renewable energies in germany - status quo and future ... filesolar biomass iii. related business...

TRANSCRIPT

© a

lph

a v

en

tus/R

EP

ow

er

20

09

Renewable Energies in Germany -

Status Quo and Future Business Potential

Esther Frey

Manager Renewable Energies & Resources

09.11.2012

www.gtai.com

I. Germany´s Energy Transformation

II. Renewable Energies in Germany

Wind

Solar

Biomass

III. Related business fields

Grid expansion, Storage, Smart Metering

Agenda

09.11.2012 2

09.11.2012 | www.gtai.com

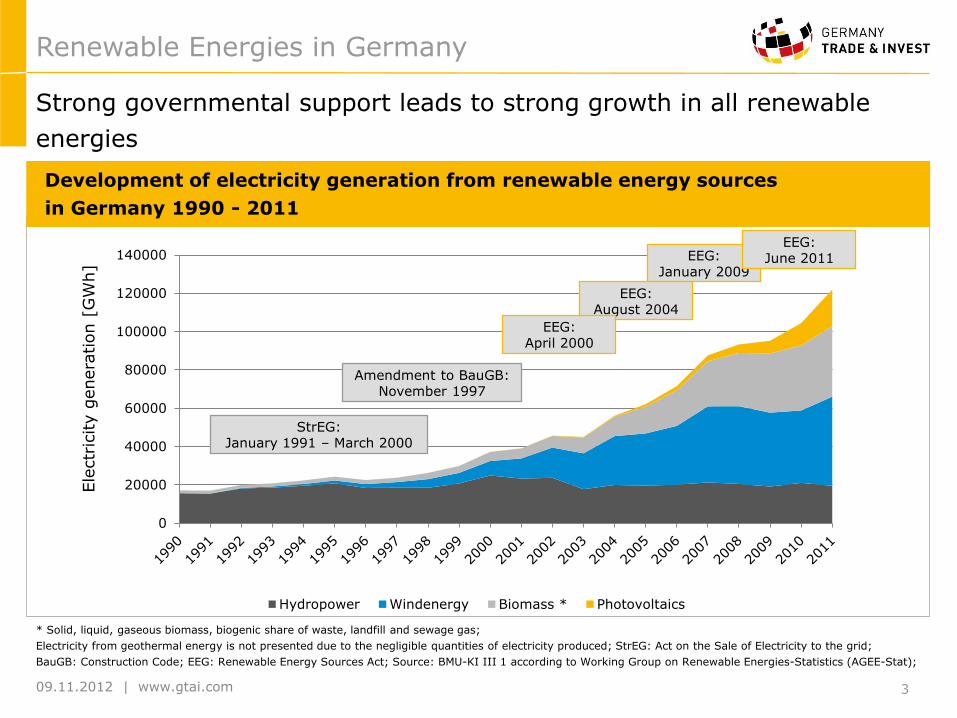

Renewable Energies in Germany

Strong governmental support leads to strong growth in all renewable

energies

* Solid, liquid, gaseous biomass, biogenic share of waste, landfill and sewage gas;

Electricity from geothermal energy is not presented due to the negligible quantities of electricity produced; StrEG: Act on the Sale of Electricity to the grid;

BauGB: Construction Code; EEG: Renewable Energy Sources Act; Source: BMU-KI III 1 according to Working Group on Renewable Energies-Statistics (AGEE-Stat);

0

20000

40000

60000

80000

100000

120000

140000

Hydropower Windenergy Biomass * Photovoltaics

Ele

ctr

icity g

enera

tion [

GW

h]

EEG: January 2009

EEG: August 2004

EEG: April 2000

Amendment to BauGB: November 1997

StrEG: January 1991 – March 2000

3

EEG: June 2011

Development of electricity generation from renewable energy sources

in Germany 1990 - 2011

09.11.2012 | www.gtai.com

Main Objectives

The New Energy Concept (2010)

Energy efficiency measures

Increase in energy productiveness 2.1% p.a.

Reduction of energy consumption -50% (2050 vs. 2008)

Reduction of electricity consumption -25% (2050 vs. 2008)

Renovation rate 2% p.a.

Reduction of energy for transportation -40% (2050 vs. 2005)

Climate protection measures 2020 2050

CO2 cuts vs. 1990 -40% -80%

Renewable share of… 2020 2050

Total energy consumption 18% 60%

Electricity consumption 35% 80%

Heat generation 14% 60%

4

www.gtai.com

Due to the nuclear disaster in Fukushima in

2011, closure of nuclear power plants was

brought forward from 2036 to 2022

8 out of 17 nuclear power plants were

already shut down in 2011

2011: 17.6% nuclear power of total energy

consumption (2010: 22.6%)1

Germany‘s nuclear power phase-out

1) Quelle: BMWi „Die Energiewende in Deutschland“, Februar 2012

2) Quelle: DAtF, 2012

09.11.2012 5

Active nuclear reactor with date of scheduled closure

Nuclear reactor already closed

Berlin

Hamburg

Cologne

Munich

Stuttgart

Frankfurt

2021

2022

2021

2021

2017 2022

20192022

2015

21.547

4.285

0 0

5000

10000

15000

20000

25000

2010 2011 2012 2015 2019 2021 2022 2023

Development of installed nuclear power plants

capacity in MW2

7% of electricity

generation (2010) 22.6 % of

electricity

generation

(2010)

09.11.2012 | www.gtai.com

Faster expansion of renewable energies

Integration of renewable energies into the overall energy system

Central component: wind energy

Increase energy R&D levels - up to €0.5 bn will be made available

Expansion of electricity and smart grids as well as energy storage capacity

Restructuring the fossil power plant park towards more flexible power stations

Increase energy efficiency (particularly in buildings)

Cost efficiency and efficient procurement

European initiatives for energy efficiency

Measures for implementing the new energy policy after the decision

taken on the gradual phase-out of nuclear power by 2022

Source: http://www.bmu.de/energiewende/beschluesse_und_massnahmen/doc/47892.php

The Federal Energy Concept

6

www.gtai.com

I. Germany´s Energy Transformation

II. Renewable Energies in Germany

Wind

Solar

Biomass

III. Related business fields

Grid expansion, Storage, Smart Metering

Agenda

09.11.2012 7

www.gtai.com

The German Wind Energy Market

Structure of Electricity Production from

Renewable Energies in Germany 20111)

of renewable energies Prognosis of

yearly installed offshore capacity (in

GW)1)

Renewable Energies have a share of 20% of the German electricity

consumption. The biggest part comes from wind energy.

Sources 1) BMU 2012: Entwicklung der EE in Deutschland in 2011 2) BMU 2012 – Langfristszenarien und Strategien für den Ausbau der EE in Deutschland

09.11.2012

Wind Energy

38,10%

Hydro Power

16,00%

Photo-voltaics

15,60%

Biogas 14,40%

Biomass 9,30%

Waste 4,10%

Others 2,50%

Prognosis of Electricity Production (in

TWh/a) from Wind in Germany2)

8 27 38 63 82 91

101 118

132

8

33 61

89

115 128

0

50

100

150

200

250

300

350

400

450

Hydro Power Wind - Onshore

Wind - Offshore PV

Biomass Geothermal

8

www.gtai.com

Offshore Wind

255

182

300

500

563

680

900

1.339

2.400

3.000

5.178

6.000

10.000

13.000

0 2.000 4.000 6.000 8.000 10.000 12.000 14.000

others

Sweden

Greece

Poland

Estonia

Belgium

Finland

Denmark

Irland

Spain

Netherlands

France

Germany

UK

Political targets for offshore wind in Europe until 2020 (in MW)

Germany and UK offshore wind markets are strongly backed up by

political targets.

Source: WAB 2011

09.11.2012 9

www.gtai.com

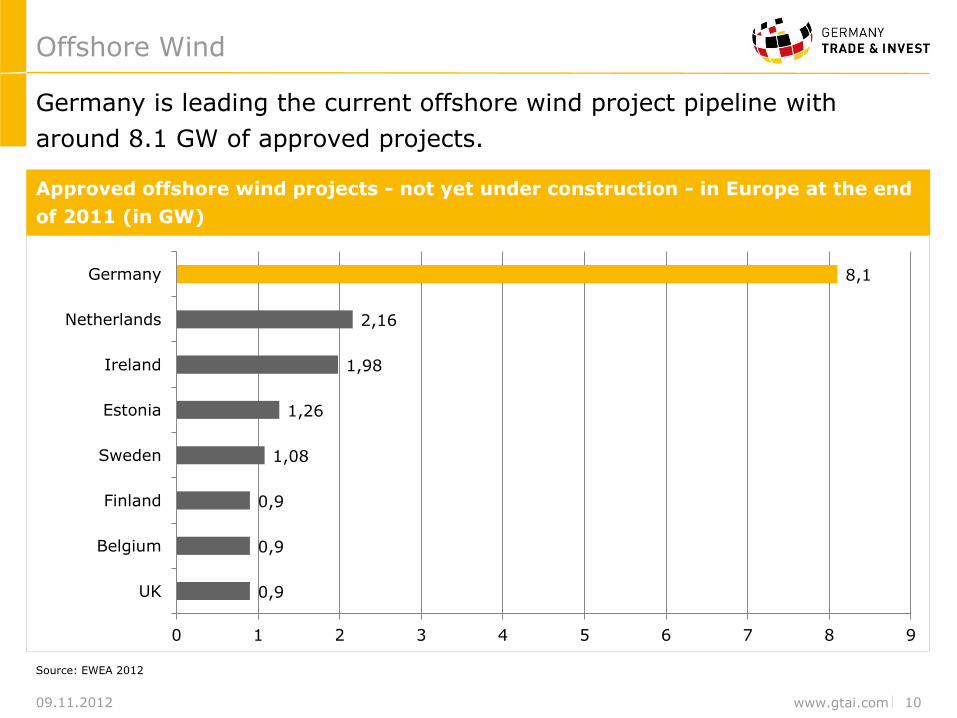

Offshore Wind

Approved offshore wind projects - not yet under construction - in Europe at the end

of 2011 (in GW)

Germany is leading the current offshore wind project pipeline with

around 8.1 GW of approved projects.

Source: EWEA 2012

09.11.2012 10

0,9

0,9

0,9

1,08

1,26

1,98

2,16

8,1

0 1 2 3 4 5 6 7 8 9

UK

Belgium

Finland

Sweden

Estonia

Ireland

Netherlands

Germany

www.gtai.com

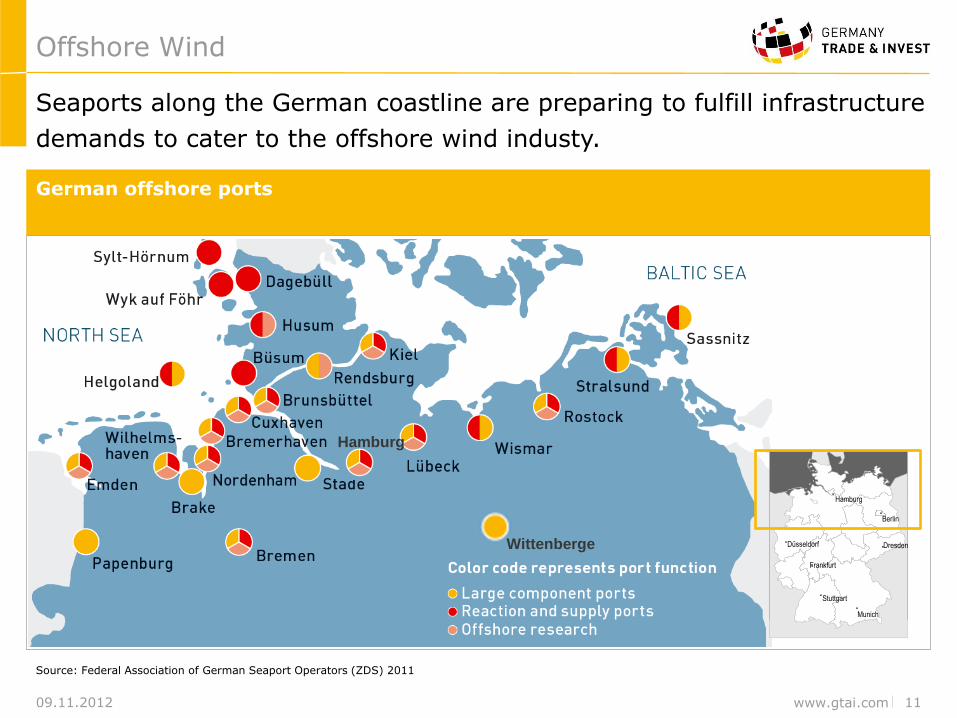

Seaports along the German coastline are preparing to fulfill infrastructure

demands to cater to the offshore wind industy.

Source: Federal Association of German Seaport Operators (ZDS) 2011

Offshore Wind

09.11.2012

German offshore ports

Stuttgart

Munich

Düsseldorf

Berlin

Dresden

Hamburg

Frankfurt

11

Hamburg

Wittenberge

www.gtai.com

Planning reliability through new legislation on liability

If Germany’s transmission system operators fail

to complete connections in time, delaying the

energy production, the damage will be

compensated.

90% of the original Feed-in-tariff from the 11th

day on.

The TSO can allocate the costs to the end

customer if not acting grossly negligent or

intentional.

New law to facilitate and accelerate offshore grid connections through binding

grid development plan and new liability rules.

Financing to be shouldered by more investors.

What‘s next?

Source: Federal Ministry for the Environment, Nature Conservation and Nuclear Safety, 2012

Offshore Wind

09.11.2012 12 R&D Support

Financing bottleneck to be solved

Mitsubishi and TenneT to partner for specific

grid connections

Allianz and Munich Re consider taking part in

German offshore grid. This is an save

investment as the Federal Network Agency

ensures an equity return 9%.

www.gtai.com

Repowering

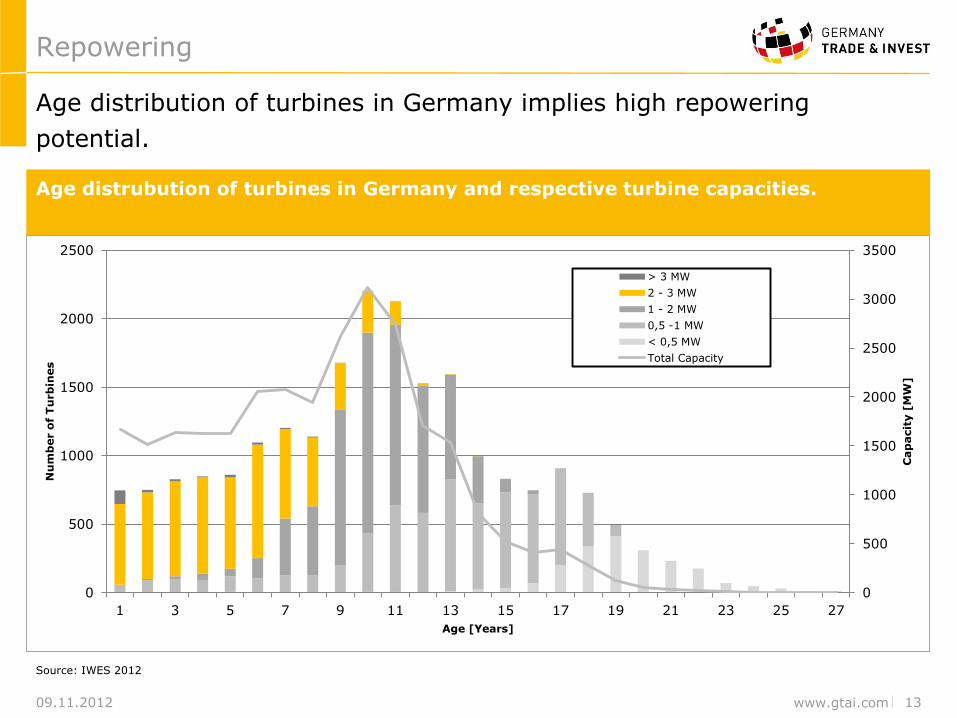

Age distrubution of turbines in Germany and respective turbine capacities.

Age distribution of turbines in Germany implies high repowering

potential.

Source: IWES 2012

09.11.2012 13

0

500

1000

1500

2000

2500

3000

3500

0

500

1000

1500

2000

2500

1 3 5 7 9 11 13 15 17 19 21 23 25 27

Cap

acit

y [

MW

]

Nu

mb

er o

f T

urb

ines

Age [Years]

> 3 MW

2 - 3 MW

1 - 2 MW

0,5 -1 MW

< 0,5 MW

Total Capacity

www.gtai.com

I. Germany´s Energy Transformation

II. Renewable Energies in Germany

Wind

Solar

Biomass

III. Related business fields

Grid expansion, Storage, Smart Metering

Agenda

09.11.2012 14

09.11.2012 | www.gtai.com 15

Germany

7485 (25%)

Italy

9284

China

2200

Japan

1296

France

1671

USA

1855

Rest of

World 3040

Greece 426

Australia 774

Total 29.7 GWp

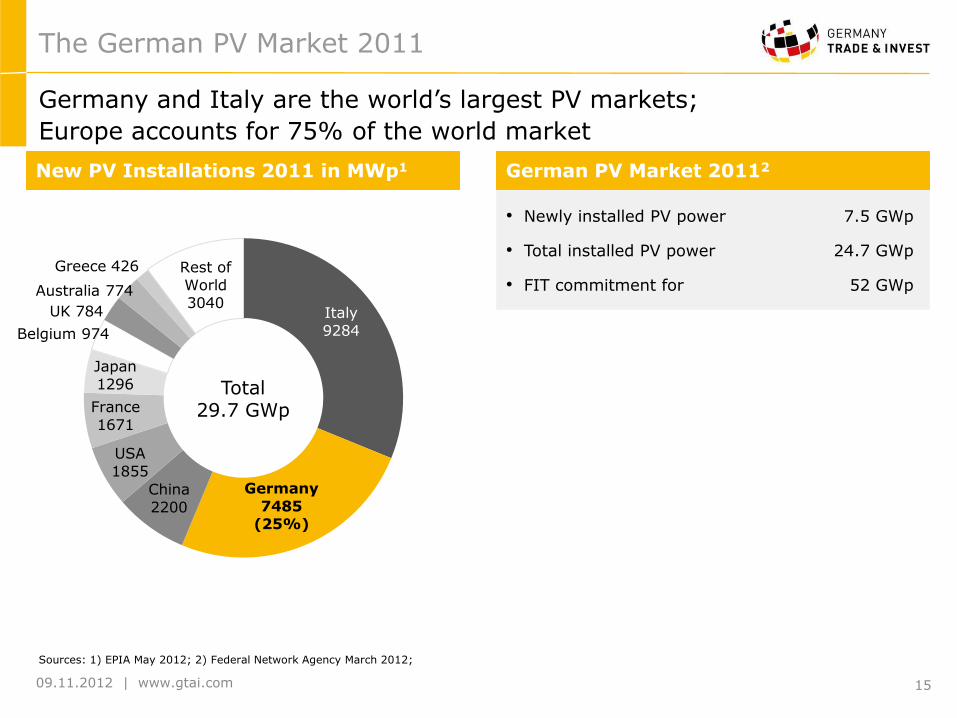

The German PV Market 2011

Germany and Italy are the world’s largest PV markets;

Europe accounts for 75% of the world market

German PV Market 20112 New PV Installations 2011 in MWp1

Sources: 1) EPIA May 2012; 2) Federal Network Agency March 2012;

• Newly installed PV power 7.5 GWp

• Total installed PV power 24.7 GWp

• FIT commitment for 52 GWp

UK 784

Belgium 974

www.gtai.com

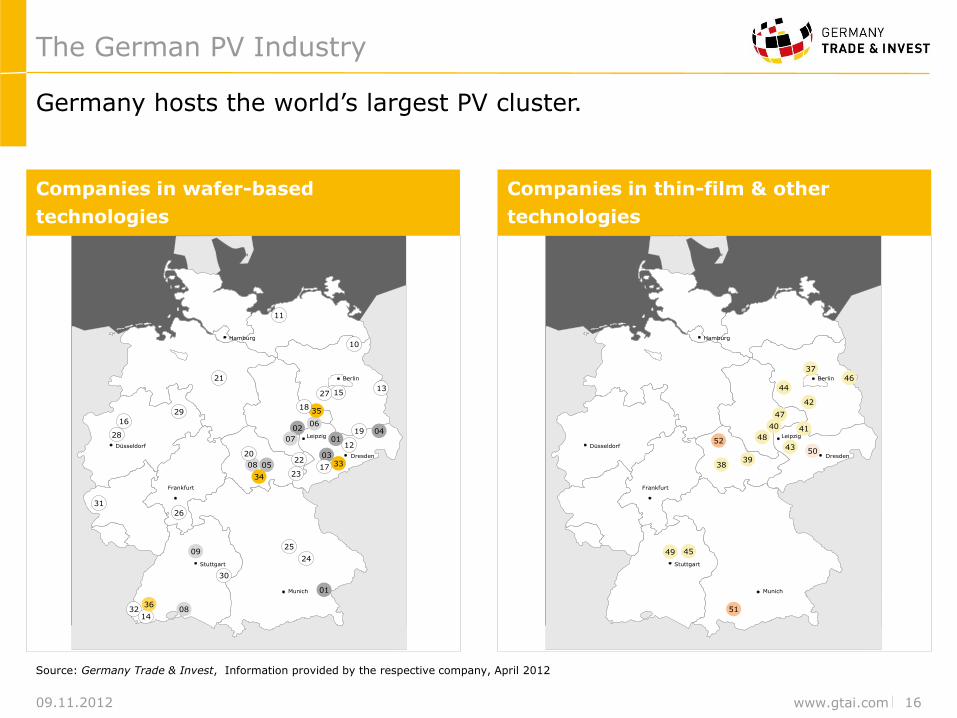

The German PV Industry

Companies in wafer-based

technologies

of renewable energies Prognosis of

yearly installed offshore capacity (in

GW)1)

Germany hosts the world’s largest PV cluster.

Source: Germany Trade & Invest, Information provided by the respective company, April 2012

09.11.2012

Leipzig

Frankfurt

Stuttgart

Munich

Hamburg

Düsseldorf

Berlin

Dresden

Frankfurt

Leipzig0402

01

01

05

09

08

07

06

08

30

35

34

16

32

15

12

11

10

21

20

19

18

22

25

29

26

27

31

28

033317

24

13

14

23

36

Companies in thin-film & other

technologies

Leipzig

Frankfurt

Stuttgart

Munich

Hamburg

Düsseldorf

Berlin

Dresden

Frankfurt

Leipzig

38

37

39

47

46

52

50

51

40

42

41

44

43

45

48

49

16

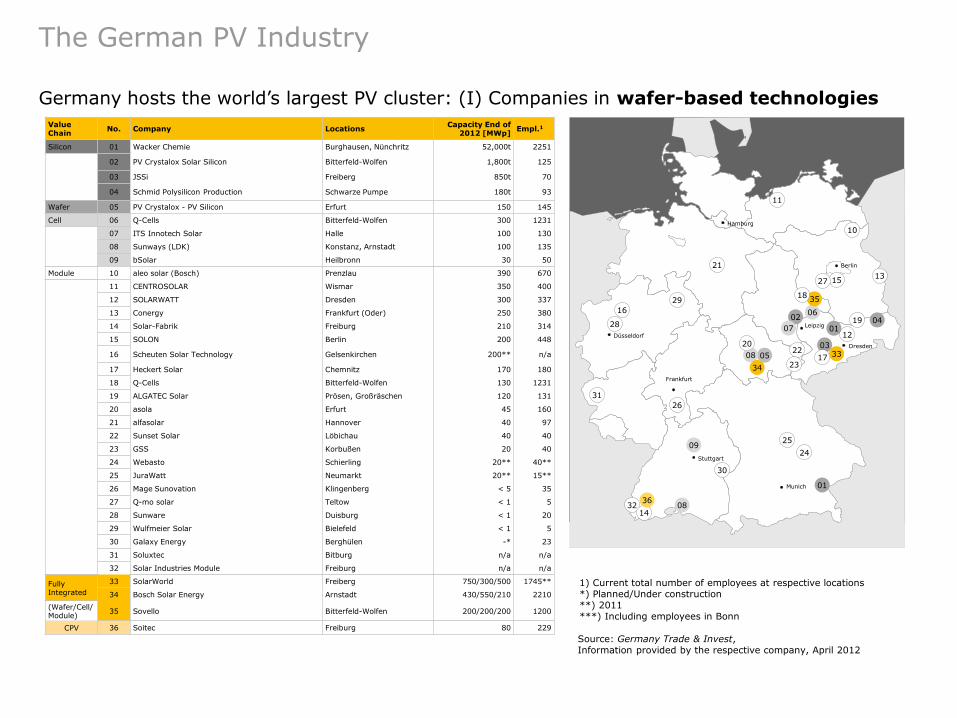

Germany hosts the world’s largest PV cluster: (I) Companies in wafer-based technologies

1) Current total number of employees at respective locations *) Planned/Under construction **) 2011 ***) Including employees in Bonn

The German PV Industry

Source: Germany Trade & Invest, Information provided by the respective company, April 2012

Value Chain

No. Company Locations Capacity End of

2012 [MWp] Empl.1

Silicon 01 Wacker Chemie Burghausen, Nünchritz 52,000t 2251

02 PV Crystalox Solar Silicon Bitterfeld-Wolfen 1,800t 125

03 JSSi Freiberg 850t 70

04 Schmid Polysilicon Production Schwarze Pumpe 180t 93

Wafer 05 PV Crystalox - PV Silicon Erfurt 150 145

Cell 06 Q-Cells Bitterfeld-Wolfen 300 1231

07 ITS Innotech Solar Halle 100 130

08 Sunways (LDK) Konstanz, Arnstadt 100 135

09 bSolar Heilbronn 30 50

Module 10 aleo solar (Bosch) Prenzlau 390 670

11 CENTROSOLAR Wismar 350 400

12 SOLARWATT Dresden 300 337

13 Conergy Frankfurt (Oder) 250 380

14 Solar-Fabrik Freiburg 210 314

15 SOLON Berlin 200 448

16 Scheuten Solar Technology Gelsenkirchen 200** n/a

17 Heckert Solar Chemnitz 170 180

18 Q-Cells Bitterfeld-Wolfen 130 1231

19 ALGATEC Solar Prösen, Großräschen 120 131

20 asola Erfurt 45 160

21 alfasolar Hannover 40 97

22 Sunset Solar Löbichau 40 40

23 GSS Korbußen 20 40

24 Webasto Schierling 20** 40**

25 JuraWatt Neumarkt 20** 15**

26 Mage Sunovation Klingenberg < 5 35

27 Q-mo solar Teltow < 1 5

28 Sunware Duisburg < 1 20

29 Wulfmeier Solar Bielefeld < 1 5

30 Galaxy Energy Berghülen -* 23

31 Soluxtec Bitburg n/a n/a

32 Solar Industries Module Freiburg n/a n/a

Fully Integrated

33 SolarWorld Freiberg 750/300/500 1745**

34 Bosch Solar Energy Arnstadt 430/550/210 2210

(Wafer/Cell/Module)

35 Sovello Bitterfeld-Wolfen 200/200/200 1200

CPV 36 Soitec Freiburg 80 229

Leipzig

Frankfurt

Stuttgart

Munich

Hamburg

Düsseldorf

Berlin

Dresden

Frankfurt

Leipzig0402

01

01

05

09

08

07

06

08

30

35

34

16

32

15

12

11

10

21

20

19

18

22

25

29

26

27

31

28

033317

24

13

14

23

36

Germany hosts the world’s largest PV cluster: (II) Companies in thin-film & other technologies

The German PV Industry

Source: Germany Trade & Invest, Information provided by the respective company, April 2012

1) Current total number of employees at respective locations *) Planned/Under construction **) 2011

Value Chain No. Company Locations Capacity End of 2012

[MWp] Empl.1

Thin Film 37 Inventux Berlin 100 220

a-Si 38 Masdar PV Ichtershausen 80 200

a-Si/μc-Si 39 SCHOTT Solar Thin Film Jena n/a n/a

40 Q-Cells Bitterfeld-Wolfen 135 1231

41 AVANCIS Torgau 120 400

CIS 42 Nanosolar Luckenwalde 115 90

CIGSSe 43 Solarion Leipzig, Zwenkau 20 90

CIGS 44 Bosch Solar CIS Tech Brandenburg 15 150

45 Manz Schwäbisch Hall 6 120

46 First Solar Frankfurt (Oder) 560 n/a

CdTe 47 Calyxo (Q-Cells) Bitterfeld-Wolfen 80 160

48 Second Solar Century Halle -* -*

GaAs 49 Azur Space Solar Power Heilbronn 350 150

OPV 50 heliatek Dresden 2 75

PV & Thermal 51 Solarzentrum Allgäu Altdorf-Biessenhofen 20 80

52 Heli Solar Blankenburg n/a n/a

Leipzig

Frankfurt

Stuttgart

Munich

Hamburg

Düsseldorf

Berlin

Dresden

Frankfurt

Leipzig

38

37

39

47

46

52

50

51

40

42

41

44

43

45

48

49

09.11.2012 | www.gtai.com 19

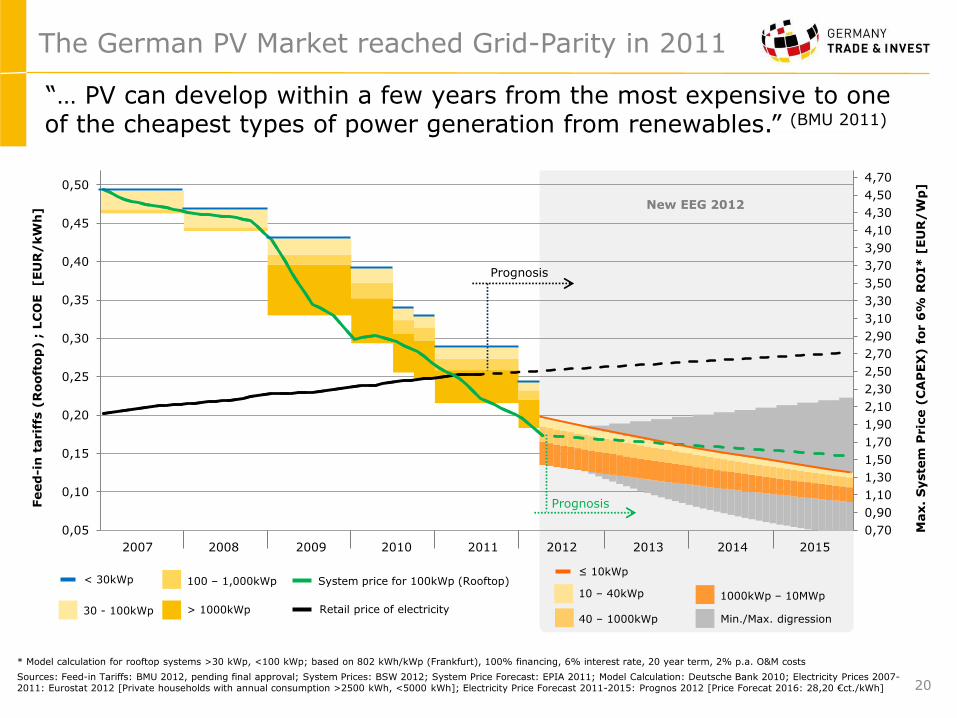

The German PV Market - Grid-Parity in 2011

* Model calculation for rooftop systems >30 kWp, <100 kWp; based on 802 kWh/kWp (Frankfurt), 100% financing, 6% interest rate, 20 year term, 2% p.a. O&M costs

Sources: Feed-in Tariffs: BMU June 2012; System Prices: BSW 2012; System Price Forecast: EPIA 2011; Model Calculation: Deutsche Bank 2010; Electricity Prices 2007-2011: Eurostat 2012 [Private households with annual consumption >2500 kWh, <5000 kWh]; Electricity Price Forecast 2011-2015: Prognos 2012 [Price Forecat 2016: 28,20 €ct./kWh]

“… PV can develop within a few years from the most expensive to one of the cheapest types of power generation from renewables.” (BMU 2011)

EEG Amendement April 2012

09.11.2012 | www.gtai.com 20

The German PV Market reached Grid-Parity in 2011

* Model calculation for rooftop systems >30 kWp, <100 kWp; based on 802 kWh/kWp (Frankfurt), 100% financing, 6% interest rate, 20 year term, 2% p.a. O&M costs

Sources: Feed-in Tariffs: BMU 2012, pending final approval; System Prices: BSW 2012; System Price Forecast: EPIA 2011; Model Calculation: Deutsche Bank 2010; Electricity Prices 2007-2011: Eurostat 2012 [Private households with annual consumption >2500 kWh, <5000 kWh]; Electricity Price Forecast 2011-2015: Prognos 2012 [Price Forecat 2016: 28,20 €ct./kWh]

System price for 100kWp (Rooftop) < 30kWp

> 1000kWp Retail price of electricity

100 – 1,000kWp

30 - 100kWp

Feed

-in

tarif

fs (

Rooft

op

) ;

LC

OE [EU

R/

kW

h]

2007 2008 2009 2010 2011 2012 2013 2014 2015

Max.

Syste

m P

ric

e (

CA

PEX

) f

or 6

% R

OI*

[EU

R/

Wp

]

Min./Max. digression

1000kWp – 10MWp

≤ 10kWp

New EEG 2012

40 – 1000kWp

10 – 40kWp

0,70

0,90

1,10

1,30

1,50

1,70

1,90

2,10

2,30

2,50

2,70

2,90

3,10

3,30

3,50

3,70

3,90

4,10

4,30

4,50

4,70

4,90

0,05

0,10

0,15

0,20

0,25

0,30

0,35

0,40

0,45

0,50

0,55

Prognosis

Prognosis

“… PV can develop within a few years from the most expensive to one of the cheapest types of power generation from renewables.” (BMU 2011)

09.11.2012 | www.gtai.com 21

The Principle of „Own-Consumption“

Wattage

Time of day

0h 3h 6h 9h 12h 15h 18h 21h 24h

Feed-in tariff: 13.50 to 19.50 €ct/kWh1

Energy from grid: Costs ~25 €ct/kWh2

Major income through cost savings on electricity from the grid, Feed-in tariff only for surplus electricity:

PV Energy

Energy Demand

„Own-Consumption“ of PV Energy

(saves ~25 €ct./kWh²)

Notes: 1) Depending on size of system according to feed-in tariff classification | 2) Depending on electricity retail price of respective utility company.

09.11.2012 | www.gtai.com 21

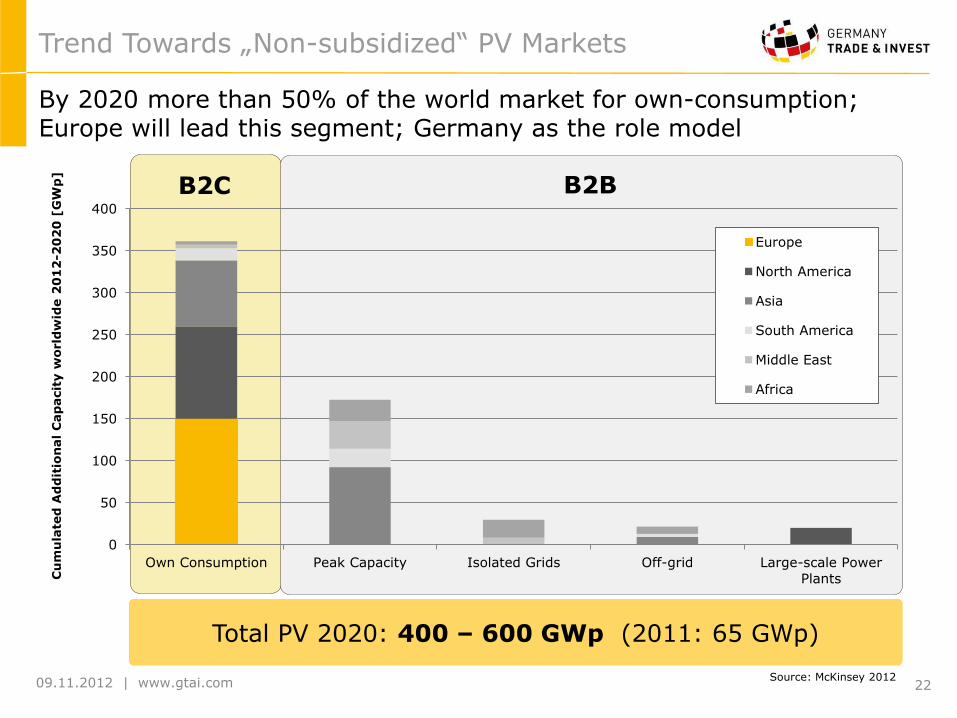

09.11.2012 | www.gtai.com 22

By 2020 more than 50% of the world market for own-consumption; Europe will lead this segment; Germany as the role model

Trend Towards „Non-subsidized“ PV Markets

B2C B2B

Cu

mu

late

d A

dd

itio

nal

Cap

acit

y w

orld

wid

e 2

01

2-2

02

0 [

GW

p]

0

50

100

150

200

250

300

350

400

Own Consumption Peak Capacity Isolated Grids Off-grid Large-scale Power

Plants

Europe

North America

Asia

South America

Middle East

Africa

Source: McKinsey 2012

Total PV 2020: 400 – 600 GWp (2011: 65 GWp)

www.gtai.com

I. Germany´s Energy Transformation

II. Renewable Energies in Germany

Wind

Solar

Biomass

III. Related business fields

Grid expansion, Storage, Smart Metering

Agenda

09.11.2012 23

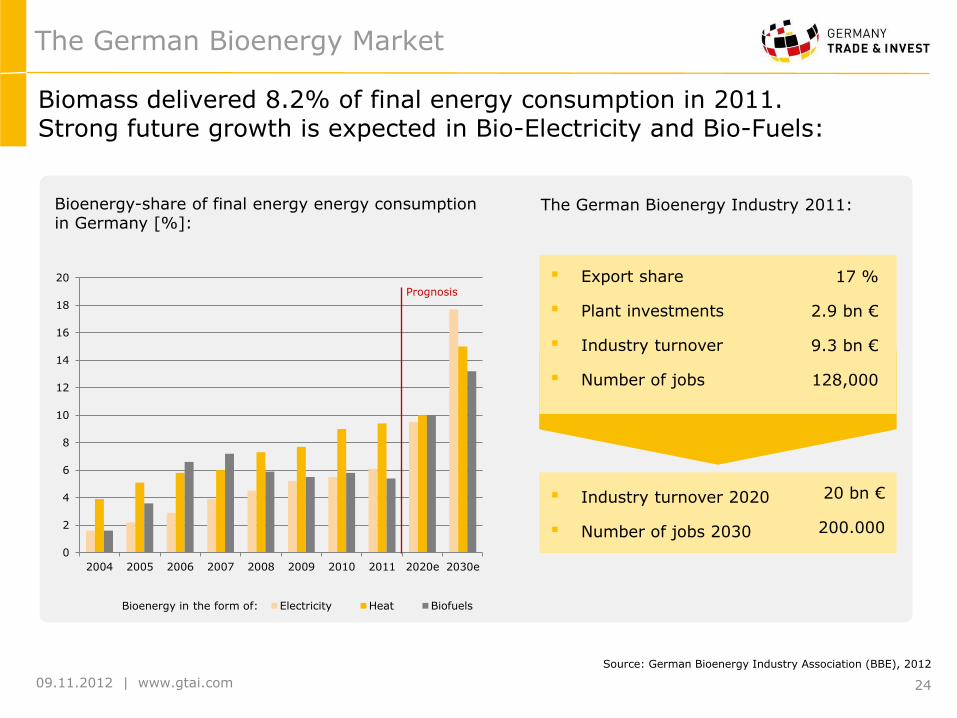

09.11.2012 | www.gtai.com 24

Biomass delivered 8.2% of final energy consumption in 2011. Strong future growth is expected in Bio-Electricity and Bio-Fuels:

Bioenergy-share of final energy energy consumption in Germany [%]:

The German Bioenergy Market

Source: German Bioenergy Industry Association (BBE), 2012

Bioenergy in the form of:

0

2

4

6

8

10

12

14

16

18

20

2004 2005 2006 2007 2008 2009 2010 2011 2020e 2030e

Electricity Heat Biofuels

Prognosis

▪ Export share

▪ Plant investments

▪ Industry turnover

▪ Number of jobs

17 %

2.9 bn €

9.3 bn €

128,000

The German Bioenergy Industry 2011:

▪ Industry turnover 2020

▪ Number of jobs 2030

20 bn €

200.000

09.11.2012 | www.gtai.com 25

0

1000

2000

3000

4000

5000

6000

7000

8000

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Num

ber

of

pla

nts

(centr

al bar)

Insta

lled e

lectr

ical capacity (

Mw

el)

63%

32%

7%

Biogas plant

Biomass combustion plant

Vegetable Oil (heating) power plant

Bioenergies in Germany

Structure of biomass-based electricity supply in Germany in 2010:

Total electricity generation (net) of

biomass 2010: ca. 25,7 TWhel

Source: German Ministry for Environment (BMU), 2012

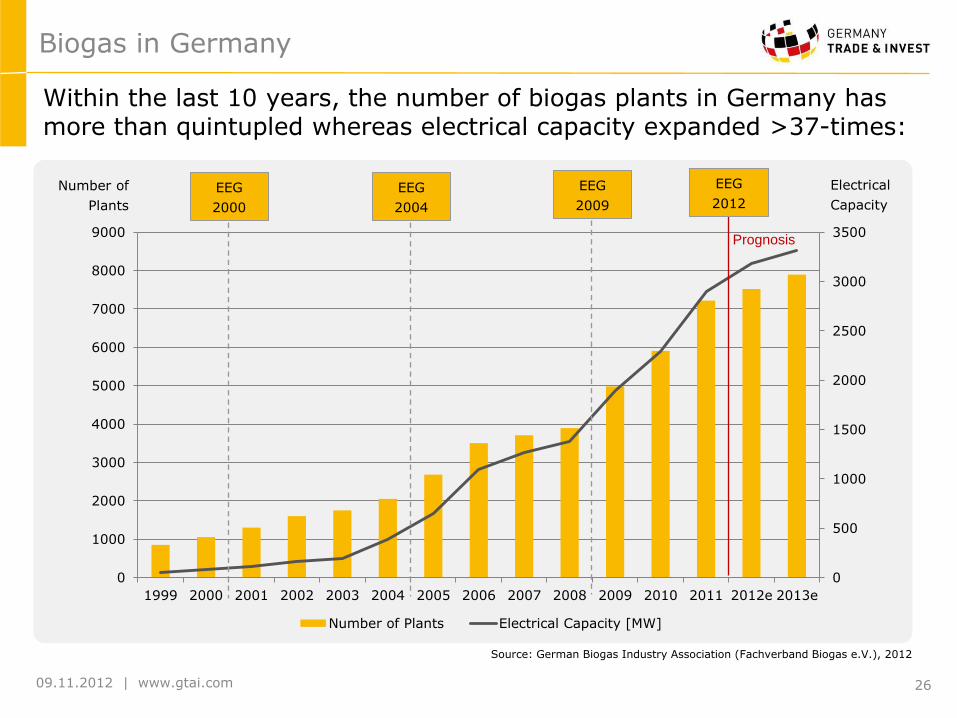

09.11.2012 | www.gtai.com 26

0

500

1000

1500

2000

2500

3000

3500

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012e 2013e

Number of Plants Electrical Capacity [MW]

Source: German Biogas Industry Association (Fachverband Biogas e.V.), 2012

Within the last 10 years, the number of biogas plants in Germany has more than quintupled whereas electrical capacity expanded >37-times:

Prognosis

Number of

Plants

Electrical

Capacity

EEG

2004

EEG

2009

EEG

2012 EEG

2000

Biogas in Germany

09.11.2012 | www.gtai.com 27

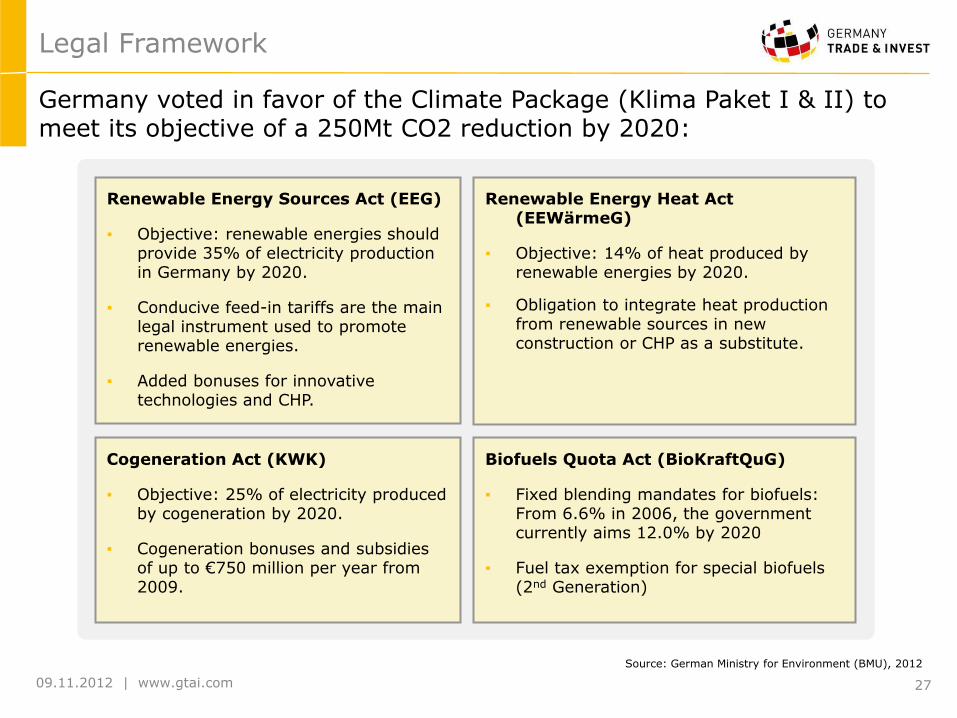

Legal Framework

Germany voted in favor of the Climate Package (Klima Paket I & II) to meet its objective of a 250Mt CO2 reduction by 2020:

Renewable Energy Sources Act (EEG)

▪ Objective: renewable energies should provide 35% of electricity production in Germany by 2020.

▪ Conducive feed-in tariffs are the main legal instrument used to promote renewable energies.

▪ Added bonuses for innovative technologies and CHP.

Renewable Energy Heat Act (EEWärmeG)

▪ Objective: 14% of heat produced by renewable energies by 2020.

▪ Obligation to integrate heat production from renewable sources in new construction or CHP as a substitute.

Cogeneration Act (KWK)

▪ Objective: 25% of electricity produced by cogeneration by 2020.

▪ Cogeneration bonuses and subsidies of up to €750 million per year from 2009.

Biofuels Quota Act (BioKraftQuG)

▪ Fixed blending mandates for biofuels: From 6.6% in 2006, the government currently aims 12.0% by 2020

▪ Fuel tax exemption for special biofuels (2nd Generation)

Source: German Ministry for Environment (BMU), 2012

09.11.2012 | www.gtai.com 28

No. Name Ort

Agro

nom

y

Fore

str

y

Oth

er

bio

m.

resourc

es

Bio

fuels

1G

Bio

fuels

2G

Com

bustion

engin

es

Bio

mass

com

busiton

Bio

gas

Gasific

ation

Bio

mass fuel

cells

CH

P

technolo

gie

s

1 ATZ Entwicklungszentrum Sulzbach-Rosenberg x x x x

2 Fraunhofer UMSICHT Oberhausen x x x x

3 Fraunhofer ICT Pfinztal x

4 Federal Agricultural Research Center (FAL) Braunschweig x x

5 University of Frankfurt - Institut for Molecular Bio Sciences Frankfurt x

6 Leibniz Institut for Agricultural Engineering (ATB) Potsdam x x

7 Technical University Munich - Chair for Biogen Raw Material (TUM) Munich x x x

8 Research Center Karlsruhe Karlsruhe x

9 Institute for Wood Chemistry und Chemical Technology of Wood (BFH) Hamburg x x

10 Institute for Energy and Environment (IE Leipzig) Leipzig x x x x x x x x x

11 CUTEC-Institut GmbH Clausthal-Zellefeld x x

12 Deutsches Biomasse Forschungszentrum (DBFZ) Leipzig x x x x x x x x x

13 Technical University Freiberg Freiberg x x

14 Institute for Farm Management, Food Sciences and Biotechnology Stuttgart x x x

15 Institute of Crop Science (INK) Kassel x x

16 University of Applied Sciences in Eberswalde Eberswalde x x

17 Technologie- und Förderzentrum (TFZ) Straubing x x x x x x

18 RWTH Aachen - Tailor-Made Fuels from Biomass (TMFB) Aachen x x x

19 Öko-Institut Freiburg x x x x x

20 KTBL Darmstadt x x

21 Thüringer Landesanstalt für Landwirtschaft (TLL) Jena x x

22 ISET Hanau x x

23 C.A.R.M.E.N. Straubing x x x x x

24 Forschungs-und Studienzentrum Landwirtschaft und Umwelt (ZLU) Göttingen x

25 ZSW Stuttgart x x x x

26 Fachhochschule Weihenstephan Weihenstephan x

27 FNR Gülzow x x x x x

28 Johann Heinrich von Thünen-Institut für NawaRo (vTI) Braunschweig x x x x x

29 European Institute for Energy Research (EIFER) Karlsruhe x x x x x x

30 Fachhochschule Ingolstadt Ingolstadt x

31 Zentrum für nachwachsende Rohstoffe (ZNR) Bad Sassendorf x x x x x

32 Institut für Getreideverarbeitung GmbH (IGV) Nurthetal x

33 Fachhochschule Südwestfalen Soest x x x

34 Bioenergie Beratung Bornim GmbH Potsdam x x x

35 Kuratorium für Waldarbeit und Forsttechnik e.V. Groß-Umstadt x x

36 Wuppertal Institut Wuppertal x x x

37 Fachhochschule Flensburg - Institute for Chemical Technologies Flensburg x x x

38 Institut für Technikfolgenabschätzung und Systemanalyse (ITAS) Karlsruhe x x x x x x x x

39 Institut für Energie- und Umweltforschung Heidelberg GmbH (IFEU) Heidelberg x x x x

40 Institut für Maschinenmesstechnik und Kolbenmaschinen (IMKO) Magdeburg x x

41 HAWK - Hochschule für angewandte Wissenschaft und Kunst Hildesheim x x x x x

42 Nordwestdeutsche Forstliche Versuchsanstalt Göttingen x x

43 Landwirtschaftliches Technologiezentrum Augustenberg (LTZ) Augustenberg x x x

44 Pilot Pflanzenöltechnologie Magdeburg Magdeburg x

45 Forschungsstelle für Energiewirtschaft (FfE) Munich x

46 Institut für umweltgerechte Landbewirtschaftung (IfUL) Müllheim x x x x

47 Kompetenzzentrum Biomassenutzung Kiel x x x x

48 Fachhochschule Münster Steinfurt x x x

49 Universität Bonn Bonn x

50 Waldzentrum Münster Münster x x x

51 Fachhochschule Köln Köln/Gummersbach x x x x

52 Bundesforschungsantalt für Getreide-, Kartoffel- & Fettforschung Detmold x x x x

53 Brandenburgische Technische Universität Cottbus Cottbus x x x x

54 Hochschule Bremen Bremen x

55 Bremer Energie Institut Bremen x x x x

56 Technologie-Transfer-Zentrum Bremerhaven Bremerhaven x

57 Internationales Holzinstitut Dresden x x

58 Technische Universität Dresden - Institut für Energietechnik Freiberg x x x x x x

59 Institut für Forstwirtschaft Tharadt x

60 Internationales Hochschulinstitut Zittau (IHI) Zittau x x

61 Technische Universität Darmstadt Darmstadt x

62 Fachhochschule Nordhausen Nordhausen x x

63 Justus-Liebig-Universität Giessen Giessen x

64 Fachhochschule Gießen-Friedberg Giessen x

65 Universität Kassel Kassel x x x x

66 Philipps-Universität Marburg Marburg x x

67 Humboldt-Universität Berlin Berlin x x x x x

68 Technische Universität Berlin Berlin x x x x x

69 Leibnitz-Zentrum für Agrarlandforschung (ZALF) Müncheberg x

70 Technische Fachhochschule Wildau Wildau x

71 Institut für ökologische Wirtschaftsforschung (IÖW) Berlin x

72 Technische Universität Kaiserslautern Kaiserslautern x x

73 University of Applied Sciences Bingen (FH-Bingen) Bingen x x x x

74 Institut für Mikrotechnik Mainz GmbH (IMM) Mainz x

75 Fachhochschule Trier - InfAR/IfaS/Fuel Cell Centre Rhineland-Palatinate Trier/Birkenfeld x x x x x x x x x

76 RLP Agroscience GmbH Neustadt a.d.W. x x x

77 Prüf- und Forschungsinstitut Pirmasens e.V , PFI Pirmasens x x x

78 Institut für ZukunftsEnergieSysteme (IZES) Saarbrücken x x x x

…by collaborating with first-class Bioenergy R&D institutes:

The Development of Cutting-edge Technologies

STUTTGART

MUNICH

HANOVER

DÜSSELDORF

BREMEN

BERLIN

DRESDEN

FRANKFURT

1 14 23

22

8

19

5

9

7

2

4

21

11

10

12

3

13

6

15

16

18

20

17

24

25

26

27

28

29 30

31

32

33

35

36

37

38

39

40 34

41

42

43

44

45

46

47

48

49

50

51

52 53

54 55

56

57

58 59

60

61

62

63 64

65

66

67 68 69

70

71

72

73 74 75

76

77 78

www.gtai.com

I. Germany´s Energy Transformation

II. Renewable Energies in Germany

Wind

Solar

Biomass

III. Related Business Fields

Grid Expansion, Storage, Smart Metering

Agenda

09.11.2012 29

09.11.2012 | www.gtai.com

Power balance 2012

New power structure in 2022 will lead to bottle necks in Germany

Offshore- Wind parks

Grid Expansion

Power balance 2022

Source: Netzentwicklungsplan 2012

30

09.11.2012 | www.gtai.com

Grid Expansion

Expansion requirements for the transmission and distribution grid

Grid expansion of 3,800km (2100km DC, 1700 AC) is required by 2020.

Baseline scenario with overhead lines requires:

20 bn. €

The connection of the offshore-grid is estimated to

10-12 bn. €

Transmission grid

By 2030, the expansion of the distribution grid requires investments of

€ 25 bn

Distribution grid

31

Sources: VKU, 2012; Netzentwicklungsplan 2012

09.11.2012 | www.gtai.com

State of the art 2040

PV - Own consumption 0.4% of the overall generated PV power is used for own consumption

2025: 20% of PV generated power for own consumption (35% in 2040).

Control reserve Required control reserve of ~14-17 GW

In 2025 the demand for control reserve increases by 50% to 2010 and by 70% in 2040.

Surplus energy Storage demand for a surplus of 150 GWh (2010)

Storage necessity 2025-2030: 3.5-8 TWh 2040-2050: 40 TWh

Potential for Energy Storage in Germany

Sources: DB Research 2012, BCG 2011, DENA Netzstudie II 2011, BAFA, Bundesnetzagentur, BMU Leitstudie 2011

32

Expected: Investment of € 25 - 30 billion in storage capacity until 2030

09.11.2012 | www.gtai.com

Intelligent Grids and Metering - EnWG

In 2011, the German Federal Law on the Energy Industry (EnWG) was

supplemented by specifications for metering elements e.g. smart meters,

smart meter installations and requirements (§ 21b, § 21d, § 21e, § 21 f, §

21i)

Smart meters are obligatory for: new constructions and complete

refurbishments, consumer loads of over 6000 kWh/Year and plant

operators under the renewable energy act (EEG) and in accordance with the

cogeneration act (KWKG) of over 7 KW (§ 21c para. 1 and 2 EnWG)

-> this would require the change of 3,5 million meters (Germany total: 43

million meters)

Smart meter legal amendment and roll-out in Germany

33

09.11.2012 | www.gtai.com

Source: Own draft according to Frost & Sullivan 2011

Expected Smart Meter Roll-Out in Germany

The market is expected to grow substantially with overall CAGR of 71.7% from 2010-

2017

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Revenues (€ Mio.) 1 3 12 17 23 33 162 409 499 721 731

Units 0,01 0,02 0,1 0,14 0,2 0,3 1,5 4 5,2 8,2 9

0

1

2

3

4

5

6

7

8

9

10

0

100

200

300

400

500

600

700

800

Un

its (

millio

n)

Reven

ue (

€ m

illio

n)

Revenues (€ Mio.)

Units

Smart meter market: unit and revenue forecast Germany

34

09.11.2012 | www.gtai.com

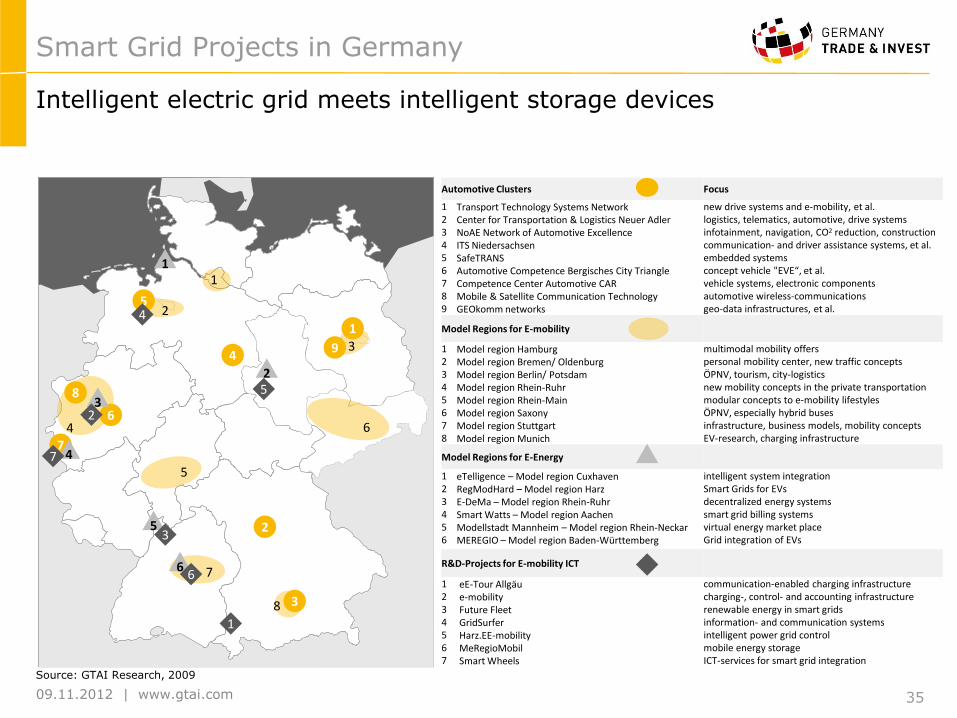

Automotive Clusters Focus

1 Transport Technology Systems Network new drive systems and e-mobility, et al. 2 Center for Transportation & Logistics Neuer Adler logistics, telematics, automotive, drive systems 3 NoAE Network of Automotive Excellence infotainment, navigation, CO2 reduction, construction 4 ITS Niedersachsen communication- and driver assistance systems, et al. 5 SafeTRANS embedded systems 6 Automotive Competence Bergisches City Triangle concept vehicle "EVE“, et al. 7 Competence Center Automotive CAR vehicle systems, electronic components 8 Mobile & Satellite Communication Technology automotive wireless-communications 9 GEOkomm networks geo-data infrastructures, et al.

Model Regions for E-mobility

1 Model region Hamburg multimodal mobility offers 2 Model region Bremen/ Oldenburg personal mobility center, new traffic concepts 3 Model region Berlin/ Potsdam ÖPNV, tourism, city-logistics 4 Model region Rhein-Ruhr new mobility concepts in the private transportation 5 Model region Rhein-Main modular concepts to e-mobility lifestyles 6 Model region Saxony ÖPNV, especially hybrid buses 7 Model region Stuttgart infrastructure, business models, mobility concepts 8 Model region Munich EV-research, charging infrastructure

Model Regions for E-Energy

1 eTelligence – Model region Cuxhaven intelligent system integration 2 RegModHard – Model region Harz Smart Grids for EVs 3 E-DeMa – Model region Rhein-Ruhr decentralized energy systems 4 Smart Watts – Model region Aachen smart grid billing systems 5 Modellstadt Mannheim – Model region Rhein-Neckar virtual energy market place 6 MEREGIO – Model region Baden-Württemberg Grid integration of EVs

R&D-Projects for E-mobility ICT

1 eE-Tour Allgäu communication-enabled charging infrastructure 2 e-mobility charging-, control- and accounting infrastructure 3 Future Fleet renewable energy in smart grids 4 GridSurfer information- and communication systems 5 Harz.EE-mobility intelligent power grid control 6 MeRegioMobil mobile energy storage 7 Smart Wheels ICT-services for smart grid integration

2

3

4

5

6

7

9

3

4

5

2

6

1

6

3

2

1

3

1

4

5

7

2

8

6

8

1 4

5

7

Intelligent electric grid meets intelligent storage devices

Smart Grid Projects in Germany

Source: GTAI Research, 2009

35

www.gtai.com

Mumbai Office Tokyo Office

Berlin - Headquarters

Mr. Tobias Homann Senior Manager Photovoltaics T. +49 30 200 099-391 [email protected]

Mr. Thomas Grigoleit Director Renewable Energies & Resources T. +49 30 200 099-224 [email protected]

Mr. Tobias Rothacher Senior Manager Photovoltaics and Bioenergy T. +49 30 200 099-225 [email protected]

Contact Data – GTAI Investment Consulting

Mr. Markus Hempel China Representative Beijing, China T. +86 10 6539 6725 F. +86 10 6590 6167 [email protected]

North America

Europe

Asia-Pacific

© 2012 Germany Trade & Invest All information provided by Germany Trade & Invest has been put together with the utmost care. However, we assume no liability for the accuracy of the information provided.

Mr. Iwami Asakawa Japan Representative Tokyo, Japan T. +81 3 5275 2072 F. +81 3 5275 2012 [email protected]

Mr. Claus Habermeier Director New York, USA T: +1 212 584 9715 F: +1 212 262 6449 [email protected]

Ms. Angelika Geiger Director San Francisco, USA T: +1 415 248 1246 F: +1 415 627 9169 [email protected]

Ms. Flérida Regueira Cortizo Senior Manager Environmental Technologies T. +49 30 200 099-230 [email protected]

Ms. Asha-Maria Sharma India Representative Mumbai, India T. +91 22 66 65 21 80 [email protected]

New York Office San Francisco Office

Beijing Office

Renewable Energy and Resources Division:

Mr. Heiko Staubitz Senior Manager Energy Storage / Smart Grid T. +49 30 200 099-226 [email protected]

Mr. Jonas Rabe Manager Wind T. +49 30 200 099-228 [email protected]

Ms. Esther Frey Manager Wind T. +49 30 200 099-253 [email protected]

36 09.11.2012

Ms. Anne Bräutigam Manager Wind T. +49 30 200 099-228 [email protected]