recording transactions in a general journal. section 1the accounting cycle what you’ll learn the...

TRANSCRIPT

Recording Transactions in a General

Journal

Recording Transactions in a General

Journal

Section 1 The Accounting Cycle

Section 1 The Accounting Cycle

What You’ll Learn

The first three steps in the accounting cycle.

Why is it necessary to journalize transactions.

The different kinds of source documents used in a business.

The difference between a calendar year and a fiscal year.

What You’ll Learn

The first three steps in the accounting cycle.

Why is it necessary to journalize transactions.

The different kinds of source documents used in a business.

The difference between a calendar year and a fiscal year.

Why It’s ImportantIn the real world, businesses follow a

similar accounting cycle, record transactions in a general journal, and operate within a predefined accounting period.

Why It’s ImportantIn the real world, businesses follow a

similar accounting cycle, record transactions in a general journal, and operate within a predefined accounting period.

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

Key Terms accounting cycle source document invoice receipt memorandum

Key Terms accounting cycle source document invoice receipt memorandum

check stub journal journalizing calendar year fiscal year

check stub journal journalizing calendar year fiscal year

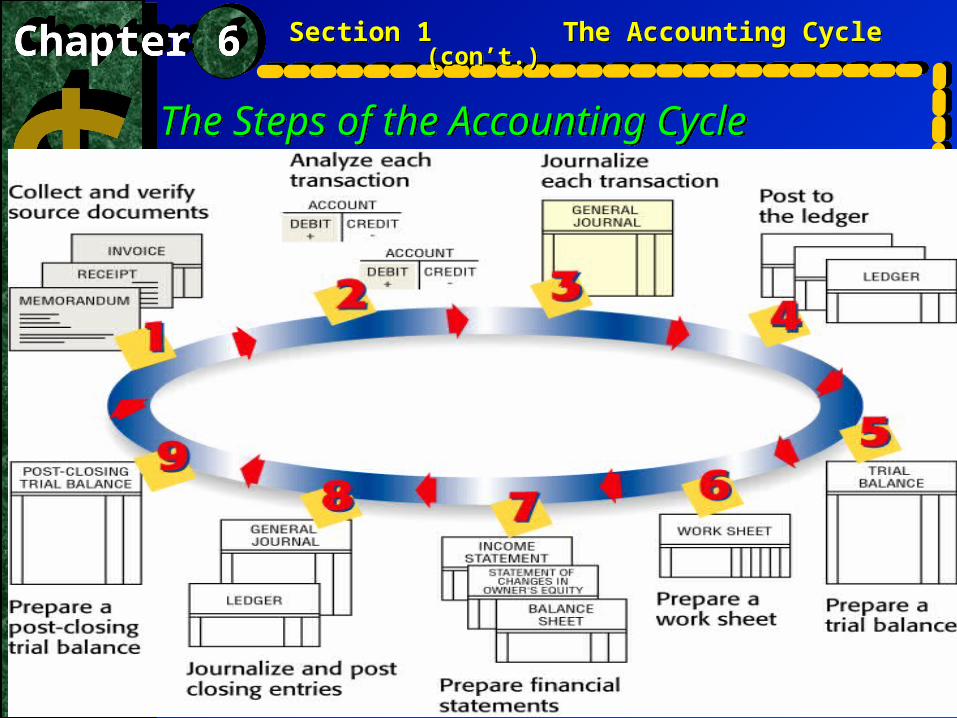

The Steps of the Accounting CycleThe Steps of the Accounting Cycle

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

The accounting cycle starts by

collecting and verifying the accuracy

of source documents.

Source document is a paper

prepared as evidence of that

transaction.

The accounting cycle starts by

collecting and verifying the accuracy

of source documents.

Source document is a paper

prepared as evidence of that

transaction.

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

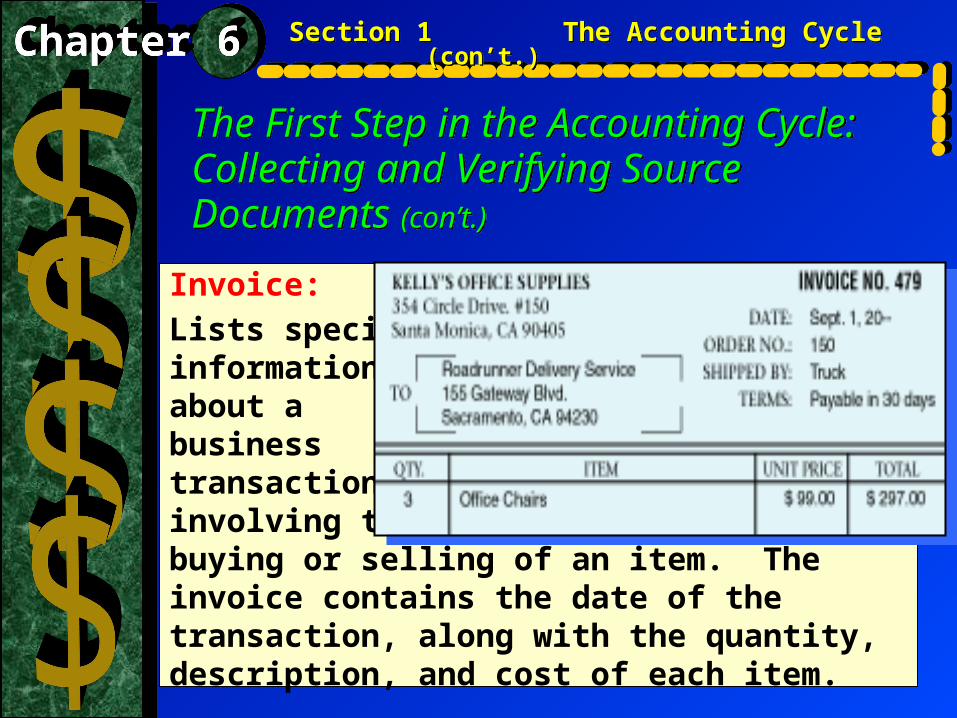

Invoice:

Lists specificinformationabout abusinesstransactioninvolving thebuying or selling of an item. The invoice contains the date of the transaction, along with the quantity, description, and cost of each item.

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

Receipt:A record ofcash receivedby a business.It indicates thedate the payment was received, thename of the person or business from whom the payment was received, and the amount of the payment.

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

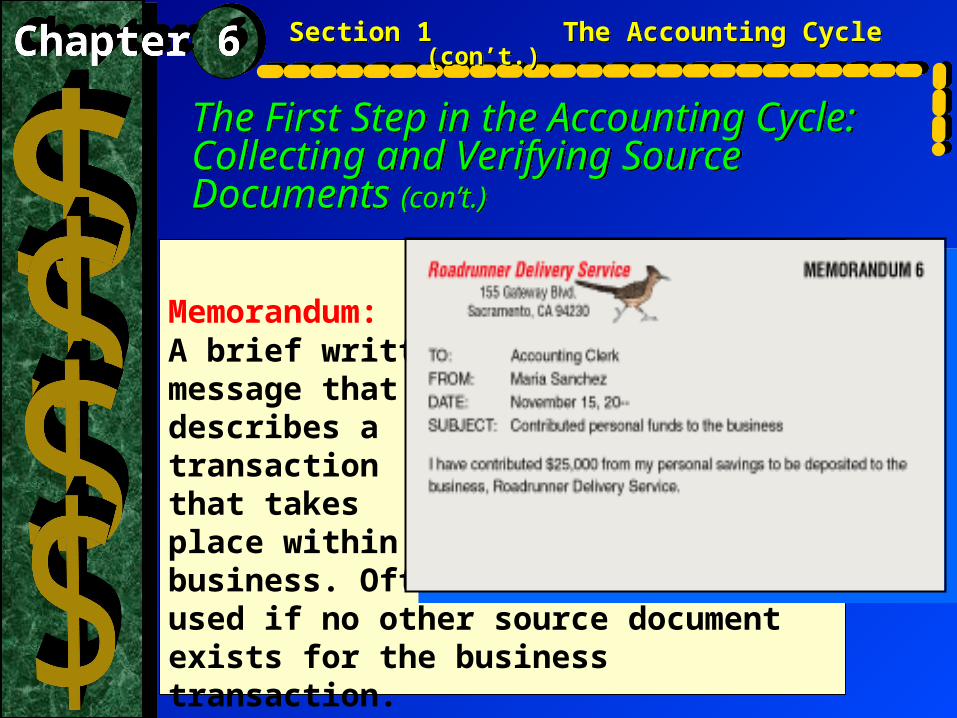

Memorandum:A brief writtenmessage thatdescribes atransactionthat takesplace within abusiness. Oftenused if no other source document exists for the business transaction.

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

The First Step in the Accounting Cycle: Collecting and Verifying Source Documents (con’t.)

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

Check Stub:The check stublists the sameinformation thatappears on acheck: the datewritten, the Person or Business to whom the check was written, and the amount of the check. The check stub also shows the balance in the checking account before and after each check is written.

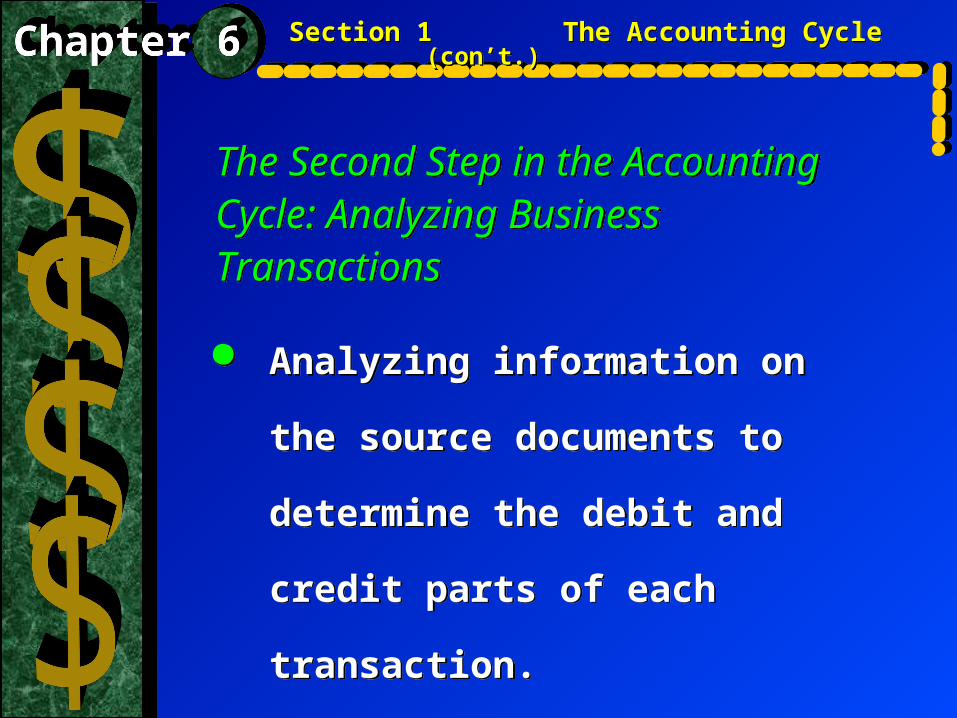

The Second Step in the Accounting Cycle: Analyzing Business Transactions

The Second Step in the Accounting Cycle: Analyzing Business Transactions

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

Analyzing information on the

source documents to determine

the debit and credit parts of each

transaction.

Analyzing information on the

source documents to determine

the debit and credit parts of each

transaction.

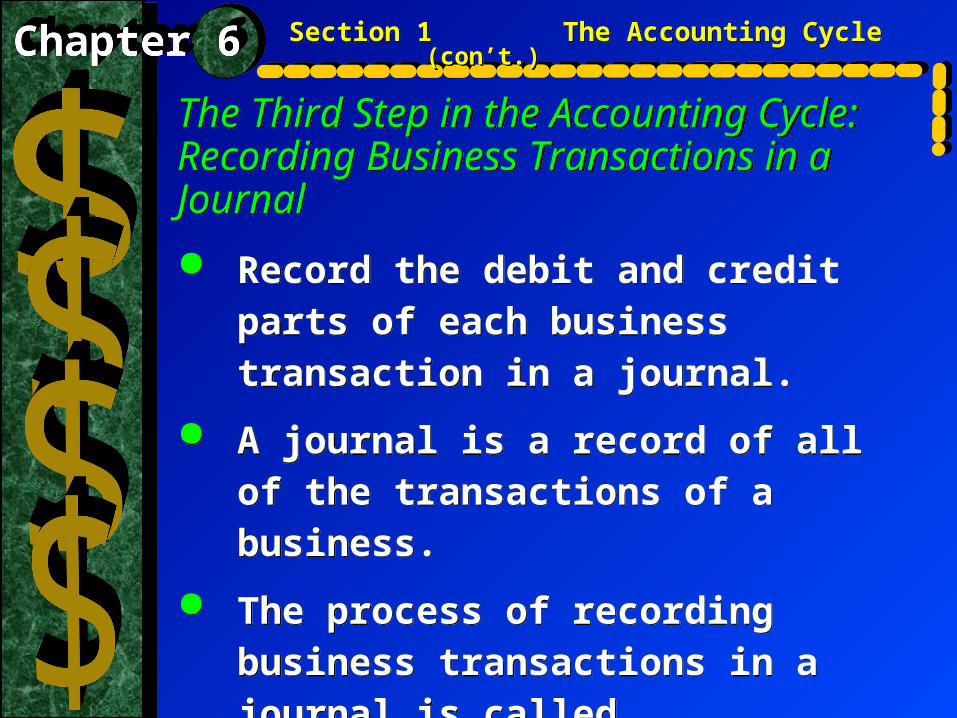

The Third Step in the Accounting Cycle: Recording Business Transactions in a Journal

The Third Step in the Accounting Cycle: Recording Business Transactions in a Journal

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

Record the debit and credit parts of each business transaction in a journal.

A journal is a record of all of the transactions of a business.

The process of recording business transactions in a journal is called journalizing.

Record the debit and credit parts of each business transaction in a journal.

A journal is a record of all of the transactions of a business.

The process of recording business transactions in a journal is called journalizing.

The Accounting PeriodThe Accounting Period

Section 1 The Accounting Cycle (con’t.)Section 1 The Accounting Cycle (con’t.)

accounting records are summarized for a certain period of time, called an accounting period

most businesses use a year as their accounting period begins on January 1 and ends on December 31

calendar year

fiscal year is an accounting period of twelve months

accounting records are summarized for a certain period of time, called an accounting period

most businesses use a year as their accounting period begins on January 1 and ends on December 31

calendar year

fiscal year is an accounting period of twelve months

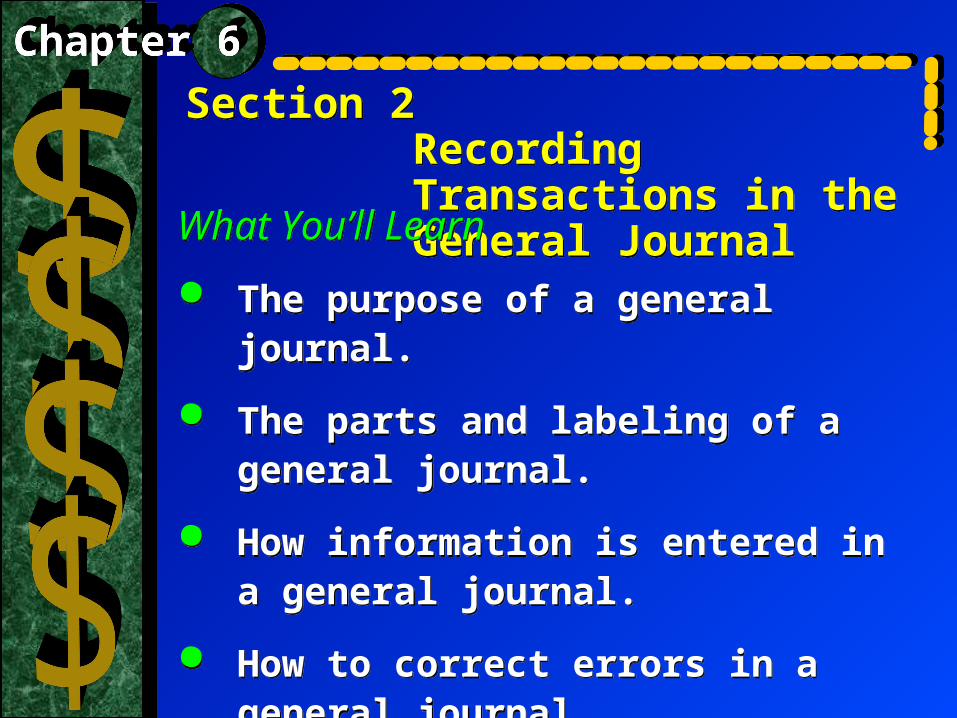

Section 2Recording Transactions in the General Journal

Section 2Recording Transactions in the General Journal

What You’ll Learn

The purpose of a general journal.

The parts and labeling of a general journal.

How information is entered in a general journal.

How to correct errors in a general journal.

What You’ll Learn

The purpose of a general journal.

The parts and labeling of a general journal.

How information is entered in a general journal.

How to correct errors in a general journal.

Why It’s Important

The general journal is a permanent

record of the financial transactions of

a business.

Why It’s Important

The general journal is a permanent

record of the financial transactions of

a business.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Key Terms

general journal

Key Terms

general journal

Recording a General Journal EntryThe general journal is an all purpose

journal in which all the transactions of a business may be recorded.

Recording a General Journal EntryThe general journal is an all purpose

journal in which all the transactions of a business may be recorded.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

1 Date of the transaction1 Date of the transaction

4 Name of the account credited4 Name of the account credited

2 Name of the account transaction2 Name of the account transaction 3 Amount of the debit3 Amount of the debit

6 Source documentreference or an explanation

6 Source documentreference or an explanation

5 Amount of the credit

5 Amount of the credit

Business Transaction

ANALYSIS Identify 1. Identify the accounts affected.

Classify 2. Classify the accounts affected.

+ / – 3. Determine the amount of the increase or decrease for each account affected.

BUSINESS TRANSACTION ANALYSIS

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Business Transaction (con’t.)

DEBIT-CREDIT RULE 4. Which account is debited? For what amount?

5. Which account is credited? For what amount?

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

BUSINESS TRANSACTION ANALYSIS (con’t.)

Business Transaction (con’t.)

T ACCOUNTS 6. What is the complete entry in T-account form?

7.What is the complete entry in

general journal form?

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

BUSINESS TRANSACTION ANALYSIS (con’t.)

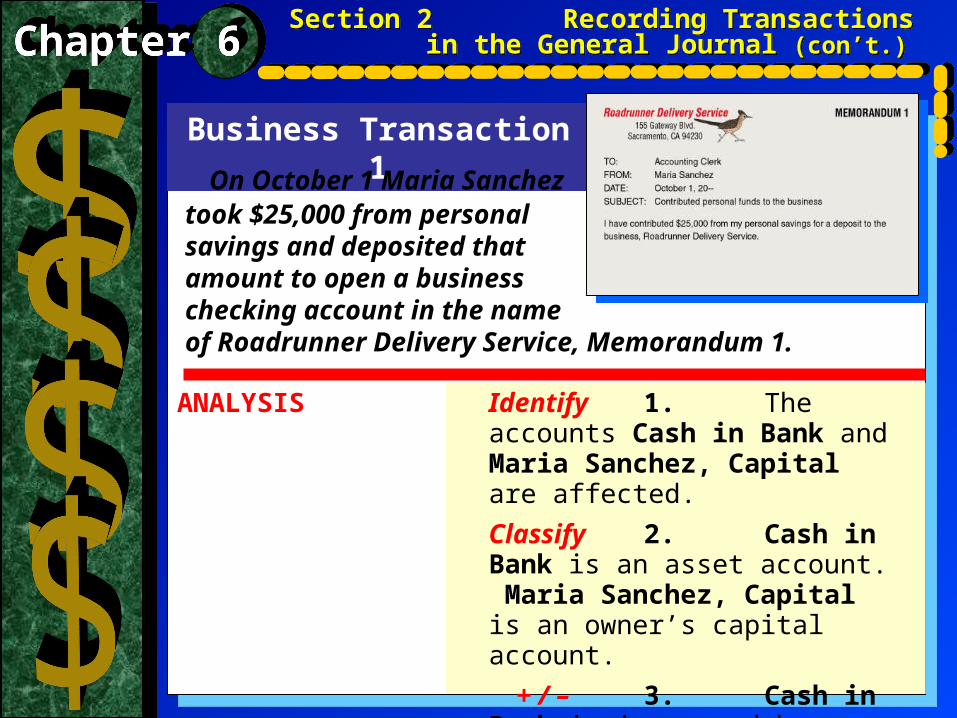

Business Transaction 1

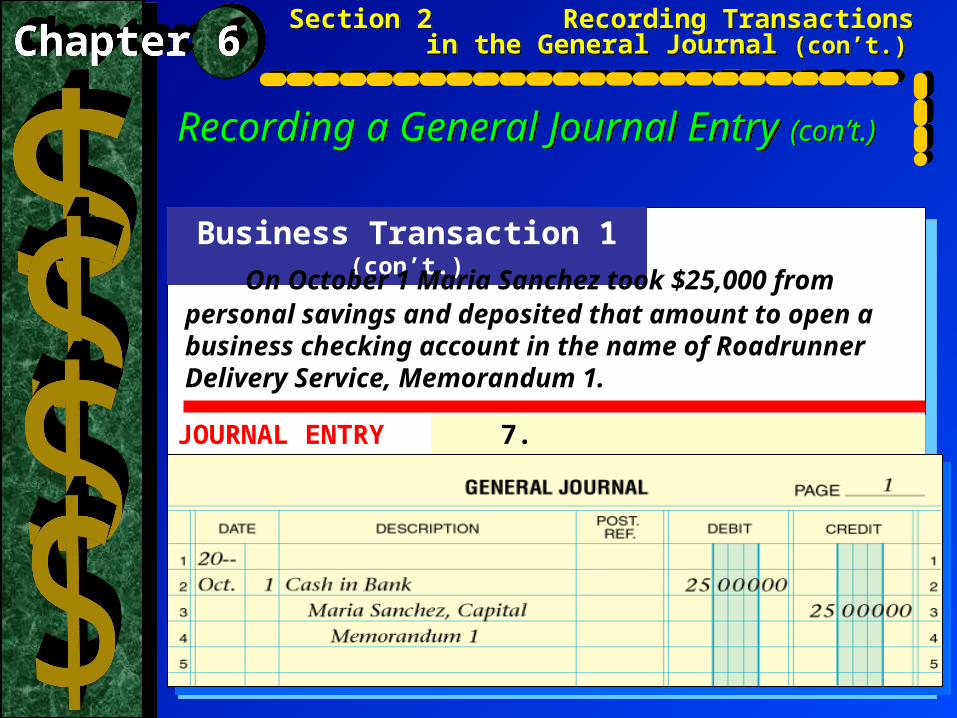

ANALYSIS Identify 1. The accounts Cash in Bank and Maria Sanchez, Capital are affected.

Classify 2. Cash in Bank is an asset account. Maria Sanchez, Capital is an owner’s capital account.

+ / – 3. Cash in Bank is increased by $25,000. Maria Sanchez, Capital is increased by $25,000.

On October 1 Maria Sancheztook $25,000 from personal savings and deposited that amount to open a businesschecking account in the nameof Roadrunner Delivery Service, Memorandum 1.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

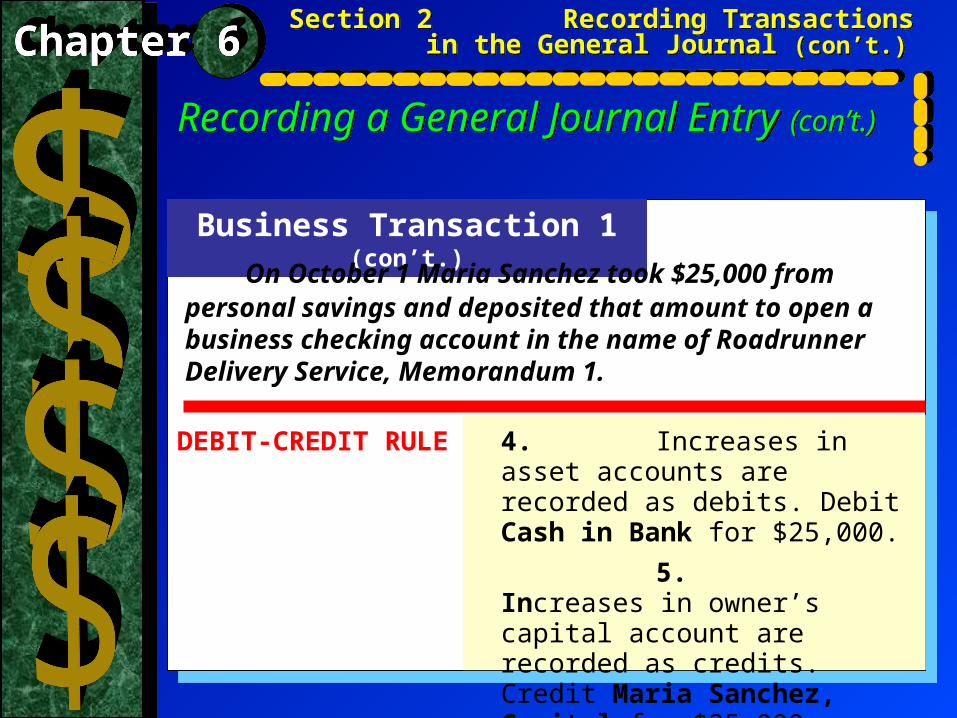

Business Transaction 1 (con’t.)

DEBIT-CREDIT RULE 4. Increases in asset accounts are recorded as debits. Debit Cash in Bank for $25,000.

5. Increases in owner’s capital account are recorded as credits. Credit Maria Sanchez, Capital for $25,000.

On October 1 Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service, Memorandum 1.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

Business Transaction 1 (con’t.)

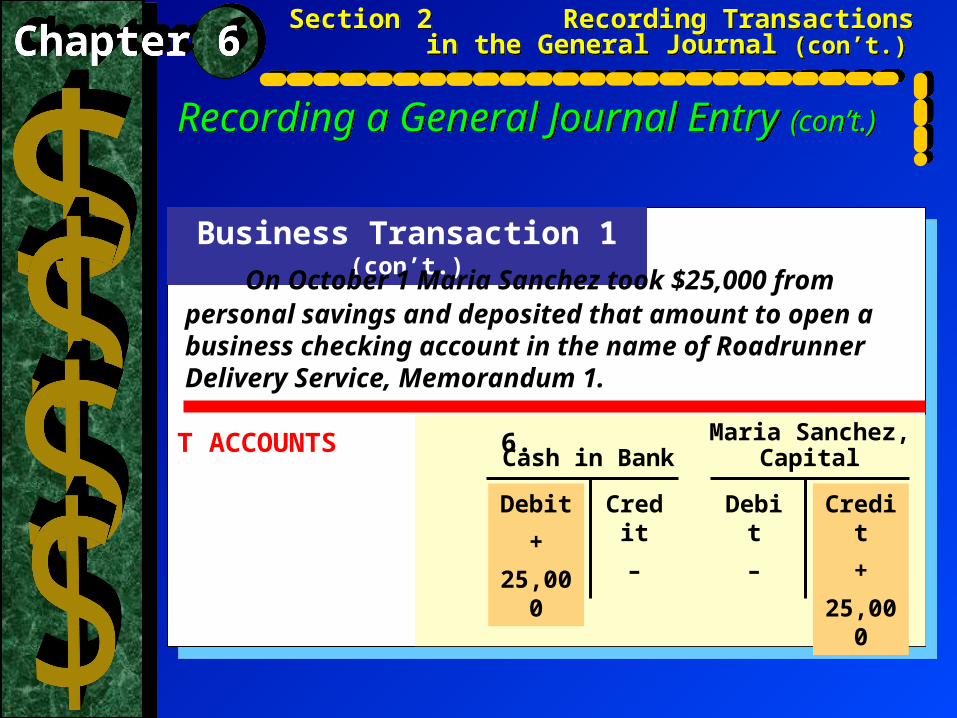

T ACCOUNTS 6.

On October 1 Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service, Memorandum 1.

Maria Sanchez,Cash in Bank Capital

Debit

+

25,000

Credit

+

25,000

Credit

–

Debit

–

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

Business Transaction 1 (con’t.)

JOURNAL ENTRY 7.

On October 1 Maria Sanchez took $25,000 from personal savings and deposited that amount to open a business checking account in the name of Roadrunner Delivery Service, Memorandum 1.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

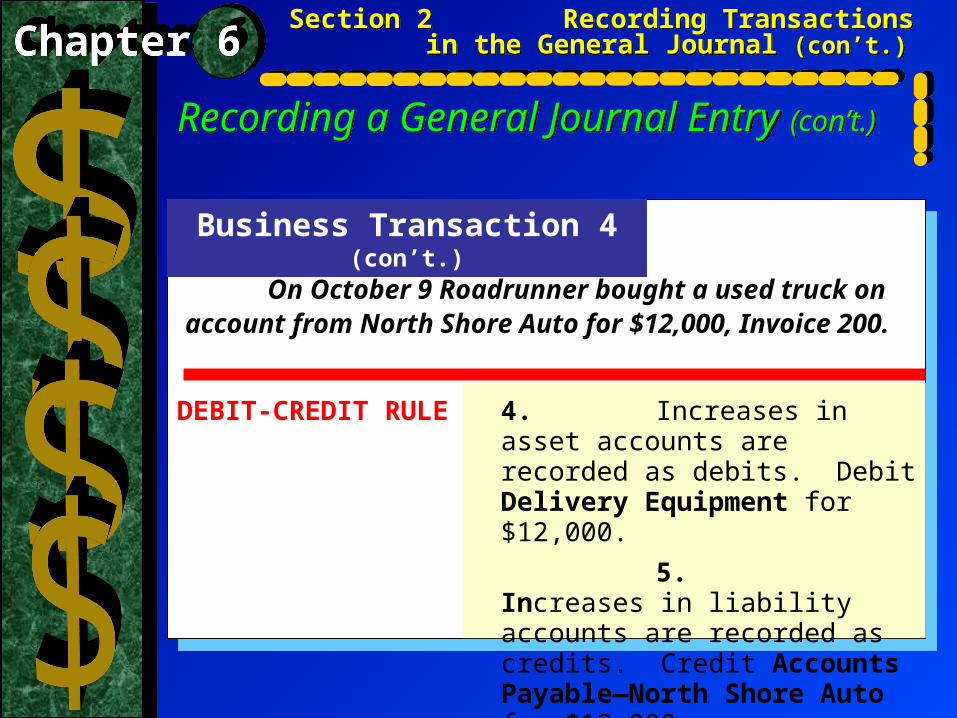

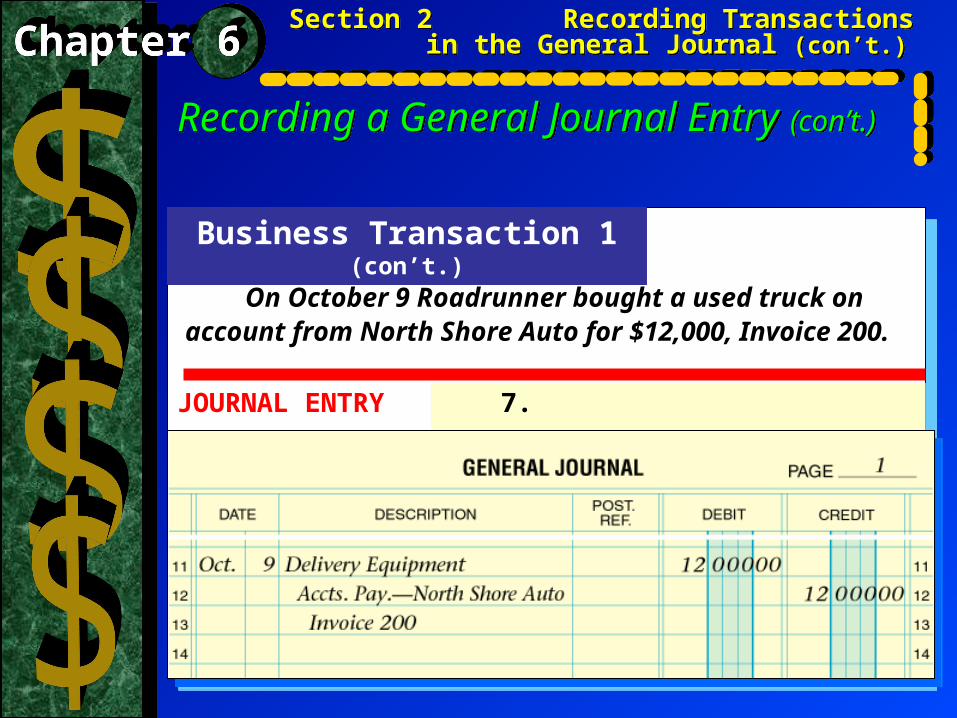

Business Transaction 4

ANALYSIS Identify 1. The accounts Delivery Equipment and Accounts Payable—North Shore Auto are affected.Classify 2. Delivery Equipment is an asset account. Accounts Payable— North Shore Auto is a liability account. + / – 3. Delivery Equipment is increased by $12,000. Accounts Payable— North Shore Auto is increased by $12,000.

On October 9 Roadrunnerbought a used truck on account from North ShoreAuto for $12,000, Invoice 200.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Business Transaction 4 (con’t.)

DEBIT-CREDIT RULE 4. Increases in asset accounts are recorded as debits. Debit Delivery Equipment for $12,000.

5. Increases in liability accounts are recorded as credits. Credit Accounts Payable—North Shore Auto for $12,000.

On October 9 Roadrunner bought a used truck on account from North Shore Auto for $12,000, Invoice 200.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

Business Transaction 4 (con’t.)

T ACCOUNTS 6.

On October 9 Roadrunner bought a used truck on account from North Shore Auto for $12,000, Invoice 200.

Delivery Accounts Payable—Equipment North Shore Auto

Debit

+

12,000

Credit

+

12,000

Credit

–

Debit

–

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

Business Transaction 1 (con’t.)

JOURNAL ENTRY 7.

On October 9 Roadrunner bought a used truck on account from North Shore Auto for $12,000, Invoice 200.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Recording a General Journal Entry (con’t.)Recording a General Journal Entry (con’t.)

Correcting Errors in General Journal EntriesCorrecting Errors in General Journal Entries An error should never be erased. Use a pen and a ruler to draw a

horizontal line through the entire incorrect item and write the correct information above the crossed-out error.

An error should never be erased. Use a pen and a ruler to draw a

horizontal line through the entire incorrect item and write the correct information above the crossed-out error.

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)

Conclusion to Chapter 6

What was covered

Conclusion to Chapter 6

What was covered

1. Introduction to the General

Journal

2. Fiscal year vs. Calendar year

3. Correcting errors

1. Introduction to the General

Journal

2. Fiscal year vs. Calendar year

3. Correcting errors

Section 2 Recording Transactions in the General Journal (con’t.)

Section 2 Recording Transactions in the General Journal (con’t.)