report on the electronic communications sector 2007quarter iv.pdf · report on the electronic...

TRANSCRIPT

COMMUNICATIONS REGULATORY AUTHORITY OF THE REPUBLIC OF LITHUANIA

REPORT ON THE ELECTRONIC COMMUNICATIONS SECTOR

according to information provided by electronic communications operators and service

providers on the electronic communications activities carried out

(Quarter IV, 2007)

Vilnius 2007 March

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 2

Content

1. Preface 3

2. Main Indicators of the Electronic Communications Market 4

3. Fixed Telephony 7

4. Mobile Telephony 23

5. Leased Lines 37

6. Internet Access Services 39

7. Data Transmission Services 53

8. Cable Television and Microwave Multi-channel Distribution System (MMDS) Networks 54

9. Wire Radio Activities 56

10. Radio and Television Programs Transmission Services 56

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 3

1. Preface

The report on the electronic communications sector has been prepared on the basis of

information provided by electronic communications operators and (or) providers of services about the electronic communications activities that were carried out in the fourth quarter of 2007, as well as on other information available to the Communications Regulatory Authority (RRT).

At the end of the fourth quarter of 2007 the following had the right to engage in the electronic communications activities (submitted notifications about the beginning of their activities): 65 undertakings � to engage in the provision of fixed public telephone network and (or) services (during the fourth quarter was submitted 1 new notification, 5 undertakings cancelled activities), 20 undertakings � to engage in the activities of providing mobile public telephone network and (or) services (during the fourth quarter were not submitted new notifications, 2 undertakings cancelled activities), and 24 undertakings � to engage in the activities of providing leased lines services (during the fourth quarter were not submitted new notifications).

During the year were submitted 12 notifications about the beginning of activities in regard to public fixed telephone network and/or service provision, in regard to public mobile telephone network and/or service provision activities were submitted 6 notifications during the year, in regard to leased lines services provision activities � 3 notifications during the year.

The number of undertakings, actually executing public fixed telephone activities decreased by 7,7% during the year, number of undertakings, actually executing public mobile telephone activities increased by 8,3% and number of undertakings, actually executing leased lines services activities unchanged.

Fig. 1. Notifications about the beginning of electronic communications activities

52 47 48

12 13 13 15 15 15

9 22 17

5 9 7 9 11 9

2426242022

17

6561

69

0

10

20

30

40

50

60

70

80

2006 12 312007 09 30

2007 12 312006 12 31

2007 09 302007 12 31

200612 312007 09 30

2007 12 31

fixed telephone activities mobile telephone activities leased lines services

active in the market non active in the market number of notifications

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 4

2. Main Indicators of the Electronic Communications Market

1 table. Summarised indicators of the fixed public telephone activity

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

1. Number of fixed telephone lines1, total, in units

799.436 800.185 -0,09 792.357 799.436 0,89

2. Number of lines per 100 population2,

23,7 23,7 0 23,4 23,7 0,3

3. Number of mobile telephone subscribers, in units

4.921.077 4.889.512 0,65 4.718.215 4.921.077 4,30

4. Number of mobile telephone subscribers per 100 population

146,2 145,0 1,1 139,4 146,2 6,6

5. Number of Internet access subscribers, in units

581.860 524.514 10,93 417.526 581.860 39,36

including: who make use of broadband communication technologies

507.572 463.122 9,60 368.715 507.572 37,66

6. Number of Internet access subscribers per 100 population

17,3 15,6 1,7 12,3 17,3 4,9

broadband subscribers per 100 population

15,1 13,7 1,4 10,9 15,1 4,2

7. Revenue, in Litas 760.105 770.529 -1,35 2.695.279 2.974.469 10,36

including: fixed telephone 103.513 101.774 1,71 424.632 412.738 -2,80 mobile telephone 344.709 361.792 -4,72 1.237.870 1.387.251 12,07 leased lines 7.222 6.877 5,02 25.384 26.651 4,99 internet access services 87.385 80.689 8,30 264.884 312.965 18,15

data transmission services 14.814 14.175 4,51 46.818 55.609 18,78

provision of physical optical fibre

2.472 1.423 73,70 6.937

cable TV and MMDS 18.404 18.066 1,87 65.934 71.699 8,74

radio and television programs transmission services

7.355 6.264 17,42 20.644 25.294 22,53

wire radio 375 380 -1,42 1629 1.568 -3,74 networks interconnection 173.857* 179.089 -2,92 607.485 673.756 10,91 8. Investments, in Litas 171.118 128.699 32,96 525.670 546.614 3,98

including the investments into the electronic communication network infrastructure

138.712 106.680 30,03 350.191 460.983 31,64

1 - fixed telephone lines, including ISDN channels 2 - population 3366,2 thousand according to the data of the Statistic Department (data for 2008.01.01)

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 5

Fig 2. Distribution of revenue by markets for the fourth quarter of 2007, in % (total revenue LTL 760,10 mill. )

In the fourth quarter of 2007 electronic communication market according to revenue from the provision of fixed telephone networks and services, mobile telephone networks and services, leased lines services, internet access, data transmission, physical optical fibre, cable TV, MMDS, wire radio, radio and television programs transmission services and revenue from the networks interconnection in comparison with the third quarter of 2007 decreased by 1,4% and constituted LTL 760,10 million. In comparison with the year 2006 in the year 2007 market increased by 10,4%.

Estimating according to the revenues, received from the provision of all the aforementioned

electronic communications services, in 2007 only four companies occupied a market share larger than 2%, the market share of all the other operators and providers of electronic communications services (156 companies) amounted to approximately 11%.

Fig. 3. Distribution of the electronic communications market against operators (estimating according to the revenues, received in 2007), % (total revenue LTL 2974,5 mill.)

Network interconnection

22,87%

Wire radio0,05%

Radio and television programs transmission

0,97%Physical optical fibre

0,33%

Cable TV and MMDS2,42%

Data transmission (excl. internet)1,95%

Internet access11,50%

Mobile telephony45,35%

Fixed telephony13,62%

Leased lines0,95%

UAB �Bitė Lietuva� 20.4%

UAB �Tele2� 15.7%

Other 11.1% UAB �Omnitel�

29.0%

TEO LT, AB 23.9%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 6

Fig 4. Distribution of revenue from network interconnection by operators for the fourth quarter of 2007, in % (total revenue LTL 173,9 mill.)

In the fourth quarter of 2007 the investments into the electronic communications network infrastructure increased by 30,0%, comparing with the third quarter of 2007 and amounted to LTL 138,7 million. As compared with the year 2006, the investments into the electronic communications network infrastructure in the year 2007 increased by 31,6%.

Other2,92%

UAB "Omnitel"27,91%

TEO LT, AB19,76%

UAB "Bitė Lietuva"27,50%

UAB "Tele2"21,91%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 7

3. Fixed Telephony 48 companies engaged in the activities of the fixed public telephone communication in the

fourth quarter of 2007. Totally 32 companies specified that their fixed telephone services are provided by using IP (14 of them employed cable television networks).

Undertakings that engaged in the activities of the fixed public telephone communication in the fourth quarter of 2007: UAB �Alderada�, UAB �Alytaus kabelinė televizija�, UAB �Arcus Novus�, UAB �Balticum TV�, UAB �Baltnetos komunikacijos�, UAB �CSC Telecom�, UAB �Cubio�, UAB �Eurocom�, UAB �Eurofonas�, UAB �Gigatelis�, UAB �Gisnetas�, VĮ �Infostruktūra�, UAB �Init�, UAB �Interneto pasaulis�, A. Judicko individuali įmonė, AB �Lietuvos gele�inkeliai�, AB �Lietuvos radijo ir televizijos centras, UAB �Linkotelus�, UAB �Linktelis�, UAB �Marsatas�, UAB �Microlink Lietuva�, UAB �Mikrovisatos TV�, UAB �Nacionalinis telekomunikacijų tinklas�, UAB �Naujasis telefonas�, UAB �NORBY Telecom�, UAB �NTT Cable Lietuva�, AB �Ogmios centras�, UAB �Penkių kontinentų komunikacijų centras�, UAB �Radijo elektroninės sistemos�, UAB �Remo televizija�, UAB �Resvera�, UAB �Roventa�, UAB �Solocomas�, UAB �Tele2 fiksuotas ry�ys�, UAB �Telekomunikaciju grupa�, UAB �Televartai�, UAB �Telerena�, UAB �Teletinklas�, TEO LT, AB, UAB �ViaCall�, UAB �Viginta�, UAB �Zirzilė� and UAB �Bitė Lietuva�, UAB �Bručas ir Ko�, UAB �Fast traffic�, UAB �Mediafon�, UAB �Teleinformacijos paslaugos�, UAB �Trys penketai�.

Most undertakings provided retail fixed telephony services (42 undertaking from the beginning of the list provided international call services, 28 of them (UAB �Alderada�, UAB �Alytaus kabelinė televizija�, UAB �Balticum TV�, UAB �Eurocom�, UAB �Gisnetas�, VĮ �Infostruktūra�, UAB �Init�, UAB �Interneto pasaulis�, A. Judicko individuali įmonė, AB �Lietuvos gele�inkeliai�, AB �Lietuvos radijo ir televizijos centras�, UAB �Linktelis�, UAB �Marsatas�, UAB �Microlink Lietuva�, UAB �Mikrovisatos TV�, UAB �Nacionalinis telekomunikacijų tinklas�, UAB �NORBY Telecom�, AB �Ogmios centras�, UAB �Penkių kontinentų komunikacijų centras�, UAB �Radijo elektroninės sistemos�, UAB �Remo televizija�, UAB �Roventa�, UAB �Tele2 fiksuotas ry�ys�, UAB �Telerena�, UAB �Teletinklas�, TEO LT, AB, UAB �Viginta�, UAB �Zirzilė�) also provided services of national calls, other 5 provided only transit services.

Table 2. Summarised indicators of the fixed public telephone activity

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

1. Total number of fixed telephone subscribers3, total, units,

840.272 842.169 -0,23 835.446 840.272 0,58

including: - consumers 630.705 634.390 -0,58 630.394 630.705 0,05 - business subscribers 209.567 207.779 0,86 205.052 209.567 2,20

2. Total number of telephone lines, used for provision of public fixed telephone service (excl. ISDN), units,

751.684 753.427 -0,23 747.081 751.684 0,62

including: - consumers 610.592 612.650 -0,34 607.857 610.592 0,45 - business subscribers 141.092 140.777 0,22 139.224 141.092 1,34

including: - the number of metallic twisted pair lines

710.048 708.403 0,23 706.079 710.048 0,56

including the lines, used or provision of high speed rate digital subscriber

231.960 218.638 6,09 178.302 231.960 30,09

3 - the number of the fixed telephone subscribers is equated to the number of telephone lines, used for provision of fixed telephone services and adding the subscribers, to whom fixed telephone services were provided by using the access, provided by other operators

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 8

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

lines (hereinafter referred to as xDSL) service - the number of wireless communication lines

34.653 35.214 -1,59 36.360 34.653 -4,69

- the number of lines of cable television networks

315 491 -35,85 524 315 -39,89

- the number of lines of data communication networks

6.668 9.319 -28,45 4.118 6.668 61,92

3. Number of ISDN, total, in units

17.226 16.939 1,69 16.170 17.226 6,53

including: - consumers 524 566 -7,42 714 524 -26,61 - business subscribers 16.702 16.373 2,01 15.456 16.702 8,06

including: - ISDN BRA (128 kbps main speed rate line, equivalent to two 64 kbps speed rate channels)

16.751 16.479 1,65 15.708 16.751 6,64

- ISDN PRA (2 Mbps primary speed rate line, equivalent to thirty 64 kbps sped rate channels

475 460 3,26 462 475 2,81

4. Number of telephone lines connected to digital automatic exchanges, units4:

699.761 696.779 0,43 694.386 699.761 0,77

including: - consumers 567.514 568.886 -0,24 564.363 567.514 0,56 - business subscribers 132.247 127.893 3,40 130.023 132.247 1,71

5. The number of subscribers, to whom public fixed telephone services are provided by using the access, provided by other electronic communications operators, units:

40.836 41.984 -2,73 43.089 40.836 -5,23

including: - consumers 19.065 20.608 -7,49 21.109 19.065 -9,68 - business subscribers 21.771 21.376 1,85 21.980 21.771 -0,95

6. The number of pre-payment cards sold, units

51.567 84.844 -39,22 51.567

7. Number of pay phones, total, units:

2.440 3.065 -20,39 3.575 2.440 -31,75

including - in cities 2.066 2.602 -20,60 3.005 2.066 -31,25 - in small towns and rural areas

374 463 -19,22 570 374 -34,39

8. Total number of disconnected telephones, units:

15.109 14.081 7,30 66.265 55.586 -16,12

including: - due to the debts for services

1.475 1.431 3,07 6.877 5.673 -17,51

- wished by the customer 13.634 12.650 7,78 59.268 49.913 -15,78 9. Volumes of calls where calls are initiated in one�s own network, total, min:

422.793.495 383.406.922 10,27 1.729.085.914 1.667.248.256 -3,58

- consumers 292.355.022 259.526.070 12,65 1.136.418.443 1.131.530.932 -0,43 - business subscribers 130.438.472 123.880.852 5,29 592.667.470 535.717.323 -9,61 including: - services over short telephone numbers

7.694.186 7.499.338 2,60 26.998.188 30.158.018 11,70

4 - excl. ISDN lines

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 9

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

(excluding 10XX and the dial-up Internet connections), when calls are terminated in own network - local calls (volume of calls when calls are terminated in own network within a geographical numbering area)

303.014.816 270.181.951 12,15 1.254.055.830 1.195.057.480 -4,70

- long-distance calls (volume of calls when calls are terminated in own network in other areas of geographical numbering)

72.540.912 66.324.112 9,37 292.845.186 282.475.149 -3,54

- international calls (calls terminated in the networks of foreign operators)

12.813.803 12.659.820 1,22 52.557.764 51.462.181 -2,08

- to other public fixed telephone networks of the Republic of Lithuania

6.915.786 6.421.485 7,70 18.897.426 26.565.478 40,58

- to public mobile telephone networks of the Republic of Lithuania

19.813.992 20.320.216 -2,49 83.731.520 81.529.951 -2,63

10. Duration of calls to internet in case of dial-up connection, min.:

13.998.301 14.856.049 -5,77 157.156.215 69.003.051 -56,09

including: - consumers 11.142.124 11.908.449 -6,44 125.137.312 54.158.100 -56,72 - business subscribers 2.856.177 2.947.600 -3,10 32.018.903 14.844.951 -53,64

11. Volumes of calls where calls are terminated in one�s own network, total, min (except the calls, initiated in the own network):

75.366.365 72.187.174 4,40 281.024.087 291.530.896 3,74

including: - calls initiated in other public fixed telephone networks of the Republic of Lithuania

12.316.796 10.665.019 15,49 60.210.231 46.168.634 -23,32

- calls initiated in public mobile telephone networks of the Republic of Lithuania

29.558.485 29.212.672 1,18 107.475.610 115.662.912 7,62

- calls initiated in the networks of operators of foreign countries

33.491.083 32.309.483 3,66 113.338.246 129.699.351 14,44

12. Volume of transit forwarded calls, min.:

123.093.566 117.099.937 5,12 347.482.429 439.478.114 26,47

- to other public telephone networks of the Republic of Lithuania

61.526.936 56.438.624 9,02 190.296.291 215.506.093 13,25

- to telephone networks of foreign countries

61.566.630 60.661.312 1,49 157.186.137 223.972.021 42,49

13. The number of users of services who make use of the public telephone service operator (carrier) (hereinafter referred to as the provider) selection

18.926 19.637 -3,62 21.884 18.926 -13,52

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 10

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

service, total, units, (who made use of these services at least once within the reporting period): - of which by means of pre-selection, units

5.165 5.252 -1,66 4.639 5.165 11,34

14. The total volume of calls, initiated by the service users, who make use of provider selection service, min.:

5.377.291 5.531.322 -2,78 30.461.478 23.526.034 -22,77

- including by those who use the pre-selection service

2.864.045 2.926.184 -2,12 13.998.728 12.498.409 -10,72

15. The number of providers whose services can be chosen by means of pre-selection or call-by-call selection, total, units

15 15 0 15 15 0

- of which by means of pre-selection, units

6 6 0 6 6 0

16. Revenues from the retail provision of the public fixed telephone network and/or services, in thou. Litas (excluding VAT).

101.698 99.836 1,87 417.972 405.754 -2,92

- consumers 54.243 53.712 0,99 215.517 216.379 0,40 - business subscribers 47.456 46.123 2,89 202.455 189.375 -6,46 including: - for local calls 17.922 16.541 8,35 79.951 71.412 -10,68 - for domestic long-distance calls

8.326 8.068 3,20 40.698 34.032 -16,38

- for international calls 8.702 8.864 -1,83 40.998 36.142 -11,84 - for the calls to other public fixed telephone networks

1.538 1.335 15,15 721 5.557 670,42

- for the calls to public mobile telephone networks

10.663 10.913 -2,30 46.669 43.950 -5,83

- other revenues 54.548 54.114 0,80 208.935 214.660 2,74 17. Revenues from wholesale public fixed telephone network and/or services, thou. LTL (excluding VAT). (the item does not include the revenues, received from network interconnection activities)

1.814 1.939 -6,41 6.660 6.984 4,87

18. The revenues from network interconnection activities, thou. Litas (excluding VAT)

43.068 44.567 -3,37 143.754 165.210 14,93

including: - the revenues for termination of calls, initiated in other public telephone networks of the Republic of Lithuania in the own network

4.926 5.172 -4,75 19.322 15.719 -18,65

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 11

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

- the revenues for termination of calls, initiated in foreign countries� networks in the own network

3.215 3.141 2,37 13.401 12.698 -5,25

- the revenues for forwarding (transit) of calls

34.660 35.753 -3,06 108.657 131.366 20,90

Total revenue from the provisions of fixed public telephone networks and services constituted

LTL 103,51 million during the fourth quarter of 2007, revenue of alternative providers of fixed telephone communication totalled LTL 4,85 million, or 4,68%. As compared with the last quarter, total revenue of the providers of fixed telephone communication increased by 1,7%, as well as revenue of the alternative providers increased by 0,9%. As compared with the year 2006 total revenue of the providers of fixed telephone communication in the year 2007 decreased by 2,8%, revenue of the alternative providers increased by 6,5%.

TEO LT, AB revenues from provision of local calls during the fourth quarter of 2007 accounted 99,1% of market share, of domestic long-distance calls � 90,6% (UAB �Eurocom� � 5,9%), of international calls � 77,9% (UAB �Telekomunikaciju grupa� � 4,1%, UAB �Cubio� � 3,6%, UAB �Solocomas� � 2,2%, other less than 2%), of calls to public mobile telephone networks � 94,5% (UAB �Eurocom� � 2,6%).

The number of subscribers of alternative providers of fixed public telephone services at the end of the fourth quarter of 2007 totalled 52,0 thousand (6,2% of the total number of the subscribers � 840,3 thousand) and during the quarter their number decreased by 7,3%. From the end of the fourth quarter of 2006 number of the subscribers of alternative providers of fixed public telephone services decreased by 1,8%. Fig. 5. Change of market share of alternative providers of fixed public telephone services according to the number of subscribers and revenues, %

The number 799,44 thousand comprises 788,32 thousand lines of TEO LT, AB and 11,12

thousand main lines of the alternative operators. During the fourth quarter of 2007 the total number of telephone lines decreased by 0,7

thousand (0,1%). During the year the number of telephone lines increased by 7,1 thousand (0,9%).

6,19 6,38 6,54 6,58

1,37

5,05

6,016,08 6,34 6,65

6,18

4,15 3,98 3,97 4,11 4,454,72 4,68

2,92

4,78

6,12

4,27

0

2

4

6

8

2003 2004 2005 2006 IQ 2006 IIQ 2006 IIIQ 2006 IVQ 2007 IQ 2007 IIQ 2007 IIIQ 2007 IVQ

%

Altern. share according to the number of subscribers Altern. share according to revenues

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 12

During the fourth quarter of 2007 the number of telephone lines per 100 population unchanged and in the 31 December 2007 constituted 23,7 lines per 100 population � 45,2 lines per 100 households5. During the year penetration increased by 0,3 per cent. Fig. 6. Number of telephone lines

According to the information, published on the Internet websites of national regulators, the fixed communication penetration at the end of the fourth quarter of 2007:

- in Spain reached 40.8% (40,8 lines per 100 population) and in comparison with the end of the year 2006, it increased by 0,5 per cent;

- in Hungary reached 32,3% and in comparison with the end of the year 2006, it decreased by 0,9 per cent.

Twisted metallic pair loops were mostly used for access to the subscribers, also there were used wireless communication lines, cable television and data transmission network lines. Fig. 7. Distribution of the number of the telephone lines according to technologies, thou. (total number � 799,44 thou.)

5 - household - 2,4 person according to the data of the Statistic Department (data for 2007)

799,44800,19799,04798,08792,357801,11820,04

824,2

935,9

1151,723,723,723,7

33,1

27,023,9 23,9 23,5 23,4 23,6

0

200

400

600

800

1000

1200

1400

2001 12 31 2002 12 31 2003 12 31 2004 12 31 2005 12 31 2006 12 31 2007 03 31 2007 06 30 2007 09 30 2007 12 310

5

10

15

20

25

30

35

Number of telephone lines, in thou. Number of telephone lines per 100 population

twisted metallic pair loops (PSTN)

88,8%

cable television network lines

0,04%

wireless communication lines

4,3%

data transmission network lines

0,8%

ISDN channels6,0%

twisted metallic pair loops (PSTN) wireless communication linescable television network lines data transmission network linesISDN channels

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 13

The alternative service providers provided fixed telephone services to approximately 21,4% (11,1 thousand) subscribers by using their lines, the remaining subscribers (40,8 thousand) were provided the services by using the access, provided by other electronic communications operators.

As of 31 December of 2007 two agreements on provision of unbundled access to the local loop service were signed and TEO LT, AB was providing fully unbundled access6 to 443 local loops.

Cable television networks and data communication networks were used for provision of the Internet telephony services (6983 lines). Totally at the end of fourth quarter of 2007 approximately 27,6 thousand subscribers used the Internet telephony services7, during the quarter their number decreased by 10%, during the year increased by 25,2%. By using the IP protocol, mostly international calls services were provided. The revenues from these services during the fourth quarter of 2007 amounted to LTL 1,17 million, i. e. they grew by 0,7% comparing with the third quarter of 2007; the revenues from these services in the year 2007 totalled LTL 4,5 million, comparing with the year 2006 they increased by 15,2% In the fourth quarter of 2007 the international call (IP) streams increased by 1,8% comparing with last quarter and amounted 2,36 million min. (about 18,4% of all the international calls).

The share of TEO LT, AB telephone lines connected to digital telephone stations (ATS) increased from 93,9% at the end of the fourth quarter of 2006 until 94,0% at the end of the fourth quarter of 2007.

During the fourth quarter of 2007 the number of main lines whereby the high-speed service of subscriber lines (hereinafter referred to as xDSL) increased by 6,1% and on 31 December 2007 totalled 232,0 thousand. From the end of the fourth quarter of 2006 it increased by 30,1%.

The total duration of the calls initiated in public fixed telephone networks in the fourth quarter of 2007 increased by 10,3% comparing with the previous quarter, and constituted 422,80 million minutes, including 408,50 million minutes (96,6%), which were initiated in the network of TEO LT, AB. As compared with the year 2006 the total duration of the calls in the year 2007 decreased by 3,6%. Share of duration of the calls initiated by alternative service providers during the year increased by 0,1 per cent.

During the fourth quarter of 2007 alternative operators initiated: - 31,5% of international calls (including: 4,8% - UAB �Telekomunikaciju grupa�, 4,5% - UAB

�Cubio�, 4,0% - UAB �CSC Telecom�, 2,5% - UAB �Linkotelus�, 2,3% - UAB �Tele2 fiksuotas ry�ys�, 2,3% - UAB �Solocomas�, 2,0% - UAB �Eurocom�, other � less 2%),

- 7,9%8 of long-distance calls (including: 4,0% - UAB �Eurocom�), - 0,7% of local calls, - 8,9% to mobile telephone networks (including: 3,5% - AB �Lietuvos gele�inkeliai�, 2,4% -

UAB �Eurocom�, other � less 2%), - 1,1% calls over service and short numbers.

6 - Full unbundled access to the local loop means the provision to a beneficiary of access to the local loop or local sub-loop of the operator bound by the procedure and conditions set out in the Electronic Communications Law, authorising the use of the full frequency spectrum of the physical circuit. 7 - according to the data of public fixed telephone communications that indicated provision of the IP telephony services 8 - including long-distance calls and calls to other public fixed telephone networks of the Republic of Lithuania

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 14

Fig. 8. The change of the market share of the alternative operators according to the initiated calls, %

Fig. 9. Duration of calls initiated in fixed public telephone networks, in mill. min. During the fourth quarter a total duration of calls terminated in fixed public telephone networks

that were initiated in other networks (of the Republic of Lithuania and foreign countries) was 75,37

0,9 1,1 1,80,8 0,6 0,7 0,7 0,7

13,5

22,9

3,8 3,3 3,1 3,6

0,7

32,331,5

33,632,8

31,431,132,1

8,310,0

8,18,9

7,9

7,4

7,3

15,1

7,7 8,07,98,1

8,8

7,4

7,713,18,9

8,65,1 3,43,43,63,0

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

2003 m 2004 m. 2005 m. 2006 m. 2007 m. Iketv.

2007 m. IIketv.

2007 m. IIIketv.

2007 m. IVketv.

2007 m.

local calls international calls to mobile telephone network long-distance calls total

0 20 40 60 80 100

local calls

long-distance calls

international calls

to mobile telephonenetwork

through the service, shortnumbers

TEO LT, AB 300,90 73,17 8,77 18,05 7,61

Alternative operators 2,12 6,29 4,04 1,76 0,09

local calls long-distance calls international calls to mobile telephone network

through the service, short numbers

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 15

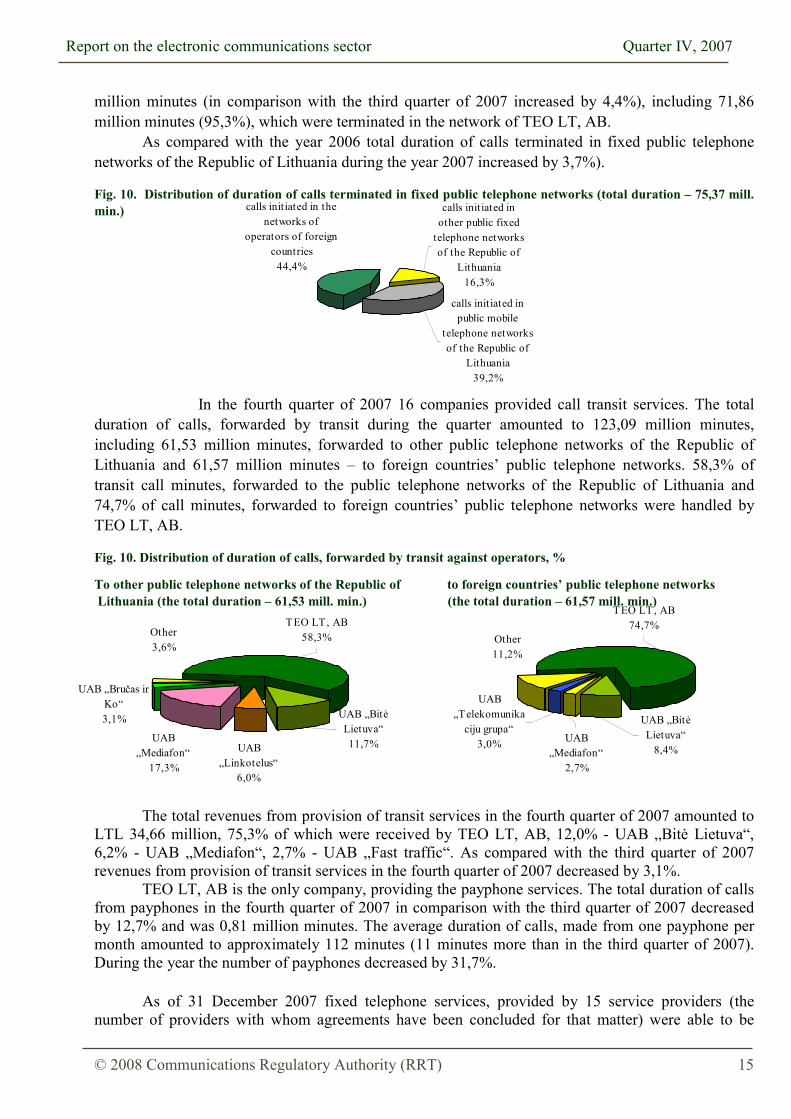

million minutes (in comparison with the third quarter of 2007 increased by 4,4%), including 71,86 million minutes (95,3%), which were terminated in the network of TEO LT, AB.

As compared with the year 2006 total duration of calls terminated in fixed public telephone networks of the Republic of Lithuania during the year 2007 increased by 3,7%). Fig. 10. Distribution of duration of calls terminated in fixed public telephone networks (total duration � 75,37 mill. min.)

In the fourth quarter of 2007 16 companies provided call transit services. The total

duration of calls, forwarded by transit during the quarter amounted to 123,09 million minutes, including 61,53 million minutes, forwarded to other public telephone networks of the Republic of Lithuania and 61,57 million minutes � to foreign countries� public telephone networks. 58,3% of transit call minutes, forwarded to the public telephone networks of the Republic of Lithuania and 74,7% of call minutes, forwarded to foreign countries� public telephone networks were handled by TEO LT, AB.

Fig. 10. Distribution of duration of calls, forwarded by transit against operators, %

To other public telephone networks of the Republic of to foreign countries� public telephone networks Lithuania (the total duration � 61,53 mill. min.) (the total duration � 61,57 mill. min.)

The total revenues from provision of transit services in the fourth quarter of 2007 amounted to

LTL 34,66 million, 75,3% of which were received by TEO LT, AB, 12,0% - UAB �Bitė Lietuva�, 6,2% - UAB �Mediafon�, 2,7% - UAB �Fast traffic�. As compared with the third quarter of 2007 revenues from provision of transit services in the fourth quarter of 2007 decreased by 3,1%.

TEO LT, AB is the only company, providing the payphone services. The total duration of calls from payphones in the fourth quarter of 2007 in comparison with the third quarter of 2007 decreased by 12,7% and was 0,81 million minutes. The average duration of calls, made from one payphone per month amounted to approximately 112 minutes (11 minutes more than in the third quarter of 2007). During the year the number of payphones decreased by 31,7%.

As of 31 December 2007 fixed telephone services, provided by 15 service providers (the

number of providers with whom agreements have been concluded for that matter) were able to be

calls initiated in other public fixed

telephone networks of the Republic of

Lithuania 16,3%

calls initiated in the networks of

operators of foreign countries

44,4%

calls initiated in public mobile

telephone networks of the Republic of

Lithuania39,2%

TEO LT, AB58,3%

UAB �Mediafon�

17,3%

UAB �Bručas ir Ko�3,1%

Other3,6%

UAB �Linkotelus�

6,0%

UAB �Bitė Lietuva� 11,7%

TEO LT, AB74,7%

UAB �Telekomunika

ciju grupa�3,0%

Other11,2%

UAB �Mediafon�

2,7%

UAB �Bitė Lietuva�

8,4%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 16

0,44

0,86

0,53

1,37

0,00

0,30

0,60

0,90

1,20

1,50

Price of 3 min call, peak Price of 3 min call, off-peak

“Calls to other fixed telephone communication networks” payment plan Standart tariff calls to other fixed networks

Subscription fee for 1 phone number

23,0025,36

“Calls to other fixedtelephone

communicationnetworks” payment

plan

Standart tariff callsto other fixed

networks

selected in the network of TEO LT, AB by individual selection (by dialling the operator code 10XX), from them 6 � and by carrier pre-selection (the possibility to use the provider�s services automatically, i. e. without dialling the operator code and without executing any other carrier selection procedure when calling). In reality 10 service providers provided public fixed telephone services by using the individual selection, including UAB �Eurocom�, UAB �Cubio�, UAB �Linkotelus� � and carrier pre-selection.

During the fourth quarter of 2007 about 18,99 thousand users made use of this service (3,6% less than during the previous quarter), 5,2 thousand of them � by means of pre-selection. The total duration of calls, initiated in the fourth quarter of 2007 decreased by 2,8%, compared with third quarter of 2007, and amounted to 5,38 million minutes, including 2,86 million minutes by pre-selection initiated calls.

Until the end of the fourth quarter of 2007 were assigned 24 operator selection codes 10XX to 22 providers of services (during the fourth quarter was assigned 1 operator selection code).

Until 31 December 2007 9013 subscribers had their numbers transferred to other networks by using the fixed telephone number portability service, during the quarter this number increased by 9,0%. During the fourth quarter were transferred 744 telephone numbers: to UAB �Mediafon� � 370 numbers (from UAB �Mediafon� - 6), accordingly to UAB �Nacionalinis telekomunikacijų tinklas� � 224 (1), UAB �CSC Telecom� � 75 (3), UAB �Eurocom� � 25 (20), AB Lietuvos radijos ir televizijos centras � 19 (4), TEO LT, AB � 16 (709), UAB �Telekomunikaciju grupa� � 10 (0), UAB �Tele2� � 3 (0), UAB �Interneto pasaulis� � 2 (1). Prices of fixed telephone calls

In the fourth quarter of 2007 TEO LT, AB, the company, holding significant power on the market of public local and/or national telephone communications services, provided to consumers and service recipients, except users, at a fixed location and the market of public international telephone communication services, provided to consumers and service recipients, except users at a fixed location offered 18 (in the 3rd Quarter of 2007 � 17) retail payment plans for private and business consumers. 12 November 2007 the tariffs and conditions for provision of the �Pokalbiai į kitus fiksuoto telefono ry�io tinklus�(�Calls to other fixed telephone communication networks�) payment plan were approved.

Figure 12. Prices of calls to other fixed telephone networks from TEO LT, AB fixed telephone network, as for December 31st, 2007, LTL w. the VAT

Note: Peak � 8 am. � 8 pm. on workdays, Off-peak � 8 pm. � 8 am. on workdays, 24 h. on weekends and holidays.

Till the end of the fourth quarter of 2007 TEO LT, AB concluded 11 networks� interconnection agreements with providers of public fixed telephone networks, thus the subscribers of those networks

9 - according to the data provided by TEO LT, AB

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 17

were given the possibility to make calls to the network of TEO LT, AB and the subscribers of TEO LT, AB were given the possibility to make calls to the networks of the said providers.

Other providers of public fixed telephone services (according to the data, provided to the RRT) did not execute any changes in the prices of the calls inside their networks and to other networks in the fourth quarter of 2007. The average prices of fixed telephone calls

The information on the average prices of installation of a telephone line and public fixed telephone services, applicable to service recipients is presented below. In all the figures, presented in the present chapter (Figures 13 - 19) the lowest and highest prices, offered on the market in the fourth quarter of 2007, as well as the average prices, calculated on the basis of all the data for the aforementioned period, presented to the Communications Regulatory Authority are presented.

Figure 13 presents the comparison of the charges for installation of a new telephone line, change of subscription to a line and monthly charges for a telephone line.

According to the data, submitted by providers of public fixed telephone services, in the fourth Quarter of 2007 the average price of installation of a new fixed telephone line reduced by 4,57% comparing with the third quarter of 2007, although the highest and lowest prices applicable did not change. Comparing the average prices of installation of a new telephone line, applicable in the fourth quarter of 2007 with the corresponding period of 2006, the prices increased by 24,4%; which is also related with the fact that certain new service providers set a larger price for the service upon their accession to the fixed telephone communication market.

The average price for changing of subscription to a line reduced insignificantly � by LTL 1,11 (4,4%) during the quarter, the average price of the monthly charge for the used telephone line, comparing with the third quarter of 2007 reduced by 16,3% and amounted to LTL 34,13.

Figure 13. Comparison of the fees for installation of a new line, changing of the subscription to a line and monthly

subscription fees for a telephone line, charged by public fixed telephone service providers, LTL w. the VAT

In the fourth quarter of 2007 18 providers presented information on the fixed telephone line installation service, 9 providers � on the service of changing of subscription to a line, 17 providers � on the monthly charge for a telephone line service.

35,0725,22

34,26 40,77

24,1134,13

105,57

25,22

104,08

115,38110,10

26,7112,00 12,00

10,0012,00 5,001,181,18

10,00 10,001,18 1,18

10,00

309,40309,40 309,40309,40

39,00

373,18373,18

39,00 39,00

373,18

39,00

373,18

0,00

74,00

148,00

222,00

296,00

370,00

2007 I 2007 II 2007 III 2007IV

2007 I 2007 II 2007 III 2007IV

2007 I 2007 II 2007 III 2007IV

New line installation fee Change of subscription to an existingline

Line subscription fee

Average price, LTL w . the VAT Bottom price, LTL w . the VAT Top price, LTL w . the VAT

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 18

Figure 14 presents the comparisons of the prices of local and national long-distance calls (during the peak and off-peak hours), without the call setup charge.

During the fourth quarter of 2007 the average price of a fixed telephone communication local call during the peak hours increased from LTL 0,15 to LTL 0,17, however, comparing with the first quarter of 2007, the average price of a fixed telephone local call reduced by approximately 15% (LTL 0,03 per minute). As the lowest price of a minute of a local call, offered on the market did not change, the change of the highest price, calculating from the beginning of the calendar year is rather significant (the price reduced by LTL 0,39 per minute).

During the fourth quarter of 2007 the average price of the peak and off-peak hour national long-distance calls, as well as the highest and the lowest price, offered on the market did not change (see Figure 14). Figure 14. Comparison of prices of local and national long-distance calls, provided by public fixed telephone service providers (peak* and off-peak** time), LTL w. the VAT Peak* - a period when the highest applicable price applied by the provider. Off-peak** - a period when the lowest applicable price applied by the provider.

Price for 1 call minute, peak

0,120,20

0,15 0,15 0,17 0,20 0,19

0,88

0,49 0,49 0,49 0,49 0,49 0,49 0,49

0,06 0,06 0,06 0,060,120,12 0,12

0,190,18

0,00

0,30

0,60

0,90

2007 I 2007 II 2007 III 2007 IV 2007 I 2007 II 2007 III 2007 IV

Local call National call

Bottom price, LTL w . the VAT Average price, LTL w . the VAT Top price, LTL w . the VAT

Price for 1 call minute, off-peak

0,02 0,02 0,020,07

0,100,13 0,13 0,14

0,17 0,15 0,15

0,26

0,49 0,49 0,49 0,49 0,49 0,49 0,49

0,070,070,070,02

0,15

0,00

0,10

0,20

0,30

0,40

0,50

0,60

2007 I 2007 II 2007 III 2007 IV 2007 I 2007 II 2007 III 2007 IV

Local call National call

Bottom price, LTL w . the VAT Average price, LTL w . the VAT Top price, LTL w . the VAT

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 19

If viewing the dynamics of the prices of local and national long-distance calls, offered to fixed telephone service recipients (see Figure 15), it can be noticed that the prices of the services were consistently reducing. Starting from the end of 2005 the average price of a local call made during peak hours reduced by 51,4%, the price of an off-peak hour call � by 63%. During the same time period the average price of a national long-distance call reduced correspondingly by 50% and 59,4%.

The information on the prices of fixed telephone local and national long-distance calls, offered at the end of the fourth quarter of 2007 was provided by 13 service providers. Figure 15. Comparison of prices of local and national long-distance calls, provided by public fixed telephone service providers (peak* and off-peak** time), year 2005 � 2007, LTL w. the VAT

Price for 1 call minute, peak

1,18

0,88

0,49

1,18

0,570,49

0,060,060,060,14 0,12 0,12

0,380,35

0,230,17

0,230,19

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

2005 IV 2006 IV 2007 IV 2005 IV 2006 IV 2007 IV

Local call National call

Bottom price, LTL w . the VATTop price, LTL w . the VATAverage price, LTL w . the VAT

Price for 1 call minute, off-peak

0,02

1,18

0,570,49

1,18

0,570,49

0,070,070,070,020,02

0,38 0,37

0,150,190,140,13

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

2005 IV 2006 IV 2007 IV 2005 IV 2006 IV 2007 IV

Local call National call

Bottom price, LTL w . the VAT Top price, LTL w . the VATAverage price, LTL w . the VAT

Peak* - a period when the highest applicable price applied by the provider. Off-peak** - a period when the lowest applicable price applied by the provider.

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 20

During the fourth quarter of 2007 the average charges for setup of local and national long-distance calls, offered by public fixed telephone service providers did not change.

Figures 16 - 17 present the comparison of the prices of international calls to the selected foreign countries (Sweden, Greece, the USA and Japan), offered by public fixed telephone service providers.

During the fourth quarter of 2007 the average prices per minute of the calls to all the selected foreign countries during the peak and off-peak hours changed insignificantly, within the limits of 5% (from 0% for calls to the USA to 5% for calls to the EU Member States). Such fluctuation of the average market price resulted from the changes of the prices, applicable by individual service providers.

At the end of the fourth quarter the average price of peak hour fixed telephone communication calls to a close European Union Member State � Sweden amounted to LTL 0,32, to Greece, the USA and Japan � correspondingly LTL 0,34, LTL 0,33 and LTL 1,11, the average price of off-peak hour calls was insignificantly lower (LTL 0,29 for calls to Sweden, LTL 0,32 � to Greece, LTL 0,30 � to the USA and LTL 1,03 � to Japan).

The information on the prices of international calls, valid at the end of the fourth quarter of 2007 was presented to the Communications Regulatory Authority by 32 fixed telephone operators and service providers.

Figure 16. Comparison of prices of peak-hour international calls to the selected foreign countries (Sweden, Greece, the USA and Japan), charged by public fixed telephone service providers (excluding the call setup fee), LTL w. the

VAT

0,11 0,110,05 0,050,050,100,100,05 0,05 0,150,050,050,15 0,15 0,15

0,05

0,310,33 0,320,30 0,330,330,33 0,32 0,36 0,340,36 0,34

1,021,15 1,13 1,111,39 1,39 1,391,391,391,391,39 1,39

7,79

1,39 1,39 1,39

7,79 7,79 7,79

1,39

0,00

3,70

7,40

2007I

2007II

2007III

2007IV

2007I

2007II

2007III

2007IV

2007I

2007II

2007III

2007IV

2007I

2007II

2007III

2007IV

Price for 1minute call to Sw eden,peak time

Price for 1 minute call to Greece,peak time

Price for 1 minute call to USA,peak time

Price for 1 minute call toJapan, peak time

Bottom price, LTL w . the VAT Average price, LTL w . the VATTop price, LTL w . the VAT

Peak* - a period when the highest applicable price applied by the provider.

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 21

Figure 17. Comparison of prices of peak-hour calls to the selected foreign countries (Sweden, Greece, the USA and Japan), charged by public fixed telephone service providers, LTL w. the VAT

Off-peak** - a period when the lowest applicable price applied by the provider

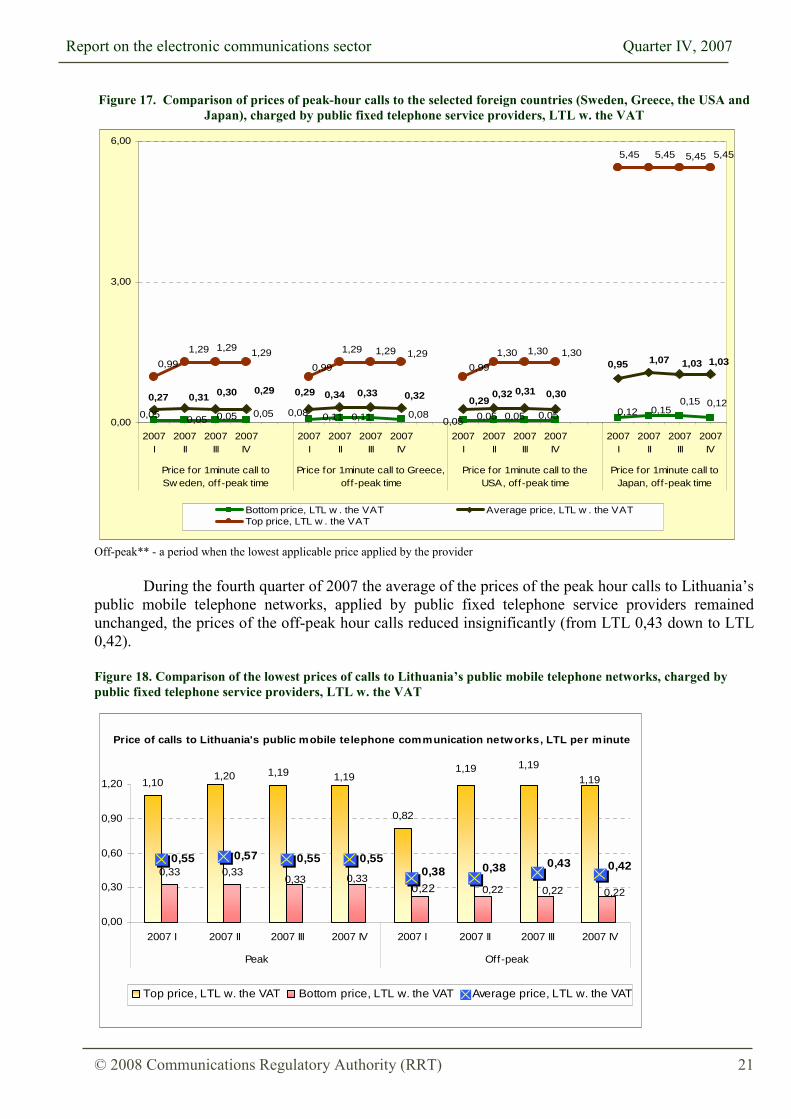

During the fourth quarter of 2007 the average of the prices of the peak hour calls to Lithuania�s public mobile telephone networks, applied by public fixed telephone service providers remained unchanged, the prices of the off-peak hour calls reduced insignificantly (from LTL 0,43 down to LTL 0,42). Figure 18. Comparison of the lowest prices of calls to Lithuania�s public mobile telephone networks, charged by public fixed telephone service providers, LTL w. the VAT

0,05 0,120,050,080,050,05 0,080,05 0,050,110,11

0,150,15 0,12

0,05 0,05

0,95 1,07 1,03 1,03

0,29 0,320,330,340,27 0,310,290,30

0,290,32 0,31 0,30

5,45 5,45 5,45 5,45

0,991,29 1,29 1,29

0,99

1,29 1,29 1,290,99

1,30 1,30 1,30

0,00

3,00

6,00

2007I

2007II

2007III

2007IV

2007I

2007II

2007III

2007IV

2007I

2007II

2007III

2007IV

2007I

2007II

2007III

2007IV

Price for 1minute call toSw eden, off -peak time

Price for 1minute call to Greece,off-peak time

Price for 1minute call to theUSA, off-peak time

Price for 1minute call toJapan, off-peak time

Bottom price, LTL w . the VAT Average price, LTL w . the VATTop price, LTL w . the VAT

1,101,19

0,82

0,33 0,33

1,191,20 1,191,191,19

0,330,330,22 0,22 0,22 0,22

0,55 0,57 0,55 0,550,38 0,38 0,43 0,42

0,00

0,30

0,60

0,90

1,20

2007 I 2007 II 2007 III 2007 IV 2007 I 2007 II 2007 III 2007 IV

Peak Off-peak

Price of calls to Lithuania's public mobile telephone communication networks, LTL per minute

Top price, LTL w. the VAT Bottom price, LTL w. the VAT Average price, LTL w. the VAT

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 22

As shown by Figure 19, the average price of the call, made from a public fixed telephone network to Lithuania�s public mobile telephone networks during peak hours, comparing with the data as of the corresponding period of 2006 remained unchanged, however comparing with the fourth quarter of 2005 � reduced by 7%. The dynamics of the price of the service as of the off-peak hours was inconsistent � from the end of 2005 till the end of 2006 the price reduced by 17,4%, however upon accession of new service providers to the market, the average price of calls slightly increased. Figure 19. Comparison of the lowest prices of calls to Lithuania�s public mobile telephone networks, charged by public fixed telephone service providers, year 2005-2007, LTL w. the VAT.

0,30 0,33 0,33

1,181,10

1,19

0,550,550,59

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

2005 IV 2006 IV 2007 IV

Price of calls to Lithuania’s public mobiletelephone communications networks, LTL per

minute, peak

Bottom price, LTL w. the VATTop price, LTL w. the VATAverage price, LTL w. the VAT

0,24

1,18

0,82

1,19

0,220,22 0,380,42

0,46

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

2005 IV 2006 IV 2007 IV

Price of calls to Lithuania’s public mobiletelephone communications networks, LTL per

minute, off- peak

Bottom price, LTL w. the VATTop price, LTL w. the VATAverage price, LTL w. the VAT

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 23

4. Mobile Telephony 8 undertakings carried out the activities of mobile public telephony in the fourth quarter of

2007: 3 operators (UAB �Omnitel�, UAB �Bitė Lietuva�, UAB �Tele2�) and 5 providers of services that did not own network (hereinafter referred to as the Service providers) (UAB �Eurocom�, UAB �Laracijos telekomunikacijos�, UAB �Teledema�, UAB �Norfos ma�mena� and UAB �CSC Telecom�) that provided services though the network of UAB �Bitė Lietuva�.

5 undertakings (UAB �Auto�vilgsnis�, UAB �Mobilus partneris�, UAB �Metameda� ir ko, UAB �Transteleservis�, UAB �AKN�) carried out the activities as resellers.

Table 3. Summarised indicators of the mobile public telephone activity

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

1. Number of active mobile telephone communication subscribers

4.921.077 4.889.512 0,65 4.718.215 4.921.077 4,30

including: - consumers, who pay for the services against the bills

1.056.634 1.042.332 1,37 1.004.507 1.056.634 5,19

- business subscribers, who pay for the services against the bills

604.154 597.324 1,14 553.590 604.154 9,13

- subscribers who make use of the prepaid service

3.260.289 3.249.856 0,32 3.160.118 3.260.289 3,17

2. The number of short messages (SMS) forwarded, in units

2.394.182.987 2.164.856.797 10,59 9.033.571.709 9.373.312.686 3,76

3. The number of multimedia messages (MMS) forwarded, in units

1.585.456 1.582.761 0,17 4.019.612 5.765.333 43,43

4. The number of subscribers, who make use of the data transmission services (GPRS and/or EDGE and/or UMTS), provided by public mobile telephone network, units

1.532.114 1.385.529 10,58 1.153.479 1.532.114 32,83

5. The number of subscribers who make use of the data transmission services (CSD and/or HSCSD) provided by the public mobile telephone networks, units

14.012 17.845 -21,48 44.731 14.012 -68,67

6. Volume of data forwarded and received by using the packet data services (GPRS and EDGE and/or UMTS), provided by mobile telephone network, megabytes:

141.096.569 89.341.994 57,93 171.607.541 356.594.407 107,80

- including the volume of received data

116.503.335 74.716.041 55,93 139.640.613 293.852.092 110,43

7. The total duration of calls, initiated in the own network, min.:

1.249.926.479 1.236.805.602 1,06 3.776.706.952 4.606.471.770 21,97

including: - the calls, terminated in the own network

925.715.520 908.873.523 1,85 2.741.554.087 3.372.534.597 23,02

- the calls to other public mobile telephone networks of the Republic of Lithuania

276.838.708 280.332.022 -1,25 870.351.770 1.050.959.572 20,75

- the calls to public fixed telephone networks of the Republic of Lithuania

28.300.329 27.999.846 1,07 104.490.152 110.676.880 5,92

- international calls 19.071.922 19.597.512 -2,68 60.310.943 72.298.023 19,888. The duration of calls, terminated in the own network, total, min:

331.381.373 336.893.910 -1,64 1.107.591.106 1.284.202.308 15,95

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 24

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

including: - from public fixed telephone networks of the Republic of Lithuania

18.134.939 19.090.929 -5,01 78.614.528 75.744.563 -3,65

- from other public mobile telephone networks of the Republic of Lithuania

268.597.080 270.734.099 -0,79 858.683.083 1.030.120.504 19,97

- from the networks of foreign countries

44.649.354 47.068.882 -5,14 170.293.495 178.337.241 4,72

9. Duration of calls of the subscribers who make use of roaming services, min.:

12.277.572 12.403.305 -1,01 36.533.316 44.595.675 22,07

including: - duration of calls when calls are initiated by the subscribers who have left for foreign countries

5.770.474 6.137.319 -5,98 18.895.950 22.117.739 17,05

- duration of calls when calls are received by the subscribers who have left for foreign countries

6.507.098 6.265.986 3,85 17.637.366 22.477.936 27,44

10. Duration of calls of the subscribers of providers of foreign public mobile telephone services, who have arrived in the Republic of Lithuania and who make use of roaming services, min.:

7.967.312 10.559.154 -24,55 26.682.394 33.465.031 25,42

including: - duration of calls when calls are initiated by the subscribers of foreign public mobile telephone services, who have arrived in the Republic of Lithuania

3.990.642 4.790.937 -16,70 13.020.021 15.595.534 19,78

- duration of calls when calls are received by the subscribers of providers of foreign public mobile telephone services who have arrived in the Republic of Lithuania

3.976.670 5.768.217 -31,06 13.662.373 17.869.497 30,79

11 The revenues from provision of retail public mobile telephone network and/or services, thou. Litas (excluding the VAT):

310.203 321.219 -3,43 1.110.721 1.236.900 11,36

from: - consumers, who pay for the services against the bills

118.214 121.759 -2,91 - 472.598 -

- business subscribers, who pay for the services against the bills

120.213 118.011 1,87 - 456.964 -

- subscribers who make use of the prepaid service

71.776 81.449 -11,88 - 307.338 -

including: -the revenues, received for voice calls, including video calls

235.634 247.571 -4,82 - 952.407 -

- the revenues received for the forwarded SMS

35.125 35.621 -1,39 - 143.070 -

- the revenues, received for the forwarded MMS

385 390 -1,33 - 1.336 -

- the revenues received for the data transmission services, (using GPRS and/or EDGE and/or UMTS)

9.034 8.883 1,70 - 35.021 -

- other revenues 30.025 28.755 4,42 - 105.067 - 12. The revenues, received from calls, made by subscribers using roaming services, thou. Litas (excluding VAT):

27.160 32.996 -17,69 105.349 119.098 13,05

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 25

Name of indicator Quarter IV of 2007

Quarter III of 2007

Change in comparison

IIIQ, % 2006 2007

Change in comparison 2007 with 2006, %

from: - consumers, who pay for the services against the bills

6.389 9.029 -29,23 25.278 29.315 15,97

- business subscribers, who pay for the services against the bills

20.498 23.523 -12,86 80.071 88.668 10,74

- subscribers who make use of the prepaid service

273 444 -38,58 0 1.115

13. The revenues, received from foreign countries� public mobile telephone service providers for the calls, made by their subscribers who visit the Republic of Lithuania and use roaming services, thou. Litas (excluding the VAT)

12.475 18.456 -32,41 70.704 61.594 -12,88

14. The revenues from wholesale public mobile telephone network and/or service provision, thou. Litas (excluding VAT) (the item does not cover the revenues from networks interconnection activities)

7.345 7.577 -3,06 21.800 31.253 43,36

15. Revenues from the networks interconnection activity, in thou. Litas (excluding VAT)

117.778 116.065 1,48 393.028 446.415 13,58

including: - the revenues for termination of calls, initiated in public telephone networks of the Republic of Lithuania in the own network

95.525 96.901 -1,42 321.189 368.829 14,83

- the revenues for termination of calls, initiated in foreign networks in the own network

15.652 16.683 -6,18 60.770 63.153 3,92

In the fourth quarter of 2007 total revenue from the provision of public mobile telephone networks and services constituted LTL 344,71 million, revenue of Service providers were LTL 11,65 million. Out of the total revenues 77,07% were those received from provision of voice services, 10,19% were the revenues, received for the forwarded SMS, 0,11% � the revenues, received for the forwarded MMS, 2,62% - the revenues received for usage of data transmission services (GPRS, EDGE, UMTS), 7,88% � the revenues, received for calls from the subscribers, using the roaming services, 2,13% � the revenues from provision of wholesale public mobile telephone network and services.

In comparison with third quarter of 2007 total revenue decreased by 4,7%, revenue of Service providers decreased by 2,4%. In comparison with the year 2006 mobile telephone market in the year 2007 increased by 12,1%.

Fig. 20. Market shares of mobile fixed public telephone operators and providers of services by revenue, in % (total revenue � LTL 344,71 mill.)

Other Service providers1,18%

UAB "Eurocom"2,20%

UAB "Bitė Lietuva"28,75%

UAB "Omnitel"44,30%

UAB "Tele2"23,57%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 26

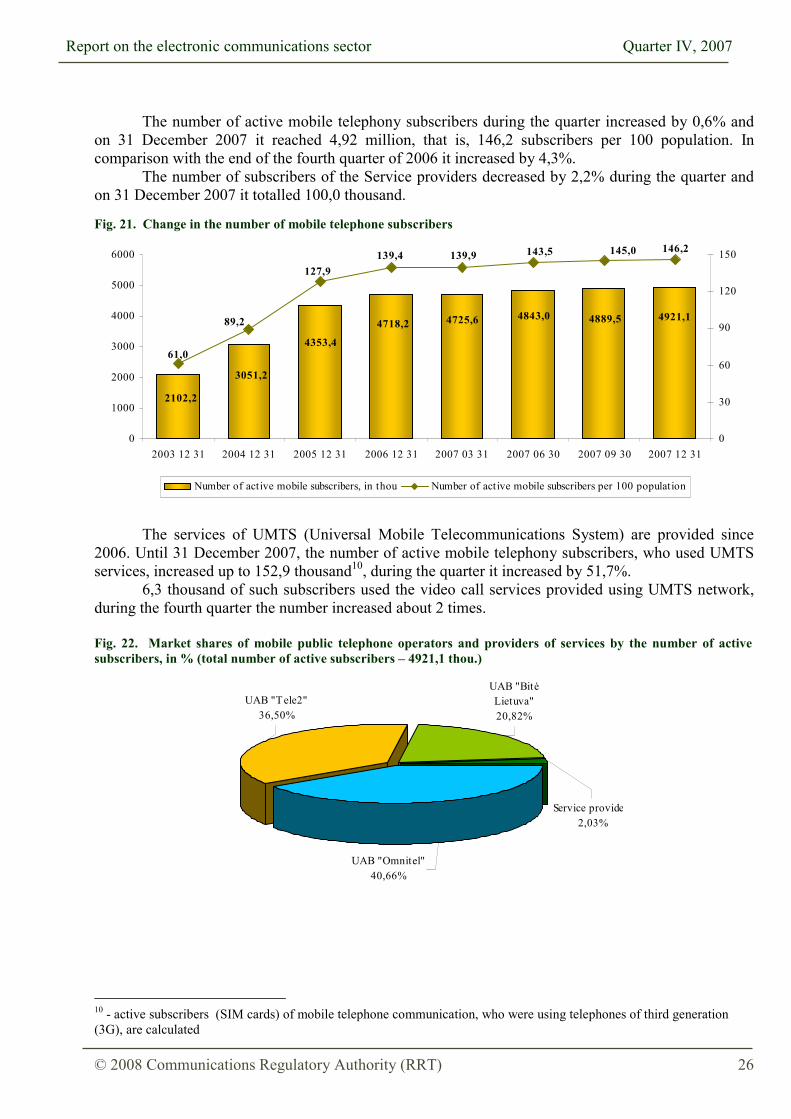

The number of active mobile telephony subscribers during the quarter increased by 0,6% and

on 31 December 2007 it reached 4,92 million, that is, 146,2 subscribers per 100 population. In comparison with the end of the fourth quarter of 2006 it increased by 4,3%.

The number of subscribers of the Service providers decreased by 2,2% during the quarter and on 31 December 2007 it totalled 100,0 thousand.

Fig. 21. Change in the number of mobile telephone subscribers

The services of UMTS (Universal Mobile Telecommunications System) are provided since

2006. Until 31 December 2007, the number of active mobile telephony subscribers, who used UMTS services, increased up to 152,9 thousand10, during the quarter it increased by 51,7%.

6,3 thousand of such subscribers used the video call services provided using UMTS network, during the fourth quarter the number increased about 2 times.

Fig. 22. Market shares of mobile public telephone operators and providers of services by the number of active subscribers, in % (total number of active subscribers � 4921,1 thou.)

10 - active subscribers (SIM cards) of mobile telephone communication, who were using telephones of third generation (3G), are calculated

4921,14889,54843,04718,2

4353,4

3051,2

2102,2

4725,6

146,2145,0143,5139,9139,4127,9

89,2

61,0

0

1000

2000

3000

4000

5000

6000

2003 12 31 2004 12 31 2005 12 31 2006 12 31 2007 03 31 2007 06 30 2007 09 30 2007 12 310

30

60

90

120

150

Number of active mobile subscribers, in thou Number of active mobile subscribers per 100 population

UAB "Tele2"36,50%

Service provide2,03%

UAB "Bitė Lietuva"20,82%

UAB "Omnitel"40,66%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 27

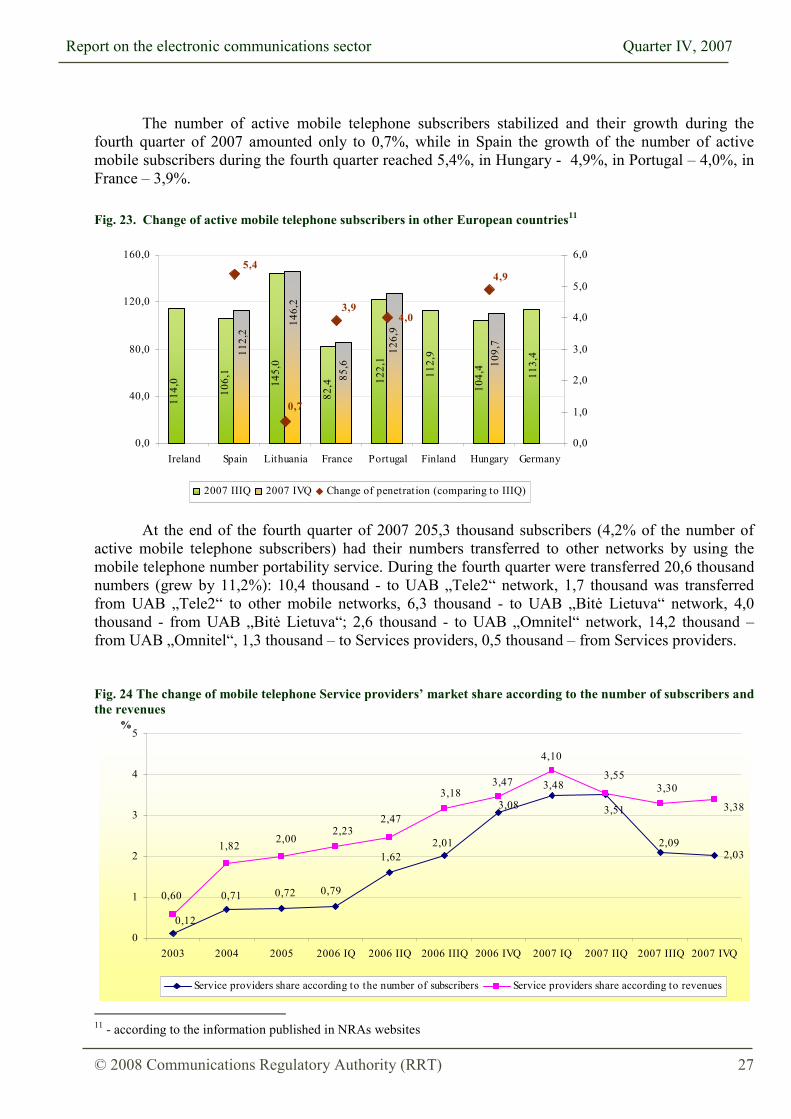

The number of active mobile telephone subscribers stabilized and their growth during the

fourth quarter of 2007 amounted only to 0,7%, while in Spain the growth of the number of active mobile subscribers during the fourth quarter reached 5,4%, in Hungary - 4,9%, in Portugal � 4,0%, in France � 3,9%.

Fig. 23. Change of active mobile telephone subscribers in other European countries11 At the end of the fourth quarter of 2007 205,3 thousand subscribers (4,2% of the number of

active mobile telephone subscribers) had their numbers transferred to other networks by using the mobile telephone number portability service. During the fourth quarter were transferred 20,6 thousand numbers (grew by 11,2%): 10,4 thousand - to UAB �Tele2� network, 1,7 thousand was transferred from UAB �Tele2� to other mobile networks, 6,3 thousand - to UAB �Bitė Lietuva� network, 4,0 thousand - from UAB �Bitė Lietuva�; 2,6 thousand - to UAB �Omnitel� network, 14,2 thousand � from UAB �Omnitel�, 1,3 thousand � to Services providers, 0,5 thousand � from Services providers.

Fig. 24 The change of mobile telephone Service providers� market share according to the number of subscribers and the revenues

11 - according to the information published in NRAs websites

113,

4

104,

4112,

9

122,

1

82,414

5,0

106,

1

114,

0

126,

9

109,

7

85,6

146,

2

112,

2

4,0

4,9

3,9

0,7

5,4

0,0

40,0

80,0

120,0

160,0

Ireland Spain Lithuania France Portugal Finland Hungary Germany0,0

1,0

2,0

3,0

4,0

5,0

6,0

2007 IIIQ 2007 IVQ Change of penetration (comparing to IIIQ)

2,031,622,01

3,48

3,51

0,71 0,72 0,79

3,08

2,09

0,12

1,82 2,002,23

2,47

3,183,47

4,10

3,553,30

0,60

3,38

0

1

2

3

4

5

2003 2004 2005 2006 IQ 2006 IIQ 2006 IIIQ 2006 IVQ 2007 IQ 2007 IIQ 2007 IIIQ 2007 IVQ

%

Service providers share according to the number of subscribers Service providers share according to revenues

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 28

Fig. 25. Market shares of mobile public telephone operators and providers of services by the number of active subscribers in different categories by consumers (paying against the bills): by business subscribers (paying against the bills): (total � 1056,6 thou.) (total number � 604,2 thou.) by pre-paid subscribers: (total number � 3260,3 thou.)

At the end of the fourth quarter of 2007 all subscribers of mobile telephone communication by categories were distributed as follows: 33,8% of subscribers who paid for the services against the bills, included 21,5% of consumers and 12,3% business subscribers, 66,2% of pre-paid subscribers. The common distribution of subscribers according to their categories has been almost changeless for several years, only the distribution according to the categories of each specific operator has been changing: share of the number of UAB �Omnitel� subscribers who paid for the services against the bills (from all active UAB �Omnitel� subscribers) at the end of the fourth quarter was 36,3% (during the year it decreased by 7,5 per cent), accordingly UAB �Bitė Lietuva� � 42,5% (during the year it increased by 9,6 per cent), UAB �Tele2� � 24,3% (during the year it increased by 1,4 per cent).

For the sake of comparison, according to the information, announced by national regulators, the number of subscribers, who have chosen the pre-paid services in Portugal as of the end of the fourth quarter of 2007 amounted to 76,7% of the total number of mobile telephone subscribers, accordingly in Hungary � 62,4%, in Spain � 41,4%, in France � 34,4%. Fig 26. Share of the number of mobile telephone pre- paid subscribers from the total mobile subscribers� number, %

UAB "Omnitel"42,4%

UAB "Tele2"34,2%

UAB "Bitė Lietuva"19,2%

Service providers

4,2%

UAB "Omnitel"46,2%

Service providers2,9%

UAB "Bitė Lietuva"38,4%

UAB "Tele2"12,4%

UAB "Omnitel"39,1%

UAB "Tele2"41,7%

UAB "Bitė Lietuva"18,1%

Service providers1,18%

76,766,0 62,4

41,434,4

0,0

20,0

40,0

60,0

80,0

100,0

Portugal Lithuania Hungary Spain France

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 29

Fig.27. Change in the number of subscribers in different categories (in thou.)

The number of the active subscribers, which use the pre-paid services in the fourth quarter of

2007 increased by 0,3% (during the year it increased by 3,2%), the number of subscribers, paying for the services against the bills: the number of consumers increased by 1,4% (during the year it increased by 5,2%), the number of business subscribers increased by 1,1% (during the year it increased 9,1%).

Fig 28. Change in the number of subscribers of mobile public telephone operators and Service providers in different categories (in thou.)

105710421015647 763 854 889 972 985 1005 1013

604597585553 482 462 467 494 522 554 568

326032503243

9021331

1737

2169

2888 29033160 3144

0

500

1000

1500

2000

2500

3000

3500

2003 1231

2004 0630

2004 1231

2005 0630

2005 1231

2006 0630

2006 1231

2007 0331

2007 0630

2007 0930

2007 1231

Consumers Business subscribers Pre-paid

362

448

304

389

450474

514 499 490 473458 457

203

134109 121 136

162 175 183 188 192 200207260

273 269 280 289 304 317 326 344

442 5 9 10 16 22 27 35 39 42

0

100

200

300

400

500

600

2003 1231

2004 0630

2004 1231

2005 0630

2005 1231

2006 0630

2006 1231

2007 0331

2007 0630

2007 0930

2007 1231

Con

sum

ers

75

18

279283279

389

299

257 238 243 252 267 270

232226219

149 153 167 176 188 198 208 215

7271

14 18 25 39 48 55 64 68

1716

113 13 14 14 16 15 16

0

100

200

300

400

500

2003 1231

2004 0630

2004 1231

2005 0630

2005 1231

2006 0630

2006 1231

2007 0331

2007 0630

2007 0930

2007 1231

Busin

ess s

ubsc

ribe

rs

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 30

Although the majority of subscribers are those using the pre-payment option the revenue

received from the subscribers of the said category in the fourth quarter of 2007 amounted about 21,4% (LTL 72,05 million, in comparison with previous quarter it decreased by 12,0%). The rest revenues received from subscribers, paying for the services against the bills, including: 36,9% (LTL 124,60 million, in comparison with previous quarter it decreased by 4,7%) revenue received from consumers, 41,7% (LTL 140,71 million, in comparison with previous quarter it decreased by 0,6%) - from business subscribers.

The duration of calls initiated in mobile public telephone networks in the fourth quarter of 2007 in comparison with the previous quarter increased by 1,1% and totalled 1249,93 million minutes: 40,1% in the network of UAB �Omnitel�, 26,5% in the network of UAB �Bitė Lietuva�, 30,5% in the network of UAB �Tele2� and 2,9% by Service providers.

Total duration of calls initiated in mobile public telephone networks in the year 2007 in comparison with the year 2006 increased by 22,0%.

Off the total duration of the calls, originated in public mobile telephone networks in the fourth quarter of 2007 74,1% were the calls inside the own network, 22,1% - the calls to other public mobile telephone networks of the Republic of Lithuania, 2,3% - the calls to public fixed telephone networks of the Republic of Lithuania, 1,5% - international calls. During the fourth quarter of 2007, in comparison with the third quarter of 2007, the duration of the calls inside the own network grew by 1,9%, the calls to public fixed telephone networks of the Republic of Lithuania - by 1,1%,duration of the calls to other public mobile telephone networks of the Republic of Lithuania decreased by 1,2%, international calls - by 2,7%.

127412581133975973

886885

683557

429353

589611681

748797817858

578

420387216

1359133713141308128711661144

897759

515

332

3943115113103

341111000

200

400

600

800

1000

1200

1400

1600

2003 1231

2004 0630

2004 1231

2005 0630

2005 1231

2006 0630

2006 1231

2007 0331

2007 0630

2007 0930

2007 1231

Pre-

paid

Omnitel Bitė Lietuva Tele2 Service providers

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 31

Fig. 29. Distribution of calls initiated in mobile public Fig. 30. Distribution of calls initiated in mobile public telephone networks, which are terminated on-net telephone networks, which are terminated in other (total duration is 925,72 mill. min. ) mobile telephone networks of the Republic of Lithuania

(total duration is 276,84 mill. min.) Fig. 31 Distribution of calls initiated in mobile public Fig. 32. Distribution of calls initiated in mobile public telephone networks, which are terminated in fixed telephone networks, which are terminated in the public telephone networks of the Republic of Lithuania networks of foreign countries

total duration is 28,30 mill. min.) (total duration is 19,07 mill. min.)

The duration of calls, initiated by Lithuania�s mobile telephone subscribers, using roaming

services, in the fourth quarter of 2007 in comparison with the third quarter of 2007 decreased by 6,0% and totalled 5,77 million minutes. Subscribers of public mobile telephone service providers of foreign countries that came to the Republic of Lithuania and used roaming services in the fourth quarter of 2007 initiated 3,99 million minutes of calls, comparing with the third quarter of 2007 the duration of such calls decreased by 16,7%.

The using of roaming services grows in average about 20% annually: in the year 2007 in comparison with the year 2006, the duration of calls, initiated by Lithuania�s mobile telephone subscribers, using roaming services, increased by 17,1%; the duration of calls initiated by subscribers of public mobile telephone service providers of foreign countries increased by 19,8%.

The duration of calls terminated in mobile telephone networks, which were initiated in other

networks, in the fourth quarter of 2007 in comparison with the last quarter decreased by 1,6% and totalled 331,38 million minutes, including 37,5% in the network of UAB �Omnitel�, 30,6% in the network of UAB �Bitė Lietuva�, 31,9% in the network of UAB �Tele2�.

Total duration of calls terminated in mobile telephone networks, which were initiated in other networks in the year 2007 in comparison with the year 2006 increased by 15,9%.

UAB "Tele2"31,9%

UAB "Bitė Lietuva"25,4%

UAB "Omnitel"40,8%

Service providers1,9%

UAB "Tele2"25,3%

UAB "Bitė Lietuva"30,5%

Service providers6,2%

UAB "Omnitel"38,0%

UAB "Tele2"33,0%

UAB "Bitė Lietuva"24,6%

Service providers2,9%

UAB "Omnitel"39,4%

UAB "Tele2"34,9%UAB "Bitė

Lietuva"23,7%

Service providers4,1%

UAB "Omnitel"37,3%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 32

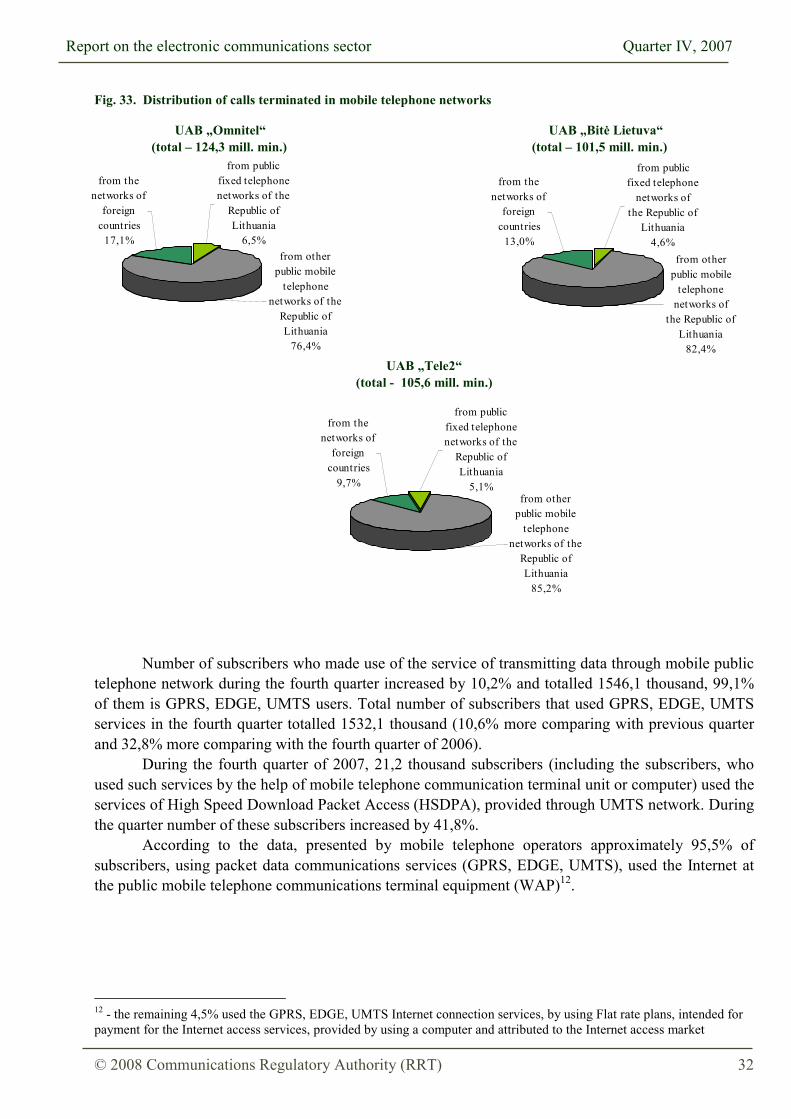

Fig. 33. Distribution of calls terminated in mobile telephone networks

UAB �Omnitel� UAB �Bitė Lietuva� (total � 124,3 mill. min.) (total � 101,5 mill. min.)

UAB �Tele2� (total - 105,6 mill. min.)

Number of subscribers who made use of the service of transmitting data through mobile public

telephone network during the fourth quarter increased by 10,2% and totalled 1546,1 thousand, 99,1% of them is GPRS, EDGE, UMTS users. Total number of subscribers that used GPRS, EDGE, UMTS services in the fourth quarter totalled 1532,1 thousand (10,6% more comparing with previous quarter and 32,8% more comparing with the fourth quarter of 2006).

During the fourth quarter of 2007, 21,2 thousand subscribers (including the subscribers, who used such services by the help of mobile telephone communication terminal unit or computer) used the services of High Speed Download Packet Access (HSDPA), provided through UMTS network. During the quarter number of these subscribers increased by 41,8%.

According to the data, presented by mobile telephone operators approximately 95,5% of subscribers, using packet data communications services (GPRS, EDGE, UMTS), used the Internet at the public mobile telephone communications terminal equipment (WAP)12.

12 - the remaining 4,5% used the GPRS, EDGE, UMTS Internet connection services, by using Flat rate plans, intended for payment for the Internet access services, provided by using a computer and attributed to the Internet access market

from public fixed telephone networks of the

Republic of Lithuania

6,5%

from the networks of

foreign countries

17,1%from other

public mobile telephone

networks of the Republic of Lithuania

76,4%

from other public mobile

telephone networks of

the Republic of Lithuania

82,4%

from the networks of

foreign countries

13,0%

from public fixed telephone

networks of the Republic of

Lithuania4,6%

from public fixed telephone networks of the

Republic of Lithuania

5,1%

from the networks of

foreign countries

9,7%from other

public mobile telephone

networks of the Republic of Lithuania

85,2%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 33

Fig. 34. Distribution of the number of mobile telephone subscribers, who made use of GPRS during the fourth quarter of 2007, % (total number � 1532,1 thou.)

In the fourth quarter of 2007 in comparison with the third quarter the amount of data, sent and

received by using the GPRS, EDGE, UMTS technologies increased by 57,9% and amounted to approximately 141,10 million megabytes (MB), including 116,50 million MB of received data. In average one subscriber sent and received 30,7 MB per month (9,2 MB more than in the third quarter of 2007), including 25,3 MB of received data.

The amount of data, sent and received by UAB �Omnitel� subscribers was 81,8 million MB (in average one subscriber sent and received 36,3 MB), accordingly UAB �Bitė Lietuva� � 57,1 million MB (39,5 MB), UAB �Tele2� � 6,0 million MB (7,0 MB).

In the fourth quarter of 2007 mobile telephone subscribers sent 2394,18 million short messages

(SMS) and 1,59 million illustrated short messages (MMS). 89,6% of the recipients of the SMS, sent in the fourth quarter were subscribers of the own

network, 9,1% were subscribers of other public mobile telephone networks of the Republic of Lithuania, 1,2% - subscribers of foreign countries� networks. 88,1% of the recipients of the MMS, sent in the fourth quarter were subscribers of the own network, 9,6% were subscribers of other public mobile telephone network of the Republic of Lithuania, 2,2% - subscribers of foreign countries� networks.

During the said quarter 10,6% more SMS and 0,2% more MMS messages were sent than during the third quarter of 2007. During the year 2007 3,8% more SMS and 43,4% more MMS were sent than during the year 2006.

Fig. 35. Distribution of the number of short messages (SMS) sent by mobile telephone subscribers during the fourth quarter of 2007, in % (total number � 2394,18 mill.)

UAB "Tele2"18,9%

UAB "Omnitel"48,6%

UAB "Bitė Lietuva"31,4%

Service providers1,1%

Service providers0,2%

UAB "Bitė Lietuva"23,9%

UAB "Omnitel"35,0%

UAB "Tele2"40,9%

Report on the electronic communications sector Quarter IV, 2007

© 2008 Communications Regulatory Authority (RRT) 34

Fig. 36. Distribution of the number of illustrated short messages (MMS) sent by mobile telephone subscribers during the fourth quarter of 2007, in % (total number � 1,59 mill.)

One subscriber sent on average 162 SMS messages and 0,1 MMS messages per month. One