reinsurance section newsletter, issue no. 50, june … news number 50 june 2002 1 the future lies...

TRANSCRIPT

REINSURANCE NEWS

NUMBER 50 JUNE 2002

1 The Future Lies Aheadby Chris C. Stroup

1 Ten Predictions for the Future ofthe Life Reinsurance Industryby Jess A. Skriletz

1 Winners and Losers in aConverging Global Marketby David B. Atkinson

2 Chairperson’s Cornerby Jeffrey S. Katz

3 Editor’s Cornerby Dean S. Abbott

16 SPRA Pools in Light of September 11th Tragediesby James B. Keller

17 Highlights of the 2001 Manulife Reinsurance Mortality Studyby Manon Laverdiere and

Valerio Valenti

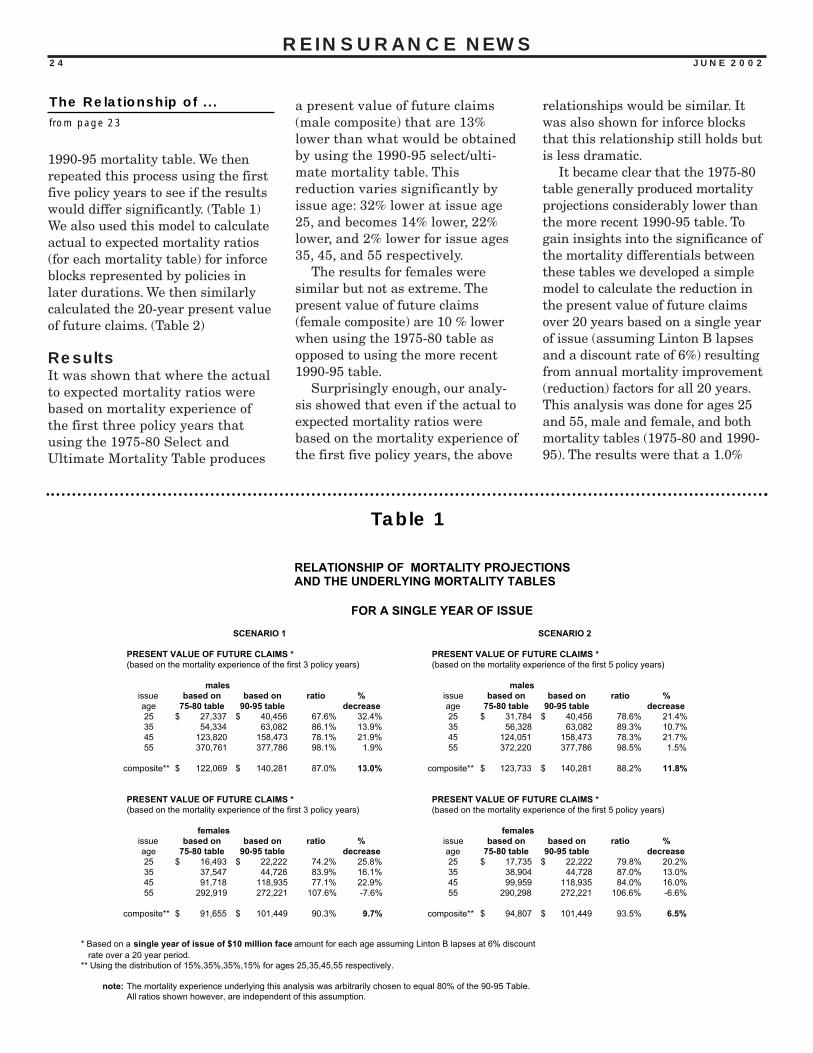

23 The Relationship of Mortality Projections and The Underlying Mortality Tables Usedby Larry Warren

28 Life Reinsurance Data From The Munich American Surveyby James L. Sweeney and

David M. Bruggeman

(SEE INSERT) Apply To Join Today!

IN THIS ISSUE

continued on page 4 continued on page 8

There is anold jokeabout the

difference betweenAmerican andSicilian actuaries.While both groupscan tell you howmany people out ofa thousand will diein the coming year,the Sicilians cantell you their names. In this article Iam going to name company names.Be rest assured that I have no tiesto La Cosa Nostra—I will not makeany offers that you cannot refuse.

I’m going to confine my observa-tions to the U.S. life mortality riskmarket. I’ll take a look back in time,roll in some discussion of currentconditions, and stick my neck out totry and predict the future.

continued on page 11

The future of life reinsurancein America is certainly oursto win or to lose. The forces of

today—expanding technology, tight-ening capital, regulatory rumblings,mergers and acquisitions—willaffect the focus of tomorrow. If wewish to win the day, one to prosperin a changing environment, we needto begin preparing ourselves now forthe challenges that lie ahead.

What are those challenges? Anyattempt to polish my crystal balland peer into that future yields bothpositives and negatives, reasons tohope and reasons to tread carefully.

We’ve all had days when wewished we could know thefuture. The business deci-

sions facing us would be mucheasier if only we had a crystal ball. Ican’t give you a crystal ball, but Ican offer a number of predictionsand observations for the future oflife reinsurance over the next fiveyears. If you are like me, you takepredictions with a healthy dose ofskepticism. I hope to give you somethings to think about that will shapeyour own opinion of the future of lifereinsurance.

What do I see? A competitivemarket with a significant slowdownin growth coming from the rapidpace of growth seen recently, anincreasing appreciation by lifeinsurance companies of the finan-cial strength of their partners,

The Future that LiesAhead...by Chris C. StroupCEO of Swiss Re Life & Health, North America

“Yesterday is not ours to recover, but

tomorrow is ours to win or to lose.”

— President Lyndon B. Johnson

address to the nation

Nov. 28, 1963

Ten Predictions for the Future...by Jess A. SkriletzGeneral Manager and CEO of ING Re

Winners & Losersin a ConvergingGlobal Marketby David B. AtkinsonExecutive Vice President and COO of

Reinsurance Group of America

NEWSLETTER OF THE REINSURANCE SECTION

THE FUTURE OF LIFE REINSURANCE

DavidAtkinson

The following articles are based upon presentations given at the ACLI’s Reinsurance Executive Roundtable held at Amelia Island, Florida, on February20-22, 2002. The Reinsurance Section newsletter thanks David Atkinson, Jess Skriletz, and Chris Stroup for writing the following articles for this edition.

This newsletter is free to Section members. A

subscription is $15.00 for nonmembers.

Current-year issues are available from the

Publications Orders Department. Back issues

of Section newsletters have been placed in

the Society library, and are on the SOA Web

site, www.soa.org. Photocopies of back

issues may be requested for a nominal fee.

Expressions of opinion stated herein are,

unless expressly stated to the contrary, not

the opinion or position of the Society of

Actuaries, its Sections, its Committees or the

employers of the authors.

The Society assumes no responsibility for

statements made or opinions expressed in

the articles, criticisms and discussions

contained in this publication.

Copyright © 2002 Society of Actuaries. All rights reserved. Printed in the United States of America.

Newsletter Editor/Web Liaison (2002)Dean S. Abbott, FSAAllianz Life Insurance Company of N. AmericaP.O. Box 884Minneapolis, MN 55440-0884Phone: (763) 765-6248Fax: (763) 765-6203E-mail: [email protected]

OFFICERSChairpersonJeffrey S. Katz, FSAVice-ChairpersonJames W. Dallas, FSASecretary/TreasurerMelville J. Young, FSA

Council MembersTimothy J. Alford, FSARobert W. Beal, FSAJay D. Biehl, FSA

D. Leigh Harrington, FSARonald L. Klein, FSARobert J. Reale, FSA

SOA StaffLois Chinnock, Section CoordinatorPhone: (847) 706-3524Fax: (847) 273-8425)E-mail: ([email protected])

Joe Adduci, DTP CoordinatorPhone: (847) 706-3548Fax: (847) 273-8548E-mail: ([email protected])

Society of Actuaries475 N. Martingale Road, Suite 800Schaumburg, IL 60173Phone: (847) 706-3500Fax: (847) 706-3599Web: www.soa.org

NUMBER 50 JUNE 2002REINSURANCE NEWSNEWSLETTER OF THE REINSURANCE SECTION

The issue I would like to bringto the Section’s attention, intwo different flavors, is an

old refrain: participation. The SOAand its various component sub-groups, such as the Sections andPractice Areas, get the vast major-ity of their work accomplishedthrough the efforts of membervolunteers. Like any organization,we are only as good as we collec-tively choose to be through our ownefforts. I urge each member to takeat least a small share of responsibil-ity for what we are as a section byvolunteering. You could write anewsletter article, present at asection session or find a variety ofother ways to contribute.

Our current volunteers arecontributing in important ways. TheSection Council members who havetaken over the creation of interest-ing and informative sessions for the

various Society meetings have donea terrific job. I expect this year’smeetings to have one of the bestsession lineups the Section has puttogether in the last several years.Another key Section activity is thisnewsletter, where over the past 18months, the editorial reins havepassed smoothly to a new editor.

Part of my concern is that I seethe same members volunteeringtime and again to contribute to ouractivities. As Section Chair, Icertainly appreciate the efforts ofthose individuals. But we need toget other members into the mix.There will come a time when theusual volunteers are not available,and we’ll need others to stepforward to shoulder the burden.Beyond that, the Section wouldbenefit from the new ideas thatothers would contribute by provid-ing new ways of seeing and doing

things that wouldbring neededrefreshment tosome of our routineactivities. Finally, Ihave observed thatthose who volun-teer today will leadtomorrow. We needto continuallydevelop new lead-ers who can takeus through the uncharted waters ofthe future.

So, don’t delay! New classes arebeing formed now! Operators arestanding by to take your call at 1-800 . . . or not. Still, if you want toparticipate but just don’t know howto get started, give me a call or sendme an e-mail. I assure you that allreplies will be kept in strictestconfidence and no salesman willcall.

2 JUNE 2002

REINSURANCE NEWS

Chairperson’s CornerParticipationby Jeffrey S. Katz

JeffKatz

At the Reinsurance HotBreakfast in New Orleanslast October, Jeff Katz

mentioned that within the monthsthat followed we would be issuinga special edition newsletter cover-ing the reinsurance impacts of theevents of September 11. It was ourintention to do so, and we hadlined up authors for multiple arti-cles on the topic. Unfortunately,only one of the promised articles

was ever written and submitted,therefore, the special editionnewsletter never was. Hopefully,you haven’t been scouring your in-basket wondering if you hadmisplaced it. The one article thatwas submitted, Jim Keller’s articlediscussing the SPRA, has beenincluded in this newsletter. Ifanyone is interested in writing anarticle for future newslettersdiscussing the impacts of

September 11, wewould be veryinterested in hear-ing from you.

Dean S. Abbott,FSA, MAAA, is vice president, rein-surance actuaries, at Allianz LifeInsurance Company of NorthAmerica in Minneapolis, MN. Hecan be reached at [email protected].

JUNE 2002 3

REINSURANCE NEWS

CorrespondentMembershipOne way to increase the odds ofadding volunteers is to add newmembers. The Reinsurance Sectionis doing that through the creation ofCorrespondent Member statuswithin the Section. Correspondentmemberships are available to non-members of the Society who wish toparticipate in the activities of theReinsurance Section. Dues forCorrespondent Members are thesame as for other Section members:$10 per year at present.

Correspondent Members haveaccess to Section activities just asother Section members do and alsoreceive a subscription to the newslet-ter. It’s a great way to participate inthe Section without having to dealwith those pesky exams!

The SOA Board of Governorsapproved Correspondent Memberstatus as a change to the Section’sby-laws earlier this year. LoisChinnock of the SOA staff hasdeveloped an application form, acopy of which is included with thisnewsletter. The form is also avail-able on the Section’s page of theSOA Web site. Please spread theword to those in your organizationwho might be interested.

Spring MeetingsAs you are reading this, the SpringMeeting in Colorado Springs will behistory and the San Francisco meet-ing will be just about to start. The

featured Reinsurance session atboth Spring Meetings is a mocktrail. The topic is a timely one—thewar exclusion. The product develop-ment/financial meeting at the endof May also offered a reinsurancesession on a unified mortalityapproach. The health/pension meet-ing offers additional reinsurancesessions on provider excess stop-lossand trends in large claims. We areco-sponsoring these sessions withthe Health Section. My thanks toRonnie Klein, the Section Councilmember responsible for the SpringMeeting sessions, for all of hisefforts in developing the sessionsand recruiting presenters.

SeminarThe Section sponsored an “Intro-duction to Life Reinsurance”seminar June 11-12 in suburbanChicago near O’Hare Airport. Theseminar focused on the basics of lifereinsurance including actuarial,legal, accounting and regulatoryaspects. We offered the seminar inconjunction with the ProductDevelopment Actuary Symposiumlater that same week. Jim Dallas,the Section’s vice-chairperson,organized the seminar. Presentersincluded Denis Loring, TomSpurling, Craig Baldwin, Al Kleinand myself. The seminar wasapproved for 10 units ofProfessional Development credit. Inaddition to actuaries, there werenon-actuaries in attendance whowanted to learn more about reinsur-ance basics.

Jeffrey S. Katz, FSA, MAAA, issenior vice president at MunichAmerican Reassurance Company inChicago. He can be reached [email protected] or by phone at(312) 863-8253.

Editor’s CornerThe Special Edition that Never Was...by Dean S. Abbott

DeanAbbott

“One way to

increase the odds

of adding volun-

teers is to add

new members.”

4 JUNE 2002

Reasons for optimismFortunately, the reasons for opti-mism are numerous. The U.S. lifeinsurance marketplace seemsheaded for a secure tomorrow, andwhat’s good news for life insurers isalso good news for life reinsurers.

As the American people lookforward to longer and healthierlifespans, they’ll need to set asidemore money for their retirementyears. The current interest rates oftraditional savings vehicles are low,which makes life insurance evenmore attractive.

In addition, the U.S. life insur-ance industry has specialcharacteristics that keep it poisedfor success. As a whole, U.S. lifeinsurers are remarkably adept atdeveloping new products, and theirmortality knowledge gives them asignificant comparative advantageon a global scale. Product distribu-tion remains an area with greatpotential that so far has not beenfully exploited. Also not fullyexploited is the U.S. insurers’investment in technology. Moneyhas been spent, improvementshave been made, but the hoped-forcost savings due to lower expenseratios are still somewhere in thefuture.

On the downside…Unfortunately, not everything ispositive. There are challenges andobstacles on the U.S. insurance hori-zon that must be successfullynavigated.

Chief among those obstaclesare formidable new competitorscreated by the convergence offinancial servicesindustries in theUnited States.Mergers andacquisitions inthis field haveled to impos-ing

competitors with substantialresources. Merrill Lynch andMorgan Stanley are good examples.Together, thesetwo companieshave greatermarket capital-ization at theirdisposal thanthe top eightU.S. life insur-ance companiescombined.Needless to say,that gives Merrill Lynch andMorgan Stanley a considerablecompetitive advantage.

In addition, these new competi-tors have a keen understanding ofconsumer needs. And if the factorsthat now give insurers an advan-tage—the tax-deferral subsidy andestate tax laws—are ever elimi-nated or restructured, these newcompetitors will eagerly move intoour marketplace.

State insurance regulationsremain, of course, a constant cloudon the horizon. Regulations drive upadministrative costs and increasecapital requirements, making itmore difficult for the insuranceindustry to compete with financialservices giants that aren’t hobbledby 50 sets of state regulation.

As these giants compete for ourclients, they also fish in our talentpool. The supply of underwriters,actuaries, accountants and manage-ment professionals is not unlimited.With more companies vying forthese talents, fewer capable peopleare available to fuel the insuranceindustry’s progress.

Fragmented roles and assets

Technology hascontributed its own

interesting wrinkleto the future oflife insurance.With theInternet’s abilityto seamlessly

link computers and systems, compa-nies across state lines andinternational boundaries, it’s now

transparent tothe consumer justwho actually isproviding theservices he’sreceiving.

In the past, asingle life insurerwould have beenresponsible formanaging invest-

ment assets, manufacturingproducts, distributing those prod-ucts, providing customer service,taking on risk and administering itsaccounts. With technology, however,those roles have fragmented withlife insurers often retaining only aportion of the responsibilities.Today, those functions fall to a vari-ety of parties:

• Managing investment assets—handled by fund managers and insurers.

• Manufacturing products—still performed by life insurers.

• Distributing products and providing customer service—may be performed by a variety of credible, trusted advisors, such as banks, brokerages and independent financial planners, in addition to insurers.

• Risk taking—often handed off to reinsurers.

• Administering accounts— may be outsourced to professional third-party administrators.

This fragmentation of traditionallife insurance roles has conse-quently led to a fragmentation ofavailable assets, as well. In 1989,before this fragmentation began,life insurers had $1.4 trillion in

REINSURANCE NEWS

The Future that Lies Ahead

from page 1

JUNE 2002 5

REINSURANCE NEWS

assets under management. Anequal amount was being managedby mutual funds, broker/dealersand market funds. This means thetotal available assets were split 50-50.

What a difference a decademakes. In 2000, with service frag-mentation well underway, lifeinsurers’ assets under managementrose to more than $3.1 trillion. Butthe assets managed by mutualfunds, broker/dealers and marketfunds leap-frogged ahead to $7.7trillion. It was no longer a 50-50split. Instead, life insurers managedonly 29 percent of those assets, withthe remaining 71 percent going toother financial services companies.

As service fragmentation contin-ues, life insurers are faced withmanaging a smaller portion of theavailable assets.

Reinsurance opportunitiesFor reinsurers, this service frag-mentation offers new opportunitiesin the United States. As more lifeinsurers look to share their risk,more business is available for rein-surance companies. We canmeasure the growth by looking atcession rates, which is the percent-age of new face amount that hasbeen ceded to the reinsurancemarketplace. In 1993, the cessionrate was 15 percent. By 2000, thatamount had more than quadrupledto 64 percent. When the numbersare in for 2001, they could top 70percent.

Overall, the U.S. reinsurancemarket grew at a compounded rateof 29 percent, compared to a mere 5percent for the primary insurancemarket. There are several reasonsfor this increase in reinsurancebuying:

• Primary insurers are eager to avoid earnings volatility, and reinsurance is a key tool to accomplish that goal.

• The transformation of insurers to a fee-based business model has made it more attractive.

• Reinsurance rates are tempting.

The last point bears expansion.Over the past five years, life rein-surance prices have actually gonedown, largely due to strict under-writing that produces lowermortality assumptions. Before leav-ing the subject of prices, it should benoted that the terrorist attack ofSeptember 11, 2001, has moderatelyaffected the price of vanilla reinsur-ance for the group life market,where there is a built-in concentra-tion of risk. September 11 has hadthe greatest effect on the price andavailability of catastrophic coverage

for both group and individual lifeinsurance. This coverage is dramati-cally more expensive and difficult toobtain. Only time and future eventswill tell us if these markets willever return to pre-September 11conditions.

Moderating the futureWith falling reinsurance prices andrising cession rates, what does thefuture hold for U.S. life reinsurers?Are we on an unstoppable upwardpath? That would be nice, but it’sunlikely. There is both good and badnews for life reinsurers:

1. Cession rates will level off. The 64 percent penetration rate of 2000 will likely hit a plateau at some point and will probably not top 75 percent.

2. An information advantage, an in-depth knowledge of under-writing and distribution effects on mortality will maintain the reinsurers’ competitive edge .

3. New entrants into the life insur-ance business will be risk-averse, preferring to outsource their mortality risk-taking and underwriting.

4. As capital markets become more efficient and technology contin-ues to make reinsurance arrangements transparent to the consumer, the cost of risk will eventually be driven down-ward to the level of commodity pricing.

Commitment and capitalWhat will it take for a reinsurer tosurvive—and even thrive—in thisnew century? Two words that cometo mind are commitment and capital.

Commitment will increasinglymatter to primary carriers. Theywon’t be satisfied with a reinsur-ance relationship that’s merely the“flavor of the month.” Instead,they’ll want to know they can counton a long-term business relation-ship with a highly rated reinsurerwho has a demonstrated commit-ment to the life reinsurancebusiness. This spells bad news forunaffiliated reinsurers and thosewith marginal operations.

Capital will also be a key issuebecause the supply of life reinsur-ance capital is bound to contract,perhaps as early as the third quar-ter of this year. The signs arealready there; just look at the costand capacity of current lines ofcredit that are used to manage the

continued on page 6

“September 11 has

had the greatest

effect on the price

and availability of

catastrophic cover-

age for both group

and individual life

insurance.”

6 JUNE 2002

strain of XXX surplus require-ments. The result is that to surviveand thrive, reinsurers must be ableto offer impressive capacity.

In the U.S. reinsurance market-place of tomorrow, primary carrierswill want three things:

• Longer-term reinsurance relationships.

• A few trusted places to concen-trate their business, thus main-taining that relationship.

• A reinsurer who can supply their capital needs, product development and underwriting capacity for the long haul.

In response, successful reinsurersmust:

• Deliver a broad range of productofferings.

• Include non-traditional reinsur-ance options.

• Improve their credit ratings,because lower-rated companies just won’t cut it in the future.

Critical regulatory issues aheadTwo critical regulatory issues arelooming on the horizon of the rein-surance world of tomorrow: theestablishment ofinternationalaccountingstandards andthe develop-ment of federalregulation ofthe reinsuranceindustry. Whileboth proposalsare likely a longway off, eachwould havesignificant long-

term effects on the industry. Thewise will keep these developingprojects in view.

Our U.S. statutory accountingsystem is under some pressure.First, non-admitted reinsurers areasking that U.S. collateral require-ments be relaxed. In addition, atleast one international organizationis pushing for reinsurer white lists.

Still, others are advocating interna-tional accounting standards. In theend, these standards may lookmuch like current U.S. or CanadianGenerally Accepted AccountingPrinciples.

No matter how the internationalaccounting standards evolve,

anything thatproduces a signifi-cant accountingchange will surely

have anequallysignificanteffect on thedemand forreinsurance.

The impo-sition offederal rulesis the othermoving regu-latory target.At the

moment, regulation of insurance isthe domain of the states, creating a50-state maze of inconsistent rulesand regulations that give insurerscompliance headaches. But unlesssome compelling arguments aremade for a single federal standard,the maze is likely to remain.

The most persuasive argumentfor a single federal standard wouldbe to show how it would benefitconsumers. But that’s been difficultto argue because of the currentperception that consumers canalready get the products and pricesthey want, when and where theywant them. Unless we can make astrong case for consumer benefit,federal regulators will be less moti-vated to seize control of theinsurance industry.

But all is not lost for those whosupport federal regulation.Consumer arguments can be devel-oped. The NAIC’s inability toregulate consistently makes federalregulation more appealing toCongress. Gramm-Leach-Bliley isan example of what can be accom-plished when the banks andinsurers approach Congresstogether. In addition, the September11, 2001, terrorist attack againstthe United States left Congressdismayed and frustrated when itrealized it had no insurance expert-ise to call upon.

Hounded by the headlinesThe September 11 terrorist attackand the collapse of Enron have hadan impact on almost everyAmerican industry. The reinsuranceindustry is no exception.

A government backstop for cata-strophic claims, such as thosestemming from the September 11attack appears dead for now,although some recent commentsfrom Alan Greenspan and a reportfrom the General AccountingOffice could breathe some life backinto the proposal. So far, the indus-try failed to prove its case to the

REINSURANCE NEWS

The Future that Lies Ahead

from page 5

“At the moment,

regulation of

insurance is the

domain of the

states, creating a

50-state maze of

inconsistent rules

and regulations

that give insurers

compliance

headaches.”

JUNE 2002 7

REINSURANCE NEWS

federal government that reinsur-ance is unavailable for lifeproducts.

No one knows if Congress willact. But whether it does or doesn’t,there are things the industry canand must do to better manage itsrisk. We need to learn from thisexperience, change how we dobusiness and better manage riskconcentrations. For this, we canlook to the property-and-casualtyindustry and study the tools andbehaviors they use to handle cata-strophic claims, such as those fromHurricane Andrew in 1992. Theindustry developed methods tobetter identify risks and, when therisks were too concentrated, theindustry worked to move thoserisks off their books.

The unprecedented collapse ofEnron is another headline-grabberwith reinsurance implications.Enron’s covert deals and

labyrinthine bookkeeping have leftinvestors and the public with awariness of big business and adistrust of complicated accounting.

For the reinsurance world, thismeans clients will be looking forsimpler, more understandablebusiness transactions—somethingthey can count on withoutunpleasant surprises somewheredown the road. They’ll want rein-surance contracts that provideguaranteed payments for definedlosses. Surplus relief, securitiza-tions and other complextransactions are bound to fallunder the magnifying glass ofinvestigators looking for account-ing sleight-of-hand.

Preparing for tomorrowClearly, there are opportunities andperils awaiting us in the future oflife reinsurance. Tomorrow will beours to win or to lose, and the prize

will surely go to those companieswho have prepared themselves toavoid the perils and seize the oppor-tunities.

Theodore Roosevelt once advised,“Whenever you are asked if you cando a job, tell ’em, ‘Certainly, I can!’Then get busy and find out how todo it.”

Can reinsurers meet the chal-lenges that lie ahead? Certainly, wecan. We’re already busy finding outhow to do it today.

When tomorrow arrives, we’ll beready.

Chris C. Stroup is chief executiveofficer of Swiss Re Life and Health,North America, and a member of theLife Executive Board of Swiss ReLife and Health. He is responsiblefor the life and health reinsurancebusiness and activities for Swiss rein the U.S. and Canada.

Annual MeetingReinsurance Section Council Meets

Reinsurance Section Council

members taking some time out of

their meeting in New Orleans to

pose for the SOA camera—

Back Row—Bob Beal (2000-2001

chairperson), Jim Keller, Bob Reale,

Mel Young, Ronnie Klein, Jeff Katz

(2001-2002 chairperson)

Front Row—Jack Bailey, Leigh

Harrington, Jay Biehl, Jim Dallas,

Dean Abbott (newsletter editor)

8 JUNE 2002

slowing consolidation of the leadinglife reinsurers and growth in theuse of strategic alliances by lifereinsurers.

Since our customers’ needs shapethe environment in which we’lloperate, my predictions are basedon the trends, issues and macroeco-nomic factors facing the lifeinsurance industry. Although stillstrong and dynamic, life insurershave evolved over the last 20 years,increasingly emphasizing invest-ment-oriented products overtraditional protection-based ones.Life insurers’ assets under manage-ment have grown rapidly throughannuity sales and the acquisition ofmutual fund businesses, while lifeinsurance sales were relatively flatover that period. The industry alsomoved into variable productsduring the economic boom of the1990’s. These trends have increasedthe importance of fee-based incometo life insurers. Additionally, theincreasing proportion of life insur-ance reinsured may be a sign of lifeinsurers striving for a morepredictable bottom line and a grow-ing aversion to earnings volatility.

The above industry trends arereflected in the top two concerns oflife company management. Surveyshave shown their two top concernsare achieving profitable growth andimproving distribution efficiencyand productivity.Management’sgoal is to improvetheir company’sprofitability, andthis is a tall orderin a competitivemarket. Many lifeinsurance compa-nies areovercapitalized.While this situa-tion is good for their financialstrength ratings, it’s poor for share-holder returns. Growth—organic or

through acquisition—can createscale and critical mass to improveshareholder returns. The strongtrends of consolida-tion anddemutualization aretwo indications ofthe underlying pres-sures life insurersare facing toimprove profitabilityand to grow andreach economies ofscale.

I also expecteconomic and demo-graphic forces tocontinue to putpressure on lifeinsurance companygrowth and prof-itability.Competitive pres-sures, overcapacityand consolidationtrends are therefore likely to resultfrom these forces as well. I expectexcess global industrial capacity tolimit inflation, which should lead torelatively low interest rates overthe next few years, as well as alackluster equity market. Such aneconomic scenario will likely resultin sluggish demand for fixed andvariable investment products.Changes in tax policy may alsoreduce sales by life insurancecompanies, not only throughchanges in the estate tax, but alsoindirectly by increasing the

amountsthat can becontributedto 401(k)plans. As thenew $20,000annual401(k) planannualcontributionphases in,there will

likely be a significantly reducedlong-term demand for annuities. Inaddition, the Baby Boomers were

behind much of the growth in assetsunder management seen over therecent past. As this demographic

group eventu-ally begins toshift fromsavings topayout as theyretire, thismajor source ofgrowth willdisappear. It isalso question-able ifGeneration Xcan providethe demand forinsuranceproducts tomake up forthe drop indemandcaused byBaby Boomersmoving into

retirement. First, the Baby Boomergeneration is much larger thanGeneration X. Furthermore,Generation X’ers are believed byexperts to be survivors, independentand “do-it-yourselfers.” Therefore,people may be less likely to beinterested in “bundled” insurancecompany investment products andmore willing to invest directly inmutual funds or equities.

In summary, the life insuranceindustry is transforming into abroader financial services businesswith a focus on savings products.The playing field is not onlycrowded with insurers, but with thelikes of Merrill Lynch, CharlesSchwab and Fidelity. Insurers mayhave a long-term advantage (ordisadvantage?) with their strong(but expensive) distribution chan-nels, but the competition from theseother players will continue to putpressure on profitability.

Demutualization and consolida-tion will continue as companiesattempt to improve profitability,resulting in fewer and largercompanies. Demographics have

REINSURANCE NEWS

Ten Predictions for the...

from page 1

JUNE 2002 9

REINSURANCE NEWS

recently helped life insurancecompanies grow their assets undermanagement, but these trends areshifting. As a result, life companieswill take increasingly strongeractions to improve shareholderreturns. My predictions are:

Prediction #1: Growth in recur-ring net amount at riskreinsured will slow to that ofthe growth of insurance saleswithin three years. As the propor-tion of face amount reinsuredcontinues to climb, it eventuallymust reach a limit. The rapidincrease seen in the 1990s impliesthat reaching this limit will comemore quickly than slowly. I expectthat ultimately, no more thanroughly 75% of the life insuranceindustry’s net amount at risk willbe reinsured. Many life insurancecompanies will continue to retainthe bulk of their mortality risk andonly reinsure risk in excess of theirretention. The life insurers thatdecide to outsource their mortalityrisk will be required by reinsurersto retain significant risk in order toavoid moral hazard. What are someimplications for life reinsurers?More competition, much slowergrowth and a growing emphasis onexpenses and efficiency.

Prediction #2: Competition forlife reinsurance new businesswill remain strong, or evenintensify, and industry prof-itability will disappointshareholders. We are in a verycompetitive market today, andoffshore start-ups continue to putpressure on the market. With apredicted decline in the growth rateof new reinsured volume, competi-tive pressures will likely increase.Some observers have suggestedsingle-digit rates of return shouldbe expected on some recent acquisi-tions by life reinsurers. This is asign of an environment in which Iexpect shareholders won’t be veryhappy with returns. The result will

be a continued healthy tensionbetween management and owners.

Prediction #3: Profitable rein-surers will be those offering acompelling value proposition toclients. In a consolidatingmarket, life insurers willoutgrow the need for commod-ity reinsurance. Most largeinsurers don’t need to outsourcetheir mortality, but they will whenenticed to do so. A good price is oneway to win business, but that does-n’t necessarily solve the cedingcompany’s problems. I expect riskmanagement will take on a lesserrole (although post September 11 itwill remain important) with capital

and earnings arbitrage coming toplay the major role as thataddresses the primary profitabilityconcerns of life insurers.

Prediction #4: Financialstrength and ratings willincreasingly separate thestrongest reinsurers from therest of the pack. Consolidation inthe life insurance industry is creat-ing ever-larger life insurancecompanies. These companies willdemand bigger and stronger coun-terparties. Along with financialstrength and rating, they will alsolook for a strong commitment to themarket. Size and financial strength

are two signs of this commitmentthat leading reinsurers will use togrow market share.

Prediction #5: Consolidationwithin the life reinsuranceindustry will continue, but at aslower pace. If my prior predictionabout market growth and size andstrength is true, then many of thesmaller reinsurers may be acquired,and that trend may even accelerate,presenting some smaller companiesthe chance to consolidate to becomeone of the top ten. Thus, I’m limit-ing this prediction to the top five toten players only. I believe that clientdiversification needs will ensureopportunities for many in the indus-try and that consolidators willeventually reach a point whereadditional acquisitions will not addincremental market share above alevel around 20%. As there are anumber of reinsurers closing in onthat limit, the top five to ten playersare a more stable group than washistorically the case. This predictionmay prove wrong if the industryfalls out of favor and if acquisitionprices fall to the point that theydon’t need substantial new businessto justify the price paid. Then wemay see many acquisitions beingcompleted as blocks of in-force busi-ness, rather than as going concerns.

Prediction #6: Securitization ofmortality or longevity risk willnot occur to a significantdegree. Reinsurers need not worryabout competition from the capitalmarkets. Why? First, life insurancecompanies don’t need a publicmarket when they already have acompetitive, efficient privatemarket for transferring risk tohighly rated life reinsurers. Second,any true transfer of risk wouldrequire a very complex structureand quite a fair amount of uncer-tainty over a long period of time.Such transactions are expensive to

continued on page 10

“The life insurers

that decide to

outsource their

mortality risk will

be required by

reinsurers to

retain significant

risk in order to

avoid moral

hazard.”

10 JUNE 2002

complete, and have very limitedmarket potential given the educa-tional hurdles with potential buyersare substantial.

I also do not believe there aremany natural buyers of long-termlongevity risk (other than life rein-surers). Pension funds to thetypical long-term investor, arealready exposed to longevity risk intheir pension plans. That makesthem a natural buyer of mortalityrisk (if old age mortality ratesimprove, they win on the securiti-zation, which can help make uplosses in their pension plans).Given a pension plans’ability to invest in equi-ties, perhaps they couldbest hedge their longevityrisk by buying stock inlife reinsurers, ratherthan entering intocomplex structures theydon’t have the expertiseto underwrite.

Prediction #7: Lifereinsurers will increas-ingly and materially participatein strategic alliances and gener-ate substantial opportunitieswith alternative distributionchannels. When your currentcustomers aren’t growing your busi-ness, you find new customers. Lifereinsurers have the expertise todevelop, underwrite and manageprotection products. They just needthe distribution. Both liberalizingfinancial services legislation andthe “new economy” present opportu-nities for non-insurers to enter thelife insurance marketplace. Lifereinsurers, with their strong expert-ise and ability to assume risk, maybe their ideal partners. What arethe implications? Such strategicalliances will be a source of stabilityand growth for life reinsurers ifinsurers lose business to other

financial service providers such asbanks, mutual funds and dot-comdistributors.

Prediction #8: The reinsurerthat enables life insurancecompanies to successfullymarket payout annuities thatprovide balanced fund returnswith guarantees against outliv-ing savings will have acompetitive edge for a month—unless they’re reckless orcrazy, in which case thecompetitive edge will last twomonths. One of the biggest oppor-tunities I see for insurers is tocapture IRA and 401(k) rolloversas the Baby Boomer generationreaches retirement age. However,

the life insurance industry doesn’tyet have a product that bothprotects the individual againstoutliving their assets and providesan attractive “balanced fund” levelof long-term return. As life rein-surers were instrumental inhelping annuity writers provideaggressive Guaranteed MinimumDeath Benefits (GMDB), they alsocould play a role developinglongevity guarantees on balancedfunds.

I’m being just a little sarcasticby saying that whoever solves thisdilemma has a month’s head start.But news travels fast in this busi-ness. With reinsurers going into,then out of, the GMDB reinsurancebusiness, I also wonder if there arecompanies out there that wouldfollow a competitor into such a

business line before having thetime to do a full risk evaluation.

Prediction #9: The real competi-tion between life reinsurers willbe recognized as one for toptalent. Life reinsurance is a busi-ness that requires strong expertiseto succeed. One of my biggest chal-lenges has been finding strong andexperienced talent. There isn’tenough is out there, especially giventhe growth the life reinsuranceindustry has seen over the last tenyears. While you can develop thestaff you need, you must also strivediligently to retain them.

Prediction #10: The fond memo-ries of Bermuda will be real, butgetting rich from an IPO oracquisition are only dreams. TheIPO mania that was rampant in thehigh tech area in the 1990’s mayhave even spilled over to reinsur-ance. If any of the offshore start-upshave a business plan of selling outafter a few years of building up abook of business, I think they willfind only modest success. Many ofthese reinsurers will build success-ful businesses, but I don’t see acompelling reason for them todemand high valuations in such acrowded and competitive market. Atleast Bermuda is a great place tolive for a few years!

Jess A. Skriletz FSA, CFA is generalmanager and chief executive officerof ING Re and ING InstitutionalMarkets. He began his 20-yearcareer with ING at Security Life ofDenver Insurance Company and hasserved in various actuarial, invest-ment and management capacities,including several years in theNetherlands as an actuary of theInternational Division of Nationale-Nederlanden. He can be reached atjess.skriletz@ ing-re.com

REINSURANCE NEWS

Ten Predictions for the...

from page 9

JUNE 2002 11

REINSURANCE NEWS

To start, I’d like to take you backto a time when the U.S. life reinsur-ance industry was quite differentfrom what we see today. It was along, long time ago—the year—1995. Way back then, there were 18

U.S. reinsurers with market sharesof two percent or more. Over thelast six years, would you believethat half of those 18 reinsurershave been acquired? Six reinsurerswere merged into other reinsurersand no longer exist. The other threeacquired reinsurers were left in tactby their new parents.

In Table 1, Swiss Re and thecompanies it has acquired areshown in bold type. A question foryou is: How do you become thelargest reinsurer? Simply combinethe second, fourth, sixth, andseventh largest reinsurers, andvoila! Altogether, Swiss Reacquired four reinsurers over the

Winners and Losers...

from page 1

Table 1: U.S. Reinsurers in 19951

Rank2 Company Market Share2 Acquired By1 Transamerica Re 16% Aegon2 Lincoln Re 13 Swiss Re3 RGA 12 MetLife4 Life Re 8 Swiss Re5 ING Re 66 Swiss Re 67 Mercantile & General 4 Swiss Re8 AUL 49 Cologne Re 4 General Re 10 CNA 4 Munich Re11 BMA 312 Employers Re 313 Phoenix Home 3 Employers Re14 Allianz 315 Hartford Intl Life Re 216 Gerling Global 217 CIGNA Re 2 Swiss Re18 Munich Re 2

1 With a 2% or greater market share2 Based on 1995 SOA survey of U.S. ordinary life reinsurance in force, excluding portfolio reinsurance

and retrocessions

last six years with a combined1995 market share of 27 percent.(See table above)

As a result of this consolidation,there are only 12 reinsurers left todaythat have market shares of 2 percentor more. On average, we’ve lost onereinsurer per year over the last sixyears. At this pace, my actuarial fore-casting skills tell me there will be noreinsurers left in 12 years!

Now let’s look at the currentstate of the market as shown in

Table 2. Of the top six reinsur-ers today, Swiss Re, EmployersRe, and Munich Re are the clearmarket share winners. Theyhave vastly increased theircombined market share from 11percent in 1995 to 48 percent in2001!

In the meantime, TransamericaRe, RGA, and ING Re managed tohold onto a collective 30 percentmarket share, which is down from34 percent in 1995.

Six years ago, the top four U.S.reinsurers were U.S.-owned. Today,only four of the top 12 reinsurers areU.S.- owned. Perhaps you’ve noticedEuropean companies purchasingU.S. life insurers over the last fewyears. That trend is even strongeramong reinsurers. European-ownedreinsurers now account for over two-thirds of all U.S. life reinsuranceinforce, excluding portfolio reinsur-ance and retrocessions.

continued on page 12

12 JUNE 2002

REINSURANCE NEWS

The U.S. life reinsurance markettripled in size from 1995 to 2000.During that time, a number of rein-surers maintained about the samemarket share, namely RGA, AUL,Cologne Re, BMA, and GerlingGlobal.

Employers Re and Munich Retripled their market shares. Whencombined with the three-foldincrease in the size of the market,Employers Re and Munich Re are10 times larger than they were in1995. Swiss Re is 15 times larger,with five times the market share ithad in 1995.

Two reinsurers, ING Re andAllianz, added a couple of points ofmarket share. Only TransamericaRe lost significant market share,but still managed to double its busi-ness in only five years.

As George Santayana said,“Those who cannot remember thepast are condemned to repeat it.”Now that we’ve examined ourrecent past, I’d like to speculate onthe future. I will espouse a large

number of questionable opinions.While I am bound to be wrong, I dohope you will find this interesting,provocative and not too offensive. Tolessen the risk, I’ll talk aboutcompanies in small groups.

The Major Acquirers:Swiss Re, Munich Re,and Employers ReThe clear market share winnersover the last five years—Swiss Re,Munich Re, and Employers Re—have three things in common:

• P&C reinsurance as a core business, which has generally produced poor financial results in recent years,

• Deep pockets and

• Major acquisitions in the U.S.life reinsurance market.

For a few years, these threecompanies stood on the sidelines andwatched the U.S. life reinsurance

business growing very fast and pass-ing them by with public companieslike RGA and Life Re reportingattractive earnings. Not surprisingly,Swiss Re, Munich Re and EmployersRe each decided to expand its U.S.life reinsurance presence throughacquisitions. At the same time, eachmoved its pricing from conservativeto more aggressive.

Acquisitions over the last sixyears have not been cheap—acquirers generally paid top dollar.Having some information aboutmost of these acquisitions, I cantell you roughly what it took tohave the winning bid:

• A willingness to settle for a return on capital in the neigh-borhood of 9-10 percent,

• An assumption that the great majority of expenses could be eliminated through consolidation and

Table 2: U.S. Reinsurers in 20011

Rank2 Company Market Share2 Ownership1 Swiss Re 30% Swiss2 Transamerica Re 11 Dutch3 RGA 11 U.S4 Employers Re 10 U.S.5 Munich Re 8 German6 ING Re 8 Dutch7 AUL 5 U.S.8 Allianz 5 German9 BMA 3 Italian10 Cologne Re 3 U.S.11 Gerling Global 3 German12 Annuity & Life Re 2 Bermudan

1 With a 2% or greater market share2 Based on 2001 SOA survey of U.S. ordinary life reinsurance in force, excluding portfolio reinsurance and

retrocessions, with adjustment to Swiss Re to include Lincoln Re recurring business3 Employers Re stands to gain an additional 4% market share pending its acquisition of American United Life’s

life reinsurance business in 2002

Winners and Losers...

from page 11

JUNE 2002 13

REINSURANCE NEWS

• An assumption that the market share of the acquired company could be added to the market share of the acquiring company,even where that meant main-taining double shares of the new business of many ceding companies.

In general, the acquirers havedone a good job of eliminatingexpenses through consolidation ofoperations. They have also done agood job of holding onto, and insome cases adding to, marketshare—largely through an increasein pricing aggressiveness that wentwell beyond the minor improvementyou’d expect from consolidation-related economies of scale.

What does the future hold forthese companies? First let’sconsider Employers Re, which isowned by General Electric. Due toits large property and casualtyreinsurance business, financialresults have been disappointing,especially by GE standards. GE isnot shy about exiting a marketthat is no longer appealing. TheirWorld Trade Center losses andconcerns about future terroristattacks could result in a decision tosell Employers Re. But who besidesMunich Re might be large enoughand interested enough to buyEmployers Re? With too littledemand, GE may elect to keepEmployers Re and even expand it.

I expect Swiss Re and Munich Reto buy a little more market share,both through acquisition andaggressive pricing. I expect thatthey will earn no better than 9percent of returns on additionalcapital invested. However, suchreturns may be quite attractivewhen compared to recent returns onproperty and casualty reinsurance.

The futures for Swiss Re andMunich Re hinge on a single ques-tion: What will their stockholdersdemand? The answers to this ques-tion hinge in turn on financialreporting issues:

• Will future financial reporting standards allow non-U.S. rein-surers to create earnings on demand by harvesting unreal-ized capital gains?

• Will non-U.S. reinsurers be able to save excess earnings for a rainy day by storing them in contingency or catastrophe reserves?

If the answers to these questionsare “no,” stockholders of non-U.S.reinsurers may be faced with muchmore volatile earnings goingforward.

Munich Re boasts “hiddensurplus” of tens of billions of dollars.If this hidden surplus becomes partof publicly reported capital andsurplus, will it create a demandamong stockholders for distributionof excess capital? Or, if capital isaugmented by hidden surplus, willfinancial results show an unaccept-ably low return on equity?

My best guess is that change isin the air. Many of these financialreporting changes will happen, butnot quickly. However, before the endof this decade, I think you will seeseveral changes including:

• The reporting of more volatileearnings,

• The reporting of more realistic capital and surplus,

• Extraordinary dividends paid to stockholders to distribute excess capital and achieve a better balance between capital and risk and

• A renewed emphasis on the pricing discipline that helped Swiss Re and Munich Re become world-class leaders in the reinsurance business.

My prediction is that over thenext few years, Swiss Re will strug-gle to maintain its market share

while Munich Re acquires addi-tional market share. After that, Iexpect both companies to lose someground as they switch their focusfrom market share to producingsatisfactory returns on equity fortheir stockholders.

The Friendly Giants: Transamerica Re, RGA, and ING ReThe other three of the top six U.S.reinsurers have grown their busi-nesses organically, rather thanthrough acquisitions. While largein the U.S. life reinsurance busi-ness, each of these reinsurers isonly a small part of a much largerparent. Transamerica Re is whollyowned by Aegon, RGA is almost 60percent owned by MetLife, and INGRe is part of ING. For each of theseparent companies, reinsurance isnot a core business.

I think a strong parental influ-ence has contributed to a generallygreater pricing discipline shown bythis group in recent years. With luckand cleverness, Transamerica RE,RGA and ING Re may be able tohold onto market share because oftheir economies of scale, establishedreputations and relationships andthe special products and servicesthey bring to bear.

On the other hand, for the rightprice, each of these reinsurers couldbe purchased, just as Lincoln Rewas recently purchased by SwissRe. However, to the extent thatthese companies produce goodfinancial results and generally keeptheir owners happy, the right pricemay be too high for a prospectivebuyer.

Collectively, I expect TransamericaRe, RGA, and ING Re to gain or losea little market share over the nextfew years. Aggressive pricing byacquirers and new entrants wouldtend to decrease their marketshares. Countering this, the desireamong ceding companies to spread

continued on page 14

14 JUNE 2002

REINSURANCE NEWS

their risk among major reinsurerscould help increase their marketshares. For example, even withaggressive pricing, it may be impos-sible for Swiss Re to hold onto a 30percent market share when mostcompanies prefer to split their rein-surance between four or morereinsurers.

Each of these companies hasexperienced some large write-offs orsignificant turnover over the lastfew years, which cannot be pleasingto their parents. As a result, I wouldnot be surprised if TransamericaRe, RGA and/or ING Re andTransamerica Re were acquiredover the next few years.

The Lonely Lighthouse—American United LifeNine of the top 10 reinsurers haveparents with market capitalizationof at least $20 billion. The loneexception is AUL, whose reinsur-ance business haslighted its way andbecome its most impor-tant line of business.

As a mutual holdingcompany, AUL haslimited access to capitalneeded to continue itsgrowth. Recent lossesfrom the World TradeCenter terrorist attacksmay have been the finalimpetus to AUL’s deci-sion to sell its life reinsurancebusiness. With an efficient, good-sized life reinsurance organization,AUL had a choice of buyers. In Mayof this year, AUL announced thesale of its life reinsurance businessto Employers Re.

The Europeans areComing!The Europeans are coming! No,wait—they’re already here! We’vealready reviewed Swiss Re, Munich

Re, Aegon, and ING. That’s just thetip of the iceberg.

Allianz and BMA aresmaller reinsurers with verylarge parents—so large, in fact,that reinsurance results maybe rounding error to their ulti-mate parents. Allianz andGenerali seem to be lettingtheir U.S. operations run theirown show as long as results aresatisfactory.

While Allianz and BMA are moreaggressive pricers than they werefive years ago, they still seem to putmore emphasis on financial resultsover market share. Unless resultstake a turn for the worse, U.S.management should have no incen-tive to sell their reinsuranceoperations. I expect Allianz andBMA to maintain or grow theirmarket share. Like other survivors,they should benefit from furtherconsolidation as ceding companiescontinue to spread their reinsur-ance among multiple reinsurers.

Cologne Re, now called Generaland Cologne Re, was acquired by

General Re in the mid-1990s. Four years ago,General Re was acquiredby Berkshire Hathaway,Warren Buffett’s company.(Warren is famous forbeing a distant relative ofJimmy Buffett, but Idigress.) In spite of itsU.S. ownership, Generaland Cologne Re’s life rein-surance business isprimarily European.

In March of 1999, when massiveworkers compensation losses weredisclosed, General Re infusedhundreds of millions of dollars toCologne Re to stabilize the situa-tion and restore customerconfidence. Since then, their U.S.life reinsurance unit has experi-enced some significant turnover,has become understandably moreconservative, and its growth haslagged behind most of the industry.

Based on Cologne Re’s success in

some life reinsurance marketsoutside the U.S., I predict that their

U.S. life reinsurance operationwill be allowed to continue onits conservative course. OnceU.S. market conditionsimprove and confidence in thelife reinsurance business isrebuilt, Warren and Jimmymay surprise us. General and

Cologne Re could find itself a smallU.S. player with a very large parentwilling to bankroll a tremendousamount of growth.

Gerling Global and two smallerU.S. players–Hannover Re andSCOR Re–are mid-sized, European-based companies specializing inproperty and casualty reinsurancewith life operations in a number ofcountries around the world.

In the U.S. and some other lifereinsurance markets, I see thesecompanies faced with a choice:Either grow the local operation tocapture a significant market shareor exit the market. I think one ortwo of these companies will decideto concentrate its resources on itscore P&C business, while refocusinglife reinsurance efforts primarily onits more profitable domesticmarket. As a result, expect one ortwo of Gerling Global, Hannover Re,and SCOR Re to sell its U.S. lifereinsurance operations, but not anytime soon. I think the remainingone or two mid-size European rein-surers will commit to developing amore significant presence in theU.S. life reinsurance market, prima-rily through an acquisition over thenext few years.

The Bermuda HighI’ll finish with the two significantnew entrants to the U.S. mortalityrisk market—Annuity and Life Re,and Scottish Re—Both Bermuda-based, publicly held companies.These two companies have beenquite active in the U.S. life reinsur-ance market over the last couple ofyears. Their IPOs in 1998 raised atotal of almost $600 million, along

Winners and Losers...

from page 13

JUNE 2002 15

REINSURANCE NEWS

with considerable pressure fromWall Street to quickly deploy thatcapital.

These two IPOs were successfulbecause of the rapid growth takingplace in the U.S. life reinsurancemarket coupled with competitiveadvantages already demonstrated byoffshore P&C reinsurers, namely theuse of more favorable GAAP account-ing, a zero percent corporate tax rate,and the low overhead typically asso-ciated with a start-up operation.

As with all new entrants,Annuity and Life Re and ScottishRe have found the U.S. life reinsur-ance market a hard nut to crack. Ittakes years to build the relation-ships and reputation needed tocompete on an equal footing withmore established players. In themeantime, both reinsurers havecompensated by using a low-pricestrategy to penetrate the market.

Because some clients won’t sendbusiness offshore and because U.S.tax regulations make it difficult for anon-U.S. taxpayer to market to U.S.customers, both Bermudan reinsur-ers have established U.S. lifereinsurance subsidiaries. Their salesresults to date have been trulyamazing. Combined, the two compa-nies boast GAAP assets of $4 billionand GAAP revenue of $500 million—and this is after less than four yearsof serving the U.S. market.

Regarding profits, annuityresults to date have been disap-pointing, mainly due to losses fromone large annuity block. So far, liferesults have been encouraging, butlife reinsurance results can bedistorted by lags in reporting.When you’re growing fast and lagsare increasing, profits tend to getoverstated. I learned that the hardway. When my company’s adminis-tration finally caught up with thegrowth of the business, backdatedpremium refunds knocked earningsfor a loop. Thankfully, that wasbefore we were a public company!

Given the thin margins on thebusiness most reinsurers have

written over the last few years, prof-its are more sensitive than ever tothe effect of lags. A company with alow-price strategy would have profitseven more sensitive to lags.

My best guess is that, over thenext few years, the Bermudan rein-surers will show a return on capitalthat disappoints investors. Bothcompanies have seen their stockprices fall to within a few percent ofage points their book values. If thestock price were to fall much belowbook value, there would be pressureto sell or liquidate the company. Ifone company performs much betterthan the other, look for the betterperformer to acquire the other andmerge the two operations.

A Look Ahead to 2006In summary, over the next fouryears, I think the U.S. market willconsolidate down to eight significantreinsurers with market shares ofthree percent or more. I think theeight winners will face a more stablefuture, with little or no additionalconsolidation, few new entrants, andpricing that more regularly producessatisfactory returns to shareholders,at least on new business.

As a postscript, I’d like to pointout that there are strong forces atwork that may be bringing morepricing discipline to the market asyou read this:

• The demand and perceived value of reinsurance is up and,due to capital losses and World Trade Center losses, the supply is down. That should cause reinsurance prices to firm up.

• Losses from the terrorist attacks and other recent earn-ings surprises are causing many reinsurers to reexamine their approaches to pricing, risk management and the connec-tion between the two.

• The Enron scandal has many reinsurers reexamining the

risks associated with movingbusiness offshore, including unknown future letter-of-credit availability and costs, the finan-cial handcuffs associated with long term placement of assets in trust and the risks associated with guaranteeing offshore companies.

• Some reinsurers have accumu-lated and analyzed a mountain of relevant mortality and lapse information by tracking the results of many millions of indi-vidual policies. This enables them to make better pricing decisions. Reinsurers without such information could become the victims of those that have it.

If these forces produce a stabiliz-ing or upward influence on prices,profit margins and returns will rise,but probably at the expense ofslower growth, since reinsurancesales are made to very astute andextremely price-sensitive buyers. Inthe past, many reinsurers have beenable to walk the fine line thatcombines rapid growth withadequate profitability. As the U.S.life reinsurance market consolidates,this will become both more difficultdue to the stronger competitors andeasier due to fewer competitors.

Four years from now, you mayrecall this article and marvel athow incredibly wrong these predic-tions were. It might be interestingto follow up in 2006.

David Atkinson, FSA, MAAA, isexecutive vice president and COO ofReinsurance Group of America Inc.in Chesterfield, MO, and co-author,with Jim Dallas, of the SOA’s newbook for product development andfinancial management, LifeInsurance Products and Finance.He can be reached at [email protected].

16 JUNE 2002

REINSURANCE NEWS

Editor’s Note: As mentioned previously inthis newsletter, this article was originallypart of the Special Edition Newsletterthat never was. The Reinsurance Sectionasked Jim to prepare this article on theSPRA for the newsletter. While SPRA isassociated with Swiss Re, this is not anadvertisement for business, but is forinformational purposes only. Thank you,Jim, for the article.

September 11, 2001, wasunprecedented in its tragicramifications on both a

personal and business level.Insurers, whose business is tomanage risk, are now looking at newissues and questions about how tomanage a world whose risks includesuch horrific acts. The property andcasualty industry has a proposed billin Congress for establishing a terror-ism reinsurance pool. The ACLI hasbeen discussing a potential high-level government backstop for thelife insurance industry.

Insurance companies use variousmechanisms to control volatility ofrisks, and ultimately, solvency.Companies set a maximum amount,i.e., a retention, which they willretain on any one life. Some may alsouse first-dollar quota share to furtherreduce volatility. Even with theseelements, many insurance companiestake steps to reduce the effects of acatastrophe, which, in insuranceterms, is defined as an event causingthe insured to have three or moreclaims that add up to more thansome predetermined deductible.

One way to reduce a catastro-phe’s effects is to buy traditionalcatastrophe coverage. Another is toparticipate in a catastrophe pool.Both are typically one-year cover-ages. With a traditional coverage,the premiums (the insured costs)are known upfront. The pool, on theother hand, should result in longer-term lower net costs and can coverrisks that are too unpredictable tobe priced for in a traditional cover.

SPRA’s assessmentpoolsSpecial Pooled RiskAdministrators, Inc. (SPRA)

administers both an ordinary and agroup assessment catastrophe pool.Each member has a share of thepool (either ordinary or group)based on the company’s in forceand number of policies relative toall others in the pool. When acatastrophe does occur and amember has three or more claimsabove its deductible, all membersare assessed. To make an assess-ment pool work well, you need asignificant number of companies.This allows a substantial maxi-mum claim cover while stilllimiting the potential assessmentto any single member.

SPRA pools are fortunate toenjoy a wide number of companieswith substantial in force.Currently, the ordinary pool repre-sents 111 life companies with morethan $3 trillion of in force (roughlya third of the industry). Throughunique formulas to determine thedeductibles and pool shares, largeand small companies are treatedequitably. As such, a wide varietyof company sizes are represented.The pool maximums are $50million per company and $125million in aggregate. The grouppool has 42 life companies with $1trillion of in force (roughly a sixthof the industry). The maximumsare $0.20/1000 ($200 million) and$0.50/1000 ($500 million).

Questions afterSeptember 11The tragedy of September 11, 2001,was unprecedented for the SPRApools. Although the pools havebeen around for more than 25years and have administered morethan $50 million of catastrophicclaims, nothing has ever come closeto the impact of September 11.Estimates from the ordinarymembers total $250 million, andestimates from the group memberstotal $160 million.

Not surprisingly, experience isanything but uniform by company.Several companies, both large andsmall, had very few claims. Severalother companies (again both largeand small) had a disproportionate

amount of claims. The pool will dowhat it was designed to do—spreadthe effects of the catastropheevenly over its member base.

The terrorist attack does causesome challenges in administeringthe pools. For example:

• How many insurable events were there? Most within theindustry have argued the WorldTrade Center’s Twin Tower attack of Sept. 11 was a single event, citing the “cause” analy-sis with various case law exam-ples. But others (such as the owner of the World Trade Center’s Twin Towers) have suggested each tower attack should be treated as a separate insurable incident. SPRA has informed its members that it accepts the “cause” analysis and intends to administer the attacks as one event.

• Should the ordinary limit be raised? Given that one event occurred, an aggregate limit of $125 million and estimates of $250 million, only 50 percent of the claims are being spread.

• Where do we go from here?Many are saying the world has now changed. Several compa-nies are finding at renewal that traditional catastrophe covers are more limited in scope (excluding terrorism and/or war) and premiums have been increased. SPRA is soliciting input from its members on any potential changes going forward.

James B. Keller, FSA, MAAA, is avice president of Swiss Re in FortWayne, IN. His current responsibili-ties are business engineer forfinancial reinsurance and AdminRe™. Jim can be reached [email protected].

SPRA Pools in Light of September 11th Tragediesby James B. Keller

JUNE 2002 17

REINSURANCE NEWS

Editor’s Note: Copies of the full studies (text and tables) areavailable in the Reinsurance Section area of the SOA homepage www.soa.org.

Manulife Reinsurance, in conjunction with theReinsurance Council of the Society ofActuaries, conducts an annual study of

mortality experience on large amount and older agepolicies. The experience data wassubmitted to the Society ofActuaries by six companies.The consolidated data isanalyzed in terms of mortalityratios by number and amount,and the results are furthersubdivided by age, sex, dura-tion, smoking and underwritingstatus, reinsurance method andlevel of retention.

The exposure includes onlysingle life policies issued in theUnited States and valued in U.S.dollars. Expected deaths are basedon 100% of the SOA 1975-80 Select& Ultimate table which varies byage and sex, age nearest and age lastbirthday. The basic tables wereextended to issue age 90 and theresulting tables were used to calculatethe expected mortality for issue agesgreater than 70. Ultimate ages were also extended toage 105 from age 100, starting with the 1991 study.

The 2001 Large Amount study covers experience forcalendar years 1997 and 1998. Manulife has beenconducting these studies since 1990, covering experi-ence during calendar years 1987 and later. TheAdvanced Age study has been conducted since 1993,covering experience in calendar years 1990 and later.Both studies present results individually for each ofthe two most recent calendar years as well as a cumu-lative result of all study years. The results of theAdvanced Age and Large Amount studies will bediscussed separately.

2001 Large Amount Study: Results

Policies for large amounts are those with a total faceamount greater than $1 million.

1997 and 1998 Results:The experience underlying the 1997 and 1998 data isbased on total exposures of $64 billion and $77 billion,respectively. Claims in 1997 were $77 million and in1998 they were $101 million. The total 1997 exposureby number is 231,965 (275,823 in 1998). In 1997, 168claims were reported (353 in 1998). The 1998 expo-sures by number and total claims represent thelargest in this study’s history.

The overall mortality ratios by amount for the1997 and 1998 study are 34% and 37%, respec-tively. By number, the ratios for the 1997 and 1998study are 27% and 48%, respectively.

1987 to 1998 Results:The experience underlying the 1987 to 1998data is based on a total exposure of $780 billionand claims of $1.6 billion. The total exposureby number is 1,597,918 with 2,395 claims.

The overall ratio by amount is 56 percent.This ratio decreases slightly when measuredon a “by number” basis to 54 percent.

This year’s study includes an analysis of theratios (and supporting exposure) by a five year rollingaverage and a four year period average. The additionaldata allows the reader to more easily view the mortalitytrends and assign credibility to those trends.

The mortality ratios are also presented for variousclassifications—first for 1997 and 1998 experience, andthen the cumulative result for the entire study periodfrom 1987 to 1998.

Sex: Males comprise approximately 88% of the 1997 and 1998 exposure by number (and by amount). Close to one-fifth of all male claims are classified as misadventure.

Highlights of the 2001 Manulife Reinsurance Mortality Studyby Manon Laverdière and Valerio Valenti

continued on page 18

18 JUNE 2002

REINSURANCE NEWS

The mortality ratio by amount for males in 1997 is 38% and for females it is 11% (1998: 38% for males, 33% for females).

The mortality ratio by number in 1997 is 28% for males and 16% for females (1998: 47% for males, 53% for females).

Based on data from 1987 to 1998, themortality ratio by amount for males is 55% and for females it is 62%. During this period male exposure was 90%.By number, the mortality ratios are 53% and 59% for males and females,respectively. Over the years female mortality has shown more improve-ment than male mortality.

Issue Age: Issue ages 30-49 represent approxi-mately 75% of the 1997 and 1998 exposure by number and approx-imately 70% of the exposure by amount. However, actual claims paid are highest in the age category 50-59 for both the 1997 and 1998 data.

The mortality ratio by amount in 1997 is 40% for issue ages 50-59 (38% in 1998). By number the 1997 ratio is 34% (51% in 1998).

From 1987 to 1998, 54% of the largest claims (over $5 million) were in the age band 50 to 69.

Policy Years: Exposure by number and by amount is the highest for the first two policy durations. The 1997 mortality ratio by number for duration one and two is 19% and 30%, respectively (36% and 29% in 1998). This compares favorably when compared to the average ratios for all durations (27% in 1997, 48% in 1998).

The 1997 mortality ratio by amount for both durations one and two is 16%.The 1998 ratios are 26% and 20%,respectively. Both 1997 and 1998 ratios are considerably better than the overall amount average of 34% in 1997 and 37% in 1998.

The 1987 to 1998 cumulative mortal-ity ratio by amount at duration one is 55% (partly due to large aviation claims in the study’s early years). It then decreases at duration two (44%) and increases over the next two durations from 51% to 56%.

In 1997 and 1998, seven out of the 19 claims with Direct Face Amounts over$5 million occurred during the first three policy durations, the remaining claims occurred in duration six andover.

Smoking Status: The mortality ratio by amount for non-smokers is 34% in both 1997 and 1998.The ratio for smokers is 56% in 1997 (49% in 1998). The exposure by amount in 1997 for non-smoker,smoker and aggregate policies are 71%, 6%, and 23% respectively (In 1998, 89%, 6%, 5%).

The overall ratios (1987-1998) by amount for non-smoker and smoker are 48% and 104%, respectively. The ratio of smoker to non-smoker mortal-ity has decreased considerably over the years. In fact, in some years the smoker ratio is less than the non-smoker ratio. However, the smoker exposure by amount is only 7% of the study and thus has low credibility.

Note that the expected 75-80 Basic Tables are not differentiated by smoker status.

Highlights of the 2001 ...

from page 17

JUNE 2002 19

REINSURANCE NEWS

UnderwritingStatus: The mortality ratio by amount for

standard policies is 32% in 1997 (34% in 1998). For substandard policies, the ratio increases to 47% in 1997 and to 59% in 1998. Approximately 96% of the exposure is accounted for by standard policies.

The overall standard ratio by amount from 1987 to 1998 is 56% (55% for substandard).

ReinsuranceStatus: The 1997 mortality ratio by amount is

21% for automatic business, and 55% for facultative (1998: 36% for auto-matic and 40% for facultative). Theexposure by dollar amount is approxi-mately 80% for automatic business in both 1997 and 1998.

The 1987 to 1998 overall amount ratio is 47% for automatic and 64% for facultative business. The facultative exposure has decreased steadily since the study’s inception. In the late 1980s, facultative business comprised more than 50% of the study’s data.

Plan of Insurance: A large portion of contributors did not

submit a plan of insurance code, and therefore, the results by plan are not very credible.

The plan of insurance was provided forapproximately half of the business submitted (and almost all of it was for Term) for 1997 and 1998 data. In 1997, Term had a 22% ratio by number and 38% ratio by amount (in 1998 the ratios were 47% and 43%,respectively).

Method of Reinsurance: The 1997 mortality ratio by amount

is 30% for YRT and 37% for Coinsurance (1998 ratios are 26% and 20%, respectively).

Data collection for reinsurance methodbegan in 1991. The 1991 to 1998 mortality ratio by amount is 48% for YRT and 50% for Coinsurance.

2001 Advanced Age Study: Results

Policies for advanced age are those with an issue age of70 or over.

1997 and 1998 Results:The experience underlying the 1997 and 1998 data isbased on total exposures of $1.9 billion and $2.3billion, respectively. Claims in 1997 were $12 millionand in 1998 they were $19 million. Total exposure bynumber in 1997 and 1998 was 20,578 and 28,175,respectively. In 1997, 237 claims were reported (333 in1998). The 1997 and 1998 exposure by number andthe 1998 claim number are the largest in this study’shistory.

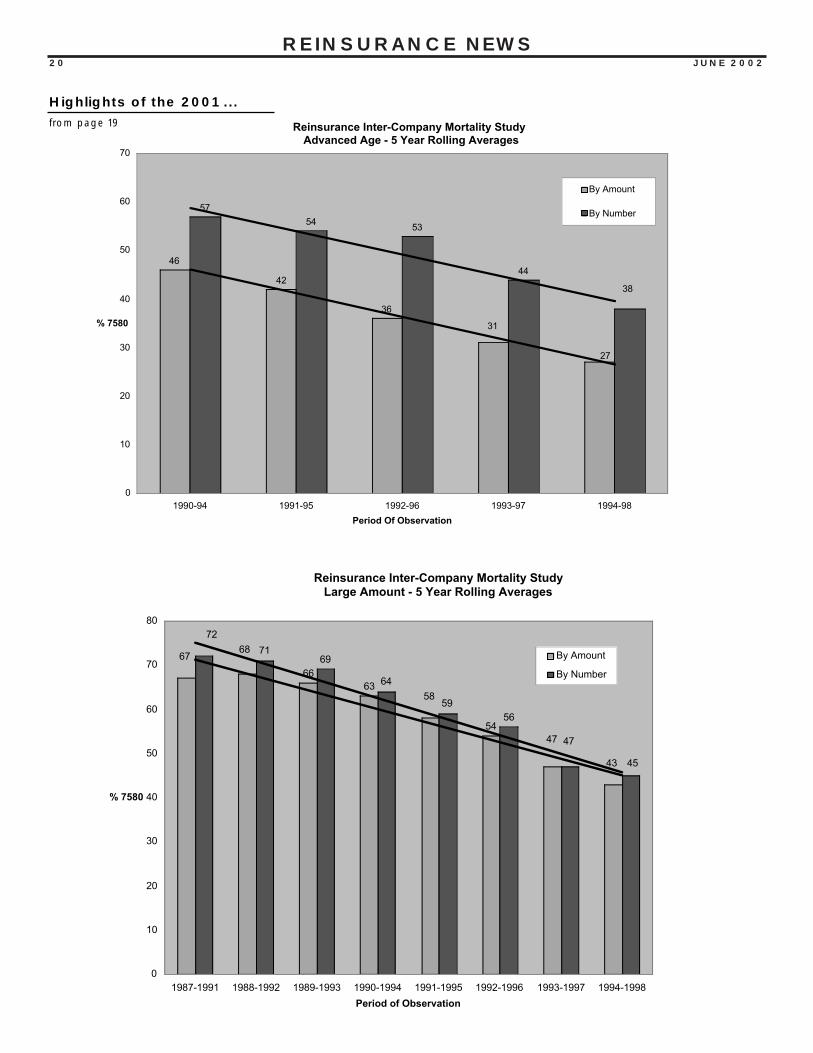

The overall mortality ratios by amounts for the 1997and 1998 study are 19% and 24%, respectively. Bynumber, the ratio for the 1997 data is 27% (31% in1998).

1990 to 1998 Results:The experience underlying the years 1990 to 1998 isbased on a total dollar exposure of $15.5 billion. Duringthose years, $188 million of claims were experienced.The total 1990 to 1998 exposure by number is 115,106policies with 2,023 claims.

The overall mortality ratio by amount for the 1990 and1998 study is 36%. By number, the overall ratio is 45%.

continued on page 20

20 JUNE 2002

REINSURANCE NEWS

Reinsurance Inter-Company Mortality Study Advanced Age - 5 Year Rolling Averages

46

42

36

57

5453

44

27

31

38

0

10

20

30

40

50

60

70

1990-94 1991-95 1992-96 1993-97 1994-98

Period Of Observation

% 7580

By Amount

By Number

Reinsurance Inter-Company Mortality StudyLarge Amount - 5 Year Rolling Averages

6663

54

7169

64

5956

58

6867

47

43

72

47

45

0

10

20

30

40

50

60

70

80

1987-1991 1988-1992 1989-1993 1990-1994 1991-1995 1992-1996 1993-1997 1994-1998

Period of Observation

% 7580

By Amount

By Number

Highlights of the 2001 ...

from page 19

JUNE 2002 21

REINSURANCE NEWS

There is a decreasing trend in both ratios when analyzedon each of a moving average and period average.

The mortality ratios are also presented for the vari-ous classifications, first for 1997 and 1998 experienceand then the cumulative result for the entire studyperiod from 1990 to 1998.

Sex: In 1997 and 1998, 45% of policy amounts were from male lives. This marks the first time in this study’s history that female amounts out-number the male amounts.

By amount, the ratio for males is 20% in 1997, and 22% in 1998. By amount the ratio for females is 17% in 1997 and 27% in 1998.

The mortality ratios by number for males in 1997 and 1998 are 27% and 29%, respectively. Similarly, the femaleby number ratios are 28% in 1997 and 33% in 1998.

The mortality ratios by amount for 1990 to 1998 data are 35% for males and 38% for females. Ratios by num-ber during the period are 44% and46% for males and females, respectively.

Issue Age: By amount, approximately 65% of policies (75% by number) have issue ages between 70 and 74 in both 1997 and 1998. By amount in 1997, the age

band 70 to 74 experienced a ratio of 14% (27% in 1998). The age band 75 to 79 experienced a 30% ratio in 1997 (26% in 1998).

Policy Years: By policy year, the ratios vary greatly from one duration to the next.

In 1998, approximately half of all exposures by number and by amount are in durations one and two,compared to 41% for the 1997 data.The mortality ratio by amount at duration 1 is 16% in 1997 and 24% in 1998.

From 1990 to 1998, the overall by amount ratio for duration one is 31%.

Advanced Age Inter-Company Mortality Study

1990-94 1991-95 1992-96 1993-97 1994-98By Amount 46 42 36 31 27By Number 57 54 53 44 38

1987-91 1988-92 1989-93 1990-94 1991-95 1992-96 1993-97 1994-98By Amount 67 68 66 63 58 54 47 43By Number 72 71 69 64 59 56 47 45

continued on page 22

22 JUNE 2002

REINSURANCE NEWS

Smoking Status: The 1997 non-smoker and smoker ratios by amount are both approxi-mately 19%. The 1998 non-smoker ratio by amount is 24%, and surprisingly the smoker ratio is lower at 16%. However, since there are far fewer smoker exposures (10% vs. 90% for non-smokers), the validity of the smoker result is weak.

From 1990 to 1998, the ratio by amount for non-smoker is 31% (63% for smoker).

Underwriting Status: The mortality ratio by number for

standard policies is 23% and 22%, for 1997 and 1998 data, respectively. The 1997 substandard ratio by amount is 8% (29% for 1998 data). However, the standard exposure is nearly four tofive times more than substandard exposure. The cumulative 1990 to 1998by amount ratio for standard policies is 37% and for substandard it is 35%.81% of the exposure by amount is comprised of standard policies.

Reinsurance Status: In 1997 and 1998, the exposure by

number for automatic reinsurance is approximately 90% for both years.However, the exposure by amount for automatic business comprises on average 65% of the study’s data.

The ratio by amount for policies rein-sured automatically is 20% (17% for facultative) for 1997 data, and 21% (28% for facultative) for 1998 data.

The 1990 to 1998 cumulative ratio by amount for policies reinsured auto-matically is 32%, compared to 39% for facultative policies. In the study’s

early years (1990 to 1992), facultative was approximately double the auto-matic exposure by amount. However,in the last few years, automatic rein-surance is now double the facultative exposure.

Plan of Insurance: In this year’s two year study, many