report on experiences with structural separation · pdf filereport on experiences with...

TRANSCRIPT

Report on Experiences with Structural Separation 2011

The OECD Competition Committee held several discussions on structural separation which resulted in a report approved in 2011. These discussions also led to a revision in December 2011 of the 2001 Council Recommendation Concerning Structural Separation in Regulated Industries.

Report on Experiences with Structural Separation (2006) Recommendation of the Council concerning structural separation in regulated industries (2001) Restructuring Public Utilities for Competition (2001)

This report reviews the experience of structural separation ten years after the adoption of the 2001 OECD Council Recommendation Concerning Structural Separation in Regulated Industries with a focus on four sectors: electricity, gas, railways and telecommunications. It shows that structural separation remains a relevant remedy to advance the process of market liberalisation. However, the impact of separation policies on investment incentives has been an issue throughout the sectors. Corporate incentives to invest require full consideration in the assessment of whether structural separation may be appropriate for a sector. As a result, the 2001 Recommendation was amended by the OECD Council on 13 December 2011 to address the role that corporate incentives to invest can play in assessing the desirability of structural separation in regulated industries.

Rep

ort

on

Exp

erie

nces

with

Str

uctu

ral S

epar

atio

n

COMPETITION COMMITTEE

JANUARY 2012

Report on Experiences with Structural Separation

COMITÉ DE LA CONCURRENCE

JANVIER 2012

Rapport sur les Expériences en Matière de Séparation Structurelle

Rap

po

rt sur les Exp

ériences en Matière d

e Sép

aration S

tructurelle

3

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

FOREWORD

On 26 April 2001, the OECD Council adopted a Recommendation Concerning

Structural Separation in Regulated Industries suggesting to Member countries

that when regulated firms have activities that are potentially competitive and

that are linked to non-competitive activities, such as natural monopoly

activities, governments should consider the benefits and costs of structural

measures separating two activities. The Recommendation was accompanied by

a detailed report, and both advocated careful consideration of the potential pros

and cons of structural separation versus the potential pros and cons of

behavioural measures. In 2006, the Competition Committee reported to Council

on the implementation of the Recommendation. This report focused on five

topics: benefits of structural separation, costs of structural separation, balancing

benefits and costs, experiences with separation in energy, railways,

telecommunications and postal services and government actions with respect to

structural separation in OECD countries. It concluded that the Recommendation

was important and relevant and should remain in its current form. The Council

endorsed these conclusions and invited the Competition Committee to continue

reporting back on the implementation of the Recommendation.

This third report reviews the experience of structural separation ten years after

the adoption of the Recommendation with a focus on four sectors: electricity,

gas, railways and telecommunications. It shows that structural separation

remains a relevant remedy to advance the process of market liberalisation.

However, the impact of separation policies on investment incentives has been

an issue throughout the sectors and the 34 member countries surveyed in the

report. Corporate incentives to invest require therefore full consideration in the

assessment of whether structural separation may be appropriate for a sector. As

a result, the 2001 Recommendation was amended by the OECD Council on

13 December 2011 to address the role that corporate incentives to invest can

play in assessing the desirability of structural separation in regulated industries.

The revised Council Recommendation is appended to this Report.

5

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

TABLE OF CONTENTS

REPORT ON EXPERIENCES WITH STRUCTURAL SEPARATION ...................... 7

1. Introduction ...................................................................................... 7 2. Structural separation as a remedy ................................................... 16 3. Developments in gas ....................................................................... 27

3.1 Gas sector in Chile ............................................................ 27 3.2 Gas sector in Estonia ........................................................ 28 3.3 Gas sector in the European Union .................................... 28 3.4 Gas sector in Greece ......................................................... 40 3.5 Gas sector in Ireland ......................................................... 41 3.6 Gas sector in Israel ............................................................ 42 3.7 Gas sector in Portugal ....................................................... 42 3.8 Gas sector in the Netherlands ........................................... 43 3.9 Gas sector in Poland ......................................................... 44 3.10 Gas sector in Slovenia ...................................................... 45 3.11 Gas sector in Turkey ......................................................... 45

4. Developments in electricity ............................................................ 46

4.1 Electricity sector in Australia ........................................... 46

4.2 Electricity sector in Chile ................................................. 48

4.3 Electricity sector in Estonia .............................................. 49

4.4 Electricity sector in the European Union .......................... 50

4.5 Electricity sector in Finland .............................................. 56

4.6 Electricity sector in Germany ........................................... 57

4.7 Electricity sector in Greece ............................................... 58

4.8 Electricity sector in Ireland ............................................... 59

4.9 Electricity sector in Israel ................................................. 60

4.10 Electricity sector in Italy ................................................... 60

4.11 Electricity sector in Mexico .............................................. 61

4.12 Electricity sector in New Zealand ..................................... 62

4.13 Electricity sector in the Netherlands ................................. 64

4.14 Electricity sector in Portugal............................................. 65

4.15 Electricity sector in Switzerland ....................................... 66

4.16 Electricity sector in Slovenia ............................................ 67

6

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

5. Developments in telecommunications ............................................ 68

5.1 Telecommunications sector in Australia ........................... 68

5.2 Telecommunications sector in Chile................................. 71

5.3 Telecommunications sector in Estonia ............................. 71

5.4 Telecommunications sector in the European Union ......... 72

5.5 Telecommunications sector in Finland ............................. 75

5.6 Telecommunications sector in Israel ................................ 75

5.7 Telecommunications sector in Italy .................................. 76

5.8 Telecommunications sector in New Zealand .................... 78

5.9 Telecommunications sector in Poland .............................. 79

5.10 Telecommunications sector in Slovenia ........................... 81

5.11 Telecommunications sector in Sweden ............................. 82

5.12 Telecommunications sector in Switzerland ...................... 82

5.13 Telecommunications sector in the United Kingdom ........ 83

6. Developments in rail .......................................................................... 85

6.1 Rail sector in Australia ..................................................... 85

6.2 Rail sector in Belgium ...................................................... 88

6.3 Rail sector in Canada ........................................................ 88

6.4 Rail sector in Chile ........................................................... 91

6.5 Rail sector in Estonia ........................................................ 92

6.6 Rail sector in the European Union .................................... 93

6.7 Rail sector in France ......................................................... 96

6.8 Rail sector in Germany ..................................................... 98

6.9 Rail sector in Israel ........................................................... 98

6.10 Rail sector in Italy ............................................................. 99

6.11 Rail sector in the Netherlands ......................................... 100

6.12 Rail sector in Slovenia .................................................... 101

6.13 Rail sector in Spain ......................................................... 102

6.14 Rail sector in Sweden ..................................................... 102

6.15 Rail sector in the United Kingdom ................................. 105

6.16 Rail sector in the United States ....................................... 107

7. Corporate Incentives to Invest and Structural Separation ................ 108

8. Conclusion........................................................................................ 112

ANNEX: RECOMMENDATION OF THE COUNCIL CONCERNING

STRUCTURAL SEPARATION IN REGULATED INDUSTRIES.............................. 118

7

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

REPORT ON EXPERIENCES WITH STRUCTURAL SEPARATION

1. Introduction

In 2001, the OECD Council adopted its ―Recommendation of the Council

Concerning Structural Separation in Regulated Industries‖,1 suggesting to

Member countries that they consider the implementation of structural measures

in regulated sectors in appropriate circumstances. This report provides an

update on Member countries‘ experiences in applying the Recommendation.

The Recommendation was accompanied by a detailed report that

considered the benefits and the costs associated with the adoption of structural

separation policies.2 The main body of the Recommendation takes a similar

approach, advocating careful consideration of both the potential pros and cons

of structural separation versus the potential pros and cons of behavioural

measures. It reads as follows:

When faced with a situation in which a regulated firm is or may in the

future be operating simultaneously in a non-competitive activity and a

potentially competitive complementary activity, Member countries

should carefully balance the benefits and costs of structural measures

against the benefits and costs of behavioural measures.

The benefits and costs to be balanced include the effects on

competition, effects on the quality and cost of regulation, the

transition costs of structural modifications and the economic and

public benefits of vertical integration, based on the economic

characteristics of the industry in the country under review.

The benefits and costs to be balanced should be those recognised by

the relevant agency(ies) including the competition authority, based on

principles defined by the member country. This balancing should

1 Structural Separation in Regulated Industries (2001).

2 OECD, Restructuring Public Utilities for Competition (2001) and OECD,

Structural Separation in Regulated Industries (2001).

8

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

occur especially in the context of privatisation, liberalisation or

regulatory reform.

A ―Report on Experiences with Structural Separation‖ was published by

the Competition Committee in 2006. The report considers the costs and benefits

of structural separation, examines in detail a selected set of examples of

structural separation in five sectors and provides a summary of country

experiences across the OECD as a whole. The 2006 report concludes that:

The Recommendation is still important and relevant;

Its suggestion to balance the costs and benefits of structural separation

still holds, as does the view that the costs and benefits will differ

based on the economic characteristics of the industry in the country

under review; and

The Council Recommendation should remain in place as it is.3

This second report provides an update on experiences with structural

separation in Member countries with respect to four industries: gas, electricity,

telecommunications and rail.4 Ten years on from the adoption of the

Recommendation, the conclusions remain broadly the same. Structural

separation is a remedy of continued relevance, which can both advance the

process of market liberalisation and address some of the difficulties inherent to

behavioural remedies and more complex and intensive sector regulation.

Nevertheless, structural separation may not be necessary or appropriate in all

industries or markets. In particular, the impact of structural separation or the

lack thereof on corporate incentives to invest in network industries has become

a prominent issue. The choice of structural versus behavioural measures, in a

given set of circumstances, therefore remains a matter that requires careful

evaluation.

Structural solutions to competition problems differ from behavioural

measures insofar as structural policies modify the incentives, whereas

behavioural remedies try to redress specific conduct in a context where

3 OECD Competition Committee, Report on Experiences with Structural

Separation, published 7 June 2006, p.6.

4 With respect to Member countries that have joined the OECD since the

publication of the 2006 report, information of a more general nature is

provided, not being limited to recent developments.

9

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

incentives remain essentially unchanged.5 The Recommendation elaborates

upon this distinction, noting that ―behavioural policies, unlike structural

policies, do not eliminate the incentive of the regulated firm to restrict

competition‖ and that ―despite the best efforts of regulators, regulatory controls

of a behavioural nature, which are intended to control the ability of an

integrated regulated firm to restrict competition, may result in less competition

than would be the case if the regulated firm did not have the incentive to restrict

competition‖. It further emphasizes that ―certain forms of partial separation of

a regulated firm (such as accounting separation or functional separation) may

not eliminate the incentive of the regulated firm to restrict competition and

therefore may be less effective in general at facilitating competition than

structural policies‖. While structural remedies are frequently viewed as more

intrusive upon property rights than behavioural remedies,6 in the longer run the

―clean break‖ offered by structural solutions may prove to be less intrusive than

requiring a firm to adhere to detailed, prescriptive behavioural commitments

that are unending in nature.

In regulated infrastructure industries, structural separation typically divides

a formerly integrated company into competitive and non-competitive parts. The

crux of separation is not merely a wholesale/retail divide; rather, the objective is

5 The 2001 report describes the distinction between these two types of

measures as ―those that primarily address the incentives on the incumbent to

restrict competition ("structural") approaches, and those that primarily

control the ability of the incumbent to restrict competition ("behavioural"

approaches)‖, and emphasises that ―[u]nder behavioural approaches, the

regulator must struggle against the incentives of the incumbent to deny, delay

or restrict access. Compared to the incumbent firm the regulator is usually at

a disadvantage with respect to information and to the possible instruments of

control. As a result, the level of competition under behavioural approaches is

less than if the incumbent did not have the incentive to restrict competition.

Certain tools, such as accounting separation, management separation or

corporate separation, are not effective on their own, but may support other

approaches, such as access regulation‖; see OECD, Restructuring Public

Utilities for Competition (2001), at p.53. See also P. Hellström, F. Maier-

Rigaud & F. Wenzel Bulst, ―Remedies in European Antitrust Law‖ (2009) 76

Antitrust law Journal 43 for further discussion of the incentive-based

distinction between behavioural and structural remedies. Of course, structural

remedies may not only change the incentives but may simply take away the

ability of the firm to influence the network.

6 Under EU competition law, for example, structural remedies can be imposed

for breaches of the competition rules only where there are no equally

effective behavioural remedies available, or where any equally effective

behavioural remedy would be more burdensome than the structural remedy.

10

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

to isolate only those assets that cannot be replicated.7 This separation can take a

variety of forms ranging from behavioural to structural measures. Accounting

separation constitutes the weakest form of separation available, and ownership

separation the strongest. In between these poles, ―six degrees‖ of functional (or

operational) separation options have been identified: creation of a wholesale

division; virtual separation; business separation; business separation with

localised incentives; business separation with separate governance

arrangements; and legal separation involving separate legal entities under the

same ownership.8 While ownership separation clearly is a structural measure,

separation measures falling short of ownership separation, such as for example

the Independent Transmission Operator (ITO) concept in energy, are typically

considered to be behavioural measures9, with the exception of certain types of

functional separation, that is, the separation of ownership and control that has

sometimes been considered a hybrid form between the two, for example the

Independent System Operator (ISO) in energy.10

The extent to which separation of a vertically integrated firm is viewed as

economically and commercially desirable, and the form of separation preferred,

tends to vary from sector to sector. As ―forcing‖ competition via structural

separation can have significant costs—both financial and efficiency-based—it is

important to determine whether increased competition in the market concerned

actually brings with it increased benefits for consumers. In the European Union

(EU), for example, Member States are required to implement either ownership

or functional separation in the electricity and gas sectors, whereas functional

separation in telecommunications markets is presented as an exceptional

measure for implementation only in cases of persistent market failure. Factors

of relevance to the determination as to whether and what form of separation

may be appropriate in a particular sector include the presence of economies of

7 European Regulators Group, Opinion on Functional Separation (ERG (07)

44) 2007, p.8.

8 M. Cave, ―Six Degrees of Separation: Operation Separation as a Remedy in

European Telecommunications Regulation‖ 64 Communications and

Strategies (4th

quarter 2006), p.1-15.

9 See the Recommendation, in particular the passages quoted above.

10 See for example OECD, Restructuring Public Utilities for Competition

(2001), p. 14. In contrast to this, others such as the French

telecommunications regulator, l‘Autorité de Régulation des Communications

Électroniques et des Postes (ARCEP), would expressly categorise legal

separation falling short of full ownership separation as a form of structural

separation; see ARCEP, La Lettre de l‘Authorité, No.55 – March/April 2007,

p.4.

11

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

scale and scope, the likely impact on levels of investment, the rate of

technological innovation in a sector and the effectiveness of other forms of

regulatory intervention. Moreover, the costs and benefits associated with each

form of separation differ. While accounting separation, the least intrusive form

of separation, may help to eliminate price discrimination against downstream

competitors, non-price discrimination may necessitate a more intensive solution

such as functional or even ownership separation.

Although the Recommendation is directed at OECD Member countries,

experience to date suggests that the decision to implement structural separation

is often taken by the vertically integrated firm itself, rather than by the national

regulatory agencies or competition authority. A firm may decide to separate

voluntarily in order to pre-empt more complete forms of separation being

imposed by legislation or in the framework of competition proceedings; it may

prefer structural measures as a means by which to escape demanding

behavioural regulation; or separation may present the most attractive business

option for the profit-maximising firm. It is unusual for a vertically integrated

firm to drive the separation process entirely of its own initiative—typically, the

issue is first introduced by regulators or other government bodies. Nevertheless,

once separation has been placed on the policy agenda, ―voluntary‖ compliance

by firms is not uncommon. This has been the experience in the

telecommunications sector in Sweden, for example, where the incumbent‘s

decision to adopt functional separation voluntarily has thus far negated the need

for the regulator to exercise its statutory power to impose compulsory functional

separation on the firm. Voluntary commitments involving structural separation

play an important role in competition law practice. While it is common practice

that structural commitments (business divestitures) are offered to obtain

regulatory clearance in the field of merger control, voluntary structural

separation commitments are increasingly offered also in the field of antitrust

enforcement in recent years. Notably the European Commission has accepted

binding commitments with respect to structural separation when settling

antitrust investigations without a formal finding of breach.11

On the other hand, in certain circumstances separation is an involuntary

process for the vertically integrated firm, being a remedy imposed upon it under

statute, or by regulators or competition law enforcers. For legislators and sector

regulators, structural separation offers a more durable resolution in cases of

persistent market failure. Structural separation can provide the means by which

to remedy market problems that behavioural regulation alone may fail to

11

See the RWE, ENI and E.ON cases discussed below. Structural commitments

were also applied in EU State Aid cases.

12

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

prevent, the classic example being non-price discrimination. Separation may

also be preferred in circumstances where the alternative behavioural regulation

would prove complex or difficult to design, follow and enforce. Structural

solutions bring the benefit of legal certainty, and typically, a simplified

regulatory regime. Compulsory separation imposed by regulation has been

common in the energy sector, particularly within the EU, where Member States

must comply with the requirements of the European Commission‘s energy

markets liberalisation programme.

Structural separation is occasionally imposed by competition authorities

for similar reasons. Where a breach of the competition rules is on-going and

linked to a vertically integrated market structure, separation can provide an

effective and durable remedy. Moreover, solutions of a structural nature require

comparatively little ex post monitoring, unlike behavioural remedies, which

frequently require competition authorities to engage in supervisory activities of

a quasi-regulatory nature.12

The break-up of AT&T in 1984, on foot of an

antitrust lawsuit brought by the Department of Justice in the United States, is a

prominent example of the use of competition law enforcement powers to effect

structural separation of an integrated firm.13

It is generally accepted that structural separation may involve a trade-off

between efficiency and competition. Since the Recommendation was issued in

2001, a voluminous literature has been produced that considers the value of

structural separation in view of its associated costs and benefits. There is

significant evidence that profit maximising vertically integrated firms typically

make efficient decisions, from the point of view of both, the firm and of

consumers, but where the vertically integrated firm controls a bottleneck

monopoly, foreclosure can be a problem.14

Others argue that discrimination by a

vertically integrated firm is never a rational strategy, on the basis that any gains

12

For a discussion of the behavioural-versus-structural remedies debate in the

EU context, see P. Lowe & F. Maier-Rigaud, Chapter 20, ―Quo Vadis

Antitrust Remedies‖ in B.E. Hawk (ed.), Annual Proceedings of the Fordham

Competition Law Institute (2008, New York), pp.597-611.

13 United States v. AT&T 552 F. Supp. 131 (D.D.C. 1982).

14 See F. Lafontaine & M. Slade, ―Vertical Integration and Firm Boundaries:

The Evidence‖ (2007) 45(3) Journal of Economic Literature 629-685, and

P.L. Joskow, Chapter 11, ―Vertical Integration‖ in ABA Section of Antitrust

Law, Issues in Competition Law and Policy, Volume I (2008, Chicago),

pp.273-292.

13

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

at the retail level will be negated by concomitant losses at the wholesale level;15

yet, plausible theories of anticompetitive leverage and foreclosure of upstream,

downstream and even related retail markets can be found in both literature and

case law.16

Within the literature addressing specifically structural separation and

its effects, one finds both work that supports and work that criticises the use of

such policies in order to address competition problems. There is no clear

consensus among scholars as to the objective value of structural separation in

the abstract. Separation can be costly, both in terms of one-off costs of

implementation and longer term efficiency losses.17

Nonetheless, within

assessments of specific examples of structural separation, it is clear that

economic benefits have been observed.18

It is important to note the strong

15

See, for example, D.W. Carlton, ―Should ―Price Squeeze‖ be a Recognized

Form of Anticompetitive Conduct?‖ (2008) 4 Journal of Competition Law &

Economics 271, at p.275, for a clear statement of the Chicago School ―one

monopoly profit‖ precept.

16 See, for example, N. Economides, ―Vertical Leverage and the Sacrifice

Principle: Why the Supreme Court Got Trinko Wrong‖ (2005) 61 NYU

Annual Survey of American Law 379 and D. Geradin & R. O‘Donoghue,

―The Concurrent Application of Competition Law and Regulation: The Case

of Margin Squeeze Abuses in the Telecommunications Sector‖ (2005) 1

Journal of Competition Law & Economics 355 for discussion of potential

harms to competition.

17 See OECD, Restructuring Public Utilities for Competition (2001) at p.24, for

a discussion of the economics of scope associated with vertical integration:

―Vertical integration may enhance the availability of information (allowing

more efficient incentive contracts); may reduce transactions costs and

improve investment in relationship specific assets by overcoming hold-up

problems; and may reduce the distortions associated with market power at

one or both of the two levels.‖ While many of these potential sources of cost

efficiencies can, alternatively, be exploited through contractual arrangements

between separate firms, in practice contractual arrangements often prove to

be impractical. However, the 2001 report argues that while the theoretical

possibility of economies of scope may be recognised, assessing their

magnitude in practice is very difficult (ibid., pp.24-26).

18 For a sample of the broad range of positions on the topic, see R.W. Crandall,

J.A. Eisenach & R.E. Litan, ―Vertical Separation of telecommunications

Networks: Evidence from Five Countries‖ (2010) 62(3) Federal

Communications Law Journal 493-539; M.G. Pollitt, ―Electricity

Liberalisation in the European Union: A Progress Report‖ EPRG Working

paper 0929, published December 2009; M. de Nooij & B. Baarsma, ―Divorce

comes at a price : An ex ante welfare analysis of ownership unbundling of the

distribution and commercial companies in the Dutch energy sector‖ (2009)

37 Energy Policy 5449-5458; T. Tropina, J. Whaley & P. Curwen,

14

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

influence of industry sponsorship on this particular issue, which raises some

questions with regards to the impartiality of work dealing with the topic.19

An issue of increasing importance, in the context of the debate regarding

structural separation, is the impact of such arrangements on investment

incentives, in particular relating to infrastructure development. On the one hand,

uncertainty regarding the possible implementation of structural separation or

misaligned incentives for the infrastructure operator where separation has

already been implemented may deter otherwise desirable investment in the

network. Given that many regulated industries will require significant

―Functional separation within the European Union: Debates and Challenges‖

(2010) 27 Telematics and Informatics 231-241; R. Cadman, ―Means not

Ends: Deterring Discrimination through Equivalence and Functional

Separation‖ (2010) 34 Telecommunications Policy 366-374; S. Dorigoni & F.

Pontoni, ―Ownership Separation of the Gas Transportation Network: Theory

and Practice‖ IEFE Working Paper Series No.9, published March 2008; R.

Gonçalves & A. Nascimento, ―The Momentum for Network Separation: A

Guide for Regulators‖ (2010) Telecommunications Policy 355-365; B.

Howell, R. Meade & S. O‘Connor, ―Structural Separation versus Vertical

Integration: Lessons for Telecommunications from Electricity Reforms‖

(2010) 34 Telecommunications Policy 392-403; A. Prandini, ―Good, BETTA,

Best? The Role of Industry Structure in Electricity Reform in Scotland‖

(2007) 35 Energy Policy 1628-1642; M.G. Pollitt, ―The Arguments For and

Against Ownership Unbundling of Energy Transmission Networks‖ (2008)

36 Energy Policy 704-713; M.A. Jamison & J. Sichter, ―Business Separation

in Telecommunications : Lessons from the US Experience‖ (2010) 9(1)

Review of Network Economics, Article 3 (available at www.bepress.com/rne);

R.W. Crandall, ―The Remedy for the ―Bottleneck Monopoly‖ in Telecom:

Isolate It, Share It or Ignore It‖ (2005) 72 University of Chicago Law Review

3; S. Everett, ―Deregulation and Reform of Rail in Australia: Some Emerging

Constraints‖ (2006) 13 Transport Policy 74; B. Moselle & D. Black,

―Vertical Separation as an Appropriate Remedy‖ (2001) 2(1) Journal of

European Competition Law & Practice 84; and F. Kirsch & C. von

Hirschhausen, ―Regulation of NGN: Structural Separation, Access

Regulation, or No Regulation at All?‖ (2008) 69 Communications & Strategies

63. A report issued recently by the Berkman Center for Internet & Society,

Next Generation Connectivity: A review of broadband Internet transitions and

policy from around the world (February 2010) Final Report, contains a

comprehensive review of the available literature assessing the effectiveness of

―open access‖ policies, including functional separation, in the

telecommunications sector.

19 Berkman Report, cited fn. 18 above.

15

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

investments in the coming years,20

the claimed negative effects of structural

separation on investment incentives and the cost of capital is an issue of general

relevance. On the other hand, where vertical integration remains in place, there

is a risk that the integrated firm will engage in strategic under-investment in its

infrastructure, in a bid to circumvent access obligations. In such circumstances,

the decision to separate may lead to greater investment in infrastructure

development. Implementation of structural separation can also result in

increased investment by new entrants into the competitive portions of the sector.

Even with respect to vertically integrated firms, the effects of uncertainty on

investment incentives can be over-exaggerated—in particular, where the sale of

the separated asset is conducted in such a manner as to secure its full market

value. Thus, the impact of structural separation on investment incentives

remains an open yet critically important issue to be considered.

The Recommendation on structural separation incorporates the various

aspects of this lively debate. It asks Member countries to evaluate both the

likely costs and benefits of structural separation within regulated sectors. These

costs and benefits are then weighed against each other, in order to assess

whether and what form of separation should be mandated for vertically

integrated firms in that market. Structural separation is not always the necessary

or best response to vertical integration of firms that operate in both competitive

and non-competitive markets, but it can be an economically efficient one in

both the short and longer terms. The following sections of the report consider

the availability of structural separation as a remedy and experiences in

implementing structural separation in Member countries since the publication of

the 2006 report, examining four regulated sectors: gas, electricity,

telecommunications and rail. Information is also included regarding the

structure of these markets in the four countries that have joined the OECD since

2006, namely Chile, Estonia, Israel and Slovenia. The report concludes with a

discussion of the major themes emerging from the evidence on experiences with

structural separation.

20

In the EU, for example, energy investments in the order of €1 trillion will be

required over the course of the next ten years; see Communication from the

Commission to the European Parliament, the Council, the European

Economic and Social Committee and the Committee of the Regions, Energy

2020: A Strategy for Competitive, Sustainable and Secure Energy, SEC(2010)

1346, COM(2010) 639 final, published 10 November 2010, at p.2. The

transition to high speed fibre telecommunications networks is another area

where very substantial investments are required to fund socially-desirable

infrastructure development.

16

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

2. Structural separation as a remedy

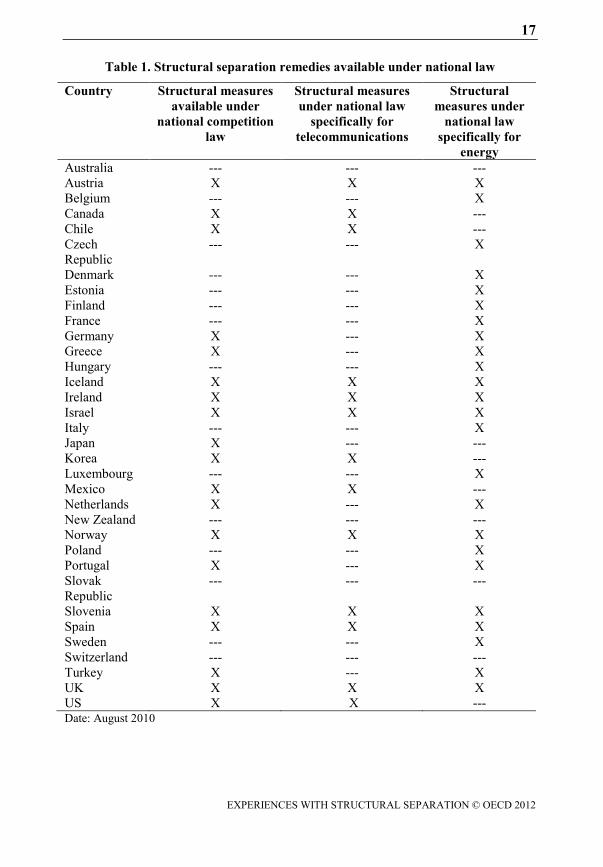

Structural separation remedies are not available in all OECD countries and

the conditions for structural separation differ: while structural separation is

usually imposed as a remedy for a competition violation, some competition

authorities can impose structural separation remedies merely to preserve a

competitive market structure, without finding an infringement of competition

law (―objective structural separation).21

The table below identifies those where

such remedies are available. Note that the revised EU competition law regime

introduced by Regulation 1/200322

made the application of the EU competition

provisions by national competition authorities and national courts compulsory,

irrespective of national sector regulation, to the extent that the conduct ―may

affect trade between Member States‖.23

Based on Article 5 of Regulation 1/2003

this does, however, not extend to procedural law, so that structural remedies are

available to competition authorities in EU Member States only to the extent that

they are foreseen under national law.24

Moreover, further sector-specific powers

may in the future be introduced at the domestic level as EU Member States

implement EU Directives relating to the sectors under consideration.

21

See e.g. the powers of the Competition Commission in the U.K. under the

Enterprise Act 2002.

22 Regulation (EC) 1/2003 of 16 December 2002 on the implementation of the

rules on competition laid down in Articles 81 and 82 of the Treaty (OJ L 1/1,

2003), hereafter ―Regulation 1/2003‖. See E. de Smijter and L. Kjølbye ―The

Enforcement System Under Regulation 1/2003‖ (2007), p. 87-180 in J. Faull

and A. Nikpay (eds.), The EC Law of Competition, 2nd

edition, Oxford

University Press, for a good overview. 23

See in particular Article 3 of Regulation 1/2003.

24 To the extent that national competition law provisions do not foresee

structural remedies but the conduct in question ―may affect trade between

Member States‖ of the EU, it can be argued that such measures may still be

required under EU law if alternative remedies would threaten effective

enforcement of competition law in the EU. In addition, again conditional

upon trade between EU Member States possibly being affected, the EU

Commission is always in a position to relieve the national competition

authority and initiate proceedings under Article 11(6) of Regulation 1/2003

itself, thereby allowing structural remedies to be imposed.

17

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Table 1. Structural separation remedies available under national law

Country Structural measures

available under

national competition

law

Structural measures

under national law

specifically for

telecommunications

Structural

measures under

national law

specifically for

energy

Australia --- --- ---

Austria X X X

Belgium --- --- X

Canada X X ---

Chile X X ---

Czech

Republic

--- --- X

Denmark --- --- X

Estonia --- --- X

Finland --- --- X

France --- --- X

Germany X --- X

Greece X --- X

Hungary --- --- X

Iceland X X X

Ireland X X X

Israel X X X

Italy --- --- X

Japan X --- ---

Korea X X ---

Luxembourg --- --- X

Mexico X X ---

Netherlands X --- X

New Zealand --- --- ---

Norway X X X

Poland --- --- X

Portugal X --- X

Slovak

Republic

--- --- ---

Slovenia X X X

Spain X X X

Sweden --- --- X

Switzerland --- --- ---

Turkey X --- X

UK X X X

US X X --- Date: August 2010

18

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

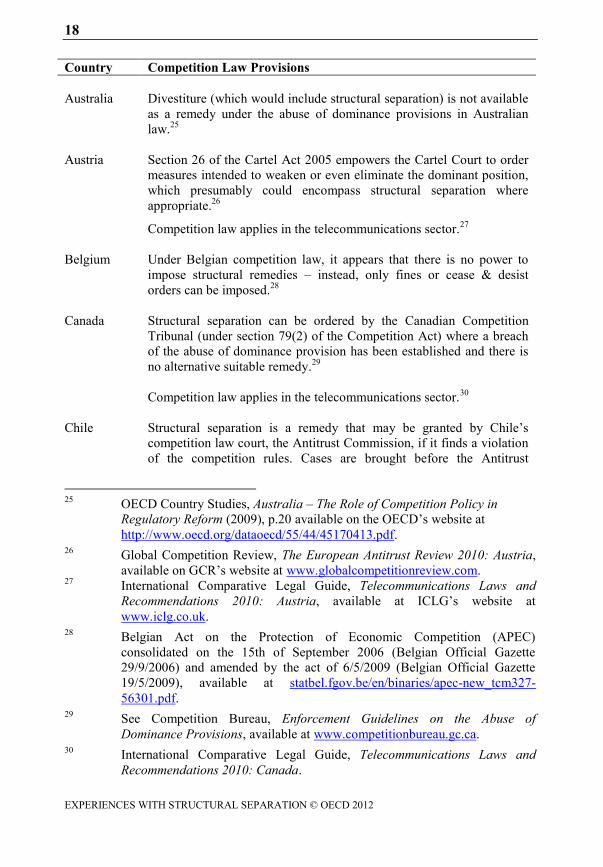

Country Competition Law Provisions

Australia

Divestiture (which would include structural separation) is not available

as a remedy under the abuse of dominance provisions in Australian

law.25

Austria

Section 26 of the Cartel Act 2005 empowers the Cartel Court to order

measures intended to weaken or even eliminate the dominant position,

which presumably could encompass structural separation where

appropriate.26

Competition law applies in the telecommunications sector.27

Belgium

Under Belgian competition law, it appears that there is no power to

impose structural remedies – instead, only fines or cease & desist

orders can be imposed.28

Canada

Structural separation can be ordered by the Canadian Competition

Tribunal (under section 79(2) of the Competition Act) where a breach

of the abuse of dominance provision has been established and there is

no alternative suitable remedy.29

Competition law applies in the telecommunications sector.30

Chile

Structural separation is a remedy that may be granted by Chile‘s

competition law court, the Antitrust Commission, if it finds a violation

of the competition rules. Cases are brought before the Antitrust

25

OECD Country Studies, Australia – The Role of Competition Policy in

Regulatory Reform (2009), p.20 available on the OECD‘s website at

http://www.oecd.org/dataoecd/55/44/45170413.pdf. 26

Global Competition Review, The European Antitrust Review 2010: Austria,

available on GCR‘s website at www.globalcompetitionreview.com. 27

International Comparative Legal Guide, Telecommunications Laws and

Recommendations 2010: Austria, available at ICLG‘s website at

www.iclg.co.uk. 28

Belgian Act on the Protection of Economic Competition (APEC)

consolidated on the 15th of September 2006 (Belgian Official Gazette

29/9/2006) and amended by the act of 6/5/2009 (Belgian Official Gazette

19/5/2009), available at statbel.fgov.be/en/binaries/apec-new_tcm327-

56301.pdf. 29

See Competition Bureau, Enforcement Guidelines on the Abuse of

Dominance Provisions, available at www.competitionbureau.gc.ca. 30

International Comparative Legal Guide, Telecommunications Laws and

Recommendations 2010: Canada.

19

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

Commission by the state enforcement agency or by private parties.31

Competition law applies to the telecommunications sector.32

Czech Rep.

The only penalties available under Czech competition law are fines,

criminal sanctions for hard core cartels and order to terminate anti-

competitive behaviour.33

There is overlapping jurisdiction between the competition authority

and the telecommunications regulator in the Czech Republic.34

Denmark

While the Danish Competition Commission can issue orders to put an

end to breaches of the competition rules, it appears not to have the

express power to impose structural measures on firms that are found to

have breached Danish competition law.35

Estonia

Upon finding a violation of the competition rules, the Estonian

competition authority can issue mandatory and prohibitory injunctions

in addition to cease and desist orders and fines. However, the authority

can only make non-binding recommendations (to government, business

etc.) regarding measures that can be taken to improve competition in

the market—which would mean that it cannot impose compulsory

structural separation itself as a competition law remedy under Estonian

competition law.

Following a merger of several agencies in 2008, the activities of the

telecommunications regulator are now included within the competition

authority.36

31

OECD, Peer Review of Competition Law & Policy – Chile (2004), pp.26-27. 32

OECD, Peer Review of Competition Law & Policy – Chile (2004), pp.48-50. 33

Global Competition Review, The European Antitrust Review 2010: Czech

Republic. See also OECD, Czech Republic – Peer Review of Competition

Law & Policy (2008).

34 Note that the telecommunications sector was excluded from the ambit of

Czech competition law between 2005 and 2007; see OECD, Czech Republic

– Peer Review of Competition Law & Policy (2008).

35 International Comparative Legal Guide, Enforcement of Competition Law

2010: Denmark.

36 International Comparative Legal Guide, Enforcement of Competition Law

2010: Estonia.

20

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

Finland As a general rule, structural separation is not available under the

Finnish Competition Act. However, a special provision exists with

regard to certain electricity market concentrations.37

France

Structural measures appear to be available under French competition

law only following a merger, where, if the merged entity abuses a

dominant position that it acquired through the merger, the competition

authority can order divestitures etc.38

Germany

The Bundeskartellamt can impose any remedy that is necessary to

effectively end the breach.39

In the telecommunications sector – as far as it is regulated by the

Bundesnetzagentur within the framework of specific

telecommunications law – the Bundeskartellamt can apply only EU

competition law, and not the general domestic competition law.40

Greece

Under general Greek competition law, structural measures can be

imposed after there has been an abuse of dominance. Structural

measures can be imposed only if there is no suitable behavioural

remedy available, or if the appropriate behavioural remedy would be

more onerous than the structural solution.41

All competition issues with regards to telecommunications fall within

the remit of the sector regulator, the Hellenic Communications and

Post Commission (EETT), and so are outside the ambit of Greek

competition law. However, EU competition law applies in the sector.

37

According to the Finnish Competition Act, the Market Court in Finland may,

upon the proposal of the Finnish Competition Authority, prohibit a

concentration in the electricity market if the combined market share of the

transmission operations of the parties exceeds 25% on a national level

(concerning electricity transmitted at 400V in the transmission grid).

38 International Comparative Legal Guide, Enforcement of Competition Law

2010: France (Dominance). See also Global Competition Review, The

European Antitrust Review 2010: France.

39 See the Bundeskartellamt‘s website at www.bundeskartellamt.de.

40 See Bundeskartellamt‘s website at www.bundeskartellamt.de.

41 International Comparative Legal Guide, Enforcement of Competition Law

2010: Greece.

21

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

Hungary

There does not appear to be any power to impose structural separation

as a competition law remedy under Hungarian competition law.42

Iceland

Structural measures can be imposed under competition law where they

are proportionate and suitable, and provided that there is no suitable

behavioural remedy available or where the available behavioural

remedy is more burdensome than the equivalent structural remedy.43

Competition law applies in the telecommunications sector.

Ireland

Under section 14(7) of the Competition Act 2002, where an abuse of

dominance has been established by a court, one remedy available to the

court is to order a variation of the dominant position in whatever way

may be required, which could include structural separation.

Under the Communications Regulation (Amendment) Act 2007, the

telecommunications regulator, ComReg, and the Irish competition

authority have concurrent jurisdiction over competition offences in the

telecommunications sector. Thus, court proceedings leading to a civil

order to vary a dominant position in the sector can be initiated by either

agency.

Israel

Structural separation is available under Article 31 of the Restrictive

Trade Practices law for firms that have been declared to be a

monopolist in a sector. Under this provision, the Antitrust Tribunal

may, at the application of the general director of the Israeli Antitrust

Authority, order the separation of a monopoly, the separation of legal

entities and the sale of the ownership and control of such entities to

third parties.44

Italy

There is no power to order structural separation under Italian

competition law.45

Competition law applies to the telecommunications sector.46

42

See the Hungarian Competition Act (Act LVII of 1996), available at

www.gvh.hu. See also OECD, Hungary – Updated Report on Competition

Policy & Institutions (2004), p.12.

43 Article 16 of Law No. 44 19th May 2005 with later amendments, No 52/2007

and No 94/2008, available on the Icelandic competition authority‘s website at

www.samkeppni.is. 44

Global Competition Review, The European Antitrust Review 2010: Israel. 45

The Italian legislation on competition is available on the website of the

competition authority, AGCM, along with further information on the

authority‘s powers under competition law, at www.agcm.it. 46

See the AGCM‘s website at www.agcm.it.

22

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

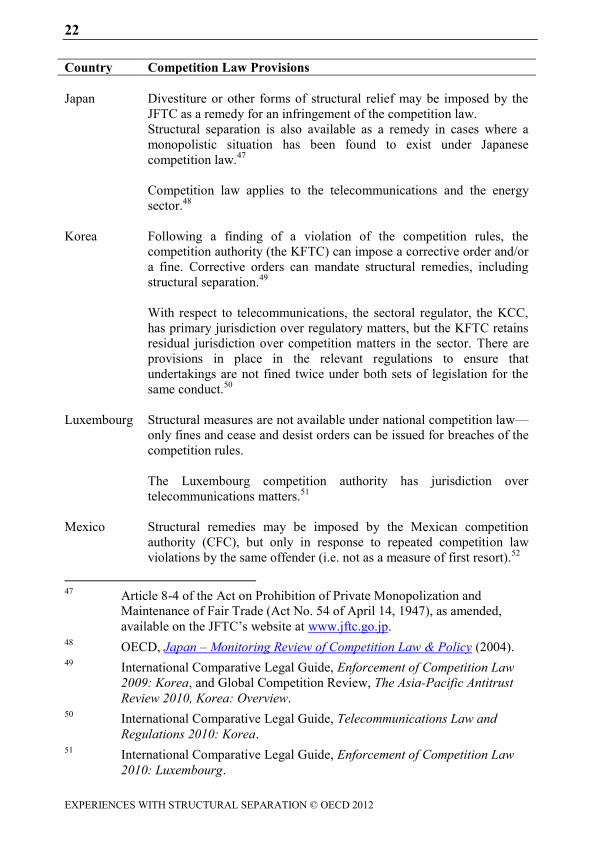

Japan

Divestiture or other forms of structural relief may be imposed by the

JFTC as a remedy for an infringement of the competition law.

Structural separation is also available as a remedy in cases where a

monopolistic situation has been found to exist under Japanese

competition law.47

Competition law applies to the telecommunications and the energy

sector.48

Korea

Following a finding of a violation of the competition rules, the

competition authority (the KFTC) can impose a corrective order and/or

a fine. Corrective orders can mandate structural remedies, including

structural separation.49

With respect to telecommunications, the sectoral regulator, the KCC,

has primary jurisdiction over regulatory matters, but the KFTC retains

residual jurisdiction over competition matters in the sector. There are

provisions in place in the relevant regulations to ensure that

undertakings are not fined twice under both sets of legislation for the

same conduct.50

Luxembourg

Structural measures are not available under national competition law—

only fines and cease and desist orders can be issued for breaches of the

competition rules.

The Luxembourg competition authority has jurisdiction over

telecommunications matters.51

Mexico

Structural remedies may be imposed by the Mexican competition

authority (CFC), but only in response to repeated competition law

violations by the same offender (i.e. not as a measure of first resort).52

47

Article 8-4 of the Act on Prohibition of Private Monopolization and

Maintenance of Fair Trade (Act No. 54 of April 14, 1947), as amended,

available on the JFTC‘s website at www.jftc.go.jp. 48

OECD, Japan – Monitoring Review of Competition Law & Policy (2004). 49

International Comparative Legal Guide, Enforcement of Competition Law

2009: Korea, and Global Competition Review, The Asia-Pacific Antitrust

Review 2010, Korea: Overview. 50

International Comparative Legal Guide, Telecommunications Law and

Regulations 2010: Korea. 51

International Comparative Legal Guide, Enforcement of Competition Law

2010: Luxembourg.

23

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

Competition law applies to the telecommunications sector.53

Netherlands

The NMa has the power to impose fines and to accept commitments

regarding structural changes. While under Article 58 (a) of the Dutch

Competition Act the NMa also has the power to impose structural

measures (which could include structural separation) on firms, such

power is subject to strict conditions, and could only be used as a last

resort.

Although there is a specific sectoral regulator for telecommunications,

the OPTA, the NMa‘s competition jurisdiction covers activities within

this sector as well.54

New

Zealand

There is no power under the Commerce Act 1986 (as amended) for

either the Commerce Commission or the courts to order structural

separation in response to a violation of competition law.55

Under the Telecommunications Act 2001 (amended by the

Telecommunications Amendment Act 2006) there is an express power

under telecommunications regulatory law for the relevant Minister to

impose ―robust operation separation‖ of the telecommunications

incumbent, which was implemented in March 2008.56

Norway

Under section 12 of Norway‘s Competition Act of 2004, structural

measures may be ordered to remedy a breach of the prohibition of anti-

competitive co-ordinated or unilateral behaviour, but only if there are

no suitable behavioural remedies available or if available behavioural

remedies are more onerous than the equivalent structural measures.57

52

Global Competition Review, The Handbook of Competition Enforcement

Agencies 2010, p.200. 53

Mexico‘s contribution to the Fourth Annual Latin American Competition

Forum Roundtable on Improving Relationships between Competition Policy

and Sectoral Regulation (2006), available at

www.oecd.org/competition/latinamerica. 54

International Comparative Legal Guide, Enforcement of Competition Law

2010: The Netherlands. See also the NMa‘s website at www.nmanet.nl. 55

The Commerce Act 1986 is available at www.legislation.govt.nz. 56

The Telecommunications Act 2001 is available at www.legislation.govt.nz. 57

The text of the Competition Act is available (also in English) on the website

of the Norwegian competition authority at www.konkurransetilsynet.no.

24

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

Competition law applies in the telecommunications sector.

Poland

Structural separation is not possible under current Polish competition

law (although it was available under earlier competition law).58

Portugal

According to Article 28, 1 (b) of the Portuguese Competition Act

structural measures are available if necessary to remedy a breach of the

prohibition of anti-competitive coordinated or unilateral behaviour.

Slovak Rep.

Slovak competition law provides the competition authority with the

power to order undertakings to ―remedy an unlawful state of affairs‖—

this does not, however, extend to imposing structural remedies on

parties.59

Pursuant to an amendment to the Slovak competition law in force since

June 2009, restrictions on the application of competition law in

markets also subject to specific sector regulation have been lifted.

Thus, the Slovak competition authority, the AMO, now has the power

to apply competition law in parallel with actions by sector regulators,

including the telecommunications regulator.

Slovenia

Structural separation may be imposed under Slovenian competition law

as a remedy for both anti-competitive co-ordinated and unilateral

behaviour.60

Competition law applies in the telecommunications sector.

Spain

Where there is a finding of breach of the competition rules (anti-

competitive co-ordinated or unilateral conduct), the CNC has the

power to impose structural measures on the guilty undertaking(s).

58

The Act of 16 February 2007 on competition and consumer protection is

available at www.uokik.gov.pl. See OECD, The Role of Competition Policy

in Regulatory Reform – Poland (2002), p.17, for a description of the previous

legislative framework. 59

Act of 27 February 2001 on Protection of Competition and on Amendments

and Supplements to Act of the Slovak National Council No. 347/1990 Coll.

on Organization of Ministries and Other Central Bodies of State

Administration of the Slovak Republic as amended, available on the website

of the Slovak Antimonopoly Office at www.antimon.gov.sk. 60

Article 37 of the Prevention of the Restriction of Competition Act (ZPOmK-

1), available on the website of the Slovenian Competition Protection Office at

www.uvk.gov.si.

25

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

Competition law applies in the telecommunications sector.61

Sweden

There is no power to impose structural separation under Swedish

competition law—only fines and orders to terminate anti-competitive

conduct are available on a finding of breach.62

Switzerland

There is no power to impose structural measures under Swiss law—

only to fine or to order termination of the competition law violation.

Competition law applies to anti-competitive conduct in the

telecommunications sector falling outside the purview of sector

specific legislation.63

Turkey

The Turkish Competition Authority has the power to impose sanctions

in the form of fines, behavioural and structural remedies in cases where

the Turkish Competition Act has been violated.64

The Turkish Competition Act applies to all sectors within Turkey, and

so the Competition Authority has jurisdiction over anti-competitive

conduct occurring in the telecommunications sector.65

UK

The Enterprise Act 2002 gives the Competition Commission the power

to impose a wide range of remedies (including structural separation

where appropriate) if, at the conclusion of a market inquiry, there is a

finding that a feature of the market has an adverse effect on

competition. Market inquiries are undertaken by the Competition

Commission following a reference by the OFT, relevant Minister or

certain sector regulators.

Ofcom (the telecommunications regulator) can make a reference to the

Competition Commission, requesting that it conduct a sector inquiry,

which may lead to the imposition of structural remedies if a

61

International Comparative Legal Guide, Enforcement of Competition Law

2010: Spain. 62

The text of the Swedish Competition Act is available (also in English) on the

website of the Swedish Competition Authority at www.konkurrensverket.se .

See also the OECD Country Study, Sweden - The Role of Competition Policy

in Regulatory Reform (2006). 63

OECD Country Studies, Switzerland - The Role of Competition Policy in

Regulatory Reform (2005). 64

See in particular Articles 9(1), 11(1)(b), 16(3), 17(1)(a) and 27(1)(a) of the

Turkish Competition Act.

65 OECD, Turkey – Peer Review of Competition Law and Policy (2005).

26

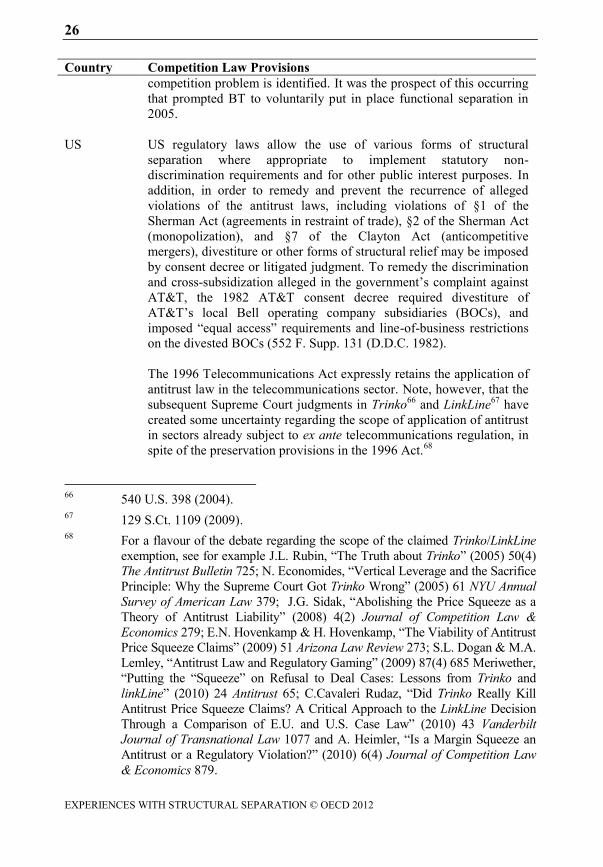

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

competition problem is identified. It was the prospect of this occurring

that prompted BT to voluntarily put in place functional separation in

2005.

US

US regulatory laws allow the use of various forms of structural

separation where appropriate to implement statutory non-

discrimination requirements and for other public interest purposes. In

addition, in order to remedy and prevent the recurrence of alleged

violations of the antitrust laws, including violations of §1 of the

Sherman Act (agreements in restraint of trade), §2 of the Sherman Act

(monopolization), and §7 of the Clayton Act (anticompetitive

mergers), divestiture or other forms of structural relief may be imposed

by consent decree or litigated judgment. To remedy the discrimination

and cross-subsidization alleged in the government‘s complaint against

AT&T, the 1982 AT&T consent decree required divestiture of

AT&T‘s local Bell operating company subsidiaries (BOCs), and

imposed ―equal access‖ requirements and line-of-business restrictions

on the divested BOCs (552 F. Supp. 131 (D.D.C. 1982).

The 1996 Telecommunications Act expressly retains the application of

antitrust law in the telecommunications sector. Note, however, that the

subsequent Supreme Court judgments in Trinko66

and LinkLine67

have

created some uncertainty regarding the scope of application of antitrust

in sectors already subject to ex ante telecommunications regulation, in

spite of the preservation provisions in the 1996 Act.68

66

540 U.S. 398 (2004). 67

129 S.Ct. 1109 (2009). 68

For a flavour of the debate regarding the scope of the claimed Trinko/LinkLine

exemption, see for example J.L. Rubin, ―The Truth about Trinko‖ (2005) 50(4)

The Antitrust Bulletin 725; N. Economides, ―Vertical Leverage and the Sacrifice

Principle: Why the Supreme Court Got Trinko Wrong‖ (2005) 61 NYU Annual

Survey of American Law 379; J.G. Sidak, ―Abolishing the Price Squeeze as a

Theory of Antitrust Liability‖ (2008) 4(2) Journal of Competition Law &

Economics 279; E.N. Hovenkamp & H. Hovenkamp, ―The Viability of Antitrust

Price Squeeze Claims‖ (2009) 51 Arizona Law Review 273; S.L. Dogan & M.A.

Lemley, ―Antitrust Law and Regulatory Gaming‖ (2009) 87(4) 685 Meriwether,

―Putting the ―Squeeze‖ on Refusal to Deal Cases: Lessons from Trinko and

linkLine‖ (2010) 24 Antitrust 65; C.Cavaleri Rudaz, ―Did Trinko Really Kill

Antitrust Price Squeeze Claims? A Critical Approach to the LinkLine Decision

Through a Comparison of E.U. and U.S. Case Law‖ (2010) 43 Vanderbilt

Journal of Transnational Law 1077 and A. Heimler, ―Is a Margin Squeeze an

Antitrust or a Regulatory Violation?‖ (2010) 6(4) Journal of Competition Law

& Economics 879.

27

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

Country Competition Law Provisions

European

Union

Under Article 7 of Regulation 1/2003, there is an explicit power to

impose structural remedies where there has been a finding of breach of

the EU competition rules. This is subject to several limitations, inter

alia that the remedy must be proportionate to the breach committed,

and structural remedies can only be imposed either where there is no

equally effective behavioural remedy or where any equally effective

behavioural remedy would be more burdensome for the undertaking

concerned than the structural remedy.69

Structural remedies in the form

of binding undertakings, given by a firm voluntarily in order to bring

an investigation to an end without a finding of breach, can also be

accepted under Article 9 of Regulation 1/2003, and this latter power is

not subject to the same limitations as remedies imposed under Article

7.70

EU competition rules apply in all sectors to conduct having an effect

on trade between EU Member States, including the energy and

telecommunications sector, regardless of the concurrent presence of

national or EU sector-specific regulation.

3. Developments in gas

The following section of this report provides a non-exhaustive overview of

developments with respect to structural and behavioural separation in the gas

sector in OECD Member countries and the EU. While the focus of the

Recommendation is on structural separation, experiences with behavioural

separation such as accounting or functional separation are included as well. In

order to focus on the most significant developments, not all countries are listed

3.1 Gas sector in Chile

The development of the natural gas market in Chile has taken place on a

regionalised basis, with separate gas transmission systems and distribution

networks operating across the regions. It is necessary to obtain a government

concession in order to build either a transmission pipeline or a distribution

network, which requires the concessionaire to adhere to certain service

69

See also recital 12 of Council Regulation (EC) No 1/2003 of 16 December

2002 on the implementation of the rules on competition laid down in Articles

81 and 82 of the Treaty.

70 See the Court of Justice‘s decision in C-441/07 P European Commission v

Alrosa (Judgment of 29 June 2010) for a discussion of the distinction

between the Commission‘s powers under Article 7 and Article 9 of

Regulation 1/2003.

28

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

conditions. In particular, transmission operators are required to grant open

access to their pipelines to distribution companies on non-discriminatory terms,

while distribution operators are obliged to provide universal service to

customers within their catchment areas. While there is no price regulation

within the Chilean gas sector, instead the competition authority has jurisdiction

over anti-competitive practices that may occur in the sector.71

3.2 Gas sector in Estonia

The Estonian market for natural gas is relatively small, isolated and highly

concentrated.72

Currently, the formerly State-owned gas company, Eesti Gaas,

has an effective monopoly on both gas transmission and supply in Estonia.73

A

separate transmission division, AS EG Võrguteenus, began operations from 1

January 2006 in order to comply with Estonia‘s requirements under EU law.74

Due to the continuing lack of competition in the natural gas sector, however,

full ownership unbundling of Eesti Gaas has been proposed by the government.

The plan would see Eesti Gaas separated into two distinct companies with

respect to its trading and transmission activities.75

3.3 Gas sector in the European Union

Structural separation within the EU gas sector has been pursued under a

two-pronged strategy which utilises both ex ante regulatory measures and ex

post competition law enforcement.

3.3.1 Energy sector inquiry

Energy reforms in the EU began in the late 1990s, with the adoption of the

first liberalisation directive for electricity in 1996,76

and gas in 1998.77

The

71

International Comparative Legal Guide, Gas Regulation 2010, Chapter 9:

Chile.

72 Herbert Smith, European Energy Review 2010: Estonia, available at

www.herbertsmith.com, p.40.

73 Herbert Smith – Estonia, cited fn. 72 above, p.41.

74 See the company information on Eesti Gaas‘s website at www.gaas.ee.

75 See Baltic Reports, ―Estonia to reform gas sector‖, published 29 July 2010,

and Baltic Reports, ―Eesti Gaas lambastes government break-up proposal‖,

published 30 July 2010, available at www.balticreports.com.

76 Directive 96/92/EC of the European Parliament and of the Council of 19

December 1996 concerning common rules for the internal market in

electricity (OJ L 27/20, 30.1.1997), hereafter the ―First Electricity Directive‖.

29

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

second liberalisation directives for both sectors were adopted in 2003,78

deepening the reform process for electricity and gas. Nevertheless, by 2005 the

European Commission was of the view that the energy markets in some EU

Member States were ―open only on paper‖,79

and so it initiated an inquiry in the

energy sector, in order to ascertain the underlying reasons why the market did

not fully function in the sector.80

The Final Report of the energy inquiry, published on 10 January 2007,81

found that, in Member States in which liberalisation efforts have been

introduced successfully, consumers have benefitted in the form of the widest

choice of suppliers and services, as well as more cost-reflective prices on

average.82

Throughout the Common Market taken as a whole, however,

significant competition problems and barriers to the creation of single markets

in gas and electricity remain. These include: a high level of concentration in

both sectors; insufficient unbundling leading to vertical foreclosure; and a lack

of cross-borders sales due to insufficient gas import pipeline capacity and

electricity interconnector capacity combined with inadequate incentives among

77

Directive 98/30/EC of the European Parliament and of the Council of 22 June

1998 concerning common rules for the internal market in natural gas (OJ L

204/1, 21.7.1998), hereafter the ―First Gas Directive‖.

78 Directive 2003/55/EC of the European Parliament and of the Council of 26

June 2003 concerning common rules for the internal market in natural gas

and repealing Directive 98/30/EC (OJ L 176/57, 15.7.2003), hereafter the

―Second Gas Directive‖, and Directive 2003/54/EC of the European

Parliament and of the Council of 26 June 2003 concerning common rules for

the internal market in electricity and repealing Directive 96/92/EC (OJ L

176/37, 15.7.2003), hereafter the ―Second Electricity Directive‖.

79 European Commission, Working together for growth and jobs – A new start

for the Lisbon Strategy COM(2005) 24, published 2 February 2005, p.8.

80 Commission Decision of 13 June 2005 initiating an inquiry into the gas and

electricity sectors pursuant to Article 17 of Council Regulation (EC) No

1/2003in Cases COMP/B-1/39.172 (electricity) and 39.173 (gas).

81 European Commission, Inquiry pursuant to Article 17 of Regulation (EC) No

1/2003 into the European gas and Electricity sectors (Final Report)

COM(2006) 851, published 10 January 2007, hereafter the ―Energy Inquiry

Report‖. See also Neelie Kroes, ―Improving Competition in European

Energy Markets through Effective Unbundling‖ (2008) 31 Fordham Journal

of International Law 1387.

82 Energy Inquiry Report, cited fn. 81 above, p.2.

30

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

incumbents to expand existing capacity.83

The Report outlined a bilateral

approach to addressing market problems within the energy sector, combining

further regulatory measures with competition law enforcement.84

3.3.2 Regulatory measures—third liberalisation package

Concurrently with publication of the Final Report on the energy inquiry,

the Commission issued its proposals for regulatory reforms of the EU energy

markets.85

In these proposals, the Commission argued that, ―[i]nherently, legal

unbundling does not suppress the conflict of interest that stems from vertical

integration, with the risk that networks are seen as strategic assets serving the

commercial interest of the integrated entity, not the overall interest of network

customers.‖86

The evidence collected by the Commission indicated that the lack

of full unbundling had created various problems in the Member States:

Non-discriminatory access to information could not be guaranteed;

The existing unbundling rules did not remove the incentives for

discrimination with respect to third party access; and

Investment incentives were distorted.87

The Commission concluded that ―only strong unbundling provisions would

be able to provide the right incentives for system operators to operate and

83

Energy Inquiry Report, cited fn. 81 above, pp.5-9. Other markets problems

include a lack of transparency on the markets, particularly with regard to

price formation; limited competition at the retail level; balancing markets that

favour incumbents and thus create barriers to entry; and the need to develop

the liquefied natural gas (LNG) sector.

84 Energy Inquiry Report, cited fn. 81 above, p.9.

85 European Commission, Communication from the Commission to the Council

and the European Parliament. Prospects for the Internal Gas and Electricity

Market COM(2006) 841, published on 10 January 2007.

86 Prospects for the Internal Gas and Electricity Market, cited fn. 85 above,

p.10.

87 Prospects for the Internal Gas and Electricity Market, cited fn. 85 above,

p.10-11.

31

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

develop the network in the interest of all users.‖88

Two options for further

transmission system operator (TSO) unbundling were foreseen:

Fully (ownership) unbundled TSO, whereby the TSO would both own

the transmission assets and operate the network. It would be

independently owned, meaning that supply/generation companies

could no longer hold a significant stake in the TSO; and/or

Separate system operators without ownership unbundling, whereby

system operation would be separated from ownership of the assets.

Supply/generation companies could no longer hold a significant stake

in the independent system operators (ISOs), but ownership of the

transmission assets could remain within a vertically integrated

group.89

The Commission expressed its preference for the first option—full

ownership unbundling—over the ISO model in the following terms:

Economic evidence shows that ownership unbundling is the most

effective means to ensure choice for energy users and encourage

investment. This is because separate network companies are not

influenced by overlapping supply/generation interests as regards

investment decisions. It also avoids overly detailed and complex

regulation and disproportionate administrative burdens.

The independent system operator approach would improve the status

quo but would require more detailed, prescriptive and costly

regulation and would be less effective in addressing the disincentives

to invest in networks.90

Both of the options presented by the Commission proved too intrusive for

some Member States, however, although the Commission‘s approach was

strongly supported by others.91

In July 2009, the Parliament and Council

88

Prospects for the Internal Gas and Electricity Market, cited fn. 85 above,

p.11.

89 Prospects for the Internal Gas and Electricity Market, cited fn. 85 above,

p.11.

90 Prospects for the Internal Gas and Electricity Market, cited fn. 85 above,

p.12.

91 See R. Boscheck, ―The EU‘s Third Internal Energy Market Legislative

Package: Victory of Politics over Economic Rationality‖ (2009) 32(4) World

32

EXPERIENCES WITH STRUCTURAL SEPARATION © OECD 2012

adopted an unbundling programme for both the gas92

and electricity93

sectors

which allows a Member State to adopt any of three potential unbundling

models: ownership unbundling, an ISO model and an independent transmission

operator (ITO) model.94

Member States are required to transpose and bring into

force the unbundling provisions of the Third Gas and Electricity Directives by 3

March 2011.

Under ownership unbundling, the owner of a gas or electricity transmission

system is required to act as the TSO,95

being the natural or legal person with

responsibility for operation, maintenance and development of a transmission

system, plus its interconnections with other systems, as well as ensuring the

long-term ability of the system to meet reasonable demand for the transmission

of gas and electricity respectively.96

Under this model, the same person is not

permitted, directly or indirectly, to exercise control over both the TSO and an

undertaking performing any of the functions of generation or supply (or

exercise control over one party and any right over the other).97

The concept of a

right includes a majority shareholding in either the TSO or the undertaking

performing generation or supply function,98

so that this model requires, in

Competition 593 for a discussion of some of the political issues surrounding

the adoption of the Third Liberalisation Package.

92 Directive 2009/73/EC of the European Parliament and of the Council of 13

July 2009 concerning common rules for the internal market in natural gas and

repealing Directive 2003/55/EC (OJ L 211/94, 14.8.2009), hereafter the

―Third Gas Directive‖.

93 Directive 2009/72/EC of the European Parliament and of the Council of 13

July 2009 concerning common rules for the internal market in electricity and