report

TRANSCRIPT

A PROJECT REPORT

ON

“WORKING CAPITAL MANAGEMENT”

@

Lamiya Silks, Thrissur, Kerala

Submitted to

Indian Institute of Planning and Management (IIPM),

New Delhi

By

JIBIN BABU

SS 11 / 13

ID- D1113SSIBSEPGP10207 (COC – 5 – CA – 1050)

in partial fulfillment of the requirement for the award of the degree of MASTER OF BUSINESS ADMINISTRATION

10th April 2012– 25th May 2012

Phone- 8860598398 Email- [email protected]

Page 1 of 72

Acknowledgement

It is a matter of great satisfaction and pleasure to present this report on Working Capital

Management of Lamiya Silks. I take this opportunity to owe my thanks to all those involved in

my training.

Firstly I would like to thank LAMIYA SILKS for giving the opportunity to complete my project

in the organization. I put on record my sincere thanks to my college, Indian Institute of

Planning and Management (IIPM), New Delhi, for giving me such an opportunity. I am

extremely grateful to Mr. Mohammed Rashin for the encouragement, discussions and critical

assessment of the project.

It was a good experience for me to work with Lamiya Silks, a pioneer in the textile industry. I

am greatly obliged to Mr. Mohammed Rashin my industry guide, and Mr. Mansoor. P.A, Mr.

Lishad. K.A who have shared their expertise and knowledge with me without which the

completion of project would not have been possible.

I express my gratitude towards staff of Lamiya Silks, those who have helped me directly or

indirectly in completing the training.

Page 2 of 72

TABLE OF CONTENTS

Sl.No. Contents Page No.

1. Executive Summary 1 – 2

2. Introduction 3 – 20

2.1 Working Capital 4 – 8

2.2 Operating Cycle 9

2.3 Working Capital Management 9 – 18

2.4 Concept of Working Capital 19 - 20

3. Research Methodology 21 – 23

4. Sector Overview 24 – 30

4.1 Textile Sector 25 – 27

4.2 SWOT of Textile Industry 28 – 30

5. Company Overview 31 – 38

6. Internship Activities 39 – 57

7. Internship Assessment 58 – 59

8. Conclusion 60 – 61

Page 3 of 72

9. Illustration 62 – 65

10. Bibliography 66 – 67

LIST OF TABLES

Table No. Contents Page No.

1. Comparative Profit & Loss Account 49

2. Trend analysis (Liability Side) 50

3. Trend Analysis (Asset Side) 51

4. Cash Flow Analysis 52

5. Cash Flow Statement 53

6. Profit & Loss Account 55

7. Balance Sheet 56

LIST OF CHARTS

Chart No Contents Page No.1. Main Department Sales 632. Other Department sales 64

Page 4 of 72

EXECUTIVE

SUMMARY

Page 5 of 72

Lamiya Silks is a very well famous textile outlet in Kerala. It has more than 10 branches all over

the state with wide variety of apparels mainly for women. It has broadened its business towards

the gulf as well.

The major purpose of the study is to analyze the working capital management of Lamiya Silks by

considering the annual report of two years. The financial statement explains the trend analyzes

and the ratio analyzes along with the comparative balance statements.

Working capital is one of the most difficult financial concepts to understand for the small-

business owner. In fact, the term means a lot of different things to a lot of different people. By

definition, working capital is the amount by which current assets exceed current liabilities. It

involves the relationship between a firm’s short term assets and its short term liabilities.

Funds needed for short term needs for the purpose like payment of wages and other day to day

expenses are known as working capital. The goal of working capital management is to ensure

that the firm is able to continue its operation and that it has sufficient cash flow to satisfy both

maturing short term debt and upcoming operational expenses. Working capital is primarily

concerned with inventories management, receivable management, cash management and payable

management.

The study involved few personal interviews with the financial heads of the company and through

observation methods. Company annual reports were being evaluated and working capital

management was being analyzed from it. For the purpose of the study convenience sampling

technique has been used.

Page 6 of 72

The study has shown that the working capital of the company has improved as the current asset

is more than that of the current liabilities.

INTRODUCTION

Page 7 of 72

Management is an art of anticipating and preparing for risks, uncertainties and overcoming

obstacles. An essential precondition for sound and consistent assets management is establishing

the sound and consistent assets management policies covering fixed as well as current assets. In

modern financial management, efficient allocation of funds has a great scope, in finance and

profit planning, for the most effective utilization of enterprise resources, the fixed and current

assets have to be combined in optimum proportions.

Working capital in simple terms means the amount of funds that a company requires for

financing its day-to-day operations. Finance manager should develop sound techniques of

managing current assets.

WHAT IS WORKING CAPITAL?

Working capital refers to the investment by the company in short terms assets such as cash,

marketable securities. Net current assets or net working capital refers to the current assets less

current liabilities.

Symbolically, it means,

Net Current Assets = Current Assets Current Liabilities.

In accounting,” Working capital is the difference between the inflow and outflow of funds. In

other words, it is the net cash inflow. It is defined as the excess of current assets over current

liabilities and provisions. In other words, it is net current assets or net working capital.

Page 8 of 72

Working capital represents the total of all current assets. In other words it is the Gross working

capital , it is also known as Circulating capital or Current capital for current assets are rotating in

their nature.

A study of working capital is of major importance to internal and external analysis because of its

close relationship with the day-to-day operations of a business. Working Capital is the portion of

the assets of a business which are used on or related to current operations, and represented at any

one time by the operating cycle of such items as against receivables, inventories of raw

materials, stores, work in process and finished goods, merchandise, notes or bill receivables and

cash.

Working capital comprises current assets which are distinct from other assets. In the first

instance, current assets consist of these assets which are of short duration.

Working capital may be regarded as the life blood of a business. Its effective provision can do

much to ensure the success of a business while its inefficient management can lead not only to

loss of profits but also to the ultimate downfall of what otherwise might be considered as a

promising concern.

The funds required and acquired by a business may be invested to two types of assets:

1. Fixed Assets.

2. Current Assets

Fixed assets are those which yield the returns in the due course of time. The various decisions

like in which fixed assets funds should be invested and how much should be invested in the fixed

assets etc. are in the form of capital budgeting decisions. This can be said to be fixed capital

management.

Other types of assets are equally important i.e. Current Assets.

These types of assets are required to ensure smooth and fluent business operations and can be

said to be life blood of the business. There are two concepts of working capital — Gross and Net.

Gross working capital refers to gross current assets. Net working capital refers to the difference

Page 9 of 72

between current assets and current liabilities. The term current assets refers to those assets held

by the business which can be converted into cash within a short period of time of say one year,

without reduction in value. The main types of current assets are stock, receivables and cash. The

term current liabilities refer to those liabilities, which are to be paid off during the course of

business, within a short period of time say one year. They are expected to be paid out of current

assets or earnings of the business. The current liabilities mainly consist of sundry creditors, bill

payable, bank overdraft or cash credit, outstanding expenses etc.

NEED FOR WORKING CAPITAL

Working capital may be regarded as the lifeblood of the business. Without insufficient working

capital, any business organization cannot run smoothly or successfully. In the business the

Working capital is comparable to the blood of the human body. Therefore the study of working

capital is of major importance to the internal and external analysis because of its close

relationship with the current day to day operations of a business. The inadequacy or

mismanagement of working capital is the leading cause of business failures.

The need of gross working capital or current assets cannot be overemphasized. The object of any

business is to earn profits. The main factor affecting the profits is the magnitude of sales of the

business. But the sales cannot be converted into cash immediately. There is a time lag between

the sale of goods and realization of cash. There is a need of working capital in the form of

current assets to fill up this time lag. Technically, this is called as operating cycle or working

capital cycle, which is the heart of need for working capital. This working capital cycle can be

described in the following words. If the company has a certain amount of cash, it will be required

for purchasing the raw material though some raw material may be available on credit basis. Then

the company has to spend some amount for labour and factory overheads to convert the raw

material in work in progress, and ultimately finished goods. These finished goods when sold on

credit basis get converted in the form of sundry debtors. Sundry debtors are converted in cash

only after the expiry of credit period. Thus, there is a cycle in which the originally available cash

is converted in the form of cash again but only after following the stages of raw material, work in

progress, finished goods and sundry debtors. Thus, there is a time gap for the original cash to get

converted in form of cash again. Working Capital needs of company arise to cover the

Page 10 of 72

requirement of funds during this time gap, and the quantum of working capital needs varies as

per the length of this time gap.

Thus, some amount of funds is blocked in raw materials, work in progress, finished goods,

sundry debtors and day-to-day requirements. However some part of these current assets may be

financed by the current liabilities also. E.g. some raw material may be available on credit basis,

all the expenses need not be paid immediately, workers are also to be paid periodically etc. But

still the amounts required to be invested in these current assets is always higher than the funds

available from current liabilities. This is precise reason why the needs for working capital arise.

From the Financial management point of view, the nature of fixed assets and current assets differ

from each other--

1. The fixed assets are required to be retained in the business over a period of time and they yield

the returns over their life, whereas the current assets loose their identity over a short period of

time, say one year.

2. In the case of current assets, it is always necessary to strike a proper balance between the

liquidity and profitability principles, which is not the case with fixed assets. E.g. If the size of

current assets is large, it is always beneficial from the liquidity point of view as it ensures smooth

and fluent business operations. Sufficient raw material is always available to cater to the

production needs, sufficient finished goods are available to cater to any kind of demand of

customers, liberal credit period can be offered to the customers to improve the sales and

sufficient cash is available to pay off the creditors and so on.

However, if the investment in current assets is more than what is ideally required, it affects the

profitability, as it may not be able to yield sufficient rate of return on investment. On the other

hand, if the size of current assets is too small, it always involves the risk of frequent stock out,

inability of the company to pay its dues in time etc. As such, the investment in current assets

should be optimum. Hence, it is necessary to manage the individual components of current assets

in a proper way. Thus, working capital management refers to proper administration of all aspects

of current assets and current liabilities. Working Capital Management is concerned with the

problems arising out of the attempts to manage current assets, current liabilities and inter-

Page 11 of 72

relationship between them. The intention is not to maximize the investment in working capital

nor is it to minimize the same. The intention is to have optimum investment in working capital.

In other words, it can be said that the aim of working capital management is to have minimum

investment in working capital without affecting the regular and smooth flow of operations. The

level of current assets to be maintained should be sufficient enough to cover its current liabilities

with a reasonable margin of safety. Moreover, the various sources available for financing

working capital requirements should be properly managed to ensure that they are obtained and

utilized in the best possible manner.

Working Capital Cycle

Working capital cycle indicates the length of time between a firm’s paying for materials entering

into stock and receiving the cash from sale of finished goods. In a manufacturing firm, the

duration of time required to complete the sequence of events is called operating cycle.

In case of a manufacturing company, the operating cycle is the length of time necessary to

complete the following cycle of events –

1. Conversion of cash into raw materials

2. Conversion of raw materials into work-in-progress

3. Conversion of work-in-progress into finished goods

4. Conversion of finished goods into accounts receivables

5. Conversion of accounts receivable into cash

The above operating cycle is repeated again and again over the period depending upon the nature

of the business and type of product etc. the duration of the operating cycle for the purpose of

estimating working capital is equal to the sum of duration allowed by the suppliers.

Working capital cycle can be expressed as

R+W+F+D+C

Where,

Page 12 of 72

R - raw material storage period = avg. stock of raw material / avg. cost of production per day

W – work in progress holding period = avg. work in progress inventory / avg. cost of production

per day

F – finished goods storage period = avg. stock of finished goods / avg. cost of goods sold per day

D – debtors collection period = avg. book debts / avg. credit sales per day

C – credit period availed = avg. trade creditors avg. credit purchases per day.

OPERATING CYCLE OF MANUFACTURING BUSINESS

Realization Sales

Accounts Receivable

Cash Finished Goods

Purchases Production

Production

Raw Materials Work-in-progress

Page 13 of 72

WORKING CAPITAL MANAGEMENT

To start any business, First of all we need finance and the success of that business entirely

depends on the proper management of day-to-day finance and the management of this short term

capital or finance of the business is called Working Capital Management.

Working Capital is the key difference between the long term financial management and short

term financial management in terms of the timing of cash. Working capital management is a

short term financial management. Working capital management is concerned with the problems

that arise in attempting to manage the current assets, the current liabilities & the inter

relationship that exists between them. The current assets refer to those assets which can be easily

converted into cash in ordinary course of business, without disrupting the operations of the firm.

Working capital management or short-term financial management is a significant facet of

financial management. It is important due to 2 reasons:

Investment in current assets represents a substantial portion of total investment

Investment in current assets and the level of current liabilities have to be geared quickly

to changes in sales.

Working capital involves activities such as arranging short-term finance, negotiating favorable

credit terms, controlling the movement of cash, administrating accounts receivables, and

monitoring the investment in inventories also take a great deal of time.

Management of working capital is concerned with the problem that arises in attempting to

manage the current assets, current liabilities. The basic goal of working capital management is to

manage the current assets and current liabilities of a firm in such a way that a satisfactory level

of working capital is maintained, i.e. it is neither adequate nor excessive as both the situations

are bad for any firm. There should be no shortage of funds and also no working capital should be

ideal. WORKING CAPITAL MANAGEMENT POLICES of a firm has a great on its

probability, liquidity and structural health of the organization. So working capital management is

three dimensional in nature as

Page 14 of 72

1. It concerned with the formulation of policies with regard to profitability, liquidity

and risk.

2. It is concerned with the decision about the composition and level of current assets.

3. It is concerned with the decision about the composition and level of current

liabilities.

Composition of working capital--

Major Current Assets

1) Cash in hand and cash at bank

2) Bills receivables

3) Sundry debtors

4) Short term loans and advances.

5) Inventories of stock as:

a. Raw material

b. Work in process

c. Stores and spares

d. Finished goods

6) Temporary investment of surplus funds.

7) Prepaid expenses

Page 15 of 72

8) Accrued incomes.

9) Marketable securities.

Major Current Liabilities

1) Accrued or outstanding expenses.

2) Short term loans, advances and deposits.

3) Dividends payable.

4) Bank overdraft.

5) Provision for taxation , if it does not amt. to app. Of profit.

6) Bills payable.

7) Sundry creditors.

The gross working capital concept is financial or going concern concept whereas net working

capital is an accounting concept of working capital. Both the concepts have their own merits.

The gross concept is sometimes preferred to the concept of working capital for the following

reasons:

1. It enables the enterprise to provide correct amount of working capital at correct time.

2. Every management is more interested in total current assets with which it has to operate

then the source from where it is made available.

3. It take into consideration of the fact every increase in the funds of the enterprise would

increase its working capital.

Page 16 of 72

4. This concept is also useful in determining the rate of return on investments in working

capital.

The Goal of Capital Management is to manage the firm s current assets & liabilities, so that the

satisfactory level of working capital is maintained. If the firm can not maintain the satisfactory

level of working capital, it is likely to become insolvent & may be forced into bankruptcy. To

maintain the margin of safety current asset should be large enough to cover its current assets.

Main theme of the theory of working capital management is interaction between the current

assets & current liabilities.

CLASSIFICATION OF WORKING CAPITAL

Working capital may be classified in two ways:

o On the basis of concept.

o On the basis of time.

On the basis of concept working capital can be classified as gross working capital and net

working capital. On the basis of time, working capital may be classified as:

Ø Permanent or fixed working capital.

Ø Temporary or variable working capital

PERMANENT OR FIXED WORKING CAPITAL

Permanent or fixed working capital is minimum amount which is required to ensure effective

utilization of fixed facilities and for maintaining the circulation of current assets. Every firm has

to maintain a minimum level of raw material, work- in-process, finished goods and cash balance.

This minimum level of current assets is called permanent or fixed working capital as this part of

Page 17 of 72

working is permanently blocked in current assets. As the business grow the requirements of

working capital also increases due to increase in current assets.

TEMPORARY OR VARIABLE WORKING CAPITAL

Temporary or variable working capital is the amount of working capital which is required to

meet the seasonal demands and some special exigencies. Variable working capital can further be

classified as seasonal working capital and special working capital. The capital required to meet

the seasonal need of the enterprise is called seasonal working capital. Special working capital is

that part of working capital which is required to meet special exigencies such as launching of

extensive marketing for conducting research, etc.

The extra working capital needed to support the changing production and sales

activities, is called variable or functioning or temporary working capital.

Temporary working capital differs from permanent working capital in the sense that is required

for short periods and cannot be permanently employed gainfully in the business.

IMPORTANCE OR ADVANTAGE OF ADEQUATE WORKING CAPITAL

Ø Solvency of the business: Adequate working capital helps in maintaining the solvency of

the business by providing uninterrupted of production.

Ø Goodwill: Sufficient amount of working capital enables a firm to make prompt

payments and makes and maintain the goodwill.

Ø Easy loans: Adequate working capital leads to high solvency and credit standing can

arrange loans from banks and other on easy and favorable terms.

Ø Cash Discounts: Adequate working capital also enables a concern to avail cash

discounts on the purchases and hence reduces cost.

Ø Regular Supply of Raw Material: Sufficient working capital ensures regular supply of

raw material and continuous production.

Page 18 of 72

Ø Regular Payment Of Salaries, Wages And Other Day TO Day Commitments: It leads to

the satisfaction of the employees and raises the morale of its employees, increases their

efficiency, reduces wastage and costs and enhances production and profits.

Ø Exploitation of Favorable Market Conditions: If a firm is having adequate working

capital then it can exploit the favorable market conditions such as purchasing its

requirements in bulk when the prices are lower and holdings its inventories for higher

prices.

Ø Ability to Face Crises: A concern can face the situation during the depression.

Ø Quick And Regular Return On Investments: Sufficient working capital enables a

concern to pay quick and regular of dividends to its investors and gains confidence of the

investors and can raise more funds in future.

Ø High Morale: Adequate working capital brings an environment of securities, confidence,

high morale which results in overall efficiency in a business.

EXCESS OR INADEQUATE WORKING CAPITAL

Every business concern should have adequate amount of working capital to run its business

operations. It should have neither redundant or excess working capital nor inadequate nor

shortages of working capital. Both excess as well as short working capital positions are bad for

any business. However, it is the inadequate working capital which is more dangerous from the

point of view of the firm.

DISADVANTAGES OF INADEQUATE WORKING CAPITAL

Every business needs some amounts of working capital. The need for working capital arises due

to the time gap between production and realization of cash from sales. There is an operating

cycle involved in sales and realization of cash. There are time gaps in purchase of raw material

and production; production and sales; and realization of cash.

Thus working capital is needed for the following purposes:

Page 19 of 72

· For the purpose of raw material, components and spares.

· To pay wages and salaries

· To incur day-to-day expenses and overload costs such as office expenses.

· To meet the selling costs as packing, advertising, etc.

· To provide credit facilities to the customer.

· To maintain the inventories of the raw material, work-in-progress, stores and spares and

finished stock.

For studying the need of working capital in a business, one has to study the business under

varying circumstances such as a new concern requires a lot of funds to meet its initial

requirements such as promotion and formation etc. These expenses are called preliminary

expenses and are capitalized. The amount needed for working capital depends upon the size of

the company and ambitions of its promoters. Greater the size of the business unit, generally

larger will be the requirements of the working capital.

FACTORS AFFECTING WORKING CAPITAL MANAGEMENT

The amount of working capital required depends upon a number of factors which can be stated as

below

Nature of Business:

Some businesses are such, due to their very nature, that their requirement of fixed capital is more

rather than working capital. These businesses sell services and not the commodities and not the

commodities and that too on cash basis. As such, no funds are blocked in piling inventories and

also no funds are blocked in receivables. E.g. Public utility services like railways, electricity

boards, infrastructure oriented projects etc. Their requirement of working capital is less. On the

other hand, there are some business like trading activity, where the requirement of fixed capital

Page 20 of 72

is less but more money is blocked in inventories and debtors. Their requirement of the working

capital is more.

Length of Production Cycle:

In some business like machine tool industry, the time gap between the acquisitions of raw

material till the end of final production of finished product itself is quite high. As such more

amounts may be blocked either in raw materials, or work in progress or finished goods or even in

debtors. Naturally, their needs of working capital are higher. On the other hand, if the production

cycle is shorter, the requirement of working capital is also less.

Size and Growth of Business:

In very small companies the working capital requirements are quite high overheads, higher

buying and selling costs etc. As such, the medium sized companies positively have an edge over

the small companies. But if the business starts growing after a certain limit, the working capital

requirements may be adversely affected by the increasing size.

Business I Trade Cycles:

If the company is operating in the period of boom, the working capital requirements may be

more as the company may like to buy more raw material, may increase the production and sales

to take the benefits of favourable markets, due to the increased sales, there may be more and

more amount of funds blocked in stock and debtors etc. Similarly, in case of depression also, the

working capital requirements may be high as the sales in terms of value and quantity may be

reducing, there may be unnecessary piling up of stocks without getting sold, the receivables may

not be recovered in time etc.

Rate of Stock Turnover:

There is an inverse co-relationship between the question of working capital and the velocity or

speed with which the sales are affected. A firm having a high rate of stock turnover wuill needs

lower amt. of working capital as compared to a firm having a low rate of turnover.

Page 21 of 72

Credit Policy:

The firm’s credit policy directly affects the working capital requirement. If the firm

has liberal credit policy, hence the more credit period will be provided to the debtors so this

will lead to more working capital requirement. With the liberal credit policy

operating cycle length increases and vice versa.

Production Policy:

If the policy is to keep production steady by accumulating inventories it will require higher

working capital.

Seasonal Variations:

In certain industries like raw material is not available throughout the year. They have to buy raw

material in bulk during the season to ensure an uninterrupted flow and process them during the

year. Generally, during the busy season, a firm requires larger working capital than in slack

season.

Earning Capacity And Dividend Policy:

Some firms have more earning capacity than other due to quality of their products, monopoly

conditions, etc. Such firms may generate cash profits from operations and contribute to their

working capital. The dividend policy also affects the requirement of working capital. A firm

maintaining a steady high rate of cash dividend irrespective of its profits needs working capital

than the firm that retains larger part of its profits and does not pay so high rate of cash dividend.

Price Level Changes:

Changes in the price level also affect the working capital requirements. Generally rise in prices

leads to increase in working capital.

Page 22 of 72

Others FACTORS:

Operating efficiency.

Management ability.

Irregularities of supply.

Import policy.

Asset structure.

Importance of labor.

Banking facilities, etc

CONCEPT OF WORKING CAPITAL:

There are 2 concepts:

Gross Working Capital

Net Working Capital

Gross working capital: - It is referred as total current assets.

Focuses on,

Optimum investment in current assets:

Excessive investments impairs firm s profitability, as idle investment earns nothing. Inadequate

working capital can threaten solvency of the firm because of its inability to meet its current

obligations. Therefore there should be adequate investment in current assets.

Financing of current assets:

Whenever the need for working capital funds arises, agreement should be made quickly. If

surplus funds are available they should be invested in short term securities.

Net working capital (NWC) defined by 2 ways,

Page 23 of 72

Difference between current assets and current liabilities

Net working capital is that portion of current assets which is financed with long term

funds.

NET WORKING CAPITAL = CURRENT ASSETS CURRENT

LIABILITIES

If the working capital is efficiently managed then liquidity and profitability both will improve.

They are not components of working capital but outcome of working capital. Working capital is

basically related with the question of profitability versus liquidity & related aspects of risk.

PLANNING OF WORKING CAPITAL:

Working capital is required to run day to day business operations. Firms differ in their

requirement of working capital (WC). Firm s aim is to maximize the wealth of share holders and

to earn sufficient return from its operations. WCM is a significant facet of financial management.

Its importance stems from two reasons:

Investment in current asset represents a substantial portion of total investment.

Investment in current assets and level of current liability has to be geared quickly to

change in sales.

Business undertaking required funds for two purposes:

To create productive capacity through purchase of fixed assets.

To finance current assets required for running of the business.

The importance of WCM is reflected in the fact that financial managers spend a great deal of

time in managing current assets and current liabilities. The extent to which profit can be earned

Page 24 of 72

is dependent upon the magnitude of sales. Sales are necessary for earning profits. However, sales

do not convert into cash instantly; there is invariably a time lag between sale of goods and the

receipt of cash. WC management affect the profitability and liquidity of the firm which are

inversely proportional to each other, hence

proper balance should be maintained between two.

To convert the sale of goods into cash, there is need for WC in the form of current asset to deal

with the problem arising out of immediate realization of cash against good sold. Sufficient WC is

necessary to sustain sales activity. This is referred to as the operating or cash cycle.

RESEARCHMETHODOLOGY

Page 25 of 72

Objective of the study

To study the various proportions of working capital of Lamiya Silks

To find out different ratios related with working capital

To check the impact of cash flows on working capital of Lamiya Silks

To know the current trend of Assets and Liabilities

Target

Working capital of Lamiya Silks

Sampling Unit

Working capital of Lamiya Silks at Thrissur Store

Sampling Area

Thrissur

Page 26 of 72

Sampling Size

Accounts of 2 years

Sampling Technique

Convenience Sampling

Limitations of the study

Department heads were busy so time for interaction was less.

The entire financial position of the company cannot be disclosed.

Company provides only secondary data, so certain type of bias is in study.

Majority of the raw materials is purchased by the main head office. So more detailed

information cannot be received about these.

SOURCES OF INFORMATION

Primary Data

The personal interview with senior officials and various members of finance and accounts

department and also with other departments and collected the data.

Secondary Data

Necessary for the study was available within the company itself. Other sources-

Website

Page 27 of 72

Textbooks

Page 28 of 72

SECTOR OVERVIEW

Textile sector

The Indian Textile sector plays an exceptionally significant role in shaping the economy of India

notably in terms of employment, foreign exchange earnings and share in value added. This sector

is the second largest sector after agriculture. The industry is rich and varied, embracing the hand-

spun and hand-woven sector at one end and the capital intensive, sophisticated mill sector at the

other. Its association with the ancient culture and tradition of the country lends it a unique

advantage in comparison with textiles industry of other countries, thus giving it an uncommon

edge to cater to a vast variety of products and market segments both domestically, as well as,

globally.

Page 29 of 72

The Indian economy is fundamentally depended upon manufacturing of textiles and its trade.

This sector has been one of the major sources for foreign exchange earnings in India . The

industry registered has ensured value of US dollar 10.1 Billion in 2003 – 2004 as compared to us

dollar 9.6 billion in the previous year. One of the key strengths of Indian textile industry is the

abundance of raw material with India being one of the major producers of fabric in the world.

Until the economic liberalization of Indian economy, the India Textile Industry was

predominantly unorganized industry. The opening up of Indian economy post 1990s led to a

stupendous growth of this industry. India Textile Industry is one of the largest textile industries

in the world. Today, Indian economy is largely dependent on textile manufacturing and exports.

The industry currently contributes about 14 per cent to industrial production, 4 per cent to GDP,

and 17 per cent to the country’s export earnings, according to the Annual Report 2010-11 of the

Ministry of Textiles. The industry accounts for nearly 12 per cent share of the country's total

exports basket. It provides direct employment to more than 35 million people.

There were various stages - from a historical perspective - where the textile industry evolved

from being a domestic small-scale industry, to the status of supremacy it currently holds. The

‘cottage stage’ was the first stage in its history where textiles were produced on a domestic basis.

During this period cloth was made from materials including wool, flax and cotton. The material

depended on the area where the cloth was being produced, and the time they were being made.

During the Industrial Revolution, new machines such as spinning wheels and handlooms came

into the picture. Making clothing material quickly became an organized industry - as compared

to the domesticated activity it had been associated with before. A number of new innovations led

to the industrialization of the textile industry in Great Britain. Clothing manufactured during the

Industrial Revolution formed a big part of the exports made by Great Britain. They accounted for

almost 25% of the total exports made at that time, doubling in the period between 1701 and

1770.

In this era, a lot of effort was made to increase the speed of the production through inventions

such as the flying shuttle in 1733, the flyer-and-bobbin system, and the Roller Spinning machine

by John Wyatt and Lewis Paul in 1738.

Page 30 of 72

In the initial phases, textile mills were located in and around the rivers since they were powered

by water wheels. After the steam engine was invented, the dependence on the rivers ceased to a

great extent. In the later phases of the 20th century, shuttles that were used in the textile industry

were developed and became faster and thus more efficient. This led to the replacement of the

older shuttles with the new ones.

Recent Trends

The mood in the Indian textile industry given the phase-out of the quota regime of the Multi-

Fibre Arrangement (MFA) is upbeat with new investment flowing in and increased orders for the

industry as a result of which capacities are fully booked up to April 2005. As a result of various

initiatives taken by the government, there has been new investment of Rs.500 billion in the

textile industry in the last five years. Nine textile majors invested Rs.26 billion and plan to invest

another Rs.64 billion. Further, India's cotton production increased by 57% over the last five

years; and 3 million additional spindles and 30,000 shuttles-less looms were installed. The

industry expects investment of Rs.1,400 billion in this sector in the post-MFA phase.

A Vision 2010 for textiles formulated by the government after intensive interaction with the

industry and Export Promotion Councils to capitalize on the upbeat mood aims to increase

India's share in world's textile trade from the current 4% to 8% by 2010 and to achieve export

value of US $ 50 billion by 2010 Vision 2010 for textiles envisages growth in Indian textile

economy from the current US $ 37 billion to $ 85 billion by 2010; creation of 12 million new

jobs in the textile sector; and modernization and consolidation for creating a globally competitive

textile industry. The textile industry is undergoing a major reorientation towards non-clothing

applications of textiles, known as technical textiles, which are growing roughly at twice rate of

textiles for clothing applications and now account for more than half of total textile production.

The processes involved in producing technical textiles require expensive equipment’s and skilled

workers and are, for the moment, concentrated in developed countries. Technical textiles have

many applications including bed sheets; filtration and abrasive materials; furniture and

healthcare upholstery; thermal protection and blood-absorbing materials; seatbelts; adhesive

tape, and multiple other specialized products and applications.

Page 31 of 72

Today, modern techniques, electronics and innovation have led to a competitive, low-priced

textile industry offering almost any type of cloth or design a person could desire.

Industry sub-sectors

The textile industry comprises the following:

Organised Cotton/Man-Made Fibre Textiles Mill Industry

Man-Made Fibre / Filament Yarn Industry

Wool and Woollen Textiles Industry

Sericulture and Silk Textiles Industry

Handlooms, Handicrafts, the Jute and Jute Textiles Industry

Textiles Exports

Anticipating massive growth in medical and automobile sectors, these sectors assures substantial

demand for non woven facilities in India. Albeit, home textiles also will lure higher demand,

there are specific demands for home textile facilities also. The 7th Five Year Plan has huge

consideration on agricultural growth that also includes cotton textile industry, resulting a

prosperous future forecast for the textile industry in India.

Strengths of Indian Textile Industry –

1. Indian Textile Industry is an Independent & Self-Reliant industry.

2. Abundant Raw Material availability that helps industry to control costs and reduces the lead-

time across the operation.

3. Availability of Low Cost and Skilled Manpower provides competitive advantage to industry.

4. Availability of large varieties of cotton fiber and has a fast growing synthetic fiber industry.

5. India has great advantage in Spinning Sector and has a presence in all process of operation and

value chain.

Page 32 of 72

6. India is one of the largest exporters of Yarn in international market and contributes around

25% share of the global trade in Cotton Yarn.

7. The Apparel Industry is one of largest foreign revenue contributor and holds 12% of the

country’s total export.

8. Industry has large and diversified segments that provide wide variety of products.

9. Growing Economy and Potential Domestic and International Market.

10. Industry has Manufacturing Flexibility that helps to increase the productivity.

11. Entrepreneurial skills

12. Huge export potential

13. Very low import content

Weaknesses of Indian Textile Industry –

1. Indian Textile Industry is highly Fragmented Industry.

2. Industry is highly dependent on Cotton.

3. Lower Productivity in various segments.

4. There is Declining in Mill Segment.

5. Lack of Technological Development that affect the productivity and other activities in whole

value chain.

6. Infrastructural Bottlenecks and Efficiency such as, Transaction Time at Ports and

transportation Time.

7. Unfavorable labor Laws.

8. Lack of Trade Membership, which restrict to tap other potential market.

Page 33 of 72

9. Lacking to generate Economies of Scale.

10. Higher Indirect Taxes, Power and Interest Rates.

Opportunities of Indian Textile Industry:

1. Growth rate of Domestic Textile Industry is 6-8% per annum.

2. Large, Potential Domestic and International Market.

3. Product development and Diversification to cater global needs.

4. Elimination of Quota Restriction leads to greater Market Development.

5. Market is gradually shifting towards Branded Readymade Garment.

6. Increased Disposable Income and Purchasing Power of Indian Customer opens New Market

Development.

7. Emerging Retail Industry and Malls provide huge opportunities for the Apparel, Handicraft

and other segments of the industry.

8. Greater Investment and FDI opportunities are available.

Threats:

1. Competition from other developing countries, especially China.

2. Continuous Quality Improvement is need of the hour as there are different demand patterns all

over the world.

3. Elimination of Quota system will lead to fluctuations in Export Demand.

4. Threat for Traditional Market for Power loom and Handloom Products and forcing them for

product diversification.

5. Geographical Disadvantages.

Page 34 of 72

6. International labor and Environmental Laws.

7. To balance the demand and supply.

8. To make balance between price and quality

Page 35 of 72

COMPANY OVERVIEW

Page 36 of 72

Page 37 of 72

COMPANY OVERVIEW

Lamiya Silks, the largest showroom network, has been the most trusted brand in Kerala. Today

Lamiya Silks prides itself in world-class showrooms all over Kerala. Lamiya Silks has its main

branch at Kozhikode, Kerala. It has about 15 branches at various places in Kerala. Thrissur store

is one among them.

Lamiya Silks’ product lines are different from other players in the textile industry. So are its

infrastructure facilities. Lamiya Silks has a string of looms in all major centers across the

country. In-house designing centers and manufacturing units help Lamiya Silks bring the latest

trends to its shelves. In addition to all this, Lamiya Silks owns India’s largest wholesale textile

showroom, which powers this heritage brand to control prices and maximize quality right

through the year.

Lamiya Silks is spread across three floors. The ground floor has kids’ collection and dhotis, the

first floor is dedicated to the women’s section and the second floor is exclusively for men.

The ground floor in this apparel store displays has clothes for kids from 5-12 years of age. The

garments are organized size-wise, making it easier to browse through. Ethnic wear like kids’

Page 38 of 72

ghaghra cholis, sherwanis for your little ones along with kasavu and cotton dhotis for men

starting at Rs. 250 are all available. Western wear for kids like shirts, trousers and T-shirts are

there too.

The stairs that lead to the first floor has door mats, curtains, bed sheets, blankets, bedspreads and

some small household items on display.

Page 39 of 72

The floor above has sarees including wedding srees, party wear designer sarees, office wear

cotton sarees and ordinary cotton sarees for Rs. 200 onwards. Salwar kameez material and

readymade churidars are there too. The wedding collection in this section has a good collection

of sarees, starting from Rs. 1,500.

Page 40 of 72

There is a wide range of designer saree collection. The area allotted for designer saree is

comparatively more than the others.

The second floor at Lamiya Silks, exclusively for men, has an assortment of branded readymade

shirts and trousers, shirting material, sherwanis and kurtas. The readymade shirts in this section

start at Rs. 200 for the unbranded ones and Rs. 400 for the branded ones. Here you can also find

shirting material, the price of which starts from Rs. 90 for a meter. Also check out the sherwanis

here that cost around Rs. 2,500.

Page 41 of 72

Lamiya Silks can be easily located since it is on the roadside. Price wise, it seems reasonable

compared to other stores in the vicinity. It accepts cash and credit card for payment. It falls short

of adequate parking space.

Lamiya Silks provides a complete wedding package to its customers. The world of wedding

fashion is witnessing a revolution in Bridal Wear. Revolutions that will alter the way millions of

Indian celebrate their weddings, and Lamiya Silks is at the helm of this revolution. The wedding

centre brings under one roof the finest selection of wedding saris and other accessories. With the

availability of wedding saris, dress material and readymade garments at the centre, marriage

shopping would be a convenient and enjoyable experience. Created by a panel of India’s best

designers, these materials conform to the highest standards of quality with wide range accessible

to all. Lamiya Silks also offers exclusive collection of life style items including perfumes, leather

accessories for men and women and a large collection of premium quality wedding gifts.

Objectives of the Company

Objectives establish the goals and the aims of the business and determine the shape of future

events. Objectives are the way of achieving motives for profit of social service.

Main objectives of Lamiya Silks are-

Increasing productivity of work force

To introduce new products and create new markets

Page 42 of 72

Customers service and customer satisfaction

Improving work culture among the employees

Capitalizing on company strength and use of corporate assets

Continuous innovation

To improve the advertising effectiveness

To ensure that a large proportion of its sales is directed towards the sectors and urban

sectors.

ORGANISATION CHART

Page 43 of 72

INTERNSHIPACTIVITIES

Page 44 of 72

METHODS OF WORKING CAPITAL ANALYSIS

There are so many methods for analysis of financial statements used in companies. Here the

following techniques are being used to analysis the working capital management of Lamiya

Silks-

Comparative size statement

Trend analysis

Cash flow statement

Ratio analysis

A detail description of these methods is as follows-

COMPARATIVE SIZE STATEMENT

When two or more than two years figures are compared to each other we call them comparative

size statements in order to estimate the future progress of the business, it is necessary to look at

the performance of the company. These statements show the absolute figures and also show the

change from one year to another.

Benefits of this method to the company-

To indicate the trends, these statements show the change in production, sales and

expenses.

To make the data simple and more understandable

TREND ANALYSIS

To analyse many years financial statements, this method is used. This indicates the direction on

movement over the long time and help in the financial statements.

Procedure for calculating trends-

1. Previous year is taken as the base year

Page 45 of 72

2. Figures of the base year are taken as 100

3. Trend % are calculated in relation to base year.

Benefits-

It is beneficial to find out the long run changes

It is helpful in future forecasting.

CASH FLOW STATEMENT

Cash flow statements are the statements of changes in the financial position prepared on the basis

of funds defined in cash or cash equivalents. In short cash flow statement summaries the cash

inflows and outflows of the firm during a particular period of time.

Benefits for the company-

To prepare the cash budget

To compare the cash budgets

To show the position of the cash and cash equivalents.

RATIO ANALYSIS

Ratio analysis is the process of the determining and presenting the relationship of the items and

group of items in the statements. Ratio can assist management in its basic functions of

forecasting, planning, coordination, control and communication.

Benefits to the company-

Helpful in analysis of financial statements

Helpful in comparative study

Helpful in locating the weak spots of the company

Helpful in forecasting

Estimate about the trend of the business

Page 46 of 72

Fixation of ideal standards

Effective control

Study of financial soundness

Types of ratio-

Liquidity Ratio- they indicate the firms ability to meet its current obligation out of current

resources.

Current ratio = current assets / current liabilities

Quick ratio = liquid assets / current liabilities

Liquid assets = current assets – stock – prepaid expenses

Leverage or Capital Structure Ratio- this ratio discloses the firms ability to meet the

interest costs regularly and long term solvency of the firm.

Debt equity ratio = long term loans / shareholders funds or net worth

Debt to total fund ratio = long term loans / shareholder funds + long term loan

Proprietary ratio = shareholders fund / shareholders fund + long term loan

Activity ratio or Turnover ratio - they indicate the rapidity with which the resources

available to the concern are being used to produce sales.

Stock turnover ratio = cost of goods sold / average stock

cost of goods sold = net sales / gross profit,

Average stock = opening stock + closing stock / 2

Debtors turnover ratio = net credit sales / average debtors + average B/R

Average collection period = debtors+ B/R Credit sales per day

Credit sales per day = net credit sales of the year /365

Creditors turnover ratio = net credit purchases / average creditors + avg. B/P

Average payment period = creditors + B/P / credit purchase perday

Fixed assets turnover ratio = cost of goods sold / net fixed assets

Net fixed assets = fixed assets – depreciation

Page 47 of 72

Working capital turnover ratio = cost of goods sold / working capital

Working capital = current assets – current liabilities

Profitability ratios or Income ratios - the main objective of every business concern is to

earn profits. A business must be able to earn adequate profit in relation to the risk and

capital invested in it.

Gross profit ratio = gross profit / net sales *100

Net sales = sales – sales return

Net profit ratio = net profit / net sales * 100

Operating net profit = operating net profit / net sales * 100 or gross profit –

operating expenses

Operating ratio = cost of goods sold + operating expenses / net sales * 100

Cost of goods sold = net sales – gross profit

Operating expenses = office and administration expenses + selling & distribution

expenses + discount + bad debts + interest on short term loans

Earning per share(EPS) = net profit – dividend on preference share / no. of equity

shares

Dividend per share (DPS) = dividend paid to equity shareholders / no. of equity

shares * 100

Dividend payout ratio (DP) = DPS /EPS * 100

RATIO ANALYSIS FOR LAMIYA SILKS

Current ratio

2010

C.R = 1321.22 / 969.15 = 1.36

2011

C.R = 1517.69 / 1266.86 = 1.20

Page 48 of 72

Comment-

As compared to previous year, current ratio has decreased in current year because of

increase in current liabilities.

Quick ratio

2010

Q.R = 570.49 / 969.15 = 0.59

2011

Q.R = 693.55 / 1266.86 = 0.55

Comment-

As compared to previous year, quick ratio has decreased in current year.

Debt equity ratio

2010

DER = 1979.67 / 4982.08 = 0.40

2011

DER = 2951.56 / 6230.04 = 0.47

Interest coverage ratio

2010

I.C.R = 1201.90 / 103.38 = 11.67 times

2011

I.C.R = 2189.26 / 111.84 = 19.57 times

Comment-

Interest coverage ratio is increasing as compared to previous year. This indicates that the

firm will be able to pay the interest on long term loans regularly.

Fixed assets turnover ratio

2010

F.A.T.R = 5159 / 3004.63 = 1.72 times

2011

Page 49 of 72

F.A.T.R = 6097 / 3390.44 = 1.80 times

Comment-

This ratio reveals how efficiently the fixed assets are being utilized. As compared to

previous year, this ratio is increasing which indicates that there is better utilization of fixed

assets.

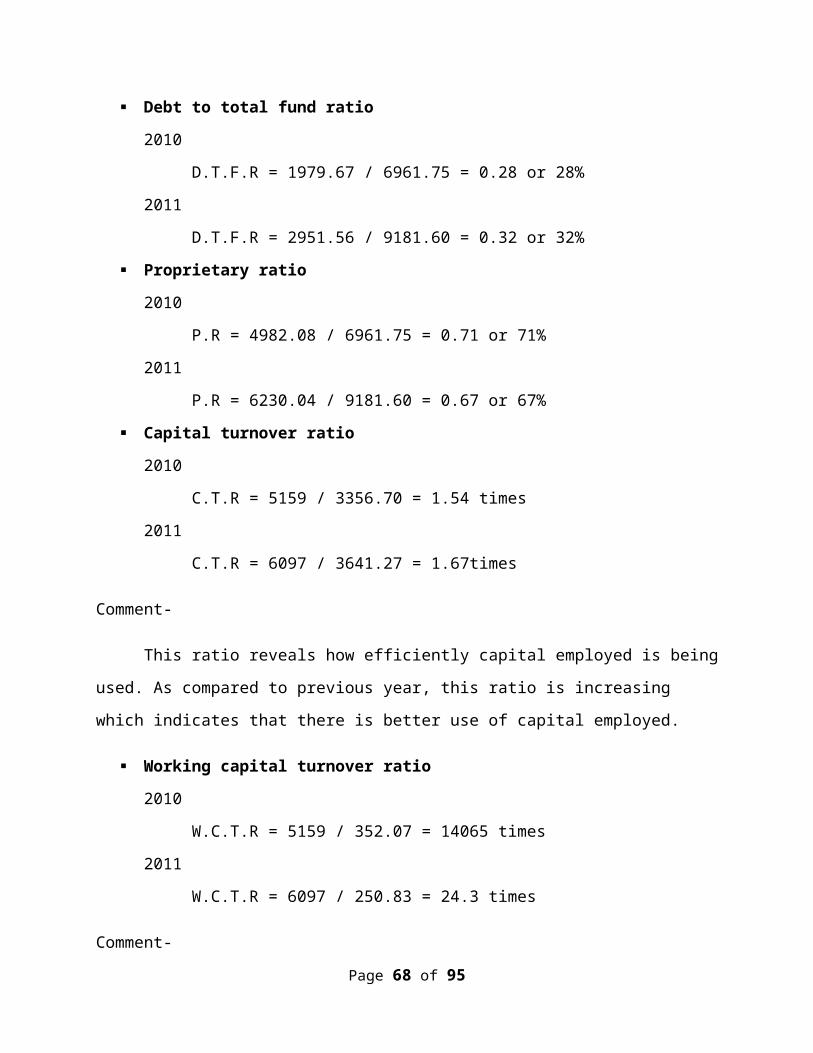

Debt to total fund ratio

2010

D.T.F.R = 1979.67 / 6961.75 = 0.28 or 28%

2011

D.T.F.R = 2951.56 / 9181.60 = 0.32 or 32%

Proprietary ratio

2010

P.R = 4982.08 / 6961.75 = 0.71 or 71%

2011

P.R = 6230.04 / 9181.60 = 0.67 or 67%

Capital turnover ratio

2010

C.T.R = 5159 / 3356.70 = 1.54 times

2011

C.T.R = 6097 / 3641.27 = 1.67times

Comment-

This ratio reveals how efficiently capital employed is being used. As compared to

previous year, this ratio is increasing which indicates that there is better use of capital employed.

Working capital turnover ratio

2010

W.C.T.R = 5159 / 352.07 = 14065 times

2011

W.C.T.R = 6097 / 250.83 = 24.3 times

Page 50 of 72

Comment-

This ratio reveals how efficiently working capital has being utilized in making sales. As

compared to previous year, this ratio is increasing which indicates the efficient use of working

capital.

Stock turnover ratio

2010

S.T.R = 5159 / 715 = 7.22 times

2011

S.T.R = 6097 / 784.44 = 7077 times

Comment-

This ratio indicates whether stock has been efficiently used or not. As compared to

previous year, there is a slight increase in this ratio.

Gross profit ratio

2010

G.P.R = 1494 / 6621 * 100 = 22.56%

2011

G.P.R = 2507 / 8604 * 100 = 29.14%

Net profit ratio

2010

N.P.R = 1202 / 6621 * 100 = 18.15%

2011

N.P.R = 2189 / 8604 * 100 = 25.44%

Operating net profit ratio

2010

O.N.P.R = 1590.9 / 6621 * 100 = 24.02%

2011

O.N.P.R = 2619 / 8604 * 100 = 30.44%

Earning per share

Page 51 of 72

2010

E.P.S = 8630000000 / 91808510 = 94 Rs

2011

E.P.S = 15360000000 / 91428571 = 168 Rs

Dividend per share

2010

D.P.S = 1836176200 / 91808510 = 20 Rs

2011

D.P.S = 2514285703 / 91428571 = 27.5 Rs

Dividend payout ratio

2010

D.P.R = 20 / 94 * 100 = 22%

2011

D.P.R = 27.5 / 168 * 100 = 17%

Proportion of various sources of working capital in percentage –

Current assets, loans and advances

Interest accured on investments

2010

1.46 / 2026.76 * 100 = 0.07%

2011

0.70 / 2342.39 * 100 = 0.02%

Inventories

2010

750.73 / 2026.76 * 100 = 37.04%

2011

824.14 / 2342.39 * 100 = 35.18%

Sundry debtors

2010

Page 52 of 72

413.45 / 2026.76 * 100 = 20.39%

2011

576.48 / 2342.39 * 100 = 24.64%

Cash and bank balances

2010

155.58 / 2026.76 * 100 = 7.67%

2011

116.38 / 2342.39 * 100 = 4.96%

Loans and advances

2010

705.54 / 2026.76 * 100 = 34.83%

2011

824.69 / 2342.39 * 100 = 35.20%

Current liabilities and provisions-

Current liabilities

2010

969.15 / 1273.37 * 100 = 76.10%

2011

1266 / 1450.06 * 100 = 87.36%

Provisions

2010

304.22 / 1273.37 * 100 = 23.90%

2011

183.20 / 1450.06 * 100 = 12.63%

Page 53 of 72

TABLE 1

COMPARATIVE P&L ACCOUNT

(For the year 2010-2011)

(Rs. in Crores)

FY 2011 FY 2010 % change

Net turnover 14095.2 10224.0 38

Other income 317.7 267.9 19

Total expenditure 10122.8 8155.3 24

Operating profit (PBIT) 4290.1 2336.6 84

Interest 228.6 218.3 5

Depreciation 610.0 563.1 8

Exceptional items - 4.1 -

Profit before tax 3451.5 1559.3 121

Total tax expenses 1092.1 402.7 171

Net profit after total tax 2359.4 1156.6 104

Minority share 391.9 116.0 238

Net profit 1967.5 1040.6 89

Page 54 of 72

TABLE 2

TREND ANALYSIS

(For the liability side of 2010-2011)

Particulars 2011 2010 Base Trend % Current Tend %

Current liability

Liability 1266.86 969.15 100 130.73

Provisions 183.20 304.22 100 60.21

Total (A) 1450.06 1273.37 100 113.87

Fixed liability

Share capital 91.69 91.69 100 100

Reserves &

surplus

6138.35 4890.39 100 125.5

Loans 2951.56 1979.67 100 149.09

Def. tax liability 582.55 584.38 100 99.68

Total (B) 9764.15 7546.13 100 129.39

Total liability

(A+B)

11214.21 8819.50 100 127.15

Page 55 of 72

TABLE 3

TREND ANALYSIS

(For assets side of 2010-2011)

Particulars 2011 2010 Base trend % Current trend

%

Fixed assets

Fixed assets 4582.79 3298.27 100 138.94

Fixed assets held

for disposable

14.33 12.76 100 112.30

Investments 4274.70 3481.71 100 122.79

Total (A) 8871.82 6792.74 100 130.60

Current assets

Stock 824.14 750.73 100 109.77

Interest accrued .70 1.46 100 47.94

Debtors 576.48 413.45 100 139.43

Cash 116.38 155.58 100 74.80

Loans 824.69 705.54 100 116.88

Total (B) 2342.39 2026.76 100 115.59

Total assets

(A+B)

11214.21 8819.50 100 127.15

TABLE 4

Page 56 of 72

CAH FLOW ANALYSIS

(For 2010-2011)

(Rs in Crores)

Particulars FY 2011 FY 2010

SOURCES OF CASH

Cash from operations 1816.0 1077.1

Increase in debts 947.6 -

Non operating cash flow 114.0 67.1

Decrease in cash and cash equivalent 39.2 -

Decrease in working capital - 205.2

2916.8 1349.4

USES OF CASH

Net increase in investments 647.1 549.2

Net capital expenditure 1598.2 399.5

Decrease in debts - 53.3

Interest 109.4 112.7

Dividend 478.8 165.8

2916.8 1349.4

TABLE 5

CASH FLOW STATEMENT

Page 57 of 72

(For year 2010 – 2011)

(Rs in Crores)

Cash flow from operating

activities

2011 2010

Net profit before tax 2189.26 1201.90

Depreciation 317.91 291.64

Interest expenses 111.84 103.38

Interest income (31.84) (29.48)

Dividend income (81.43) (38.04)

Profit / loss on sale of fixed

assets (Net)

(4.62) 3.99

Profit on sale of long term

investments(Net)

(2.70) (62.57)

Profit on sale of current

investments (Net)

(49.41) (7.27)

Operating profit before

working capital changes

2449.01 1330.06

Trade and other receivables (314.56) (116.66)

Inventories (73.41) (72.41)

Assets held for disposal (1.57) 0.97

Trade payables 306.17 159.70

Cash generated from

operations

2365.64 1668.74

Direct taxes paid(Net) (632.97) (380.42)

Net cash from operating

activities

1732.67 1288.32

Cash flow from investing

activities

Purchase of fixed assets 326.4 410.5

Sale of fixed assets (354.13) (388.73)

Page 58 of 72

Purchase of investments (150.11) (173.66)

Sale of investments (128.19) (91.57)

Investments / advances in joint

ventures, subsidiaries & others

(16.77) (11.75)

Interest received (322.8) (255.21)

Net cash from investing

activities

(301.75) (231.24)

Cash flow from financing

activities

19.71 5.65

Proceeds from borrowings (75.41) (792.83)

Repayments of borrowings 666.13 53.64

Interest paid (1294.15) 24.74

Dividends paid 3.37 1.79

Corporate dividend tax 74.29 55.28

Dividend received 39.37 86.32

Net cash from financing

activities

(868.44) (796.65)

Net increase / decrease in

cash & cash equivalent

(140.78) 117.37

At beginning of year 227.48 110.11

At end of year 86.7 227.48

TABLE 6

PROFIT & LOSS A/C

of the year ending 2010-2011

Page 59 of 72

(Rs. in Crores)

2011 2010

INCOME

Gross sales

Less- Excise Duty

9607.97

986.29

7638.41

985.80

Net sales 8603.59 6652.61

Interest & dividend income 113.27 67.53

Other income 168.49 152.41

Increase / decrease in stock (16.44) (43.48)

868.91 6829.07

EXPENDITURE

Raw material consumed 2219.32 1822.69

Manufacturing expenses 1744.33 1580.34

Purchases of finished & other products 321.16 240.15

Payments to & provisions for employees 459.40 407.64

Selling, distribution, administration & other expenses 1505.69 1181.33

Interest 111.84 103.38

Depreciation 317.91 291.64

6679.65 5627.17

Profit before tax & exceptional items 2189.26 1201.90

Surplus on pre-payment of sales tax loan - 4.13

Write back of provision for diminution 37.10 -

Profit before tax 2226.36 1206.03

Provision for current tax (692.38) (369.82)

Deferred tax 1.83 27.00

Profit after tax 1535.81 863.21

Debenture redemption reserve no longer required 38.56 8.62

Investment allowance reserve no longer required 0.05 0.25

Balance brought forward from previous year 878.37 815.35

Profit available for appropriation 2452.79 1687.43

Page 60 of 72

Appropriations-

Interim dividend 252.10 -

Proposed dividend - 183.35

Corporate dividend tax 35.36 25.41

General reserve 1200.00 600.00

Balance carried to balance sheet 965.33 878.37

2452.79 1687.43

TABLE 7

BALANCE SHEET

For the year ended 2011

(Rs in Crores)

SOURCES OF FUNDS

SHAREHOLDERS FUND

FY(2010-2011) FY(2009-

2010)

Share capital 91.69 91.69

Reserve & surplus 6138.35 4890.39

Loan funds

Secured loans 2291.00 1386.12

Unsecured loans 660.56 593.55

2951.56 1979.67

Deferred tax liabilities 582.55 584.38

TOTAL 9764.15 7546.13

APPLICATIONS OF FUNDS

Fixed assets

Gross block 6770.97 6114.12

Page 61 of 72

Less – depreciation 3380.53 3109.49

Net block 3390.44 3004.63

Capital work-in-progress 1192.35 293.64

4582.79 3298.27

Fixed assets held for disposal 14.33 12.76

Investments 4274.70 3481.71

Current assets, loans & advances

Interest accrued on investments 0.70 1.46

Inventories 824.14 750.73

Sundry debtors 576.48 413.45

Cash and bank balances 116.38 155.58

Loans and advances 824.69 705.54

2342.39 2026.76

Less-

Current liabilities & provisions

Liabilities 1266.86 969.15

Provisions 183.20 304.22

1450.06 1273.37

Net current assets 892.33 753.39

TOTAL 9764.15 7546.13

Page 62 of 72

INTERNSHIPASSESSMENT

Internship has helped a lot to understand the practical side of job, which is different from

the textbook theories. It has also helped me to improve my communication skills.

Customer handling was one of the important learning that I gained from my internship.

From the customer point of view, it is easy. But not so when in the position of a staff or

employee. Was also able to maintain a good relationship with the employees on and off

the shop floor. I did my internship on ‘working capital management’. It helped me to

Page 63 of 72

know how the analysis is being done by comparing the Balance Sheets of 2subsequet

years.

During the period of internship, I was supposed to thoroughly go through the financial

statements of the company and understand the aspects and concepts involved in it. In the

meanwhile, I also contributed in the sales department and helped in the billing session,

which gave me a very different experience.

Having done my internship in the finance sector my interest for it has increased which

will help me in my coming semesters.

It is very well said that “Finance always need a theory backup”. One needs to really know

what finance is all about and how much it is important for the company’s smooth

functioning.

Page 64 of 72

CONCLUSION

FINDINGS

In 2011 there is increase in current assets by 24% than 2010 and there is increase in current

liability by 17%, because of greater increase in current assets than in current liabilities, the

position of Working Capital has improved.

Page 65 of 72

The % of fixed assets has come down in 2011 from 2010

As per current ratio firm is able to pay its current liability

Quick ratio presents a better test of short term financial position, which shows better

working capital position of the firm

Debt equity ratio and debt to total fund ratio presents protection to long term lenders and

shows sufficient working capital in the firm

Gross profit and net profit have increased from previous year

Cash flow statement indicates outflow of cash in comparison to past year

Due to better long term and short term financial conditions firm’s working capital is

better than that of previous year.

RECOMMENDATIONS

The company must concentrate on the percentage of fixed assets in the coming years.

The company must keep on maintaining the firms’ debt and equity and debt to total fund

so as to maintain the working capital.

Apart from the topic recommendations, the billing sector must involve more number of

persons in order to reduce the rush.

The company should try to improve working capital turnover ratio by efficient utilization of

working capital.

The company should try to use more proprietors fund in current assets, so that they can

improve current assets to proprietors fund.

By using proprietors fund properly, the company can increase return on capital employed.

Page 66 of 72

ILLUSTRATION

The details of sales in different sessions in the store during the month of April – June 2012.

CHART 1

MAIN DEPARTMENT SALES

Page 67 of 72

36%

17%14%

15%

19%

Department SalesDesigner Saree Wedding Saree Churidhar Kids Wear Gents Wear

The statistics of the apparels department shows that the customers demand more for designer

sarees. Now-a-days lady customers are increasing and so is such a result. The trend of churidhars

and salwars have come down when compared to the designer sarees. 35% of the department sales

is in the designer saree session.

The different sales percentage of each apparels are-

Designer Saree 35%

Gents Wear 19%

Wedding Saree 17%

Kids Wear 15%

Churidhar 14%

Page 68 of 72

Sales details of other sessions in the store, which includes cosmetics, bed spreads, blankets,

curtains, etc.

CHART 2

SALES OF OTHER DEPARTMENTS

28%

35%

14%

18%

5%

SalesCosmetics Bed Spreads Blanket Curtain Doormat

When conducting a study among the other accessories and materials, we can come to a

conclusion that customers give more preference to cosmetics and then to others. The demand for

blanket is relatively less when compared to bed spreads. This is because of the climate conditions

in Kerala.

The different sales percentage of other materials in the store are-

Bed Spreads 35%

Cosmetics 28%

Page 69 of 72

Curtains 18%

Blanket 14%

Doormat 5%

Page 70 of 72

BIBLIOGRAPHY

COMPANY REPORTS

Annual reports of Lamiya Silks

2009-10

2010-11

Page 71 of 72

BOOKS REFERRED

Khan, M.Y. and Jain, P.K., 2011, Financial Management, Tata McGraw-Hill, New

Delhi.

Sekaran, U. and Bougie, R., 2010, Research Methods for Business, New Delhi, Wiley-

India Edition, 5th edition.

2. Kothari, C.R., 1985, Research Methodology- Methods and Techniques, New Delhi,

Wiley Eastern Limited.

WEBLIOGRAPHY

http://lamiyasilks.com/

http://en.wikipedia.org/wiki/Textile_industry

http://www.textilehistory.org/

http://en.wikipedia.org/wiki/Working_capital

Page 72 of 72