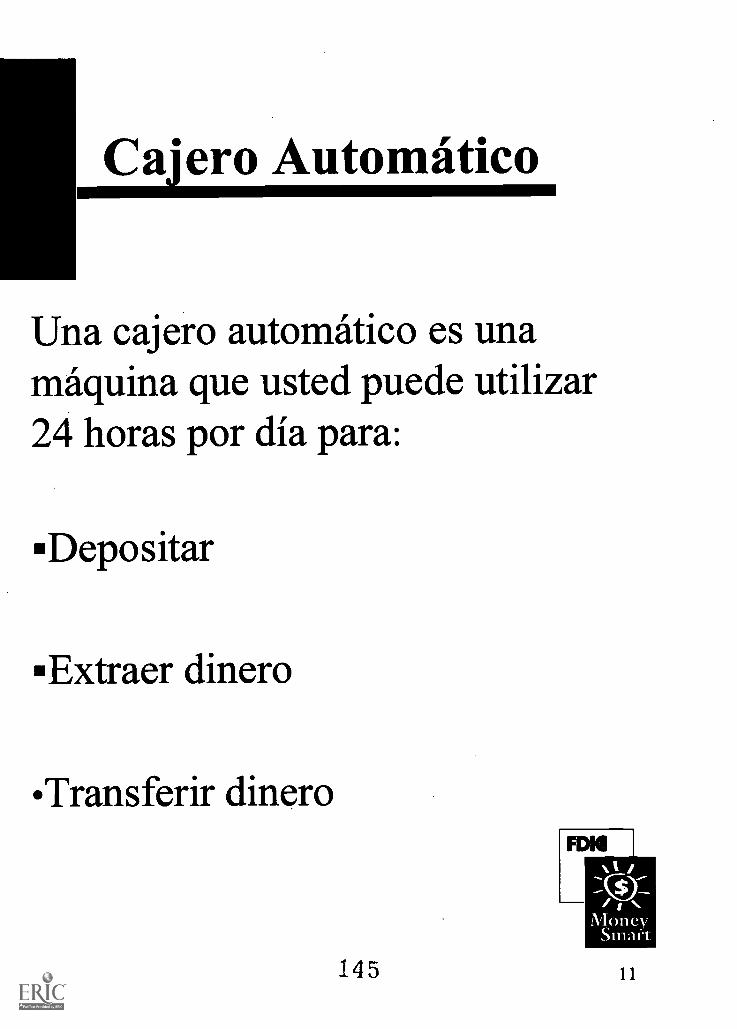

ATM

An ATM is a machine you canuse 24 hours a day to:

Deposit

Withdraw

Transfer money

13

Slide 11

Show Slide 11 (ATM).

Explain: "Use of an ATM requires a card issuedby the bank and a personal identificationnumber or PIN. A PIN is a special password orset of numbers to use your ATM card. The PINis used for security purposes, so no one elsecan access your account.

You can use the ATM for many services, butthere might be a fee involved. Most people usethe ATM to get cash from their account. If youuse another bank's ATM, you might be chargedan additional fee. Generally, you can only makedeposits at your bank's ATM."

Read: "When you use this card to buysomething from a store or other business, themoney comes out of your bank accountimmediately."

Ask: "Who can guess what I am describing?"

Answer: Debit Card

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

27

23

Instructor Cue Instructions

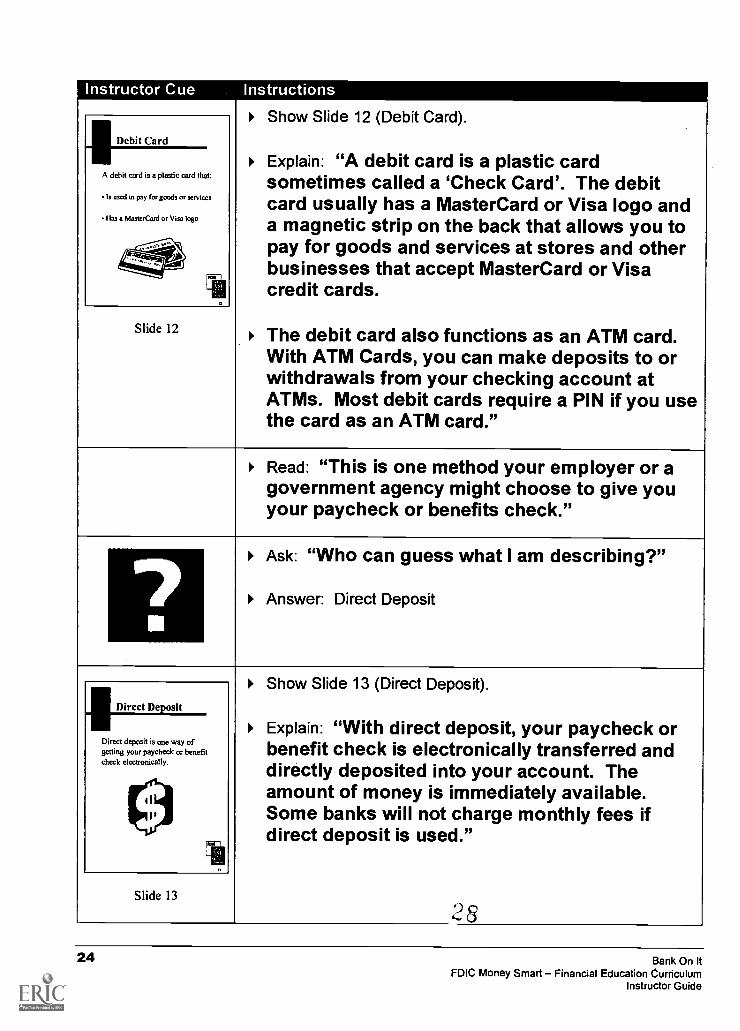

Show Slide 12 (Debit Card).

Explain: "A debit card is a plastic cardsometimes called a 'Check Card'. The debitcard usually has a MasterCard or Visa logo anda magnetic strip on the back that allows you topay for goods and services at stores and otherbusinesses that accept MasterCard or Visacredit cards.

The debit card also functions as an ATM card.With ATM Cards, you can make deposits to orwithdrawals from your checking account atATMs. Most debit cards require a PIN if you usethe card as an ATM card."

Debit Card

12

A debit card is a plastic card that:

Has a MasterCard or Visa logo

Slide 12

Read: "This is one method your employer or agovernment agency might choose to give youyour paycheck or benefits check."

Ask: "Who can guess what I am describing?"

Answer: Direct Deposit

Show Slide 13 (Direct Deposit).

Explain: "With direct deposit, your paycheck orbenefit check is electronically transferred anddirectly deposited into your account. Theamount of money is immediately available.Some banks will not charge monthly fees ifdirect deposit is used."

Direct Deposit

Direct deposit is one way ofgetting your paycheck or benefitcheck electronically.

Slide 13

24 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

InstructorCue Instructions.Read: "This is money you borrow from a bankwith a written promise to pay it back later."

Ask: "Who can guess what I am describing?"

Answer: Loans

Show Slide 14 (Loans).

Explain: "Banks charge you fees and interest.This is extra money you pay to borrow themoney. You can talk to the customer servicerepresentative for more information about loansoffered at a bank."

Loans

A loan is money you borrowfrom a bank with a writtenpromise to pay it back later.

'''4:9.

Slide 14

Read: "This is used like a check to pay a bill."

Ask: "Who can guess what I am describing?"

Answer: Money Order

U

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 2 9

25

Instructor Cue Instructions

Money Order

A money order is similar to acheck. It is used to:

Pay bills

Make purchases

Lb

Slide 15

Show Slide 15 (Money Order).

Explain: "A money order is similar to a check. Itis used to pay bills or make purchases whencash is not accepted. Many businesses sellmoney orders for a fee. If you need to use amoney order, it is best to shop around for thebest price."

Instructor Note: Refer to the definitions below, if theparticipants ask about the differences between:

Cashier's check

Certified check

Money orders

Teller's check

Cashier's check For a cashier's check, you provide cashor money from your account in the amount of the check plusa service charge (usually from $2 to $5). You also tell theinstitution who is receiving the check. The institution writesa check (also called a bank check or teller's check) for you.This check is guaranteed not to bounce. A cashier's checkis available from financial institutions.

Certified Check A certified check is a check you write andtake to your financial institution. The bank will mark it"certified" for a fee (usually $2-$5) and place a hold on themoney in your account until the check is processed. Acertified check is guaranteed not to bounce.

Teller's check A teller's check is similar to a money order,but a teller's check is provided by a financial institutioninstead of other businesses.

3026 Bank On It

FDIC Money Smart Financial Education CurriculumInstructor Guide

Instructor Cue Instructions

Read: "This allows you to check your accountbalance by phone."

Ask: "Who can guess what I am describing?"

Answer: Telephone Banking

Show Slide 16 (Telephone Banking).

Explain: "Telephone banking allows you to:

Check account balances

Transfer money between accounts

Obtain account history, such as most recentdeposits or withdrawals

Stop payment on a check

Obtain information on branch hours or otherinformation, and

Report a lost, stolen, or damaged card."

Telephone Banking

Telephone banking allows you to:

Check your account

Transfer money

Obtain account history

Stop payment on cherlObtain branch hours

Report a lost, stolen Of damaged card

fi'

Slide 16

Read: "This is a method of electronicallytransferring money from one bank to another. "

Ask: "Who can guess what I am describing?"

Answer: Wire Transfer

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

27

Instructor Cue Instructions

Transition: "Now that you've learned some basicbanking terms, the types of accounts andservices, let's talk about the people who work ina bank."

32

28 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

Tour of a BankInstructor Cue Instructions

Explain: "A financial institution has people whocan help you with different banking services.Understanding the jobs of these bank workerswill allow you to know who you should talk towhen you go to the bank."

Ask four participants to volunteer.

Assign a person to each of the following:

Customer

Teller

Loan Officer

Branch Manager

Prompt the participant assigned as a customer to beginwalking through the "bank."

Greet and introduce yourself as a Customer ServiceRepresentative.

Take the customer on a tour of the bank.

Explain: "As a customer service representative, Ican:

Help you open your account

Explain services

Answer general questions

Refer you to a person who can help you, and

Provide written information explaining thebank products"

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

33

29

Instructor Cue Instructions

Introduce the teller.

Explain: "The teller stands behind a counter and:

Takes money

Answers questions

Cashes checks, and

Refers you to the person who can help you.

The teller is often the main contact at the bank.Any time you come in the bank, you can go toany teller."

Introduce the loan officer.

Explain: "The loan officer:

Takes applications for loans offered at thebank

Answers questions

Provides written information explaining loanproducts, and

Helps you fill out a loan application."

Introduce the branch manager.

Explain: "The branch manager:

Supervises the bank operations, and

Helps fix problems that cannot be solved byother bank employees."

3430 Bank On It

FDIC Money Smart Financial Education CurriculumInstructor Guide

Instructor Cue Instructions

Explain: "Here are some key points to remember:

If you don't know who to talk to, ask for help.Someone will take you to the right person.

Always ask questions until you are clear onall the information, and don't sign anythingyou don't understand.

Ask for written information to take home toreview."

1rPrompt: "Turn to page 6 of your Take-HomeGuide, Choosing a Bank."

Explain: "Remember you can use this checklistand the checklist on page 5 to help you choosea bank and the account that's right for you."

Review the content of the forms with the participants.

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 35

31

Course SummaryInstructor Cue Instructions

Summarize the course: "Congratulations! You'vecompleted the Bank On It course. We'vecovered a lot of information today about basicbanking:

Types of insured financial institutions

Basic banking terms

Differences between banks and check-cashing services

Bank employees and their jobs

Types of accounts, and

Types of banking services.

Remember, banks offer more services than acheck-cashing service. Using the informationyou've learned in this course, you should beable to begin using the services of a bank.

Building a relationship with a bank can help youestablish a record of paying bills, can help yousave money, and is necessary for obtainingcredit."

Transition: "To improve the course, we will needyour feedback. The After-the-Course columnand Course Evaluation will identify changesthat can make this course better."

36

32 Bank On ItFDIC Money Smart Financial Education Curriculum

Instructor Guide

End of Course EvaluationInstructor Cue Instructions

Explain: "Please complete the After-the-Coursecolumn and the Course Evaluation. Theseforms are the last two pages of your Take-HomeGuide."

Allow time for participants to complete it.

Collect the What Do You Know and Course Evaluationforms.

Conclusion: "Great job on completing the BankOn It course! Thank you for participating."

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide

33

Handouts

Play Money

Bank On ItFDIC Money Smart Financial Education CurriculumInstructor Guide 38

35

A

VI]V

v MONEY SMART

V,

SMART cl

v MONEY

te, -"-

SMART

/)1.t

-""/: III

MOit\

SMART

V

V MONEY

4-,

SMART

,l'iir,-Mb , TI,

') I !1 ,

itv,

v MONEY SMARTV

I'a

PTivv,...-----i- '4

? 11,

MONEY I SMART]

1 /7

- --)

CI

'D)

MONEY SMART

PD1) I.P,

MONEY SMART

L

PDI) 1-MONEY

INSERT "OVERHEADS" TAB HERE

41

Building: Knowledge, Security, Confidence

FDIC Financial Education Curriculum

42

on ..ill Know

Major types of insuredfinancial institutions

Basic banking terms

Differences between banks andcheck-cashing services

Bank employees and their jobs

Types of accounts

Banking services

43

FDIG

MoneySmart

2

_ee our Moneyin e ank

Safety

Convenience

Cost

Security

Financial Future

Each depositor insured to $100,000

FDIFEDERAL DEPOSIT INSURANCE CORPORATION

BEST COPY AVAILABLE

4 4

FDIG

MoneySmart

3

pes of Financialnstitutions

Banks

Credit Unions

Thrifts

45

FDIG

2*_Money

Smart

4

e osit

A deposit is money you add toyour account using a deposit slip.

Your NameYour Address

Your Phone Number

11 1 DATEw mil DEPOSITS AIRY NOT BE AVAILABLE FOR IMMEDIATE WITHDRAWAL

00. MON HEREIF CASH RECEIVED FROMDEFOSff

LLIYOUR FINANCIAL INSTITUTION

YOUR CITY, CA 92453

DO NOT USE FOR AUTOMATIC PAYMENTOR CHECK TRANSACTIONS

:000000: 12345 67890.:

CURRENCY

COIN

E OR TOTALC FROM REVERSE

SUBTOTAL

LESS CASHRECEIVED

NETDEPOSIT

FDIE

46

MoneySmart

5

a ance

Balance is the amount of moneyyou have in your bank account.

47

FOG

-*Money

Smart-.

6

Withdrawal slips

IS7

ees

A fee is when banks take moneyout of your account for:

Services (monthly maintenance fee)

Penalties (bouncing a check)

49

FDIGvt

MoneySmart

8

n eres

Interest is extra money in youraccount that the bank pays youfor keeping your money at thatbank.

50

FDIC1

MoneySmart

9

e osi Accounts

Checking AccountAn account that lets you writechecks to pay bills or buy goods.

Savings AccountAn account that always earnsinterest.

FDIC

$ _Money,Smarr

10

An ATM is a machine you canuse 24 hours a day to:

Deposit

Withdraw

Transfer money

52

FDIG

MoneySmart

11

e i and

A debit card is a plastic card that:

Is used to pay for goods or services

Has a MasterCard or Visa logo

BEST COPY AVAILABLE

53

FDIG

MoneySmart

12

irect Deposit

Direct deposit is one way ofgetting your paycheck or benefitcheck electronically.

54

FDIG

MoneySmart

13

oans

A loan is money you borrowfrom a bank with a writtenpromise to pay it back later.

r-J

FDIG

MoneySmaft-

14

iv.one Order

A money order is similar to acheck. It is used to:

Pay bills

Make purchases

56

FDIC

MoneySmart

15

...eem2.IBaLLkin

Telephone banking allows you to:

Check your accountTransfer money

Obtain account history

Stop payment on checkObtain branch hours

Report a lost, stolen or damaged card

57

FD11 1

MoneySmart

16

INSERT "PROMOTIONAL FLYER" TAB HERE

58

Bank On ItAn Introduction to Bank Services

Date:

Time:

Place:

Sponsored by:

To Register:

The Money Smart Training Program

Building: Knowledge, Security, Confidence

59

" ,, ,

MoneySmart

INSERT "TAKE-HOME GUIDE" TAB HERE

60

Bank On It

1111161111

Building: Knowledge, Security, Confidence

FDIC Financial Education Curriculum

61

Table of Contents

Table of Contents 1

Money Smart 2

Bank On It 3

Frequently Asked Questions 4

Choosing an Account 5

Choosing a Bank 6

Glossary 7

For Further Information 12

Acknowledgements 13

Course Evaluation - Bank On It 14

What Do You Know - Bank On It 15

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide

Money SmartThe Money Smart curriculum is brought to you by the Federal Deposit InsuranceCorporation (FDIC). The Money Smart program includes the following courses:

> Bank On Itan introduction to bank services

> Borrowing Basicsan introduction to credit

> Check It Outhow to choose and keep a checking account

> Money Mattershow to keep track of your money

> Pay Yourself Firstwhy you should save, save, save

> Keep It Safeyour rights as a consumer

> To Your Credithow your credit history will affect your credit future

> Charge It Righthow to make a credit card work for you

> Loan to Ownknow what you're borrowing before you buy

> Your Own Homewhat homeownership is all about

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 63

Bank On ItWelcome to Bank On It! By taking this course, you are making an important first step tobuilding a better financial future for yourself and your family. It all starts withunderstanding the basics of personal finances. This course introduces the basics ofbanking -- from the different types of financial institutions to the services they mightoffer. When you have completed this course, you will be able to begin using theservices of a bank or other financial institution.

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 64

Frequently Asked Questions

What is a bank?

A bank is a business that offers you a place to keep your money and uses it to makemore money. This business is also called a financial institution. Banks offer differentservices for keeping your money at their business.

Why should you keep your money in the bank?

Reasons why you should keep your money in the bank include:

Safety - Money is safe from theft, loss and fires.

Convenience - You can get money quickly and easily.

Cost - Using a bank is probably cheaper than using other businesses to cash yourcheck.

Security - The basic insured amount of a depositor is $100,000. This means that iffor some reason the bank closes and cannot give its customers the money they hadin the bank, the Federal Deposit Insurance Corporation (FDIC) will return the moneyto the customer.

You can tell if the FDIC insures a bank by the FDIC logo. Similarly, most creditunions are insured by the National Credit Union Administration (NCUA).

Financial Future Building a relationship with a bank will establish a record ofpaying bills, can help you save money, and is necessary for getting a loan.

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide

65

4

Choosing an AccountWhen looking for an account, take this checklist with you. The questions below canhelp you choose an account that is right for you.

Bank A Bank B Bank C

Type of accountHow much money do I needto open the account?How much do I have tokeep in my account to avoidfees?What are the fees forbounced checks?How many checks can Iwrite before extra fees arecharged?How many withdrawals canI make each month?Does this account payinterest?Does an ATM or debit cardcome with this account?Will I be charged to use theATM or debit card at thisbank?Will I be charged to use theATM or debit card atanother bank?Are there any other fees?

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 66

5

Choosing a BankWhen looking for a bank, carry this checklist with you. The questions below can helpyou choose a bank that is right for you.

Bank A Bank B Bank C

Name of bank

Does it offer the services Ineed?

Is it close to home?

Does it have reasonablehours?Does it have ATMs? If so,are they located nearwhere I live, work, orshop?If I am choosing a creditunion, am I eligible?Do any employees speakmy language?What, if any, fees will becharged?

Is this bank insured?

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide

6 -1

GlossaryAccount VerificationBefore opening an account, most banks will review your history of using checkingaccounts through companies such as Tele Check or ChexSystems. Some banks will runa full credit report to determine the level of risk.

The account information is collected from financial institutions. If you have a history ofbouncing checks or misusing your accounts, financial institutions may not open anaccount for you.

Automated Teller Machines (ATM)

This is a computer where you can deposit, withdraw, or transfer money from oneaccount to another 24 hours a day. Use of an ATM requires a card issued by the bankand a personal identification number (PIN). A PIN is a special password or set ofnumbers to use your debit or ATM card. The PIN is used for security purposes, so noone else can access your account.

You can use the ATM for many services, but there might be a fee involved. Mostpeople use the ATM to get cash from their account. If you use another bank's ATM, youmight be charged an additional fee. Generally, you can only make deposits at yourbank's ATM.

Balance

Balance is the amount of money you have in your bank account.

Bank

A bank is a business that offers you a place to keep your money and uses it to makemore money. Banks offer you different services for keeping your money.

Branch Manager

A branch manager is the person who supervises the bank operations and helps fixproblems that cannot be solved by other bank workers.

Checking Account

A checking account is an account that lets you write checks to pay bills or to buy goods.The financial institution takes the money from your account and pays it to the personnamed on the check. The financial institution sends you a monthly record of thedeposits made and the checks written.

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide

68

7

Credit Union

A nonprofit financial institution owned by people who have something in common. Youhave to become a member of the credit union to keep your money there.

Customer Service Representative or New Account Officer

The customer service representative is the person who can help you open youraccount. The representative explains services, answers general questions, refers youto a person who can help you, and provides written information explaining the bankproducts.

Debit Card

A debit card is a plastic card sometimes called a "Check Card." The debit card has aMasterCard or Visa logo and a magnetic strip on the back that allows you to pay forgoods and services at stores and other businesses that accept MasterCard or Visacredit cards. When you use a debit card, the money comes out of your bank accountimmediately.

The bank might give you a debit card that also functions as an ATM card. With a debitcard, you can make deposits to or withdrawals from your checking account at ATMs.Some debit card uses might require a PIN if you use the card as an ATM card.

Deposit Products

Deposit products are bank accounts that allow you to add money to the account.Checking and savings accounts are two examples of deposit products.

Deposit

A deposit' is' money you add to your account. When you add money to your account,you must fill out a deposit slip. A deposit slip tells the bank how much money you areadding to your account. Depending on what you deposit cash, a payroll check, or acheck drawn on an out-of-state bank, you may not have immediate use of the funds.The bank must first make sure there are funds at the originating bank to cover yourcheck. You can ask the bank when you can use the money you deposited.

Direct Deposit

Direct deposit is one method your employer or a government agency might choose togive you your paycheck or benefit check. With direct deposit, your paycheck or benefitcheck is electronically transferred and directly deposited into your account. Somebanks will not charge monthly fees if direct deposit is used.

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 69

Fees

Financial institutions charge different fees for different services. For example, a monthlymaintenance fee might be charged for keeping your account open. In addition, youmight also be charged a penalty fee if you misuse your account, such as by bouncing acheck.

Example:

One of the participants in an earlier class used a check-cashing store to cash herchecks. She cashed four checks a month and was charged $5 each time. That meansshe paid $20 a month (4 x $5) or $240 a year ($20 x 12 months) just to cash herchecks.

In comparison, another participant had an account at a bank that charged a monthly feeof $5, which included 8 free checks per month and free use of the ATM. Additionally,ordering a box of 100 checks cost her about $18, since she purchased the checksthrough the bank.

In this case, using a checking account for one year cost her $78 ($5 x 12 months = $60+ $18 = $78). In one year, she saved $162 ($240 - $78) by using a checking accountinstead of a check-cashing store.

InterestInterest is the extra money in your account that the bank pays you for keeping yourmoney. One of the main advantages of having a deposit account is the interest youearn.

Loan OfficerThe loan officer is the person who takes applications for loans offered at the bank. Theofficer can answer your questions, provide written information explaining loan products,and help you fill out a loan application.

Loans

A loan is money you borrow from a bank with a written promise to pay it back later.Banks charge you fees and interest. This is extra money you pay to borrow the money.You can talk to the customer service representative for more information about loansoffered at a bank.

Money Order

A money order is similar to a check. It is used to pay bills or make purchases in caseswhere cash is not accepted. Many businesses sell money orders for a fee. If you needto use a money order, it is best to shop around for the best price.

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 70

9

Nondeposit ProductsMany banks also offer nondeposit products that are not insured by the FDIC. Stocks,bonds, and mutual funds are examples of nondeposit investment products.

Bank personnel are supposed to provide a written explanation stating that theseproducts are not insured by the FDIC and may lose value. You can find out more aboutnondeposit products at your bank.

Savings AccountA savings account is an account that earns interest. You can open a savings accountwith a few dollars, but you might pay a monthly fee if your balance is below a certainamount. Some banks will give you a booklet called a "passbook" to keep track of yourmoney.

Telephone Banking

A bank service which allows you to:

Check account balances

Transfer money between accounts

Obtain account history, such as most recent deposits or withdrawals

Stop payment on a check

Obtain information on branch hours or other information

Report a lost, stolen, or damaged credit, debit, or ATM card

Teller

The teller is the person behind the counter who takes money, answers questions,cashes checks, or refers you to the person who can help you. Tellers are the maincontact people at the bank. You can go to any teller in the bank.

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 7 1

10

ThriftA thrift is a savings bank or savings and loan association that is similar to a bank.Thrifts were created to promote homeownership and must have a majority of theirassets in housing-related loans.

Wire Transfer

A wire transfer is a method of electronically transferring money from one bank to

another.

WithdrawalA withdrawal is the process of taking money from your bank account. You do this bywriting a check, using an ATM, or by giving a teller a withdrawal slip. A withdrawal sliplooks similar to a deposit slip, except you are taking money out rather than addingmoney to your account.

You need to be sure you do not withdraw more moneythan you have in your account.If you do, you will be overdrawn, or bounce a check, and be charged a fee.

Bank On ItFDIC Money Smart Financial Education CurriculumTake -Home. Guide 72

11

For Further Information

Federal Deposit Insurance Corporation (FDIC)

Division of Compliance and Consumer Affairs550 17th Street, NWWashington, DC 204291-877-ASK-FDIC (1-877-275-3342)Email: [email protected]

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 73

12

AcknowledgementsThe FDIC thanks the following organizations for their help in developing andpiloting the Money Smart curriculum:

Naylor Road One-Stop Career Center, Washington, D.C.

Government of the District of Columbia, Department of Employment Services

Government of the District of Columbia, Department of Banking and Financial

Institutions

Reference materials from the following sources were especially helpful in thedevelopment of the Money Smart program:

Consumer Action Handbook, 2001, Federal Consumer Information Center, UnitedStates General Services Administration

Fannie Mae

Federal Trade Commission

Gateway to a Better Life Making Every Dollar Count, 1998, Cooperative Extension,University of California

Helping People in Your Community Understand Basic Financial Services, FinancialServices Education Coalition

Internal Revenue Service

Saving Fitness A Guide to Your Money and Your Financial Future, U.S. Departmentof Labor, Pension, and Welfare Benefits Administration

Social Security Administration

United States DepartmentOf Agriculture, Rural Development, Rural Housing Service

United States Department of Housing and Urban Development

United States Veterans Administration, Department of Veterans Affairs Home Loan

Program

Bank On ItFDIC Money Smart Financial Education CurriculumTake-l-lome Guide 7 4

13

Course Evaluation - Bank On It

Instructor: Date:

Thank you for your participation in this course. Your responses will help us improve thetraining for future participants. Please circle the number that shows how much youagree with each statement. Then answer the questions at the bottom of this form. Ifyou have any questions, please feel free to ask your instructor.

a)112

a)eav)b

aa)i.a)<

> s >.cac2r)

1-to:a

d

EIT

a).2ts

1. The course was interesting and kept my attention. 1 2 3 4

2. The examples in the course were clear and helpful. 1 2 3 4

3. The activities in the course helped me understand the information. 1 2 3 4

4. The slides were clear and easy to follow. 1 2 3 4

5. The take-home materials were easy to read and useful to me. 1 2 3 4

6. The instructor presented the information clearly and understandably. 1 2 3 4

7. The information/skill taught in the course is useful to me. 1 2 3 4

8. I am confident that I can use the information/skill on my own. 1 2 3 4

9. I am satisfied with what I learned from this course. 1 2 3 4

What was the most helpful part of this course?

What was the least helpful part of this course?

Would you recommend this course to others?

Any comments or suggestions?

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide

75

14

What Do You Know - Bank On It

Instructor: Date:

This form will allow you and the instructors to see what you know about banking basicsboth before and after the class. Read each statement below. Please circle the numberthat shows how much you agree with each statement.

I know:

Before-the-Coursea)20)

a)a)

a ....0<0)b

a)Z.. a) >.a) .- a) a)c 0) c0 Cotli 2 2i._ __ 0)to' 5 a ti 5

After-the-Coursea)2ccom a)

._ 2m <0)o

a)>. a) >,a) a) a)c a) c2 Co

i-- 2cy,c I 5 b < 65

1. The major types of insured financialinstitutions.

2. Basic banking terms.

3. The difference between banks andcheck-cashing services.

4. Bank employees and their jobs.

5. The types of accounts.

6. Banking services.

1

1

1

1

1

1

2

2

2

2

2

2

3

3

3

3

3

3

4

4

4

4

4

4

1

1

1

1

1

1

2

2

2

2

2

2

3

3

3

3

3

3

4

4

4

4

4

4

Bank On ItFDIC Money Smart Financial Education CurriculumTake-Home Guide 46

15

Para Promover: Conocimiento, Seguridad y Confianza

FDIC Plan de Educacion para Capacitacion en Finanzas

Curso Bancario Basico

Guia del Instructor

Para Promover: Conocimiento, Seguridad y Confianza

FDIC Plan de Educachin para Capacitacicin en Finanzas

78

Indice

Informacian para el InstructorAntes de la Sesion 1

Materiales y Equipos 1

Pasos para el Instructor 2Simbolos Graficos 3

La Conflanza en los Bancos 4IntroducciOn al Curso 54Que Sabe Usted? 7IntroducciOn a los bancos 8Guarde su Dinero en el Banco 10Tipos de Instituciones Financieras 11Terminos Bancarios Basicos 12Depositos y Productos que no son de DepOsito 20Otros Servicios Bancarios 22Visita a un Banco 29Resumen del Curso 33Evaluacion al Finalizar el Curso 34

Materiales 35

Curso Bancario Basic°FDIC Money Smart Plan de Educaci6n para Capacitacion en FinanzasDula del Instructor

79

Informacion para el Instructor

Antes de la SesionA fin de presentar adecuadamente el curso Curso Bancario Basico:

Examine todos los materiales en la Gula del Instructor y la Guia delParticipante.

Haga copias de las Guias del Participante.

Copie las diapositivas en transparencias.

Haga copias y recorte dinero de juguete

Cuando corresponda, prepare ejemplos en laminas de papel.

ldentifique probables puntos problematicos en los ejercicios, asi comosugerencias para ayudar a los participantes.

Seleccione y prepare anecdotas de experiencias del mundo real, quepueden utilizarse para ilustrar casos hipoteticos especiales, generardebates y mantener el interes de los participantes.

Materiales y equiposProyector de transparencias

Transparencias sobre el Curso Bancario Basic°

Laminas de papel y caballete

Marcadores para laminas de papel y transparencias

Carte les con nombres

!Apices o lapiceras para cada participante

Sobres

Billetes de juguete

Envase denominado "Banco" (por ejemplo, caja, sombrero)

Guias del Participante

Curso Bancario Basic°FDIC Money Smart Plan de Educaci6n pare Capacitacidn en FinanzasGula del Instructor

80

Pasos para el Instructor

Se suministran instrucciones paso por paso para el instructor. El texto acontinuation es un ejemplo de un paso para el instructor:

Pauta para elinstructor

Usted conoceni

ftiociptdes tipos detnatnuctones financierasaseguradas

Terrninos bancarios basicos

Diferencias entre bancos ycases de carnbio

Empleados bancarios y susposiciones

Tipos de cuentas

Servicios bancarios

Diapositiva 2

Instrucciones

Muestre la diapositiva 2 (Usted conocera).

Revise los objetivos del curso.

En terminos generales, estos pasos permiten al instructor formular preguntas,ofrecer explicaciones, mostrar diapositivas, entregar materiales y presentarejercicios.

BEST COPY AVAILABLE 81

2 Curso Bancario BasicaFDIC Money Smart Plan de Education para Capacitaci6n en Finanzas

Guia del Instructor

Sim bolos Graficos

Los simbolos graficos indican al instructor preguntas para el debate,ejercicios, transiciones y resiimenes; se introducen en el margen izquierdo:

/I\

Ir

Formule preguntas o conduzca o una discusiOn.

Distribuya un folleto.

Informe sobre los ejercicios o registre los resultados de una sesion deintercambio de ideas.

Haga referencia al material de actividades.

Indique el comienzo de una actividad o ejercicio individual.

Indique el comienzo de una actividad o ejercicio de grupo.

Resuma una actividad o verifique que se haya comprendido.

Resuma el curso.

Transicion al tema siguiente.

En la columna izquierda se han incluido copias pequefias de las diapositivas.

Curso Bancario Basic°FDIC Money Smart Plan de Educacian para CapacitaciOn en FinanzasGula del Instructor

823

Curso Bancario Basico

Tiempo65 minutos

ObjetivosAl finalizar el curso, los participantes estaran en condiciones de establecer una relaciOncon una institucion financiera/banco. A fin de lograr este objetivo, los participantespodran:

Reconocer los principales tipos de instituciones financieras aseguradas

Reconocer terminos bancarios

Reconocer diferencias entre bancos y casas de cambio

Identificar empleados bancarios y sus posiciones

Identificar tipos de cuentas

Describir servicios bancarios

4 Curso Bancario Basic°FDIC Money Smart Plan de EducaciOn para Capacitacidn en Finanzas

Gu la del Instructor

Introduccion al CursoPauta para elinstructor

Instrucciones

Antes de comenzar Ia clase, entregue los siguientesmateriales a cada participante:

Guia del Participante

Cartel con el nombre

Lapiz o lapicera

$100 (dolares) en billetes de juguete

Sobre

Curso BancarioBasic°

=n111.1,.

Diapositiva 1

Muestre Ia diapositiva 1 (Curso Bancario Basico).

"iBienvenidos al curso Curso BancarioBaskol" Presentese (por ejemplo, mencione su nombrey su experiencia como instructor o banquero).

Explique: "Al tomar este curso, usted esti dandoun primer paso importante para establecer unfuturo financiero mejor para usted y su familia.Todo cornienza por entender los aspectosbasicos de las finanzas personales".

84

Curso Bancario Basic°FDIC Money Smart Plan de EducaciOn pare CapacitaciOn en FinanzasGula del Instructor

5

Pauta para elinstructor

Usted conoceni

luttensetlisl.aseguradasTdminos bancarios bdsicos

Diferencias entre bancos ycasas de cambio

Empleados bancarios y susposiciones

Tipos de cuentas

Servicios bancarios

Diapositiva 2

Instrucciones

Muestre Ia diapositiva 2 (Usted conocera).

Explique: "Al finalizar el curso, podran estableceruna relacion con una institucion financiera.Conoceran:

Principales tipos de instituciones financierasaseguradas

Terminos bancarios basicos

Diferencias entre bancos y casas de cambio

Empleados bancarios y sus posiciones

Tipos de cuentas, y

Servicios bancarios."

Muestre Ia Guia del Participante a Ia clase.

Explique: "Cada uno de ustedes tiene una copiadel Curso Bancario Basic° que contieneaspectos destacados del curso. Utilizaremosesta guia a lo largo del curso. Llevenla al hogary utilicenla como referencia."

85

Curso Bancario BasicoFDIC Money Smart Plan de EducaciOn para Capacitacion en Finanzas

Gula del Instructor

QuO Sabe Usted?Pauta para elinstructor

lnstrucciones

Explique: "Saquen Ia Ultima pagina de Ia Guia delParticipante, el formulario 4Que Sabe Listed?"

Explique: "El formulario 4Que Sabe Usted? Lespermite medir cuanto han aprendido en elcurso."

Lea las instrucciones y guie a los participantes en cadaafirmacion.

Explique: "Completen solamente la columnaAntes del Curso. Completarin Ia otra columnaal finalizar el curso."

Asigne suficiente tiempo para completar el formulario LQueSabe Usted? (1-2 minutos)

Haga que los participantes dejen estos formularios hasta elfinal del curso, momento en el que completaran Ia columnaDespues del Curso.

Transicion: "IComencemos por los aspectosbancarios basicos!"

Curso Bancario Basics)FDIC Money Smart Plan de Educaci6n para Capacitaci6n en FinanzasGula del Instructor

7

Introduccion a los BancosPauta para elinstructor

Instrucciones

Pregunte: "Cuando digo `banco' en este curso, eltannin," tambien incluye cooperativas decredit() e instituciones de ahorro. 4Que piensancuando escuchan Ia palabra `banco'?"

Escriba las respuestas de los participantes en Ia lamina depapel.

Explique: "Estas palabras reflejan como ustedesven a los bancos. Un banco es una entidad queofrece un lugar para guardar el dinero y empleasu dinero para hacer mas dinero.

Este negocio se denomina tambien unainstitucion financiera. Los bancos ofrecendiferentes servicios para guardar el dinero."

/I \

Guie una breve discusiOn de grupo formulando las trespreguntas siguientes para ayudarlo a comprender lasexperiencias y el entendimiento de los participantes sobresistema bancario basico.

Pregunte: "4Cuales han sido sus experienciascon los bancos?"

Pregunte: "E,Donde guardan su dinero?"

878 Curso Bancario Basic°

FDIC Money Smart Plan de Educaci6n para Capacitacidn en FinanzasGula del Instructor

Pauta para elinstructor

lnstrucciones

Pregunte: "i,Cuales son sus razones paraguardar el dinero en un banco?"

Escriba las respuestas de los participantes a la Ultimapregunta en una lamina de papel.

/I\Transicion: "Muchas personas guardan su dineroen bancos. Veamos algunas de las rezonespara guardar el dinero en un banco."

-1-0fr

J;

Curso Bancario BasicoFDIC Money Smart Plan de Educacion para Capacitacion en FinanzasGula del Instructor

9

Guarde su Dinero en el BancoPauta para elinstructor

Guarde su diner° en elbanco

ProteccianConvenienciaCostoSeguridadFuturo financiero

Fali

1Diapositiva 3

Instrucciones

Muestre Ia diapositiva 3 (Guarde su Dinero en el Banco).Muestre las razones una por una.

Relacione cada una de las razones con el debate de losparticipantes al comienzo del curso. Si los participantes nocubren todos los factores, suministre las respuestas quefaltan.

Responda:

Seguridad El dinero esta protegido contra robos,perdidas e incendios.

Conveniencia Pueden obtener dinero de manerarapida y facil.

Costo Usar un banco es probablemente maseconomic° que usar casas de cambio para cobrarun cheque.

Seguridad La cantidad asegurada basica de undepositante es $100.000. Esto significa que si poralguna razon el banco cierra y no puede devolver alos clientes el diner° que tenian en el banco, laFederal Deposit Insurance Corporation (FDIC porsus siglas en ingles) devolvera el dinero a losclientes.

Si un banco tiene el logo de la FDIC significa queesta asegurado por dicha corporacion. De igualmodo, Ia mayoria de las cooperativas de credit°estan aseguradas por Ia National Credit UnionAdministration (NCUA por sus siglas en ingles).

Futuro financiero Crear una relacion con un bancoestablece una trayectoria de pago de cuentas, puedeayudarle a ahorrar dinero y es necesario paraobtener un prestamo.

Transicion: "Durante esta conversacion hablamossobre las razones por las que deben guardar sudinero en un banco. Ahora hablemos sobre losdiferentes tipos de instituciones financieras."

8')10 Curso Bancario Basic°

FDIC Money Smart Plan de Educaci6n pare Capacitacion en FinanzasGufa del Instructor

Tipos de Instituciones FinancierasPauta para elinstructor

Tipos de institucionesfinancieras

Bancos

Cooperatives de credit()

Institutions de ahorro

Diapositiva 4

Instrucciones

Muestre Ia diapositiva 4 (Tipos de InstitucionesFinancieras).

Recuerde a los participantes que los terminos "banco" e"institucion financiera" se utilizan indistintamente en estecurso. Todos los tipos de instituciones estan reguladas porleyes estatales y federales.

Explique: "Existen tres tipos principales deinstituciones financieras:

Banco Una institucion financieraadministrada por leyes y reglamentosfederales y estatales.

Cooperativa de Credit° Una institucionfinanciera sin fines de lucro propiedad depersonas que tienen algo en comtin. Esnecesario ser miembro de Ia cooperativa decredit° para guardar el dinero alli.

Institution de Ahorro Un banco de ahorro ouna asociacion de ahorro y prestamo similara un banco. Las instituciones de ahorro secrearon a fin de propiciar la compra deviviendas por particulares y deben contarcon Ia mayor parte del patrimonio enprestamos para Ia vivienda."

Transition: "Independientemente del tipo deinstitucion financiera que utilise, todas usant6rminos bancarios basicos."

Cs 0

Curso Bancario Basic°FDIC Money Smart Plan de Education pare Capacitation en FinanzasGula del Instructor

11

Terminos Bancarios BasicosPauta para elinstructor

Instrucciones

Explique: "Saquen el sobre y billetes de juguete.

Ayude a los participantes a sumar el dinero. Escriba lostotales en Ia lamina de papel.

Explique: "Cada uno debe tener $100 (dOlares).

Dos billetes de $20 = $40

Cuatro billetes de $10 = $40

Tres billetes de $5 = $15

Cinco billetes de $1 = $5"

Explique: "El sobre representa una cuenta. Nopueden abrir Ia cuenta hasta despues de Iaverificacion de Ia misma. Hablemos sobre Iaverificacion de cuentas."

12 Curso Bancario BasicoFDIC Money Smart Plan de Educed& para Capacitacidn en Finanzas

Gula del Instructor

Pauta para el Instruccionesinstructor

Explique: "Antes de abrir una cuenta, Ia mayoriade los bancos estudiaran sus antecedentes enel uso de cuentas corrientes mediantecompariias como Tele Check o ChexSystems.Algunos bancos Ilevaran a cabo un informecompleto sobre su historial de credit() paradeterminar el nivel de riesgo.

La informacion sobre sus cuentas se obtiene deinstituciones financieras. Si tienenantecedentes de cheques rechazados o usoincorrecto de sus cuentas, las institucionesfinancieras tal vez se nieguen a abrirles unacuenta.

El banco necesitara su identificacion confotografia, en general permiso de conducir, y sunirmero de seguro social para verificar Iainformacion".

Explique: "Despues de que el banco determinaque son elegibles para abrir una cuenta,ustedes depositan el dinero en Ia cuentanueva."

9 2

Curso Bancario Basic()FDIC Money Smart Plan de Educacion para CapacitaciOn en FinanzasGufa del Instructor

13

Pauta para elinstructor

De bait°deptelfs &am p.m mgr. wow&

me ma Iola. de *glib.

51.4

193aragal.a.aapsa ''''.---'

.^:.'7:a....^. !...'

Diapositiva 5

Instrucciones

Muestre Ia diapositiva 5 (Deposito).

Explique: "Un deposit° es dinero que se agrega asu cuenta. Para agregar dinero a su cuenta, esnecesario completar una boleta de deposit°.

Una boleta de deposit° le dice al banco cuantodinero estan agregando a su cuenta.

Segim lo que depositen dinero en efectivo, uncheque de sueldo o un cheque girado sobre unbanco de otro estado - es posible que nopuedan utilizar los fondos inmediatamente.

Primero el banco debe asegurarse de que hayfondos en el banco de origen para cubrir suscheque. Pueden preguntarle al banco cuandopodran utilizar el dinero depositado."

Indique: "Ahora coloquen todo el dinero en elsobre".

Explique: "Acaban de hacer un deposito".

Saldo

Saldo es la cantidad de dineroque usted tiene en su cuentabancaria.

[El

Diapositiva 6

Muestre Ia diapositiva 6 (Saldo).

Explique: "Saldo es Ia cantidad de dinero quetienen en su cuenta bancaria".

BEST COPY AVAILABLE

93

14 Curso Bancario BasicoFDIC Money Smart Plan de Educacian para CapacitaciOn en Finanzas

Dula del Instructor

Pauta para elinstructor

Instrucciones

Pregunte: "lCual es el saldo?"

Respuesta: $100 (Mares)

Dibuje en una lamina de papel un cuadro de tres columnaspara seguir el saldo de transacciones futuras. Por ejemplo:

Descripci6n +1- Saldo

Saldo de apertura +$100 $100

Explique: "Al hacer un retiro, se saca dinero desus cuentas bancarias. El retiro se hacemediante un cheque, Ia entrega de una boletade retiro al cajero o usando un cajeroautomatico."

...

11,I

Muestre la diapositiva 7 (Retiro).

Explique: "Una boleta de retiro es parecida a unaboleta de deposito, con excepcion de que seretira dinero en vez de agregar dinero a Iacuenta.

Necesitan asegurarse de que no retiren masdinero del que tienen en su cuenta. Si lo hacen,estaran sobregirados o "el cheque serechazara" y se les cobrara una penalidad."

Retiro

Reimo . el prooeso de rebrar anew de= "'"'sBoletes

Cajaos aulonldbcal

Diapositiva 7

Indique: "Saquen un billete de $20 del sobre."

Explique: "Acaban de hacer un retiro."

94Curso Bancario BdsicoFDIC Money Smart Plan de Educaci6n para Capacitaci6n en FinanzasDula del Instructor

15

Pauta para elinstructor

Instrucciones

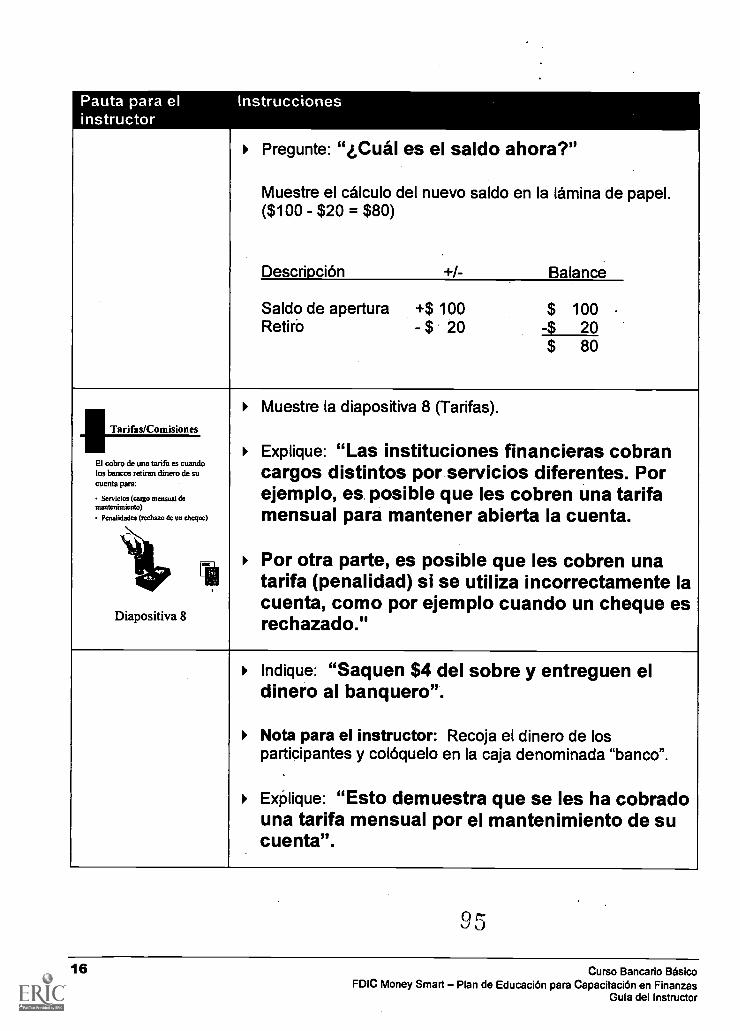

Pregunte: "lCual es el saldo ahora?"

Muestre el calculo del nuevo saldo en Ia lamina de papel.($100 - $20 = $80)

Descripcion +1- Balance

Saldo de apertura +$ 100 $ 100Retiro - $ 20 -$ 20

$ 80

Tarifas/Comisiones

El cobra de una tarifa es cuandolos bancos retiran dinero de sucuenta para:

Servicios (cargo mensual demantenimiento)

Penalidadcs (=haw de un cheque)

Diapositiva 8

I

Muestre Ia diapositiva 8 (Tarifas).

Explique: "Las instituciones financieras cobrancargos distintos por servicios diferentes. Porejemplo, es posible que les cobren una tarifamensual para mantener abierta Ia cuenta.

Por otra parte, es posible que les cobren unatarifa (penalidad) si se utiliza incorrectamente Iacuenta, como por ejemplo cuando un cheque esrechazado."

Indique: "Saquen $4 del sobre y entreguen eldinero al banquero".

Nota para el instructor: Recoja el dinero de losparticipantes y coloquelo en la caja denominada "banco".

Explique: "Esto demuestra que se les ha cobradouna tarifa mensual por el mantenimiento de sucuenta".

95

16 Curso Bancario BasicaFDIC Money Smart Plan de Educaci6n para Capacitacidn en Finanzas

Guia del Instructor

Pauta para elinstructor

InstruCciones

Pregunte: "lCual es el saldo ahora?"

Muestre el calculo del nuevo saldo en Ia lamina de papel.($80 - $4 = $76)

Descripcion +/- Saldo

Saldo de apertura +$100 $ 100Retiro - $ 20 -$ 20

$ 80ComisiOn - $ 4 44

$ 76

Muestre Ia diapositiva 9 (Interes).Interes

Explique: "Interes es dinero extra en su cuentaInter& es dinero extra en sucuenta =am:nice:LT

\\/1,.... a

que el banco paga por guardar el dinero en esebanco. Una de las ventajas principales de teneruna cuenta de deposit° es el interes que segana. I 9ollp

hil/

Diapositiva 9

Entregue $1 mas en billete de juguete a cada participante.

Indique: "Agreguen $1 a su sobre."

Explique: "Esto demuestra que la cuenta ganaintereses."

9b

Curso Bancario Basic°FDIC Money Smart Plan de Educaci6n para Capacitaci6n en FinanzasGuta del Instructor

17

Pauta para elinstructor

Instrucciones

Pregunte: "e,Cual es el saldo ahora?"

Muestre el calculo del nuevo saldo en Ia lamina de papel.($76 + $1 = $77)

Descripcion +1- Saldo

Saldo de apertura +$ 100 $ 100Retiro - $ 20 -$ 20

$ 80ComisiOn - $ 4

$ 76I nteres +$ 1 -±$1

$77

Pregunte: "e,Quien cambia cheques en casas decambio?"

Pregunte a un participante voluntario:

"i,Cuantos cheques cambian por mes?"

"4Cuanto les cobran por cheque?"

/ I \

Escriba las respuestas del participante en el margenizquierdo de Ia lamina de papel.

Si nadie ofrece informacion, utilice este ejemplo:

"Uno de los participantes en una clase anteriorutilizaba una casa de cambio para cambiar suscheques. Canjeaba cuatro cheques por mes ypagaba $5 cada vez.

Esto significa que pagaba $20 por mes (4 x $5)6 $240 por ano ($20 x 12 meses) solo porgirar/cambiar sus cheques."

9

18 Curso Bancario Basic°FDIC Money Smart Plan de Educacidn para Capacitaci6n en Finanzas

Guia del Instructor

Pauta para elinstructor

Instrucciones

Compare el costo total anual por utilizar una casa decambio contra utilizar los servicios del banco en el margenderecho de Ia lamina de papel.

"Otro participante tenia una cuenta en un bancoque cobraba un cargo mensual de $5, Ia cualincluia 8 cheques gratis por mes y utilizaciongratis del cajero automatic°.

Por otra parte, una caja de 100 cheques lecostaba aproximadamente $18, dado quecompraba los cheques por medio del banco.

En este caso, el use de una cuenta corriente lecostaba $78 ($5 x 12 meses = $60 + $18 = $78).lEsto equivale a ahorros de $162 ($240 - $78)por alio!"

Explique: "A pesar de que los bancos cobrancargos mensuales, estos ejemplos demuestranque es mucho mas economic° utilizar unacuenta de deposit° en un banco."

Transicion: "Entender estos terminos bancariosbasicos les ayudard a escoger el mejor tipo decuenta para ustedes. Hablemos sobre los tiposde cuentas."

98Curso Bancario BdsicoFDIC Money Smart Plan de Educaci6n para Capacitacion en FinanzasDula del Instructor

19

Depositos y Productos que no son de Deposit°Pauta para elinstructor

Instrucciones

Explique: "Las cuentas bancarias que leperiniten agregar dinero a la cuenta sedenominan cuentas de deposit°. Las cuentascorrientes y de ahorro son dos ejemplos deproductos de deposito".

Cuentas de de .6sito

Muestre Ia diapositiva 10 (Cuentas de Deposito).

Explique: "Una cuenta corriente es una cuentaque le permite mar cuentas o comprarmercancias. La institucion financiera retira eldinero de la cuenta y lo paga a la persona cuyonombre esti en el cheque. La instituciOnfinanciera envia un informe mensual de losdepositos y retiros realizados. Esto sedenomina un estado de cuenta bancario."

Cuenta corriente

Una cuenta que le pennite girarcheques para pagar cuentas ocomprar mercancias.

Cuenta de ahorroa cueUn nta que siempre gana

inteMs.

tDiapositiva 10

Explique: "Una cuenta de ahorro es una cuentaque siempre gana interes. No puede!), girarcheques en una cuenta de ahorro.

Pueden abrir una cuenta de ahorro con unospocos dolares, pero tal vez deba pagar unatarifa mensual si el saldo es inferior a unacantidad determinada.

El banco los ayudara a Ilevar un control de suscuenta mediante el envio de un resumen o Iaentrega de una cartilla denominada libreta dedeposito."

99

20 Curso Bancario BdsicoFDIC Money Smart Plan de Educacion para Capacitaci6n en Finanzas

Gufa del Instructor

Pauta para elinstructor

Instrucciones