report pfmrp joint supervision mission 17-28 … supervision report...kpa key policy action kra key...

TRANSCRIPT

REPORT

PFMRP Joint Supervision Mission

17-28 September 2012

November 20, 2012

2

List of Acronyms (Not exhaustive)

AccGen

Accountant General

AFROSAI-E African Organisation of Supreme Audit Institutions – English speaking Africa

BoT

Bank of Tanzania

CAG

Controller and Auditor General

CPAD

Commissioner for Policy Analysis Division

CSOs

Civil Society Organisations

DEV

Development

DFIMS

Director of Financial Information Management Systems

DGAM

Director of Government Asset Management

DPs

Development Partners

EFT

Electronic Fund Transfer

GBS

General Budget Support

GDP

Gross Domestic Product

GoT

Government of Tanzania

HCMIS

Human Capital Management Information System

IAS

International Accounting Standards

ICT

Information Communication & Technology

IFMS

Integrated Financial Management System

IMF

International Monetary Fund

IPSAS

International Public Sector Accounting Standards

ISSAI

International Standards of Supreme Audit Institutions

JAST

Joint Assistant Strategic Framework

KPA

Key Policy Action

KRA

Key Result Area

LGA

Local Government Authority

M&E

Monitoring and Evaluation

MDAs

Ministries, Departments and Agencies

MoF

Ministry of Finance

MoHSW

Ministry of Health and Social Welfare

MoNRT

Ministry of Natural Resources and Tourism

MTEF

Medium Term Expenditure Framework

MTSPBM

Medium Term Strategic Planning and Budgeting Manual

NAO

National Audit Office

OC

Other Charges

OI

Outcome Indicator

PAC

Public Accounts Committee

PAF

Performance Assessment Framework - General Budget Support

PBB

Program Based Budgeting

PEFA

Public Expenditure and Financial Accountability

3

PE

Procuring Entities

PFA

Public Finance Act

PFM

Public Financial Management

PFMRP

Public Financial Management Reform Program PMO-RLG

Prime Ministers Office - Regional Authorities and Local Government

PO-PSM

President's Office - Public Service Management

PPA

Public Procurement Act

PPRA

Public Procurement Regulatory Authority

RAs

Regional Administrative Secretariat

SP

Strategic Plan

TISS

Tanzania Interbank Settlement System

TR

Treasury Registrar

TRA

Tanzania Revenue Authority

TWG

Technical Working Groups

VFM

Value for Money

WB

World Bank

4

Table of Contents

1. SUMMARY AND INTRODUCTION ....................................................................................................................... 5

2. METHODOLOGY .................................................................................................................................................. 6

3. FINDINGS ............................................................................................................................................................. 6

PAF 2012 ....................................................................................................................................................................... 6

Key Results Areas – Status Report ............................................................................................................................ 9

KRA 1 Revenue Management ...................................................................................................................... 10

KRA 2 Budgeting and planning ..................................................................................................................... 11

KRA 3 Budget Execution, Transparency and Accountability ............................................................................ 12

KRA 4 Budget Control and Oversight ............................................................................................................ 13

KRA5 Change Management, Program Management and Communication ........................................................ 15

PMO-RALG ................................................................................................................................................ 16

4. SUMMARY AND COMMENTS ........................................................................................................................... 18

ANNEX A: PFMRP IV MONITORING AND EVALUATION RESULT FRAMEWORK 2012-2017 –September

2012 ......................................................................................................................................................... 19

ANNEX B: ToRs of the PFMRP Joint Supervision Mission 2012 ............................................................... 67

ANNEX C: Mission Participation from GoT (not exhaustive) ................................................................... 70

ANNEX D: Mission Participants From Development Partners ................................................................. 72

ANNEX E: Final meeting schedule ............................................................................................................ 74

ANNEX F: Draft terms of reference for PEFA study on Central and local level ........................................ 80

5

1. SUMMARY AND INTRODUCTION

PFMRP IV is the fourth phase of the Government of Tanzania`s PFM reform agenda and runs from July

2012 to June 2017. This report describes the findings of the first in a series of annual Joint Supervision

Missions intended to evaluate results being achieved, and where necessary revise strategic directions to

ensure effective delivery. The present review focuses on the first 3 months of implementation of PFMRPIV

and feeds into the annual GBS review via assessment of the PAF by 31 October.

The mission´s main observations are organised under five Key Results areas (KRAs) relating to: (i)

Revenue management (ii) Budget and planning (iii) Budget execution, transparency and accountability (iv)

Budget control and oversight and (v) Change management, programme monitoring and communication.

The joint assessment concluded that PFM reforms are making tangible progress. In regard to the PAF

2012 assessments, PFM as an underlying process has been rated as satisfactory with 90% achievement.

Three of four assigned KPAs were not achieved although work has been initiated on all KPAs and progress

will continue to be followed under the M&E framework. Three of the five PFM RP outcome indicators were

achieved while targets were not met for the remaining two.

The PFMRPIV M&E framework includes 160 detailed milestones. The majority of these were found to be

broadly on track where “on track” is defined as an activity that is planned and in process or that is

considered achievable based on the deadline established in the M&E. A small number have already been

achieved; others are considered to be at risk, in need of revision or delayed. Further details are contained in

the main body of the report and M&E matrix. A series of actions were identified during the mission that

require follow up by the Technical Working Groups within the respective KRAs.

Objective of the Supervision Mission

A Joint Supervision Mission of Phase IV of the PFMRP was successfully conducted from September 17th to

28th, 2012. The objective of the mission was to:

Assess progress against the jointly agreed General Budget Support (GBS) Performance

Assessment Framework (PAF) indicators,

Assess the implementation status of PFMRP under each Key Results Area (KRA) based on the

milestones that have been established in the Phase IV M& E framework

To identify issues, challenges and opportunities that needs to be considered or addressed in the

future in order to enhance and improve the PFM outcomes under each KRA.

To establish the dialogues within the Technical Working Groups for each Key Result Area (KRA)

and to establish the ongoing engagement of these groups as the focal point for the collaboration

and engagement between the DPs and the GoT component managers.

To develop the Terms of Reference for the 2012-13 PEFA Study (see draft tors in annex E)

6

2. METHODOLOGY

The Supervision Mission Team consisted of Government of Tanzania officials, members of the Development

Partners PFM Group, and the PFM DPG Secretariat. One consultant was engaged to coordinate and

facilitate the process. It was agreed that this Supervision Mission should not take the form of a performance

audit but rather it should be used as an opportunity to share knowledge, jointly assess progress, identify

challenges at an early stage, discuss and chart the way forward.

The documents used as guidance for the mission were the PAF 2012 Document together with the PFMRP

IV Strategy, its Monitoring and Evaluation Framework and the Operations Manual. A selection of other

documents including PEFA reports, recent CAG reports and recent IMF and WB reviews were also used to

inform discussions during the mission.

The mission activities were structured around the 5 Key Result Areas (KRAs) that are articulated in the

Phase IV Strategy and the Monitoring and Evaluation Framework.

The KRAs are as follows:

KRA 1: Revenue Management

KRA 2: Budget and Planning

KRA 3: Budget execution, Transparency and Accountability

KRA 4: Budget control and Oversight

KRA 5: Change management, Program Monitoring and Communication

Technical Working Groups (TWG) consisting of the key PFMRP Component Managers and DP

representatives have been formed under each KRA. The TWG will share the responsibility for their

respective Key Result Areas, under supervision of the PFMRP secretariat and leadership of the MoF

Permanent Secretary. The TWG discussions were the primary methodology used during the mission and

initial feedback from these meetings has been very positive. In most cases the discussions provided

valuable opportunities for learning and information sharing that was specifically directed at improving the

shared understanding on the status of key PFM reform activities together with any challenges and

constraints that are impacting performance. Discussions with other stakeholder groups including CSOs were

also conducted during the mission to ensure that the interests and representations of these groups were

considered in the review.

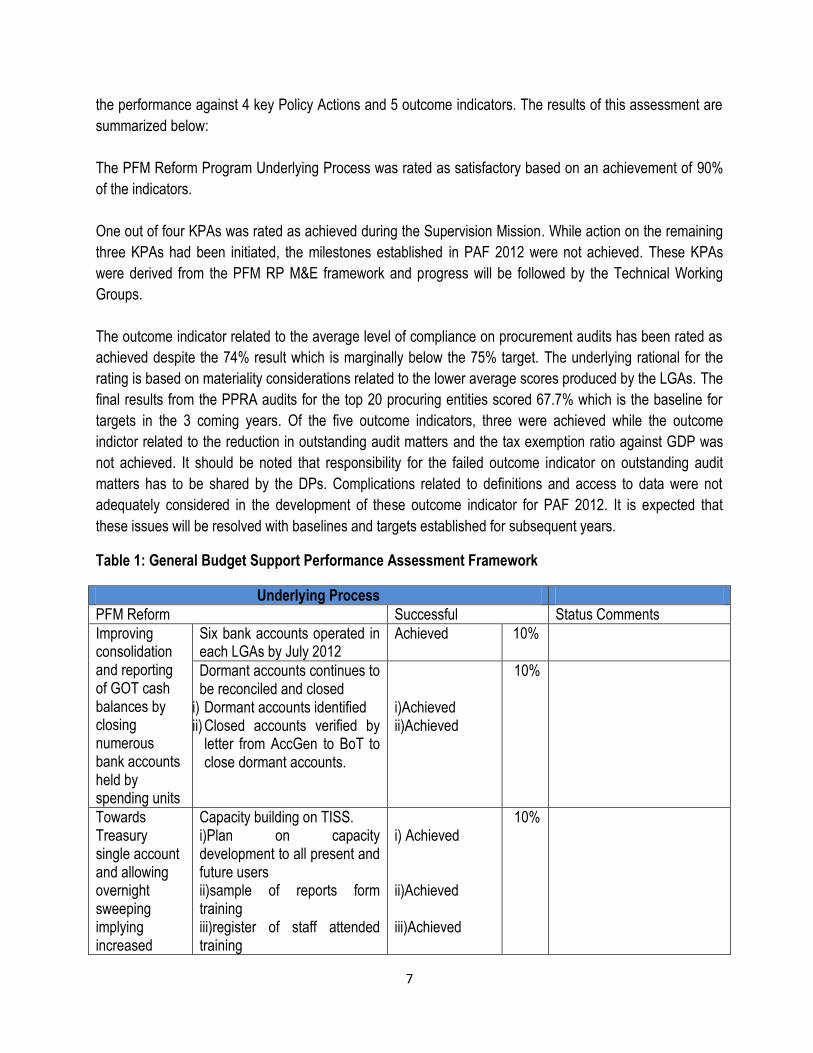

3. FINDINGS

PAF 2012

The assessments completed during this supervision mission will feed into the GBS Annual Review, including

the GBS 2012 Report. The assessment will include the rating of PFM as an underlying process together with

7

the performance against 4 key Policy Actions and 5 outcome indicators. The results of this assessment are

summarized below:

The PFM Reform Program Underlying Process was rated as satisfactory based on an achievement of 90%

of the indicators.

One out of four KPAs was rated as achieved during the Supervision Mission. While action on the remaining

three KPAs had been initiated, the milestones established in PAF 2012 were not achieved. These KPAs

were derived from the PFM RP M&E framework and progress will be followed by the Technical Working

Groups.

The outcome indicator related to the average level of compliance on procurement audits has been rated as

achieved despite the 74% result which is marginally below the 75% target. The underlying rational for the

rating is based on materiality considerations related to the lower average scores produced by the LGAs. The

final results from the PPRA audits for the top 20 procuring entities scored 67.7% which is the baseline for

targets in the 3 coming years. Of the five outcome indicators, three were achieved while the outcome

indictor related to the reduction in outstanding audit matters and the tax exemption ratio against GDP was

not achieved. It should be noted that responsibility for the failed outcome indicator on outstanding audit

matters has to be shared by the DPs. Complications related to definitions and access to data were not

adequately considered in the development of these outcome indicator for PAF 2012. It is expected that

these issues will be resolved with baselines and targets established for subsequent years.

Table 1: General Budget Support Performance Assessment Framework

Underlying Process

PFM Reform Successful Status Comments

Improving consolidation and reporting of GOT cash balances by closing numerous bank accounts held by spending units

Six bank accounts operated in each LGAs by July 2012

Achieved 10%

Dormant accounts continues to be reconciled and closed

i) Dormant accounts identified ii) Closed accounts verified by

letter from AccGen to BoT to close dormant accounts.

i)Achieved ii)Achieved

10%

Towards Treasury single account and allowing overnight sweeping implying increased

Capacity building on TISS. i)Plan on capacity development to all present and future users ii)sample of reports form training iii)register of staff attended training

i) Achieved ii)Achieved iii)Achieved

10%

8

usage of EFT and TISS

Progress against action plan on TISS connectivity to regions and Sub-treasuries

Achieved 10%

Steps Towards a comprehensive Debt Management Office

Debt management report from WB Debt management mission and action plan on steps towards establishment of Debt management office circulated before 1st of September 2012

Not Achieved 0% GoT have sent the draft report to WB in October requesting it to be finalised and are awaiting WB approval.

Submit request to Public Service Management for approval to Commission a new Debt management Department in the MoF

Achieved 10%

Progress towards a completed asset valuation of MDAs and RAs

i)Completed valuation of 16 MDAs ii)TOR for asset management policy approved by DGAM iii) 5 year plan for valuation of 34 MDAs approved by DGAM

i) Achieved ii) Achieved iii) Achieved

10%

PFM Reforms continues smoothly

Annual and end-report of PFMRP III

Achieved 10% The draft Annual and end report for PFMRP III has been prepared and approved for a positive rating. Revisions and adjustments have been agreed with dead-line attached

All Phase IV guiding documents are finalized/approved with 2012-13 annual work plan under execution

Achieved 20%

Key Policy Action

Interface central and local government ICT with technical control and new software acquisition, and all new software developed becomes centrally coordinated

Not achieved Procurement process expected to be finalised in November

Increase budget transparency and public access to key fiscal information

A) Budget Guidelines - achieved B) Executive Budget – not achieved C) Approved Budget - achieved

Achieved To note; C: Volume 1 not posted on webpage but available. Parliament decision inconsistent and GoT awaits corrective mandate. Citizen Budget published.

9

D) Citizen Budget – pending

Streamline and rationalize national systems and processes for intergovernmental transfers to LGAs

Not achieved Procurement process expected to be concluded in November.

The Government enhances domestic tax revenue (tax and non-tax) mobilization with better transparency and business environment

Not achieved The bill is formulated and in process but not submitted to parliament.

Outcome Indicators

Average level of compliance of:

i) All audited procuring entities and – ii) The top 20 procuring entities with the (revised) Procurement Act 2010

Achieved i) 74% (target 75%) ii) 20 top procuring entities

was 67.7%. The future compliance targets for the 20 top procuring entities will be as follows; FY 2012/13 : 71.1% FY 2013/14 : 74.5% FY 2014/15 : 77.9%

Non-salary (OC-DEV) funds released to RAS and LGAs by end Q3, as percentage of the Resources Available3 (OC+DEV) for the year

Achieved 60.1% of originally approved budget against target of 60%

Reduction in outstanding audit matters

i) Reduction in cases from last year ii) Targets for 2013 and 2014 by June – not met

Not met NAO reports that the data is available but not in desired format. The targets have not been set by GoT. It is recognised by DPs, NAO and GoT the development of this indicator has been more challenging than anticipated.

Domestic tax revenue + non-tax revenue as a share of GDP

Achieved 17. 5% against target of 17.6% (considered as achieved) for the purpose of this report.

Value of tax exemptions as a share of GDP

Not met 3,8% against target of 1,9%

Key Results Areas – Status Report

The following section provides an overview of the results of the Technical Working Group discussions within

each KRA. These discussions were guided by an agenda which included the review of PAF 2012 indicators,

10

the status of and progress achieved against the milestones set out in the M& E framework together with a

discussion of any challenges or obstacles that have been experienced by the component managers.

These findings are summarized in the chart below:

Note: 1. The X- axis represent the status on the implementation of milestones, where as the Y- axis

represent a number of milestones in the PFMRP IV M&E Result Framework.

2. On track refers to milestones that are in the process of being implemented or for which there is no

known impediments toward being achieved.

The detailed findings have been captured in the M&E framework which is attached as Annex A.

Where required in support of the PAF 2012 appropriate documentation has been collected and provided to

the PFM DPG secretariat.

KRA 1 Revenue Management

Strengthened systems, processes and procedures for improving the operational capability of the revenue collection by June 2017 Output 1.1 Improved quality of forecasting of fiscal aggregates for three years on a rolling basis

Output 1.2 The Government improves efficiency in domestic revenue mobilization both at the policy and the administration levels by updating legal instruments towards international best practices

Output 1.3 Strengthened capacity of local government authorities to collect revenue by 2015

Output 1.4 Increase of donor funding that flows through the exchequer system by 2016

11

It was jointly agreed during discussions that the milestones established for output 1.1 needs to be defined

further and the activity should be held in abeyance until clarification was obtained. The methodology for

training in revenue forecasting is under discussion however budgets will limit training in 2012.

The non-tax revenue study is in process and the draft report is being developed at this time. The Draft Tax

Administration Act has been submitted to the inter-ministerial committee for approval and is expected to be

submitted for cabinet approval in October. It is not expected that the bill will be submitted to parliament in

November. Some further definition of the longer term milestones attached to the non-tax revenue study will

be required.

The new TR Act is expected to be submitted to Cabinet in October. Once this bill is passed the revision of

Parastatal Acts can begin. TR’s capacity development plans which include much needed increased staff

levels and specialized training have been submitted for approval and needs to be reviewed in tandem with

act being approved.

Revenue training for PMO RALG staff appears to be on track. The LGA own source revenue study is yet to

begin. Training on own source revenue and the development of the own source database will follow on the

completion of the study. The review of the LGA Finance Act is underway but amendments will likely not go

to cabinet prior to June 2014.

The revision of the JAST II is underway but the December deadline for implementation of the new guidelines

will not be met. There is lack of clarity on the planned revision of the JAST II guidelines and further

discussion would be needed prior to completion. The report on the trends of donor project funds using the

exchequer system will be available in 2012 and each October thereafter – ahead of the target date.

The need to continue technical working group discussion involving multiple components were suggested by

several component managers and backed by the DPs. Challenges going forward includes sequencing of

activities (studies, legislative changes, capacity building and training etc.), identifying and quantifying

different sources of revenue at various levels, coordinating and standardizing training and harmonizing

revenue collection methods (at both central and local levels).

KRA 2 Budgeting and planning

Strengthened capacity of planning and budget management, including results and program based budgeting, within MOF, MDAs and LGAs by June 2017.

Output 2.1 Strengthened capacity of MDAs, RSs and LGAs in implementing program based budgeting by June 2016.

Output 2.2 Increased effective utilization of Planning and budgeting tools by 2016

Output 2.3 Strengthened capacity of LGAs for MTEF preparation by 2015

12

The Program Based Budget (PBB) action plan has been developed with support of East Afritac and is

currently in process of implementation. The definition of programs-/sub programs required for this process

have started and is well on its way and the chart of accounts has been modified with indicators extracted

from the MKUKUTA and five year development plans. PBB will be piloted in 5 MDAs. The plan to train

MDAs, RSs and LGAs staff on PBB has not been developed to date and will require a follow up.

The review of the MTSPBM, undertaken by a team of MDAs representatives, is projected to be completed

by February 2013 for application in 2013-14. The revision of the budget cycle, initiated by the PAC, is

waiting for cabinet approval and should be in place for budget year 2013-14. IMF East Afritac has provided

to GoT the recommendations to review the PFM legal framework. The government is still reviewing the

recommendations. Training on resource prioritization for RSs and LGAs started in 2012 with PMO RALG

involvement. During the mission it was jointly agreed that further discussion is required to clarify an

appropriate methodology for quality assurance on quarterly budget performance reports.

The development of ToRs by PMO - RALG for the in depth review of budget allocation formula had not been

initiated prior to the mission. This process will need to be accelerated in order to meet the proposed

December 2012 deadline. It should be noted that progress on this activity may be impacted by delays in

PMO- RALG’s access to basket funding.

While generally satisfactory progress is evident in all areas follow up discussions in the Technical Working

Group are recommended to ensure that there is appropriate engagement and division of labour between

PMO - RALG and other Ministries on the budget allocations, the transition to Programme Based Budgeting

and capacity development issues.

KRA 3 Budget Execution, Transparency and Accountability

Improved utilization of public resources in a more effective, efficient and transparent manner by June 2017

Output 3.1 Improved public procurement performance by PEs by 2015

Output 3.2 Strengthened public sector procurement by June 2015

Output 3.3 Strengthened capacity of MDAs, RSs and LGAs in Cash management by 2015

Output 3.4 Strengthened public debt management capacity by 2015

Output 3.5 Improved integrity and content of government financial statements and the migration from IPSAS cash to IPSAS accrual accounting for all government accounts is progressing in accordance with plans.

Output 3.6 Improved accountability in management of Government Assets for supporting migration to IPSAS Accrual

The results of annual procurement audits were published in Nov.2012 with an average compliance rate of

74%. The new compliance targets under output 3.1 are expected to be established in November 2012. The

13

development of new procurement implementation and monitoring tools and the dissemination of the new

procurement regulation is on track for completion by December 2012.

The Action Plan for implementing the PPD as per the Public Procurement Act (PPA) was completed. The

finalization of the PPA regulations and the development of the National Procurement Policy are on track.

The draft policy is expected by June 2103. Capacity development for the Procurement Policy Department

staff has not yet started but the ToRs for the training needs assessment have been completed and this

activity is on track for completion by June 2013. A database of procurement staff is in place.

The Acc Gen had completed cash management training for 200 staff. A total of 16,760 bank accounts have

been closed to date and an additional 8256 dormant accounts have been identified for closure. All LGAs

are using the prescribed 6 accounts for operations with effect from July 1, 2012.

The agreed action plan from the World Bank debt management review has not been formally shared;

however, actions are underway to establish the new unified debt management division. The proposed

structure of the new debt management office has been endorsed by the National Debt Management

Committee and is expected to be passed at the next meeting of the Civil Service Commission. No further

development activity can be completed until this approval is in place. The development of the national debt

management policy by June 2013 may be impacted if the approval is delayed. The MoF now maintains the

debt database.

The Accountant General’s plan for the transition to accrual accounting has not been shared but discussions

suggest that the activity is on track. Training at the MDAs level has started and all MDAs have been advised

to provide accurate closing balances for 2012 to support the first steps in the transition. The Accountant

General’s office confirmed that draft MDAs financial statements including the major accrual balances were

at hand. Valuation of asset to 36 MDAs have completed and assets for 20MDAs are already uploaded to

EPICOR and the completion of the remaining institutions is planned and considered on track.

Technical Working Group discussions with the Accountant General and CPAD should be scheduled for early

November in order to update the status on the major KRA 3 outputs.

KRA 4 Budget Control and Oversight

Improved adherence and enforcing of MDAs and LGAs to financial internal controls, rules, laws, regulations and audit recommendations by June 2017

Output 4.1 Increased coverage and quality of the internal audit functions by 2016

Output 4.2 Strengthened External audit functions by 2016

Output 4.3 Improved transparency on audit reports (central, local and Parastatal levels) to strengthen scrutiny and accountability.

Output 4.4 Improved performance of Parastatals by June 2016.

14

Output 4.5 Strengthened capacity of oversight functions of Parliamentary Accounts Committee in Tanzania Mainland

The internal Auditor General’s operational plan is awaiting approval and the process to develop the

necessary manuals and guidelines is on track and expected to be completed by June 2013. Surveys have

been undertaken to identify weaknesses in MDAs audit committees and the plan to acquire and pilot audit

software is on track and expected to be completed in 2014. A training needs assessment and plan was

completed and training of champions and senior management personnel is underway. Technical audits have

now been completed for 30 projects. Progress towards the amendment of the Local Government Finance

Act giving the IAG authority over the LGAs internal audit function should be followed by PFM RP as a critical

element for output 4.1

The report on the legal amendments required to move the NAO to AFROSAI level 3 is on track for

submission to the Attorney General by December. 2012. The plan to move 50% of the NAO staff to

independent accommodation is on track but challenges may develop as a result of increased staff numbers

and funding constraints. The NAO have completed five performance audits (VFM) this year and are well on

track to reach target on producing reports without external assistance. The training of auditors on IAS

standards, using a Champions group, is on track. The alignment of audit methodology with ISSAIs is also on

track for completion by June 2013.

The NAOs transition to the use of automated audit systems and software is on track with the completion of a

training needs assessment and the plan to activate four additional modules in TEAM MATE. Work on the

Citizen’s Audit reports by two CSOs is reportedly underway at this time.

The Treasury Registrar’s (TR) plan for the harmonization of Parastatals financial years and audit coverage

has not been completed to date. Follow up TWG discussions will be scheduled to ensure this activity is

supported and facilitated by the NAO and other stakeholders. The TR has selected 10 Parastatals to pilot

performance contracts and follow up TWG discussions will focus on the details of these contracts. TR has

started to input data into the Treasury Registrar Information System and plans to develop a monitoring

framework and compliance mechanism once the TR bill has been enacted.

It has been agreed that the output related to parliamentary committees and parliament office will be revised

following discussion with committee members in order to define PFMRP support that is coordinated with

other donor support programs.

Discussions confirmed that satisfactory progress has been made against most major milestones, but several

require further definition and the technical working groups should aim to meet regularly to clarify and

maintain momentum. A common understanding on how the value of outstanding audit findings is calculated

has not been reached but the NAO has agreed to set these out in writing and is committed to creating a

comprehensive database. Follow up meetings will be held with Donor Partners during October. Setting

15

targets for 2013 and 2014 – critical for the PAF - will require further discussion with NAO, the Internal Audit

General and Accountant General as a matter of priority

KRA5 Change Management, Program Management and Communication

Improved management practices with increased accountability and leadership to better manage performance of PFMRP by June 2017

Output 5.1 Coordinate Integration, interfacing and rationalization of Government financial systems.

Output 5.2 Utilization of EPICOR modules Increased from seven to ten

Output 5.3 All software development and module upgrades are coordinated with the overarching plans for ICT integration.

Output 5.4 Improved communication and public access to key fiscal information to stakeholders

Output 5.5 Coordination and Standardization of PFM Training Achieved.

Output 5.6 PFMRP component Managers are being guided by detailed multi-year operating plans.

Output 5.7 PFM activities are effectively planned and implemented

Output 5.8 Effective coordination of activities and support provided to the program implementers

Output 5.9 PFM Program oversight and review is being guided by clearly defined Milestones derived from an agreed M&E framework,

Output 5.10 All major PFM reforms have been coordinated with and informed by the relevant government and DP stakeholder groups

Output 5.11 PFMRP implemented efficiently and effectively through result based management approach.

Output 5.12 National systems and processes for intergovernmental transfers to LGAs Streamlined and rationalized

Output 5.13 Strengthened Public Financial Management Reforms in Zanzibar by 2016

KRA 5 includes a relatively diverse group of outputs related to the management of change within PFM RP,

the coordination and management of the program, ICT integration, LGA fund flow architecture and other

matters that have cross cutting implications. The PAF 2012 includes 2 KPAs related to the completion of the

first steps in the ICT integration (5.1) and fund flow (5.12) outputs. It is unlikely that either of these KPAs will

be achieved by the target dates.

16

The Technical Working Group discussions with the responsible component managers suggest that little

attention has been given to the sequential planning of activities under these outputs beyond the mapping

studies and follow up TWG discussions are required.

Outputs 5.5, 5.7 and 5.11 related to PFM, change management, strategic planning and Result Based

Management capacity development have been assigned to the MOF Human Resources department. The

TWG discussions with the Director suggest that activity planning for these outputs is complete and the major

milestones should be achieved on schedule.

The recruitment of the PFM secretariat (5.8) is well behind schedule but 4 of the 6 core positions are likely to

be filled by the end of October, 2012. The remaining 2 positions will have to be re advertised. It is

acknowledged that the secretariat personnel will come under significant performance pressure from the

outset and will require support and guidance to develop detailed work plans prior to the December, 2012. A

fully functional secretariat has implications for the whole program. In this regard the development of effective

internal / external communication and the execution of program coordination activities should receive

focused attention.

The leadership provided by the Planning Division, MoF, is a necessary element for the successful

implementation of the key outputs under KRA 5. The effectiveness of this leadership and the absence

PFMRP secretariat during the start-up period have been raised as a concern in most TWG discussions. It

was observed that the schedules of the senior program management personnel prevented them from

participating in the supervision mission. This restricted the time and scope of TWG meetings related to

program and change management. There is still opportunity to intensify the effort directed towards program

management and coordination in order to ensure the effective and timely execution of key KRA 5 activities.

Follow up TWG discussions with DFMIS, Planning Division and the Administration and Human Resources

Division within MoF should be scheduled for early November.

The incorporation of Zanzibar into PFMRP Phase IV will require further discussion between the relevant

Zanzibar and DP representatives. The PFMRP DPs have planned a review trip to Zanzibar in October,2012

to start the discussions with a view to identifying appropriate areas for support that are coordinated with

other donor support to PFM reform.

PMO-RALG

Representatives of the PFMRP supervision mission met with PMORALG staff in Dodoma in order to

improve the overall understanding of the current and potential areas of PFM RP’s engagement with PMO-

RALG and the LGAs. The major outcome of these meetings was an acknowledgement that current support

levels do not reflect the levels of funding that needs to be directed to PMO RALG in order to support their

PFM reform initiatives. It was agreed that the PFMRP would conduct follow up discussions with PMO- RALG

in order to develop a more appropriate funding and activity plan. It was further recognised that consultation

and coordination with PMO-RALG on PFMRP IV activities that have a direct or latent impact on LGA

operations requires improvement. The TWG discussions with PMO RALG should include Planning Division,

17

PMO- RALG and representatives from the relevant Central Government Departments and should be

scheduled to get underway by mid-November at the latest.

Technical Working Groups

The TWG discussions confirmed that the PFM component managers under KRAs are engaged and working

towards the achievement of the PFM objectives that have been defined in the M&E framework. These

discussions also confirmed the underlying value of the TWGs as the format for the continued engagement

between PFMRP DPs and the individual component managers. There are a number of clear gains for both

the component managers and the DPs in using these groups strategically to keep the reform on track and to

keep essential information channels open so that the broader DP community has more up to date access on

PFM Reform progress and issues. This will require that the both the DPs and the GoT ensure the continuity

of the TWG members and it is recommended that TWG membership be formalized under each KRA. The

counterpart managers identified the need to periodically widen TWG discussions to include the component

managers that are engaged in common and interrelated activities.

Program Management - Coordination

The coordination of the PFMRP Phase IV program has been raised as an issue in discussions with the

component managers and amongst the DPs. The issues that have been elevated during the mission focus

on the weak planning and execution of essential program coordination activities including communication

and collaboration amongst the stakeholders, the preparation of activity and financial reports and the

dissemination of PFMRP IV documents and manuals to the stakeholder group. A number of component

managers expressed frustration regarding accessing fund in the first quarter.

It is recognized that starting implementation of PFMRP phase IV requires the presence of a new PFMRP

Secretariat to be in place by 1st July 2012. The absence of PFMRP Secretariat has been a challenge for the

GoT in implementing PFMRP IV. Efforts to recruit PFMRP secretariat is at final stages and thus it is

expected that PFMRP IV will be smoothly implemented after that secretariat has been put in place. In order

to address communication challenges encountered in the previous phases, the new secretariat will have a

communication specialist responsible for communicating and liaising with different stakeholders on PFMRP

interventions and achievements.

Donor Coordination

Discussions with the component managers and senior officials have confirmed that the Donor community is

not doing enough to internally coordinate their activities within the overall scope of PFM reforms. The

overlap of missions, each of which creates time demands on the same PFM component managers has been

recognized as a problem. Issues have also been identified with donors moving ahead to develop and plan

PFM reform activities without reference to the joint PFMRP program group. This has obvious implications for

18

duplication of effort and the overall cohesion of PFM efforts. There is a similar issue related to the provision

of technical and advisory supports to PFMRPs component managers that ultimately lead to action plans.

These plans are not being communicated or shared with PFMRP so that they can be coordinated with or

factored into the existing program structure and the M&E framework. The correction of this weakness will

require the coordinated effort of all DPs in different sectors.

4. SUMMARY AND COMMENTS

The review of progress against the M&E framework would suggest that PFMRP Phase IV started fairly. The

TWG discussion confirmed that component managers are engaged, activities have been defined and work

is underway to advance the key PFM agendas under most KRAs. At the same time the volume of work that

is scheduled for completion in the next 12 to 24 months is quite ambitious. It is important to note that a

number of the key PFM reform initiatives are dependent on the amendment of Acts which require approval

of the Parliament. The parliament being an independent organ with its procedures of approving different acts

and such procedure can not be questioned by the Government.

Discussions also highlighted that the complexities of some PFM initiatives may not have been fully reflected

in the M&E framework and adjustments will be required to more accurately define the milestones and

schedule associated with these initiatives. The broad scope of the PFM program remains a concern in terms

of programme coordination and management, resources mobilization to finance programme activities and

linkage with interrelated reforms. Program coordination and the early identification of emerging challenges

will be critical to ensuring that the momentum of the major cross cutting initiatives is maintained.

The continued strengthening of PFM systems is a critical element for Accountability, Transparency and

ultimately Good Governance. As such, the overall performance of PFMRP as a reform program and the

results that it produces will continue to be under close scrutiny by Government and Development Partners. It

is important that PFMRP strengthens its collaboration with different stakeholders to build and sustain

momentum on PFM reform agenda.

Given the slow start up on some of the activities, the review of progress at the mid year will help to identify if

there is any improvement in the areas highlighted in this report.

5. ANNEXES

ANNEX A: PFMRP IV MONITORING AND EVALUATION RESULT FRAMEWORK 2012-2017 –September 2012

KRA 1 Revenue Management:

Strengthened systems, processes and procedures for improving the operational capability of the revenue

collection by June 2016

Outputs Performance

Indicators

Indicator Baseline

2011

Indicator Target 2017 Milestones Comments from

Supervision Mission

2012

Output 1.1: Improved

quality of forecasting of

fiscal aggregates for

three years on a rolling

basis

Aggregate revenue

out-turn compared

to original approved

budget (PEFA: PI-3)

Actual domestic

revenue collection was

below 92% of

budgeted domestic

revenue estimated in

no more than one of

the last three years.

(PEFA: C)

Actual domestic

revenue collection is

below 94% of budgeted

domestic revenue in no

more than one of the

last three years. (PEFA:

B)

Study on forecasting targets and actual revenue collection by June 2013

Needs to be revised. The mission agreed that there is a need to review Output 1.1 (June 2013) (no budget envisaged) and that there is a need for additional and solid milestones and activities to be formulated. There is a general need for capacity building in terms of forecasting also within MoF. There is also room for improvement on the Non-tax revenue forecasting.

20

Recommendations from study on forecasting targets and actual revenue collection informs budget preparations for budget 2014/15.

Subsequently to be revised. One element to be considered is a revision of the model used by MoF to capture both newer aspects within tax such as regional elements and the non-tax elements.

Increase in number

and quality of

participating MDAs

and LGAS with staff

capable providing

accurate, realistic

revenue projections

Less than 5% of

participating MDAs

and LGAS providing

accurate, realistic

revenue projections in

2010/11

50% of participating

MDAs and LGAS

providing accurate,

realistic revenue

projections by 2017

A team of trainers in revenue forecasting developed by June 2014 (milestone to be reviewed in line with recommendations from the study)

On track – target within reach. Priority will be given to those MDA’s with higher revenue potential (5 MDA’s suggested to be chosen (including MEM and MNRT). Training for LGA’s is also found to be very important, but potentially also costly. With limited resources, there is need for prioritization and possibly sequencing on LGA level.

Output 1.2: The

Government improves

efficiency in domestic

revenue mobilization

both at the policy and

the administration

levels by updating legal

instruments towards

Increase in collection

of Total and non-tax

revenues as

percentage of GDP

Total revenue

collection was 16.5 %

of GDP in 2010/11

Non-tax revenue was

1.2% of GDP in

Total revenue collection

will be at least 17.8% of

GDP by 2013/14-

Non-tax revenue will

be at least 1.9% of GDP

by 2013/14

The study on Non Tax Revenue (NTR)-“Integration and Harmonization of Revenue Collection Systems” completed by November 2013.

On track. Non-tax revenue study is progressing. An inception report has been discussed with key stakeholders (income-generating MDA’s). The actual report is under development.

21

international best

practices

2010/11

Submission of a bill to Parliament to enact Tax Administration Act for the purpose of establishing a common tax procedure among different taxes collected by Tanzania revenue authority (TRA) by November 2013

Review Laws, rules and Regulations for Local Government revenue system to improve LGA’s own sources in line with best practices by June, 2016.

Take policy action to improve revenue mobilisation from natural resource sectors by June 2014

At risk. Cabinet approval process is on-going. Currently submitted to Inter-ministerial Technical Committee (Permanent Secretaries) awaiting a date for discussion. Expect Cabinet approval mid-October with the aim of submitting a draft Act to Parliament in November. Before this can happen, it needs to go through the Attorney General.

The review of LGA legislation is treated below in output 1.3.

On track –target within reach. Policy action on non-tax revenue – to be defined. This does not necessarily have to stem from non-tax study as this deal with collection. Relevant actions should be discussed with MNRT, where many initiatives are already

22

The action plan to implement the recommendations from review of non tax collection developed and implemented by 2016

Computerised revenue collection to at least 50% of participating MDAs and LGAs by 2016

on-going.

On track – target within reach. Agreed to include an interim milestone in order to track progress, so that the action plan should be developed by June 2014, while implementation of the plan is still assessed in 2016.

Needs to be revised. Computerization: needs a clearer definition. MDA’s and LGA’s clearly found a need for increased use of ICT as collection method. The non-tax study partly addresses the issue and the milestone could therefore be revisited once the study is finalised and the action plan developed. MNRT are already planning a pilot in this area and lessons should be drawn from this.

Increase in Revenue

from Parastatals as

percentage of

Approved domestic

Revenue from

Parastatals was 0.55 %

of total approved

domestic revenue

Revenue from

Parastatals will be 4%

of total approved

domestic revenue

New TR's Bill presented to the Parliament by June 2013

On track. The final draft Bill is being submitted to Cabinet in October. Aim for presenting the Bill to

23

revenue collection

collection in 2010/11 collection by June 2014

150 Parastatals’ Acts Reviewed to be in line with the New TR Act by June 2014

TR’s Office Capacities enhanced by June 2014

parliament in October (or February if October is not possible).

On track. The Review of individual parastatal Acts begins after the Bill is passed. Several pieces of legislation have been identified as needing revision after the Bill is passed. This will begin shortly after. The need for early planning and budgeting of such activities was underlined.

At Risk. Capacity building at TR (human and office) was recognised as a priority and a big task. TR has currently 56 staff but the organisational structure provides for 205. It is acknowledged that this cannot happen at once due to limitations in terms of salary, office equipment etc. There are plans for 50 this year, but it still needs central approval.

24

M& E system for Parastatals reviewed and implemented by June 2015

Training of new and existing staff (mainly in specialised functions) was also underlined. There is need for highly specialised training as well as more routine training. The need for a long-term capacity development and training plan was underlined. Further, an overview should be provided of what is realistic in terms of hiring, training and equipment this FY year.

On track – target within reach

Tax exemptions as a

percentage of GDP

2.2% Target :

2012 ; 1.9%

2013; 1.6%

2014: 1.2%

Review the current system of tax exemptions with the value-added Tax (VAT) regime and amend the VAT Act with a view to be in line with international best practices by

On track. The process of amending the VAT act is progressing. TA is provided by IMF. A mission in July will be followed up by a mission in October working on the revised Act. The Act is expected to be

25

November 2014 approved by cabinet by November 2013. It is recognized that incorporation of changes in the FY 2014 budget will be unlikely. It has further been decided to conduct a broader PER on the costs and benefits of tax exemptions. This study will probably be available from March 2013 to feed into the 2013/14 budget.

Output 1.3:

Strengthened capacity

of local government

authorities to collect

revenue by 2015

Local Government

Own source revenue

to GDP

Actual revenue

collection by LGAs

2010/11: Tsh 158,280

million and 0.46 % of

GDP

Local Government Own

source revenue will be

1.5% of GDP

Completed assessment and evaluation of revenue potential for all major own sources of revenue to all LGAs by June 2013

PMO - RALG staff and Finance Management Officers at RS to be trained in tax revenue plans and budgets to spearhead LGAs tax

At risk. The assessment of revenue potential was found to be crucial. ToRs should be drafted soon. Due to limited budget, it may not be possible to assess all sources in all LGA’s, so a representative selection should be considered to begin with.

On track. PMORALG is in contact with TRA about using consultants from the Tax Training Institute to carry out the training in revenue plans and budgets.

26

reviews and reforms. June 2013

Local Authorities Tax administration teaching and practice modules established and TOT completed for all finance management staff at the regional level. June 2013.

Four (4) Revenue Accountants, 3 Council management team members and 1 FMO from each LGA and RS are trained on own source revenue management by June 2014.

Establishment of known and clear revenue database by each source of revenue, presence of trained

Budget constrains might put the milestone at risk.

At risk. No update was given concerning the training modules and TOT.

Need to be revised. The planned training on own sources of revenue will only start after the study/assessment is done. However it is already in the budget for this FY – agreed that is should be removed and money can be spent on other activities, i.e. the study. Step-by-step approach is envisaged and should be reflected in AW&B: Study Train PMORALG and RS Develop training modules Train LGA.

On track. The database

is supposed to be

developed based on

the study and

encompass i.e.

sources, rates,

27

personnel and a clear follow up arrangement at PMORALG and RS levels by June, 2014.

potentials, budget,

and collection

methods.

Local Government

legislation reviewed

by 2016 (Act No. 7, 8

and 9)

The last amendment of

the Local Government

Finances Act No.9 of

1982 was done in year

2002. The act does not

adequately address

issues of equity,

change of technology

and other

administrative issues

to enhance local

revenue mobilization

considering the

present and future

LGAs circumstances.

Local Government

Finances Act No. 9

reviewed by 2014

Completed study on the effectiveness, relevancy and sufficiency of the provisions of the Local Government Finances Act No. 9 by June, 2013.

A bill for an act to amend the Local Government Finances Act No.9 of 1982 is finalized and submitted to the Cabinet by February, 2014

On track. This FY the review of Local Government Finance Act ongoing.

At risk. The discussions concluded that the actual amendments will probably not go to cabinet before June 2014. Stakeholder workshops will be very important.

Output 1.4: Increase of

donor funding that

flows through the

exchequer system by

2016

Percentage of

disbursement of

direct project fund

portfolio via the

exchequer

20% 50% National framework for managing development co-operation (JAST) reviewed and put in operation by December 2012

At risk. The JAST II process is rolling. A draft concept note expected in October to be discussed among key stakeholders after which a draft JAST II will be developed and presented for broad consultations. Final draft is expected to need cabinet

28

Revised JAST and AMP user guideline clearly communicated to both parties by December 2012

Analysis of trends of the direct project fund portfolio disbursed via the exchequer system published and shared annually by June 2015

approval. The discussion concluded that the deadline December 2012 will probably not be met (June 2013 more likely).The output/ target might need to be revised.

To be revised. The content of the proposed revision of JAST and AMP needs to be further defined and milestone should possibly be split into two separate activities – one is the AMP guidelines, which are updated every year and needs to continuously be disseminated to DP’s, MDA’s, LGA’s, RS’s, NSA’s etc.

On track. The annual report of trends will be available already this year (target was 2015) as it can now be generated from the AMP and published every year in October.

29

KRA 2 Budgeting and planning:

Strengthened capacity of planning and budget management, including results and program based budgeting,

within MOF, MDAs and LGAs by June 2016.

Outputs Performance Indicator Indicator Baseline

2011

Indicator Target

2016

Milestones Comments from

Supervision Mission

2012

Output 2.1:

Strengthened

capacity of MDAs,

RSs and LGAs in

implementing

program based

budgeting by June

2016.

Presence of Programs-based

budget classification (PI-5)

The 2008/09 budget

formulation and

execution is based

on administrative

and GFS –

compatible

economic

classification. There

is no CoFoG-based

functional

classification and

budget

documentation and

reporting system

(PI-5C)

The budget

formulation and

execution will be

based on

administrative ,

economic and

functional

classification

(Using at least the 10

main CoFoG

functions), using

GFS/CoFoG standards

or a standard data can

produce consistent

documentation

according to those

standards

All sub programs, objectives and performance indicators defined by Dec 2012

Chart of accounts Modified to accommodate program based budgeting by August 2013 (ACCGen)

MTEF reviewed to make program based budget compatible by

On track. Programs and sub-programs have been (tentatively) defined and indicators are fed in by strategic documents like MKUKUTA II and FYDP. The MoF, MoE, MoHSW, MoAgr and MoW will be piloted.

Achieved

On track - target within reach

30

(PI-5B) September 2014

Progress on the PB Action Plan implementation

On track. Action Plan to move to PBB (Program Based Budgeting) is in place and the work has started. PMO RALG and LGAs representatives are in the process of being included into the work as this has not been initiated yet. The LGAs autonomy in the budgeting process needs to be preserved and needs to be recognised. DPs and GoT agreed to have a follow up meeting on PBB.

Increase in number of MDAs and

RSs with skilled staff for

implementing a program based

budgeting

In 2011, there are

no staff in MDAs and

RSs with necessary

skills to implement

program based

budgeting

95 % of MDAs and RSs

have staff with

necessary skills to

implement program

based budgeting

Completed phased training for all MDAs and RSs by 2014

Completed phased training for all LGAs by 2014

On track. Training involving staff from MDAs, RSA and LGAs are programmed.

On track. Synergies can be sought with LGRP II.

Output 2.2:

Increased

effective

utilization of

Planning and

budgeting tools

Percentage increase in number

of MTEF budgets meeting the

MTSPBM requirements by 2016

In 2011, less than

75% of MTEF

budgets are meeting

the standards of

MTSPBM

98% of MTEF budgets

are meeting the

MTSPBM standards

MTSPBM reviewed by June 2013

On track. MTSPBM is planned to be reviewed to accommodate the FYDP. A National facilitation team is to undertake the

31

by 2016

Sixty MDAs, 21 RSs and 133 LGA trained in MTSPBM by June 2014

Reviewed MTSPBM to be applied during FY 2013/14

Annexes to budget book volume II for Executive Agencies completed by June 2014

review. It consists of representatives of MoF, PoPSM, PMO RALG, PM Office, Planning Commission. The work has not started but GoT is confident it will be finalized by February 2013.

On track. Review will be followed by change of manual and training of stakeholders. Training will be done by facilitation team;

On track. Application of new MTSPBM in FY 13/14 is foreseen.

On track. GoT will introduce more details on expenditures of public institutions that partially depend on GoT budget such as TRA, University, etc

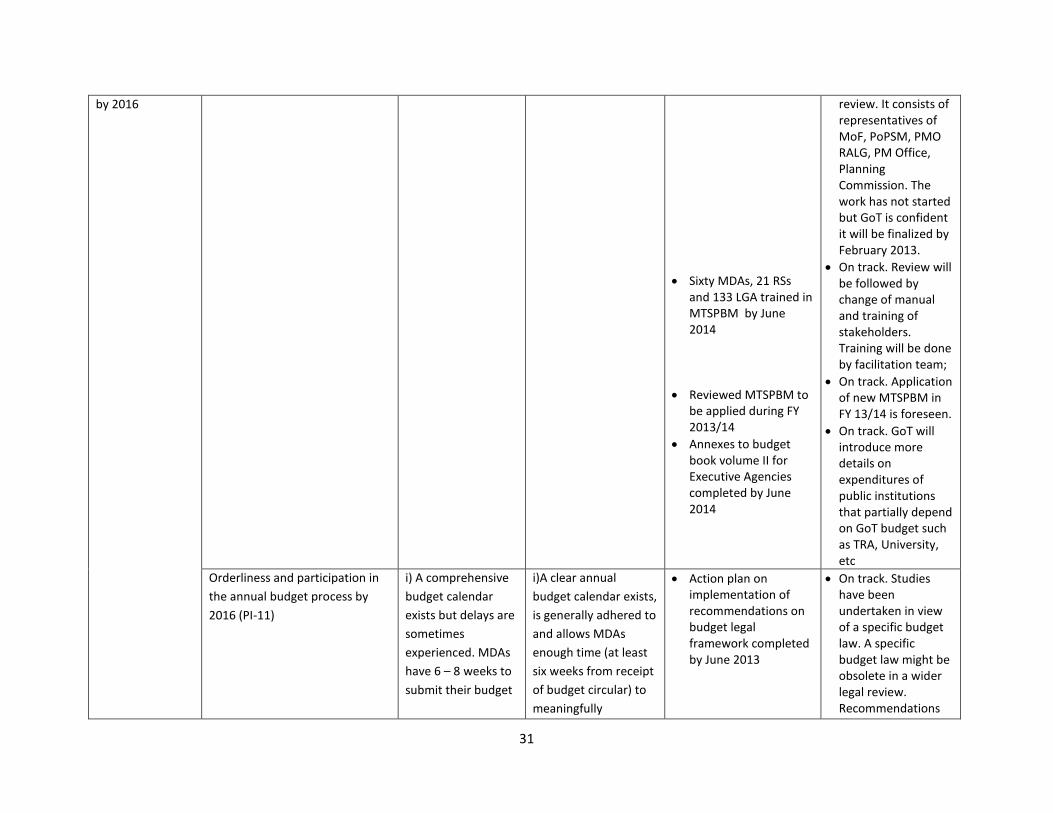

Orderliness and participation in

the annual budget process by

2016 (PI-11)

i) A comprehensive

budget calendar

exists but delays are

sometimes

experienced. MDAs

have 6 – 8 weeks to

submit their budget

i)A clear annual

budget calendar exists,

is generally adhered to

and allows MDAs

enough time (at least

six weeks from receipt

of budget circular) to

meaningfully

Action plan on implementation of recommendations on budget legal framework completed by June 2013

On track. Studies have been undertaken in view of a specific budget law. A specific budget law might be obsolete in a wider legal review. Recommendations

32

ii) A comprehensive

budget circular and

budget preparation

guidelines are issued

but the MDAs

ceilings are not

always approved by

cabinet before issue

(B)

completes their

detailed estimates on

time

ii) A comprehensive

and clear budget

circular is issued to

MDAs which reflect

ceilings approved by

cabinet or equivalent

prior to the circular

distribution to

MDAs(A)

At least 10 PER Main Dialogue meetings held by June 2016

on legal review have been submitted by AFRITAC.

On track. PER Main dialogue process has started.

Percentage reduction in

deviation of actual expenditure

from approved budget

In 2011, the

percentage of

deviation of actual

recurrent

expenditure MDAs

budget at vote level

compared to

approved budget

but excluding salary

adjustments,

contingency and

debt service was at

13.7%

Actual expenditure

deviated from

budgeted expenditure

by an amount

equivalent to not

more than 10%

Phased training to MDAs, RSs and LGAs Budget Committees on resource prioritization and planning

On track. Training was done to selection of RS and LGAs in 2012 on how to plan and implement.

Quality and timeliness of in-year

budget report (P-24) by 2016

Comparison to

budget is possible

only for main

administrative

headings.

Expenditure is

Classification allows

comparison to budget

but only with some

aggregation.

Expenditure is covered

at both commitment

Mechanism for quality

assurance of

Quarterly Budget

Performance Reports

(level of detail,

At risk: It was agreed to take PEFA study 2009/10 and PEFA methodology paper as starting point for coming discussions.

33

captured either at

commitment or at

payment stage (not

both)

Reports are

prepared quarterly(

Possibly excluding

first quarter), and

issued within 8

weeks of end of

quarter

There are some

concerns about the

accuracy of

information, which

may not always be

highlighted in the

reports, but this

does not

fundamentally

undermine their

basic usefulness (C+)

and payment stages.

Reports are prepared

quarterly and issued

within 6 weeks of end

of quarter

There are some

concerns about the

accuracy, but data

issues are generally

highlighted in the

reports and do not

compromise overall

consistency/usefulness

(B)

timeliness, accuracy,

consistency and

usefulness to decision

makers, as well as for

budget transparency

to citizens)

established by June

2013

Follow up meetings are foreseen.

Output 2.3:

Strengthened

capacity of LGAs

for MTEF

preparation by

2015

Comprehensiveness of

information included in budget

documentation (PI-6)

Currently there no

sufficient

information on LGAs

revenue planning

and budgeting

which is included in

the budget

documentation.

Supportive and

verifiable revenue

data and information

to be included in the

LGAs budget

documentation.

Proposal for budget information to be included in the Budget guideline to be submitted to National Budget Guideline committee by October annually.

Recommendations

To be reviewed.

At risk (Sequence

34

of various studies on LGAs budget allocation formulas reviewed by December, 2012 which will include recommendations to be made by the fiscal decentralization taskforce in LGRPII by June 2014. The M&E framework under LGRPII included performance indicator to measure application of formulae based allocations to actual fund transfers.

Agreement on improvement of

needs to be revised). The revision and full application of LGA budget allocations formulas is a challenging process involving numerous stakeholders (MoF, PMO-RALG, sector ministries, PO-PSM). From the discussions, it was confirmed that PMO-RALG is expected to initiate the process through a consultancy. PMO-RALG would then prepare a Cabinet paper recommending formal approval. It was recognised that ToRs for such study should be prepared urgently in order to achieve PFMRP IV milestone. The ToRs should take into account the intended transition to PBB. Access to funding from the basket for this activity has been delayed.

On track pending above actions.

35

LGAs budget allocation formulas among the Sector Ministries (PMO-RALG, MOF, PO-PSM and Sectors) completed by June, 2013

Various studies in fiscal transfers

and decentralization process in

Tanzania indicates that Budget

allocation to LGAs reflects a more

inequitable distribution of

resources to LGA, and that the

allocation formulae are not fully

applied. There is a need to revisit

all the existing budget allocation

formulae to clearly reflect

equitable allocation of financial

resources by June 2016.

Currently budget

allocation formula

follow, population,

land area and

poverty level,

Budget allocation

formula reflects

resource needs,

distances from service

facilities, special area

diseases, number of

projects to be

implemented, number

of orphans etc.

All LGAs budget allocation formulae reviewed by June, 2014

All reviewed LGA budget allocation formulae applied in the budget preparation during 2014/15 for the FY 15/16 budget.

Monitoring arrangements in place for measuring deviations in actual releases against all formula-based allocations to LGAs for FY 15/16.

All on track pending actions above.

KRA:3 Budget Execution, Accountability and Transparency:

Improved utilization of public resources in a more effective, efficient and transparent manner by June 2016

Outputs Performance

Indicator

Indicator Baseline

2011

Indicator Target

2016

Milestones Comment

36

Output 3.1:

Improved public

procurement

performance by

PEs by 2015

Average level

of compliance

of i) all

procuring

entities (for

follow-up

audits) and ii)

the top 20

procuring

entities with

the (revised)

Procurement

Act 2011

Competition,

value for

money and

controls in

procurement

(PI – 19)

Old target

(63%+75%)/2=68%

i. 66 % of tenders under open tendering process were advertised in fiscal year 2006/2007 (B)

ii. Using less competitive procurement methods is allowed with justification. PPRA audits in 2008/09 show that the great majority of contracts now use the correct methods (B)

iii. A comprehensive complaints mechanism operates, but for unknown reasons the number of complaints has declined (B)

Target will be

based on new set

of indicators +20%

of baseline (new

BL by October

2012)

i) Accurate data on the method used to award public contracts exists and shows that more than 75% of contracts above the threshold are awarded on the basis of open competition(A)

ii) Other less competitive methods when used are justified in accordance with clear regulatory requirements (A)

iii) A process (defined by legislation) for submission and timely resolution of procurement process complaints is operative and subject to oversight of an external body with data on resolution of

Annual PPRA audit results confirm positive trend on a yearly basis

Revised procurement implementation and monitoring tools issued by December 2013

New Public Procurement Act, 2011, Regulations and Tools disseminated to major PEs and other key stakeholders by December 2015

Procurement plans aligned with MDAs, LGAs and parastatal Institution Strategic plans by June 2015

Value for money procurement enhanced through Framework contract in procurement of common use items and services by June 2017

PPRA operational and outreach capacity strengthened by June 2014

On track. Apparently annual audit results indicate positive trend based on compliance and Value for money audits. Final figures due in October.

On track, implementation and monitoring tools to be in place after the on-going new audit report is ready and being approved by the end of 2012.

On track, Procurement Regulation will be out at the end of 2012 and in 2013/14 PPRA will plan for milestones. New Public Procurement Act, not yet in use; it is waiting for regulations to be approved. But, expect to be ready by late 2013.

On track. It has been made mandatory that Public Procurement Plan to be part of Strategic Plan and Budget Plan.

On track. The on-going Audit has conducted Value for Money Audit for 30 PE. The final report of the referred audit will inform on the progress

On track. There is on-going recruitment of staff and providing training to existing staff. Moreover,

37

complaints accessible to public scrutiny (A)

PPRA expects to open new zonal offices and employ up to 141 staff from current 52 staff. The Government has set aside budget to recruit PPRA staff

Increase in

number of PEs

using e-

procurement

system (PMIS)

Currently, 203 PEs are

using PMIS

(Procurement

Management

Information System)

393 PEs will have a

functional PMIS and

pilot e-procurement

system will start

functioning by Nov

2016.

All (393) PEs will have a fully functional PMIS as a reporting tool for procuring entities to report back to PPRA by Nov 2014

e-procurement will start functioning as pilot stage by Nov 2016

On track. PMIS progresses well (PPRA have a plan of providing tender portal, which is within PMIS and it has budget).

On track, the survey has been conducted on how to move online (there are initiatives in place) and e-procurement will be achieved by April, 2013).

Increase in

number of PEs

reached for

procurement

audit

Currently 330 PEs have

already been audited.

In June 2012 all 393

PE’s will be audited,

then beyond F/Y

2012/2013 will be “

Follow-up Audits

(should be repeatedly

process especially on

Top 20 PE’s

393 PEs audited by June 2012

Follow up audit of 100 PEs

to be done annually by

2016

Annual Procurement Performance Evaluation Report prepared and published Annually

Achieved. Done with the exception on newly PE within established District.

On track, with expected new zonal offices and staff easy to make follow up audit.

On track. Annual procurement performance evaluation report will be published on PPRA Journal and Website.

Output 3.2:

Strengthened

public sector

procurement by

June 2015

Number of

Public

procurement

regulations

issued

None( to be established

after baseline study)

% increase in number

of Public procurement

regulations issued

Action plan for

implementing PPA is

developed by December

2012 (Milestones to be

revised after finalization of

the action plan)

On track pending written

actionplan. To implement

the PPA, PPPD will conduct

training with government

procurement service

agents, and information

38

Number of

Skilled

procurement

staff

None( to be established

after baseline study)

% increase in number

of skilled Procurement

personnel in PEs

New public procurement

regulations prepared and

issued by June 2013

Procurement training

needs assessment exercise

completed by June, 2013

[300] procurement staff

trained on public

procurement by June, 2017

as per TNA

Strategy on public

procurement human

will be disseminated,

including on their website

The PPA regulations are on

track. Parliament passed

the law in 2011 and the

minister has prepared the

draft regulations. These are

currently with the Attorney

General’s office for

verification. The Minister

will then finalise the

regulations, present them

to Parliament and they will

become effective. This

could happen any time

now.

A ToR has been written for

a consultant to do the

training needs assessment

exercise. This is on track.

PPRA will conduct the

training of procurement

staff. It was agreed that the

number will be revisited.

Focus on strategy to be

revised to instead focus on

how organizational

structures within

procurement management

units should look.

On track. The staff

database already exists and

has about 2000 people on

39

resource developed and

disseminated by June, 2015

Procurement and supplies

staff database maintained

and updated by December,

2015

it. This is a continuing task

as it must be updated.

On track – target

within reach

Presence of

procurement

policy draft by

June, 2013

PPDs’ capacity

enhanced by

June, 2013

National

procurement

policy and

procurement

law

None

None

None

National procurement

policy developed and

disseminated to

stakeholders

i) Motor vehicle

and office

equipment

acquired

ii) Short training

for 20 members

of PPD staff

conducted

Public Procurement

Act 2011 reviewed

National procurement

policy draft finalized by

June, 2013

Stakeholders’ comments

incorporated by June, 2013

PPDs’ capacity enhanced by

June, 2013

20 members of PPD staff

equipped with skills on

public policy formulation,

implementation and

On track. The national

procurement policy draft

will explain the PPA and

covers central and local

government. A consultant

has been hired from Dar Es

Salaam University.

On track. The consultant

has submitted a framework

paper and after discussion

of this, a first draft for

comments will be

circulated. Comments will

be sought using meetings,

websites and newspapers.

On track. PPD will offer

training on public

procurement policies for

those with relevant

responsibilities. There

currently 18 staff currently

The 2014 onwards targets

for the national

procurement policy are all

on track – targets within

40

synchronised

Stakeholders

acquainted

with the

National

procurement

policy

National

procurement

policy

strategy in

place by

December,

2013

None

None

None

800 Stakeholders

acquainted with the

National procurement

policy

National procurement

policy strategy

implemented

evaluation by June, 2014

National procurement

policy developed and

shared by December, 2014

National procurement

policy strategy developed

and implemented by June

2015

Printing and uploading the

NPP on the website by

June, 2015

National procurement

policy and procurement law

synchronised by June, 2015

Monitoring the

implementation of the

National procurement

policy by June, 2015

Evaluation and feedback of

the implementation of the

National procurement

policy by June, 2016

1000 Stakeholders

acquainted with the

National procurement

Policy by June, 2016

reach.

Output 3.3: Increase in 10 staff with cash 610 staff with cash 600 staff of MDAs and LGAs Trained on cash

On track. 200 have been trained already from the 21

41

Strengthened

capacity of MDAs,

RSs and LGAs in

Cash management

by 2015

number of

staff with

adequate

skills on cash

management

management skills management skill Management using standardized materials by June 30 2014 (Milestones to be reviewed and aligned after the East AFRITAC recommendations on Cash and Banking Arrangement Mission)

regions (now 25). Training modules (in house) developed from Afritac hand out on banking arrangement, credible cash flow,,,. In house training made by AccGen personnel, with support of BoT and Afritac. Recommendations from E-AFRITAC not seen.

Decrease in

the aggregate

number of

bank accounts

operated by

LGAs by 2015.

The aggregate number of

bank accounts operated

by LGA are 4,736 in 2011

3938 bank accounts

will be closed by

December 2013

Six bank accounts operated

by each LGAs by December

2013

Milestone Achieved. Since July 1

st 2012, 6 bank

accounts per LGA are now operated. A substantial reduction of bank accounts will thus be possible during the F/Y 2012/2013 as bank accounts needs to be dormant for at least 6 month before closed.

Output 3.4:

Strengthened

public debt

management