reducing variation in credit risk-weighted assets ... · reducing variation in credit risk-weighted...

TRANSCRIPT

A response by the British Bankers Association to the Basel Committee on Banking Supervision’s consultative document on

Reducing variation in credit risk-weighted assets – constraints on the use of internal model approaches

June 2016

The BBA is the leading association for UK banking and financial services representing members on the full range of UK

and international banking issues. It has over 200 banking members active in the UK, which are headquartered in 50

countries and have operations in 180 countries worldwide. Eighty per cent of global systemically important banks are

members of the BBA, so as the representative of the world’s largest international banking, cluster the BBA is the voice of

UK banking.

All the major banking groups in the UK are members of our association as are large international EU banks, US and

Canadian banks operating in the UK as well as a range of other banks from Asia, including China, the Middle East, Africa

and South America. The integrated nature of banking means that our members are engaged in activities ranging widely

across the financial spectrum from deposit taking and other more conventional forms of retail and commercial banking to

products and services as diverse as trade and infrastructure finance, primary and secondary securities trading, insurance,

investment banking and wealth management.

Our members manage more than £7 trillion in UK banking assets, employ nearly half a million individuals nationally,

contribute over £60 billion to the UK economy each year and lend over £150 billion to UK businesses. BBA members

include banks headquartered in the UK, as well as UK subsidiaries and branches of EU and 3rd country banks.

Introduction

The British Bankers’ Association (BBA) is pleased to respond to the Basel Committee’s consultation

paper 362 on constraints on the use of internal models for credit risk1.

Many of our members currently use Internal Ratings Based (IRB) approaches for determining their

regulatory capital requirements for credit risk weighted assets and broadly support the Basel

Committee’s goals of reducing complexity and improving comparability. Therefore, our objectives

mirror those of the Basel Committee.

This response represents the views of all our members and in responding to the consultation paper

we outline some key messages before providing more granular observations on the consultation

paper.

1 https://www.bis.org/bcbs/publ/d362.pdf

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

2

Our key messages

1. Risk sensitivity matters

In our view it is important to recognise that the global financial crisis had its genesis in a Basel I

credit risk weighting environment.

The simple Basel I rules, which were effectively an 8% leverage ratio for a wide range of exposure

classes, were widely acknowledged to have incentivised banks to focus their lending on riskier asset

classes, which required the same amount of regulatory capital as exposures to less risky borrowers.

Less liquid securitisation structures, often nonetheless held in the trading book, were a key tool in his

regulatory arbitrage.

This risk insensitivity was corrected by the introduction of the Basel II framework which also

introduced internal ratings based credit modelling for banks, subject to regulatory approval, provided

that detailed and extensive model and data governance requirements were met.

Basel II was not introduced for most internationally active banks until the end of 2007 and has yet to

be fully implemented in a number of jurisdictions. While the origins of the global financial crisis were

multi-factoral, we do not believe the use of credit risk modelling was a key component.

Our members support the Basel Committee’s objective of reducing the complexity of the regulatory

framework for the modelling of credit risk exposures and improving its comparability with the

standardised approaches to credit risk so that the capital banks hold against their exposures reflects

the risk of loss. But this should not be achieved at the expense of risk sensitivity.

We would like to stress that risk sensitivity matters and our members believe that modelling for more

portfolios than the Committee is currently proposing remains relevant. Supervisors should aim to

measure credit risks using banks’ own assessments as a starting point, in order to assess the

adequacy of the capital they hold to support those portfolios and confirm that it is broadly

commensurate with that allocated by similar banks against similar portfolios using similar

underwriting standards.

If implemented, the effective outcome of this consultation paper’s proposals would be a wide ranging

constraint on the use of credit risk modelling approaches in the assumed belief that more risk

sensitive approaches are poorer indicators of counterparty failure, when compared to simpler

approaches such as a leverage ratio. We do not agree that this is the case. Indeed, the introduction

of multi-layered floors (PD, LGD, DT LGD, EAD as well as overall aggregate output floors) will result

in lower levels of transparency and additional complexity, which is the opposite of what the proposals

are purported to be seeking to achieve.

2. Increasing levels of capital

We understand the Committee’s objective of reducing the complexity of internal modelling and

improving comparability, as well as addressing excessive variability in the capital requirements for

credit risk. This follows other ongoing regulatory work from the Committee on the standardised

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

3

approach for credit risk2, as well as the advanced modelling approach for operational risk3 to which

the BBA has also replied.

The Committee has repeatedly stated that, through these regulatory initiatives, it does not aim to

significantly increase aggregate capital levels across the industry, but aims to deploy it in a more risk

sensitive way to ensure capital is more closely matched to the riskiness of the assets and exposures

it supports. Nevertheless, many of our members consider that the new requirements under this

consultation will result in exactly that, as substantial changes in how capital is calculated under

certain portfolios are likely to result in increased capital requirements, even were a floor to be

established at the lower end of the proposed range.

This may impact the profitability of such portfolios and result in the unintended consequence of some

industry participants choosing to stop lending to them. This deleveraging may occur in some of the

portfolios, such as higher LTV residential mortgages and lending to SMEs and other corporates, that

are vital in promoting economic growth and creating jobs, particularly in countries where those

borrowers do not have the alternative of tapping the capital markets. If implemented, these proposals

may drive some businesses to other areas of financial services, such as insurance and ‘shadow

banking,’ some of which may be outside the current scope of prudential supervision and oversight.

This would not be a good outcome and would appear to be at odds with other regulatory initiatives.

While diversification of funding sources for borrowers is important, driving choice and competition, it

will be necessary to ensure that they are able to continue to access long term funding during a crisis.

We still expect banks to be the ‘lender of last resort’ for borrowers in times of economic stress.

Revisions to the approaches to credit risk capital calculations should ensure that banks are able to

play this role when called upon.

Many of our members, large or small, are fully engaged in completing the Quantitative Impact Study

(QIS). We look forward to a better understanding of the likely impact of the revised proposals on

overall levels of bank capital held against credit risk, and how these might differ between regions, in

order that the Committee’s stated objective of ensuring that the aggregate level of capital held

against credit risk does not increase is met and to highlight the possibility that increases in one

region might be offset by decreases in others.

It will be important that, as the debate continues about the relevance of flooring IRB approaches, the

Committee shares the results of the QIS with industry at an early stage and we would appreciate

confirmation from the Committee that this is its intention.

3. Moving to the standardised approach

The consultation proposes to move some portfolios to the standardised approach namely exposures

to Banks and Equity, and partly for corporate exposures and Specialised Lending.

However, since the standardised approach is also under review and subject to change (following the

recent consultation from the Committee), it is not yet possible to understand the impact of such

proposals. As a result, the new requirements regarding the standardised approach need to be

finalised before any conclusions can be drawn with respect to the above portfolios.

2 http://www.bis.org/bcbs/publ/d347.pdf

3 http://www.bis.org/bcbs/publ/d355.pdf

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

4

We note that the Committee intends to consider further the extent to which banks adopting the IRB

approach should be required to apply it to all material asset classes for which the IRB approach

remains available. We wish to reiterate the importance of allowing flexibility in implementation of the

IRB approach, which is particularly important for new and smaller banks. As the Committee has

already proposed applying a hybrid-type approach where both IRB and standardised approach may

be used depending on the portfolio, we can see no justification for not relaxing the materiality

constraint, subject, of course, to developing appropriate guidelines to address possible “cherry-

picking”.

4. Why do risk weightings vary?

The Basel Committee’s consultation paper asserts that its own analysis, based on hypothetical

portfolio exercises (HPE), has demonstrated that there is significant unwarranted variability in risk

weighted assets calculated under the IRB approaches, which therefore limits the comparability of

capital ratios mitigating the effectiveness of market discipline provided by Pillar 3.

We note that the Basel Committee’s own July 2013 analysis of risk-weighted assets for credit risk in

the banking book4 identified a number of possible reasons for reasons for the observed variability,

including:

underlying differences in the risk composition of banks’ assets

supervisory choices exercised at the national level

banks’ own choices under the IRB framework

It also recognised that RWA variation is consistent with the greater risk sensitivity intended by the

Basel framework.

To these three drivers of variability we would also add:

what is an economic cycle

point in time or through the cycle approaches

different approaches to the identification of default

different approaches to ‘curing ‘ of default

jurisdictional differences affecting ability to realise of collateral

differences in recovery strategies between banks leading to different LGDs

variations of credit risk profile within asset classes e.g. mortgages

A number of these drivers of variability are already being addressed by regulators, a process we

support and are participating in.

5. An alternative approach - harmonising the choices

As we have noted above, there are a number of legitimate reasons why risk weighted assets vary

between banks, the most significant one of which is underlying differences in banks’ portfolios.

4 http://www.bis.org/publ/bcbs256.pdf

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

5

Other factors that influence comparability arise from different supervisory or individual banks’

choices in relation to credit risk modelling implementation.

An alternative approach would be to address the parameter definitional issues that have been shown

to create variability and then repeating the HPE analysis to identify, once these definitional changes

have been made, the extent to which unwarranted variability persists. Our belief is that greater

definitional harmonisation in the way proposed by the EBA in the EU, would eradicate much of this

credit risk capital variability. Once the 2013 analysis had been repeated, the floors could be

calibrated to impact outlying banks and ensure comparability is maintained. Without this re-analysis

the introduction of floors must be called into serious question.

We comment below on the consultation paper’s more specific proposals.

Sovereign Exposures

The proposed treatment for sovereigns is still under review by the Committee. So we will comment

on them once they are finalised.

Exposures to Banks and Financial Institutions

The Committee should clarify the definition of Financial Institutions as we believe this refers to banks

and insurance companies only. Funds should be treated as corporates and not Financial Institutions.

Alternative modelling approaches for financial institutions

There are many different ways in which modelling approaches could be developed rather than

resorting to the standardised approach and we encourage the Committee to consider the merits of a,

for instance, more constrained approach to modelling, which we out line below.

The Basel revised Standardised Approach does not have the necessary risk sensitivity or granularity

to be a suitable replacement of AIRB for banks and financial institutions. A significant number of

exposures to financial institutions are to unrated counterparties which would be subject to a fixed

100%. This means that the capital framework would not discriminate between good and bad credits

for a large number of obligors. The binding nature of capital constraints, and the market pressure to

maximise return on equity/capital, would encourage banks to reduce exposure to good quality credit

counterparties and increase exposures to poorer credit quality counterparties. We believe Basel’s

concerns on excessive RWA variability and comparability can be addressed without significantly

removing risk sensitivity.

A number of alternative options are possible, which would promote progressive risk management.

We believe use of the Foundation IRB approach for financial institutions would promote progressive

risk management. We do not believe PD estimates represent a material driver in variances in risk

weights, which we expect are more likely to arise from variances in LGD, CCF and different

interpretations and applications of the rules. The retention of the PD estimates will deliver risk

sensitivity with the use of supervisory LGDs and CCFs delivering enhanced comparability.

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

6

Alternatively, given the lower contribution of CCF to variability in risk weighting and measurement

potential, the Foundation IRB approach could be modified to allow the CCF to be modelled.

Another viable alternative to the Basel proposal is an approach which we have termed the

“Constrained Internal Ratings Based approach” (CIRB).

Firstly, the Basel IRB risk weight function - which is a function of Probability of Default (PD), Loss

Given Default (LGD) and Maturity (M) – remains an appropriate approach to determine conservative

risk weights. It is based on sound academic credit risk theory and Basel proposes to retain the use of

the IRB risk weight function for other classes of exposure such as corporates and retail.

Secondly, concerns that have been expressed by the regulatory community relate to the inputs into

the IRB approach rather than the internal ratings approach itself. We believe that internal ratings

should remain a core part of the framework. Retaining the use of internal ratings has several

advantages. It will reduce mechanistic reliance on external credit ratings where they are used to

calculate capital in the standardised approach. It will also significantly increase the universe of

“rated” counterparties since many financial institutions are not rated by public credit rating agencies.

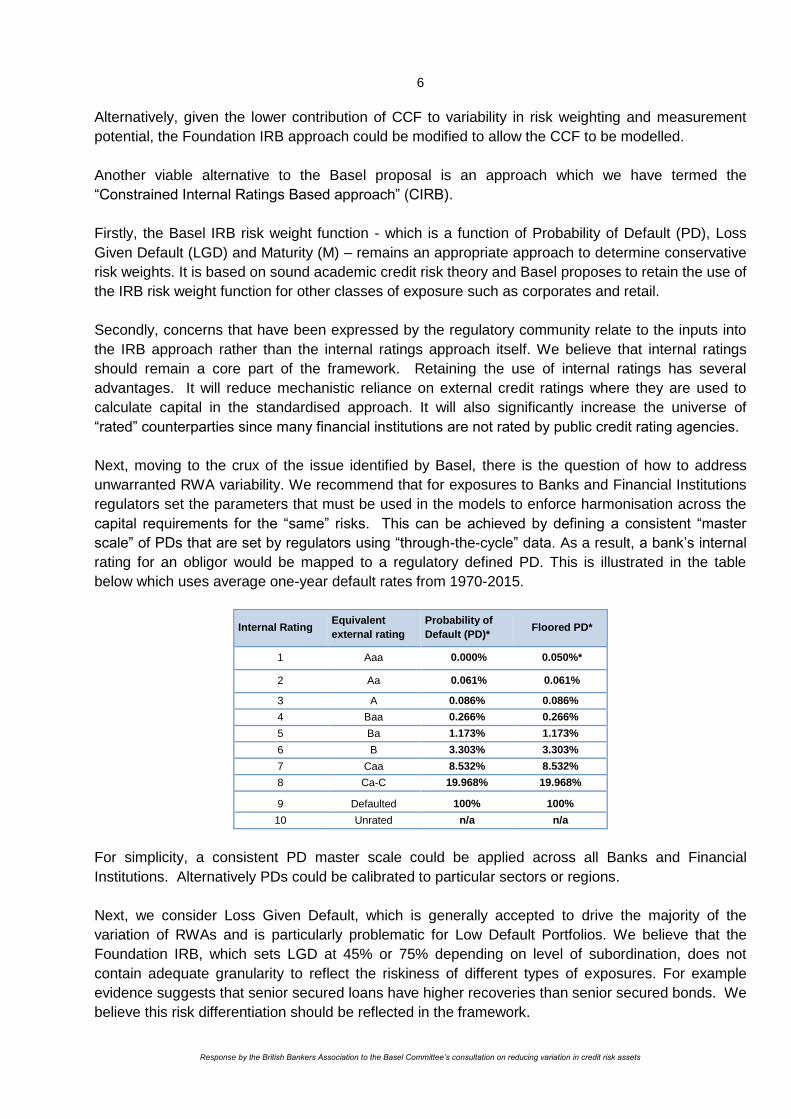

Next, moving to the crux of the issue identified by Basel, there is the question of how to address

unwarranted RWA variability. We recommend that for exposures to Banks and Financial Institutions

regulators set the parameters that must be used in the models to enforce harmonisation across the

capital requirements for the “same” risks. This can be achieved by defining a consistent “master

scale” of PDs that are set by regulators using “through-the-cycle” data. As a result, a bank’s internal

rating for an obligor would be mapped to a regulatory defined PD. This is illustrated in the table

below which uses average one-year default rates from 1970-2015.

Internal Rating Equivalent

external rating

Probability of

Default (PD)* Floored PD*

1 Aaa 0.000% 0.050%*

2 Aa 0.061% 0.061%

3 A 0.086% 0.086%

4 Baa 0.266% 0.266%

5 Ba 1.173% 1.173%

6 B 3.303% 3.303%

7 Caa 8.532% 8.532%

8 Ca-C 19.968% 19.968%

9 Defaulted 100% 100%

10 Unrated n/a n/a

For simplicity, a consistent PD master scale could be applied across all Banks and Financial

Institutions. Alternatively PDs could be calibrated to particular sectors or regions.

Next, we consider Loss Given Default, which is generally accepted to drive the majority of the

variation of RWAs and is particularly problematic for Low Default Portfolios. We believe that the

Foundation IRB, which sets LGD at 45% or 75% depending on level of subordination, does not

contain adequate granularity to reflect the riskiness of different types of exposures. For example

evidence suggests that senior secured loans have higher recoveries than senior secured bonds. We

believe this risk differentiation should be reflected in the framework.

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

7

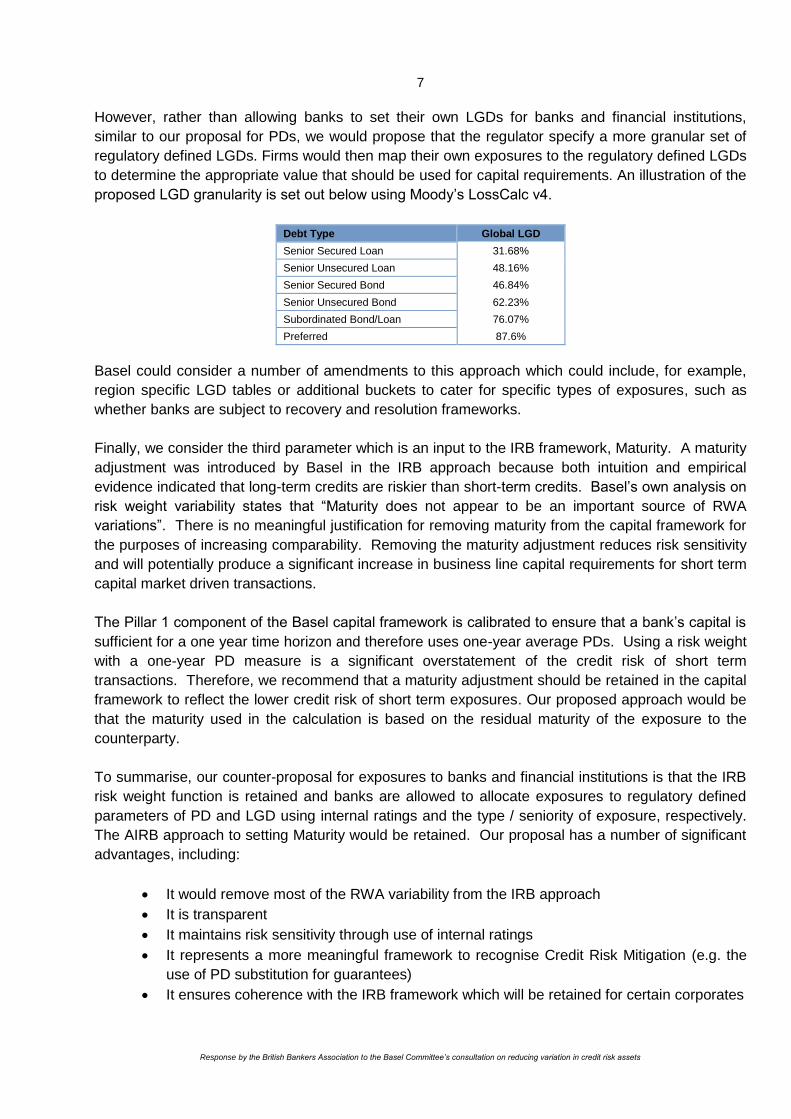

However, rather than allowing banks to set their own LGDs for banks and financial institutions,

similar to our proposal for PDs, we would propose that the regulator specify a more granular set of

regulatory defined LGDs. Firms would then map their own exposures to the regulatory defined LGDs

to determine the appropriate value that should be used for capital requirements. An illustration of the

proposed LGD granularity is set out below using Moody’s LossCalc v4.

Debt Type Global LGD

Senior Secured Loan 31.68%

Senior Unsecured Loan 48.16%

Senior Secured Bond 46.84%

Senior Unsecured Bond 62.23%

Subordinated Bond/Loan 76.07%

Preferred 87.6%

Basel could consider a number of amendments to this approach which could include, for example,

region specific LGD tables or additional buckets to cater for specific types of exposures, such as

whether banks are subject to recovery and resolution frameworks.

Finally, we consider the third parameter which is an input to the IRB framework, Maturity. A maturity

adjustment was introduced by Basel in the IRB approach because both intuition and empirical

evidence indicated that long-term credits are riskier than short-term credits. Basel’s own analysis on

risk weight variability states that “Maturity does not appear to be an important source of RWA

variations”. There is no meaningful justification for removing maturity from the capital framework for

the purposes of increasing comparability. Removing the maturity adjustment reduces risk sensitivity

and will potentially produce a significant increase in business line capital requirements for short term

capital market driven transactions.

The Pillar 1 component of the Basel capital framework is calibrated to ensure that a bank’s capital is

sufficient for a one year time horizon and therefore uses one-year average PDs. Using a risk weight

with a one-year PD measure is a significant overstatement of the credit risk of short term

transactions. Therefore, we recommend that a maturity adjustment should be retained in the capital

framework to reflect the lower credit risk of short term exposures. Our proposed approach would be

that the maturity used in the calculation is based on the residual maturity of the exposure to the

counterparty.

To summarise, our counter-proposal for exposures to banks and financial institutions is that the IRB

risk weight function is retained and banks are allowed to allocate exposures to regulatory defined

parameters of PD and LGD using internal ratings and the type / seniority of exposure, respectively.

The AIRB approach to setting Maturity would be retained. Our proposal has a number of significant

advantages, including:

It would remove most of the RWA variability from the IRB approach

It is transparent

It maintains risk sensitivity through use of internal ratings

It represents a more meaningful framework to recognise Credit Risk Mitigation (e.g. the

use of PD substitution for guarantees)

It ensures coherence with the IRB framework which will be retained for certain corporates

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

8

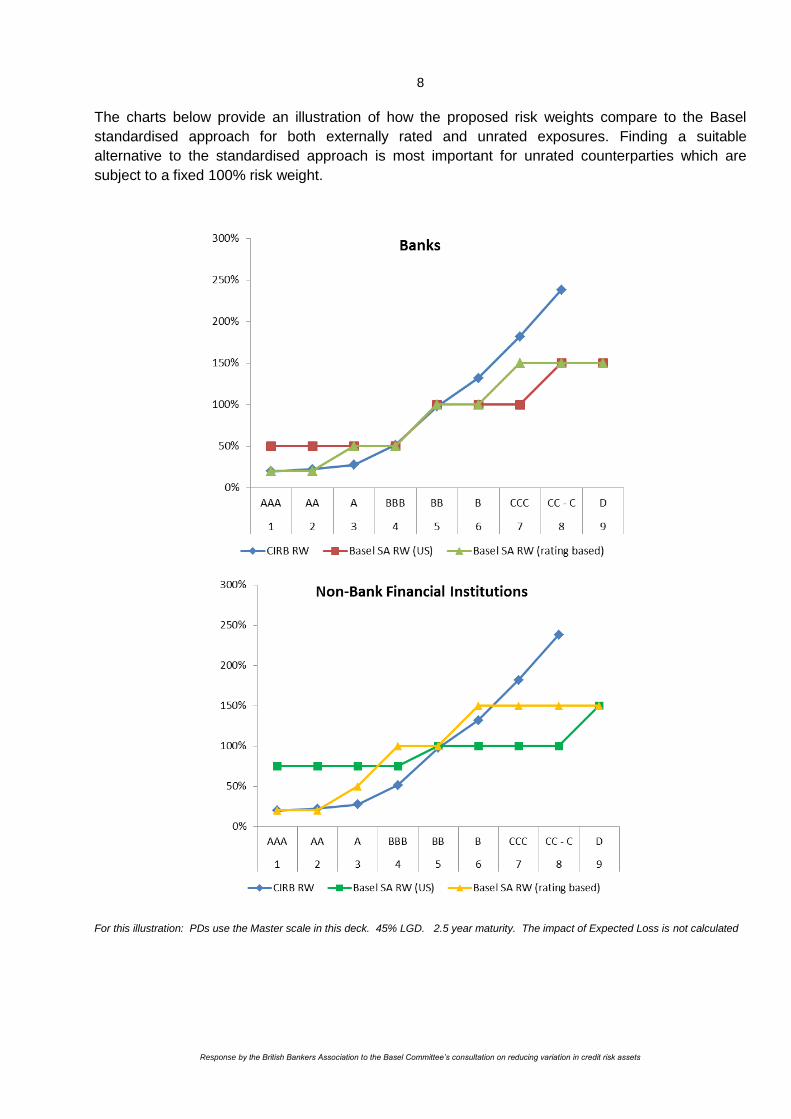

The charts below provide an illustration of how the proposed risk weights compare to the Basel

standardised approach for both externally rated and unrated exposures. Finding a suitable

alternative to the standardised approach is most important for unrated counterparties which are

subject to a fixed 100% risk weight.

For this illustration: PDs use the Master scale in this deck. 45% LGD. 2.5 year maturity. The impact of Expected Loss is not calculated

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

9

Exposures to Corporates

The Committee proposes that exposures to corporates belonging to consolidated groups with total

assets exceeding EUR 50bn would be subject to the standardised approach, whereas exposures to

corporates belonging to consolidated groups with total assets less than or equal to EUR 50bn and

annual revenues greater than EUR 200m would be eligible to apply the Foundation IRB approach.

Lastly, exposures to corporates belonging to consolidated groups with total assets less than or equal

to EUR 50bn and annual revenue less than or equal to EUR 200m would be eligible to apply the A-

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

10

IRB approach. We would welcome some clarity on how these thresholds for exposures determining

the use of the standardised or IRB approach have been defined.

We encourage the Basel Committee to consider particularly carefully the calibration of exposures to

corporates to ensure that different jurisdictions are not materially and differentially impacted. For

instance, in some countries smaller corporate borrowers have much greater access to capital

markets. But in Europe, for instance, capital markets for all but the largest corporate borrowers are

much less well developed and there is no viable alternative to bank borrowing.

A further factor to be taken into account is that there may be insufficient capacity in many local

markets to rapidly risk weight corporates wishing to allow their bankers to take advantage of the

lower risk weights, based on external ratings, as permitted in the revised standardised approach.

We do not welcome the use of the standardised approach for larger corporate exposures which does

not take into account all PD predictors and ratings transition data available from additional external

data. Nor do we believe that PD estimates represent a material driver in variances in risk weights.

We therefore recommend that banks should be able to maintain at least the FIRB approach for the

largest corporate category. The ability for banks to model CCF for risk weight calculation could

additionally be considered.

In this way, assessment of RWA for corporate exposures will be characterised by increased

consistency and objectivity, whilst also maintaining some of the benefits that the IRB approach

offers.

In addition, we note that for very large international corporates, different banks would have fairly

similar PDs calculated under the IRB approach, as the information used by different institutions to

feed their internal models will be consistent.

Specialised Lending

The Committee proposes to remove the IRB approaches for specialised lending that use banks’

estimates of model parameter, as it expects that banks are unlikely to have sufficient data to produce

reliable estimates of PD and LGD.

It is however important to retain risk sensitivity in capital requirements for Specialised Lending to

ensure that finance for low risk lending can be provided by the banking sector, particularly for all

forms of long-term financing (including infrastructure lending) that support economic growth.

Specialised lending by its nature covers a wide range of activities with differing risk levels, for which

the limited range of risk weightings available under the IRB supervisory slotting approach (or the

Standardised approach) are not appropriate. Low risk lending at initiation is effectively assigned

either a 70% or 90% risk weighting under the current slotting approach. This does not seem

intuitively correct.

A major limitation of the current IRB slotting approach is the limited recognition it gives to risk

mitigation through guarantees, including guarantees provided by Export Credit Agencies.

Furthermore, under the Committee’s Securitisation framework, both the current supervisory formula

method and the proposed SEC-IRBA approach cannot be used for IRB slotting exposures to obtain

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

11

capital relief for significant risk transfer transactions. The sensitivity of capital requirements to

maturity is also limited, as it only distinguishes between exposures of less than 2.5 years maturity

and those greater than or equal to 2.5 years maturity whereas the maturity of infrastructure

transactions is typically in excess of 2.5 years, but can vary widely.

We would suggest that if the Committee does not wish to continue to permit the use of the AIRB

approach for Specialised Lending, then the current IRB slotting approach should be reviewed in

order to increase risk sensitivity to adequately reflect the underlying risks from projects. In particular

the approach needs to provide appropriate recognition of the risk-reducing benefits of risk mitigation

techniques. Further risk sensitivity could be introduced by the use of more granular maturity buckets.

The Committee should also consider the interaction of the IRB slotting approach and the

Securitisation framework to ensure that appropriate capital relief can be achieved under significant

risk transfer securitisations under either the supervisory formula approach or the proposed SEC-

IRBA. It is important that efficient securitisation opportunities are available for banks to transfer the

risks of Project Finance to the market, in order to provide market capacity for the financing of such

activity.

Retail Exposures

Mortgage LGD floors

Floors are only appropriate where risk cannot be measured properly. For large Retail portfolios, the

richness of the data allows risk to be modelled with a high degree of confidence.

A 10% account level LGD floor would not encourage a risk sensitive approach in the UK mortgage

market but rather would penalise low risk assets. This potentially results in a situation that is to

customers’ detriment (lower risk lending is more costly) or creates systemic distortion (higher risk

lending is favoured).

Directionally the floor would lead to models assuming the same level of loss for all accounts with a

Debt to Value (DTV) of less than 80%.

The simple calculation below demonstrates the impact of a 10% LGD account floor. It utilises

publicly available parameters where possible.

Scenario DTV Collateral Exposure Haircut LGP PPD DT LGD

DT LGD 10% Floor

1 60% 100 60 40% 0 40% 0 10

2 80% 100 80 40% 20 40% 8 10

3 80% 100 80 40% 20 50% 10 10

We would therefore propose that any floor be applied at portfolio, rather than exposure level. This

would increase comparability without creating perverse incentives.

This constancy of loss is not reflected in observed data where losses demonstrate strong correlation

with increasing Loss to Value (LTV). Analysis based on 2008 / 2009 vintages shows losses for 80%

LTV were significantly higher than for ≤ 60% LTV accounts.

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

12

For the lower DTV bands, losses would only be expected in a small number of cases. The overall

loss rate for that band would be very low as a result.

Buy to let

In reading this consultation alongside the Committee’s earlier consultation, ‘Revisions to the

Standardised Approach for Credit Risk’5, we are extremely concerned that Buy-to-Let (BTL) lending

in the UK will be subject to significantly higher capital requirements under these proposals.

The Annex to the consultation paper proposes that exposures to individuals and owner occupiers in

the case of mortgages move to the A-IRB approach. This results in some confusion regarding the

treatment of BTL portfolios, where the borrower purchases a property with the intention of subletting

and where the repayment is ‘materially dependent’ on cash flows generated by the property on

which the loan is secured. Do the current proposals imply that BTL portfolios are not fit for the IRB

approach and will hence move to the standardised approach? A revised standardised approach is

relatively risk insensitive compared to the IRB approach where risk is informed by a bank’s detailed

understanding of the risk factors and loss experience in this type of lending. If a move to

standardised approach is the case, we stress our concern regarding the treatment of BTL portfolios

under the standardised approach, as expressed in the BBA response to the Committee CP on

revisions to the standardised approach6. The capital treatment under the standardised approach is

unjustifiably penal. A dramatic increase in capital requirements applicable to BTL lending could have

a serious impact on the wider UK housing market, with potential social and political consequences.

BTL mortgage lending in the UK is collateralised in the same way as owner-occupied residential

mortgage lending and robust BTL lending that takes into account the high financial quality of the

landlord is little different in its risk profile when compared with mortgage lending to owner occupiers.

Such exposures could be viewed as being more robust in the sense that (i) the tenant’s contracted

income flow is subject to a formal tenancy agreement and to credit references (ii) the property

owner’s covenant as the property and the borrowing will be held in the name of the landlord.

We re-iterate our recommendation that the revised rules should allow for jurisdictional specificities by

allowing a national discretion for regulators to permit a specific type of lending to receive the general

treatment where they have evidence of a well-established residential property market, with readily

available market prices and low observed loss rates. In our view, the Committee’s stated objectives

could be achieved while allowing national competent authorities the discretion to determine the

appropriate approach for certain types of lending, provided that appropriate criteria are met.

The Committee should consider the impact of these proposals on the market for BTL mortgage

lending in the UK. Inappropriately high capital requirements could lead to detrimental outcomes for

customers and for the UK housing market, through an increase in pricing and a reduction in the

availability of credit. It is clear to us that it would be wholly inappropriate and counterproductive to

treat UK BTL in the same way as more risky, cyclical, speculative lending.

We urge the Committee to clarify as soon as possible whether this is indeed the intention of the

proposals and provide clarity on the treatment of BTL portfolios under the IRB approach.

5 http://www.bis.org/bcbs/publ/d347.htm

6 https://www.bba.org.uk/policy/financial-and-risk-policy/prudential-capital-and-risk/credit-risk/bba-response-to-

basel-committee-cp-revisions-to-the-standardised-approach-for-credit-risk/

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

13

Qualified Revolving Retail Exposure floors

We have concerns regarding the proposed parameter floors of QRRE (Qualified Revolving Retail

Exposures) transactors and revolvers. In particular, the consultation defines QRRE transactors as

facilities such as credit cards and charge cards where the balance has always been repaid at each

scheduled repayment date and that at least six months have passed since the facility was first used

as a means of payment. Facilities not meeting these requirements are classified as QRRE revolvers,

with higher parameter floors assigned (10bps as opposed to 5bps for QRRE transactors).

However, this definition may penalise certain cases where historical information that would otherwise

not be deemed as significant classifies a facility as QRRE revolver. For example, historical data

indicating that an individual missed a payment, say 20 years ago, would result in that individual not

qualifying for the QRRE transactor category, even if recent data confirms that balances have ever

since been paid before the scheduled repayment date. We recommend a more pragmatic approach

that permits a facility to be classified as a QRRE transactor if the balance has been repaid on the

due repayment date in each of the previous six months. Such definition should also include clarity on

the treatment of inactive accounts.

The proposed QRRE definition does not adequately cover retail current accounts. As they have no

scheduled repayment date all such accounts would be treated as revolvers regardless of the

underlying risk. We do not believe that this is appropriate treatment.

Definition of Commitment

We welcome the clarification of ‘commitment’ and note that it does not include commitments that are

documented as uncommitted, and require specific bank approval prior to each drawdown. So such

facilities will not require a CCF at all. We request that the Committee clarifies this point to avoid

impacting facilities, such as factoring lines and trade facilities which are particularly important

sources of finance for SMEs.

Parameter estimation practices and fixed supervisory parameters

Availability of data

Our members acknowledge that there are some portfolios where modelling is a challenge due to low

numbers of defaults and subsequent losses. However whilst the availability of default and loss data

is scarce for these portfolios, the very nature of a low default portfolio is of relatively lower risk when

compared against other asset classes. A key control within the capital IRB framework is to ensure

prudent capital allocation where uncertainty exists, but in the case of low default portfolios the

quantity and quality of both internal and publically available data on these entities materially

mitigates the uncertainty introduced through the low volumes of default events. As a result we feel

that removing IRB would result in an excessive increase in capital requirement for what are better-

quality obligors and that constraints should be introduced through minimum standards of data and

modelling rather than at the portfolio level.

A lack of default can be ‘good news’ for PD estimation and the observation of no or limited default

experience for a portfolio of clients over a sufficiently long time horizon can be used to make

inference on the ‘true PD’ for the portfolio. There are now well established ‘low default portfolio’

techniques which can support the derivation of robust PD model calibration for such portfolios. The

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

14

standardisation of key assumptions which underpin these techniques (e.g. asset correlation,

confidence interval for a ‘Pluto-Tasche’ estimator) may lead to consistency of PD calibration across

different institutions for similar portfolios. The discrimination of risk within a low default portfolio, i.e.

the selection of model drivers for given level of PD calibration, would still need to rest on expert

judgement. Nevertheless, the Merton model of credit risk - commending the inclusion of proxies of

leverage and asset volatility as drivers of default risk, is well accepted amongst practitioners and this

should drive consistency in model selection as well.

No or limited default experience is on the other hand ‘no news’ for LGD/EAD estimation which

depends on information of loss realisation ‘given a default has occurred’. The reference to

conventional benchmarks (e.g. FIRB LGD and EAD values) when a defined, minimum number of

default observations is not available may be the only way to produce consistent estimates across

institutions.

Through the cycle

It is our belief that the requirement being outlined is that PD estimates reflect ‘Through the Cycle’

(TTC) estimates. This should not be confused with risk insensitivity which is what is described by

“rating categories generally remain stable over time”. TTC estimates are expected to lead to

relatively stable capital requirements since the distribution of ratings across large portfolios are

expected to remain relatively stable over time – this is not to say individual ratings should be stable.

On the contrary if the underlying risk changes ratings should change to reflect that. We would also

note the notion of TTC has been a source of debate for a number of years. It may be that

inconsistency between institutions will not be entirely removed by requiring the use of TTC estimates

since contentious aspects such as defining a cycle will be subjective and a source of difference.

Additionally determining accurate TTC estimates for some portfolios has been deemed as infeasible

by some Competent Authorities.

As a result a number of UK banks apply a Point In Time approach to PD estimation in their Retail

portfolios. Without further guidance on the expectations for an ‘approvable’ TTC model, it is unlikely

that this position can be addressed in the short-term. Our members therefore acknowledge the

desire for consistency, but request that consideration be applied to the ability of, and time required

for firms to develop and gain approval for large numbers of models.

Additional guidance will be required with regards to how to interpret what constitutes “downturn”

data. This is particularly true for low default portfolios.

Clarity is also required with regard to the requirements for the “Granularity of PD estimates”.

Parameter floors

Parameter floors may be legitimate in circumstances where data does not allow robust development

of models/model components. However, where the richness of data enables risk to be modelled

effectively floors should not be used, as they remove risk sensitivity and will inevitably incentivise

lending to poorer quality borrowers. Additionally, the use of exposure-level floors is nonsensical for

highly secured obligors. In our opinion where parameter floors are absolutely necessary, they should

be applied at a portfolio level.

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

15

Downturn LGD

The Committee’s requirements with regards to downturn LGD need to be clarified. For instance does

the add-on methodology proposed apply only to unsecured LGDs? Are banks required to model

unsecured and secured components separately? While the paper notes that downturn LGDs are a

significant source of variability, we do not believe this issue will only be addressed by considering

unsecured LGDs as we believe the impact of competent authority mandated parameters is a

considerable source of variation across jurisdictions. The proposed approach may lose sight of the

actual risk if an arbitrary floor is applied.

EAD

We do not believe there is value in restricting EAD estimates to a fixed 12 month horizon. If own

estimates back test appropriately then any variation across banks can be justified and the

introduction of relatively arbitrary modelling choices is unnecessary.

Maturity for F-IRB

The Committee recognise that competent authorities have a national discretion to allow FIRB banks

to use a fixed 2.5 year maturity factor or maturity based on an A-IRB approach. For consistency

within FIRB banks it would be preferable to have one approach only rather than allowing the national

discretion.

Rating system design and use

Within the proposals there are statements about how rating systems ‘should’ be designed and data

‘should’ be used. Much greater definition is required if a harmonised, risk sensitive framework is to

be achieved, including a statement of the consequences for inadequately meeting requirements.

IMM Floor

The industry has significant concerns regarding Basel’s proposal to introduce a floor to the

counterparty credit risk capital derived from the Internal Model Method (IMM). A floor which is based

on SA-CCR - still a notional based measure of risk – will encourage banks to reduce notionals, but

not necessarily risk. We believe it is imperative to reiterate the importance of risk-sensitivity to the

capital framework and the incentivisation of sophisticated credit risk measurement in the capital

framework.

The IMM approach allows banks to model the specific risk factors to which they are exposed, as well

as portfolio composition, volatilities and correlations. The level of accuracy delivered by IMM is

simply not achievable with SA-CCR.

The IMM approach is already subject to a floor introduced in the Basel III framework which was only

implemented at the beginning of 2014. Basel III requires that banks must use the greater of the

portfolio-level capital charge based on Effective EPE using current market data and the portfolio-

level capital charge based on Effective EPE using a stress calibration. This floor required significant

investment in computing power and infrastructure to run all model simulations under different

assumptions.

Response by the British Bankers Association to the Basel Committee’s consultation on reducing variation in credit risk assets

16

The current IMM floor has had less than 18 months in place before being replaced by another IMM

floor. We would strongly recommend that Basel gives the current floor time to be reviewed and

reconsiders the relevance of the proposed IMM floor given the significant expense that has only

recently been incurred.

Concerns around the design and calibration of any output floor

The consultation refers to the ongoing consideration of the design and calibration of a capital floor to

replace the ‘transitional’ Basel I floor. Aside from the very brief consultation paper published in

December 2014, ‘Capital floors: the design of a framework based on standardised approaches’7, the

implementation of an output floor has not yet been through a consultation process. We would expect

a full consultation on the design of any output floor.

When considered in conjunction with the wide-ranging proposed changes to both the IRB and

standardised approaches (including the proposed input floors), it is difficult to see what benefits an

output floor would deliver beyond what is achieved by the application of Leverage Ratio

requirements. Indeed, many of the arguments for an output floor put forward in the December 2014

consultation are identical to those put forward to justify the introduction of Leverage Ratio

requirements.

Conclusion

It will be important that as the Committee moves towards adoption of a finalised package it does so

in a sensitive and measured manner. Simplicity and comparability should not trump risk sensitivity.

Modelling of appropriate exposures, including low default portfolios should be retained, not least

because it supports progressive risk management behaviours and competition within the industry.

All necessary time should be taken, by regulators and the industry alike, to get the significant

changes the proposals represent right, based on a thorough understanding of the likely impacts on

bank capital requirements. We look forward to continuing to work with the Committee to further

develop our suggested alternative approaches to find solutions which achieve greater consistency

within the IRB framework yet retain a risk sensitive approach.

The timelines for the QIS and Consultation have been very tight. It has not been possible in them to

fully quantify the impact of the proposals as so many aspects are still work in progress, including the

revised standardised approach and the impact of the overall capital floors. We strongly recommend

that there be a second consultation and QIS exercise where the impact of the complete reform

programme can be assessed holistically and used to inform final calibration.

At the moment it is difficult to align the full range of changes proposed with the high level

commitment to keep the overall level of capital in the system unchanged. It is only after a complete

assessment of the full set of rule changes and appropriate calibration that the Committee will be able

to meet this commitment. It should ensure that this is done.

Responsible executive Simon Hills British Bankers Association +44 (0) 207 216 8861

7 http://www.bis.org/bcbs/publ/d306.htm