reg multiple choice notes1

TRANSCRIPT

EXCLUDED FROM GROSS INCOME

Annuities

Contribution prorated over life of annuityExample:Brown’s contribution = $12,000Life expectancy = 10 years12,000 ÷ 120 months = $100 per month excluded from income6/2007: annuity payments started so 100 x 7 mos = 700 excluded2008: 12 mos x 100 = 1200 excluded

Life insurance proceeds

Generally, life insurance proceeds are excluded from gross income. Example: 200,000 policy (for Halle’s parents)Frank bought policy from Halle for $25K,Frank paid additional $40K in premiumsHalle’s parents dies: Frank must include in gross income excess: $200K – 25K – 40K = $135K

Installment payments:principal amount divided by number of annual payments is excluded. Example: Frank name Halle beneficiary of $100K, Halle expected to live 25 years100K ÷ 25 yrs = 4K per year, any excess over this amount to be included in income

Employee Benefits

Cafeteria plans- Participants select their own menu of benefits- For employee only.- No minimum period required- Do not qualify: deferred comp plans, scholarships, educational assistance, other fringe bens

Only $50,000 of group-term insurance coverage is excluded from gross income but entire proceeds excluded in beneficiary’s income.

Death payments to employee’s wife/son from Employer included in wife/son’s gross income.

Moving expenses are a fringe benefit & excluded from gross income.

Gifts & InheritancesAlternate valuation date is 6 months after date of bequeath of stockInheritance and gift excluded from gross income. If stock was distributed to Halle before alternate date then that date is date of basis.

Stock Dividends

Include in GI:- Dividends from common & preferred stock- recognize in year dividend received in mail - from company in foreign country (Canada)- Company gives Halle stock dividend on Preferred Stock @ FMV

Exclude in GI:- Dividends from life insurance policy if not yet exceeded accum premiums paid.

Interest income

Bond premium amortization- computed under constant yield to maturity method- treated as an offset to the interest income on the bond

Interest income on redemption of US Series EE Bonds generally excluded from GI subject to modified GI limitation and a limit of total bond proceeds is not in excess of qualified higher education expenses:

1

Example: received proceeds of principal of 5,000 and interest of 2,132 = 7,132. Qualified educational expenses totaled 4,000. Take 4,000/7,132 = .561 x 2,132 = 1,196 may be excluded from interest income.

- exclusion applies for education expenses by taxpayer, spouse, dependent claimed- Qualified higher education expenses must be reduced by qualified scholarships not included in GI.- Purchaser of bonds must be sole owner of the bonds or joint with spouse

Include Interest income in GI:- on US Treasury certificates- on Federal & state income tax refund- on Federal government obligations- on award for personal injuries

Exclude interest income from GI:- on State government obligations- on State or municipal bonds- political subdivisions (New York Port Authority)- US possessions (Puerto Rico)- Award for personal injuries

Forfeiture penalty for premature withdrawal – deduction from GI to arrive at AGI.

Scholarships & Fellowships

Include in GI:- payment to graduate assistant for part-time teaching- grant to PHD candidate for research for benefit of university- stipend for research services required for scholarship

Exclude in GI:- scholarship for tuition, fees, books, & supplies required for course

Lease Improvements

Include in GI:- Lessor include if improvements made in lieu of rent payments

Farm income – Schedule F- Crop insurance proceeds- Payments from agriculture programs whether cash, materials, or services- Discharge of indebtedness for farm assets

Insurance payments for temporary housing, living expensesTaxpayer whose residence is damage or destroyed

Exclusion limited to excess of actual expenses over normal living expenses.Example: Actual rent & food 1,500

Normal rent & food 800 Exclusion amt 700

Insurance payment 1,100 Less exclusion 700 Amt to include in GI 400

Employee exclude cost of employee achievement award to extent employer may deduct itAllows employer deduction up to $400 per award (or 1,600 for qualified plan)

Example: bike cost (awarded to employee under achievement program) 1,200Employee may exclude cost of bike from GI.

Full-time clergyman use of rental fair valueUse of parsonage, fair rental value $4,800Annual salary church pays 13,200S.E. income 18,000

Medical savings account (MSA)Small business (50 or fewer emps)

2

Limited to 65% (75% for family coverage) of annual health insurance deduction amount

Educational assistance program Exclude max $5,250

Dependent care assistanceEmployer payments to employee, nondiscriminatory planExclude max $5,000 for joint file; $2,500 MFS

Qualified adoption expenses – paid by employerMax exclusion $12,150 per eligible childPhased out between $182,180 and $222,180

Employee fringe benefitsNo additional cost services (airline passes)Employee discountWorking condition fringesTransportation fringes – $230 per month for employer-provided parking or transit passes

Foreign income exclusionExclude $91,400 for 2009.

ITEMS TO BE INCLUDED IN GROSS INCOME

Alimony Alimony recapture:Example: Alimony payments:2006: 50,0002007: 20,0002008: zero

2007 recapture: 20k – 15K = $5,0002006 recapture: 50K – (15K +7.5K) = 27,5002008 recapture: 5,000 + 27,500 = 32,500

Excess alimony in 2nd year = Alimony paid in 2nd yr – sum of $15K & alimony paid in 3rd yr. Excess alimony in 1st year = Alimony paid in 1st year – sum of $15K & Average of [alimony paid in 2nd yr – excess alimony in 2nd year (see above)]

Shortcut:

2E = 2P – (15K + 3P)1E = 1P – [15K + (2P – 2E)]

÷2

E2 + E1 = GI for 3rd Year

Deductible alimony by payor: - payments must be in cash- payment must end at recipient’s death

Alimony must be included in GI by payeeChild support is not alimony – neither taxable nor deductible

Example: 20% reduced on 18th birthdayPayor paid $7K to mom, $3K for tuition = 10,000 x .80 = 8,000 (include as income for mom) Remaining $2K is considered child support

Payments allocated to Child support first, remaining goes to alimony.

Payments for ex-wife mortgage is not alimony bc not considered cash payment

Dividend income on shares of stock that taxpayer received for services rendered included in GI

Social Security Benefits

3

Include as taxable income of lesser of:50% * (AGI + tax-exempt income + 50% SS – base amount) or50% * (SS)

Base amounts: $32,000 joint$0 MFS$25,000

85% of SS benefits is max amount to be included in GI or85%*(Provisional income – base amount.

Provisional income 65,200 – base amount 34,000 = 31,200 x 85% = 26,520 + 50% of SSIf 85% of SS benefits is below above formula then use this as amount to include in taxable income.

For joint return: If Modified AGI + ½ SS benefits < 34,000, none of SS benefits are included in GI. Modified AGI = AGI + tax-exempt interestIncludible portion of SS benefits = lesser of ½ SS bens or ½ of excess greater than 32,000 above

+Modified AGI+1/2 SS benefits-$25,000 (single) or $32,000 (joint) base amount=excess (if positive

Excess x 50% = amount included in GI

State tax refund - do not include on Form 1040EX, only on 1040- Include interest on tax refund

Compensation for services - recognized at FMV.

Stock options- employee not subject to tax until stock option is sold. - If employee holds exercised stock option for 2 years from date option granted, emp’s realized gain treated as

LTCG in year of sale and employer receives no deduction. - If do not meet 2 year rule, then employee report as ordinary income to extent stock’s FMV at exercise exceeded

option price, as result employer receives compensation deduction equal to amt of ordinary income reported by employee.

Cash-basis decedent- Include bonus earned before taxpayer’s death but not collected until after death.

Foster child payments are excluded from GI to extent they represent reimbursement for expenses incurred for care of foster child.

Tips over $20 must be reported to employer by 10th day of next month and reported in income for year reported. Example:2,000 in tips in Dec. 2007, reported to employer on January 5, 2008, Employee to report on 2008 return

Award for civic achievement – exclude from GI if:- directly transferred by payor to gov’t unit, charity, educational, or religious group- recipient was selected without action of own- recipient not required to render future services

Lottery winnings- include in GI- money spent on buying lottery tickets can be deducted if you itemize, NOT subject to 2% of AGI floor.

Rents & Royalties- include advance rental payments- lease cancellation payments- value received for modifying lease- improvements in lieu of rent- bonus received for granting lease

4

- Accrual-basis taxpayers report: difference of rent receivable of both years plus rents and advance rent received during year. Example: Rent receivable 2007: 35,000Rent receivable 2008: 25,000Decrease (10,000)Rent collection 2008 50,000Rent deposit 2008 5,000Rent revenue 2008 45,000

State unemployment benefits- include all in AGI. For 2009, up to 2,400 excluded from GI.

Noncompete agreement payments - include all as ordinary income – do not amortize

Dividend reinvestment plans - report difference as ordinary income (form of dividends)Example: purchased 100 shares at $30, FMV $32, therefore $2 x 100 = 200 is ordinary income

Amounts paid for future services required to be included in year of receipt. EXCEPT: accrual taxpayers allowed a limited 1-yr deferral of income. Example: received in Nov 2007 for 2-y contract, payment for work in 2007 included in income for 2007 return, remaining deferred to 2008 even if some work into 2009.

Discharge of debt is gross income or reduce basis in building mortgaged.

Original issue discount bondsHow much original issue discount to include in GI assuming current market yield?

10% bonds at original issue for 12,000. Stated redemption price of 15,000Market yield 14%

Original issue price x market yield 12,000 x 14% = 1,680Less interest payable (stated redemption price x original issue %) 15,000 x 10% = 1,500 Pro rata amount included in GI = 180

Interest-free loansCorp made interest-free loan of 15,000 to shareholder on 1/1/08, payable on demand. If loan not repaid as of 12/31/08, statutory federal rate is 5%. = 750 is dividend paid by Corp and dividend income to shareholder.

Noncontributory pension plan paymentsInclude in gross income

No-additional-cost-services Include if provided on discriminatory basis

TAX ACCOUNTING METHODS

Cash-basis taxpayer should report gross income for year in which income is either actually or constructively received, whether in cash or property.

Change in accounting method; IRS permission for:1) Units-of-production method to straight line2) LIFO to FIFO3) Cash basis to accrual basis

In calculating rent payments, take FMV of promissory note.

Clear reflection of income – most important principle in valuing inventoriesAcceptable methods of valuing inventories:

1) Specific-cost-identification method (cost method)2) Retail method used with FIFO method3) Lower-of-cost-or-market method

5

Entities that CAN used cash method accounting1. Personal service corporation2. Entity for every year has avg gross receipts of $5 million or less for prior 3-year period and has no inventories3. small taxpayer with avg annual gross receipts of less than $1 million for prior 3-year period & exempt from

requirement to account for inventories.4. PSC examples: accounting firm, health, law firm, consulting,

Can NOT use cash method:1. C-corps2. Partnerships that have C-corp as a partner3. Tax shelters4. Tax-exempt trusts5. Corp or partnership that has inventories and avg annual gross receipts for 3yr period exceeding $5 million.

Bonus expense for accrual method taxpayer- payment must be made within 2 ½ months (March 15)

Prepaid interest on loan : if extend beyond end of tax year, advance payment should be spread over period it coversExample:$12,000 advance payment in Dec. 1, 2007Loan period: Dec. 1, 2007 to Nov. 30, 20082007 interest deductible: 1,000 (1 month)2008 interest deductible: 11,000 (11 months)

Stock received in satisfaction of services rendered for Cash-basis taxpayer:- recognize at FMV when stock received.

Accrual method mandatory for sole proprietor when there are year-end merchandise inventory.

Salary taxable when actually or constructively received for cash-basis taxpayerExample:Halle (cash-basis taxpayer) earned 80,000 in 2008Grosvenor was able to pay 80,000Halle elected to take only 50,000 in 2008Halle has to report full $80,000 in 2008

Cash-basis taxpayer can not include year-end 2008 bonus paid in 2009 in net income.

Installment basis – gross profit (does not require IRS approval)Question: does not live in community property.

land with basis of 10,000 in 1992Wife died in 2002 when land valued at $50,000Husband (widow) sold land for $100,000 on installment basis. What is gross profit?

As surviving spouse, basis is half of property. 1. Reduce cost by depreciation /depletion. 2. Increase the reduced cost by your basis in half you inherited. Therefore widow’s adjusted basis at time of sale is:

10,000 / 2 = 5,000 + ½(50,000) = 30,000 is widow’s basis3. Gross profit = (100,000 sale price – 30,000 basis) / 100,000 = 70% GP

Completed-contract method allowed for:Only for construction contract for small business (defined as: <10M gross receipts for prior 3 years) if expected to take < 2 yrs to complete or home construction.

- Any non-housing contract does not apply.- Any non-housing project by large business does not qualify

Percentage-of-completion method(Actual costs / total costs to complete) x profit = gross profit in year to report

LIFO vs FIFO when prices are risingLIFO = lower current tax liability and COGS is higher.

STANDARD DEDUCTION AND PERSONAL EXEMPTIONS

Standard deduction for student under age 24 = greater of $900 or dependent’s earned income + $300.

6

In joint return, parents can claim as dependents?1) 19 yr old full time student, earned 5,650 – YES –under age 24 student, income no matter2) Daughter, 23, bank teller earned 13,150 – NO – earned over exemption amt $3,6503) Elder parent, earned 7,325 dividend, 6,325 SS –NO –earned over exemption amt; SS exempt from earned

income rule.

Personal exempts for each taxpayerblind and over 65 age - Extra standard deduction

Personal Exemption reduced by 2% for each 2,500 or fraction thereof, by which AGI exceeds threshold. For 2009, it is Joint 250,200MFS 125,100HOH 208,500Single 166,800 Question: AGI 260,000, single, no dependents. What is personal exemption? AGI: 260,000Threshold (166,800) 93,200 divided by $2,500 = 37.28 (round up) so 38.

Exemption: $3,650 (for 2009)Percentage deduct 93,200/2,500 x 2% = 76%Reduction by 1/3 (925) or (3,650 x 76% x .333333)Exemption amt: 2,725

Qualify as dependent:Citizen, national, or resident of U.S. or resident of Canada or Mexico

Taxpayer must furnish ½ of total support provided during calendar year.1. FV of lodging2. Medical expenses paid for benefit of dependent3. proportionate share of expenses incurred in supporting whole household.

Watch for questions that ask for exemption amount or number of dependents. Wife is not dependent, rather, get an exemption. Additional standard deduction for blind or over 65, not exemption.

TAX CREDITS

Earned income credit - REFUNDABLERefundable even if no tax withheld from wagesQualifications:

1. principal resident in U.S for more than half of taxable year2. at least 25 years old, not more than 64 yrs.3. Individual can’t be claimed as dependent of another taxpayer

Does not include:1. Dividends & interest2. Welfare benefits3. Veteran’s benefits4. Pensions, annuities, SS bens5. Workers & unemployment compensation6. Taxable scholarships or fellowships

Earned income includes:1. Value of meals or lodging for convenience of employer2. Combat-zone pay3. Earnings from self-employment4. Dependent care benefits5. Union strike benefits

Research creditAlternate calculation Base amount (B) = avg gross receipts for 4 yrs prior to curr taxable yearTier 1: 3% x [(B x 1.5%) – (B x 1%)]

7

Tier 2: 4% x [(B x 2%) – (B x 1.5%)]Tier 3: 5% x [qualified expenses – (B x 2%)]Add together all 3 tier calcs to get credit amt. Basic calculation:= 20% x [qualified expenses – (ratio of total qualified research expense over total gross receipts x B)

First time qualified research expense (‘start-ups’)20% x (75% of qualified research exp - 3% of gross receipts)(Qualified exp x 75%) – (gross receipts x 3%) Example: $25,000 paid to research studioGross receipts $50,000Had qualified research exp for 1st year (considered startup)(25,000 x 75%) = 18,750(50,000 x 3%) = 1,500Credit: 17,250

Business energy credit30% credit

Disabled Access Credit50% of lesser of expense or (10,250 limit – 250 floor)Exp amt must exceed $250 floor but not exceed $10,250 limit.Example: Corp incurred $25,000 building accessible expenditures.

25,000 or (10,250 – 250 = 10,000)25,000 or (10,000) =10,000 x 50% = 5,000 credit

Child & dependent care credit -NONREFUNDABLEEqual to 35% of up to $3,000 for 1 child; $6,000 for 2 or more less any employer paymentsChild must live with...cannot claim if child lived with former spouse all year. Cost of

- household services partly for well-being of qualifying person- care provided outside of home- sending child to school if grade below first grade & incident to cost of care

Child care credit when have applicable employment-related expensesApplicable rate is 35%, reduced by 1% for each 2,000 by which AGI exceeds $15,000. Example: divorced, AGI of $30,000, employer provides childcare service at $3,000 for younger child. Pay neighbor $2,400 for other child. What is child care credit?30,000 – 15,000 = 15,000 / 2,000 = 7.5 ~ 8 rounded upReduce Applicable rate of 35% - 8% = 27%

Total expenses – employer paid = allowable amt for credit x reduced applicable rate above. 5,400 – 3000 = 2,400 x 27% = 648

Not work-related exp: payment to housekeeper who provide dependent care while parent off from work because of illness.

Child Tax CreditDependent child under 17 yrs qualify$1,000 credit per childPhased out at 75,000 single; 110,000 joint; reduced by $50 for each $1,000 over AGI.

Adoption creditMax credit of 12,150

Hope Credit100% for 1st $2,00025% for 2nd $2,000So total up to $2,500 a year per studentPhased out at $96,000 for Joint filers in 2008.Available for student’s first 4 years in college – graduate school does not countBoth Hope and Lifetime phase out at $59K for Single.

8

Phase out prorated calcs for example:Phase out starts at 96,000Phase out completely at 116,000AGI: 102,000Take (AGI – phase out start) / (phase out completely – Phase out start)(102 – 96)/ 20 = .30 (this amt times the credit)

Lifetime learning creditCan not be claimed at same time as Hope credit. Only claim in years Hope not claimed. Limited to 20% of 1st 10,000 of tuition paid. Phase out at jointly 100,000 – 120,000

Work opportunity credit40% of first $6,000 of wages paid for over 400 hrs of service by employee25% “ “ if meet 120-hr minimum requirement but less than 400 hrs.

work opportunity credit paid to employees who are long-term family assistance recipients.- 50% of first $10,000 of qualified 2nd year wages- Combined credit for 2 years may not exceed $9,000 per qualified employee.

Rehabilitation building credit - recaptureCredit for rehab exp recaptured if structure sold in less than 5 years. 100% recapture if disposed within First year.20% decline for each year after 1st year.Example: C-corp claimed credit of 30,000, held for 3 years.

100% - (20% x 3 yrs) = 40%30,000 x 40% = 12,000

Rehab cost must exceed adjusted basis of property before credit can be taken.

Disabled or Elderly CreditInitial Sec22 amt $5,000 single or joint w/1 spouse over 65Less Social security or tax-exempt income (x,xxx)Less AGI limitation: [AGI - $7,500) x 50%] (x,xxx) = Sec22 amount xxx

x 15% credit: xxx cannot be more than tax liability before credit.

credit only up to taxpayer’s tax liability before credit.

ALTERNATIVE MINIMUM TAXExcess of tentative AMT over regular tax

Itemized deductions allowed for AMT calculation (GIMC)- Medical expenses exceeding 10% of AGI (instead of 7.5%)- Mortgage interest exp for resident- Charitable contributions

FICA AND FUTA TAXESEmployee who has SS tax w/h in amt greater than minimum for particular year may claim excess as credit against income tax, if that excess resulted from correct w/h by two or more employers.

Net earnings from self-employment – Form SENet profit or loss minus business expenses. Line 4 on Schedule SE must multiply net profit by .9235.

Do not include for self-employment purposes:1. Capital gains losses2. Contributions to retirement plans3. NOL

9

TAX PROCEDURES

Unearned income of minorHow much will be taxed at Chris’ parents maximum tax rate assuming standard deduction is 900.

- Taxed at dependent parents’ marginal rate.- Calculated as net unearned income – ($900 + $900 std. ded.)

Estimated tax payments90% of current year tax, paid in 4 equal installments or110% prior year’s tax liability, paid in 4 equal installments

Each installment meets 25% of 90% of current’s year’s threshold for no penalty.

Return must be filed if taxpayer’s gross income equals or exceeds sum of personal exemptions & standard deductions & additional standard deduction for blind & over 65

exemption: $3,650,

Standard deduction is $11,400 for married couples filing a joint return $5,700 for singles and married individuals filing separately $8,350 for heads of household

Claim of refunds3 yrs from filed or2 yrs from time tax paid, whichever is laterIf no return filed: claim of refund is due 2 yrs from time tax was paid7-yr period of limitation if due to worthless stock

Statute of limitations for assessment of deficiency3 yrs from later of date the return was due or date filed6 yrs if 25% or more omission of GI;

For trade or business, GI is amounts received before sale goods deduction and COGS.Gross receipts 400,000Capital gains 39,000

4399,000 X 25% = 109,000 omitted from GI, 6 yr limitation applies

Federal tax lien:- applies to all taxpayer’s real & personal property, rights to property until tax paid- by law, filed notice to tax lien can be withdrawn if it speeds collecting of tax- require IRS to notify taxpayer in writing within 5 business days after filing lien.

Must file return if income equals:GI >= sum of personal exemptions $3,650f(exclude dependency exemptions) & standard deductionOne expemption for husband & spouse and standard deduction but not for child.

Farmers & fishermensCan avoid estimated tax penalty if they make one estimated tax payment by January 15 of Yr2

BUSINESS INCOME AND DEDUCTIONS

Uniform capitalization rules- must be used by manufacturers of tangible personal or real property- Do NOT apply to retailers or wholesaler who acquires personal property for resale if retailer’s avg annual gross

receipts for 3 preceeding years do not exceed $10 million. - Costs to include in inventory include factory repairs, maintenance, factory administration, officers’ salary related

to production, taxes other than income taxes, cost of quality control & inspection, current & past service costs of pension & profit sharing plans, service support (purchasing, payroll, & warehousing & off-site storage costs)

- Nonmanufacturing costs include selling, advertising, research & experimental costs are not required to be included in inventory.

10

Business selling illegal narcotics- Can deduct cost of merchandise

Business meals and entertainment- 50% deductible

Bad Debts- all taxpayers (except for banks or financial institutions) must use the direct charge-off method rather than

reserve method.- Cash basis taxpayers’ accounts receivable has zero tax basis because income not reported yet, therefore

receivable is nondeductible loss. Example if CPA (cash-basis taxpayer) billed 3,500 in services for client and client declared bankrupt, CPA can deduct zero.

- Non-business bad debt report as Short Term Capital Loss. Example: Halle let Frank Corp. borrow $1,000; Frank went bankrupt; Halle loss$1,000 and is reported as short-term capital loss.

Life insurance premium for officer- company can not deduct if they are the beneficiary

Business gifts deduction: limit to $25 per recipient

Net Operating Loss- personal casualty loss can be deducted against income to come to NOL- 2 back, 20 forward- NOT deductible:

o personal exemption o standard deduction o non-trade, non-business income o capital loss

Losses & Credits from Passive Activities- individual can offset upto $25,000 of income not from passive activities by losses from a rental real estate activity

if individual actively participates in rental real estate. 25,000 is reduced by 50% of taxpayer’s AGI in excess of $100K and completely phased out when AGI exceeds $150K. Example: Halle’s AGI is 200K; incurred $30,000 loss in rental real estate that I activity participate. Zero loss can be used to offset against 200K income because over $150K AGI limit.

- Rules limiting allowability of passive activity loss & credits apply to:

o Individualso Estateso Trustso Closely held C Corpso Personal service corporations

- interest income from temporary investment is considered portfolio income and can not be netted with operating loss

- term “passive activity” includes any rental activity w/o regard as to whether or not the taxpayer materially participates in the activity.

- Passive losses & credits relating to rental activities not used in current year can be carried forward indefinitely or until property is disposed in taxable transaction.

Depreciation, Depletion, and Amortization

Sec 179 expense election

- $250K max of cost of qualifying depreciable personal property as an expense rather than as a capital expenditure. $250,000 is reduced dollar for dollar by the cost exceeding $800,000.

o Example : purchased $820K of production machinery; taxable income before Sec.179 expense deduction was $195K. What is max deduction in current year and carryover? 250K – (820K-800K) = 230K max; therefore 195K expense, carryover = 35K (230-195)

- property must be purchased for use in the taxpayer’s active trade or business

- property must be purchased from unrelated party

- limit to taxable income too, remaining carried forward.

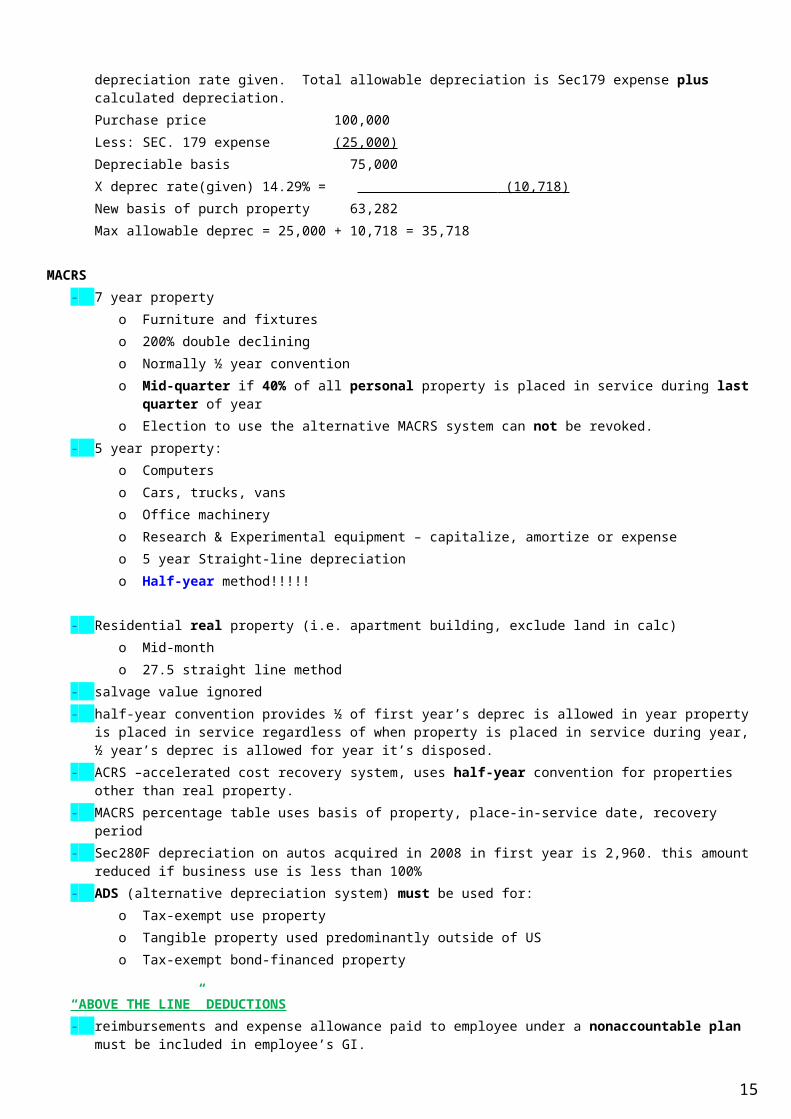

- Say bought computer equipment for $10, received $2 trade-in, adjust basis in old computer $3. used equipment 90% of time. Allowable 179 exp is $10 x 90% = $9; ignore trade in & old basis.

11

- In problems asking you the maximum allowable depreciation with a Sec179 limit in current year, subtract Sec179 expense first to get depreciable basis then times the depreciation rate given. Total allowable depreciation is Sec179 expense plus calculated depreciation.

Purchase price 100,000

Less: SEC. 179 expense (25,000)

Depreciable basis 75,000

X deprec rate(given) 14.29% = (10,718)

New basis of purch property 63,282

Max allowable deprec = 25,000 + 10,718 = 35,718

MACRS

- 7 year property

o Furniture and fixtures

o 200% double declining

o Normally ½ year convention

o Mid-quarter if 40% of all personal property is placed in service during last quarter of year

o Election to use the alternative MACRS system can not be revoked.

- 5 year property:

o Computers

o Cars, trucks, vans

o Office machinery

o Research & Experimental equipment – capitalize, amortize or expense

o 5 year Straight-line depreciation

o Half-year method!!!!!

- Residential real property (i.e. apartment building, exclude land in calc)

o Mid-month

o 27.5 straight line method

- salvage value ignored

- half-year convention provides ½ of first year’s deprec is allowed in year property is placed in service regardless of when property is placed in service during year, ½ year’s deprec is allowed for year it’s disposed.

- ACRS –accelerated cost recovery system, uses half-year convention for properties other than real property.

- MACRS percentage table uses basis of property, place-in-service date, recovery period

- Sec280F depreciation on autos acquired in 2008 in first year is 2,960. this amount reduced if business use is less than 100%

- ADS (alternative depreciation system) must be used for:

o Tax-exempt use property

o Tangible property used predominantly outside of US

o Tax-exempt bond-financed property

“ABOVE THE LINE” DEDUCTIONS

- reimbursements and expense allowance paid to employee under a nonaccountable plan must be included in employee’s GI.

- Utilities and maintenance on property must be divided between personal and rental use.

- Unreimbursed employee business-related expense can not be deducted if you do not itemize. If itemized, limit to 2% AGI floor.

- Indirect moving expenses not deductible: premove house hunting, temporary living and meals while moving, penalty for breaking lease are not deductible. (rules: move 50 miles away, keep job for 39 weeks out of 12 months)

Contributions to Certain Retirement Plans

- Distributions from Roth IRA not included in taxpayer’s gross income if:

o Held for 5 years and must;

12

o Age 59 ½ or older

o Disabled

o First time homebuyer expense

Roth IRA

- max annual contribution to Roth IRA is reduced if AGI exceeds certain threshold

- contributions to Roth not deductible

- can contribute even after age 70 ½

- contribution must be made by due date (apr 15) for year (not including extensions)

- conversion from Traditional IRA to Roth can occur if AGI does not exceed $100,000.

IRA

- allowable deduction is lesser of $5,000 or 100% compensation (earned income, does not include pensions or interest income)

- if 50 or older, $6,000 deductible. = 12,000 for joint.

Education IRA (Coverdell)

- contributions not deductible but earnings are tax-free

- contribute upto $2,000 in 2009/2008

- Eligibility phased out if AGI exceeds certain threshold levels. 190K – 220K joint, 95K - $110K single

- Can be made on behalf of beneficiary until 18 years old.

IRA Deduction ($5,000 limit for each spouse)

Example: Frank & Ha filed joint; Frank earned $35k in wages & covered by employer’s pension plan; Ha unemployed & received $4,000 in alimony first 4 months. Each contributed $5,000 to IRA. Total deduction is $10,000.

- MAGI limit for 2009 if covered by qualified employer plan: $89,000 joint; $65,000 single

- Not covered by employer plan: no limit

- If one spouse covered by employer plan and their AGI are over the phased out $106K, then they can not deduct but other spouse does not have a plan she can deduct upto max if combined income is below phaseout of 160K.

- If age 50, can contribute catchup upto 1,000. so over 50 years and not covered on employer plan can contribute max of $12,000.

- Max contribution for SE individual is $46,000

Keogh profit-sharing:

- “earned income” defined as net self-employment earnings reduced by deductible Keogh contribution and one-half of Self-employment tax. (SE earnings – deductible Keogh contribution – ½ SE tax = earned income)

Jury duty fees

- deducted from GI in arriving at AGI if required to remit fees to employer

- Include in gross income.

READ QUESTIONS FIRST – MIGHT ASK FOR “TAXABLE INCOME”, “GROSS INCOME”

BUSINESS EXPENSE

Advance rental payments made by cash basis taxpayer must allocate payments over period of time

13

LOSSES AND LIMITS – INDIVIDUAL TAX

Casualty & Fire loss

Before consideration of any “floor”, casualty loss calculated as

Lesser of decrease in FMV or adjusted basis

Example:

Adjusted basis 150,000 200 – 150 = 50

FMV before fire 200,000 200 – 180 = 20 Casualty loss

FMV after fire 180,000

Federally declared disaster

1) Option of deducting loss in year of loss or previous year

2) Loss deductions figured using usual rules for nonbusiness casualty losses

3) Can revoke election to deduct loss on preceding year return if made before expiration.

4) Declared unsafe by state or local gov’t.

Passive loss rules

Term “passive activity” loss limitations does not apply to rental real estate activity when individual performs:

1) More than 50% of personal services during year in real property trades or business materially participates and;

2) At least 750 hours of service is performed in those real property trades or business which materially participates.

Passive losses not used in current year can be carried forward indefinitely or until property is disposed of in a taxable transaction.

Generally losses arising from passive activity may be used to offset income from other passive activity but may not use to offset active or portfolio income. (interest & dividends are portfolio income)

Rental activity is passive activity whether materially participate or not.

Individual who participates in rental real estate activity may use up to $25,000 of net losses from rental real estate activity to offset other income. $25,000 reduced by 50% of amount AGI exceeds $100,000. AGI determined w/o regard to SS, IRA contributions, & passive losses)

Example: AGI = 200,000; passive loss 30,000 from rental real estate

200 – 100 AGI = 100 x 50% = 50. 50 is greater than the $25K limit.-

At-risk rules

Limit a taxpayer’s deductible losses from investment activities

Capital losses incurred by married couple filing a joint return will be allowed to the extent of capital gains plus up to $3,000 of ordinary income.

Amount of capital losses that can be deducted are lesser of

- excess of capital losses over cap gains

- or $3,000

Maximum amount of excess of capital gains allowed as deduction is $3,000.

Net Operating Loss – defined

Excess of allowable items over gross income.

NOL generally includes business income or loss:

- Personal casualty loss

- Wages

- Salary income

- Gain on sale of business property

14

Exclude nonbusiness items such as

- Interest & dividends

- Gain on sales of investment property (capital gain)

Net business loss (16,000)

Wages 5,000

Net rental income 4,000

NOL (7,000)

Kiddie tax (taxed at parent’s rate)

Unearned income in excess of $1,900 of child under 18 taxed at parent’s rate

Formula: Childs’s unearned income less sum of(any penalty for early withdrawal + $950 + greater of $950 or child’s itemized deductions)

Parent can report child’s unearned income solely of interest and dividends on parent’s return if between $950 and $9,500.

Child then does not have to file return.

Personal & dependency exemption: $3,650,

Standard deduction is $11,400 for married couples filing a joint return $5,700 for singles and married individuals filing separately $8,350 for heads of household (up $350). Nearly two out of three taxpayers take the standard deduction, rather than itemizing deductions, such as mortgage interest, charitable contributions and state and local taxes.

Tax-bracket thresholds increase for each filing status. For a married couple filing a joint return, for example, the taxable-income threshold separating the 15-percent bracket from the 25-percent bracket is $67,900, up from $65,100 in 2008.

The maximum earned income tax credit for low and moderate income workers and working families with two or more children is $5,028, up from $4,824. The income limit for the credit for joint return filers with two or more children is $43,415, up from $41,646.

The annual gift exclusion rises to $13,000, up from $12,000 in 2008.

Medical expenses (7.5% AGI floor)

- Medical insurance premiums

- Medicine prescribed by doctor

- Unreimbursed doctor fees

- Transportation to/from doctors office

Self-employed can itemize deductions on Schedule A:

- foreign real estate taxes

- foreign income taxes

- personal property taxes

Taxes

- one-half SE tax deductible from gross income to arrive at AGI

- cash-basis taxpayer state & local taxes deductible for year in which paid or withheld.

- Can itemized full realty taxes even if own half the house and back taxes owed if you were part owner then.

- Real estate taxes should be apportioned between buyer and seller even if agreed not to prorate.

Interest expense

- individual taxpayer for interest on investment indebtedness is limited to taxpayers net investment income

- home equity indebtedness to purchase personal goods is deductible upto $100K. “secured by home” , home “unencumbered” by other debt

15

- late file penalty & negligence penalty; deficiency on federal income tax return is not deductible

Charitable contributions

- objects bought at church bazaar, take price paid minus FMV on date of purchase. Excess is deductible.

- Excess carryforward 5 years

- 30% AGI for stock contribution, capital gain property, intangible at FMV, cash contribution at 50% AGI.

- Promissory notes to charity deductible when matured and paid.

- Student expenses deductible with agreement with charity organization is $50 per school month.

- Charity must have full possession. Example: collector reserve right to collection’s use and possession during lifetime.

Personal Casualty and Theft Gains and Losses

-10% AGI floor

- personal casualty insurance is not deductible

Nonbusiness casualty loss computed as:

Lesser of:

Adjusted basis: $70,000

Decline in FMV (130k – 120k ): $10,000

Reduce by:

Insurance recovery:

$100 floor: 10,000-100 =9,900

10% of AGI: = 7,000; 9,900 -7,000 =2,900

Loss: lesser of FMV decline or adjusted basis 10,000

Less: insurance proceeds

100 per casualty

` 10% of AGI (7000)

Appraisal fee to determine fire loss is a miscellaneous deduction subject to 2% AGI floor

Donation of stock

If held short term, it is ordinary income. Deduction = lesser of FMV or adjusted basis

Donation of Land (or any capital assets i.e. art work )

30% of AGI limit. FMV of assets

Year 1: bought land for investment for 14,000

Year 13: donated land to church. FMV at 25,000

AGI of taxpayer: 90,000; therefore limit is 27,000

25,000 deductible.

Contribution of services not deductible

Pledge not deductible until actually paid.

Casualty insurance premium not deductible.

Private nonoperating foundation Charitable contribution deduction

Limit to 20% of AGI for contributions of LTCG

Generally 30% of AGI for all others.

Remaining carried forward for 5 years.

16

State and city sales tax are deductible in lieu of state income taxes, but not deductible in conjunction with state income taxes.

Qualified residence interest

1) Acquisition indebtedness – used to purchase, build, or improve residence. Limit $1M

2) Home equity indebtedness – any debt secured by residence other than acquisition indebtedness. Limit $100,000 or excess of FMV of residence over acquisition.

Adoption expenses – not deductible

Investment interest expense

Limit deduction on investment interest to amt of net investment income.

Capital gain from disposition of investment property generally not considered investment income unless elect to treat as investment income by paying taxes at ordinary rate. Investment income includes:

1) Investment income from dividends and interest 24

2) LTCG on stock held for investment (pay tax at ordinary rate) 25

3) Investment expenses (net with 2 items above) 4

Net investment income 45 – amt deduct

Interest exp on funds borrowed to purchase investment property 70

Cannot take investment interest expense deduction on portion of loan to purchase tax-exempt obligation bonds.

Federal income taxes, penalties, and interest not deductible. Interest paid on amounts owed to IRS considered personal and not deductible.

Miscellaneous deductions itemized deduction subject to 2% AGI floor

- legal fee for tax advice for divorce

- IRA trustee’s fees that are separately billed and paid

- Appraisal fee for charity

- Legal fee to collect alimony

- Unreimbursed business expenses (i.e. outside salesman)

- Initiation fee for membership in union

- Union dues and initiation fees

- Specialized uniforms for work

- Unreimbursed auto expenses

- Income tax preparation

- Income producing fees (management fees on taxable income-producing investments)

- Education expenses deductible as long as already met the minimum requirements for taxpayer’s established employment and does not qualify for new trade or business and education is necessary to keep present job status or pay rate.

-

MISCELLANEOUS ITEMIZED DEDUCTIONS NOT SUBJECT TO 2% FLOOR

- lottery tickets expense limited to lottery winnings

- 2008 state & local income taxes withheld; 2008 state estimated income taxes paid 12/30/08 deductible in 2008 Schedule A.

- Taxes (realty) only deductible by person on whom legally levied. Owner only entitled to deduction if they pay the taxes.

- Gambling losses (to extent of gains), investment interest expense, medical exp, casualty or theft losses.

preparing a Will is not deductible

Reduction in itemized deductions

- Investment interest expenses not subject to phaseout

17

- Lesser of 3% of the excess of AGI over applicable amount or 80% of certain itemized deductions. For 2009, if AGI exceeds 166,800. GIMC does not apply. (Gambling, investment interest, medical, casualty

- For 2009, only 1/3 of reduction apply.

Exemptions

- What is included in determining total support of a dependent?

o Fair value of lodging

o Medical insurance premiums

o Birthday presents given to dependent

- What is NOT included in determining total support of a dependent?

o Nontaxable scholarships

o Life insurance premiums

o Funeral expenses

o Income and social security taxes paid from dependent’s own income

Can not claim exemption for Son who had no income, lived with divorced person, if son filed a joint return and had a tax liability.

Wife is never a dependent.

Cousin and foster parent is not a relationship in IRC. They must be part of household to get dependency exemption.

FILING STATUS

Qualifying widower available for 2 years after spouse’s death if:

1. surviving eligible to file joint return year of death

2. does not remarry before current year

3. surviving pays over 50% of cost of maintaining household for home for entire year.

Head of household

Cost of maintaining household includes:

- rent, mortgage interest, taxes, insurance on home, repairs, utilities, and food eaten in the home

- Does not include cost of clothing, education, medical treatment, vacations, life insurance, transportation, rental value of home an individual owns, value of individual’s services.

Filing joint return

- can file even if have different accounting methods

- must have same tax year to file joint

- if one spouse was non-resident alien at any time during tax year, both spouses must elect to be taxes as US citizens

- can not file joint if divorced before year end

AMTDeduction NOT allowed for:

- personal, state, and local income taxes- miscellaneous itemized deductions subject to the 2% of AGI income threshold- home mortgage interest if loan proceeds were not used to buy, build or substantially improve home.- Personal exemptions and standard deductions

Deductions allowed:- gambling losses

Medical expenses computed using 10% AGI floor instead of 7.5% floorInstallment method can not be used for sales of dealer propertyLong-term contracts, excess of income under percent-of-completion method over amt using completed-contract method

18

Preference items (ADD to taxable income)- private activity bonds – tax exempt interest- accelerated depreciation on real property- percentage of depletion over property’s adjusted basis

Credit for ElderlyLesser of:1) tax liability2) 15%x [initial amount (5,000 S; 7,500 MFJ) – social security benefits – 50%(AGI – amount 7,500 S, 10,000 MFJ)]Example: AGI 20,200, owed $60 tax liability; 3,000 SocSec; both over 65yrsComputation: 15% x [7,500-3,000 – 50%(20,200 – 10,000)] = -90Answer: zero credit because -90 is less than 60.

Child care credit20-35% Reduce by 1% for each 2,000 over 15,000 AGI (only do this calc if 2 or more kids) Max 3,000 for 1 childMax 6,000 for more than 1 child

Foreign tax credit limitation

deductible in full: investment interest expense not exceeding net investment income

Above the line deductions:Business deductions of SELosses from sale or exchangeRents & royalties deductionsSE tax ½ deductibleSE retirement plans up to $5,000SE health insurance 100%Education loans interests up to $2,500Early withdrawal from time depositsAlimony paymentsMoving expenses 100% if employed 39 weeks 1 yr after move. Discrimination suits costsJury DutyTeacher’s expenses

2% floor Outside salesman expenses Unreimbursed employer expense (50% meals & entertainment) Employment agency fees Appraisal fees Subscription to professional journals Dues to professional societies, union dues, initiation fees Physical exams required by employer College professors research, lecturing and writing expenses Teacher pays to a substitute Surety bond premiums Malpractice insurance premiums Chemist laboratory breakage fees Small tools and supplies Tax counseling Tax preparation Expenses for production of income other than those incurred in business or rent and royalties.

No 2% floor Gambling losses to extent of gambling winnings Impairment related work expenses for handicapped Estate tax related to income in respect of a decedent Certain adjustments when a taxpayer restores amounts held under a claim of right Certain costs of cooperative housing corporations Certain expenses of short sales

19

Balance of employee’s investment in annuity contract where employee dies before recovering entire investment

Not subject to reduction (GIMC)Gambling lossesInvestment interest (mortgage interest)Medical expensesCasualty losses

AMT CalcRegular taxable income+- Adjustments+ Preferences= AMT income (AMTI)- Exemptions [46,700 single – (25% of AMTI over $112,500 for single)]= AMT baseX 26% (first $175K) or 28% (> 175K)= Tentative tax before foreign tax credit (alcohol fuels, electricity, coal credit)- AMT foreign tax credit= Tentative minimum tax- Regular tax liability= AMT

AMT Adjustments- medical expenses computed using a 10% floor instead of 7.5%- no home mortgage interest if not used to buy build or improve home- real, personal, state, local & foreign taxes- personal exemptions, standard deductions- LT contracts: percentage of completion method over completed-contract method- Subtract prior year state income tax- Miscellaneous itemized deductions

Preference or adjustment items for noncorporate taxpayers only- Tax-exempt interest on certain private activity bonds- Incentive stock options- Personal exemptions

TRANSACTIONS IN PROPERTY

Basis of PropertyProperty acquired by purchase includes:- cash paid- liabilities incurred, settlement fees- closing costs, title fees, installation utility service, legal fees, title search, contract, deed fees- recording fees, surveys, transfer taxes, owners’ title insurance- any amt owner owes, back taxes & interest, recording or mortgage fees, charges for improvements or repairs,

sales commissions

Acquired by gift- donee’s basis of appreciated property generally donor’s basis.

Land gift – basis- 13,000 annual exclusionAdj basis + [Gift tax paid * FMV – Basis FMV – $13K

Stock received as giftIf sold at a gain: Basis is donor’s basis If sold at a loss: basis is lesser of 1) basis or 2) FMVHolding period starts when gift was received.

Gain LossSold amount Sold amountGreater of FMV or basis Lesser of FMV or basis Gain if positive loss if negative

Acquired from decedent

20

Property received from decedent regardless of actual period is Long-term

Basis of property at:- FMV at decedent’s death or - FMV on alternative valuation date or- FMV at date of distribution if within 6 months of death

Stock received as a dividendIf tax basis of preferred stock is determined in part by the basis of the common stock, holding period of preferred stock includes holding period of common stock.

If get stock dividend, add additional stock to existing stock shares. Divide amount paid by total shares to get price per share (this is new basis)When sell the stock dividend, take the price per sharePrice paid $90,000/(450 old + 50 share dividend) = 180 per shareSell 50 shares for 11,00050 x 180 = 900011,000 – 9000 = 2,000 gain

New shares has same holding period as old shares so LTCG.

Like-Kind ExchangeRealized gain will be recognized only to the extent of unlike property received. Basis of acquired like-kind property is:+Basis of property transferred+amount of gain recognized- amount of boot received

Like-kind means “same class of property”, real for real, personal for personal- exchange of apartment building for office building is like-kind thus no gain or loss. (if no boot or unlike property

was received)- if realized gain, then not recognized.

Nonrecognition of gain or loss of like-kind does not apply to:- exchanges of stock- bonds- notes- convertible securities- partnership interests- property held for personal use

Book value of original truck + (List price – trade in allowance is cash paid) = basis of new truck

Involuntary conversionsReplacement period for nonrecognition of gain ends 3 years after close of taxable year which gain is first realized. Always a December 31 year. Sales and Exchanges of Securities- No loss can be deducted on sale of stock if substantially identical stock is purchased within 30 days before or after sale.- Any loss not deductible is added to the basis of new stock. - worthless securities usually receive capital loss treatment- if loss is incurred by corporation on its investment of 80% or more ownership affiliate then loss treated as ordinary loss.

Losses on deposits in insolvent financial institutions generally treated as a nonbusiness bad debt deductible as a - casualty loss- misc itemized deduction- short-term capital loss

Can NOT as long-term cap loss.

Losses, Expenses, and Interest between Related Taxpayers- losses are disallowed on sales or exchanges of related taxpayers- any gain later realized by the related transferee on subsequent disposition of the property is not recognized to the extent of the transferor’s disallowed loss. Example: Father basis 30,000, sold to daughter for 20,000, realized loss of 10,000 disallowed. Daughter then sold to outside party for 25,000 = gain of 5,000. gain not recognized because of father’s disallowed 10,000.

21

- sale between in-laws and uncles are OK- related transactions by corp and related shareholder (owns more than 50%) losses disallowed.

Capital Gains and Losses-Cash basis taxpayer, gain loss on year-end sale of listed stock arises on Trade date.- Individual’s net long-term loss can be offset against ordinary income upto max of $3,000, the remaining loss is carryover to next year. - Corporation’s net long-term loss can not be offset against ordinary income. Net Capital Loss is carried back 3 year, forward 5 years as STCL. - antique held for personal use; loss is not deductible

Capital assets defined:- property held as investment- investment in US bonds- property held for personal use (residence & furnishings)

Married couple a capital loss incurred will be allowed to offset to the extent of capital gains, plus up to $3,000 of ordinary income.

Section 1231 assets generally include business assets held more than 1 year. “Used in/for business”. Example: land and shed were used in conjunction with parking lot business, they are Sec. 1231 assets.

Sec. 1245 & 1250 include depreciable assets

Covenant not to compete is not a capital asset. Report as ordinary income.

Personal Casualty and Theft Gains and LossesIndividual’s losses on transactions entered into for personal use are deductible only if the losses qualify as casualty or theft losses.

Gains and losses on business propertySec 1231 generally treated as LTCG, instead must be treated as ordinary income to the extent of the taxpayers’ nonrecaptured net Sec.1231 losses for preceding 5 years.

Inventory and property held for sale to customers , accts and notes receivable arising in ordinary course of trade is excluded from Sec. 1231 property.

Sale of building is Sec. 1250 property.Sec. 1250 recaptures gain as ordinary income to the extent of “excess” depreciation

Depreciable property converted to business use – find depreciable basisBasis for depreciation is lesser of FMV at date of conversion or adjusted basis at conversion. Example:Ann received gift of typewriter with FMV $350, original cost $500. Typerwriter then used in Ann’s business and allowable depreciation was $35. On 12/31, typewrite sold for $315. What is loss that can be deducted? $350 – 35 = 315 new basisSold for 315 – basis of 315 = zero

PARTNERSHIPS

-No gain if services or property contributed for interest in partnership-Service at FMV and ordinary income-holding period of partnership interest acquired in exchange for a contributed capital asset begins on date partner’s holding period of the capital asset began.

If FMV of acquired interest is greater than FMV of contributed asset, must add that gain to basis to determine new basis:Example: contributed asset with basis of 25K, FMV of 40K, FMV of 25% interest is 50K. 50-40 = 10+25 = 35K new basis in partnership interest

Organizational expense when first setup partnership –$5,000 amount must be reduced (but not below zero) by the amount by which organizational expenditures exceed $50,000. Remaining expenditures must be deducted ratably over the 180-month period beginning with the month in which the corporation begins business.

22

Partnership income and loss

Loss deductible: +Basis +capital gains - distributions = new basis (this is extent of how much loss can be deducted)

Deductible in computation of ordinary income:- guaranteed payments

Limitations to determine partner’s share of loss:- At-risk- Passive loss

Add charitable contributions to book income to determine ordinary income on partnershipExample: book income 100K, guaranteed payments 60K, charitable contributions 1KOrdinary income = 100K + 1K = 101K

Halle’s share is $50K as of 12/31/08. 25K distributed 12/15, remaining dist in January. My partnership income is $50K. does not matter when paid out.

Services provided by family members are compensated first before allocating according to capital interests. Trung and Ha each own 50% interest. Trung’s services are worth 40K, ordinary income is 100K, therefore 100-40 = 60 x 50% = 30 allocated to each.

Example: Ha contributed cash 45K, Frank contributed land with 30K basis subject to 12K mortgage. 12K x 50% = 6; Ha’s basis 45+6 = 51; Frank basis 30-6=24.

Guaranteed payment increases partner’s ordinary income.

PARTNER’S BASIS IN PARTNERSHIP

Basis of property received as inheritance is generally FMV at date of death.

Liabilities increase basisLoss decrease basis

Loss disallowed if transaction btw partnership and person owning more than 50% interest. Even if only own 50%, not more than, but if constructively or directly owns 50% then loss disallowed.

Or

Halle owns 55% interest in P. Sold her lamp, cost 1,000 5 yrs ago, held for personal use. Sold to P for $5,000 as P’s investment. Halle has $4,000 LTCG since lamp was for personal use.

Loss on land: add back to net income. Example: sold land at loss of 6000, P’s net income 94,000, P’s ordinary income is 94+6 = 100

Section 444 election – deferral period not longer than 3 months

Deceased partner, tax year closes at date of death. Prorate by month. The remaining months distributive share

Partnership terminates when sale or exchange of 50% or more to total partnership capital and profits within 12-month period. Effects of termination:

- deemed distribution of assets to remaining partners and purchaser- hypothetical recontribution of assets to a new partnership.

Sale of partnership typically capital gain/loss. But if have unrealized accounts receivable, then distributive share is considered ordinary.

Use tax basis at date of gift to determine capital gain/loss.

23

Basis to partner of property distributed in “in kind” in complete liquidation of the partner’s interest is the adjusted basis of the partner’s interest reduced by any cash distributed to the partner in the same transaction.

Purchased goodwill or intangibles – straight line amort over 15 yrs.- question will ask amount deductible for purchase of dealer’s franchise (or any intangible for business use).

Divide amount paid by 15 years or 180 months. Prorate for month put in use.

ESTATEDistribution deduction is lesser of required distribution or DNIRequired distribution includes:-interest income-dividend income-tax-exempt income

Distributable Net Income (DNI) includes:-Interest income-Dividend income -NO Capital gains or Tax-exempt income

CORPORATIONS

partial liquidation a stock redemption should be treated as gain/loss by a noncorporate shareholder if the redemption qualifies as a partial liquidation of the distributing corporation. A corporate stock redemption is treated as an exchange, generally resulting in capital gain or loss treatment to a shareholder if the redemption meets any 1 of 5 tests. Redemptions qualifying for exchange treatment include (1) a redemption that is not essentially equivalent to a dividend, (2) a redemption that is substantially disproportionate, (3) a redemption that completely terminates a shareholder's interest, (4) a redemption of a noncorporate shareholder in a partial liquidation, and (5) a redemption to pay death taxes. If none of the above 5 tests are met, the redemption proceeds are generally treated as a dividend.

Liquidating distribution of propertyNo gain or loss recognized by a parent corporation on the receipt of property in complete liquidation of an 80% or more owned subsidiary

Nonliquidating distribution of propertyIf a corporation makes a nonliquidating distribution of appreciated property to a shareholder, the corporation must recognize gain just as if the property were sold at its fair market value. A liability assumed by shareholder increases the recognized gain only when the amount of liability exceeds fair market value.Example:C-Corp distributed asset to shareholderFMV: 30,000Liability assumed by s/h: 40,000Adjusted basis: 25,000What gain does C-Corp recognize?

Generally: FMV – adjusted basis = gainIf, Liability assumed by s/h greater than FMV, then use liability to measure gain. (40 liability – 25 basis = 15 gain)

No loss can be recognized on nonliquidating corporate distributions to shareholders.

Constructive dividends to shareholderWhen corporation sells property to a shareholder for less than FMV, the shareholder is considered to have received a constructive dividend to the extent of the difference between the fair market value of the property and the price paid. Example:Sold property for 50KFMV: 80KBasis: 40KThus, the shareholder's dividend income is $30,000 ($80,000 FMV – $50,000 purchase price).

ReorganizationsNo gain or loss recognized except to extent of cash received.Basis to shareholder is basis of old stock transferred

Types of Reorganization:

24

- Recapitalization- Mere change in identity- Statutory merger

Issuance by C-Corp of its preferred stock in exchange for its bonds is a nontaxable "Type E" reorganization (i.e., a recapitalization). No recognized gain unless boot received.

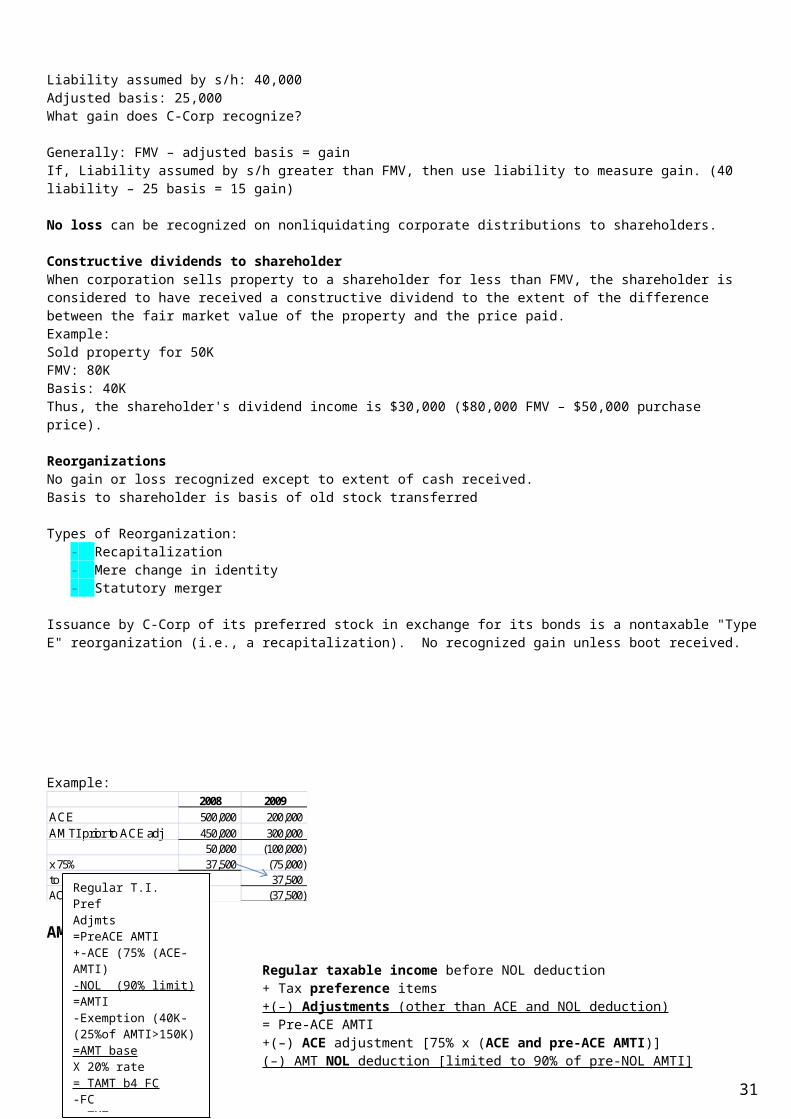

Example:2008 2009

ACE 500,000 200,000

AMTI prior to ACE adj 450,000 300,000 50,000 (100,000)

x 75% 37,500 (75,000) to extent of prior yrs' positive 37,500 ACE for 2009 (37,500)

AMT formula

Regular taxable income before NOL deduction+ Tax preference items+(–) Adjustments (other than ACE and NOL deduction) = Pre-ACE AMTI+(–) ACE adjustment [75% x (ACE and pre-ACE AMTI)](–) AMT NOL deduction [limited to 90% of pre-NOL AMTI] = AMTI(–) Exemption ($40,000 less 25% of AMTI over $150,000) AMT base× 20% rate Tentative AMT before foreign tax credit(–) AMT foreign tax credit TMT(–) Regular income tax (less regular tax foreign tax credit)Alternative minimum tax (if positive)

Small corporation AMT exemption. 1st year: Exempt2nd year: Exempt if Gross Receipts < $5mil3rd year: Exempt if Average gross receipts for the first two years do not exceed $7.5 million. 4th year and subsequent years: All prior three-year periods must not exceed $7.5 million.

Corporate tax rates:Additional 5% over $100,000, up to $11,750Additional 3% over $15 million up to $100,000

S-CORPS

An S corporation loss is passed through to shareholders and is deductible to the extent of a shareholder's basis for stock plus the basis for any debt owed the shareholder by the corporation.Example:Shareholder invested 5,000Loan to S corp 15,000S Corp operating loss (45,000)Loss shareholder can claim on income tax return is: 15,000 + 5,000 = 20,000 basis

Treatment of S-Corp distributions:1. Reduce AAA and stock basis– nontaxable to extent of AAA2. Reduce E&P – treated as ordinary dividends

25

Regular T.I.PrefAdjmts=PreACE AMTI+-ACE (75% (ACE-AMTI)-NOL (90% limit)=AMTI-Exemption (40K-(25%of AMTI>150K) =AMT baseX 20% rate= TAMT b4 FC-FC= TMT-RIT=AMT (if positive)

3. Distributions in excess of stock basis treated as capital gain

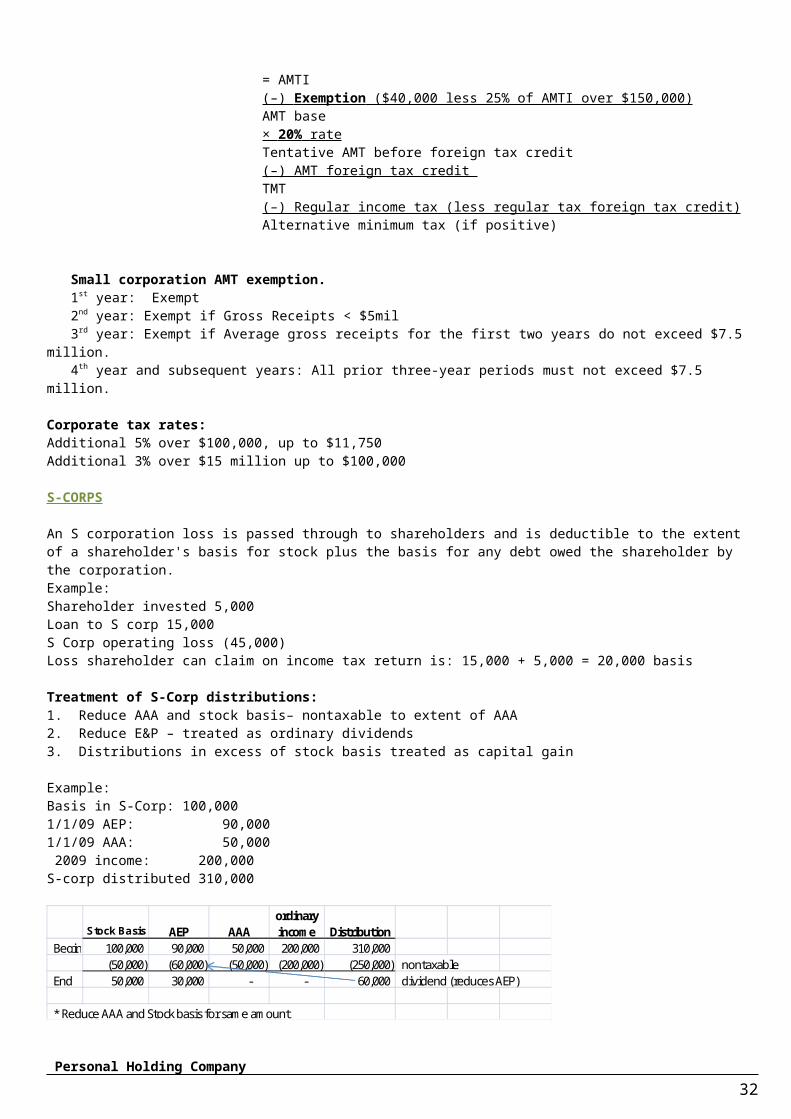

Example: Basis in S-Corp: 100,0001/1/09 AEP: 90,0001/1/09 AAA: 50,000 2009 income: 200,000S-corp distributed 310,000

Stock Basis AEP AAAordinary income Distribution

Begin 100,000 90,000 50,000 200,000 310,000 (50,000) (60,000) (50,000) (200,000) (250,000) nontaxable

End 50,000 30,000 - - 60,000 dividend (reduces AEP)

* Reduce AAA and Stock basis for same amount

Personal Holding Company-more than 50% of the outstanding stock must be owned directly or indirectly by five or fewer individuals.- at least 60% of corp’s adjusted ordinary G.I. for taxable year is PHC income.

CORPORATE - DEDUCTIONS

Compensation deduction = compensation less golden parachute.

Charity deduction: limit to 10% of taxable income before DRD, NOL carryback, Cap Loss carryback; excess carryforward for 5 yearsDo not include charity contribution in taxable income when trying to compute charitable contribution deduction. Think of the problem where answer is 68,000 instead.

If taxpayer receives unsolicited samples from supplier (pharmacy getting samples) that typically inventoried in ordinary course of business, FMV of samples is gross income. FMV then allowed a charitable contribution deduction.

Dividend Received Deduction70% DRD for less than 20% owned

1) if net income is more than dividend income, then use dividend income 2) or 70%* (dividend – NOL)3) if corporation has NOL, then can use FULL DRD. Limit of T.I does not apply

1. sample: income before dividends 900; deduction 1100 (excluding DRD). Dividends of 100. what is NOL? 900+100-1100 –(100 *70%) = (170) NOL

The DRD (normally 80% of dividends from unaffiliated corporations 20%-owned) may be limited to 80% of TI before the DRD, except when the full 80% DRD creates or increases a net operating loss.

Gross business income $ 160,000Dividend income 100,000 $ 260,000Less business deductions (170,000)Taxable income before DRD $ 90,000DRD ($90,000 × 80%) (72,000)Taxable income $ 18,000

Since the full deduction (80% × $100,000 = $80,000) would not create a NOL, the limitation applies.

for a domestic corporation to deduct a percentage of dividends it receives from a foreign corporation:1) domestic corporation owns at least 10% of the foreign corporation2) corporation is not a foreign PHC3) foreign corporation has income connected to trade or business in US4) subject to federal income tax

corporate DRD is affected by requirement that investor corporation must own investee’s stock for 45 days to qualify for DRD. (90 days for divs more than a year in arrears on pref. stock)

a regulated investment company can take DRD deduction.

26

repurchased own outstanding bonds in open market for $258 on May 31, 2004 originally issued on May 5, 2004 at face value for 250. Difference of $8 is a deduction.

Contributions of computer technology & equipment to elementary or secondary school, deduction is FMV of contribution – [(FMV – basis) x 50%] deduction can not exceed 2x equipment’s basis.

If corporation distributes stock in lieu of salaries, FMV of stock deductible as salary expense to corporation, but must recognize gain of (FMV – basis). Employee report FMV in income.

Organizational expenses deducted up to $5,000 but reduce dollar-for-dollar if expenditures exceed $50,0000 and amortized balance over 180 months.

Research and experimental expenditures has a choice capitalize, amortize, or expense.

Contribution of inventory to public charity cost 8500, FMV 10,000, taxable income before deduction 95,000. compute contribution deduction: 10,000 – [(10,000 – 8500) * 50%)]Limited to 10% of taxable income (95,000 * 10%)

Deduct insurance premiums for group term life insurance. Do not deduct for premiums paid for life insurance for which corporation is beneficiary.

Bond premium amortization should be 1) Computed under the constant-yield-to maturity method2) Treated as an offset to the interest income on the bond

Miscellaneous deductions:2. gifts to customers up to $25 per person3. travel expenses to influence legislation up to $2,000

political contributions NOT deductible

non-financial institutions, deduction for bad debts must use direct charge-off method rather than reserve method.

Casualty losses in business (i.e. machine) fully deductible in amount of adjusted basis immediately before loss. (remember $100 per loss and 10% of AGI floors apply to personal tax)

Compute charitable contribution deduction with 10% limit BEFORE 2. charitable contributions3. DRD (include the received dividends, not the deduction)4. NOL carryback5. Capital loss carryback

Interest on borrowings used to repurchase stock is fully deductibleOther expenses such as legal and accounting fees in connection with repurchase are capitalized.

Education expenses – corporation can claim deduction for (even if not required for job)- tuition- textbooks- travel- laboratory fees

TRICK! – in calculating Book to Tax: do not do anything for - provision for state income tax expense (only add federal income tax expense)- interest earned on US Treasury bonds (only state and muni bonds)- interest expense on bank loan to purchase US Treasury bonds (only muni & state)

Contribution deduction carryover – use current year deduction first, then prior year carryover. FIFO

Do not recognize gain or loss on sale or exchange of own stock.

BOOK TO TAX

Book income

27

+ Federal Tax+Excess contributions (cap loss over cap gains)+Excess depreciation over book depreciation+life insurance premiums on corporate officers+50% of meals & entertainment+Political contributions+interest expense on muni bonds+bad debt expense on allowance/reserve method/ (only write-off method deductible)+ amortization of goodwill (self created)

- Tax exempt interest income- Life insurance proceeds- Prepaid rent or interest previously received and recorded for tax purposes but not earned until current year-Goodwill amortization base on 15 years-Income on books not subject to tax-Deduction on return not charged against book (depreciation)Taxable income

FEDECL50PiBD

Partial liquidations: Noncorporate shareholder treats gain on redemption of stock that qualifies as partial liquidation entirely as a capital gain.

INSURANCE

Earliest time a purchaser of existing goods will acquire an insurable interest in those goods is when title passes to the purchaser.

Amt of loss x amt of insurance Coinsurance x FMV at time of loss

CAPITAL COST RECOVERY

Nonresidential (office building), 39 year recovery period, SL depreciation.

Tangible & depreciable property (office machine) can be expensed up to $250,000. Reduce dollar for dollar if over $800,000.

Section 1231 = g/l from trade or business1st: net all casualty & theft g/l on property held over a year

If net loss: treat all as ordinary g/l & do not net with other Sec. 1231 g/l.If net gain: net with other with other Sec. 1231 g/l.

2nd: net all other SEC.1231 g/l (except casualty & theft above)Include casualty & theft net gain (from above)Include g/l from condemnations (other than nonbusiness, non-income producing property)Include g/l from sale or exchange of property used in trade.

If net loss, treat all g/l as ordinary.If net gain, treat all SEC.1231 net gain as LTCG.Net Sec. 1231 gain treated as ordinary (instead of LTCG) to extent of nonrecaptured net Sec. 1231 losses for 5 most recent tax years. Any remaining treated as LTCG.

Sec.1245 property, depreciable tangible & intangible personal property (i.e. desks, machines, equipment, cars, trucks, special purpose storage facilities, covenants not to compete, patents, livestock, athletic contracts, leaseholds of 1245 property)

- Sold 1245 property, treat gain as ordinary income if gain is less than depreciation taken.

LOSSES of a CORPORATION

Net Short term Gain with Long-term gain. Losses deductible to extent of gains.

28

Capital losses carried back 3 years, forward 5 years as Short-term

If capital losses are carried from 2 or more years to the same year, loss should be deducted from earliest year first. . When loss is fully deducted, loss from next earliest year is deducted.

Passive activity losses & credits applies to:IndividualsEstatesTrustsClosely held corporation – last half of year, 50% or more of value of stock held by 5 or fewerPersonal service corporations

C corporation gross receipts $150, $35 other income, deductible expenses $95, net LTCL $25. what is taxable income? 150+35-95=90. capital loss only deductible to extent of capital gains.

Charitable contributions deduction not allowed if have net operating loss. If it’s included in expenses then subtract it from operating expenses.

Depreciation may not create or increase a NOL. Subtract depreciation from total expense to get new income. The difference is allowable and allocated among the different depreciations (i.e. car, machine)

Net Cap Loss = Cap Loss (ST. + LT) – Cap Gain (ST. + LT)

DRD is computed without regard to 80% (or 70%) of taxable income limitation. Net loss per books (60,000)Allowable DRD (20,000 x 80%) (16,000)NOL carryover (76,000)

This is opposite from charity contributions which can not cause loss.

Form 1120X, amended corporate income tax return, filed within 3 years of time return was filed or 2 years from time tax was paid which ever expires later. If filed before due date 3/15, then use due date to determine 3 years.

Fire loss deductible (leave alone if it’s already included in ‘loss from operations’) in calculating NOL.

Deduct capital losses only to extent of capital gains!!!!

BASIS

Decreases basis- casualty or theft loss deductions and insurance premiums- exclusion from income of subsidies for energy conservation measures- section 179

basis of new stock (stock dividend) determined by allocating the old stock1000 shares owned with basis 22,000, FMV 33,000. corporation paid nontaxable 10% common stock dividend. What is basis of common stock after stock dividen? 22,000 / 1100 = 20 per share.

Basis for bequeathed or gifted is at FMV at date of death (6mons for altern date).

Gifts of items for own use (diamond necklace) cost 10,000 ten yrs ago. FMV 12,000. sell for 13,000. gain is 3 (can not do G – L formula)

Taxes for local benefit that tend to increase value of real property, sidewalks, added to property’s adjusted basis and not deductible as expense.

CAPITAL GAINS AND LOSSES

Goodwill is capital asset if internally generated

NOT capital assets- depreciable property- A/R for inventory sold- Real property used in trade or business

If stock acquired from decedent is sold or otherwise disposed of by the recipient within 12 months, then it is long-term.

29

Non-business bad debt is short-term capital loss

Wash sale – sold at a loss and within 30 days before or after the sale, substantially identical stock or securities (or options to acquire them) in the same corporation are purchased.

EXAMPLE: C purchased 100 shares of XYZ Corporation stock for $1,000. C later sold the stock for $700, and within 30 days acquired 100 shares of XYZ Corporation stock for $800. The loss of $300 on the sale of stock is not recognized. However, the unrecognized loss of $300 is added to the $800 cost of the new stock to arrive at the basis of the new stock of $1,100. The holding period of the new stock includes the period of time the old stock was held.

“Capital gain net income” when capital gains and losses all net to a gain“net capital gain” excess of net LTCG over net STCL, not include STCG, apply 28,25,15 rule“net long-term capital gain” means excess of long-term capital gains for the taxable year over long-term capital losses.

15%-28%-35% baskets15% LT capital gain or loss held over 12 months28% Sec1202 certain small business stock – if loss then reclass to 15% basket during b35% STcapital gain loss

Return of capital is tax-free distribution that reduces stock’s basis. And excess over basis treated as capital gain.

Individuals can deduct upto $3,000 of capital loss against ordinary income. Excess carried over indefinitely.

Corporate NOL 2/20Corporate capital loss 3/5Individual capital loss –deduct upto $3K and forward indefinitely but not to decedent estate

Sec.1244 stock – small businessIf owner of Sec1244 stock invest additional capital but is not issued additional shares of stock, amount of additional investment is added to the basis of the original issued stock. Subsequent increase to basis of originally issued stock does not qualify for ordinary loss treatment. And resulting loss be apportioned between qualifying 1244 stock and nonqualifying additional capital interest. Example: acquired original stock of 1244 small business for 10,000.

Contributed additional $9,000 before selling. (no shares issued)Sold stock for 10,000. (19,000 basis – 10,000 sell price = 9000)Apportion loss of 9,000 as 9,000/19,000 x 9000 = 4,263 is capital loss, remaining is ordinary loss.

Loss from sale of Sec.1244 stock: deduct up to $50,000 (100,000 joint) as ordinary loss; excess treat as capital loss.

$3,000 capital loss deduction is $1,500 for married filing separately.

Gains from sale of collectible items taxed at 28%

Sec1250 gain is 25% bracket. (no losses in this bracket)Unrecaptured SEC.1250 gain is LTCG.

Short-term capital loss first offset net gain for highest LT rate basket, then to offset next highest rate basket.

FEDERAL SECURITIES ACTS AND ANTITRUST LAWS

Exempt securities- Commercial papers = note, draft, check with maturity less than 9 months- Intrastate issues- Regulation A – upto $5 million in 12-mo period exempt if

o Filed w SECo Offering circular onlyo Nonissuers sell up to 1,500,000

- government securities- existing shareholders- nonprofits

30

- insurance and annuity contracts

Regulation D Rule 504

- $1 million- general offering restricted to “accredited investors”- no restrictions for resell- no audited financials

Rule 505- $5 million within 12 months- No general offering or solicitation within 12 months- 35 unaccredited, unlimited accredited- Restrict for resell to 2 years- Audited financials if nonaccredited purchases, no need if all accredited

Rule 506- unlimited amount of securities- up to 35 unaccredited must be ‘sophisticated’ investors

SEC Act of 1934Register with if assets > than 10M and 500 or more shareholdersRequired disclosures – Name of officers

Nature of businessFinancial structure of firmAny bonus or profit-sharing provision

Joint tenancy with right of survivorship: interest of person that dies passes to survivor.

Parole evidence rule: Proof of the existence of a prior oral agreement that contradicts the written contract is inadmissible. - Does not exclude evidence that tends to prove contract is void or voidable or understanding reached after the

integrated writing was executed.

COMMERCIAL PAPER

To be negotiable, an instrument must:- Be written- Signed by maker or drawer- Unconditional promise or older to pay- State a fixed amount in money- Be payable on demand or at definite time- Be payable to order or bearer

Special, Restrictive, Qualified endorsement“Pay to X if she completes work today, without recourse”Special restrictive qualified

Holder in Due Course – entitled to payment on negotiable instrument despite personal defenses.