red flags (ccsa study guide)

TRANSCRIPT

8/16/2019 Red Flags (CCSA Study Guide)

http://slidepdf.com/reader/full/red-flags-ccsa-study-guide 1/3

.

Domain III: Elements

of

the

CSA

Process

95

m I I rio:

mt

nt nbl' , It_ tbe ndc lIae or current . . osed controls mitigating identified

ri k ,

In lh '::.;'

as S.

the issul' may

need to

be

discussed a ain or the)ack

of

consensus on the

• u

nH:l\

nt"

i

h.1

bt'

includl'd

in

the

fino report.

s

_ r

.J. F

n

d

UI fness

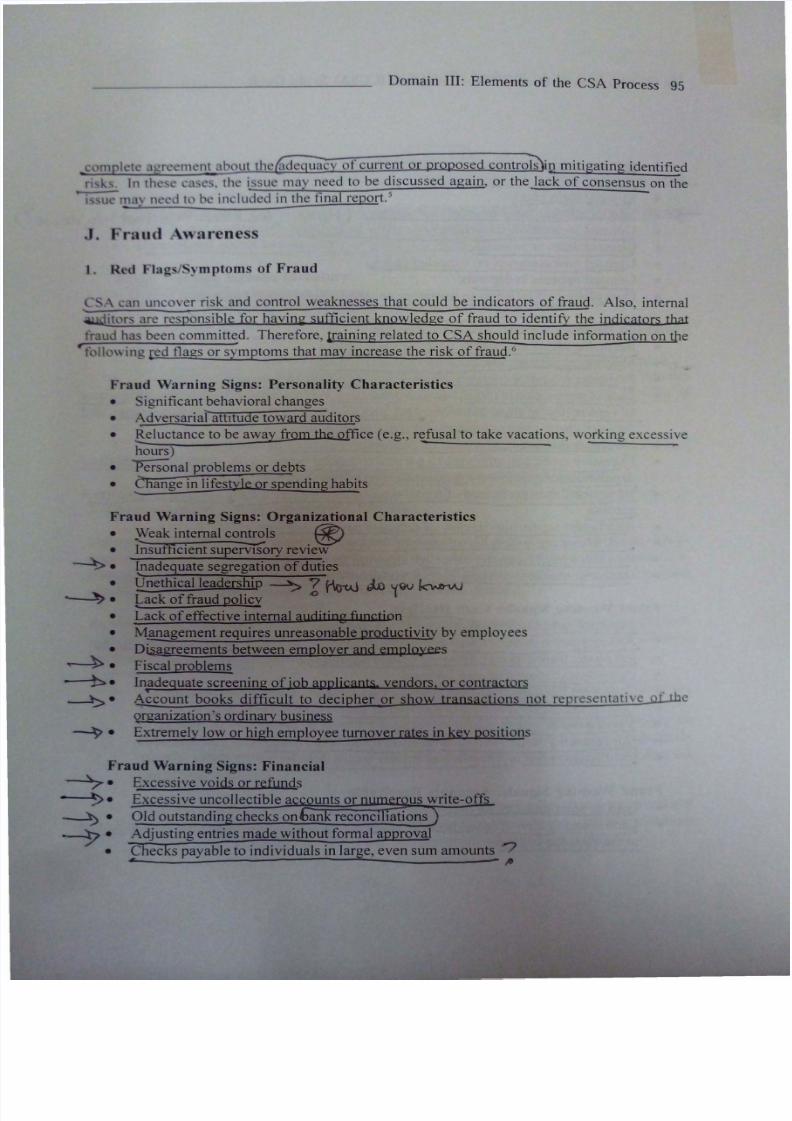

1. Reo laas/Sy mptoms

of Fraud

- - \ ,Hl UtKO\ er risk and control weaknesses that could be indicators of fraud. Also, internal

.?\lkiit

rs ilr responsible for h a v i n ~ sufficient knowledge of fraud to identify the indjcators that

fi ud

h : ~

been committt:d. Therefore, training related to CSA should include information

on

the

•

fi II wing ,ed flags or symptoms that

may

increase the risk offraud.

6

Fraud 'Varning Signs: Personality Characteristics

• Significant behavioral changes

• Adversarial attItude toward auditors

• E-eluctance

to

be away from the office (e.g.,

r ~ f u s a l

to take vacations, working excessi\ e

hours)

• Personal problems or debts

• ~ h a n g e in lifestyle or spending habits

Fraud

Warning Signs: Organizational Characteristics

•

~ e a k

internal c o n t r ~ l s

®

• Insufficient supervisory review

-

~

lnadequate segregation of duties

• Unethicalleadership

,>?

f \o-uJ k ~ Q v

kv..e-vJ

'>

•

--ack

of fraud policy

.0

• Lack

of

effective internal auditjng fimction

• Management requires unreasonable productivity by employees

• Disagreements between employer and emplQ)'ees

..-, ~ . Fiscal problems

_.

-:b1 . Inadequate screening of job applicants vendors, or contractors

•

- t ;> •

~ c c o u n t

books difficult to decipher or show transactions not repre

~ n t a t i v

of

the

organization's ordinary business

~ . ~ x t r e m e l y

low or high employee turnover rates in key positions

Adj

usting entries made without formal a roval

fhec s payable to individuals in large, even sum amounts .

Z

8/16/2019 Red Flags (CCSA Study Guide)

http://slidepdf.com/reader/full/red-flags-ccsa-study-guide 2/3

nf

I 1·

m flt

S ) Stud y Guide

•

•

11 • I I 1

IOWl a

dd

r

css ( -tow... we

<bn t

-P ''/'0

dz,

we ?)

r

1.

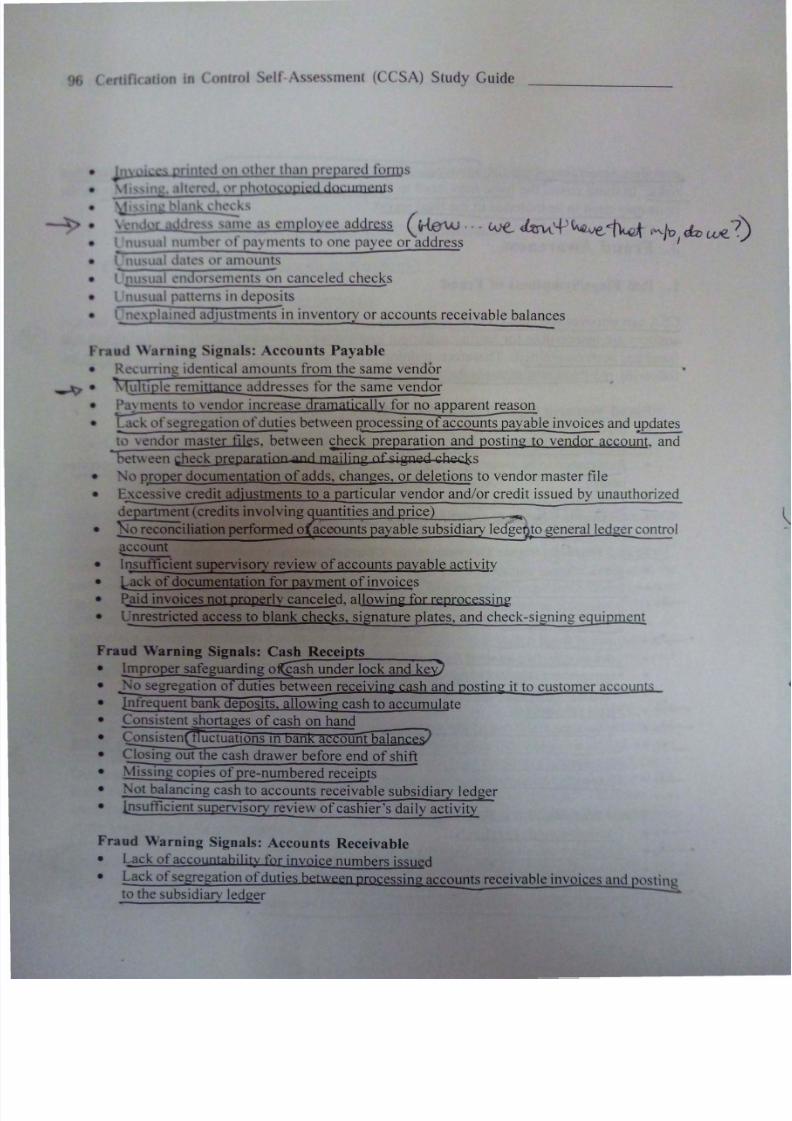

' 111 nt to one

pa

yee

or

address

•

in depos its

a ) ustments in inventory

or

accounts receivable balances

rning

ianals:

Accounts

Payable

,,",,-,-,urnl

H

identical amounts from the same vendor

Ie r ni ce addresses for the same

vendor

•

m 11t to vendor increase r

I

for

no

apparent reason

•

k k

f

egregation

f d u t i ~ s

between Rrocessing

0

accounts payable invoices and l pdates

t endor master s.

between ~ h e k

preparation and posting to vendor account, and

t \ \ een

~ e k

preparationand mailing

of£iSIleQ

cbecks

•

Rroper documentation

of

adds, changes,

or

deletions to vendor master file

•

E cessive credit ad'ustments to a articular vendor and/or credit issued by unauthorized

d partment (credits involving ll:antities n ~ rice . . .

~ o

reconciliation

pet fanned 0

acoounts a able subsidia ledge to · eneral led er control

account

• Insuttlcient S'PMSOry review

of

accounts payable activity

• Lack

of

documentation for payment

of n v o i c ~ s

•

I .aid

invoices

ot

prOJ)erly c a n c e l ~ d a l l o w i n ~ for

r e p r o c e s s i n ~

• Unrestricted access to blank checks si ature plates, and check-si

ment

Fraud Warning Signals: Cash Recei ts

• {mpro r safe ding 0 cash under lock and ke

• 0 segregation 0 uties between rec . . sh and ostin it to customer accou

• Infrequent batik epos.its. allowing cash to accumulate

• Consistent shorta es

of

cash on hand

• Consisten uctuatlOns

In

an ount bal

• <;:losing out

t

e cash drawer before end

of

shift

• issing copies of pre-numbered receipts

• ot balancing cash to accounts receivable subsidiary ledger

• insufficient supervisory review

of

cashier's daily activity

Fraud

Warning Signals: Accounts Receivable

• Lack ofaccountabil jt¥ for invoice numbers issyed

• Lack

of

se e ation

of

dutie es in accounts receivable invoi

· ~ s

and

to

the subsidiary ledger

•

8/16/2019 Red Flags (CCSA Study Guide)

http://slidepdf.com/reader/full/red-flags-ccsa-study-guide 3/3

Domain III: Elements

of

the CSA Process

97

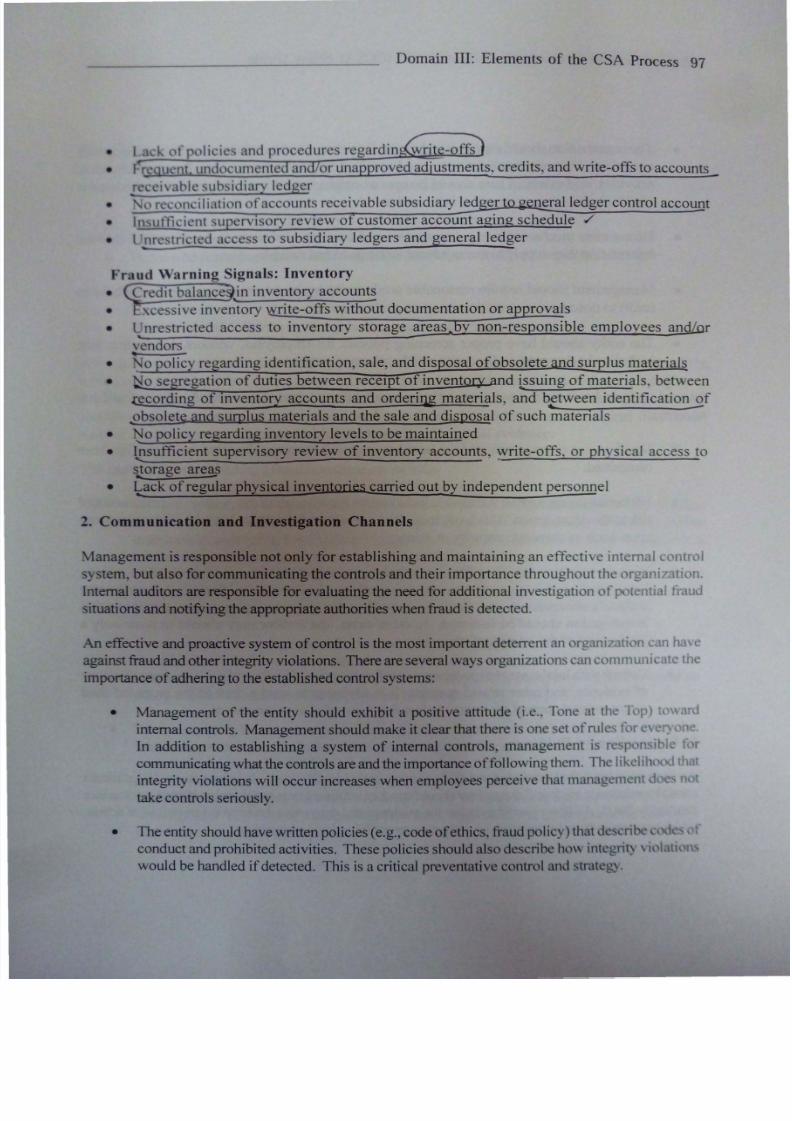

• )Iicil.:: and procedures regardin writ -

ffs

• h

III

nt.

unlit

ollllcntl: an

or

unapproved adjustments, credits, and write-offs to accounts _

~ i V l b l

suh, idi.

I

kdger

• )

[ t

. )Ill'ilhtion

offIce unts receivable subsidiary led er neralledger control account

• It

urn

iI. m

supt::rvlsory revIew 0 customer account aging schedule /

• UIlI

t T i ~ t c d

acct:.

s to subsidiary ledgers and general ledger

Fr Iud \ I riling Signals: Inventory

• ledll balance in inventory accounts

~ ~ ~ ~ - - ~

• . cessive inventory write-offs without documentation or approvals

• llnrestricted access to inventory storage areas,..by non-responsible employees and/or

vendors

.

• ~ polic

re

arding identification, sale, and dis osal ofobsolete nd SUrPlus materials

• ~ segregation of duties between recelp of inventory and jssuing

of

materials, between

.recording

of

inventory accounts and ordering materials, and b ~ t w e e n identification qf

obsolete and surplus m a t e ~ i a l s and the sale and disposal of such materials

• ~ policy regarding inventory levels to be maintained

• ~ s u f f i c i e n t supervisory review of inventory accounts, write-offs, or physical access to

s., orage areas

•

I.:,ack

of regular physical inventories carried out by independent personnel

2. Communication and Investigation Channels

Management

is

responsible not only for establishing and maintaining an effective int rn I ntr01

system, but also for communicating the controls and their importance throughout th r , t iznti n.

Internal auditors are responsible for evaluating the need

for

additional investig

ation

ofp

t ntial ud

situations and notifying the appropriate authorities

when

fraud is detected.

An effective

and

proactive system of control is the most important deterr nt

an

1rgani

tic

nCdn ha

against fraud

and

other integrity violations. There

are

several

ways

organizati ns

e n . mmuni ale

th

importance ofadhering

to the

established control systems:

• Management

of

the

entity should exhibit a positive attitude (i.e.,

Tone

at

the

1

p)

t

ard

internal controls. Management should

make it

clear that

there i one

set of

rule l' I .

In addition

to

establishing a system

of

internal controls, management is r

l

n. ibl {; r

communicating what the controls are and the importance

of

ollowi

ng

them. Til lik lih t

t

integrity violations will occur increases when employees perceive that mana ...eOl nt n

take controls seriously.

• The

entity

should have written

policies

(e.g.,

code

ofethics. fraud

policy)

that

d 'crit

conduct and prohibited activities. These policies should also describe ho\\ int brit)

,i(

1

ti

would be handled if detected. This is a

critical

preventative

control

and · t r n h : g ~