religare health trust - listed...

TRANSCRIPT

Religare Health Trust STRICTLY PRIVATE AND CONFIDENTIAL

This presentation is focused on comparing actual results from the period from 1 October 2013 to 31 December 2013 (“3Q

FY 2014”) versus the projected figures for the financial year 2014. No other comparative figures will be presented as the

acquisition of the Portfolio of RHT as well as listing on the Singapore Stock Exchange was completed on 19 October 2012.

This presentation may contain forward-looking statements that involve risks and uncertainties. Actual future performance,

outcomes and results may differ materially from those expressed in forward-looking statements as a result of a number of

risks, uncertainties and assumptions. Representative examples of these factors include (without limitation) general industry

and economic conditions, interest rate trends, cost of capital and capital availability, competition from other developments or

companies, shifts in expected levels of income and occupancy rate, changes in operating expenses (including employee

wages, benefits and training), governmental and public policy changes and the continued availability of financing in the

amounts and the terms necessary to support future business. Investors are cautioned not to place undue reliance on these

forward-looking statements.

The Indian Rupee and Singapore Dollar are defined herein as “INR” and “S$” respectively. Any discrepancy between

individual amounts and total shown in this presentation is due to rounding. Unless otherwise stated, all Indian Rupee

amounts in this set of slides have been translated into Singapore dollars based on the fixed exchange rate of ₹49.62 =

S$1.00.

Disclaimer

Agenda

3Q FY 2014 Key Highlights & Financial Review

Portfolio Highlights

Acquisition of Mohali Clinical Establishment

Growth Strategy

Peer Analysis

Religare Health Trust

Issuer Religare Health Trust (“RHT”)

Sponsor Fortis Healthcare Ltd (“Fortis” or the “Sponsor”)

Trustee-Manager Religare Health Trust Trustee Manager Pte Ltd (“TM”)

Sponsor Stake 28.0% Sponsor stake (220.7 m units) Lock-up of 6 months (100%) and further 6 months (50%) from 19 October 2012

Funds Raised at IPO S$510 mil 567.5 m units (72.0% of total units)

Distribution Yield based on unit price of S$0.775 (1) 10.5% (Projection Year 2014)

Listing Exchange Mainboard of SGX-ST

Notes:(1) Projected yields excludes distributions to Sponsor, which has committed to waiving rights to distribution until Mar 31, 2014 in favor of holders of Common Units. Based on

unit price of S$ 0.775 as at 31 December 2013

Listed on 19 October 2012

4

Fortis and Religare Partnership

One of the largest healthcare chains in India growing multi vertical healthcare delivery system

– 65 healthcare delivery facilities

– Over 10,000 potential beds

– Presence in India, Mauritius, Sri Lanka, Singapore and Dubai

– Listed on the BSE and NSE

Part of Religare Enterprises, a diversified financial services firm listed on the BSE and NSE

Global multi-boutique asset management platform with over US$13.0 billion in Assets Under Management

RGAM AffiliatesInvestment mandate to

acquire healthcare assets across Asia, Australasia

and global emerging markets

Leveraging the Complementary Strengths and Expertise of Fortis and Religare

Unique Healthcare Offering

5

Fortis – An Overview

– Amongst the largest healthcare service providers in India with ~4,100(1) operational beds across 62 healthcare

facilities and total potential bed capacity of over 9,500(2) beds

– Leader in the organized diagnostics segment with 12 Reference Labs, over 245 network laboratories and a

footprint spanning over 5000 Collection points across 450 cities in India.

– Amongst the largest private diagnostic and imaging companies in Singapore

– A state of the art Greenfield specialty hospital for colorectal treatment in Singapore

International Business

6

Fortis – Specialty Revenue Split & Procedure Volume for FY 2013

Source: Fortis Healthcare website, results presentation slides

7

Overview of Religare Health Trust

Notes:(1) Independently valued by DTZ in INR as at March 31, 2013 based on S$1 = INR 43.75. Valuation of operating assets based on DCF and Hospital and

Medical Services Agreements (“HMSAs”) as relevant; valuation of greenfield assets based on Market Value.

Fortis Healthcare (“Sponsor”)

Institutional & Public Investors

Trustee-Manager

Current Portfolio

S$773m total valuation (1)

• 11 Clinical Establishments• 4 Greenfield Clinical

Establishments• 2 hospitals managed and

operated by RHT

Fortis Operating

Companies

28.0% 72.0%

OwnershipDistributions

Service Fee

Clinical Establishment

Services

TM Fees

Acts on behalf of unitholders and

provides management

services

HMSA Overview

15 year Hospital and Medical Services Agreements (“HMSA”) with Fortis over the Initial Portfolio, with extension of further 15 years on mutual agreement

Service Fee

Base Service Fee Fixed quarterly payments with 3%

escalation per annum Upward revision for any capex/

expansion

Variable Service Fee 7.5% of the Fortis Operating

Companies’ Operating Revenue for each quarter

Sponsor ROFR

Right of First Refusal (“ROFR”) over Sponsor’s medical and healthcare infrastructure located in Asia, Australasia and emerging markets in the rest of the world

RHT Structure

Singapore

India

8

Dr Virender SobtiChief Operating Officer

India

Experienced Board and Management Team Majority independent directors with proven track record in healthcare and funds management

Executive Directors / Management Religare Health Trust

Gurpreet Singh DhillonExecutive Director & CEO

Eng Meng LeongIndependent Director

Michael Hwang S.CIndependent Director

Peter Joseph Seymour RoweAudit & Risk Committee Chairman

Independent Director

Pawanpreet SinghExecutive Director & CFO

Tan Suan HuiHead of Compliance / IR

Dr. Yogendra Nath MathurLead Independent Director

Ravi MehrotraExecutive Chairman

9

Naveen BhatiaHead, Finance & Accounts

India

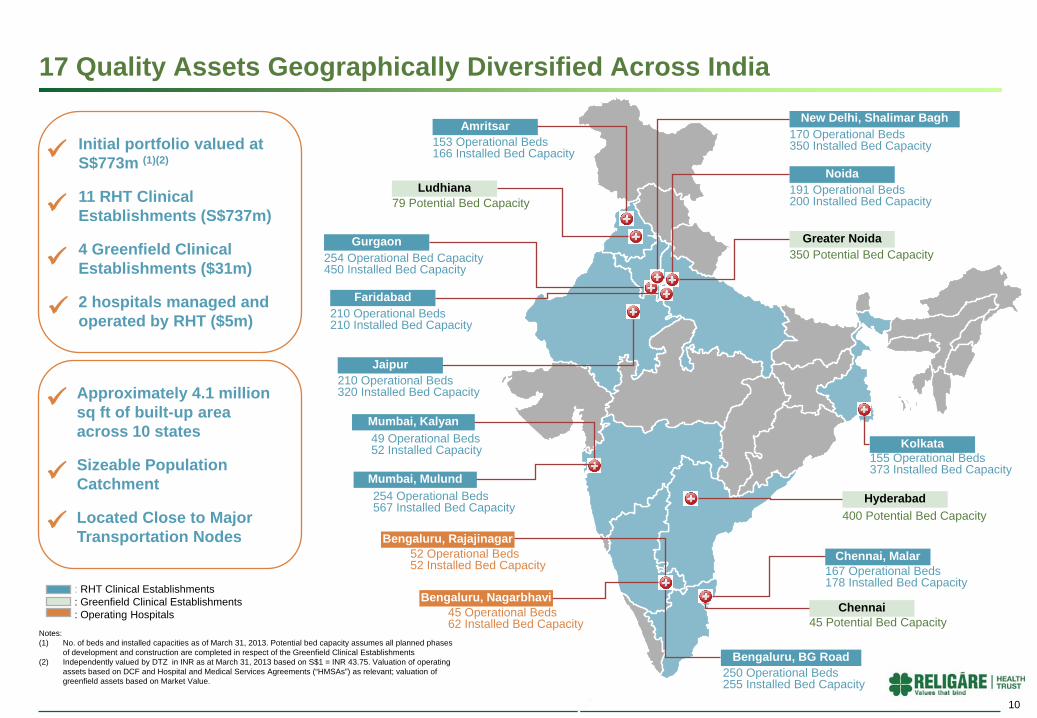

17 Quality Assets Geographically Diversified Across India

: RHT Clinical Establishments: Greenfield Clinical Establishments: Operating Hospitals

Notes:(1) No. of beds and installed capacities as of March 31, 2013. Potential bed capacity assumes all planned phases

of development and construction are completed in respect of the Greenfield Clinical Establishments (2) Independently valued by DTZ in INR as at March 31, 2013 based on S$1 = INR 43.75. Valuation of operating

assets based on DCF and Hospital and Medical Services Agreements (“HMSAs”) as relevant; valuation of greenfield assets based on Market Value.

Initial portfolio valued at S$773m (1)(2)

11 RHT Clinical Establishments (S$737m)

4 Greenfield Clinical Establishments ($31m)

2 hospitals managed and operated by RHT ($5m)

Approximately 4.1 million sq ft of built-up areaacross 10 states

Sizeable Population Catchment

Located Close to Major Transportation Nodes

400 Potential Bed Capacity

Amritsar

Ludhiana

153 Operational Beds166 Installed Bed Capacity

79 Potential Bed Capacity

Faridabad

Gurgaon

Jaipur210 Operational Beds320 Installed Bed Capacity

210 Operational Beds210 Installed Bed Capacity

254 Operational Bed Capacity450 Installed Bed Capacity

Mumbai, Mulund

Mumbai, Kalyan

254 Operational Beds567 Installed Bed Capacity

49 Operational Beds52 Installed Capacity

250 Operational Beds255 Installed Bed Capacity

Bengaluru, BG Road

Bengaluru, Nagarbhavi45 Operational Beds62 Installed Bed Capacity

Bengaluru, Rajajinagar52 Operational Beds52 Installed Bed Capacity

Chennai, Malar

Chennai

167 Operational Beds178 Installed Bed Capacity

45 Potential Bed Capacity

Hyderabad

Noida

Kolkata

New Delhi, Shalimar Bagh

155 Operational Beds373 Installed Bed Capacity

191 Operational Beds200 Installed Bed Capacity

170 Operational Beds350 Installed Bed Capacity

Greater Noida350 Potential Bed Capacity

10

Financial Highlights

Distributable income 4.2% higher compared to the last quarter and 4.9% higher than projected

DPU of 2.14 cents translates to an annualised yield of 11.0%

Tighter cost controls helped improve the operating margin

Hedging helps provide stability to Distribution

Both Current Yield and P/B are based on unit price of S$0.775 as at 31 December 2013

Figures for Current Yield and Projected Yield based on a total number of Common Units of 570,341,000 and results for the quarter ended 31 December 2013

P/B is based on NAV per unit of S$0.80 as of 31 December 2013

11.0%

10.5%

Current Yield Projected Yield (FY 2014)

YieldCurrent Yield Projected Yield (FY 2014)

Current Yield

(annualised) 11.0%

Gearing ratio, 7.9.%

P/B, 0.96

RHT

11DPU of 2.14 cents as against 2.04 cents projected, translating to a 11.0% annualised yield as against 10.5% projected

Continued growth in DPU

2

2.06

2.14

FY14 1Q 2Q 3Q

3%3.9%

12

DPU (Singapore Cents)

0.8

11,35211,719

12,210

1Q FY14 2Q 3Q

Distributable Income (S$ '000)

3.2%

Distributions are paid on a semi-annual basis for the six-month periods ending 31 March and 30 September of each year.

4.2%

Review of FY14 Quarter Comparisons

Actual FY14 3Q ActualFY14 2Q

ProjectedFY14 3Q

Total Revenue (S$ ‘000) 26,862 26,505 27,363

Net Service and Hospital Income (S$ ‘000) 15,843 15,394 16,529

Distributable Income (S$ ‘000) 12,210 11,719 11,651

*Exchange rate for actual FY14 YTD was S$ 1 = ₹ 48.19, Exchange rate for actual FY13 YTD was S$1 = ₹ 47.79. Exchange rate for projected FY14 YTD was S$1 = ₹ 46.7

13

Actual FY14 YTD Actual FY13 YTD ProjectedFY14 YTD

Total Revenue (S$ ‘000) 81,339 21,932 82,089

Net Service and Hospital Income (S$ ‘000) 47,492 13,892 49,591

Distributable Income (S$ ‘000) 35,281 9,394 34,956

^Actual FY14 3Q against Projected FY14 3Q

*Actual FY14 YTD against Projected FY14 YTD

^Exchange rate for actual FY14 3Q was S$ 1 = ₹ 49.62, Exchange rate for actual FY14 2Q was S$1 = ₹ 49.69. Exchange rate for projected FY14 3Q was S$1 = ₹ 46.7

Actual FY14 3Q ActualFY14 2Q

Variance (%)

Total Revenue (S$ ‘000) 26,862 26,505 1.3

Net Service and Hospital Income (S$ ‘000) 15,843 15,394 2.9

Distributable Income (S$ ‘000) 12,210 11,719 4.2

Actual FY14 3Q against Actual FY14 2Q

FY 14 3QActual

FY14 3Q Projection Variance

S$'000 S$'000 S$'000

Service fee 23,816 25,569 (1,753) Hospital income 1,800 1,311 489 Other income 1,246 483 763 Total revenue 26,862 27,363 (501)

Total service fee and hospital expenses (11,019) (10,834) (185)

Finance income 195 5 190 Finance expenses (647) (566) (81) Trustee-Manager fee (1,310) (1,217) (93) Other trust expenses (252) (368) 116 Foreign exchange gain 2,007 - 2,007 Total expenses (11,026) (12,980) 1,954

Profit before changes in fair value of financial derivatives 15,836 14,383 1,453

Fair value loss on financial derivatives (3,262) - (3,262) Profit Before Taxes 12,574 14,383 (1,809)

Taxes (5,026) (3,216) (1,810) Net Profit 7,548 11,167 (3,619)

Variance from Forecast Statement

For the quarter ended 31 December 2013

14

FY 14 3QActual

FY 14 3QProjection Variance

S$'000 S$'000 S$'000Net profit for the period attributable to unitholders of the Trust 7,548 11,167 (3,619)

Distribution Adjustments:Impact of non-cash Straight Lining (2,888) (3,079) 191 Technology Renewal Fee (151) (164) 13 Depreciation and Amortisation 3,282 2,794 488 Amortisation of debt arrangement fee 196 158 38 Trustee-Manager Fees payable in Units 656 608 48 Foreign exchange differences 1,764 - 1,764 Deferred Tax 1,803 167 1,636 Total distributable income attributable to the unitholders of the Trust 12,210 11,651 559

Variance from Forecast Statement

15

For the quarter ended 31 December 2013

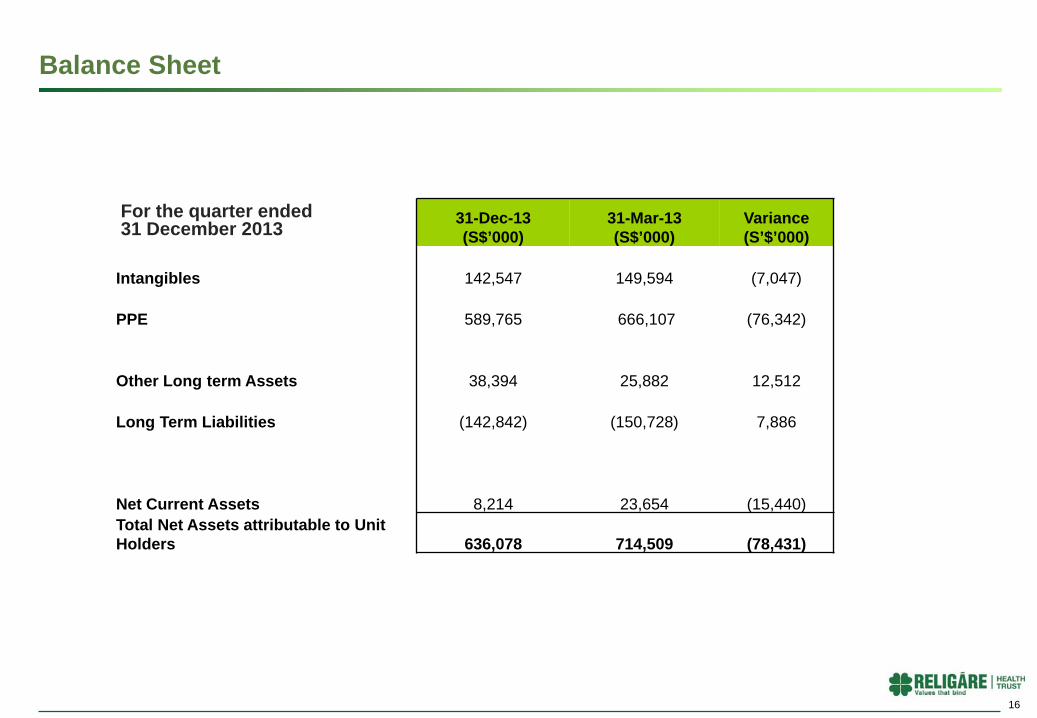

Balance Sheet

16

For the quarter ended 31 December 2013 31-Dec-13

(S$’000)31-Mar-13(S$’000)

Variance (S’$’000)

Intangibles 142,547 149,594 (7,047)

PPE 589,765 666,107 (76,342)

Other Long term Assets 38,394 25,882 12,512

Long Term Liabilities (142,842) (150,728) 7,886

Net Current Assets 8,214 23,654 (15,440)Total Net Assets attributable to Unit Holders 636,078 714,509 (78,431)

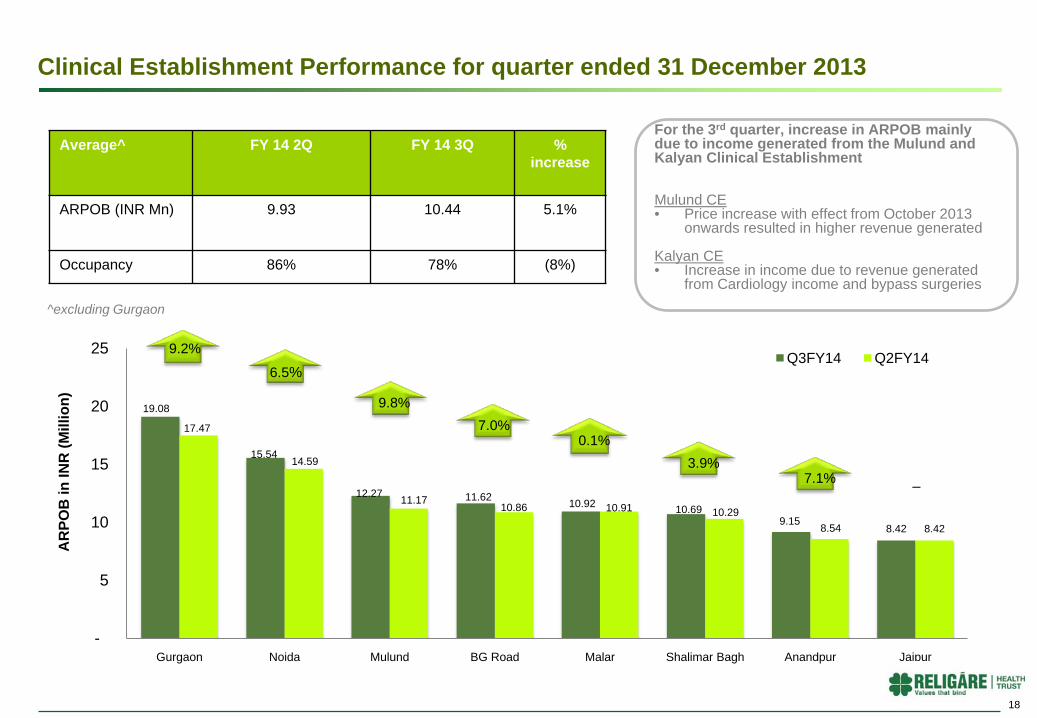

Portfolio

19.08

15.54

12.27 11.62 10.92 10.699.15

8.42

17.47

14.59

11.1710.86 10.91 10.29

8.54 8.42

-

5

10

15

20

25

Gurgaon Noida Mulund BG Road Malar Shalimar Bagh Anandpur Jaipur

AR

POB

in IN

R (M

illio

n)

Q3FY14 Q2FY149.2%

0.1%

6.5%

9.8%7.0%

3.9%7.1% –

Average^ FY 14 2Q FY 14 3Q % increase

ARPOB (INR Mn) 9.93 10.44 5.1%

Occupancy 86% 78% (8%)

^excluding Gurgaon

Clinical Establishment Performance for quarter ended 31 December 2013

18

For the 3rd quarter, increase in ARPOB mainly due to income generated from the Mulund and Kalyan Clinical Establishment

Mulund CE• Price increase with effect from October 2013

onwards resulted in higher revenue generated

Kalyan CE• Increase in income due to revenue generated

from Cardiology income and bypass surgeries

49%

79% 79%

83%

89%88%

84%

61%

254 254250

191210

170 155 167

450

567

255

200

320

350373

178

0

100

200

300

400

500

600

Gurgaon Mulund BG Road Noida Jaipur Shalimarbagh Anandpur Malar

Occupancy Operating Bed Capacity Installed Bed Capacity

Strong Portfolio Occupancy

Figures as of 31 December 2013

Occupancy for the period ended 31 December 201319

Current Portfolio for quarter ended 31 December 2013

20

Hospitals Operational Bed Capacity Installed Bed Capacity

Amritsar 153 166

Anandapur, Kolkata 155 373

BG Road, Bengaluru 250 255

Gurgaon 254 450

Faridabad 210 210

Jaipur 210 320

Kalyan, Mumbai 49 52

Malar, Chennai 167 178

Mulund, Mumbai 254 567

Nagarbhavi, Bengaluru 45 62

Noida 191 200

Rajajinagar, Bengaluru 52 52

Shalimar Bagh, New Delhi 170 350

Total 2,164 3,235

Development Project Status

Ground Breaking Ceremony held on 16 January 2014

21

Ludhiana BG Road

Estimated Time of Completion

2016 2016

No. of Beds Planned 79 200

Specialities Obstetrics & Gynaecology, IVF services, Cosmetology, Neonatology, Health Checks

Oncology, OT

Current Status Government approval process has been initiated and will take at least a month. Demolition work started on 6 January 2014 and will take 45 days to complete. Ground Breaking Ceremony was held on 16 January 2014

Revised layout designs see an increase of 200 in Bed Capacity. Government approvals will take at least 3 months for approval.

Hedging - Foreign currency exposure

Particulars Minimum Hedging (percentage to total exposure)

Semi-annual distributions 100% (on one year forward basis)

RHT has hedged the following foreign exchange exposures

Contracted rate SettlementINR 47.79 to SGD 1 15-May-14INR 53.36 to SGD 1 05-Dec-14

Forward contracts already entered

22

Ample Debt Headroom Post Acquisition

Gearing remains low with ample headroom for future growth opportunities

^Net of Cash (Based on audited financial statements of RHT Group as of 31 December 2013)

Actual^ (S$ millions)

54.7

Debt Headroom (without credit rating) to 40%

Current Gearing:

7.9%

Headroom of approximately

S$ 314.1 million

Debt Headroom (with credit rating) to 60%Headroom of

approximatelyS$843.3 million

23

About Mohali Clinical Establishment

Fortis Hospital, Mohali

Operator Fortis Healthcare Limited (“Fortis”)

Nature of Interest Freehold

Care Type Tertiary

Operational Bed Capacity(as of 31 December 2013)

298

Installed Bed Capacity(as of 31 December 2013)

355 (including new Oncology block)

Independent Valuationas at 31 December 2013

INR 2,867 million

Purchase Price^ S$ 58.1 million(₹2,850 million )

Breakdown of Purchase Price:

Sale Deed ConsiderationBusiness Transfer Agreement ConsiderationAsset Transfer Deed Consideration

₹2,700 million

₹38.8 million ₹111.5 million

Asset Overview

24

Investment Rationale

1. An internationally accredited hospital in a strategic location in North India

2. A hospital with a proven financial performance and strong operations

3. Enhanced Cashflow Stability 15 years agreement with a fixed base service fee component in addition to growth upside with variable fee

participation

4. Yield Accretive acquisition Positive impact on distributable income

25

More about MohaliOncology BlockOPD

CCU Patient Room

26

Historical Financial Performance (Q-o-Q)

Note: Figures for quarters ending March are not available as Fortis releases full year figures in March.

Figure for September 2012 and December 2012 were not publicly released by Fortis.

Revenue has been converted at SGD 1 = ₹49.62 as of 31 December 2013

Source: Results presentation slides from Fortis website

Average operating margin for the quarters above ~ 23.2%

0

2

4

6

8

10

12

14

16

18

20

Jun '09 Sep '09 Dec '09 Jun '10 Sep '10 Dec '10 Jun '11 Sep '11 Dec '11 Jun '12 Jun '13

Mohali Hospital Revenue (S$ million)

Revenue

27

Peer Analysis

Name Currency Last Price Open Close Change (%) Total Volume* Daily Average Volume*

Religare Health Trust SGD 0.775 0.795 0.775 (2.52) 97,840,000 1,553,016

First Real Estate Investment Trust SGD 1.06 1.11 1.06 (4.50) 58,314,000 925,619

Ascendas India Trust SGD 0.68 0.625 0.68 8.80 53,540,000 849,841

Parkway Life REIT SGD 2.35 2.32 2.35 1.29 21,987,000 349,000

Source: Miraqle

Figures as of 31 December 2013

Unit Price Performance

29

85%

90%

95%

100%

105%

110%

115%

01 Oct 13 10 Oct 13 22 Oct 13 31 Oct 13 11 Nov 13 20 Nov 13 29 Nov 13 10 Dec 13 19 Dec 13 31 Dec 13

RHT FTSE REIT STI AIT First REIT Plife REIT

RHT’s release of financial results for FY14

Comparative Analysis – Financial Analysis

Yield figures as at 13 January 2014 (OCBC Investment Research Weekly SREITs), Gearing figures are as announced by respective REIT/BT

RHT figures based on actual numbers, annualised yield and using share price of $0.775 as at 31 December 2013

P/B is based on NAV per unit of S$0.80 as of 31 December 2013

Figures for First Reit based on press release of their FY13 Q4 results released on 17 January 2014

7.9% 4.6% 7.0%11.0%

20%

33% 33%

7.9%

1.20

1.49

1.10

0.96

AIT Plife First Reit RHT

Yield Gearing ratio P/B

30

7.9% 7.6%

3.1% 2.9%

Actual Yr 2014 (annualised)

Projection Yr 2014

Financial Projection FY2014

Notes:(1) Exchange rate for annualised actual FY14 was S$ 1 = ₹ 49.62, Exchange rate for projected FY14 was S$1 = ₹ 46.7(2) Includes straight lining of Base Service Fee.(3) DPU calculated based on unit price of S$ 0.775 as at 31 December 2013(4) Annualised figures based on results for the quarter ended 31 December 2013

Revenue (1)(2)

(S$m)DPU Yield (3)

107.5109.4

Distributable Income (1)

(S$m)

11.0%

Gearing: 7.9%

Sponsor Waiver

4.7%

31

95.3

102.3

7.2

5.25

1.9

Actual Year 2014 (annualised)

Projection Year 2014

Service Fee Hospital Income Other Income

48.8

46.6

Actual Year 2014 (annualised)

Projection Year 2014

10.5%

Appendix

Awards & Accolades

Fortis Jaipur awarded ‘Six Sigma Healthcare Excellence Awards – 2013’ for Best Hospital in Patient Care, Best Hospital in Patient Safety and Best Hospital in Quality Initiatives.

Fortis Hospital, Anandpur has been ranked as No.2 Best Hospital in Multi-specialty category in Kolkata in a survey conducted by AC Nielson for The Week Magazine (Source: Fortis 3Q FY14 Presentation slides)

Fortis Hospital, Bannerghatta Road (BG Road), Bengaluru, has been ranked No. 4 on the 2013 World's Best Hospitals list for Medical Tourists. – The hospital has been recognised for the fourth consecutive year by the Medical Travel Quality Alliance

(MTQUA).

Fortis Healthcare Ltd has been conferred with the ‘Best Integrated Healthcare’ award for 2013 by Today’s Traveller.

33

Fortis – a stronger balance sheet Sale of international assets in 2013

Australia- Dental Corp for AUD 270 million

Vietnam- Hoan My Medical Medical Corp for US$80 million

Hong Kong- Quality Healthcare for US$355 million

Public Issue of Foreign Currency Convertible Bonds (FCCBs)

Issue of US$30 million listed on Singapore Exchange Ltd (SGX)

International Financial Corporation (IFC)

Invested a total of US$100 million through a mix of preferential allotment and FCCBs

Preferential Allotment of Equity Shares – Standard Chartered

3.7 million equity shares to Standard Chartered Pvt Equity Mauritius III (SCPE)

US$5.5 million raised

Gearing

Net Debt-to-Equity ratio stood at 0.2 (Dec’13) vs 0.6(Sep ‘13)1

1 Source: Fortis Q3 FY14 Presentation Slides

34

• 0.5% - 1.0% of acquisition price

• 0.5% of the sale price (Divestment to 3rd party)

• No divestment fee (Divestment to Sponsor)

Performance based management fees designed to align Management’s interests with Unitholders

Base fee Performance fee Acquisition / divestment fee

• 0.4% p.a. of the value of the Trust Property

• 50% to be paid in Units (1)• 4.5% p.a. of Distributable Income (2)

• 50% to be paid in Units (1)

• 2.0% of total development project costs• Payable in the form of cash and/ or units

Development fee Asset management fee

Fee Structure

• 1.0% of gross revenue• Paid quarterly in arrears• No asset management fee paid for assets

operated by Sponsor

Note (1) For the Forecast Year 2013 and Projection Year 2014(2) Distributable Income means the distributable amount determined by the Trustee-Manager in accordance with the terms of the Trust Deed

to be distributable for the relevant distribution period (pro-rated if applicable based on the number of months the relevant financial quarter bears to such distribution period) 35

Efficient Trust Structure

Note:(1) Promoters comprise Malvinder Mohan Singh, Shivinder Mohan Singh and their associates.

India Singapore

Acts on behalf ofUnitholders and provides

management servicesDistributions

Others New Unitholders Trustee-Manager

~19%~81%

Hospital and Medical Services Agreements(“HMSAs”)

Fortis Operating Companies

(“FOCs”) CCD Interest paymentsand dividends

Investments in CompulsoryConvertible Debentures

(“CCDs”) and equity shares

TM Fees

Distributions

100%

Hospital operatingcapabilities

Ownership of medical andhealthcare infrastructure facilities

Dividends 100%

28.0%

72.0%

Promoters (1)

Fortis Global Healthcare

InfrastructureService Fees

Clinical Establishment

Services Hospital Services

Companies (“HSCs”)

Fortis Health International Limited

(Mauritius)

100%

Dividends

36

Term of Agreement

15 years with option to extend by another 15 years by mutual consent

Primary Obligations of HSCos

Making available and maintaining the Clinical Establishments

Provision of outpatient services

Provision of radio diagnostic services

Primary Obligations of FOCs

Provision of healthcare services at the Clinical Establishments

Pay to HSCos the Services Fees and Commitment Deposits

Services Fee

Base Service Fee– Increased by 3% p.a.– Upward revision for any capex / expansion– Provision for capex to replace medical equipment

(“Technology Renewal Fee”) added to Base Fee (2)

– HSCos entitled to request for an advance of up to 60% of the Base Service Fee

Variable Service Fee– 7.5% of the operating income of the FOC

Commitment Deposits

FOC to pay to HSCo 25% of cost for expansions of capacity / modification of Fortis Hospitals as an interest free refundable commitment deposit

Income Secured Through Long Term Working Agreements

Mechanics of the HMSA Key Terms of the HMSA

Services Fees

Fortis OperatingCompany

Clinical Establishment

Operated by

Hospital Services Company

Ownership

Services

B

AC

Ancillary Services

Ownership Earnings

Commitment Deposits

D+

Public

Source: TMNotes:(1) Fortis has signed commitment agreements to enter into similar HMSAs for the greenfield healthcare infrastructure assets.(2) Technology Renewal Fee will be paid into a Technology Renewal Fund to be maintained by Fortis.

A

B

C

D

Prior to listing, the Hospital Services Companies (“HSCos”) will enter into Hospital and Medical Services Agreements (“HMSAs”) with the Fortis Operating Companies (“FOCs” ) to operate the healthcare infrastructure assets (1).

37

Thank You

38