regulation of the unconditioned local loop service (ulls) presentation to acma international...

TRANSCRIPT

Regulation of the Unconditioned Local Loop Service (ULLS)

Presentation to ACMA International Training program 2006

Michael EadyCommunications Group

Compliance and Regulatory OperationsAustralian Competition and Consumer Commission

The telecommunications access regime

• What is the ULLS?

• Declaration

• Level of prices for the ULLS

• Recovery of ULLS-specific costs

• Averaging vs. de-averaging

• Conclusion

1. What is the ULLS?

Technical definition

• The unconditioned local loop service is the use of unconditioned communications wire between the boundary of a telecommunications network at an end-user’s premises and a point on a telecommunications network that is a potential point of interconnection located at or associated with a customer access module and located on the end-user side of the customer access module.

Or in other terms…

• More usefully (but less accurately):– piece of unconditioned wire between an

end-user and a customer access module

• Most often:– copper between a residence/business and

a telephone exchange

What is the ULLS used for?

• ULLS gives the access seeker complete control over the wire

• Access seekers will use the ULLS in conjunction with exchange equipment to provide:– Broadband internet access– Traditional voice services– VoIP

2. Declaration

8

When was ULLS declared?

• ULLS was originally declared by the ACCC in 1999

• It was re-declared for a further three years in July 2006.

9

How does declaration occur?

• Declaration can only occur if the ACCC is satisfied that declaration will promote the long-term interests of end-users.– promotion of competition– ensuring any-to-any connectivity– economically efficient use of and

investment in infrastructure

10

Relevant markets

• wholesale and retail supply of fixed voice services

• wholesale and retail supply of customer access services

• wholesale and retail supply of:– business grade broadband– residential grade broadband

11

Facilities- and quasi-facilities based competition

• Some alternative access networks– wireless, Optus cable, other fixed-line

• Telstra’s copper network is dominant:– around 87% of Australian homes rely on

voice services over Telstra’s Customer Access Network (CAN)

– 12% over Optus cable– alternative networks are typically in

geographically discrete areas

12

Facilities- and quasi-facilities based competition

• Also these networks’ existence does not necessarily imply effective competition

• However quasi-facilities-based competition is developing:– access seekers use ULLS and LSS – deliver services via Telstra’s network but

also using own infrastructure – e.g. Optus, iiNet, Primus, TPG, others

13

Basic access

• Resale of Telstra’s services still the primary form of competition in the retail supply of basic access

• Telstra still the predominant retail supplier of basic access (around 79%)

• Overall number of basic access lines decreasing

14

Broadband internet

• Around 80% of broadband connections are provided using DSL technology

• Increasing use of ULLS for supplying broadband in past year or two.

• Wireless is growing, but in early stages, although significant in rural areas.

15

Barriers to effective and sustainable competition

• Substantial sunk costs

• Economies of scale

• High customer switching costs

• Customer inertia

16

Assessment of declaration – promotion of competition

• Wholesale– Before 1999 declaration, Telstra did not

provide a ULLS service– Alternative networks provide only localised

pressure on Telstra’s ULLS pricing

17

Assessment of declaration – promotion of competition

• Retail– ULLS important basis for competition in

basic access, voice and broadband– larger variety of possible providers– speed and price variation much greater on

own infrastructure– without it, companies limited in many cases

to reselling Telstra’s products

18

Assessment of declaration – promotion of competition

• ACCC signalled would be open to providing exemptions for certain geographic areas where effective and sustainable competition existed– audit of competitive infrastructure

19

Assessment of declaration – economic efficiency

• Depends on price, but– increased competition encourages

investment in infrastructure by Telstra and its competitors

– need to use infrastructure more efficiently– Telstra keeps ability to exploit economies

of scope and scale and recover costs– allows alternative technologies where

appropriate

3. Level of prices for ULLS

21

History

• Long history since declaration of dispute between Telstra, ACCC and industry over appropriate pricing and costs for ULLS

• Incentives fairly clear for Telstra and access seekers

• Cost-based (TSLRIC+) pricing

22

History

• Pricing principles paper Mar 02

• Undertakings submitted by Telstra in Jan 03, Nov 03, Dec 04 and Dec 05 – the first two withdrawn by Telstra, the latter two rejected by ACCC

• Model prices Oct 03

• Access disputes (currently 9)

23

Issues in dispute

• Demand adjustment mechanism

• Access deficit contribution

• Cost of capital

• Network costs

• Recovery of ULLS-specific costs

• Averaging of prices

4. Recovery of ULLS-specific costs

25

ULLS-specific costs?

• Certain computer systems had to be put in place to enable Telstra to supply the ULLS (and LSS)

• Telstra must employ people to– manage the ULLS project– liaise with wholesale customers

• Indirect costs

26

ULLS-specific costs?

• ACCC and Telstra in disagreement over the level of costs

• However main area of disagreement is how the costs should be recovered.

27

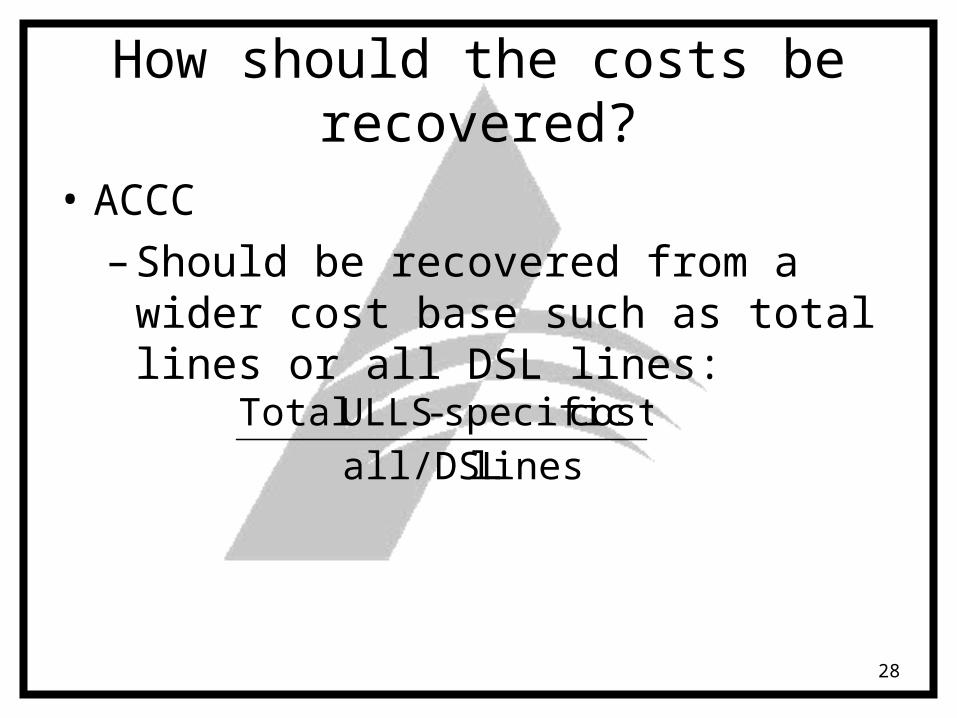

How should the costs be recovered?

• Telstra

– Should be recovered only from the current number of ULLS lines:

lines ULLS#

costs specific- ULLSTotal

28

How should the costs be recovered?

• ACCC

– Should be recovered from a wider cost base such as total lines or all DSL lines:

lines all/DSL

costs specific- ULLSTotal

29

How should the costs be recovered?

• Disagreement stems from debate over:– the causation of the costs

• Declaration?• Users of the ULLS?

– consideration of statutory criteria• e.g. effect on promotion of competition

30

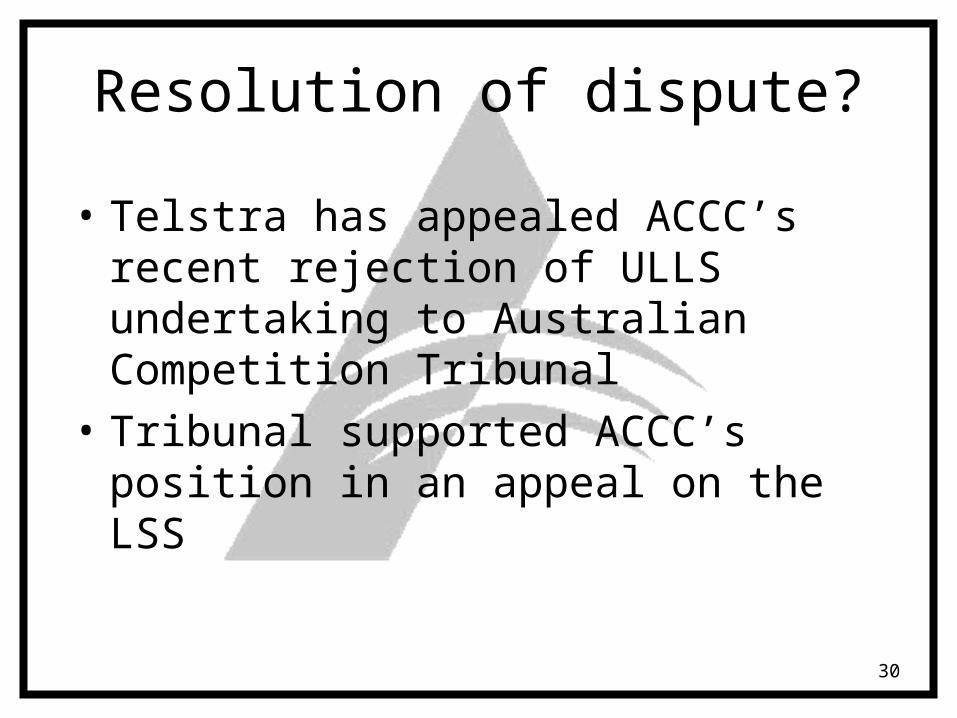

Resolution of dispute?

• Telstra has appealed ACCC’s recent rejection of ULLS undertaking to Australian Competition Tribunal

• Tribunal supported ACCC’s position in an appeal on the LSS

5. Averaging vs. de-averaging

32

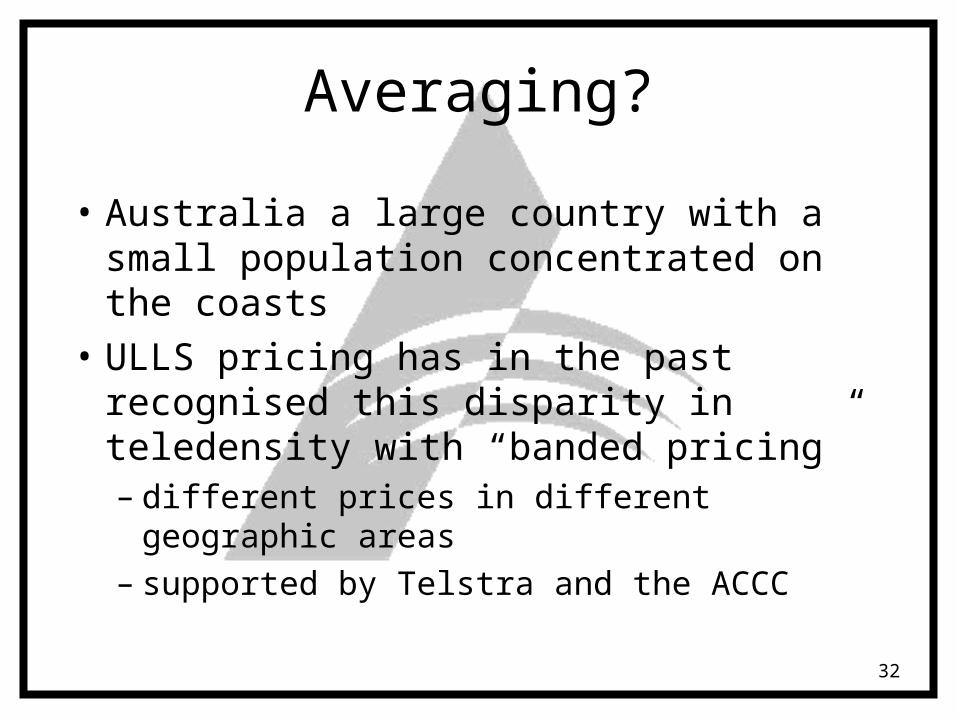

Averaging?

• Australia a large country with a small population concentrated on the coasts

• ULLS pricing has in the past recognised this disparity in teledensity with “banded pricing”– different prices in different geographic

areas– supported by Telstra and the ACCC

33

Averaging?

• The model prices in October 2003 had prices in CBDs of $13, in metropolitan areas of $22, regional areas of $40 and rural areas of $100

34

Averaging?

• Telstra’s most recent undertaking proposed averaged prices– Government has placed obligation on

Telstra to provide a basic line rental and local call product at the same retail price across the country

– Telstra now proposes one $30 price for ULLS in all geographic regions

35

Reasons for disagreement

• Disagreement stems from views on:– effect of Government retail pricing

obligation– feasibility of bypass– ability to recover overall costs

36

Reasons for disagreement

• Some considerations:– might induce inefficient bypass in

metropolitan areas– ability to compete in rural areas might be

limited

37

Resolution of dispute?

• Telstra has appealed ACCC’s recent rejection of ULLS undertaking to Australian Competition Tribunal

6. Conclusion

39

ULLS pricing

• Long history of dispute

• Contentious issue between Telstra and ACCC

• Large number of issues in dispute

• Examples include:– recovery of ULLS-specific costs– averaging or de-averaging

40

ULLS pricing

• Large number of access disputes over ULLS charges

• ACCC has made interim determinations in some of these disputes

• Australian Competition Tribunal appeal to be heard in coming months

41

Further information

• ACCC, Declaration inquiry for the ULLS, PSTN OTA and CLLS—final determination, July 2006.

• ACCC, Assessment of Telstra’s ULLS monthly charge undertaking—final decision, August 2006.

• www.accc.gov.au