regional economic and energy outlook: perspectives on · pdf fileregional economic and energy...

TRANSCRIPT

Strategic Advisors in Global EnergyStrategic Advisors in Global EnergyStrategic Advisors in Global Energy

Regional Economic and Energy Outlook: Perspectives on Malaysia

Ben CahillSenior Manager, Markets and Country Strategies Group

12 July 2011

3rd Energy Forum | PFC Energy | Page 2

Overview: Malaysia’s Energy Challenges

Challenges: – Shallow-water production declines– Small size of recent discoveries– Difficult reserves– Growing gas demand—and subsidy burden

Proposed Solutions:– Upstream incentives for marginal field development– Increased investment by PETRONAS, especially downstream– Increase in gas prices to tackle the subsidy burden– Proposed reduction in PETRONAS dividends to the state

Will these reforms be sufficient to position Malaysia for the years ahead?

3rd Energy Forum | PFC Energy | Page 3

Emerging Markets, Especially in Asia, Still Driving Oil Demand Growth

World oil demand growth is projected to rise by close to +1.4 mmb/d in 2011, and to slow in 2012 to +1.2 mmb/d.

– OECD economies, especially Japan, are expected to return to demand contraction in 2012.

– Poor economic performance in the advanced economies will hinder global growth, limiting EM growth.

Demand in 2013 will end some 5.0 mmb/d above the pre-recession high, absorbing the bulk of the upstream capacity brought on line since 2008.Emerging Asia (with China as its core) and the Middle East are likely to remain the world’s main growth centers for oil demand in the next two years.

OECD51%

China11%

Emerging Asia11%

Middle East9%

FSU and Eastern Europe

6%

Latin America8%

Africa4%

Global Oil Demand in 2012(Total = 88.6 mmb/d)

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

mb/d

Global Demand Growth

OECD Non-OECD Total

Source: PFC Energy, Market Intelligence Service

3rd Energy Forum | PFC Energy | Page 4

Slower Growth in Asia Emerging Asia’s oil demand growth in the next few years will be weighed by higher oil prices, sluggish advanced economy growth and a maturing Chinese economy.

In the longer term, growth will slow, in particular in Southeast Asia (except for Indonesia), where countries are trying to substitute away from oil by using more natural gas and biofuels.

China will also see slower (albeit still very strong) growth, as GDP growth will probably moderate to around 9% in 2012-2013, in tandem with Beijing’s plans to shift the economy to qualitative domestic demand-fueled growth and cool off fixed asset investment.

0

200

400

600

800

1,000

1,200

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Non-OECD Asia Demand Growth(year-on-year)

China India Indonesia Other Asiamb/d

PFC Energy expects non-OECD Asia’s oil demand to grow by 660 mb/d and 800 mb/d in 2012 and 2013 respectively.

India’s demand growth will buck the regional trend and accelerate in the next two years, likely averaging 150 mb/d and 190 mb/d in 2012 and 2013 vis-à-vis the 140 mb/d expected for 2011.

Source: PFC Energy, Market Intelligence Service

3rd Energy Forum | PFC Energy | Page 5

Malaysian Production Outlook: Shallow Water in Decline, Deepwater Growth Expected

Deepwater production is likely to grow markedly over the decade, and necessary to counterbalance shallow water decline

Deep

Malaysian Oil & Gas Reserves19.5 Billion BOE

Source: PFC Energy

3rd Energy Forum | PFC Energy | Page 6

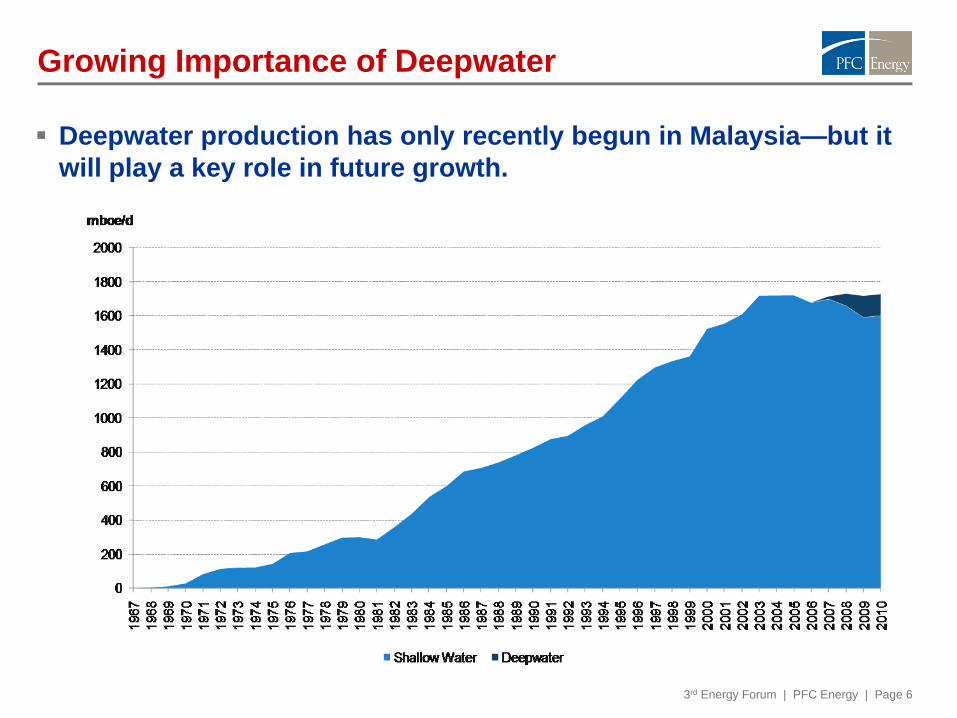

Growing Importance of Deepwater

Deepwater production has only recently begun in Malaysia—but it will play a key role in future growth.

3rd Energy Forum | PFC Energy | Page 7

Recent Discoveries Are Smaller in Size

Oil Field Size Distribution (mmbo)

Gas Field Size Distribution (bcf)

Discoveries of oil and gas in the past decade have been significantly smaller.

3rd Energy Forum | PFC Energy | Page 8

Distribution of High CO2 Gas Fields by Country

5 Dev.3 Undev.

4 Dev.1 Undev.

1 Dev.4 Undev.

6 Dev.4 Undev.

1 Dev.2 Undev.

0 Dev.1 Undev.

1 Dev.1 Undev.

1 Dev.0 Undev.

Natuna D Alpha

3rd Energy Forum | PFC Energy | Page 9

MLNG Accounts for 10% of Global LNG Supply

Malaysia is a major world exporter of LNG

But 60% of existing MLNG contracts expire between 2015 and 2019

New sources of gas will be needed to extend these contracts

Source: PFC Energy

3rd Energy Forum | PFC Energy | Page 10

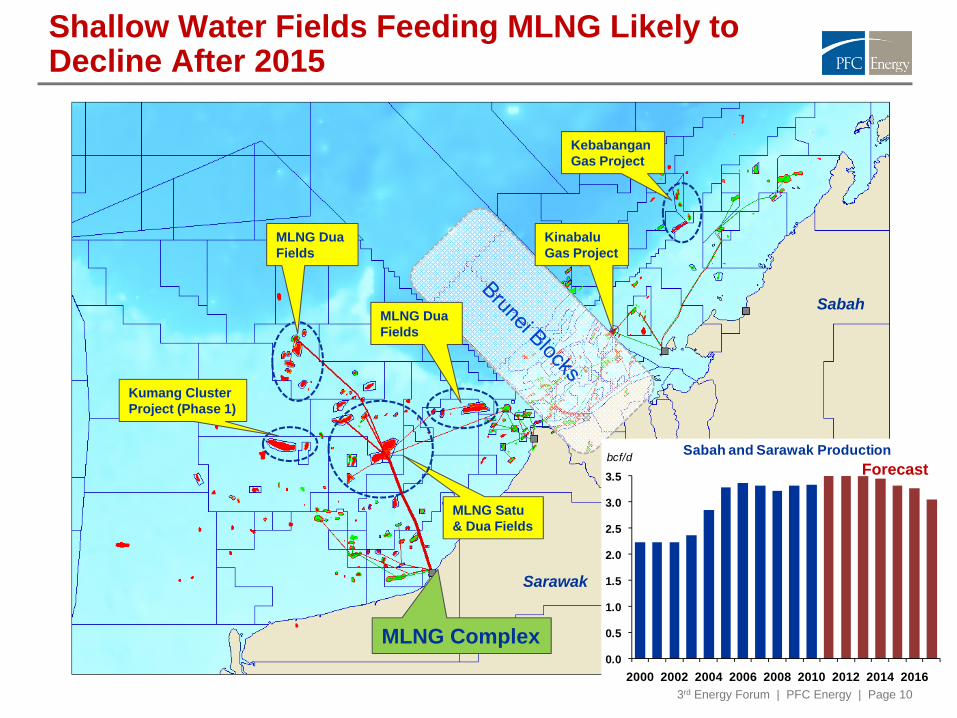

Shallow Water Fields Feeding MLNG Likely to Decline After 2015

MLNG Satu & Dua Fields

MLNG Complex

Kebabangan Gas Project

KinabaluGas Project

Kumang ClusterProject (Phase 1)

MLNG Dua Fields

MLNG Dua Fields

Sabah

Sarawak

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2000 2002 2004 2006 2008 2010 2012 2014 2016

bcf/d Sabah and Sarawak ProductionForecast

3rd Energy Forum | PFC Energy | Page 11

Deepwater Sabah is Key for Future Production

New deepwater developments Shell Kakap Gumusut, Shell Malikaiand KPOC Kebabangan Cluster will boost production post 2012

O p e n B l o c k s

PETRONAS

Open BlocksNewfield

PETRONAS

PETRONAS

Shell

BHP Billiton

BHP Billiton

Murphy

Murphy

Murphy

Shell

Jangas

Pisagan

Kakap-GumusutLimbayong

Kikeh

Kerisi

Senangin

SiakapKikeh Kecil

Open Block

Kebabangan

Kamansu EastKamansu EastUpthrown

Kamansu EastUpthrown Canyon

Malikai Kinarut

Sabah

Sarawak

3rd Energy Forum | PFC Energy | Page 12

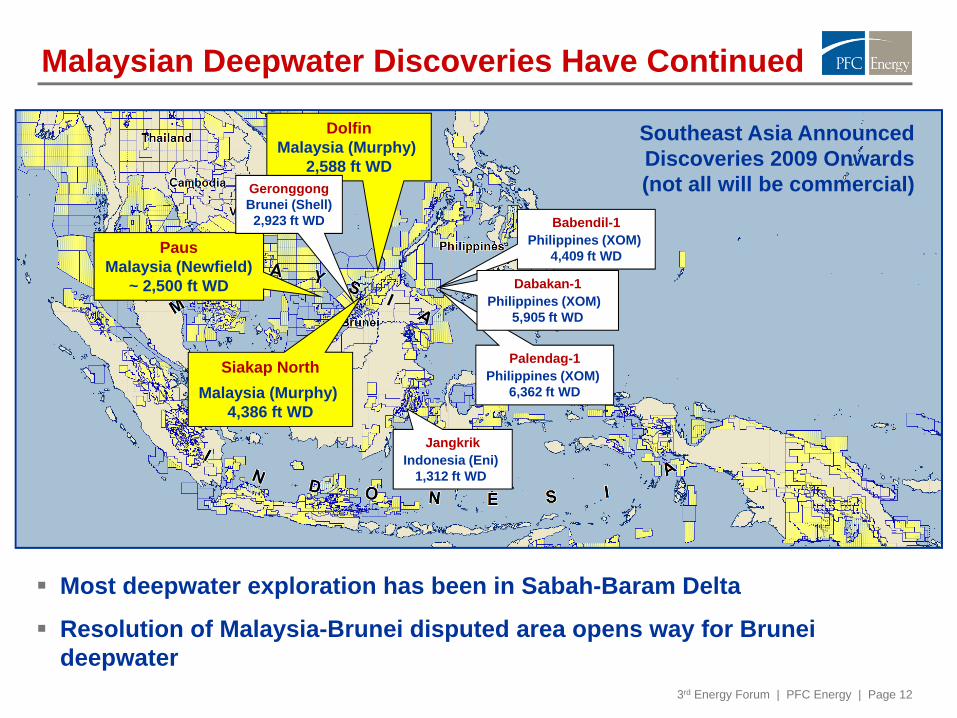

Malaysian Deepwater Discoveries Have Continued

PausMalaysia (Newfield)

~ 2,500 ft WD

JangkrikIndonesia (Eni)

1,312 ft WD

Siakap NorthMalaysia (Murphy)

4,386 ft WD

Babendil-1Philippines (XOM)

4,409 ft WD

DolfinMalaysia (Murphy)

2,588 ft WD

Palendag-1Philippines (XOM)

6,362 ft WD

GeronggongBrunei (Shell)

2,923 ft WD

Dabakan-1Philippines (XOM)

5,905 ft WD

Most deepwater exploration has been in Sabah-Baram Delta

Resolution of Malaysia-Brunei disputed area opens way for Brunei deepwater

Southeast Asia Announced Discoveries 2009 Onwards(not all will be commercial)

3rd Energy Forum | PFC Energy | Page 13

Offshore Drilling is Expected to Grow

Shallow water drilling to remain relatively steady, then slow decline

Deepwater drilling to increase throughout the decade

Deep

Source: PFC Energy

3rd Energy Forum | PFC Energy | Page 14

The "Malaysian Petroleum Resources Center" Would Foster Local Content and Attract Investment

New government Malaysian Petroleum Resources Center (formerly OFSU) is being set up to create a more competitive service sector.

MPRC will– Restructure industry to

improve competitiveness– Attract foreign

businesses to partner– Promote Malaysian

companies

Proposed as both a Policy Maker and Regulator

EnergySector Structure

PolicyPM’s Office, Economic Planning Unit

Ministry of Energy, Green Technology and Water

PETRONAS & PM

MPRC (proposed)

OperatorRegulatorPETRONAS Petroleum Management Unit (Upstream)

Ministry of Trade and Industry (Downstream)

Ministry of Domestic Trade and Consumer Affairs

MPRC (proposed)

Source: PFC Energy

3rd Energy Forum | PFC Energy | Page 15

Active and Expanding Local Service SectorMISC : MSE and MMHE

– Engineering and Fabrication– FPSO/FSO construction– Marine conversions

Kencana Petroleum– Engineering, fabrication,

installation services– Drilling services– Marine vessel conversions

SapuraCrest Petroleum– Installation of pipelines & facilities– Support vessels and services– Tender drilling rigs

Sime Darby– Engineering– Construction

Kikeh FPSO

Sapura 3000Newfield W. Belumut

Pasir Gudang

3rd Energy Forum | PFC Energy | Page 16

PETRONAS: Large Capex IncreasesPETRONAS recently announced a massive increase in capex for the next five years, reaching RM300 bn (~US$100 bn) over the period. This is double what it spent in the last five years, and more than double what it spent the five years prior to that.

The increase in capex is needed given the large number of capital-intensive projects to which PETRONAS is committed. The composition will also likely look different from previous years, with a greater capexshare directed to downstream, including PETRONAS’s commitment to the RAPID project.

In the domestic upstream, PETRONAS will look to increase spending on exploration, EOR for mature fields, as well as deepwater projects.

3rd Energy Forum | PFC Energy | Page 17

Gas Subsidies: Tackling a Growing BurdenRising gas subsidies, borne by PETRONAS, have been a challenge for some time. The recent announcement of a subsidy reduction reflects gas supply challenges.

Gas prices will rise by 28% for the power sector and 7% for the industrial sector, and continue to increase by RM3 every six months until market prices are reached (by 2015).

This increase in gas prices will improve the economics of PETRONAS’s domestic E&P developments serving Peninsular Malaysia, as well as the two regasification projects under consideration in Melaka and Pengerang, Johor (as part of the RAPID project).

Without the price changes, the commercial case for increased supply to the domestic market is weak, incentivizing PETRONAS to focus on higher value export markets.

3rd Energy Forum | PFC Energy | Page 18

PETRONAS: Change to Dividend System to Free Up Cash for Investment

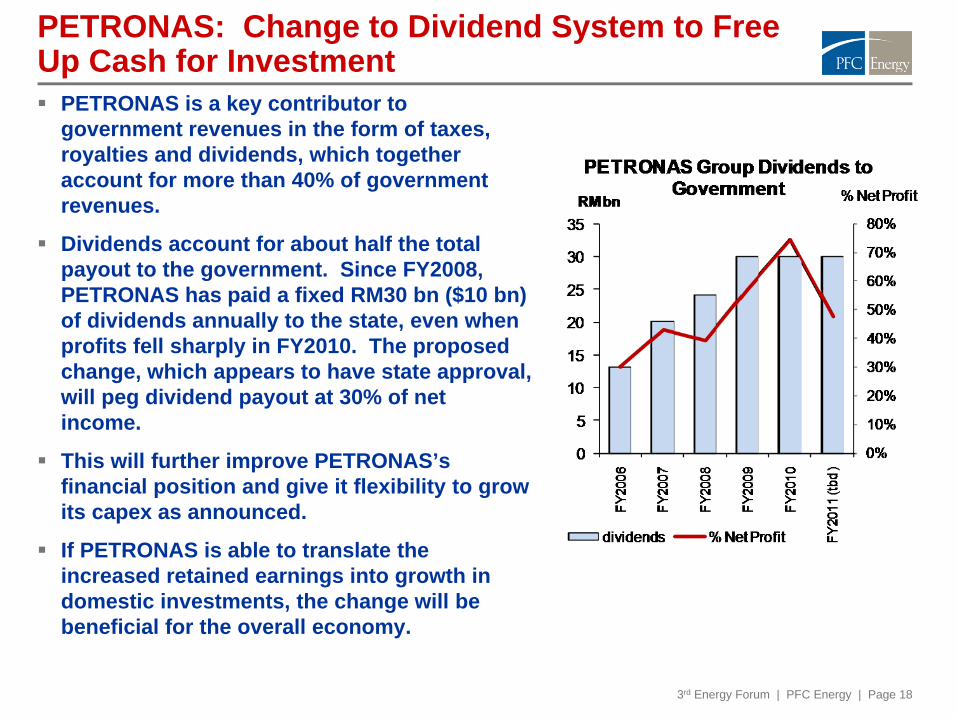

PETRONAS is a key contributor to government revenues in the form of taxes, royalties and dividends, which together account for more than 40% of government revenues.

Dividends account for about half the total payout to the government. Since FY2008, PETRONAS has paid a fixed RM30 bn ($10 bn) of dividends annually to the state, even when profits fell sharply in FY2010. The proposed change, which appears to have state approval, will peg dividend payout at 30% of net income.

This will further improve PETRONAS’s financial position and give it flexibility to grow its capex as announced.

If PETRONAS is able to translate the increased retained earnings into growth in domestic investments, the change will be beneficial for the overall economy.

3rd Energy Forum | PFC Energy | Page 19

Key Conclusions

Progress toward addressing upstream challenges:– Increased capex– Focus on challenging reserves and play types– New incentives

But other challenges remain:– Gas pricing – lack of incentives for deepwater gas– Small contribution of marginal field developments

Strategic Advisors in Global Energy

www.pfcenergy.com | [email protected] regional offices are shown in blue.

PFC Energy consultants are present in the following locations:

Beijing

Brussels

Delhi

Ho Chi Minh City

Houston

Kuala Lumpur

Lausanne

London

Mumbai

New York

Paris

Singapore

Vancouver

Washington, DC

Main regional offices:

AsiaPFC Energy, Kuala LumpurLevel 27, UBN Tower #2110 Jalan P. Ramlee50250 Kuala Lumpur, MalaysiaTel (60 3) 2172-3400Fax (60 3) 2072-3599

PFC Energy, China79 Jianguo RoadChina Central Place Tower II, 9/F, Suite J Chaoyang DistrictBeijing 100025, ChinaTel (86 10) 5920-4448Fax (86 10) 6530-5093

PFC Energy, Singapore9 Temasek Boulevard#09-01 Suntec Tower TwoSingapore 038989SingaporeTel (65) 6407-1440Fax: (65) 6407-1501

EuropePFC Energy, France19 rue du Général Foy75008 Paris, France Tel (33 1) 4770-2900Fax (33 1) 4770-5905

PFC Energy International,Lausanne1-3, rue Marterey1003 Lausanne ,SwitzerlandTel (41 21) 721-1440 Fax: (41 21) 721-1444

North AmericaPFC Energy, Washington D.C.1300 Connecticut Avenue, N.W. Suite 800Washington, DC 20036, USATel (1 202) 872-1199 Fax (1 202) 872-1219

PFC Energy, Houston4545 Post Oak Place, Suite 312 Houston, Texas 77027-3110, USA Tel (1 713) 622-4447 Fax (1 713) 622-4448