remarketing - not a new issue (see “ratings” herein) book … · 2018-07-24 · remarketing -...

TRANSCRIPT

REMARKETING - NOT A NEW ISSUE (See “Ratings” herein) BOOK-ENTRY ONLY

SECOND SUPPLEMENT TO OFFICIAL STATEMENT DATED MAY 31, 2012 SUPPLEMENTING THE OFFICIAL STATEMENT DATED OCTOBER 7, 2004

AS PREVIOUSLY SUPPLEMENTED BY THE FIRST SUPPLEMENT TO OFFICIAL STATEMENT DATED OCTOBER 19, 2004

On October 19, 2004, Dilworth Paxson LLP and Jettie D. Newkirk Law Offices, Co-Bond Counsel, delivered an opinion, that under existing statutes, regulations, rulings and court decisions, interest on the Fifth Series A-2 Bonds will not be includible in gross income of the holders thereof for federal income tax purposes and will not be a specific preference item for purposes of computing the federal alternative minimum tax imposed on individuals and corporations, however, interest on the Fifth Series A-2 Bonds is taken into account in determining adjusted current earnings for the purpose of computing the Federal alternative minimum tax imposed on corporations (other than an S Corporation, regulated investment company, real estate investment trust or real estate mortgage investment conduit) and that interest on the Fifth Series A-2 Bonds is included in effectively connected earnings and profits for purposes of computing the branch profits tax on certain foreign corporations doing business in the United States and interest on the Fifth Series A-2 Bonds may be subject to federal income taxation under Section 1375 of the Code for S corporations which have subchapter C earnings and profits at the close of the taxable year if more than 25% of the gross receipts of such S corporation is passive investment income. In connection with the initial remarketing of the Fifth Series A-2 Bonds as a result of the replacement of the letter of credit applicable to the Fifth Series A-2 Bonds, as described in this Second Supplement to Official Statement, Blank Rome LLP, as Bond Counsel, will deliver an opinion to the effect that the replacement of the letter of credit applicable to the Fifth Series A-2 Bonds does not, in and of itself, adversely affect the exclusion of interest on the Fifth Series A-2 Bonds from gross income of the owners thereof for federal income tax purposes.

$30,000,000 CITY OF PHILADELPHIA, PENNSYLVANIA

GAS WORKS VARIABLE RATE DEMAND REVENUE BONDS, FIFTH SERIES A-2

(1998 GENERAL ORDINANCE)

Dated: October 19, 2004 Due: September 1, 2034

INTRODUCTION

This Second Supplement to Official Statement, dated May 31, 2012 (this “Second Supplement”) supplements and amends certain information contained in the Official Statement, dated October 7, 2004 (the “Original Official Statement”), as previously supplemented by the First Supplement to Official Statement, dated October 19, 2004 (the “First Supplement”), as such Original Official Statement and First Supplement relate to the $30,000,000 City of Philadelphia, Pennsylvania, Gas Works Variable Rate Demand Revenue Bonds, Fifth Series A-2 (1998 General Ordinance) (the “Fifth Series A-2 Bonds”). The Fifth Series A-2 Bonds were originally issued on October 19, 2004 in the original principal amount of $30,000,000, the entire original principal amount of which is currently outstanding.

The Fifth Series A-2 Bonds were issued pursuant to the First Class City Revenue Bond Act of the Commonwealth of Pennsylvania, Act No. 234, approved October 18, 1972, P.L. 955 (the “Act”), the

2

General Gas Works Revenue Bond Ordinance of 1998, approved on May 30, 1998, Bill No. 980232, as amended and supplemented from time to time (the “1998 General Ordinance”), the Sixth Supplemental Ordinance to the 1998 General Ordinance approved July 1, 2004, Bill No. 040599 (the “Sixth Supplemental Ordinance”), and a determination of the Bond Committee of the City (consisting of the Mayor, the City Controller and the City Solicitor, and acting by at least a majority thereof), dated October 19, 2004 (the “Bond Authorization”).

This Second Supplement presents certain information concerning the replacement of the irrevocable direct pay letter of credit that enhances the Fifth Series A-2 Bonds, as described herein, and should be read together with the Original Official Statement and the First Supplement (copies of which are attached hereto as Appendix A and incorporated herein by reference). To the extent that the information in this Second Supplement, including information incorporated by reference herein, conflicts with the information in the Official Statement, as supplemented by the First Supplement, the information in (and incorporated in) this Second Supplement shall govern. Unless otherwise defined in this Second Supplement, all terms used herein shall have the same meanings as in the Original Official Statement.

In accordance with the requirements of the Bond Authorization, and as a result of the replacement of the letter of credit applicable to the Fifth Series A-2 Bonds (as hereinafter described), the Fifth Series A-2 Bonds are subject to and have been called for mandatory tender for purchase on June 6, 2012 (the “Mandatory Purchase Date”). The Fifth Series A-2 Bonds will be remarketed on the Mandatory Purchase Date by J.P. Morgan Securities LLC, as remarketing agent for the Fifth Series A-2 Bonds (the “Remarketing Agent”). The Fifth Series A-2 Bonds currently are in the Weekly Mode and bear interest at the Weekly Rate as determined by the Remarketing Agent, and will remain in the Weekly Mode and bear interest at the Weekly Rate on and after the Mandatory Purchase Date. See “REMARKETING” herein.

J.P. Morgan as Remarketing Agent

JPMorgan Chase Bank, National Association (the “Credit Provider”) will issue an irrevocable, direct-pay letter of credit (the “Letter of Credit”) with respect to the Fifth Series A-2 Bonds on the Mandatory Purchase Date, which will entitle the Trustee to draw up to an amount equal to the principal of and up to fifty (50) days’ accrued interest at a maximum rate of 10% to be used to pay the principal or redemption price of and interest on the Fifth Series A-2 Bonds or the purchase price of the Fifth Series A-2 Bonds based on a 365 day year. The Letter of Credit will expire on December 31, 2014 unless terminated earlier or extended as described herein. See “SUMMARY OF CERTAIN PROVISIONS OF THE LETTER OF CREDIT AND THE REIMBURSEMENT AGREEMENT” herein.

THE INFORMATION CONTAINED IN THIS SECOND SUPPLEMENT IS SUBJECT TO MORE COMPLETE INFORMATION CONTAINED IN THE ORIGINAL OFFICIAL STATEMENT, AS SUPPLEMENTED BY THE FIRST SUPPLEMENT. THIS SECOND SUPPLEMENT IS REQUIRED TO BE PHYSICALLY AFFIXED TO, AND IS TO BE READ ONLY IN CONJUNCTION WITH, THE ORIGINAL OFFICIAL STATEMENT, AS SUPPLEMENTED BY THE FIRST SUPPLEMENT. THIS SECOND SUPPLEMENT SHOULD NOT BE SEPARATED FROM THE ORIGINAL OFFICIAL STATEMENT, AS SUPPLEMENTED BY THE FIRST SUPPLEMENT, AND NEITHER THIS SECOND SUPPLEMENT NOR THE ORIGINAL OFFICIAL STATEMENT, AS SUPPLEMENTED BY THE FIRST SUPPLEMENT, MAY BE RELIED UPON IN ANY WAY INDEPENDENT OF EACH OTHER.

THE FINANCIAL AND OTHER INFORMATION WITH RESPECT TO PGW CONTAINED IN THE ORIGINAL OFFICIAL STATEMENT SHOULD NOT BE RELIED

3

UPON. PGW’S MOST RECENT BASIC FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION REPORT (WITH INDEPENDENT AUDITOR’S REPORT THERON) ARE AVAILABLE FOR REVIEW BY INVESTORS AND ARE FILED ANNUALLY BY THE CITY WITH THE MSRB VIA THE ELECTRONIC MUNICIPAL MARKET ACCESS SYSTEM (“EMMA”) AT http://emma.msrb.org AND ARE INCLUDED AS CONTINUING DISCLOSURE FOR THE FIFTH SERIES A-2 BONDS.

THE INDEPENDENT ENGINEERING CONSULTANT’S REPORT WITH RESPECT TO PGW CONTAINED IN THE ORIGINAL OFFICIAL STATEMENT SHOULD NOT BE RELIED UPON. FOR MORE RECENT INFORMATION RELATING TO PGW, INVESTORS SHOULD VIEW THE INDEPENDENT ENGINEERING CONSULTANT’S REPORT DATED JUNE 15, 2011 CONTAINED IN “APPENDIX B - INDEPENDENT CONSULTANT’S REPORT” OF THE OFFICIAL STATEMENT RELATING TO THE MOST RECENTLY CLOSED CITY OF PHILADELPHIA GAS WORKS REVENUE BOND ISSUE WHICH WAS FILED WITH THE MSRB VIA EMMA (http://emma.msrb.org).

THE FINANCIAL AND OTHER INFORMATION WITH RESPECT TO THE CITY OF PHILADELPHIA CONTAINED IN THE ORIGINAL OFFICIAL STATEMENT SHOULD NOT BE RELIED UPON. FOR MORE RECENT FINANCIAL AND OTHER INFORMATION WITH RESPECT TO THE CITY OF PHILADELPHIA, INVESTORS SHOULD VIEW THE APPENDICES TITLED “GOVERNMENET AND FINANCIAL INFORMATION” AND “CITY SOCIOECONOMIC INFORMATION”, RESPECTIVELY, CONTAINED IN THE OFFICIAL STATEMENT RELATING TO THE $21,295,000, CITY OF PHILADELPHIA, PENNSYLVANIA, GENERAL OBLIGATION REFUNDING BONDS, SERIES 2012A WHICH WAS FILED WITH THE MSRB VIA EMMA (http://emma.msrb.org).

The Remarketing Agent has provided the following sentence for inclusion in this Second Supplement. The Remarketing Agent has reviewed the information in this Second Supplement in accordance with, and as part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Remarketing Agent does not guarantee the accuracy or completeness of such information.

The Original Official Statement, as supplemented by the First Supplement and this Second

Supplement, in general describes the Fifth Series A-2 Bonds only during the period that such Fifth Series A-2 Bonds bear interest at the Weekly Rate. If the Fifth Series A-2 Bonds are converted from a Weekly Mode to another Mode, information regarding the new Mode will be provided to prospective purchasers.

REPLACEMENT OF LETTER OF CREDIT APPLICABLE TO FIFTH SERIES A-2 BONDS

On October 19, 2004, JPMorgan Chase Bank, N.A. and The Bank of Nova Scotia, acting through its New York Agency (together, the “Original Credit Provider”) issued an irrevocable, direct-pay letter of credit with respect to the Fifth Series A-2 Bonds (the “Initial Letter of Credit”) as a several, but not joint, obligation, pursuant to a Letter of Credit and Reimbursement Agreement dated as of October 19, 2004 among the City, JPMorgan Chase Bank, N.A. and The Bank of Nova Scotia, acting through its New York Agency (the “Initial Reimbursement Agreement”). The Initial Letter of Credit was previously extended on two occasions and will expire on October 19, 2012 (the “Expiration Date”). JPMorgan Chase Bank, National Association and the Bank of Nova Scotia, acting through its New York Agency, have agreed to terminate the Initial Letter of Credit prior to the Expiration Date and JPMorgan Chase Bank, National Association has agreed to issue a new direct pay letter of credit (the “Letter of Credit”) for the benefit of

4

the Fifth Series A-2 Bonds pursuant to a Letter of Credit and Reimbursement Agreement, dated as of June 1, 2012, by and between the City and JPMorgan Chase Bank, National Association (the “Reimbursement Agreement”). The Replacement of the Initial Letter of Credit with the Letter of Credit, the execution and delivery of the Reimbursement Agreement and the remarketing of the Fifth Series A-2 Bonds are authorized pursuant to the Act, the 1998 General Ordinance, the Sixth Supplemental Ordinance, the Bond Authorization and a Resolution of the Bond Committee of the City (consisting of the Mayor, the City Controller and the City Solicitor, and acting by at least a majority thereof), dated June 6, 2012.

The Letter of Credit provides that, while the Fifth Series A-2 Bonds are in the Weekly Mode, the outstanding principal of and up to fifty (50) days’ interest on Fifth Series A-2 Bonds calculated on the basis of a year 365 or 366 days, as applicable, for the number of days actually elapsed, when and as the same shall be due and payable, and payment of the purchase price of the Fifth Series A-2 Bonds tendered for purchase, as described herein and in the Original Official Statement, will be paid by the Fiscal Agent using funds drawn under the Letter of Credit. The Letter of Credit is subject to certain terms and conditions as described herein and in the Reimbursement Agreement. See “SUMMARY OF CERTAIN PROVISIONS OF THE LETTER OF CREDIT AND THE REIMBURSEMENT AGREEMENT” herein.

THE CREDIT PROVIDER

The information under this heading has been provided solely by the JPMorgan Chase Bank, National Association. This information has not been verified independently by the City. The City makes no representation whatsoever as to the accuracy, adequacy or completeness of such information.

JPMorgan Chase Bank, National Association (the “Credit Provider”) is a wholly owned subsidiary of JPMorgan Chase & Co., a Delaware corporation whose principal office is located in New York, New York. The Credit Provider offers a wide range of banking services to its customers, both domestically and internationally. It is chartered and its business is subject to examination and regulation by the Office of the Comptroller of the Currency.

As of March 31, 2012, JPMorgan Chase Bank, National Association, had total assets of $1,842.7 billion, total net loans of $584.6 billion, total deposits of $1,188.5 billion, and total stockholder’s equity of $134.3 billion. These figures are extracted from the Credit Provider’s unaudited Consolidated Reports of Condition and Income (the “Call Report”) as of March 31, 2012, prepared in accordance with regulatory instructions that do not in all cases follow U.S. generally accepted accounting principles. The Call Report including any update to the above quarterly figures is filed with the Federal Deposit Insurance Corporation and can be found at www.fdic.gov.

Additional information, including the most recent annual report on Form 10-K for the year ended December 31, 2011, of JPMorgan Chase & Co., the 2011 Annual Report of JPMorgan Chase & Co., and additional annual, quarterly and current reports filed with or furnished to the Securities and Exchange Commission (the “SEC”) by JPMorgan Chase & Co., as they become available, may be obtained without charge by each person to whom this Official Statement is delivered upon the written request of any such person to the Office of the Secretary, JPMorgan Chase & Co., 270 Park Avenue, New York, New York 10017 or at the SEC’s website at www.sec.gov.

The information contained under this caption “THE CREDIT PROVIDER” relates to and has been obtained from the Bank. The delivery of this Second Supplement shall not create any implication that there has been no change in the affairs of the Bank since the date hereof, or that the information

5

contained or referred to under this caption “THE CREDIT PROVIDER” is correct as of any time subsequent to its date.

SUMMARY OF CERTAIN PROVISIONS OF THE LETTER OF CREDIT AND THE REIMBURSEMENT AGREEMENT

The Letter of Credit

The following is a summary of certain provisions of the Letter of Credit. This summary does not purport to be comprehensive or definitive, and is subject to all of the terms and provisions of the Letter of Credit to which reference is hereby made. Wherever defined terms in the Letter of Credit are referred to, such defined terms are incorporated herein by reference as a part of the statement made, and the statement is qualified in its entirety by such reference. Capitalized terms used under this heading “SUMMARY OF CERTAIN PROVISIONS OF THE LETTER OF CREDIT AND THE REIMBURSEMENT AGREEMENT” but not defined shall have the meaning assigned to such term in the Reimbursement Agreement or Letter of Credit, as applicable. The Initial Letter of Credit will be an irrevocable transferable direct pay obligation of the Credit Provider to pay to the Fiscal Agent for the Fifth Series A-2 Bonds, upon request and in accordance with the terms thereof, an aggregate amount not exceeding $30,410,959 (as reduced and reinstated from time to time as provided therein), of which (a) an amount not exceeding $30,000,000 may be drawn upon by the Fiscal Agent with respect to payment of the principal amount of the Fifth Series A-2 Bonds, whether at maturity or upon redemption, or the principal portion of the purchase price of Fifth Series A-2 Bonds tendered or deemed tendered under the Fifth Series A-2 Bond Authorization and (b) an amount not exceeding $410,959 may be drawn upon by the Fiscal Agent with respect to the payment of interest on the Fifth Series A-2 Bonds, or the interest portion of the purchase price of Fifth Series A-2 Bonds so tendered for purchase, representing interest for a period of fifty (50) days at a rate of 10.0% per annum, as calculated on the basis of a year of 365 days. Multiple drawings may be made under the Letter of Credit, provided, that each drawing made for payment of principal of the Fifth Series A-2 Bonds (other than any Bank Bonds or Ineligible Bonds) at maturity or redemption (an “A Drawing”) and each drawing made for the payment of the portion of the purchase price on Fifth Series A-2 Bonds (other than any Bank Bonds or Ineligible Bonds) tendered equal to the principal amount thereof (a “C Drawing”) honored by the Credit Provider thereunder shall pro tanto reduce the amount available under the Letter of Credit for such Drawings and provided, further, that, each drawing made for the payment of interest on the Fifth Series A-2 Bonds (other than any Bank Bonds or Ineligible Bonds) on an interest payment date, at maturity or redemption (a “B Drawing”) and each drawing made for the payment of the portion of the purchase price on Fifth Series A-2 Bonds (other than any Bank Bonds or Ineligible Bonds) tendered equal to the amount of accrued and unpaid interest on such Fifth Series A-2 Bonds to the date of such purchase (a “D Drawing”) honored by the Bank thereunder shall pro tanto reduce the amount available under the Letter of Credit for such Drawings. Payments made in respect of any drawing (whether or not complying with the terms of the Letter of Credit) shall so reduce by the amount of such payment the amounts which the Fiscal Agent may draw under the Letter of Credit notwithstanding any acts or omissions, whether authorized or unauthorized, of the Fiscal Agent or any officer, director, employee or agent of the Fiscal Agent in connection with any drawing under the Letter of Credit of the proceeds of the Letter of Credit or otherwise in connection with the Letter of Credit. In addition, prior to the Conversion Date, in the event of the remarketing of the Fifth Series A-2 Bonds (or portions thereof) previously purchased with the proceeds of a C Drawing and D Drawing, the Credit Provider’s obligation to honor drawings under the Letter of Credit shall be automatically reinstated concurrently upon receipt by the Credit Provider, or the Fiscal Agent on the Credit Provider’s behalf, of

6

an amount equal to the Original Purchase Price of such Fifth Series A-2 Bonds (or portion thereof) plus accrued interest thereon as required under the Reimbursement Agreement as specified in a certain certificate; the amount of such reinstatement shall be equal to the Original Purchase Price of such Fifth Series A-2 Bonds (or portion thereof). If the Fiscal Agent shall draw on the Letter of Credit by presentation of a B Drawing to the Credit Provider without regard to an A Drawing and shall not have received, at or prior to 11:00 a.m., New York City time, on the tenth (10th) calendar day from the date of the Credit Provider honoring such drawing, a notice from the Credit Provider stating an Event of Default has occurred under the Reimbursement Agreement, an amount equal to the payment of a B Drawing shall be automatically and immediately reinstated, effective on the eleventh (11th) day from the date of such drawing, subject to any further subsequent reductions in the Stated Amount of the Letter of Credit pursuant to the terms thereof. The Letter of Credit will terminate upon the earliest of (i) December 31, 2014 (such date as extended from time to time, the “Expiration Date”); (ii) the fifth (5th) Business Day following the first date on which all of the “Bonds outstanding” have been converted to bear interest at a rate other than the Weekly Mode (“Non-Covered Rate Bonds”) as certified by the Fiscal Agent; (iii) upon our receipt from the Fiscal Agent of a fully executed certificate stating that (i) no Fifth Series A-2 Bonds (other than Non-Covered Rate Bonds) remain outstanding within the meaning of the Bond Authorization or (ii) a substitute or replacement letter of credit or alternate credit facility has been issued to replace the Letter of Credit in accordance with the Reimbursement Agreement and the Bond Authorization or (iii) all drawings required to be made under the Bond Authorization and available under the Letter of Credit have been made and honored; or (iv) the fifteenth (15th) day after the Fiscal Agent’s receipt of written notice from the Credit Provider that an Event of Default under the terms of the Letter of Credit and under the terms of the Reimbursement Agreement has occurred (the earliest of the dates set forth in clauses (ii), (iii) and (iv) above being referred to herein as the “Stated Termination Date”). The Reimbursement Agreement The following is a summary of certain provisions of the Reimbursement Agreement. This summary does not purport to be comprehensive or definitive, and is subject to all of the terms and provisions of the Reimbursement Agreement, to which reference is hereby made. Wherever defined terms in the Reimbursement Agreement are referred to, such defined terms are incorporated herein by reference as a part of the statement made, and the statement is qualified in its entirety by such reference. Reimbursement Obligation The City intends to enter into the Reimbursement Agreement, which provides for the issuance of the Letter of Credit. A draw under the Letter of Credit creates a reimbursement obligation on the part of the City in favor of the Credit Provider. The City’s payment obligations under the Reimbursement Agreement are limited to those amounts payable from Gas Works Revenues pledged for the benefit of Senior 1998 Ordinance Bonds. Events of Default Each of the following events, acts or occurrences shall constitute an Event of Default under the Reimbursement Agreement: (a) The City shall fail to pay (a) the principal amount of any A Drawing or B Drawing when due, (b) any interest on any A Drawing or B Drawing when due, (c) any amount due with respect to any

7

Bank Bond, or (d) any fees or other amounts owing under the Reimbursement Agreement within five (5) Business Days after the same shall be due and payable. (b) The City shall default in the payment when due (subject to any applicable notice or grace period), whether at stated maturity or otherwise, of any principal of or interest on (howsoever designated) any indebtedness for borrowed money payable from Revenues in excess of $500,000, whether such indebtedness now exists or shall hereafter be created. (c) An event of default as defined in any mortgage, indenture, instrument or resolution under which there may be issued, or by which there may be secured or evidenced, any indebtedness for money borrowed of, or guaranteed by, the City and payable from Revenues in excess of $500,000, whether such indebtedness now exists or shall hereafter be created, shall occur and shall result in the indebtedness becoming due and payable prior to the stated maturity or due date thereof. (d) Any event shall occur which shall permit such indebtedness described in (a) or (b) above in excess of $500,000 to be so declared due and payable prior to its stated maturity or due date and such event shall continue unremedied past any period of grace provided for in any mortgage, indenture, instrument or resolution under which such indebtedness is issued. (e) Any representation or warranty made by the City in the Reimbursement Agreement or in any other Document or in any certificate, letter or other writing or instrument furnished or delivered by the City to the Credit Provider pursuant thereto or in connection with the Reimbursement Agreement or therewith shall prove to have been untrue or incorrect in any material respect when made or when reaffirmed, as the case may be. (f) (i) The City or PGW shall commence any case, proceeding or other action (A) under any existing or future law of any jurisdiction relating to bankruptcy, insolvency, reorganization or relief of debtors, seeking to have an order for relief entered with respect to it or seeking to adjudicate it insolvent or a bankrupt or seeking reorganization, arrangement, adjustment, winding-up, liquidation, dissolution, composition or other relief with respect to it or its debts, or (B) seeking appointment of a receiver, trustee, custodian or other similar official for itself or for any substantial part of its property, or the City shall make a general assignment for the benefit of its creditors, or (ii) there shall be commenced against the City or PGW any case, proceeding or other action of a nature referred to in clause (i) and the same shall remain undismissed for a period of 30 days, or (iii) there shall be commenced against the City or PGW any case, proceeding or other action seeking issuance of a warrant of attachment, execution, distraint or similar process against all or any substantial part of its property which results in the entry of an order for any such relief which shall not have been vacated, discharged, or stayed or bonded pending appeal, within 30 days from the entry thereof, or (iv) the City shall take action in furtherance of, or indicating its consent to, approval of, or acquiescence in, any of the acts set forth in clause (i), (ii) or (iii) above, or (v) the City shall generally not, or shall be unable to, or shall admit in writing its inability to, pay its debts as they become due. (g) The City shall default in the due observance of any covenant, condition or agreement contained in the General Ordinance or any Document and the expiration of any applicable grace period shall have occurred. (h) The City shall (a) default in the observance of certain covenants set forth in the Reimbursement Agreement, or (b) default in the observance of its other covenants under the Reimbursement Agreement not specifically referred to under this heading “Events of Default”, and such default shall continue unremedied for thirty (30) days (or, if the City is diligently pursuing a cure of such

8

default, and such default is capable of cure within such time period, sixty (60) days) after written notice of such default shall have been given to the City by the Credit Provider. (i) The Credit Account, the Sinking Fund Account or any funds on deposit in, or otherwise to the credit of, such accounts shall become subject to any writ, order, judgment, warrant of attachment, execution or similar process and such writ, order, judgment, warrant of attachment, execution or similar process prevents payment into or out of such Accounts for the purposes and at the times contemplated by the Documents, unless such writ, order, judgment, warrant of attachment, execution or similar process shall be fully bonded. (j) Any judgment arising out of the operation of the City or PGW in an aggregate amount in excess of $5,000,000 as to the City and an aggregate amount in excess of $2,500,000 as to PGW shall be entered against the City or PGW as the case may be and which is not (a) appealed, stayed or bonded, or (b) paid within ninety (90) days of becoming final. (k) Any provision of the Reimbursement Agreement or any of the other Documents or the General Ordinance shall at any time for any reason cease to be valid and binding on the related obligor thereunder or shall be declared to be null and void by any court or Governmental Authority or agency having jurisdiction over the City, or the validity or the enforceability thereof shall be contested by the City or PGW in a judicial or administrative proceeding. (1) Any change shall be made in any provision of the Act if such change would, in the reasonable judgment of the Credit Provider, materially and adversely affect the ability of the City to pay any amount coming due under the Reimbursement Agreement. (m) (a) The City shall default in the payment when due of any obligations (subject to any applicable notice or grace period) owed to the issuer of any Swap; (b) if the City is permitted to post collateral for a Swap under applicable law, the City shall fail to post collateral as required by the terms of any Swap; or (c) any event shall occur under any Swap which shall permit any obligation under any Swap in excess of $500,000 to be terminated or otherwise declared due and payable prior to its stated maturity and such event shall continue unremedied past any period of grace provided for in any agreement under which such Swap is issued. (n) A Governmental Authority with appropriate jurisdiction shall impose a debt moratorium, debt restructuring or debt adjustment on any indebtedness for borrowed money payable from the Revenues. Remedies If any Event of Default shall occur and be continuing under the Reimbursement Agreement, then, and in any such event, the Credit Provider may immediately in its sole discretion take any or all of the following actions: (a) Notify the Fiscal Agent of such Event of Default and direct the Fiscal Agent to cause a mandatory tender of the Fifth Series A-2 Bonds within two (2) Business Days following the date of receipt by the Fiscal Agent of such notice, and after payment of such mandatory tender, declare the Letter of Credit to be terminated, whereupon the Letter of Credit shall forthwith terminate on the tenth day following the date of receipt by the Fiscal Agent of such notice. (b) Declare all amounts payable under the Reimbursement Agreement, to be due and payable, whereupon the same shall become, immediately due and payable without presentment, demand,

9

protest or other notice of any kind, all of which are waived by the City; provided that in the case of any Event of Default specified in clause (f) under the heading “Events of Default” above, with respect to the City, all amounts payable under the Reimbursement Agreement shall be immediately due and payable without the giving of any notice to the City or the taking of any other action by any Person. (c) Upon not less than thirty (30) days’ prior notice to the City, direct the Fiscal Agent to declare all the unpaid principal amount of the Bank Bonds, interest accrued thereon and all other amounts owing by the City under the Reimbursement Agreement or under the Bank Bonds to be due and payable without presentment, demand, protest or notice of any kind, all of which are expressly waived, and an action therefor shall immediately accrue; provided, however, that with respect to an Event of Default under clause (f) under the heading “Events of Default” above, all the unpaid principal amount of the Bank Bonds interest accrued thereon and all other amounts owing by the City under the Reimbursement Agreement or under the Bank Bonds shall be immediately due and payable without presentment, demand, protest or notice of any kind, all of which are expressly waived, and an action therefor shall immediately accrue. (d) Exercise any rights and remedies available to it by law or under the Reimbursement Agreement or under the Documents or otherwise.

REMARKETING

The Fifth Series A-2 Bonds are being remarketed by the Remarketing Agent, pursuant to Original Remarketing Agreement, dated as of October 1, 2004 (the “Original Remarketing Agreement”) and the First Amendment to the Original Remarketing Agreement, dated June 6, 2012 (the “First Amendment” and, together with the “Original Remarketing Agreement”, the “Remarketing Agreement”) between the City and the Remarketing Agent. Subject to certain conditions, upon the delivery or deemed delivery of Fifth Series A-2 Bonds tendered for purchase by any owners thereof in accordance with the provisions of the Fifth Series A-2 Bonds and the Remarketing Agreement, the Remarketing Agent will offer for sale and use its commercially reasonable efforts to remarket such tendered Fifth Series A-2 Bonds, any such remarketing to be made on the date such tendered Fifth Series A-2 Bonds are to be purchased, at a price equal to 100% of the principal amount thereof plus accrued interest, if any. The interest rate will reflect, among other factors, the level of market demand for the Fifth Series A-2 Bonds (including whether the Remarketing Agent is willing to purchase Fifth Series A-2 Bonds for its own account). There may or may not be Fifth Series A-2 Bonds tendered and remarketed on a rate determination date and the Remarketing Agent may or may not be able to remarket any Fifth Series A-2 Bonds tendered for purchase on such date at par. The Remarketing Agent is not obligated to advise purchasers in a remarketing if it does not have third party buyers for all of the Fifth Series A-2 Bonds at the remarketing price.

The Remarketing Agent may be removed or replaced by the City and the Remarketing Agent may

also resign in accordance with the provisions of the Remarketing Agreement. The Remarketing Agent will receive a periodic fee from the City for its services based upon the average principal amount of Fifth Series A-2 Bonds which are outstanding during each such period and which bear interest at a Weekly Rate.

The Remarketing Agent is Paid by the City

The Remarketing Agent’s responsibilities include determining the interest rate from time to time and using its commercially reasonable efforts to remarket each subseries of Fifth Series A-2 Bonds that are optionally or mandatorily tendered by the owners thereof (subject, in each case, to the terms of the Remarketing Agreement). The Remarketing Agent is appointed by the City and is paid by the City for its services. As a result, the interests of the Remarketing Agent may differ from those of existing holders and potential purchasers of Fifth Series A-2 Bonds.

10

The Remarketing Agent Routinely Purchases Fifth Series A-2 Bonds for its Own Account

The Remarketing Agent acts as remarketing agent for a variety of variable rate demand obligations and, in its sole discretion, routinely purchases such obligations for its own accounts. The Remarketing Agent is permitted, but not obligated, to purchase tendered Fifth Series A-2 Bonds for its own account and, in its sole discretion, routinely acquires such tendered Fifth Series A-2 Bonds in order to achieve a successful remarketing of the Fifth Series A-2 Bonds (i.e., because there otherwise are not enough buyers to purchase the Fifth Series A-2 Bonds) or for other reasons. However, the Remarketing Agent is not obligated to purchase Fifth Series A-2 Bonds for its own account, and may cease doing so at any time without notice. The Remarketing Agent may also make a market in the Fifth Series A-2 Bonds by routinely purchasing and selling Fifth Series A-2 Bonds other than in connection with an optional or mandatory tender and remarketing. Such purchases and sales may be at or below par. However, the Remarketing Agent is not required to make a market in the Fifth Series A-2 Bonds. The Remarketing Agent may also sell any Fifth Series A-2 Bonds they have purchased to one or more affiliated investment vehicles for collective ownership or enter into derivative arrangements with affiliates or others in order to reduce its exposure to the Fifth Series A-2 Bonds. The purchase of Fifth Series A-2 Bonds by the Remarketing Agent may create the appearance that there is greater third party demand for the Fifth Series A-2 Bonds in the market than is actually the case. The practices described above also may result in fewer Fifth Series A-2 Bonds being tendered in a remarketing.

The Ability to Sell the Fifth Series A-2 Bonds Other Than through Tender Process May Be Limited

The Remarketing Agent may buy and sell Fifth Series A-2 Bonds other than through the tender process. However, it is not obligated to do so and may cease doing so at any time without notice and may require holders that wish to tender their Fifth Series A-2 Bonds to do so through the Tender Agent with appropriate notice. Thus, investors who purchase the Fifth Series A-2 Bonds, whether in a remarketing or otherwise, should not assume that they will be able to sell their Fifth Series A-2 Bonds other than by tendering the Fifth Series A-2 Bonds in accordance with the Bond Authorization and the Fifth Series A-2 Bonds.

TAX MATTERS

On October 19, 2004, Dilworth Paxson LLP and Jettie D. Newkirk Law Offices, Co-Bond Counsel, delivered their opinions (the “Bond Opinions”) with respect to the issuance of the Fifth Series A-2 Bonds. Copies of the Opinions are attached as Appendix F of the Original Official Statement, attached hereto as APPENDIX A. The Bond Opinions speak only as of the date thereof.

In connection with the remarketing of the Fifth Series A-2 Bonds on June 6, 2012, Blank Rome LLP, Bond Counsel, will deliver its opinion (the “No Adverse Affect Opinion”) to the effect that the initial remarketing of the Fifth Series A-2 Bonds as a result of the replacement of the letter of credit applicable to the Fifth Series A-2 Bonds will not, in and of itself, adversely affect the exclusion from gross income for federal income tax purposes of interest on the Fifth Series A-2 Bonds. The form of the No Adverse Affect Opinion is attached hereto as APPENDIX B.

RATINGS

Moody’s Investors Service (“Moody’s”) is expected to assign the ratings of “Aa1” and “VMIG1” to the Fifth Series A-2 Bonds based upon: (i) the ratings of the Credit Provider, (ii) the long-term ratings

11

of the City’s Gas Works Revenue Bonds (1998 Ordinance), and (iii) Moody’s credit correlation of the ratings of the Credit Provider and PGW.

Standard & Poor’s Ratings Services, a Division of The McGraw-Hill Companies, Inc. is expected to assign the ratings of “A+” and “A-1” to the Fifth Series A-2 Bonds based upon the long-term and short-term ratings, respectively, of the Credit Provider. Fitch Ratings is expected to assign the ratings of “A+” and “F1” to the Fifth Series A-2 Bonds, based upon the long-term and short-term ratings, respectively, of the Credit Provider.

Any explanation of these ratings may only be obtained from the rating agencies. A credit rating is not a recommendation to buy, sell or hold securities. No assurance is given that such ratings will be maintained for any given period of time or that they may not be lowered or withdrawn entirely by the rating agencies if, in their judgment, circumstances so warrant. Any such downward change in or withdrawal of any of such ratings may have an adverse effect on the market price of the Fifth Series A-2 Bonds.

CERTAIN LEGAL MATTERS

In connection with the replacement of the letter of credit applicable to the Fifth Series A-2 Bonds and the remarketing of the Fifth Series A-2 Bonds, certain legal matters will be passed upon by Blank Rome LLP, Philadelphia, Pennsylvania, Bond Counsel. Certain legal matters will be passed upon for the City of Philadelphia by the City Solicitor. Certain legal matters will be passed upon for Philadelphia Gas Works by the Office of General Counsel of the Philadelphia Gas Works. Certain legal matters will be passed upon for the Credit Provider by Chapman and Cutler LLP, Chicago, Illinois, Counsel to the Credit Provider.

FINANCIAL ADVISOR

Public Financial Management, Inc., Philadelphia, Pennsylvania, has served as financial advisor to the City in respect of the remarketing of the Fifth Series A-2 Bonds. The Financial Advisor assisted in the preparation of this Second Supplement to Official Statement and the structuring of the Fifth Series A-2 Bonds and has provided other advice. The Financial Advisor has received and reviewed but, except for the information contained under this section of the Second Supplement captioned “Financial Advisor”, have not independently verified information in this Second Supplement for accuracy or completeness. Investors should not draw any conclusions as to the suitability of the Fifth Series A-2 Bonds from, or base any investment decisions upon, the fact that the Financial Advisor has advised the City with respect to the remarketing of the Fifth Series A-2 Bonds. The Financial Advisor is a financial advisory and consulting organization and is not engaged in the business of remarketing or marketing of municipal securities or any other negotiable instruments.

NO LITIGATION

To the knowledge of the City of Philadelphia Law Department and, solely with respect to (E) below, based upon certain representations from PGW’s General Counsel, after customary inquiry, no litigation is pending against the City before any court, public board or agency, or threatened in writing against the City (A) to restrain or enjoin the remarketing of the Fifth Series A-2 Bonds, (B) which contests the validity or enforceability of the Fifth Series A-2 Bonds or any proceedings of the City taken with respect to the remarketing thereof, (C) which contests the pledge or application of any monies or security provided for the payment of the Fifth Series A-2 Bonds, (D) challenges the existence or powers of the City or (E) in which a final adverse determination, singly or in the aggregate, would have a material and adverse effect on PGW’s operations or financial condition.

12

CERTAIN REFERENCES

All summaries of the provisions of the Fifth Series A-2 Bonds and the security therefor, the Act, the General Ordinance and the Sixth Supplemental Ordinance set forth in the Original Official Statement and all the summaries and references to other materials not purported to be quoted in full are only brief outlines of certain provisions thereof and do not constitute complete statements of such documents or provisions. Reference is made hereby to the complete documents relating to such matters for the complete terms and provisions thereof. So far as statements are made in this Second Supplement involving matters of opinion, whether or not expressly so stated, they are made merely as such and not as representations of fact.

CONTINUING DISCLOSURE

In connection with the original issuance of the Fifth Series A-2 Bonds, the City entered into a Continuing Disclosure Agreement with Digital Assurance Certification, L.L.C., which constitutes a written undertaking for the benefit of the owners and beneficial owners of the Fifth Series A-2 Bonds. A copy of the form of the Continuing Disclosure Agreement is attached to the Original Official Statement as Appendix E thereto.

[The remainder of this page is intentionally left blank]

13

This Second Supplement to Official Statement has been duly executed and delivered by the

following officers on behalf of the City of Philadelphia.

CITY OF PHILADELPHIA, PENNSYLVANIA

By: /s/ Michael A. Nutter Honorable Michael A. Nutter, Mayor

By: /s/ Alan L. Butkovitz Honorable Alan L. Butkovitz, City Controller

By: /s/ Shelley R. Smith Shelley R. Smith, City Solicitor

Approved:

By: /s/ Rob Dubow Rob Dubow, Director of Finance

[THIS PAGE INTENTIONALLY LEFT BLANK]

APPENDIX A

ORIGINAL OFFICIAL STATEMENT, AS SUPPLEMENTED BY FIRST SUPPLEMENT TO OFFICIAL STATEMENT

[THIS PAGE INTENTIONALLY LEFT BLANK]

The purpose of this supplement (the "Supplement") is to update certain information included in the Official Statement dated October 7, 2004 (the "Original Official Statement") relating to the below-referenced bonds (the "Fifth Series A-2 Bonds"). The Original Official Statement was delivered in connection with the offering of the following three series of bonds by the City of Philadelphia, Pennsylvania: (1) Gas Works Revenue Bonds, Fifth Series A-1 (1998 General Ordinance) in the original principal amount of$120,000,000; (2) the Fifth Series A-2 Bonds in the original principal amount of $30,000,000; and (3) Gas Works Revenue Bonds, Eighteenth Series (1975 General Ordinance) in the original principal amount of $57,820,000. This Supplement pertains only to the offering of the Fifth Series A-2 Bonds. Terms not otherwise defmed herein have the meanings set forth in the Original Official Statement.

SUPPLEMENT TO OFFICIAL STATEMENT

Relating to:

$30,000,000 City of Philadelphia, Pennsylvania

Gas Works Variable Rate Demand Revenue Bonds, Fifth Series A-2 (1998 General Ordinance)

This Supplement is an amendment to the Original Official Statement and relates only to the offering of the Fifth Series A-2 Bonds. This Supplement should be read together with the Original Official Statement (which is incorporated herein by reference). To the extent the information in this Supplement conflicts with the information in the Original Official Statement, this Supplement shall govern. Please retain a copy of this Supplement to Official Statement with your copy of the Original Official Statement.

Subsequent to the printing of the Original Official Statement, Moody's, S&P and Fitch issued ratings for the Fifth Series A-2 Bonds which varied from the expected ratings set forth in the Original Official Statement. Moody's, S&P and Fitch have assigned (a) long term ratings of "Aaa," "A+" and "A+", respectively, and (b) short term ratings of "VMIG-1," "Al" and "Fl+", respectively, to the Fifth Series A-2 Bonds, based upon the issuance of the Initial Letter of Credit. Additionally, the amount of interest coverage provided under the Initial Letter of Credit is $410,959 for a total stated amount of the Initial Letter of Credit of$30,410,959, not $416,667 and $30,416,667, respectively, as stated in the Original Official Statement. The Original Official Statement is modified by this Supplement to reflect these changes.

JPMorgan

Dated: October 19,2004

A-1

THE INITIAL LETTER OF CREDIT (Page 30 of Original Official Statement)

In the fourth line of the second full paragraph under the heading "THE INITIAL LEITER OF CREDIT", the amount "$30,416,667" is hereby deleted and replaced by the amount "$30,410,959". In the eighth line ofthe second full paragraph under the heading "THE INITIAL LETTER OF CREDIT", the amount "$416,667" is hereby deleted and replaced by the amount "$410,959".

UNDERWRITING (Page 77 of Original Official Statement)

The second sentence of the first full paragraph under the heading "UNDERWRITING" is hereby deleted and replaced in its entirety by the following sentence:

J.P. Morgan Securities Inc. has agreed, pursuant to a second purchase contract dated the date hereof, subject to certain terms and conditions contained therein, to purchase the Fifth Series A-2 Bonds from the City for a purchase price of$29,880,563.97, which is equal to the par amount of$30,000,000 less the underwriter's discount of$119,436.03.

RATINGS (Page 77 of Original Official Statement)

The second sentence of the first full paragraph under the heading "RATINGS" is hereby deleted and replaced in its entirety by the following sentence:

Moody's, S&P and Fitch have assigned (a) long term ratings of"Aaa," "A+" and "A+", respectively, and (b) short term ratings of "VMIG-1," "AI" and "Fl+", respectively, for the Fifth Series A-2 Bonds, based upon the issuance of the Initial Letter of Credit.

A-2

This Supplement to Official Statement dated October 19, 2004 has been duly executed and delivered by the following officers on behalf of the City of Philadelphia.

CITY OF PHILADELPHIA, PENNSYLVANIA

By: Is/ John F. Street Honorable John F. Street, Mayor

By: Is/ Jonathan A. Saidel Honorable Jonathan A. Saidel, City Controller

By: Is/ Pedro A. Ramos Pedro A. Ramos, City Solicitor

Approved:

By: Is/ Everett Ray Zies Everett Ray Zies, Acting Secretary of Financial Oversight and Acting Director of Finance

A-3

[THIS PAGE INTENTIONALLY LEFT BLANK]

(See ‘‘RATINGS’’ herein)

New Issue Book-Entry OnlyIn the opinion of Co-Bond Counsel, interest on the Bonds is not includable in gross income for purposes of federal income taxation under existing statutes, regulations, rulings and

court decisions, subject to the conditions described in ‘‘TAX MATTERS’’ herein. Interest on the Bonds will not be a specific preference item for purposes of the individual and corporatealternative minimum taxes; however, such interest may be subject to certain other federal taxes affecting corporate holders of the Bonds. Under the laws of the Commonwealth ofPennsylvania, as enacted and construed on the date hereof, the Bonds are exempt from Pennsylvania personal property taxes and the interest on the Bonds is exempt from Pennsylvaniaincome tax and Pennsylvania corporate net income tax. For a more complete discussion see ‘‘TAX MATTERS’’ herein.

$207,820,000City of Philadelphia, Pennsylvania

Gas Works Revenue Bondsconsisting of:

$120,000,000GAS WORKS REVENUE BONDS,

FIFTH SERIES A-1(1998 GENERAL ORDINANCE)

$30,000,000GAS WORKS VARIABLE RATE DEMANDREVENUE BONDS, FIFTH SERIES A-2

(1998 GENERAL ORDINANCE)

$57,820,000GAS WORKS REVENUE BONDS,

EIGHTEENTH SERIES(1975 GENERAL ORDINANCE)

Dated: Date of Delivery Due: As shown on inside cover page

The City of Philadelphia, Pennsylvania Gas Works Revenue Bonds, Fifth Series A-1 (1998 General Ordinance) (the ‘‘Fifth Series A-1 Bonds’’), The City of Philadelphia,Pennsylvania Gas Works Variable Rate Demand Revenue Bonds, Fifth Series A-2 (1998 General Ordinance) (the ‘‘Fifth Series A-2 Bonds’’ and together with the Fifth Series A-1 Bonds,the ‘‘Fifth Series Bonds’’) and The City of Philadelphia, Pennsylvania Gas Works Revenue Bonds, Eighteenth Series (1975 General Ordinance) (the ‘‘Eighteenth Series Bonds’’ andtogether with the Fifth Series Bonds, the ‘‘Bonds’’) are issued pursuant to the Act and the General Ordinances (as such terms are defined herein). The Fifth Series A-1 Bonds and theEighteenth Series Bond, issuable as fully registered bonds in denominations of $5,000 or any integral multiple thereof, will mature in the aggregate principal amounts and bearing interest atthe rates set forth on the inside front cover hereof. The Fifth Series A-2 Bonds, issuable as fully registered bonds in denominations of $100,000 or any integral multiple of $5,000 in excessthereof, will initially bear interest at the Weekly Rate, subject to conversion to another Rate Mode, as described herein, and will mature on September 1, 2034. The Bonds, when issued, willbe registered in the name of Cede & Co., as registered owner and nominee of The Depository Trust Company (‘‘DTC’’), which will act as securities depository for the Bonds. Purchases ofthe beneficial ownership interests in the Bonds will be made in book-entry only form. Purchasers will not receive certificates representing their ownership interests in the Bonds purchased,so long as Cede & Co. is the owner of the Bonds, as nominee of DTC. References herein to the bondholders, holders and registered owners shall mean Cede & Co., as aforesaid, and shallnot mean the beneficial owners of the Bonds. See ‘‘DESCRIPTION OF THE BONDS – Book-Entry Only System.’’

The principal and redemption price of the Bonds are payable at the corporate trust office of Wachovia Bank, National Association, as Fiscal Agent and Sinking Fund Depository, inPhiladelphia, Pennsylvania, at the times and in the amounts set forth herein. Interest is payable (i) semiannually on each March 1 and September 1, commencing March 1, 2005 with respectto the Fifth Series A-1 Bonds; (ii) semiannually on each February 1 and August 1, commencing February 1, 2005 with respect to the Eighteenth Series Bonds; and (iii) while in the WeeklyMode, on the first Business Day of each month commencing on November 1, 2004 with respect to the Fifth Series A-2 Bonds, by check mailed by the Fiscal Agent to the persons in whosenames the Bonds are registered on the Business Day immediately preceding each interest payment date. So long as DTC or its nominee, Cede & Co., is the registered owner of the Bonds,principal of and interest on the Bonds are payable directly to Cede & Co. for redistribution to Participants and in turn to Beneficial Owners as described herein. For so long as any purchaseris the Beneficial Owner of Bonds, such purchaser must maintain an account with a broker or dealer who is, or acts through, a Participant to receive payment of the principal of and intereston such Bonds.

The Bonds are subject to redemption prior to maturity as described herein under the heading ‘‘DESCRIPTION OF THE BONDS.’’ The Fifth Series A-2 Bonds are also subject tooptional and mandatory tender while in the Weekly Mode, as set forth herein.

THE BONDS DO NOT PLEDGE THE CREDIT OR TAXING POWER OF THE CITY OF PHILADELPHIA OR CREATE ANY DEBT OR CHARGE AGAINST THE TAX ORGENERAL REVENUES OF THE CITY OF PHILADELPHIA OR CREATE A LIEN AGAINST ANY CITY PROPERTY OTHER THAN CERTAIN REVENUES AND FUNDS OFTHE PHILADELPHIA GAS WORKS REFERRED TO HEREIN.

THE FIFTH SERIES BONDS SHALL BE ISSUED ON A PARITY WITH OTHER SENIOR 1998 ORDINANCE BONDS ISSUED UNDER THE 1998 GENERAL ORDINANCEBUT SHALL BE SUBORDINATED IN RIGHT OF PAYMENT AND SECURITY TO THE EIGHTEENTH SERIES BONDS AND ALL OTHER BONDS ISSUED ANDOUTSTANDING UNDER THE 1975 GENERAL ORDINANCE AS DESCRIBED HEREIN.

The scheduled payment of principal of and interest on the Fifth Series A-1 Bonds when due will be guaranteed under separate municipal bond insurance policies to be issuedconcurrently with the delivery of such series of Bonds by Financial Security Assurance Inc. and Assured Guaranty Corp. Each policy will insure one or more maturities, as set forth on theinside cover hereof.

The scheduled payment of principal of and interest on the Eighteenth Series Bonds when due will be guaranteed under separate municipal bond insurance policies to be issuedconcurrently with the delivery of such series of Bonds by Ambac Assurance Corporation, CDC IXIS Financial Guaranty North America, Inc. and Assured Guaranty Corp. Each policy willinsure one or more maturities or portions thereof, as set forth on the inside cover hereof.

While in the Weekly Mode, the scheduled payment of principal of and interest for up to 50 days at a maximum interest rate of 10% per annum on the Fifth Series A-2 Bonds, and thepayment of the principal of and interest, for up to 50 days at a maximum interest rate of 10% per annum, for any tendered but unremarketed Fifth Series A-2 Bonds, will be funded initiallyfrom draws on an irrevocable direct pay letter of credit to be issued on the date of delivery of the Fifth Series A-2 Bonds, as a several but not joint obligation, by

JPMORGAN CHASE BANK and THE BANK OF NOVA SCOTIA(collectively, the ‘‘Banks’’).

The Fifth Series Bonds are being issued to provide funds for any or all of the following purposes: (i) the capital projects included in the capital program of the Philadelphia GasWorks (‘‘PGW’’ or the ‘‘Gas Works’’), as from time to time included in the capital budgets of PGW and approved by the City Council of the City of Philadelphia, which may include,without limitation, (a) the acquisition of land or rights therein; (b) the acquisition, construction or improvement of buildings, structures and facilities together with their related furnishings,equipment, machinery and apparatus; (c) the acquisition, construction or replacement of pipes and pipe lines; and (d) the acquisition or replacement of property of a capital nature for use inthe operation, maintenance and administration of PGW’s gas works system; (ii) paying the costs of issuing the Fifth Series Bonds and any required deposits to the Sinking Fund Reserveestablished under the 1998 General Ordinance; (iii) paying any other Project Costs, which may include, without limitation, the repayment to any fund of the City or to accounts of the GasWorks of amounts advanced for Project Costs, and the funding or refunding of outstanding bond anticipation notes or other obligations of the City issued in respect of Project Costs; and(iv) financing of capitalized interest for the Fifth Series Bonds.

The Eighteenth Series Bonds are being issued for the purpose of providing funds for any or all of the following purposes: (i) the refunding and redeeming on a current basis of aportion of the outstanding City of Philadelphia, Pennsylvania, Gas Works Revenue Bonds, Fifteenth Series (1975 General Ordinance) consisting of certain maturities of Subseries 1 andSubseries 3 (the ‘‘Refunded Bonds’’); (ii) paying the costs of issuing the Eighteenth Series Bonds and any required deposits to the Sinking Fund Reserve established under the 1975 GeneralOrdinance; and (iii) paying any other Project Costs relating to the refunding of the Refunded Bonds or the issuance of the Eighteenth Series Bonds which may include, without limitation,the repayment to any fund of the City of Philadelphia or the accounts of PGW of amounts advanced for the Project Costs, and the funding or refunding of outstanding bond anticipationnotes or other obligations of the City of Philadelphia issued in respect of Project Costs.

THE COVER PAGE CONTAINS CERTAIN INFORMATION FOR QUICK REFERENCE ONLY. IT IS NOT A SUMMARY OF THIS ISSUE. PROSPECTIVE INVESTORSMUST READ THE ENTIRE OFFICIAL STATEMENT TO OBTAIN INFORMATION ESSENTIAL TO MAKING AN INFORMED INVESTMENT DECISION.

The Bonds are offered when, as and if issued and accepted by the Underwriters, subject to the prior sale, withdrawal, or modification of the offer without notice, and subject to theapproval as to the legality of the issuance of the Bonds by Dilworth Paxson LLP and Jettie D. Newkirk Law Offices, Co-Bond Counsel, both of Philadelphia, Pennsylvania. Certain legalmatters will be passed upon for the Underwriters by Greenberg Traurig, LLP and Law Offices of Denise Joy Smyler, both of Philadelphia, Pennsylvania, Co-Counsel to the Underwriters.Certain legal matters will be passed upon for the City of Philadelphia by the City of Philadelphia Law Department and by Blank Rome LLP, Philadelphia, Pennsylvania, Special Counsel.Certain legal matters will be passed upon for PGW by the Office of General Counsel. Certain legal matters will be passed upon for the Banks by Duane Morris LLP, New York, New York,counsel to the Banks. It is anticipated that the Fifth Series A-1 Bonds and the Eighteenth Series Bonds will be available for delivery through the facilities of DTC in New York, New Yorkon or about October 14, 2004 and that the Fifth Series A-2 Bonds will be available for delivery through the facilities of DTC in New York, New York on or about October 19, 2004.

JPMorganGoldman, Sachs and Co. Loop Capital Markets, LLC

Doley Securities, Inc. UBS Financial Services Inc.

Wachovia Bank, National Association Sovereign Securities Corporation, LLC Morgan Stanley

Dated: October 7, 2004

MATURITY SCHEDULE $120,000,000

CITY OF PHILADELPHIA, PENNSYLVANIA GAS WORKS REVENUE BONDS, FIFTH SERIES A-1

(1998 GENERAL ORDINANCE)SERIES A-1 (SERIALS INSURED BY ASSURED GUARANTY)

Maturity (September 1)

Amount

Interest Rate

Yield

2012 2,865,000 4.000% 3.60% 2013 3,000,000 5.000% 3.74% 2017* 3,665,000 5.250% 4.11% 2018* 3,865,000 5.250% 4.19% 2019* 4,075,000 5.250% 4.25%

SERIES A-1 (SERIALS INSURED BY FINANCIAL SECURITY)

Maturity (September 1)

Amount

Interest Rate

Yield

Maturity (September 1)

Amount

Interest Rate

Yield

2009 2,480,000 5.000% 2.75% 2022* 4,735,000 5.000% 4.33% 2010 2,605,000 5.000% 3.02% 2023* 4,980,000 5.000% 4.41% 2011 2,740,000 5.000% 3.21% 2024* 5,235,000 5.000% 4.48% 2014 3,150,000 5.000% 3.62% 2025* 5,505,000 5.000% 4.55% 2015* 3,315,000 5.000% 3.73% 2026* 5,785,000 5.000% 4.62% 2016* 3,485,000 5.000% 3.82% 2020* 4,285,000 5.000% 4.16% 2021* 4,505,000 5.000% 4.24%

$19,205,000 5.000% Term Bond due September 1, 2029, Priced at 102.503 to Yield 4.680% $30,520,000 5.000% Term Bond due September 1, 2033, Priced at 102.106 to Yield 4.730% ________________________ * Priced to the September 1, 2014 call date at 100%.

$30,000,000 CITY OF PHILADELPHIA, PENNSYLVANIA

GAS WORKS VARIABLE RATE DEMAND REVENUE BONDS, FIFTH SERIES A-2 (1998 GENERAL ORDINANCE)

Maturity: September 1, 2034 Price: 100% $57,820,000

CITY OF PHILADELPHIA, PENNSYLVANIA GAS WORKS REVENUE BONDS, EIGHTEENTH SERIES

(1975 GENERAL ORDINANCE) REFUNDING SERIAL MATURITIES (AMBAC)

Maturity (August 1)

Amount

Interest Rate

Yield

2007 665,000 3.000% 2.160% 2008 870,000 3.000% 2.440% 2009 870,000 3.000% 2.750% 2010 9,675,000 5.000% 3.020% 2011 125,000 3.125% 3.210% 2012 125,000 3.250% 3.350% 2013 125,000 3.375% 3.490% 2014 115,000 3.500% 3.620% 2015* 4,470,000 5.000% 3.730%

REFUNDING SERIAL MATURITIES (CIFGNA) Maturity

(August 1)

Amount Interest

Rate

Yield

2006 975,000 5.000% 2.040% 2007 1,125,000 5.000% 2.260% 2011 2,790,000 5.000% 3.270% 2014 3,195,000 5.000% 3.710% 2015* 3,350,000 5.000% 3.820%

REFUNDING SERIAL MATURITIES (ASSURED GUARANTY) Maturity

(August 1)

Amount Interest

Rate

Yield Maturity

(August 1)

Amount Interest

Rate

Yield 2005 420,000 5.000% 2.000% 2020* 3,485,000 5.250% 4.320% 2008 1,185,000 5.000% 2.760% 2021* 3,700,000 5.250% 4.390% 2009 1,240,000 5.000% 3.050% 2010 1,305,000 5.000% 3.280% 2012 2,925,000 4.000% 3.600% 2013 3,040,000 5.000% 3.740% 2016* 2,745,000 5.250% 4.030% 2017* 2,915,000 5.250% 4.110% 2018* 3,095,000 5.250% 4.190% 2019* 3,290,000 5.250% 4.250%

________________________ * Priced to the August 1, 2014 call date at 100%

THE CITY OF PHILADELPHIA ________________________

MAYOR JOHN F. STREET

_________________________

MAYOR’S CHIEF OF STAFF Joyce S. Wilkerson

_________________________

MAYOR’S CABINET

Everett Ray Zies .................................................. Acting Secretary of Financial Oversight/Acting Director of FinancePedro A. Ramos......................................................................................................................................... City Solicitor Philip R. Goldsmith .......................................................................................................................... Managing Director George R. Burrell, Jr..........................................................................................................Secretary of External Affairs Stephanie Naidoff .................................................................................City Representative and Director of Commerce Debra A. Kahn............................................................................................................................ Secretary of Education Sylvester M. Johnson.......................................................................... Police Commissioner/Secretary of Public Safety Maxine Griffith....... Secretary of Strategic Planning and Initiatives/Executive Director of City Planning Commission Dianah L. Neff........................................................................................................................Chief Information Officer

_________________________ CITY CONTROLLER

Jonathan A. Saidel

_________________________

PHILADELPHIA GAS WORKS

800 W. Montgomery Avenue Philadelphia, Pennsylvania 19122

Thomas E. Knudsen, President and Chief Executive Officer Craig E. White, Acting Chief Operating Officer

Joseph R. Bogdonavage, Senior Vice President – Finance Abby L. Pozefsky, Senior Vice President and General Counsel

Janice L. Walsh, Senior Vice President – Operations Les A. Fyock, Vice President – Regulatory Affairs

David Griesing, Vice President – Strategic Planning Randy Gyory, Vice President – Customer Affairs

Steven P. Hershey, Vice President – Community Initiatives Thomas L. Kuczynski, Vice President – Information Services & Chief Information Officer

Paul Mondimore, Vice President – Field Operations Douglas Moser, Vice President – Gas Management

John P. Straub, Vice President – Labor, Safety and Preparedness Joseph F. Golden, Jr., Controller

FINANCIAL ADVISORS

Public Financial Management, Inc. P.G. Corbin and Company, Inc.

FISCAL AGENT

Wachovia Bank, National Association

No dealer, broker, salesperson or other person has been authorized to give any information or to make any representations, other than those contained in this Official Statement and, if given or made, such other information or representations must not be relied upon. This Official Statement does not constitute an offer to sell or the solicitation of an order to buy, nor shall there be any sale of the Bonds by any person in any jurisdiction in which it is unlawful to make such offer, solicitation or sale.

The Underwriters have provided the following sentence for inclusion in this Official Statement. The Underwriters have reviewed the information in this Official Statement in accordance with and as part of their responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriters do not guarantee the accuracy or completeness of such information. The information and the opinions expressed herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the operations of the Philadelphia Gas Works or the City of Philadelphia since the date hereof, or as to the information under “PGW BUDGET, RATES AND FINANCES – Fiscal Years 2003 and 2004 Operating Budgets,” since August 31, 2003.

The order and placement of materials in this Official Statement, including the Appendices hereto, are not to be deemed to be a determination of relevance, materiality or importance, and this Official Statement, including the Appendices, must be considered in its entirety.

This Official Statement is not to be construed as a contract with the purchasers of the Bonds. All summaries of statutes and documents are made subject to the complete text of such statutes and documents, respectively, and do not purport to be complete statements of any or all of such provisions.

This Official Statement is submitted in connection with the sale of securities referred to herein and may not be reproduced or be used, as a whole or in part, for any other purpose.

The Bonds have not been registered under the Securities Act of 1933, as amended, in reliance upon an exemption contained therein, and have not been registered or qualified under the securities laws of any state.

THESE SECURITIES HAVE NOT BEEN RECOMMENDED BY ANY FEDERAL OR STATESECURITIES COMMISSION OR REGULATORY AUTHORITY.

IN CONNECTION WITH THE OFFERING OF THE BONDS, THE UNDERWRITERS MAYOVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OFSUCH BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPENMARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME WITHOUTPRIOR NOTICE.

Other than with respect to information concerning Financial Security Assurance Inc., Ambac Assurance Corporation, CDC IXIS Financial Guaranty North America, Inc. and Assured Guaranty Corp. (collectively, the “Bond Insurers”) contained under the caption “Bond Insurance” and APPENDIX G — “Specimen Municipal Bond Insurance Policies” herein, none of the information in this Official Statement has been supplied or verified by the Bond Insurers and the Bond Insurers make no representation or warranty, express or implied, as to (i) the accuracy or completeness of such information; (ii) the validity of the Bonds; or (iii) the tax exempt status of the interest on the Bonds.

Other than with respect to information concerning the Initial Letter of Credit (as defined herein) and certain information regarding JPMorgan Chase Bank and The Bank of Nova Scotia, acting through its New York Agency (collectively, the “Banks”) contained in APPENDIX H — “Certain Information Concerning the Banks” herein, none of the information in this Official Statement has been supplied or verified by the Banks, and the Banks make no representation or warranty, express or implied, as to (i) the accuracy or completeness of such information; (ii) the validity of the Bonds; or (iii) the tax exempt status of the interest on the Bonds.

This Official Statement speaks only as of the date printed on the cover page hereof. The information contained herein is subject to change. The Official Statement will be made available through one or more of the Nationally Recognized Municipal Securities Information Repositories.

TABLE OF CONTENTS INTRODUCTION.........................................................2

The Philadelphia Gas Works .................................3Prior Issues of Gas Works Revenue

Bonds .............................................................4Authorization to Issue the Bonds...........................4The Bonds..............................................................5Purpose of the Bonds .............................................5Security for the Bonds ...........................................6Bond Insurance ......................................................8Initial Letter of Credit ............................................8Independent Consultant’s Report...........................8Continuing Disclosure .........................................11Miscellaneous ......................................................11

PLAN OF FINANCE AND ESTIMATED SOURCES AND USES OF FUNDS...................11Plan of Finance ....................................................11Estimated Sources and Uses of Funds .................12

DESCRIPTION OF THE BONDS..............................13General ................................................................13Book-Entry Only System.....................................14Discontinuation of Book-Entry System ...............15Optional Redemption...........................................16Extraordinary Redemption at Direction of

Bond Insurers ...............................................16Mandatory Redemption .......................................16Selection of Bonds to be Called for

Redemption ..................................................17Notice of Redemption of Bonds ..........................18Transfer of Bonds ................................................18Description of the Fifth Series A-2 Bonds

in the Weekly Mode .....................................18Conversion of Fifth Series A-2 Bonds to

Another Rate Mode ......................................22SECURITY .................................................................23

Security for the Fifth Series A-2 Bonds...............23Pledge of Revenues and Funds ............................23Covenant Against Commingling with

Other City Funds ..........................................24Priority in Application of Revenues.....................25Rate Covenant and Rate Requirements................27Sinking Fund........................................................28Sinking Fund Reserve..........................................29

THE INITIAL LETTER OF CREDIT ........................30THE REIMBURSEMENT AGREEMENT.................31

Reimbursement Obligation ..................................32Covenants ............................................................32Defaults and Remedies ........................................32

REPLACEMENT LETTERS OF CREDIT ................34Notices of Extension or Replacement..................35

BOND INSURANCE..................................................35Bond Insurance Policies.......................................35Bond Insurers.......................................................38

ADDITIONAL BONDS .............................................42Additional 1975 Ordinance Bonds.......................42Additional 1998 Ordinance Bonds.......................42Bond Anticipation Notes .....................................42

OTHER OUTSTANDING DEBT OBLIGATIONS ...42Lease Obligations ................................................42Short-Term Borrowings.......................................43City Loan .............................................................43

SWAP AND OPTION AGREEMENT .......................43REMEDIES OF BONDHOLDERS ............................46

Limitation on Remedies of Bondholders .............46

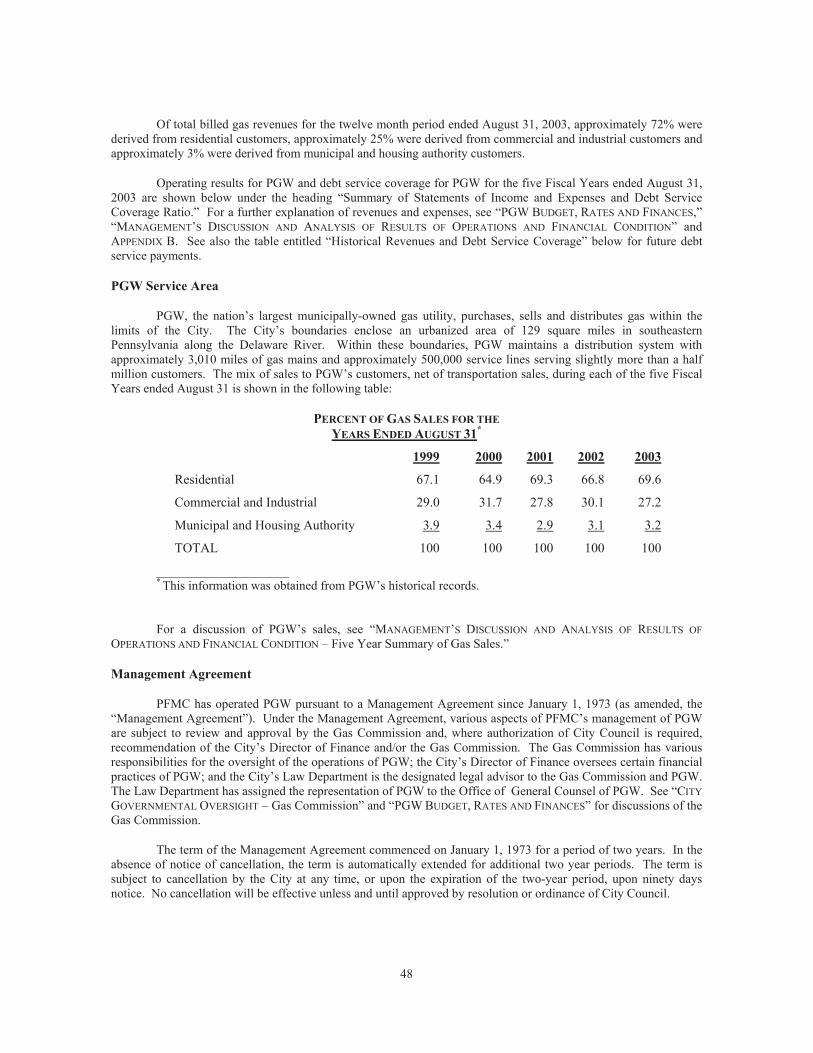

PHILADELPHIA GAS WORKS................................47General ................................................................47PGW Service Area...............................................48Management Agreement......................................48Management ........................................................49Management and Governance of the Gas

Works ...........................................................51Labor Relations....................................................52Facilities...............................................................52Environmental Matters ........................................54Gas Supply and Federal Regulation.....................55Competition .........................................................55Insurance..............................................................55Litigation .............................................................56Effects of the Natural Gas Choice and

Competition Act ...........................................56Litigation Relating to the Gas Choice Act ...........57Collections, Senior Citizen Discount and

Universal Service Issues...............................58CITY GOVERNMENTAL OVERSIGHT..................59

Gas Commission..................................................59PGW BUDGET, RATES AND FINANCES ..............59

Budget Approval..................................................59Rates and Charges................................................60Gas Cost Rate ......................................................61Base Rate Filings .................................................62Restructuring’s Effect on PGW Rates .................62Capital Improvement Program.............................63Other Funding Sources ........................................64Fiscal Year 2004 and 2005 Operating

Budgets.........................................................64Fiscal Year 2004 and 2005 Capital Budget

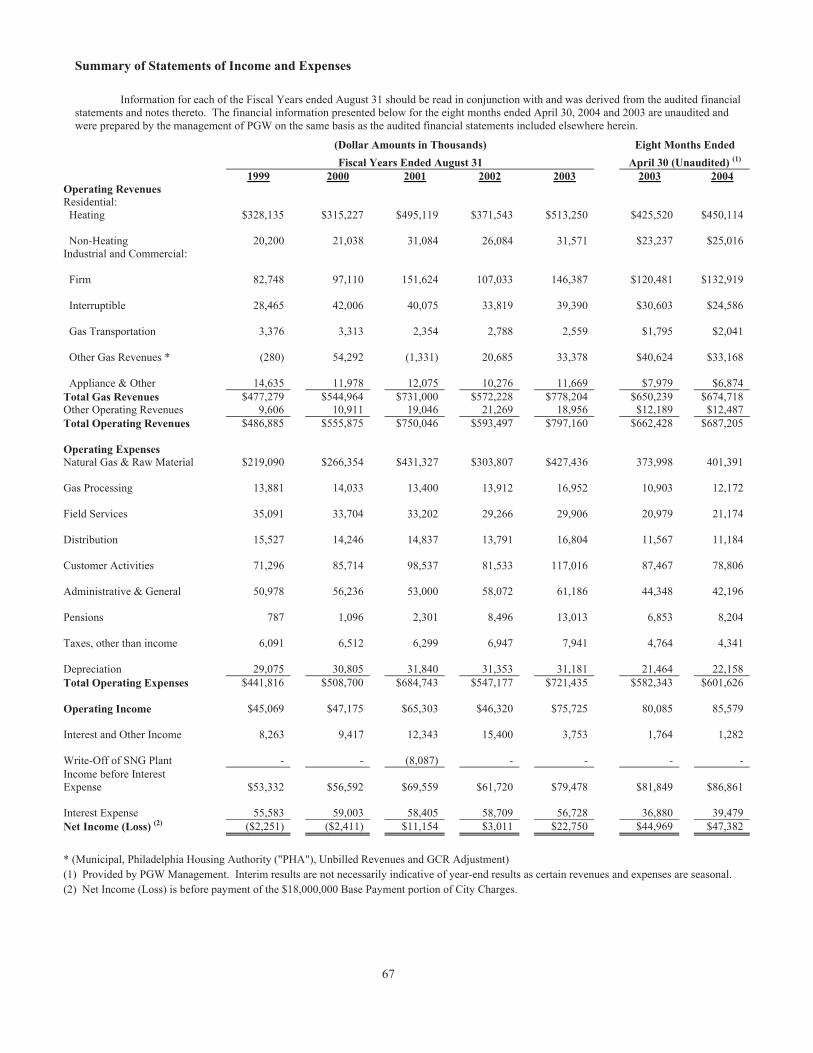

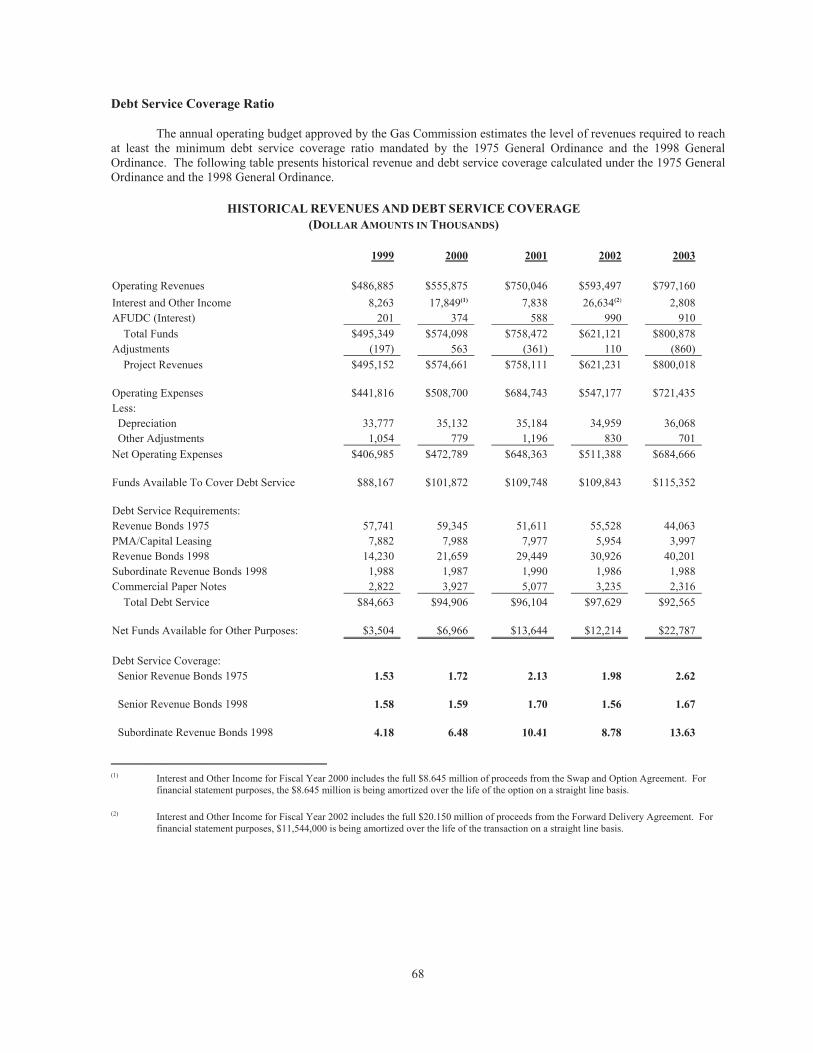

and Forecasts................................................64Debt Service Coverage Ratio...............................68

MANAGEMENT’S DISCUSSION AND ANALYSIS RESULTS OF OPERATIONS AND FINANCIAL CONDITION .......................69Financial Highlights.............................................69Overview of the Financial Statements .................69Five Year Summary of Gas Sales ........................74Natural Gas ..........................................................75Accounts Receivable ...........................................75

UNDERWRITING......................................................77VERIFICATION OF MATHEMATICAL

COMPUTATIONS ..............................................77RATINGS ...................................................................77TAX MATTERS.........................................................78

Federal Tax Exemption........................................78Tax Accounting Treatment of Original

Issue Discount ..............................................78Original Issue Premium .......................................78Pennsylvania Tax Exemption ..............................79

CERTAIN LEGAL MATTERS..................................79FINANCIAL ADVISORS ..........................................79INDEPENDENT AUDITORS ....................................79INDEPENDENT CONSULTANT’S REPORT..........79CERTAIN RELATIONSHIPS....................................79NO LITIGATION .......................................................80NEGOTIABLE INSTRUMENTS...............................80CERTAIN REFERENCES..........................................80CONTINUING DISCLOSURE ..................................80ADDITIONAL INFORMATION ...............................80

A. Financial Statements of PGW for Fiscal Year Ended August 31, 2003 and 2002 .............................................A-1 B. Independent Consultant’s Report .......................................................................................................................B-1 C. Certain Information Concerning the City of Philadelphia..................................................................................C-1 D. Summaries of the Act and Legislation Authorizing the Issuance of the Bonds .................................................D-1 E. Form of Continuing Disclosure Agreement ....................................................................................................... E-1 F. Forms of Opinions of Co-Bond Counsel............................................................................................................ F-1 G. Specimen Municipal Bond Insurance Policies ...................................................................................................G-1 H. Certain Information Concerning the Banks........................................................................................................H-1 I. Definitions of Certain Terms Pertaining to the Fifth Series A-2 Bonds.............................................................. I-1

2

OFFICIAL STATEMENT

$120,000,000 CITY OF PHILADELPHIA,

PENNSYLVANIA GAS WORKS REVENUE BONDS,

FIFTH SERIES A-1 (1998 GENERAL ORDINANCE)

$30,000,000 CITY OF PHILADELPHIA,

PENNSYLVANIA GAS WORKS VARIABLE RATE

DEMAND REVENUE BONDS, FIFTH SERIES A-2

(1998 GENERAL ORDINANCE)

$57,820,000 CITY OF PHILADELPHIA,

PENNSYLVANIA GAS WORKS REVENUE BONDS,

EIGHTEENTH SERIES (1975 GENERAL ORDINANCE)

INTRODUCTION

General