recommendation: buy cvs caremark corp. - fisher … stock... · · 2013-07-11revenue growth...

TRANSCRIPT

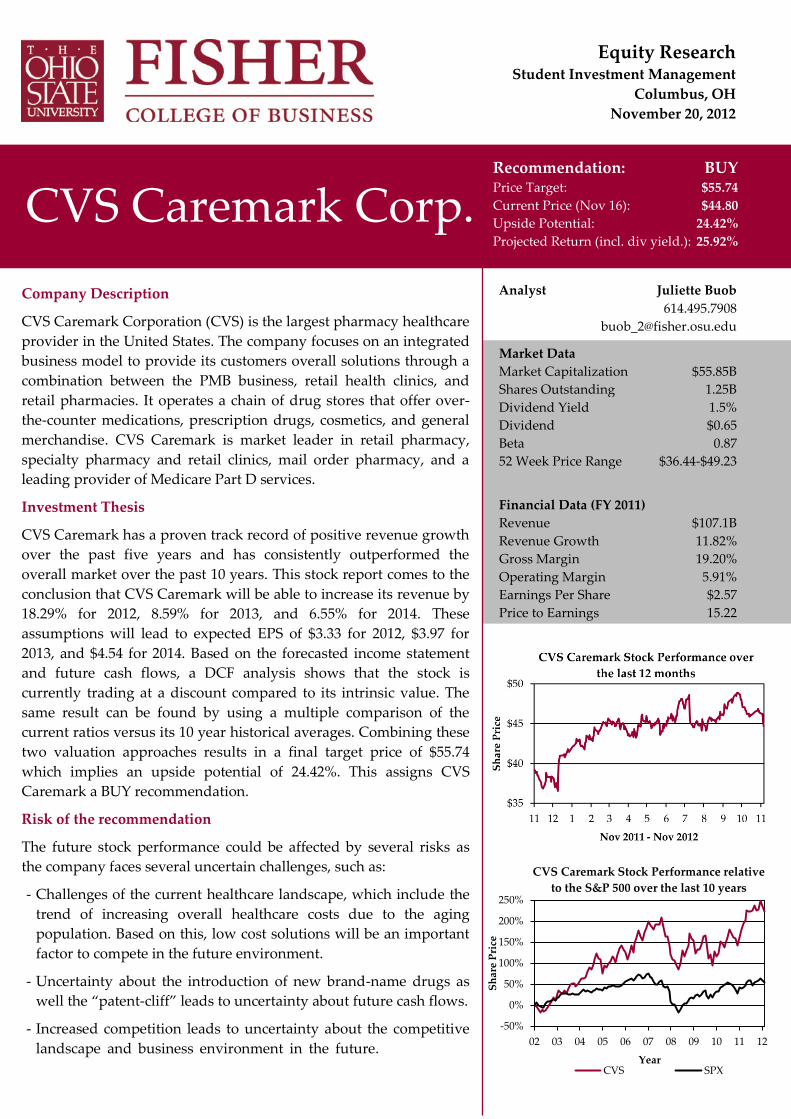

Market Data

Market Capitalization $55.85B

Shares Outstanding 1.25B

Dividend Yield 1.5%

Dividend $0.65

Beta 0.87

52 Week Price Range $36.44-$49.23

Financial Data (FY 2011)

Revenue $107.1B

Revenue Growth 11.82%

Gross Margin 19.20%

Operating Margin 5.91%

Earnings Per Share $2.57

Price to Earnings 15.22

-50%

0%

50%

100%

150%

200%

250%

02 03 04 05 06 07 08 09 10 11 12

Sh

are

Pri

ce

Year

CVS Caremark Stock Performance relative

to the S&P 500 over the last 10 years

CVS SPX

Djkdff d

Company Description

CVS Caremark Corporation (CVS) is the largest pharmacy healthcare

provider in the United States. The company focuses on an integrated

business model to provide its customers overall solutions through a

combination between the PMB business, retail health clinics, and

retail pharmacies. It operates a chain of drug stores that offer over-

the-counter medications, prescription drugs, cosmetics, and general

merchandise. CVS Caremark is market leader in retail pharmacy,

specialty pharmacy and retail clinics, mail order pharmacy, and a

leading provider of Medicare Part D services.

Investment Thesis

CVS Caremark has a proven track record of positive revenue growth

over the past five years and has consistently outperformed the

overall market over the past 10 years. This stock report comes to the

conclusion that CVS Caremark will be able to increase its revenue by

18.29% for 2012, 8.59% for 2013, and 6.55% for 2014. These

assumptions will lead to expected EPS of $3.33 for 2012, $3.97 for

2013, and $4.54 for 2014. Based on the forecasted income statement

and future cash flows, a DCF analysis shows that the stock is

currently trading at a discount compared to its intrinsic value. The

same result can be found by using a multiple comparison of the

current ratios versus its 10 year historical averages. Combining these

two valuation approaches results in a final target price of $55.74

which implies an upside potential of 24.42%. This assigns CVS

Caremark a BUY recommendation.

Risk of the recommendation

The future stock performance could be affected by several risks as

the company faces several uncertain challenges, such as:

- Challenges of the current healthcare landscape, which include the

trend of increasing overall healthcare costs due to the aging

population. Based on this, low cost solutions will be an important

factor to compete in the future environment.

- Uncertainty about the introduction of new brand-name drugs as

well the “patent-cliff” leads to uncertainty about future cash flows.

- Increased competition leads to uncertainty about the competitive

landscape and business environment in the future. dddddddd

Equity Research Student Investment Management

Columbus, OH

November 20, 2012

CVS Caremark Corp. Recommendation: BUY

Price Target: $55.74

Current Price (Nov 16): $44.80

Upside Potential: 24.42%

Projected Return (incl. div yield.): 25.92%

Analyst Juliette Buob

614.495.7908

Stock Data !

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 2/20

Table of Content

CVS Caremark - Company Overview ...................................................................................... 3

Business segments .................................................................................................................................. 3

Pharmacy Services .............................................................................................................................. 4

Retail Pharmacy Segment .................................................................................................................. 4

Corporate Segment ............................................................................................................................. 4

Business Strategy and Competitive Advantages ............................................................................... 4

Drivers and Strategy of the Pharmacy Services Segment ............................................................. 5

Drivers and Strategy of the Retail Pharmacy Services .................................................................. 5

Competitors and Market Share............................................................................................................. 5

Recent Developments and Stock Performance ................................................................................... 6

Investment Thesis ........................................................................................................................ 7

Relative Stock Performance................................................................................................................... 7

Financials ............................................................................................................................................... 10

Peer Comparison .............................................................................................................................. 12

Valuation Analysis and Price Target ................................................................................................. 12

Discounted Cash Flow Model ......................................................................................................... 12

Multiples Evaluation ........................................................................................................................ 13

Risks.............................................................................................................................................. 15

Conclusion ................................................................................................................................... 15

References .................................................................................................................................... 17

Appendix 1: Income Statement Forecasting .......................................................................... 18

Appendix 2: Peer Comparison ................................................................................................. 19

Appendix 3: Discounted Cash Flow Analysis ...................................................................... 20

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 3/20

CVS Caremark - Company Overview

Founded in 1892, CVS Caremark Corporation, headquartered in

Woonsocked, Rhode Island, is the largest pharmacy healthcare

provider in the United States. The company is divided in three

business segments, pharmacy services, retail pharmacy, and the

corporate division. Through its segments, the company is a market leader in retail pharmacy,

specialty pharmacy and retail clinics, mail order pharmacy, and a leading provider of Medicare

Part D services. With approximately 200,000 employees, CVS Caremark provides a network of

more than 65,000 pharmacies, including more than 7,300 CVS/pharmacy stores, to provide the

best available service for its customers across the United States (CVS Caremark Corp. (2012b)).

Business segments

As mentioned before, CVS Caremark operates its business through three main segments: phar-

macy services, retail pharmacy, and the corporate segment. Pharmacy and retail pharmacy ser-

vices accounted for about 50% each of total sales in the last three years with a slightly over-

weight of pharmacy services (53.64%) compared to retail pharmacy (46.36%) in the third quarter

of 2012. A summary of the three segments of CVS Caremark for the last three years and the third

quarter of 2012 is provided in Figure 1.

Business segments 2012 Q3 2011 2010 2009

in millions Net

Revenue in %

Net

Revenue in %

Net

Revenue in %

Net

Revenue in %

Pharmacy Service Segment $54,802 53.64% $58,874 49.69% $47,145 45.12% $50,551 47.73%

Retail Pharmacy Segment $47,373 46.36% $59,599 50.31% $57,345 54.88% $55,355 52.27%

Corporate Segment - 0.00% - 0.00% - 0.00% - 0.00%

Intersegment eliminations ($10436)

($11373)

($8712)

($7691)

Consolidated Revenue $91,739 $107,100

$95,778 $98,215

Consolidated Revenue (excl.

Intersegment eliminations) $102,175 100% $118,473 100% $104,490 100% $105,906 100%

Even though the pharmacy services segment and the retail pharmacy segment attribute almost

the same sales numbers to the consolidated revenue of CVS Caremark, the distribution of the

percentage attribution to the gross profit and the operating profit shows another view on the

two segments. Figure 2 provides an overview about the numbers for the last quarter and the

year 2011. It is obvious that the retail pharmacy segment accounted more than twice as much as

j

Business segments 2012 Q3 2011

in millions Gross

Profit in %

Operat-

ing Profit in %

Gross

Profit in %

Operat-

ing Profit in %

Pharmacy Service Segment $2,474 15.00% $1,644 31.59% $3,279 15.80% $2,220 34.07%

Retail Pharmacy Segment $14,014 85.00% $4,071 78.23% $17,468 84.20% $4,912 75.38%

Corporate Segment - 0.00% ($511) -9.82% - 0.00% ($616.00) -9.45%

Intersegment eliminations ($279)

($279)

($186)

($186)

Consolidated Profit $16,209

$4,925 $20,561 $6,330

Consolidated Profit (excl.

Intersegment eliminations) $16,488 100% $5,204 100% $20,747 100% $6,516 100%

Figure 1: Overview about revenue by segments (CVS Caremark Corp. (2012c) and CVS Caremark Corp. (2012e)).

Figure 2: Gross and operating profit by segments (CVS Caremark Corp. (2012e) and CVS Caremark Corp. (2012c)).

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 4/20

the pharmacy services segment to the consolidated gross and operating profit, which clearly

indicates that the costs in the first segment are much higher than in the second one.

Pharmacy Services

Through its pharmacy service segment, CVS Caremark provides a full range of Pharmacy Bene-

fit Management (PBM) services, which includes for example the mail order and the specialty

pharmacy services, the discounted drug purchase arrangements, Medicare Part D services, clini-

cal services, and pharmacogenomics. The provided services mainly focus on clients like employ-

ers, unions, insurance companies, managed care organizations, and government employee

groups. The pharmacy service segment operates under different names, such as CVS Caremark®

Pharmacy Services, Caremark®, CVS Caremark®, CarePlus, CVS/pharmacy®, CarePlus™,

RxAmerica® and Accordant® (CVS Caremark Corp. (2012c)).

Retail Pharmacy Segment

The retail pharmacy segment focuses on the sale of prescription drugs and general merchandise,

such as over-the-counter drugs, greeting cards, beauty products and cosmetics, seasonal mer-

chandise, and convenience foods through its CVS/pharmacy retail store network and through

the CVS.com website, whereas the majority of the retail pharmacy revenue is generated through

the sale of prescription drugs. Another branch of the retail pharmacy segment is the offer of

healthcare services through its MinuteClinic healthcare clinics, which are operated by nurse

practitioners and physician assistants. The aim of these clinics is to diagnose and treat minor

health conditions, e.g. by performing health screenings, monitoring chronic conditions, or deliv-

ering vaccinations. The segment operates mainly under the names CVS/pharmacy®, Longs

Drugs®, and MinuteClinic®, and the website CVS.com (CVS Caremark Corp. (2012c)).

Corporate Segment

The corporate segment does not contribute any revenue to the company’s income statement. Its

main activity focuses on providing management and administrative services in order to support

the overall company. Services of the corporate segment include corporate relations, human re-

sources, legal, information technology, finance activities, and compliance (CVS Caremark Corp.

(2012c)).

Business Strategy and Competitive Advantages

CVS Caremark’s strategy focuses on its integrated business model, which means providing its

customers overall solutions through a combination between the PMB business, the retail health

clinics and the retail pharmacies. The aim of this business model is to provide its customers with

greater access, choice, and convenience to pharmacy care, to deliver solutions to improve their

health, and to reduce the overall healthcare costs. Besides the customer focus, CVS Caremark’s

strategy also focuses on enhancing shareholder value through productive and long-term

growth, the generation of significant free cash, and the adherence to the company’s disciplined

capital allocation strategy (CVS Caremark Corp. (2012a)). Through its unique business model,

CVS Caremark is well-positioned in the market and owns a market share of about 26.3% (see

subchapter about “Competitors and Market Share” for more details).

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 5/20

Drivers and Strategy of the Pharmacy Services Segment

The pharmacy services segment includes several drivers to support the overall business strategy

and to expand its competitive advantages. One major driver is the clinical expertise that allows

the company to deliver innovative plan designs and best-in-class services for its clients and

members and therefore enjoying a high client retention rate. Besides the PMB business, CVS

Caremark is an industry leader in its specialty pharmacy and a strong player in the field of Med-

icare Part D prescription drug plans. Another focus area of the company includes the building a

leadership position in the Part D business and investing in new systems to handle its challeng-

ing regulatory requirements and complex benefit designs (CVS Caremark Corp. (2012a)).

Drivers and Strategy of the Retail Pharmacy Services

The major drivers behind the growth in the retail pharmacy segment include increased customer

access, superior customer service, and patient care improvements. Almost 17.5% of the front-

store revenue was reached by the store brand category, which represents another growth driver

in the retail pharmacy business. These products not only provide higher margins for the compa-

ny, they also help create loyalty and are less expensive for customers. The strategy includes the

release of more store brand products every year. Another powerful competitive advantage in

this business branch is the ExtraCare® Loyalty Program, which is the largest and most success-

ful retail loyalty program. This program provides the opportunity to execute targeted promo-

tional strategy and increase front-store profitability (CVS Caremark Corp. (2012a)).

Further, a major growth opportunity in this segment and part of the company’s business strate-

gy is the operation of its MinuteClinic®, which achieved breakeven profitability in 2011 (CVS

Caremark Corp. (2012a)). The number of operated MinuteClinics across the US was approxi-

mately 600 at the end of 2011c and is expected to increase to 1,000 by 2016 (CVS Caremark Corp.

(2012b)). A major driver behind the MinuteClinics is the belief that they will play an important

role in addressing the cost challenges of healthcare in the US and the shortage of primary care

physicians. This situation will be exacerbated through the healthcare reform in 2014 (See sub-

chapter “Key Fundamental and Economic Drivers” for more information, CVS Caremark Corp.

(2012a)).

Competitors and Market Share

The competitive environment in the pharmacy and retail drug industry is intensive due to the

increasing demand for healthcare and prescription drugs in the upcoming years (IBISWorld Inc.

(2012)). Several factors, such as the US healthcare reform act, the aging baby boomers or the ex-

piring patents support this demand even more (Murphy (2012), Wikinvest (2012), and Zanoni

(2011)). The growing sales of pharmaceuticals and retail drugs have elicited increased competi-

tion from non-traditional drugstores, such as mass merchandisers, online pharmacies, conven-

ience stores, supermarkets, or health clinics. As a response to the higher competition, traditional

drugstores like CVS Caremark or Walgreen Company try to stay competitive by offering con-

venience factors to their customers (e.g. drive-through pharmacy windows, longer operation

hours, standalone capabilities). However, due to the high competition, a continuing consolida-

tion within the industry is expected (IBISWorld Inc. (2012)).

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 6/20

The main competitors of CVS Caremark are Walgreen Company, Rite Aid Corporation, and Ex-

press Scripts Holding Company. Other competitors include Costco Wholesale Corporation, as

well as Wal-Mart Stores Incorporation (Yahoo! Finance (2012a), and IBISWorld Inc. (2012)). Fig-

ure 3 provides an overview about the market share of the three traditional drugstore companies

in the US. CVS Caremark is, with a market share of 26.3%, only 4% behind Walgreen Company

(30.9%). Even though all of these competitors operate similar business activities as CVS Care-

mark, it is difficult to make out one main

competitor because all have slightly differ-

ent business models, do not address exactly

the same clientele, and their geographic

region does not match completely. An eval-

uation of the comparison between key fi-

nancial ratios in terms of size, growth rates

and multiples will follow in the subchapter

“Peer comparison” on page 12. Further, ap-

pendix 2 on page 19 provides a detailed

overview of the key financial ratios of CVS

Caremark and its competitors.

Recent Developments and Stock Performance

The most recent event affecting the stock price of CVS Caremark was the release of the third

quarter result on November 6, 2012. According to the management of CVS Caremark the net

revenues increased by 13.3% and reached a record level of $30.2 billion. The increase in sales is

the result of a 22.2% increase in the pharmacy services and a moderate increase of 5.5% in the

retail pharmacy segment. As explained by the company, the revenue growth mostly results from

the growth in the Medicare Part D program, drug cost inflation, and the gain of new clients in

the retail pharmacy segment.

Further, the Management of CVS Caremark adjusted the guidance for the 2012 EPS to $3.38 to

$3.41 (former guidance was $3.32 to $3.38) due to the strong third-quarter performance, the ben-

efits from the share repurchase program announced on September 19, and the optimism about

keeping more than 60% of the prescriptions gained during the impasse between its two competi-

tors Walgreen and Express Scripts pharmacy. The stock market reacted slightly positively to

these news, shares rose by 25 cents and closed at $46.88 on November 6, 2012 (CVS Caremark

Corp. (2012d), and Johnson (2012)).

Figure 4 depicts a timeline with the events that affected CVS Caremark during the last 12

months. Most of the developments are related to the announcement of the company’s EPS guid-

ance for the fiscal year 2012 and there were no exceptional events that had a big influence on the

stock price. The continuing increase of the EPS guidance compared to the end of 2011 until the

last earnings report is a positive development and a good indicator for the estimated revenue

growth assumed in the pro forma income statement later in this report.

11.8%

26.3%

30.9%

31.0%

Major Players (Market share)

Rite Aid Corporation

CVS Caremark

Walgreen Company

Other

Figure 3: Major players in retail drug industry in the US

(IBISWorld Inc. (2012)

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 7/20

Dec 20, 2011

CVS Caremark

announced 2012

Guidance for

diluted EPS of

$3.15 to $3.25.

Analysts are

expecting $3.21.

Jan 12, 2012

Agreement to pay $5m

charges for inaccurate

pricing of some drugs for

elderly and disabled

Feb 8, 2012

EPS Guidance

for first quarter:

$0.61 to $0.63.

Analysts are

expecting $0.61.

May 2, 2012

Increase of 2012

EPS Guidance:

$3.23 to $3.33.

Analysts are

expecting $3.27.

Jun 12, 2012

CVS Caremark

announced that

it expects to add

$12.6b in net

revenues with

98% retention

rate.

Aug 7, 2012

Increase of 2012

EPS Guidance:

$3.32 to $3.38.

Analysts are

expecting $3.33.

Sep 19, 2012

Announcement of

$6.0b share repur-

chase program

authorization and

approval of

$0.1625 quarterly

dividend

Nov 6, 2012

Increase of 2012

EPS Guidance:

$3.38 to $3.41.

Analysts are

expecting $3.37.

Jan 10, 2012

Reaffirmation of

2012 Guidance

for diluted EPS of

$3.15 to $3.25.

Analysts are

expecting $3.24.

Figure 4: CVS Caremark stock timeline for past 12 months (Yahoo! Finance (2012b), and CVS Caremark Corp. (2012d)).

Investment Thesis

The aim of this paragraph is to provide a brief overview about the investment analysis and the

calculation of the target prices for the CVS Caremark stock. Before taking a briefer look at the

discounted cash flow model and the valuation outcome, the following paragraphs first consider

the relative price movements over the last years, the fundamental and economic drivers behind

the stock performance, the forecasting of the income statement for the next three years and the

underlying assumptions of the overall process.

Relative Stock Performance

CVS Caremark is part of the consumer staples sector which typically moves non-cyclical within

the overall market. The demand for staples goods such as pharmaceutical drugs, groceries, and

healthcare products, which are part of CVS Caremark product range, is generally independent

of the state of the economy and a good buffer during economic downturns or recessions. If we

consider the performance of the CVS Caremark stock relative to the S&P 500, the consumer sta-

ples sector and the retail drugs industry over the last 10 years, we see that the stock continuous-

ly outperformed the market. On the other hand, the price does not move completely inversely to

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 8/20

the market as expected by most of the staple companies (see figure 5). This observation is sup-

ported by the fact that Yahoo! Finance provides a beta of 0.87.

If we execute a regression analysis between the stock and the S&P 500 with a time horizon of

one year, the analysis shows that CVS Caremark is positively correlated with the market. The

price movement of the S&P 500 explains, according to the adjusted R Square, 73.05% of the vari-

ation in CVS Caremark’s stock price over the last year. However, the beta received by the re-

gression is with 1.1375 slightly higher than the beta provided by Finance! Yahoo. To conclude, it

is difficult to say whether the CVS Caremark stock acts as a typical counter-cyclical company or

moves in line with the market, but the stock price outperformed the market in every state of the

economy over the last 10 years and therefore provided a good and constant performance for its

investors.

Key Fundamental and Economic Drivers

The performance of CVS Caremark depends on several key drivers and industry trends that

affect the future growth opportunities. The following paragraphs give a brief overview about

the most important drivers behind prospective performance. Keep in mind that the list is not

exhaustive and that other factors can affect the company’s performance as well.

Healthcare Reform

An important driver among the industry is the number of people with health insurance, which

is one of the factors whether people can afford the pharmaceuticals or not. The upcoming

healthcare reform in the United States, starting in 2014, will lead to an increase in revenue vol-

ume for the overall retail drugs industry as an estimated amount of 32 million Americans will

gain insurance coverage for prescription drugs (IBISWorld Inc. (2012)). Therefore, the change in

healthcare regulation positively affects the future growth opportunities of CVS Caremark (CVS

Caremark (2012f)).

Influence of Brand-Drugs and “Patent Cliff”

The introduction of new released brand-name drugs of pharmaceutical manufactures is ex-

pected to decrease, which will result in an adverse affection of CVS Caremark’s revenue growth.

-50%

0%

50%

100%

150%

200%

250%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Sh

are

Pri

ce

Year

CVS Caremark Stock Performance over the last 10 years

CVS SPX CVS.S CVS.I

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.8553

R Square 0.7315

Adjusted R Square 0.7305

Standard Error 3.6634

Observations 264

Coefficients

Intercept 5.0404

Beta CVS Caremark 1.1375

Figure 5: CVS Caremark stock performance and regression output (data based on Thomson Baseline, 11/18/2012).

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 9/20

On the other side, the upcoming “patent cliff”, which means the expiration of number of patents

through 2013, will lead to the replacement of various brand-name drugs by generic versions.

This process will likely decline the average pharmacy prices but also will allow higher gross

profit margins for the retail drugstores and therefore positively affect industry’s future growth

opportunities (IBISWorld Inc. (2012)), Murphy (2012), and Zanoni (2011)).

Shortage of primary care physicians

The number of primary care physicians in the United States is expected to decrease over the fol-

lowing years and will result in a shortfall of a least 45,000 by 2020. This shortage will positively

affect the demand and therefore the revenue of in-store clinic provider like CVS Caremark offers

throughout its retail pharmacy services, as well as through its MinuteClinic (IBISWorld Inc.

(2012), and CVS Caremark Corp. (2012b)).

Consumer Spending

Another driver for future growth opportunities within the drugstore industry is the amount of

consumers’ disposable income per capita. The per capita income determines the ability of a con-

sumer to purchase consumer goods. As we mentioned before, the demand for prescription

products is not very susceptible to changes in consumer expenditures because they can be nec-

essary for health concerns. However, the demand of nonessential goods, such as cosmetics, can

vary a lot with changes in the per capita disposable income (IBISWorld Inc. (2012)). Figure 6

shows the positive correlation between the consumer spending, as well as the correlation be-

tween the disposable income and the CVS Caremark stock performance. Both variables have a

highly positive correlation of more than 0.90 with the price chart of the share.

Demographics

Another factor that increases the demand for pharmaceuticals is the aging population in the

United States. The so called “aging baby-boomers” and the fact that life expectancy is raising

will positively affect the sales volume in the industry as the need for healthcare will increase.

The reason for this need is due to the fact that this age group shows an increased risk of diseases

(IBISWorld Inc. (2012), and Wikinvest (2012)). Figure 7 provides an overview about the expected

demographics of the population in 2025 and 2050. Especially in more developed regions, like the

United States, the percentage of the people aged over 60 will be more than one third of the

population which means increased demand for healthcare products.

Figure 6: Correlation between consumer spending or disposable income and CVS Caremark (data from Thomson

Baseline, 11/18/2012)

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 10/20

Government activities

Even though the revenue of prescrip-

tion drugs is positively affected by the

above mentioned drivers, such as the

expected increase in insured people

due to the healthcare reform, it is ex-

pected that the government will also

initiate cost cutting measures to re-

duce the overall healthcare costs. Such

activities could adversely affect the

profit margin across the industry

(IBISWorld Inc. (2012)).

Financials

A copy of the total pro forma income statement for segment data as well as the consolidated

income statement can be found in appendix 1 on page 18. The resulting numbers are based on

the following assumptions:

Revenue

Historically, CVS Caremark used to have strong positive growth rates for its revenue over the

past five years except for the fiscal year 2010. Even in the critical years of the financial crisis of

2008/2009, the growth rates were still positive, which is another indicator that CVS Caremark’s

products are not that highly correlated with consumer’s disposable income as other consumer

goods are.

Forecasting the income statement for the following three fiscal years, the assumed growth rates

for the consolidated revenue are 18.29% for FY2012, 8.59% for FY2013, and 6.55% for FY2014.

The large growth rate for 2012 is based on the assumption that the revenue in the pharmacy

segment is supposed to increase with a rate of 27% and the revenue of the retail pharmacy seg-

ment with a moderate rate of 4.5%. The immense growth in pharmacy services results from sev-

eral changes in business, including the increase in the mail choice claims due to significant num-

ber of new clients, drug cost inflation in specialty business, increase in generic dispensing rate

because of new generic prescription drug instructions, increase in pharmacy network claim due

to new clients and higher activity with Medicare Part D program, and new activities resulting

from the acquisition of UAM Medicare PDP. Considering the third quarter results of November

6, 2012, the published net revenue numbers for the pharmacy service segment underline the

growth rate of 27%, as the third quarter net revenue increased by 27.4% compared to the prior

year period. On the other side, the assumption for the retail pharmacy segment is positive as

well but in a more moderate dimension that the one of the first segment. The revenue increase of

4.5% is based on several business drivers, including the increase in front store and pharmacy

store sales, significant increase due to the win of new clients resulting of the contractual impasse

between Walgreen Company and Express Scripts Holding, and positive affection due to the ma-

jor industry trends. These favorable industry trends include primarily an aging American popu-

lation which results in a greater consumption of prescription drugs and the increased use of

pharmaceuticals for individual healthcare as a first line of defense. However, the net revenue in

8 9 11

15

22

12 15

21

27

33

6 6 8

13

20

0

5

10

15

20

25

30

35

40

1950 1975 2009 2025 2050P

erc

en

tag

e

Proportion of population aged 60 or over, 1950-2050

World

More developed regions

Less developed regions

Figure 7: Expected demographics 1950-2050 (United Nations (2009)).

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 11/20

the retail pharmacy segments is adversely affected by the negative impact of the replacement of

brand name drugs by equivalent generic drugs (which have a lower selling price), the reduced

amount of new brand name drug releases, and higher consumer co-insurance arrangements and

co-payments. Again, taking into consideration the third quarter results, the assumption of a

4.5% growth rate is a bit more conservative but almost in line with the 5.5% increase compared

to its prior year revenue (CVS Caremark Corp. (2012c)). A revenue growth rate of 18.29% is not

sustainable over several years, even if the company can benefit from the mentioned industry

trends and revenue growth drivers. Because of this, the forecasted income statement uses lower

growth rates for 2013 and 2014 but still in a positive range.

Cost of Revenues and Operating Expenses

Considering the cost of revenues in percentage of the net revenue, the costs were in a range of

78.84%-80.80% over the past five years. Therefore, the spread between the historical percentages

was only 1.96%. The assumed numbers for the forecasted three years slightly decrease due to the

fact that they were quite high in 2011 compared to the previous four years. However, they still

stay higher than in 2010 due to higher revenue expectations and investment opportunities to

support future growth.

The same thoughts apply for the forecasting of the operating expenses in percentage of the net

revenue. To include a more conservative view regarding the expenses, the ratio is slightly higher

in 2012 compared to 2011 and decreases in 2013 and 2014. The reason for these thoughts is the

higher percentages for the years 2008-2010. However, the increase in the operating expenses

mainly results of higher costs associated with the Medicare Part D business, whereas the per-

centage is positively affected by the high revenue growth rate (CVS Caremark Corp. (2012c)).

Interest Expense and Income Tax Provision

The rate of interests in percentage of the revenue moved in a range between 0.53%-0.59% and

result in an average of 0.56% over the past five years. The forecasted percentages amounts with

0.55% to a lower level than its historical average due to the general low interest rate level in the

current economy and therefore lower average borrowing costs. On the other side, the lower per-

centage is also positively affected by the assumed future revenue growth.

Income Tax Provisions were lower in the second quarter results compared to the past five years.

Therefore, the applied rate for the forecast of the income statement amounted to 38.80%, which

is slightly less than its five year historical average. However, the uncertainty about the “fiscal

cliff” leads to an increase in uncertain tax positions and the tax rate for the third quarter was

with 39.2% slightly higher as assumed in the financial statement (CVS Caremark Corp. (2012c)).

Average Outstanding of Common Shares

The amount of outstanding shares in the forecasted income statement will decrease due to the

authorization of two share repurchase program in 2011 and in 2012. The latest authorization in

September 2012, include a repurchase for up to $6.0 billion of outstanding shares. Further, the

company entered into a share repurchase agreement with Barclays with a value of $1.2 billion on

September 19, 2012. These assumptions lead to a diluted EPS of $3.33 for 2012, $3.97 for 2013,

and $4.54 for 2014. The expected EPS of $3.33 is slightly below the consensus value of $3.40 and

lower than the company’s guidance of $3.38-3.41 (Yahoo! Finance (2012c)). These differences

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 12/20

results from a more conservative approach regarding future cost savings and future growth op-

portunities. For 2013 the estimated EPS of $3.97 is slightly higher than the consensus of $3.82

(Yahoo! Finance (2012c)).

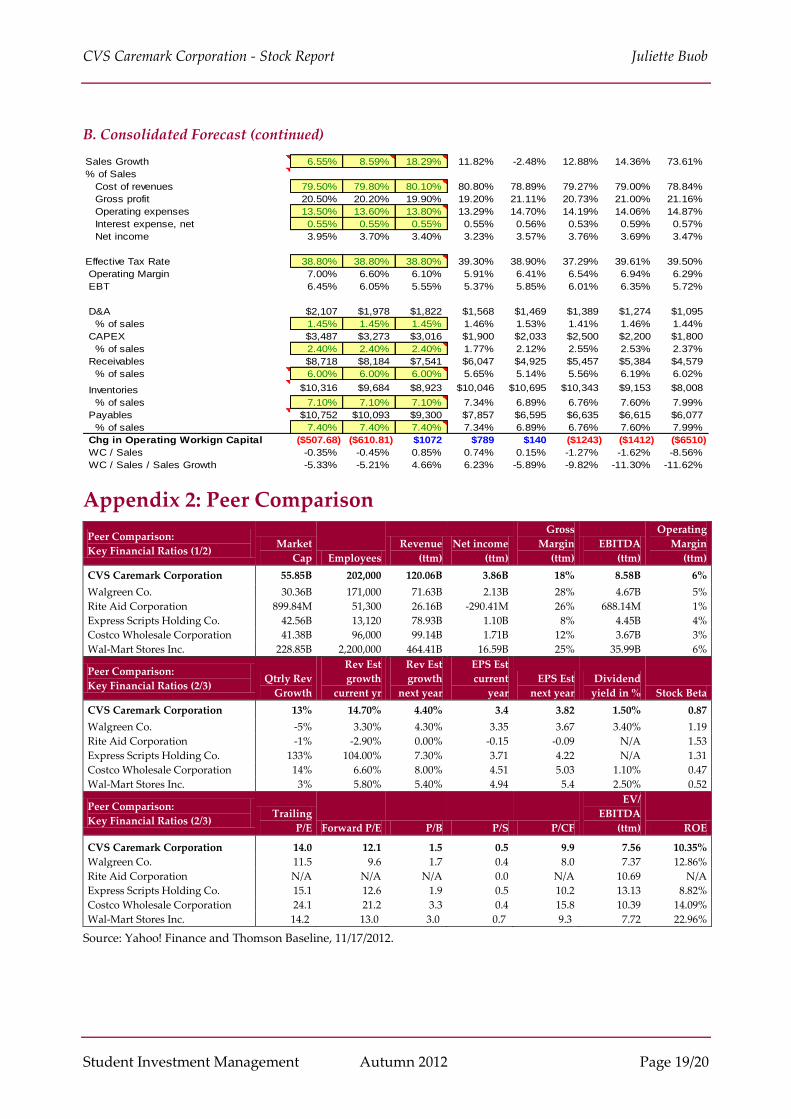

Peer Comparison

A detailed comparison of various key financial ratios including margins, growth rates, and mul-

tiples can be found in appendix 2 on page 19. The company that resembles CVS Caremark the

most in terms of size is Walgreen Company, especially in the number of employees, revenue and

market capitalization even though the numbers are smaller than the ones of CVS Caremark. The

other competitors have more or less lower ratios, except for Wal-Mart Incorporation. Comparing

the quarterly and the future expected revenue growth rates, CVS Caremark has one of the best

future growth opportunities among its competitors, whereas the EPS consensus is ranked in the

average range. Finally, considering the valuation ratios, CVS Caremark has slightly higher mul-

tiples than Walgreen Company, expect the P/B and ROE ratio. Compared to the other competi-

tors, the ROE ratio has a slightly lower value with exception of Express Scripts Holding Compa-

ny.

Valuation Analysis and Price Target

The following two subchapters use two different approaches, namely the DCF model and a mul-

tiples analysis, to estimate the target price for the CVS Caremark stock. We should be aware that

both approaches are based on various assumptions and depend on current economic circum-

stances.

Discounted Cash Flow Model

The detailed discounted cash flow analysis for CVS Caremark can be found in appendix 3 on

page 20. The model provided an estimated value per share of $57.93 and indicates that CVS

Caremark is currently traded at a discount relative to its implied intrinsic value with upside po-

tential of 29.3% over the closing price on November 16, 2012. The underlying calculations of a

DCF analysis are extremely sensitive to changes in the assumptions, especially in variations of

the cash flow’s growth and the discount rate. According to this sensitivity, the following para-

graphs provide an overview about these two factors used in the model.

The terminal growth rate of 3% is only slightly lower than the assumed 4% growth rate of the

overall market. As CVS Caremark is part of the consumer staples sector and therefore a defen-

sive stock, the revenue will grow steadily and constant but slower than the market. The positive

long-term growth rate results from the industry trends discussed in the subchapter “Key Funda-

mental and Economic Drivers”. On the other side, the possibility of these growth opportunities

will likely increase the competition and saturation of the US market will lead to a lower growth

rate in perpetuity.

As part of the consumer staples sector, CVS Caremark inhibits relatively modest risk compared

to the overall market. This phenomenon is also reflected in the low beta of 0.87. According to

this, the terminal discount rate used in the model is 9.30% which is 70 basis points below the

overall market discount rate. Besides the terminal growth and discount rate, the model is based

on cost in percentage of the revenue of 79%, a final operating margin of 6.3%, constant interest of

0.55%, and a constant tax rate of 38.8%.

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 13/20

As mentioned before, the estimated growth and the discount rate have a huge impact on the

intrinsic value implied by the DCF model. The sensitivity analysis presented in figure 8 shows

how sensible the implied share price reacts to changes in these two variables and which influ-

ences this has on the upside potential over the current stock price. If we limit the terminal

growth rate to a reasonable range between 1.5% in the worst case and 3.5% in the best case, as

well a range for the discount rate between 8.5% and 9.5%, the implied value ranges from $51.46-

$71.21. This is equivalent to a spread of $19.75. These wide spread is also visible if we consider

the upside potential over the stock price of $44.80. The span of the upside potential ranges from

10.72%-58.96%, which means a spread of more than 48.24%.

Growth Rate

Terminal

Discount Rate

1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0%

6.5% $77.04 $82.26 $88.64 $96.62 $106.87 $120.55 $139.69

7.0% $70.14 $74.31 $79.32 $85.43 $93.08 $102.91 $116.02

7.5% $64.31 $67.70 $71.70 $76.50 $82.36 $89.69 $99.12

8.0% $59.33 $62.11 $65.36 $69.19 $73.80 $79.42 $86.46

8.5% $55.02 $57.34 $60.00 $63.12 $66.80 $71.21 $76.61

9.0% $51.26 $53.21 $55.42 $57.99 $60.97 $64.50 $68.74

9.5% $47.96 $49.60 $51.46 $53.59 $56.05 $58.92 $62.31

10.0% $45.02 $46.43 $48.01 $49.79 $51.84 $54.20 $56.95

Growth Rate

Terminal

Discount Rate

1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0%

6.5% 71.96% 83.62% 97.86% 115.67% 138.55% 169.08% 211.81%

7.0% 56.56% 65.87% 77.04% 90.70% 107.77% 129.71% 158.97%

7.5% 43.55% 51.11% 60.04% 70.75% 83.84% 100.21% 121.25%

8.0% 32.43% 38.64% 45.89% 54.45% 64.73% 77.28% 92.98%

8.5% 22.82% 27.98% 33.94% 40.89% 49.10% 58.96% 71.01%

9.0% 14.43% 18.76% 23.72% 29.43% 36.10% 43.98% 53.44%

9.5% 7.05% 10.72% 14.87% 19.63% 25.11% 31.51% 39.08%

10.0% 0.50% 3.63% 7.15% 11.15% 15.71% 20.97% 27.12%

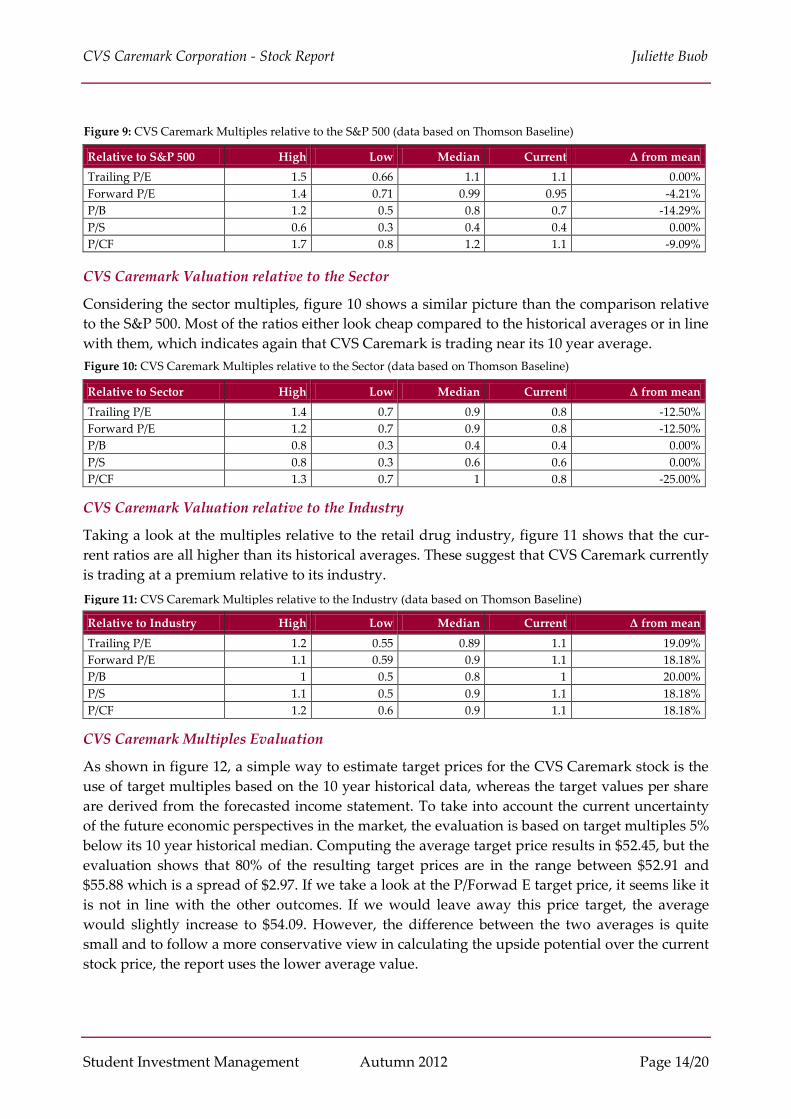

Multiples Evaluation1

The aim of a multiple analysis is to show whether the stock price of CVS Caremark is underval-

ued, fairly valued, or overvalued relative to the S&P 500, the consumer staples sector, or the re-

tail drug industry. The data is based on a 10 year historical average and is extracted from Thom-

son Baseline.

CVS Caremark Valuation relative to the S&P 500

As shown in figure 9, most of the ratios indicate that CVS Caremark is trading near to its 10 year

average of S&P 500 multiples or is slightly undervalued compared to its historical average. The

undervaluation could be a result of the 10 year horizon, as it includes a period of time where the

premium for certainty was extremely high.

1 Based on data of November 16, 2012.

Figure 8: DCF sensitivity analysis of target price and resulting upside potential due to changes in the growth and

discount rate

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 14/20

Relative to S&P 500 High Low Median Current Δ from mean

Trailing P/E 1.5 0.66 1.1 1.1 0.00%

Forward P/E 1.4 0.71 0.99 0.95 -4.21%

P/B 1.2 0.5 0.8 0.7 -14.29%

P/S 0.6 0.3 0.4 0.4 0.00%

P/CF 1.7 0.8 1.2 1.1 -9.09%

CVS Caremark Valuation relative to the Sector

Considering the sector multiples, figure 10 shows a similar picture than the comparison relative

to the S&P 500. Most of the ratios either look cheap compared to the historical averages or in line

with them, which indicates again that CVS Caremark is trading near its 10 year average.

Relative to Sector High Low Median Current Δ from mean

Trailing P/E 1.4 0.7 0.9 0.8 -12.50%

Forward P/E 1.2 0.7 0.9 0.8 -12.50%

P/B 0.8 0.3 0.4 0.4 0.00%

P/S 0.8 0.3 0.6 0.6 0.00%

P/CF 1.3 0.7 1 0.8 -25.00%

CVS Caremark Valuation relative to the Industry

Taking a look at the multiples relative to the retail drug industry, figure 11 shows that the cur-

rent ratios are all higher than its historical averages. These suggest that CVS Caremark currently

is trading at a premium relative to its industry.

Relative to Industry High Low Median Current Δ from mean

Trailing P/E 1.2 0.55 0.89 1.1 19.09%

Forward P/E 1.1 0.59 0.9 1.1 18.18%

P/B 1 0.5 0.8 1 20.00%

P/S 1.1 0.5 0.9 1.1 18.18%

P/CF 1.2 0.6 0.9 1.1 18.18%

CVS Caremark Multiples Evaluation

As shown in figure 12, a simple way to estimate target prices for the CVS Caremark stock is the

use of target multiples based on the 10 year historical data, whereas the target values per share

are derived from the forecasted income statement. To take into account the current uncertainty

of the future economic perspectives in the market, the evaluation is based on target multiples 5%

below its 10 year historical median. Computing the average target price results in $52.45, but the

evaluation shows that 80% of the resulting target prices are in the range between $52.91 and

$55.88 which is a spread of $2.97. If we take a look at the P/Forwad E target price, it seems like it

is not in line with the other outcomes. If we would leave away this price target, the average

would slightly increase to $54.09. However, the difference between the two averages is quite

small and to follow a more conservative view in calculating the upside potential over the current

stock price, the report uses the lower average value.

Figure 9: CVS Caremark Multiples relative to the S&P 500 (data based on Thomson Baseline)

Figure 10: CVS Caremark Multiples relative to the Sector (data based on Thomson Baseline)

Figure 11: CVS Caremark Multiples relative to the Industry (data based on Thomson Baseline)

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 15/20

Absolute Valu-

ation (10year) High Low Median Current

Target

Multiple

Target E, S,

B, etc/Share Target Price

P/Forward E 22.0 9.6 14.5 12.1 13.775 $3.33 $45.87

P/S 0.8 0.4 0.6 0.5 0.57 $98.03 $55.88

P/B 3.7 1.0 1.9 1.5 1.805 $29.57 $53.37

P/EBITDA 12.63 4.88 7.71 6.45 7.3245 $7.4 $54.20

P/CF 18.3 7.5 11.9 9.9 11.305 $4.68 $52.91

Average of Target Prices $52.45

Average of Target Prices (excluding P/Forward E) $54.09

Upside/Downside Potential over Current Stock Price ($44.80) +9.83%

Risks

There are several risks in this stock report. The pro forma income statement and the DCF model

are based on various assumptions about future growth opportunities of CVS Caremark. Howev-

er, these opportunities might turn out to be wrong or not fully reachable. The company faces

several uncertain challenges that can have an impact on the company in the future, e.g.:

- Challenges of the current healthcare landscape, which includes the trend of increasing overall

healthcare costs due to the aging population. Based on this, the focus on low cost solutions,

such as preventive care and prescription drugs, plays an important factor within the future

environment (CVS Caremark Corp (2012a)).

- Uncertainty about future new brand-name drugs and as well the “patent-cliff”, which results

in the exchange of brand-name drugs by similar generic products, can lead to uncertainty in

future cash flows (CVS Caremark Corp. (2012a)).

- Increase in the competitive landscape within the retail drug sector can lead to future consoli-

dations among competitors. The expected consolidation process leads to uncertainty about

future circumstances of CVS Caremark and its position in the market. Also changes in the

market presents a risk to the assumptions, as we do not know how the business will change

in the future, especially if the demand for prescription drugs shifts from drugstores to mass

merchandisers or even to online retailers (IBISWorld Inc. (2012)).

Conclusion

In order to come up with a final target price for the CVS Caremark stock, we will combine the

two target prices of the DCF analysis and the multiples valuation. To do so, the two target prices

will be weighted with a ratio of 60:40 which results in a final target price of $55.74 and an upside

potential of 24.42% compared to the closing price of November 16, 2012. The reason for the

heavier weight of the DCF value is that it is believed to be the most accurate value for the com-

pany. Even if considered a more conservative view and weighted both valuation methods equal-

ly, we would still receive a target price of $55.19. According to this great upside potential, CVS

Caremark has been given a BUY recommendation. An overview about the final target price cal-

culation can be found in figure 13.

As the underlying assumptions of the DCF model are chosen on the conservative side of the

possible range, the price of $55.74 represents a conservative suggestion as well. As we have seen

Figure 12: CVS Caremark multiples evaluation and target price (data based on Thomson Baseline)

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 16/20

Calculation of Final Target Price

for CVS Caremark Corporation Price Upside/Downside Potential Weight

Current Price $44.80

DCF Target Price $57.93 +29.31% 60%

Multiple Valuation Target Price $52.45 +9.83% 40%

Weighted Final Target Price $55.74 +24.42% 100%

in the sensitivity analysis of the DCF model, the calculations are highly sensitive to changes in

the discount rate and the terminal growth rate. On the other side, we should also consider the

sensitivity of the multiples valuation, as the median changes if we choose different time hori-

zons. With the decision to choose target multiples that were below the historical median, the

target price of this model is chosen more conservative as well. However, even a conservative

view of the future growth opportunities suggests that the CVS Caremark share is a great BUY

opportunity with high upside potential of 24.42%. Besides the quantitative upside potential, the

stock includes other advantages that make it a good BUY, such as:

- CVS Caremark is a strong company within the US market and operates a long-lasting

product and retail range across the country with future growth opportunities due to key

industry trends (e.g. aging population, patent-cliff, healthcare reform, etc.).

- The fact that the company is part of the non-cyclical consumer staples companies makes

it a less risky investment compared to other companies within the market. Especially in

these times where there are major uncertainties in the economy, the stock provides the

opportunity to diversify the overall risk in the portfolio.

- CVS Caremark provided strong positive revenue growth for the last quarter’s earnings

announcement, as well as for the past years the stock outperformed the market constant-

ly.

Taking into account the current dividend yield of 1.5%, CVS Caremark is supposed to provide a

projected return of 25.92%.

Figure 13: Calculation of CVS Caremark’s final target price and upside potential

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 17/20

References

CVS Caremark Corporation (Corp.), 2012a, CVS Caremark 2011 Annual Report from website,

http://media.corporate-ir.net/media_files/IROL/99/99533/CVSCaremark2011_AR.pdf,

11/14/2012.

CVS Caremark Corporation (Corp.), 2012b, 2011 Corporate Responsibility Report - Helping

people on their path to better health from website,

http://info.cvscaremark.com/sites/cvscaremark.com/files/2011_CVS_Caremark_CSR-

Report_Secured.pdf, 11/14/2012.

CVS Caremark Corporation (Corp.), 2012c, Form 10-Q for the Quarterly Period Ended Septem-

ber 30, 2012 from website, http://services.corporate-

ir.net/SEC.Enhanced/SecCapsule.aspx?c=99533&fid=8446842, 11/11/2012.

CVS Caremark Corporation (Corp.), 2012d, Press Releases from website, http://phx.corporate-

ir.net/phoenix.zhtml?c=99533&p=irol-news, 11/14/2012.

CVS Caremark Corporation (Corp.), 2012e, Form 10-K for the fiscal year ended December 31,

2011 from website, http://services.corporate-

ir.net/SEC.Enhanced/SecCapsule.aspx?c=99533&fid=8016313, 11/10/2012.

CVS Caremark, 2012f, Connected from website, http://www.cvscaremarkfyi.com/blogs/cvs-

caremark-2012-insights-report-reviews-pbm-trends, 11/18/2012.

IBISWorld Incorporation (Inc.), 2012, IBISWorld Industry Report 44611 Pharmacies & Drug

Stores in the US from website,

http://clients1.ibisworld.com/reports/us/industry/default.aspx?entid=1054, 11/12/2012.

Johnson, Linda A., 2012, CVS Caremark 3Q profit up 16 pct. as sales rise from website,

http://finance.yahoo.com/news/cvs-caremark-3q-profit-16-123246513.html, 11/14/2012.

Murphy, Tom, 2012, CVS Caremark profit jumps 18 pct; boosts outlook from website,

http://finance.yahoo.com/news/cvs-caremark-profit-jumps-18-pct-boosts-outlook-

125317628--finance.html, 09/02/2012.

United Nations, 2009, World Population Ageing 2009 from website,

http://www.un.org/esa/population/publications/WPA2009/WPA2009_WorkingPaper.pdf,

11/18/2012.

Wikinvest, 2012, CVS Caremark Corporation (CVS) from website,

http://www.wikinvest.com/wiki/CVS_Caremark_corporation, 09/02/2012.

Yahoo! Finance, 2012a, CVS Caremark Corporation (CVS) - Competitors from website,

http://www.wikinvest.com/wiki/CVS_Caremark_corporation, 11/17/2012..

Yahoo! Finance, 2012b, CVS Caremark Corporation (CVS) - Interactive Chart from website,

http://finance.yahoo.com/echarts?s=CVS+Interactive#symbol=cvs;range=1y;compare=;indica

tor=ke_sd+volume;charttype=line;crosshair=on;ohlcvalues=0;logscale=off;source=undefined,

11/14/2012.

Yahoo! Finance, 2012c, CVS Caremark Corporation (CVS) – Analyst estimates from website

http://finance.yahoo.com/q/ae?s=CVS+Analyst+Estimates, 11/17/2012.

Zanoni, David, 2011, CVS Caremark, Walgreen To Benefit From Expiring Patents from website,

http://seekingalpha.com/article/303465-cvs-caremark-walgreen-to-benefit-from-expiring-

patents, 09/02/2012.

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 18/20

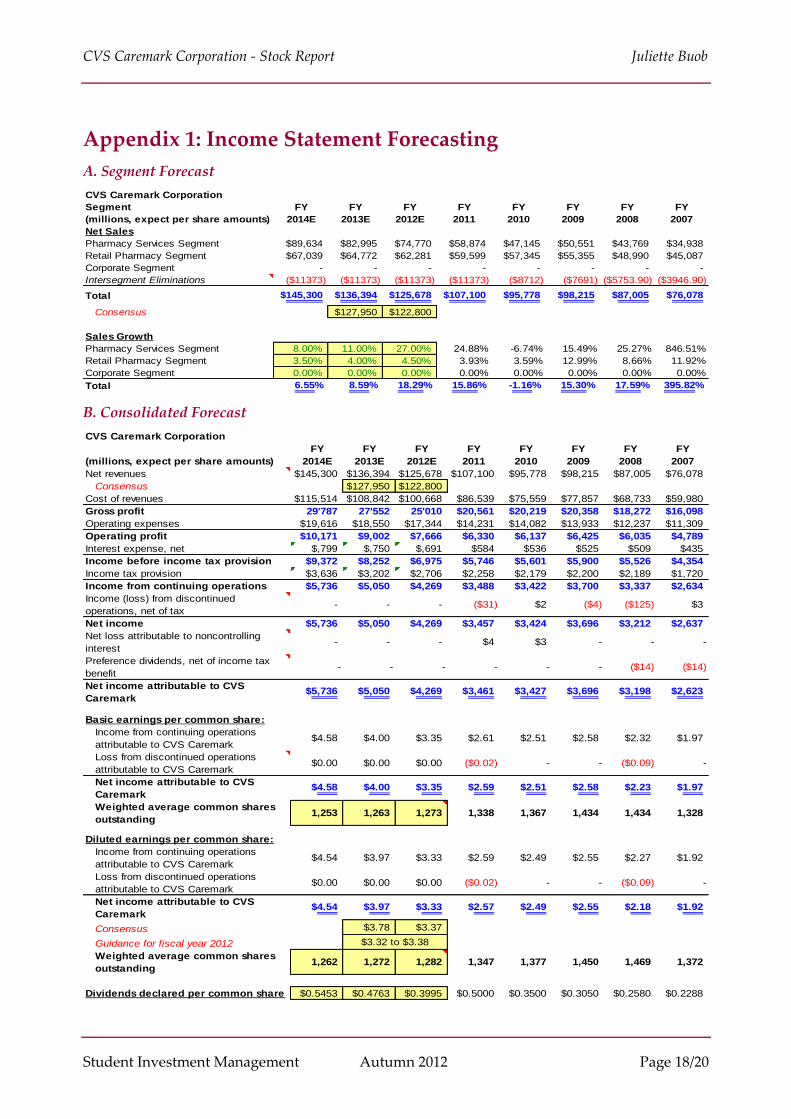

Appendix 1: Income Statement Forecasting

A. Segment Forecast

B. Consolidated Forecast

CVS Caremark Corporation

Segment FY FY FY FY FY FY FY FY

(millions, expect per share amounts) 2014E 2013E 2012E 2011 2010 2009 2008 2007

Net Sales

Pharmacy Services Segment $89,634 $82,995 $74,770 $58,874 $47,145 $50,551 $43,769 $34,938

Retail Pharmacy Segment $67,039 $64,772 $62,281 $59,599 $57,345 $55,355 $48,990 $45,087

Corporate Segment - - - - - - - -

Intersegment Eliminations ($11373) ($11373) ($11373) ($11373) ($8712) ($7691) ($5753.90) ($3946.90)

Total $145,300 $136,394 $125,678 $107,100 $95,778 $98,215 $87,005 $76,078

Consensus $127,950 $122,800

Sales Growth

Pharmacy Services Segment 8.00% 11.00% 27.00% 24.88% -6.74% 15.49% 25.27% 846.51%

Retail Pharmacy Segment 3.50% 4.00% 4.50% 3.93% 3.59% 12.99% 8.66% 11.92%

Corporate Segment 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Total 6.55% 8.59% 18.29% 15.86% -1.16% 15.30% 17.59% 395.82%

CVS Caremark Corporation

FY FY FY FY FY FY FY FY

(millions, expect per share amounts) 2014E 2013E 2012E 2011 2010 2009 2008 2007

Net revenues $145,300 $136,394 $125,678 $107,100 $95,778 $98,215 $87,005 $76,078

Consensus $127,950 $122,800

Cost of revenues $115,514 $108,842 $100,668 $86,539 $75,559 $77,857 $68,733 $59,980

Gross profit 29'787 27'552 25'010 $20,561 $20,219 $20,358 $18,272 $16,098

Operating expenses $19,616 $18,550 $17,344 $14,231 $14,082 $13,933 $12,237 $11,309

Operating profit $10,171 $9,002 $7,666 $6,330 $6,137 $6,425 $6,035 $4,789

Interest expense, net $,799 $,750 $,691 $584 $536 $525 $509 $435

Income before income tax provision $9,372 $8,252 $6,975 $5,746 $5,601 $5,900 $5,526 $4,354

Income tax provision $3,636 $3,202 $2,706 $2,258 $2,179 $2,200 $2,189 $1,720

Income from continuing operations $5,736 $5,050 $4,269 $3,488 $3,422 $3,700 $3,337 $2,634

Income (loss) from discontinued

operations, net of tax- - - ($31) $2 ($4) ($125) $3

Net income $5,736 $5,050 $4,269 $3,457 $3,424 $3,696 $3,212 $2,637

Net loss attributable to noncontrolling

interest- - - $4 $3 - - -

Preference dividends, net of income tax

benefit- - - - - - ($14) ($14)

Net income attributable to CVS

Caremark$5,736 $5,050 $4,269 $3,461 $3,427 $3,696 $3,198 $2,623

Basic earnings per common share:

Income from continuing operations

attributable to CVS Caremark$4.58 $4.00 $3.35 $2.61 $2.51 $2.58 $2.32 $1.97

Loss from discontinued operations

attributable to CVS Caremark$0.00 $0.00 $0.00 ($0.02) - - ($0.09) -

Net income attributable to CVS

Caremark$4.58 $4.00 $3.35 $2.59 $2.51 $2.58 $2.23 $1.97

Weighted average common shares

outstanding1,253 1,263 1,273 1,338 1,367 1,434 1,434 1,328

Diluted earnings per common share:

Income from continuing operations

attributable to CVS Caremark$4.54 $3.97 $3.33 $2.59 $2.49 $2.55 $2.27 $1.92

Loss from discontinued operations

attributable to CVS Caremark$0.00 $0.00 $0.00 ($0.02) - - ($0.09) -

Net income attributable to CVS

Caremark$4.54 $3.97 $3.33 $2.57 $2.49 $2.55 $2.18 $1.92

Consensus $3.78 $3.37

Guidance for fiscal year 2012

Weighted average common shares

outstanding1,262 1,272 1,282 1,347 1,377 1,450 1,469 1,372

Dividends declared per common share $0.5453 $0.4763 $0.3995 $0.5000 $0.3500 $0.3050 $0.2580 $0.2288

Sales Growth 6.55% 8.59% 18.29% 11.82% -2.48% 12.88% 14.36% 73.61%

% of Sales

Cost of revenues 79.50% 79.80% 80.10% 80.80% 78.89% 79.27% 79.00% 78.84%

Gross profit 20.50% 20.20% 19.90% 19.20% 21.11% 20.73% 21.00% 21.16%

Operating expenses 13.50% 13.60% 13.80% 13.29% 14.70% 14.19% 14.06% 14.87%

Interest expense, net 0.55% 0.55% 0.55% 0.55% 0.56% 0.53% 0.59% 0.57%

Net income 3.95% 3.70% 3.40% 3.23% 3.57% 3.76% 3.69% 3.47%

Effective Tax Rate 38.80% 38.80% 38.80% 39.30% 38.90% 37.29% 39.61% 39.50%

Operating Margin 7.00% 6.60% 6.10% 5.91% 6.41% 6.54% 6.94% 6.29%

EBT 6.45% 6.05% 5.55% 5.37% 5.85% 6.01% 6.35% 5.72%

D&A $2,107 $1,978 $1,822 $1,568 $1,469 $1,389 $1,274 $1,095

% of sales 1.45% 1.45% 1.45% 1.46% 1.53% 1.41% 1.46% 1.44%

CAPEX $3,487 $3,273 $3,016 $1,900 $2,033 $2,500 $2,200 $1,800

% of sales 2.40% 2.40% 2.40% 1.77% 2.12% 2.55% 2.53% 2.37%

Receivables $8,718 $8,184 $7,541 $6,047 $4,925 $5,457 $5,384 $4,579

% of sales 6.00% 6.00% 6.00% 5.65% 5.14% 5.56% 6.19% 6.02%

Inventories $10,316 $9,684 $8,923 $10,046 $10,695 $10,343 $9,153 $8,008

% of sales 7.10% 7.10% 7.10% 7.34% 6.89% 6.76% 7.60% 7.99%

Payables $10,752 $10,093 $9,300 $7,857 $6,595 $6,635 $6,615 $6,077

% of sales 7.40% 7.40% 7.40% 7.34% 6.89% 6.76% 7.60% 7.99%

Chg in Operating Workign Capital ($507.68) ($610.81) $1072 $789 $140 ($1243) ($1412) ($6510)

WC / Sales -0.35% -0.45% 0.85% 0.74% 0.15% -1.27% -1.62% -8.56%

WC / Sales / Sales Growth -5.33% -5.21% 4.66% 6.23% -5.89% -9.82% -11.30% -11.62%

$3.32 to $3.38

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 19/20

B. Consolidated Forecast (continued)

Appendix 2: Peer Comparison

Peer Comparison:

Key Financial Ratios (1/2) Market

Cap Employees

Revenue

(ttm)

Net income

(ttm)

Gross

Margin

(ttm)

EBITDA

(ttm)

Operating

Margin

(ttm)

CVS Caremark Corporation 55.85B 202,000 120.06B 3.86B 18% 8.58B 6%

Walgreen Co. 30.36B 171,000 71.63B 2.13B 28% 4.67B 5%

Rite Aid Corporation 899.84M 51,300 26.16B -290.41M 26% 688.14M 1%

Express Scripts Holding Co. 42.56B 13,120 78.93B 1.10B 8% 4.45B 4%

Costco Wholesale Corporation 41.38B 96,000 99.14B 1.71B 12% 3.67B 3%

Wal-Mart Stores Inc. 228.85B 2,200,000 464.41B 16.59B 25% 35.99B 6%

Peer Comparison:

Key Financial Ratios (2/3) Qtrly Rev

Growth

Rev Est

growth

current yr

Rev Est

growth

next year

EPS Est

current

year

EPS Est

next year

Dividend

yield in % Stock Beta

CVS Caremark Corporation 13% 14.70% 4.40% 3.4 3.82 1.50% 0.87

Walgreen Co. -5% 3.30% 4.30% 3.35 3.67 3.40% 1.19

Rite Aid Corporation -1% -2.90% 0.00% -0.15 -0.09 N/A 1.53

Express Scripts Holding Co. 133% 104.00% 7.30% 3.71 4.22 N/A 1.31

Costco Wholesale Corporation 14% 6.60% 8.00% 4.51 5.03 1.10% 0.47

Wal-Mart Stores Inc. 3% 5.80% 5.40% 4.94 5.4 2.50% 0.52

Peer Comparison:

Key Financial Ratios (2/3) Trailing

P/E Forward P/E P/B P/S P/CF

EV/

EBITDA

(ttm) ROE

CVS Caremark Corporation 14.0 12.1 1.5 0.5 9.9 7.56 10.35%

Walgreen Co. 11.5 9.6 1.7 0.4 8.0 7.37 12.86%

Rite Aid Corporation N/A N/A N/A 0.0 N/A 10.69 N/A

Express Scripts Holding Co. 15.1 12.6 1.9 0.5 10.2 13.13 8.82%

Costco Wholesale Corporation 24.1 21.2 3.3 0.4 15.8 10.39 14.09%

Wal-Mart Stores Inc. 14.2 13.0 3.0 0.7 9.3 7.72 22.96%

Source: Yahoo! Finance and Thomson Baseline, 11/17/2012.

CVS Caremark Corporation

FY FY FY FY FY FY FY FY

(millions, expect per share amounts) 2014E 2013E 2012E 2011 2010 2009 2008 2007

Net revenues $145,300 $136,394 $125,678 $107,100 $95,778 $98,215 $87,005 $76,078

Consensus $127,950 $122,800

Cost of revenues $115,514 $108,842 $100,668 $86,539 $75,559 $77,857 $68,733 $59,980

Gross profit 29'787 27'552 25'010 $20,561 $20,219 $20,358 $18,272 $16,098

Operating expenses $19,616 $18,550 $17,344 $14,231 $14,082 $13,933 $12,237 $11,309

Operating profit $10,171 $9,002 $7,666 $6,330 $6,137 $6,425 $6,035 $4,789

Interest expense, net $,799 $,750 $,691 $584 $536 $525 $509 $435

Income before income tax provision $9,372 $8,252 $6,975 $5,746 $5,601 $5,900 $5,526 $4,354

Income tax provision $3,636 $3,202 $2,706 $2,258 $2,179 $2,200 $2,189 $1,720

Income from continuing operations $5,736 $5,050 $4,269 $3,488 $3,422 $3,700 $3,337 $2,634

Income (loss) from discontinued

operations, net of tax- - - ($31) $2 ($4) ($125) $3

Net income $5,736 $5,050 $4,269 $3,457 $3,424 $3,696 $3,212 $2,637

Net loss attributable to noncontrolling

interest- - - $4 $3 - - -

Preference dividends, net of income tax

benefit- - - - - - ($14) ($14)

Net income attributable to CVS

Caremark$5,736 $5,050 $4,269 $3,461 $3,427 $3,696 $3,198 $2,623

Basic earnings per common share:

Income from continuing operations

attributable to CVS Caremark$4.58 $4.00 $3.35 $2.61 $2.51 $2.58 $2.32 $1.97

Loss from discontinued operations

attributable to CVS Caremark$0.00 $0.00 $0.00 ($0.02) - - ($0.09) -

Net income attributable to CVS

Caremark$4.58 $4.00 $3.35 $2.59 $2.51 $2.58 $2.23 $1.97

Weighted average common shares

outstanding1,253 1,263 1,273 1,338 1,367 1,434 1,434 1,328

Diluted earnings per common share:

Income from continuing operations

attributable to CVS Caremark$4.54 $3.97 $3.33 $2.59 $2.49 $2.55 $2.27 $1.92

Loss from discontinued operations

attributable to CVS Caremark$0.00 $0.00 $0.00 ($0.02) - - ($0.09) -

Net income attributable to CVS

Caremark$4.54 $3.97 $3.33 $2.57 $2.49 $2.55 $2.18 $1.92

Consensus $3.78 $3.37

Guidance for fiscal year 2012

Weighted average common shares

outstanding1,262 1,272 1,282 1,347 1,377 1,450 1,469 1,372

Dividends declared per common share $0.5453 $0.4763 $0.3995 $0.5000 $0.3500 $0.3050 $0.2580 $0.2288

Sales Growth 6.55% 8.59% 18.29% 11.82% -2.48% 12.88% 14.36% 73.61%

% of Sales

Cost of revenues 79.50% 79.80% 80.10% 80.80% 78.89% 79.27% 79.00% 78.84%

Gross profit 20.50% 20.20% 19.90% 19.20% 21.11% 20.73% 21.00% 21.16%

Operating expenses 13.50% 13.60% 13.80% 13.29% 14.70% 14.19% 14.06% 14.87%

Interest expense, net 0.55% 0.55% 0.55% 0.55% 0.56% 0.53% 0.59% 0.57%

Net income 3.95% 3.70% 3.40% 3.23% 3.57% 3.76% 3.69% 3.47%

Effective Tax Rate 38.80% 38.80% 38.80% 39.30% 38.90% 37.29% 39.61% 39.50%

Operating Margin 7.00% 6.60% 6.10% 5.91% 6.41% 6.54% 6.94% 6.29%

EBT 6.45% 6.05% 5.55% 5.37% 5.85% 6.01% 6.35% 5.72%

D&A $2,107 $1,978 $1,822 $1,568 $1,469 $1,389 $1,274 $1,095

% of sales 1.45% 1.45% 1.45% 1.46% 1.53% 1.41% 1.46% 1.44%

CAPEX $3,487 $3,273 $3,016 $1,900 $2,033 $2,500 $2,200 $1,800

% of sales 2.40% 2.40% 2.40% 1.77% 2.12% 2.55% 2.53% 2.37%

Receivables $8,718 $8,184 $7,541 $6,047 $4,925 $5,457 $5,384 $4,579

% of sales 6.00% 6.00% 6.00% 5.65% 5.14% 5.56% 6.19% 6.02%

Inventories $10,316 $9,684 $8,923 $10,046 $10,695 $10,343 $9,153 $8,008

% of sales 7.10% 7.10% 7.10% 7.34% 6.89% 6.76% 7.60% 7.99%

Payables $10,752 $10,093 $9,300 $7,857 $6,595 $6,635 $6,615 $6,077

% of sales 7.40% 7.40% 7.40% 7.34% 6.89% 6.76% 7.60% 7.99%

Chg in Operating Workign Capital ($507.68) ($610.81) $1072 $789 $140 ($1243) ($1412) ($6510)

WC / Sales -0.35% -0.45% 0.85% 0.74% 0.15% -1.27% -1.62% -8.56%

WC / Sales / Sales Growth -5.33% -5.21% 4.66% 6.23% -5.89% -9.82% -11.30% -11.62%

$3.32 to $3.38

CVS Caremark Corporation - Stock Report Juliette Buob

Student Investment Management Autumn 2012 Page 20/20

Appendix 3: Discounted Cash Flow Analysis

Analyst: 9.30%

Date: 29.09.2012 3.00%

TERMINAL

Year 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E

Net Revenues $125,678 $136,394 $145,300 $153,292 $160,497 $167,077 $173,259 $179,150 $184,883 $190,429 $196,142

% Growth 8.53% 6.53% 5.50% 4.70% 4.10% 3.70% 3.40% 3.20% 3.00% 3.00%

Cost of revenues $100,668 $108,842 $115,514 $121,714 $127,290 $132,375 $137,152 $141,707 $146,150 $150,458 $154,952

% of Net Revenues 80.10% 79.80% 79.50% 79.4% 79.3% 79.2% 79.2% 79.1% 79.1% 79.0% 79.0%

Gross profit $25,010 $27,552 $29,787 $31,578 $33,207 $34,702 $36,107 $37,442 $38,733 $39,971 $41,190

Gross margin 19.90% 20.20% 20.50% 20.60% 20.69% 20.77% 20.84% 20.90% 20.95% 20.99% 21.00%

Operating expenses $17,344 $18,550 $19,616 $21,001 $22,293 $23,508 $24,672 $25,798 $26,900 $27,974 $28,833

% of Net Revenues 13.80% 13.60% 13.50% 13.70% 13.89% 14.07% 14.24% 14.40% 14.55% 14.69% 14.70%

Operating Profit $7,666 $9,002 $10,171 $10,577 $10,914 $11,194 $11,435 $11,645 $11,832 $11,997 $12,357

Operating Margin 6.10% 6.60% 7.00% 6.90% 6.80% 6.70% 6.60% 6.50% 6.40% 6.30% 6.30%

Interest expense, net $691 $750 $799 $843 $883 $919 $953 $985 $1,017 $1,047 $1,079

Interest % of Sales 0.550% 0.550% 0.550% 0.550% 0.550% 0.550% 0.550% 0.550% 0.550% 0.550% 0.550%

Income before income tax

provision$6,975 $8,252 $9,372 $9,734 $10,031 $10,275 $10,482 $10,659 $10,816 $10,950 $11,278

Income tax provision $2,706 $3,202 $3,636 3'777 3'892 3'987 4'067 4'136 4'196 4'248 4'376

Tax Rate 38.80% 38.80% 38.80% 38.80% 38.80% 38.80% 38.80% 38.80% 38.80% 38.80% 38.80%

Income from continuing

operations$4,269 $5,050 $5,736 $5,957 $6,139 $6,288 $6,415 $6,524 $6,619 $6,701 $6,902

Income (loss) from

discontinued operations,

net of tax

- - - - - - - - - - -

Net Income $4,269 $5,050 $5,736 $5,957 $6,139 $6,288 $6,415 $6,524 $6,619 $6,701 $6,902

% Growth 18.30% 13.57% 3.86% 3.05% 2.43% 2.01% 1.69% 1.47% 1.24% 3.00%

Add Depreciation/Amort $1,822 $1,978 $2,107 $2,223 $2,327 $2,423 $2,512 $2,598 $2,681 $2,761 $2,844

% of Sales 1.45% 1.45% 1.45% 1.45% 1.45% 1.45% 1.45% 1.45% 1.45% 1.45% 1.45%

Plus/(minus) Changes WC $1072 ($610.81) ($507.68) ($463.71) ($414.88) ($376.76) ($352.58) ($335.01) ($325.39) ($314.21) ($323.63)

% of Sales 0.85% -0.45% -0.35% -0.30% -0.26% -0.23% -0.20% -0.19% -0.18% -0.17% -0.17%

Subtract Cap Ex $3016 $3273 $3487 $3,497 $3,471 $3,415 $3,335 $3,236 $3,120 $2,987 $2,844

Capex % of sales 2.40% 2.40% 2.40% 2.28% 2.16% 2.04% 1.93% 1.81% 1.69% 1.57% 1.45%

Free Cash Flow 4'165 3'416 4'117 4'467 4'803 5'115 5'407 5'689 5'964 6'238 6'625

% Growth -17.98% 20.53% 8.51% 7.51% 6.50% 5.71% 5.21% 4.83% 4.60% 6.20%

NPV of Cash Flows 31'313 41%

NPV of terminal value 44'511 59% Terminal Value 108'310

Projected Equity Value 75'824 100%

Free Cash Flow Yield 7.10% Free Cash Yield 6.12%

Current P/E 13.7 11.6 10.2 Terminal P/E 15.7

Projected P/E 17.8 15.0 13.2

Current EV/EBITDA 7.0 6.1 5.4 Terminal EV/EBITDA 7.6

Projected EV/EBITDA 8.8 7.6 6.8

Shares Outstanding 1,309

Current Price $44.80

Implied equity value/share $57.93

Upside/(Downside) to DCF 29.30%

Debt $9,208

Cash $1,413

Cash/share 1.08

Total Assets $64,543

Debt/Assets 14.3%

Working Capital % of

Growth5.5%

CVS Caremark Corporation

Terminal Discount Rate =Juliette Buob

Terminal FCF Growth =