record this!. question 1 the chelsea video sells of $9000 of merchandise on account fob destination...

TRANSCRIPT

Record this!

Question 1

• The Chelsea Video sells of $9000 of merchandise on account FOB destination on May 4.

• A/R 9000– Sales 9000

Question 2

• $200 of goods is returned on May 8.

• Sales Returns and Allowances 200– Accounts Receivable

200

Question 3

• Chelsea Video purchases $7000 of merchandise on account from Highpoint Co. on May 9.

• Purchases 7000– A/P 7000

Question 4

• Some of the merchandise purchased on May 9 is inoperable. Chelsea returns $500 worth of merchandise on May 10th.

• Accounts Payable 500– Purchase returns and allowances 500

Question 5

• The correct company pays for the freight from the May 4th transaction of $500 in cash on May 11th.

• Delivery Expense 500– Cash 500

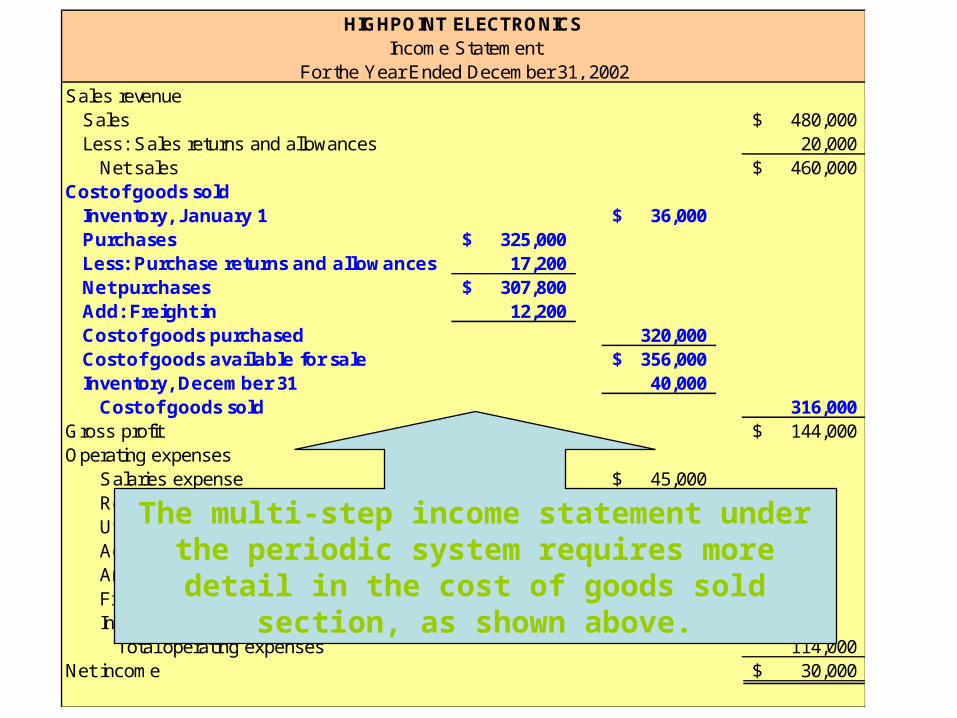

Sales revenueSales 480,000$ Less: Sales returns and allowances 20,000

Net sales 460,000$ Cost of goods sold

Inventory, January 1 36,000$ Purchases 325,000$ Less: Purchase returns and allowances 17,200 Net purchases 307,800$ Add: Freight in 12,200 Cost of goods purchased 320,000 Cost of goods available for sale 356,000$ Inventory, December 31 40,000

Cost of goods sold 316,000 Gross profit 144,000$ Operating expenses

Salaries expense 45,000$ Rent expense 19,000 Utilities expense 17,000 Advertising expense 16,000 Amortization expense 8,000 Freight out 7,000 Insurance expense 2,000

Total operating expenses 114,000 Net income 30,000$

For the Year Ended December 31, 2002

HIGHPOINT ELECTRONICSIncome Statement

The multi-step income statement under the periodic system requires more detail in the cost

of goods sold section, as shown above.

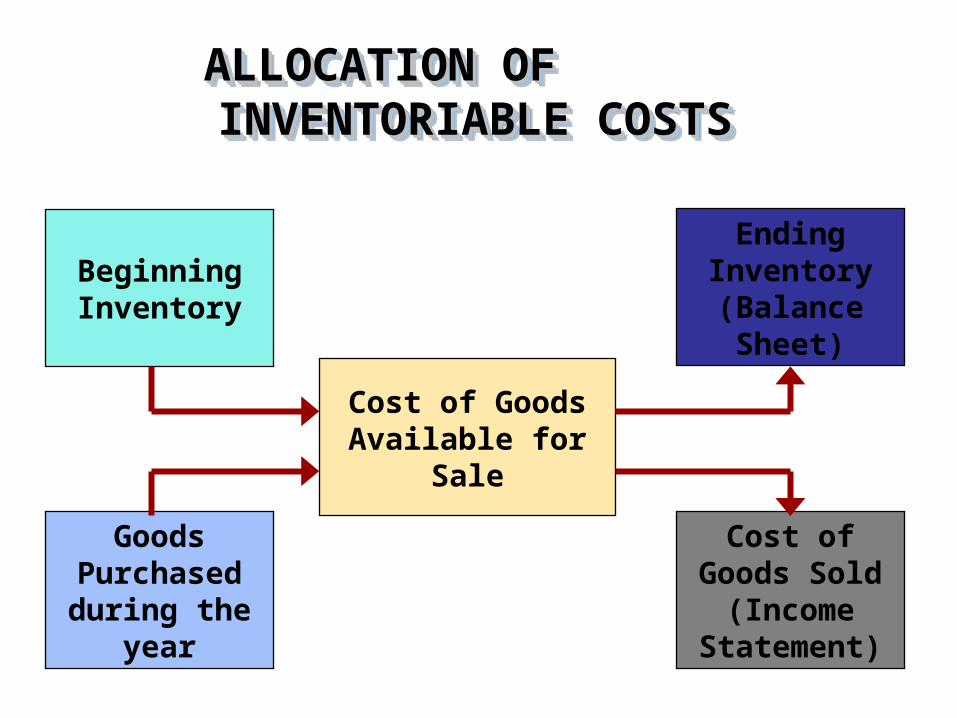

ALLOCATION OF ALLOCATION OF INVENTORIABLE COSTSINVENTORIABLE COSTS

ALLOCATION OF ALLOCATION OF INVENTORIABLE COSTSINVENTORIABLE COSTS

Beginning Inventory

Goods Purchased during the

year

Cost of Goods Available for Sale

Ending Inventory (Balance

Sheet)

Cost of Goods Sold

(Income Statement)

Question 6

• Prices are rising

• FIFO is used

• Question: – Are the highest or lowest priced purchases

used to calculate Cost of goods sold?

• Answer: – LOWEST (first purchases)

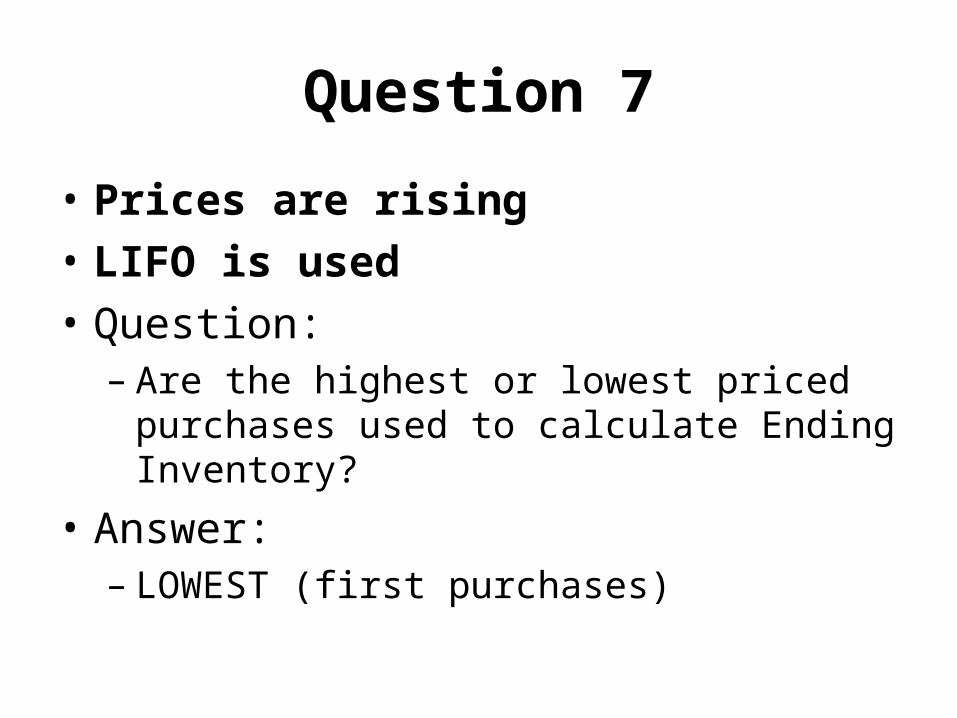

Question 7

• Prices are rising

• LIFO is used

• Question:– Are the highest or lowest priced purchases

used to calculate Ending Inventory?

• Answer: – LOWEST (first purchases)

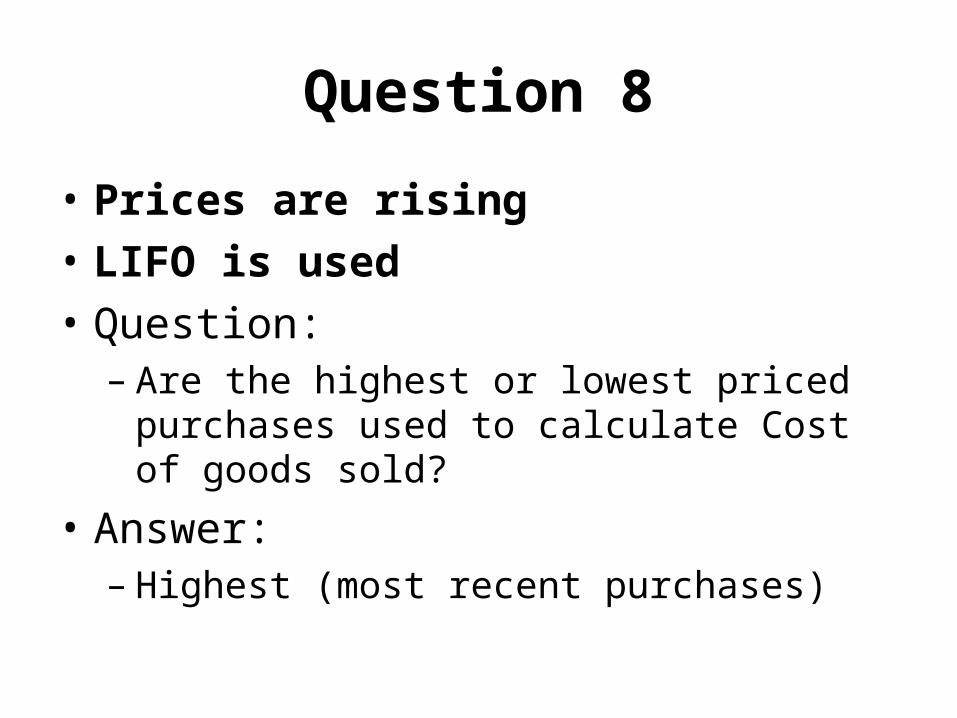

Question 8

• Prices are rising

• LIFO is used

• Question:– Are the highest or lowest priced purchases

used to calculate Cost of goods sold?

• Answer: – Highest (most recent purchases)

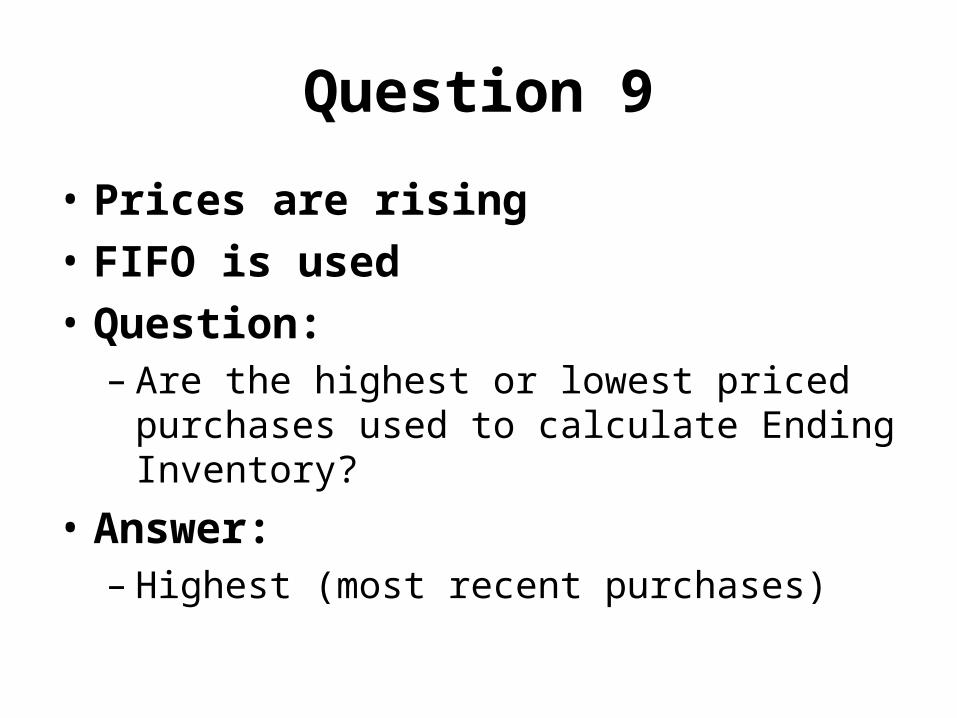

Question 9

• Prices are rising

• FIFO is used

• Question:– Are the highest or lowest priced purchases

used to calculate Ending Inventory?

• Answer: – Highest (most recent purchases)

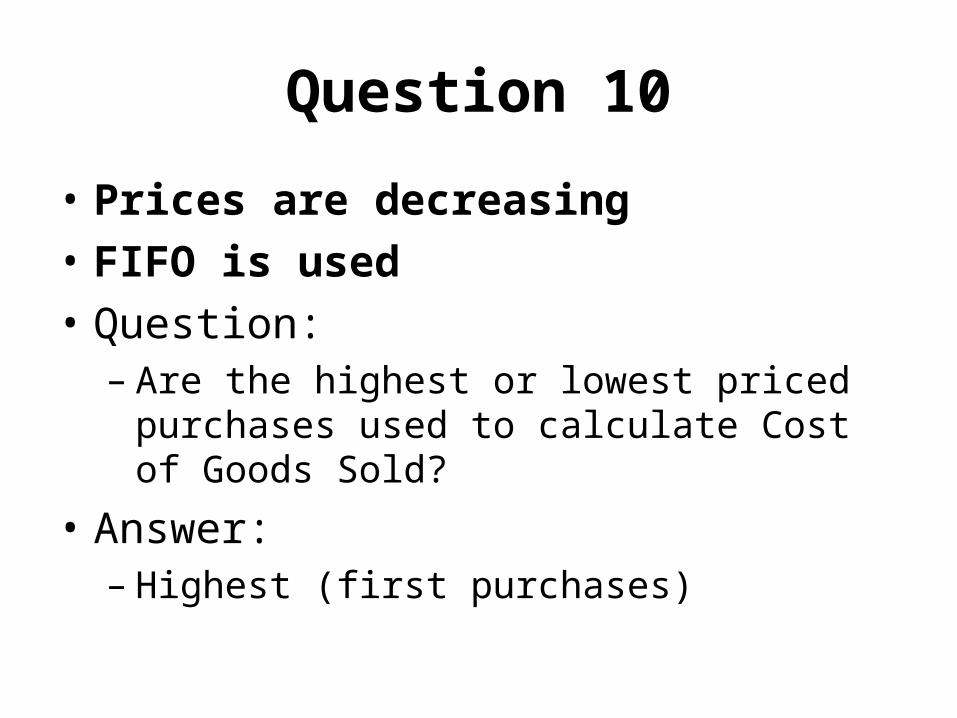

Question 10

• Prices are decreasing

• FIFO is used

• Question:– Are the highest or lowest priced purchases

used to calculate Cost of Goods Sold?

• Answer: – Highest (first purchases)

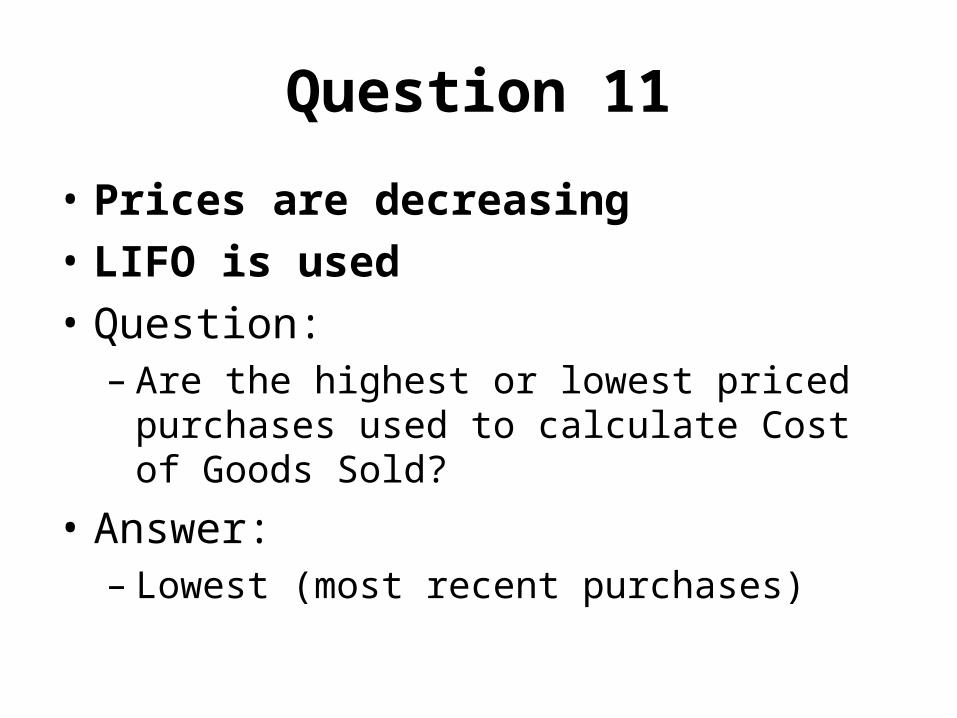

Question 11

• Prices are decreasing

• LIFO is used

• Question:– Are the highest or lowest priced purchases

used to calculate Cost of Goods Sold?

• Answer: – Lowest (most recent purchases)

Question 12

• Prices are increasing

• FIFO is used

• The lowest costs are used in COGS

• Question:– Is net income higher or lower than if we used

LIFO?

• Answer: – Higher.

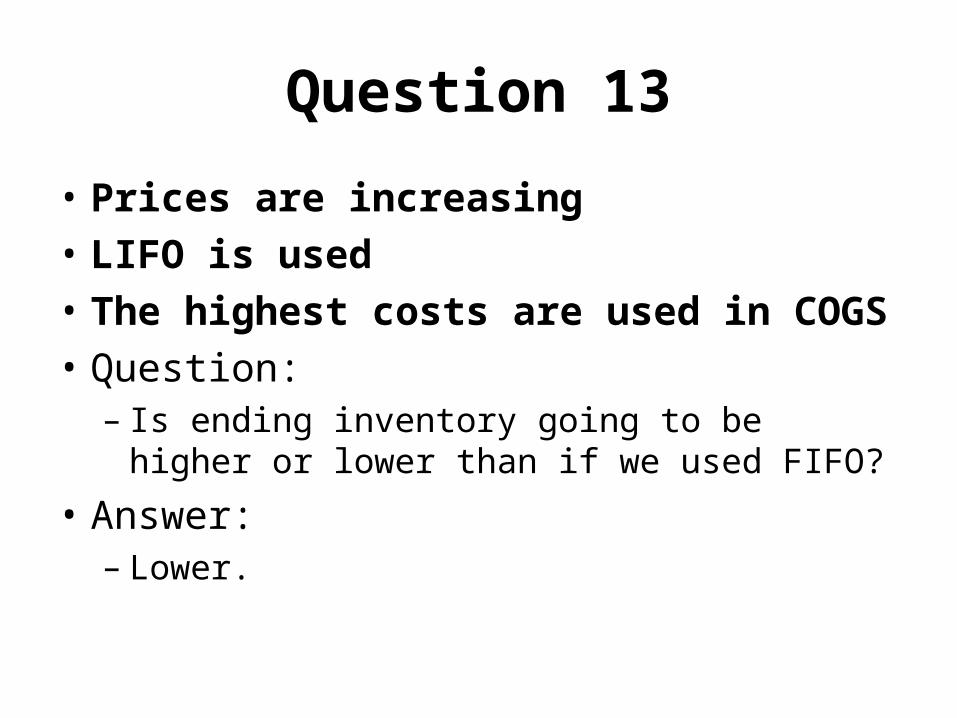

Question 13

• Prices are increasing

• LIFO is used

• The highest costs are used in COGS

• Question:– Is ending inventory going to be higher or

lower than if we used FIFO?

• Answer: – Lower.

USING ACTUAL PHYSICAL USING ACTUAL PHYSICAL FLOW COSTINGFLOW COSTING

USING ACTUAL PHYSICAL USING ACTUAL PHYSICAL FLOW COSTINGFLOW COSTING

• The specific identification method tracks the actual physical flow of the goods.

• Each item of inventory is marked, tagged, or coded with its specific unit cost.

• It is most frequently used when the company sells a limited variety of high unit-cost items.

USING ASSUMED COST USING ASSUMED COST FLOW METHODSFLOW METHODS

USING ASSUMED COST USING ASSUMED COST FLOW METHODSFLOW METHODS

• Other cost flow methods are allowed since specific identification is often impractical.

• These methods assume flows of costs that may be unrelated to the physical flow of goods.

• Cost flow assumptions:1. First-in, first-out (FIFO).2. Average cost.3. Last-in, first-out (LIFO).

FIFOFIFOFIFOFIFO• The FIFO method assumes that the earliest

goods purchased are the first to be sold.• Often reflects the actual physical flow of

merchandise.• Under FIFO, the costs of the earliest goods

purchased are the first to be recognized as cost of goods sold. The costs of the most recent goods purchased are recognized as the ending inventory.

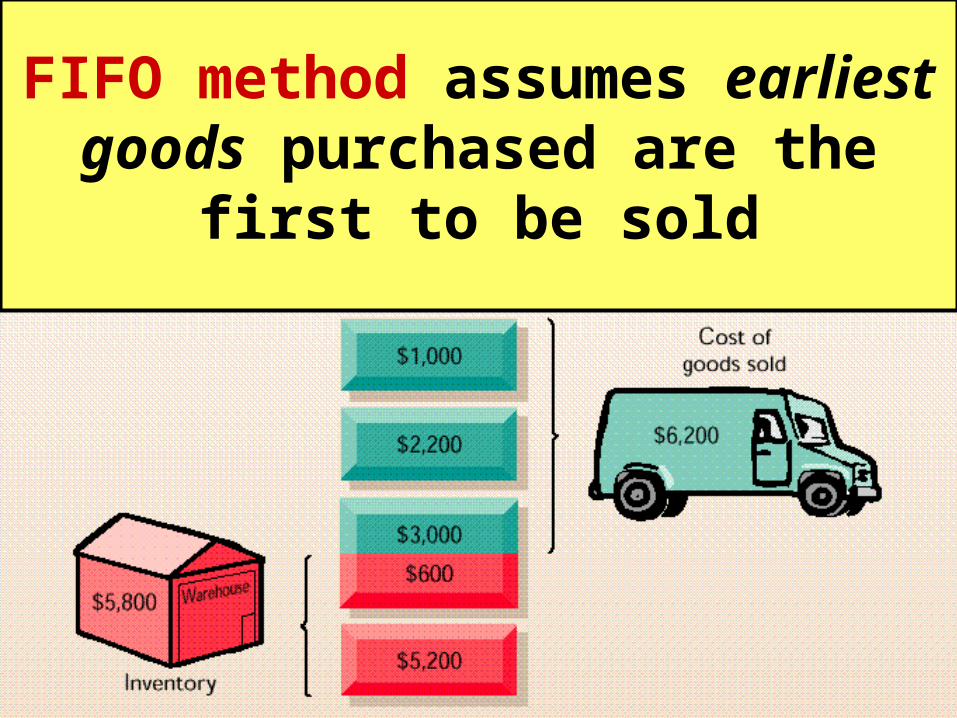

FIFO method assumes earliest goods purchased

are the first to be sold

LIFOLIFO

• The LIFO method assumes that the latest goods purchased are the first to be sold and that the earliest goods purchased remain in ending inventory.

• Seldom coincides with the actual physical flow of inventory.

• Under the periodic method, all goods purchased during the year are assumed to be available for the first sale, regardless of date of purchase.

• Rarely used in Canada.

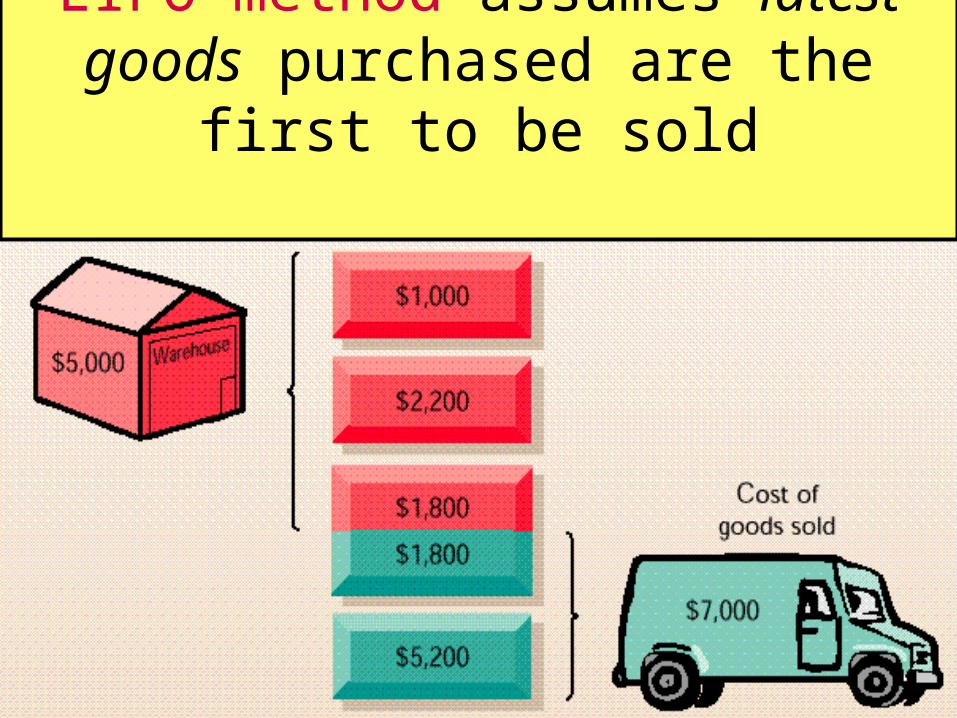

LIFO method assumes latest goods purchased are the first

to be sold

AVERAGE COSTAVERAGE COSTAVERAGE COSTAVERAGE COST

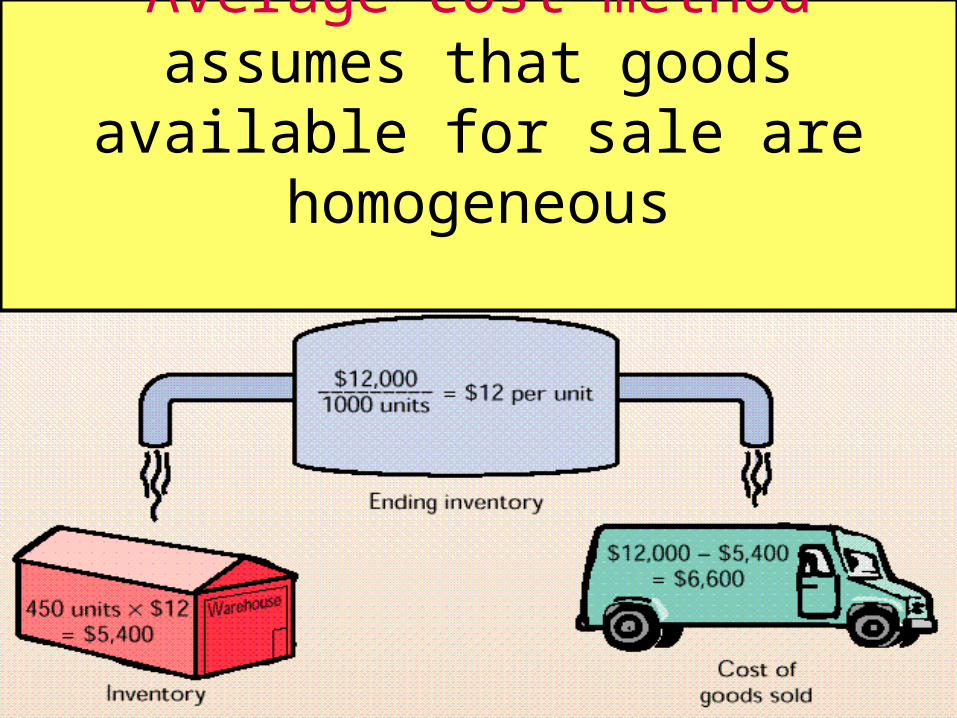

• The average cost method assumes that the goods available for sale are homogeneous.

• The allocation of the cost of goods available for sale is made on the basis of the weighted average unit cost incurred.

• The weighted average unit cost is then applied to the units sold to determine the cost of goods sold and to the units on hand to determine the ending inventory.

Allocation of the cost of goods available for sale in average cost method is made on the basis of the weighted average unit cost

Average cost method assumes that goods available for sale

are homogeneous

INCOME STATEMENT EFFECTSINCOME STATEMENT EFFECTSINCOME STATEMENT EFFECTSINCOME STATEMENT EFFECTS

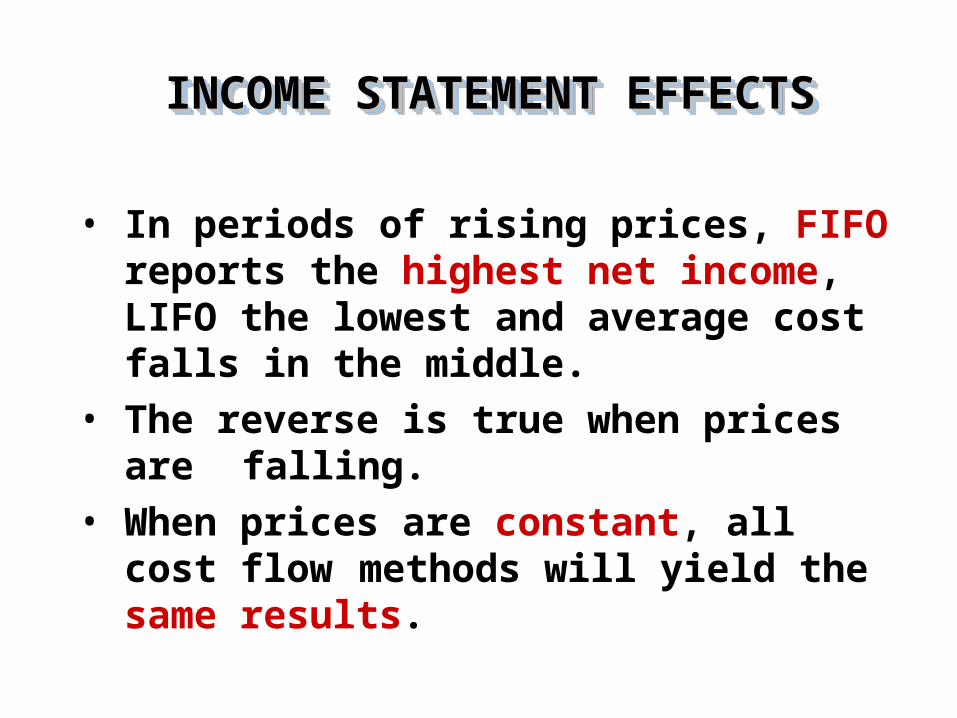

• In periods of rising prices, FIFO reports the highest net income, LIFO the lowest and average cost falls in the middle.

• The reverse is true when prices are falling.

• When prices are constant, all cost flow methods will yield the same results.

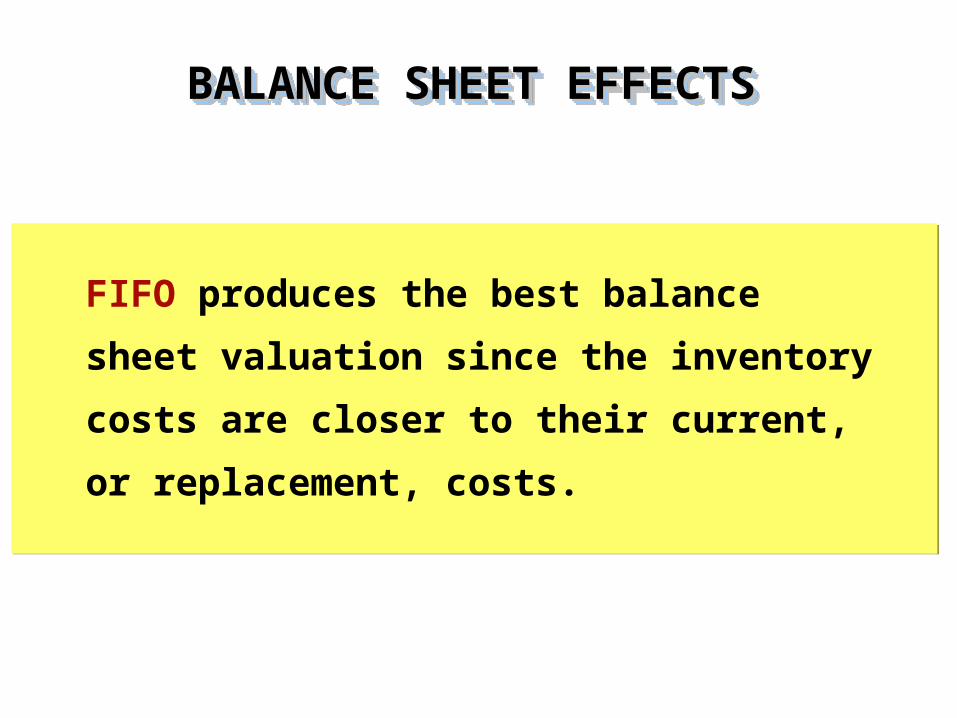

FIFO produces the best balance sheet

valuation since the inventory costs are

closer to their current, or replacement,

costs.

BALANCE SHEET EFFECTSBALANCE SHEET EFFECTSBALANCE SHEET EFFECTSBALANCE SHEET EFFECTS

USING INVENTORY COST FLOW USING INVENTORY COST FLOW METHODS CONSISTENTLYMETHODS CONSISTENTLY

USING INVENTORY COST FLOW USING INVENTORY COST FLOW METHODS CONSISTENTLYMETHODS CONSISTENTLY

• A company needs to use its chosen cost flow method consistently from one accounting period to another.

• Such consistent application enhances the comparability of financial statements over successive time periods.

• When a company adopts a different cost flow method, the change and its effects on net income should be disclosed in the financial statements.