relevance of securitisation for urban ccoo- … seminar-securitisation... · whether a cowhether a...

TRANSCRIPT

RELEVANCE OF RELEVANCE OF SECURITISATION FOR URBAN SECURITISATION FOR URBAN COCO--OPERATIVE BANKSOPERATIVE BANKS

PRESENTED BY

CA. Prafulla Chhajed

9821090612

What is UCB?What is UCB?

� Urban Co-operative Bank is a business organization owned and operated by a group of individuals for their mutual group of individuals for their mutual benefit.

� It refers to primary cooperative banks located in urban and semi-urban areas

SARFESI ACT,2002SARFESI ACT,2002

� The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 allows banks and financial institutions to auction properties (residential and commercial) when borrowers fail to repay their loans without when borrowers fail to repay their loans without intervention of the court.

� It enables banks to reduce their non-performing assets (NPAs) by adopting measures for recovery or reconstruction.

UCB VS SARFESI ACT…..UCB VS SARFESI ACT…..

Whether a coWhether a co--operative bank is a operative bank is a Securitisation Creditor? Securitisation Creditor?

Co-operative Banks fall within the definitionof “secured creditor” under SARFESI Act by virtueof “secured creditor” under SARFESI Act by virtueof the definition contained in section 2(1)(c )(v) ofthe Act in view of the notification No. SO.105(E)dated 28th January, 2003 of the CentralGovernment declaring “Co-operative Bank” asdefined in clause (cci) of section 5 of BankingRegulation Act, 1949 to be a bank for the purposesof SARFAESI.

JUDGMENTJUDGMENT…..…..

CASE NO.:Appeal (civil) 432 of 2004

PETITIONER:Greater Bombay Co-op. Bank LtdGreater Bombay Co-op. Bank Ltd

RESPONDENT:M/s United Yarn Tex. Pvt. Ltd. & Ors

DATE OF JUDGMENT: 04/04/2007

In the judgment of the Greater Bombay Cooperative Bank Ltd. v. United Yarn Tex. Pvt. Ltd. and Ors. 2007 AIR SCW 232 the Apex court has also ruled that SARFAESI Apex court has also ruled that SARFAESI shall apply to the co-operative banks.

NonNon-- Performing Assets (NPA)Performing Assets (NPA)

What is an NPA?

NPA would be a loan or an advance where in –i. Interest and/ or installment of principal remain

overdue for a period of more than 90 days in respect of term loan.overdue for a period of more than 90 days in respect of term loan.

ii. Account remains “out of order” for a period of more than 90 days in respect of overdraft/ cash credit.

iii. The bill remains overdue for a period of more than 90 days in the case of bills purchased and discounted.

Methods for Recovery of NPAsMethods for Recovery of NPAs

A. Asset Reconstruction

B. Action u/s 91 &101 of Maharashtra State Co-operative Societies Act,1960

C. SecuritisationC. Securitisation

A. A. Asset ReconstructionAsset Reconstruction

� Origination occurs from a bank or financial institution; and

� The mindset and the approach is for � The mindset and the approach is for asset reconstruction (as opposed to regular Securitisation).

B. Action u/s 91B. Action u/s 91

� Approach to Co-operative Court

- Question related Interpretation of law

- Queries related to documents

� Regular court proceedings� Regular court proceedings

� After judgment, appeal can be made to Co-operative Appellate Court and further appeal to High Court.

Action u/s101

� It is a “Summary Suit”.

� It is fastest procedure

� Dispute has to be against a member only.

� On acceptance of the liability by � On acceptance of the liability by borrower , immediate award is given

C. SecuritisationC. Securitisation

� In respect of banks, a part of their loanportfolio can be packed together and off-loaded in the form the debt instruments(called pass-through certificate, SecurityReceipts) to the prospective investors withReceipts) to the prospective investors withthe provision that the inflow of cash in theform of recoveries shall be distributedamongst the investors.

� This allows the securitizing bank to get fundsupfront.

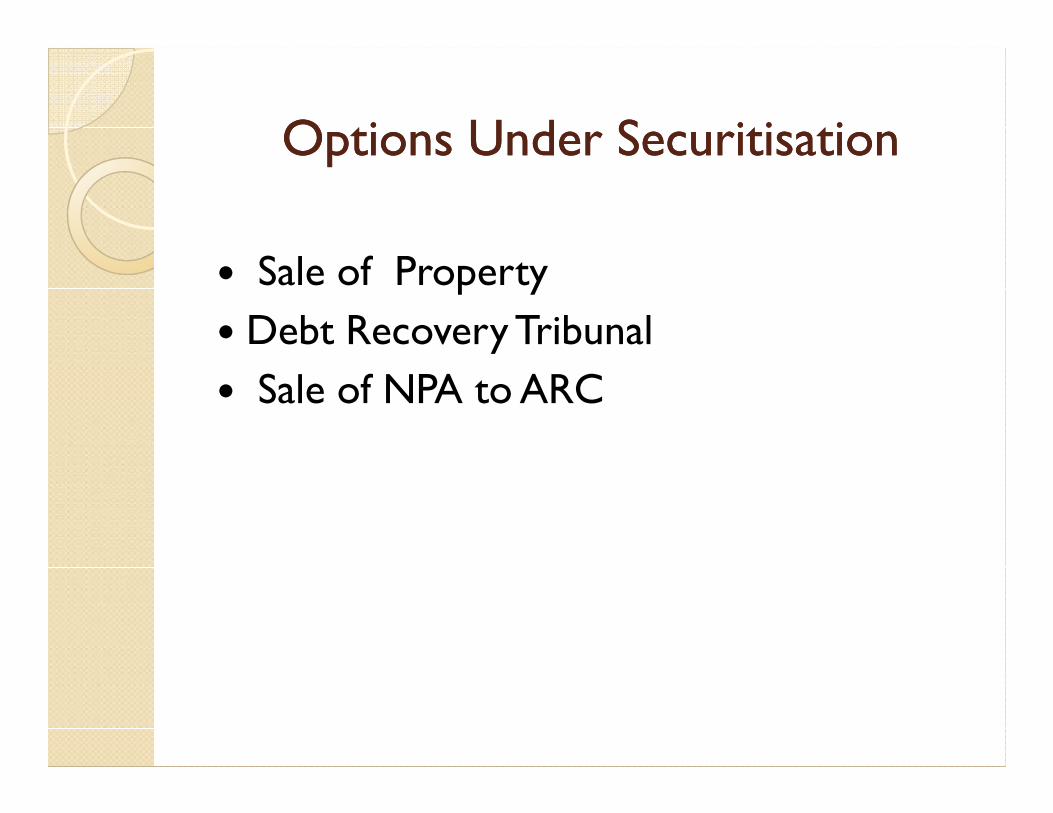

Options Under SecuritisationOptions Under Securitisation

� Sale of Property

� Debt Recovery Tribunal

� Sale of NPA to ARC � Sale of NPA to ARC

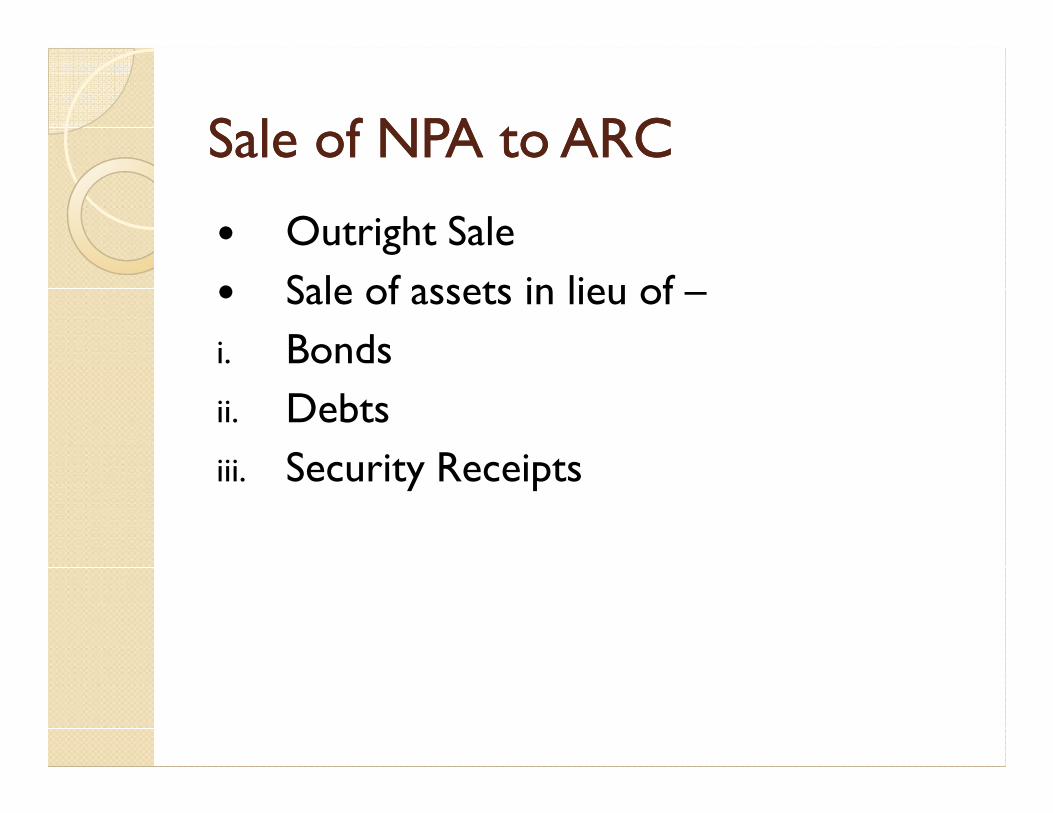

Sale of NPA to ARCSale of NPA to ARC

� Outright Sale

� Sale of assets in lieu of –

i. Bonds

ii. Debtsii. Debts

iii. Security Receipts

Process of SecuritisationProcess of Securitisation

• Bank agrees to sell various types of loans to ARC (which may promote a subsidiary for this purpose called Special Purpose Vehicle, which is a sort of Trust); • The special purpose vehicle- SPV (called • The special purpose vehicle- SPV (called issuer also) makes the payment to the bank for the loans purchased under the arrangement; • These loans are converted into a pool of securities like debentures (called PTC, SR.) by SPV.

• These SR are then sold to institutional investors, who are willing to make investments; • The bank may keep on getting recoveries from the original borrowers; • Bank passes on these recoveries to the • Bank passes on these recoveries to the SPV. • The SPV in turn passes on these recoveries to the institutional investors as per the arrangement made.

Bank

BorrowerARC

Sale of distressed loans assets

Reconstruction

Purchase Consideration

(Banks,Fis)Investors

(Banks,Fis)

Fund/Scheme

Reconstruction

Sale of Instrument

Payment for subscription of Instruments

Intermediaries in the Securitisation Intermediaries in the Securitisation Transaction Transaction

� Originator Bank

� ARC

� Due Diligence Agencies� Due Diligence Agencies

� SPV(Trust)

� Recovery Agents

� Collecting Banks

� Rating Agencies

IllustrationIllustration

NPA in Co-op Bank..

Assume the total NPA identified fortransfer to ARC is Rs.20Cr.Further assume that for these accounts,the bank has made provision underthe bank has made provision underBDDR @ 30 % i.e Rs.6 Cr

� Now, if the accounts are not recoveredthen bank has to provide @ 100% i.eadditional Rs.14 Cr provision is required

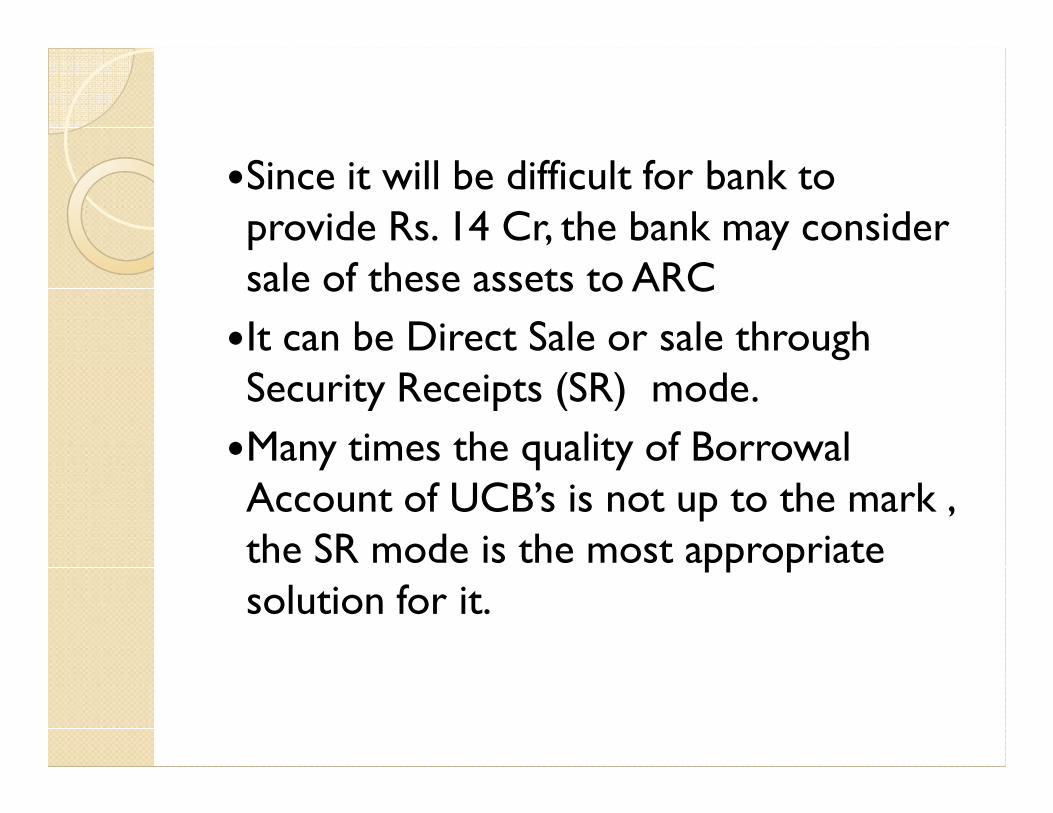

�Since it will be difficult for bank to provide Rs. 14 Cr, the bank may consider sale of these assets to ARC

�It can be Direct Sale or sale through Security Receipts (SR) mode. Security Receipts (SR) mode.

�Many times the quality of Borrowal Account of UCB’s is not up to the mark , the SR mode is the most appropriate solution for it.

MethodologyMethodology

� Identification of ARC

� Due Diligence of the portfolio done by ARC

� Factors for Due Diligence:� Factors for Due Diligence:

i. Date of NPA

ii. Quality of asset

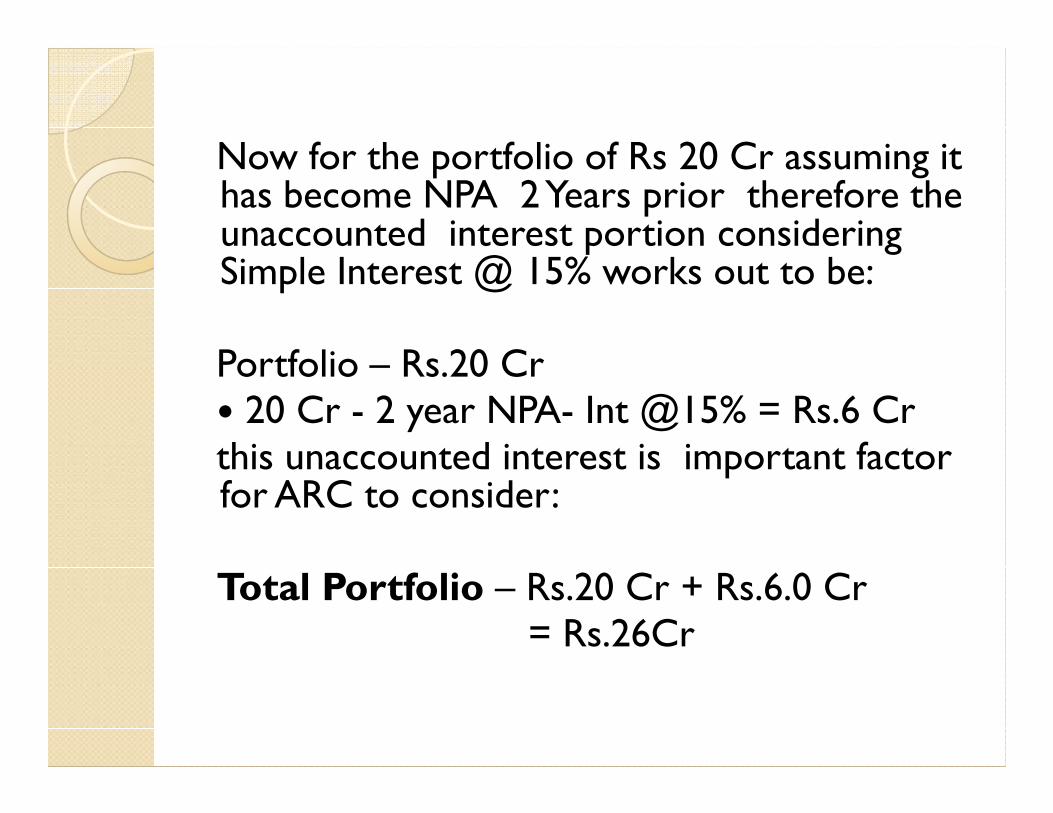

Now for the portfolio of Rs 20 Cr assuming it has become NPA 2 Years prior therefore the unaccounted interest portion considering Simple Interest @ 15% works out to be:

Portfolio – Rs.20 Cr� 20 Cr - 2 year NPA- Int @15% = Rs.6 Cr� 20 Cr - 2 year NPA- Int @15% = Rs.6 Crthis unaccounted interest is important factor for ARC to consider:

Total Portfolio – Rs.20 Cr + Rs.6.0 Cr= Rs.26Cr

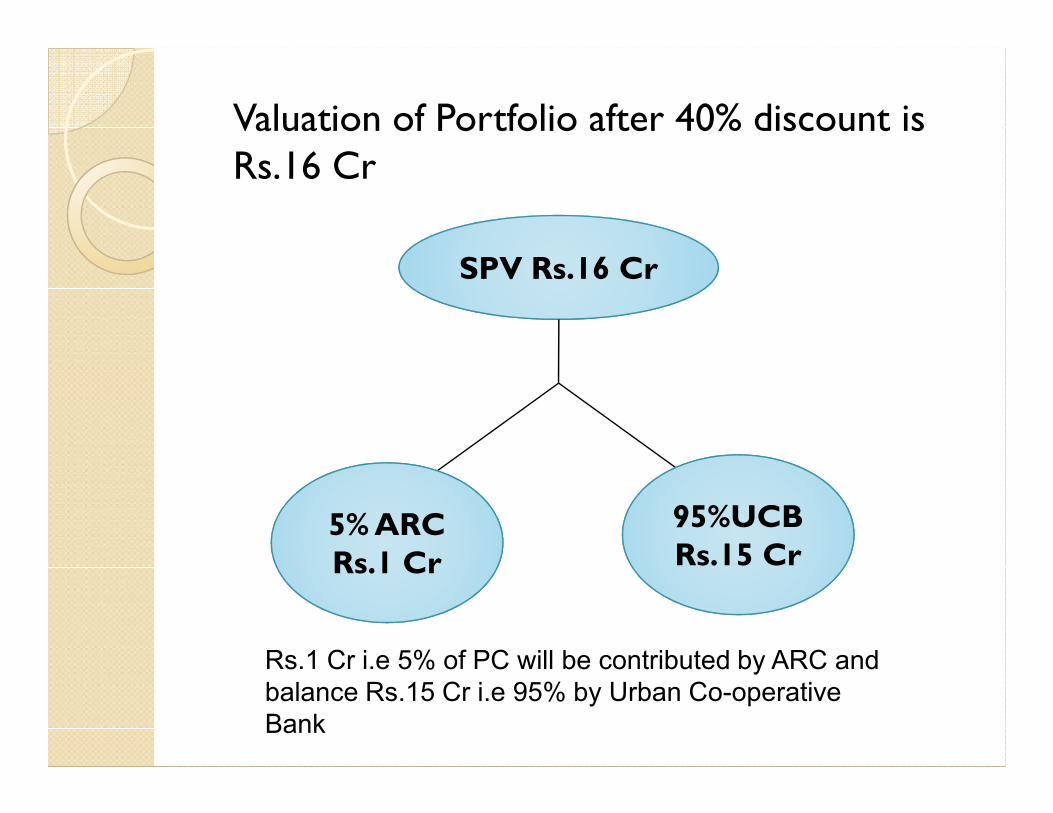

� Assuming ARC after Due Diligence values this portfolio at discount of 40% ie 60% of Rs. 26 Cr which works out to be Rs.15.6 Cr (rounded off to Rs.16 Cr)

Now under SR route the structure of � Now under SR route the structure of transaction will be as under:

SPV Rs.16 Cr

Valuation of Portfolio after 40% discount is Rs.16 Cr

95%UCBRs.15 Cr

5% ARCRs.1 Cr

Rs.1 Cr i.e 5% of PC will be contributed by ARC and

balance Rs.15 Cr i.e 95% by Urban Co-operative

Bank

Accounting Treatment of Accounting Treatment of Securitisation TransactionsSecuritisation TransactionsSecuritisation TransactionsSecuritisation Transactions

In the books of bank :

I. Rs. 15Cr (95%) Investment for Subscription of SR will be treated as Non- SLR investment.

Investment A/c Dr Rs.15 Cr

To Bank A/c Rs.15 Cr

(Being investment made in SR)

II. On receipt of Rs.16 Cr from SPV trust :

Bank a/c Dr Rs. 16 CrTo Borrower a/c Rs. 16 Cr

(For money received)

Provision for BDDR a/c Dr Rs.4 CrProvision for BDDR a/c Dr Rs.4 CrTo Borrower a/c Rs.4Cr

Hence, Borrower a/c becomes NILAnd balance in BDDR remains at Rs.2 Cr

Other Points:

a. Any loss arising on account of the saleshould be accounted accordingly and reflectedin the Profit & Loss account for the periodduring which the sale is effected

b. In case the securitized assets qualify forb. In case the securitized assets qualify forderecognition from the books of the originator,the entire expenses incurred on thetransaction, say, legal fees, etc., should beexpensed at the time of the transaction andshould not be deferred

RecoveryRecovery

� Technically SPV acting through ARC becomes owner and they can recover money from the borrower under SARFESI.SARFESI.

� However, ARC can appoint the same bank as Collecting Agent.

What happens to NonWhat happens to Non-- SLR SLR Investments….Investments….

After 1 year –The trust will get its portfolio rated by approved rating agencies .

- Rating would depend on asset quality / recovery into those accounts.recovery into those accounts.

Suppose for total portfolio of Rs.26 Cr , recovery into these accounts during 1 year is Rs.6 Cr so balance is Rs. 20 Cr. Depending upon the rating provided by rating agencies it indicates that 10% discount in NAV of portfolio i.e Rs.2 Cr then bank has to provide for this NAV based discount.

DocumentationDocumentation

� Proposal Letter for sale of NPA� Offer Letter from ARC to Bank� Acceptance from Bank to ARC� Offer Document� Trust Deed� Trust Deed� Agency Agreement� Assignment Agreement� Application for subscription of S.R. issued by ARC

� Issue of S.R.