regulatory update: eu and uk liquidity regime interim · pdf fileeu and uk liquidity regime...

TRANSCRIPT

www.lombardrisk.com

Regulatory update:

EU and UK liquidity regime

Interim LCR, AMM and much more!(EU Leverage Ratio, Funding Plan Templates and

Supervisory Benchmark Portfolio…)

Tuesday 28th July 2015

Lombard Risk | Enabling regulatory compliance

3RD IN 2015 regulatory webinar series29TH since series started!

www.lombardrisk.com

Welcome and introductionRebecca Bond, Group Marketing Director

PresentationJames Phillips, Global Director Regulatory Strategy

Introducing …Edward Cole, Regulatory Strategy Manager

Real-time polling questions

Questions & Answers

Online questionnaire upon exit

Webinar agenda – < 60 min

Lombard Risk - | Enabling regulatory compliance

www.lombardrisk.com

2 STREAMS: (i) Regulatory updates(ii) Collateral management

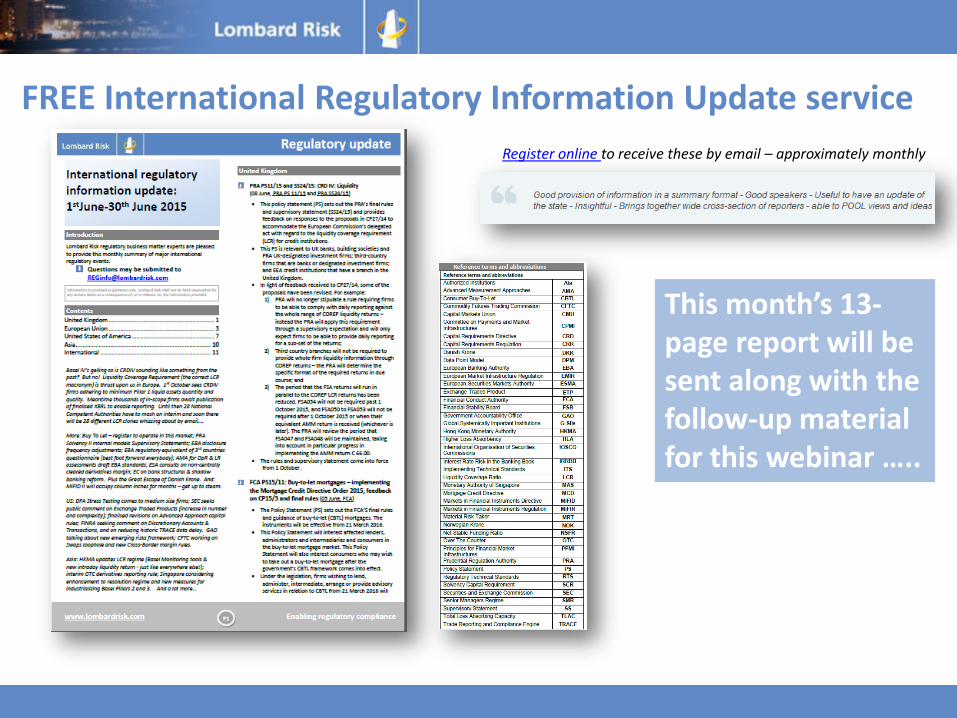

FREE International Regulatory Information Update service

Email: [email protected]

Please give us your opinion by completing the short, online questionnaire that appears on screen after the webinar

Register online to receive these by email – approximately monthly

“Has become industry renownedas THE regulatory update series”

www.lombardrisk.com

FREE International Regulatory Information Update service

Register online to receive these by email – approximately monthly

This month’s 13-page report will be sent along with the follow-up material for this webinar …..

www.lombardrisk.com

www.lombardrisk.com/events

Regulatory programme - 2015

13th February EBA EU and PRA UK liquidity regime: LIQREP (1)

15th April EBA EU and PRA UK liquidity regime: LIQREP (2)

16th June

“2nd ANNUAL REGULATORY UPDATE” EVENT

REPORTER User Group

TODAYEBA EU and PRA UK liquidity regime: LIQREP (3)

Interim LCR, AMM and much more!

4th AugustThe recast Deposit Guarantee Schemes Directive (DGSD)

- developing the Single Customer View (SCV)

1st September PRA branch reporting requirements

13th October Basel IV – revised standard approach

n.b. Look under www.lombardrisk.com/past-events for earlier webinars

www.lombardrisk.com

Over 300 delegates!

http://www.lombardrisk.com/products/regulatory-compliance/reporter/2nd-annual-regulatory-update-conference

www.lombardrisk.com

Introducing:

Edward ColeRegulatory Strategy

ManagerEd Cole joins the regulatory strategy team.Previously Ed was a business analyst and on-boarding manager at Deutsche Boerse, providing regulatory reporting solutions to EMIR & REMIT requirements, and ongoing change in global compliance, including Mifid II.

He has 15+ years’ investment banking experience in the trading, sales and analysis of fixed income products, particularly inflation bonds and derivatives, project leadership of a bespoke electronic trading platform for derivative products, and the start-up of an alternative, intelligence led pricing model, for the insurance of satellites.

Email: [email protected] / [email protected]

Lombard Risk - | Enabling regulatory compliance

www.lombardrisk.com

Regulatory update:

The recast Deposit Guarantee

Schemes Directive (DGSD)

- developing the Single

Customer View (SCV)

4th August 2015

Lombard Risk | Enabling regulatory compliance

www.lombardrisk.com

What is the Single Customer View?

When will it come into effect?

Who will be effected by it?

How will the directive be implemented?

Summary

Agenda

Lombard Risk - | Enabling regulatory compliance

www.lombardrisk.com

Quick review

A key element of the Deposit Guarantee Schemes Directive

(DGSD) is the requirement on deposit takers to develop a Single

Customer View (SCV), to allow scheme administrators to make

faster pay-outs

The update to the SCV has already begun but the transition to

final delivery continues through to December 2016

It is relevant to UK banks, building societies and credit unions,

UK branches of European Economic Area (EEA) credit

institutions, third-country firms with PRA deposit-taking

permission, dormant account holders and dormant account fund

operators

Reporting will require fully electronic direct transmission with

enhanced customer security, shorter timeframes (reports and

pay-outs), more rules and requirements

Lombard Risk - | Enabling regulatory compliance

www.lombardrisk.com

Introducing Lombard Risk

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

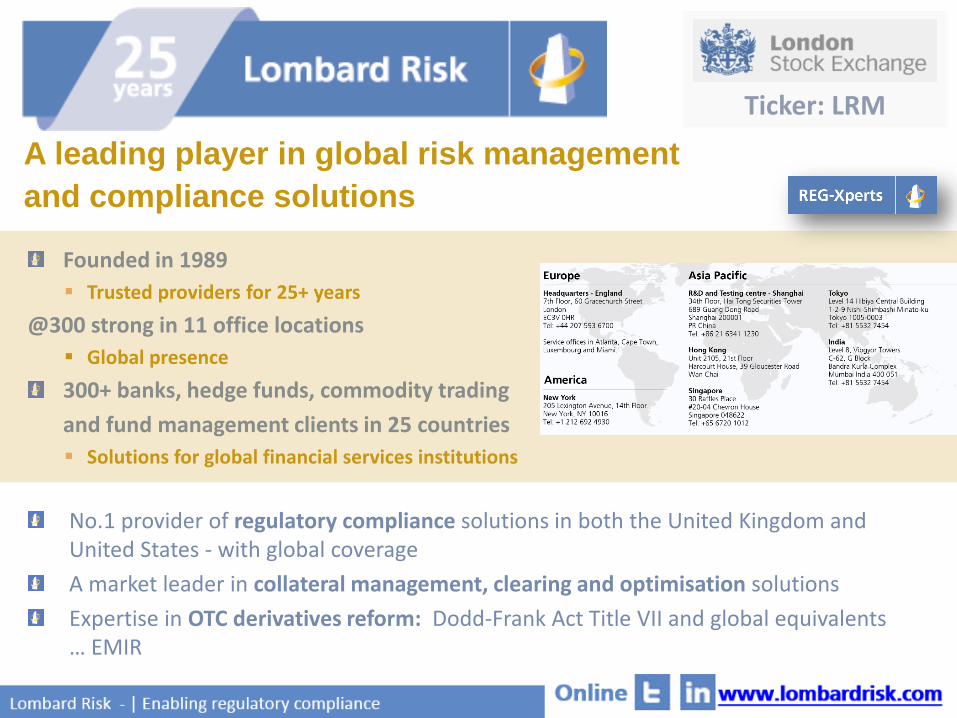

A leading player in global risk management

and compliance solutions

Founded in 1989

Trusted providers for 25+ years

@300 strong in 11 office locations

Global presence

300+ banks, hedge funds, commodity trading

and fund management clients in 25 countries

Solutions for global financial services institutions

No.1 provider of regulatory compliance solutions in both the United Kingdom and United States - with global coverage

A market leader in collateral management, clearing and optimisation solutions

Expertise in OTC derivatives reform: Dodd-Frank Act Title VII and global equivalents … EMIR

Ticker: LRM

www.lombardrisk.com

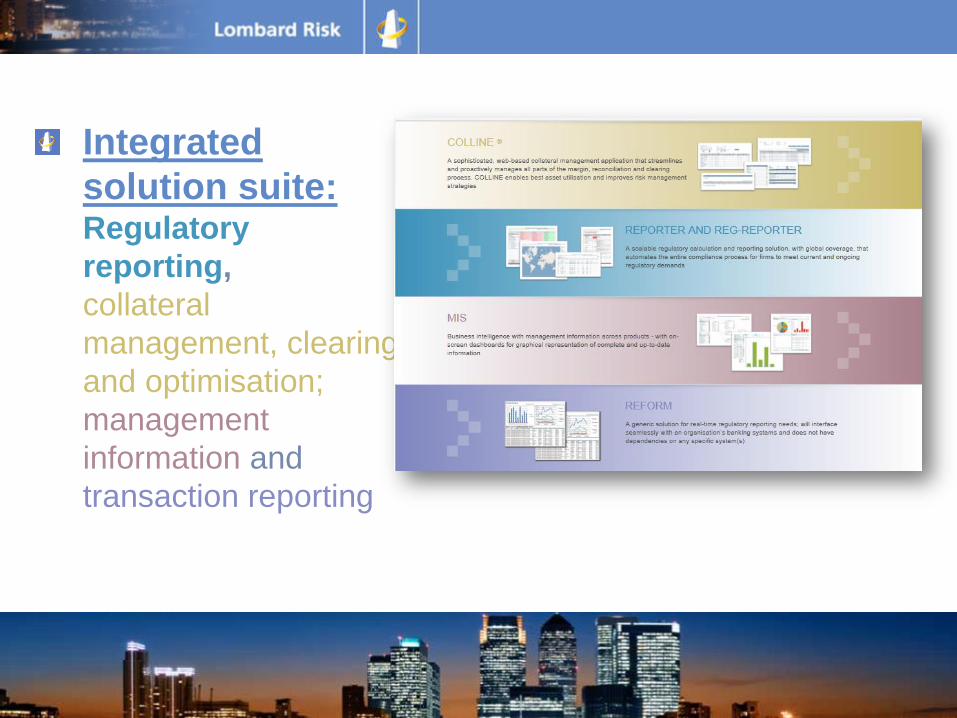

Integrated

solution suite: Regulatory

reporting,

collateral

management, clearing

and optimisation;

management

information and

transaction reporting

www.lombardrisk.com

Speaker:

James PhillipsGlobal Director

Regulatory Strategy

James Phillips has responsibility for Lombard Risk’s regulatory solution strategy.

He is an industry expert on regulatory issues monitoring them on a global, regional and country/regulator basis through frequent interaction with regulatory groups and financial institutions. As a result he fully understands financial services institutions’ operational procedures relating to internal and external monitoring and reporting demands.

Email: [email protected] / [email protected]

Lombard Risk - | Enabling regulatory compliance

www.lombardrisk.com

Agenda

Lombard Risk - | Enabling regulatory compliance

Liquidity reporting: what's coming up and why

Legislative framework and timeframe

Implementation of LCR

Implementation of AMM

PRA expectations

THREE TIMES THE FUN

Consider also the other moving pieces

Other horizons to beware of…

Project work & ongoing preparation for all this?

Holiday edition!

www.lombardrisk.com

Liquidity reporting: what's coming

up and why

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Lombard Risk - | Enabling regulatory compliance

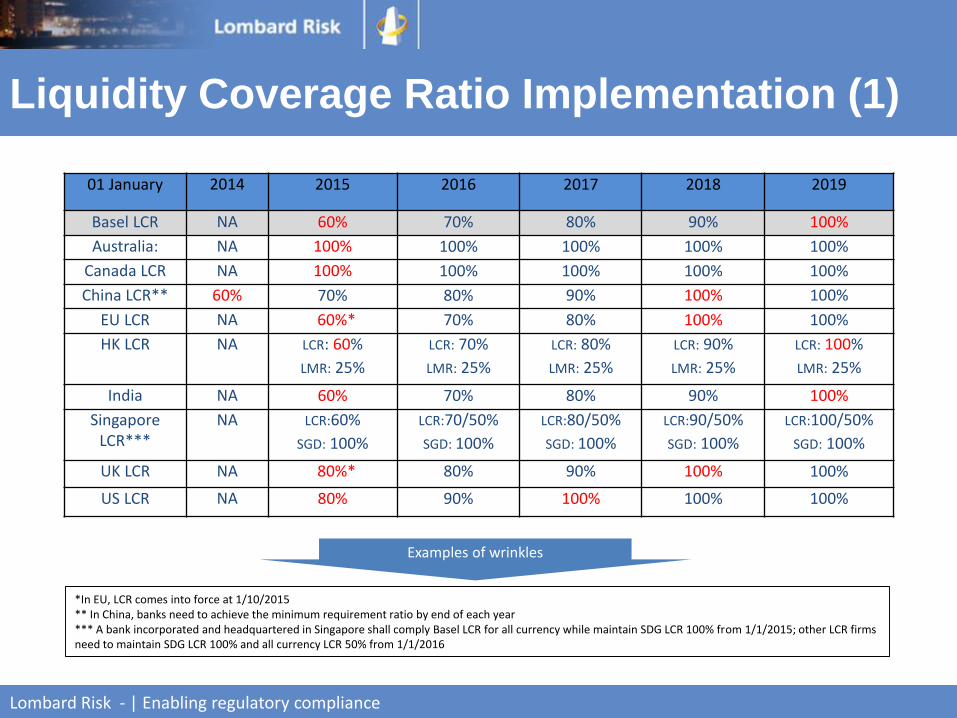

Liquidity Coverage Ratio Implementation (1)

01 January 2014 2015 2016 2017 2018 2019

Basel LCR NA 60% 70% 80% 90% 100%

Australia: NA 100% 100% 100% 100% 100%

Canada LCR NA 100% 100% 100% 100% 100%

China LCR** 60% 70% 80% 90% 100% 100%

EU LCR NA 60%* 70% 80% 100% 100%

HK LCR NA LCR: 60%

LMR: 25%

LCR: 70%

LMR: 25%

LCR: 80%

LMR: 25%

LCR: 90%

LMR: 25%

LCR: 100%

LMR: 25%

India NA 60% 70% 80% 90% 100%

Singapore LCR***

NA LCR:60%

SGD: 100%

LCR:70/50%

SGD: 100%

LCR:80/50%

SGD: 100%

LCR:90/50%

SGD: 100%

LCR:100/50%

SGD: 100%

UK LCR NA 80%* 80% 90% 100% 100%

US LCR NA 80% 90% 100% 100% 100%

*In EU, LCR comes into force at 1/10/2015** In China, banks need to achieve the minimum requirement ratio by end of each year*** A bank incorporated and headquartered in Singapore shall comply Basel LCR for all currency while maintain SDG LCR 100% from 1/1/2015; other LCR firms need to maintain SDG LCR 100% and all currency LCR 50% from 1/1/2016

Examples of wrinkles

www.lombardrisk.com

Lombard Risk - | Enabling regulatory compliance

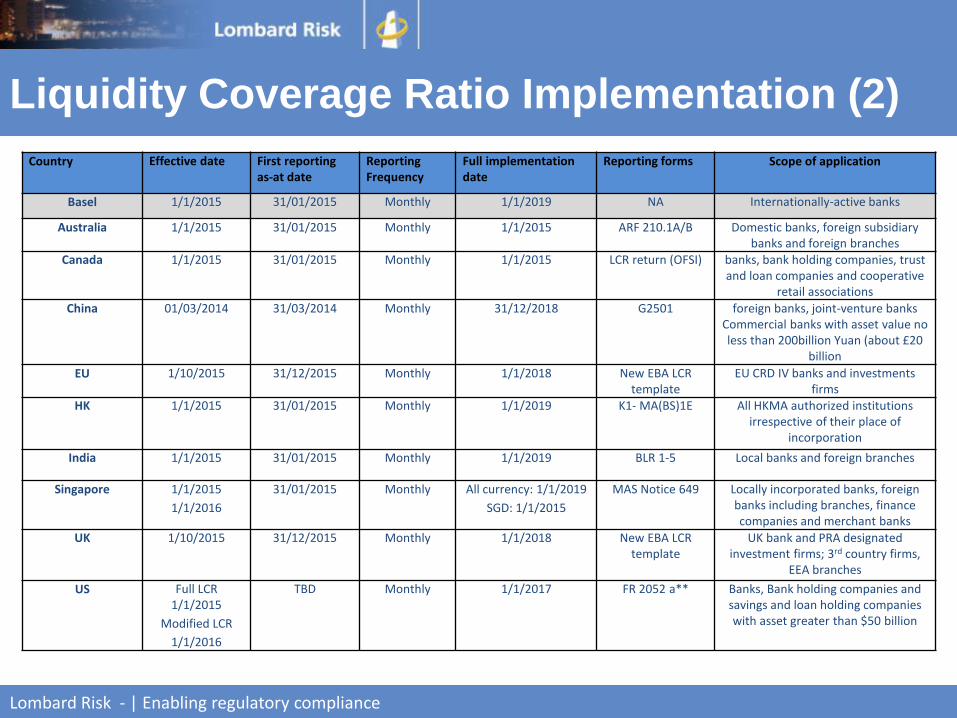

Liquidity Coverage Ratio Implementation (2)

Country Effective date First reporting as-at date

Reporting Frequency

Full implementation date

Reporting forms Scope of application

Basel 1/1/2015 31/01/2015 Monthly 1/1/2019 NA Internationally-active banks

Australia 1/1/2015 31/01/2015 Monthly 1/1/2015 ARF 210.1A/B Domestic banks, foreign subsidiary banks and foreign branches

Canada 1/1/2015 31/01/2015 Monthly 1/1/2015 LCR return (OFSI) banks, bank holding companies, trust and loan companies and cooperative

retail associations

China 01/03/2014 31/03/2014 Monthly 31/12/2018 G2501 foreign banks, joint-venture banks Commercial banks with asset value no less than 200billion Yuan (about £20

billion

EU 1/10/2015 31/12/2015 Monthly 1/1/2018 New EBA LCR template

EU CRD IV banks and investments firms

HK 1/1/2015 31/01/2015 Monthly 1/1/2019 K1- MA(BS)1E All HKMA authorized institutions irrespective of their place of

incorporation

India 1/1/2015 31/01/2015 Monthly 1/1/2019 BLR 1-5 Local banks and foreign branches

Singapore 1/1/2015

1/1/2016

31/01/2015 Monthly All currency: 1/1/2019

SGD: 1/1/2015

MAS Notice 649 Locally incorporated banks, foreignbanks including branches, finance companies and merchant banks

UK 1/10/2015 31/12/2015 Monthly 1/1/2018 New EBA LCR template

UK bank and PRA designated investment firms; 3rd country firms,

EEA branches

US Full LCR 1/1/2015

Modified LCR

1/1/2016

TBD Monthly 1/1/2017 FR 2052 a** Banks, Bank holding companies and savings and loan holding companies with asset greater than $50 billion

www.lombardrisk.com

Legislative framework & timeframe

Lombard Risk - Enabling regulatory compliance

…Rule books

and technical

implementati

on of these…

www.lombardrisk.com

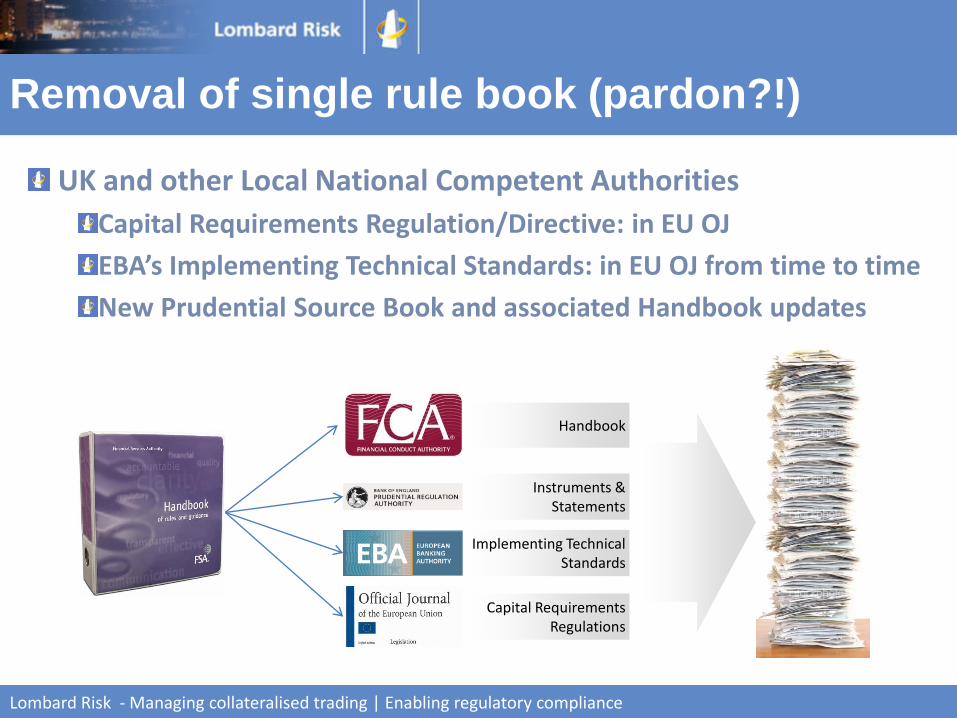

Removal of single rule book (pardon?!)

Lombard Risk - Managing collateralised trading | Enabling regulatory compliance

UK and other Local National Competent Authorities

Capital Requirements Regulation/Directive: in EU OJ

EBA’s Implementing Technical Standards: in EU OJ from time to time

New Prudential Source Book and associated Handbook updates

Handbook

Instruments & Statements

Implementing Technical Standards

Capital Requirements Regulations

www.lombardrisk.com

Implementation of LCR

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Lombard Risk - | Enabling regulatory compliance

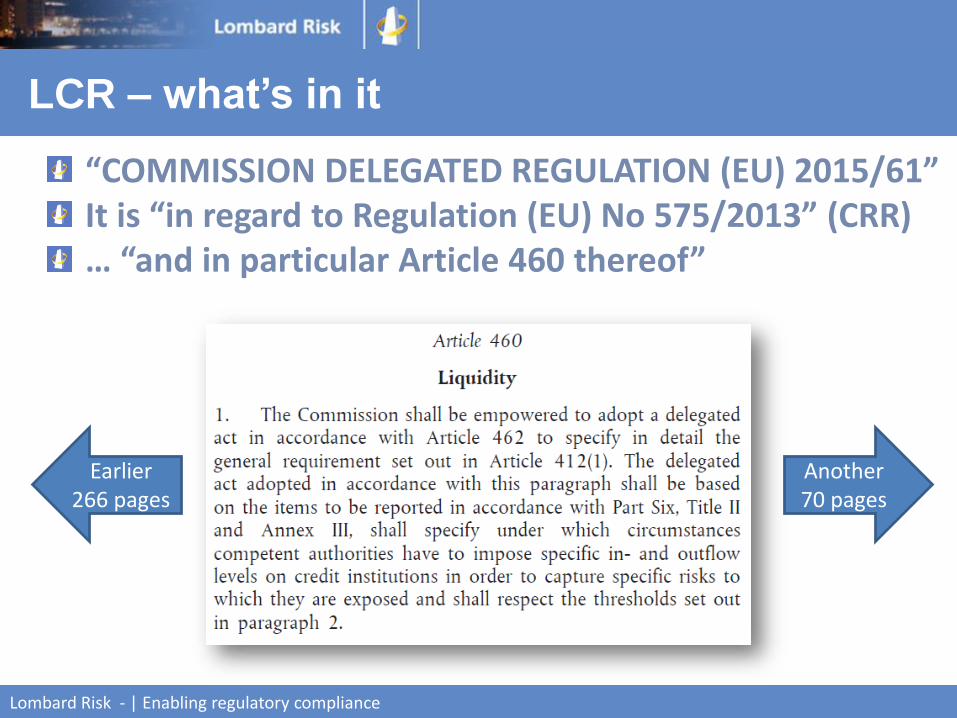

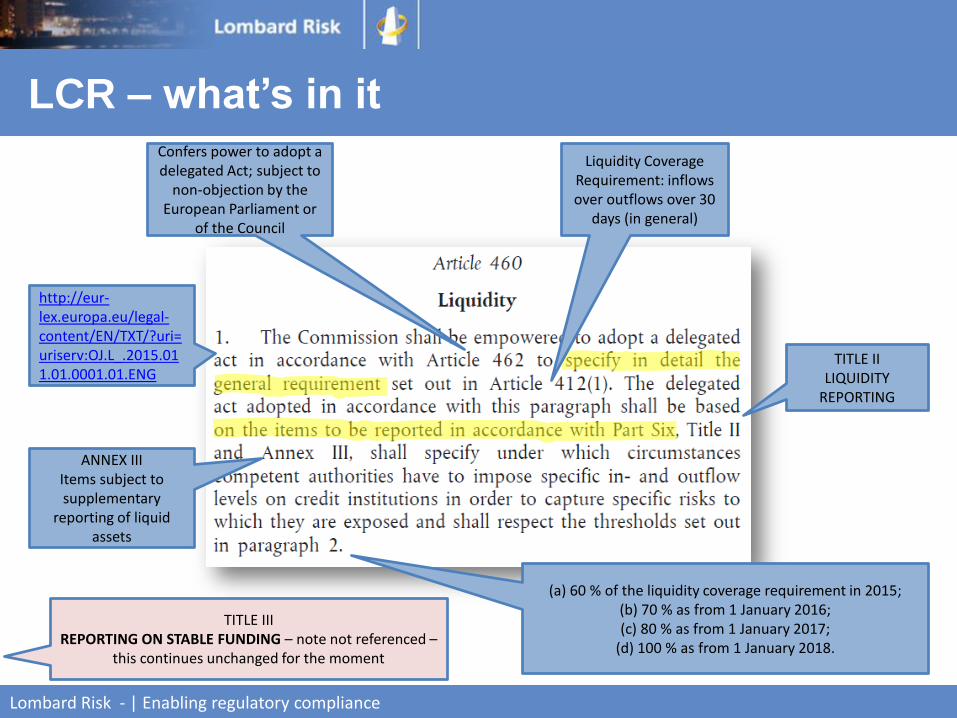

“COMMISSION DELEGATED REGULATION (EU) 2015/61”It is “in regard to Regulation (EU) No 575/2013” (CRR)… “and in particular Article 460 thereof”

LCR – what’s in it

Another 70 pages

Earlier 266 pages

www.lombardrisk.com

Lombard Risk - | Enabling regulatory compliance

LCR – what’s in itConfers power to adopt a delegated Act; subject to

non-objection by the European Parliament or

of the Council

TITLE IILIQUIDITY

REPORTING

Liquidity Coverage Requirement: inflows over outflows over 30

days (in general)

TITLE IIIREPORTING ON STABLE FUNDING – note not referenced –

this continues unchanged for the moment

(a) 60 % of the liquidity coverage requirement in 2015;(b) 70 % as from 1 January 2016;(c) 80 % as from 1 January 2017;

(d) 100 % as from 1 January 2018.

ANNEX IIIItems subject to supplementary

reporting of liquid assets

http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2015.011.01.0001.01.ENG

www.lombardrisk.com

LCR – what’s in it

Lombard Risk - | Enabling regulatory compliance

Lombard Risk Impact Analysis of

the reporting changes – useful

summaries

UK impact analysisEurope impact

analysis

www.lombardrisk.com

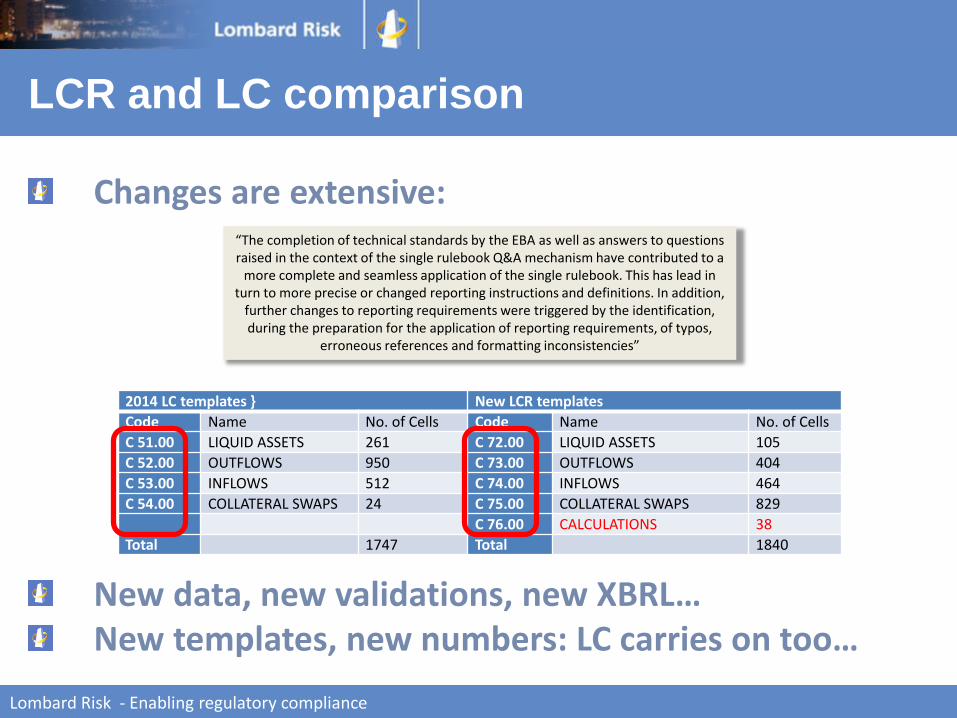

Changes are extensive:

New data, new validations, new XBRL…New templates, new numbers: LC carries on too…

Lombard Risk - Enabling regulatory compliance

2014 LC templates } New LCR templates

Code Name No. of Cells Code Name No. of Cells

C 51.00 LIQUID ASSETS 261 C 72.00 LIQUID ASSETS 105

C 52.00 OUTFLOWS 950 C 73.00 OUTFLOWS 404

C 53.00 INFLOWS 512 C 74.00 INFLOWS 464

C 54.00 COLLATERAL SWAPS 24 C 75.00 COLLATERAL SWAPS 829

C 76.00 CALCULATIONS 38

Total 1747 Total 1840

LCR and LC comparison

“The completion of technical standards by the EBA as well as answers to questions raised in the context of the single rulebook Q&A mechanism have contributed to a

more complete and seamless application of the single rulebook. This has lead in turn to more precise or changed reporting instructions and definitions. In addition,

further changes to reporting requirements were triggered by the identification,during the preparation for the application of reporting requirements, of typos,

erroneous references and formatting inconsistencies”

www.lombardrisk.com

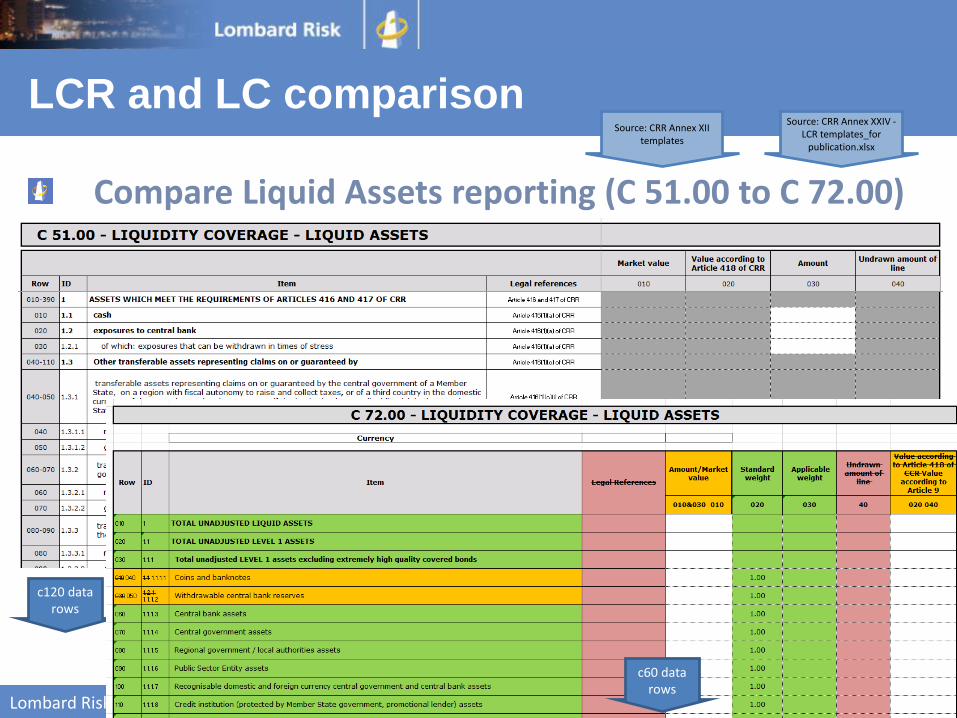

Compare Liquid Assets reporting (C 51.00 to C 72.00)

Lombard Risk - Enabling regulatory compliance

LCR and LC comparison

c120 data rows

c60 data rows

Source: CRR Annex XII templates

Source: CRR Annex XXIV -LCR templates_for

publication.xlsx

www.lombardrisk.com

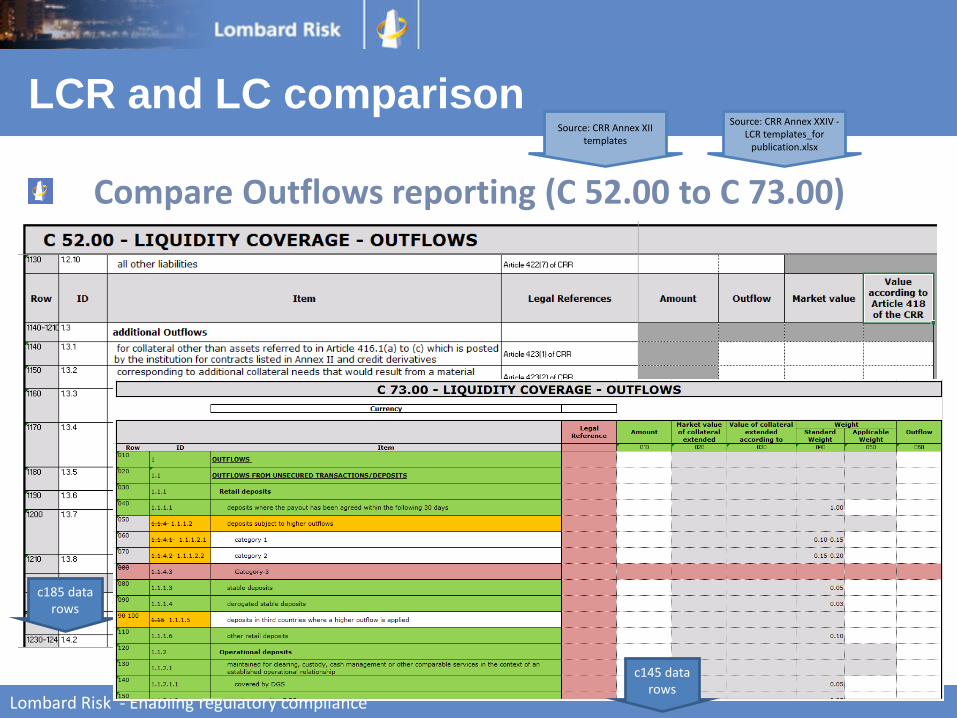

Compare Outflows reporting (C 52.00 to C 73.00)

Lombard Risk - Enabling regulatory compliance

LCR and LC comparisonSource: CRR Annex XII

templates

Source: CRR Annex XXIV -LCR templates_for

publication.xlsx

c185 data rows

c145 data rows

www.lombardrisk.com

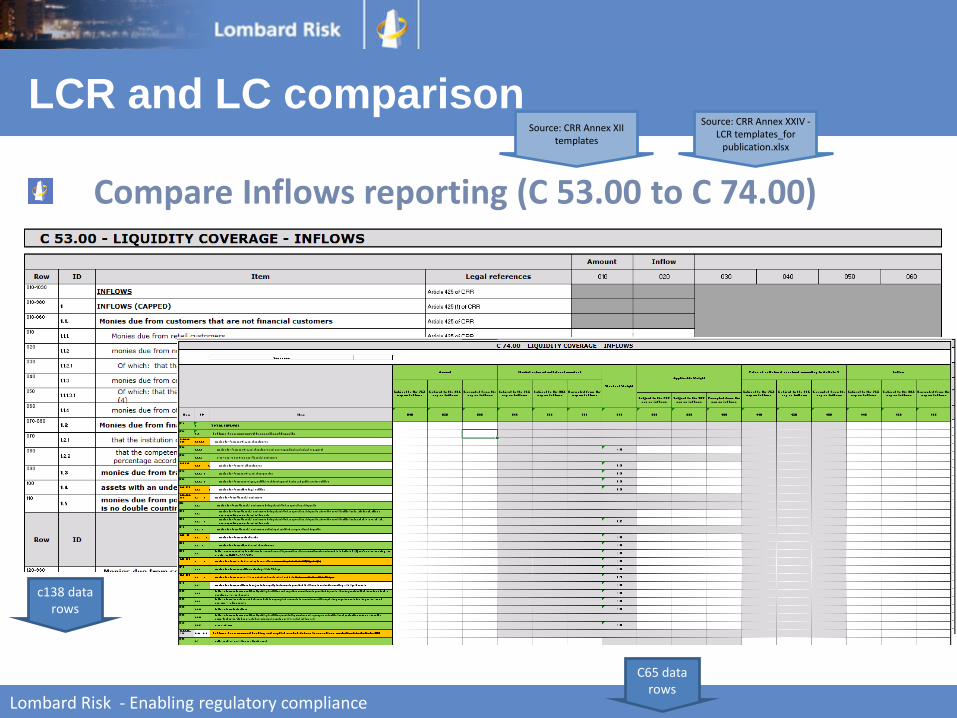

Compare Inflows reporting (C 53.00 to C 74.00)

Lombard Risk - Enabling regulatory compliance

LCR and LC comparisonSource: CRR Annex XII

templates

Source: CRR Annex XXIV -LCR templates_for

publication.xlsx

c138 data rows

C65 data rows

www.lombardrisk.com

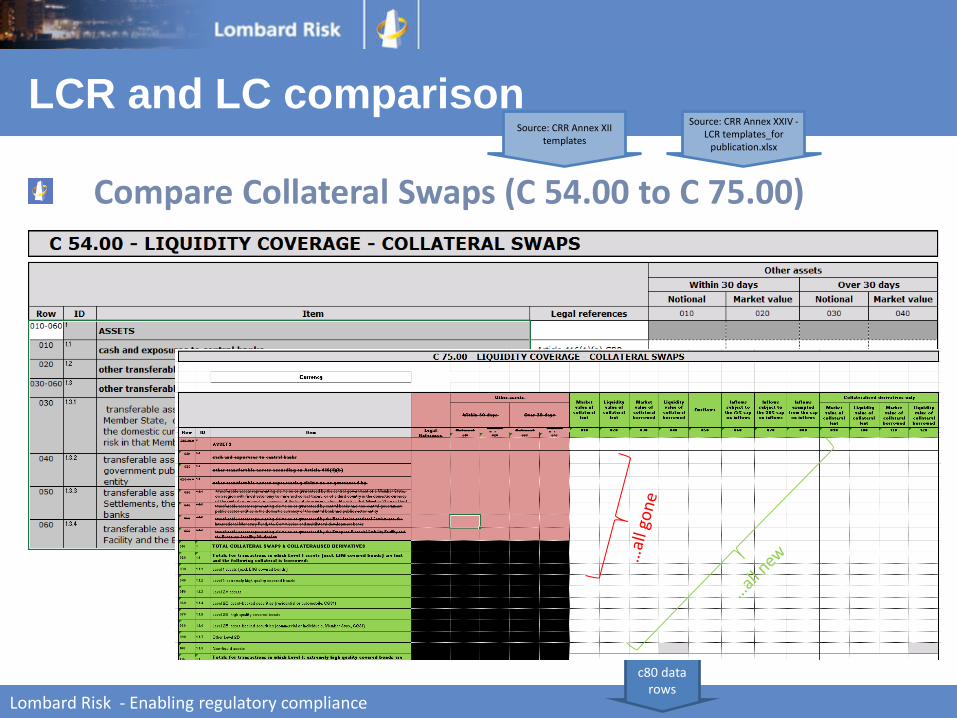

Compare Collateral Swaps (C 54.00 to C 75.00)

Lombard Risk - Enabling regulatory compliance

LCR and LC comparisonSource: CRR Annex XII

templates

Source: CRR Annex XXIV -LCR templates_for

publication.xlsx

c80 data rows

www.lombardrisk.com

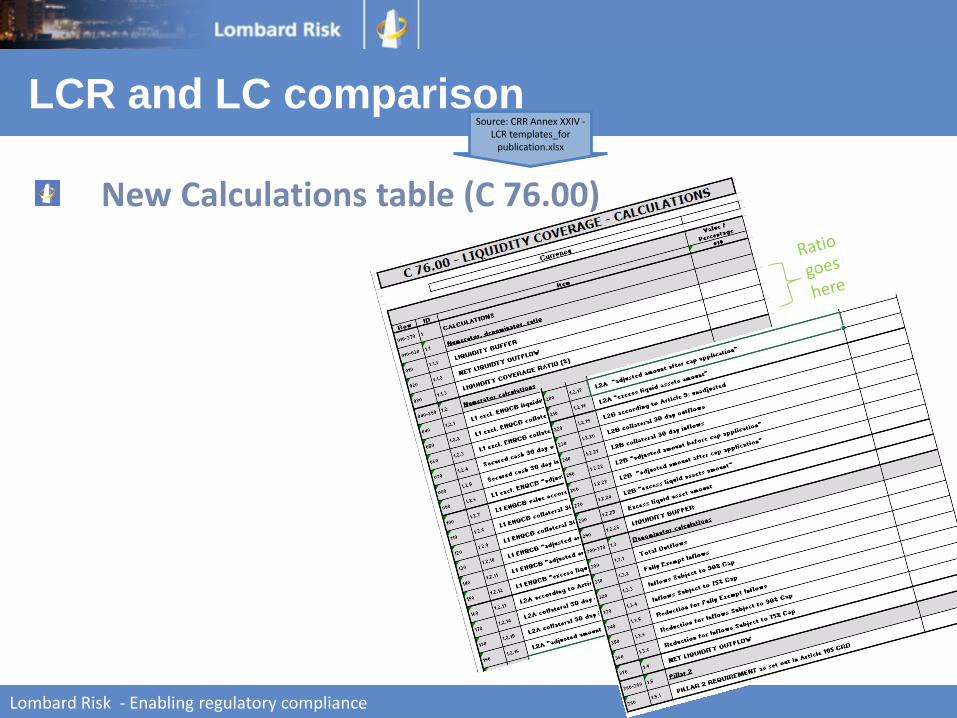

New Calculations table (C 76.00)

Lombard Risk - Enabling regulatory compliance

LCR and LC comparisonSource: CRR Annex XXIV -

LCR templates_for publication.xlsx

www.lombardrisk.com

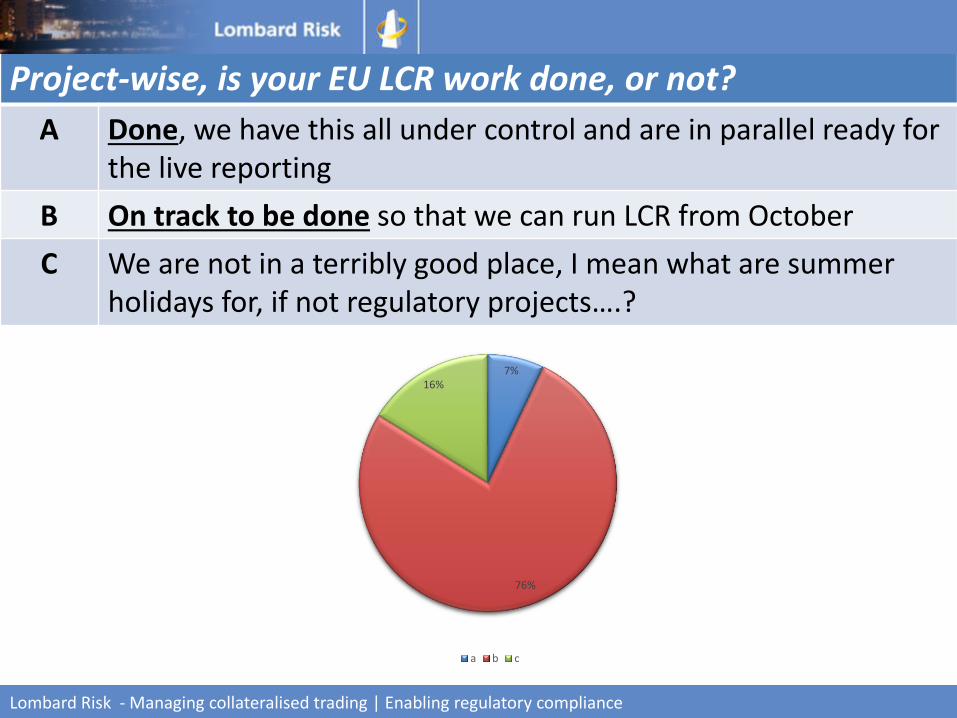

Project-wise, is your EU LCR work done, or not?

A Done, we have this all under control and are in parallel ready for the live reporting

B On track to be done so that we can run LCR from October

C We are not in a terribly good place, I mean what are summer holidays for, if not regulatory projects….?

Lombard Risk - Managing collateralised trading | Enabling regulatory compliance

7%

76%

16%

a b c

www.lombardrisk.com

(Technical) Implementation of LCR

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Technical implementation – 4 scoops of XBRL

Lombard Risk - Managing collateralised trading | Enabling regulatory compliance

XBRL Taxonomy - role

Concrete technical representation of the data point model

(and thus of the BTS, and thus of the CRR)

Remember: templates are only for human-readability; the XBRL taxonomy provides digital representation of that

www.lombardrisk.com

Lombard Risk - Managing collateralised trading | Enabling regulatory compliance

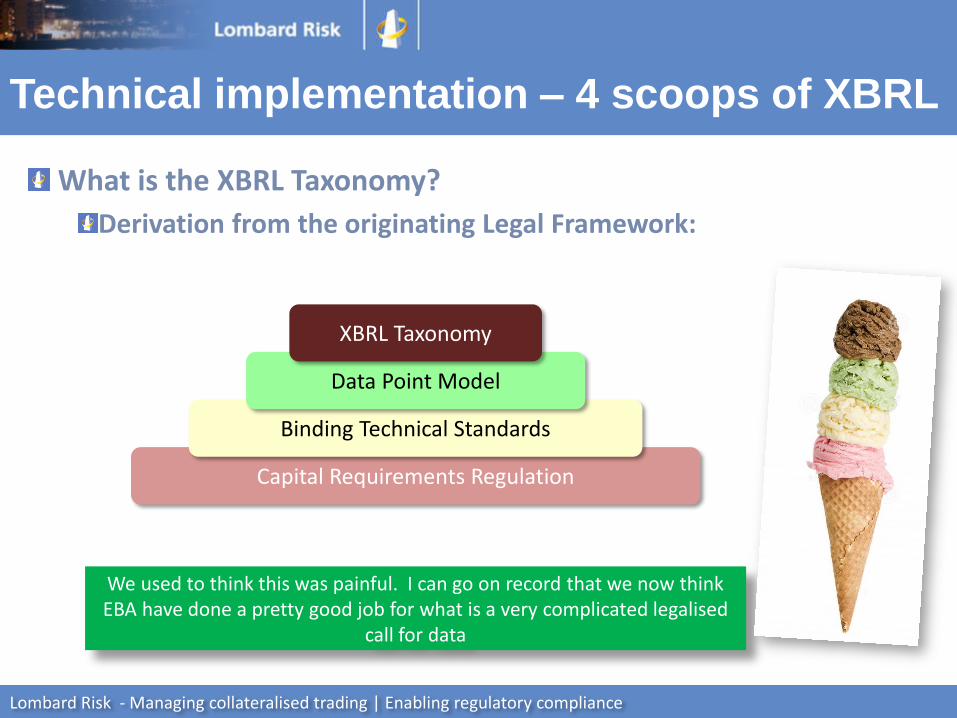

What is the XBRL Taxonomy?

Derivation from the originating Legal Framework:

Capital Requirements Regulation

Binding Technical Standards

Data Point Model

XBRL Taxonomy

Technical implementation – 4 scoops of XBRL

We used to think this was painful. I can go on record that we now think EBA have done a pretty good job for what is a very complicated legalised

call for data

www.lombardrisk.com

Implementation of AMM

Lombard Risk - Enabling regulatory compliance

On 17th July 2015, the EBA announced that the implementation of AMM will be postponed by at

least three months (i.e. 1st October 2015). The final application date will depend on the timeline of

adoption of the ITS by the European Commission.

www.lombardrisk.com

Implementation of AMM

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Impact of LCR:

New UK

liquidity regime

Lombard Risk - Enabling regulatory compliance

http://www.bankofengland.co.uk/pra/Documents/publications/ps/2015/ps1115.pdf

http://www.bankofengland.co.uk/pra/Documents/publications/ss/2015/ss2415.pdf

www.lombardrisk.com

EU Delegated Act (10th Oct 2014)• Credit institutions; applicable 1/10/15

PRA Consultation Paper CP27/2014 (28th Nov 2014)• “CRD IV: Liquidity” (revoke rules, restate PRA approach)• Main proposals:

• Revoke BIPRU 12• Apply higher minimum LCR• Carry forward existing add-ons• Amend existing FSA047-054 reporting requirements• Impose requirements on UK-designated investment firms• Consider approach for third country firms

PRA Policy Statement (PS11/15)– …over the page!

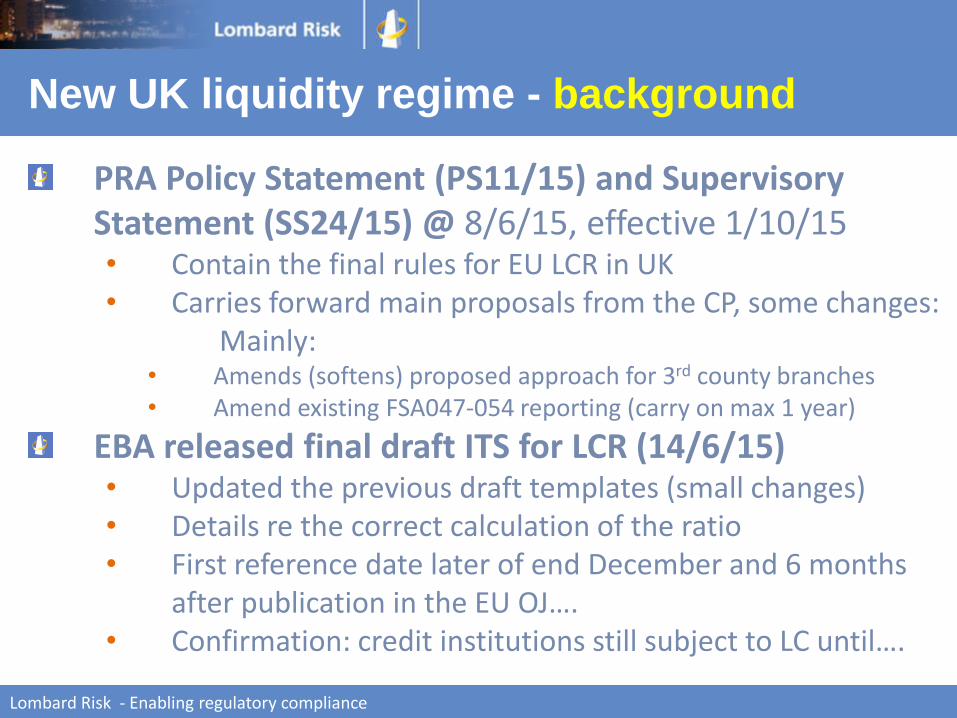

New UK liquidity regime - background

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

PRA Policy Statement (PS11/15) and Supervisory Statement (SS24/15) @ 8/6/15, effective 1/10/15• Contain the final rules for EU LCR in UK• Carries forward main proposals from the CP, some changes:

Mainly:• Amends (softens) proposed approach for 3rd county branches• Amend existing FSA047-054 reporting (carry on max 1 year)

EBA released final draft ITS for LCR (14/6/15)• Updated the previous draft templates (small changes)• Details re the correct calculation of the ratio• First reference date later of end December and 6 months

after publication in the EU OJ….• Confirmation: credit institutions still subject to LC until….

New UK liquidity regime - background

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

PRA new liquidity regime will apply to:• UK banks & Building Societies• UK incorporated investment firms regulated by the PRA

• (so-called PRA UK-designated investment firms)

• Third-country-firms (non-EU firms)• EEA credit institutions with a branch in the UK• It does NOT cover FCA-regulated investment firms

New UK liquidity regime - scope

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

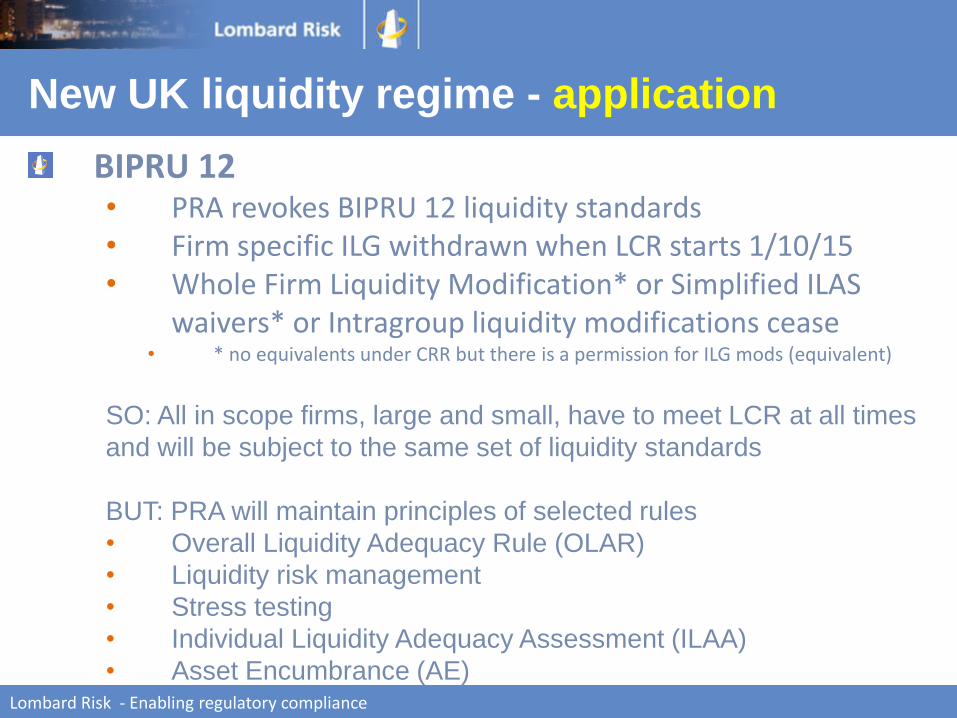

BIPRU 12• PRA revokes BIPRU 12 liquidity standards• Firm specific ILG withdrawn when LCR starts 1/10/15• Whole Firm Liquidity Modification* or Simplified ILAS

waivers* or Intragroup liquidity modifications cease• * no equivalents under CRR but there is a permission for ILG mods (equivalent)

SO: All in scope firms, large and small, have to meet LCR at all times

and will be subject to the same set of liquidity standards

BUT: PRA will maintain principles of selected rules

• Overall Liquidity Adequacy Rule (OLAR)

• Liquidity risk management

• Stress testing

• Individual Liquidity Adequacy Assessment (ILAA)

• Asset Encumbrance (AE)

New UK liquidity regime - application

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

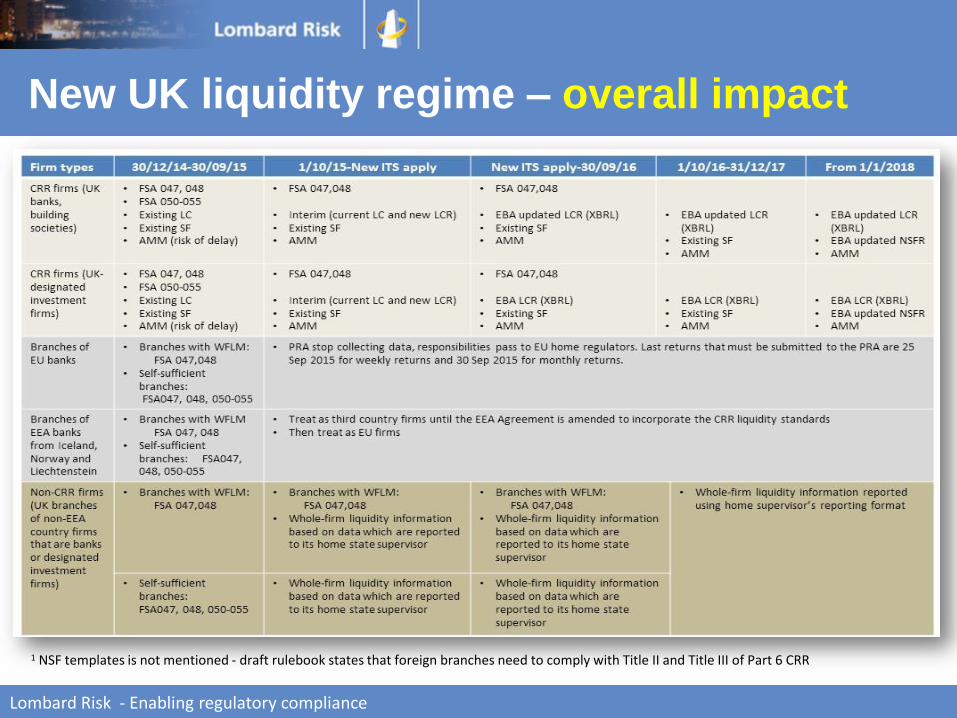

New UK liquidity regime – overall impact

Lombard Risk - Enabling regulatory compliance

1 NSF templates is not mentioned - draft rulebook states that foreign branches need to comply with Title II and Title III of Part 6 CRR

www.lombardrisk.com

THREE TIMES THE FUN!

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

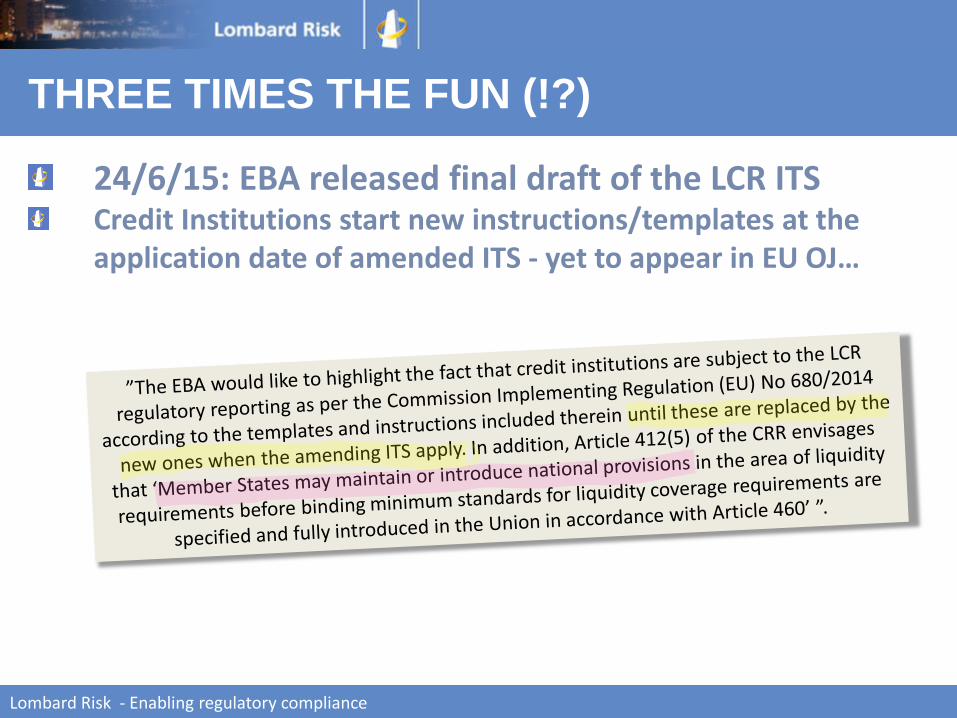

24/6/15: EBA released final draft of the LCR ITSCredit Institutions start new instructions/templates at the application date of amended ITS - yet to appear in EU OJ…

THREE TIMES THE FUN (!?)

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Which means what? (1)

PRA’s requirements for switch from old to new regime include use

of an interim tool before EU LCR XBRL standards are ready

There is no EBA interim process for reporting purposes. Meaning

until current European legislation which requires LC to be reported

by in-scope firms is replaced by live legislation requiring the LCR

reported, then nothing changes. So LC will still be required to be

reported by in scope firms during interim period

Supervisory process – be reminded – there is only ever ONE

process. From 1st October 2015 that is the Liquidity Coverage

REQUIREMENT i.e. liquidity coverage RATIO which meets the REQUIREMENT (EBA state 60% but

80% for UK firms)

THREE TIMES THE FUN (!?)

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Which means what? (2)

During interim period from 1st Oct for N months, CRDIV credit institutions (investment firms not in scope of new LCR but continue with the LC)…have to report each of:

LC (as it is, existing XBRL via Gabriel to EBA)

Interim LCR (XML/Excel direct to PRA) and

FSA047/048 (as it is, XML via Gabriel to PRA)

THREE TIMES THE FUN (!?)

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

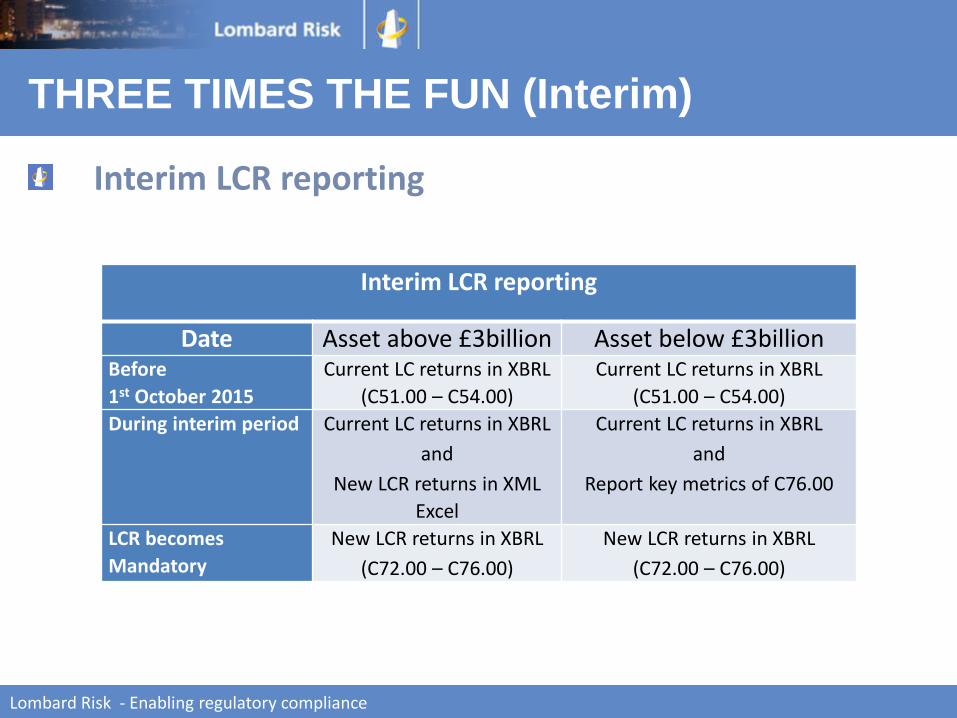

Interim LCR reporting

THREE TIMES THE FUN (Interim)

Lombard Risk - Enabling regulatory compliance

Interim LCR reporting

Date Asset above £3billion Asset below £3billionBefore

1st October 2015

Current LC returns in XBRL

(C51.00 – C54.00)

Current LC returns in XBRL

(C51.00 – C54.00)

During interim period Current LC returns in XBRL

and

New LCR returns in XML

Excel

Current LC returns in XBRL

and

Report key metrics of C76.00

LCR becomes

Mandatory

New LCR returns in XBRL

(C72.00 – C76.00)

New LCR returns in XBRL

(C72.00 – C76.00)

www.lombardrisk.com

EC has only adopted one ITS (at 9th July ) since February 2015…AMM 18th on the listBenchmarking portfolios which is proposed to go live at Q4 2015 is 21st on this listLCR ITS is no. 25 Funding Plan is a guideline so not on the list

Conclusion?

THREE TIMES THE FUN (how long?)

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Lombard Risk - | Enabling regulatory compliance

EBA 2015 work plan state of play

http://ec.europa.eu/finance/bank/docs/regcapital/acts/overview-crr-crdiv-its_en.pdf

www.lombardrisk.com

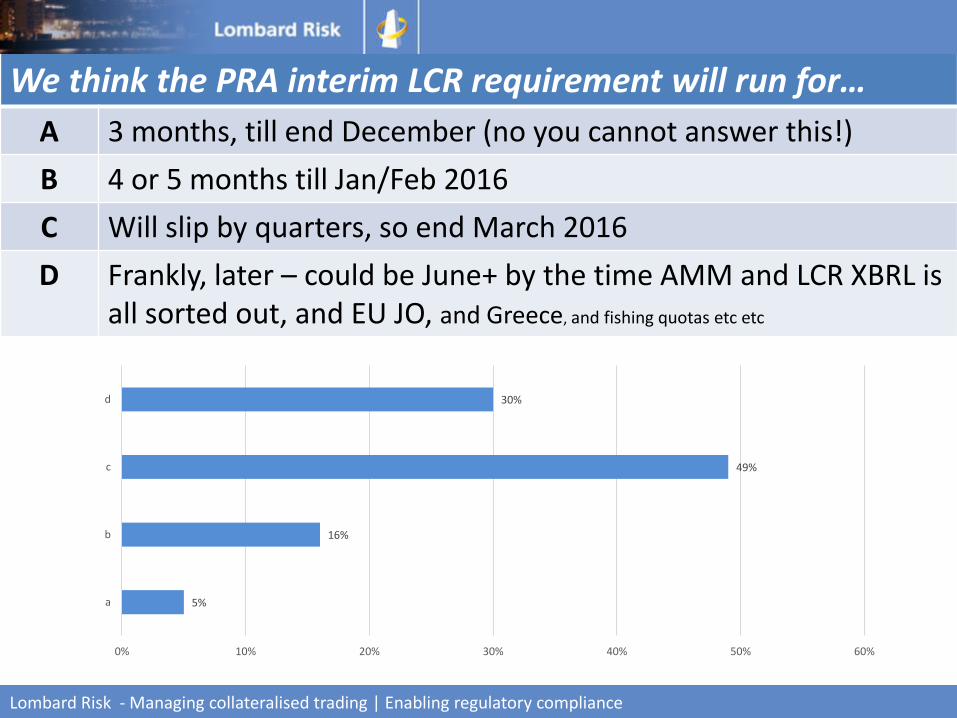

We think the PRA interim LCR requirement will run for…

A 3 months, till end December (no you cannot answer this!)

B 4 or 5 months till Jan/Feb 2016

C Will slip by quarters, so end March 2016

D Frankly, later – could be June+ by the time AMM and LCR XBRL is all sorted out, and EU JO, and Greece, and fishing quotas etc etc

Lombard Risk - Managing collateralised trading | Enabling regulatory compliance

5%

16%

49%

30%

0% 10% 20% 30% 40% 50% 60%

a

b

c

d

www.lombardrisk.com

Consider also the other moving

pieces….

Lombard Risk - Enabling regulatory compliance

…and other

horizons to be

aware of

www.lombardrisk.com

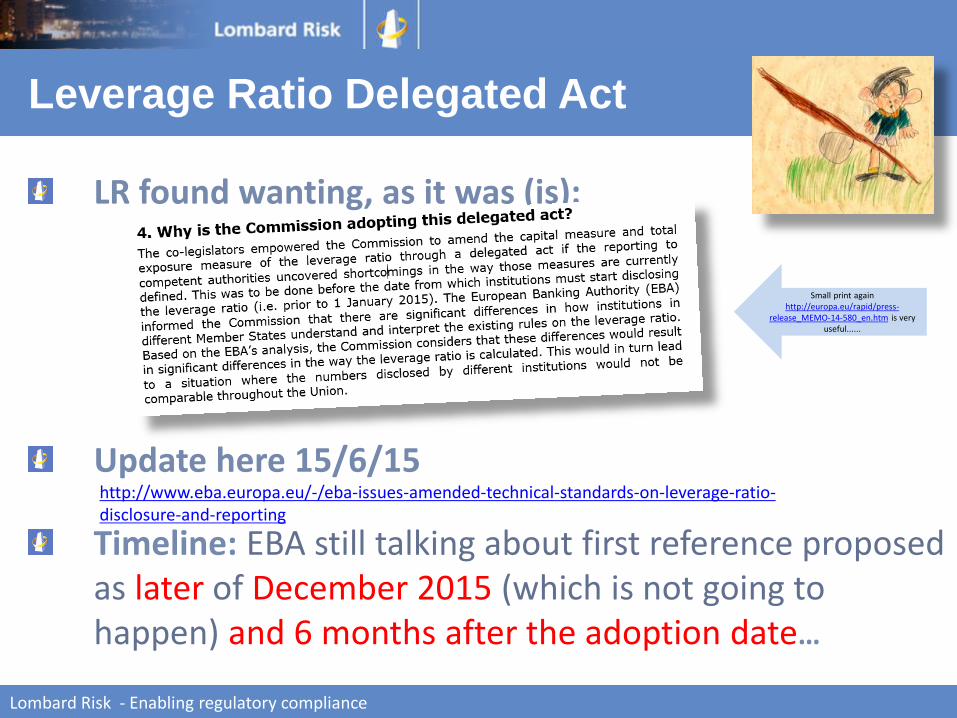

LR found wanting, as it was (is):

Update here 15/6/15

Timeline: EBA still talking about first reference proposed as later of December 2015 (which is not going to happen) and 6 months after the adoption date…

Leverage Ratio Delegated Act

Lombard Risk - Enabling regulatory compliance

http://www.eba.europa.eu/-/eba-issues-amended-technical-standards-on-leverage-ratio-disclosure-and-reporting

Small print againhttp://europa.eu/rapid/press-

release_MEMO-14-580_en.htm is very useful......

www.lombardrisk.com

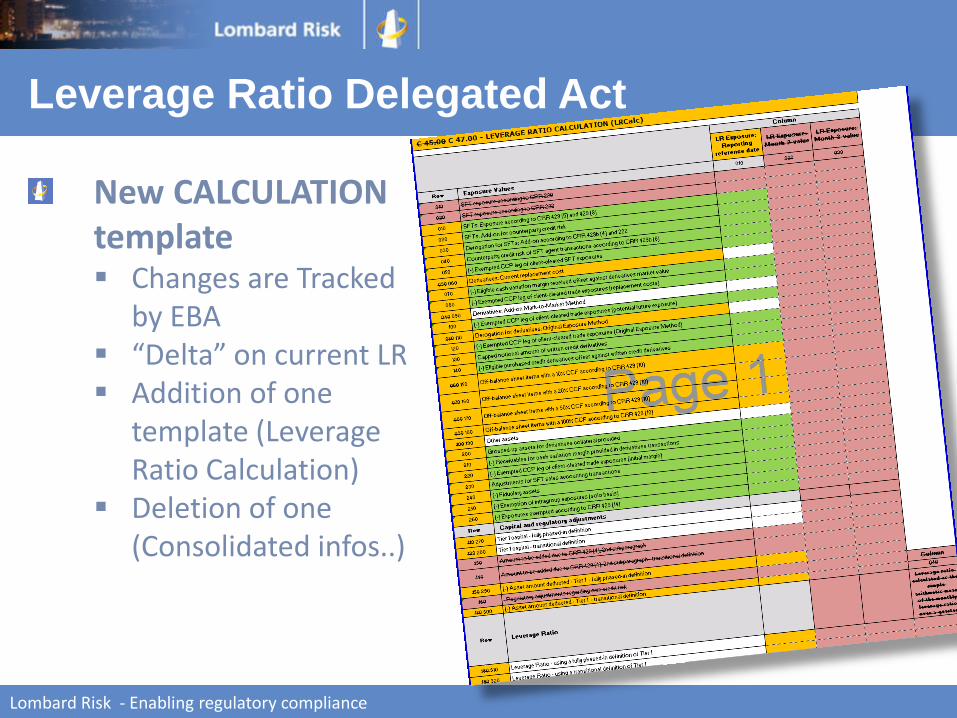

New CALCULATION template Changes are Tracked

by EBA “Delta” on current LR Addition of one

template (Leverage Ratio Calculation)

Deletion of one (Consolidated infos..)

Leverage Ratio Delegated Act

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Changed templates…. Changes are tracked by EBA “Delta” on the current LR

Leverage Ratio Delegated Act

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

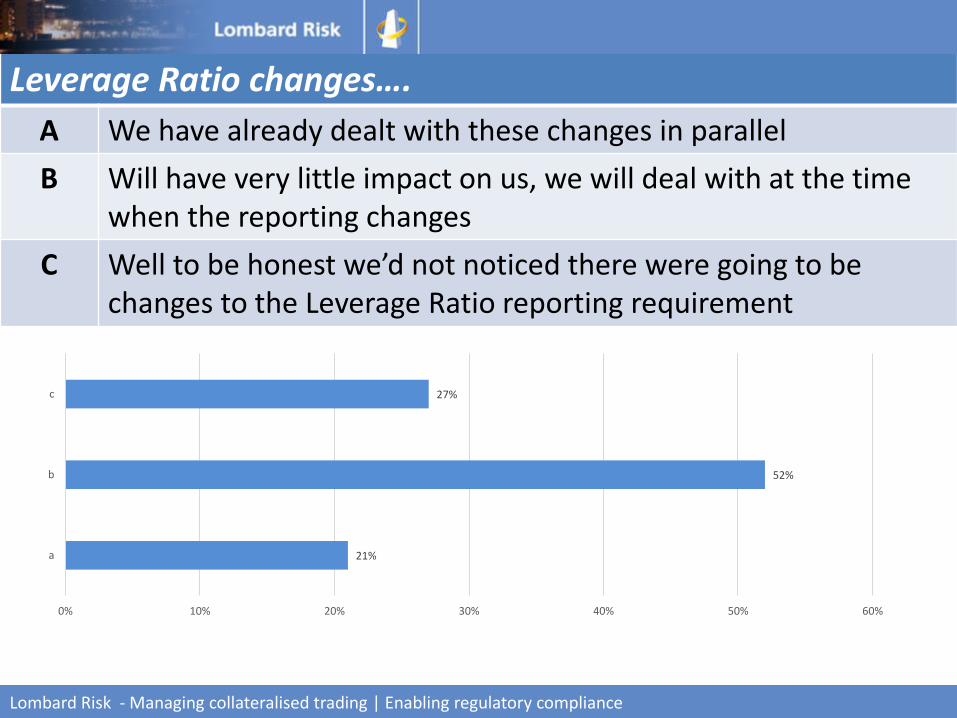

Leverage Ratio changes….

A We have already dealt with these changes in parallel

B Will have very little impact on us, we will deal with at the time when the reporting changes

C Well to be honest we’d not noticed there were going to be changes to the Leverage Ratio reporting requirement

Lombard Risk - Managing collateralised trading | Enabling regulatory compliance

21%

52%

27%

0% 10% 20% 30% 40% 50% 60%

a

b

c

www.lombardrisk.com

Consider also the other moving

pieces….

Lombard Risk - Enabling regulatory compliance

…and other

horizons to be

aware of

www.lombardrisk.com

Funding plan templates

Lombard Risk - | Enabling regulatory compliance

Reporting of funding plans for 2014 and thereafter

For 2014 and 2015, institutions report funding plans with a reference date no later than 30th June 2015 and submit it to CAs by 30th September 2015

For subsequent years, institutions report their funding plans with a reference date of 31st December of the previous year and submit it to CAs by 31st March of the following year

XBRL submission

www.lombardrisk.com

Funding plan templates

Lombard Risk - | Enabling regulatory compliance

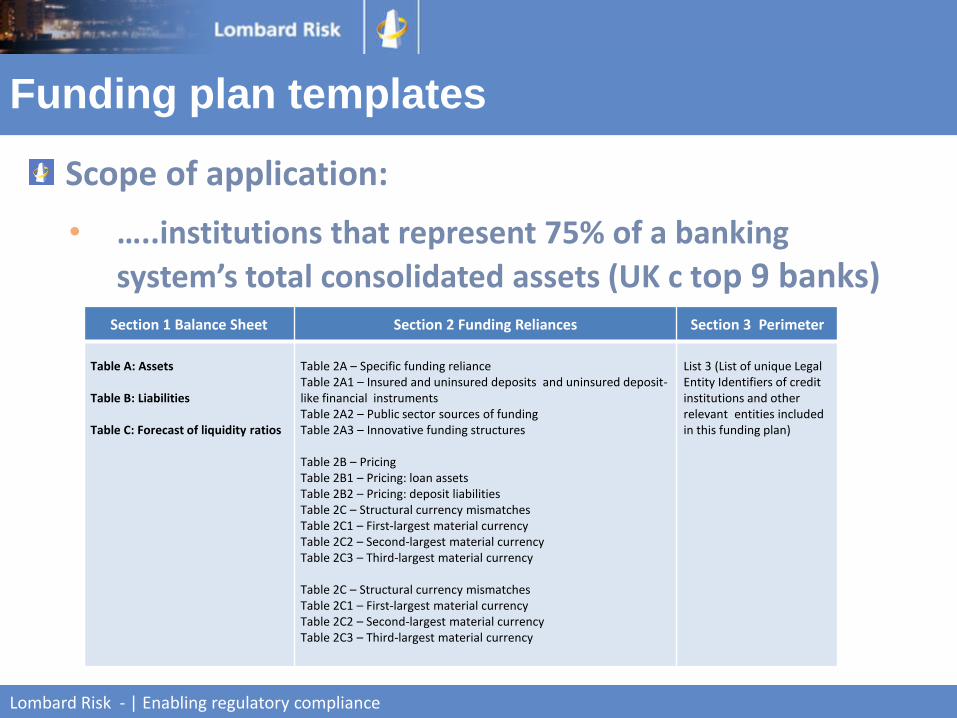

Scope of application:

• …..institutions that represent 75% of a banking

system’s total consolidated assets (UK c top 9 banks)Section 1 Balance Sheet Section 2 Funding Reliances Section 3 Perimeter

Table A: Assets

Table B: Liabilities

Table C: Forecast of liquidity ratios

Table 2A – Specific funding relianceTable 2A1 – Insured and uninsured deposits and uninsured deposit-like financial instrumentsTable 2A2 – Public sector sources of fundingTable 2A3 – Innovative funding structures

Table 2B – PricingTable 2B1 – Pricing: loan assetsTable 2B2 – Pricing: deposit liabilitiesTable 2C – Structural currency mismatchesTable 2C1 – First-largest material currencyTable 2C2 – Second-largest material currencyTable 2C3 – Third-largest material currency

Table 2C – Structural currency mismatchesTable 2C1 – First-largest material currencyTable 2C2 – Second-largest material currencyTable 2C3 – Third-largest material currency

List 3 (List of unique Legal Entity Identifiers of credit institutions and other relevant entities included in this funding plan)

www.lombardrisk.com

Consider also….

….the other moving pieces

Lombard Risk - Enabling regulatory compliance

…and other horizons to

be aware of

www.lombardrisk.com

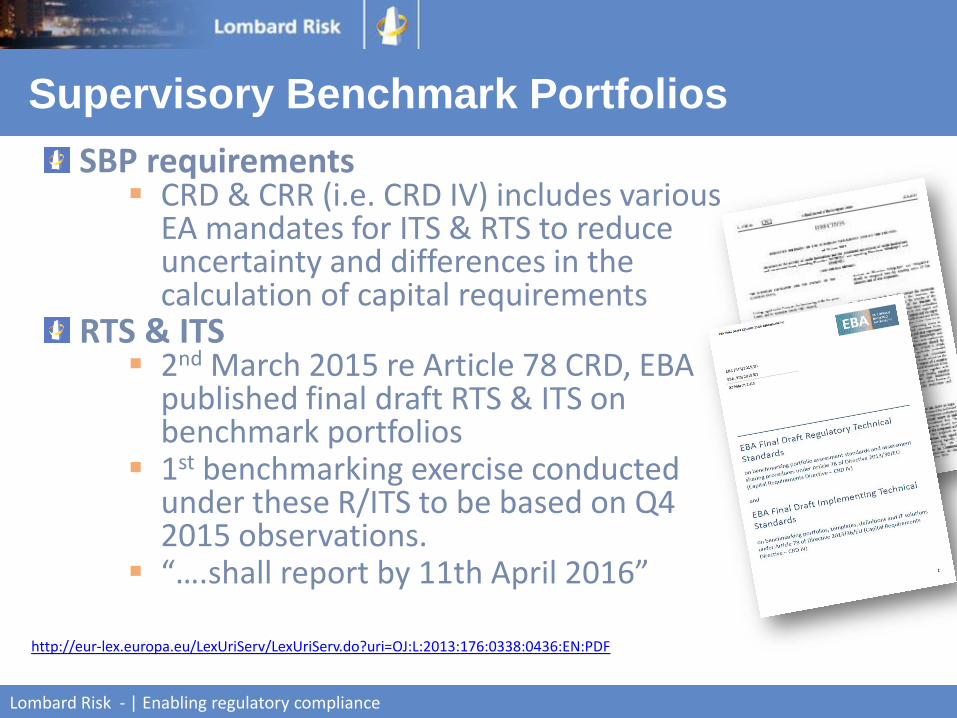

Lombard Risk - | Enabling regulatory compliance

SBP requirements CRD & CRR (i.e. CRD IV) includes various

EA mandates for ITS & RTS to reduce uncertainty and differences in the calculation of capital requirements

RTS & ITS 2nd March 2015 re Article 78 CRD, EBA

published final draft RTS & ITS on benchmark portfolios

1st benchmarking exercise conducted under these R/ITS to be based on Q4 2015 observations.

“….shall report by 11th April 2016”

Supervisory Benchmark Portfolios

http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2013:176:0338:0436:EN:PDF

www.lombardrisk.com

Lombard Risk - | Enabling regulatory compliance

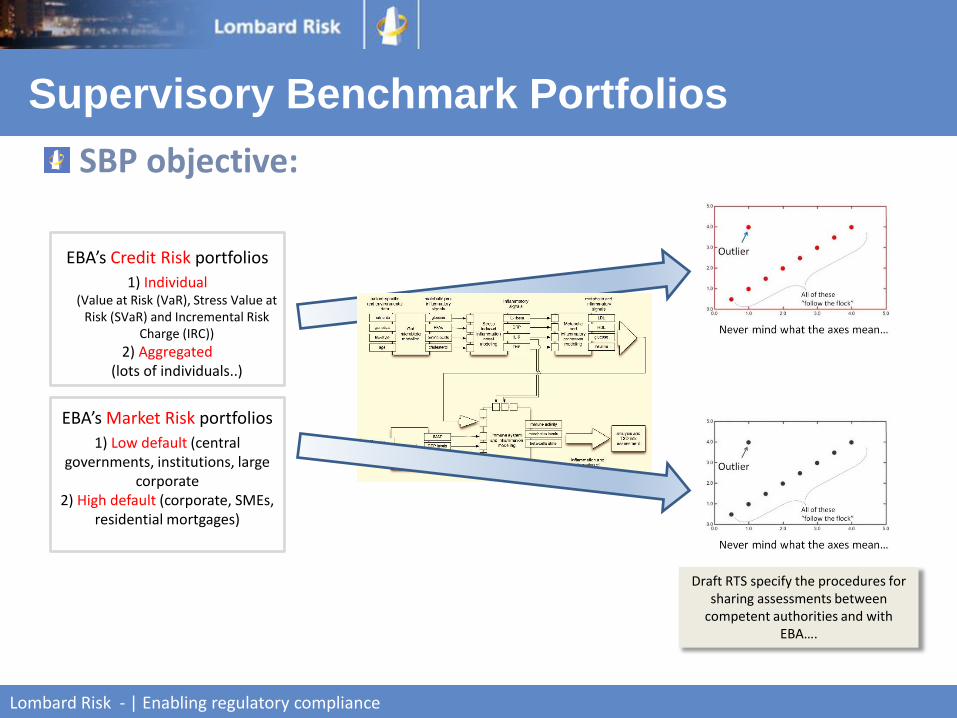

SBP objective:

Supervisory Benchmark Portfolios

EBA’s Credit Risk portfolios

1) Individual(Value at Risk (VaR), Stress Value at

Risk (SVaR) and Incremental Risk Charge (IRC))

2) Aggregated (lots of individuals..)

EBA’s Market Risk portfolios

1) Low default (central governments, institutions, large

corporate2) High default (corporate, SMEs,

residential mortgages)

Draft RTS specify the procedures for sharing assessments between

competent authorities and with EBA….

www.lombardrisk.com

Supervisory Benchmark Portfolios

Lombard Risk - | Enabling regulatory compliance

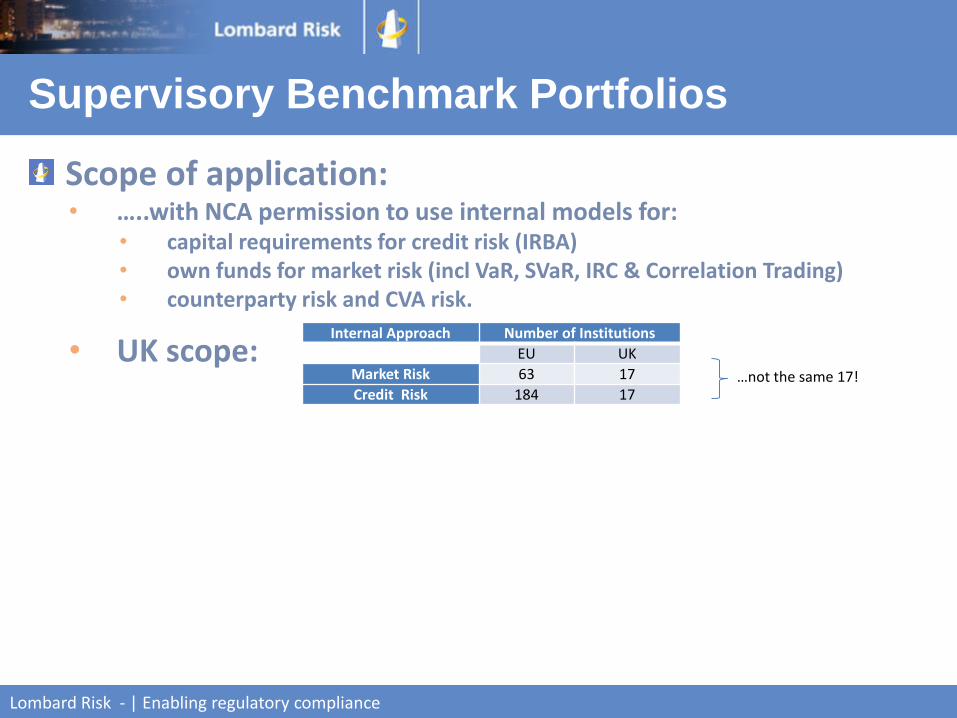

Scope of application:• …..with NCA permission to use internal models for:

• capital requirements for credit risk (IRBA) • own funds for market risk (incl VaR, SVaR, IRC & Correlation Trading)• counterparty risk and CVA risk.

• UK scope:Internal Approach Number of Institutions

EU UK

Market Risk 63 17

Credit Risk 184 17…not the same 17!

www.lombardrisk.com

Supervisory Benchmark Portfolios

Lombard Risk - | Enabling regulatory compliance

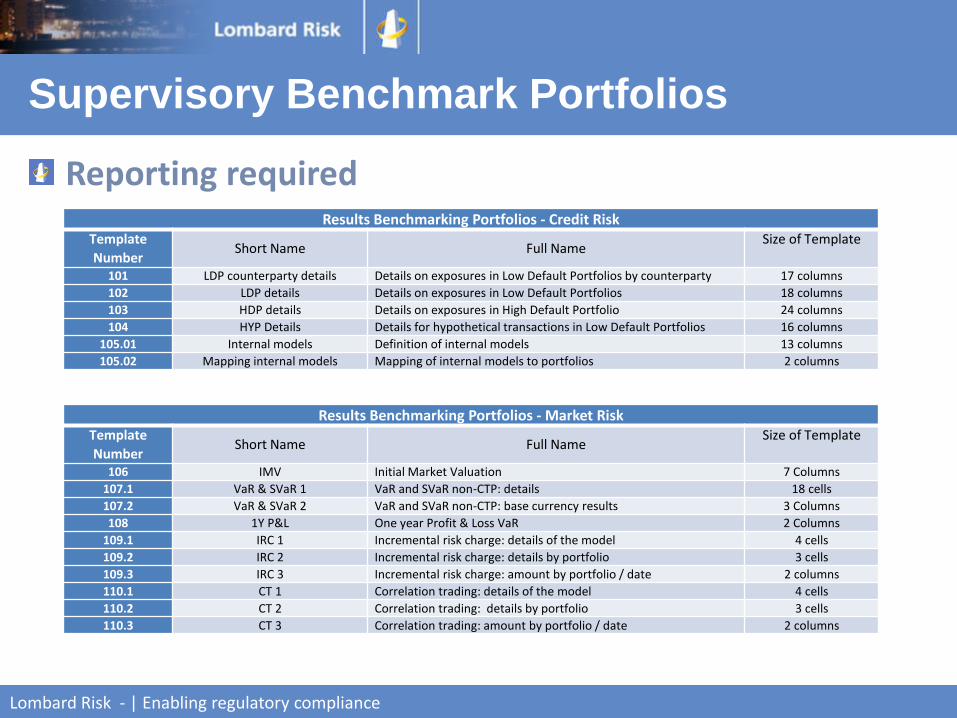

Reporting requiredResults Benchmarking Portfolios - Credit Risk

Template

NumberShort Name Full Name

Size of Template

101 LDP counterparty details Details on exposures in Low Default Portfolios by counterparty 17 columns

102 LDP details Details on exposures in Low Default Portfolios 18 columns

103 HDP details Details on exposures in High Default Portfolio 24 columns

104 HYP Details Details for hypothetical transactions in Low Default Portfolios 16 columns

105.01 Internal models Definition of internal models 13 columns

105.02 Mapping internal models Mapping of internal models to portfolios 2 columns

Results Benchmarking Portfolios - Market RiskTemplate

NumberShort Name Full Name

Size of Template

106 IMV Initial Market Valuation 7 Columns

107.1 VaR & SVaR 1 VaR and SVaR non-CTP: details 18 cells

107.2 VaR & SVaR 2 VaR and SVaR non-CTP: base currency results 3 Columns

108 1Y P&L One year Profit & Loss VaR 2 Columns

109.1 IRC 1 Incremental risk charge: details of the model 4 cells

109.2 IRC 2 Incremental risk charge: details by portfolio 3 cells

109.3 IRC 3 Incremental risk charge: amount by portfolio / date 2 columns

110.1 CT 1 Correlation trading: details of the model 4 cells

110.2 CT 2 Correlation trading: details by portfolio 3 cells

110.3 CT 3 Correlation trading: amount by portfolio / date 2 columns

www.lombardrisk.com

Project work & ongoing preparation

for all this?

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

Project work

Business issues:Glide path to new ratios and adjustment to business modelsAdjusting quality of and quantity capitalAdjusting quality and quantity of high quality liquid assetsChanging business operating model: more, and more frequent reportingSerious liquidity supervisory reporting

Operational issues:Many data challenges

New data types Existing data but at deeper granularity

No current reporting – project time to develop expected resultsDeeper reconciliation with management informationReporting peaks exacerbated with more reports due at the same timeAdditional people and equipment resources…

Lombard Risk - Enabling regulatory compliance

www.lombardrisk.com

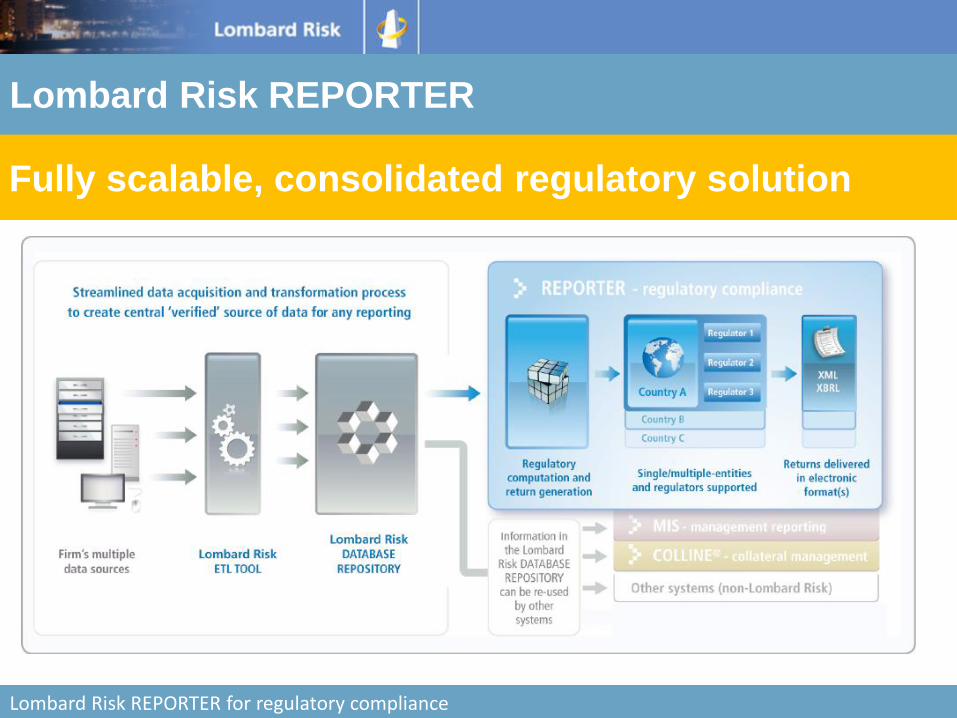

Lombard Risk REPORTER

Lombard Risk REPORTER for regulatory compliance

Fully scalable, consolidated regulatory solution

www.lombardrisk.com

Implications of DFA for BBVAQuestions & Answers

Question submitted in advance:Will this new regime apply to FCA-regulated investment firms, or will they

continue to report under the current regime (FSA047-48, 50-54)?

FCA hasn’t released any LCR statement since LCR delegated act, but FCA stated in PS13/10 ‘we confirm our

approach to continue the UK’s liquidity regime (including ILAS) until binding minimum standards for liquidity

coverage requirements are implemented in the CRR in 2015. FCA will issue a further statement on our liquidity

approach in due course. Until then, BIPRU 12 requirements continue to apply to all IFPRU firms and some

Significant IFPRU / ILAS firms will continue to report CRD IV LCR (i.e. current LC templates) and NSFR COREP

templates”.

Early 2015: FCA stated FCA PS15/2 Recovery and Resolution Directive: “… in October 2014, the European

Commission adopted a Delegated Regulation on the liquidity coverage requirement (LCR). This Delegated

Regulation does not apply to investment firms which means that, initially, there is no CRR binding minimum liquidity

requirement on investment firms. Furthermore, there is to be a review of the applicability of the LCR to investment

firms, which we would not wish to pre-judge”

Conclusion is that FCA regulated investment firms will continue to report what they are current reporting (FSA047-

054 or/and existing LC return) from 1st October. No change from 2015 status quo.

Questions raised during the webinar?

Open for additional questions now ….

Lombard Risk - Managing collateralised trading | Enabling regulatory compliance

www.lombardrisk.com

Implications of DFA for BBVA

The material supporting today’s event will be made available to DELEGATES ONLY and is confidential material - please respect that. - PowerPoint presentation- Results of on-line polls

Recording upon request

You will receive an invitation to future webinars in the Regulatory update series

What’s next?

Lombard Risk - | Enabling regulatory compliance

Thank you for joining us today – we hope you enjoyed and benefited from it.

Please complete the short post-event survey online. If you

have any questions please do not hesitate to contact us on: [email protected]

Next webinar