refining perspective – crude availability, investments in ... obrien argus... · residuum...

TRANSCRIPT

0 Baker & O’Brien, Inc. All rights reserved.

35th Argus Fuel Oil and Feedstock Summit Miami, Florida

October 26, 2015

Mark A. Heersema

Refining Perspective – Crude Availability, Investments in Residuum Processing and Impact on Residual Fuel Oil

1

Baker & O’Brien: Independent Energy Consultants

Capital Project Services

Operations Support

Commercial Analyses

Mergers and Acquisitions

Dispute Resolution

Overview – Independently owned and managed – Technical and commercial expertise – Active over full life cycle of assets: new

project development -> business support -> commercial disputes

Consulting Staff – Chemical, Mechanical, and

Electrical engineers – Consultants average over 25 years

industry experience – Experienced problem solvers Materials presented are for informational purposes only. Opinions expressed are

solely those of the individual author.

2

Refining Industry Outlook – Key Drivers

• Global Oil Demand • Regional Economic Activity Changes • Refined Product Demand Factors

Macro Economic

Regulations

Industry Fundamentals

• Crude Oil Flows • Refinery Competitiveness – rationalization vs. expansion • Key Drivers in Heavy Crude Train Investment • Refined Product Forecasting

• Stationary source emissions – including CO2 • Fuel specifications • MARPOL Annex VI – SOx, ECA

3

• Current Crude Oil Quality and Vacuum Residuum Production

• Crude Oil Volume and Quality Trends

• Changes to “Bottom of the Barrel” Processing Capability

• Scenario for Residual Fuel Availability to 2020

View on Residual Fuel Production to 2020

4

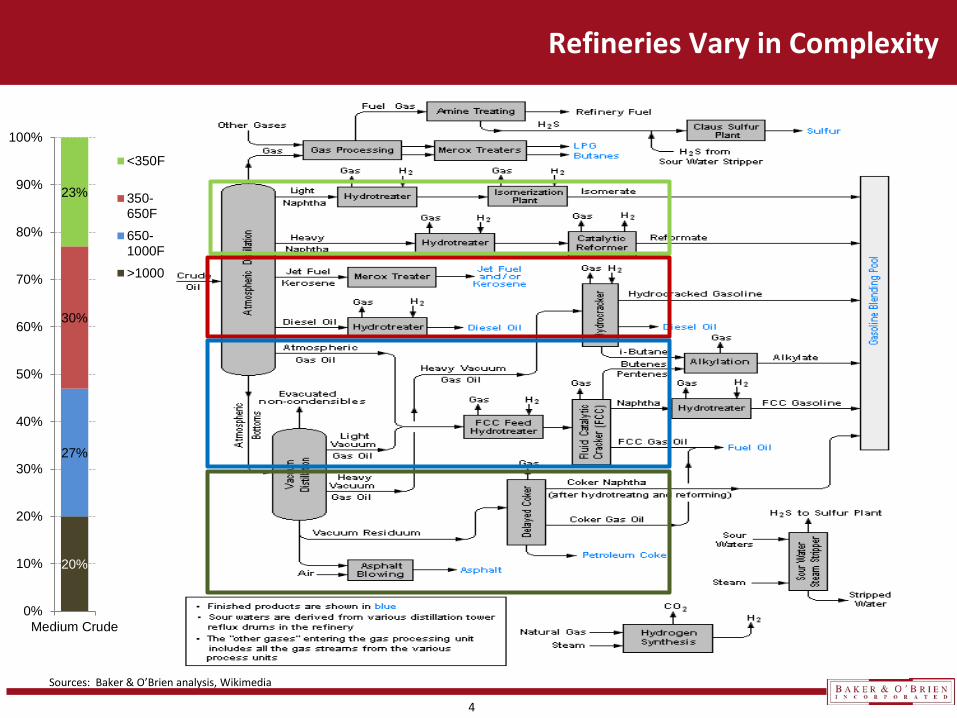

Refineries Vary in Complexity

20%

27%

30%

23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Medium Crude

<350F

350-650F

650-1000F

>1000F

Sources: Baker & O’Brien analysis, Wikimedia

5

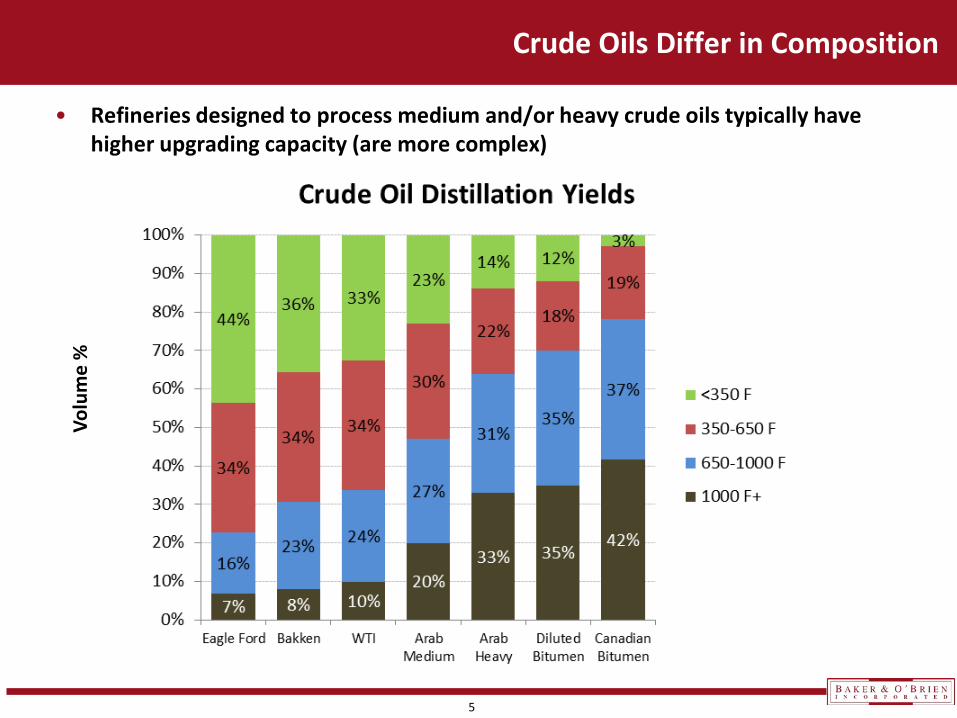

Crude Oils Differ in Composition

• Refineries designed to process medium and/or heavy crude oils typically have higher upgrading capacity (are more complex)

Volu

me

%

6

(2,000) (1,000) - 1,000 2,000 3,000 4,000

United StatesIraq

CanadaRussia

All other gainers (10)Kazakhstan

ChinaBrazil

Saudi ArabiaUnited Arab Emirates

ColombiaAzerbaijan

AngolaKuwaitYemen

SyriaMexico

United KingdomIran

NorwayLibya

All other decliners (17)

Shift in Crude Oil Production Over Last 10 Years, 000 B/D

Major Shifts in Crude Oil Production: Last 10 Years

• Net production increase: 4.2 MMB/D • Volumes lost to civil wars, sanctions

and natural field declines (North Sea and Mexico factor large) were replaced primarily with U.S. shale, Iraq, Canada and Russia

Sources: Baker & O’Brien analysis, EIA, Oil & Gas Journal, BP Statistics, Canadian Association of Petroleum Producers

7

Crude Oil Production Will Find A Market

Crude By Rail

Source: EIA

Source: EIA

0200400600800

1000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

U.S

. Cru

de R

ail

Mov

emen

ts M

B/D

0%

2%

4%

6%

8%

10%

2010 2011 2012 2013 2014

Cru

de D

eliv

ered

By

Rai

l, %

of

Cru

de In

put

Year

8

0.0

0.5

1.0

1.5

2.0

2.5

North America South & CentralAmerica

Europe & Eurasia Middle East Africa Asia Pacific World

Prod

uced

Sul

fur,

wt%

Crude Sulfur Evolution

2005 2010 2014

Significant “Sweetening” of Crude Slate in North America; Relatively Static Global Sulfur Levels

• Western hemisphere trending to lower sulfur levels

• Europe and Mideast trending higher • Relatively flat on global basis

Sources: Baker & O’Brien analysis, EIA, Oil & Gas Journal, BP Statistics, Canadian Association of Petroleum Producers

9

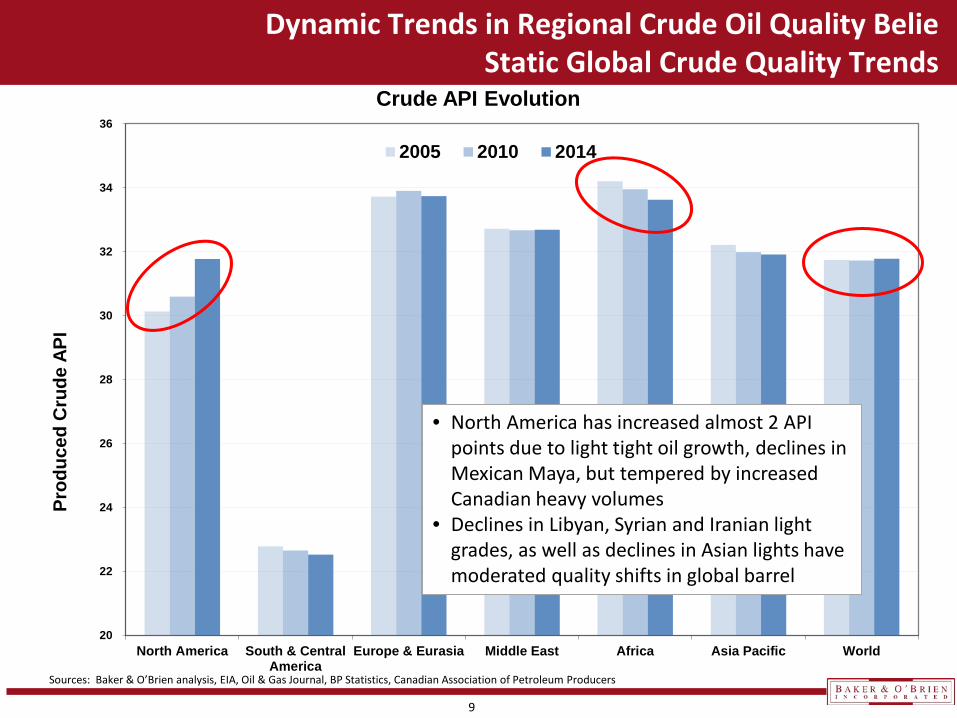

20

22

24

26

28

30

32

34

36

North America South & CentralAmerica

Europe & Eurasia Middle East Africa Asia Pacific World

Prod

uced

Cru

de A

PI

Crude API Evolution

2005 2010 2014

Dynamic Trends in Regional Crude Oil Quality Belie Static Global Crude Quality Trends

• North America has increased almost 2 API points due to light tight oil growth, declines in Mexican Maya, but tempered by increased Canadian heavy volumes

• Declines in Libyan, Syrian and Iranian light grades, as well as declines in Asian lights have moderated quality shifts in global barrel

Sources: Baker & O’Brien analysis, EIA, Oil & Gas Journal, BP Statistics, Canadian Association of Petroleum Producers

10

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MB

/D

Crude Oil Production by Quality Classification

Light SweetLight SourHeavy SweetHeavy Sour

Shifting Suppliers and Impact on Crude Oil Quality Trends: Grade Shifts Are Subtle, Not Easily Discernible

Sources: Baker & O’Brien analysis, EIA, Oil & Gas Journal, BP Statistics, Canadian Association of Petroleum Producers

11

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

North America South & CentralAmerica

Europe & Eurasia Middle East Africa Asia Pacific World

Vac

Res

id Y

ield

from

Cru

de O

Il, 0

00 B

/D

Vacuum Residuum from Crude Oil (1050F+)

2005 2010 2014

Vacuum Residuum Production Has Been Increasing In Line With Total Production

• Western hemisphere trending slightly higher (higher total production, Canadian heavy, Colombia, Brazil), despite declining Mexican Maya

• Increases globally: • 120 MB/D 2005 to 2010 • 450 MB/D 2010 to 2014

Sources: Baker & O’Brien analysis, EIA, Oil & Gas Journal, BP Statistics, Canadian Association of Petroleum Producers

12

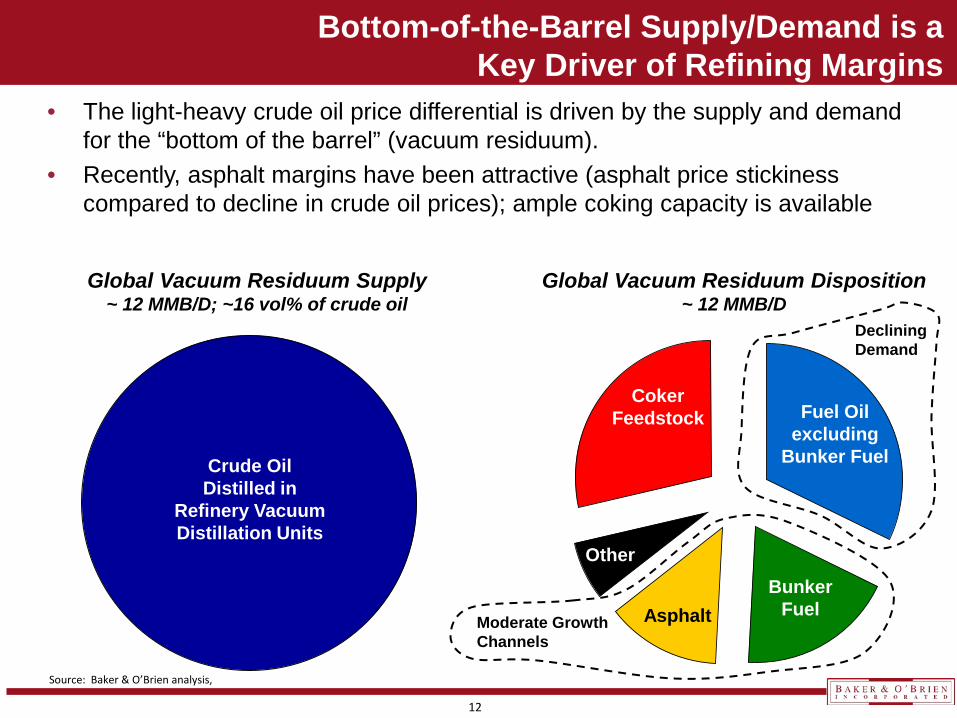

Bottom-of-the-Barrel Supply/Demand is a Key Driver of Refining Margins

• The light-heavy crude oil price differential is driven by the supply and demand for the “bottom of the barrel” (vacuum residuum).

• Recently, asphalt margins have been attractive (asphalt price stickiness compared to decline in crude oil prices); ample coking capacity is available

Fuel Oil excluding

Bunker Fuel

Bunker Fuel Asphalt

Coker Feedstock

Other

Global Vacuum Residuum Supply ~ 12 MMB/D; ~16 vol% of crude oil

Global Vacuum Residuum Disposition ~ 12 MMB/D

Crude Oil Distilled in

Refinery Vacuum Distillation Units

Moderate Growth Channels

Declining Demand

Source: Baker & O’Brien analysis,

13

• Key factors that will drive global oil balance and price – Global demand growth (China, U.S.) – OPEC resolution and actions – Shale oil production response – Return of Iranian and Libyan barrels

Crude Oil Availability Over Next Five Years: What’s Going to Happen?

Scenario A – Lower Oil Prices Linger Some combination of the following occur: • OPEC continues to defend market

share and pump oil • Stronger but moderate global demand

growth • Iranian and Libyan barrels return to

market

Scenario B – Oil Price Rebounds Faster Some combination of the following occur: • OPEC reaches consensus to support

price at some level • Chinese economy recovers • U.S. gasoline demand remains healthy • Iranian production slow to rebound • Libya remains in turmoil

Indicative net crude oil production growth required over next 5 years:

3-5 MMB/D (from 2015)

14

• Both cases assume lifting of Iran sanctions and production gains from Libya and Iraq • Under the low price scenario, the call on OPEC is fairly large by 2020, which implies price

strengthening with or without OPEC’s support • Scenario B does not require much additional production from OPEC, considering volume

gains from Iran, Iraq and Syria

Supply Scenarios 2020: Incremental Global Crude Oil Supply of 4 MMB/D

Scenario A – Sustained Low Prices

(2,000) (1,000) - 1,000 2,000 3,000 4,000 5,000 6,000

OPEC

Canada

All other gainers

China

United States

All other decliners

Possible Shift in Crude Oil Production - Scenario A (Low Price), 000 B/D

Scenario B – Price Rebound

(2,000) (1,000) - 1,000 2,000 3,000 4,000 5,000 6,000

OPEC

United States

Canada

All other gainers

China

Brazil

All other decliners

Possible Shift in Crude Oil Production - Scenario B (High Price), 000 B/D

Note: OPEC includes all OPEC member countries and reflects anticipated lifting of Iran sanctions, growth in Iraq, and production rebound from Libya

15

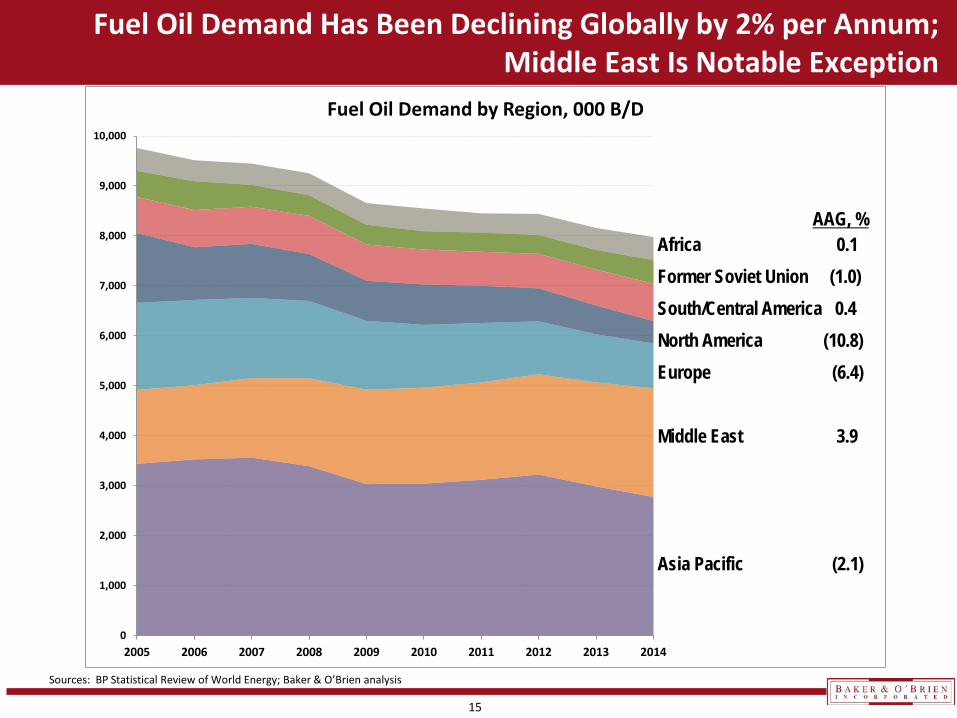

Fuel Oil Demand Has Been Declining Globally by 2% per Annum; Middle East Is Notable Exception

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Fuel Oil Demand by Region, 000 B/D

Africa

Former Soviet Union

S. & Cent. America

North America

Europe

Middle East

Asia Pacific

AAG, % Africa 0.1 Former Soviet Union (1.0) South/Central America 0.4 North America (10.8) Europe (6.4) Middle East 3.9 Asia Pacific (2.1)

Sources: BP Statistical Review of World Energy; Baker & O’Brien analysis

16

Most New Export-Oriented Refineries Aiming for Full Conversion

0%

10%

20%

30%

40%

50%

60%

70%

USGC Average NWE Average New Middle East Refinery

Perc

ent o

f Cru

de C

harg

e

Conversion/Upgrading Units - USGC vs. NW Europe and Middle East

FCC

Hydrocracking

Coking

17

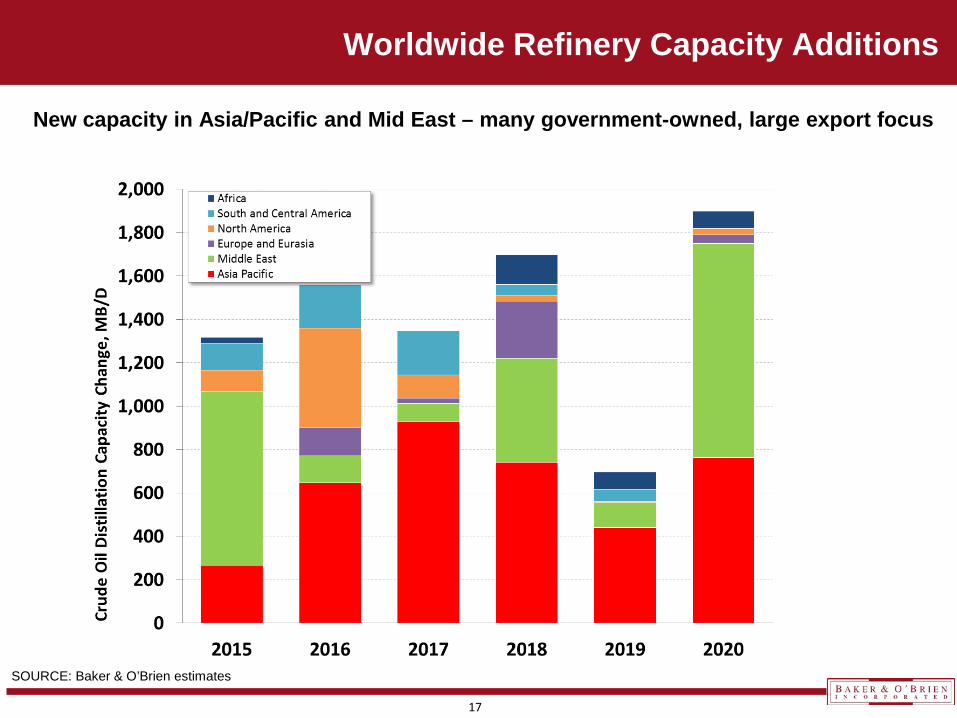

Worldwide Refinery Capacity Additions

New capacity in Asia/Pacific and Mid East – many government-owned, large export focus

SOURCE: Baker & O’Brien estimates

18

• Delayed cokers are very capital intensive, typically $3+ billion • Investment motivations vary based on owner type, location

Coker Investment Decisions

• Vertically-integrated to monetize poor-quality grades with limited markets

• Vertically-integrated and export-oriented to capture maximum value and grow industrial job base

• Long-view strategic / regulatory pressure / shrinking fuel oil markets / economics (capture light/heavy spreads)

Types of Owner • WRB, CNRL, BP, ConocoPhillips;

PDVSA – several coker JVs; PEMEX JVs going back decades

• Saudi Aramco, UAE, PDVSA

• Exxon/Antwerp; TOTAL/Port Arthur; Marathon/Garyville: Motiva/Port Arthur; Reliance/Jamnagar

Examples

19

2015 Will Cap Off a Large Wave of Coker Investments and Set Stage For Second Wave

Aruba & Hovensa Refinery Closures

Announced Capacity Additions

20

Coker Capacity Availability is Expected to Outstrip Residuum Supply Availability

SOURCE: Baker & O’Brien Analysis;

Changes in “Coker” Capacity vs. Incremental Vacuum Residuum Availability (Capacity includes a portion of new RFCC capacity and handicaps announced

coker capacity)

MB/D

21

Scenario for Residual Fuel Oil Product Supply Changes 2015 to 2020

• Incremental North America residuum is consumed by new and existing cokers • Middle East shows slight growth • Europe/Eurasia adding cokers (XOM/Antwerp, Lukoil/Perm) • Asia/Pacific adding significant full-conversion refining capacity

Note: All charts on same absolute scale to highlight regional differences

North America Europe/Eurasia

Central & South America

Africa

Asia/Pacific Middle East

22

• Static Global Crude Quality

• Net Refining Capacity Gain

• Overall Refinery Complexity Increasing

• New, world-scale high-complexity refineries replacing smaller, lower-complexity refineries

• Residue Production Will Increase

• Increase in crude production and refinery inputs will overcome any shift to lighter crude

• Incremental residue processing unit throughput (new units and increased utilization of existing) likely to exceed additional residue production

• RFO Demand Drop May Exceed Incremental Residue Conversion

• Would keep light-heavy spreads narrow

Summary and Conclusions

23

Baker & O’Brien – Independent Energy Consultants

www.bakerobrien.com

Dallas Headquarters

12001 N. Central Expressway Suite 1200

Dallas, TX 75243 Phone: 1-214-368-7626

Fax: 1-214-368-0190

Houston Office

1333 West Loop South Suite 1350

Houston, TX 77027 Phone: 1-832-358-1453

Fax: 1-832-358-1498

London Office

146 Fleet Street Suite 2

London EC4A 2BU Phone: 44-20-7373-0925