religare corporate presentation · 3 sunil godhwani, cmd – religare enterprises (joined religare...

TRANSCRIPT

Religare Enterprises Limited Corporate Overview

June 2016

Leading financial services platform

Religare Enterprises Limited (REL) through its

subsidiaries has established itself in some of the

most promising verticals within Financial Services,

viz. Lending, Health Insurance and Capital Markets

Nationwide distribution footprint

Subsidiaries service over 1.14 mn. clients from

over 1,450 locations with more than 7,200

employees

Professional management team

Stable team with average senior management

tenure of ~7 years and experience of ~18 years

Key Financials (as at/quarter ended 31-Mar-2016)

Net worth: ₹3,863 cr. (USD 584 mn.)

Total assets: ₹27,429 cr. (USD 4.15bn.)

Total revenues: ₹4,503 cr. (USD 689 mn.)

Pre-exceptional PAT: ₹225 cr. (USD 34.5 mn.)

Market information

Listed on NSE and BSE: market capitalization of

₹5,109 cr. (~USD 773 mn.) as of 31-Mar-2016

Religare Overview Religare is focused on the most promising opportunities in the financial services space in India

1

Business Lines Religare Snapshot

Note: REL has exited the India Asset Management business in April 2016 and is in the process of exiting the Global Asset Management business

Lending

Leading SME-focused NBFC with deep domain knowledge

SMEs are constrained by lack of funding; the gap presents a lucrative opportunity for specialist financiers

Tapping the growing opportunity in lending for affordable housing

Capital Markets

Large retail broking platform, open architecture wealth management platform a and mid-market focused

institutional equities and investment banking platform

Immense opportunity from structurally high savings and low penetration of financial assets; equities in particular to benefit

Health Insurance

One of five standalone health insurers in India

Low insurance density; health insurance in particular growing rapidly due to rising cost of healthcare and disproportionate share of out-of-

pocket expenditure

Each of the verticals has attained critical scale and is proposed to be independently listed on the stock exchanges in order to sharpen focus on the individual businesses,

simplify structure and unlock value for stakeholders

Proposed Independent Listing of Verticals REL proposes to simplify its corporate by reorganizing itself into three independently listed companies

2

# Certain segments of the Capital Markets business are separately regulated and therefore operated through different legal entities

Current Structure

Religare Enterprises Limited

Proposed Structure (Indicative)

Shareholders

Religare Finvest Limited

Religare Housing Development Finance Corporation Limited

Religare Securities Limited

Operating Subsidiaries#

Lending Health Insurance Capital Markets

Shareholders

Housing Finance Operating Subsidiaries#

Len

din

g

• All stakeholders are likely to benefit from the simplification of structure

Each business able to define growth strategy independently; direct

management accountability for accomplishment of strategic objectives

Increased customer focus as each business will operate in one segment

Greater shareholder choice as shareholders will be able to participate to

different extents in different businesses

• REL’s Board has appointed a Management Committee to examine and

evaluate all aspects of the plan; the Committee will drive the preparation of a

detailed scheme of arrangement

• The plan is subject to final approval by the Board, shareholders, regulators and

judicial authorities

Highlights of the Proposed Reorganization

Ca

pit

al

Ma

rket

s

↑ Listed

↓ Unlisted

Religare Health Insurance Company Limited

Hea

lth

In

sura

nce

3

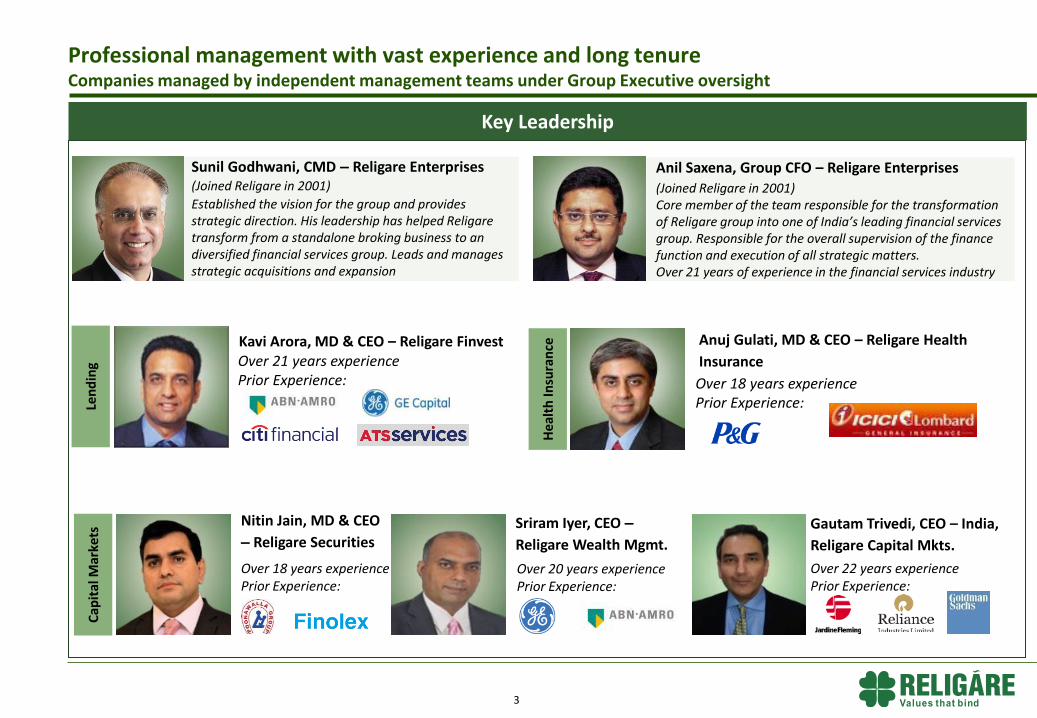

Sunil Godhwani, CMD – Religare Enterprises (Joined Religare in 2001)

Established the vision for the group and provides strategic direction. His leadership has helped Religare transform from a standalone broking business to an diversified financial services group. Leads and manages strategic acquisitions and expansion

Anil Saxena, Group CFO – Religare Enterprises

(Joined Religare in 2001) Core member of the team responsible for the transformation of Religare group into one of India’s leading financial services group. Responsible for the overall supervision of the finance function and execution of all strategic matters. Over 21 years of experience in the financial services industry

Professional management with vast experience and long tenure Companies managed by independent management teams under Group Executive oversight

Len

din

g C

apit

al M

arke

ts

Hea

lth

Insu

ran

ce

Kavi Arora, MD & CEO – Religare Finvest Over 21 years experience Prior Experience:

Anuj Gulati, MD & CEO – Religare Health

Insurance

Over 18 years experience Prior Experience:

Nitin Jain, MD & CEO

– Religare Securities

Over 18 years experience Prior Experience:

Sriram Iyer, CEO –

Religare Wealth Mgmt.

Over 20 years experience Prior Experience:

Gautam Trivedi, CEO – India,

Religare Capital Mkts.

Over 22 years experience Prior Experience:

Key Leadership

4

Robust platform in place to capture opportunities in financial services Multi-product manufacturing capabilities and distribution network

All data as at/for the quarter ended 31-Mar-2016

Lending

SME-focused Lending • Balance sheet size of ₹21,049 cr. (USD 3.18 bn.)

• High quality portfolio: net NPA of 2.31% (90-day basis)

• Capital adequacy (CRAR) of 16.7%

Affordable Housing Finance

• Loan book of ₹829 cr. (USD 126 mn.)

Capital Markets

Retail Broking Distribution across more than 440 cities, 1,320

locations and catering to over 1.14 mn. clients

Wealth Management Advisory-led open architecture platform

Institutional Equities and Investment Banking India institutional research team covers 155 stocks

Empanelled with more than 450 clients globally

Health Insurance

Health Insurance Leveraging group’s healthcare assets

GWP of ₹161 cr. (USD ~24 mn.); QOQ growth of 43%

4,869 hospitals in provider network

Multi-channel distribution including significant online

presence

Religare is poised to capture the buoyancy in Financial Services Financial Services highly correlated to economic growth and will gain from India’s superior growth trajectory

5

Leading financial services

platform with presence

across three verticals

Focus on servicing entire

customer spectrum

Judicious mix of balance

sheet-led and fee-based

businesses

Capital Markets Channelising risk capital to the markets

Retail and Mass Retail Higher savings from rising incomes

HNIs Allocating growing wealth across asset classes

Lending Providing debt capital to power growth of SMEs and affordable housing

Relig

are

Op

era

tin

g B

usin

esses

Targ

et C

usto

mer S

eg

men

ts

Health Insurance Protection for individuals, SMEs

Financial Institutions Capital flows tracking superior returns

SME & Mid-corporates Debt financing, equity raise, M&A, ECM

Financial Services businesses are highly correlated with economic growth; at India’s current stage of development, Financial Services is likely to grow at a multiple of the broader economy, unlocking the structural potential across the spectrum

The Indian economy is the fastest growing large economy; set to sustain world leadership in GDP growth rate

Key Businesses

Overview

Lending Business Overview

One of India’s largest Non-Banking

Financial Companies,

focusing on the SME segment

Business Highlights

Improve ROE

Grow Book Size

Ensure High Quality Portfolio

Strategic Priorities

8% 62%

Offerings

NBFC Balance Sheet of

₹21,049 cr. (USD 3.18 bn.)

Affordable Housing Finance book of

₹829 cr. (USD 126 mn.)

(as of 31-Mar-2016)

SME Lending

Capital Market

Lending

Affordable Housing Finance

7

Recognition CIBIL ‘Fast and

Upcoming’ Data Quality

Award - 2016

8

Non-Performing Assets§

Growth capital provider focused

on fast-growing SME segment

• The sector contributes 17%

to India’s GDP, 45% to

manufacturing output and

40% to the total value of

exports

Strong performance across credit

and operating benchmarks

• Secured asset finance

portfolio over 83%

• Net NPA of 2.31% on 90-day

basis and 1.77% on 150-day

basis as at 31-Mar-2016

Significant headroom for

operating leverage through

tested management strength,

processes and systems

Winner of ‘The Most Innovative

Risk Management Strategy’ at the

ERM Leadership Summit and

CIBIL ‘Fast and Upcoming’ Data

Quality Award

Key highlights Continued traction in SME-Secured segment: book size up 29% YOY

12.6

64.6

20.9

13.5

66.1

22.3 23.5

66.2

15.0

23.2

58.7

14.4

21.6

51.8

17.6

Religare Finvest SME-Secured drives growth in book size

(₹ cr.)

*Net of portfolio assigned to other lenders § NPAs are recognised at 90 days since Oct 2011 whereas regulations require transitioning from 180-day NPA recognition to 90-day recognition by 31-Mar-2018

285076118150

31-Mar-16

16,313

1,080

13,259

1,946

31-Dec-15

15,536

1,092

12,698

1,696

30-Sep-15

14,631

1,169

11,966

1,420

30-Jun-15

13,890

1,425

11,121

1,226

31-Mar-15

13,274

1,762

10,250

1,112

Capital Market Lending

SME-Secured*

Others

SME-Unsecured*

3.07%

3.49%

2.95%2.86%

2.24%

2.31%

2.78%

2.29%2.21%

1.69%

2.44%

1.77%

2.17%

1.65% 1.64%1.46%

1.19%

31-Dec-15 30-Sep-15

1.99%

30-Jun-15 31-Mar-15

1.19%

1.63%

31-Mar-16

NNPA 90 dpd

GNPA 90 dpd

NNPA 180 dpd

GNPA 180 dpd

NNPA 150 dpd

GNPA 150 dpd

Borrowing programme supported by superior ratings

NIM and Opex to ANR

4.23%4.13%4.54%

4.74%4.59%

2.06%2.42%2.37%

2.19%2.47%

Q4FY16 Q3FY16 Q2FY16 Q1FY16 Q4FY15

Opex/ ANR NIM

Additionally obtained Long Term rating of ‘CARE AA-’ for ₹1,400 mn. [~USD 212 mn]

Rating Type Rating Agency Amount

₹ cr. USD mn.

Commercial Paper [ICRA] A1+ ICRA 2,700 408 ST Debt [ICRA] A1+ ICRA 1,000 151 ST Bank Loans [ICRA] A1+ ICRA 600 91 LT Debt [ICRA] AA- (stable) ICRA 3,400 514 LT Bank Loans [ICRA] AA- (stable) ICRA 11,400 1,725 Market-Linked Deb. ICRA pp-MLD AA- ICRA 100 15 Tier-2 Sub. Debt IND AA- (stable) Ind-Ra 750 113 Commercial Paper IND A1+ Ind-Ra 3,000 454 ST Bank Loans IND A1+ Ind-Ra 3,000 454 LT Debt IND AA - (stable) Ind-Ra 3,000 454 LT Bank Loans IND AA - (stable) Ind-Ra 10,000 1,513

2.2 2.1 2.2 2.2 2.47 (USD bn.)

9

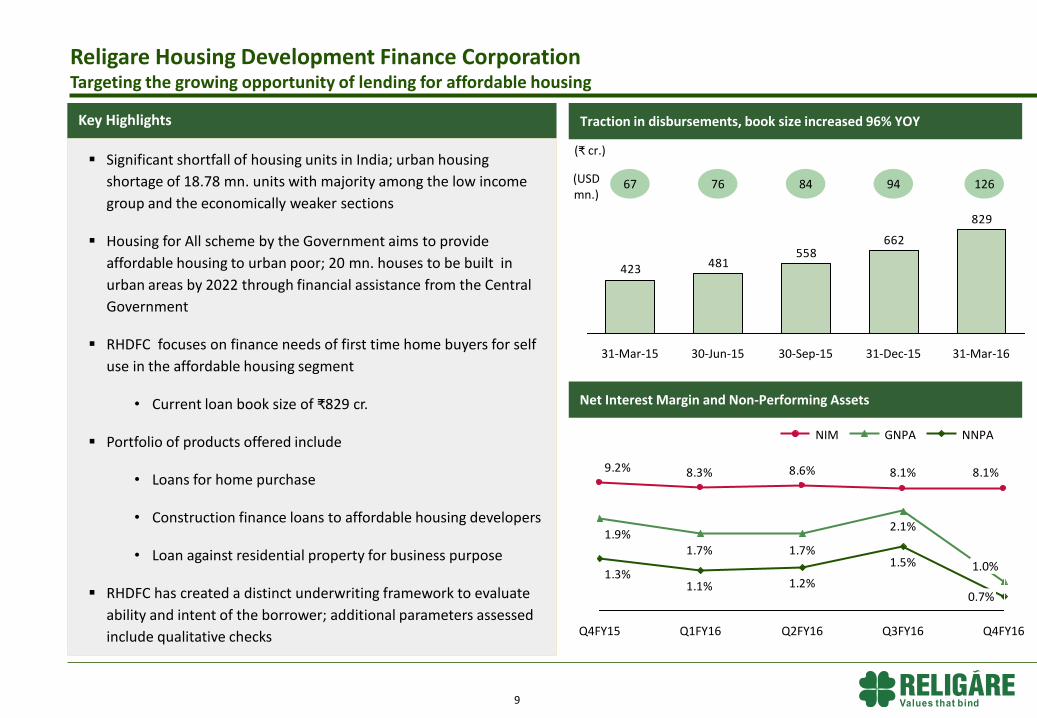

Traction in disbursements, book size increased 96% YOY

12.6

64.6

20.9

Religare Housing Development Finance Corporation Targeting the growing opportunity of lending for affordable housing

829

662558

481423

31-Mar-16 30-Jun-15 30-Sep-15 31-Dec-15 31-Mar-15

Net Interest Margin and Non-Performing Assets

2.1%

1.7%1.7%1.9%

1.5%

1.1%1.3%

1.2%

8.1%8.1%8.6%9.2% 8.3%

Q2FY16 Q3FY16

1.0%

Q4FY16

0.7%

Q1FY16 Q4FY15

Significant shortfall of housing units in India; urban housing

shortage of 18.78 mn. units with majority among the low income

group and the economically weaker sections

Housing for All scheme by the Government aims to provide

affordable housing to urban poor; 20 mn. houses to be built in

urban areas by 2022 through financial assistance from the Central

Government

RHDFC focuses on finance needs of first time home buyers for self

use in the affordable housing segment

• Current loan book size of ₹829 cr.

Portfolio of products offered include

• Loans for home purchase

• Construction finance loans to affordable housing developers

• Loan against residential property for business purpose

RHDFC has created a distinct underwriting framework to evaluate

ability and intent of the borrower; additional parameters assessed

include qualitative checks

Key Highlights

(₹ cr.)

67 (USD mn.)

76 84 94 126

NNPA GNPA NIM

10

Health Insurance Business Overview

Positioned to capture

significant Group Synergies

Retail & Group Health Plans

Retail & Group Accident Plans

International Travel Plan

GWP of

₹503 cr. (USD 77 mn.) in

FY16

4,869 hospitals in

provider network

(as of 31-Mar-2016)

Grow GWP with

efficient use of

Capital

‘FICCI Healthcare

Excellence Award –

2015’

Recognition

Business Highlights

Strategic Priorities

Offerings

11

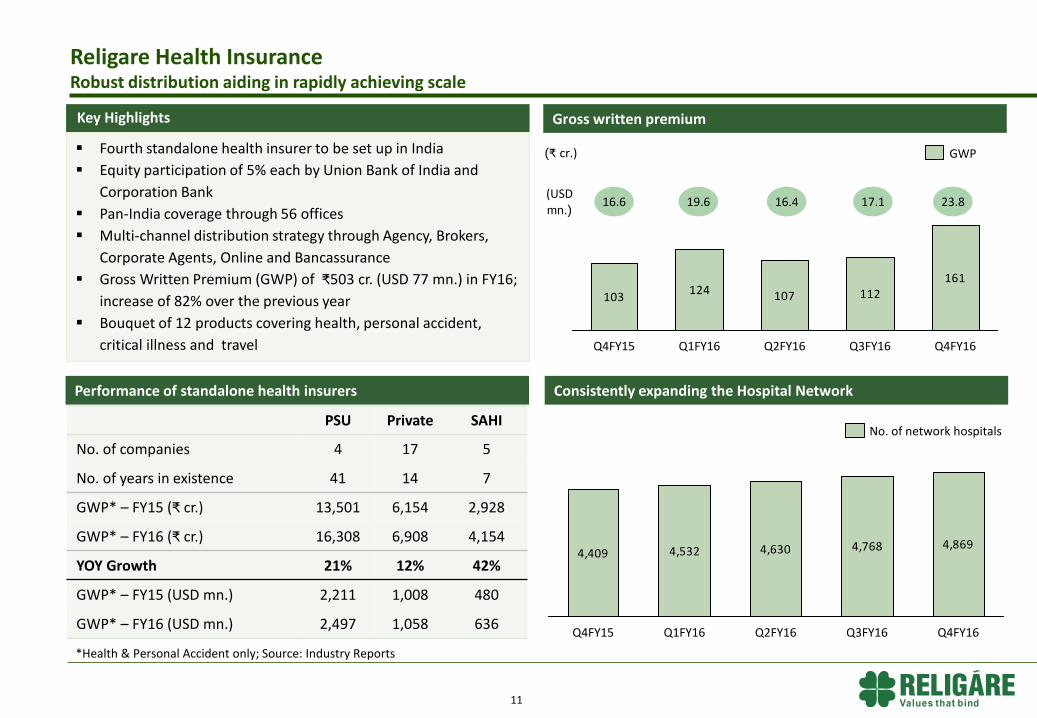

Performance of standalone health insurers

Religare Health Insurance Robust distribution aiding in rapidly achieving scale

Key Highlights

Fourth standalone health insurer to be set up in India

Equity participation of 5% each by Union Bank of India and

Corporation Bank

Pan-India coverage through 56 offices

Multi-channel distribution strategy through Agency, Brokers,

Corporate Agents, Online and Bancassurance

Gross Written Premium (GWP) of ₹503 cr. (USD 77 mn.) in FY16;

increase of 82% over the previous year

Bouquet of 12 products covering health, personal accident,

critical illness and travel

Gross written premium

Consistently expanding the Hospital Network

103124 107 112

161

Q2FY16 Q3FY16 Q4FY16 Q4FY15 Q1FY16

GWP

4,409 4,532 4,630 4,768 4,869

Q4FY16 Q1FY16 Q4FY15 Q2FY16 Q3FY16

No. of network hospitals PSU Private SAHI

No. of companies 4 17 5

No. of years in existence 41 14 7

GWP* – FY15 (₹ cr.) 13,501 6,154 2,928

GWP* – FY16 (₹ cr.) 16,308 6,908 4,154

YOY Growth 21% 12% 42%

GWP* – FY15 (USD mn.) 2,211 1,008 480

GWP* – FY16 (USD mn.) 2,497 1,058 636

(₹ cr.)

16.4 16.6 19.6 17.1 23.8 (USD

mn.)

*Health & Personal Accident only; Source: Industry Reports

12

Capital Markets Business Overview

A formidable capital markets platform with

extensive distribution capabilities

1.14 mn. Retail

Broking clients

Wealth Mgmt. AUM ₹4,055 cr. (USD

613 mn.) 155 stocks under

Research coverage

(q.e. 31-Mar-2016)

Retail Broking

Wealth Mgmt

Institutional Equities and

Investment Banking

Generate Superior

ROE

Attain Sustainable Profitability

Business Highlights

Strategic Priorities

Offerings Recognition

“Leveraging Digital and Technology for Business Growth”

Award at the Skoch BSE Award For

Aspiring India 2015

13

• One of India’s largest retail broking

networks

• Asset light broking model to

enhance efficiency

• Growing use of online and mobile

platforms by customers

• Focus on compliance adherence

and improvement in customer

service and experience

• Pricing standardized to improve

yields in the equities and

commodities segments

• Steady growth in equities and

commodities broking clients –

total client base of over 1.14

million

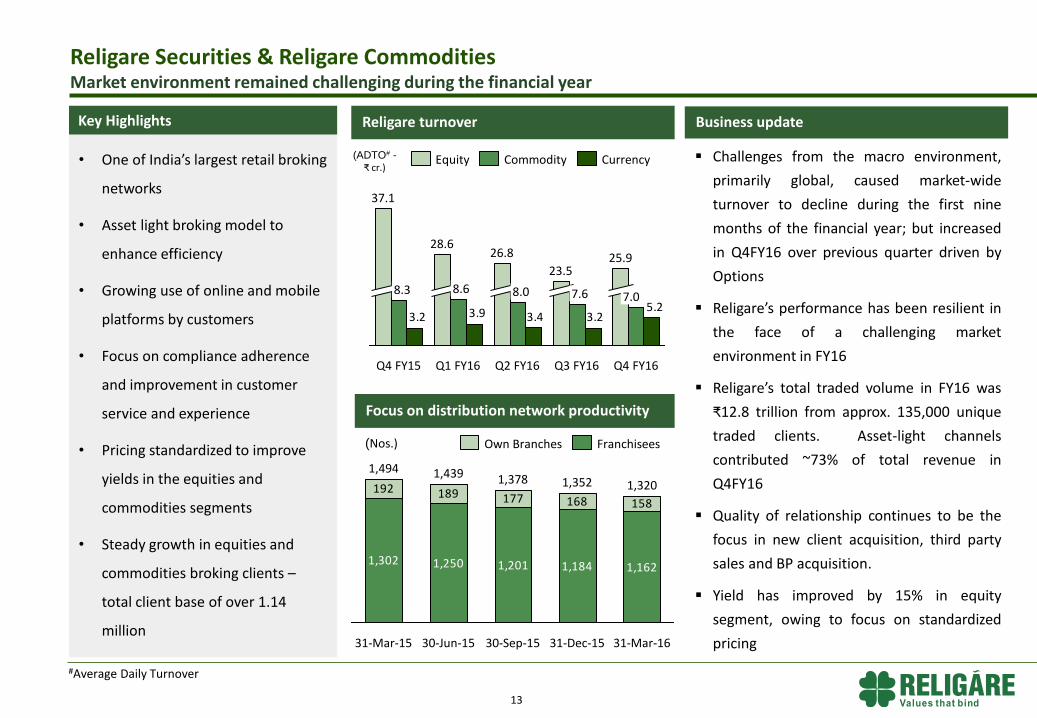

Key Highlights Religare turnover

Religare Securities & Religare Commodities Market environment remained challenging during the financial year

333

935

292

995

313

1,015

260

940

270

950

(ADTO# - ₹ cr.)

Focus on distribution network productivity

(Nos.)

Business update

#Average Daily Turnover

1,302 1,250 1,201 1,184 1,162

192 189 177 168 158

31-Mar-16

1,320

31-Dec-15

1,352

30-Sep-15

1,378

30-Jun-15

1,439

31-Mar-15

1,494

Franchisees Own Branches

Challenges from the macro environment,

primarily global, caused market-wide

turnover to decline during the first nine

months of the financial year; but increased

in Q4FY16 over previous quarter driven by

Options

Religare’s performance has been resilient in

the face of a challenging market

environment in FY16

Religare’s total traded volume in FY16 was

₹12.8 trillion from approx. 135,000 unique

traded clients. Asset-light channels

contributed ~73% of total revenue in

Q4FY16

Quality of relationship continues to be the

focus in new client acquisition, third party

sales and BP acquisition.

Yield has improved by 15% in equity

segment, owing to focus on standardized

pricing

5.23.23.43.93.2

Q4 FY16

7.0

25.9

Q3 FY16

7.6

23.5

Q2 FY16

8.0

26.8

Q1 FY16

8.6

28.6

Q4 FY15

8.3

37.1

Currency Equity Commodity

14

Key value proposition of

‘Simplified Wealth Solutions’ for

the customers

Seen as trusted advisors to

clients, enabled by our tripod

delivery model

Active advisory calls helping

clients position portfolios to gain

from high-impact events

Expanding product solutions to

enhance ability to win clients

across the group

Size and scale aligned to market

Focus on Relationship Manager

productivity

Key Highlights Client Base

Relationship Manager productivity Business update

4,492

4,972

4,687 4,662 4,631

₹ cr.

AUM

Religare Wealth Management Differentiating through a focused idea-driven approach

Inflows into Equity PMS schemes has become

one of the key contributors to the business,

with significant traction also having been built

up in Structured Products and Real Estate

backed high-yielding NCDs

Incrementally equity MF sales have declined

given the mood in the market. All the same,

trail income contribution to revenue has

improved significantly as an outcome of the

focus on building an annuity book

(₹ cr.)

3,945 4,029 4,008 4,0554,400

31-Mar-15 31-Mar-16 31-Dec-15 30-Sep-15 30-Jun-15

Total AUM

703 (USD mn.) 620 609 606 613

16.0 (USD mn.)

13.5 12.2 13.2 12.7

848781

86100

31-Mar-16 31-Dec-15 30-Sep-15 30-Jun-15 31-Mar-15

4,5144,4774,5074,5234,549

30-Sep-15 31-Mar-16 31-Dec-15 30-Jun-15 31-Mar-15

No. of Clients

Jan 2016 ₹120 cr.

Mar 2016 ₹118 cr.

Jan 2016 ₹250 cr.

Religare Capital Markets Poised to capitalise on multi-decade growth story in India

• Mid-market focused institutional equities and

investment banking platform

• Investment Banking platform offers life-cycle

investment banking services i.e. growth capital raise to

IPO to QIP to Block placements

• Closed calendar year 2015 as the No. 2 QIP manager in

India for transactions of more than USD 10 mn.

(excluding transactions for BFSI companies)

• Equity transactions of size aggregating to ₹940 cr. (USD

144 mn.) successfully executed during FY16

• Syndicated multiple debt issues aggregating to ₹440 cr.

(USD 67 mn.) during FY16

• 20 analysts in India’s Institutional Research team cover

155 stocks

• Equities businesses serve 452 clients globally with

differentiated research

Key Highlights

15

Select deals completed during FY2016

Block

Sole Placement Agent

Debt Syndication

Arranger

Aug 2015 ₹235 cr.

Open Offer

Lead Manager

Block

Sole Placement Agent

Crompton Greaves

Differentiating through original, on-the-ground research

Financial Services Opportunity in India

17

SMEs constitute a large contributor to national output and exports

SME Lending

Share of SMEs in India’s manufacturing

output

40%

Share of SMEs in India’s total exports

Source: CRISIL

Credit flow to the sector has improved in recent years as the potential of the sector is better understood

45%

6,8405,2804,860

3,6602,5802,160

1,260

2013 2009 2012 2011 2007 2008 2010

+33%

24.0% 16.5% Share of SMEs in banks’ industry and services portfolio

Outstanding SME credit as % of total outstanding bank credit

The SME sector is one of the largest generators of employment in India, employing 73 million people. The sector has been observed to outpace GDP growth in years of high growth.

However, providing credit to the sector commensurate with its contribution to national output is too daunting a task for banks

Bank credit to SMEs (₹ billion)

SMEs are the backbone of India’s economy but are constrained by lack of funding; specialist NBFCs with deep understanding of the workings of SMEs are crucial for bridging the gap

Gap in funding for SMEs presents a lucrative opportunity for specialist financiers

Health Insurance is on a high growth trajectory

18

532

33027824714589665428

DE KR BR IN ZA RU JP US

1,259

CN UK

xx% GWP as % of GDP Total premium (USD bn.)

1% 15% 4% 12% 7% 3% 12% 11% 8% 4%

Out-of-Pocket as % of Total Healthcare Expenditure

59%

35%35%31%

11%9%

CN IN RU BR US UK

Healthcare spend as a % of GDP

Source: Reserve Bank of India, World Bank, Economist Intelligence Unit, India Brand Equity Foundation, Karvy, Industry reports, Swiss Re, IRDAI SG=Singapore, MY=Malaysia, KR=S. Korea, JP= Japan, TH=Thailand, IN=India, ID=Indonesia, CN=China, RU=Russia, ZA=South Africa, DE=Germany, UK=United Kingdom, US= United States

Non-life insurance penetration in India is a mere 0.7% and Health Insurance is growing rapidly as healthcare costs are spiraling and share of out-of-pocket expense is among the highest

Health Insurance

17.90%

9.40%9.30%

6.30%5.40%

4.00%

RU CN IN US BR UK

248204

176153132

1128466513222

27%

FY08 FY07 FY06 FY09 FY16 FY15 FY14 FY13 FY12 FY11 FY10

Health Insurance GWP (₹ bn.)

Source: Reserve Bank of India, World Bank, Economist Intelligence Unit, India Brand Equity Foundation, Karvy, Industry reports Market Capitalization for US is of NYSE and for China of Shanghai Stock Exchange; Cash Trading velocity is defined as annual cash turnover divided by market capitalisation; Data for 31-Dec-2013 for all countries except India which is for 31-Mar-2014 SG=Singapore, MY=Malaysia, KR=S. Korea, JP= Japan, TH=Thailand, IN=India, ID=Indonesia, CN=China;

Surge in wealth and reallocation across asset classes to revive interest in Equities

19

274061

929395

160

252

MY SG CN ID IN TH JP KR

Market cap*/GDP (%)

32.254.6

25.3

45.5

24.3

63.7

0.90.49.13.5

5.2

43.2

18.9

228.4

109.9

2013

11.4

2018E

Provident Fund

Others

Mutual Funds

Small Savings/Cash

Insurance

Bank Deposits/ Bonds

Equity Distribution of individual wealth in India invested in financial assets (₹ trillion)

Capital Markets

38% xx% Cash Trading Velocity

Wealth Management

10%

39%17%26%

35%73%

59%

26%

15%

US Asia-Pacific India

51–65

Over 65

Under 50

177

94

2020E 2015E

+89% Total wealth of Ultra High Net Worth Individuals in India (₹ trillion)

Distribution of Ultra High Net Worth Individuals by Age Group

+162%

30%

104% 143% 106% 45% 33% 304%

Equity-related businesses to benefit from tailwinds as India is under-penetrated c.f. regional peers and a

correction to under-ownership of equities is imminent

Total wealth of UHNIs set to grow nearly 90% in 5 years; younger UHNI age profile provides opportunity to

innovate and make intense use of technology

Religare Enterprises Limited

A - 3,4,5, GYS Global, Sector - 125, Noida, U.P. – 201301, India